Embed Size (px)

Citation preview

SPECIAL ISSUE

Ten Years After the Asian Currency Crisis— Lessons Learned for Further Development in Asia, Including Japan —

Participants:

Mr. Akira Ariyoshi

Prof. Takatoshi Ito

Mr. Masahiro Kawai

Mr. Rintaro Tamaki

Mr. Fumio Hoshi

Director, IMF Regional Office for Asia and the PacificGraduate School of Economics, and Graduate School of Public PolicyDean, Asian Development Bank InstituteDirector-General, International Bureau, Ministry of Finance, JapanSenior Executive Director, Japan Bank for International Cooperation (JBIC)

JBIC TODAY Round-Table Discussion

— Lessons Learned for Further Development in Asia, Including Japan —

Participants:Mr. Akira Ariyoshi Prof. Takatoshi Ito Mr. Masahiro KawaiMr. Rintaro Tamaki Mr. Fumio Hoshi

Moderator:Mr. Masaaki Amma

Director, IMF Regional Office for Asia and the PacificGraduate School of Economics, and Graduate School of Public PolicyDean, Asian Development Bank InstituteDirector-General, International Bureau, Ministry of Finance, JapanSenior Executive Director, Japan Bank for International Cooperation (JBIC)

Director General, JBIC Institute

One decade has passed since the Asian currency crisis hit in 1997. The crisis was triggered in Thailand then spread to Indonesia, Malaysia, the Republic of Korea and other countries. Japanese companies were also seriously impacted. The main reason for the crisis was that Asian countries tried to meet their need for long-term funds for capital investments in local currencies through short-term, foreign currency loans from other countries. This created a double mismatch (a combination of a currency mismatch and a maturity mismatch) that could not be supported by existing financial or monetary systems.

Taking lessons from this bitter experience, during the 10 years that followed financial and capital markets in Asian countries were strengthened, and proactive measures were taken within the framework of ASEAN+3 (ASEAN plus Japan, China and Korea). These measures included regional financial cooperation and the Asian Bond Markets Initiative (ABMI) proposed by the Japanese government. Japan Bank for International Cooperation (JBIC) also began offering a range of support measures to Asian countries outside Japan, and supporting Japanese corporations active in those countries.

Although Asian economies are growing steadily today, challenges still remain — for example, capital inflows are increasing as they were 10 years ago, there is a global current account imbalance, and oil money is creating excess liquidity. There is no reason to expect another currency crisis in the immediate future, but appropriate, timely mechanisms are needed to respond to any crisis situation appearing on the horizon.

We asked experts with extensive knowledge of these issues to offer their views, and to give us insight into how the international financial order should be maintained.

(This article is an abridged English translation of the transcript of the round-table discussion held in the Japanese language)

Ten Years After the Asian Currency Crisis

JBIC TODAY Round-Table Discussion

2 JBIC TODAY SPECIAL ISSUE 2007

double mismatch, with short-term, foreign currency funds

being used for long-term domestic investments in local cur-

rencies. It was against this backdrop that local currencies

depreciated, creating obvious balance sheet problems on

the part of banks and corporations that borrowed heavily

from abroad.

Thailand, the trigger country of the Asian currency crisis,

suffered a failure in its domestic financial system because of

mounting non-performing loans. The currency crisis

occurred against this backdrop. The double mismatch also

affected the Indonesian and Thai corporate sectors, forcing

them to curtail their business activities, which further

reduced the value of their currencies. The solvency of some

companies was questioned, creating concerns that they

would not be able to pay back their loans. By 1998, economic

activity, especially investment, had shrunk dramatically. In

Indonesia, distrust towards the Suharto regime exacerbated

financial instability.

In early 1997 several corporate groups (chaebols) that

had over-invested in Korea had begun falling into bankrupt-

cy. In addition, major commercial banks that had borrowed

from abroad began to find it difficult to repay due to won

depreciation in late 1997. Unsuccessful Korean investments

in Russia and Indonesia also added to the problem.

Amma: What countermeasures were taken to eradicate

the crisis?

Kawai: Asian economies recovered quickly, and econom-

ic growth, which was highly and alarmingly negative in

1998, returned to positive figures in 1999. Growth has con-

tinued since 2000. Three major factors account for the

recovery:

1.The crisis-affected countries went through diffi-

cult financial and corporate restructuring with

help from IMF and World Bank programs, which

helped them rebound from severe economic con-

traction. Enhancements in the legal framework,

especially bankruptcy laws, promoted a healthy

weeding out and restructuring of corporate debt

and successful reconstruction of the banking and

corporate sectors.

2.There was a significant improvement in external

financial conditions. National governments kept their

spending to a minimum, and fiscal restraints kept a

The Asian Currency Crisis in PerspectiveAmma: During this round-table discussion we will examine

how the real economies and financial sectors changed in

affected countries as a result of the Asian currency crisis,

and whether the crisis management measures introduced 10

years ago were suitable. The crisis presented an opportunity

to learn how to predict and prevent a future currency or

financial crisis, and to discover what measures can help

mitigate it in the event of a recurrence. I’ll ask you to discuss

some of the financial challenges facing Asia today, as well

as international issues.

First, let’s look back at the Asian currency crisis itself,

and remedial responses in the countries involved.

Kawai: Well, first of all even though we talk about an Asian

currency crisis, the situations in Thailand, Indonesia, Korea

and Malaysia were each a little different. A common denom-

inator was that the strong economic growth and boom

before the crisis, driven by active investment and heavy

inflows of capital, exhibited signs of economic and financial

vulnerabilities.

Much of capital inflows were in the form of short-term

bank funds and portfolio investments, money that could be

easily withdrawn. In general, foreign capital was not neces-

sarily used for productive investments that would strengthen

the supply side of the economy, but for investments in real

estate and stocks. Though the profitability of capital began to

fall across the board, foreign capital continued to flow in.

Rampant currency attack took place in Thai foreign

exchange markets in February and May 1997, with sudden

flights of capital out of the country. Thailand’s foreign

exchange reserves ran out due to spot and forward market

interventions, and on July 2 it became evident that the Bank

of Thailand could not maintain the value of the baht. The baht

quickly depreciated, and the contagion then spread to

Malaysia, Indonesia, the Philippines, Korea and other coun-

tries. By early 1998, the banking sectors and real economies

of all affected countries had been seriously impacted.

The currency crisis and the financial system crisis, cou-

pled together, set off a chain reaction. Different from the typ-

ical cases of current account crises occurring after foreign

exchange reserves are emptied due to current account

deficits, the crisis ten years ago was a capital account crisis

resulting from large capital inflows that suddenly stopped

and turned into massive outflows, causing foreign exchange

reserves to vanish over a short period of time. There was a

JBIC TODAY SPECIAL ISSUE 2007 3

Round-Table Discussion Ten Years After the Asian Currency Crisis — Lessons Learned for Further Development in Asia, Including Japan —

4 JBIC TODAY SPECIAL ISSUE 2007

Mr. Masahiro KawaiDean, Asian Development Bank Institute

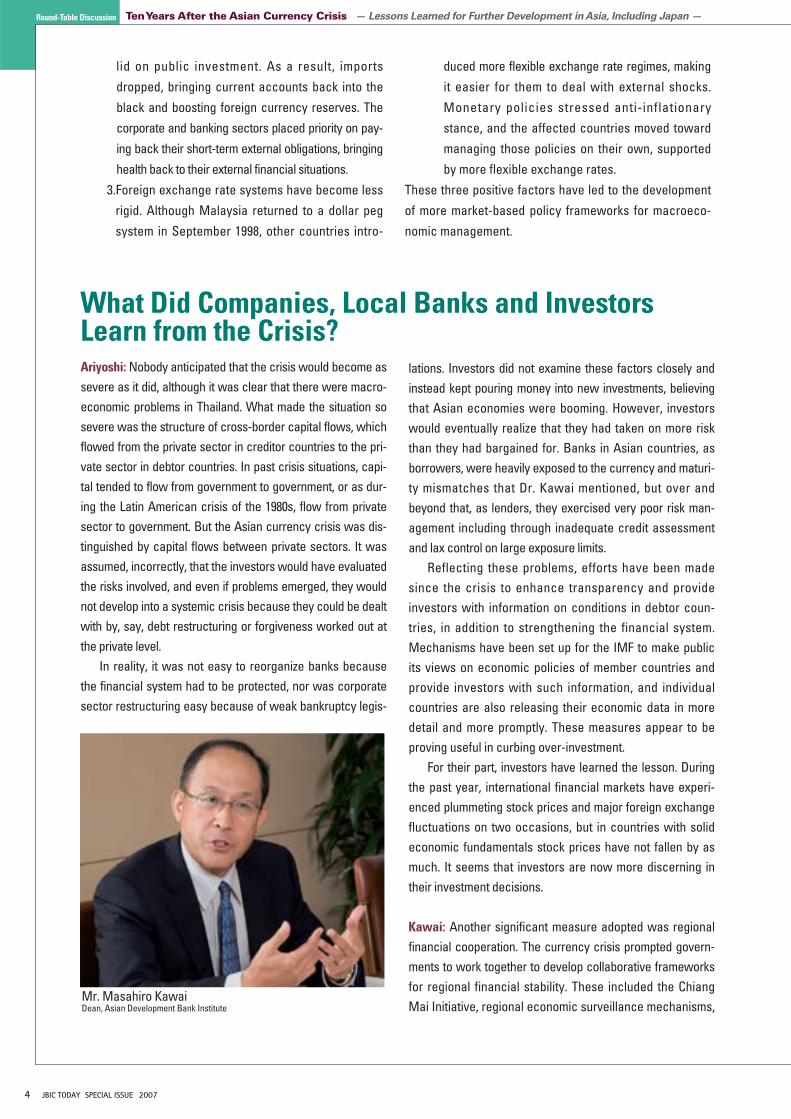

lations. Investors did not examine these factors closely andinstead kept pouring money into new investments, believingthat Asian economies were booming. However, investorswould eventually realize that they had taken on more riskthan they had bargained for. Banks in Asian countries, asborrowers, were heavily exposed to the currency and maturi-ty mismatches that Dr. Kawai mentioned, but over andbeyond that, as lenders, they exercised very poor risk man-agement including through inadequate credit assessmentand lax control on large exposure limits.

Reflecting these problems, efforts have been madesince the crisis to enhance transparency and provideinvestors with information on conditions in debtor coun-tries, in addition to strengthening the financial system.Mechanisms have been set up for the IMF to make publicits views on economic policies of member countries andprovide investors with such information, and individualcountries are also releasing their economic data in moredetail and more promptly. These measures appear to beproving useful in curbing over-investment.

For their part, investors have learned the lesson. Duringthe past year, international financial markets have experi-enced plummeting stock prices and major foreign exchangefluctuations on two occasions, but in countries with solideconomic fundamentals stock prices have not fallen by asmuch. It seems that investors are now more discerning intheir investment decisions.

Kawai: Another significant measure adopted was regionalfinancial cooperation. The currency crisis prompted govern-ments to work together to develop collaborative frameworksfor regional financial stability. These included the ChiangMai Initiative, regional economic surveillance mechanisms,

What Did Companies, Local Banks and InvestorsLearn from the Crisis?Ariyoshi: Nobody anticipated that the crisis would become assevere as it did, although it was clear that there were macro-economic problems in Thailand. What made the situation sosevere was the structure of cross-border capital flows, whichflowed from the private sector in creditor countries to the pri-vate sector in debtor countries. In past crisis situations, capi-tal tended to flow from government to government, or as dur-ing the Latin American crisis of the 1980s, flow from privatesector to government. But the Asian currency crisis was dis-tinguished by capital flows between private sectors. It wasassumed, incorrectly, that the investors would have evaluatedthe risks involved, and even if problems emerged, they wouldnot develop into a systemic crisis because they could be dealtwith by, say, debt restructuring or forgiveness worked out atthe private level.

In reality, it was not easy to reorganize banks becausethe financial system had to be protected, nor was corporatesector restructuring easy because of weak bankruptcy legis-

lid on public investment. As a result, imports

dropped, bringing current accounts back into the

black and boosting foreign currency reserves. The

corporate and banking sectors placed priority on pay-

ing back their short-term external obligations, bringing

health back to their external financial situations.

3.Foreign exchange rate systems have become less

rigid. Although Malaysia returned to a dollar peg

system in September 1998, other countries intro-

duced more flexible exchange rate regimes, making

it easier for them to deal with external shocks.

Monetary policies stressed anti-inflationary

stance, and the affected countries moved toward

managing those policies on their own, supported

by more flexible exchange rates.

These three positive factors have led to the development

of more market-based policy frameworks for macroeco-

nomic management.

JBIC TODAY SPECIAL ISSUE 2007 5

Mr. Fumio HoshiSenior Executive Director, Japan Bank for International Cooperation (JBIC)

volumes of forward in May 1997, and the Thai central

bank signed one contract after another to sell dollars in

forward to hedge funds. Forward dollar sales grew to

about the same volume as the country’s foreign currency

reserves; with the result that Thailand lost its foreign

reserves in forward trading. Realizing that the reserves

would be depleted within six months, Thailand switched to

a floating rate system in July.

On the other hand, Indonesia had ample foreign

The Crisis As a Learning Experience— A Catalyst for Financial Cooperation in Asia — Amma: Looking back at the situation 10 years ago, can you tell

us, Professor Ito, whether it was possible to predict and pre-

vent the crisis before it happened, and whether the measures

put in place after it occurred were appropriate or not.

Ito: I’ll confine my discussion to Thailand, Indonesia and

Korea, examining the different situations and responses

in each.

In Thailand, stocks had been declining for two years

before the crisis, and the current account deficit was 8%

of the GDP, so there were very clear signs that a crisis

could occur. The IMF was working behind the scenes

giving the Thai government advice, but the government

didn’t follow it. On the other hand, it was not possible to

predict a crisis in Indonesia. For one, stock prices didn’t

fall to the extent where one would expect a crisis until

the crisis actually occurred. In Korea, a few small finan-

cial groups had gone bankrupt, but this alone was not

enough to set the stage for a currency crisis, so a crisis

wasn’t forecast there either.

Some say that hedge funds caused the currency cri-

sis, but that would be true only in the case of Thailand.

Hedge funds were hardly involved at all in the process in

Indonesia or Korea. In Thailand, hedge funds sold large

and the Asian Bond Markets Initiative (ABMI) under theauspices of ASEAN+3 finance ministers.

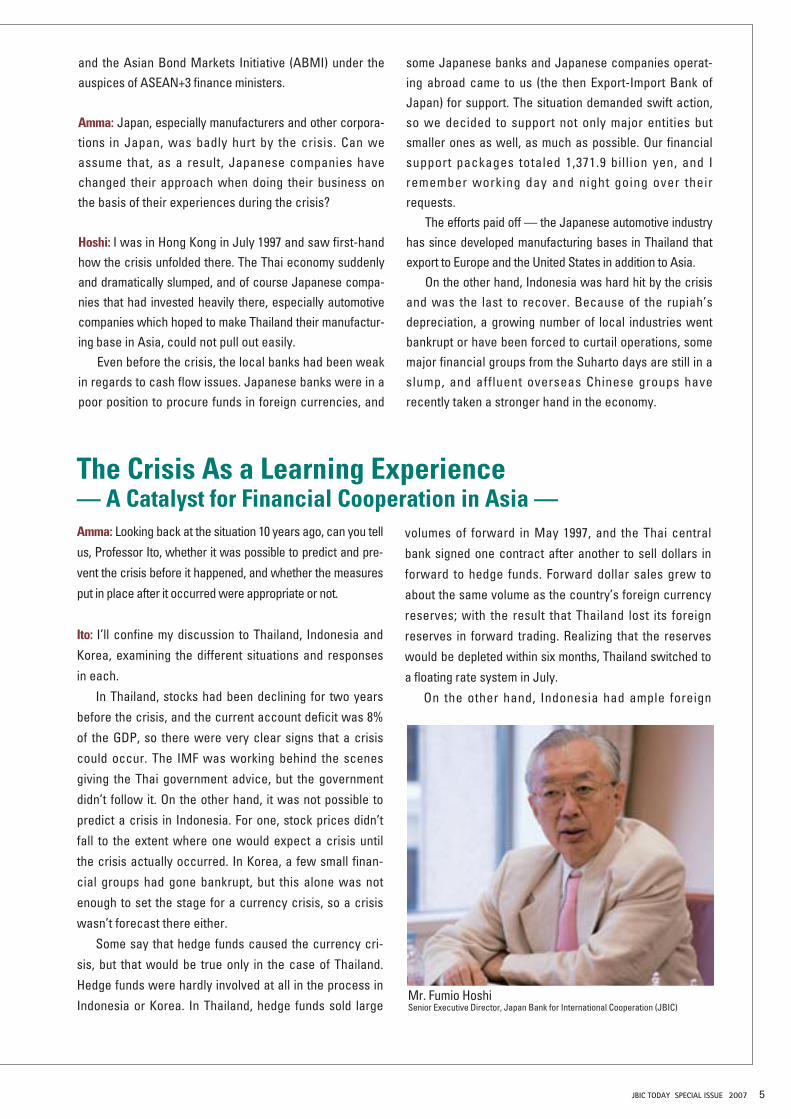

Amma: Japan, especially manufacturers and other corpora-tions in Japan, was badly hurt by the crisis. Can weassume that, as a result, Japanese companies havechanged their approach when doing their business onthe basis of their experiences during the crisis?

Hoshi: I was in Hong Kong in July 1997 and saw first-handhow the crisis unfolded there. The Thai economy suddenlyand dramatically slumped, and of course Japanese compa-nies that had invested heavily there, especially automotivecompanies which hoped to make Thailand their manufactur-ing base in Asia, could not pull out easily.

Even before the crisis, the local banks had been weakin regards to cash flow issues. Japanese banks were in apoor position to procure funds in foreign currencies, and

some Japanese banks and Japanese companies operat-ing abroad came to us (the then Export-Import Bank ofJapan) for support. The situation demanded swift action,so we decided to support not only major entities butsmaller ones as well, as much as possible. Our financialsupport packages totaled 1,371.9 billion yen, and Iremember working day and night going over theirrequests.

The efforts paid off — the Japanese automotive industryhas since developed manufacturing bases in Thailand thatexport to Europe and the United States in addition to Asia.

On the other hand, Indonesia was hard hit by the crisisand was the last to recover. Because of the rupiah’sdepreciation, a growing number of local industries wentbankrupt or have been forced to curtail operations, somemajor financial groups from the Suharto days are still in aslump, and affluent overseas Chinese groups haverecently taken a stronger hand in the economy.

Round-Table Discussion Ten Years After the Asian Currency Crisis — Lessons Learned for Further Development in Asia, Including Japan —

6 JBIC TODAY SPECIAL ISSUE 2007

Mr. Akira AriyoshiDirector, IMF Regional Office for Asia and the Pacific

reserves. That’s why I find it strange that the Indonesian

government approached the IMF for support. The then-

governor of the central bank later wrote that they wanted

advice on precautionary measures.

In Korea, the crisis was triggered by the refusal of foreign

creditor banks to roll over loans. Korea’s central bank

deposited foreign currency reserves in commercial

banks and the banks then used the deposits, which were

in dollars, in sales to companies that were having trouble

paying back their loans. This is how the country’s foreign

currency reserves dried up.

It’s difficult to find a common denominator among the

three countries that can serve as a learning experience.

The only thing we can say is that in Thailand, predictions

were made correctly and no preventive measures were

taken, but the crisis could not be avoided.

Even today experts disagree on whether hedge funds

should be placed under stricter regulation. Since the crisis

they haven’t undermined any country’s currency system,

and this would seem to indicate that countries have

learned from the Thai case. It is now evident that the

countries did not have enough foreign reserves at the

time, and learning from the experience — Asian coun-

tries have since accumulated substantial reserves as a

form of self-insurance.

Amma: How do you view of crisis management measures

taken at the time?

Ito: Attempts to manage the crisis in Thailand took the

form of loans provided under a package organized by the

IMF and Asian countries. IMF loans are limited to

amounts representing 3 to 5 times the amount invested in

the IMF by that country. That was not nearly enough for

Thailand, so a financial support package was put together

with the IMF contributing $4 billion, JBIC (at that time the

Export-Import Bank of Japan) another $4 billion, and other

Asian countries from $500 million to 1 billion. The total value

of the rescue package provided was $17.2 billion.

Indonesia and Korea received loans from three

organizations: the IMF, the World Bank, and the Asian

Development Bank (ADB). The support packages for

these two countries included Japan and the United

States as second-line of defense, but they did not in fact

lend any funds and the market hardly reacted favorably

to the packages at all. It is still necessary to examine a

desirable structure of the support package.

In this discussion it’s important to keep in mind the

size of the rescue package for Thailand. When the

amount contained in the package — $17.2 billion — was

made known in Thailand on August 20, it was also dis-

closed that the central bank had liabilities of $23.4 billion,

so the mood remained pessimistic and the baht did not

appreciate. Therefore, the funding package did not serve

its purpose as a barrier to stop the contagion of the finan-

cial crisis from spreading to other countries. During the

1994 Mexican crisis, the financial support offered was

large enough to stop the contagion to other parts of Latin

America, but this success story was not repeated in Asia.

The lesson here is clear: it is important to place

enough funds in a rescue package to regain market con-

fidence and prevent contagion. However, as Mr. Ariyoshi

said regarding Thailand, the problem involved capital

flows from one part of the private sector to another. It

was argued at the time that if the rescue package were

made too large, moral hazard issues could arise. So in

the end a half-hearted approach was taken.

As for Indonesia, the most prevalent theory why the

IMF was approached is that technocrats had misgivings

about the Suharto regime and seized the crisis as an oppor-

tunity to press for structural reform. Under this theory, the

“technocrats vs. Suharto” template evolved into “IMF vs.

Suharto”. I would say that the financial crisis became a

political one, and that this prolonged the economic

recession. The lesson here is that the IMF should not

become involved in domestic political disputes. Of course

it’s important that financial resources be used appropriately,

and that corruption be prevented, but the general opinion

JBIC TODAY SPECIAL ISSUE 2007 7

is that IMF should not be a tool for political use.

Another problem was that the Indonesian government,

motivated by the IMF support package, closed 16 banks

in November 1997 and ordered a cut in deposit amounts

held by large depositors. This led to a run on the banks,

which fanned the flames of the crisis. The government

should have ensured full protection of deposits, as was

done in Thailand. And even if it had mandated a cut in

deposits, it should have guaranteed the full amount

remaining.

In Korea, the IMF decided to extend its support at the

beginning of December, but there again the amount was

not enough to contain fears. So on December 24 the IMF

and G7 governments jointly issued guidelines to foreign

creditor banks, recommending that they maintain bal-

ance sheets rather than try to call in loans and end up

forcing borrowers into default. This eliminated fears to

some extent.

It’s difficult to discover lessons in all this, but the

experience does shine a light on the responsibility of

lenders, and did lead to discussions on whether mecha-

nisms should be established to support restructuring

efforts. Here I would like to point out that in Korea, banks

were lending to other banks. In Latin America, bonds

were issued as a way to procure capital from diverse

sources, but in Korea the funds were lent by a limited

number of banks, making it possible for IMF and G7 govern-

ment persuasions to work effectively. The situation in

Korea at the time, and the response to that situation, offer

plenty of food for thought.

I would say that it’s important to develop mechanisms

in which creditors are required to assume responsibility.

However, those types of mechanisms have not yet been

established.

Ariyoshi: Let me add a word so that what Professor Ito

said does not get misinterpreted. The IMF never acts with

the intention of changing the political system of a coun-

try. It conducts discussions with national governments

and offers financing so that the government can imple-

ment the most appropriate policies for economic recov-

ery. It is true that those policies will have a political

impact. What the experience in Indonesia shows is that

things will not go well unless the country is united behind

its policies.

It is also true that the IMF programs during the crisis

included a large number of conditions to ensure the success

of reform measures. In hindsight, if there are too many

conditions the credibility of the program — whose main

objective is to promote macroeconomic stability — may

suffer. That is why the recent IMF policy is to avoid

including conditionalities that do not have a clear linkage

with macroeconomic stability. Having said that, in the Asian

currency crisis, it was recognized that bank and company

balance sheets were in trouble, and that unless something

was done about that problem, confidence could not be

restored. This is why policy conditionality spanning various

areas were included in the IMF program.

With regard to the point that the financing package have

to be large enough to deal with the crisis, the IMF does not

have the resources to cope with very large needs on its own.

It would be practically impossible for the IMF, working alone,

to completely cover a shortfall during a capital account crisis,

and that is why it should collaborate with national govern-

ments, other international organizations and the private sector.

For example, during the Latin American crisis, the IMF asked

private banks to maintain exposure and also provide new

money to the affected countries to shore over the crisis. But

as Professor Ito pointed out, when existing debt is in the

form of bonds, there is the challenge of how we could

secure the cooperation of numerous and diverse creditors.

Kawai: As the crisis in Asia made financial systems dys-

functional, efforts were made to restore healthy banking

and corporate sectors. But the authorities were late in

recognizing the need to create a framework for restructur-

ing impaired corporate debt and revitalizing indebted, but

Prof. Takatoshi ItoGraduate School of Economics, and Graduate School of Public Policy

Round-Table Discussion Ten Years After the Asian Currency Crisis — Lessons Learned for Further Development in Asia, Including Japan —

Mr. Rintaro TamakiDirector-General, International Bureau, Ministry of Finance, Japan

8 JBIC TODAY SPECIAL ISSUE 2007

Development of Mechanisms for Prediction,Prevention and ResponseAmma: You have mentioned a number of lessons learned

from the crisis. How have those lessons guided efforts to

establish international financing mechanisms (which

would include collaboration among the Japanese gov-

ernment and the governments of other Asian countries,

plus the involvement of the IMF) to predict and prevent

another crisis, and to respond to one if it were to occur?

Tamaki: This has been a most useful discussion of the

origin, responses, and the lessons learned from the Asian

currency crisis.

With the strong economic performance in the region

today, there may be a tendency, as time goes by, for people

to forget the bitter experience of the crisis. I think it is

imperative that those of us who are involved in international

finance not take the past lightly — instead, we need to

work to prevent another currency crisis and to be prepared

for a recurrence.

In East Asia, we have come to recognize the impor-

tance of regional financial cooperation from our experience

dealing with the Asian currency crisis . From this coopera-

tive spirit sprang the current ASEAN+3 Finance Ministers’

process promoting regional cooperation for currency and

financial stability.

viable, corporations. When Japan’s speculative bubble

burst later, one very difficult challenge was also to find

ways to create a framework for dealing with impaired

corporate liabilities. Unless appropriate frameworks are

developed to deal with corporate debt, bankruptcies and

restructuring, it will be impossible to respond properly to

a financial system crisis.

Legal procedures concerning bankruptcies should be

designed to ensure transparency, but it is difficult to

manage a situation when so many companies fall into

dire strains and difficulties at the same time. That’s why

the affected Asian countries developed their own informal

processes to cope outside the parameters of bankruptcy

legislation. For example, the Malaysian government estab-

lished an asset management company (Danaharta) to buy

non-performing bank loans, an entity (Danamodal) to

recapitalize capital-short financial institutions, and an

organization (Corporate Debt Restructuring Committee) to

facilitate voluntary restructuring of corporate debt obliga-

tions outside of the court system. It announced that these

would act over a clearly specified period. There is much

we can learn from the Malaysian model, which I believe

was the best of all. An informal response system for cor-

porate bankruptcies would only work in countries that

already have adequate bankruptcy legislation and a

strong court system.

In Indonesia, the IMF and the World Bank were calling

the attention of the government to structural problems well

before the crisis, but the government ignored them

because the economy was surging ahead at the time. After

the crisis hit, technocrats had a good grasp of the underlying

structural issues and ended up involving the IMF and World

Bank in their own clamor for reform. They and these IFIs

were a bit too optimistic in assuming that medium- to long-term

reform items that did not relate directly to crisis manage-

ment and resolution would be achieved through the IMF

packages. The situation should have called for priority

measures to put the financial system back on track and

deal with corporate debt.

JBIC TODAY SPECIAL ISSUE 2007 9

We can say that the first step in preventing another

currency crisis is predicting it. In order to do this, we

need the kind of surveillance mechanisms that Mr. Kawai

mentioned. Surveillance includes ongoing studies exam-

ining the economic, fiscal and financial situations of

countries in order to quickly determine risk levels. This

should lead to regional efforts to promote improvements

in an economy at risk. These cooperative efforts not only

include exchanges of opinions and policy dialogues on

economic conditions among ASEAN+3 finance ministers,

but also studies such as those conducted by the IMF, the

Asian Development Bank (ADB) and other international

financial institutions.

In 2006, two groups — a “Group of Experts” to study

and analyze themes pertaining to all countries in the

region, and a “Technical Working Group” to examine

early warning systems — were established within the

ASEAN+3 framework. The May 2007 Joint Ministerial

Statement of ASEAN+3 Finance Ministers announced an

agreement to seek ways to further strengthen regional

surveillance through these and similar initiatives.

The Japanese government is also working to prevent

another currency crisis by supporting the development of

sound financial systems in Asia. As previously mentioned,

in the 1990s, around the time the crisis hit, there were

also weaknesses in capital procurement procedures in

the affected countries.

I believe that (i) alleviating both currency and maturity

mismatches, and (ii) using private-sector savings to

finance economic development needs are both linked to

preventing another crisis.

In pursuit of these objectives, Japan (in collaboration

with the ASEAN countries, China, and Korea) is promot-

ing a series of programs to revitalize financial markets

through mechanisms such as the Asian Bond Markets

Initiative (ABMI). In what will surely make significant

contributions for further developments in this area, JBIC

has also been conducting studies, research, and semi-

nars on ways to develop bond markets.

Steps are also being taken to ensure sufficient short-

term liquidity if another currency crisis were to occur in

Asian region. The Chiang Mai Initiative created a network

of bilateral swap arrangements among a number of coun-

tries in Asia. Under these agreements, if a currency crisis

were to occur in one country, other countries in the region

would provide capital to that country in order to prevent the

crisis from expanding or spreading to other countries. The

initiative gained the agreement of ASEAN+3 nations in May

2000, and currently encompasses a network of bilateral

swap arrangements among eight countries, including

Japan. At the present time, the parties are working to multi-

lateralize the Chiang Mai Initiative, by which the existing

bilateral agreements would be bundled into a single multi-

lateral network. This effort aims to strengthen the effective-

ness of the regional support arrangement and to increase

the efficiency of the support activation mechanism. Both

the original Initiative and CMI Multilateralisation are

intended to supplement existing capital-provision frame-

works managed by international financial institutions

such as the IMF and the Asian Development Bank, to

ensure a higher level of crisis response.

Rapid Growth in Asia Today — No Pitfalls Ahead?Amma: Last year, East Asian and Pacific region countries

enjoyed economic growth at an average of 9.5%, and the

total net inflow of private-sector capital amounted to $180

billion for the region as a whole. In addition, prices for

assets like real estate and securities have risen. At least

in these respects, the situation is similar to that of 10

years ago, before the currency crisis, except, of course,

for the economic fundamentals. Is there anything we

should be concerned about now?

Kawai: East Asian economies have performed differently

since the crisis. There is a clear difference between

China and ASEAN countries. China’s growth rate has

remained high, while growth rates in ASEAN countries

have been lower than before the crisis. The main reason

for the latter’s lower growth rates is lower investment

rates in ASEAN members.

China is exposed to a certain level of over-investment.

Because its savings rate is even higher than its high

investment rate, China has a current account surplus.

ASEAN countries are also posting current account sur-

pluses because their savings rates have not dropped as

Round-Table Discussion Ten Years After the Asian Currency Crisis — Lessons Learned for Further Development in Asia, Including Japan —

10 JBIC TODAY SPECIAL ISSUE 2007

much as the decline in their investment rates. These fac-

tors are the mirror image of the continued deficit in the U.S.

current account. We are thus seeing a global payments

imbalance. Recently the U.S. capital market has experienced

a confidence crisis since the subprime loan problem came

to light. The question we must ask now is whether Asian

economies will be able to deal with a situation where the

dollar depreciates and the Asian currencies appreciate

sharply as capital flows out of the United States and into

Asia.

As Asia is already experiencing capital inflows, I am

concerned about how such foreign capital is being used.

Most of the capital is not being used to boost production,

but for speculation in equity markets and real estate. I’m

afraid these countries are facing a situation similar to

that before the currency crisis. They are also applying

different exchange rate systems. China, which is compet-

ing in third markets against ASEAN countries such as

Thailand, has allowed only a moderate pace of apprecia-

tion of its currency (and under strict official oversight),

whereas the latter countries adopt relatively flexible sys-

tems and have seen more rapid currency appreciation.

For instance, to cope with capital inflows, Thailand

used capital inflow controls without much success in

December 2006 and has since lowered interest rates to

avoid a rapid appreciation of the baht. Monetary easing

can be justified since inflation and asset bubbles have not

become serious problems. However, if asset prices rise

much further and inflation becomes a concern, the Thai

government may have to allow a substantial appreciation

of the baht so as to reduce national macroeconomic risks

and maintain financial sector health. If this happens, it

would be preferable for the Chinese government to take

similar actions by permitting a steeper appreciation of the

yuan given the similar macroeconomic challenges in China

as well as the competitive relationship between China and

Thailand. In a word, the key lies in macroeconomic control

of national economies, including adjustments in the

Chinese exchange rate system. One country’s macroeco-

nomic policy can have an impact on neighboring countries.

I would hope for a regionally coordinated framework

capable of achieving regional financial stability, if not

through full-fledged official policy coordination.

Ito: The most important issue hanging over the global

economy is the mix of current account balances between

countries. The United States has a current account

deficit of almost 7% of its GDP. Because a corresponding

amount of capital is flowing into the country at the present

time, the dollar has not fallen much. On the opposite side

of the coin, China, other Asian countries, and oil-producing

countries such as those in the Middle East and Russia,

are showing a surplus in their current accounts, and the

governments of these countries are intervening in markets

to prevent their currencies from rising in value. Here we

must ask: (i) can such control policies be maintained for

much longer, and (ii) when, how and at what rate can

current account imbalances be reduced?

It is suggested that Asian currencies will have to be

revalued in relation to the U.S. dollar as part of the coming

imbalance reduction process. But because the Chinese

government currently permits an annual appreciation of

just 5%, the governments of other Asian countries are not

likely to let their currencies rise at a higher rate. For this

reason, Asian countries will probably soon get together

to discuss concerted action regarding exchange rate

systems. If they fail in such discussions, the economies of

some countries may overheat and some others may fall

into recession.

Countries have to watch carefully to see how the U.S.

government will act to reduce the imbalance, how long

crude oil prices will keep rising, and how long Asian coun-

tries will continue to show a surplus in their current

accounts.

Hoshi: Some significant changes have occurred over the

past 10 years: for some time investment was concentrated

almost exclusively in China, but after the SARS epidemic,

JBIC TODAY SPECIAL ISSUE 2007 11

Mr. Masaaki AmmaDirector General, JBIC Institute

other countries became concerned about investor depend-

ence on China and manufacturing bases were moved to

other countries, as part of the “China + 1” transition.

In Malaysia, where labor costs are rising, there have

been efforts to shift to high value-added industries. One

noticeable trend is for Japanese companies to acquire

high value-added businesses with excellent growth

potential. Capital will increasingly be invested in the priority

market segments of selected countries. As more free

trade agreements are signed, international specialization

will become more prevalent. Future regional financial

cooperation in Asia will have to take these trends into

account.

Ariyoshi: Asian countries’ foreign currency reserves, current

account balances and domestic financial systems are in

a far better position than at the time of the Asian currency

crisis. It is true, though, that capital flows into Asia are

reaching levels seen prior to the crisis, but large capital

inflows is a worldwide phenomenon, and we need to

remember that the economic fundamentals in Asia are

generally sound. Nonetheless, we need to keep an eye

on whether financial risk management, though much

improved, is up to the task of coping with increasingly

complex international financial markets.

Apart from these macroeconomic issues, I think the

Japanese government and JBIC chould play a more signifi-

cant role to reduce medium- and long-term risks in Asian

economies, for example in the areas of reducing income

inequality and resolving energy and environmental issues.

Such a bubble is now occurring in Vietnam as well,

and on a very large scale. Neither Indonesia has been

immune from this trend. In China and the Philippines,

investment is rising for the construction of large shopping

malls and similar projects. My personal view is that

investment in real property creates no added value,

unlike investment in facilities and equipment, and that

investments should therefore focus on projects that

boost productivity. This would be a major factor for con-

tributing to further development in Asia.

Capital Inflow Oversight: Avoiding the Collapse ofAnother Real Estate BubbleAmma: Last year, East Asia and the Pacific region received

direct foreign investments of $90 billion, portfolio investments

of $50 billion and private loan capital of more than $40 billion

(all net values). We should note that short-term loan funds

have increased rapidly and now represent 80% of all loan

funds.

Capital inflows through bond issues have remained

slightly under $10 billion over the last few years, but since last

year funds have poured into Asian countries as short-term

commercial loans. Should we be worried about these recent

movements?

Kawai: Asian countries now hold much larger foreign

exchange reserves. They maintain strong external finan-

cial positions and positive economic growth, and these

factors also attract foreign capital. The capital inflows

should be monitored to encourage the capital to be used

for productive purposes and not for speculation (equity

markets and real estate, for example), and to see

whether financial institutions are taking on additional

risks.

Hoshi: The main concern right now is that all of the Asian

countries we are talking about are in the midst of a real

estate bubble. The big worry is that rising real estate

prices may exert upward pressure on inflation rates.

Round-Table Discussion Ten Years After the Asian Currency Crisis — Lessons Learned for Further Development in Asia, Including Japan —

12 JBIC TODAY SPECIAL ISSUE 2007

lance programs.

In this way, the crisis has become an opportunity for

the countries in the Asian region to develop a stronger

sense of solidarity, and awareness that they must

respond in concert to any future crisis.

A moment ago, I spoke about the Chiang Mai

Initiative. It is a manifestation of this renewed sense of

regional solidarity. These cooperative efforts continue to

progress. and to evolve by means of, for example, the

multilateralization of the Chiang Mai Initiative and further

linkages outside of ASEAN+3, such as with India.

If one looks at the economic trends in Asia, it shows a

slowdown in infrastructure development around the

same time that governments began to try to reduce their

outstanding liabilities. However, there is still a great need

for new infrastructure to promote economic growth. An

important issue in meeting this need is improving and fur-

ther developing regional capital markets. In this regard,

the Japanese government is taking steps to (i) promote

the issuance of new debt instruments for infrastructure

Maintaining the International Financial Order: The Role Japan and JBIC Can PlayAmma: What role should the Japanese government play to

promote the objectives of the international financial order ?

Tamaki: As a result of the Asian currency crisis, authori-

ties in the affected countries became acutely aware of

the weaknesses in their financial markets and, in particu-

lar, of the dangers presented by a currency mismatch

combined with a maturity mismatch. They also realized

that if such a crisis goes uncontained it has the potential

to create a chain reaction and spread to other countries.

Additionally, a major currency or financial crisis can

bring about substantial damage to the real economy,

including higher levels of unemployment and poverty.

Finally, governments also shared the conviction that it is

important to collaborate when responding to a financial

crisis.

To prevent a recurrence of the Asian currency crisis,

the Japanese government stands ready to make every

effort towards the development of sound currency and

financial systems, and the promotion effective surveil-

If the ADB, the IMF, the World Bank and the

Japanese government are able to promote changes in

current investment patterns toward the model I am

describing, they will contribute greatly to development in

Asia and this will prove beneficial to Japan as well.

Ariyoshi: IIt is certainly true that real estate prices have

risen, and are still rising. Whether this could trigger

another Asian currency crisis depends on to what extent

the financial system is exposed to risk and whether they

are capable of absorbing those risks. For example, Hong

Kong has often experienced dramatic ups and downs in

real estate prices, but this did not cause systemic problems

because they were largely self-financed. In addition, the

fact that the speculative bubble in Japan spread nation-

wide caused a major problem, but the results of studies

we conducted several months ago show that currently in

Asia, real estate prices have not risen across the board in

an indiscriminate fashion.

Short-term capital inflows to Asia have been increasing

recently, and the rising proportion of yen-denominated

loans in some sectors could be a source of concern. If

the yen exchange rate rebounds, then that could inflict

large capital losses for the borrower.

Ito: Even if the bubble in Hong Kong bursts, banks in Hong

Kong would not be affected much. This is because Hong

Kong banks lower the loan to value ratio whose prices

have risen — for example; a maximum credit ceiling of

50% is applied to a property whose price has doubled.

Before the speculative bubble burst in Japan, credit ceil-

ings rose as the bubble expanded, and this proved to be a

mistake.

It has been said that investment in Asia has not

attained the level observed in the period preceding the

currency crisis, but I would suggest that investment was

far too high just before it. According to the economists

Alwyn Young and Paul Krugman, before the crisis the invest-

ment rate rose to an unnecessarily high level. Many firm

were renewing machinery in a manner that was inefficient. If

this hypothesis is correct, the current investment rate and

the current growth rate may be the most sustainable.

JBIC TODAY SPECIAL ISSUE 2007 13

financing; (ii) further promote the securitization of loan

credits and Receivables ; and (iii) encourage the use of

Asian Medium Term Note Programme. These steps are

being taken in line with the May 2007 Joint Ministerial

Statement of ASEAN+3 Finance Ministers.

From the time the crisis struck in 1997 through June

2006, the market for local currency denominated bonds

grew by about 680% in ASEAN countries plus China and

Korea (ASEAN+3 except for Japan). Some of this growth

came from local currency denominated bonds, for which

JBIC provided issuance support and guarantees. These

have become important instruments for promoting busi-

ness activities in Asia, especially the development of the

overseas business of Japanese companies. The

Japanese government is keen to see these efforts further

expanded.

The role Japan can play in Asia is now greater than

before the crisis. As Japan and other countries in Asia

deepen their economic ties, region-wide economic

growth becomes essential to sustainable development.

For this reason, the Japanese government hopes to con-

tinue to strengthen its economic ties in the region.

Kawai: There is no doubt that Asia needs much more

investment in infrastructure, especially for passenger and

freight transportation, and for the IT and electric power

sectors. Asia has vast amounts of savings, and conducive

financing frameworks are needed to guide those savings to

be invested in new productive infrastructure projects and

SMEs in Asia. The savings will flow to new projects if

investors are sure of a good return with minimum risk. Such

bankable projects could be developed under the leadership

of organizations such as JBIC and the ADB, and their lead-

ership could also be instrumental in developing financial

mechanisms, which combined with the bankable projects,

create opportunities for utilizing capital flows for produc-

tive purposes.

Hoshi: The ideas you have expressed today offer a broad

perspective on ways to prevent another Asian currency

crisis, and I thank you for this and for your complimentary

assessment of JBIC’s efforts and expectations of what

JBIC can do in the future.

JBIC has followed Japanese government policies in

responses immediately after the crisis hit and in the

implementation of diverse measures over the subsequent

10 years. We have been especially involved in promoting

the Asian Bond Markets Initiative proposed by the

Japanese government. As part of those efforts, we have

issued and provided guarantees for local currency

denominated bonds, and this has energized bond markets

in various Asian countries. These efforts are encouraging

local Japanese companies to raise capital locally.

We are also conducting studies and research projects

through tie-ups with the IMF, Asian Development Bank

Institute and other organizations. We then submit various

proposals to relevant countries, including suggestions on

drawing up legislation governing financial systems. We

hope to further deepen the close relationships of trust

that we have with many countries, relationships that have

grown through our many years of financing and policy

proposals. We also hope to continue encouraging

employment expansion in Asian countries, the transfer of

Japanese technology, human resources development,

and private sector promotion. These efforts, we hope, will

also facilitate successful development of Japanese manu-

facturing and banking industries.

Ten Years After the Crisis: Next On the Agenda for Cooperation

Dr. Kanit Sangsubhan Director, Fiscal Policy Research Institute (FPRI)

Thailand

– Fostering the Wealth of Asians While Dealing with the Global Imbalance

During the 10-year period since the Asian Crisis, the health of Asian economieshas been thoroughly examined. Information from one international conferenceafter another has confirmed that Asia is now far from being in a crisis of theprevious type, the capital account crisis. Although some countries have experi-enced massive capital inflows and a certain degree of excessive investment,which have led to bubbles in real estate and capital markets, the size of short-term foreign obligations (debts and equities) of each ASEAN+3 country is farless than the size of their foreign reserves. Capital account surpluses continueto pile up in tandem with current account surpluses, as the U.S. continues tospend more than it earns.

While Asia continues to reinforce its fortresses to prevent another crisis,Asian cooperation should turn to another chapter — fostering the wealthof Asians citizens and dealing with the global imbalance. There are threeissues for which close cooperation is required.

Managing the Twin SurplusEach of the ASEAN+3 countries is now facing difficulties in setting macro-economic parameters to cope with the flood of funds from current andcapital account surpluses. Fearing the loss of their export competitive-ness, each country attempts to manage its exchange rate so that its currencydoes not appreciate much above the currencies of other Asian countries.As a result, Asia has accumulated more foreign reserves than the financialintermediaries in Asia can handle. The reserves then end up mainlyfinancing the twin deficits in the U.S.

Unlike during the time of the Plaza and Louvre Accords, when Japanalone was earning a surplus, most East Asian countries now gain surplusesagainst the U.S. To correct this imbalance requires more than appreciationof the yen and the yuan against the dollar. If the U.S. current accountdeficit continues, other Asian currencies will also continue to receiveupward pressure.

To prevent further disruptive competition, Asian countries can moveto align their currency values and their rates of currency appreciation. Astrade within East Asia has already reached about 50% of the region’s totaltrade, a gradual appreciation of all local currencies vis-à-vis the dollarwould not change price competitiveness for intra-regional trade, but itwould correct the trade imbalance with the U.S. In this way, East Asiawould find its own solution, and the same solution could also help to correctthe global imbalance.

A more comprehensive currency alignment in the form of an AsianCurrency Unit (ACU) was proposed by two Japanese researchers.1

However, to proceed toward an ACU would require strong political support anddetailed analysis. Barry Eichengreen has suggested that, since the Asia oftoday is not the E.U. of 1957, Asia should innovate and find its own waysand means to achieve an ACU, using the ECU experience simply as a referenceand not try to duplicate it.2

Managing Information Flows, and a Surveillance SystemUnder Asian norms, directly criticizing other countries’ policies is prohibited.Nonetheless, there is nothing forbidding us from providing information and

analysis to support policymakers. In fact, if the Chiang Mai Initiative (CMI)progresses to a more comprehensive level, a more rigorous surveillancesystem will also be required.

At one extreme, the CMI, which is now moving toward a multilateralarrangement probably in some form of foreign reserve pooling, might someday evolve into an Asian Monetary Fund (AMF). If that were to happen, asubstantial degree of information flow, rigorous analysis and a surveillancesystem would be necessary to ensure AMF sustainability. As an intermediatesolution, Max Corden has suggested that one practical solution for Asiamight be the formation of an organization that focuses on informationgathering and solid analysis without political intervention, somewhat likethe Organization for Economic Co-operation and Development (OECD).3

Managing Regional InvestmentA big puzzle for East Asia is why investment is so small, compared to theavailable funds. For those countries that have come out of the crisis, theanswer would be fears of another bubble and non-performing loans.Lately, it seems to be a consensus that the first wave of investment shouldbe by a government promoting the necessary infrastructures.

Looking around ASEAN, for example, most road and rail transportationroutes linking the countries in Indochina have not reached the desiredstandard. Transportation among islands in Indonesia and the Philippinesneeds more investment to reduce travel costs and raise quality standards.In many ASEAN countries, the use of information and communicationtechnology is relatively low.

Even so, not many major investment projects have emerged or beenrealized since the crisis. Because countries are now so close, economi-cally and socially, infrastructure development is no longer confined withina country’s perimeter. It will now need to be implemented at the regionalor sub-regional scale. Road links like the North-South Corridor connectingSouthern China, the Lao PDR, Thailand, Myanmar, Malaysia and Singaporewould benefit the population in the region. Mega-projects across nationalborders may be extended to include cooperation in energy, telecommuni-cations, satellite, water supply, tourism and air transportation. However,trans-border mega-projects require strong cooperation among govern-ments.

Asia needs investment projects that provide real business activities,making good use of the available funds. Without new investment projects,surplus funds can only end up contributing to a bubble economy.

Asia’s next development phase requires closer cooperation to rein-force each other and secure the next growth path. Moreover, as East Asiabecomes an economic super-power — the GDP of the EA-9 (China, Korea,Taiwan, Hong Kong, Singapore, Malaysia, Indonesia, the Philippines andThailand) and Japan combined is now approximately 20% of the world’sGDP — it is the obligation of Asia to unite and act as one.

(This opinion piece is an abridged version of Next on the Agenda for Cooperation, found in Dr.Sangsubhan’s article, 10 Years After the Crisis: Is Asia Ready To Move On? )

Notes:1 T. Ito, T. and Ogawa, E. (2002), On the Desirability of a Regional Basket Currency Arrangement, Journal

of Japanese International Economies2 Eichengreen, B. (2007), Integrating Asia: Lessons from Europe3 Corden, M. (2007), Global Payments Imbalance: Issues and Regional Solutions

14 JBIC TODAY SPECIAL ISSUE 2007

Dr. M. Chatib Basri Director, Institute for Economic and Social Research, Faculty of Economics, University of Indonesia

Indonesia

– Events in IndonesiaDuring 1997 and 1998 Indonesia was haunted by the questions, when willwe begin to emerge from the crisis, and where will signs of improvementappear? The crisis began with Thailand. The contagious effect in Thailandreceived a poor response from the government and was followed by someerrors in policy responses, such as tightening the budget and raising interestrates substantially. These responses eventually brought the country into aneven more difficult situation.

In 1997 there was a lending boom in Indonesia, but this was accompaniedby a high ratio of non-performing loans to total credit. As the economy wentinto a deep recession due to contracting devaluation, many firms found them-selves in trouble. The response of the government and the central bank —tightening the budget and raising interest rates — simply increased theprobability of default and therefore increased capital outflows. Thisbrought Indonesia deeper into the crisis. Experience shows that the 1997-1998 economic crisis embroiled the banking sector, financial markets,exchange rates and short-term debt, and brought about the flight of capitaland political unrest.

– Needed Improvements for the Domestic Investment Climate

Ten years after the economic crisis, per-capita income in Asia has reboundedand surpassed the pre-crisis level, as have the GDP, consumption and exports.However, investment is still below the pre-crisis level. The debt-to-GDPratio has declined substantially to less than 40%, inflation has decelerated, andexchange rates are relatively stable. Macroeconomic progress is continuing, withinflationary pressure significantly lower and inflation under control. The CentralBank has started to reduce the interest rate. The rupiah has been stabilisedat around Rp 9,200 to the dollar, and stock prices have surged. In the firstsemester of 2007, the economy grew at an annually adjusted rate of 6.1%,although the growth still depends heavily on consumption — mostly gov-ernment consumption — and on the export of goods and services. This isdue to high commodity prices in the international market. In contrast to theacceleration of consumption and exports, investment remains sluggish,although it has started to pick up since early 2007.

It is worth noting that the decline of foreign direct investment in Indonesiasince the crisis was broad and not country-specific. In addition, a breakdownof the investment decline shows that the major contributor was lowerdomestic investment. Improvement in the investment climate is still neces-sary, but any revival of investment should also rely on domestic invest-ment. Ten years after the crisis, financial intermediation is still not in goodshape. Two actions need to be taken:

-Reduce agency costs and resolve asymmetric information issuesin the banking sector to facilitate credit expansion to the corporatesector. This cannot be solved simply by cutting interest rates, butby providing information that bridges the gap between lenders andborrowers while reducing risk in the production sector. Interestrate cuts will induce demand, but structural factors such as infra-structure bottlenecks and problems of asymmetric information hinder supply response, and thus could create inflationary pressure.

-Improve the supply side by increasing the ability of government tospend money on infrastructure and remove rigidity in the labor market.

– Raising Capacity to Satisfy Economic Expectations

Recently there have been concerns that the rapid portfolio capital inflows nowseen in many Asian countries could leave those countries vulnerable if a suddenreversal of capital flow were to occur. Indeed, the risk is still there. But this doesnot mean that if there were a sudden reversal of capital flow Indonesia wouldreturn to an economic crisis. The country is now quite different from what it was10 years ago when the crisis began. Major differences are:

-The financial sector is healthier than it was 10 years ago. Banks are nolonger overextended, and they follow more conservative and prudentlending standards.

-Unlike 10 years ago, economic entities have learned the need to diversi-fy their risk. Before Bank Indonesia abandoned its managed floatingsystem in 1997, there was no point in hedging assets because theIndonesian rupiah constantly depreciated by 5% every year. Now eco-nomic entities have diversified their portfolios and hedged their assets.Thus, even if there were a sudden reversal of capital flows, the impactwould be less than it was 10 years ago.

-Institutional reform. Ten years after political change, institutional andgovernment reform has progressed and the political system has beensignificantly democratized. Nevertheless, we must admit that given theexisting political structure, Indonesia still needs reforms before it can beconsidered substantively democratic.

Despite these positive developments, in Indonesia there is a growing concernover the realization of reform measures. Many good policy recommendationscannot be implemented because institutions do not work effectively. On the otherhand, expectations that government is able to bring the economy back to the pre-crisis situation are very high. There is thus a large gap between expectations andthe ability to deliver economic reform. Under this situation, managing expecta-tions is the key issue.

(This opinion piece is an abridged version of an article by Mr. Basri.)

JBIC TODAY SPECIAL ISSUE 2007 15

No part of this magazine may be reproduced without the written permission of JBIC.

For inquiries, please contact:JBIC Public Relations Office4-1, Otemachi 1-Chome, Chiyoda-ku, Tokyo, Japan 100-8144Tel. +81-3-5218-3101 URL http://www.jbic.go.jp/english/index.php

This magazine is printed on recycled paper using environmental-friendly soy ink.

Printed in Japan

Cover: Tenryu-ji temple, Japan

Contributing to Development of the InternationalCommunity and Efforts to Raise Living StandardsIn October 2008, of the two types of operations conducted by thecurrent JBIC, Japan Finance Corporation (JFC)* will take over theInternational Financial Operations (IFOs) in its international financesector. However, to maintain international trust and confidenceenjoyed by JBIC, the international finance sector of JFC willcontinue to use the name of JBIC as it conducts internationalfinance operations. The “New JBIC” will perform the followingthree functions in order to contribute to the sound develop-ment of the international economy, including Japan.

1.Promoting overseas development of natural resources whichare strategically important;

2.Supporting efforts of Japanese industries to developinternational business operations; and

3.Responding to financial disorder in the internationaleconomy.

This issue has looked back at the Asian currency crisis thatstruck 10 years ago, focusing particularly on measures that canbe taken to prevent monetary disruptions at the Asian or inter-national level. While pursuing the third function mentionedabove, JBIC will strengthen its efforts to prevent another crisis,and will continue to explore ways to rapidly implement optimummeasures that would respond to a wide variety of needs if another

crisis were to break out. These efforts will be based on theexperience JBIC gained while providing comprehensive emer-gency support during diverse crises in the past, especially theAsian currency crisis.

*Tentative name in English

Crisis Prevention and Response: JBIC’s RoleEfforts to prevent the recurrence of a crisis require the establish-ment and maintenance of close relations with other countries, andnetworking with international organizations and the governmentsand government institutions of the countries involved. Mutualrelations of trust are very difficult to establish at a moment’snotice, and for this reason JBIC places importance on maintainingrelations on a continual basis. Relationships like these includecooperation in many areas, and direct talks with the peopleinvolved to obtain information on the political and economicsituations in the countries concerned.

Accurate information analysis and situation monitoringrequire sustained efforts to improve the capacity of interna-tional financing. JBIC will continue to maintain close ties withinternational monetary authorities, and will strengthen its systemsto raise its ability to gather information in all relevant sectors,whether government or the private, to understand financing needs,and to respond rapidly and seamlessly if another crisis occurs.

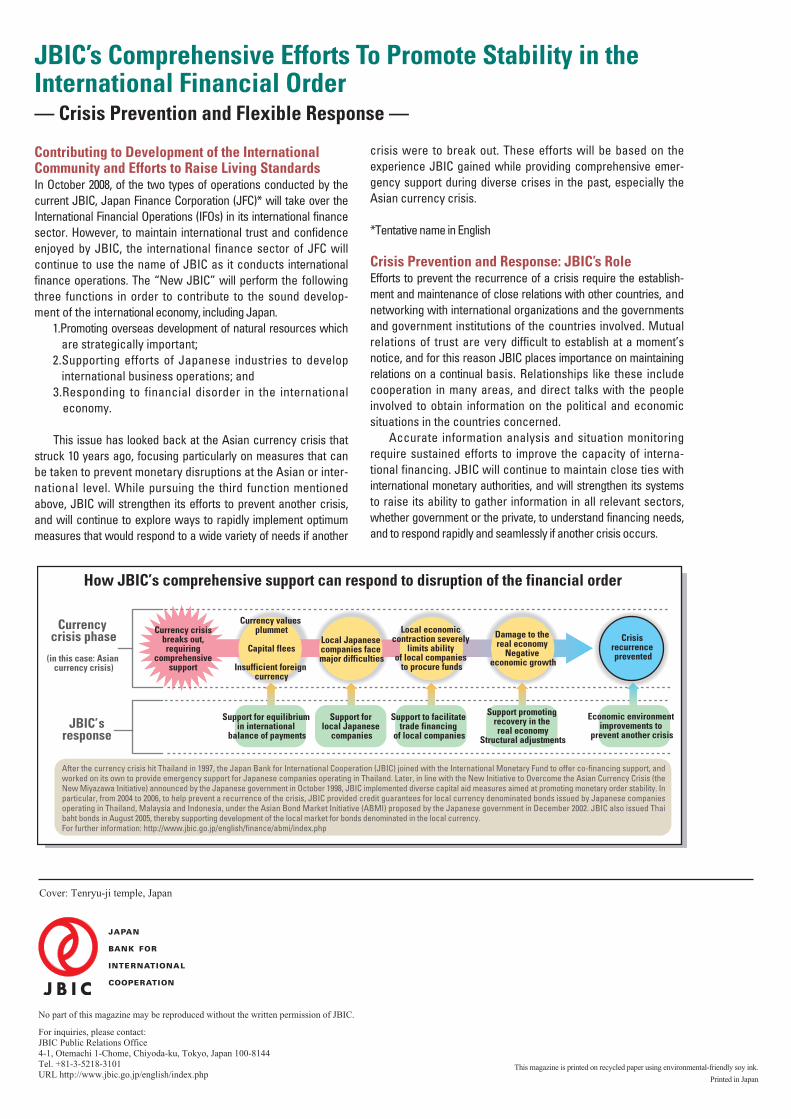

JBIC’s Comprehensive Efforts To Promote Stability in theInternational Financial Order — Crisis Prevention and Flexible Response —

After the currency crisis hit Thailand in 1997, the Japan Bank for International Cooperation (JBIC) joined with the International Monetary Fund to offer co-financing support, and worked on its own to provide emergency support for Japanese companies operating in Thailand. Later, in line with the New Initiative to Overcome the Asian Currency Crisis (the New Miyazawa Initiative) announced by the Japanese government in October 1998, JBIC implemented diverse capital aid measures aimed at promoting monetary order stability. In particular, from 2004 to 2006, to help prevent a recurrence of the crisis, JBIC provided credit guarantees for local currency denominated bonds issued by Japanese companies operating in Thailand, Malaysia and Indonesia, under the Asian Bond Market Initiative (ABMI) proposed by the Japanese government in December 2002. JBIC also issued Thai baht bonds in August 2005, thereby supporting development of the local market for bonds denominated in the local currency. For further information: http://www.jbic.go.jp/english/finance/abmi/index.php

How JBIC’s comprehensive support can respond to disruption of the financial order

Currency crisis phase

(in this case: Asian currency crisis)

Currency crisis breaks out, requiring

comprehensive support

Support for equilibrium in international

balance of payments

Support for local Japanese

companies

Support to facilitate trade financing

of local companies

Support promoting recovery in the real economy

Structural adjustments

Economic environment improvements to

prevent another crisis

Local Japanese companies face major difficulties

Crisis recurrence prevented

Currency values plummet

Capital flees

Insufficient foreign currency

JBIC’s response

Local economic contraction severely

limits ability of local companies

to procure funds

Damage to the real economy

Negative economic growth