Embed Size (px)

Citation preview

US Multifamily Strategy & 2016 Outlook

Jeff AdlerVice President, Matrix

Jack KernDirector, Research and Publications

Spring 2016

2

ALTHOUGH EVERY EFFORT IS MADE TO ENSURE THE ACCURACY, TIMELINESS AND COMPLETENESS OF THE INFORMATION PROVIDED IN THIS PUBLICATION, THE INFORMATION IS PROVIDED “AS IS” AND YARDI MATRIX DOES NOT GUARANTEE, WARRANT, REPRESENT OR UNDERTAKE THAT THE INFORMATION PROVIDED IS CORRECT, ACCURATE, CURRENT OR COMPLETE. YARDI MATRIX IS NOT LIABLE FOR ANY LOSS, CLAIM, OR DEMAND ARISING DIRECTLY OR INDIRECTLY FROM ANY USE OR RELIANCE UPON THE INFORMATION CONTAINED HEREIN.

Disclaimer

3

We Laid Out a Pretty Positive Case for US Multifamily Investment:

1. US macroeconomic conditions, while not great, were good enough to generate job growth of ~200,000 jobs per month Enough to maintain MF occupancy and good, but probably decelerating, rent growth

2. Demand was a big tailwind, both Short and Long Term Job Formation, Demographics, Affordability, and Technological change were all combining for a positive perfect storm for the next 10-20 years

3. Supply was, relatively speaking, in check and peaking in ‘16- which would slow, but not stop, continued rent growth Supply surges were focused in major urban hubs of a select number of primary and secondary cities, at very high rental price points

4. Oil price declines would be a net positive, but there would be regional pain- Houston, OKC, Denver, smaller oil patch

5. “Secondary” markets, and their emerging intellectual capital nodes represented a high probability way to target a position in US Multifamily that had good odds of generating capital appreciation with income

Value Add was a strategy that had good odds of success, given the large price gap between Luxury and Middle Market rents in most markets

6. Yardi Matrix is a powerful tool to execute investment strategies- whether value add, stabilized cash flow, or new Development.

When We Last Met in November….

4

The Outlook is Still Positive, but the risk of a Global Debt Driven Macroeconomic Dislocation has risen:

1. Demand still looks really good, as does the Investment Thesis for Secondary Markets & Value Add

Sustained high occupancy on stabilized properties- 96% and stable

Strong rent growth- 6% still; deceleration in Houston, Denver, and San Fran; acceleration in Atlanta, Orlando, Phoenix

Structural components of demand are still big tailwinds as before

Wage pressures in the US among skilled workers are increasing in our bifurcated economy

2. Supply is still, relatively speaking, in check and peaking in ‘16- which may slow, but not stop, continued rent growth

No meaningful change in New supply pipeline from prior expectations- 240K in lease-up, 572K Under Construction

3. Dislocation in Comm’l Real Estate Debt Markets, driven by regulatory influences, is restraining growth in new construction financing

In addition, disruption in the CMBS market due to capital regulations, is encouraging private debt funds to enter, but at a higher cost

These dislocations will extend the apartment rental growth up-cycle, absent a demand driven crack-up

Debt availability and cost is more tied than ever to global financial markets, despite the steadying influence of the GSEs (50% debt market share).

Asset Value growth will be restrained, but not stopped, due to these cross-currents

How do Things Look Six Months On?….

5

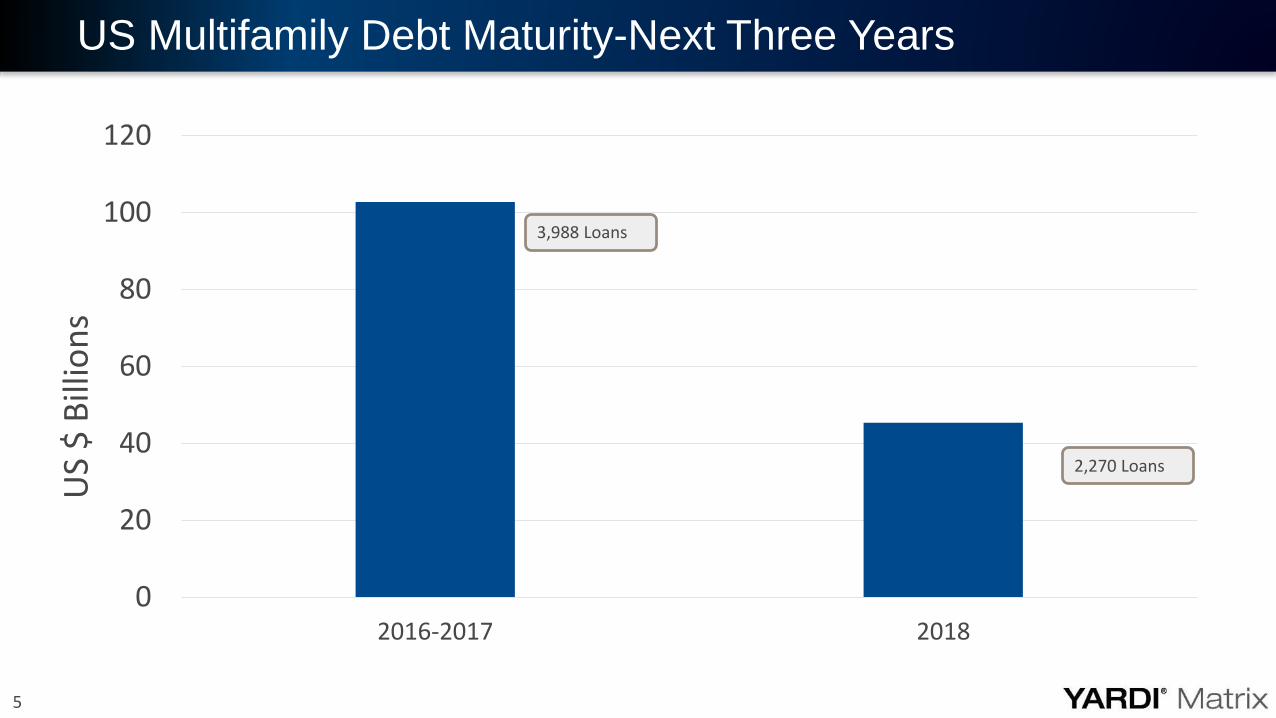

US Multifamily Debt Maturity-Next Three Years

0

20

40

60

80

100

120

2016-2017 2018

US

$ B

illio

ns

2,270 Loans

3,988 Loans

6

The Outlook is Still Positive, but the risk of a Global Debt Driven Macroeconomic Dislocation has risen:

4. Global Macroeconomic concerns and slow US GDP growth in Q1 (0.5%), along with stretched equity market valuations, and coincident probable equity market volatility, are the chief reasons driving near term caution

US economy is the relative “one-eyed” man among the land of the blind- Europe, Japan, and a transforming China

Interest rate increases in 2016 are very unlikely

Monetary Policy, and the Debt Surge it has engendered in the Govt & Corporate Sector, has reached its limits (or very near its limits)—

Pro-Growth Structural Government Policies are Needed, but is unlikely.

US Multifamily is still the place to be, even if the ride is at risk of a few potential transitory bumps in the road

5. Yardi Matrix is still a powerful tool to execute investment strategies- whether value add, stabilized cash flow, or new Development.

How do Things Look Six Months On?….

Macroeconomic Outlook

8

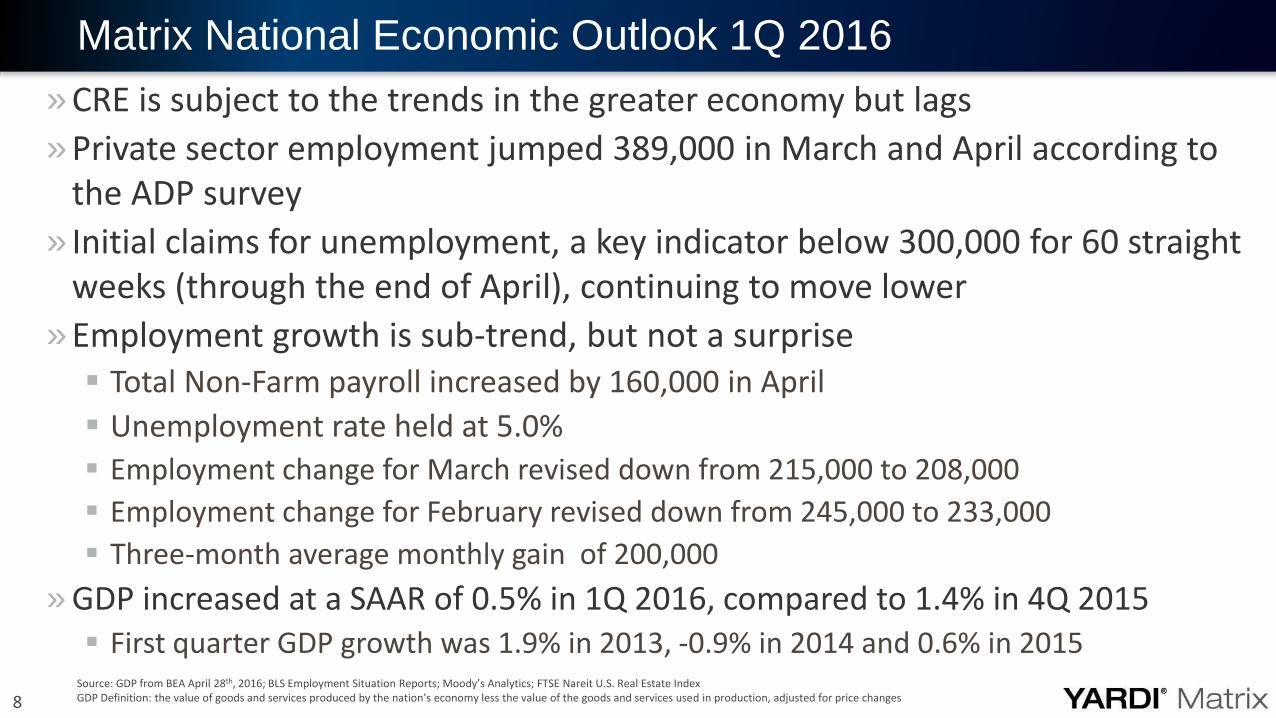

» CRE is subject to the trends in the greater economy but lags

» Private sector employment jumped 389,000 in March and April according to the ADP survey

» Initial claims for unemployment, a key indicator below 300,000 for 60 straight weeks (through the end of April), continuing to move lower

» Employment growth is sub-trend, but not a surprise Total Non-Farm payroll increased by 160,000 in April

Unemployment rate held at 5.0%

Employment change for March revised down from 215,000 to 208,000

Employment change for February revised down from 245,000 to 233,000

Three-month average monthly gain of 200,000

» GDP increased at a SAAR of 0.5% in 1Q 2016, compared to 1.4% in 4Q 2015 First quarter GDP growth was 1.9% in 2013, -0.9% in 2014 and 0.6% in 2015

Matrix National Economic Outlook 1Q 2016

Source: GDP from BEA April 28th, 2016; BLS Employment Situation Reports; Moody’s Analytics; FTSE Nareit U.S. Real Estate Index GDP Definition: the value of goods and services produced by the nation’s economy less the value of the goods and services used in production, adjusted for price changes

9

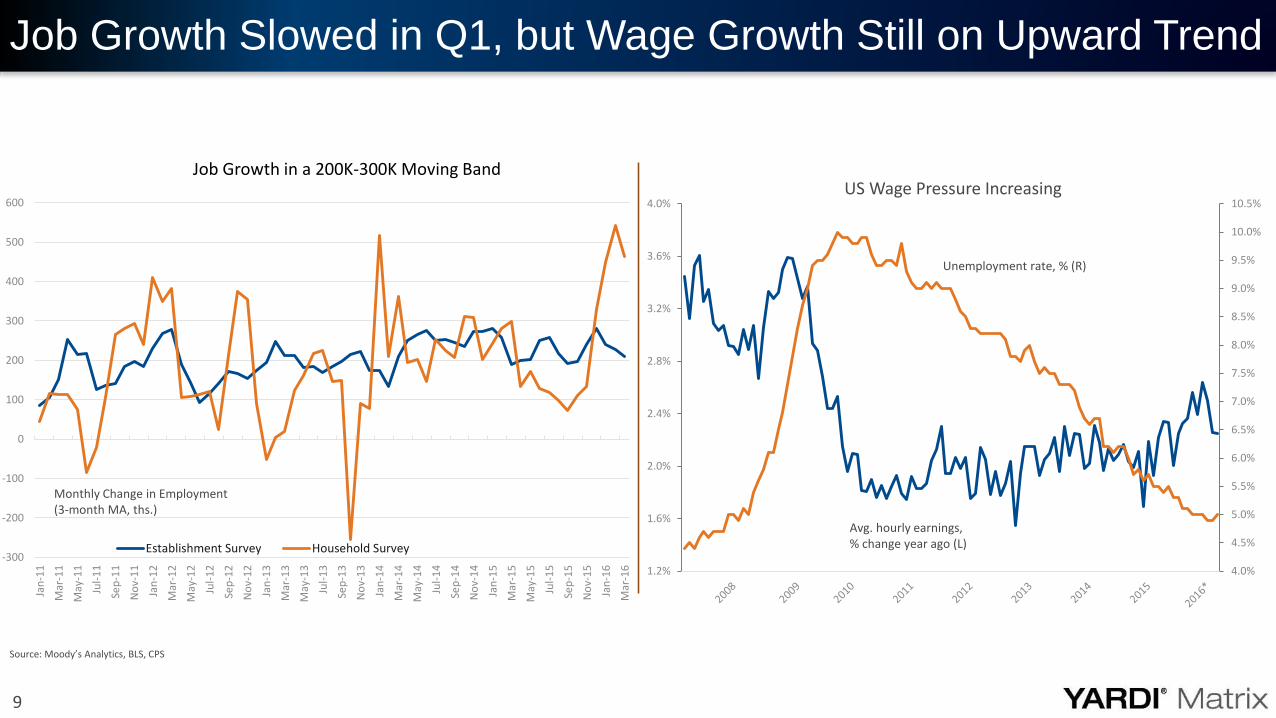

Job Growth Slowed in Q1, but Wage Growth Still on Upward Trend

Source: Moody’s Analytics, BLS, CPS

Monthly Change in Employment(3-month MA, ths.)

-300

-200

-100

0

100

200

300

400

500

600

Jan

-11

Mar

-11

May

-11

Jul-

11

Sep

-11

No

v-1

1

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Jan

-15

Mar

-15

May

-15

Jul-

15

Sep

-15

No

v-1

5

Jan

-16

Mar

-16

Job Growth in a 200K-300K Moving Band

Establishment Survey Household Survey

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

10.0%

10.5%

1.2%

1.6%

2.0%

2.4%

2.8%

3.2%

3.6%

4.0%US Wage Pressure Increasing

Unemployment rate, % (R)

Avg. hourly earnings,% change year ago (L)

10

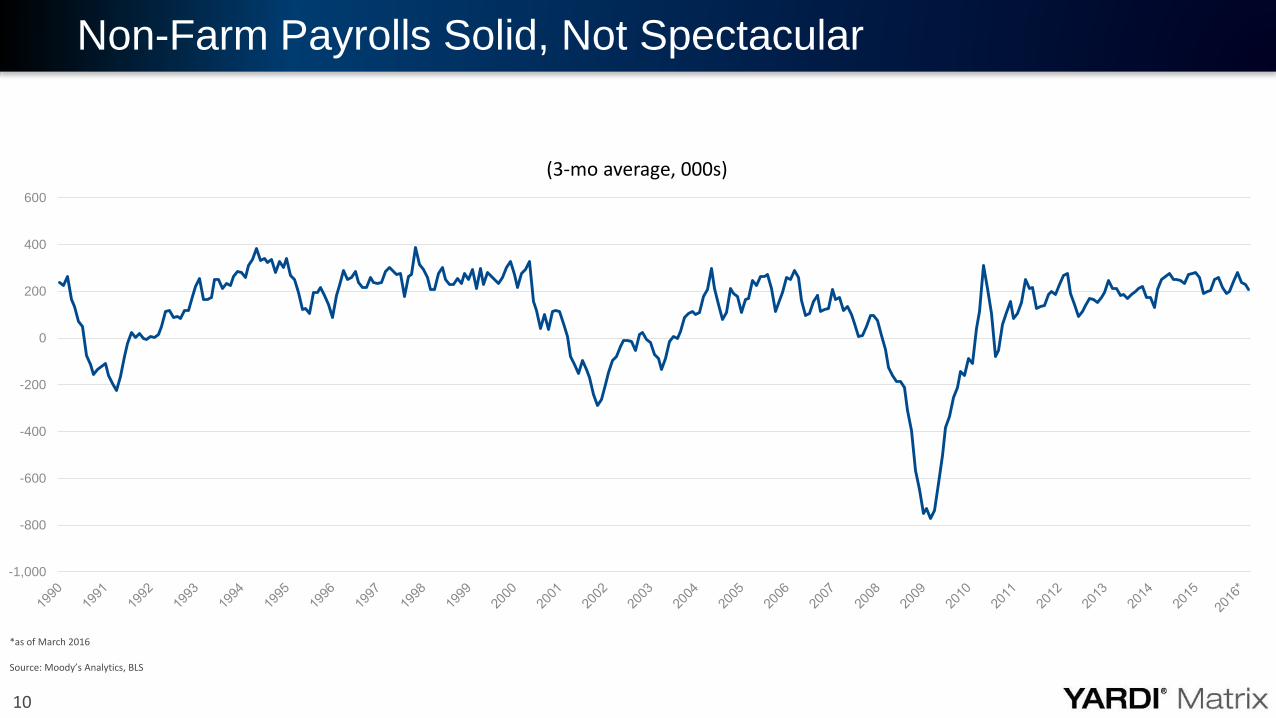

Non-Farm Payrolls Solid, Not Spectacular

-1,000

-800

-600

-400

-200

0

200

400

600

(3-mo average, 000s)

*as of March 2016

Source: Moody’s Analytics, BLS

11

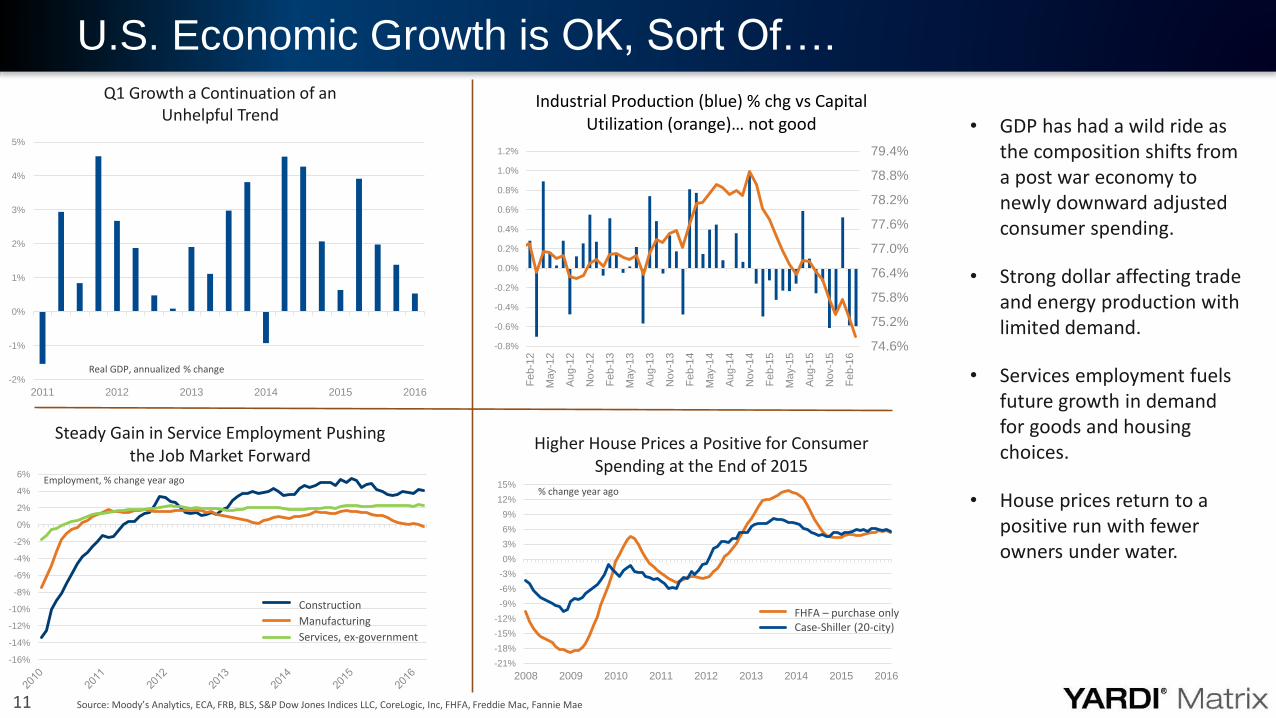

• GDP has had a wild ride as the composition shifts from a post war economy to newly downward adjusted consumer spending.

• Strong dollar affecting trade and energy production with limited demand.

• Services employment fuels future growth in demand for goods and housing choices.

• House prices return to a positive run with fewer owners under water.

U.S. Economic Growth is OK, Sort Of….

-2%

-1%

0%

1%

2%

3%

4%

5%

2011 2012 2013 2014 2015 2016

Q1 Growth a Continuation of an Unhelpful Trend

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

Steady Gain in Service Employment Pushing the Job Market Forward

Employment, % change year ago

Construction

Manufacturing

Services, ex-government

74.6%

75.2%

75.8%

76.4%

77.0%

77.6%

78.2%

78.8%

79.4%

-0.8%

-0.6%

-0.4%

-0.2%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

Fe

b-1

2

Ma

y-1

2

Au

g-1

2

Nov-1

2

Fe

b-1

3

Ma

y-1

3

Au

g-1

3

Nov-1

3

Fe

b-1

4

Ma

y-1

4

Au

g-1

4

Nov-1

4

Fe

b-1

5

Ma

y-1

5

Au

g-1

5

Nov-1

5

Fe

b-1

6

Industrial Production (blue) % chg vs Capital Utilization (orange)… not good

-21%

-18%

-15%

-12%

-9%

-6%

-3%

0%

3%

6%

9%

12%

15%

2008 2009 2010 2011 2012 2013 2014 2015 2016

Higher House Prices a Positive for Consumer Spending at the End of 2015

FHFA – purchase onlyCase-Shiller (20-city)

Source: Moody’s Analytics, ECA, FRB, BLS, S&P Dow Jones Indices LLC, CoreLogic, Inc, FHFA, Freddie Mac, Fannie Mae

Real GDP, annualized % change

% change year ago

12

» Household spending fueled by modest income gains (2%) and drop in oil/energy prices, gains in apparel and restaurant receipts

» Light vehicle sales at 17.4 million units (SAAR) in March, a year-over year growth of 1.68%

» Consumer Confidence Index at 96.11 in March, slightly below pre-recessionary levels

» March retail* sales holds steady in early 2016, and grew 1.73% year-over-year

» No inflation issue, but deflation watch

» Federal Reserve reticent on rate increases, even if warranted

Fed had limited options and unattractive choices going forward

» Current oil price opened at $45.43 compared to $38.00 three months ago

One year ago, oil prices about $64/barrel

Baker-Hughes U.S. oil rig count down by 11 to 332 from a high over 1,600

Household Spending, Income and Oil

Source: Moody’s Analytics, The Conference Board, AutoData, U.S. Census, Monthly Retail Trade and Food Services, FOMC, WTI (NYMEX)*Retail sales and food services, excludes motor vehicle and parts

13

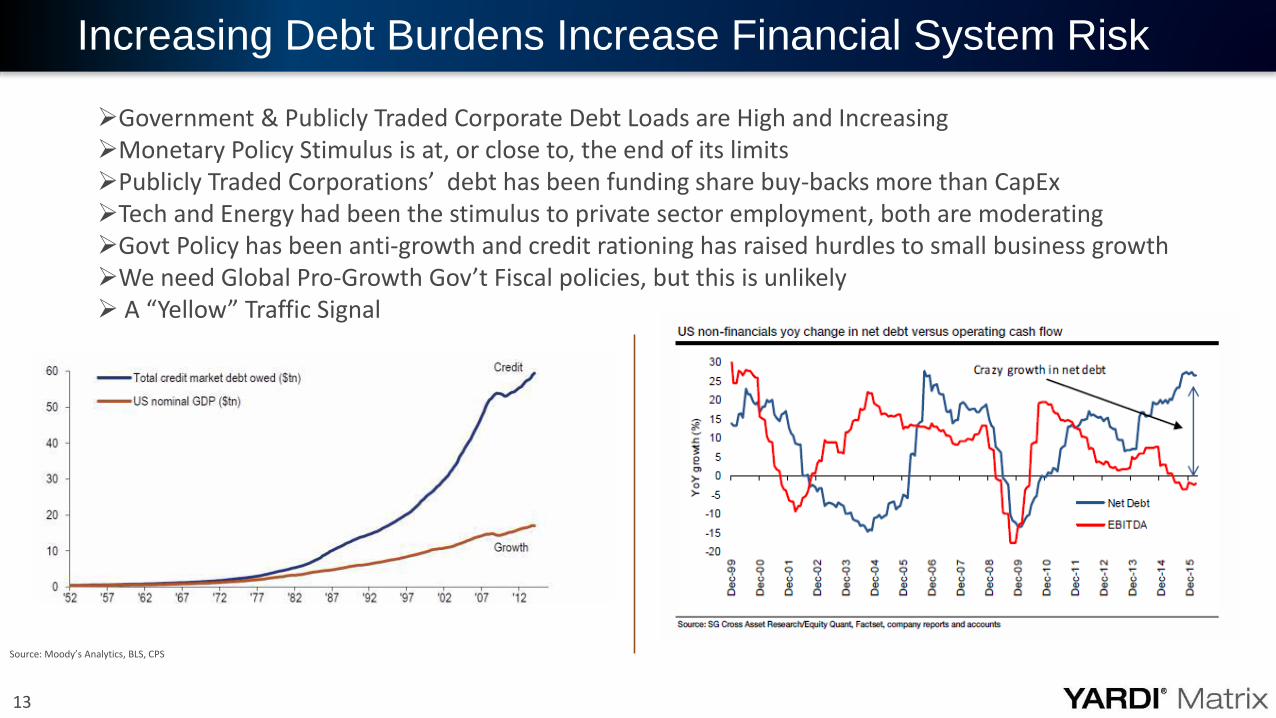

Increasing Debt Burdens Increase Financial System Risk

Source: Moody’s Analytics, BLS, CPS

Government & Publicly Traded Corporate Debt Loads are High and IncreasingMonetary Policy Stimulus is at, or close to, the end of its limitsPublicly Traded Corporations’ debt has been funding share buy-backs more than CapExTech and Energy had been the stimulus to private sector employment, both are moderatingGovt Policy has been anti-growth and credit rationing has raised hurdles to small business growthWe need Global Pro-Growth Gov’t Fiscal policies, but this is unlikely A “Yellow” Traffic Signal

14

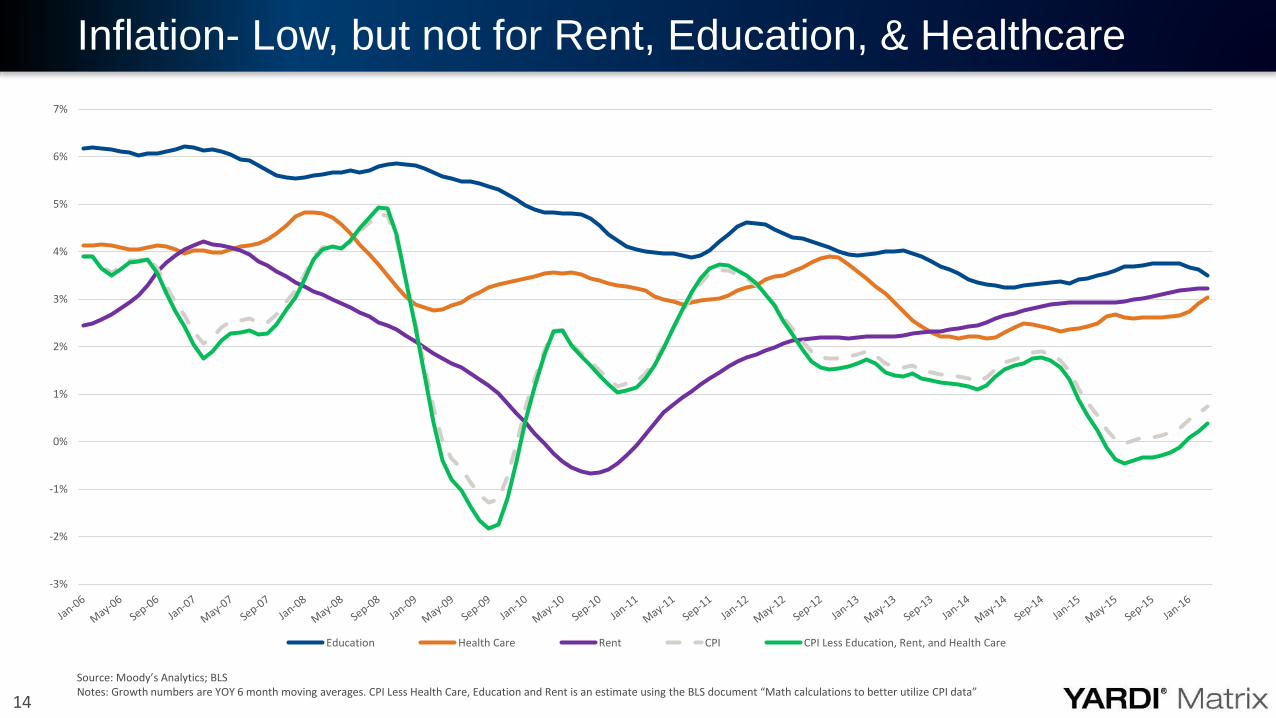

Inflation- Low, but not for Rent, Education, & Healthcare

Source: Moody’s Analytics; BLSNotes: Growth numbers are YOY 6 month moving averages. CPI Less Health Care, Education and Rent is an estimate using the BLS document “Math calculations to better utilize CPI data”

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

Education Health Care Rent CPI CPI Less Education, Rent, and Health Care

Demographics & Real Estate Fundamentals

16

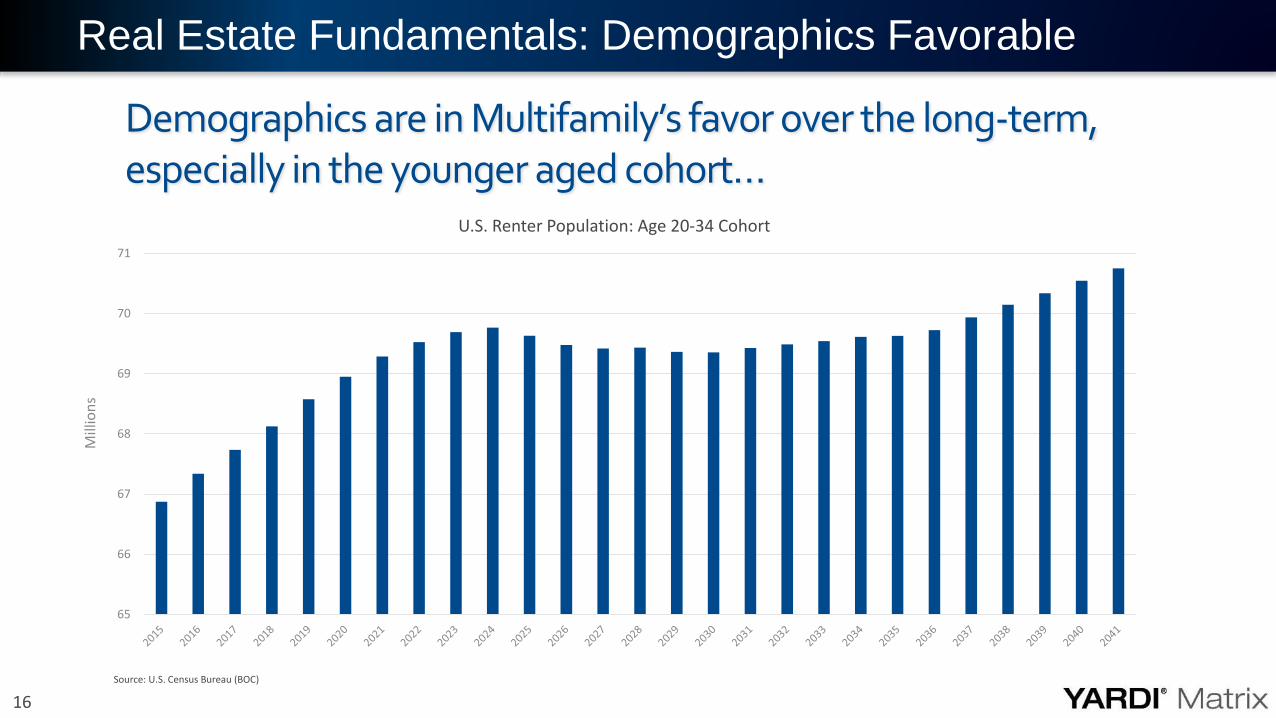

Demographics are in Multifamily’s favor over the long-term, especially in the younger aged cohort…

Real Estate Fundamentals: Demographics Favorable

65

66

67

68

69

70

71

Mill

ion

s

U.S. Renter Population: Age 20-34 Cohort

Source: U.S. Census Bureau (BOC)

17

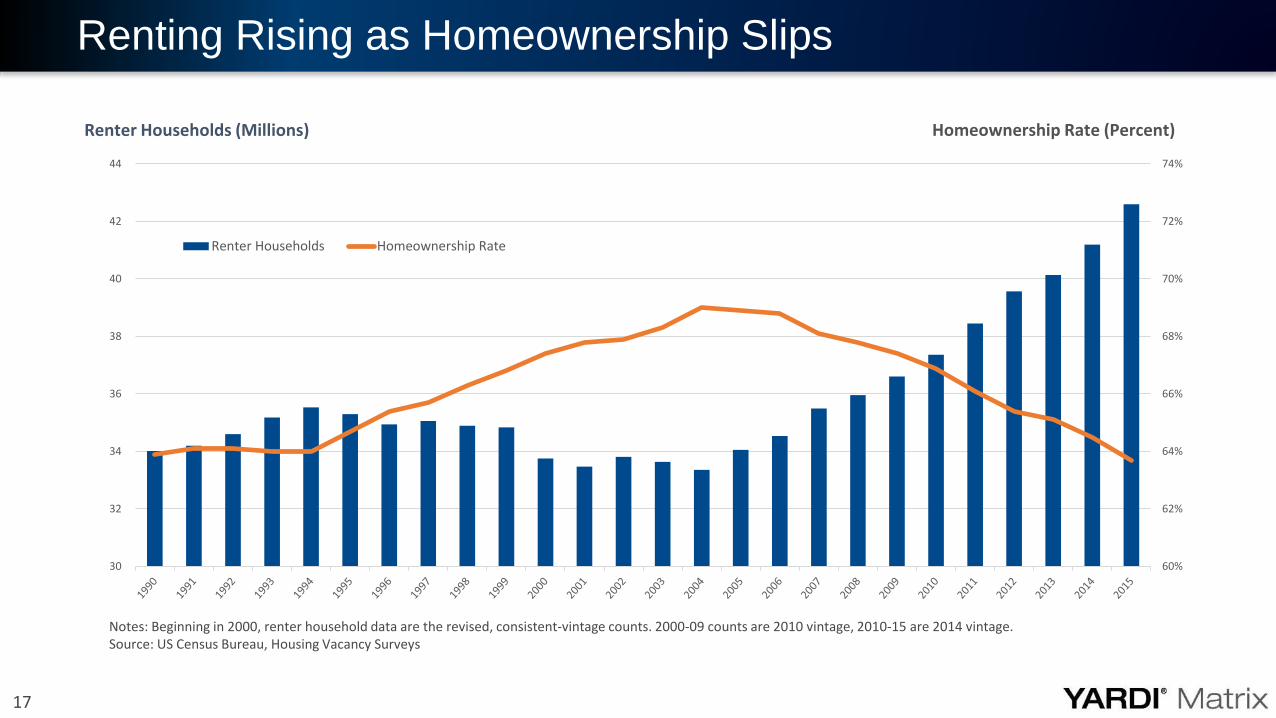

Notes: Beginning in 2000, renter household data are the revised, consistent-vintage counts. 2000-09 counts are 2010 vintage, 2010-15 are 2014 vintage.Source: US Census Bureau, Housing Vacancy Surveys

Renting Rising as Homeownership Slips

60%

62%

64%

66%

68%

70%

72%

74%

30

32

34

36

38

40

42

44

Renter Households Homeownership Rate

Renter Households (Millions) Homeownership Rate (Percent)

18

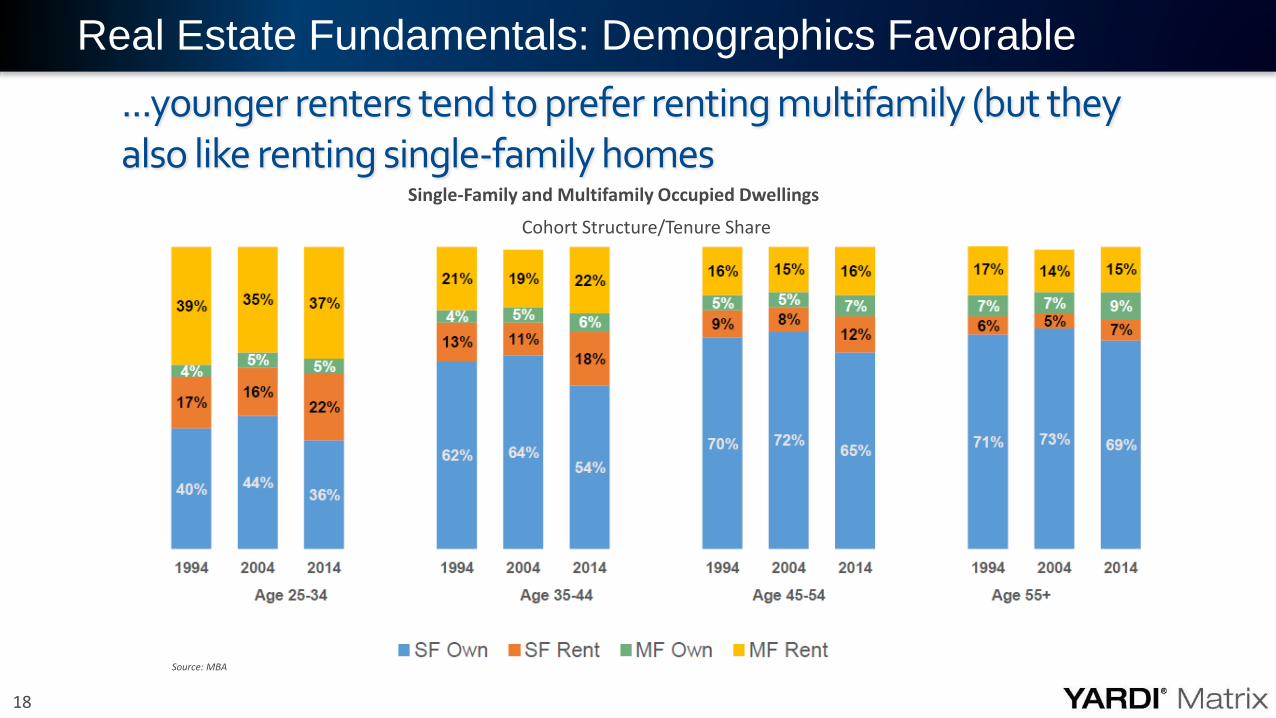

...younger renters tend to prefer renting multifamily (but they also like renting single-family homes

Real Estate Fundamentals: Demographics Favorable

Single-Family and Multifamily Occupied Dwellings

Cohort Structure/Tenure Share

Source: MBA

19

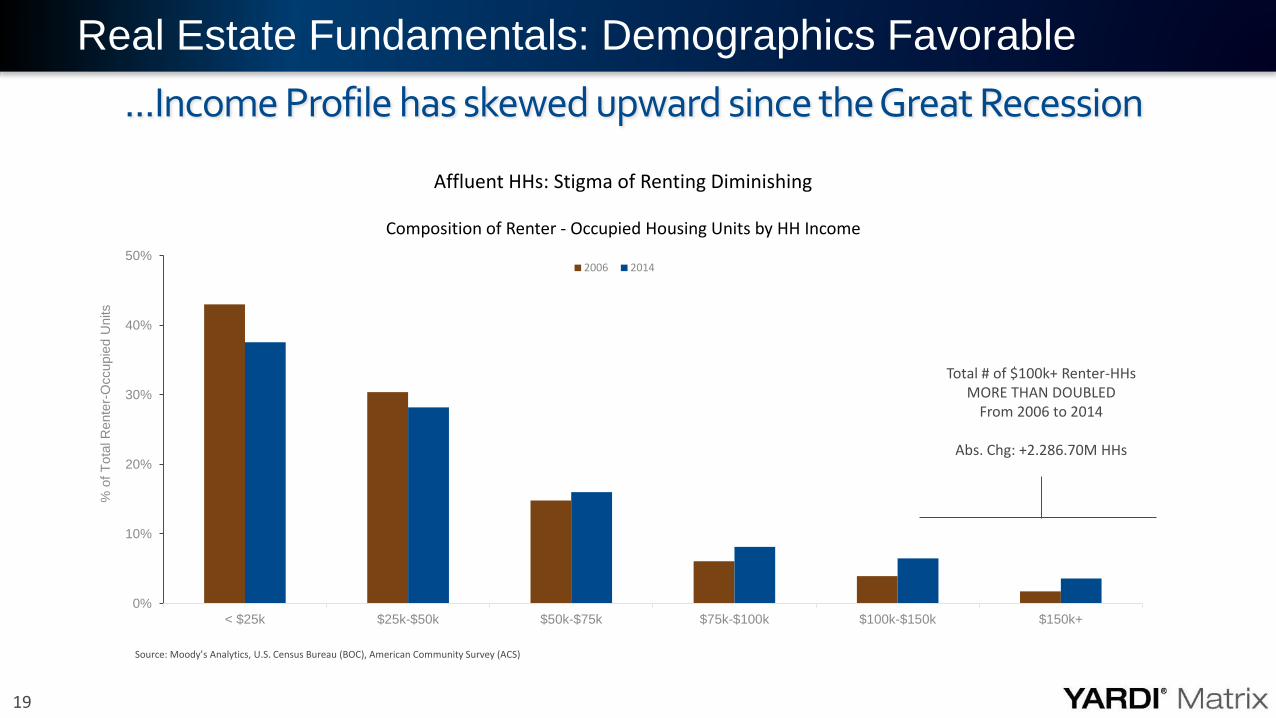

...Income Profile has skewed upward since the Great Recession

Real Estate Fundamentals: Demographics Favorable

0%

10%

20%

30%

40%

50%

< $25k $25k-$50k $50k-$75k $75k-$100k $100k-$150k $150k+

% o

f T

ota

l R

ente

r-O

ccupie

d U

nits

Affluent HHs: Stigma of Renting Diminishing

Composition of Renter - Occupied Housing Units by HH Income

2006 2014

Total # of $100k+ Renter-HHsMORE THAN DOUBLED

From 2006 to 2014

Abs. Chg: +2.286.70M HHs

Source: Moody’s Analytics, U.S. Census Bureau (BOC), American Community Survey (ACS)

20

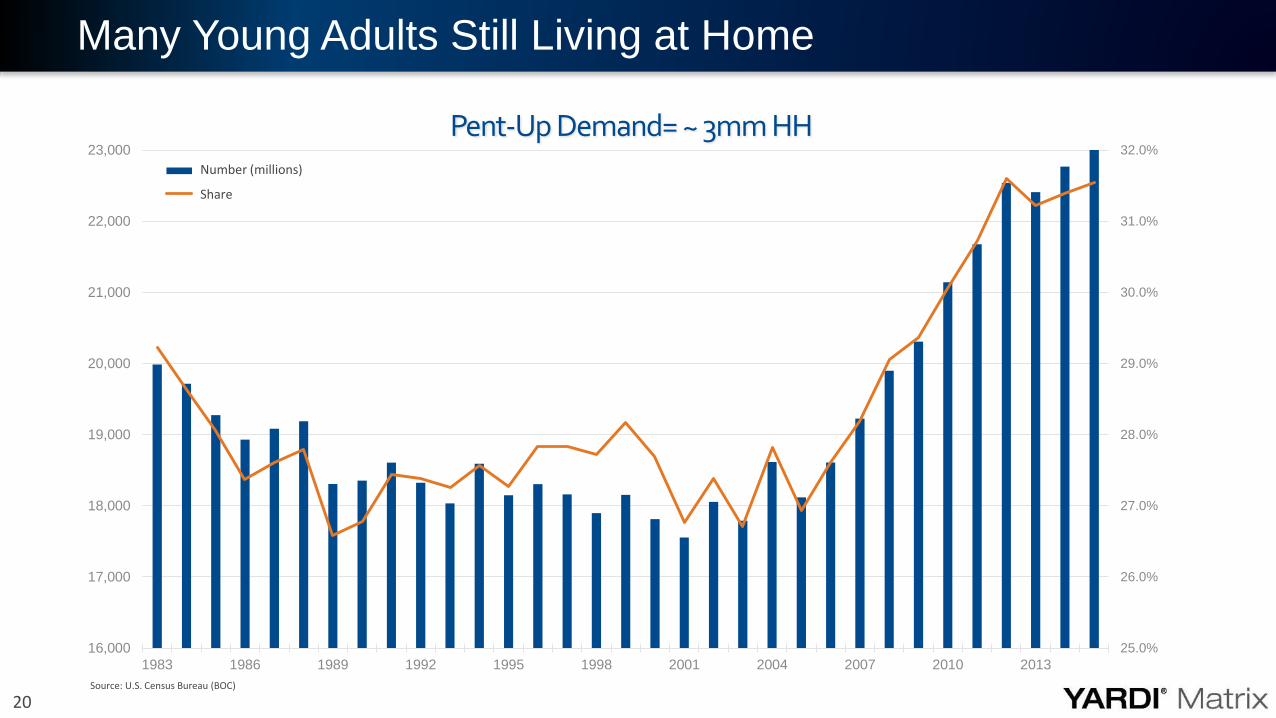

Many Young Adults Still Living at Home

25.0%

26.0%

27.0%

28.0%

29.0%

30.0%

31.0%

32.0%

16,000

17,000

18,000

19,000

20,000

21,000

22,000

23,000

1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013

Pent-Up Demand= ~ 3mm HHNumber (millions)

Share

Source: U.S. Census Bureau (BOC)

21

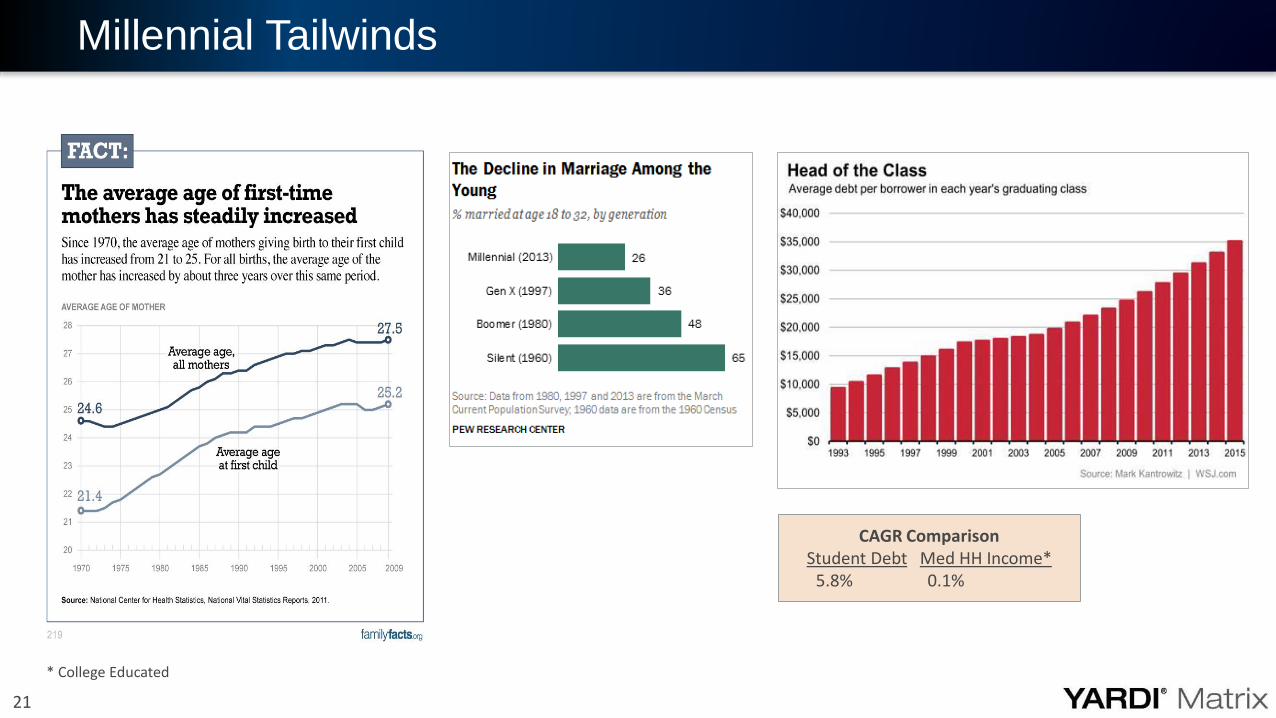

Millennial Tailwinds

CAGR ComparisonStudent Debt Med HH Income*

5.8% 0.1%

* College Educated

22

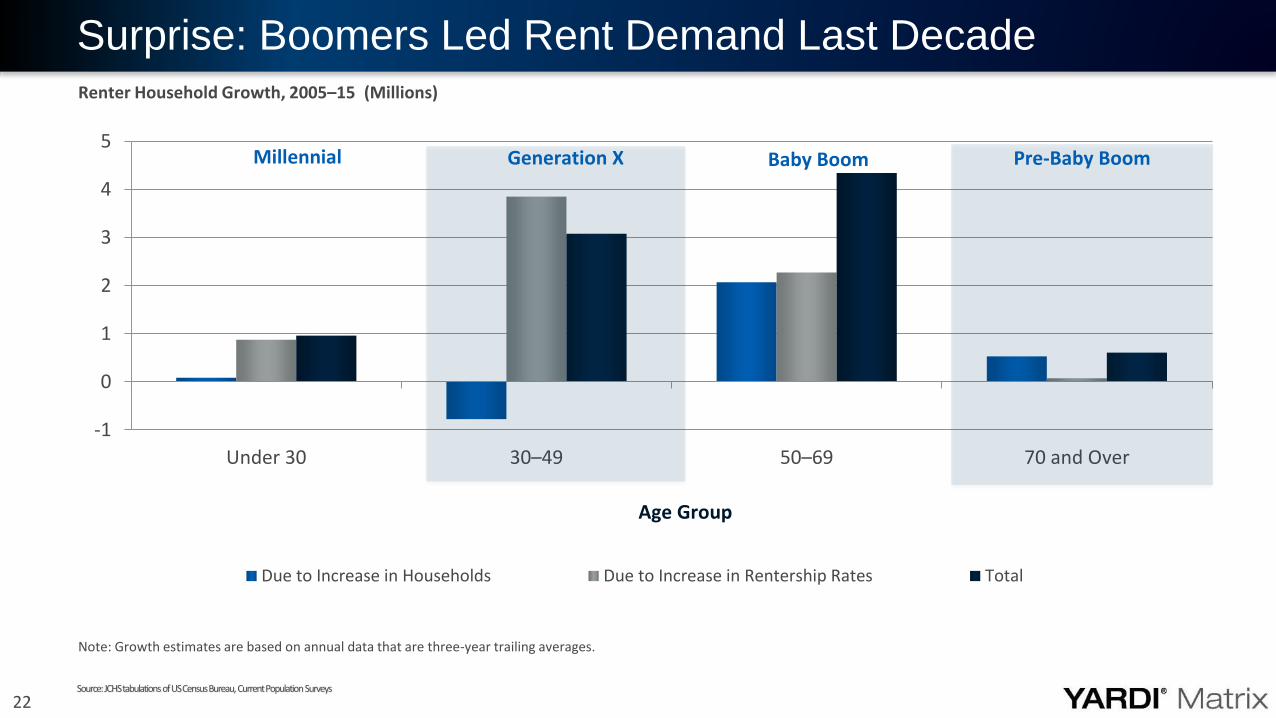

Surprise: Boomers Led Rent Demand Last Decade

-1

0

1

2

3

4

5

Under 30 30–49 50–69 70 and Over

Due to Increase in Households Due to Increase in Rentership Rates Total

Renter Household Growth, 2005–15 (Millions)

Age Group

Generation X Baby BoomMillennial Pre-Baby Boom

Note: Growth estimates are based on annual data that are three-year trailing averages.

Source: JCHS tabulations of US Census Bureau, Current Population Surveys

23

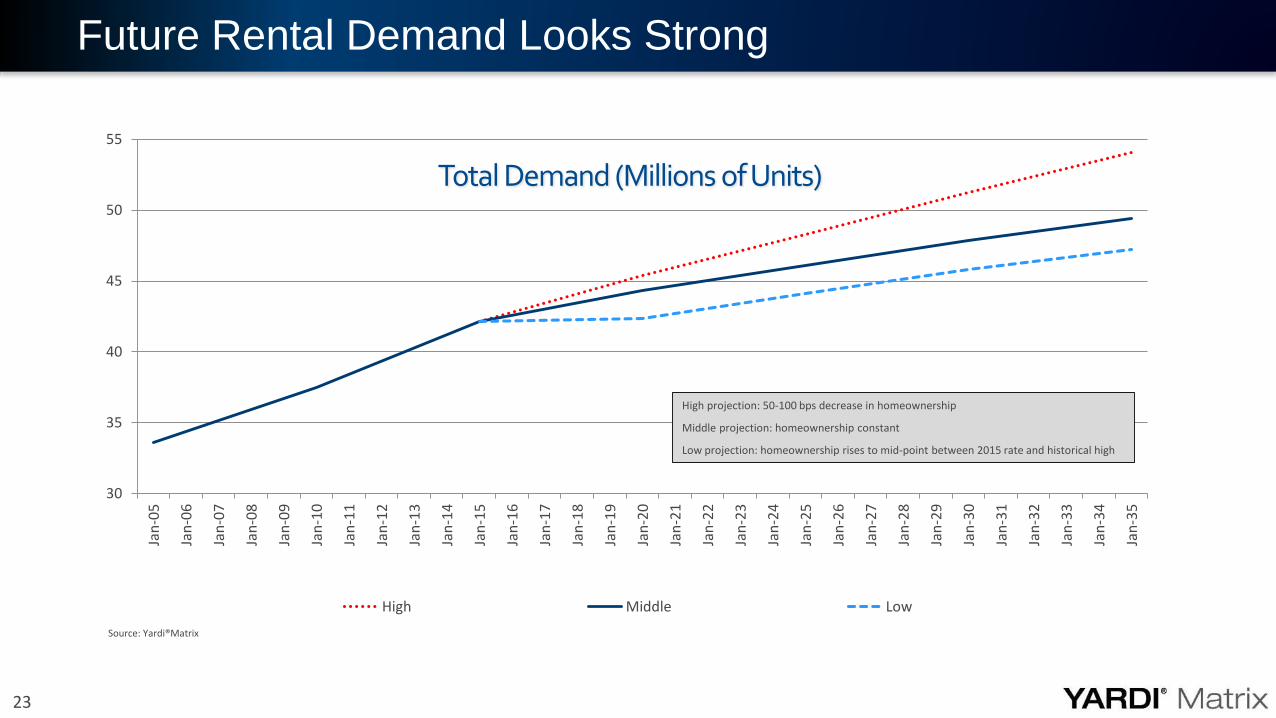

Future Rental Demand Looks Strong

Source: Yardi®Matrix

30

35

40

45

50

55Ja

n-0

5

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

Jan

-18

Jan

-19

Jan

-20

Jan

-21

Jan

-22

Jan

-23

Jan

-24

Jan

-25

Jan

-26

Jan

-27

Jan

-28

Jan

-29

Jan

-30

Jan

-31

Jan

-32

Jan

-33

Jan

-34

Jan

-35

Total Demand (Millions of Units)

High Middle Low

High projection: 50-100 bps decrease in homeownership

Middle projection: homeownership constant

Low projection: homeownership rises to mid-point between 2015 rate and historical high

24

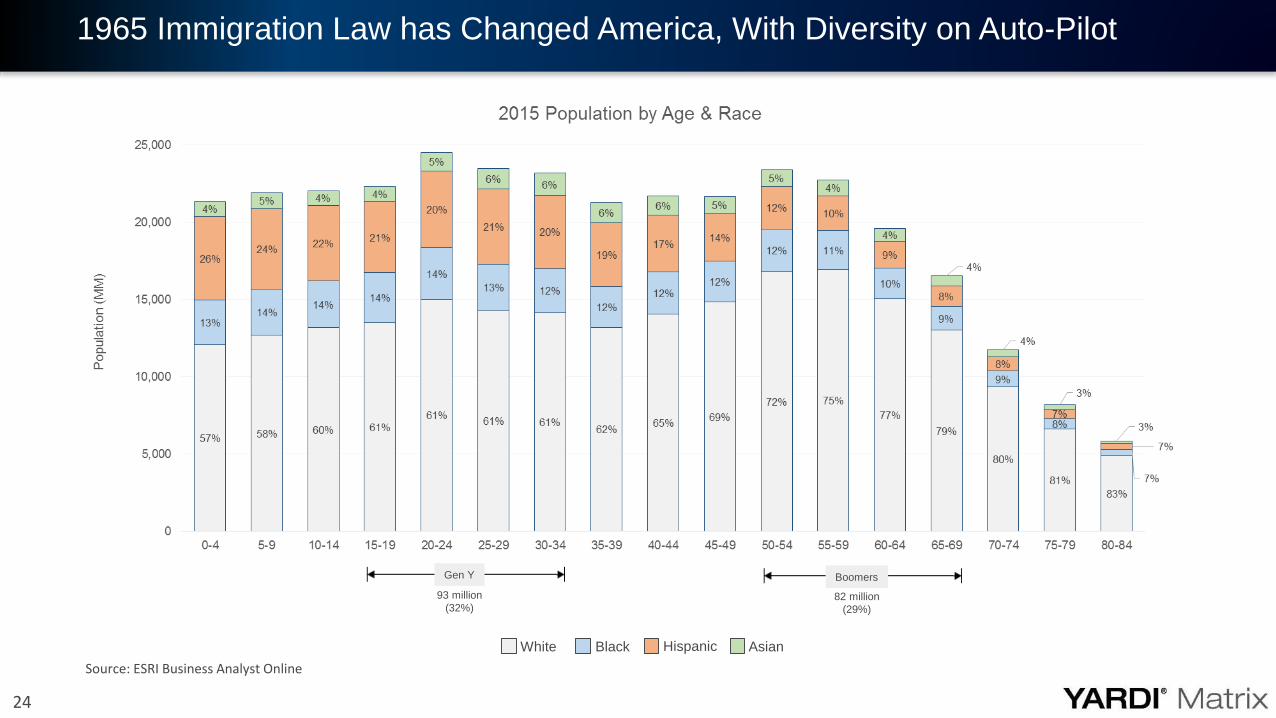

1965 Immigration Law has Changed America, With Diversity on Auto-Pilot

Gen Y

93 million

(32%)

Boomers

82 million

(29%)

Hispanic AsianBlackWhite

Source: ESRI Business Analyst Online

25

Radical Mobility

The Internet of Things

Collaborative Economy

Autonomous Vehicles

3D Printing

Major Technology Trends Driving Down Costs

26

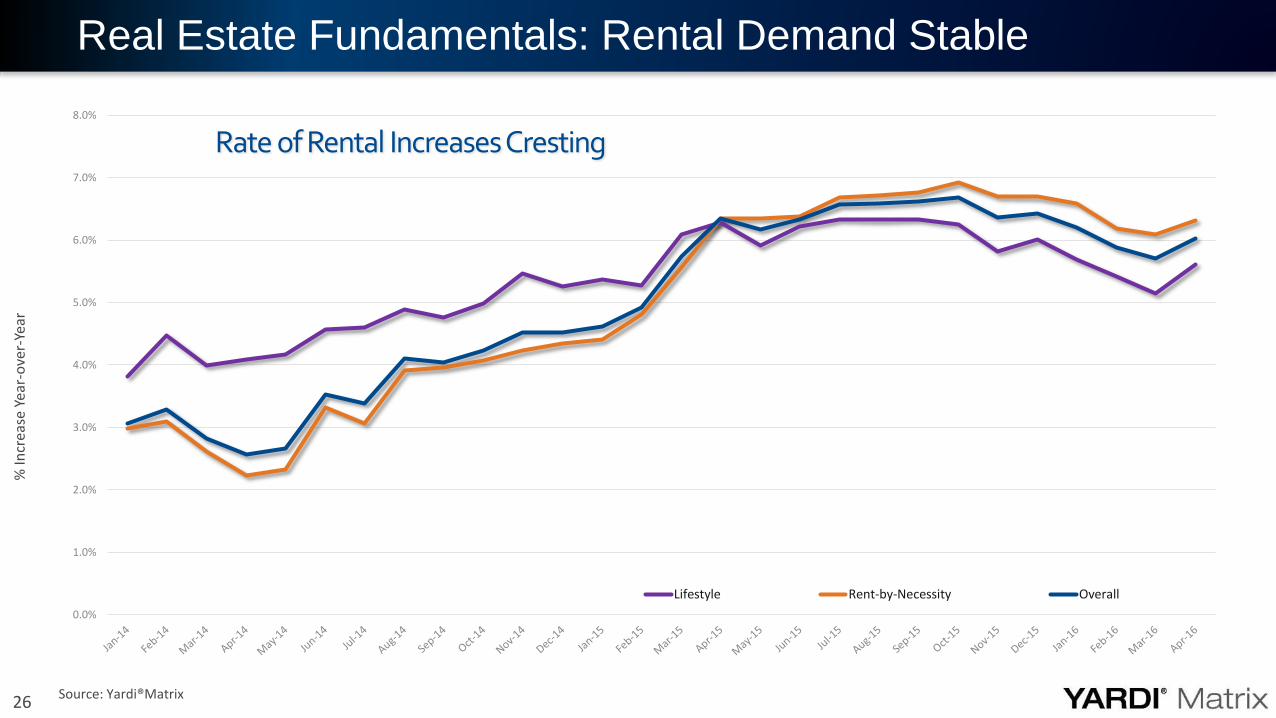

Real Estate Fundamentals: Rental Demand Stable%

Incr

ease

Yea

r-o

ver-

Year

Source: Yardi®Matrix

Rate of Rental Increases Cresting

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

Lifestyle Rent-by-Necessity Overall

27

Absolute Rent Spreads by Asset Type have Widened

$600

$700

$800

$900

$1,000

$1,100

$1,200

$1,300

$1,400

$1,500

$1,600

Average Rental Rate by Asset Class

Discretionary Upper Mid-Range Low Mid-Range Workforce - Upper Workforce - Lower

2010-2016 CAGR

6.0% Discretionary

5.3% Upper Mid-Range

4.1% Low Mid-Range

2.2% Workforce-Upper

2.9% Workforce-Lower

Jan 2008 Mar 2016

Discretionary-Upper-Mid

$270 $322

Discretionary-Lower-Mid

$343 $500

28

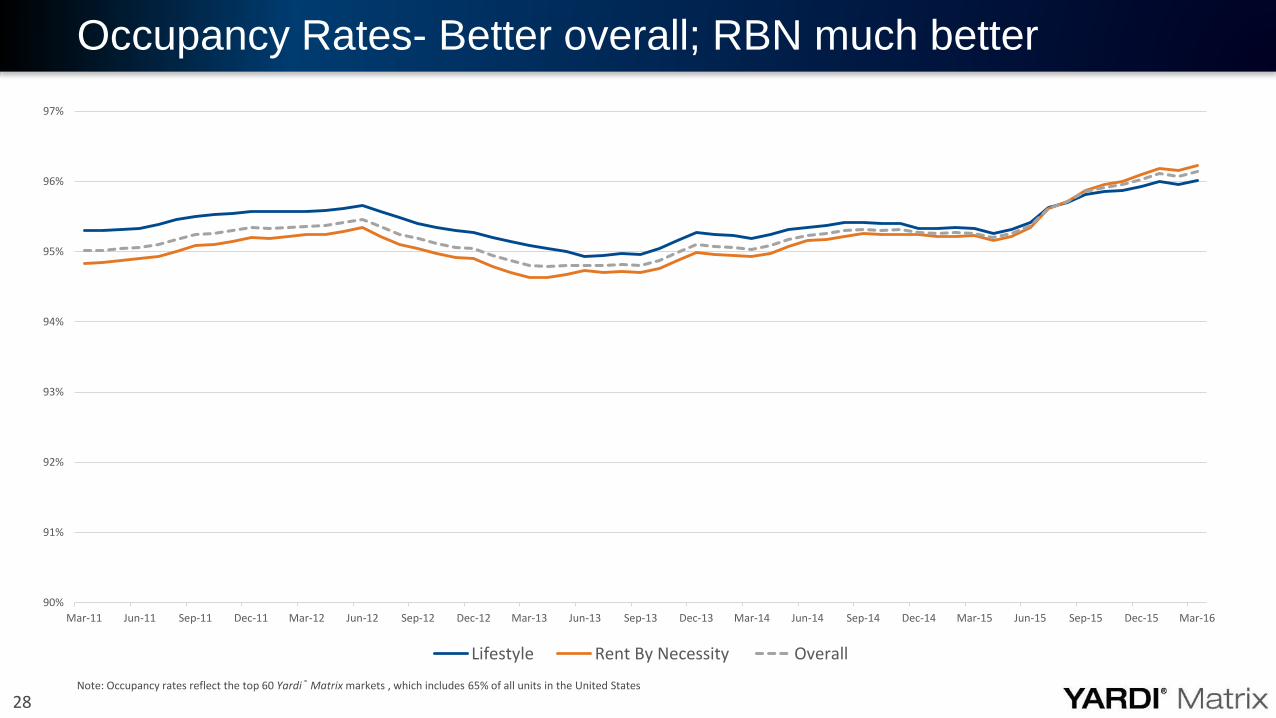

Occupancy Rates- Better overall; RBN much better

90%

91%

92%

93%

94%

95%

96%

97%

Mar-11 Jun-11 Sep-11 Dec-11 Mar-12 Jun-12 Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16

Lifestyle Rent By Necessity Overall

Note: Occupancy rates reflect the top 60 Yardi® Matrix markets , which includes 65% of all units in the United States

29

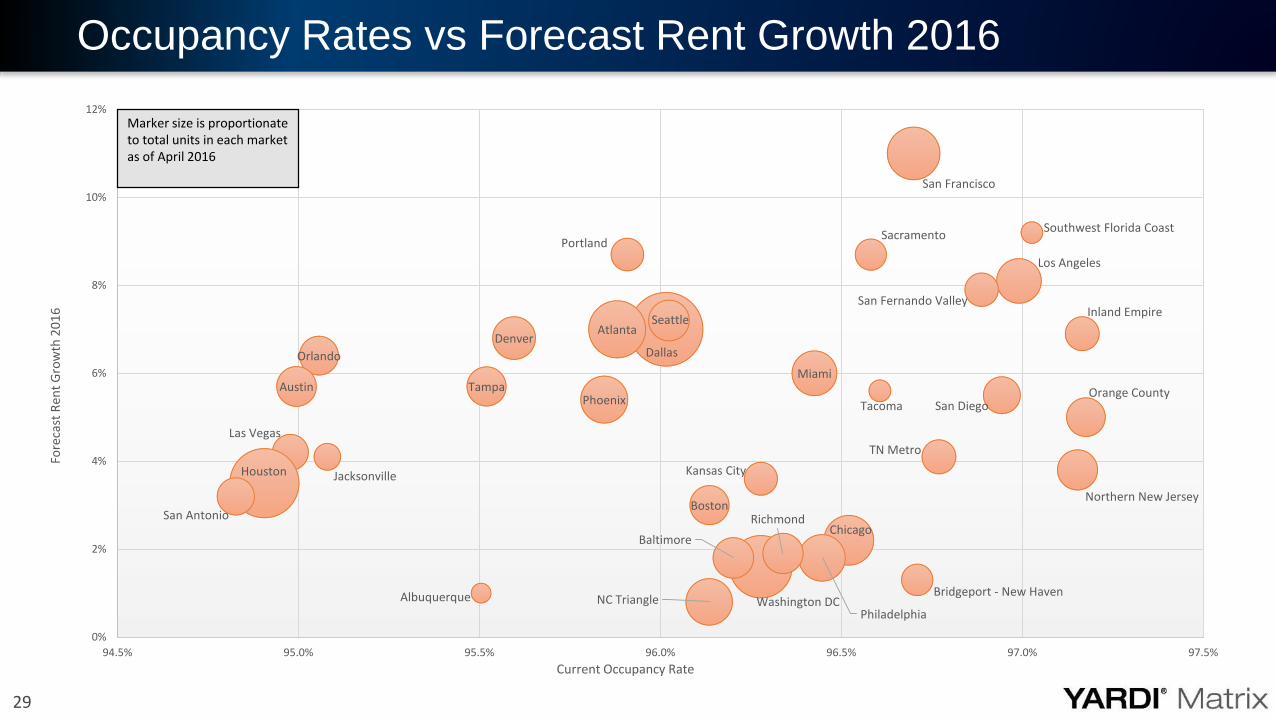

Occupancy Rates vs Forecast Rent Growth 2016

Orange County

Inland Empire

Northern New Jersey

Southwest Florida Coast

Los Angeles

San Diego

San Fernando Valley

TN Metro

Bridgeport - New Haven

San Francisco

Tacoma

Sacramento

Chicago

Philadelphia

Miami

Kansas City

Washington DC

Richmond

Baltimore

Boston

Dallas

NC Triangle

Seattle

Portland

Atlanta

Phoenix

Denver

Tampa

Albuquerque

Jacksonville

Orlando

Austin

Las Vegas

Houston

San Antonio

0%

2%

4%

6%

8%

10%

12%

94.5% 95.0% 95.5% 96.0% 96.5% 97.0% 97.5%

Fore

cast

Ren

t G

row

th 2

01

6

Current Occupancy Rate

Marker size is proportionate to total units in each market as of April 2016

30

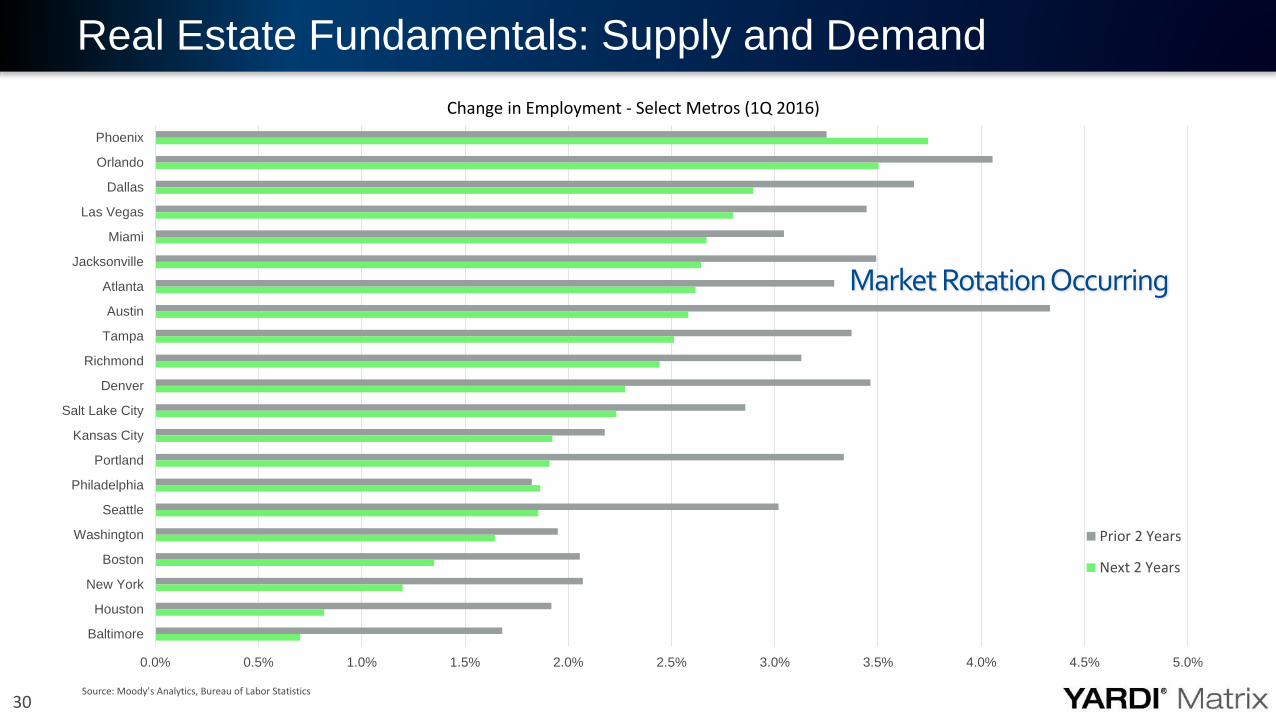

Real Estate Fundamentals: Supply and Demand

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5% 5.0%

Phoenix

Orlando

Dallas

Las Vegas

Miami

Jacksonville

Atlanta

Austin

Tampa

Richmond

Denver

Salt Lake City

Kansas City

Portland

Philadelphia

Seattle

Washington

Boston

New York

Houston

Baltimore

Change in Employment - Select Metros (1Q 2016)

Prior 2 Years

Next 2 Years

Source: Moody’s Analytics, Bureau of Labor Statistics

Market Rotation Occurring

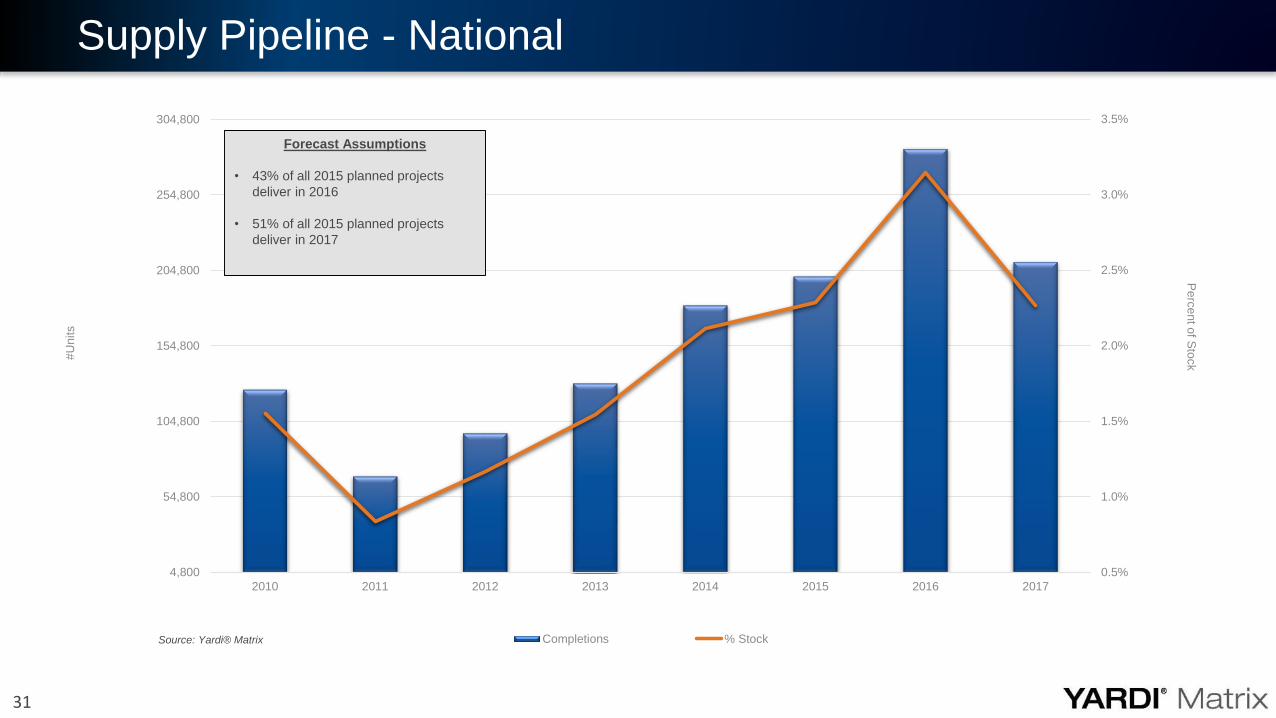

31

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4,800

54,800

104,800

154,800

204,800

254,800

304,800

2010 2011 2012 2013 2014 2015 2016 2017

Pe

rce

nt o

f Sto

ck#U

nits

Completions % Stock

Forecast Assumptions

• 43% of all 2015 planned projects

deliver in 2016

• 51% of all 2015 planned projects

deliver in 2017

Source: Yardi® Matrix

Supply Pipeline - National

32

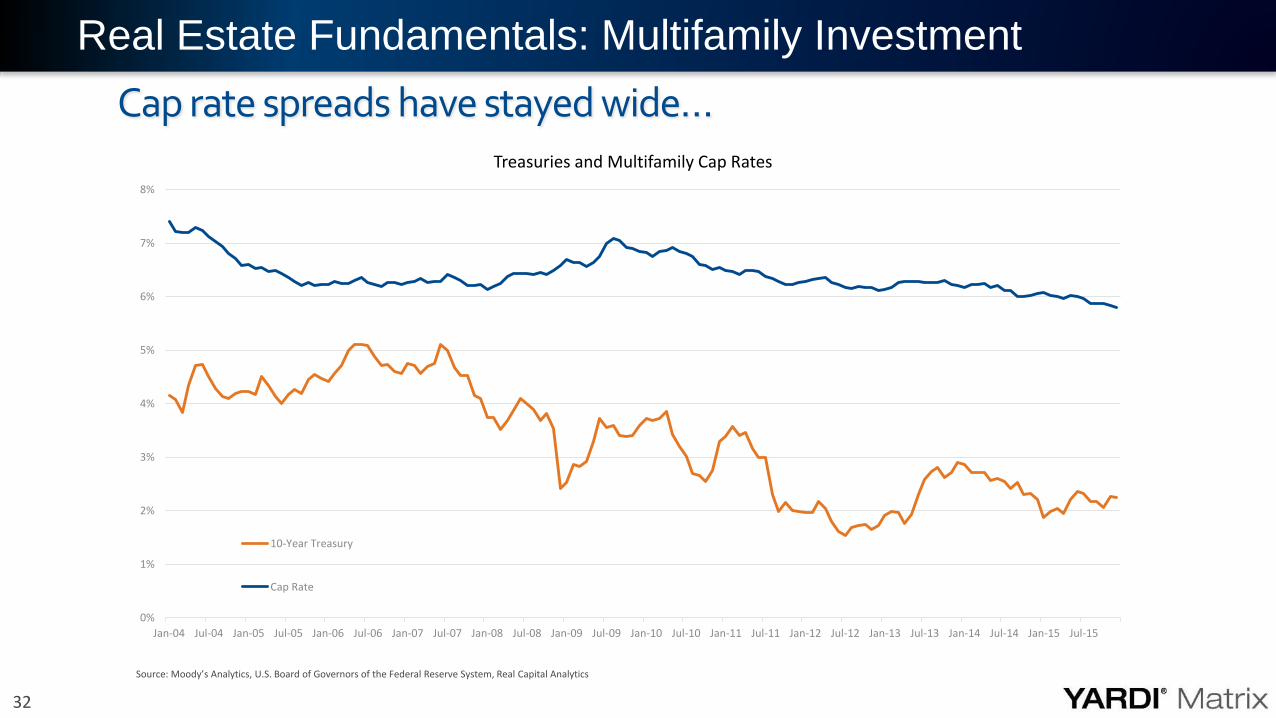

Cap rate spreads have stayed wide…

Real Estate Fundamentals: Multifamily Investment

0%

1%

2%

3%

4%

5%

6%

7%

8%

Jan-04 Jul-04 Jan-05 Jul-05 Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15

Treasuries and Multifamily Cap Rates

10-Year Treasury

Cap Rate

Source: Moody’s Analytics, U.S. Board of Governors of the Federal Reserve System, Real Capital Analytics

33

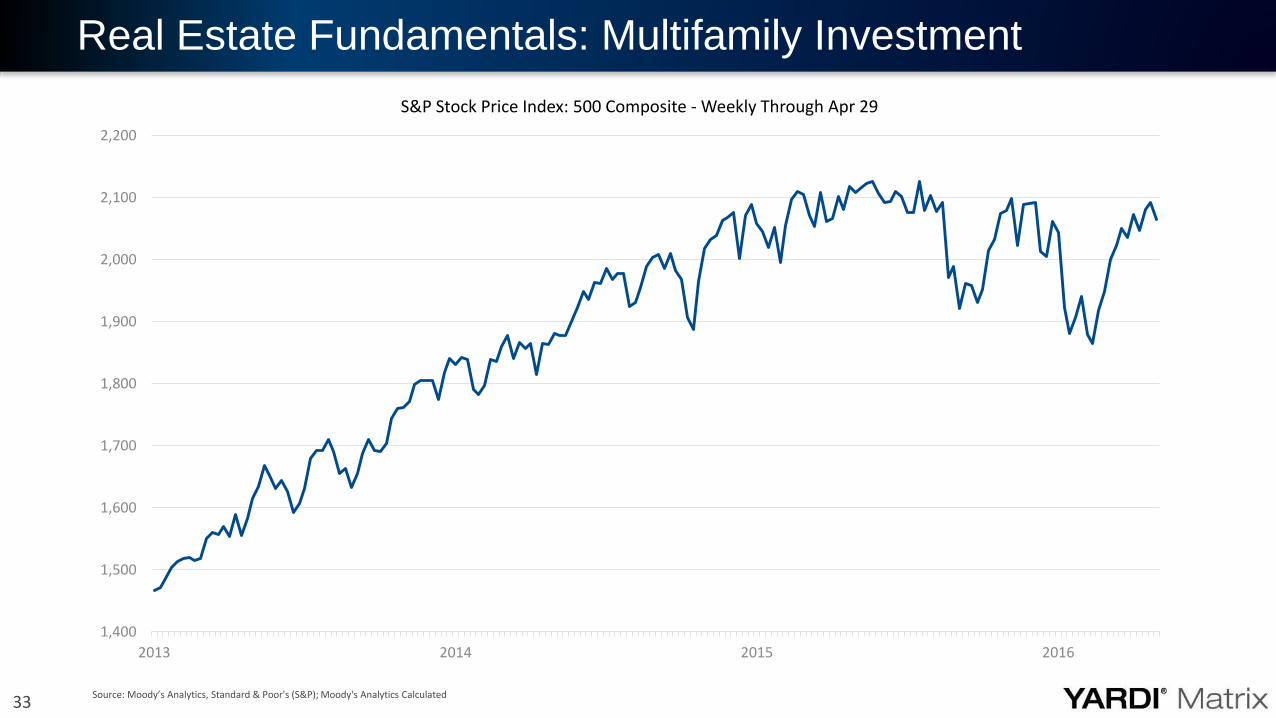

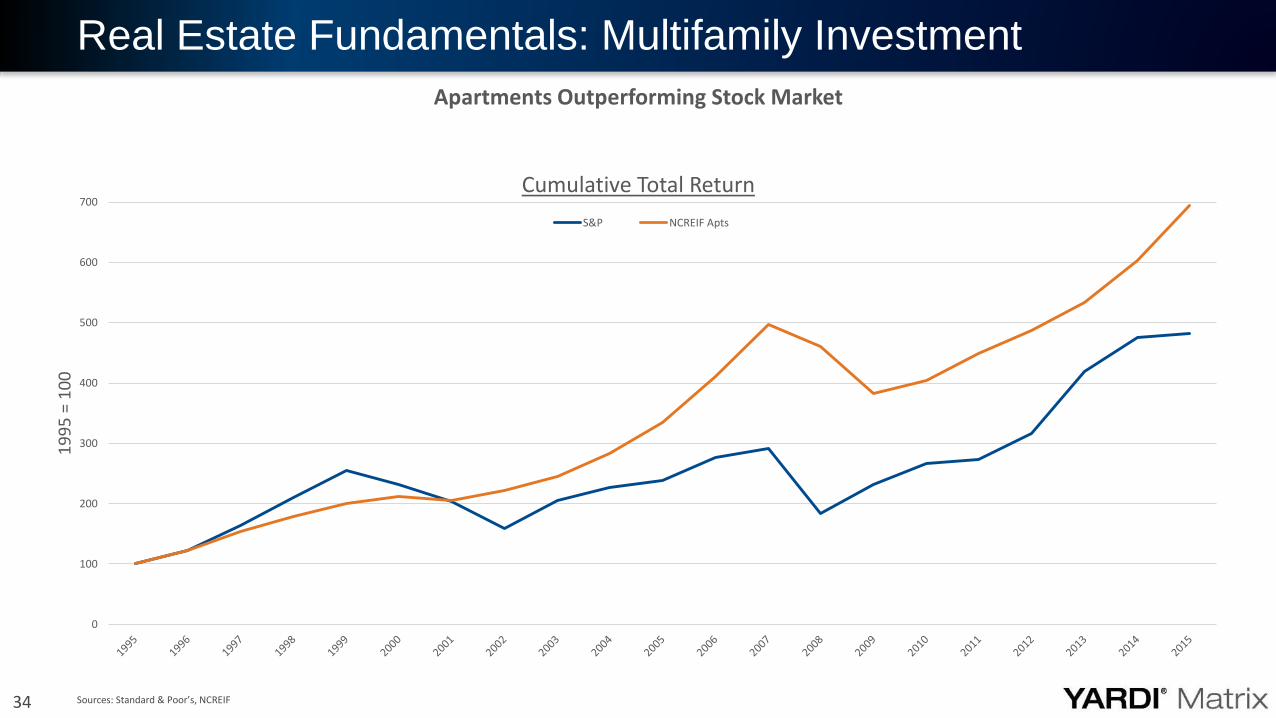

Real Estate Fundamentals: Multifamily Investment

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2,200

2013 2014 2015 2016

S&P Stock Price Index: 500 Composite - Weekly Through Apr 29

Source: Moody’s Analytics, Standard & Poor's (S&P); Moody's Analytics Calculated

34

Real Estate Fundamentals: Multifamily Investment

Sources: Standard & Poor’s, NCREIF

0

100

200

300

400

500

600

700

19

95

= 1

00

Apartments Outperforming Stock Market

Cumulative Total Return

S&P NCREIF Apts

Secondary Investment Grade Market Selection

Jeff AdlerVice President, Matrix

36

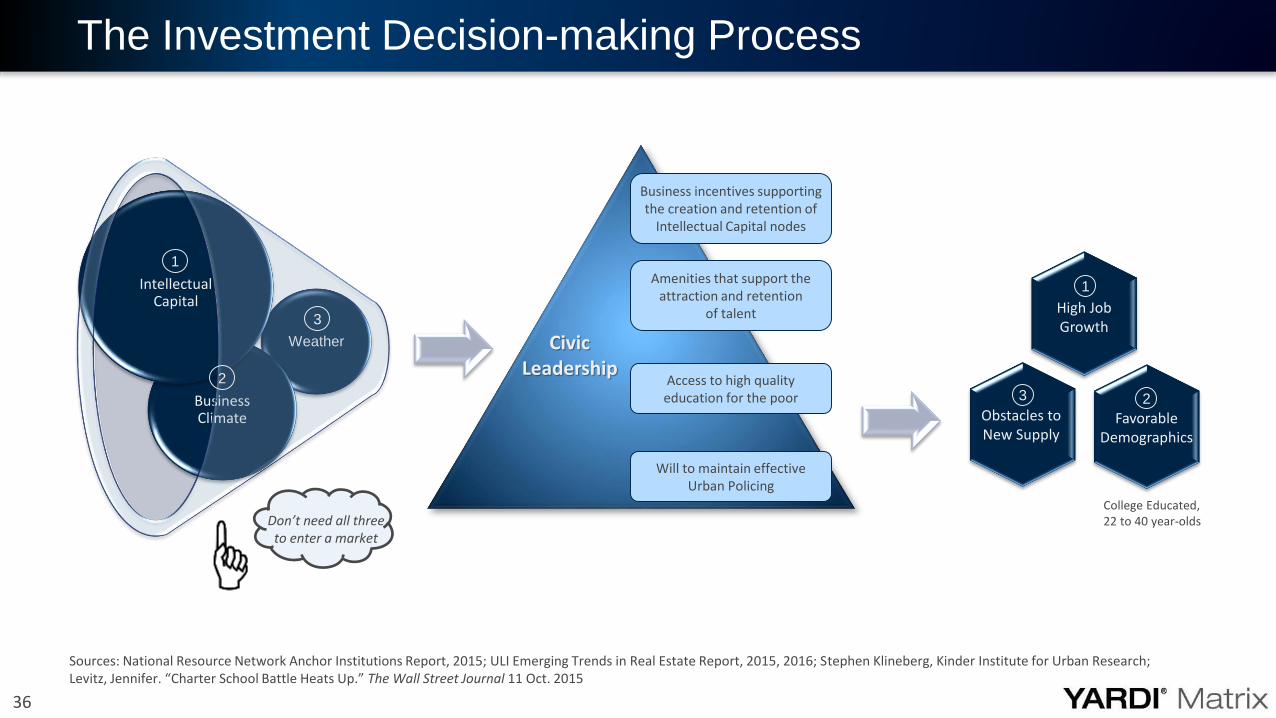

The Investment Decision-making Process

Don’t need all three to enter a market

Weather

Business Climate

IntellectualCapital

1

3

2 Access to high quality education for the poor

Amenities that support the attraction and retention

of talent

Business incentives supporting the creation and retention of

Intellectual Capital nodes

Civic Leadership

High Job Growth

1

College Educated, 22 to 40 year-olds

Favorable Demographics

2Obstacles toNew Supply

3

Will to maintain effective Urban Policing

Sources: National Resource Network Anchor Institutions Report, 2015; ULI Emerging Trends in Real Estate Report, 2015, 2016; Stephen Klineberg, Kinder Institute for Urban Research;Levitz, Jennifer. “Charter School Battle Heats Up.” The Wall Street Journal 11 Oct. 2015

37

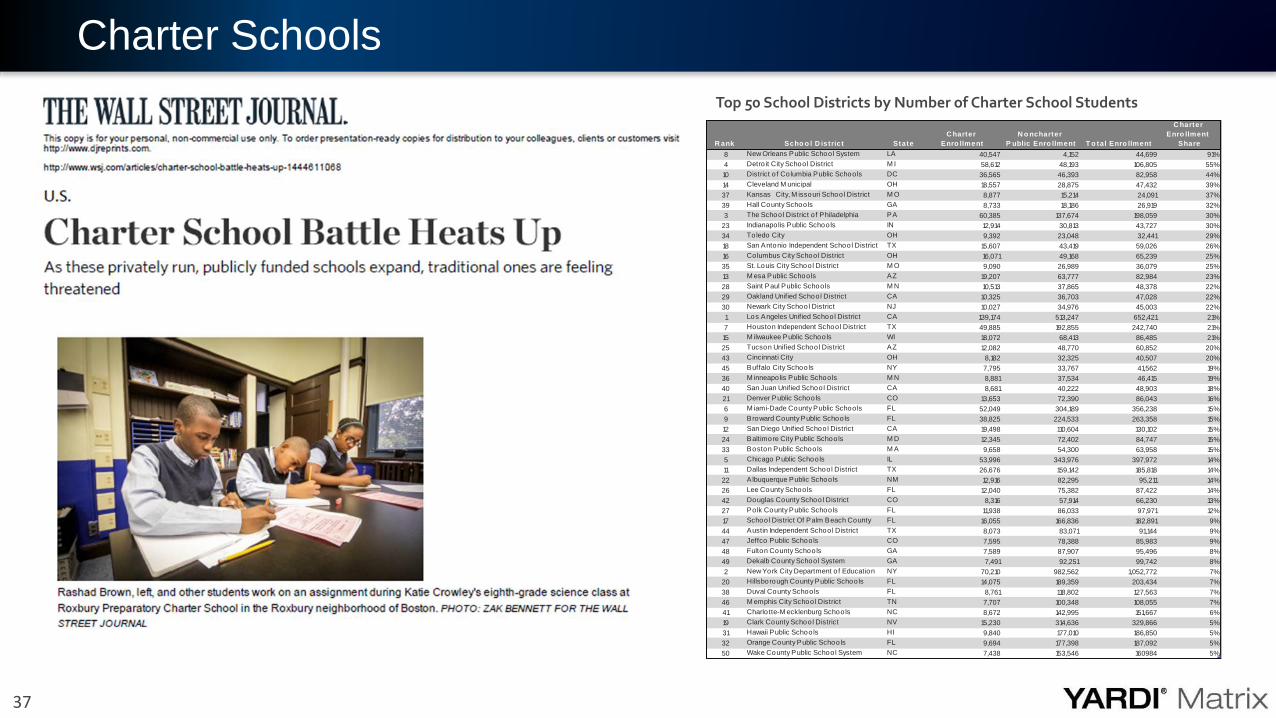

Charter Schools

R ank Scho o l D istrict State

C harter

Enro llment

N o ncharter

P ublic Enro llment T o tal Enro llment

C harter

Enro llment

Share

8 New Orleans Public School System LA 40,547 4,152 44,699 91%

4 Detro it City School District M I 58,612 48,193 106,805 55%

10 District o f Columbia Public Schools DC 36,565 46,393 82,958 44%

14 Cleveland M unicipal OH 18,557 28,875 47,432 39%

37 Kansas City, M issouri School District M O 8,877 15,214 24,091 37%

39 Hall County Schools GA 8,733 18,186 26,919 32%

3 The School District o f Philadelphia PA 60,385 137,674 198,059 30%

23 Indianapolis Public Schools IN 12,914 30,813 43,727 30%

34 Toledo City OH 9,392 23,048 32,441 29%

18 San Antonio Independent School District TX 15,607 43,419 59,026 26%

16 Columbus City School District OH 16,071 49,168 65,239 25%

35 St. Louis City School District M O 9,090 26,989 36,079 25%

13 M esa Public Schools AZ 19,207 63,777 82,984 23%

28 Saint Paul Public Schools M N 10,513 37,865 48,378 22%

29 Oakland Unified School District CA 10,325 36,703 47,028 22%

30 Newark City School District NJ 10,027 34,976 45,003 22%

1 Los Angeles Unified School District CA 139,174 513,247 652,421 21%

7 Houston Independent School District TX 49,885 192,855 242,740 21%

15 M ilwaukee Public Schools WI 18,072 68,413 86,485 21%

25 Tucson Unified School District AZ 12,082 48,770 60,852 20%

43 Cincinnati City OH 8,182 32,325 40,507 20%

45 Buffalo City Schools NY 7,795 33,767 41,562 19%

36 M inneapolis Public Schools M N 8,881 37,534 46,415 19%

40 San Juan Unified School District CA 8,681 40,222 48,903 18%

21 Denver Public Schools CO 13,653 72,390 86,043 16%

6 M iami-Dade County Public Schools FL 52,049 304,189 356,238 15%

9 Broward County Public Schools FL 38,825 224,533 263,358 15%

12 San Diego Unified School District CA 19,498 110,604 130,102 15%

24 Baltimore City Public Schools M D 12,345 72,402 84,747 15%

33 Boston Public Schools M A 9,658 54,300 63,958 15%

5 Chicago Public Schools IL 53,996 343,976 397,972 14%

11 Dallas Independent School District TX 26,676 159,142 185,818 14%

22 Albuquerque Public Schools NM 12,916 82,295 95,211 14%

26 Lee County Schools FL 12,040 75,382 87,422 14%

42 Douglas County School District CO 8,316 57,914 66,230 13%

27 Polk County Public Schools FL 11,938 86,033 97,971 12%

17 School District Of Palm Beach County FL 16,055 166,836 182,891 9%

44 Austin Independent School District TX 8,073 83,071 91,144 9%

47 Jeffco Public Schools CO 7,595 78,388 85,983 9%

48 Fulton County Schools GA 7,589 87,907 95,496 8%

49 Dekalb County School System GA 7,491 92,251 99,742 8%

2 New York City Department o f Education NY 70,210 982,562 1,052,772 7%

20 Hillsborough County Public Schools FL 14,075 189,359 203,434 7%

38 Duval County Schools FL 8,761 118,802 127,563 7%

46 M emphis City School District TN 7,707 100,348 108,055 7%

41 Charlo tte-M ecklenburg Schools NC 8,672 142,995 151,667 6%

19 Clark County School District NV 15,230 314,636 329,866 5%

31 Hawaii Public Schools HI 9,840 177,010 186,850 5%

32 Orange County Public Schools FL 9,694 177,398 187,092 5%

50 Wake County Public School System NC 7,438 153,546 160984 5%

Top 50 School Districts by Number of Charter School Students

38

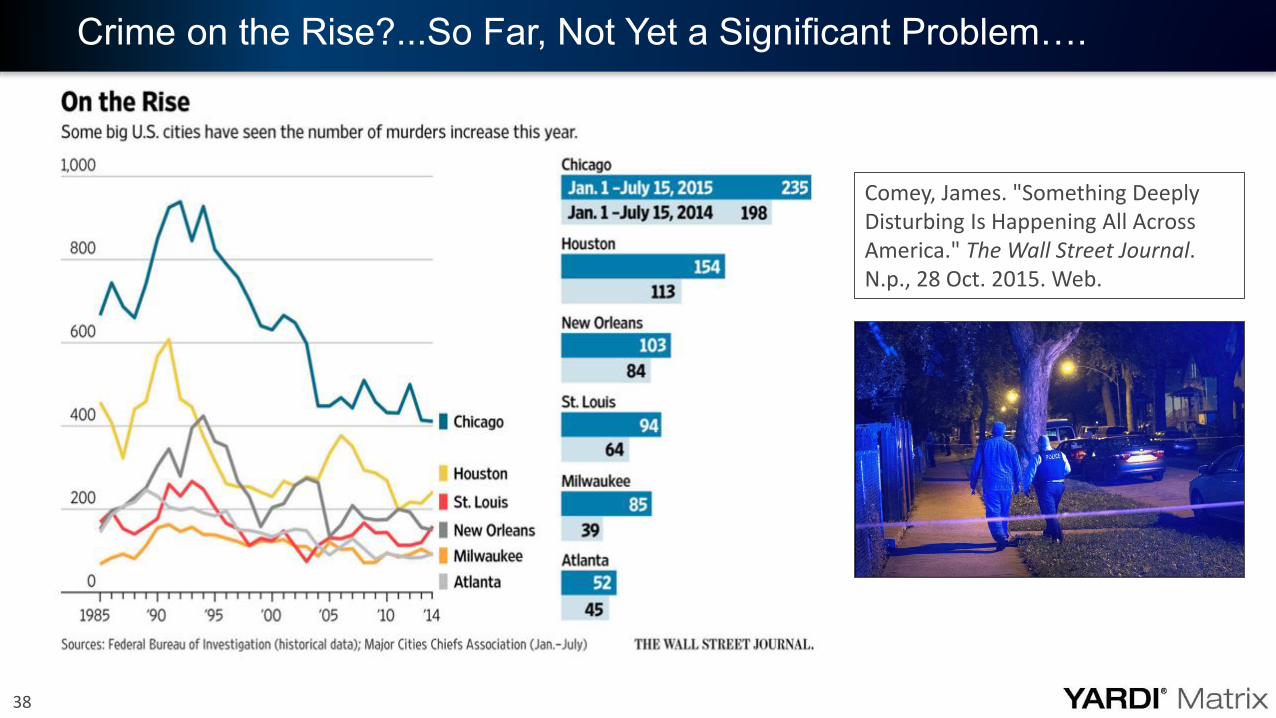

Crime on the Rise?...So Far, Not Yet a Significant Problem….

Comey, James. "Something Deeply Disturbing Is Happening All Across America." The Wall Street Journal. N.p., 28 Oct. 2015. Web.

39

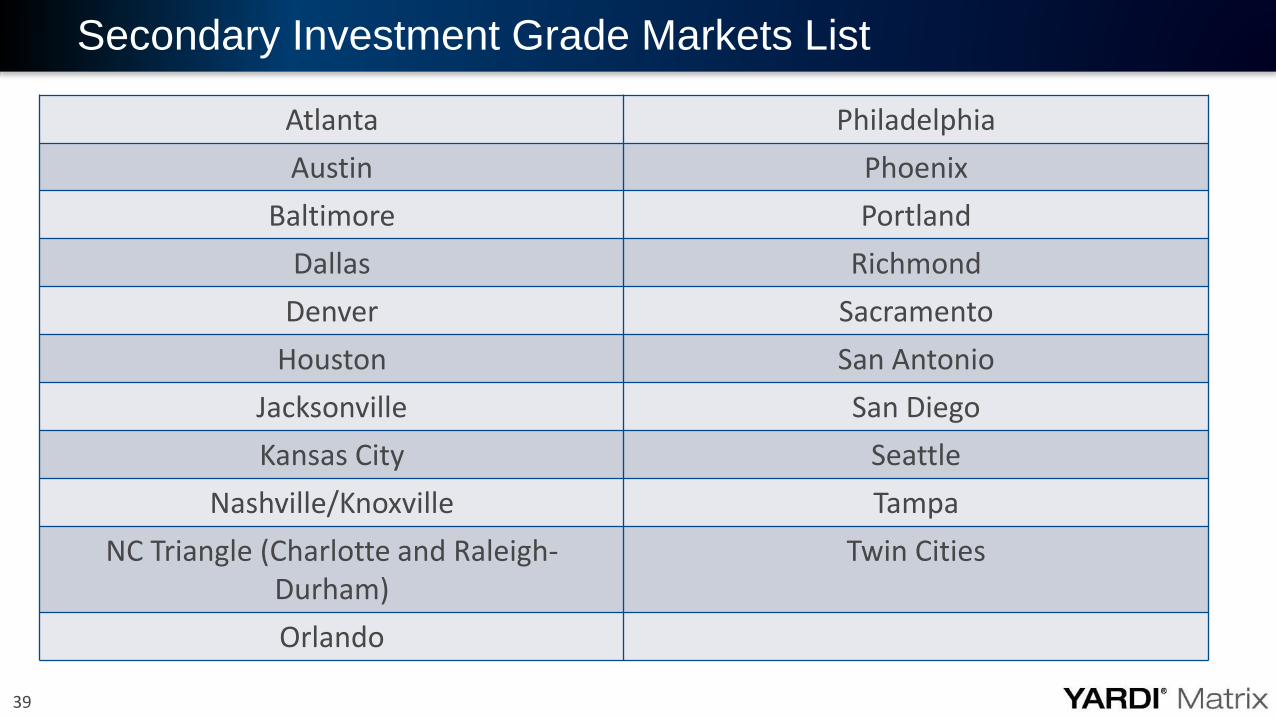

Secondary Investment Grade Markets List

Atlanta Philadelphia

Austin Phoenix

Baltimore Portland

Dallas Richmond

Denver Sacramento

Houston San Antonio

Jacksonville San Diego

Kansas City Seattle

Nashville/Knoxville Tampa

NC Triangle (Charlotte and Raleigh-Durham)

Twin Cities

Orlando

40

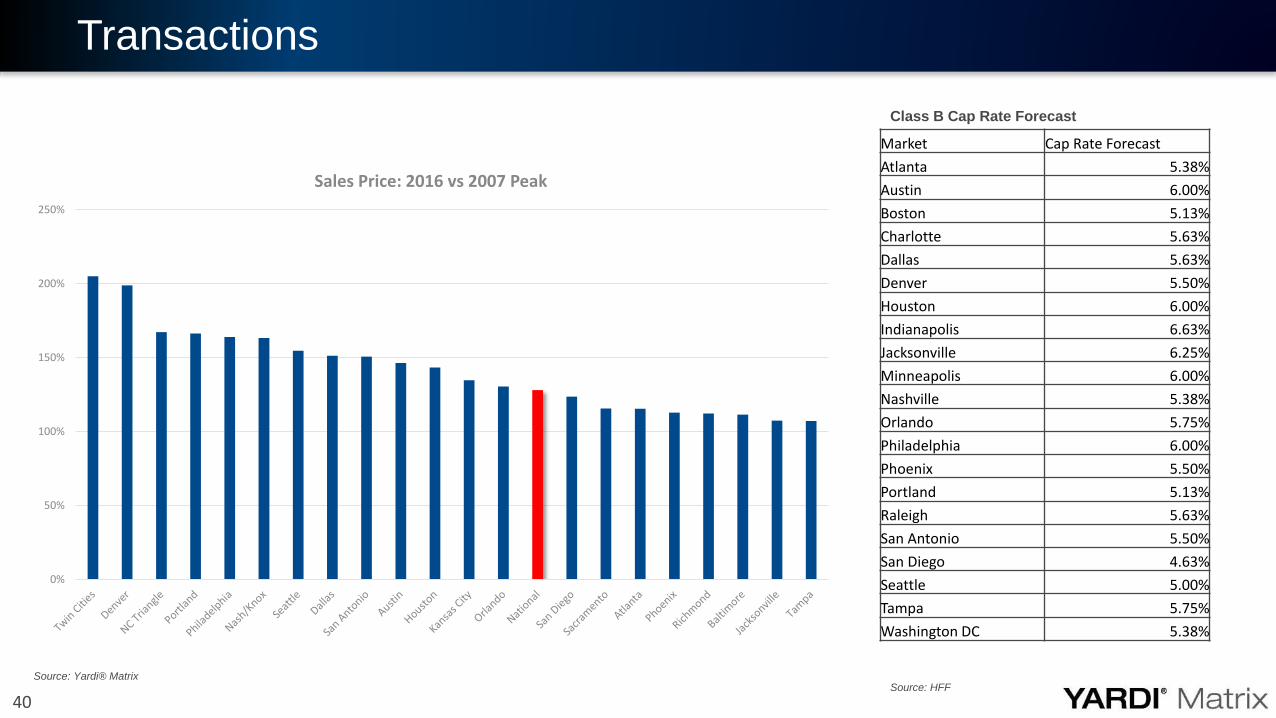

Transactions

Source: Yardi® Matrix

Market Cap Rate Forecast

Atlanta 5.38%

Austin 6.00%

Boston 5.13%

Charlotte 5.63%

Dallas 5.63%

Denver 5.50%

Houston 6.00%

Indianapolis 6.63%

Jacksonville 6.25%

Minneapolis 6.00%

Nashville 5.38%

Orlando 5.75%

Philadelphia 6.00%

Phoenix 5.50%

Portland 5.13%

Raleigh 5.63%

San Antonio 5.50%

San Diego 4.63%

Seattle 5.00%

Tampa 5.75%

Washington DC 5.38%

Class B Cap Rate Forecast

Source: HFF

0%

50%

100%

150%

200%

250%

Sales Price: 2016 vs 2007 Peak

41

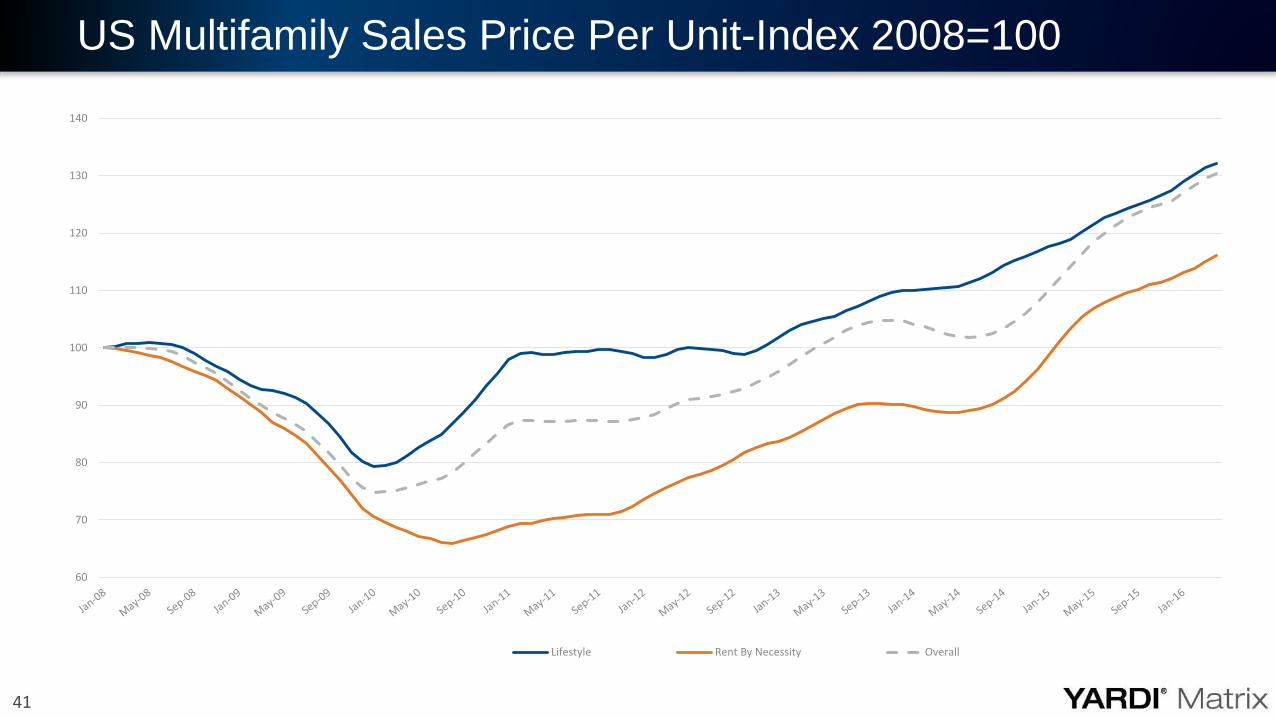

US Multifamily Sales Price Per Unit-Index 2008=100

60

70

80

90

100

110

120

130

140

Lifestyle Rent By Necessity Overall

42

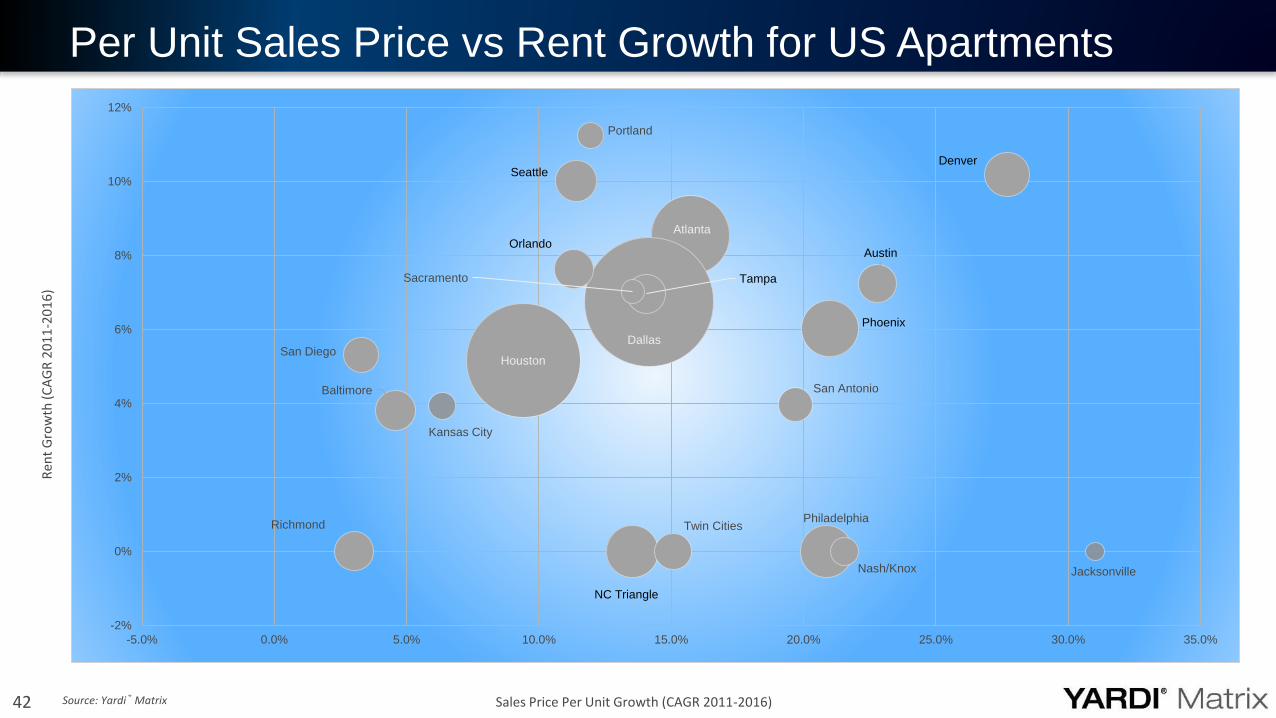

Per Unit Sales Price vs Rent Growth for US Apartments

Source: Yardi® Matrix Sales Price Per Unit Growth (CAGR 2011-2016)

Ren

t G

row

th (

CA

GR

20

11

-20

16

)

Atlanta

Austin

Baltimore

Dallas

Denver

Houston

Jacksonville

Kansas City

NC Triangle

Orlando

Philadelphia

Phoenix

Portland

Richmond

TampaSacramento

San Antonio

San Diego

Seattle

Nash/Knox

Twin Cities

-2%

0%

2%

4%

6%

8%

10%

12%

-5.0% 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0%

43

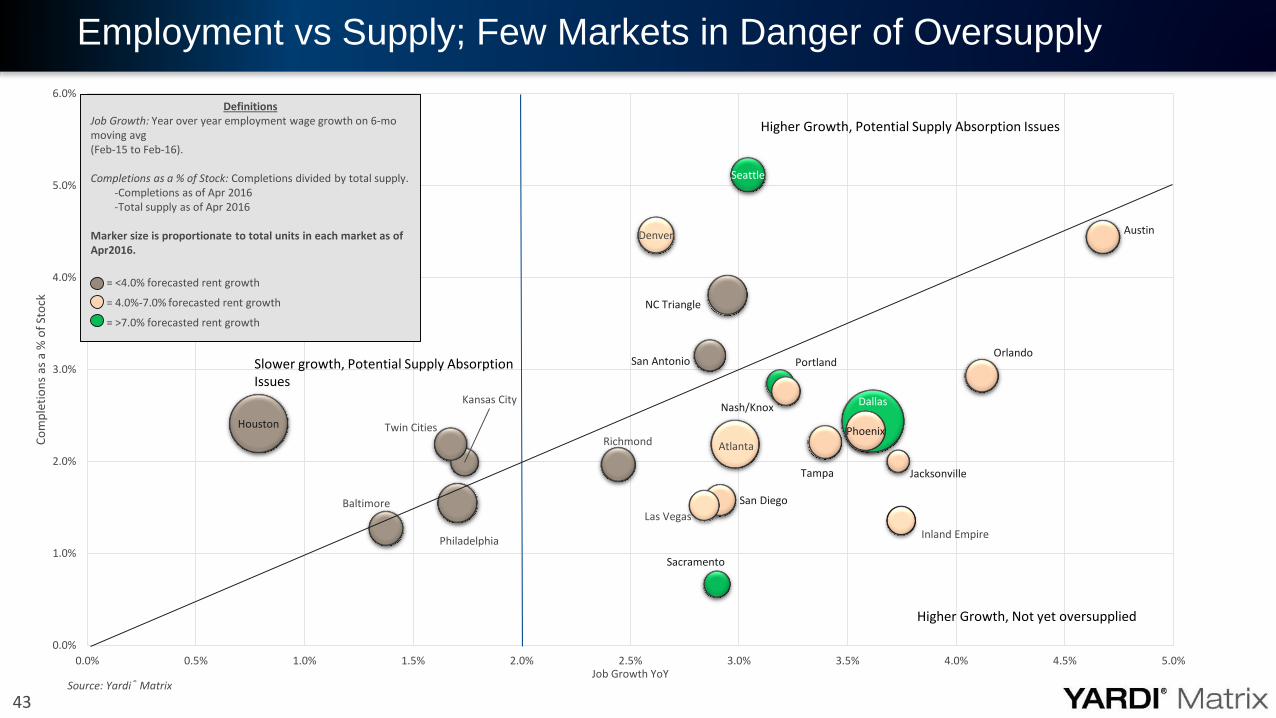

Employment vs Supply; Few Markets in Danger of Oversupply

Source: Yardi® Matrix

Portland

Denver

Sacramento

Seattle

Atlanta

San Diego

Orlando

Dallas

Houston

Austin

Nash/Knox

Phoenix

Tampa

Kansas City

NC Triangle

Jacksonville

San Antonio

Twin Cities

Philadelphia

Baltimore

Richmond

Inland Empire

Las Vegas

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5% 5.0%

Co

mp

leti

on

s as

a %

of

Sto

ck

Job Growth YoY

DefinitionsJob Growth: Year over year employment wage growth on 6-mo moving avg(Feb-15 to Feb-16).

Completions as a % of Stock: Completions divided by total supply.-Completions as of Apr 2016-Total supply as of Apr 2016

Marker size is proportionate to total units in each market as of Apr2016.

= <4.0% forecasted rent growth

= 4.0%-7.0% forecasted rent growth

= >7.0% forecasted rent growth

Slower growth, Potential Supply Absorption Issues

Higher Growth, Potential Supply Absorption Issues

Higher Growth, Not yet oversupplied

44

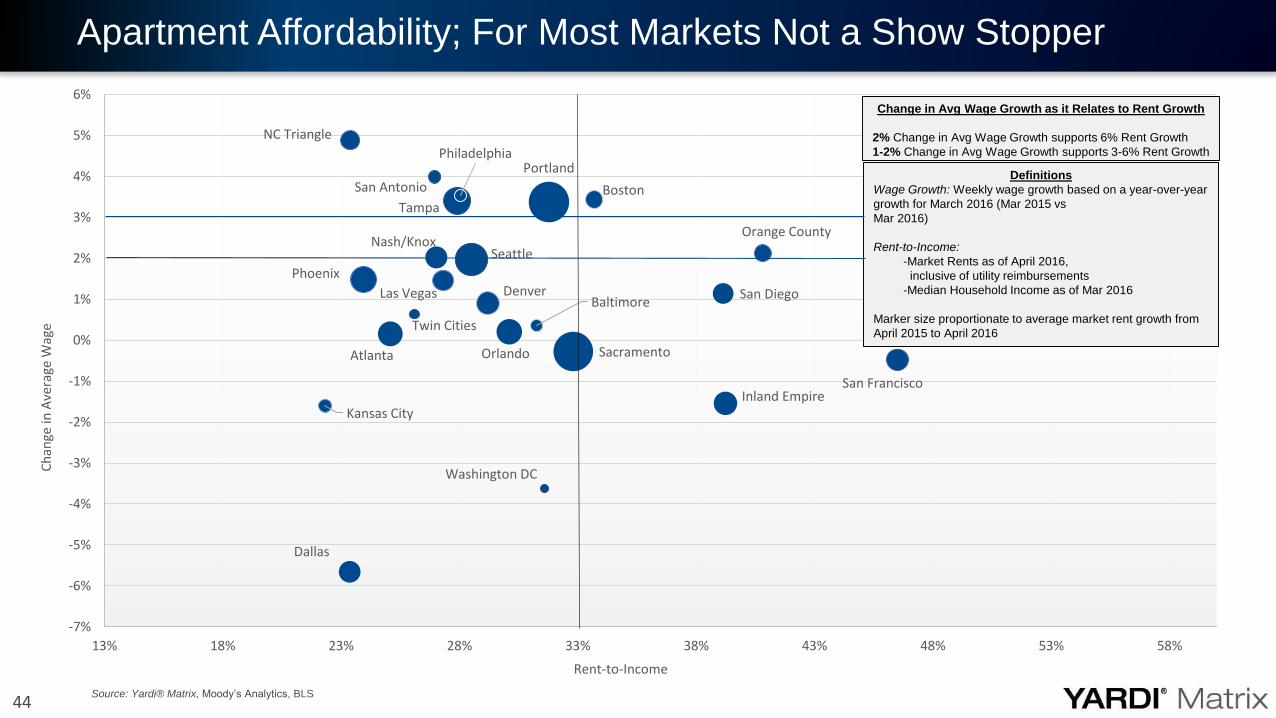

Apartment Affordability; For Most Markets Not a Show Stopper

Source: Yardi® Matrix, Moody’s Analytics, BLS

OrlandoAtlanta

Baltimore

Boston

Dallas

Denver

Inland EmpireKansas City

Nash/Knox

NC Triangle

Tampa

Philadelphia

Orange County

Phoenix

San Antonio

San Diego

San Francisco

Seattle

Twin Cities

Washington DC

Las Vegas

Portland

Sacramento

-7%

-6%

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

13% 18% 23% 28% 33% 38% 43% 48% 53% 58%

Ch

ange

in A

vera

ge W

age

Rent-to-Income

Definitions

Wage Growth: Weekly wage growth based on a year-over-year

growth for March 2016 (Mar 2015 vs

Mar 2016)

Rent-to-Income:

-Market Rents as of April 2016,

inclusive of utility reimbursements

-Median Household Income as of Mar 2016

Marker size proportionate to average market rent growth from

April 2015 to April 2016

Change in Avg Wage Growth as it Relates to Rent Growth

2% Change in Avg Wage Growth supports 6% Rent Growth

1-2% Change in Avg Wage Growth supports 3-6% Rent Growth

45

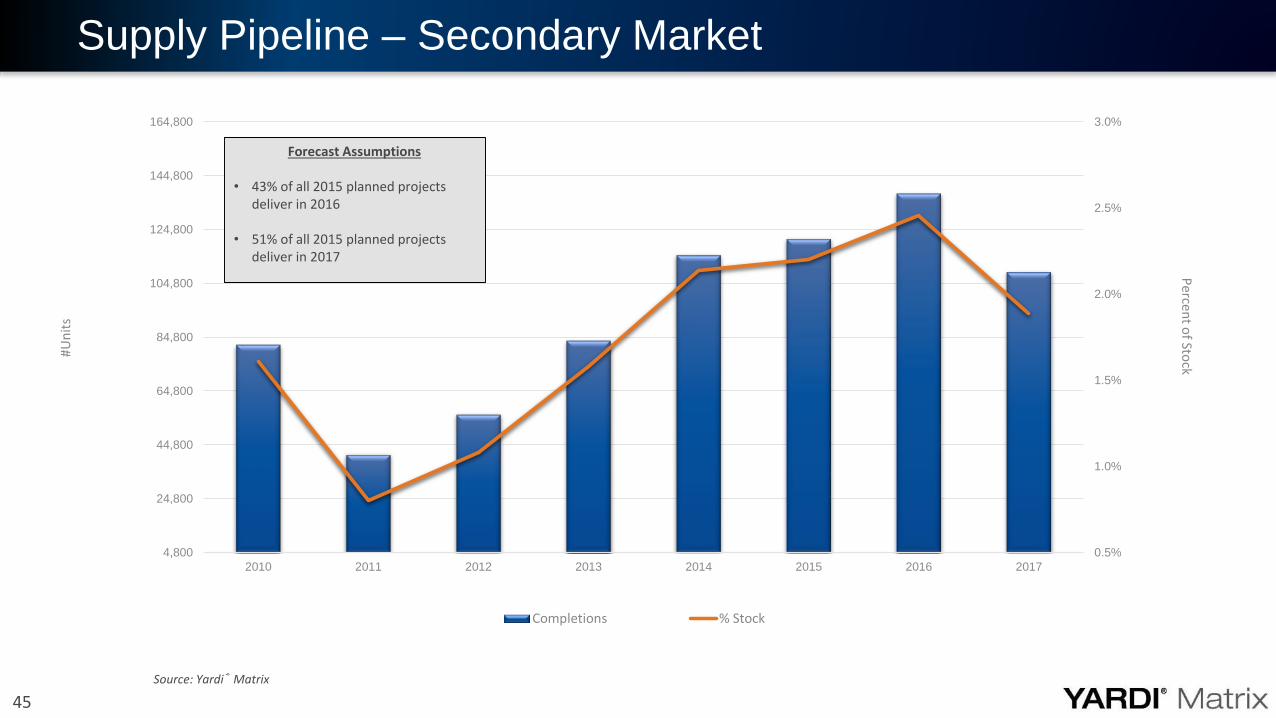

Supply Pipeline – Secondary Market

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

4,800

24,800

44,800

64,800

84,800

104,800

124,800

144,800

164,800

2010 2011 2012 2013 2014 2015 2016 2017

Perce

nt o

f Stock

#Un

its

Completions % Stock

Forecast Assumptions

• 43% of all 2015 planned projects deliver in 2016

• 51% of all 2015 planned projects deliver in 2017

Source: Yardi® Matrix

46

Potential Secondary Investment Grade Markets

Market Intellectual Node Business Climate Physical Climate

Denver

Energy & MiningGovernmentHealthcare

Communications

PortlandHealthcare

ApparelTech

SeattleTech

AerospaceEducation

AtlantaHealthcare

MediaCommunications

HoustonOil & Gas

Healthcare

DallasAerospaceHealthcare

Banking

TampaHealthcare

RetailEducation

AustinTech

Education

NC TriangleHealthcare

BankingTech

Good But Oversupplied Short Term

• Charlotte

• Raleigh-Durham

Structurally Unattractive, But Open to Being Persuaded

• Jacksonville

• Phoenix

• Orlando

47

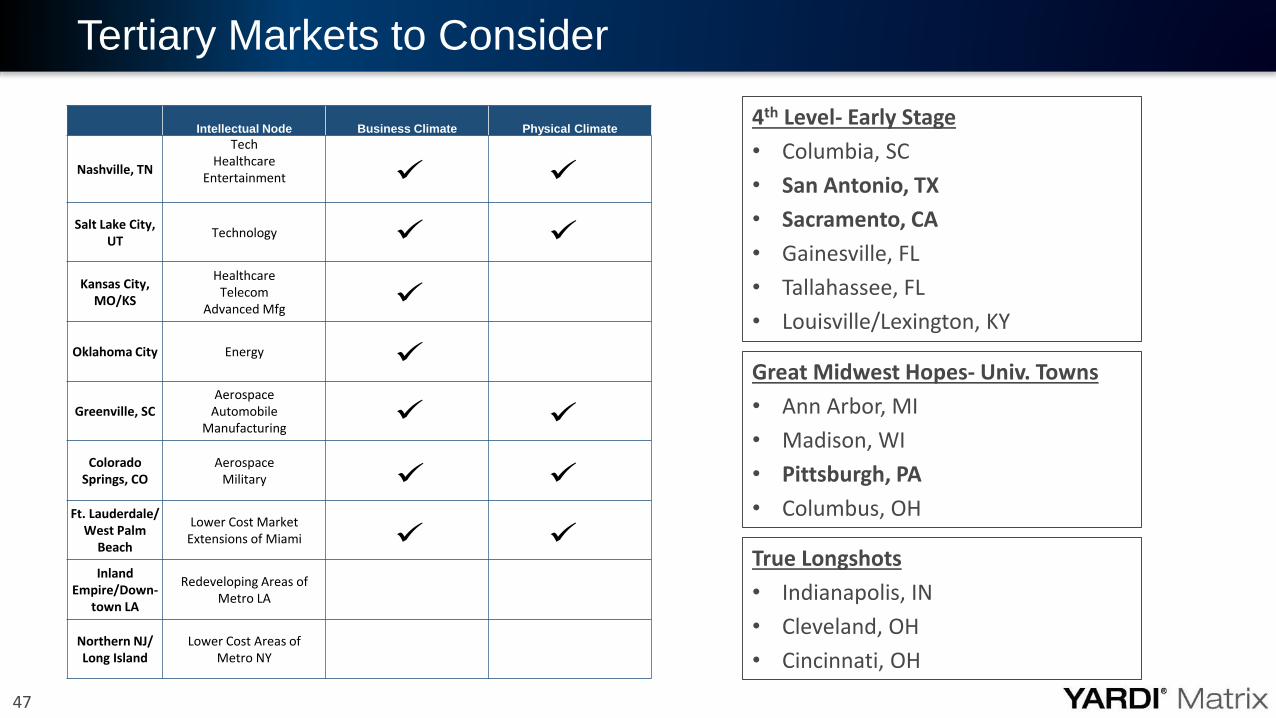

Tertiary Markets to Consider

Intellectual Node Business Climate Physical Climate

Nashville, TN

TechHealthcare

Entertainment

Salt Lake City, UT

Technology

Kansas City, MO/KS

Healthcare Telecom

Advanced Mfg

Oklahoma City Energy

Greenville, SCAerospace

AutomobileManufacturing

Colorado Springs, CO

AerospaceMilitary

Ft. Lauderdale/ West Palm

Beach

Lower Cost Market Extensions of Miami

Inland Empire/Down-

town LA

Redeveloping Areas of Metro LA

Northern NJ/ Long Island

Lower Cost Areas of Metro NY

4th Level- Early Stage

• Columbia, SC

• San Antonio, TX

• Sacramento, CA

• Gainesville, FL

• Tallahassee, FL

• Louisville/Lexington, KY

Great Midwest Hopes- Univ. Towns

• Ann Arbor, MI

• Madison, WI

• Pittsburgh, PA

• Columbus, OH

True Longshots

• Indianapolis, IN

• Cleveland, OH

• Cincinnati, OH

48

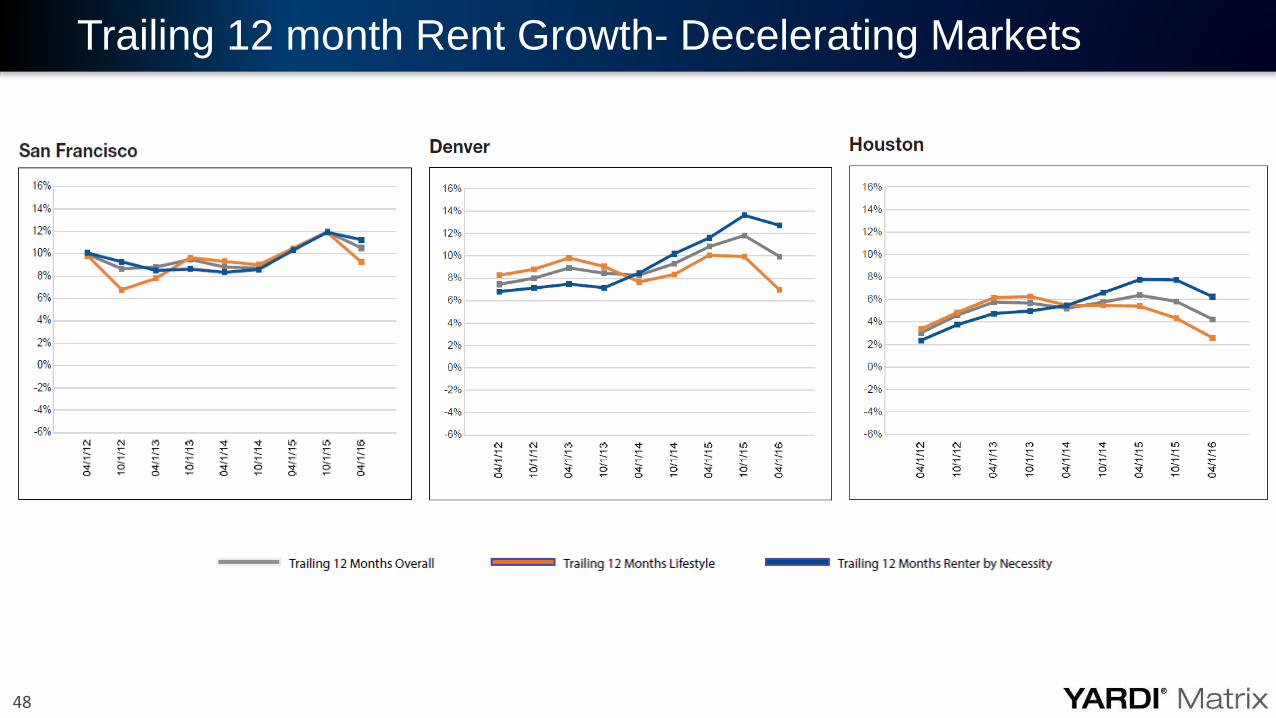

Trailing 12 month Rent Growth- Decelerating Markets

49

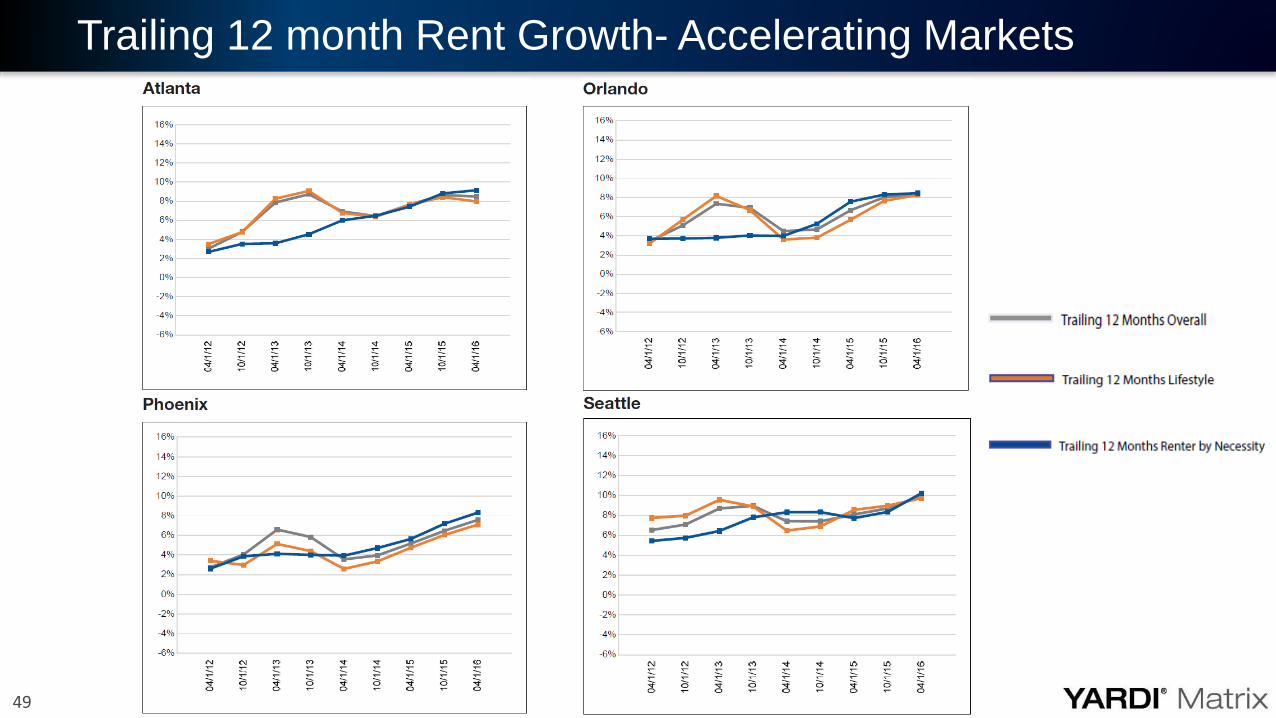

Trailing 12 month Rent Growth- Accelerating Markets

50

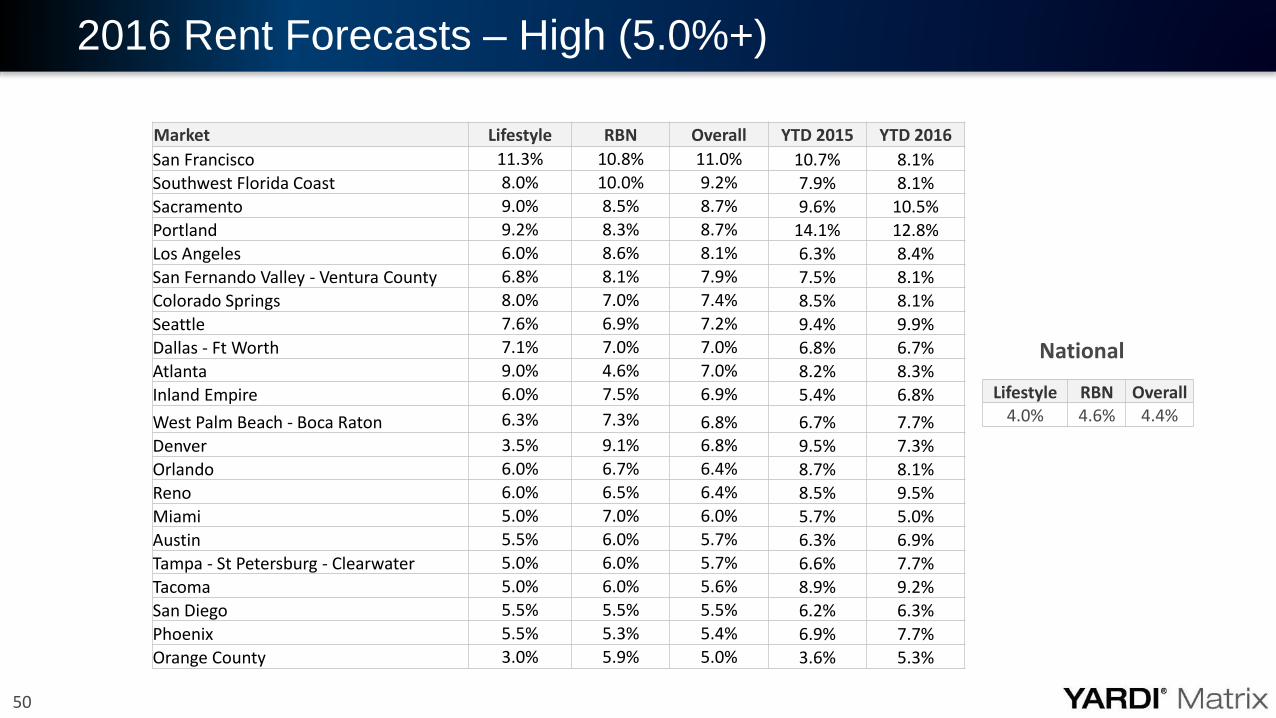

2016 Rent Forecasts – High (5.0%+)

Market Lifestyle RBN Overall YTD 2015 YTD 2016

San Francisco 11.3% 10.8% 11.0% 10.7% 8.1%

Southwest Florida Coast 8.0% 10.0% 9.2% 7.9% 8.1%

Sacramento 9.0% 8.5% 8.7% 9.6% 10.5%

Portland 9.2% 8.3% 8.7% 14.1% 12.8%

Los Angeles 6.0% 8.6% 8.1% 6.3% 8.4%

San Fernando Valley - Ventura County 6.8% 8.1% 7.9% 7.5% 8.1%

Colorado Springs 8.0% 7.0% 7.4% 8.5% 8.1%

Seattle 7.6% 6.9% 7.2% 9.4% 9.9%

Dallas - Ft Worth 7.1% 7.0% 7.0% 6.8% 6.7%

Atlanta 9.0% 4.6% 7.0% 8.2% 8.3%

Inland Empire 6.0% 7.5% 6.9% 5.4% 6.8%

West Palm Beach - Boca Raton 6.3% 7.3% 6.8% 6.7% 7.7%

Denver 3.5% 9.1% 6.8% 9.5% 7.3%

Orlando 6.0% 6.7% 6.4% 8.7% 8.1%

Reno 6.0% 6.5% 6.4% 8.5% 9.5%

Miami 5.0% 7.0% 6.0% 5.7% 5.0%

Austin 5.5% 6.0% 5.7% 6.3% 6.9%

Tampa - St Petersburg - Clearwater 5.0% 6.0% 5.7% 6.6% 7.7%

Tacoma 5.0% 6.0% 5.6% 8.9% 9.2%

San Diego 5.5% 5.5% 5.5% 6.2% 6.3%

Phoenix 5.5% 5.3% 5.4% 6.9% 7.7%

Orange County 3.0% 5.9% 5.0% 3.6% 5.3%

National

Lifestyle RBN Overall4.0% 4.6% 4.4%

51

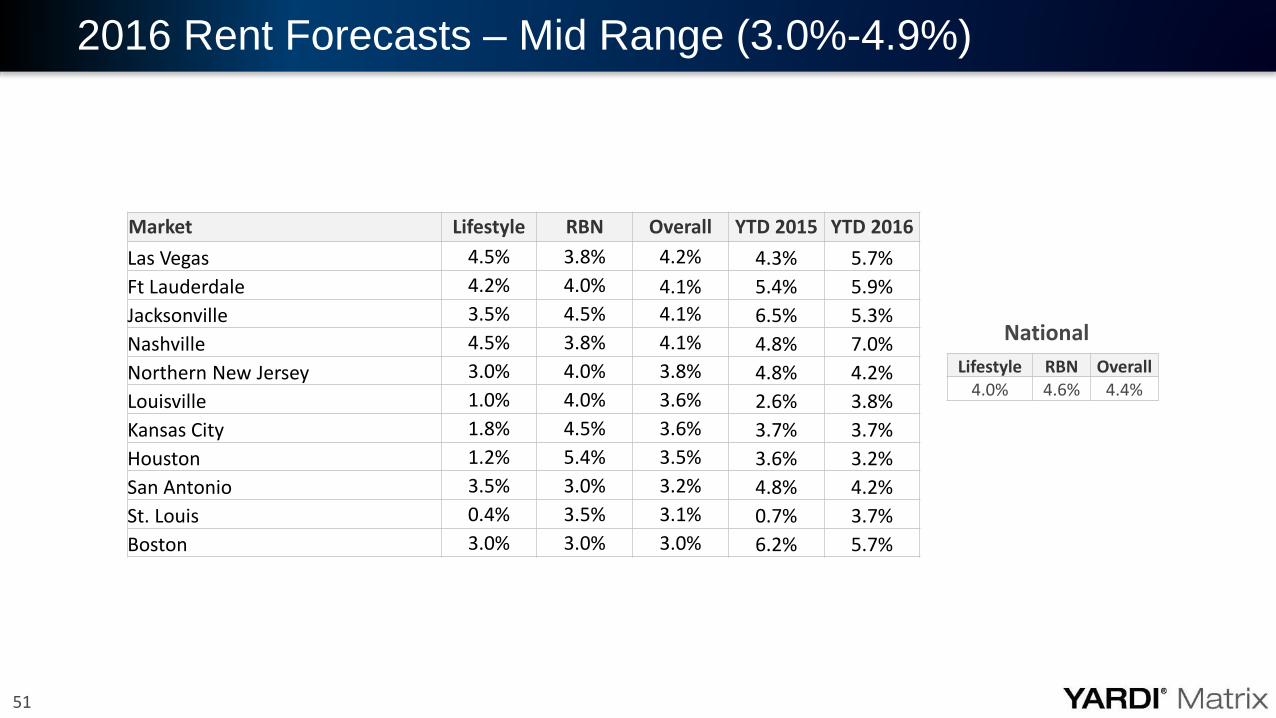

2016 Rent Forecasts – Mid Range (3.0%-4.9%)

Market Lifestyle RBN Overall YTD 2015 YTD 2016

Las Vegas 4.5% 3.8% 4.2% 4.3% 5.7%

Ft Lauderdale 4.2% 4.0% 4.1% 5.4% 5.9%

Jacksonville 3.5% 4.5% 4.1% 6.5% 5.3%

Nashville 4.5% 3.8% 4.1% 4.8% 7.0%

Northern New Jersey 3.0% 4.0% 3.8% 4.8% 4.2%

Louisville 1.0% 4.0% 3.6% 2.6% 3.8%

Kansas City 1.8% 4.5% 3.6% 3.7% 3.7%

Houston 1.2% 5.4% 3.5% 3.6% 3.2%

San Antonio 3.5% 3.0% 3.2% 4.8% 4.2%

St. Louis 0.4% 3.5% 3.1% 0.7% 3.7%

Boston 3.0% 3.0% 3.0% 6.2% 5.7%

National

Lifestyle RBN Overall4.0% 4.6% 4.4%

52

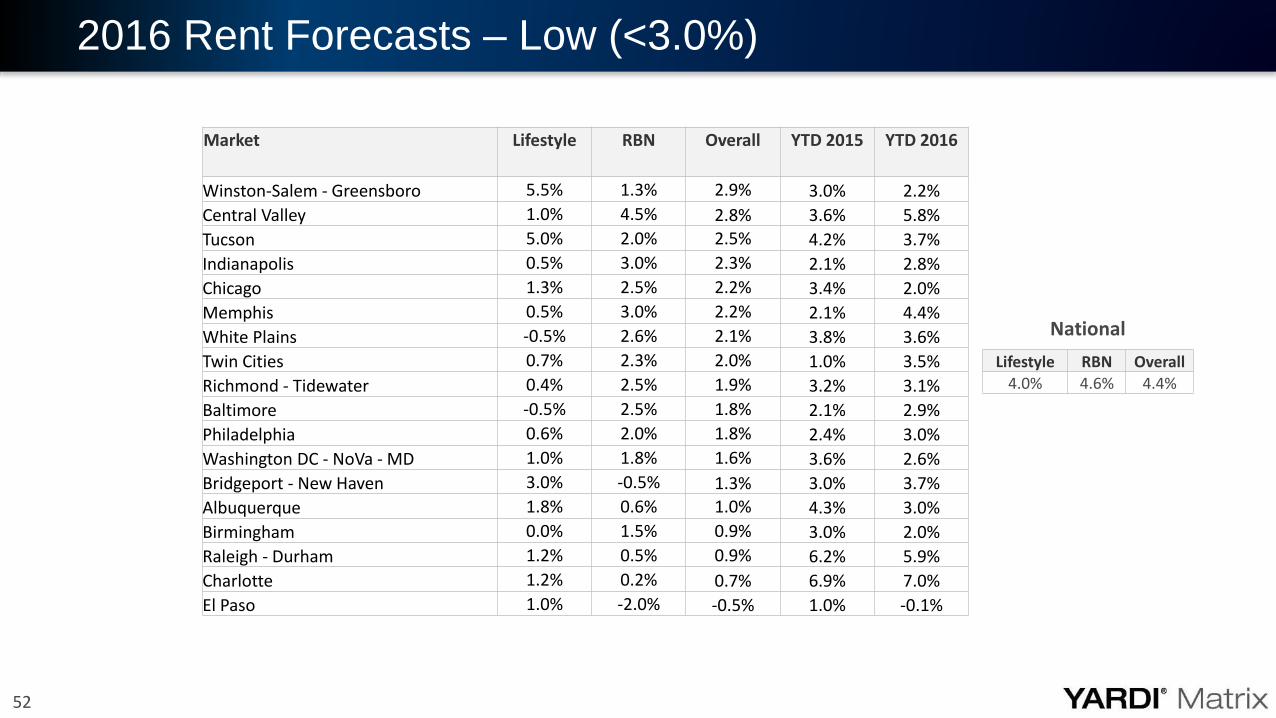

2016 Rent Forecasts – Low (<3.0%)

Market Lifestyle RBN Overall YTD 2015 YTD 2016

Winston-Salem - Greensboro 5.5% 1.3% 2.9% 3.0% 2.2%

Central Valley 1.0% 4.5% 2.8% 3.6% 5.8%

Tucson 5.0% 2.0% 2.5% 4.2% 3.7%

Indianapolis 0.5% 3.0% 2.3% 2.1% 2.8%

Chicago 1.3% 2.5% 2.2% 3.4% 2.0%

Memphis 0.5% 3.0% 2.2% 2.1% 4.4%

White Plains -0.5% 2.6% 2.1% 3.8% 3.6%

Twin Cities 0.7% 2.3% 2.0% 1.0% 3.5%

Richmond - Tidewater 0.4% 2.5% 1.9% 3.2% 3.1%

Baltimore -0.5% 2.5% 1.8% 2.1% 2.9%

Philadelphia 0.6% 2.0% 1.8% 2.4% 3.0%

Washington DC - NoVa - MD 1.0% 1.8% 1.6% 3.6% 2.6%

Bridgeport - New Haven 3.0% -0.5% 1.3% 3.0% 3.7%

Albuquerque 1.8% 0.6% 1.0% 4.3% 3.0%

Birmingham 0.0% 1.5% 0.9% 3.0% 2.0%

Raleigh - Durham 1.2% 0.5% 0.9% 6.2% 5.9%

Charlotte 1.2% 0.2% 0.7% 6.9% 7.0%

El Paso 1.0% -2.0% -0.5% 1.0% -0.1%

National

Lifestyle RBN Overall

4.0% 4.6% 4.4%

Submarket Selection

Jeff AdlerVice President, Matrix

54

Determining Intellectual Nodes

Evidence of

knowledge-based job

& business

formation/expansion

Public/Private

partnerships for

education and

healthcare

initiatives

Examples of

multifamily &

commercial development

55

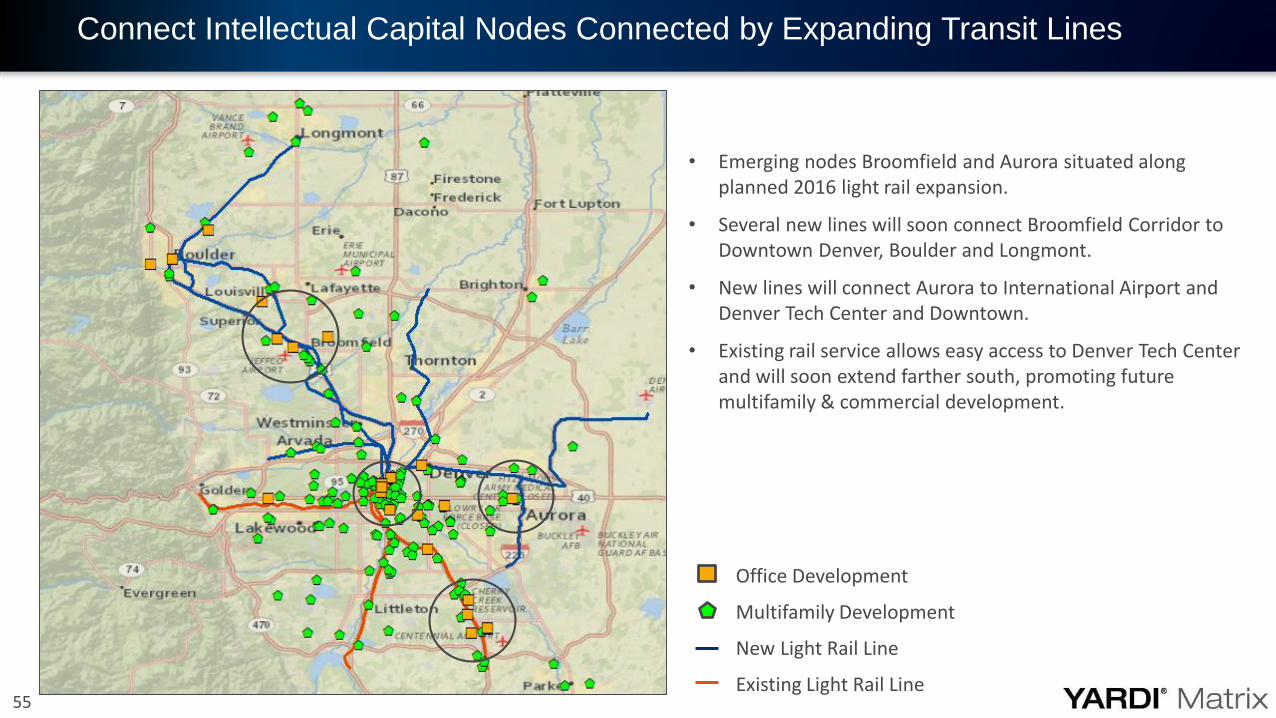

Connect Intellectual Capital Nodes Connected by Expanding Transit Lines

• Emerging nodes Broomfield and Aurora situated along planned 2016 light rail expansion.

• Several new lines will soon connect Broomfield Corridor to Downtown Denver, Boulder and Longmont.

• New lines will connect Aurora to International Airport and Denver Tech Center and Downtown.

• Existing rail service allows easy access to Denver Tech Center and will soon extend farther south, promoting future multifamily & commercial development.

Office Development

Multifamily Development

New Light Rail Line

Existing Light Rail Line

56

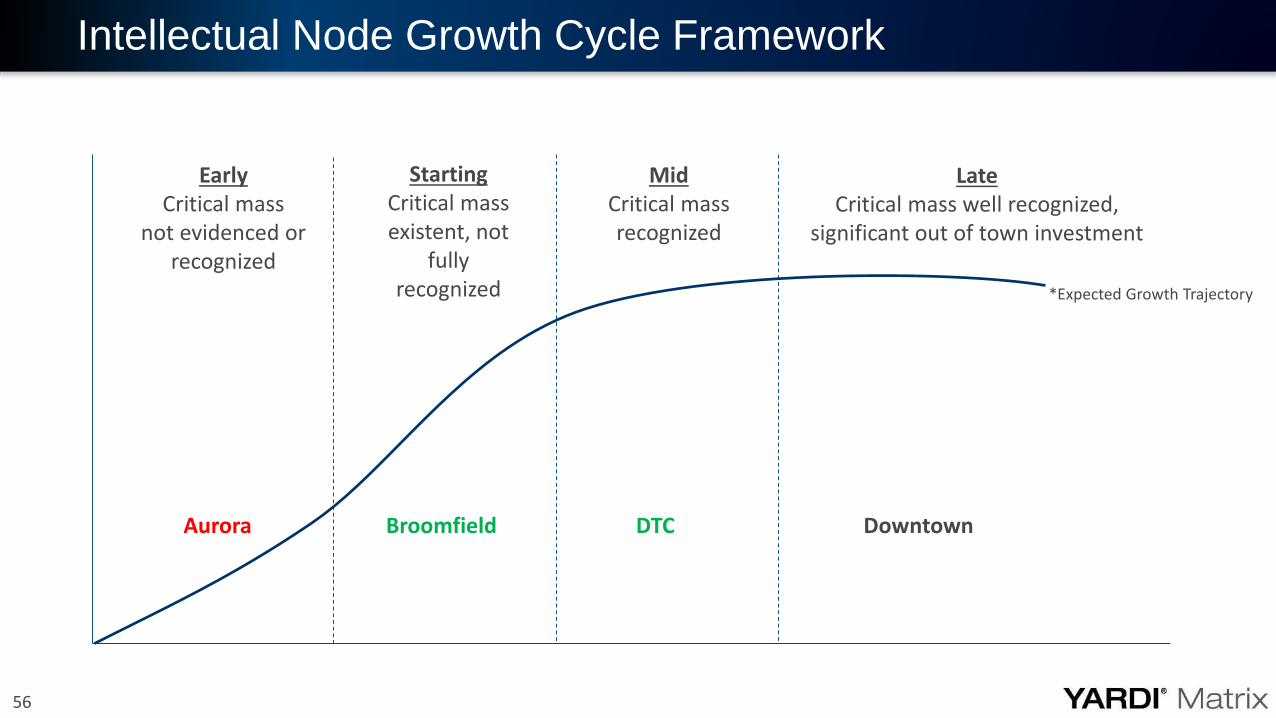

Intellectual Node Growth Cycle Framework

EarlyCritical mass

not evidenced or recognized

StartingCritical mass existent, not

fully recognized

MidCritical mass recognized

LateCritical mass well recognized,

significant out of town investment

Aurora Broomfield DTC Downtown

*Expected Growth Trajectory

57

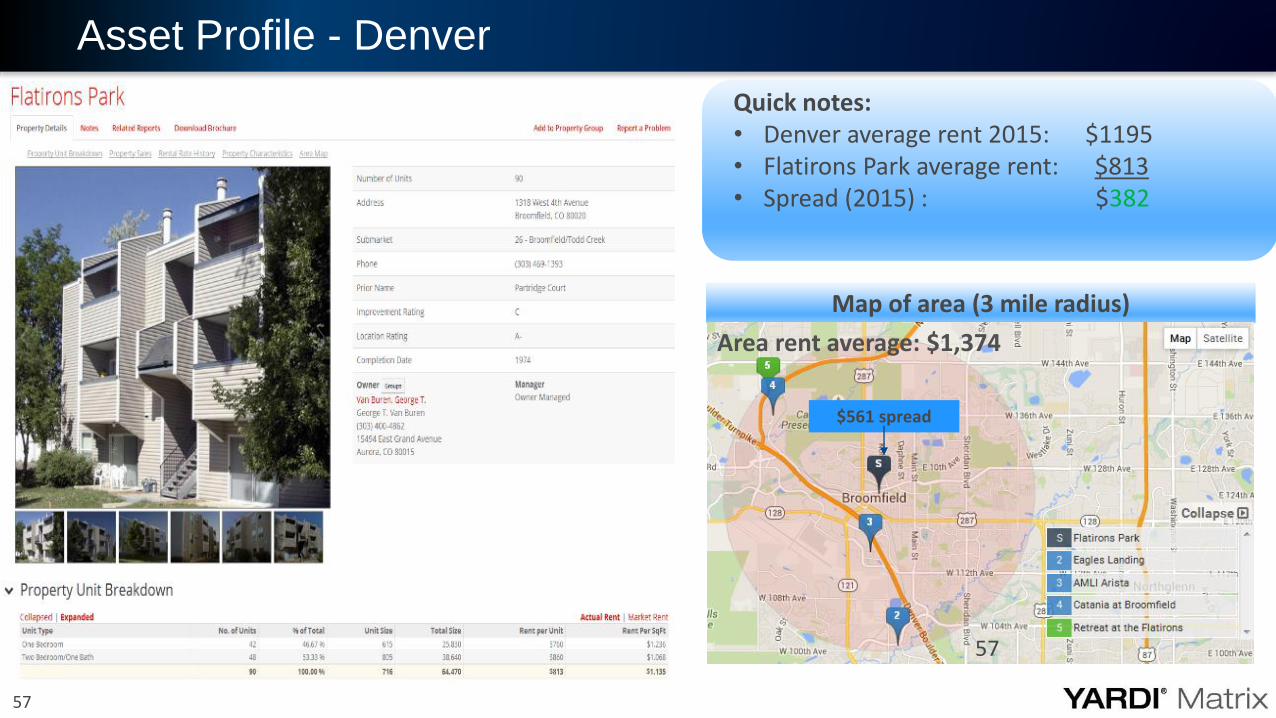

Asset Profile - Denver

Quick notes:• Denver average rent 2015: $1195• Flatirons Park average rent: $813• Spread (2015) : $382

Map of area (3 mile radius)

Area rent average: $1,345

$403 spread$561 spread

Area rent average: $1,374

57

58

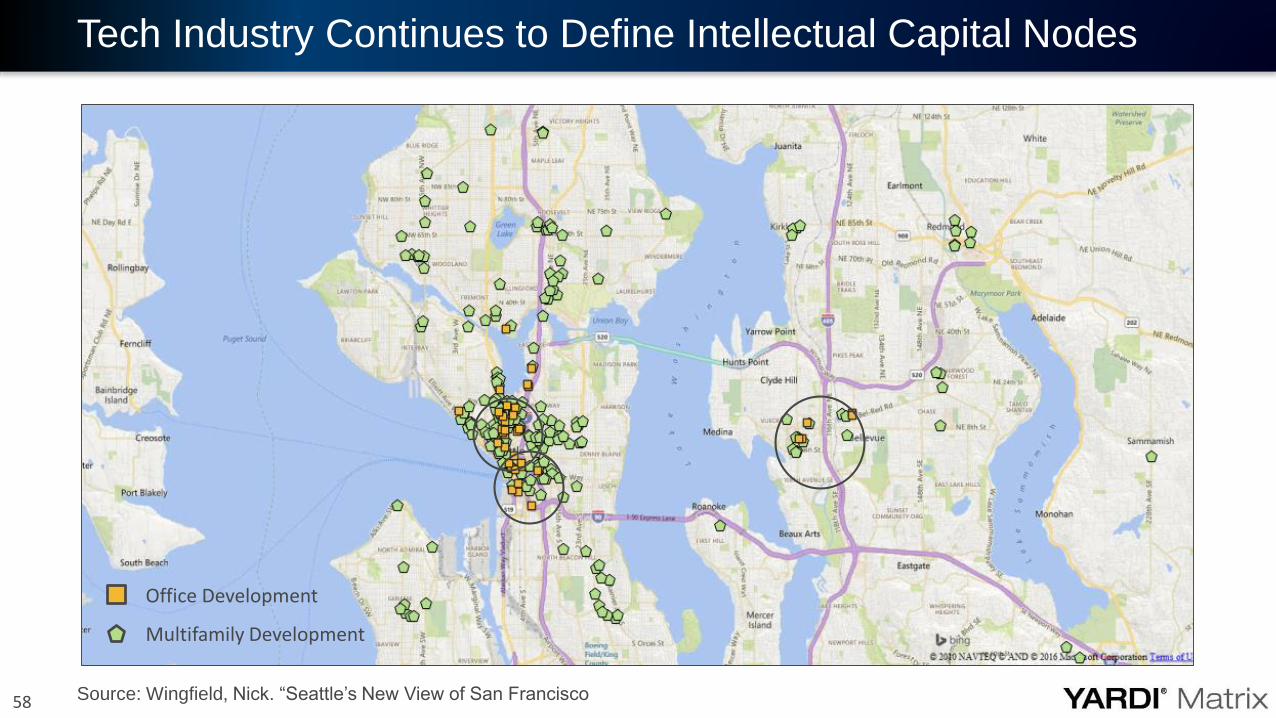

Tech Industry Continues to Define Intellectual Capital Nodes

Office Development

Multifamily Development

Source: Wingfield, Nick. “Seattle’s New View of San Francisco

59

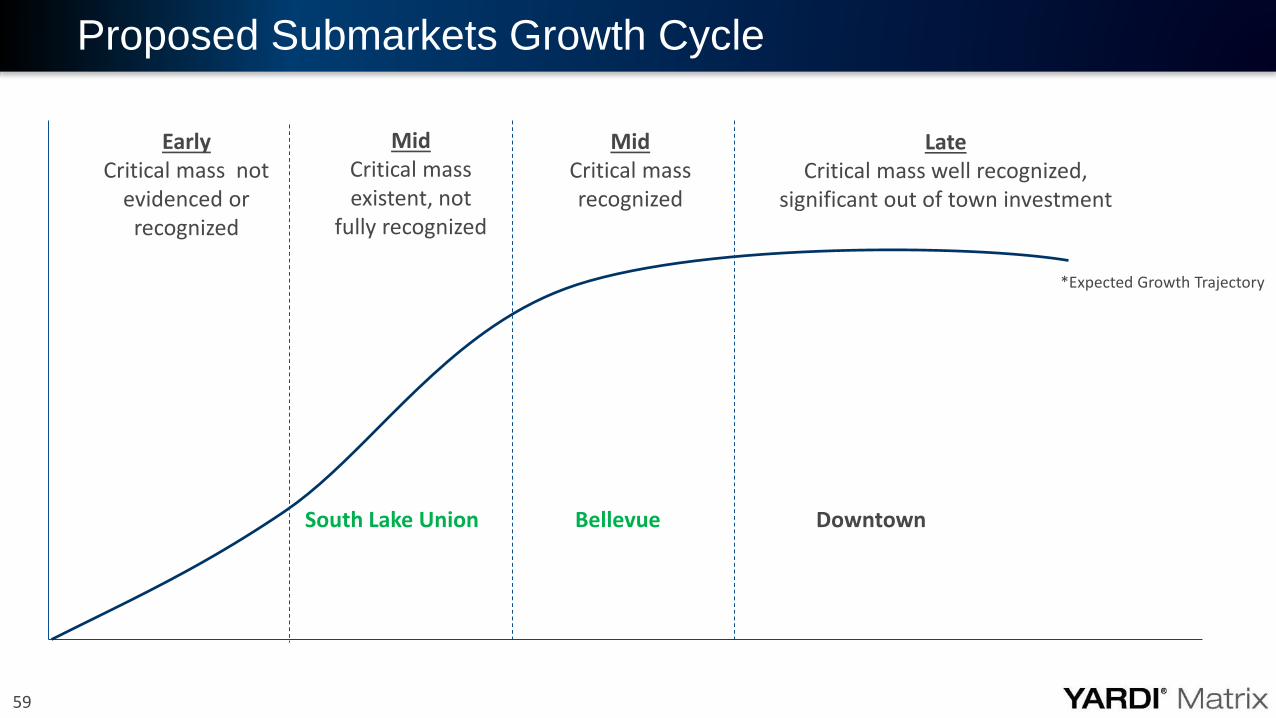

Proposed Submarkets Growth Cycle

EarlyCritical mass not

evidenced or recognized

Mid Critical mass existent, not

fully recognized

MidCritical mass recognized

LateCritical mass well recognized,

significant out of town investment

South Lake Union Bellevue Downtown

*Expected Growth Trajectory

60

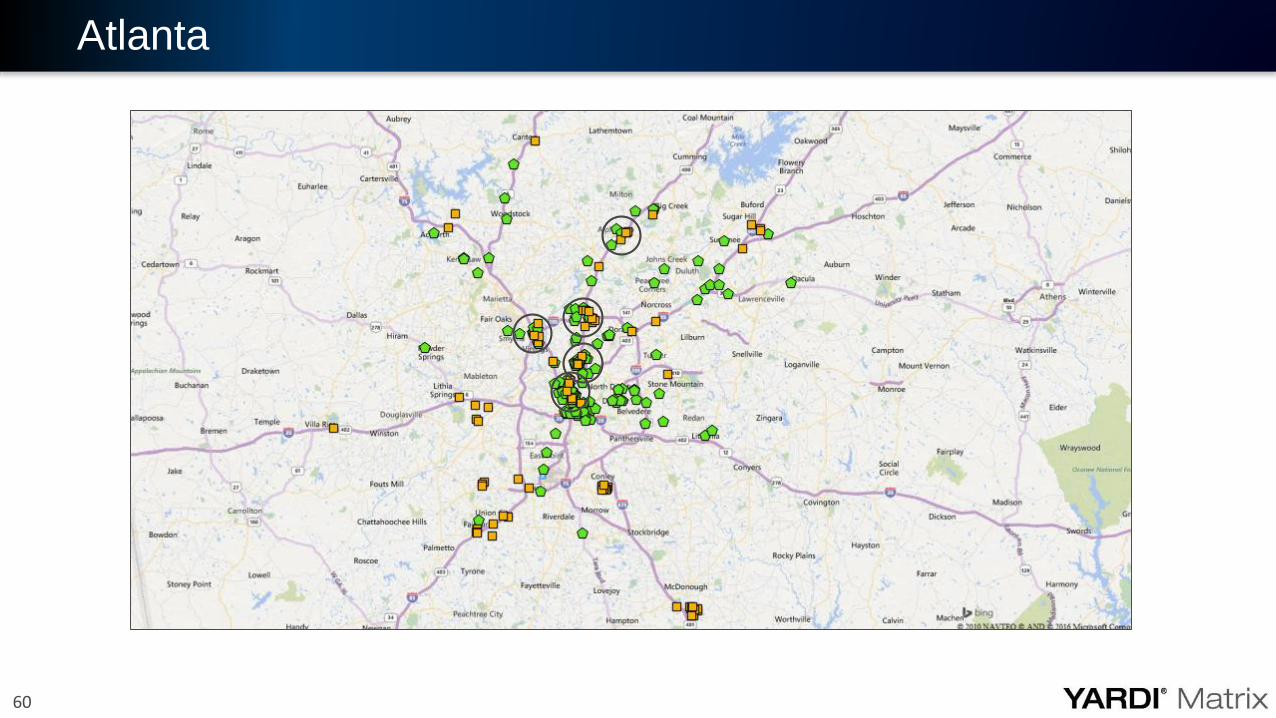

Atlanta

61

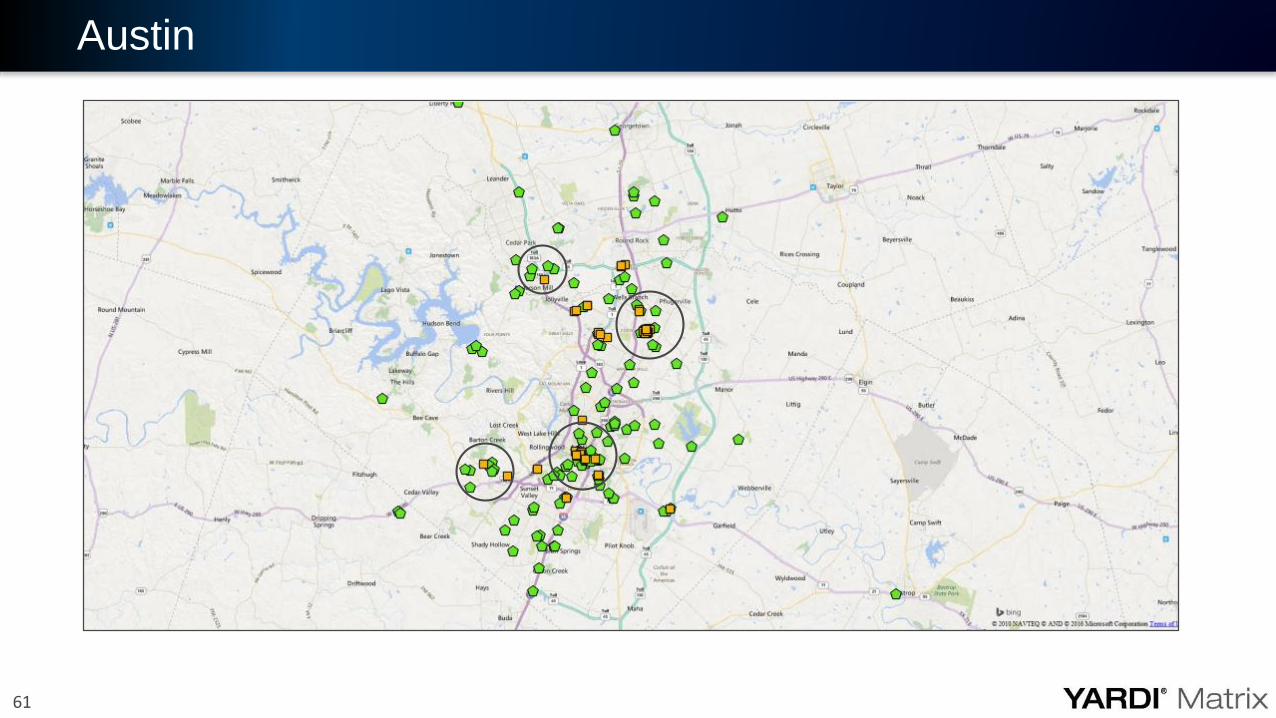

Austin

62

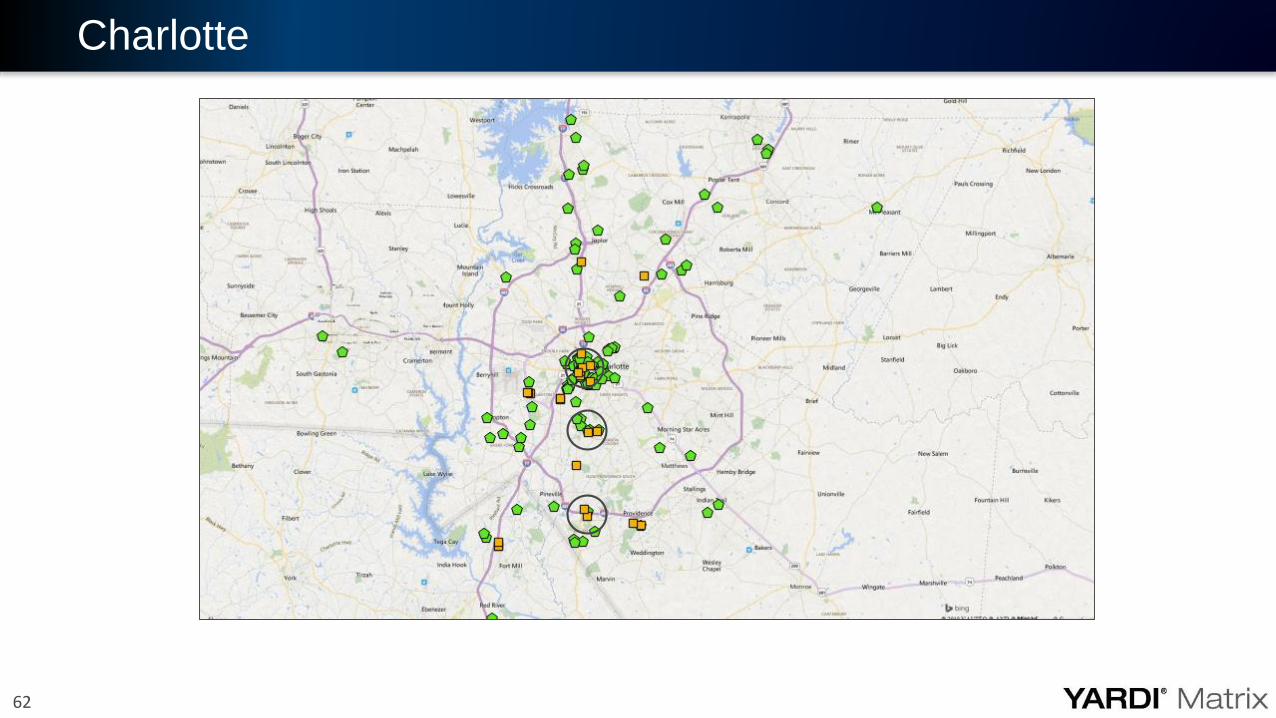

Charlotte

63

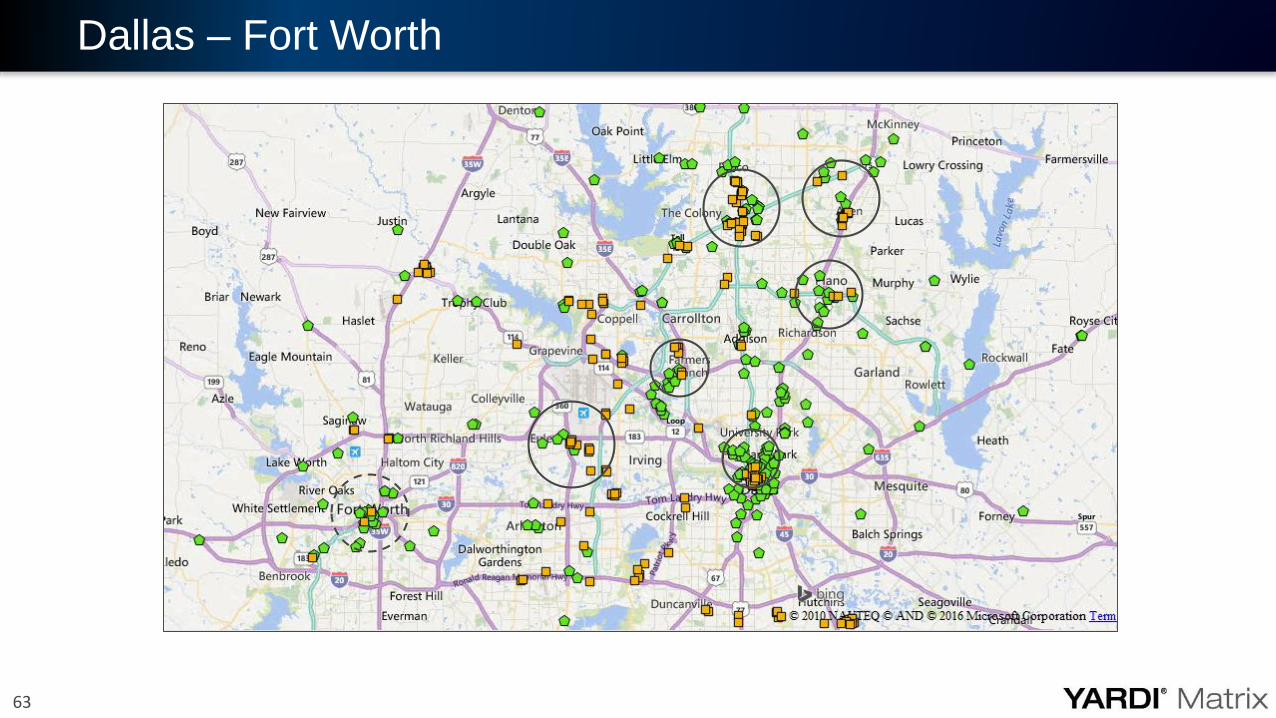

Dallas – Fort Worth

64

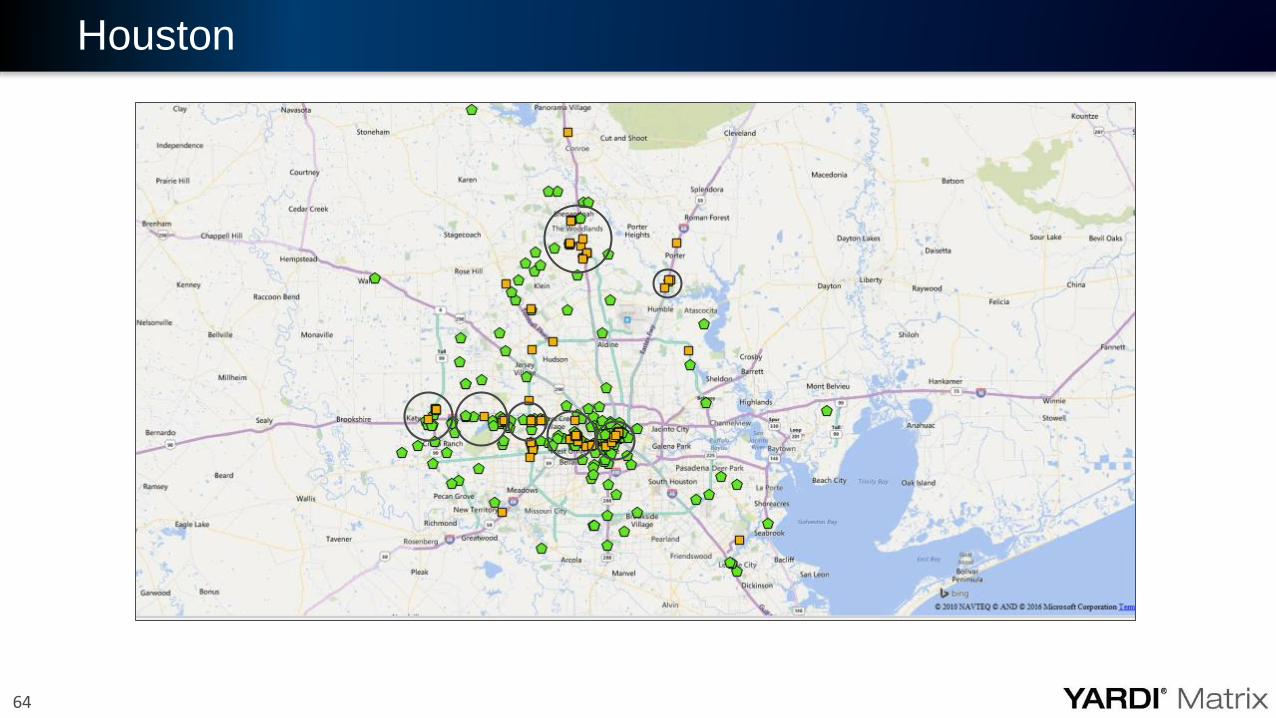

Houston

65

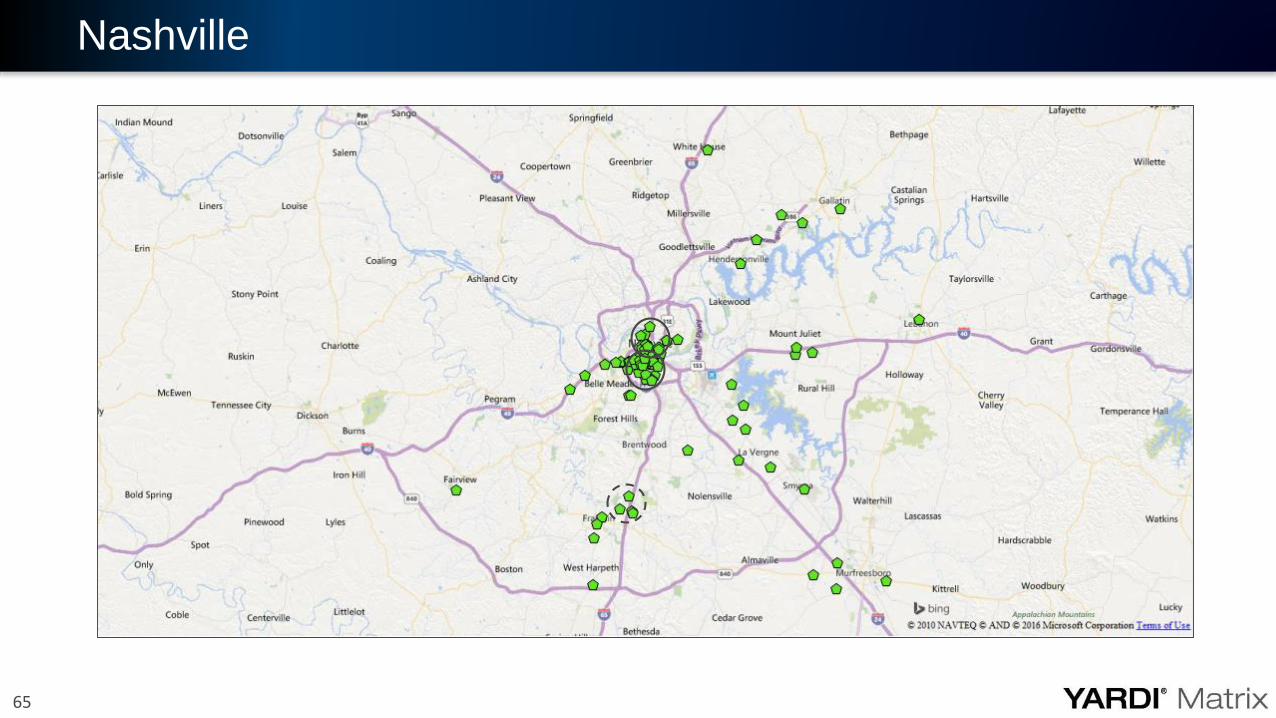

Nashville

66

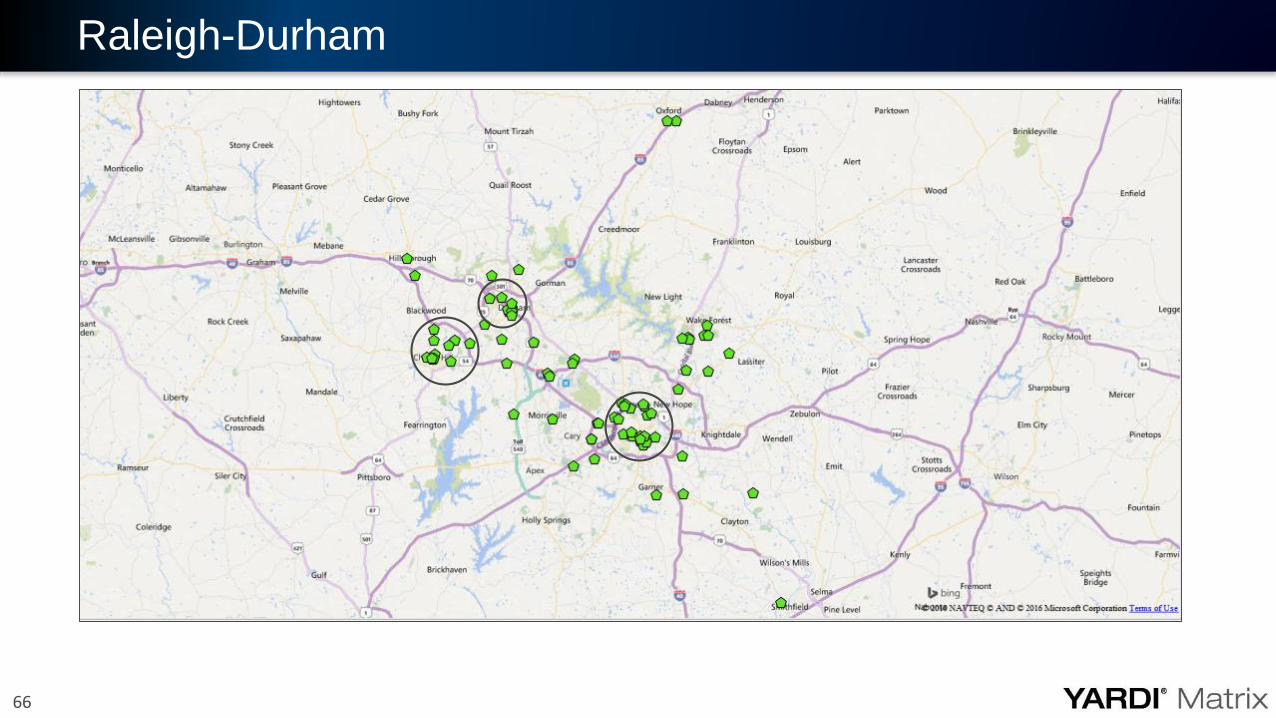

Raleigh-Durham

67

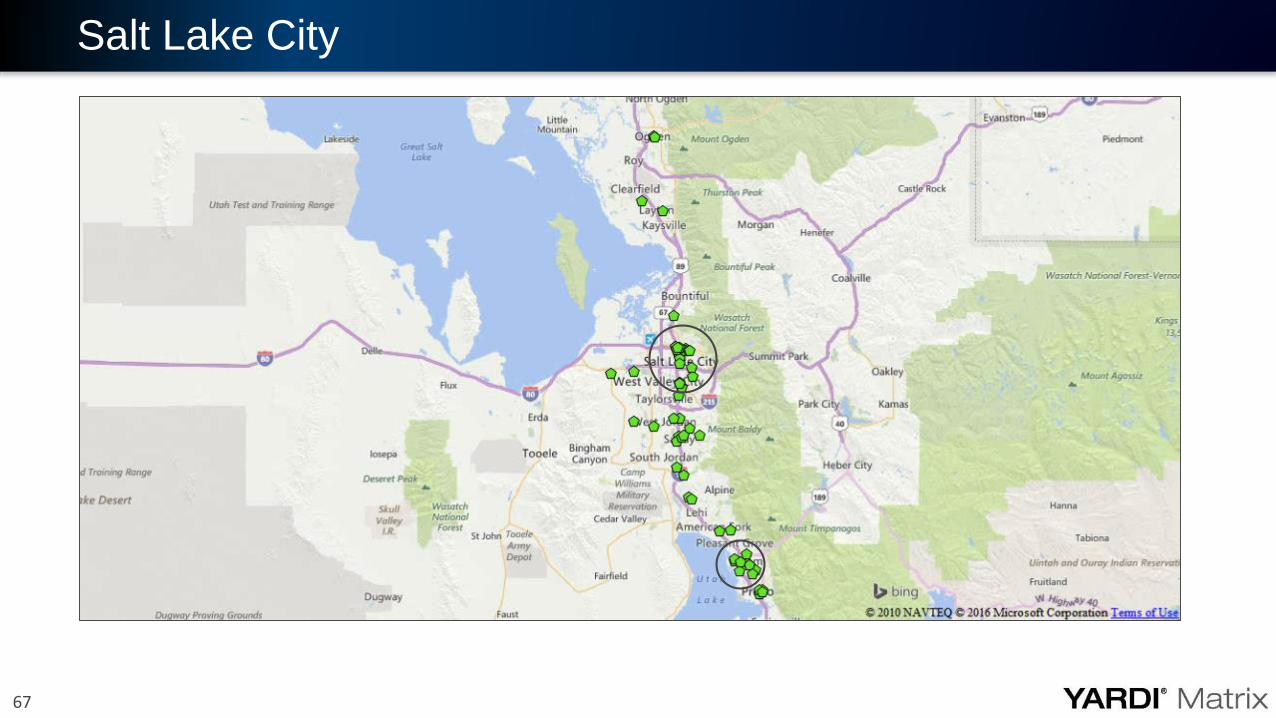

Salt Lake City

68

Appendix

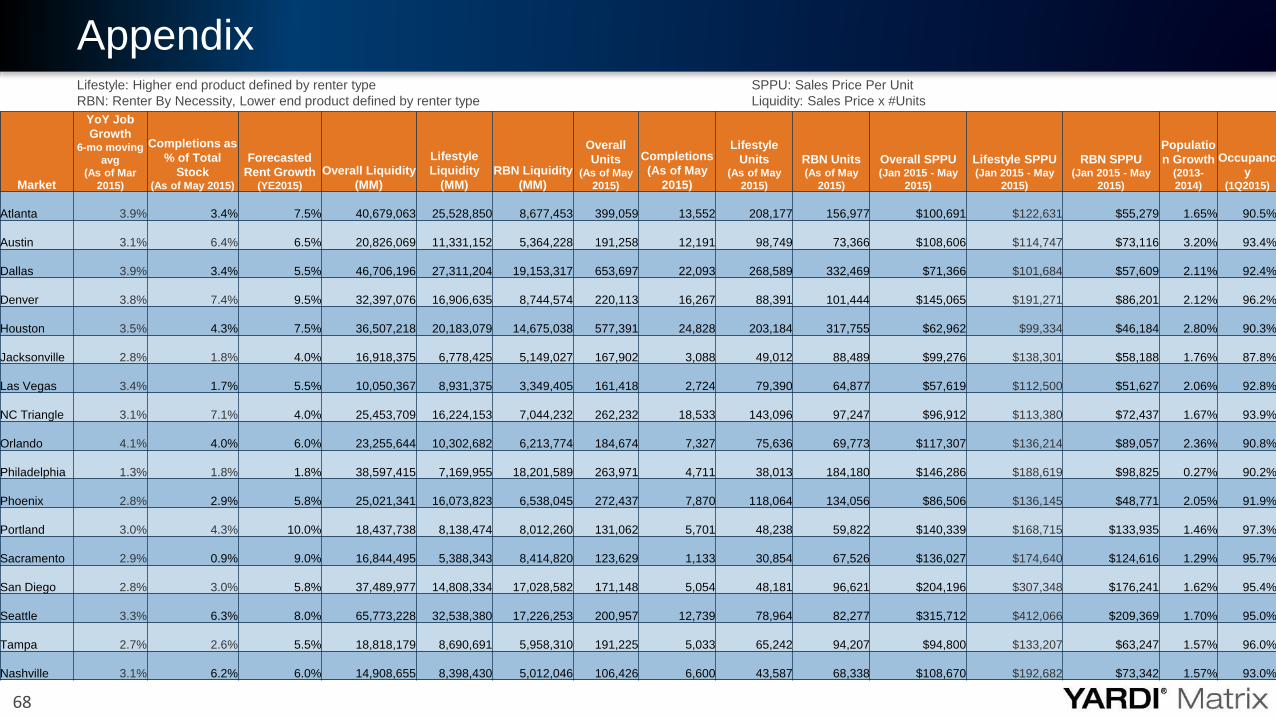

Appendix

Market

YoY Job

Growth6-mo moving

avg

(As of Mar

2015)

Completions as

% of Total

Stock (As of May 2015)

Forecasted

Rent Growth (YE2015)

Overall Liquidity

(MM)

Lifestyle

Liquidity

(MM)

RBN Liquidity

(MM)

Overall

Units(As of May

2015)

Completions

(As of May

2015)

Lifestyle

Units(As of May

2015)

RBN Units(As of May

2015)

Overall SPPU(Jan 2015 - May

2015)

Lifestyle SPPU(Jan 2015 - May

2015)

RBN SPPU(Jan 2015 - May

2015)

Populatio

n Growth(2013-

2014)

Occupanc

y(1Q2015)

Atlanta 3.9% 3.4% 7.5% 40,679,063 25,528,850 8,677,453 399,059 13,552 208,177 156,977 $100,691 $122,631 $55,279 1.65% 90.5%

Austin 3.1% 6.4% 6.5% 20,826,069 11,331,152 5,364,228 191,258 12,191 98,749 73,366 $108,606 $114,747 $73,116 3.20% 93.4%

Dallas 3.9% 3.4% 5.5% 46,706,196 27,311,204 19,153,317 653,697 22,093 268,589 332,469 $71,366 $101,684 $57,609 2.11% 92.4%

Denver 3.8% 7.4% 9.5% 32,397,076 16,906,635 8,744,574 220,113 16,267 88,391 101,444 $145,065 $191,271 $86,201 2.12% 96.2%

Houston 3.5% 4.3% 7.5% 36,507,218 20,183,079 14,675,038 577,391 24,828 203,184 317,755 $62,962 $99,334 $46,184 2.80% 90.3%

Jacksonville 2.8% 1.8% 4.0% 16,918,375 6,778,425 5,149,027 167,902 3,088 49,012 88,489 $99,276 $138,301 $58,188 1.76% 87.8%

Las Vegas 3.4% 1.7% 5.5% 10,050,367 8,931,375 3,349,405 161,418 2,724 79,390 64,877 $57,619 $112,500 $51,627 2.06% 92.8%

NC Triangle 3.1% 7.1% 4.0% 25,453,709 16,224,153 7,044,232 262,232 18,533 143,096 97,247 $96,912 $113,380 $72,437 1.67% 93.9%

Orlando 4.1% 4.0% 6.0% 23,255,644 10,302,682 6,213,774 184,674 7,327 75,636 69,773 $117,307 $136,214 $89,057 2.36% 90.8%

Philadelphia 1.3% 1.8% 1.8% 38,597,415 7,169,955 18,201,589 263,971 4,711 38,013 184,180 $146,286 $188,619 $98,825 0.27% 90.2%

Phoenix 2.8% 2.9% 5.8% 25,021,341 16,073,823 6,538,045 272,437 7,870 118,064 134,056 $86,506 $136,145 $48,771 2.05% 91.9%

Portland 3.0% 4.3% 10.0% 18,437,738 8,138,474 8,012,260 131,062 5,701 48,238 59,822 $140,339 $168,715 $133,935 1.46% 97.3%

Sacramento 2.9% 0.9% 9.0% 16,844,495 5,388,343 8,414,820 123,629 1,133 30,854 67,526 $136,027 $174,640 $124,616 1.29% 95.7%

San Diego 2.8% 3.0% 5.8% 37,489,977 14,808,334 17,028,582 171,148 5,054 48,181 96,621 $204,196 $307,348 $176,241 1.62% 95.4%

Seattle 3.3% 6.3% 8.0% 65,773,228 32,538,380 17,226,253 200,957 12,739 78,964 82,277 $315,712 $412,066 $209,369 1.70% 95.0%

Tampa 2.7% 2.6% 5.5% 18,818,179 8,690,691 5,958,310 191,225 5,033 65,242 94,207 $94,800 $133,207 $63,247 1.57% 96.0%

Nashville 3.1% 6.2% 6.0% 14,908,655 8,398,430 5,012,046 106,426 6,600 43,587 68,338 $108,670 $192,682 $73,342 1.57% 93.0%

Lifestyle: Higher end product defined by renter type

RBN: Renter By Necessity, Lower end product defined by renter type

SPPU: Sales Price Per Unit

Liquidity: Sales Price x #Units

69

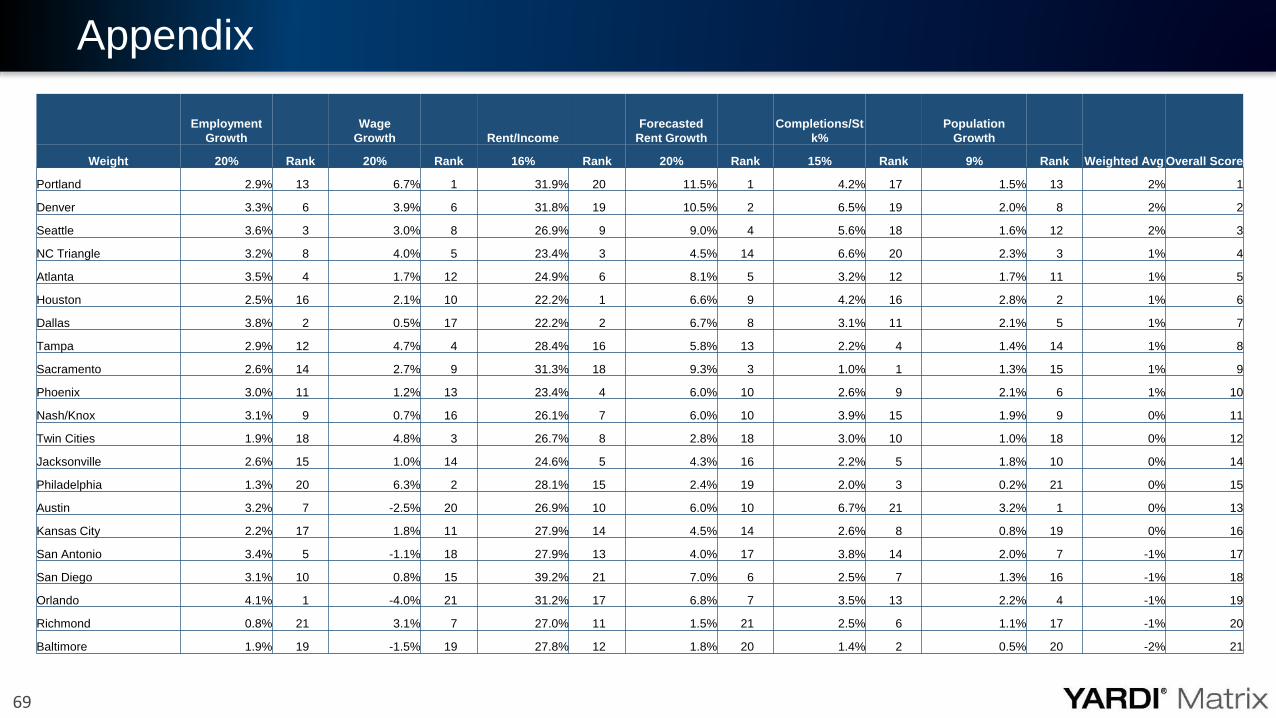

Appendix

Employment

Growth

Wage

Growth Rent/Income

Forecasted

Rent Growth

Completions/St

k%

Population

Growth

Weighted Avg Overall ScoreWeight 20% Rank 20% Rank 16% Rank 20% Rank 15% Rank 9% Rank

Portland 2.9% 13 6.7% 1 31.9% 20 11.5% 1 4.2% 17 1.5% 13 2% 1

Denver 3.3% 6 3.9% 6 31.8% 19 10.5% 2 6.5% 19 2.0% 8 2% 2

Seattle 3.6% 3 3.0% 8 26.9% 9 9.0% 4 5.6% 18 1.6% 12 2% 3

NC Triangle 3.2% 8 4.0% 5 23.4% 3 4.5% 14 6.6% 20 2.3% 3 1% 4

Atlanta 3.5% 4 1.7% 12 24.9% 6 8.1% 5 3.2% 12 1.7% 11 1% 5

Houston 2.5% 16 2.1% 10 22.2% 1 6.6% 9 4.2% 16 2.8% 2 1% 6

Dallas 3.8% 2 0.5% 17 22.2% 2 6.7% 8 3.1% 11 2.1% 5 1% 7

Tampa 2.9% 12 4.7% 4 28.4% 16 5.8% 13 2.2% 4 1.4% 14 1% 8

Sacramento 2.6% 14 2.7% 9 31.3% 18 9.3% 3 1.0% 1 1.3% 15 1% 9

Phoenix 3.0% 11 1.2% 13 23.4% 4 6.0% 10 2.6% 9 2.1% 6 1% 10

Nash/Knox 3.1% 9 0.7% 16 26.1% 7 6.0% 10 3.9% 15 1.9% 9 0% 11

Twin Cities 1.9% 18 4.8% 3 26.7% 8 2.8% 18 3.0% 10 1.0% 18 0% 12

Jacksonville 2.6% 15 1.0% 14 24.6% 5 4.3% 16 2.2% 5 1.8% 10 0% 14

Philadelphia 1.3% 20 6.3% 2 28.1% 15 2.4% 19 2.0% 3 0.2% 21 0% 15

Austin 3.2% 7 -2.5% 20 26.9% 10 6.0% 10 6.7% 21 3.2% 1 0% 13

Kansas City 2.2% 17 1.8% 11 27.9% 14 4.5% 14 2.6% 8 0.8% 19 0% 16

San Antonio 3.4% 5 -1.1% 18 27.9% 13 4.0% 17 3.8% 14 2.0% 7 -1% 17

San Diego 3.1% 10 0.8% 15 39.2% 21 7.0% 6 2.5% 7 1.3% 16 -1% 18

Orlando 4.1% 1 -4.0% 21 31.2% 17 6.8% 7 3.5% 13 2.2% 4 -1% 19

Richmond 0.8% 21 3.1% 7 27.0% 11 1.5% 21 2.5% 6 1.1% 17 -1% 20

Baltimore 1.9% 19 -1.5% 19 27.8% 12 1.8% 20 1.4% 2 0.5% 20 -2% 21

70

»Jeff Adler, Vice President & General Manager of Yardi Matrix

[email protected], 1-800-866-1124 x2403

»Jack Kern, Director of Research and Publications

[email protected], 1-800-866-1124 x2444

Contact Information

Source: GDP from BEA April 28th, 2016; BLS Employment Situation Reports; Moody’s Analytics; FTSE Nareit U.S. Real Estate Index GDP Definition: the value of goods and services produced by the nation’s economy less the value of the goods and services used in production, adjusted for price changes