Embed Size (px)

Citation preview

Sergey Vasnetsov Sr. Vice President Strategic Planning & Transactions August 2012

Jefferies 2012 Global Industrial and A&D Conference

lyondellbasell.com

Cautionary Statement

The information in this presentation includes forward-looking statements. These statements relate to future events, such as anticipated revenues, earnings, business strategies, competitive position or other aspects of our operations or operating results. Actual outcomes and results may differ materially from what is expressed or forecast in such forward‐looking statements. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict. Factors that could cause actual results to differ from forward-looking statements include, but are not limited to, availability, cost and price volatility of raw materials and utilities; supply/demand balances; industry production capacities and operating rates; uncertainties associated with worldwide economies; legal, tax and environmental proceedings; cyclical nature of the chemical and refining industries; operating interruptions; current and potential governmental regulatory actions; terrorist acts; international political unrest; competitive products and pricing; technological developments; the ability to comply with the terms of our credit facilities and other financing arrangements; the ability to implement business strategies; and other factors affecting our business generally as set forth in the “Risk Factors” section of our Form 10-K for the year ended December 31, 2011, which can be found at www.lyondellbasell.com on the Investor Relations page and on the Securities and Exchange Commission’s website at www.sec.gov.

This presentation contains time sensitive information that is accurate only as of the date hereof. Information contained in this presentation is unaudited and is subject to change. We undertake no obligation to update the information presented herein except as required by law.

2

lyondellbasell.com

Information Related to Financial Measures

We have included EBITDA in this presentation, which is a non-GAAP measure, as we believe that EBITDA is a measure commonly used by investors. However, EBITDA, as presented herein, may not be comparable to a similarly titled measure reported by other companies due to differences in the way the measure is calculated. For purposes of this presentation, EBITDA means earnings before interest, taxes, depreciation and amortization, as adjusted for other items management does not believe are indicative of the Company’s underlying results of operations such as impairment charges, reorganization items, the effect of mark-to-market accounting on our warrants. EBITDA also includes dividends from joint ventures. EBITDA should not be considered an alternative to profit or operating profit for any period as an indicator of our performance, or as an alternative to operating cash flows as a measure of our liquidity. See Table 9 of our accompanying earnings release for reconciliations of EBITDA to net income. While we also believe that net debt is a measure commonly used by investors, net debt, as presented herein, may not be comparable to a similarly titled measure reported by other companies due to differences in the way the measure is calculated. For purposes of this presentation, net debt means short-term debt plus current maturities of long-term debt plus long-term debt minus cash and cash equivalents and minus restricted cash.

3

lyondellbasell.com

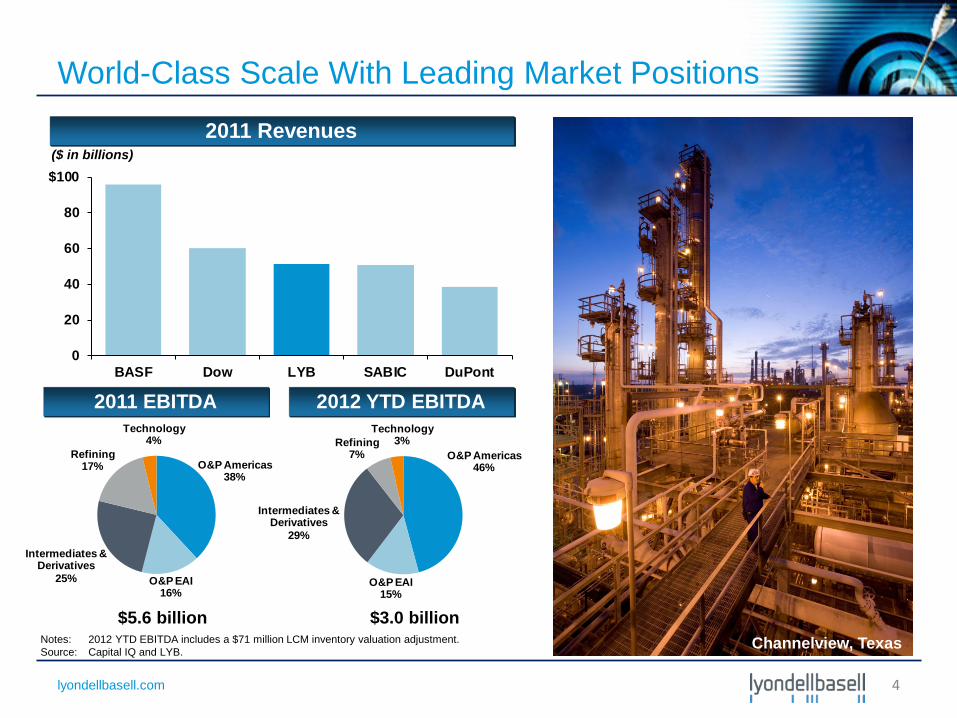

O&P Americas38%

O&P EAI16%

Intermediates & Derivatives

25%

Refining17%

Technology4%

O&P Americas46%

O&P EAI15%

Intermediates & Derivatives

29%

Refining7%

Technology3%

World-Class Scale With Leading Market Positions

$3.0 billion

Notes: 2012 YTD EBITDA includes a $71 million LCM inventory valuation adjustment. Source: Capital IQ and LYB.

2011 Revenues

2012 YTD EBITDA

($ in billions)

Channelview, Texas

4

0

20

40

60

80

$100

BASF Dow LYB SABIC DuPont

2011 EBITDA

$5.6 billion

lyondellbasell.com

500

1,000

1,500

$2,000

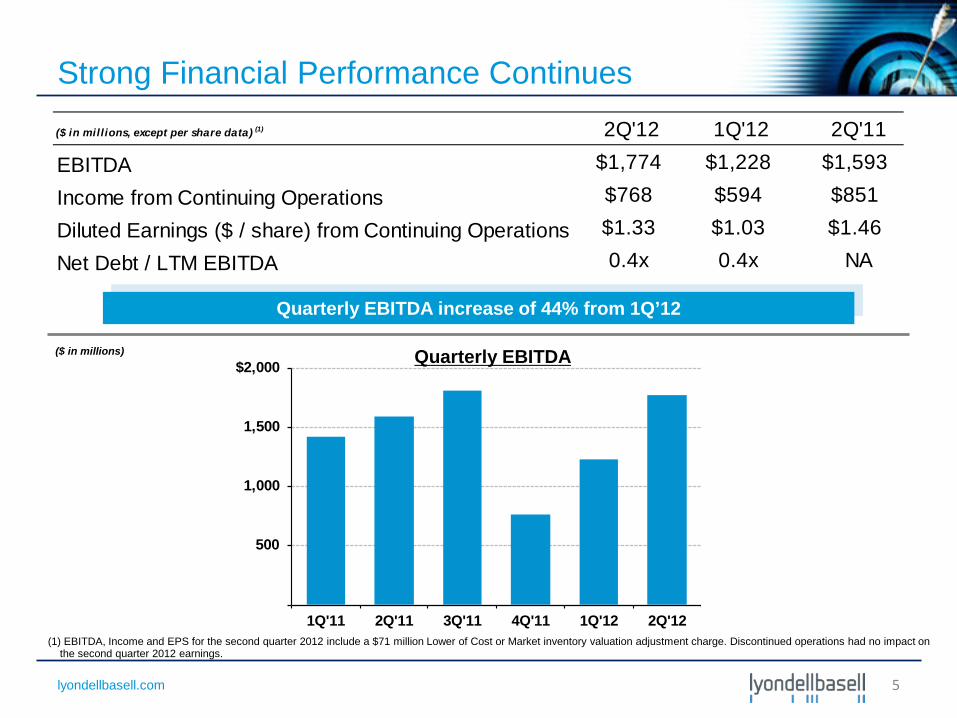

1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12

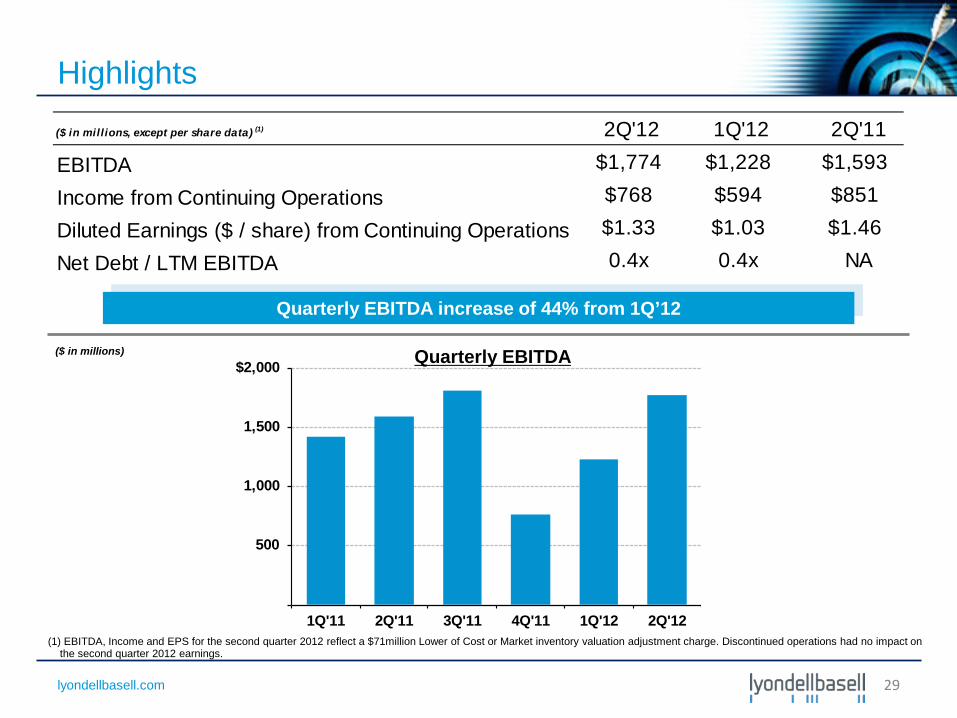

Strong Financial Performance Continues

Quarterly EBITDA

Quarterly EBITDA increase of 44% from 1Q’12

($ in millions)

5

($ in millions, except per share data) (1) 2Q'12 1Q'12 2Q'11

EBITDA $1,774 $1,228 $1,593

Income from Continuing Operations $768 $594 $851

Diluted Earnings ($ / share) from Continuing Operations $1.33 $1.03 $1.46

Net Debt / LTM EBITDA 0.4x 0.4x NA

(1) EBITDA, Income and EPS for the second quarter 2012 include a $71 million Lower of Cost or Market inventory valuation adjustment charge. Discontinued operations had no impact on the second quarter 2012 earnings.

lyondellbasell.com

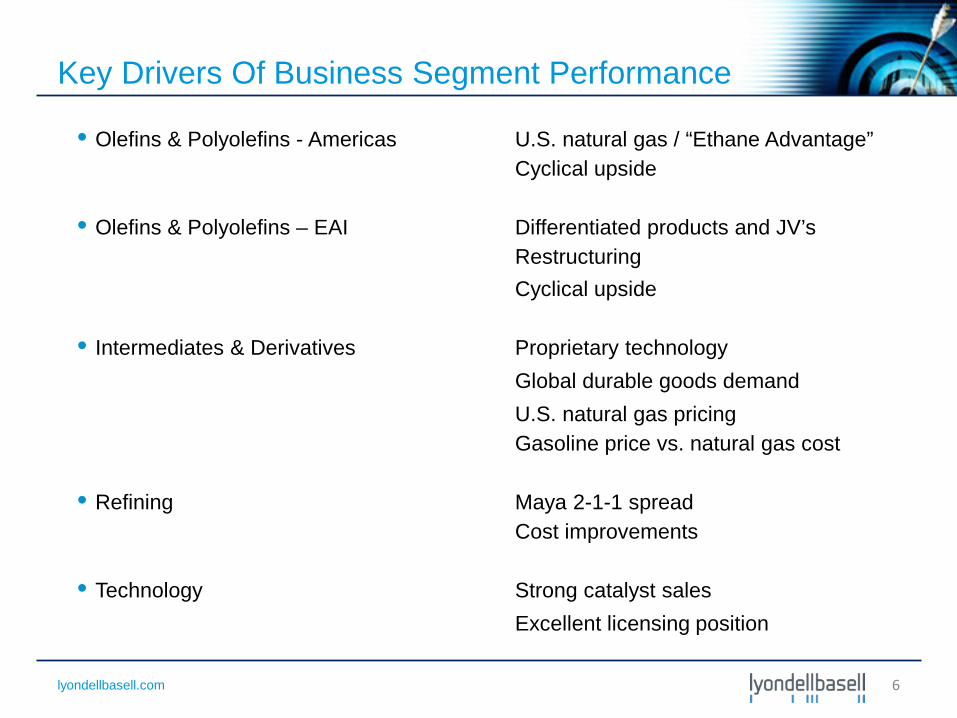

• Olefins & Polyolefins - Americas U.S. natural gas / “Ethane Advantage” Cyclical upside

• Olefins & Polyolefins – EAI Differentiated products and JV’s Restructuring Cyclical upside

• Intermediates & Derivatives Proprietary technology Global durable goods demand U.S. natural gas pricing

Gasoline price vs. natural gas cost

• Refining Maya 2-1-1 spread Cost improvements

• Technology Strong catalyst sales Excellent licensing position

Key Drivers Of Business Segment Performance

6

lyondellbasell.com

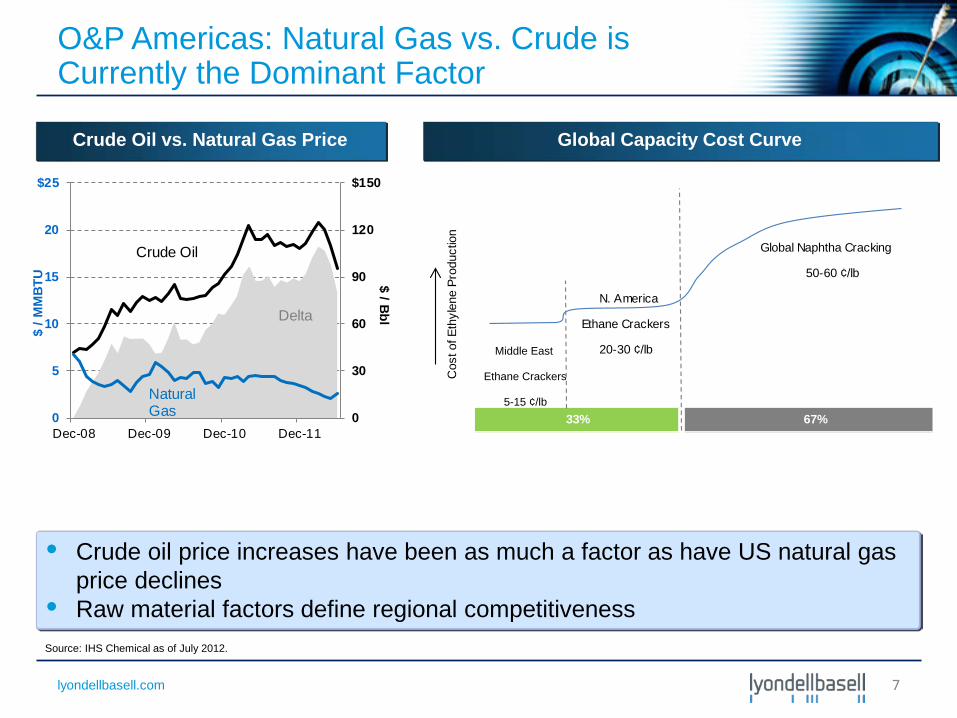

• Crude oil price increases have been as much a factor as have US natural gas price declines

• Raw material factors define regional competitiveness

Crude Oil vs. Natural Gas Price Global Capacity Cost Curve

Source: IHS Chemical as of July 2012.

67%33%

Cos

t of E

thyl

ene

Prod

uctio

n

Global Naphtha Cracking

50-60 ¢/lb

Middle East

Ethane Crackers

5-15 ¢/lb

N. America

Ethane Crackers

20-30 ¢/lb

O&P Americas: Natural Gas vs. Crude is Currently the Dominant Factor

7

0

30

60

90

120

$150

0

5

10

15

20

$25

Dec-08 Dec-09 Dec-10 Dec-11

$ / Bbl

$ / M

MBT

U

Crude Oil

Natural Gas

Delta

lyondellbasell.com

0

20

40

60

80

NE AsiaNaphtha

U.S. Naphtha U.S. Propane U.S. Ethane

2Q11 1Q12 2Q12

Indexed Commodity Prices Cost of Ethylene Production

Source: IHS Chemical.

8

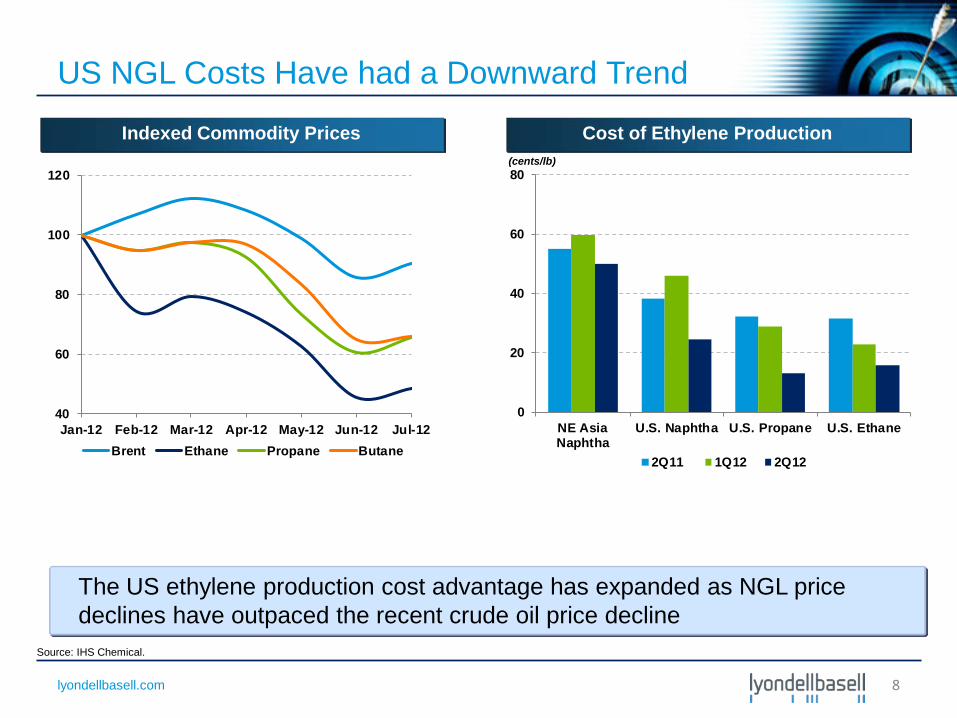

US NGL Costs Have had a Downward Trend

The US ethylene production cost advantage has expanded as NGL price declines have outpaced the recent crude oil price decline

40

60

80

100

120

Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12Brent Ethane Propane Butane

(cents/lb)

lyondellbasell.com

0

1

2

3

4

5

Dry Gas Rich Gas (2.5GPM) Very Rich Gas(5.5GPM)

$/M

MBT

UFeb'12 Jul'12

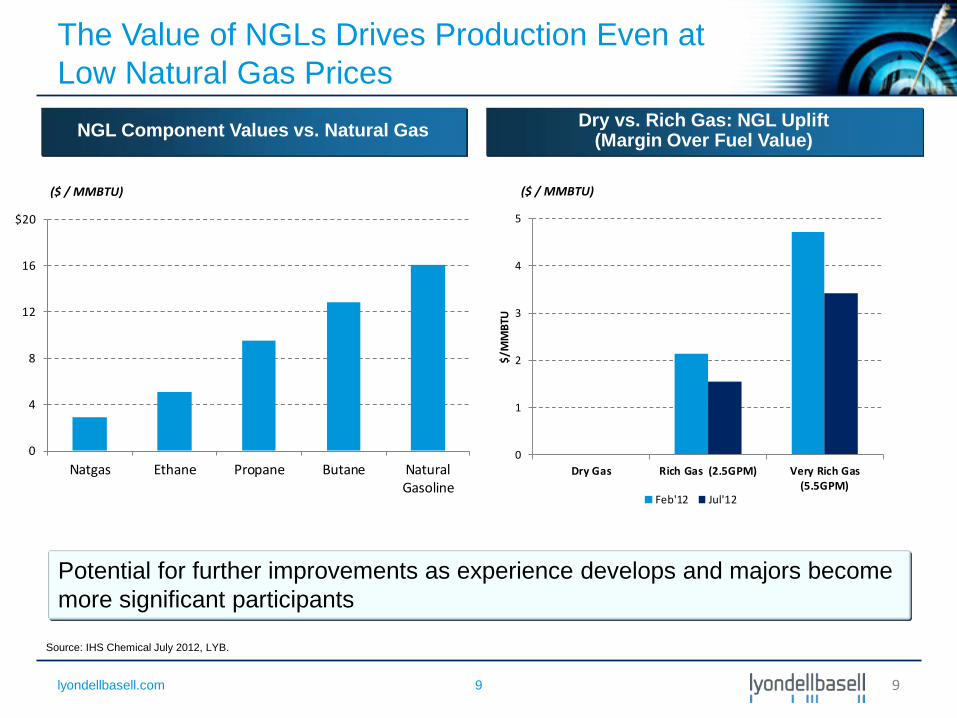

The Value of NGLs Drives Production Even at Low Natural Gas Prices

9

Dry vs. Rich Gas: NGL Uplift (Margin Over Fuel Value) NGL Component Values vs. Natural Gas

Potential for further improvements as experience develops and majors become more significant participants

Source: IHS Chemical July 2012, LYB.

9

($ / MMBTU) ($ / MMBTU)

0

4

8

12

16

$20

Natgas Ethane Propane Butane NaturalGasoline

lyondellbasell.com

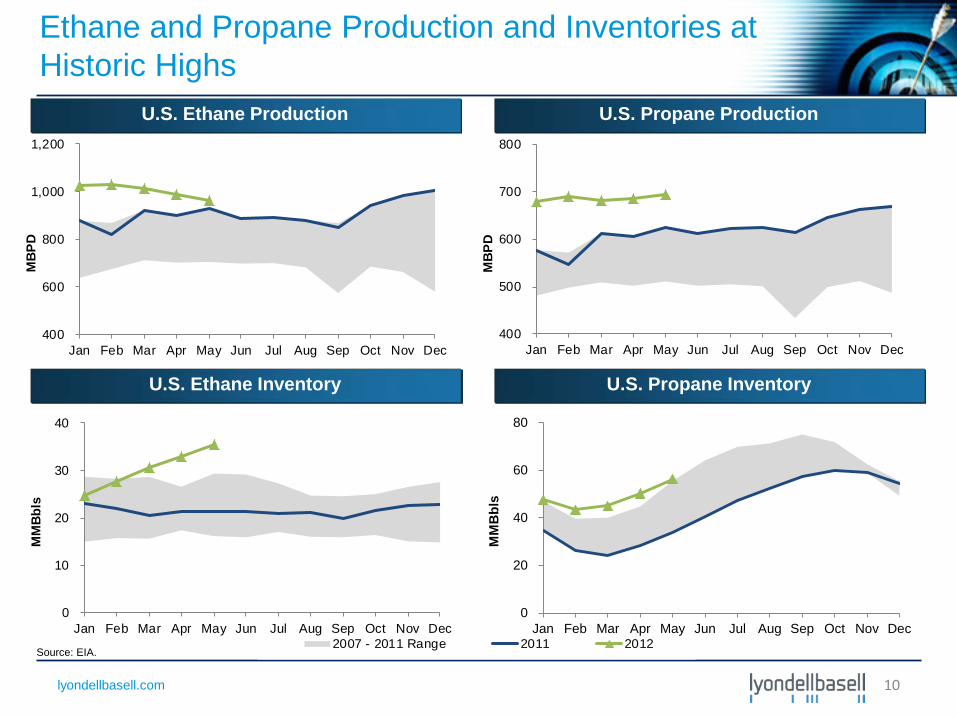

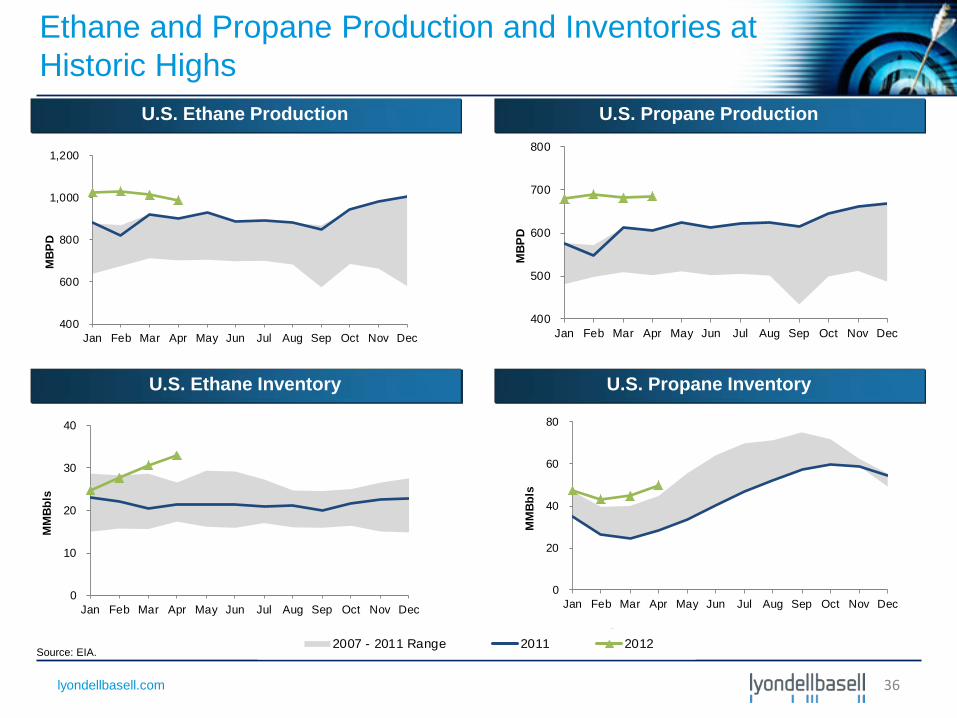

Ethane and Propane Production and Inventories at Historic Highs

U.S. Ethane Production U.S. Propane Production

2007 - 2011 Range 2011 2012

U.S. Ethane Inventory U.S. Propane Inventory

Source: EIA.

10

400

600

800

1,000

1,200

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MBP

D

400

500

600

700

800

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MBP

D

0

10

20

30

40

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MM

Bbls

0

20

40

60

80

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MM

Bbl

s

lyondellbasell.com

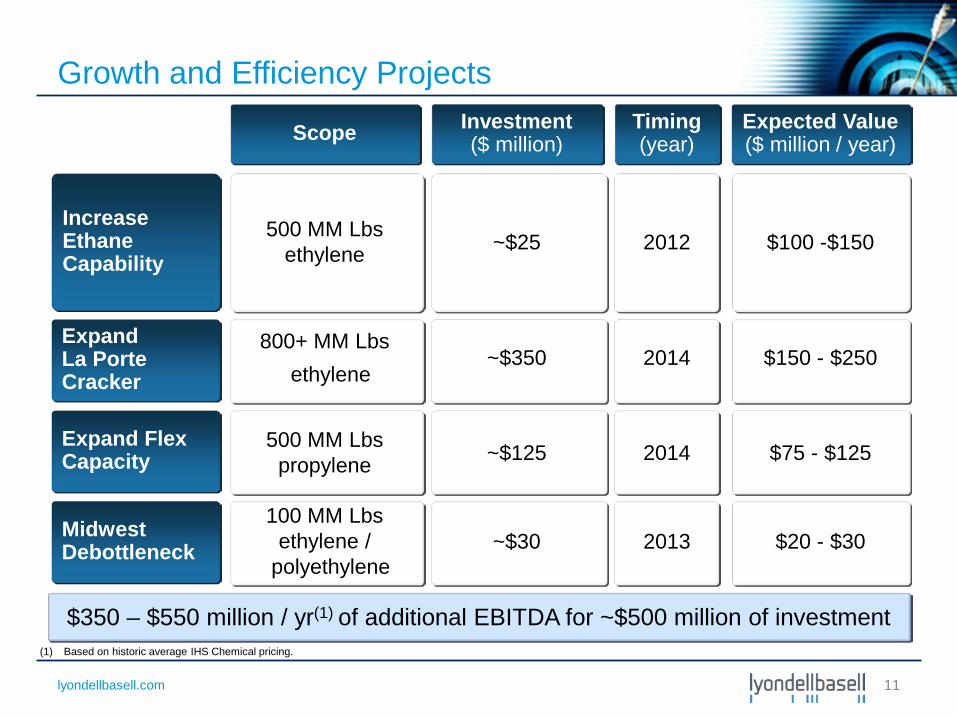

Growth and Efficiency Projects

Increase Ethane Capability

Expand La Porte Cracker

Scope

Expand Flex Capacity

500 MM Lbs ethylene

Investment ($ million)

Timing (year)

Expected Value ($ million / year)

800+ MM Lbs ethylene

100 MM Lbs ethylene /

polyethylene

Midwest Debottleneck

500 MM Lbs propylene

~$25

~$350

~$30

~$125

2012

2014

2013

2014

$100 -$150

$150 - $250

$20 - $30

$75 - $125

$350 – $550 million / yr(1) of additional EBITDA for ~$500 million of investment (1) Based on historic average IHS Chemical pricing.

11

lyondellbasell.com

----

300

600

900

1,200

1,500

2012 2013 2014 2015

U.S. LYB

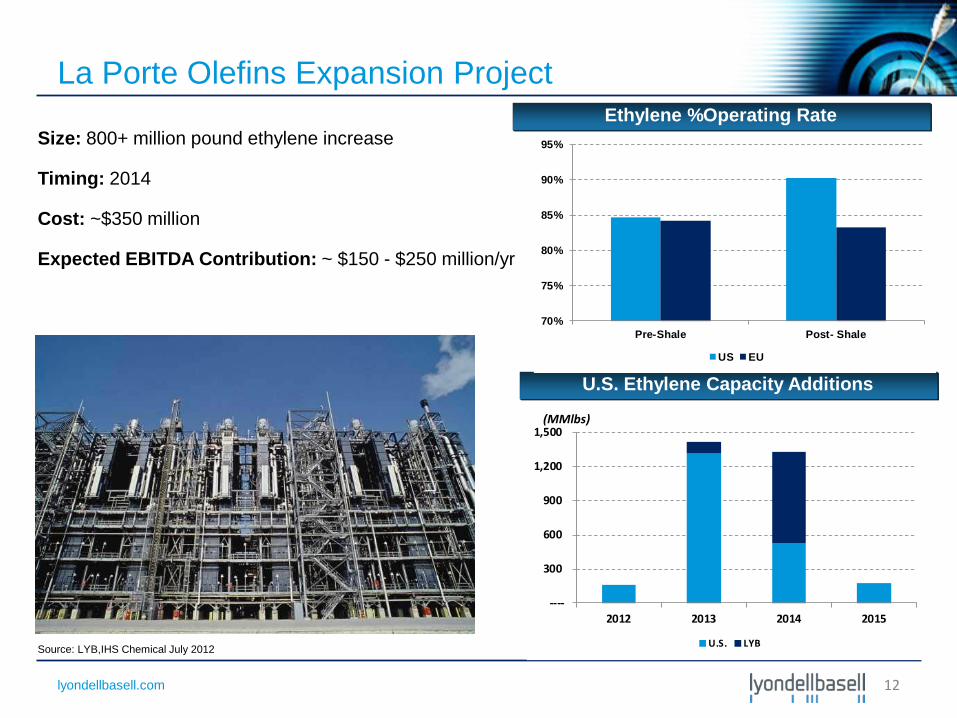

La Porte Olefins Expansion Project

12

Size: 800+ million pound ethylene increase Timing: 2014 Cost: ~$350 million Expected EBITDA Contribution: ~ $150 - $250 million/yr

La Porte, Texas Source: LYB,IHS Chemical July 2012

Ethylene %Operating Rate

U.S. Ethylene Capacity Additions

(MMlbs)

70%

75%

80%

85%

90%

95%

Pre-Shale Post- Shale

US EU

lyondellbasell.com

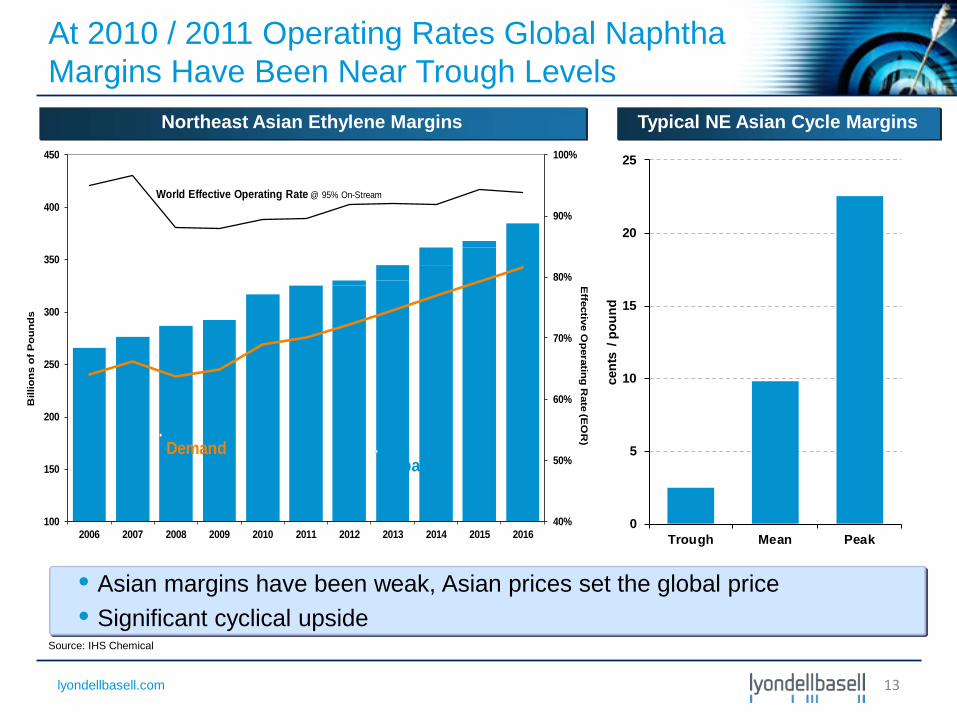

At 2010 / 2011 Operating Rates Global Naphtha Margins Have Been Near Trough Levels

Typical NE Asian Cycle Margins Northeast Asian Ethylene Margins

Source: IHS Chemical

• Asian margins have been weak, Asian prices set the global price • Significant cyclical upside

0

5

10

15

20

25

Trough Mean Peak

cent

s / p

ound

13

40%

50%

60%

70%

80%

90%

100%

100

150

200

250

300

350

400

450

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Effective O

perating Rate (E

OR

)

Bill

ions

of P

ound

s

DemandCapacity

World Effective Operating Rate @ 95% On-Stream

lyondellbasell.com

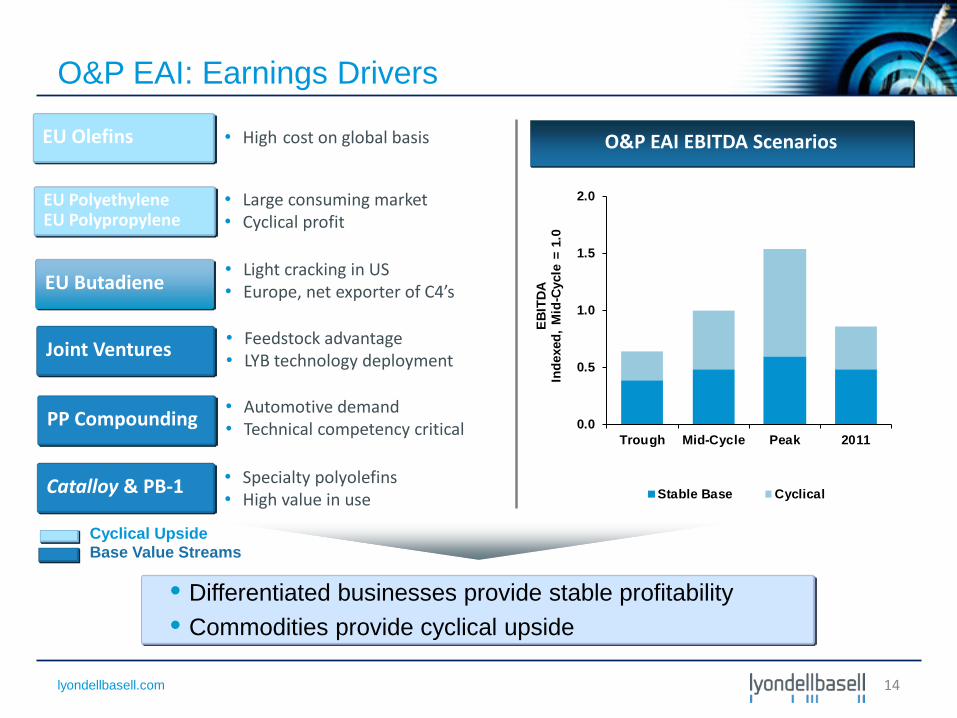

O&P EAI: Earnings Drivers

• Differentiated businesses provide stable profitability • Commodities provide cyclical upside

• High cost on global basis EU Olefins

• Specialty polyolefins • High value in use

Joint Ventures • Feedstock advantage • LYB technology deployment

Catalloy & PB-1

PP Compounding • Automotive demand • Technical competency critical

EU Polyethylene EU Polypropylene

• Large consuming market • Cyclical profit

Base Value Streams Cyclical Upside

O&P EAI EBITDA Scenarios

EU Butadiene • Light cracking in US • Europe, net exporter of C4’s

0.0

0.5

1.0

1.5

2.0

Trough Mid-Cycle Peak 2011

EBIT

DA

Inde

xed,

Mid

-Cyc

le =

1.0

Stable Base Cyclical

14

lyondellbasell.com

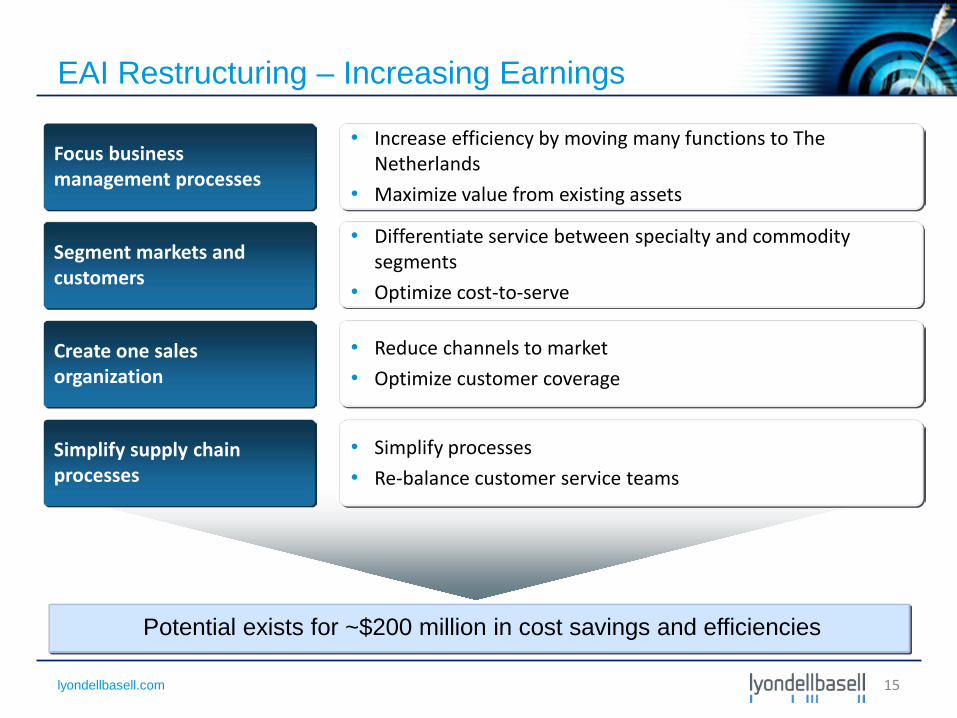

EAI Restructuring – Increasing Earnings

Potential exists for ~$200 million in cost savings and efficiencies

Focus business management processes

Segment markets and customers

Create one sales organization

Simplify supply chain processes

• Increase efficiency by moving many functions to The Netherlands

• Maximize value from existing assets

• Differentiate service between specialty and commodity segments

• Optimize cost-to-serve

• Reduce channels to market • Optimize customer coverage

• Simplify processes • Re-balance customer service teams

15

lyondellbasell.com

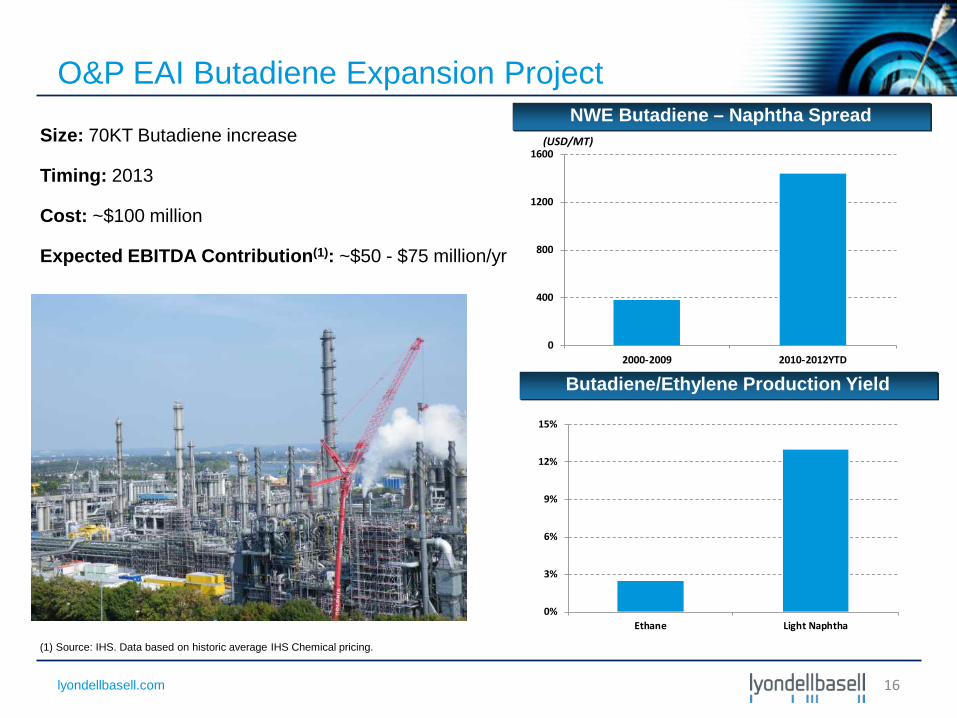

O&P EAI Butadiene Expansion Project

(1) Source: IHS. Data based on historic average IHS Chemical pricing.

16

Size: 70KT Butadiene increase Timing: 2013 Cost: ~$100 million Expected EBITDA Contribution(1): ~$50 - $75 million/yr

0

400

800

1200

1600

2000-2009 2010-2012YTD

NWE Butadiene – Naphtha Spread (USD/MT)

Butadiene/Ethylene Production Yield

0%

3%

6%

9%

12%

15%

Ethane Light Naphtha

lyondellbasell.com

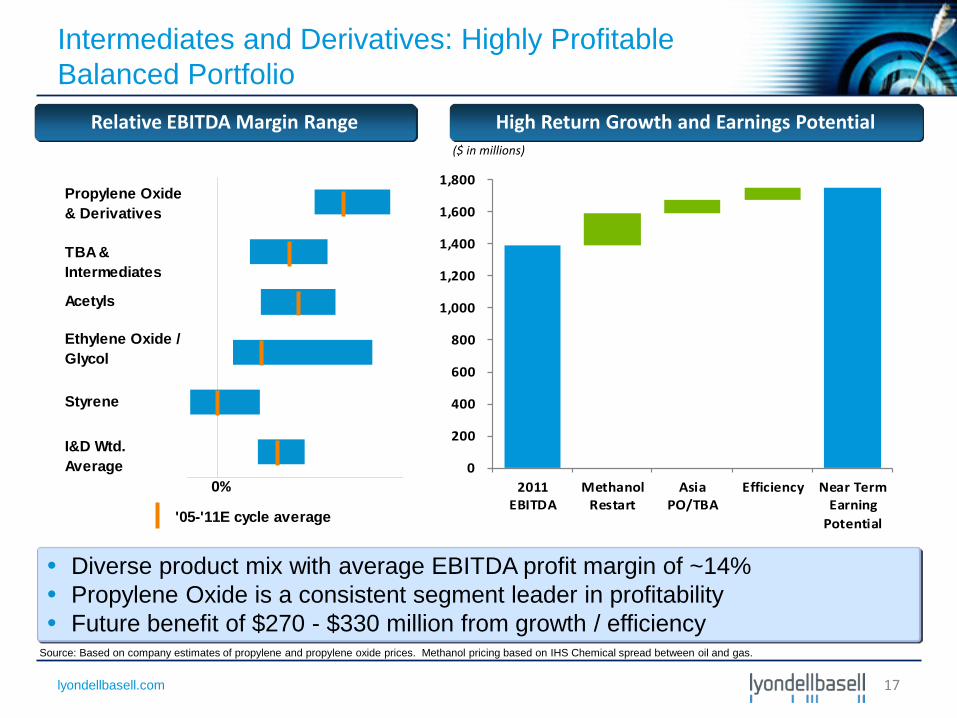

Propylene Oxide& Derivatives

TBA &Intermediates

Acetyls

Ethylene Oxide /Glycol

Styrene

I&D Wtd. Average

'05-'11E cycle average

Propylene Oxide & Derivatives

TBA & Intermediates

Acetyls

Ethylene Oxide / Glycol

Styrene

I&D Wtd. Average

Intermediates and Derivatives: Highly Profitable Balanced Portfolio

• Diverse product mix with average EBITDA profit margin of ~14% • Propylene Oxide is a consistent segment leader in profitability • Future benefit of $270 - $330 million from growth / efficiency

High Return Growth and Earnings Potential Relative EBITDA Margin Range

0%

Source: Based on company estimates of propylene and propylene oxide prices. Methanol pricing based on IHS Chemical spread between oil and gas.

($ in millions)

17

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2011EBITDA

MethanolRestart

AsiaPO/TBA

Efficiency Near TermEarning

Potential

lyondellbasell.com

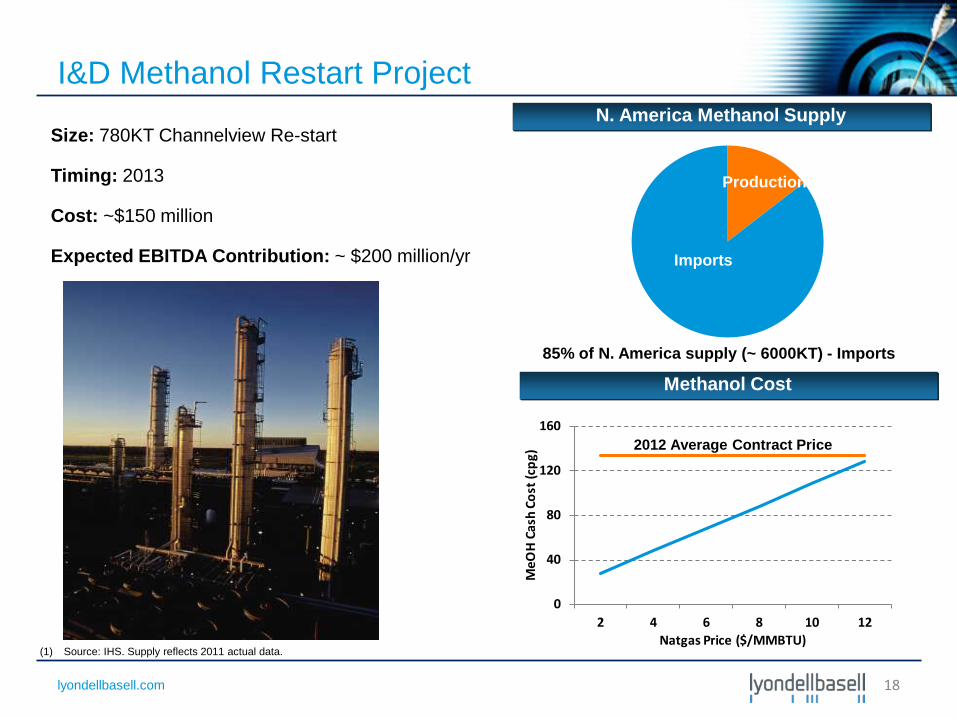

I&D Methanol Restart Project

(1) Source: IHS. Supply reflects 2011 actual data.

18

Size: 780KT Channelview Re-start Timing: 2013 Cost: ~$150 million Expected EBITDA Contribution: ~ $200 million/yr

N. America Methanol Supply

Methanol Cost

0

40

80

120

160

2 4 6 8 10 12

MeO

H C

ash

Cost

(cpg

)

Natgas Price ($/MMBTU)

85% of N. America supply (~ 6000KT) - Imports

Imports

2012 Average Contract Price

Production

lyondellbasell.com

0

50

100

150

200

250

300

2008 2009 2010 2011 2012 YTD

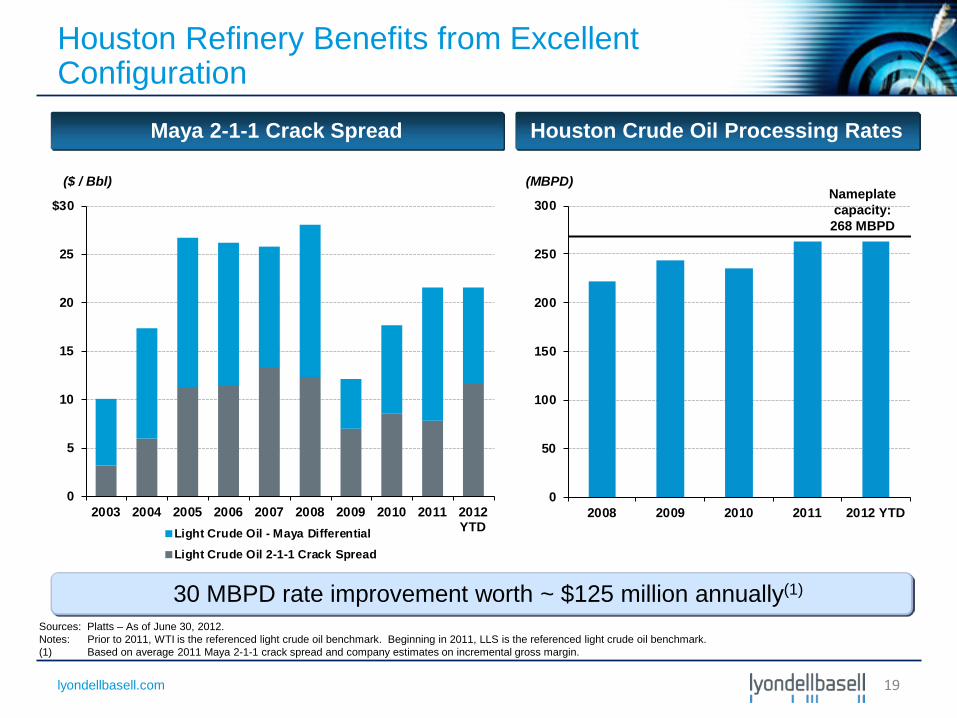

Sources: Platts – As of June 30, 2012. Notes: Prior to 2011, WTI is the referenced light crude oil benchmark. Beginning in 2011, LLS is the referenced light crude oil benchmark. (1) Based on average 2011 Maya 2-1-1 crack spread and company estimates on incremental gross margin.

30 MBPD rate improvement worth ~ $125 million annually(1)

Houston Crude Oil Processing Rates

(MBPD)

Maya 2-1-1 Crack Spread

($ / Bbl) Nameplate capacity:

268 MBPD

19

Houston Refinery Benefits from Excellent Configuration

0

5

10

15

20

25

$30

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012YTDLight Crude Oil - Maya Differential

Light Crude Oil 2-1-1 Crack Spread

lyondellbasell.com

$0

$200

$400

$600

$800

'10 '11 2012 ProForma

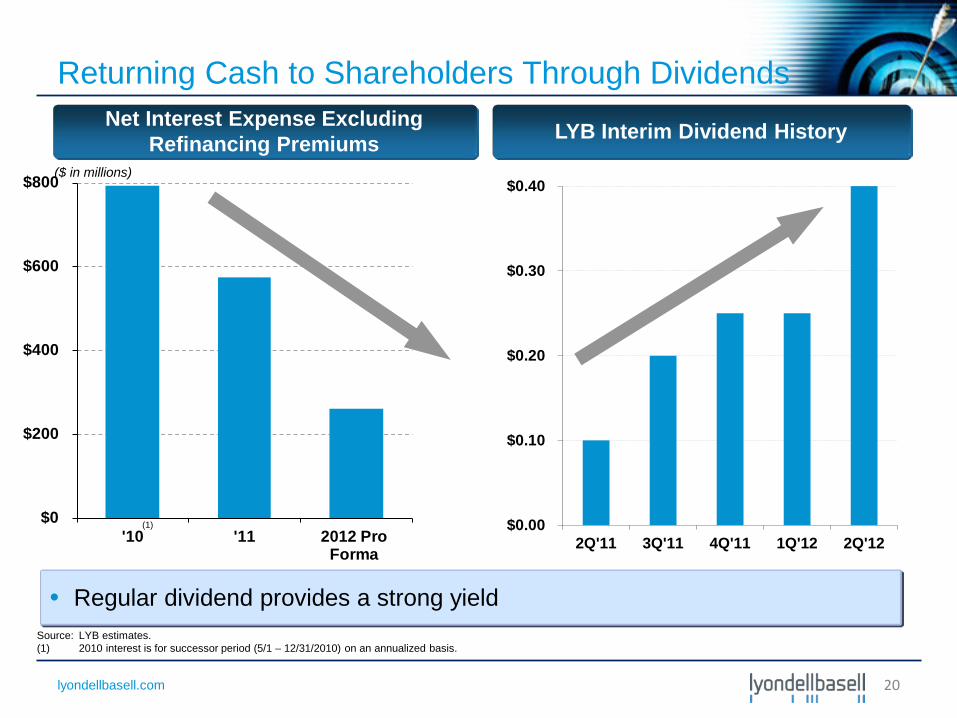

Returning Cash to Shareholders Through Dividends

• Regular dividend provides a strong yield

LYB Interim Dividend History Net Interest Expense Excluding Refinancing Premiums

Source: LYB estimates. (1) 2010 interest is for successor period (5/1 – 12/31/2010) on an annualized basis.

20

($ in millions)

(1) $0.00

$0.10

$0.20

$0.30

$0.40

2Q'11 3Q'11 4Q'11 1Q'12 2Q'12

lyondellbasell.com

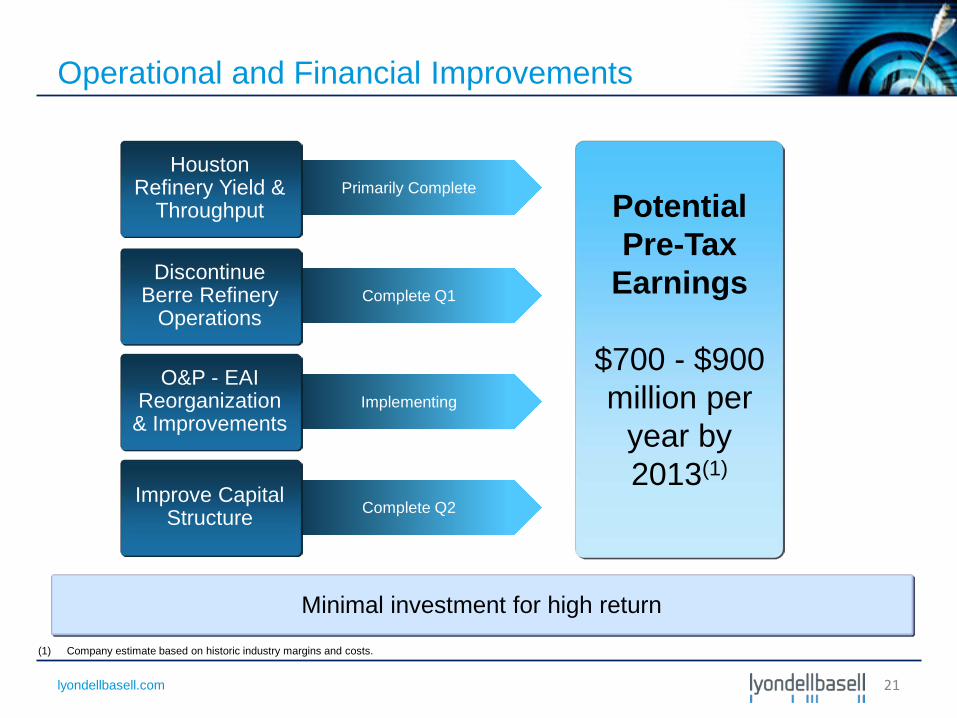

Primarily Complete

Complete Q1

Implementing

Complete Q2

Operational and Financial Improvements

Houston Refinery Yield &

Throughput

Discontinue Berre Refinery

Operations

O&P - EAI Reorganization

& Improvements

Improve Capital Structure

Minimal investment for high return

Potential Pre-Tax

Earnings

$700 - $900 million per

year by 2013(1)

(1) Company estimate based on historic industry margins and costs.

21

lyondellbasell.com

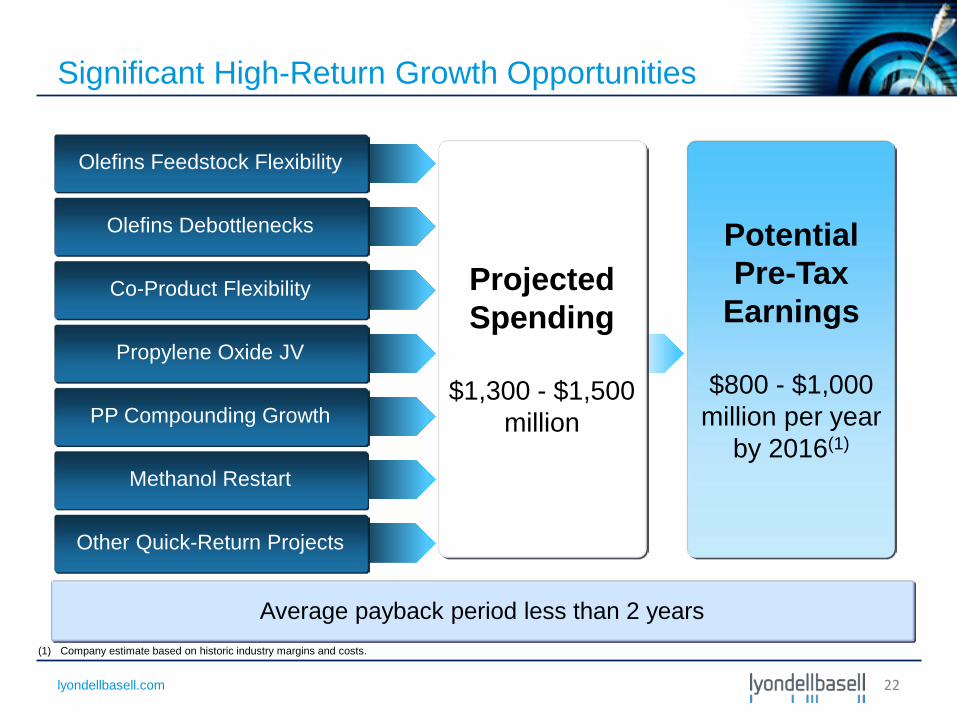

Significant High-Return Growth Opportunities

Other Quick-Return Projects

Olefins Feedstock Flexibility

Olefins Debottlenecks

Co-Product Flexibility

Average payback period less than 2 years

Propylene Oxide JV

PP Compounding Growth

Methanol Restart

Projected Spending

$1,300 - $1,500

million

Potential Pre-Tax

Earnings

$800 - $1,000 million per year

by 2016(1)

(1) Company estimate based on historic industry margins and costs.

22

lyondellbasell.com

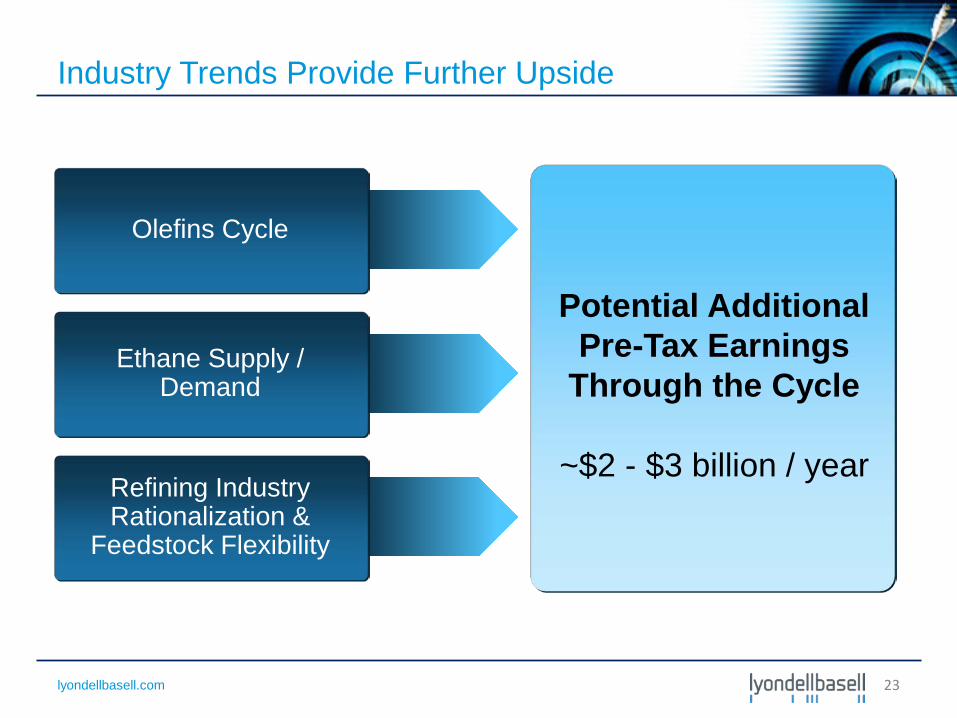

Industry Trends Provide Further Upside

Olefins Cycle

Ethane Supply / Demand

Refining Industry Rationalization &

Feedstock Flexibility

Potential Additional Pre-Tax Earnings

Through the Cycle

~$2 - $3 billion / year

23

lyondellbasell.com

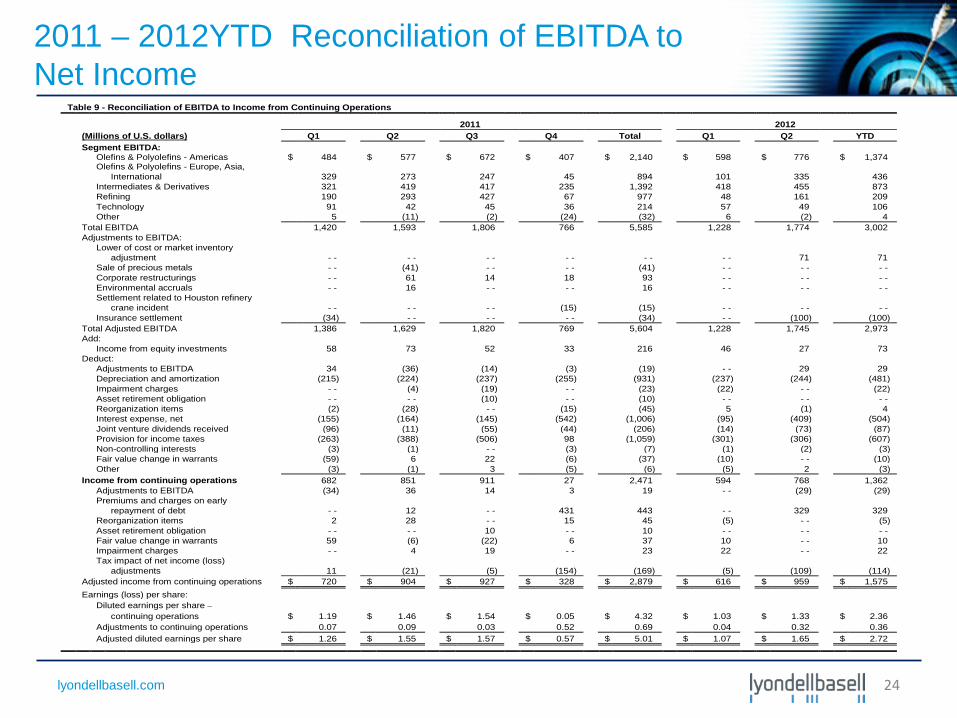

2011 – 2012YTD Reconciliation of EBITDA to Net Income

24

Table 9 - Reconciliation of EBITDA to Income from Continuing Operations 2011 2012 (Millions of U.S. dollars) Q1 Q2 Q3 Q4 Total Q1 Q2 YTD Segment EBITDA: Olefins & Polyolefins - Americas $ 484 $ 577 $ 672 $ 407 $ 2,140 $ 598 $ 776 $ 1,374 Olefins & Polyolefins - Europe, Asia, International 329 273 247 45 894 101 335 436 Intermediates & Derivatives 321 419 417 235 1,392 418 455 873 Refining 190 293 427 67 977 48 161 209 Technology 91 42 45 36 214 57 49 106 Other 5 (11) (2) (24) (32) 6 (2) 4 Total EBITDA 1,420 1,593 1,806 766 5,585 1,228 1,774 3,002 Adjustments to EBITDA: Lower of cost or market inventory adjustment - - - - - - - - - - - - 71 71 Sale of precious metals - - (41) - - - - (41) - - - - - - Corporate restructurings - - 61 14 18 93 - - - - - - Environmental accruals - - 16 - - - - 16 - - - - - - Settlement related to Houston refinery crane incident - - - - - - (15) (15) - - - - - - Insurance settlement (34) - - - - - - (34) - - (100) (100) Total Adjusted EBITDA 1,386 1,629 1,820 769 5,604 1,228 1,745 2,973 Add: Income from equity investments 58 73 52 33 216 46 27 73 Deduct: Adjustments to EBITDA 34 (36) (14) (3) (19) - - 29 29 Depreciation and amortization (215) (224) (237) (255) (931) (237) (244) (481) Impairment charges - - (4) (19) - - (23) (22) - - (22) Asset retirement obligation - - - - (10) - - (10) - - - - - - Reorganization items (2) (28) - - (15) (45) 5 (1) 4 Interest expense, net (155) (164) (145) (542) (1,006) (95) (409) (504) Joint venture dividends received (96) (11) (55) (44) (206) (14) (73) (87) Provision for income taxes (263) (388) (506) 98 (1,059) (301) (306) (607) Non-controlling interests (3) (1) - - (3) (7) (1) (2) (3) Fair value change in warrants (59) 6 22 (6) (37) (10) - - (10) Other (3) (1) 3 (5) (6) (5) 2 (3) Income from continuing operations 682 851 911 27 2,471 594 768 1,362 Adjustments to EBITDA (34) 36 14 3 19 - - (29) (29) Premiums and charges on early repayment of debt - - 12 - - 431 443 - - 329 329 Reorganization items 2 28 - - 15 45 (5) - - (5) Asset retirement obligation - - - - 10 - - 10 - - - - - - Fair value change in warrants 59 (6) (22) 6 37 10 - - 10 Impairment charges - - 4 19 - - 23 22 - - 22 Tax impact of net income (loss) adjustments 11 (21) (5) (154) (169) (5) (109) (114) Adjusted income from continuing operations $ 720 $ 904 $ 927 $ 328 $ 2,879 $ 616 $ 959 $ 1,575 Earnings (loss) per share: Diluted earnings per share – continuing operations $ 1.19 $ 1.46 $ 1.54 $ 0.05 $ 4.32 $ 1.03 $ 1.33 $ 2.36 Adjustments to continuing operations 0.07 0.09 0.03 0.52 0.69 0.04 0.32 0.36 Adjusted diluted earnings per share $ 1.26 $ 1.55 $ 1.57 $ 0.57 $ 5.01 $ 1.07 $ 1.65 $ 2.72

lyondellbasell.com

Back-up

25

lyondellbasell.com

Jim Gallogly, Chief Executive Officer Karyn Ovelmen, Chief Financial Officer Sergey Vasnetsov, SVP - Strategic Planning and Transactions Doug Pike, VP - Investor Relations July 27, 2012

Second-Quarter 2012 Earnings

lyondellbasell.com

Cautionary Statement

The information in this presentation includes forward-looking statements. These statements relate to future events, such as anticipated revenues, earnings, business strategies, competitive position or other aspects of our operations or operating results. Actual outcomes and results may differ materially from what is expressed or forecast in such forward‐looking statements. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict. Factors that could cause actual results to differ from forward-looking statements include, but are not limited to, availability, cost and price volatility of raw materials and utilities; supply/demand balances; industry production capacities and operating rates; uncertainties associated with worldwide economies; legal, tax and environmental proceedings; cyclical nature of the chemical and refining industries; operating interruptions; current and potential governmental regulatory actions; terrorist acts; international political unrest; competitive products and pricing; technological developments; the ability to comply with the terms of our credit facilities and other financing arrangements; the ability to implement business strategies; and other factors affecting our business generally as set forth in the “Risk Factors” section of our Form 10-K for the year ended December 31, 2011, which can be found at www.lyondellbasell.com on the Investor Relations page and on the Securities and Exchange Commission’s website at www.sec.gov.

This presentation contains time sensitive information that is accurate only as of the date hereof. Information contained in this presentation is unaudited and is subject to change. We undertake no obligation to update the information presented herein except as required by law.

27

lyondellbasell.com

Information Related to Financial Measures

We have included EBITDA in this presentation, which is a non-GAAP measure, as we believe that EBITDA is a measure commonly used by investors. However, EBITDA, as presented herein, may not be comparable to a similarly titled measure reported by other companies due to differences in the way the measure is calculated. For purposes of this presentation, EBITDA means earnings before interest, taxes, depreciation and amortization, as adjusted for other items management does not believe are indicative of the Company’s underlying results of operations such as impairment charges, reorganization items, the effect of mark-to-market accounting on our warrants. EBITDA also includes dividends from joint ventures. EBITDA should not be considered an alternative to profit or operating profit for any period as an indicator of our performance, or as an alternative to operating cash flows as a measure of our liquidity. See Table 9 of our accompanying earnings release for reconciliations of EBITDA to net income. While we also believe that net debt is a measure commonly used by investors, net debt, as presented herein, may not be comparable to a similarly titled measure reported by other companies due to differences in the way the measure is calculated. For purposes of this presentation, net debt means short-term debt plus current maturities of long-term debt plus long-term debt minus cash and cash equivalents and minus restricted cash.

28

lyondellbasell.com

500

1,000

1,500

$2,000

1Q'11 2Q'11 3Q'11 4Q'11 1Q'12 2Q'12

Highlights

Quarterly EBITDA

Quarterly EBITDA increase of 44% from 1Q’12

($ in millions)

29

($ in millions, except per share data) (1) 2Q'12 1Q'12 2Q'11

EBITDA $1,774 $1,228 $1,593

Income from Continuing Operations $768 $594 $851

Diluted Earnings ($ / share) from Continuing Operations $1.33 $1.03 $1.46

Net Debt / LTM EBITDA 0.4x 0.4x NA

(1) EBITDA, Income and EPS for the second quarter 2012 reflect a $71million Lower of Cost or Market inventory valuation adjustment charge. Discontinued operations had no impact on the second quarter 2012 earnings.

lyondellbasell.com

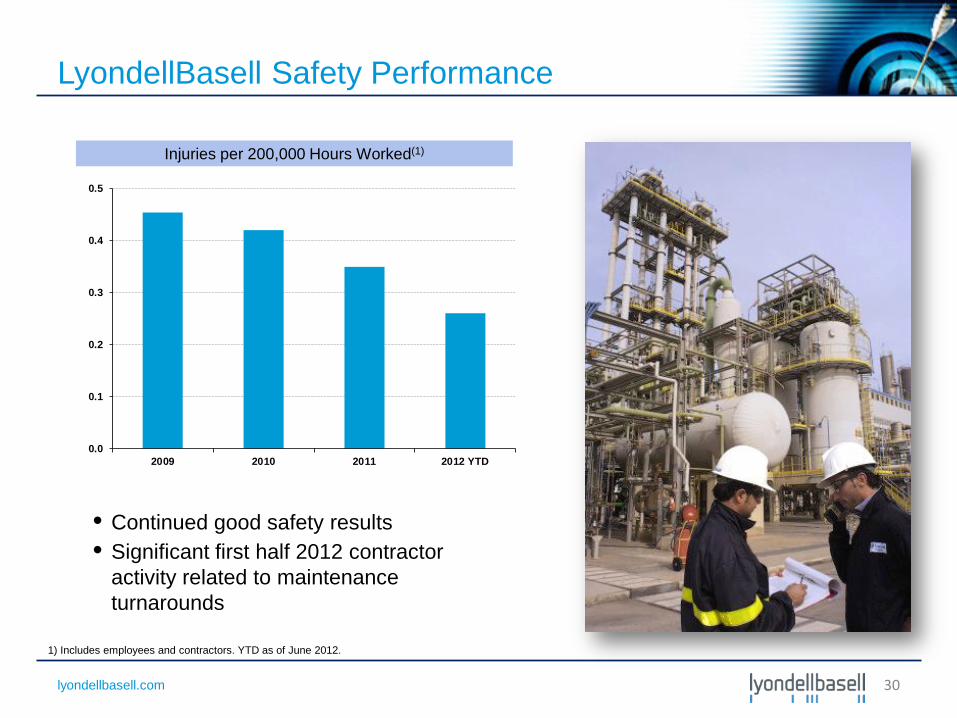

LyondellBasell Safety Performance

• Continued good safety results • Significant first half 2012 contractor

activity related to maintenance turnarounds

Injuries per 200,000 Hours Worked(1)

1) Includes employees and contractors. YTD as of June 2012.

30

0.0

0.1

0.2

0.3

0.4

0.5

2009 2010 2011 2012 YTD

lyondellbasell.com

500

1,000

1,500

2,000

2,500

$3,000

Olefins &Polyolefins -

Americas

Olefins &Polyolefins -

EAI

Intermediates& Derivatives

Refining Technology

150

300

450

600

750

$900

Olefins &Polyolefins -

Americas

Olefins &Polyolefins -

EAI

Intermediates& Derivatives

Refining Technology

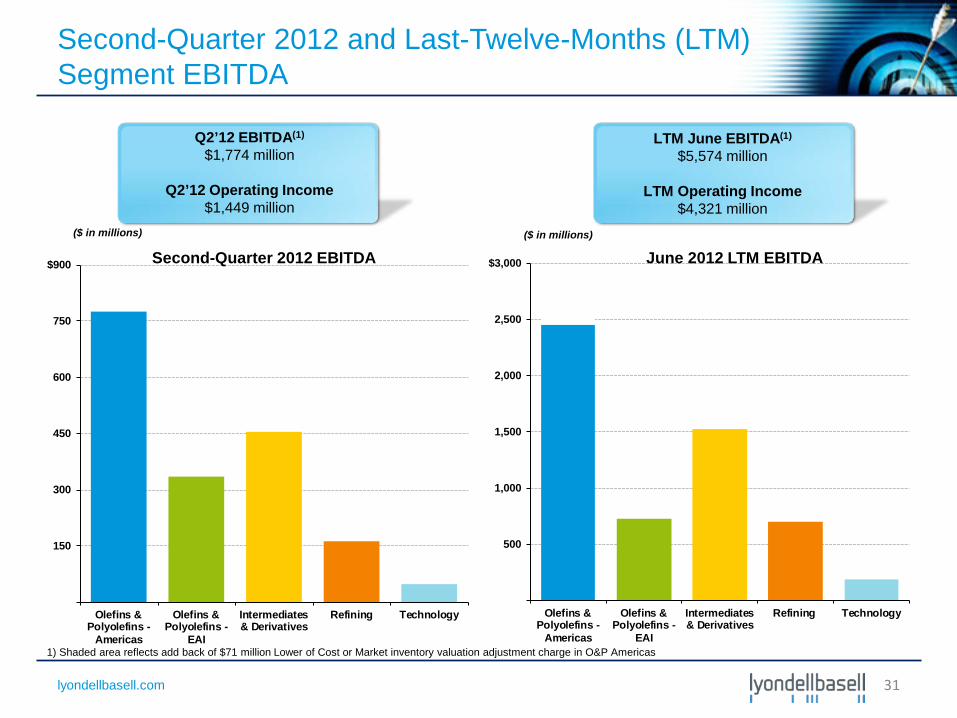

June 2012 LTM EBITDA

LTM June EBITDA(1)

$5,574 million

LTM Operating Income $4,321 million

Q2’12 EBITDA(1)

$1,774 million

Q2’12 Operating Income

$1,449 million

Second-Quarter 2012 and Last-Twelve-Months (LTM) Segment EBITDA

Second-Quarter 2012 EBITDA ($ in millions) ($ in millions)

31

1) Shaded area reflects add back of $71 million Lower of Cost or Market inventory valuation adjustment charge in O&P Americas

lyondellbasell.com

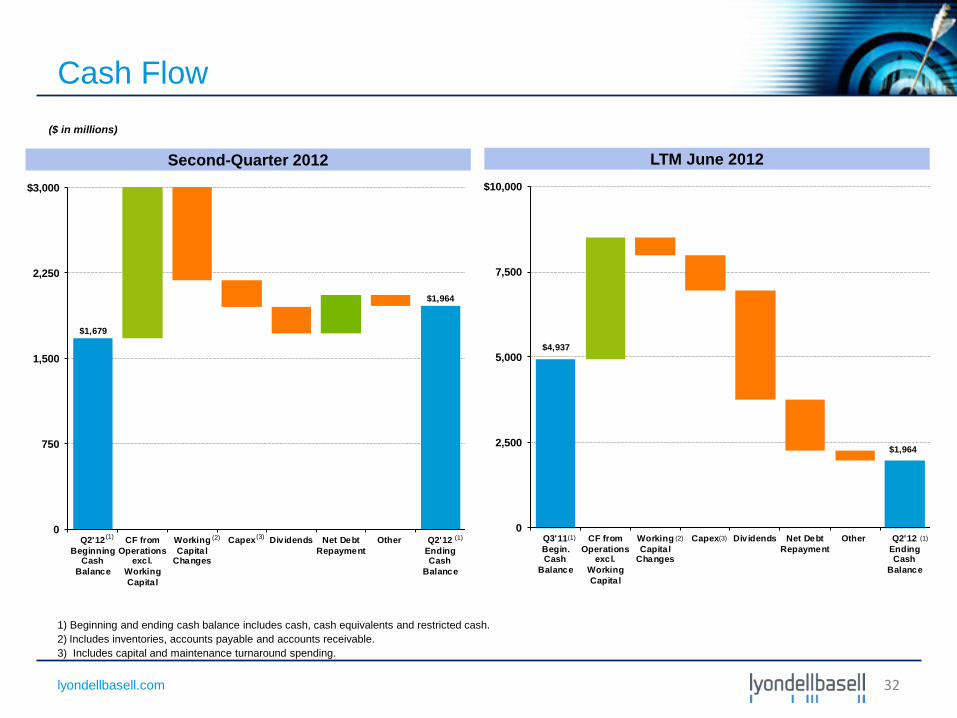

$4,937

$1,964

0

2,500

5,000

7,500

$10,000

Q3'11Begin.Cash

Balance

CF fromOperations

excl.WorkingCapital

WorkingCapital

Changes

Capex Dividends Net DebtRepayment

Other Q2'12EndingCash

Balance

$1,679

$1,964

0

750

1,500

2,250

$3,000

Q2'12Beginning

CashBalance

CF fromOperations

excl.WorkingCapital

WorkingCapital

Changes

Capex Dividends Net DebtRepayment

Other Q2'12EndingCash

Balance

Cash Flow

1) Beginning and ending cash balance includes cash, cash equivalents and restricted cash. 2) Includes inventories, accounts payable and accounts receivable. 3) Includes capital and maintenance turnaround spending.

(3) (2) (1)

($ in millions)

(2) (1)

Second-Quarter 2012 LTM June 2012

(3) (1)

32

(1)

lyondellbasell.com

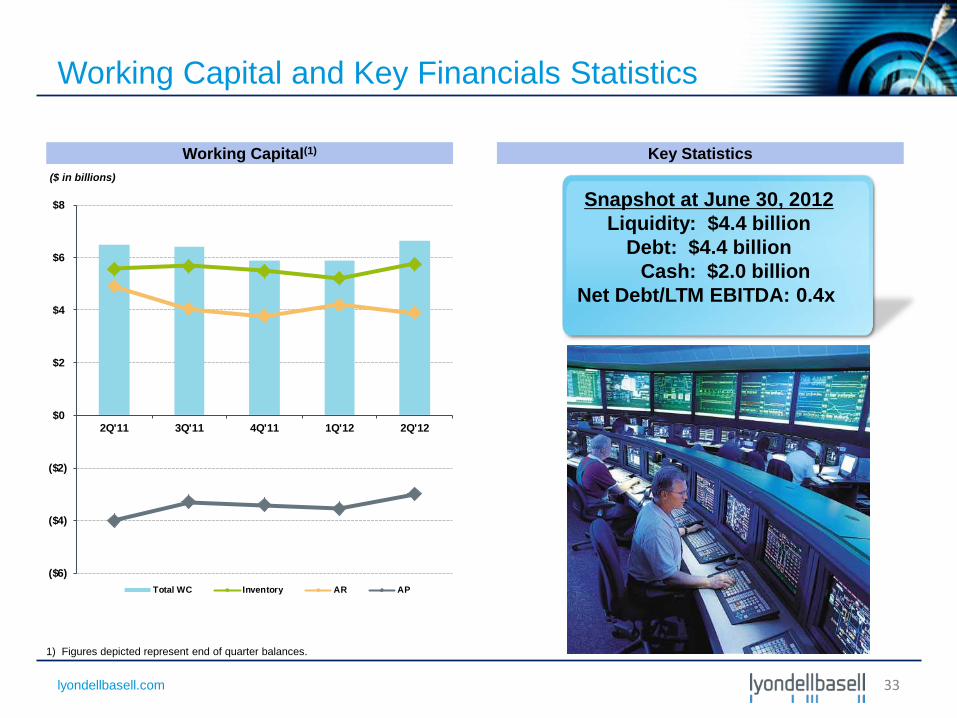

Working Capital and Key Financials Statistics

Snapshot at June 30, 2012 Liquidity: $4.4 billion

Debt: $4.4 billion Cash: $2.0 billion

Net Debt/LTM EBITDA: 0.4x

1) Figures depicted represent end of quarter balances.

($ in billions)

Working Capital(1) Key Statistics

33

($6)

($4)

($2)

$0

$2

$4

$6

$8

2Q'11 3Q'11 4Q'11 1Q'12 2Q'12

Total WC Inventory AR AP

lyondellbasell.com

(10)

0

10

20

30

40

50

Ethane Margin Naphtha Margin HDPE Margin Ethylene/HDPE Chain

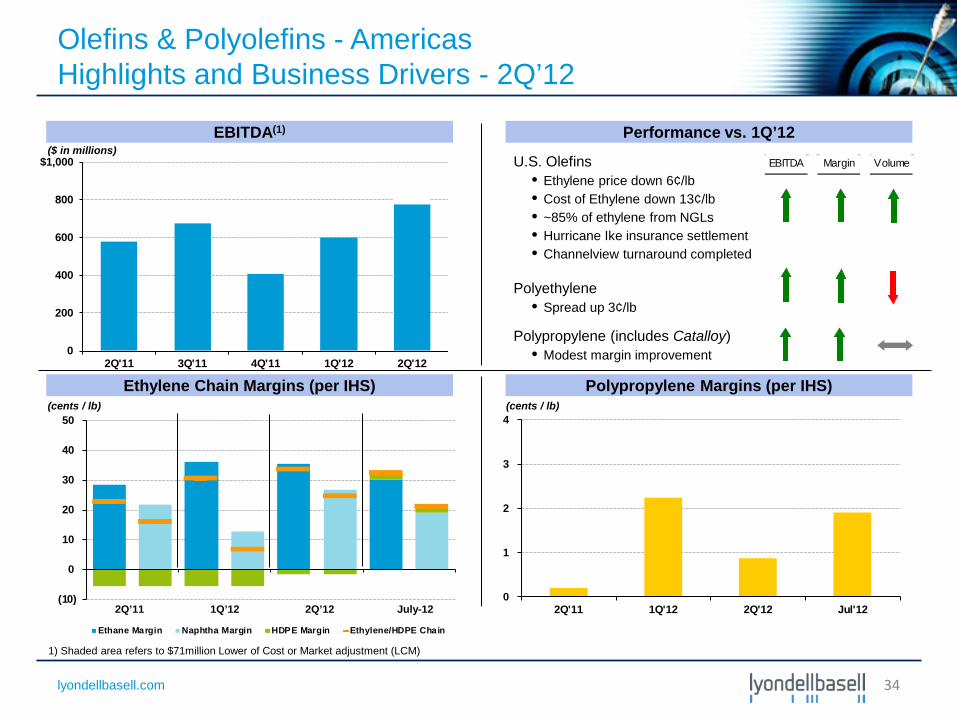

Olefins & Polyolefins - Americas Highlights and Business Drivers - 2Q’12

U.S. Olefins • Ethylene price down 6¢/lb • Cost of Ethylene down 13¢/lb • ~85% of ethylene from NGLs • Hurricane Ike insurance settlement • Channelview turnaround completed

Polyethylene • Spread up 3¢/lb

Polypropylene (includes Catalloy)

• Modest margin improvement

Ethylene Chain Margins (per IHS)

EBITDA(1) Performance vs. 1Q’12

Polypropylene Margins (per IHS)

EBITDA Margin Volume($ in millions)

(cents / lb) (cents / lb)

2Q’11 1Q’12 2Q’12 July-12

0

200

400

600

800

$1,000

2Q'11 3Q'11 4Q'11 1Q'12 2Q'12

34

0

1

2

3

4

2Q'11 1Q'12 2Q'12 Jul'12

1) Shaded area refers to $71million Lower of Cost or Market adjustment (LCM)

lyondellbasell.com

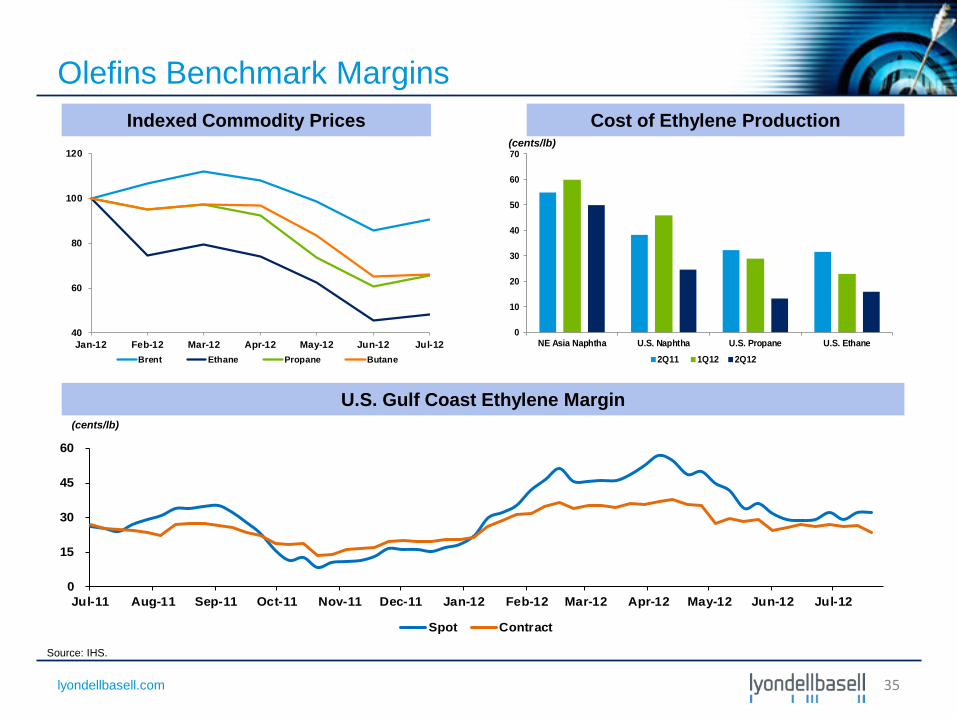

Olefins Benchmark Margins

U.S. Gulf Coast Ethylene Margin

(cents/lb)

Source: IHS.

35

0

15

30

45

60

Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12

Spot Contract

40

60

80

100

120

Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12Brent Ethane Propane Butane

0

10

20

30

40

50

60

70

NE Asia Naphtha U.S. Naphtha U.S. Propane U.S. Ethane

2Q11 1Q12 2Q12

Indexed Commodity Prices Cost of Ethylene Production

(cents/lb)

lyondellbasell.com

Ethane and Propane Production and Inventories at Historic Highs

U.S. Ethane Production U.S. Propane Production

2007 - 2011 Range 2011 2012

U.S. Ethane Inventory U.S. Propane Inventory

Source: EIA.

36

400

600

800

1,000

1,200

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MBP

D

400

500

600

700

800

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MBP

D

0

10

20

30

40

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MM

Bbls

0

20

40

60

80

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

MM

Bbls

lyondellbasell.com

(10)

0

10

20

30

40

50

2Q'11 1Q'12 2Q'12 Jul' 12

HDPE Margin Naphtha Margin Ethylene/HDPE Chain

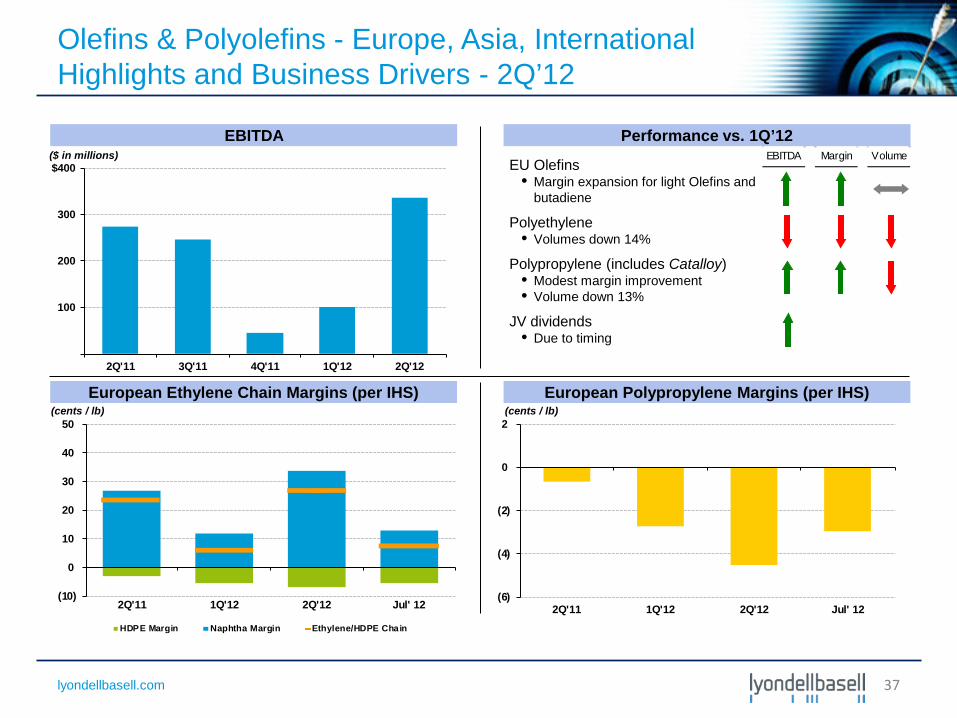

Olefins & Polyolefins - Europe, Asia, International Highlights and Business Drivers - 2Q’12

EU Olefins • Margin expansion for light Olefins and

butadiene

Polyethylene • Volumes down 14%

Polypropylene (includes Catalloy)

• Modest margin improvement • Volume down 13%

JV dividends • Due to timing

European Ethylene Chain Margins (per IHS)

EBITDA Performance vs. 1Q’12

European Polypropylene Margins (per IHS)

EBITDA Margin Volume($ in millions)

(cents / lb) (cents / lb)

100

200

300

$400

2Q'11 3Q'11 4Q'11 1Q'12 2Q'12

37

(6)

(4)

(2)

0

2

2Q'11 1Q'12 2Q'12 Jul' 12

lyondellbasell.com

0

15

30

45

2Q11 1Q12 2Q12 3Q12 E

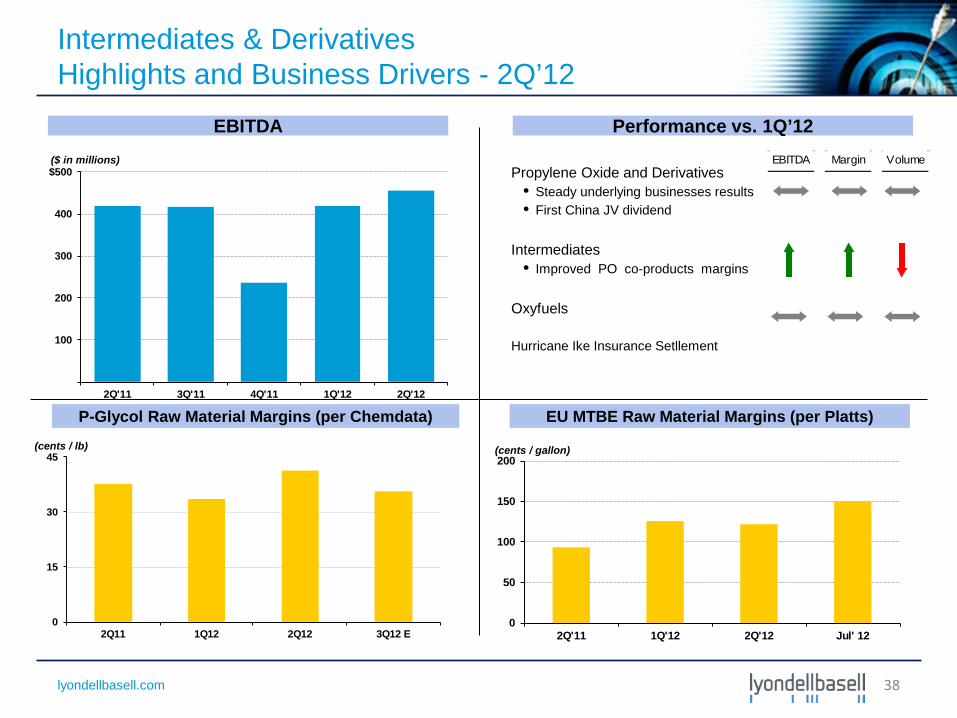

Intermediates & Derivatives Highlights and Business Drivers - 2Q’12

EBITDA

Propylene Oxide and Derivatives • Steady underlying businesses results • First China JV dividend

Intermediates

• Improved PO co-products margins Oxyfuels

Hurricane Ike Insurance Setllement

EBITDA Margin Volume

Performance vs. 1Q’12 ($ in millions)

38

EU MTBE Raw Material Margins (per Platts)

(cents / gallon)

0

50

100

150

200

2Q'11 1Q'12 2Q'12 Jul' 12

P-Glycol Raw Material Margins (per Chemdata)

(cents / lb)

100

200

300

400

$500

2Q'11 3Q'11 4Q'11 1Q'12 2Q'12

lyondellbasell.com

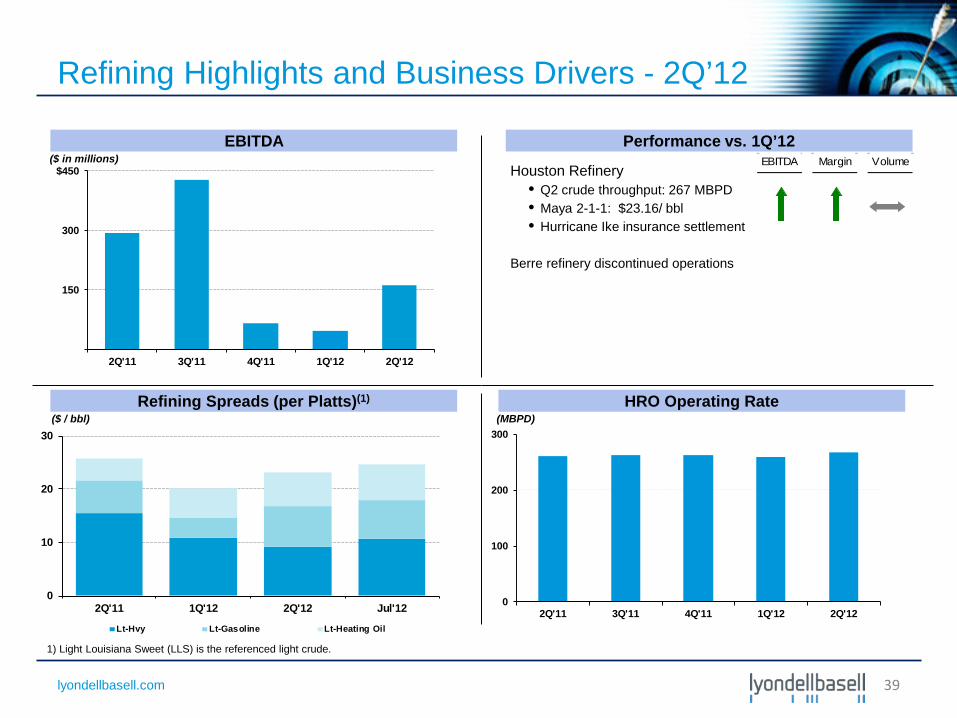

Refining Highlights and Business Drivers - 2Q’12

Houston Refinery • Q2 crude throughput: 267 MBPD • Maya 2-1-1: $23.16/ bbl • Hurricane Ike insurance settlement

Berre refinery discontinued operations

Refining Spreads (per Platts)(1)

EBITDA Performance vs. 1Q’12 EBITDA Margin Volume($ in millions)

($ / bbl)

1) Light Louisiana Sweet (LLS) is the referenced light crude.

39

0

10

20

30

2Q'11 1Q'12 2Q'12 Jul'12

Lt-Hvy Lt-Gasoline Lt-Heating Oil

HRO Operating Rate

0

100

200

300

2Q'11 3Q'11 4Q'11 1Q'12 2Q'12

150

300

$450

2Q'11 3Q'11 4Q'11 1Q'12 2Q'12

(MBPD)

lyondellbasell.com

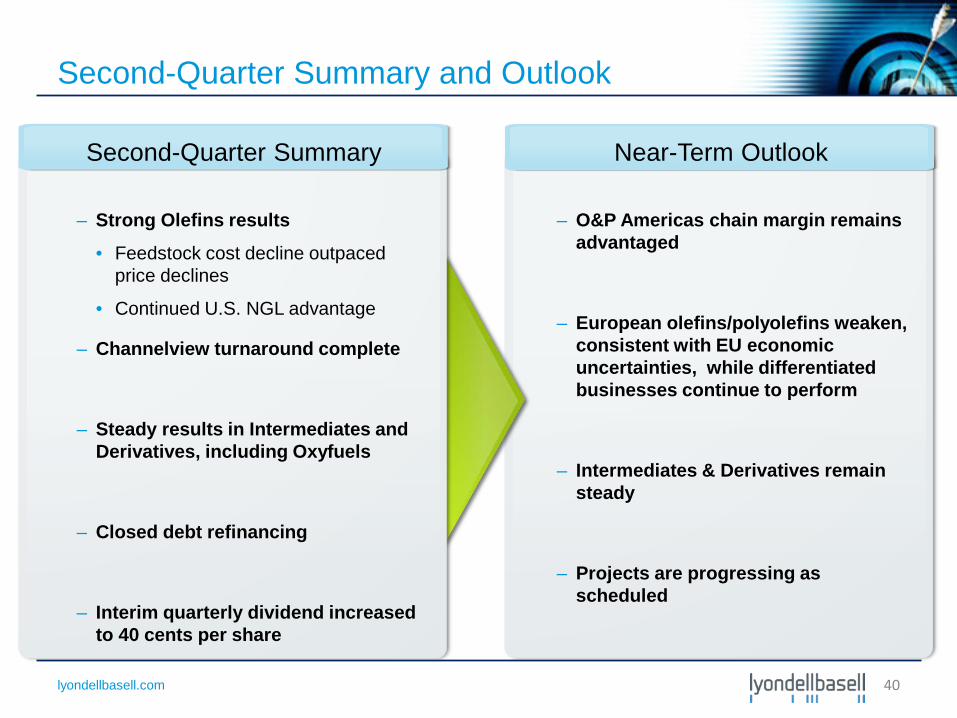

– O&P Americas chain margin remains advantaged

– European olefins/polyolefins weaken, consistent with EU economic uncertainties, while differentiated businesses continue to perform

– Intermediates & Derivatives remain steady

– Projects are progressing as scheduled

Second-Quarter Summary and Outlook

– Strong Olefins results

• Feedstock cost decline outpaced price declines

• Continued U.S. NGL advantage

– Channelview turnaround complete

– Steady results in Intermediates and Derivatives, including Oxyfuels

– Closed debt refinancing

– Interim quarterly dividend increased to 40 cents per share

Second-Quarter Summary Near-Term Outlook

40