Embed Size (px)

Citation preview

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 1/24

CITY OF JACKSONVILLE

DISABILITY PROGRAM

2009 ACTUARIAL VALUATION REPORT - REVISED

MARCH 2010

ACTUARIAL VALUATION AS OF OCTOBER 1, 2009

TO DETERMINE CONTRIBUTIONS TO BE PAID

IN THE FISCAL YEARS BEGINNING OCTOBER 1, 2009

AND OCTOBER 1, 2010

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 2/24

March 29, 2010

Board of Pension TrusteesCity of Jacksonville Disability ProgramCity of Jacksonville117 West Duval Street Jacksonville, Florida 32202

Gentlemen:

CITY OF JACKSONVILLE DISABILITY PROGRAM2009 ACTUARIAL VALUATION REPORT

This report presents the results of the 2009 actuarial valuation of the City of JacksonvilleDisability Program. Actuarial Concepts was retained by the City to perform theactuarial valuation and prepare this report. This actuarial valuation was prepared andcompleted by us or under our direct supervision, and we acknowledge responsibilityfor the results. To the best of our knowledge, the results are complete and accurate and,in our opinion, the techniques and assumptions used are reasonable and meet theprovisions and intent of Part VII, Chapter 112 Florida Statutes. There is no benefit orexpense to be provided by the Program and/or paid from the Program’s assets forwhich liabilities or current costs have not been established or otherwise taken intoaccount in the valuation. All known events or trends that require a material increase inProgram costs or required contribution rates have been taken into account in the

valuation.

The use of the valuation results for financial or administrative purposes other thanthose outlined in the report is not recommended without an advance review byActuarial Concepts of the appropriateness of such application.

Members of our staff are available to discuss this report and related issues.

Very truly yours,

ACTUARIAL CONCEPTS

By:Michael J. Tierney

ASA, MAAA, FCA, EA #08-1337

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 3/24

TABLE OF CONTENTS

SECTION 1KEY VALUATION RESULTS SUMMARY.........................................................................1-1

Initial Valuation...........................................................................................................1-1Valuation Basis ............................................................................................................ 1-1City Contribution Requirements ..............................................................................1-1City Contribution Breakdown...................................................................................1-2Current Funded Status...............................................................................................1-3True Costs ....................................................................................................................1-4

SECTION 2ACTUARIAL VALUATION DEVELOPMENT .................................................................2-1

Date and Basis of Valuation ...................................................................................... 2-1Valuation Financial Values........................................................................................2-2

Explanation of Financial Values ...............................................................................2-3

SECTION 3ANALYSIS OF VALUATION RESULTS.............................................................................3-1

Discussion of Valuation Results ...............................................................................3-1Valuation Results ........................................................................................................ 3-2

APPENDIX A PROGRAM PROVISIONS SUMMARY................................................A-1

APPENDIX B ACTUARIAL ASSUMPTIONS ANDACTUARIAL COST METHOD SUMMARY .......................................B-1

APPENDIX C ACTUARIAL VALUE OF ASSETS........................................................C-1

APPENDIX D CENSUS DATA SUMMARY..................................................................D-1

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 4/24

1-1

SECTION 1

KEY VALUATION RESULTS SUMMARY

The 2009 valuation of the Disability Program presents a statement of the estimated

financial position of the Program as of October 1, 2009. Information in the reportprovides bases for determining contribution requirements.

Initial Valuation

This is the initial valuation of the Disability Program, created via spinoff from the

General Employees Pension Plan (GEPP).

The spinoff from the GEPP has assigned actuarial value of assets equal to the actuarial

accrued liability; thus, there is no initial unfunded actuarial accrued liability or

amortization payments.

Valuation Basis

The valuation was based on the same assumptions and cost method as used for the

GEPP.

City Contribution Requirements

Annual Requirements* 2009-10 2010-11

Normal Cost 1,122,476$ 1,161,763$UAAL Amortization - -

Total Plan Contributions 1,122,476$ 1,161,763$

Estimated Member Contributions 838,513 867,861 Net City Contributions 283,963$ 293,902$

* The 2009 valuation determines contribution requirements for fiscal years 2009-2010 and

2010-2011.

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 5/24

1-2

City Contribution Breakdown

2009-2010 Total Member Net CityCity 598,087$ 446,783$ 151,304$ JEA 505,926 377,937 127,989

JHA 16,680 12,460 4,220 JPA - - - JAA - - - FLA - - - MPO 1,783 1,332 451 SB - - - TOTAL 1,122,476$ 838,513$ 283,963$

2010-2011 Total Member Net City

City 619,020$ 462,421$ 156,599$

JEA 523,634 391,165 132,468 JHA 17,264 12,896 4,367

JPA - - -

JAA - - -

FLA - - -

MPO 1,845 1,379 467

SB - - - TOTAL 1,161,763$ 867,861$ 293,902$

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 6/24

1-3

Current Funded Status - Projected Liabilities

Current Funded Status

$9,981,282 $9,981,282

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

Actuarial Value of Assets Actuarial Accrued Liability (AAL)

100%

Funded

A comparison of assets with the AAL is used by GASB to judge the progress to date of

funding the "ultimate" liability associated with service earned to date. A common goal

is to have 100% funding of the AAL, and a maturing plan's funded ratio should increase

over time.

The disability benefit liability APVs were developed using the assumed rate of future

investment return of 8.4%. On this basis the current liability is 100% funded.

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 7/24

1-4

True Costs

It should be noted that the true costs of a disability program cannot be determined until

its future unfolds. No one can precisely predict the interest earnings on fund assets,

member disability rates, future salary levels, mortality experience, etc. Estimates based

on experience with similar groups, along with the judgment of the actuary and theprogram sponsor, can provide a reasonable approximation of this true cost. As actual

experience emerges under the Program, it will be necessary to study the continued

appropriateness of the techniques and assumptions employed and to adjust the

contribution rate as necessary.

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 8/24

2-1

SECTION 2

ACTUARIAL VALUATION DEVELOPMENT

Date and Basis of Valuation

Estimated liabilities with respect to the disability benefits provided by the DisabilityProgram and the contributions recommended to fund these liabilities have been

determined as of October 1, 2009, based upon:

1. the provisions of the Program, as in effect on October 1, 2009, as summarized in

Appendix A;

2. the actuarial assumptions and actuarial cost method, as summarized in

Appendix B;

3. the fund assets at October 1, 2009, provided by the City, as summarized in

Appendix C;

4. the member data as of September 30, 2009, as summarized in Appendix D.

The fund assets have been established as of October 1, 2009, via spinoff from the

Jacksonville Retirement System. The member data has been supplied by the City and

provided as an actual representation of the current participating group. While the

member information was reviewed for overall reasonableness, Actuarial Concepts has

relied on the City for this information and does not assume responsibility for either its

accuracy or completeness.

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 9/24

2-2

Valuation Financial Values

1. Participation

(a) Number of Active Members 5,112

(b) Number of Disabled Members -

(c) Annual Valuation Payroll 279,504,240$

2. Actuarial Present Value (APV) of Future Benefits as of 10/1/09

(a) Active Members 20,007,502

(b) Disabled Members -

(c) Total 20,007,502$

3. APV Apportionment of line 2(c)*

(a) APV of Total Future Normal Costs 10,026,220

(b) Actuarial Accrued Liability [(2c)-(3a)] 9,981,282

(c) Actuarial Value of Assets 9,981,282

(d) Unfunded AAL (UAAL) [(3b)-(3c)] -$4. Breakdown of UAAL on line 3(d)

(a) UAAL [3(d)] -

(b) Change in UAAL Due to Assumption & Plan Changes -

(c) UAAL Before Change [(4a)-(4b)] -$

(d) Expected UAAL -

(e) Actuarial (Gain) Loss [(4c)-(4d)] -$

5. Development of City Normal Cost Rate**

Percentage of

Payroll

(a) Plan Normal Cost 1,143,636$ 0.40%

(b) Expense Normal Cost 18,127 0.01%

(c) Total Plan Normal Cost 1,161,763$ 0.41%

(d) Amortization of UAAL - 0.00%

(e) Total Required Plan Contribution [(5c)+(5d)] 1,161,763$ 0.41%

(f) Estimated Member Contributions 867,861 0.30%

(g) Net Required City Contribution Amount [(5e)-(5f)] 293,902$ 0.11%

* Calculated in accordance with the Individual Entry Age Actuarial Cost Method.

** Assumed payable in 12 equal installments at the end of each month beginning 10/31/10.

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 10/24

2-3

Explanation of Financial Values - Valuation Table

Actuarial Present Value (APV) of Future Benefits (line 2c)

The APV of future benefits is determined by first measuring what future

disability benefit amount would be available for each member at various future

dates (assuming future salary increases awarded) under disability conditionsprovided for by the Program. Then the future value of those disability

entitlements is determined by multiplying the various disability benefit amounts

by the then current value of the annuities associated with those amounts. Finally,

the APV of those future disability benefit values is determined by applying

discounts to recognize the time value of money and probabilities of disability,

death, termination of employment, etc.

APV of Total Future Normal Costs (line 3a)

The APV of future normal costs is that portion of the total APV of future

disability benefits, as described above, that is assigned to future plan years by the

Individual Entry Age Actuarial Cost Method (described in Appendix B).

Actuarial Accrued Liability (line 3b) and

Unfunded Actuarial Accrued Liability (line 3d)

The AAL and the UAAL (the AAL less the actuarial value of assets) are actuarial

values generated under the Individual Entry Age Actuarial Cost Method, as

described in Appendix B. These liability amounts are not the APV of disability benefits accrued to date by members. They are actuarially determined amounts

based on the accrual of Individual Entry Age normal cost amounts due prior to

the valuation date. The liability for disability benefits accrued to date (the APV of

accrued disability benefits) is presented in Section 3.

Explanation of Financial Values - Funding Requirements

Program Normal Cost (line 5)

The normal cost rate has been determined by first calculating for each member

an individual yearly normal cost (that changes in dollar amount as pay increases,

but is constant as a percent of each individual’s pay), then adding together to

obtain the Program normal cost amount as of the beginning of the year. This

preliminary total is then adjusted for interest credits assuming contributions are

made monthly and an amount to allow for expected annual expenses.

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 11/24

3-1

SECTION 3

ANALYSIS OF VALUATION RESULTS

Discussion of Valuation Results

If the participating group remained unchanged and all the actuarial assumptions wererealized, the Program's experience would be as anticipated, and there would be no

actuarial gain or loss. If the experience were less favorable than anticipated, an actuarial

loss would result; if more favorable, an actuarial gain would result.

Future valuations will monitor the Program's experience to determine whether actuarial

gains or losses have occurred since the previous valuation. Recognition of these

actuarial gains or losses will be made through adjustments to the UAAL and amortized

over the same period as used for the pre-adjusted UAAL.

It should be noted that the true costs of a disability program cannot be determined until

its future unfolds. No one can precisely predict the interest earnings on fund assets,

member termination rates, future salary levels, mortality experience, etc. Estimates

based on experience with similar groups, along with the judgment of the actuary and

the Program sponsor, can provide a reasonable approximation of this true cost. As

actual experience emerges under the Program, it will be necessary to study the

continued appropriateness of the techniques and assumptions employed and to adjust

the contribution rate as necessary.

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 12/24

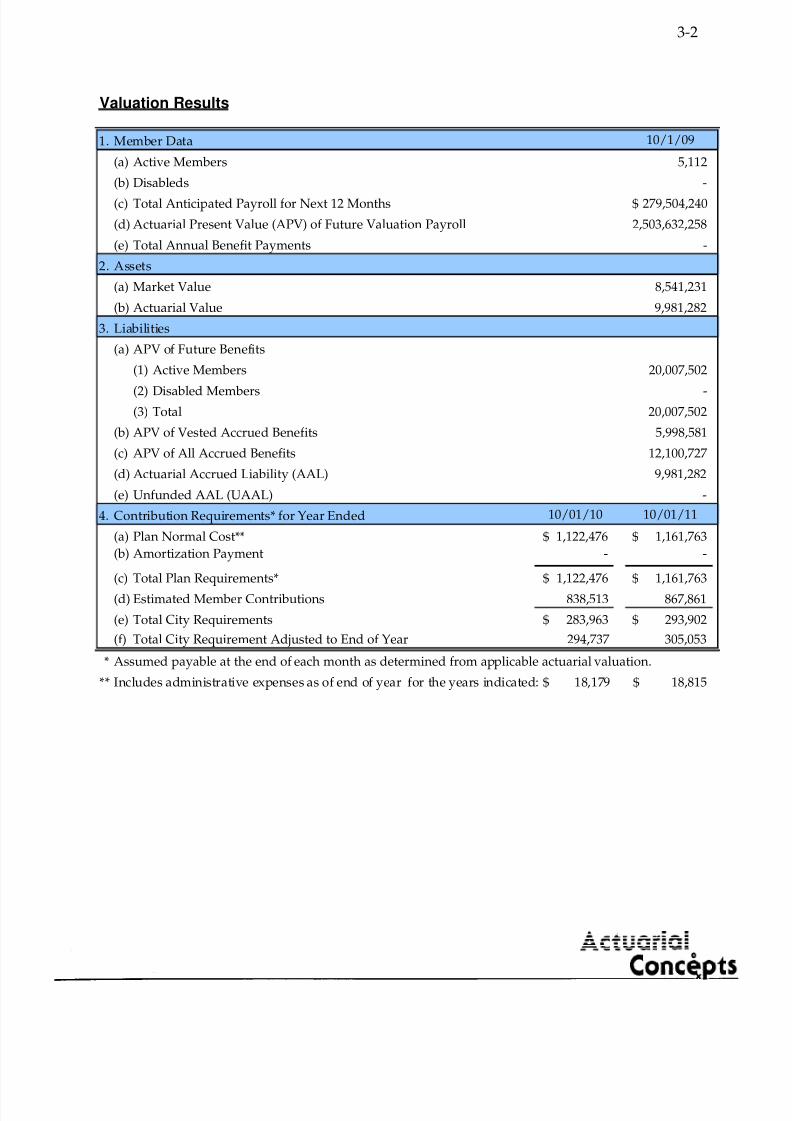

3-2

Valuation Results

1. Member Data 10/1/09

(a) Active Members 5,112

(b) Disableds -

(c) Total Anticipated Payroll for Next 12 Months 279,504,240$

(d) Actuarial Present Value (APV) of Future Valuation Payroll 2,503,632,258

(e) Total Annual Benefit Payments -

2. Assets

(a) Market Value 8,541,231

(b) Actuarial Value 9,981,282

3. Liabilities

(a) APV of Future Benefits

(1) Active Members 20,007,502

(2) Disabled Members - (3) Total 20,007,502

(b) APV of Vested Accrued Benefits 5,998,581

(c) APV of All Accrued Benefits 12,100,727

(d) Actuarial Accrued Liability (AAL) 9,981,282

(e) Unfunded AAL (UAAL) -

4. Contribution Requirements* for Year Ended 10/01/10 10/01/11

(a) Plan Normal Cost** 1,122,476$ 1,161,763$

(b) Amortization Payment - -

(c) Total Plan Requirements* 1,122,476$ 1,161,763$

(d) Estimated Member Contributions 838,513 867,861

(e) Total City Requirements 283,963$ 293,902$

(f) Total City Requirement Adjusted to End of Year 294,737 305,053

* Assumed payable at the end of each month as determined from applicable actuarial valuation.

** Includes administrative expenses as of end of year for the years indicated: 18,179$ 18,815$

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 13/24

APPENDIX A-1

CITY OF JACKSONVILLE

DISABILITY PROGRAM

SUMMARY OF PROGRAM PROVISIONS THAT AFFECT THE VALUATION

Definitions

1. Member: All members of the General Employees PensionPlan and the Defined Contribution Plan.

2. Member Contributions: 0.3% of Earnings via employer pickup.

3. Creditable Service: The number of full years and months workedfrom date of participation to date of terminationor retirement, plus any prior service purchased.

4. Earnings: Base earnings plus service raises received by aMember as compensation for services to theCity, excluding overtime pay, bonuses and otherextra pay.

5. Disability Benefit: Off the JobMembers who have completed 5 years of serviceat the time of becoming disabled shall be entitledto a benefit equal to 25% of Earnings, increased by 2.5% per year for service in excess of five

years, up to a maximum of 50% of Earnings,determined as of date of disability and payableas of the Disability Retirement Date.

Members who have not completed 5 years of service at the time of becoming disabled shallreceive a return of employee contributions.

On the JobA benefit equal to 50% of Earnings, payable as of the Disability Retirement Date, but not less than

$43.31 per whole year of Creditable Service notto exceed 30.

6. Death Benefit: If a Member should die while disabled with anEligible Spouse, 75% of the Disability Benefitshall be paid to the surviving spouse as defined

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 14/24

APPENDIX A-2

in Section 120.207(a) of the General EmployeesPension Plan Ordinance.

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 15/24

APPENDIX B-1

CITY OF JACKSONVILLE

DISABILITY PROGRAM

ACTUARIAL ASSUMPTIONS AND ACTUARIAL COST METHOD SUMMARY

Actuarial Assumptions

1. Investment Return: 8.4% per annum, compounded annually; net of investment expense (includes underlying long-term inflation rate of 3.5% per annum).

2. Salary Increase Rate: Years of Service Rate5 and Under 7.5%6 - 10 6.011 - 15 5.016 and Over 4.0

3. Mortality Rates: RP-2000 Mortality Table for all programmembers (actives, retirees and disableds)

Probability of DeathWithin One Year

After Attaining Age ShownAge Male Female25 0.04% 0.02%35 0.08 0.0545 0.15 0.1155 0.36 0.2765 1.27 0.97

4. Retirement Rates Based on Service and Age:

COJYears of Service under 50 50-54 55-59 60-64 65-69 70+under 20 0% 0% 0% 0% 20% 100%

20 0% 5% 25% 50% 50% 100%21-27 5% 5% 5% 20% 20% 100%

28-29 0% 5% 10% 20% 20% 100%30 15% 15% 15% 15% 20% 100%31 5% 5% 5% 5% 15% 100%32-34 15% 15% 15% 15% 15% 100%35 30% 30% 30% 20% 50% 100%

Age

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 16/24

APPENDIX B-2

JEAYears of Service under 50 50-54 55-59 60-64 65-69 70+under 20 0% 0% 0% 0% 20% 100%

20 0% 5% 15% 50% 50% 100%

21-27 5% 5% 10% 10% 20% 100%28-29 1% 5% 10% 10% 20% 100%

30 5% 10% 15% 15% 20% 100%31 5% 10% 10% 15% 15% 100%32-34 5% 10% 20% 15% 15% 100%35 0% 30% 40% 40% 40% 100%

Age

5. Termination Rates:

COJMales durations

ages 0 1 2 3 4 5 6 7 8 9 ultimate

under 20 26.0% 22.0% 22.0% 22.0% 15.0% 12.0% 12.0% 11.0% 11.0% 11.0% 7.0%

20–24 26.0% 18.0% 18.0% 18.0% 15.0% 12.0% 12.0% 11.0% 11.0% 11.0% 7.0%

25–29 26.0% 14.0% 14.0% 14.0% 11.0% 11.0% 6.0% 5.0% 5.0% 4.0% 3.0%

30–34 24.0% 14.0% 14.0% 11.0% 9.0% 6.0% 6.0% 5.0% 5.0% 4.0% 2.5%

35–39 18.0% 14.0% 12.0% 9.0% 6.0% 6.0% 6.0% 5.0% 5.0% 3.0% 2.5%

40–44 15.0% 10.0% 10.0% 9.0% 6.0% 6.0% 6.0% 5.0% 5.0% 3.0% 2.5%

45–49 14.0% 10.0% 10.0% 6.0% 6.0% 6.0% 6.0% 4.0% 4.0% 3.0% 2.5%

50–54 14.0% 10.0% 8.0% 6.0% 4.0% 4.0% 4.0% 4.0% 4.0% 3.0% 2.5%

55–59 12.0% 6.0% 6.0% 4.0% 4.0% 4.0% 4.0% 4.0% 4.0% 3.0% 2.5%

60 & over 8.0% 6.0% 4.0% 4.0% 4.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

COJ

Females durations

ages 0 1 2 3 4 5 6 7 8 9 ultimate

under 20 24.0% 22.0% 20.0% 16.0% 15.0% 15.0% 15.0% 15.0% 15.0% 15.0% 6.0%

20–24 24.0% 18.0% 18.0% 15.0% 14.0% 14.0% 12.0% 12.0% 12.0% 12.0% 6.0%

25–29 22.0% 18.0% 18.0% 14.0% 11.0% 10.0% 10.0% 10.0% 10.0% 10.0% 3.0%

30–34 22.0% 14.0% 14.0% 10.0% 7.0% 7.0% 7.0% 7.0% 7.0% 7.0% 2.7%

35–39 22.0% 11.0% 10.0% 10.0% 7.0% 6.0% 6.0% 6.0% 6.0% 6.0% 2.5%

40–44 20.0% 10.0% 10.0% 10.0% 7.0% 6.0% 6.0% 6.0% 6.0% 6.0% 2.5%

45–49 15.0% 10.0% 9.0% 7.5% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 2.5%50–54 15.0% 10.0% 9.0% 7.5% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 2.5%

55–59 15.0% 10.0% 9.0% 7.5% 5.0% 5.0% 5.0% 5.0% 5.0% 5.0% 2.5%

60 & over 12.0% 10.0% 9.0% 7.5% 5.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 17/24

APPENDIX B-3

JEA

Males durations

ages 0 1 2 3 4 5 6 7 8 9 ultimate

under 20 7.5% 6.0% 3.5% 3.5% 3.0% 3.0% 2.5% 2.5% 2.0% 2.0% 2.0%

20–24 7.5% 6.0% 3.5% 3.5% 3.0% 3.0% 2.5% 2.5% 2.0% 1.5% 1.5%

25–29 7.5% 6.0% 3.5% 3.5% 3.0% 3.0% 2.5% 2.5% 2.0% 1.5% 1.5%

30–34 2.5% 2.0% 2.0% 2.0% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5%

35–39 2.5% 2.0% 2.0% 2.0% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5% 1.5%

40–44 2.5% 2.0% 2.0% 2.0% 1.5% 1.5% 1.0% 1.0% 1.0% 1.0% 1.0%

45–49 2.5% 2.0% 1.5% 1.5% 1.0% 1.0% 0.5% 0.5% 0.5% 0.5% 0.5%

50–54 2.5% 2.0% 1.5% 1.5% 1.0% 1.0% 0.5% 0.5% 0.5% 0.5% 0.5%

55–59 2.5% 2.0% 1.5% 1.0% 1.0% 0.5% 0.5% 0.5% 0.5% 0.5% 0.5%

60 & over 2.5% 2.0% 1.5% 1.0% 0.5% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

JEA

Females durations

ages 0 1 2 3 4 5 6 7 8 9 ultimateunder 20 7.5% 5.0% 5.0% 5.0% 5.0% 5.0% 4.0% 4.0% 2.5% 2.5% 2.5%

20–24 7.5% 5.0% 5.0% 5.0% 5.0% 5.0% 4.0% 4.0% 2.5% 2.5% 2.5%

25–29 7.5% 5.0% 5.0% 5.0% 5.0% 5.0% 4.0% 4.0% 2.5% 2.5% 2.5%

30–34 7.5% 5.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 2.0% 2.0% 2.0%

35–39 6.0% 5.0% 3.0% 3.0% 3.0% 3.0% 3.0% 3.0% 2.0% 2.0% 2.0%

40–44 4.0% 3.0% 2.0% 2.0% 2.0% 2.0% 1.5% 1.5% 1.5% 1.5% 1.5%

45–49 3.0% 2.5% 2.0% 2.0% 1.5% 1.5% 1.5% 1.0% 1.0% 1.0% 1.0%

50–54 2.5% 2.0% 2.0% 1.5% 1.5% 1.5% 1.0% 1.0% 1.0% 1.0% 1.0%

55–59 2.5% 2.0% 1.5% 1.5% 1.5% 1.0% 1.0% 1.0% 1.0% 1.0% 1.0%

60 & over 2.5% 2.0% 1.5% 1.5% 1.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

6. Disability Incidence Rates: Probability of Disability

Within One YearAfter Attaining Age Shown

Age Male Female25 0.02% 0.01%35 0.04 0.0445 0.09 0.0955 0.24 0.22

7. Marital Status and

Spouse's Age: 65% of active members assumed to be marriedwith the male spouse 3 years older and femalespouses 3 years younger. No remarriages areassumed. Marital status of retirees is actual asreported.

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 18/24

APPENDIX B-4

8. Actuarial Value of Assets: Current market value adjusted by a 5-yearweighted average trend in actual yieldscompared to those expected, as described inAppendix C.

9. Growth Rate of FutureMembership Payroll: 3.5% per year.

10. Program Expenses: Previous year’s actual expenses.

11. Underlying Long-TermInflation Rate: 3.5% per annum, compounded annually.

Actuarial Cost Method To determine the Program’s contribution requirements, the Individual Entry Age

Actuarial Cost Method was used. Under this method, the cost of each member’s

projected retirement benefit is funded through a series of annual payments, determined

as a level percentage of each year's earnings from age at hire to assumed exit age. This

level percentage, known as normal cost, is thus computed as though the Program had

always been in effect. A yearly normal cost for each member is individually determined

by multiplying each member’s level percentage by the applicable yearly earnings, then

adding together to obtain the normal cost amount for the Program for that year. The

accrued value of normal cost payments due prior to the valuation date is termed the

actuarial accrued liability (AAL). This amount minus the actuarial value of assets is

known as the unfunded actuarial accrued liability (UAAL). The annual cost of a plan

has two components: normal cost and an amortization payment, which may vary

between prescribed limits, toward the UAAL.

An actuarial gain (or loss), a measurement of the difference between actual experience

and that expected based upon the actuarial assumptions during the period between two

actuarial valuation dates, reduces (or increases) the UAAL. This amount is amortized

over selected periods not greater than 30 years. Initially, a 30-year period is usually

chosen. Periodically, some or all of the remaining balance of any actuarial gain may

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 19/24

APPENDIX B-5

offset the remaining balance of a prior liability base, starting with the earliest base.

Similarly, any actuarial loss may be offset with the remaining balance of a prior credit

base or actuarial gain, starting with the earliest base. After all liability or loss bases have

been eliminated, remaining gains may be amortized over 10 years. Any remaining past

excess contributions may be used to offset payouts of normal cost and/or amortization

payments.

When plan amendments liberalize benefits or when actuarial assumptions are modified,

the difference in the AAL due to the changes is established as a supplement to the

UAAL amortized over 30 years from date of establishment, net of any negative UAAL

credits. To the extent that increases or losses occur that move the UAAL out of a surplus

position, negative outstanding bases will be used to offset such increases before any

new bases are established.

It is intended that each UAAL base be amortized over its specified period through

monthly contributions expressed as a level percentage of each month's payroll,

incorporating an assumption that future payroll will grow at the rate of 3.5% per year.

Payments are assumed to begin one year after initial recognition of the base, and

continue monthly for the remaining period of each base.

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 20/24

APPENDIX B-6

Miscellaneous Valuation Procedures

1. 100% of disabilities were assumed to be off the job.

2. No recovery from disability was assumed. Any differences in the liabilities due

to the probability of recovery for current and future disabled employees was

expected to be minor, and this simplification will tend to overstate somewhat

expected liabilities, thus producing a somewhat conservative result.

3. Covered payroll is the amount of total participating salaries paid from October 1,

2008 through September 30, 2009, for employees who are currently active

members in the Program. Valuation payroll is payroll expected to be paid during

the 2009-10 fiscal year, determined using covered payroll and the payroll growth

assumption.

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 21/24

APPENDIX C-1

CITY OF JACKSONVILLE

DISABILITY PROGRAM

TRUST FUND BALANCE AS OF 10/1/09

MarketValue

Receivable from City of Jacksonville General Employees Pension Plan 8,541,231$

Total 8,541,231$

Actuarial Value as of 10/1/09 9,981,282$

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 22/24

APPENDIX D-1

CITY OF JACKSONVILLE

DISABILITY PROGRAM

CURRENT PLAN MEMBERS

10/01/09 Members Actives

General 3,333

JEA 1,779

Total 5,112

DISABLED MEMBERS 10/01/09

Number Benefit

Disableds Receiving Payments - -$

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 23/24

APPENDIX D-2

CITY OF JACKSONVILLE

DISABILITY PROGRAM

DISTRIBUTION OF ACTIVE MEMBERS BY ATTAINED AGE AND

COMPLETED YEARS OF SERVICE AS OF 10/01/09

Completed Years of Service

Attained Age 0 1 2 3-4 5-9 10-14 15-19 20-24 25-29 30-34 35 & Over Total

Under 25 37 46 31 28 1 0 0 0 0 0 0 143

25-29 35 82 57 80 56 1 0 0 0 0 0 311

30-34 29 42 51 87 106 44 1 0 0 0 0 360

35-39 20 50 41 111 144 88 28 4 0 0 0 486

40-44 29 32 55 91 168 123 71 93 4 0 0 666

45-49 25 27 45 96 177 130 115 208 102 5 0 930

50-54 11 25 40 74 165 94 114 164 141 70 11 909

55-59 9 16 19 48 122 93 82 109 64 82 39 683

60 1 2 3 13 25 16 21 15 11 15 6 128

61 1 1 2 10 16 14 22 14 10 9 7 106

62 0 2 1 7 17 8 17 19 8 10 4 93

63 1 1 1 7 15 19 11 6 6 2 7 76

64 0 2 1 2 10 6 5 6 5 7 2 46

65 & Over 0 1 1 14 18 36 27 36 13 19 10 175

Total 198 329 348 668 1040 672 514 674 364 219 86 5112

Average Age at Entry = 34.5

Average Age at Valuation = 47.2

Average Years of Service = 12.7

8/3/2019 Jax Disability 09 Val Rpt

http://slidepdf.com/reader/full/jax-disability-09-val-rpt 24/24

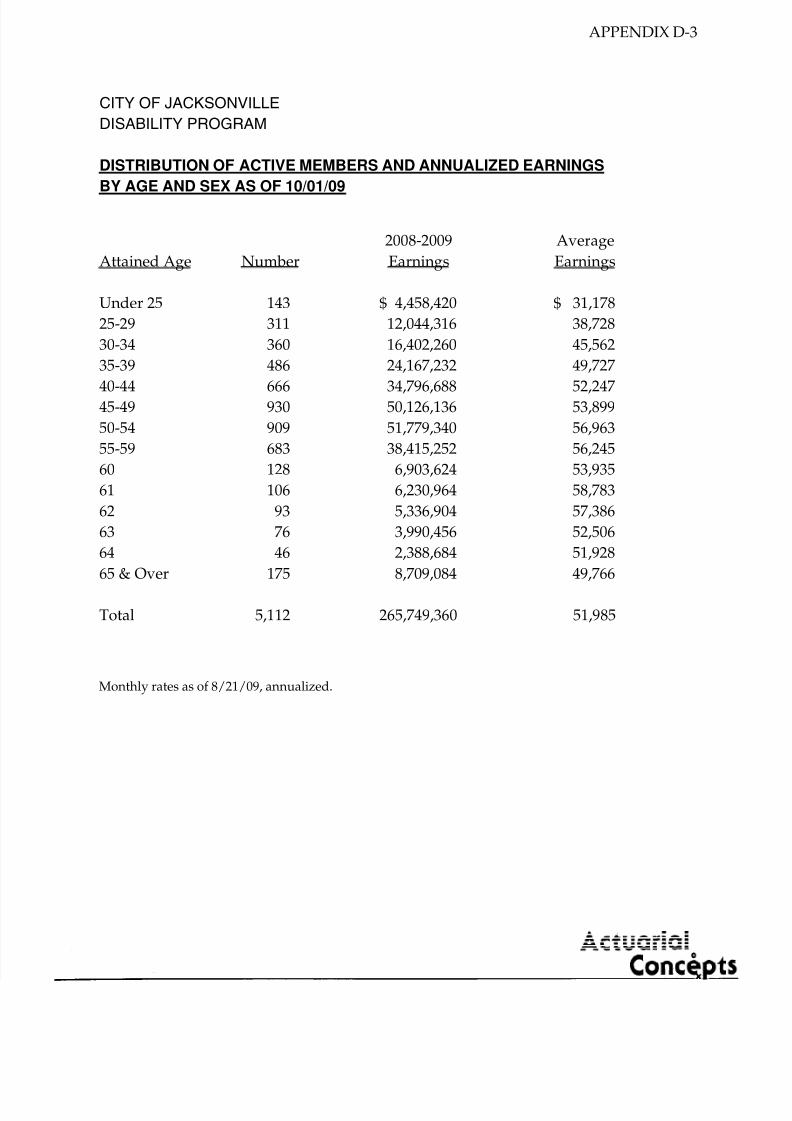

APPENDIX D-3

CITY OF JACKSONVILLE

DISABILITY PROGRAM

DISTRIBUTION OF ACTIVE MEMBERS AND ANNUALIZED EARNINGS

BY AGE AND SEX AS OF 10/01/09

2008-2009 Average

Attained Age Number Earnings Earnings

Under 25 143 4,458,420$ 31,178$

25-29 311 12,044,316 38,728

30-34 360 16,402,260 45,562

35-39 486 24,167,232 49,727

40-44 666 34,796,688 52,247 45-49 930 50,126,136 53,899

50-54 909 51,779,340 56,963

55-59 683 38,415,252 56,245

60 128 6,903,624 53,935

61 106 6,230,964 58,783

62 93 5,336,904 57,386

63 76 3,990,456 52,506

64 46 2,388,684 51,928

65 & Over 175 8,709,084 49,766

Total 5,112 265,749,360 51,985

Monthly rates as of 8/21/09, annualized.

![Loading [MathJax]/jax/output/CommonHTML/jax](https://img.pdfslide.us/doc/110x75/625335b291158e3f663c6c05/loading-mathjaxjaxoutputcommonhtmljax.jpg)