Embed Size (px)

Citation preview

JationalArchives

3—058—74—109 (A)

1969 Individual Tax Model

Documen tat ion

Washington,Dc2o48

*

Record Group 58

Records of the Internal Revenue Service

69 001NationalArchives and Records Adm in ist ration

CONTENTS

Taxpayers' income exceeded $600 billion, ILow-income taxpayers made increased use of head of household and surviving

spouse tax rates. 3Married persons filed separate returns mainly when both spouses had

income. 3Patterns of income virtually unchanged over 2-year pericxf. 4Nontaxable returnS, 5Dividends on 4.5 million returns tax free. 5W-2 Wage and Tax Statement provided. 6Income of men, women, and married couples, 7

rext tables1A Returns, income, and taxes. 1968 and 1969. 219 Number of returns by marital status and adjusted gross income classes.

1958 and 1969. 21C Separate returns of husbands and wives: Spouse filing status by adjusted

gross income classes. 41D Selected patterns of income by income category. 41E Nontaxable returns by adjusted gross income classes. 4iF Dividends by adjusted gross income classes. 510 Form W-2 and related data by adjusted gross income classes, 61H Selected sources of income by marital Status or sex of taxpayer, 7ii Joint returns with wages and other compensation from Form W-2: Wages of

husbands and wives by adjusted gross income classes. 7

Charts1A Cononents of income and relative change. 218 Change in number of returns, income, and tax. 1968-1969. 21C Change in number of returns by size of adjusted gross income, 1960-

1969, 310 Joint returns with husband's wages as a percent or total wages by

adjusted gross income class, 81E Wages and other compensation from Form W-2 by sex of taxpayer. 8

Basic tables1.1 Returns, adjusted gross income, taxable income, and income tax after

credits, by adjusted gross income classes and classes cumulated, 91.2 All returns: Adjusted gross income, total deductions, exemptions

taxable income, and income tax after credits, by adjusted gross incomeclasses and by marital status of taxpayer, 10

1.3 Alt returns: Sources of income and loss, by marital status of tax-payer, 12

1.4 All returns: Sources of income and loss, exemptions, taxable income,and tax items, by adjusted gross income classes, 13

1.5 Joint returns of husbands and wives and returns of surviving spouses:Sources of income and loss, exemptions, taxable income and tax items.by adjusted gross income classes. 17

1.6 Separate returns of husbands and wives and returns of single persons:Sources of income and loss exemptions, taxable income. and tax items,by adjusted gross income classes. 21

Section

Returns Filed anc

Sources of lncom

1.7 Returns of heads of households: Sources of income and loss. exemptiotaxable income, and tax items, by adjusted gross income classes. 2t

1.8 All returns: Sources of income and loss, exemptions. taxable income,and tax items, by adjusted gross income classes. 29

1.9 Nontaxable returns: Sources of income and loss, exemptions, taxableincome, and tax items, by adjusted gross income classes, 33

1.10 Returns with dividends by adjusted gross income classes. 371.11 Selected patterns of income: Returns and income by adjusted gross

income classes, 381.12 Retuths with capital gains or losses: Gains and losses by type, by

adjusted gross income classes. 401.13 Selected major sources of income and loss by adjusted gross income

classes, 431.14 Returns with farm net profit or loss: Sources of income and loss.

exemptions, taxable income, and tax items, by adjusted gross incorclasses. 45

1.15 Returns with farm net prof it or loss: Number of returns by size of farmand nonfarm income by adjusted gross income classes, 49

1.16 Returns with farm net profit or loss: Farm net profit or loss as a percaof adjusted gross income, by adjusted gross income classes. 53

1.17 Returns with pension and annuity income: Adjusted gross income. incrtax after credits, taxable and partially taxable pension and annuitycome, by adjusted gross income classes, 54

1.18 Returns with Form W-2: Adjusted gross income, salaries and wages, to-deductions, exemptions, tax items, and Form W-2 items, by adjustedgross income classes, 55

1.19 Nuner of Forms W-2 filed by marital status and adjusted gross incomeclasses. 61

1.20 Joint returns: Husband's wages as a percent of total Form W-2 wages.by adjusted gross income classes. 65

1.21 Male filers of non-joint returns: Sources of income and loss. exemptictaxable income, and tax items, by adjusted gross income classes. 6'

1.22 Female filers of non-joint returns: Source of income and loss. exemp-tions, taxable income, and tax items, by adjusted gross incomeclasses. 71

1.23 Exemptions and selected items by marital status and sex of taxpayeradjusted gross income classes, 75

TAXPAYERS' INCOME EXCEEDED $600 BILLION

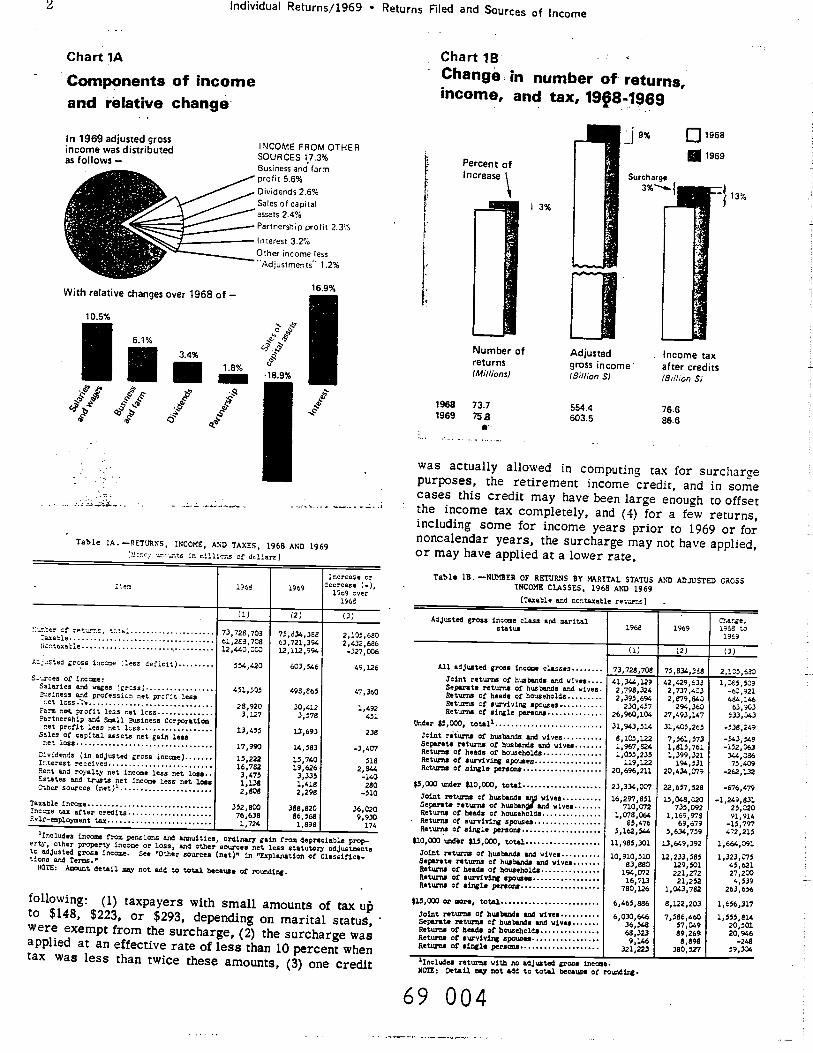

Taxpayers' adjusted gross Income reported on their1969 individual returns totaled $603.5 billion, increasingby $49.1 billion or 8.9 percent over 1968. Table lAand chart 1A show that most of the major sources ofIncome except net gain from sales of capital assets andnet Income from rents and royalties increased over1968 levels. Capital gains registered a sharp dropof 18.9 percent, contrasting markedly with the 31.5 per-cent increase for 1968 over 1967.

Income tax liability of individuals, labelled "incometax after credits" in table 1A and chart lB. totaled$86.6 billion for 1969. This was $10.0 bllllon.or 13 per-cent more than the comparable figure for 1968 and wasthe second largest single-year increase since the enact-ment of the Internal Revenue Code of 1954. The increaseIn tax liability was associated with three Important

developments delineated in chart 1B: (1) an increa- of 3 percent in returns filed, (2) an increase of 9 pe

cent In adjusted gross income, and (3) the extensionthe surcharge on income tax before credits to coythe whole of calendar year 1969.

A 49 percent increase in the surcharge was attri!table not grily to the Increase in income tax before credto which'he surcharge was applied but also to the i:position of the surcharge at the 10 percent ratethe' full year. For 1968, the .10 percent surcharge win effect for only the last 9 months of the year amountitin effect, to a 7.5 percent surcharge. For 1969, tsurcharge totaled $7.7 billion. This was less thanpercent based on the income tax before credits shothroughout this report, partly because only 52.3 miii:of the 64.2 million returns with tax before creshowed the amount of the surcharge. The smalnumber and also the smaller amount resulted from'

69 003

Individual Returns/1969 Returns Filed and Sources of Income

Chart 1A

Components of incomeand iëlative change

3.4%

R 1.8%5,I/i /

'.5,'9 '9 ':5'

INCOME FROM OTHERSOURCES 17.3%Business and farmprofit 5.6%Dividends 2.6%Sales of capitalastets 2.4%

• Partnership profit 2.3%

• Interest 3.2%

Other income less"Adjustments" 1.2%

Table LA.—RETIJRNS INCOME, AND TAXES, 1968 AND 1.969vnunts in rnllljcr,z of dcl].crsj

'.,,a. .- 1966 1969Ir,crease Cr

decrease I—),Uo9 over1966

..rler of ret"r.s, to.v1.

(1) 2) (3)

73,728,703 7234,3s 2,105,630

12,440,33263,721,39412,112,994

2,432,686—327,006

•to,_cted grosS income .esn deficit) 554,423 603,S46 49,126S..s'ces Of ir.come:

Selaries and wages 'gross)Stslness and profession cc'. profit lea, 451,005 498,860 47,360net lcss.'a

Farm net. profit less net loss 28,920 30,412 1,492

?artnershp and Small BusIness Ccrporation 3,578 451

net profit less set icesSales of capital assets net gain less

13,415 13,693 238

net loss17,990 14,083

Dovidends (in adjusted gross income)Interest received 15,222 15,740 518Sent end royalty net Income less net loss..

16,782 19,826 2,844Estates end trusts net income less net lossOther sources (net)1

3,4751,1382,808

3,3351,4182,298

—140280

—510

Taxable incomeIncome tax after credits 302,800 388,820 36,020

Selfemployment taI 1,72486,5681,898

9,930

'Includea income from pensions and annuities, ordizsay gain from depreciable prop-erty, other property income or loss, and other sources net less atatutorT adjustmentsto adjusted gross income. See "Other courses (net)" in 'Explanation Of Classifica-tions and Terms."SOTE: Auot detail may not add to total because of rounding.

following: (1) taxpayers with small amounts of taxufto $148, $223, or $293, depending on marital status,were exempt from the surcharge, (2) the surcharge wasapplied at an effective rate of less than 10 percent whentax was less than twice these amounts, (3) one credit

Adjusted gross income class and maritalstatus 1963 1969

Charge,lo8t5

All, adjusted gross income classesJoint returns of husbands and wives....Separate returns of husbands and wives.Returns of heads of householdsReturns of surviving spouses

(1) (2) (3)

73,728,70541,344,1292,798,3242,395,694230,457

70,834,36842,429,633

2,737,4132,579,643

294,360

2,105,620

1,065,509—61,921464,04663,903Returns of single persons 26,960,106 27,493,147 533,063

tinder $5,000, total.1Joint riturna of husbands and wivesSeparate returns of husbands end wivesReturns of heads of householdsReturns of surviving spousesReturns of

31,943,014

8,105,1221,967,8241,055,235119,122

31,400,265

7,561,5731,810,7611,309,321194,031

-538,249

54),549-152,563344,38675,409single persons 20,696,211 20,434,079 —262,1.32

$5,000 under $10,000, totalJoint returns of husbands ant wivesSeparate returns or husban and wivesReturns of heads or householdsReturns of surviving spouses

23,334,03716,297,851

710,0721,078,064

65,476

22,657,52815,068,020

735,0921,169,978

69,679

—676,479

—1,249,831.25,32091,914—15,797Returns of single persons 5,162,544 5,634,759 472,215

$10,000 w,dër $15,000, totalJoint returns of husbands and wivesSeparate returns of husbands and wivesReturns of head. of householdsReturns of surviving spouses

11,985,301

10,910,51083,880

194,07216,71.3

13,649,392

12,233,585129,501221,27221,252

1,664,391

1,323,07045,62127,2104,539of singl, persons 780,126 1,063,782 263,656

$15,000 or more, totalJoint returns of husbands sod wivesSeparate returns of husband. Snd wivesReturns of heads of householdsReturns of surviving 5pOUBUReturns of

6,465,886

6,030,64636,04868,3239,146

5,122,203

7,586,46057,06989,2698,898.

1,656,317

1,555,81420,50120,966

-248

'Includes returns with no adjusted gross income.NOTE: Detail y not add to total because of rounding.

In 1969 adjusted grossincome was distributedas follows —

Chart 18Change. in number of returns,income, and tax, 198-i969

9% 1968

1969

With relative changes over 1968 of —

13%

Percent ofIncrease

IiNumber ofreturns(Millions)

1968 73.71969 758

13%

]Adjustedgross income(Billion Si

554.4603.5

Income taxafter credits(B'i/ion S1

76.686.6

was actually allowed in computing tax for surchargepurposes, the retirement income credit, and in somecases this credit may have been large enough to offsetthe income tax completely, and (4) for a few returns,including some for income years prior to 1969 or fornoncalendar years, the surcharge may not have applied,or may have applied at a lower rate.

Table 18. —NUMBER OF RETURNS BY MARITAL STATUS AND ADJUSTED CROSSINcoME CLASSES, 1968 AND 1969

I Taxable and ncctaxable returns) -

69 004

Individual Returns/1969 • Returns Filed and Sources of Income

Chart 1C

Change in number of returns by sizeof adjusted gross Income, 1960-1969

Millions of returns

80— -

70 ___________________________

60

410r-

2C

15

10

5

Returns $5000 under $10000——

I0 i I4Cr

LOW-INCOME TAXPAYERS MADE INCREASEDUSE OF HEAD OF HOUSEHOLD AND

SURVIVING SPOUSE TAX RATES

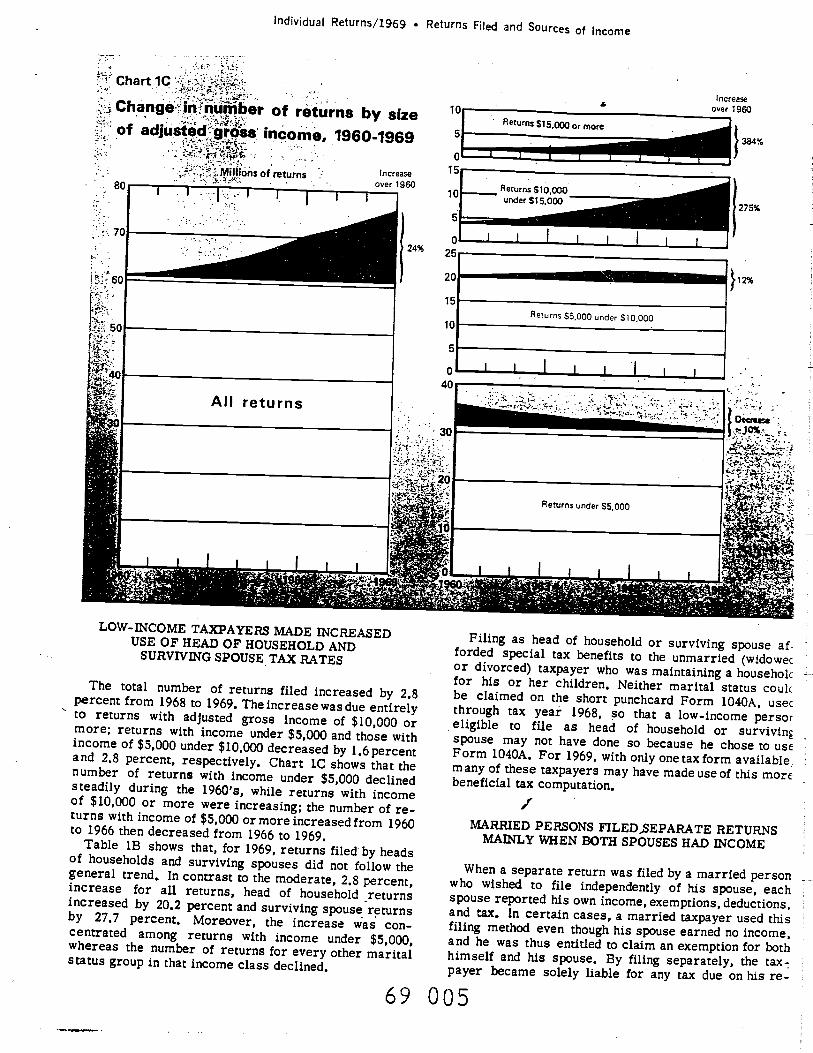

The total number of returns filed increased by 2.8percent from 1968 to 1969. The Increase was dueentirelyto returns with adjusted gross income of $10,000 ormore; returns with income under $5,000 and thosewithincome of $5,000 under $10,000 decreased by 1.6 percentand 2.8 percent, respectively. Chart IC shows that thenumber of returns with income under $5,000 declinedsteadily during the 1960's, while returns with incomeof $10,000 or more were increasing; the number of re-turns with income of $5,000 or more increasedfrom 1960to 1966 then decreased from 1966 to 1969.

Table 13 shows that, for 1969, returns filed by headsof households and surviving spouses did not follow thegeneral trend. In contrast to the moderate, 2.8 percent,increase for all returns, head of household returnsincreased by 20.2 percent and surviving spouse returnsby 27.7 percent. Moreover, the increase was con-centrated among returns with income under $5,000,whereas the number of returns for every other maritalstatus group in that income class declined.

Filing as head of household or surviving spouse af-forded special tax benefits to the unmarried (widowecor divorced) taxpayer who was maintaininga househokfor his or her children. Neither marital status coulcbe claimed on the short punchcard Form 1040A, usecthrough tax year 1968, so that a low-income persoreligible to file as head of household or survivingspouse may not have done so because he chose to useForm 1040A. For 1969, with only one tax form available,many of these taxpayers may have made use of this morebeneficial tax computation.I

MARRIED PERSONS FILEDSEPARATE RETURNSMAINLY WHEN BOTH SPOUSES HAD INCOME

When a separate return was filed by a married personwho wished to file independently of his spouse, eachspouse reported his own income, exemptions, deductions,and tax. In certain cases, a married taxpayer used thisfiling method even though his spouse earned no income,and he was thus entitled to claim an exemption for bothhimself and his spouse. By filing separately, the tax-payer became solely liable for any tax due on his re-

0

-.-I'- I•

Increase

-;I. j I

overl96O

:-- II

Increaseover 1960

384%

25

•1All returns

:-

• •• z•• .

Returns under S5,000

I I

69 005

individual Returns/1969 • Returns FiJed and Sources of Income

able l,C.—SEPARATE RETURNS OF HUSBANDS AND

BY SPOUSE-FILING STATUS AND BY ADJUSTED GROSS INCOME CLASSES

jostedgro0r.C0neC1e5 turnsSoefilir.g

sosenot filing

6:0CC tctal

a5le ret_Cr.S, totaler$l,...0

52.0033,0OO

033:0 ..-.0er $4,000ur.Oe: 5,0OO

$4,000:30 order 87,Ccx

ev: orOer 5.3,030s,::0 ..-jer $9,03039, 333 .nOnr $10,003

onCe: $15,000r0e: $20,000

on3er $25,000$25, 333 •o.0e: $33,300533:30 rer $50,000

under $100,030order $2300,030

30,33.. er 5so3,C00000.033 orOer $1,003,000

5:, Cr OCTC

r.taxalle returns, total,, uoted g° OtCOle

$..33 'er $1,330$1,300 coder $2,003

0303 u-Ocr $3,000$3,300 under $4,000$4063 under $5,000$5,330 Cr more

Returr.5 under $5,000Return.. $5,000 under $10,000Returns $10,000 under $15,030Returns $15,000 or more

(1) (2) (3)

2,737,403 0,348,307 369,066

2,152,742 1,946,376 206,366

42,896252,650291,232365,837291,080

240,035160,134136,303111,72470,333

129,02129,05711,1195,3257,684

2,1174o72134738

41,231230,602271,405325,44.4

260,623

225,550140,777120,59699,20863,239

117,56625,8139,6604,5387,129

2,1411.08

1934437

(')22,04319,82740,39330,407

19,48519,35715,70712,516(•)

11,4553,1791,439737555

336352331

024,601 401,931 182,730

17,243 13,220

122,295 109,714125,324 38,490176,097 115,20573,123 38,43437,997 18,40819,987 9,81912,595 8,641

(—)

12,58136,83460,89234,68919,58914 122

1,815,761 1,022,595 293,166735,092 657,212 77,830

129,501 117,845 11,656

57,049 50,655 6,334

(.) An asterich in a cell, denotes that the estimate is nOt sho,n separately beca.,seCf 5.056 sanplthg variab1ity. However, the data are included on the appropriatetCla1o'

Table OD.—.SELECTED PATTERNS

(Money aS000ts in

1Adjusted groms income lees deficit.

69 006

turn, and solely eligible to receive any refunds. How-ever, unless his taxable income was under $500, heended up being taxed at a higler rate than if he hadelected joint return filing status.

For the first time, on the 1969 Form 1040, the tax-payer filing a separate return was supposed to checka special box to indicate whether or not his spouse wasalso filing. Table 1C shows that of the 2.7 million re-turns of married persons filing separately for 1969,only 0.4 million indicated that the spouse was not alsofiling.

PATTERNS OF INCOME VIRTUALLY UNCHANGEDOVER 2-YEAR PERIOD

In classifying a return for patterns of income tables,each source of income reported was classified as be-longing to one of four categories. The four categoriesused in classifying the returns were salaries andwages, business income, income from sales of property,and all other income (mainly from investments).

As shown in table 1D, somewhat more than half ofall returns for 1969 showed only one category of income,and, as expected, in the vast majority of cases it wassalaries and wages. Roughly one-third of the returnsshowed two categories of income and these usually in-cluded salaries and wages and "all other income,"which encompasses interest and dividends. Table 1,11

OF INCOME BY INCOME CATEGORY

thousands of dCllftr.1

Income categoryTotal, all

returns

(1)

One Two 5.ree Fourcategory categor5es

(2) (3)

categories(4)

categorIes(5).81 OF RET'JRNS

Totals, all income categoriesSalaries ad wages (gross)B0500eos net income or 1ossSales Cf property net gain or baa2Other saurces (net)'

75,834,388

67,855,186

10,612,0159,355,2E3

36,649,276

39,039,584

35,445,448

1,038,6879,259

2,596,190

26,686,037

23,644,650

3,172,898

1,854,38724,301,139

8,223,966

6,930,787

4,166,129

5,457,3367,917,646

-1,834,301

1,834,3011,834,301

1,834,3011,334.301.

Totals, all income categoriesSalur005 and Iges (gross)uoineos 'et income or 10551Sales of property net gain or l05sOther source. (net)3

610,660,027498,864,69647,682,04214,635,59649,276,194

234,927,680 245,299,683

191,512,528 208,786,714

4,547,392 14,274,190

23,240 2,313,395

8,844,,520 j 19,925,384

117,988,68276,658,73420,433,312

6,731,86714,114,769

42,244,43221,936,719

8,377,1485,567,0946,393,521

11r.c1'ldes business or profession, fare, partnership md SaaU Business Corporation net profit or net loss.2Includes gain or loss from sales of capital assets, &i5 from sales of depreciable property, and gain or loss from sales of property other than capital assets'3lncludes dividends in adjusted gross thc, interest received, rent, royalty, estate and trust, net income or net loss, pension

and annuities, other sources net income or loss,

and income or 5,oss not allocable.'Entries in this portion of the table do not overlap, as an example, for the 23,644,650 returns with salaries and wages and one other income

category, the total amount of

salarIes and wages of these returns was $2Ce,786,72.4,.

Table IC. —NONTAXABLE RETURNS BY ADJUSTED GROSS INCOME CLAS(ES

(Money amounts in thousandS of dollars) __________ _________

Adjusted gross income classesNumber

returns

(1)

Adjusted

(2)

I -'deductions

(3)

Exemptions

Number AmoISlfl

(4) (5)

bl

(6) (7)

remSurcharge credits

(3) (9)

8,Total

Under

$5,000 under $10,

$10,000 under $15,000

$13,000 or more

12,132,934 1l5;376,575 8,103,384 28,976,996 17,386.198 665,758

240,278

128,966

33,8l 3.66 34,03911,708,2

364,981

23,993

13,998

112,,6,126

2,288;967

283,232

738,270

6,1,15,772 26,563,

976,818 2,251,529

219,740 1,200791,053 59,667

5.5,938,160

1,350,917

61,320

33,800

224,740

66,759

133,981

34.861 2,097 36,960

11,904 1,,l47 13,220

4,393 67O4 53

Individual Returns/1969 • Returns Filed and Sources income

presents data for each of the fifteen combinations ofone to four categories of income. It shows virtuallyno change in the percentage distribution of returnsover the fifteen patterns of income since 1967, the lastyear for which such data were presented.

NONTAXABLE RETURNS

Characteristics of nontaxable returns are summa-rized in table IE. About one of every six returns wasnontaxable, that is, the returns showed no income taxafter credits for 1969. About 97 percent of these returnsindicated adjusted gross income under $5,000. Thedollar amount of exemptions on nontaxable returnswith adjusted gross income under $5,000 exceeded theadjusted gross income, indicating that many of theselower income taxpayers had less than $600 of income foreach exemption to which they were entitled.

Table 1E also shows that, for taxpayers with incomeof $15,000 or more who paid no income tax, total de-ductions exceeded adjusted gross income. Some tax-payers reported deductions in excess of their incomein order to qualify for the charitable contribution carry-over. The carryover provision allowed taxpayers to"use up" in any of the 5 succeeding years that portionof their contributions to certain charitable institutionswhich could not be deducted in the current year, pro-vided they were within the percentage ceiling limitationfor each year.

More detailed information on nontaxable returns isshown in basic table 1.9. It shows that the 12.1 millionnontaxable returns consisted of 0.5 million returns withno adjusted gross income, 11.2 million returns withpositive, adjusted gross income which was fully offsetby personal deductions and exemptions, and 0.5 millionreturns with taxable income but with the tax offset bycredits. Tax credits Included those granted on retire-

ment income for certain types of investments, andtaxes paid to foreign covernments.

While nearly all nontaxable returns showed moclevels of income, there were also 745 returns that sho'adjusted gross income of $100,000 or more. Totaljusted gross income on these high income retuamounted to $338.0 million. The major reason for tnontaxability was the $432.1 million of personal dedtions reported. Data published for tax year 1968,last year for which we tabulated deductions by trevealed that over half these deductions resulted f:contributions to charitable, religious, and educatiorganizations. Personal exemptions totaled $1.6 mufor 1969. Only $295.9 million of these deductionsexemptions were subtracted from adjusted gross incin the computation of taxable income. The amountover was in excess of adjusted gross income and cnot be used (althoughsomeofthecharitable contributin excess of income may have been carried over andin a later year). After deduction of these amoupts,of these high-income returns had no taxable income90 had taxable income of $42.1 million in aggreg

On the 90 nontaxable returns with taxable inccincome tax before credits of nearly $27.8 millionassessed as well as the additional surcharge wtotaled $2.8 million. These assessments were, hoveriore than offset by $30.7 millionof statutory tax creof which the major type, the credit for tax paidforeign government, amounted to $29.2 million.

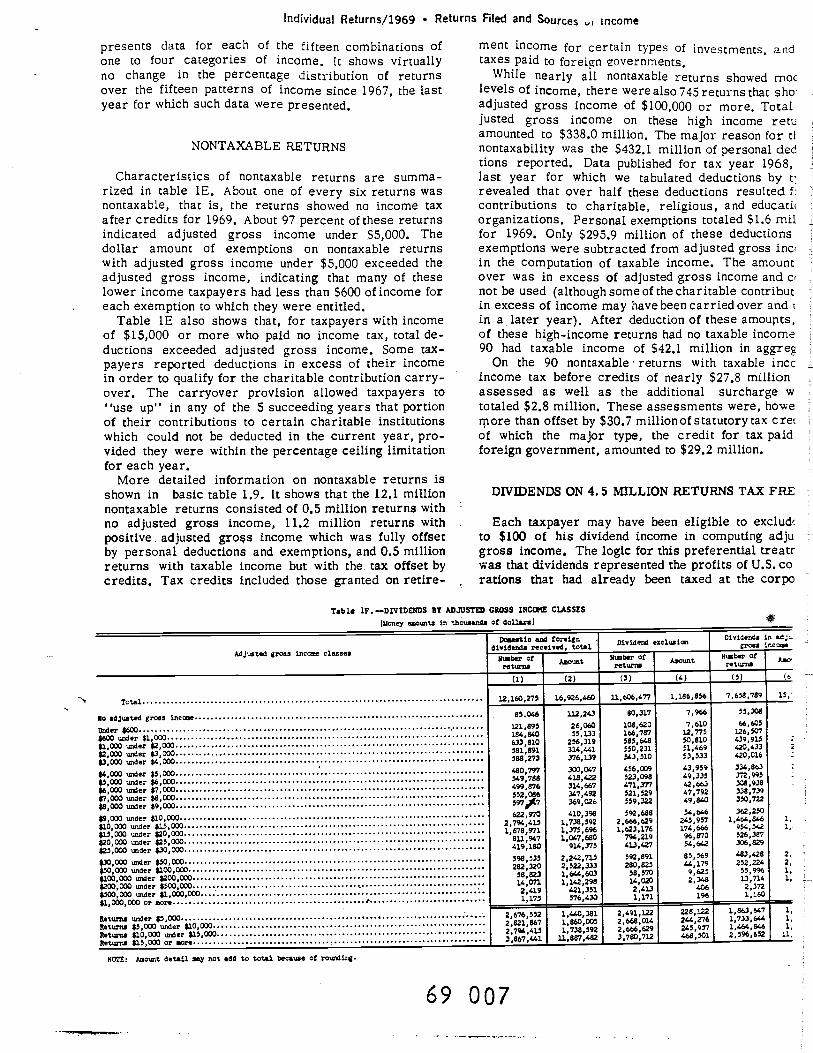

DWIDENDS ON 4.5 MILLION RETURNS TAX FRE

Each taxpayer may have been eligible to exclud'to $100 of his dividend income in computing adjugross income. The logic for this preferential treatrwas that dividends represented the profits of U.S. corations that had already been taxed at the corpo

NOlE: 4ouni detail —•. not •dd to total. becauSe of rounding.

Tabi. iF. —DiVIDENDS BY ADJUSTED GROSS INC CLASSES(one3r eounts in thoujindi of doUazsJ 4

69 007

Mjuated gross ince clenneS

tiC - foreigndividends receiv.d. total Divid od . i°

Ncb.r of

Dividends ingros inc

Ntb.D 0*N,b.zreturns return. A,o1nt Mc-return.

Total

Mo adjusted gross in

(1) (2) (3) (4) (5)

7,638,789 15,'72,160,275 16,926,1.60 iioo'n 1,186,856

85.046 112,243 80,317108,620

7,9667,610

13,30866,605

Under $600$600 under $1,000

$2, under $3,000$3, under $4,000$4,000 under $5,000s,000 wer $6,

$6,000 under $7,000uz,aer

$8, under $9,000

121,895184,840633,810581,891588,273480,797549,788499,876552,086597$7

55,3.33256,319314,441376,139300,04743.8,422314,667347,492369,026410,398

166,787585,648550,231543,53.0

456,009523,098471,377521.529559,322592,688

12,77550,81051,46953,53343,95949,33542,66347,79249,84054,646

126,507439,915420,433420,016

334,863372,995308,938338,739350,722

362,250$9, under $10,000$10,000 under $15,000$15,000 under $20,$20,000 under $25,000$25, under $30000$30, ner $30,000$50,000 under $100,000$100,000 under $200,000$200,000 wtder $500,000$500,000 under $l,,000$1,000,000 or sore

R,etwna under $5,000Returns $5, under $l.0,Returns $l.0, ,z,der $15,000Returns $15,000 or .ors

2,796,4131,678,971

811,967419,180598,535282,32058,82,314,0712,4191,175

1,738,5921,375,6961,047,680

914,3752,242,7132,522,3331,844,6031,142,298

421,351576,430

2,666,6291.623,176

794,219413,427592,891280,825

58,57014,0202,41.31,171

245,957174,66696,87054,64285,56944,1799,6252,348

1.06196

1,464.846 1,954.542 1,526,387306,829483,428 2,252,224 2,

55,996 1,13,714 1,2,3721,160 —

2,676,5522,821,8672,796,4133,867,441

1,440,3811,860,0051,738,592

11,887,482

2,491,1222,668,0162,666,6293,780,712

228,122244,276245,957468,301

1,863,647 1,1,733,644 1,1,464,846 1,2,596,652 11,

Individuat Returns/1969 • Returns Filed and Sources of Income

Table 1G. —SELECTED CHARACTERISTICS OF RETUR%S 145TH ECRM 14-2 ATTACHED BY ADJ1.JSTEO GloSS 11C055E CIASOES

[Taxable and osotaushlO to-nc; o.o.:.cyae:usts in tI;000a.;S :" Ocilurs)

A.00S1ed gross incomeclo.sSes Iirsbor of

returns

I

Adjustedgrossir.come

Salarie ad age

lumber ofreturns disGust

moose taxafter

credits

I to.)' tt

butler Cfretorts At.'"'

C a t-a ._—na

a —

a_nd n.)ter . Sto.a net txos

000pc-r.sat:or.2tX ._ ._—.C

200rlf ,3000f

(3) () (10) (11)

5,7D3,5;5 492,243,227 45,435,901ag1,tld

retns

Ittal3',dor $',030

$5,::: onler 910,203...

$10,330 onOer $15,000..

915,303 or sore

(1) (2) (3) (4) (5) () (2) (:3,

66,701,493 535,202,513 66,6,259 493,740,255 74,736,365 45,053,719 75,169,311 e2,t':,63_

25,393,391

20,303,505

12,521,922

7,092,712

5S,O,295

155,145,349

156,770,219

165,222,450

25,045,299

20,794,315

12,917,125

7,037,17

57,997,392

149,909,153

150,á7O,2t

135,243,33s

4,262,151

17,129,042

20,41.0,367

32,995,347

25,247,362

23,721,223

12,522,509

7,2e3,024

6,956,324 25,333,133 d,122,316 6,ddd,224 24,424,22

2C,477,6 23,933,535 149,553,569 23,072,221 23,323,311 :3,234,333

22,775,34 .2,521,456 150,333,322 :2,357,217 22,922,30: :2,305,046

24,75,24' 7,552,436 134,230,022 7,303,247 24,d:s,9:.6

2,627,237

'o,'_do,363

5,1'2,SC'.

2,133,324

°:rcl_dex excess social socurity taxes withheld.23 malL number of returnS (499) had wages of other somper.oaticn suteot to 1306 but 030 XuloCt to. tt'O . 306300004 Cf ur.cone tax.

level. Dividends from foreign corporations were noteligible for the exclusion. In the case of a husband andwife filing a joint return, each spouse could exclude upto $100 of eligible dividends.

Table iF shows that $1.2 billion of the $16.9 billionof dividends reported on tax returns were excluded fromadjusted gross income. Of the 12.2 million taxpayersreporting such income, 4.5 million excluded the entireamount, indicating that their total dividend income wasless than the allowable exclusion.

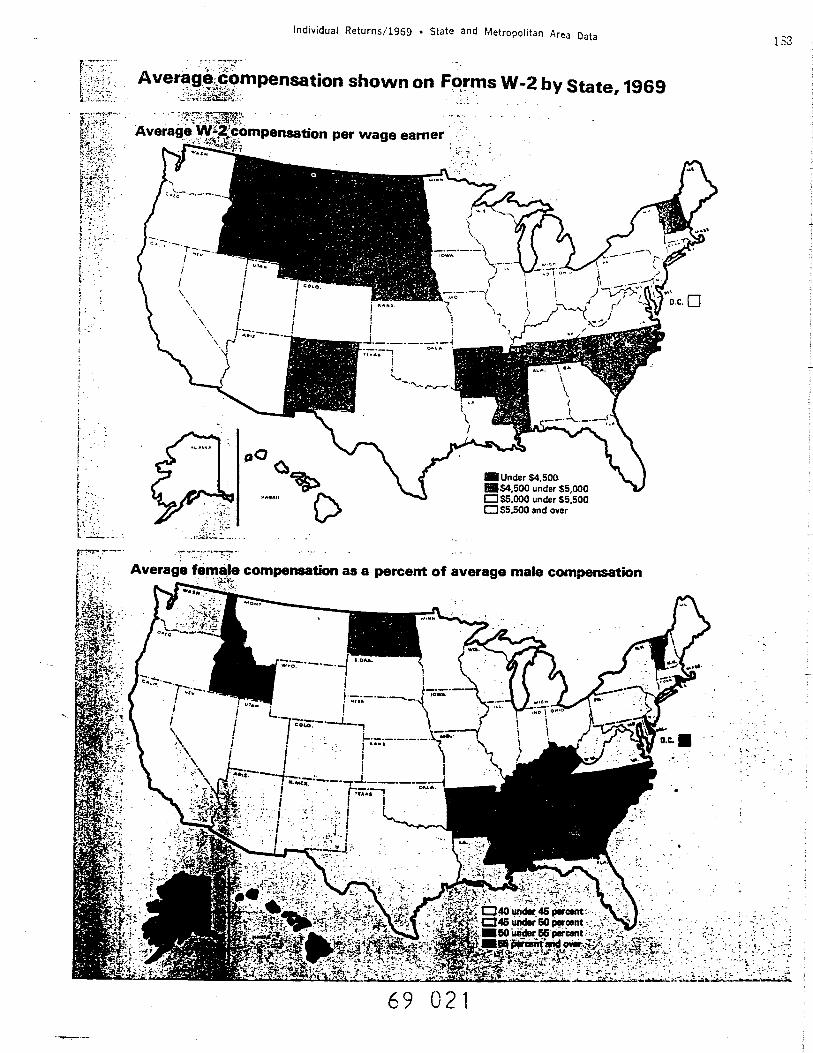

W-2 WAGE AND TAX STATEMENT PROVIDED

Tabulations of items shown on Form W-2, the wage andtax statement supplied by the employer, are included inthis report.

Table 1.19 shows that 130.3 million Forms W-2 wereattached to 66.7 million returns, an average of two perreturn. Thirty-two million returns, or 48 percent, hadone Form W-2 attached to the return. About 19.5 millionreturns, or 29 percent, had two Forms W-2 and the re-maining returns, 15.2 million--23 percent of the total--had three or more W-2's per return. Joint returns ac-counted-.for a much higher proportion of multiple FormsW -2 '(62 percent) than nonjoint returns (39 percent) re-flecting the employment of both husband and wife andmultiple jobholding by one or both spouses. The latteris more clearly indicated by joint returnswithmore thantwo Forms W-2 attached. Of the total joint returns withForms W-2 attached, 38 percent indicated one W-2, 34percent indicated two W-2'� and 28 percent indicatedmore than two W-2's. In contrast, 61 percent of non-joint returns had one Form W-2; 23 percent, two; and16 percent, more than two.

Employers issued Form W-2 to their employees toindicate:

(1) the amount of wages paid subject to withholdingfor Income tax as well as other employee compensation;

(2) the amount of Federal income tax withheld;(3) the amount of social security taxes (FICA)

withheld on wages covered by social security.

Employees in turn were required to file this form withtheir tax return and to enter the amounts of wages,other compensation, and income tax withheld on the re-turn. Columns 8 through 13 of table IC show theseamounts tabulated along with the associated returncounts.

The wages subject to withholding and, as explainedbelow, most of the other compensation shown on FormsW-2 were to be entered by taxpayers as salaries andwages on Form 1040. Income tax withheld was enteredas such on the return. Columns 1 through 7 of table IGshow amounts tabulated from Forms 1040 to whichForms W-2 were attached. The amounts of salariesand . wages and income tax withheld, taken from Form1040, were closely related to the corresponding amountsof wages and other compensation, and to income tax with-held, taken from Form W-2.

Although approximately equal, the salaries and wagesfrom the return and the attached Form W-2 statementwere not entirely comparable. Form 1040 salaries andwages included all salaries and wages whether or notsubject to withholding except tax-exempt salaries earnedabroad. They also included directors' fees, bonuses,and excess reimbursement for employee travel ex-penses. Form W-2 wages did not include wages paid toemployees of foreign governments or international or-ganizations, wages paid to agricultural laborers, andwages paid to household employees because none ofthese were subject to tax withholding. (Agriculturallaborers and household employees were subject towithholding of social security taxes, however, and arethus included in the FICA tax data.) In addition, FormW-2 sometimes included tax-exempt salaries and wagesearned abroad. /

Other compensation, which is combinedwithFormW-2wages in column 9 of table 1G. included commissionspaid to certain self-employed individuals, travel allow-ances, and employer payments (to the extent that theywere not tax exempt) toward their employees' lifeinsurance. On separate returns of husbands and wivesin community property States, W-2 income and taxwithheld were often twice the amounts entered on thereturn, since each spouse reported only one-half thecouple's combined wages on his or her return.

9 OO

Individual Returns/1969 • Returns FIed and Sources of Income

Table IH. —SELECTED SOIRCES OR INCOME BY MARITAL STATUS OP. 9(5 ' TAXPAYER

rs ,. t:._ Cou.S 11' retltrr.C; ..r.ty •t5 in :.ll1ir.s o: 4cflsrs.

Seletud sn..rces of joenne211 rCtunc

IC.ir.t returnsuf husban4s end

. , Flelw-n7.lCr Arsur.t luster JO S'usl Colt luster kuC'.lt 1:_nIne

A3usted gr005 inosnu (less th:ficit)

(1) )2) (3) (4) (5) () ) (3) :9,

75,424 42,430 470,952 33,405 122,193 17,253 43,44 '047 44

Sslerles 0o2 .'uec (4rsnc) 67,455 4,043 35,107 3*9,790 27,245 123,104 15,937 43,232 33(11 45

Business orSet zrcfitlet loss

4,171,171

33,53.1

2,7204,114

95230,0262,195

793223

3,096505

442129

2,311331

211

475

Fern:let profItlet 14_

1, 3'/1,155

6,1422,563

1,1351,112

.

5,43*2,247

382143

714279

24390

441176

3.2913

Sales Cf ospetal lends:let gainNet lcss

Oividen43 in 53Jus1n3 frell in.:r.e

Interest receilo2PensIons e.-.d o:.vlitles (toxatle pcr'.inn)

s,'l2,1117,01532,33.2

3,244

u.3741,4331,4J4,olv4,918

0,"791,5914,77021,2942,015

12,4441,3.39,72412,5734,710

1,776512,2$s13,4331,229

3,195379

5,5199,7222,164

74429393

4,11148

1,2932:3

1,5232,117

743

1,3252o1

1,7284,322

241

:

-.1

Estates 2r_ntn;Bet insureNetlsso

1,7Id,

1,40542

21324

74243

21416

7432s

245

1514

14.411

BITE: iC't1 no:. I_t Oto 10 'LIaL

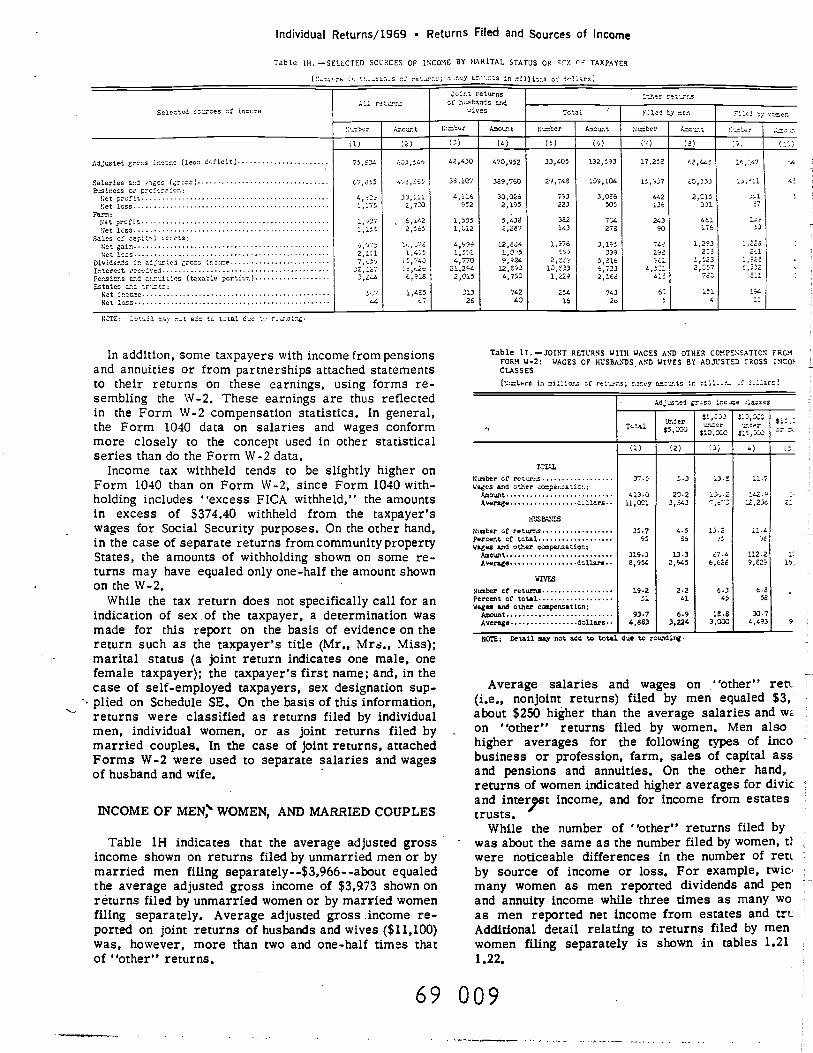

In addition, some taxpayers with income from pensionsand annuities or from partnerships attached statementsto their returns on these earnings, using forms re-sembling the W-2. These earnings are thus reflectedin the Form W-2 compensation statistics. In general,the Form 1040 data on salaries and wages conformmore closely to the concept used in other statisticalseries than do the Form W-2 data.

Income tax withheld tends to be slightly higher onForm 1040 than on Form W-2, since Form 1040 with-holding includes ''excess FICA withheld," the amountsin excess of $374.40 withheld from the taxpayer'swages for Social Security purposes. On the other hand,in the case of separate returns from community propertyStates, the amounts of withholding shown on some re-turns may have equaled only one-half the amount shownon the W-2,

While the tax return does not specifically call for anindication of sex of the taxpayer, a determination wasmade for this report on the basis of evidence on thereturn such as the taxpayer's title (Mr., Mr.,., Miss);marital status (a joint return indicates one male, onefemale taxpayer); the taxpayer's first name; and, in thecase of self-employed taxpayers, sex designation sup-plied on Schedule SE. On the basis of this information,returns were classified as returns filed by individualmen, individual women, or as joint returns filed bymarried couples. In the case of joint returns, attachedForms W-2 were used to separate salaries and wagesof husband and wife.

INCOME OF MEN, WOMEN, AND MARRIED COUPLES

Table 1H indicates that the average adjusted grossincome shown on returns filed by unmarried men or bymarried men filing separately- -$3,966- -about equaledthe average adjusted gross income of $3,973 shown onreturns filed by unmarried women or by married womenfiling separately. Average adjusted gross income re-ported on joint returns of husbands and wives ($11,100)was, however, more than two and one-half times thatof "other" returns.

Table 11.—JOINT RETURNS WITH WAGES AND OTHER COMPENSATION FROMFORM W-2: WAGES OF HUSBANDS AND WIVES BY ADJtISTED CROSS 115007CTSSES

(lusterS in oil.llons of rnI'_nr.S; n.snvy az:'.r.ts .0 L11.to I s.ars

,

A43ssted gras sr.e.ce ..a4sos

.eceal 11.3cr- -$5,o20

I,112._.r

530,030.o'._er

*11,33

did.:

TCV,L

(1) (2) (3) :) (5,

Ns.,ber of returns 37.5 5.3 13.9 11.7Wages and Other 4csper.catio:.:

f,asunt 413.0 23.2 124.2 1.42.9 I.

Average u.1ars.. 11,031 3,443 1,c' 1.2,234 11

W,DSINsaber of returr.s 37.7 4.5 13.2 11.4Percent of total 95 56 5 75Wages and other cccper.satEsr.:

Amount 319.) 1.3.3 47.4 11.2.2 31

Average dollars.. 8,954 2,945 6,626 9,227 19,

WIVES

Bomber of returns 19.2 2.2 4.3 4.9 .percent of total. 11 41 41 56

Wages and othe cpenSation:Amount 93.7 6.9 19.8 30.7Average dollars.. 4,683 3,224 3,003 4,493 9

NOTE: DetaIl. 553 not add to total due to rundlng.

Average salaries and wages on "other" retL(i.e., nonjoint returns) filed by men equaled $3,about $250 higher than the average salaries and woon "other" returns filed by women. Men alsohigher averages for the following types of incobusiness or profession, farm, sales of capital assand pensions and annuities. On the other hand,returns of women indicated higher averages for divicand inter,pst Income, and for Income from estatestrusts.

While the number of "other" returns filed by- was about the same as the number filed by women, ti

were noticeable differences in the number of retlby source of income or loss. For example, twicmany women as men reported dividends and penand annuity income while three times as many woas men reported net income from estates and trtAdditional detail relating to returns filed by menwomen filing separately is shown in tables 1.211,22.

69 009

Individual Returns/1969 • Returns Filed and Sources of Income

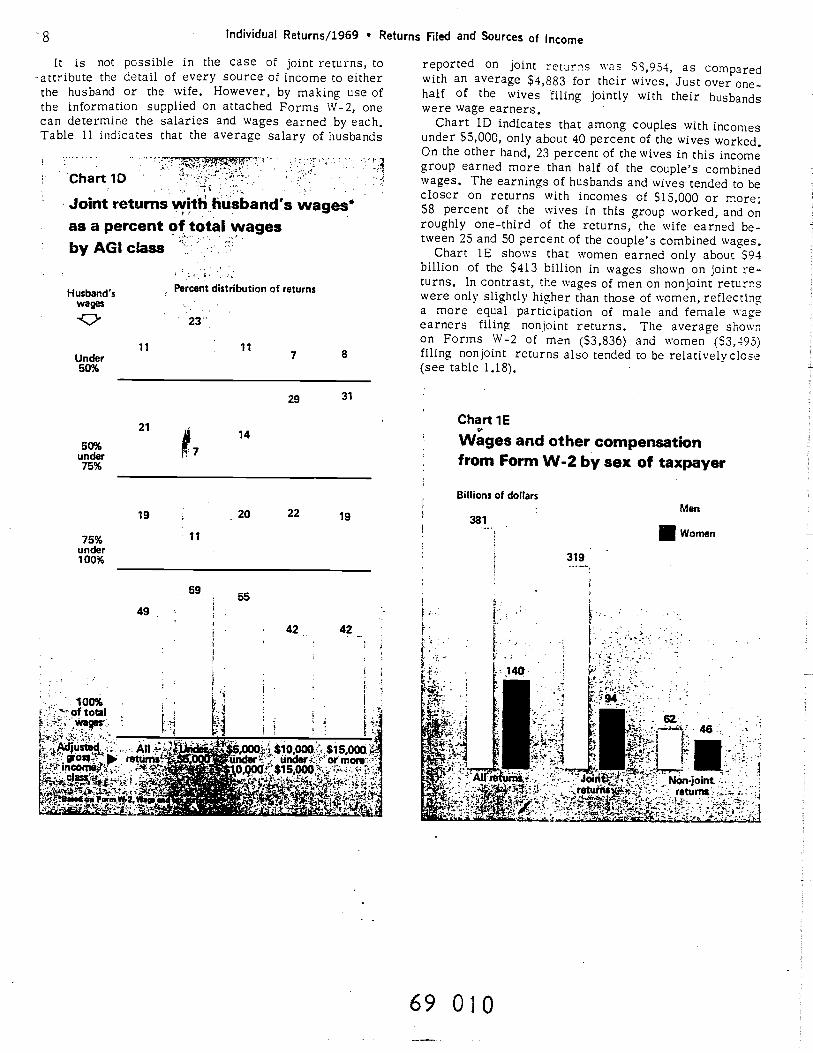

It is not possible in the case of joint returns, toattribute the detail of every source of income to eitherthe husband or the wife. However, by making use ofthe information supplied on attached Forms W-2, onecan determine the salaries and Wages earned by each,Table 11 indicates that the average salary of husbands

..

ChartiD

Joint returns witl husband's wages*as a percent of total wagesby AG1 cEass

Under 7 8

50%

29 31

50%under

21

,,

14

75%

19 20 22 19

75% •11under100%

59. 55

H 42 42,

••

• -

::100%

oftotalI.

,

Ii ii .: ,.

reported on joint returrs was S,954, as Comparedwith an average $4,883 for their wives. Just over one-half of the wives filing jointly with their husbandswere wage earners.

Chart 1D indicates that among couples with incomesunder $5,000, only about 40 percent of the wives worked.On the other hand, 23 percent of the wives in this incomegroup earned more than half of the couple's combinedwages. The earnings of husbands and wives tended to becloser on returns with incomes of $15,000 or more;58 percent of the wives in this group worked, and onroughly one-third of the returns, the wife earned be-tween 25 and 50 percent of the couple's combined v.'ages.

Chart lE shows that women earned only about $94billion of the $413 billion in wages shown on joint re-turns. In contrast, the wages of men on non joint returnswere only slightly higher than those of women, reflectinga more equal participation of male and female Wageearners filing nonjoint returns. The average shownon Forms W-2 of men ($3,836) and women (53,493)filing nonjoint returns also tended to be relatively close(see table 1.18).

69 010

Husband'swages

Percent distribution of returns

23

11

Chart 1E

Wages and other compensationfrom Form W-2 by sex of taxpayer

Billions of dollars

319

Men

Women

CONTENTS

Section 7

Sources of data, 353Description of the sample and limitations of the data. 353

Description of the sample, 353Sample selection. 353Method of estimation, 354

Limitations of the data, 355SampUng variability, 355Other limitations due to sampling, 355Sample management and non-sampling controls, 355

Text tab/es7A Number of individual income tax returns in population, number in sample,

prescribed and achieved sampling rates by sample class. 1969. 35478 Relative sampling variability at the one standard deviation level of esti-

mated numb of returns. 1969, 3557C Relative Sampling variability at the one standard deviation level for

sources of income and loss, exemptions, taxable income, and tax items, byadjusted gross income classes, 357

Sources of the Data,Description of the Sample

and Limitations

of the Data70 Relative sampling variability at the one standard deviation level ft'

number of returns and selected income and tax items, by 125 largeststandard metropolitan statistical areas and sumary adjusted gross incomeclasses. 359

SOURCES OF DATA

Individual income tax data in this report were esti-mated from a sample of unaudited tax returns, Forms1040, filed by U.S. citizens and residents and revenue-processed during the calendar year 1970 in the servicecenters and district offices of the Internal Revenue Serv-ice and at the Office of International Operations in theNational Office,

The statistics in this report are intended to representthe total returns for income year 1969. While the over-whelming majority of returns revenue-processed in 1970were for calendar year 1969, a few of them were for non-calendar years ended .during 1969 and 1970, and someothers were delinquent returns for prior years. Prioryear delinquent returns were used for the 1969 statisticsin place of 1969 returns processed after December31,1970. In general, the characteristics of returns due butnot yet filed could be represented best by the returns forprevious income years that were processed in 1970.

All returns processed during 1970 were subjected tosampling, with a few exclusions. The exclusions con-sisted of tentative returns and amended returns for in-come year 1969, and certain returns for prior years.Tentative returns were not subjected to sampling becausethe revised returns may have beensampled later on, whileamended returns were excluded because theoriginal re-turns were already subjected to sampling. With the ex-ception of returns filed at the Office of International Op-erations, returns for income years prior to 1962(gener-ally speaking, a very small number) were excluded tosimplify sampling procedures.

Art individual income tax return was required of (1)every citizen or resident alien of the U.S., and everybona fide resident of Puerto Rico, under 65 years of age(including minors), who had $600 or more of "gross in-come" for the year, (2)everycjtjzenorresjdent 65 yearsof age or over who had $1,200 or more grosà income forthe year, and (3) everyperson, regardless of age or grossincome, who had self-employment income of $400or more

during the tax year. Gross income, forpurposes of filing,included income earned from sources outside the UnitedStates, even though the income wasexempt from tax. How-ever, in the case of individuals who were residents ofPuerto Rico, gross income, for purposes of filing, did notinclude income derived from sources within Puerto Rico,except amounts received for services performed as anemployee of the United States Government.

Individuals who had tax withheld fromwages, but whoseincome was less than that required forfiling, usually filedto obtain a refund of tax withheld, although they were nototherwise required to file.

DESCRIPTION OF THE SAMPLE ANDLIMITATIONS OF THE DATA

Description of the Sample

The data presented for individual incometax returns fortax year 1969 are estimates based on a stratified sampleof all Form 1040 returns processed in the calendar year1970. The total sample consisted of 254,166returns, aboutthree-tenths of one percent of the total numberprocessedfor the year.

Sample selection

All returns filed with the seven Internal Revenueservicecenters, the 58 djstrjct offices, and with the Office ofInternational Operations were initially grouped for reve-nue processing based on the presence or absence of busi-ness schedules. However, special criteria were neededfor sampling.

For this purpose, service center and district office re-turns were stratified by computer in each service centerbased on size of adjusted gross income or deficit, totalbusiness receipts, and the largest source of income orloss. Sampling of nonbusiness returns was based on sizeof adjusted gross income or deficit or the largest sourceof income or loss; whereas sampling of business returns

69 011353

354 Individual Returns/1969 Sources, Sample, and Limitations

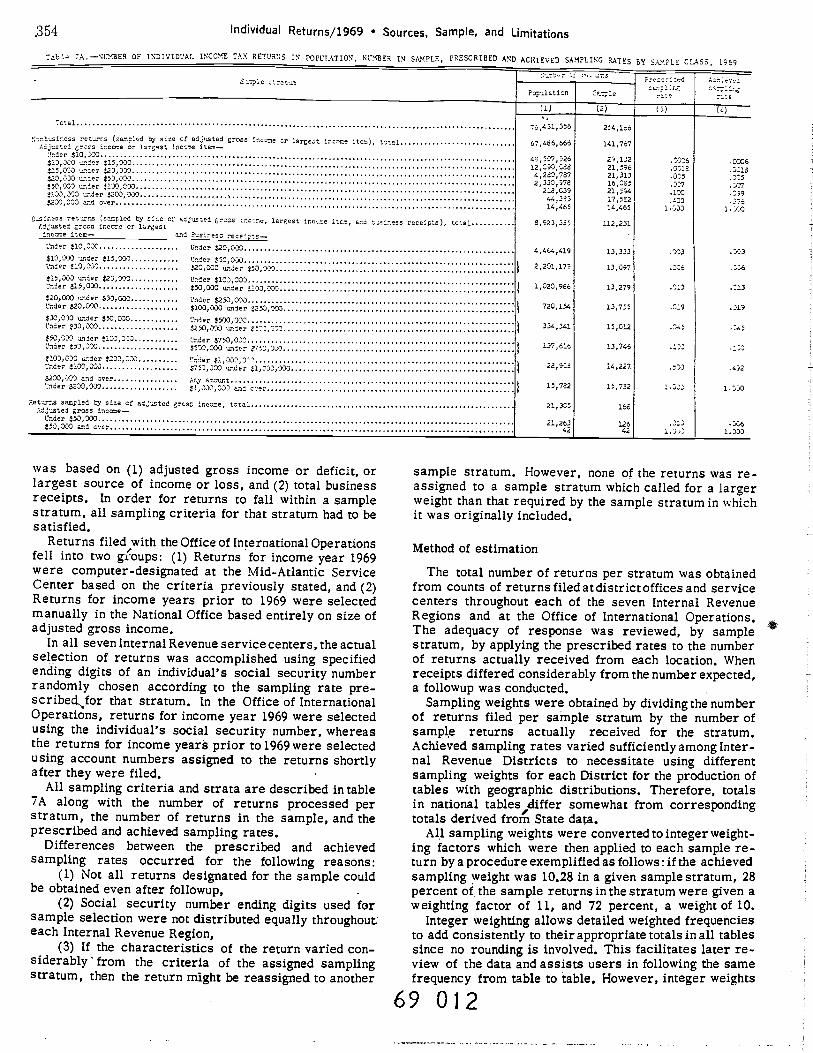

Tab1 7A.—'LMBER OF INDIVIDUAL INCOME TAX RETURNS IN POPUlATION, NUMBER IN SAMPLE, PRESCRIBED AND ACHIEVED SAMPLING RATES BY S°Y.PLE ClASS, 1969

S epIc t..o:1 :.

PepulstSCn

.le_eple

:e;Ir3..,.

Tctal

(1)

24,166

(3)

76,431,356sr1esir.ess reeurr.s (.p:ed by size Cf adJusted gross locose Cr largest izeurse itee), te'.el

/,0 jutted gr.rss locate or largest thcooe lIce—7rder $10,$1,C0 $15,303535,303 order 523,373..$23,330 o..:er $5300'

.3,003 under 5030,0)35130,003 tender 5.203,000$23O333 end over

67,466,666

42,507,5.269.3,300

4,255,7$72,330,Y78

1.4,35314,465

141,767

23,13221,5962131316,330

17, 50214,465

.o30o

.O1,

737130

.33313.33

.ccc6

.::g

.

.07

.2)

53s110t5 rete,rres (storied by cite Cf edj1.stei cr005 icc toe, lorgest ir,ctoe lIce, cr0 loolness receipts), totalAdjusted grzca boccus or lurgestlocate item— and Suslreesc recelpts_Soder $10,330 lode'. $20,030

6,923,335

4,444,419

112,231

13,333 .003 .003$15,030 under 615,31) Coder $53,030Under $10,730 0,300 under $53 O3 2 201 17° 13 '97 36. .

$15,003 under $23,300 lode'. $103,033330cr 53.5,030 $50,030 u..er 530,0)3 I 1 020 96 13 279, 3. .13$20,003 order $30,330 Lode'. $250,030Under $20,000 $100,030 under 2250,°03 720 151., 13 7'S, - 9. - .319

334,341 15,012 .51.5 ,$50,030 under 5335,500 Coder $750,033.Coder 553,030 3,300 undc-'. 5755,73' 137 °'b' '3 71.6' .303 .5103,2-30 under $233,030 Coder $1,130,3'Under $100,030 51,3)0,333 23 913' 14 227' .)3 .45.2

$230,730 sod Over unenent330cr 5230,00' $J.,003,O)3 15 762' '5 7°2- ' .7•- 1...

Retenr.s sampled by size cc adjusted grzss 33cc-ne, tcta:AdJustei gross locate—

Under $50,303$53,310 and

21,335

21,26342

140

12642

.0351.300

.,,1.oJ

was based on (1) adjusted gross income or deficit, orlargest source of income or loss, and (2) total businessreceipts. In order for returns to fall within a samplestratum, all sampling criteria for that stratum had to besatisfied.

Returns filed with the Office of International Operationsfell into two groups: (1) Returns for income year 1969were computer-designated at the Mid-Atlantic ServiceCenter based on the criteria previously stated, and (2)Returns for income years prior to 1969 were selectedmanually in the National Office based entirely on size ofadjusted gross income.

In all seven Internal Revenue service centers, the actualselection of returns was accomplished using specifiedending digits of an individual's social security numberrandomly chosen according to the sampling rate pre-scribed.,,for that stratum. In the Office of InternationalOperations, returns for income year 1969 were selectedusing the individual's social security number, whereasthe returns for income years prior to 1969 were selectedusing account numbers assigned to the returns shortlyafter they were filed.

All sampling criteria and strata are described in table7A along with the number of returns processed perstratum, the number of returns in the sample, and theprescribed and achieved sampling rates.

Differences between the prescribed and achievedsampling rates occurred for the following reasons:

(1) Not all returns designated for the sample couldbe obtained even after followup,

(2) Social security number ending digits used forsample selection were not distributed equally throughout.each Internal Revenue Region,

(3) If the characteristics of the return varied con-siderably from the criteria of the assigned samplingstratum, then the return might be reassigned to another

sample stratum. However, none of the returns was re-assigned to a sample stratum which called for a largerweight than that required by the sample stratum in whichit was originally included.

Method of estimation

The total number of returns per stratum was obtainedfrom counts of returns filed at district offices and servicecenters throughout each of the seven Internal RevenueRegions and at the Office of International Operations.The adequacy of response was reviewed, by samplestratum, by applying the prescribed rates to the numberof returns actually received from each location. Whenreceipts differed considerably from the number expected,a followup was conducted.

Sampling weights were obtained by dividing the numberof returns filed per sample stratum by the number ofsample returns actually received for the stratum.Achieved sampling rates varied sufficiently among Inter-nal Revenue Districts to necessitate using differentsampling weights for each District for the production oftables with geographic distributions. Therefore, totalsin national tables/iffer somewhat from correspondingtotals derived from State data.

All sampling weights were converted to integer weight-ing factors which were then applied to each sample re-turn by a procedure exemplified as follows: if the achievedsampling weight was 10.28 in a given sample stratum, 28percent of the sample returns in the stratum were given aweighting factor of 11, and 72 percent, a weight of 10.

Integer weighting allows detailed weighted frequenciesto add consistently to their appropriate totals in all tablessince no rounding is involved. This facilitates later re-view of the data and assists users in following the samefrequency from table to table. However, integer weights

69 012

ti(P,,c,,)

] () I

do not have the same effect on dollar amounts. This isbecause dollars per return were later rounded to thous-ands during statistical processing. Nevertheless, effortswere made to establish ''control totals" of those dollaramounts that appear in more than one national table andthese totals were substituted in other tables for theconvenience of the user.

A comparison of the estimated number of returns shownin the national tables of this reportwith the number of re-turns reported filed, as shown in table 7A, will discloseslight differences. These differences occur for the follow-ing reasons: (1) an estimated 555,500 returns were ex-cluded fron the tables because they showed no incomeinformation and (2) returns were classified into the propersize classes during tabulation regardless of the strata towhich they were assigned for sampling purposes.

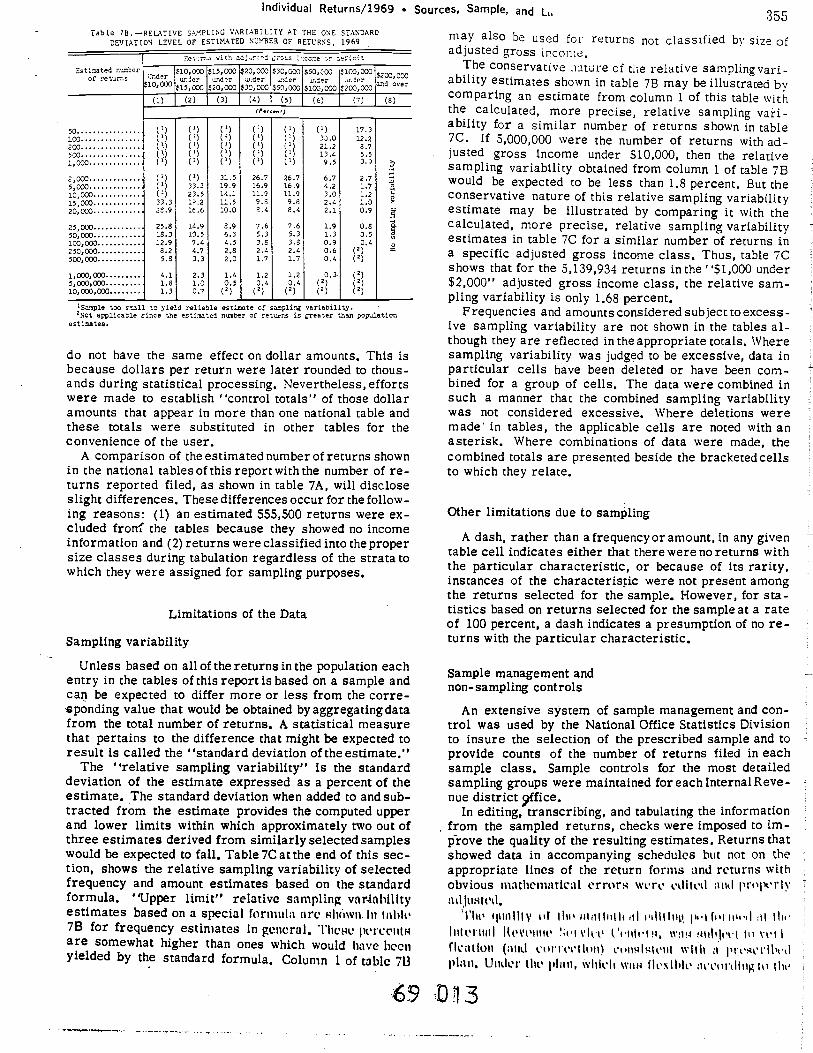

Sampling variability

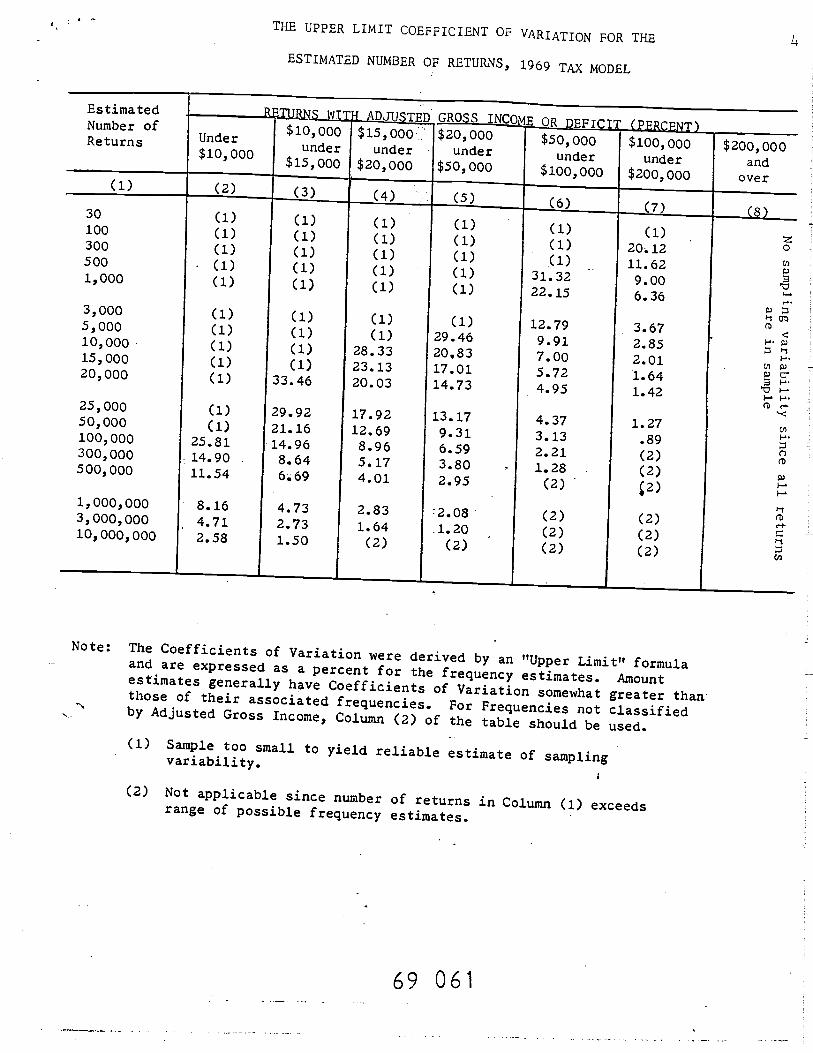

Limitations of the Data

Unless based on all of the returns in the population eachentry in the tables of this report is based on a sample andcai be expected to differ more or less from the corre-sponding value that would be obtained by aggregating datafrom the total number of returns. A statistical measurethat pertains to the difference that might be expected toresult is called the "standard deviation oftheestimate,"

The "relative sampling variability" is the standarddeviation of the estimate expressed as a percent of theestimate. The standard deviation when added to and sub-tracted from the estimate provides the computed upperand lower limits within which approximately two out ofthree estimates derived from similarly selected sampleswould be expected to fall. Table 7C at the end of this sec -tion, shows the relative sampling variability of selectedfrequency and amount estimates based on the standardformula. "Upper limit" relative sampling var4abilityestimates based on a special formula nrc shown In Inith'7B for frequency estimates in general. 'l'hcse .'1CefltMare somewhat higher than ones which would have beenyielded by the standard formula. Column 1 of table 713

355

may also be used foi returns not classified by size ofadjusted gross income.

The conservative nature of the relative samplingvan-abtlity estimates shown in table 7B may be illustrated bycomparing an estimate from column 1 of this table withthe calculated, more precise, relative sampling vari-ability for a similar number of returns shown in table7C. If 5,000,000 were the number of returns with ad-justed gross income under $10,000, then the relativesampling variability obtained from column I of table 7Bwould be expected to be less than 1.8 percent. But theconservative nature of this relative sampling variabilityestimate may be illustrated by comparing it with thecalculated, more precise, relative sampling variabilityestimates in table 7C for a similar number of returns ina specific adjusted gross income class. Thus, table 7Cshows that for the 5,139,934 returns in the ''$1,000 under$2,000" adjusted gross income class, the relative sam-— pling variability is only 1.68 percent.

F requencies and amounts considered subject to excess -lye sampling variability are not shown in the tables al-though they are reflected in the appropriate totals. Wheresampling variability was judged to be excessive, data inparticular cells have been deleted or have been com-bined for a group of cells. The data were combined insuch a manner that the combined sampling variabilitywas not considered excessive. Where deletions weremade in tables, the applicable cells are noted with anasterisk. Where combinations of data were made, thecombined totals are presented beside the bracketed cellsto which they relate.

Other limitations due to sampling

A dash, rather than afrequencyoramount,in any giventable cell indicates either that there were no returns withthe particular characteristic, or because of its rarity,instances of the characteristic were not present amongthe returns selected for the sample. However, for sta-tistics based on returns selected for the sample at a rateof 100 percent, a dash indicates a presumption of no re-turns with the particular characteristic.

Sample management andnon-sampling controls

An extensive system of sample management and con-trol was used by the National Office Statistics Divisionto insure the selection of the prescribed sample and toprovide counts of the number of returns filed in eachsample class. Sample controls for the most detailedsampling groups were maintained for each Internal Reve-nue district ffice.

In editing, transcribing, and tabulating the informationfrom the sampled returns, checks were imposed to im-prove the quality of the resulting estimates. Returns thatshowed data in accompanying schedules hut not on theappropriate lines of the return forms and returns withobvious mathematical errors were ediled n ud projx' r Iadlusted.

hit' illilihhlS' I1 hit' tilniltilhi ii i'tIhhhiij 1t,'i t'itii'iI II liiihiil'iuiiI I(eveitut' it V l&i' tiiIt't ', •iiiI'jtt Itt vi'i Ifleatlon (niid cu ii'i't'I k'ii cuiisIiieiil whit 1 j'iecthI't't1l)lni. Under Ilk' ithin, whik'l, witH ilcxlI'l(' ;ectttdhi1 Itt tiw

Table 78.—RELATIVE SAMPLING VARIABILITY AT THE ONE STANDARDDEVIATION LEVEL OP ESTIMATED NUMBER OF RETURNS 1969

Individual Returns/1969 • Sources, Sample, and L.

510,0:0inderlO,00O eioio

gersaith 4nznc v

l5,OOO $20,000 $30,003 $50,000 $100,000under under under -under .r.dnr

2O,C0O $30,000 $50,000 $100,000 5203,000

Estizated reunionof retures

So1002005001,000

2,0005,00010,00015,00020,000

25,00050,000100,000250,000500,000

1,000,000S,000,00010,000,000

( )(1)( )(1)(1)

( )( )( :)33.32S.9

25.818.312.98.25.8

4.11.81.3

(1)( :)(1)(1)(1)

(1)33.323.51°.216.6

3.1.910.57.44.73.3

2.31.00.7

(2)(2)(1)(1)(2)

31.519.914.111.510.0

8.96.34.52.82.0

1.40.5(2)

( :)(2)(1)(2)(2)

26.716.911.99.85.4

7.65.3

2.41.7

1.20.4(2)

(2)

(1)(2)(1)

26.716.911.99.88.4

7.65.33.82.41.7

1.23.4

(2)

(1)33.021.213.49.5

6.74.23.02.42.1

1.91.30.90.60.4

0.3-(2)(2)

17.312.28.75.53.9

2.71.71.21.00.9

0.83.50.4

(2)(2)

(2)(2)(2)

1Sa.epla too onull to yield reliable estioste of sa.np1ir variability.250t applicalle since the estImated nnber of returr.s is greater than population

estimates.

£9 O1i3

356

proficiency of the editors, screening and fractional sam-pling were used to determine the returns to be verified.

In order to provide measures of accuracy of the sta-tistical processing and secure greater consistency amongthe processing centers, a sub-sample of the returns andabstract sheets were independently reprocessed in theStatistics Division. Data generated under this programwere utilized to clarify the editing instructions and toinform the processing centers of the findings.

Keypunching of all data was also key verified in theservice center. Prior to tabulation at the Internal Reve-nue Service Data Center, numerous tests for internalconsistency were designated by the Statistics Division andwere applied to the data by computer. This assured that

proper balance aflu r1acionships among the return itand statistical classifications were maintained.

Finally, prior to publication, all statistics wereviewed for accuracy and reasonableness, in light ofVisions of tax law, taxpayer reporting variationslimitations, economic conditions, comparabilityother statistical series, and statistical techniquesin data processing.

However, the controls maintained over the seleof the sample returns, the processing of the sourceand the review of the statistics did not completely elnate the possibility of error. In addition, practicaerating considerations necessitated allowance of reaable tolerances in the statistical processing of the

69 014

Individual Returns/1969 • Sources, Sample, at ..,1i,itations

/

CONTENTS

Section

Standard metropolitan statistical areas, 179Other geographic classifications. 182Compensation reported on Forms W-2, 182

Text tables5A Number of returns, number of taxpayers, number of persons represented on

tax returns, and 1970 population, by states. 17858 Counties or cities comprising the 125 largest standard metropolitan

statistical areas and standard Consolidated areas, 1969. 180

4Iaps

125 largest standard metropolitan statistical areas. 184Internal Revenue Service Regions. 1969. 177Average compensation shown by Form W-2 by state. 1969, 183

Basic tables

5.1 Selected sources of income, deductions, taxable income, and income tax.by states and regions, 185

5.2 Adjusted gross income, salaries and wages, exemptions, taxable income,and income tax, by adjusted gross income classes and states. 188

5.3 Returns, adjusted gross income, and tax by marital status and by statesand regions, 250

State and Metropoifta

Area Dat

5.4 Number of returns, number of exemptions by type, and number of returnnumber of exemptions other than age and blindness, by state, !53

5.5 Number of returns, adjusted gross income, income tax after credits.average income, by number of exemptions other than age or blindnaradjusted gross income classes, and states. 255

5.6 Selected sources of income, deductions, taxable income, and incorr taby 125 largest standard metropolitan statistical areas. 269

5.7 Adjusted gross income, salaries and wages, exemptions. taxable rcorand income tax by adjusted gross income classes and 125 largeststandard metropolitan statistical areas. 273

5.8 Number of returns, number of exemptions by type, and number of return5number of exemptions other than age and blindness, by 125 l3rgeststandard metropolitan statistical areas, 337

69 015 17

178

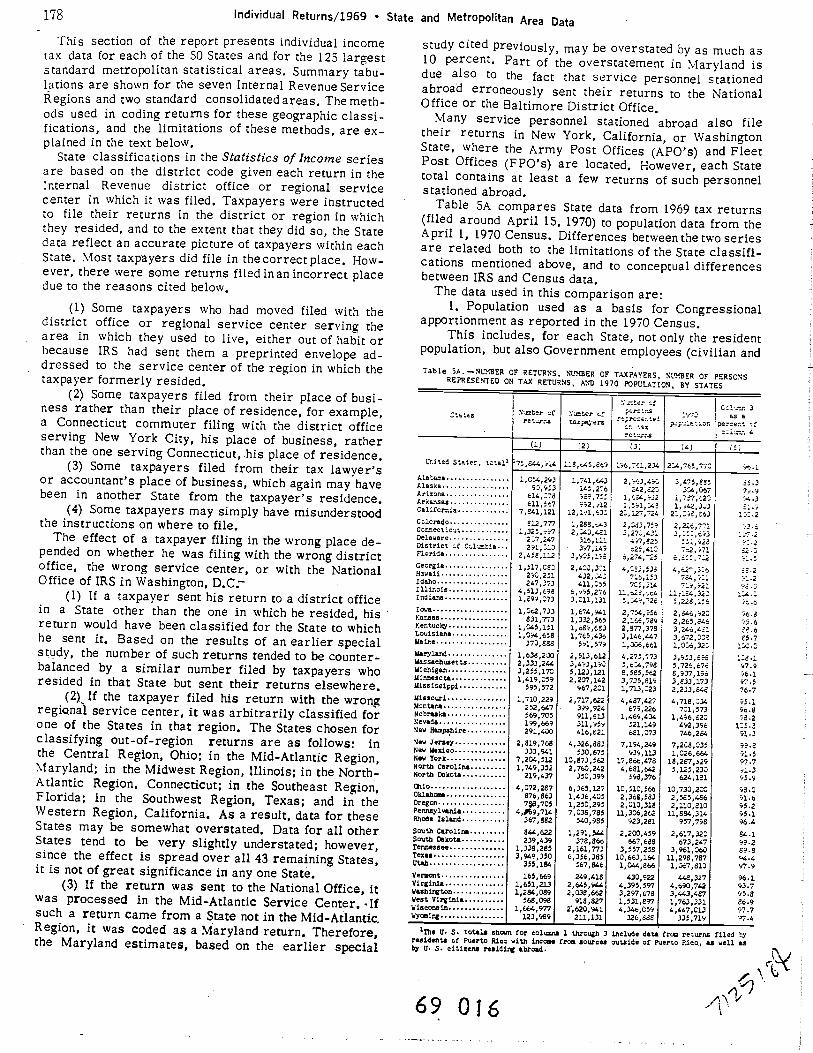

This section of the report presents individual incometax data for each of the 50 States and for the 125 largeststandard metropolitan statistical areas, Summary tabu-lations are shown for the seven Internal Revenue ServiceRegions and two standard consolidated areas. The meth-ods used in coding returns for these geographic classi-fications, and the limitations of these methods, are ex-plained in the text below.

State classifications in the Statistics of Income seriesare based on the district code given each return in theInternal Revenue district office or regional servicecenter in which it was filed. Taxpayers were ihstructedto file their returns in the district or region in whichthey resided, and to the extent that they did so, the Statedata reflect an accurate picture of taxpayers within eachState. Most taxpayers did file in the correct place. How-ever, there were some returns filed in an incorrect placedue to the reasons cited below,

(1) Some taxpayers who had moved filed with thedistrict office or regional service center serving thearea in which they used to live, either out of habit orbecause IRS had sent them a preprinted envelope ad-dressed to the service center of the region in which thetaxpayer formerly resided.

(2) Some taxpayers filed from their place of busi-ness rather than their place of residence, for example,a Connecticut commuter filing with the district officeserving New York City, his place of business, ratherthan the one serving Connecticut, his place of residence,

(3) Some taxpayers filed from their tax lawyer'sor accountant's place of business, which again may havebeen in another State from the taxpayer's residence,

(4) Some taxpayers may simply have misunderstoodthe instructions on where to file.

The effect of a taxpayer filing in the wrong place de-pended on whether he was filing with the wrong districtoffice, the wrong service center, or with the NationalOffice of IRS in Washington, D.C-

(1) If a taxpayer sent his return to a district officein a State other than the one in which he resided, hisreturn would have been classified for the State to whichhe sent it. Based on the results of an earlier specialstudy, the number of such returns tended to be counter-balanced by a similar number filed by taxpayers whoresided in that State but sent their returns elsewhere.

(2) If the taxpayer filed his return with the wrongregional service center, it was arbitrarily classified forone of the States in that region. The States chosen forclassifying out-of-region returns are as follows: inthe Central Region, Ohio; in the Mid-Atlantic Region,Maryland; in the Midwest Region, Illinois; in the North-Atlantic Region, Connecticut; in the Southeast Region,Florida; in the Southwest Region, Texas; and in theWestern Region, California. As a result, data for theseStates may be somewhat overstated. Data for all otherStates tend to be very slightly understated; however,since the effect is spread over all 43 remaining States,it is not of great significance in any one State.

(3) If the return was sent to the National Office, itwas processed in the Mid-Atlantic Service Center. Ifsuch a return came from a State not in the Mid-Atlantic.Region, it was coded as a Maryland return. Therefore,the Maryland estimates, based on the earlier special

study cited Previously, may be overstated by as much as10 percent. Part of the overstatement in Maryland isdue also to the fact that service personnel stationedabroad erroneously sent their returns to the NationalOffice or the Baltimore District Office.

Many service personnel stationed abroad also filetheir returns in New York, California, or WashingtonState, where the Army Post Offices (APO's) and FleetPost Offices (FPO's) are located. However, each Statetotal contains at least a few returns of such personnelstationed abroad,

Table 5A compares State data from 1969 tax returns(filed around April 15, 1970) to population data from theApril 1, 1970 Census, Differences between the two seriesare related both to the limitations of the State classifi-cations mentioned above, and to conceptual differencesbetween IRS and Census data,

The data used in this comparison are:1. Population used as a basis for Congressional

apportionment as reported in the 1970 Census.This includes, for each State, not only the resident

population, but also Government employees (civilian andabie SA.—NUMBER OF RETURNS, NUMBER OF TAXPAYERS, NUMBER OF PERSONS

REPRESENTED ON TAX RETURNS. AND 1970 PL'LATICN, BY STATES

....., tber tretun-.c

0ber oftaxpa,ers

''',_, '7 ao apercer., cf.

0.ited S0ate, tcOall

Alatae,a

Ala:1aArzor.aAroa.sas

retr.3 1.4(1) (2) (3) )i.) (0)

70,44.4, ,4

1,004,29393,903

614:75611,097

1,040,869

1,741,043140,2769,75

992, —

194,741,234

2,,o3,491242,4201,4,

.12:,0,1,.43

24,760,770

3,475,8313C.4,147

j,757,201, '42,313

,,.51.37,.9.4.3

Calitcr1aColoradoCCr.nectic.,t....DelawareDistrict or Col1ia...

7,841,121812,777

l,320,9727,247291,013

i.2,11,6)0

l,283,o.432,040,451

31.6,111397,149

2:127,724

5,27.,42].4?7,525625,410

2:,:-,8,o93

2,226,771, :o:,?3

00,923o2,971

10:2

:.-'J.252.0

CeorgiaH3waiiIdahoI11iCcS

2,418,112

l,5].7,CS

292,201247,373

4,013,a93

,2.?82,432,3:1'

411,0350,995,274

6,274,715

4,2,0357l,133703,204

1l,455,4

6,500,702

4,42,30475.4,9:1

.54,320

:.s552:.2s.:

OA.IndIana

Io.'aKansas

Ker.tuc1,Louisiana

1,499,073

062,733831,773

1,145,1311,4,658

3,111,1.31

1,674,9411,332,5651,69,6831,76.5,43o

0,04,'25

2,754,9562,104,7892,877,3783,146,4.47

0,22d,13628462O2,34s,5.043,244,4.3,o72,208

91.6

?.395.655.455.7

Mair.e

MylandMassachusettsMichiganMinnesota

373.885

1,638,2302,333,2443,255,1701,419,159

591,579

2,513,6123,493,1925,14212,207,142

1,306,661

4,275,7735,604,7988585'423,713,819

1,004,32;

3,913,55,726,6768,937,1963,833,173

Ix.:(.12.197.996.197.5

Mi5SiOippi

MissouriMontanaNebraskaNevada

595,572

1,710,229252,647069,705199,669

967,201

2,717,422399,924911,6133ll,95

1,713,123

4,457,427679,226

1,469,434021,1.49

2,223,544

4,718,:347:1,573

1,496,820492,396

74.7

90.196.88.2113.3

Rev Haspohire

Nec JerseyRev MexicoNew YorkNorth Carolina

291,430

2,819,768333,941

7,206,5121,749,352

416,821

4,326,883530.675

10,873,5622,760,242

81,073

7,154,249939,113

17,866,4784,681,642

746,294

7,208,0351,026,66418,287,5295,125,230

91.3

99.891.597.791.3

North DakotaioOkiahoas

OregonPennsylvania

219,437

4,072,287876,86378,7O5

4,9,7l4

350,399

6,365,1271,436,4051,250,2957,036,785

098,376

10,010,5662,368,0832,010,318

1.1,306,262

624,181

10,730,2002,565,4862,110,310

11,884,316

95.9

93.091.695.295.1

Rhode Island

South CarolinaSouth DakotaTennesseeTexas

367,882

844,622239,439

1,338,2853,949,350

540,985

1,291,544378,866

2,161,7736,356,385

923,281

2,200,459667,688

3,557,25810,663,164

957,798

2,617,320673,247

3,961,36011,298,787

96.4

54.199.269.8"4.4

Utah

VermontVirginiaWashingtonWest VirginiaWisconsin

355,184

165,6691,651,2131,284,089

568,0981,664,977

567,846

249,6182,645,9442,038,662

918,5272,620,941

1,044,864

'30,9224,395,5973,297,4781,531,8974,34o,059

1,067,813

442,3274,690,7423,443,4871,763,3314,467,013

97.996.193.795.884.997.7

1The U. S. total.. shnin for colonos 1 through 3 include data trc returns tiled 19residenta at Puerto Rico with thccc. from source. outside of Puerto Rico., as well as1' U. S. citizens residing abroad.

,.

Individual Returns/1969 • State and Metropolitan Area Data

69 016

Individual Returns/1969 • State and Metropolitan Area Data Imilitary) stationed abroad, as well as their families,whose permanent addresses were in that State.

2. Number of exemptions other than age and blind-ness as shown on tax returns for 1969.

This includes one exemption for each taxpayer, forthe taxpayer's spouse (if that spouse did not file aseparate return), and for each qualified dependent. Foreach State, this should include those Government em-ployees (civilian and military) stationed abroad whomaintained a permanent residence in that State. How-ever, as mentioned above, some Government employeesalso filed with APO and FF0 addresses in New York,California, and Washington State, or with the BaltimoreDistrict Office.

The two concepts of population differ in several otherrespects. Taxation data would exceed Census counts fortwo reasons. Exemptions could be claimed on 1969 taxreturns for anyone living at any time during calendaryear 1969, even though he may have died before the endof the year. Furthermore, in the tax return data, somedependents who earned small amounts of income werecounted twice- -once as taxpayers on their own returnsand once as dependents on their parents' returns. Onthe other hand, the IRS statistics exclude those individ-uals whose income was so low that they did not meet thetax return filing requirements and who did not file fora refund of tax withheld.

The Census count applies to the population at one mo-ment in time--April 1, 1970. Incontrasttothe tax returndata, it does not include anyone who died during the periodJanuary 1 to December 31, 1969. On the other hand, itdoes include children born during the period January 1 toApril 1, 1970, and not eligible for exemptions on 1969 in-come tax return-.

Table 5A shows that, for the Nation as a whole, exemp-tions other than age and blindness reported on tax returnsfor 1969 equalled 96.1 percent of the April 1, 1970 popu-lation. As might be expected, the percentage was some-what higher in most of the States chosen for c1assifyingreturns filed "out-of-region." The percentage was gen-erally lower in States with low average incomes, wheremany residents may not have met the filing requirements.The relatively low percentage for Florida may be due inpart to the fact that many older people live there- -personsaged 65 and over enjoyed more liberal filing require-ments--and in part to the fact thatmanypeople who werein Florida at the time of the Census had a permanent ad-dress in another State, from which they filed their re-turns.

Not shown in table 5A, but included in all the basictables in this section, are data on the 35,548 returnsfiled from Puerto Rico. The 131,046 exemptions otherthan age and blindness shown on these returns representless than 5 percent of the population of Puerto Rico.Income earned by bona fide residents of Puerto Ricofrom sources within that Commonwealth was, as a rule,exempt from taxation under U.S. tax law, and most resi-dents of Puerto Rico therefore did not have to file U.S.income tax returns. Those returns that were filed re-flected amounts earned by Puerto Rico residents fromsources outside the Commonwealth, or in Puerto Rico asemployees of the United States Government, and amounts

earned by persons who were not residents of Puerto Rfor the full taxable year.

STANDARD METROPOLITAN STATISTICAL AREA.

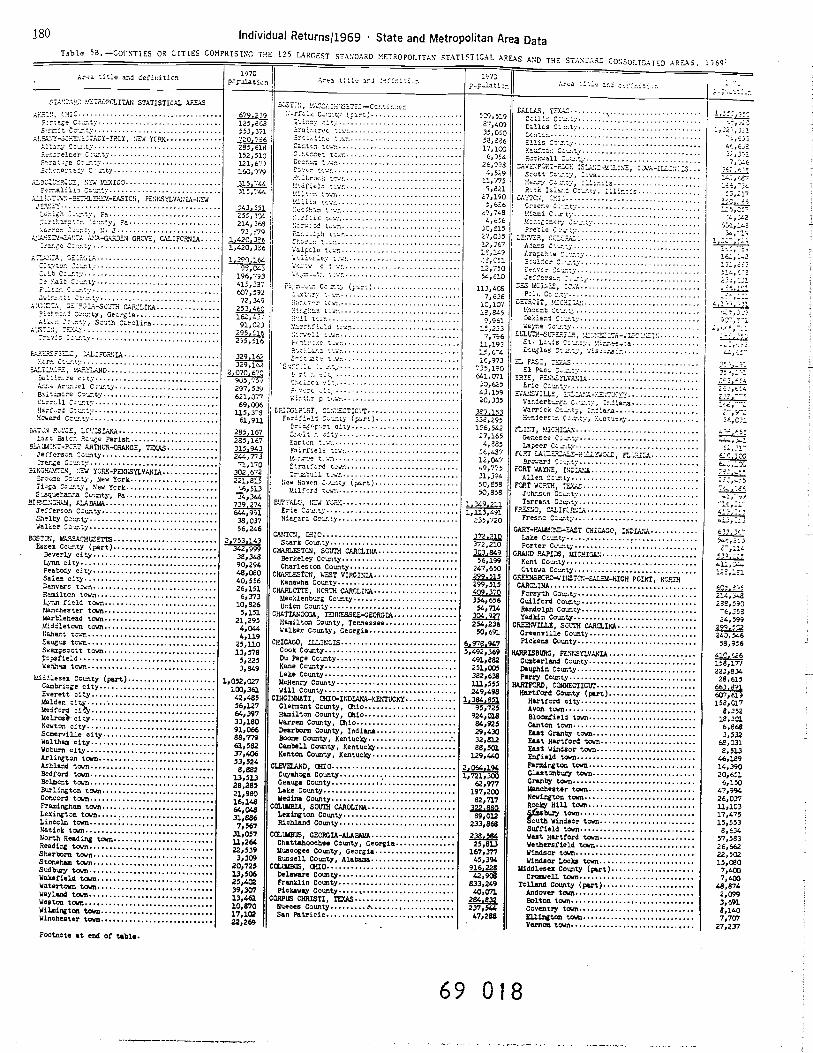

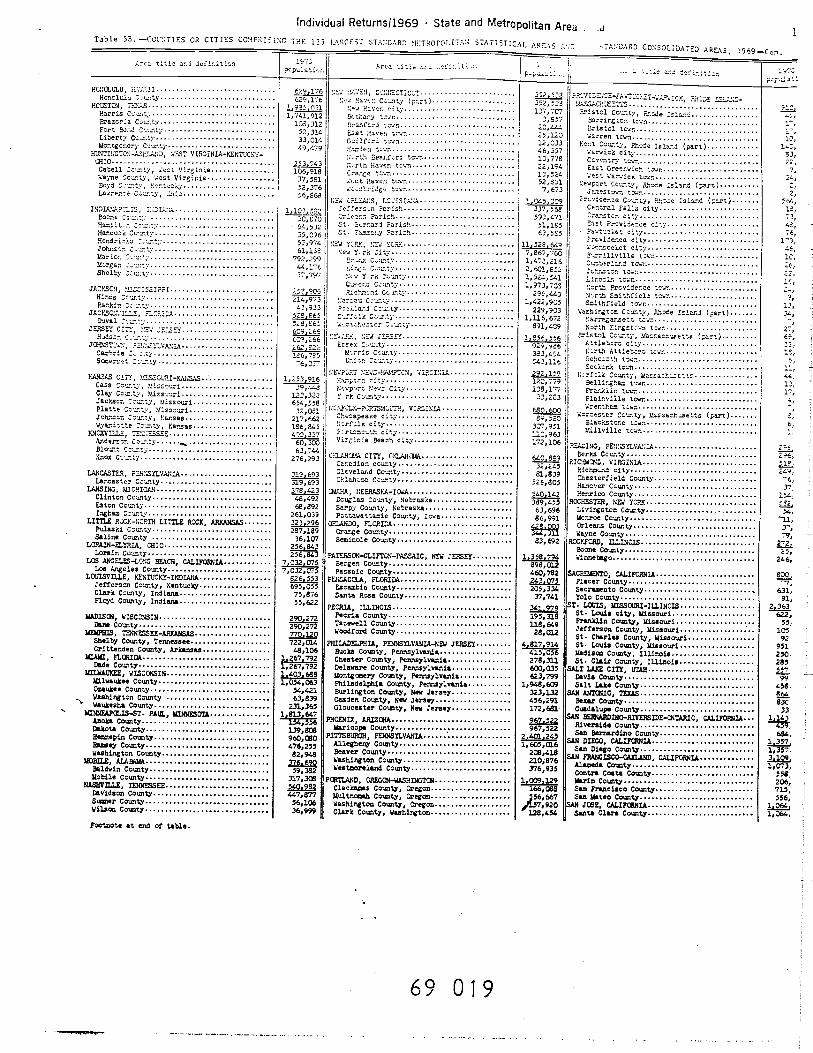

Standard metropolitan statistical areas (SMSAs)defined by the Office of Management and Budget in orto make it possible for all Federal Statistical agencto utilize the same boundaries in publishing statist:data useful for analyzing metropolitan problems. Estandard metropolitan statistical area contains a citycontiguous ''twin" cities) with at least 50,000 inhabitaand includes the county of such central city as wel:adjacent counties found to be metropolitan in characand economically and socially integrated with the coof the central city. (In New England, the basic ucomprising the SMSA are cities and towns rathercounties.)

In this report, data are shown for the 125 larSMSA's. These include most of the metropolitan awith a 1960 population of 200,000 or more. The counor cities and towns comprising each of these areasshown in table 5B. It should be noted that, as counad joining a metropolitan area meet the criteria of mepolitan character and socioeconomic integration,SMSA is redefined to include these counties. Theref'the definitions in this report, which conform to cestablished by the Office of Management and Budgeof March 1967, differ in some cases from those useStatistics of Income reports for tax years before 1 -

The criteria for including a return in a stanmetropolitan statistical area were the return add2indicated by the taxpayer and the district code entcby the district office or service center. Sincedistrict code was the primary classifier, any rewith an incorrect district code was automatically ccas not belonging to any metropolitan area. Most otother limitations of the State classifications mentkabove apply to the metropolitan area classificionwell.

The SMSA data shown in this report are subjespecial limitations. Since metropolitan areas tebe smaller than States, metropolitan area datasubject to higher sampling variability. Moreover,pling weights for States are based on actual courreturns filed In each State. No such counts were avaiby SMSA, so no special metropolitan area wecould be devised. For a measure of the samrvariability in the metropolitan area tables see tableSpecial limitations of the SMSA tables also result Ithe involved statistical coding required in determiwhether/or not a taxpayer's address lay within a mepolitan area.

It should be noted that coding for Washington, D.which Is not a separate Internal Revenue districtis combined with Maryland in the Baltimore distr:involves a process similar to that used for ccSMSA's, with determination based on taxpayer adthThe limitations described for the metropolitandata therefore also apply to the District of Columbiashown in the State tabulations.

69 017

LANL9IFIIL, .L:FCREIA.141112475, 5519t210.

Cu24::e.rec;t;.Arc.c1 C.utt,•Boltincre Ct•=oy.YornilC:.tt::.Howard Cotot:..

12:33 94244, LYVISLANA.tort Bator. 1oe Parish.

RLAS4:NT-PCST ARThUR-ORANGE, T011A5.Jefferson 24onty.rar.ge loony.

RSi2522111, IV YIP&-P01071V52434.irooce loony, hew York.Tioga Co.otty, New YorkS_uoeiar.r.a Cc'onty, Pa

BS9TC:.311118, ALABEIdA

Jefferson Cour.ty

Shelby Coortyodsoer .:orty

BINTIN, VJSSACHl2EnzEsnea Coooty (part)Beverly cityLynn hltyPeabody cotySale: cItyCanve.rn tonHamilton tcw-Lyr.n field tenMancheater townMarblehead townRdldsletcwn townRuhant toot

Saugun townSwespnnott townTcpsfieldberOcax ton

kiiillaaex County (part)Cambringe cityEverett cItyMaidenci-Menfnrd cMeLrca cityNewton cityScoerville cityWaltham cityWnburn cityArlington townAshland townBedford townBelocnt townBurlington townConcord townP'raoingham townLexington townLincoln townRatick townNorth Reading townReading townSherborn townStonehan townSudbony townWakefield townWatertown townWayland townWeston townWilmingtma townWinchester town

Footnote at end of table.

kNOT:::, !.l24J.CWLYTCC.—C:ttot24::;rn:o Coo.ty (yort(

sra;r.troc to.

Canton tao-nC.1.ascct too-n

OtafirlI

AulpIc t..on-

Fiat.' C; (;o:

0. 11 tco

2ci•.an to-,.

i11231?tir, C:C::E:TICCTPurii1c12 24aoty (port)

Foirfielo •

Ctrutfcnd toe-'

lr-.tboil tn.'low hoses 3 -onty (.crt)

ldilf;rJ toe'BUFFALO, 12.1 141.

Erietlogoru Coonty

CAETCII, 01450Stark County

CHANAESTCS, SotIfli CAR01IUABerkeley CcuntyCharleaton County

CHANAF.STCB, WEST VIRGINIAKanawha County

CHtNAC'C'fE, RCRYN GARCLIK6Mecklenborg CountyUnion County

CHATEAHG00A, TSN1ILSSEE-GEGRGIAHamilton County, Ter.neaaeeWalker County, Georgia

CHICAGO, ILLINOIS ________Cook CountyPu Page CountyKane CountyLake CcuntyMcHerry CountyWill County

CINCINNATI, 0101 O-IHDIANA-EZHTUCKY _______Cleroont County, QioHamilton County, thioWarren County, 01,ioDearborn County, IndianaBoone County, Eentuc'Caobell County, Eentuc'Kenton County, Kentucty

CI.EVtRND, 2410 ________C,n'alooga CountyGeauga CountyLake CountyMedina County

CGLIIEIA, SGtI24 CARGLIHALexington CountyRichland County

COLIUBI2S, GElIA—AI.AB#MAChattahoochee County, GeorgiaMusccgee County, GeorgiaRuanell County, Alabama

CGLISBIZ, 01410Delaware CotsityFranklin CountyPickaway County

CORnS CHRISTI, ItIASRueces CountySan Patricio

69 018

4t,'135

7,7.04

1-:,r

24242€, to-i

1L,—2

4;,t:4

24,C21

62,200:;

lsc,2:3r,114

'1.1,:.;..

214,348288,590'6,31824,599

242, Iwo58,916

1.58,177223,83628,615

607,619158,017

8,35218,301.6,8683,532

68,1318, 513

46,18914,39020,611

6,15047,99426,03711,10317,4'S15,5538,634

57,58326,66222,50215,0807,4107,400

48,8742,0993,6918,1407,707

27,237

180

Table SR. —COINTiES OR CITIES COMPRISING THE

tn-ru totle and definItIon

Individual Returns/1969 State and Metropolitan Area Data125 L9RCEST STANDARD METROPOLITAN STATISTICAL AR14 AND THE STANCAID CONSOL I0;T°D ARati. 1949°

1970- _.; -pnculati;, re.. 0 ...-; -'-i

174:10?: YLTRnPCLITAJ1 STATISTICAL AREAS

CHIC

F;rtngeCc.o.ty

.ttkt:rf-3;HS::t:7ACd-TRNY, :24.1 lIRE

Annoneloor 24unt,

2;tct0000G; C.onty412:9225 ,tTdlClIt

lo=.elilko C000t5-Li:.T?,O-IADO.13413.1-EASTCI1, PENNSYLVANIA-trw

Ic-nogs oonty, Pa::;rtLrr.pt:n:oon'.y, Pu

ANAI102J-JACCA .210-CARTEl GROVE, CALCPCRSIA

0241214

Or Cain Co-ant,

2400:4, CEJt2I.A_SC.05jI_o41_IlaRi:1.n :nd 14o.nty, CeorgIa

c-arty, Sooth Curnlur.o

125,81.8553,371

285,61w122, 210l21,6'S160,979

315,744

25t225, 304

214,76873,479

1,420,3R61,420,3560164

98,043196,793415,397607, 59272,349

162,43;91,023l6

295,116

329,1922,070, 671

Si2,72r297, 539621,377

69,006115,37861,911.

285,167

244,77271,170

221,815'.6,513t,344ma

644,99138,03756,246

2,753,143342,99938,34890, 29448,08040,55626,1516,373

10,8265,151.

21,2954,0444,119

25, 11013,578

5,2253,849

1,052,027100,36142,48556,12764,39733,18091,06688,77961,58237,40653,5248,882

13,51328,28521,98016,14864,04831,8867,56731,05711,26422,539

3,30920,72513,50625,40239,30713,46110,87°17,10222,269

D9,otg4740735, 01058,24517,100

6,91426,9384,51911,7759,821

27,1905,624

29,7484,616

30,21537,02512,3i719,149

12, 7S050,610

113,4067,626

10,10718,8459,941

iS, 2237,796

11,19312,67416,973