Embed Size (px)

Citation preview

Jefferies Global Health Care

Conference

June 3, 2014

Health care is too important to stay the same.TM

Marc Naughton Executive Vice President and Chief Financial Officer

© 2014 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 2

Safe Harbor Statement

This presentation may contain forward-looking statements, including without limitation, those regarding

projections of future revenues or earnings, operating margins, operating expenses, product development

and new markets or prospects for the Company’s solutions. Actual results may differ materially from

those expressed in such forward-looking statements. Factors that could cause or contribute to such

differences include, but are not limited to: (a) the possibility of product-related liabilities; (b) potential claims for system errors and warranties; (c) the possibility of interruption at our data

centers or client support facilities; (d) our proprietary technology may be subject to claims for infringement or misappropriation of intellectual

property rights of others, or may be infringed or misappropriated by others; (e) risks associated with our non-U.S. operations; (f) risks associated

with our ability to effectively hedge exposure to fluctuations in foreign currency exchange rates; (g) the potential for tax legislation initiatives

that could adversely affect our tax position and/or challenges to our tax positions in the United States and non-U.S. countries; (h) risks

associated with our recruitment and retention of key personnel; (i) risks related to our dependence on third party suppliers; (j) risks inherent

with business acquisitions and combinations; (k) the potential for losses resulting from asset impairment charges; (l) risks associated with

volatility and disruption resulting from global economic conditions; (m) managing growth in the new markets in which we offer solutions, health

care devices and services, (n) changing political, economic, regulatory and judicial influences; (o) government regulation; (p) significant

competition and market changes; (q) variations in our quarterly operating results; (r) potential inconsistencies in our sales forecasts compared

to actual sales; (s) volatility in the trading price of our common stock and the timing and volume of market activity; (t) our directors’ authority to

issue preferred stock and the anti-takeover provisions in our corporate governance documents; and (u) material adverse resolution of legal

proceedings.

Additional discussion of these and other risks, uncertainties and factors affecting the Company's business

is contained in the Company's periodic filings with the Securities and Exchange Commission. The reader

should not place undue reliance on forward-looking statements, since the statements speak only as of the

date that they are made. The Company undertakes no obligation to update forward-looking statements to

reflect changed assumptions, the occurrence of unanticipated events or changes in future operating

results, financial condition or business over time.

A reconciliation of non-GAAP financial measures discussed in this presentation can be found in the

Appendix to this presentation and the Company’s most recent earnings release that was furnished to the

SEC and posted on the investor section of Cerner.com.

© 2014 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 3

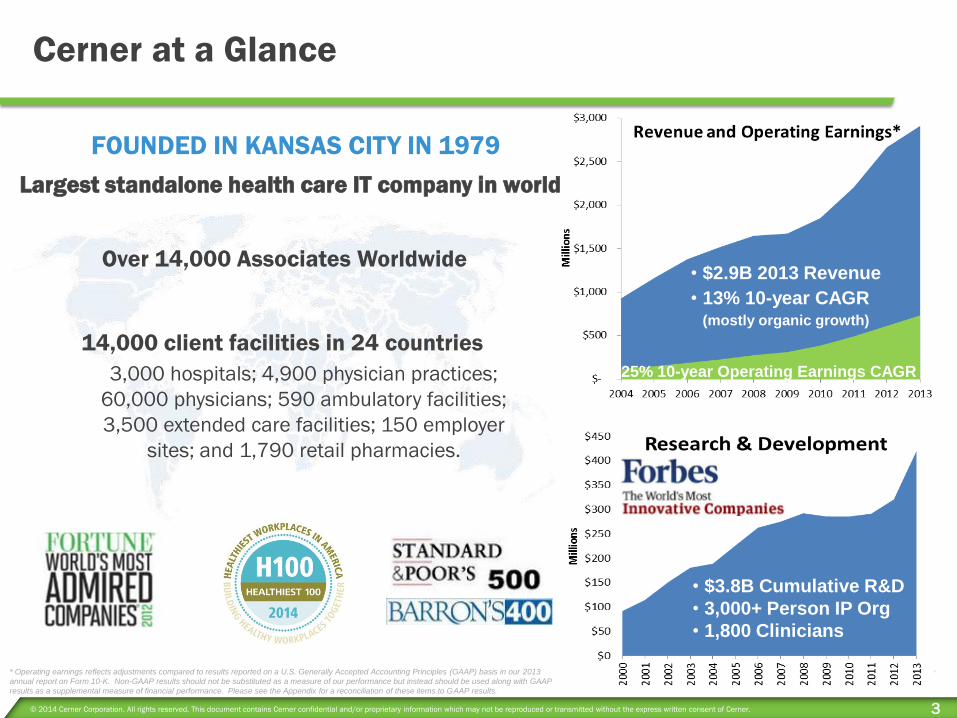

Cerner at a Glance

Over 14,000 Associates Worldwide

* Operating earnings reflects adjustments compared to results reported on a U.S. Generally Accepted Accounting Principles (GAAP) basis in our 2013

annual report on Form 10-K. Non-GAAP results should not be substituted as a measure of our performance but instead should be used along with GAAP

results as a supplemental measure of financial performance. Please see the Appendix for a reconciliation of these items to GAAP results.

• $3.8B Cumulative R&D

• 3,000+ Person IP Org

• 1,800 Clinicians

25% 10-year Operating Earnings CAGR

• $2.9B 2013 Revenue

• 13% 10-year CAGR (mostly organic growth)

14,000 client facilities in 24 countries

3,000 hospitals; 4,900 physician practices;

60,000 physicians; 590 ambulatory facilities;

3,500 extended care facilities; 150 employer

sites; and 1,790 retail pharmacies.

Largest standalone health care IT company in world

FOUNDED IN KANSAS CITY IN 1979

© 2014 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 4

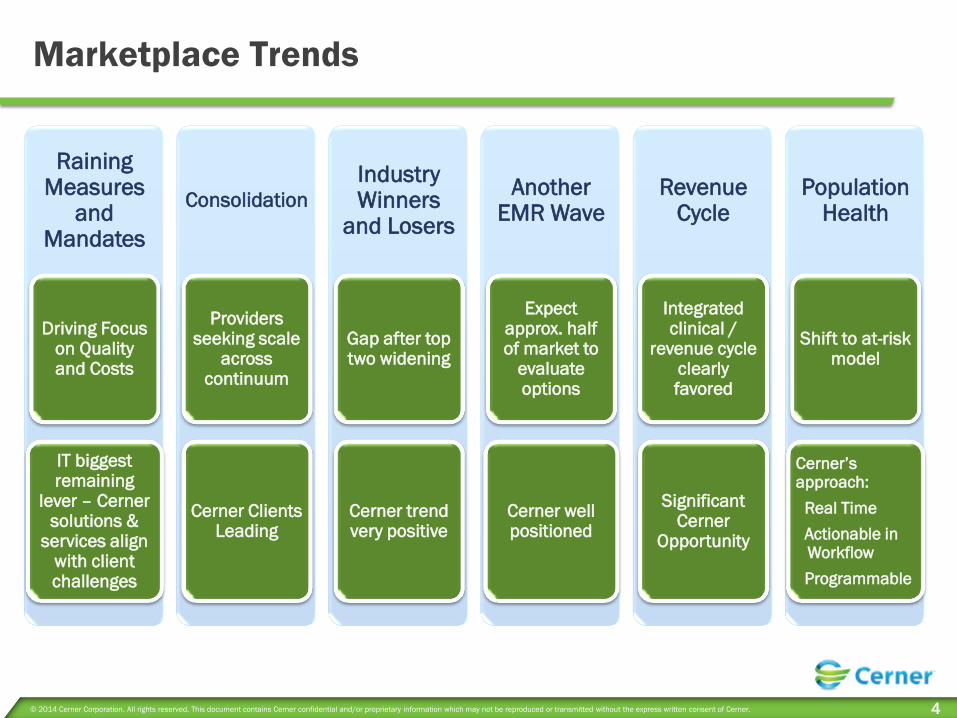

Marketplace Trends

Raining Measures

and Mandates

Driving Focus on Quality and Costs

IT biggest remaining

lever – Cerner solutions &

services align with client challenges

Consolidation

Providers seeking scale

across continuum

Cerner Clients Leading

Industry Winners

and Losers

Gap after top two widening

Cerner trend very positive

Another EMR Wave

Expect approx. half of market to

evaluate options

Cerner well positioned

Revenue Cycle

Integrated clinical /

revenue cycle clearly favored

Significant Cerner

Opportunity

Population Health

Shift to at-risk model

Cerner’s approach:

Real Time

Actionable in Workflow

Programmable

© 2014 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 5

EHR Incentive Program

ICD-10 Value-Based Purchasing

Readmission Reduction Program

New Electronic Claims Submission Rules

Increased Quality Metrics

Raining Measures & Mandates

Driving focus on Quality and Costs

IT biggest remaining lever

© 2013 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 6

-30

-10

10

30

50

70

90

110

130128

26 23

12

2 6

116

24 18

-12 -13

-25

104

11

-7

Acq

uir

ed H

osp

ita

ls

Potential HIT impact of Hospital M&A 2013 Cumulative Year

MEDITECH

Cerner clients accounted for 61% of buying activity

*Total Acquisitions – Total acquisitions by clients

**Potential Losses – Total acquisitions by competitors clients

Source: HIMSS Analytics 2013

**

*

EMR footprint in 17 of top 30

U.S. Health Systems

7 © Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information belonging to Cerner and/or its related affiliates which may not be reproduced or transmitted in any form or by any means without the express written consent of Cerner.

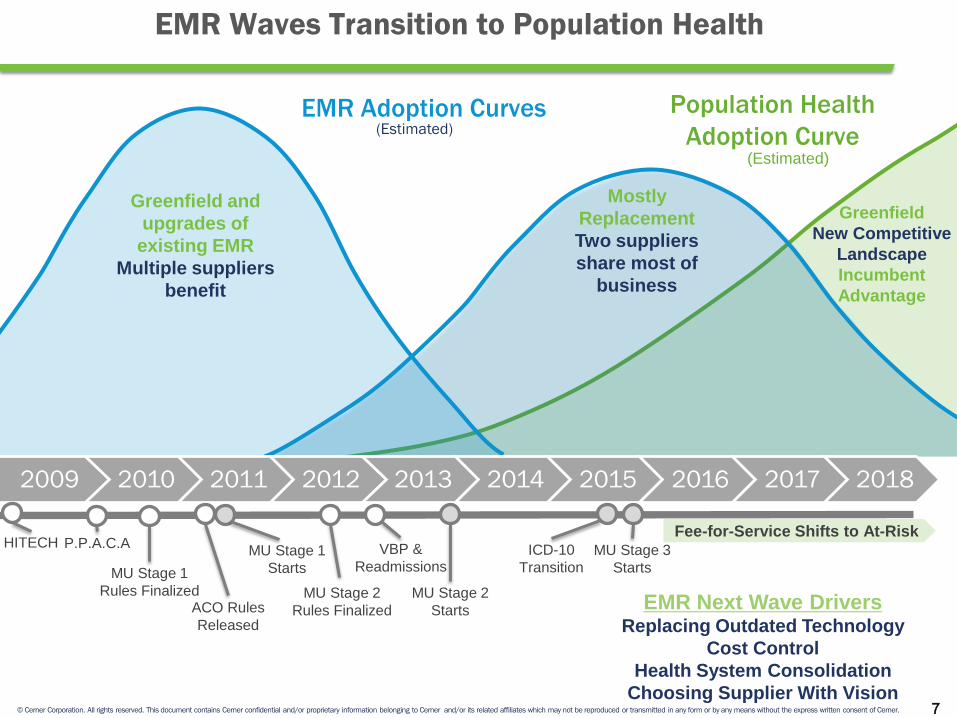

EMR Waves Transition to Population Health

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

HITECH MU Stage 1

Starts

VBP &

Readmissions

MU Stage 2

Starts

ICD-10

Transition

MU Stage 3

Starts

P.P.A.C.A

MU Stage 1

Rules Finalized MU Stage 2

Rules Finalized ACO Rules

Released

Population Health

Adoption Curve (Estimated)

EMR Adoption Curves (Estimated)

EMR Next Wave Drivers Replacing Outdated Technology

Cost Control

Health System Consolidation

Choosing Supplier With Vision

Fee-for-Service Shifts to At-Risk

Mostly

Replacement

Two suppliers

share most of

business

Greenfield and

upgrades of

existing EMR

Multiple suppliers

benefit

Greenfield

New Competitive

Landscape

Incumbent

Advantage

© 2014 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 8

Revenue Cycle

•Revenue up 51% to $156M in 2013

•Strength across all revenue cycle solutions and services

•Delivering Patient Accounting

•Over 900 live sites

•150 hospitals; 800 clinics

•Significant demand for fully integrated platform

Strong Growth &

Operational Progress

•Partner with client to manage revenue cycle operations

•Modernize revenue cycle by innovating real time – remove human intervention

•Focus on controlling cost to collect

•Preparing for future reimbursement models

RevWorks

© 2014 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 9

Population Health

Market Trends

•Fee-for-service models going away

•Providers will be accountable for health, not just care

•Will assume financial risk for defined population

•Market size estimates $10B-$50B+

•Competition

•No comprehensive approach, most rely on latent data

•Similar to failed strategy of 80s and 90s clinical solutions

Cerner’s Approach

•Healthe Intent Cloud Platform

•Facilitate optimal care and workflow across all stakeholders

•Real-time, Actionable in Workflow, Programmable

•Partnership with Advocate Heath Care

•Joint development of sophisticated predictive models

•Automating population health workflow across ACO

•Foundational Offerings (~$370M revenue)

•Interoperability and HIE offerings

•Enterprise Data Warehousing & Quality solutions

•Patient portal platform and PHR solutions

•Employer, Home Health, Long-term Care, Retail Pharmacy

“In every briefing I had with a purported PHM

solution provider I asked a simple question: What is

your process map to enable a client to effectively

move to a PHM model of care across the

community they serve with your solution suite?

Only one vendor, Cerner, was able to

articulate such a process map, everyone

else just sort of waved their hands about and spoke

of ‘high-level this, high-level that.’”

-Chilmark Research

Cerner Millennium® localized in four

languages: English, Spanish, French, German

Stage 7 Clients: Spain: Hospital Marina Salud de Dénia

Stage 6 Clients: UAE: Al Ain Hospital //Al Rahba Hospital// Madinat Zayed - Al Gharbia Hospitals// Corniche Hospital// Tawam Hospital //

Chile: Clínica las Condes

France: Centre Hospitalier de Belfort Montbéliard // Centre Hospitalier de Valenciennes //

Saudi Arabia: King Faisal Specialist Hospital & Research Center, Riyadh and Jeddah

Canada: North York General Hospital

Malaysia: Prince Court Medical Centre

2,000 Associates

Live and work outside the US

400+ Millennium facilities outside the USA

USA

1979

Saudi

Arabia

1991 Germany

1992

Malaysia

1996

Australia

1991

Spain

2005 Ireland

2005

Egypt

2005

Chile

2008

Qatar

2008

France

2005

Canada

1985

24 Total

Countries

United Arab

Emirates

2004 India

2004

Argentina

2000

Austria

1999

Switzerland

2002

Cayman Islands

2002

Singapore

1990

UK

1987

Aruba

2008 Morocco

2005

Mexico

2012

Unmatched Global Experience

$0

$50

$100

$150

$200

$250

$300

$350

$400

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Mil

lio

ns

Global Revenue

Brazil

2013

Financial Highlights and Quantifying Long-Term

Growth Opportunities

© 2014 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 12

Financial Highlights

Income statement

•Bookings

•2013: up 20% to $3.8B

•Q114: up 14% to $910M

•Revenue

•2013: up 9% to $2.9B

•Q114: Up 15% to $785M

•Adjusted Operating Margin*

•2013: up 220 basis points to 25.1%

•Q114: 24.6% (down 10 bp YoY)

•Adjusted Diluted EPS*

•2013: up 18% to $1.41

•Q114: up 12% to $0.37

•Met or exceeded guidance 56 / 57 quarters

Balance Sheet and Cash Flow – Q114

•$1.5B cash and investments

•$161M debt

•Expect strong increase in free cash flow in 2014

•Cash Deployment

•Investments in R&D and infrastructure

•$317M repurchase program

•Strategic Acquisitions

$0

$100

$200

$300

$400

$500

$600

$700

$800

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

$’s

in

Mil

lio

ns

Operating Cash Flow

Free Cash Flow*

*FCF = Operating CF less Capital Expenditures and

Capitalized Software

* Adjusted operating margin, adjusted diluted earnings per share and free cash flow reflect adjustments compared to results reported on a U.S. Generally Accepted Accounting Principles

(GAAP) basis in our 2013 annual report on Form 10-K and most recent Form 10-Q. Non-GAAP results should not be substituted as a measure of our performance but instead should be used

along with GAAP results as a supplemental measure of financial performance. Please see the Appendix for a reconciliation of these items to GAAP results.

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$0

$300

$600

$900

$1,200

$1,500

$1,800

$2,100

$2,400

$2,700

$3,000

'04 '05 '06 '07 '08 '09 '10 '11 '12 '13

EP

S

Reven

ue

($ M

illi

on

s)

Revenue

Earnings Per Share

© 2014 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 13

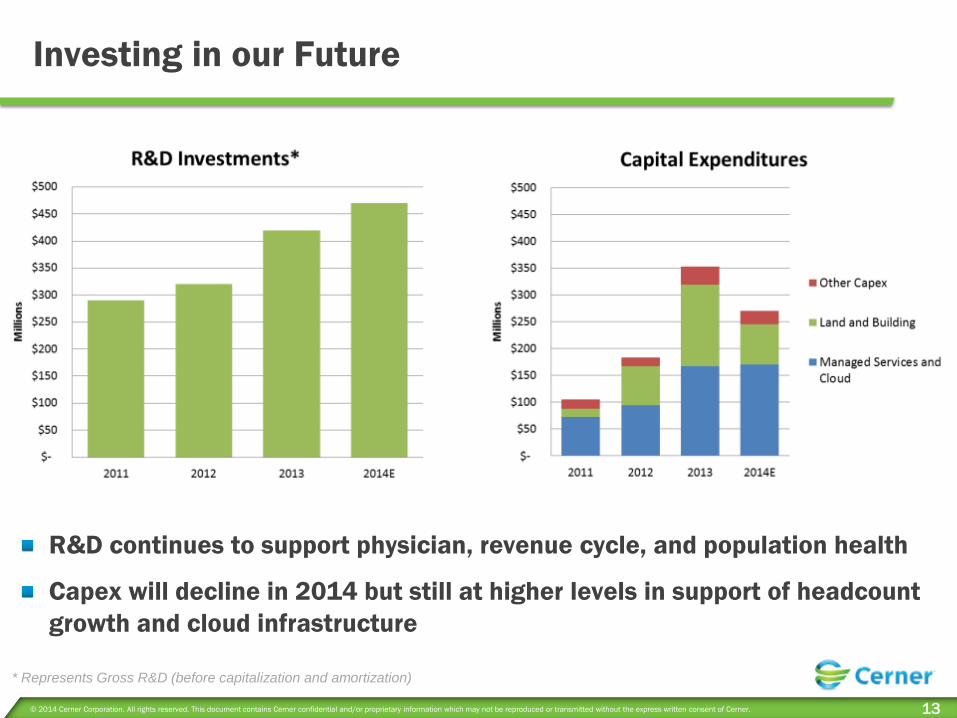

Investing in our Future

* Represents Gross R&D (before capitalization and amortization)

R&D continues to support physician, revenue cycle, and population health

Capex will decline in 2014 but still at higher levels in support of headcount

growth and cloud infrastructure

Bookings

$3,772

Cerner 2013 Business Model Sales Pipeline

Contract Backlog

$8,128

Support Contracts

and Backlog

$786

(Dollars in Millions)

* Operating margin reflects adjustments compared to

results reported on a GAAP basis in our 2013 Form

10-K. Non-GAAP results should not be substituted as

a measure of our performance but instead should be

used along with GAAP results as a supplemental

measure of financial performance. Non-GAAP

results are used by management along with GAAP

results to analyze our business, make strategic

decisions, assess long-term trends on a comparable

basis, and for management compensation purposes.

Revenue Streams Revenue

Contribution

Margin %

Contribution

Margin $

Licensed Software $388 89% $347

Technology Resale $263 18% $47

Subscription / Transaction $197 60% $119

Professional Services $851 31% $267

Managed Services $480 34% $162

Support & Maintenance $662 75% $497

Reimbursed Travel $70 0% $0

Totals $2,911 49% $1,439

Indirect Expenses

Research and Development -11% ($328)

Selling, General and Administrative -13% ($380)

Operating Margin* 25% $731

Net Other Income

Taxes -8% ($245)

Net Other Income 0.4% $12

Net Earnings 17% $498

Shares Outstanding 352.3

Diluted EPS $1.41

System

Sales

Support,

Maintenance

and Services

© 2014 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 15

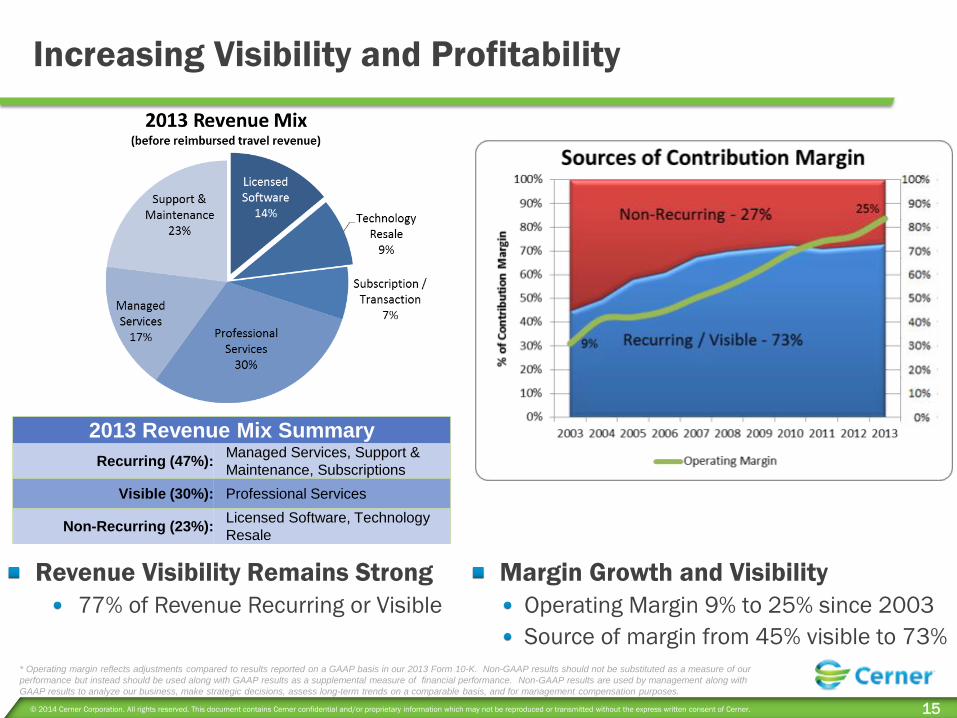

Increasing Visibility and Profitability

2013 Revenue Mix Summary

Recurring (47%): Managed Services, Support &

Maintenance, Subscriptions

Visible (30%): Professional Services

Non-Recurring (23%): Licensed Software, Technology

Resale

* Operating margin reflects adjustments compared to results reported on a GAAP basis in our 2013 Form 10-K. Non-GAAP results should not be substituted as a measure of our

performance but instead should be used along with GAAP results as a supplemental measure of financial performance. Non-GAAP results are used by management along with

GAAP results to analyze our business, make strategic decisions, assess long-term trends on a comparable basis, and for management compensation purposes.

Margin Growth and Visibility

Operating Margin 9% to 25% since 2003

Source of margin from 45% visible to 73%

Revenue Visibility Remains Strong

77% of Revenue Recurring or Visible

© 2014 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 16

Growth Initiatives Support Strong Growth

Growth scenarios do

not represent formal

financial guidance.

© 2014 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 17

Guidance as of April 24, 2014

Reg FD Disclaimer – This slide reflects guidance provided in the most recent earnings press release and

does not imply a reiteration or update of guidance.

Metric Q214 2014

Revenue $770M - $810M $3.25B - $3.4B

Adjusted Diluted Earnings Per Share $0.39 - $0.40 $1.63 - $1.67

New Business Bookings $1.00B - $1.06B

Share-based Compensation Expense $0.03 $0.11 - $0.12

* Adjusted Diluted Earnings Per Share reflects adjustments compared to results reported on a U.S. Generally Accepted Accounting Principles (GAAP) basis in our 2013 annual report on Form

10-K and most recent Form 10-Q. Non-GAAP results should not be substituted as a measure of our performance but instead should be used along with GAAP results as a supplemental

measure of financial performance. Please see the Appendix for a reconciliation of these items to GAAP results.

Health care is too important to stay the same.TM

© 2014 Cerner Corporation. All rights reserved. This document contains Cerner confidential and/or proprietary information which may not be reproduced or transmitted without the express written consent of Cerner. 19

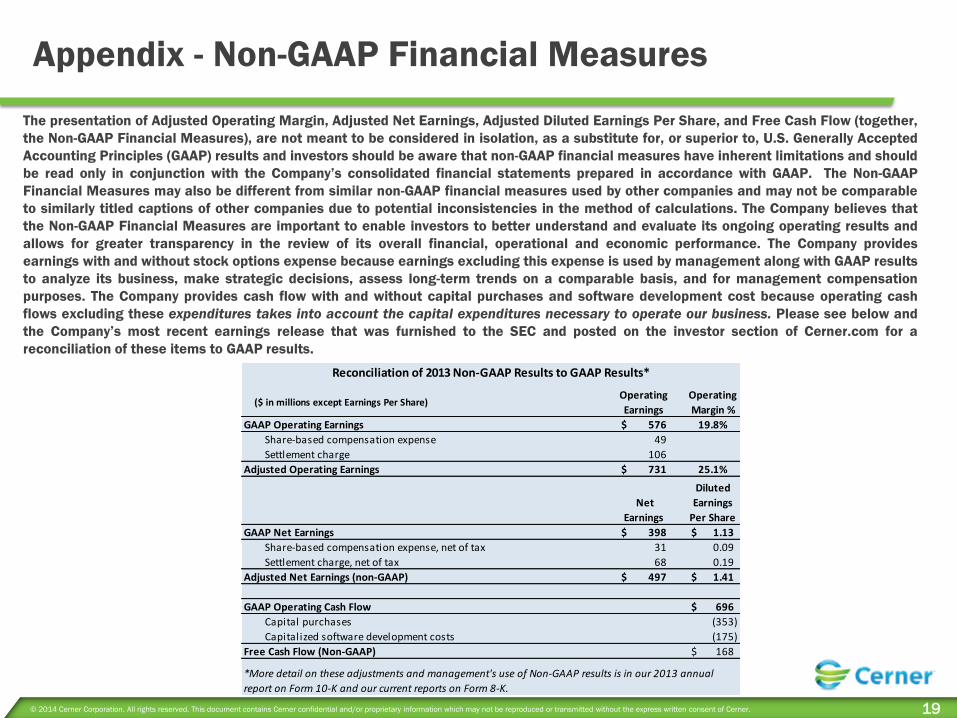

Appendix - Non-GAAP Financial Measures

The presentation of Adjusted Operating Margin, Adjusted Net Earnings, Adjusted Diluted Earnings Per Share, and Free Cash Flow (together,

the Non-GAAP Financial Measures), are not meant to be considered in isolation, as a substitute for, or superior to, U.S. Generally Accepted

Accounting Principles (GAAP) results and investors should be aware that non-GAAP financial measures have inherent limitations and should

be read only in conjunction with the Company’s consolidated financial statements prepared in accordance with GAAP. The Non-GAAP

Financial Measures may also be different from similar non-GAAP financial measures used by other companies and may not be comparable

to similarly titled captions of other companies due to potential inconsistencies in the method of calculations. The Company believes that

the Non-GAAP Financial Measures are important to enable investors to better understand and evaluate its ongoing operating results and

allows for greater transparency in the review of its overall financial, operational and economic performance. The Company provides

earnings with and without stock options expense because earnings excluding this expense is used by management along with GAAP results

to analyze its business, make strategic decisions, assess long-term trends on a comparable basis, and for management compensation

purposes. The Company provides cash flow with and without capital purchases and software development cost because operating cash

flows excluding these expenditures takes into account the capital expenditures necessary to operate our business. Please see below and

the Company’s most recent earnings release that was furnished to the SEC and posted on the investor section of Cerner.com for a

reconciliation of these items to GAAP results.

($ in millions except Earnings Per Share)Operating

Earnings

Operating

Margin %

GAAP Operating Earnings 576$ 19.8%

Share-based compensation expense 49

Settlement charge 106

Adjusted Operating Earnings 731$ 25.1%

Net

Earnings

Diluted

Earnings

Per Share

GAAP Net Earnings 398$ 1.13$

Share-based compensation expense, net of tax 31 0.09

Settlement charge, net of tax 68 0.19

Adjusted Net Earnings (non-GAAP) 497$ 1.41$

GAAP Operating Cash Flow 696$

Capital purchases (353)

Capitalized software development costs (175)

Free Cash Flow (Non-GAAP) 168$

Reconciliation of 2013 Non-GAAP Results to GAAP Results*

*More detail on these adjustments and management's use of Non-GAAP results is in our 2013 annual

report on Form 10-K and our current reports on Form 8-K.