Embed Size (px)

Citation preview

J.A.S.B. & Associates Chartered Accountants

1

BUDGET DIGEST 2013-14

PREAMBLE

This digest summarises the important changes proposed in the Finance Bill 2013 (herein after referred as “Finance Bill” ) relating to Income Tax, Sales Tax, Federal Excise Duty and Customs etc. and has been prepared for the guidance and information of our clients and staff only. Subject to approval of the National Assembly, all changes through the Finance Bill are effective from July 1, 2013, unless otherwise specifically stated. It is recommended that while considering the application of the proposed amendments discussed here-in-after, reference should be made to the specific wordings of the relevant statute. The digest can also be accessed & downloaded from www.jasb-associates.com J.A.S.B. & Associates June 14, 2013 Chartered Accountants

For your feedback and queries….

KARACHI OFFICE ISLAMABAD OFFICE

Mr. Jibran S. Hassan, FCA, Partner [email protected]

Mr. Arsalan S Vardag, FCA, Partner [email protected]

J.A.S.B. & Associates Chartered Accountants

2

BUDGET DIGEST 2013-14

VOTE OF THANKS We would like to sincerely thank the team JASB for putting in round the clock efforts to make this Budget Digest 2013-14 possible in such a short time. We hope and believe that this document would assist our clients and team members in better understanding and evaluation of the Budget proposals. As part of our strategy for continuous improvement, we would appreciate feedback on the document.

J.A.S.B. & Associates Chartered Accountants

3

BUDGET DIGEST 2013-14

TABLE OF CONTENTS

1. Budget at Glance 4

2. Salient Features 6

3. Income Tax 10

4. Sales Tax 35

5. Federal Excise 45

6. Customs 50

J.A.S.B. & Associates Chartered Accountants

4

BUDGET DIGEST 2013-14

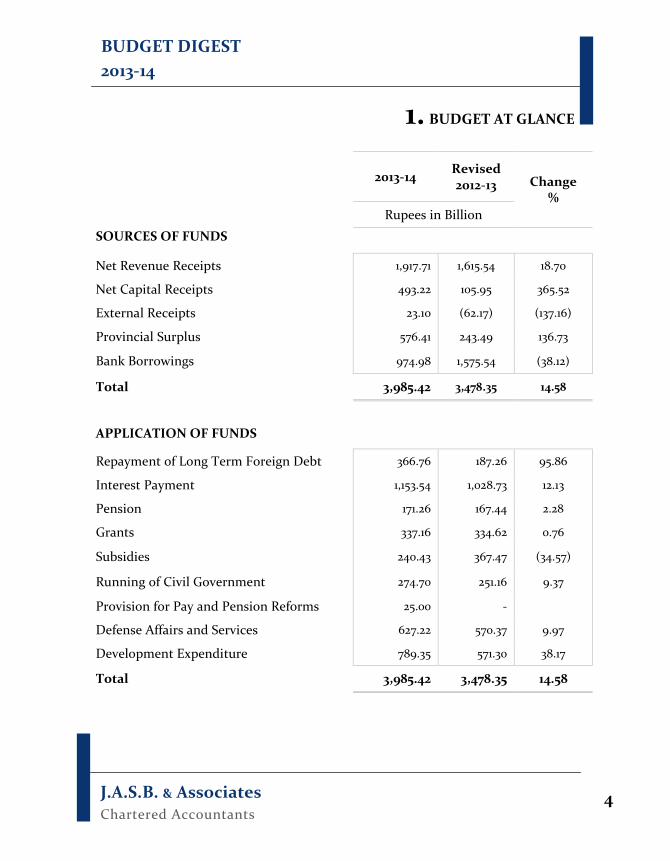

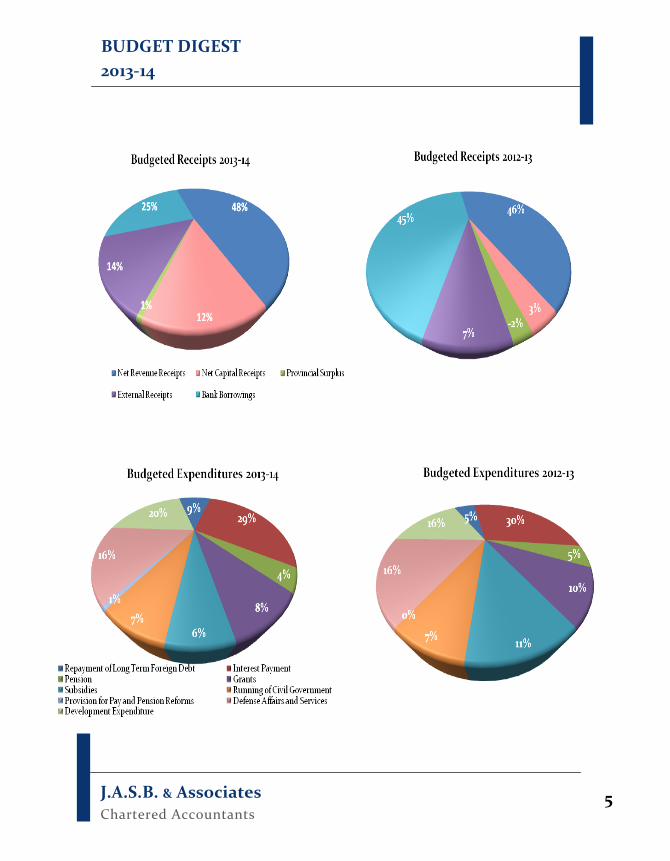

1. BUDGET AT GLANCE

2013-14 Revised 2012-13 Change

%

Rupees in Billion

SOURCES OF FUNDS

Net Revenue Receipts 1,917.71 1,615.54 18.70

Net Capital Receipts 493.22 105.95 365.52

External Receipts 23.10 (62.17) (137.16)

Provincial Surplus 576.41 243.49 136.73

Bank Borrowings 974.98 1,575.54 (38.12)

Total 3,985.42 3,478.35 14.58

APPLICATION OF FUNDS

Repayment of Long Term Foreign Debt 366.76 187.26 95.86

Interest Payment 1,153.54 1,028.73 12.13

Pension 171.26 167.44 2.28

Grants 337.16 334.62 0.76

Subsidies 240.43 367.47 (34.57)

Running of Civil Government 274.70 251.16 9.37

Provision for Pay and Pension Reforms 25.00 -

Defense Affairs and Services 627.22 570.37 9.97

Development Expenditure 789.35 571.30 38.17

Total 3,985.42 3,478.35 14.58

J.A.S.B. & Associates Chartered Accountants

5

BUDGET DIGEST 2013-14

J.A.S.B. & Associates Chartered Accountants

6

BUDGET DIGEST 2013-14

2. SALIENT FEATURES INCOME TAX • New income and tax slabs proposed for non-salaried individuals,

salaried individuals and AOPs; • In case of non-salaried individuals and AOP, the taxable income

exceeding Rs. 6 million is now proposed to be taxed at 35%; • In case of salaried individual maximum tax at rate of 30% on taxable

income exceeding Rs. 7 million will be applicable while marginal relief proposed to be withdrawn;

• Tax rate is proposed to be 34% for the Tax Year 2014 for companies other than banking companies;

• New slab rates proposed to tax gross rental income beyond Rs. 1Million; • Corporate dividend income is proposed to be brought under the Final

Tax Regime; • Initial allowance on plant & machinery is proposed to be reduced from

50% to 25%; • Rate of minimum tax on turnover is proposed to enhance to one

percent; • Builders and Developers of residential, commercial or other buildings

proposed to be liable to pay minimum tax at the rate specified; • Members of Chamber of Commerce and Industry, trade or any business

association, any Market Committee or any professional body including PEC, PMDC, Bar Councils, ICAP and ICMAP made liable to file return of income;

• Banks are required to share information of its customers with the tax authorities, necessary amendment in laws proposed;

• Computerized National Identity Card of individuals is proposed to be used as National Tax Number;

• Tax at the rate of 10% is proposed on margin financing, margin trading and securities lending;

J.A.S.B. & Associates Chartered Accountants

7

BUDGET DIGEST 2013-14

• Advance tax at the rate of 10% is proposed on functions & gatherings; • Advance tax at rate of 0.1% of gross sales is proposed on distributers,

dealers and wholesalers of electronics, sugar, cement, iron and steel products, fertilizer, motorcycles, pesticides, cigarettes, glass, textile, beverages, paint or foam sector. The retailers of these sectors are also liable to pay advance tax at the rate of 0.5% of gross sales;

• Advance tax on import stage is proposed to enhance from 5% to 5.5% for all taxpayers other than Companies and Industrial undertakings and companies, which remain taxed at 5%;

• Withholding tax on supply of goods , services and contracts is proposed to enhance to 4%,7% and 6.5% respectively;

• Advance tax is proposed to be chargeable on distributors of foreign produced films, TV Plays and Serials at such rates as specified;

• Advance tax is proposed to be chargeable on cable and other media operators at such rates as specified;

• Withholding tax rate on prize bonds or cross-puzzle is proposed to enhance to 15%;

• Rate of advance tax on cash withdrawals is proposed to increase to 0.3% from 0.2%;

• Exemption of free or concessional passage provided to employees by the transporters and airlines is proposed to be withdrawn

• Exemption available to universities and educational institutions stands is proposed to be withdrawn;

• Exemption on dividend in specie is proposed to be withdrawn; • Reduction in tax liability available to full time teachers and researchers

is proposed to be withdrawn; • Rate of tax is proposed to be reduced to 25% in case of dividend income

from money market funds and income funds by Banks from Tax Year 2014 onwards.

J.A.S.B. & Associates Chartered Accountants

8

BUDGET DIGEST 2013-14

SALES TAX • Standard rate of sales tax increased from 16% to 17%; • Additional tax at the rate of 2% will be charged if supplies are made to

a un-registered person; • Extra sales tax at the rate of 5% is collectible through electricity and

natural gas bills in addition to sales tax at standard rate from unregistered commercial and industrial consumers of electricity and gas whose monthly bill exceeds Rs. 15,000;

• Expansion in list of items which are chargeable to sales tax on retail price with effect from 13 June 2013 inter-alia including lubricating oils, cement, fertilizers, tyres & tubes, batteries, tiles, biscuits & confectionary items, paints, varnishes, household electrical goods including air conditioners, finished articles of textile & leather, etc.;

• Zero-rating on cotton-seed oil withdrawn and standard rate of 17% applies;

• Sales tax exemption on milk products withdrawn; • Exemption to local supplies against international tender is withdrawn. FEDERAL EXCISE DUTY • Further Duty at 2% of the value of excisable goods and services in

addition to applicable rate of FED when such goods / services are supplied to un-registered persons;

• Federal Excise Duty on aerated water increased from 6% to 9% of retail price with effect from 01st July 2013;

• FED @ 40 paisa per kg on imported oil seeds and Rs. 1 per kg on locally produced vegetable oil charged with effect from 13th June 2013;

• FED on financial services is being expanded by making all kinds of financial services chargeable to FED at the rate of 16% with effect from 13th June 2013.

J.A.S.B. & Associates Chartered Accountants

9

BUDGET DIGEST 2013-14

CUSTOMS

• Custom duty and other taxes on Hybrid Electric Vehicles are reduced

from 25% to 100% depending on vehicle’s engine capacity • Duty free import of “bio re-absorbable vascular scaffold” (heart stents) • Exemption of duty on energy saving tubes • Reduction of duty on office and school supplies to 20% from 25%. • Duty free import of solar submersible pumps presently dutiable at 20% • Reduction of duty on water treatment & purifying machinery from 25%

to 15%. • Duty on betel nuts increased from 5% to 10% and on betel leaves from

Rs 200 per kg to Rs 300 per kg proposed • Reduction of duty on Medium Density Fiber (MDF) Board from 20% to

15% • Post-dated cheques no more acceptable as security for provisional

assessment

J.A.S.B. & Associates Chartered Accountants

10

BUDGET DIGEST 2013-14

3. INCOME TAX General Provisions Relating to Taxes Imposed U/S 5, 6 & 7 [Section 8 (e) (ii)] It is proposed that withholding tax on dividend received by a company shall be final tax. Set Off of Losses [Section 56(1)] It is proposed that loss sustained by a person under any head of income in any tax year shall not be set off against his income under the head Salary. Group Taxation & Group Relief [Section 59AA (5), 59B (2) (g)] Sub-section 5 of Section 59 AA and clause (g) of sub-section 2 of Section 59 B are proposed to be amended to include another prerequisite i.e. compliance with “Group Designation Rules or Regulations” for group taxation and group relief option in addition to compliance with such corporate governance requirements as may be specified by SECP. Person [Section 80 (2)(b (v)] It is proposed to expand the definition of company by including the followings in the definition of company; • Non-profit organization; • An entity or body of persons established or constituted by or under any

law for the time being in force.

J.A.S.B. & Associates Chartered Accountants

11

BUDGET DIGEST 2013-14

In addition to cooperative and finance societies, all other societies will also be treated as company from now onward. Unexplained Income or Assets [Section 111 (1)] It is proposed that where a taxpayer explains the nature and source of income or assets by way of agriculture income, such income is to be considered as non-taxable source, to the extent on which agriculture tax was paid under the relevant provincial law. Minimum Tax on the Income of Certain Persons [Section 113 (1) (e)] Increase in minimum tax from 0.5% to 1% on annual turnover is proposed. It is further proposed that Individuals and Associations of Persons may also carry forward the excess of minimum tax paid over the actual tax in the subsequent five tax years. Presently, this facility is available to Companies only. Tax on Income of Certain Persons [Section 113A & 113B] It is proposed to withdraw the entitlement of Retailers to be assessed under final tax by substituting the following sections 113A & 113B: 113A. Minimum Tax on Builders:

It is proposed that income from business of construction and sale of residential, commercial or other buildings shall be subject to

J.A.S.B. & Associates Chartered Accountants

12

BUDGET DIGEST 2013-14

minimum tax at the rate of Rs.25 per square foot. Such minimum tax is to be computed on the basis of total number of square feet sold or booked for sale during the year.

113B. Minimum Tax on Land Developers

It is proposed that income from business of development and sale of residential, commercial or other plots shall be subject to minimum tax at the rate of Rs.50 per square yard. Such minimum tax is to be computed on the basis of total number of square yards sold or booked for sale during the year.

Return of Income [Section 114 (1)(b)(viii), Section 114(1A), Section 114(4) & Section 114(6)] • It is proposed to reduce the limit of annual electricity bill to Rs.

500,000 from Rs. 1,000,000 for filing of annual return of income. • It is further proposed to include sub-clause (ix) to make following

persons liable to file income tax return: - Person registered with any Chamber of Commerce and Industry or

any trade or business association or any market committee; - Person registered with any professional body including Pakistan

Engineering Council, Pakistan Medical and Dental Council, Pakistan Bar Council or any Provincial Bar Council, Institute of Chartered Accountants of Pakistan or Institute of Cost and Management Accountants of Pakistan.

• It is proposed to increase the limit of income under the head ‘Income from business’ to Rs. 400,000 from Rs. 350,000 to furnish the return of income for the tax year.

• It is proposed that Commissioner can issue notice for a period of less than thirty days requiring any person to file income tax return.

J.A.S.B. & Associates Chartered Accountants

13

BUDGET DIGEST 2013-14

• It is proposed that approval of Commissioner in writing is necessary for

filing of revised return. Person not Required to Furnish a Return of Income [Section 115(1) ] By omitting sub-section (1), it is proposed that filing of income tax return shall be mandatory for all salaried individuals deriving taxable income. Previously the Annual Employer Statement filed by the employers was treated as return of income furnished by the tax payer. It is proposed to omit the proviso to sub-section (1) of section 115 which presently deals with the method of filing of return of income by a salaried individual. The method of filing of return of income by a salaried individual is now proposed to be covered under section 118. Wealth Statement [Section 116] It is proposed to make the filing of wealth statement along with its reconciliation mandatory by every resident individual, even in case where income is within the ambit of Final Tax Regime. In case of filing of revised wealth statement, reason for revision along with revised wealth statement reconciliation should also be provided.

J.A.S.B. & Associates Chartered Accountants

14

BUDGET DIGEST 2013-14

Method of Furnishing Returns and Other Documents [Section 118] It is proposed that where the salary income for the tax year is Rs.500,000 or more, the individual shall file return of income electronically accompanied with the proof of deduction or payment of tax and wealth statement. Extension of Time for Furnishing Returns and Other Documents [Section 119] It is proposed to streamline section 119 to include the proposed effect of doing away with the requirement of employer’s certificate u/s 115. Investment Income Tax on Income [Section 120A] It is proposed to withdraw the Scheme of investment tax under which undisclosed income, representing investment made in movable or immovable assets was to be taxed. Provisional Assessment [Section 122C] It is proposed to reduce the time gap to 45 days from 60 days for treating the issued provisional assessment order as final assessment order.

J.A.S.B. & Associates Chartered Accountants

15

BUDGET DIGEST 2013-14

Appointment of Appellate Tribunal [Section 130 (3) (c)] It is proposed to be inserted that officer of Inland Revenue Service being a law graduate and having at least fifteen years of service in BS-17 and above may be appointed as a judicial member of the Appellate Tribunal. Salary [Section 149 (1)(i)] It is proposed that every person (previously was employer) paying salary to an employee shall deduct tax at average rate without taking into account the tax credits available i.e. charitable donation, investment in shares etc. The only adjustment he can make is excess deduction or deficiency from previous deduction. Payments to non-residents & Payments for Goods, Services and Contracts [Section 152(8) & 153 (7)(j)]

It is proposed that scope of these provisions be expanded by including the person registered under Sale Tax Act, 1990 in definition of “prescribed Person” as withholding agents.

Payments to Traders and Distributors [Section 153A]

Collection of Advance Tax by manufacturers from Traders and Distributors was introduced in the last Finance Act which is now been proposed to be discontinued by omitting this section.

J.A.S.B. & Associates Chartered Accountants

16

BUDGET DIGEST 2013-14

Income from Property [Section 155 (3)(v)(vi)] It is proposed that following shall be included in the definition of prescribed person for the purpose of withholding taxes on rent on immovable property; • A charitable institution • A private educational institution, a boutique, a beauty parlour, a

hospital, a clinic or a maternity home • Individual or associations of persons paying gross rent of rupees one

and a half million and above in a year Certificate of Collection or Deduction of Tax [Section 164(2)] It is proposed to streamline section 164 to include the proposed effect of doing away with the requirement of employer’s certificate under section 115. Statements [Section 165 (1)(6)] It is proposed to insert an explanation to clarify that the provisions of section 165 shall override all conflicting provisions in following laws restricting certain divulgence of information;

• Protection of Economic Reforms Act, 1992 • Banking Companies Ordinance, 1962 • Foreign Exchange Regulations Act, 1947 • Regulations made under the State Bank of Pakistan Act, 1956.

J.A.S.B. & Associates Chartered Accountants

17

BUDGET DIGEST 2013-14

Further, it is proposed to remove the requirement for including particulars of salary paid, where the income exceeds Rs 300,000 but does not exceed Rs 350,000 from annual statement of tax deduction from salary. Furnishing of Information by Banks [Section 165A] To broaden tax net, a full-fledged new section has been proposed to be introduced that requires every bank to furnish information to the Board in the prescribed form and manner. The information so required shall be used only for tax purposes and be kept confidential: • online access to its central database containing details of its account

holders and all transactions made in their accounts; • a list containing particulars of deposits aggregating rupees one million

or more made during the preceding calendar month; • a list of payments made by any person against bills raised in respect of

a credit card issued to that person, aggregating to rupees one hundred thousand or more during the preceding calendar month;

• a consolidated list of loans written off exceeding rupees one million during a calendar year;

• a copy of each Currency Transactions Report and Suspicious Transactions Report generated and submitted by it to the Financial Monitoring Unit under the Anti-Money Laundering Act, 2010 (VII of 2010); and

• any other information as may be required by the Board. Each bank shall nominate a Senior Officer to coordinate with the Board for provision of information as listed above. However, the banking companies and their officers shall not be liable to any civil, criminal or disciplinary proceedings against them for furnishing information required under Income Tax Ordinance,2001.

J.A.S.B. & Associates Chartered Accountants

18

BUDGET DIGEST 2013-14

Provision of Section 165A shall be applicable notwithstanding anything contained in any law for the time being in force including but not limited to the following;

• Banking Companies Ordinance, 1962, • Protection of Economic Reforms Act, 1992, • Foreign Exchange Regulation Act, 1947 and • Regulations made under the State Bank of Pakistan Act, 1956.

Tax Collected or Deducted as a Final Tax [Section 169 (3)] It is proposed to streamline sub-section (3) to reflect the change in section 8 where tax on dividend is proposed to be treated as final tax for companies. Additional Payment for Delayed Refunds [Section 171 (2)] Proposed explanation provides that refund becomes due from the date, the refund order is made and not from the date on which assessment of income treated to have been made by the Commissioner u/s 120. Representative [Section 172 (3)] It is proposed to elaborate the expression “business connection”. The said expression includes the transfer of an asset or business in Pakistan by a non-resident.

J.A.S.B. & Associates Chartered Accountants

19

BUDGET DIGEST 2013-14

Audit [Section 177 (10)] The proposed explanation enhances the power of the Commissioner to conduct audit and is proposed to be made independent of the powers of the FBR. The Commissioner is now empowered to call for the record or documents including books of accounts of a taxpayer for audit. Taxpayer’s Registration [Section 181 (3), 181C]

The bill seeks to empower the Board, by adding proviso after sub-section (3) of section 181, to allow individual to use Computerized National Identify Card (CNIC) issued by National Database and Registration Authority (NADRA) in place of National Tax Number (NTN).

Displaying of National Tax Number [Section 181C] The bill seeks to add a new section that require every person deriving income from business chargeable to tax, shall display his National Tax Number at a conspicuous place at every place of business. Delegation [Section 210 (1)] The bill proposed that Commissioner can delegate his powers to Additional Commissioner, Deputy Commissioner, Assistant Commissioner or Inland Revenue Officer only.

J.A.S.B. & Associates Chartered Accountants

20

BUDGET DIGEST 2013-14

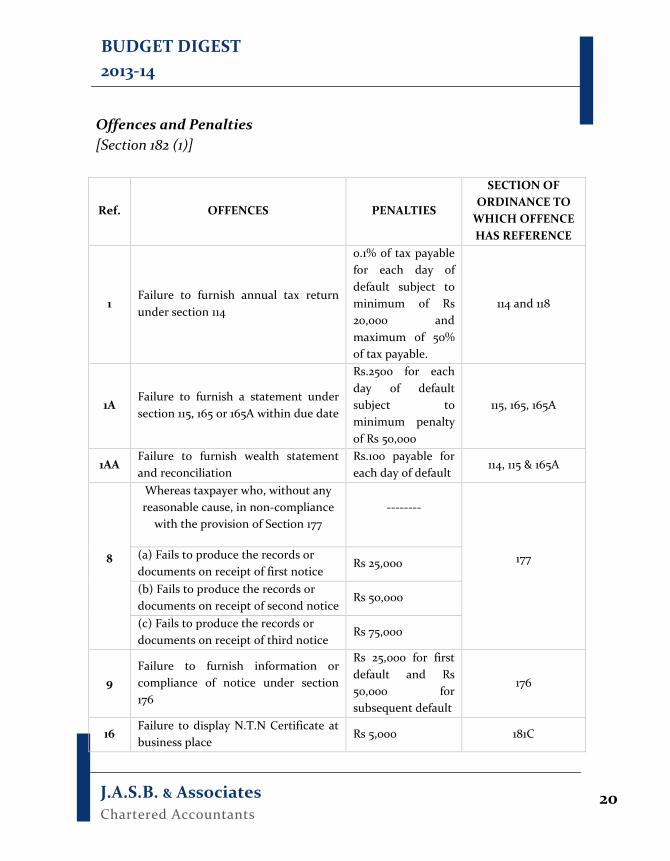

Offences and Penalties [Section 182 (1)]

Ref. OFFENCES PENALTIES

SECTION OF ORDINANCE TO

WHICH OFFENCE HAS REFERENCE

1 Failure to furnish annual tax return under section 114

0.1% of tax payable for each day of default subject to minimum of Rs 20,000 and maximum of 50% of tax payable.

114 and 118

1A Failure to furnish a statement under section 115, 165 or 165A within due date

Rs.2500 for each day of default subject to minimum penalty of Rs 50,000

115, 165, 165A

1AA Failure to furnish wealth statement and reconciliation

Rs.100 payable for each day of default

114, 115 & 165A

8

Whereas taxpayer who, without any reasonable cause, in non-compliance

with the provision of Section 177 --------

177 (a) Fails to produce the records or documents on receipt of first notice

Rs 25,000

(b) Fails to produce the records or documents on receipt of second notice

Rs 50,000

(c) Fails to produce the records or documents on receipt of third notice

Rs 75,000

9 Failure to furnish information or compliance of notice under section 176

Rs 25,000 for first default and Rs 50,000 for subsequent default

176

16 Failure to display N.T.N Certificate at business place

Rs 5,000 181C

J.A.S.B. & Associates Chartered Accountants

21

BUDGET DIGEST 2013-14

Selection for Audit by the Board [Section 214C (1) (3)] The bill proposed to add a new sub-section that restricts the board to keep the parameters confidential for the purpose of selecting person for audit. The proposed explanation enhances the power of the Commissioner to conduct audit and is proposed to be made independent of the powers of the FBR. Reward to Inland Revenue officers and Officials [Section 227A] The Bill proposes to insert a new section to provide cash rewards to officials of Inland Revenue for their meritorious conduct in full or partial realization of income tax and other taxes from cases of concealment or evasion of sales tax and other taxes. The Board shall by notification specify procedures for the apportionment of sanctioned reward. Directorate Generals of Law and Research & Development [Sections 230B & 230C] It is proposed to create two new directorates i.e. “Directorate-General of Law” and “Directorate-General of Research and Development”. Collection of Tax by National Clearing Company of Pakistan Limited [Section 233AA & Division IIB of Part IV of the First Schedule] It is proposed to enhance the scope of collection of advance tax at the rate of 10 per cent by NCCPL on margin financing, margin trading or securities lending under Securities (Leveraged Markets and Pledging) Rules, 2011 in

J.A.S.B. & Associates Chartered Accountants

22

BUDGET DIGEST 2013-14

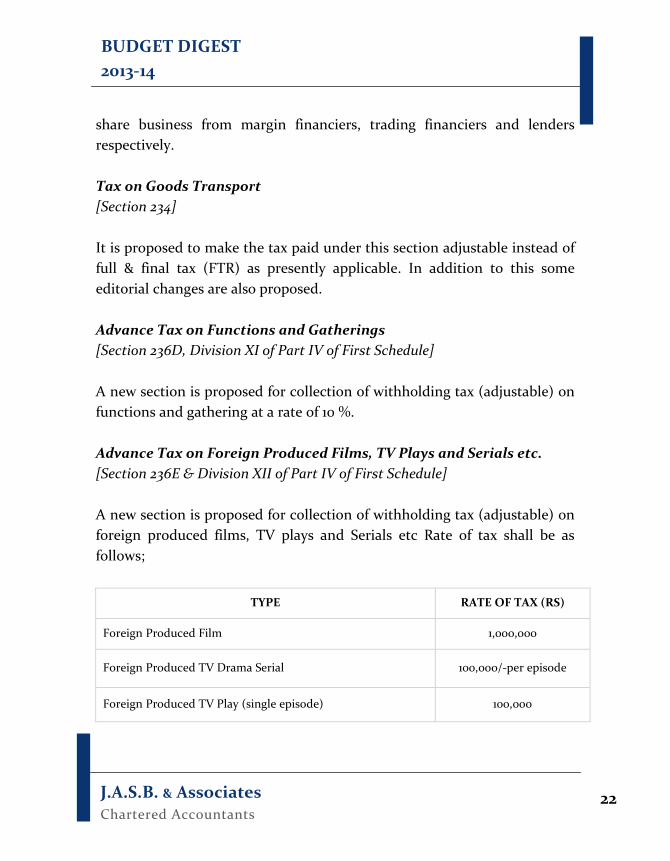

share business from margin financiers, trading financiers and lenders respectively. Tax on Goods Transport [Section 234] It is proposed to make the tax paid under this section adjustable instead of full & final tax (FTR) as presently applicable. In addition to this some editorial changes are also proposed. Advance Tax on Functions and Gatherings [Section 236D, Division XI of Part IV of First Schedule] A new section is proposed for collection of withholding tax (adjustable) on functions and gathering at a rate of 10 %. Advance Tax on Foreign Produced Films, TV Plays and Serials etc. [Section 236E & Division XII of Part IV of First Schedule] A new section is proposed for collection of withholding tax (adjustable) on foreign produced films, TV plays and Serials etc Rate of tax shall be as follows;

TYPE RATE OF TAX (RS)

Foreign Produced Film 1,000,000

Foreign Produced TV Drama Serial 100,000/-per episode

Foreign Produced TV Play (single episode) 100,000

J.A.S.B. & Associates Chartered Accountants

23

BUDGET DIGEST 2013-14

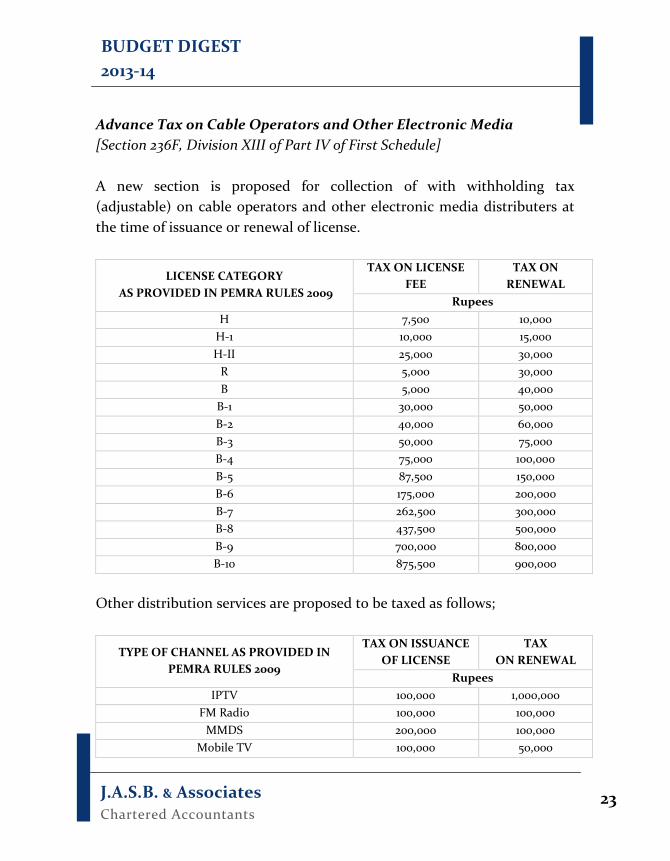

Advance Tax on Cable Operators and Other Electronic Media [Section 236F, Division XIII of Part IV of First Schedule] A new section is proposed for collection of with withholding tax (adjustable) on cable operators and other electronic media distributers at the time of issuance or renewal of license.

LICENSE CATEGORY AS PROVIDED IN PEMRA RULES 2009

TAX ON LICENSE FEE

TAX ON RENEWAL

Rupees H 7,500 10,000

H-1 10,000 15,000 H-II 25,000 30,000

R 5,000 30,000 B 5,000 40,000

B-1 30,000 50,000 B-2 40,000 60,000 B-3 50,000 75,000 B-4 75,000 100,000 B-5 87,500 150,000 B-6 175,000 200,000 B-7 262,500 300,000 B-8 437,500 500,000 B-9 700,000 800,000 B-10 875,500 900,000

Other distribution services are proposed to be taxed as follows;

TYPE OF CHANNEL AS PROVIDED IN PEMRA RULES 2009

TAX ON ISSUANCE OF LICENSE

TAX ON RENEWAL

Rupees IPTV 100,000 1,000,000

FM Radio 100,000 100,000 MMDS 200,000 100,000

Mobile TV 100,000 50,000

J.A.S.B. & Associates Chartered Accountants

24

BUDGET DIGEST 2013-14

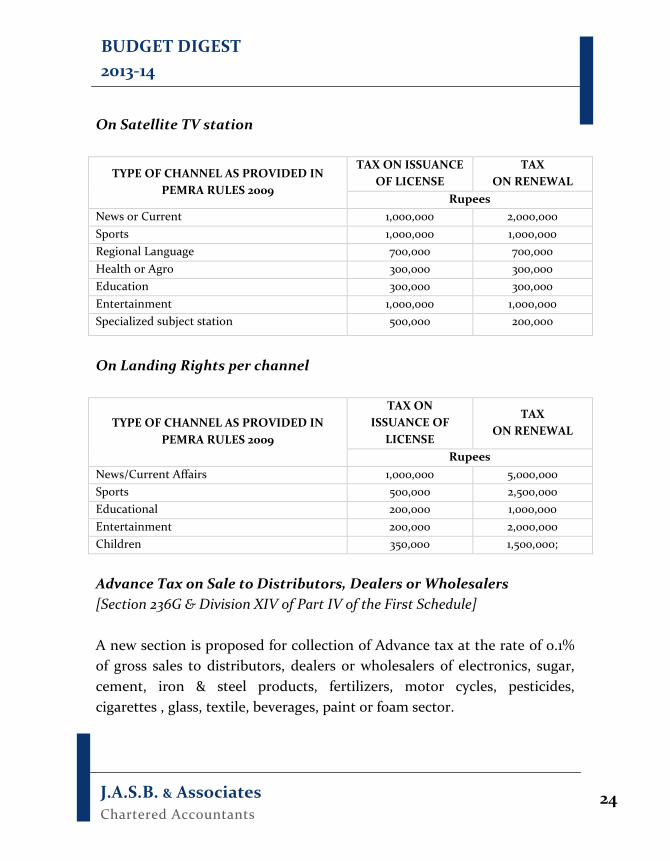

On Satellite TV station

TYPE OF CHANNEL AS PROVIDED IN PEMRA RULES 2009

TAX ON ISSUANCE OF LICENSE

TAX ON RENEWAL

Rupees News or Current 1,000,000 2,000,000 Sports 1,000,000 1,000,000 Regional Language 700,000 700,000 Health or Agro 300,000 300,000 Education 300,000 300,000 Entertainment 1,000,000 1,000,000 Specialized subject station 500,000 200,000

On Landing Rights per channel

TYPE OF CHANNEL AS PROVIDED IN PEMRA RULES 2009

TAX ON ISSUANCE OF

LICENSE

TAX ON RENEWAL

Rupees News/Current Affairs 1,000,000 5,000,000 Sports 500,000 2,500,000 Educational 200,000 1,000,000 Entertainment 200,000 2,000,000 Children 350,000 1,500,000;

Advance Tax on Sale to Distributors, Dealers or Wholesalers [Section 236G & Division XIV of Part IV of the First Schedule] A new section is proposed for collection of Advance tax at the rate of 0.1% of gross sales to distributors, dealers or wholesalers of electronics, sugar, cement, iron & steel products, fertilizers, motor cycles, pesticides, cigarettes , glass, textile, beverages, paint or foam sector.

J.A.S.B. & Associates Chartered Accountants

25

BUDGET DIGEST 2013-14

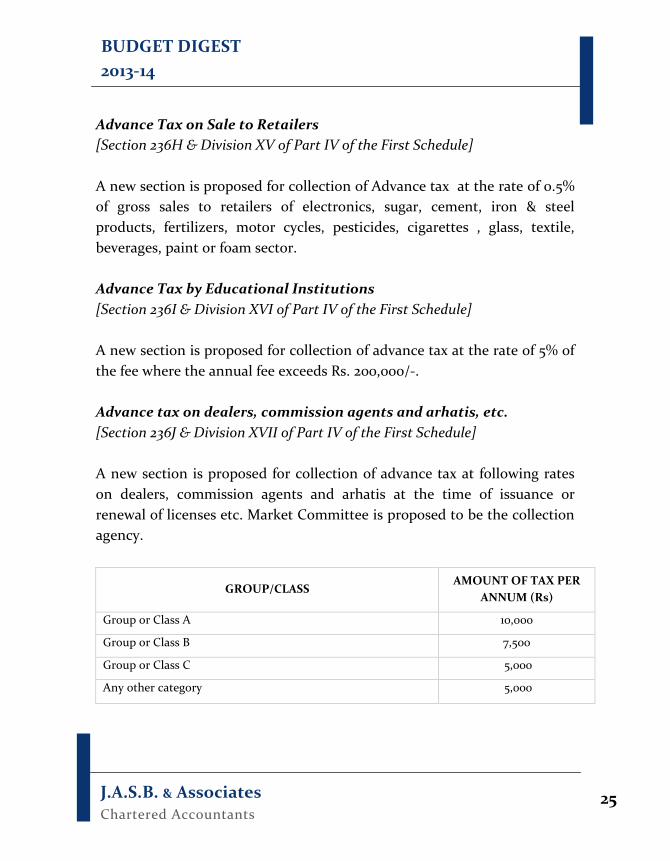

Advance Tax on Sale to Retailers [Section 236H & Division XV of Part IV of the First Schedule] A new section is proposed for collection of Advance tax at the rate of 0.5% of gross sales to retailers of electronics, sugar, cement, iron & steel products, fertilizers, motor cycles, pesticides, cigarettes , glass, textile, beverages, paint or foam sector. Advance Tax by Educational Institutions [Section 236I & Division XVI of Part IV of the First Schedule] A new section is proposed for collection of advance tax at the rate of 5% of the fee where the annual fee exceeds Rs. 200,000/-. Advance tax on dealers, commission agents and arhatis, etc. [Section 236J & Division XVII of Part IV of the First Schedule] A new section is proposed for collection of advance tax at following rates on dealers, commission agents and arhatis at the time of issuance or renewal of licenses etc. Market Committee is proposed to be the collection agency.

GROUP/CLASS AMOUNT OF TAX PER

ANNUM (Rs)

Group or Class A 10,000

Group or Class B 7,500

Group or Class C 5,000

Any other category 5,000

J.A.S.B. & Associates Chartered Accountants

26

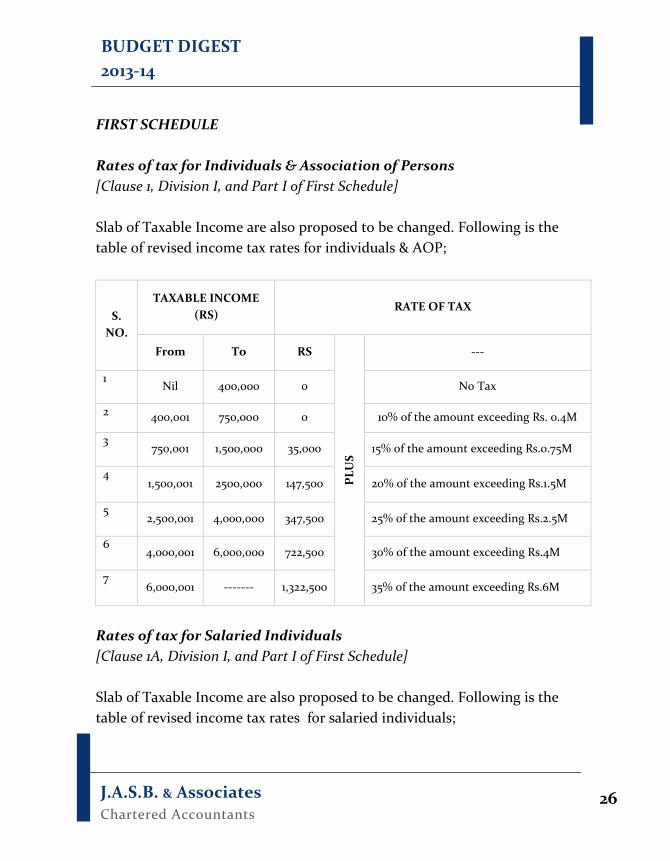

BUDGET DIGEST 2013-14

FIRST SCHEDULE Rates of tax for Individuals & Association of Persons [Clause 1, Division I, and Part I of First Schedule] Slab of Taxable Income are also proposed to be changed. Following is the table of revised income tax rates for individuals & AOP;

S. NO.

TAXABLE INCOME (RS)

RATE OF TAX

From To RS PL

US

---

1 Nil 400,000 0 No Tax

2 400,001 750,000 0 10% of the amount exceeding Rs. 0.4M

3 750,001 1,500,000 35,000 15% of the amount exceeding Rs.0.75M

4 1,500,001 2500,000 147,500 20% of the amount exceeding Rs.1.5M

5 2,500,001 4,000,000 347,500 25% of the amount exceeding Rs.2.5M

6 4,000,001 6,000,000 722,500 30% of the amount exceeding Rs.4M

7 6,000,001 ------- 1,322,500 35% of the amount exceeding Rs.6M

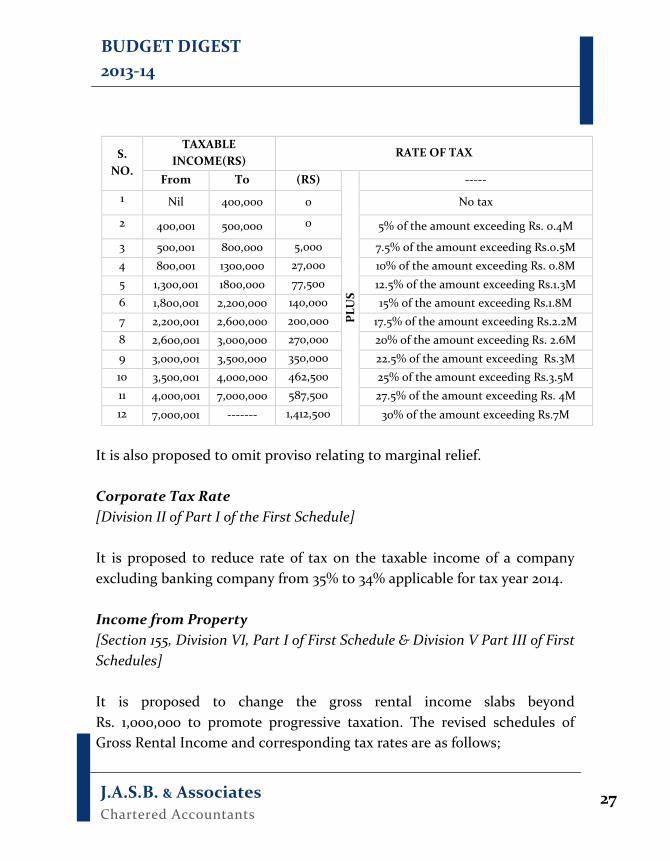

Rates of tax for Salaried Individuals [Clause 1A, Division I, and Part I of First Schedule]

Slab of Taxable Income are also proposed to be changed. Following is the table of revised income tax rates for salaried individuals;

J.A.S.B. & Associates Chartered Accountants

27

BUDGET DIGEST 2013-14

S. NO.

TAXABLE INCOME(RS)

RATE OF TAX

From To (RS) ----- 1 Nil 400,000 0

PLU

S

No tax

2 400,001 500,000 0 5% of the amount exceeding Rs. 0.4M

3 500,001 800,000 5,000 7.5% of the amount exceeding Rs.0.5M 4 800,001 1300,000 27,000 10% of the amount exceeding Rs. 0.8M 5 1,300,001 1800,000 77,500 12.5% of the amount exceeding Rs.1.3M 6 1,800,001 2,200,000 140,000 15% of the amount exceeding Rs.1.8M 7 2,200,001 2,600,000 200,000 17.5% of the amount exceeding Rs.2.2M 8 2,600,001 3,000,000 270,000 20% of the amount exceeding Rs. 2.6M 9 3,000,001 3,500,000 350,000 22.5% of the amount exceeding Rs.3M 10 3,500,001 4,000,000 462,500 25% of the amount exceeding Rs.3.5M 11 4,000,001 7,000,000 587,500 27.5% of the amount exceeding Rs. 4M 12 7,000,001 ------- 1,412,500 30% of the amount exceeding Rs.7M

It is also proposed to omit proviso relating to marginal relief. Corporate Tax Rate [Division II of Part I of the First Schedule] It is proposed to reduce rate of tax on the taxable income of a company excluding banking company from 35% to 34% applicable for tax year 2014. Income from Property [Section 155, Division VI, Part I of First Schedule & Division V Part III of First Schedules] It is proposed to change the gross rental income slabs beyond Rs. 1,000,000 to promote progressive taxation. The revised schedules of Gross Rental Income and corresponding tax rates are as follows;

J.A.S.B. & Associates Chartered Accountants

28

BUDGET DIGEST 2013-14

INDIVIDUALS & AOP

S. NO.

GROSS RENT (RS) RATE OF TAX

From To RS

PLU

S

---

1 Nil 150,000 0 No Tax

2 150,001 400,000 0 5% of the amount exceeding Rs. 0.15M

3 400,001 1,000,000 12,500 7.5% of the amount exceeding Rs.0.4M

4 1,000,001 2,000,000 57,500 10% of the amount exceeding Rs.1M

5 2,000,001 3,000,000 157,500 12.5% of the amount exceeding Rs.2M

6 3,000,001 4,000,000 282,500 15% of the amount exceeding Rs.3M

7 4,000,001 ------- 432,500 17.5% of the amount exceeding Rs.4M

COMPANY

S. NO.

GROSS RENT (Rs) RATE OF TAX

From To Rs

PLU

S

--- 1 Nil 400,000 0 5%

2 400,001 1,000,000 20,000 7.5% of the amount exceeding Rs.0.4M

3 1,000,001 2,000,000 57,500 10% of the amount exceeding Rs.1M

4 2,000,001 3,000,000 165,000 12.5% of the amount exceeding Rs.2M

5 3,000,001 4,000,000 290,000 15% of the amount exceeding Rs.3M

6 4,000,001 --------- 440,000 17.5% of the amount exceeding Rs.4M

Imports [Section 148 & Part II of the First Schedule] The rate of advance tax to be collected u/s 148 is proposed to be increased from 5% to 5.5%. However this proposed change is not applicable to companies and industrial undertakings on which existing rate of 5% will remain applicable.

J.A.S.B. & Associates Chartered Accountants

29

BUDGET DIGEST 2013-14

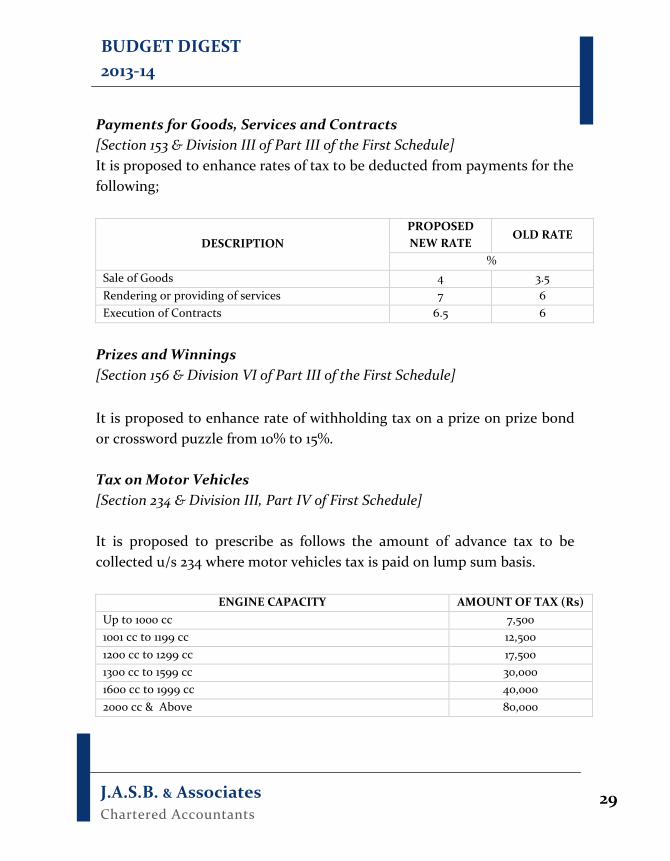

Payments for Goods, Services and Contracts [Section 153 & Division III of Part III of the First Schedule] It is proposed to enhance rates of tax to be deducted from payments for the following;

DESCRIPTION PROPOSED NEW RATE

OLD RATE

% Sale of Goods 4 3.5 Rendering or providing of services 7 6 Execution of Contracts 6.5 6

Prizes and Winnings [Section 156 & Division VI of Part III of the First Schedule] It is proposed to enhance rate of withholding tax on a prize on prize bond or crossword puzzle from 10% to 15%. Tax on Motor Vehicles [Section 234 & Division III, Part IV of First Schedule] It is proposed to prescribe as follows the amount of advance tax to be collected u/s 234 where motor vehicles tax is paid on lump sum basis.

ENGINE CAPACITY AMOUNT OF TAX (Rs) Up to 1000 cc 7,500 1001 cc to 1199 cc 12,500 1200 cc to 1299 cc 17,500 1300 cc to 1599 cc 30,000 1600 cc to 1999 cc 40,000 2000 cc & Above 80,000

J.A.S.B. & Associates Chartered Accountants

30

BUDGET DIGEST 2013-14

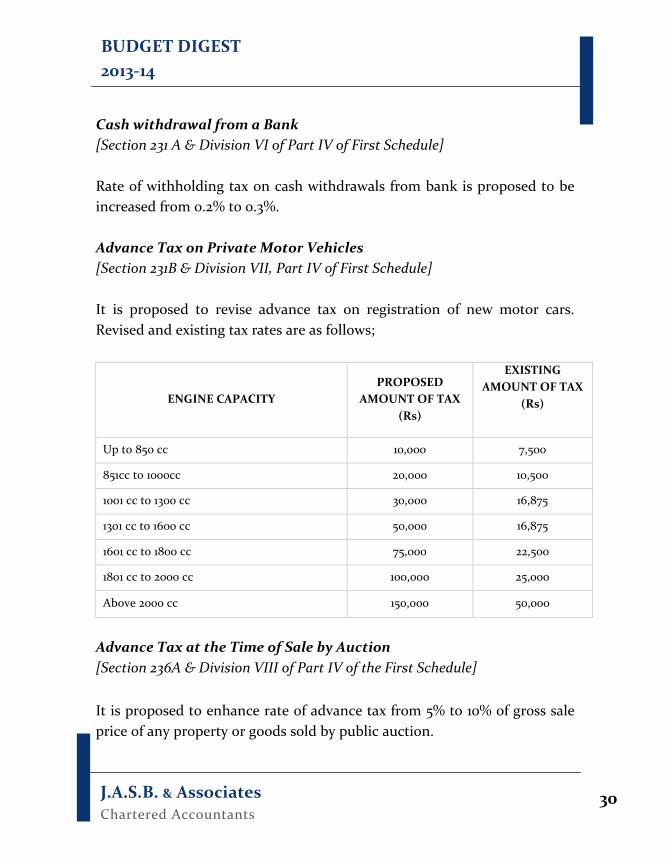

Cash withdrawal from a Bank [Section 231 A & Division VI of Part IV of First Schedule] Rate of withholding tax on cash withdrawals from bank is proposed to be increased from 0.2% to 0.3%. Advance Tax on Private Motor Vehicles [Section 231B & Division VII, Part IV of First Schedule] It is proposed to revise advance tax on registration of new motor cars. Revised and existing tax rates are as follows;

ENGINE CAPACITY PROPOSED

AMOUNT OF TAX (Rs)

EXISTING AMOUNT OF TAX

(Rs)

Up to 850 cc 10,000 7,500

851cc to 1000cc 20,000 10,500

1001 cc to 1300 cc 30,000 16,875

1301 cc to 1600 cc 50,000 16,875

1601 cc to 1800 cc 75,000 22,500

1801 cc to 2000 cc 100,000 25,000

Above 2000 cc 150,000 50,000

Advance Tax at the Time of Sale by Auction [Section 236A & Division VIII of Part IV of the First Schedule] It is proposed to enhance rate of advance tax from 5% to 10% of gross sale price of any property or goods sold by public auction.

J.A.S.B. & Associates Chartered Accountants

31

BUDGET DIGEST 2013-14

SECOND SCHEDULE Part 1 Exemption from Total Income Perquisite of Free or Concessional Passage [Clause 53 A] It is proposed to withdraw the exemption available to perquisite of free or concessional passage provided by transporters including airlines to their employees (including the members of their households and dependents). Income of University or Other Educational Institutions [Clause 92] It is proposed to withdraw exemption on any income of any university or other educational institution established solely for educational purposes and not for purposes of profit. Income from ICC Champions Trophy 2008 [Clause 98A] It is proposed to withdraw this exemption. Dividend in Specie [Clause 103B] It is proposed to withdraw the exemption allowed with respect to tax on dividend in specie.

J.A.S.B. & Associates Chartered Accountants

32

BUDGET DIGEST 2013-14

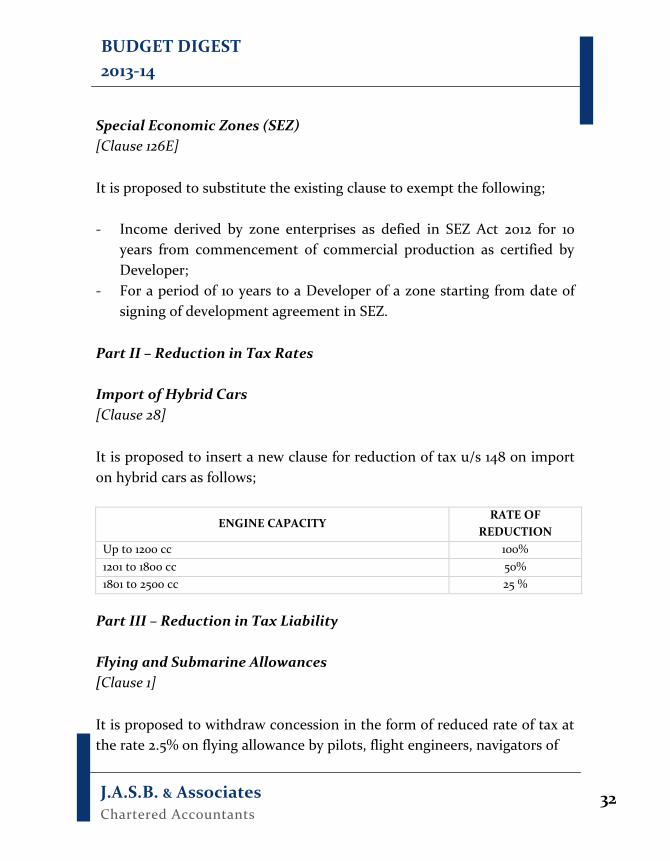

Special Economic Zones (SEZ) [Clause 126E] It is proposed to substitute the existing clause to exempt the following; - Income derived by zone enterprises as defied in SEZ Act 2012 for 10

years from commencement of commercial production as certified by Developer;

- For a period of 10 years to a Developer of a zone starting from date of signing of development agreement in SEZ.

Part II – Reduction in Tax Rates Import of Hybrid Cars [Clause 28] It is proposed to insert a new clause for reduction of tax u/s 148 on import on hybrid cars as follows;

ENGINE CAPACITY RATE OF

REDUCTION Up to 1200 cc 100% 1201 to 1800 cc 50% 1801 to 2500 cc 25 %

Part III – Reduction in Tax Liability Flying and Submarine Allowances [Clause 1] It is proposed to withdraw concession in the form of reduced rate of tax at the rate 2.5% on flying allowance by pilots, flight engineers, navigators of

J.A.S.B. & Associates Chartered Accountants

33

BUDGET DIGEST 2013-14

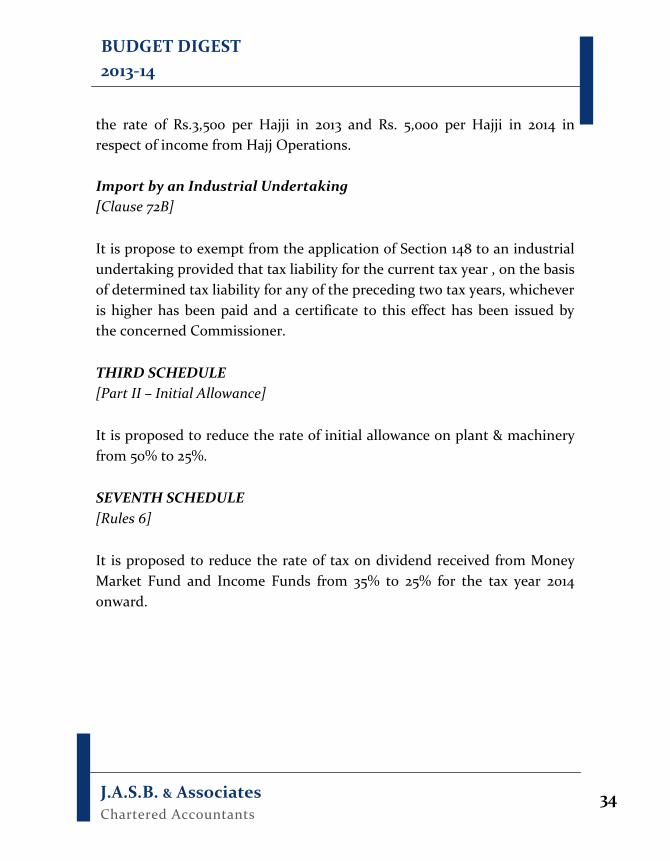

PAF, PIA, CAA, Junior Commissioned Offices or other ranks of Pakistan Armed Forces and submarine allowance by the officers of Pakistan Navy. Tax payable by a Full Time Teacher or a Researcher [Clause 2] It is proposed to withdraw reduction in tax liability allowed to full time teacher or researcher. Distributer of Cigarettes [Clause 7] It is proposed to extend the concession to individuals and AOPs who are distributors of locally manufactured cigarettes. Part III – Exemption from Specific Provisions Profit on Debt [Clause 59 (iv)(a)] It is proposed to withdraw tax exemption available to resident individuals with respect tax on profit or income on deposits not exceeding Rs. 150,000 invested in DSC, SSC, SA, POSA, TFC. Income from Hajj Operations [Clause 72A] It is proposed to exempt Hajj Group Operators in respect of Hajj Operations from application of Section 21(1), Section 113 and Section 152 of the Income Tax Ordinance 2001 provided that such operator has paid tax at

J.A.S.B. & Associates Chartered Accountants

34

BUDGET DIGEST 2013-14

the rate of Rs.3,500 per Hajji in 2013 and Rs. 5,000 per Hajji in 2014 in respect of income from Hajj Operations. Import by an Industrial Undertaking [Clause 72B] It is propose to exempt from the application of Section 148 to an industrial undertaking provided that tax liability for the current tax year , on the basis of determined tax liability for any of the preceding two tax years, whichever is higher has been paid and a certificate to this effect has been issued by the concerned Commissioner. THIRD SCHEDULE [Part II – Initial Allowance] It is proposed to reduce the rate of initial allowance on plant & machinery from 50% to 25%. SEVENTH SCHEDULE [Rules 6] It is proposed to reduce the rate of tax on dividend received from Money Market Fund and Income Funds from 35% to 25% for the tax year 2014 onward.

J.A.S.B. & Associates Chartered Accountants

35

BUDGET DIGEST 2013-14

4. SALES TAX CREST [Section 2 Clause (5AC)] It is proposed to insert new clause (5AC) in Section 2 to define the term “CREST” acronym of Computerized Risk- based Evaluation of Sales Tax which is a computerized program for analyzing and cross-matching of sales tax returns. Provincial Sales Tax [Section 2 Clause (22A)] The Bill seeks to amend definition of “Provincial Sales Tax” through re-phrasing without effecting the purpose and meaning. Supply Chain [Section 2 Clause (33)] The Bill proposes to insert new clause (33) in section (2) to define the term “Supply Chain” which means the series of transactions between buyers and sellers from the stage of first purchase or import to the stage of final supply. Time of Supply [Section 2 Clause (44)] The Bill proposes to insert words “or the time when any payment is received by supplier in respect of that supply, whichever is earlier” to enhance the definition of “Time of Supply”.

J.A.S.B. & Associates Chartered Accountants

36

BUDGET DIGEST 2013-14

The bill also proposes to insert a new proviso in sub-clause (c) of Clause (44) with respect to treatment of partial payment received for supply in tax period or exempt supply. Scope of Tax [Section 3] The Bill seeks to enhance standard rate of sales tax from 16% to 17%. The bill also seeks to insert following two new sub-sections with respect to; (1A) Charge additional tax at the rate of 2% of the value on taxable

supplies made to unregistered person; (1B) Taxation on capacity of plant, machinery, undertakings,

establishments or installations producing or manufacturing or on fixed basis from any person who is in a position to collect such tax due to the nature of the business.

The Bill also proposes to amend sub-section (5) of section 3 to allow chargeability of tax at extra rate or amount not exceeding 17% of value of goods or class of goods. Tax Credits not Allowed [Section 8(1)(caa)] The bill proposes to insert new clause “(caa)” to disallow adjustments on the basis of discrepancies indicated by CREST or where input tax is not verifiable in the supply chain.

J.A.S.B. & Associates Chartered Accountants

37

BUDGET DIGEST 2013-14

De-registration, Black Listing and Suspension of Registration [Section 21 (3) & (4)] The Bill seeks to omit reference of Section 73 “Certain Transactions not Admissible” appearing in sub-section 3 of section 21. The Bill proposes to insert a new sub-section (4) in section 21 to block input tax adjustment/refunds to persons engaged in fraudulent activities i.e. issuing fake /flying invoices, claiming fraudulent input tax or refunds, does not physically exist or conduct actual business etc. Records [Section 22(1)(ea)] It is proposed to insert a new clause (ea) after clause (e) to prescribe inward and outward gate passes and transport receipts as legal documents for the purposes of sales tax. Access to Records, Documents etc. [Section 25(5)] An explanation is proposed to be inserted to declare that powers of the Board, Commissioner or Officer of Inland Revenue under section 25, 38, 38A, 38B and 45A are independent of powers of the Board, Commissioner or Office of Inland Revenue under section 72B “Selection for the Audit by the Board”. Posting of Inland Revenue Officer [Section 40B]

J.A.S.B. & Associates Chartered Accountants

38

BUDGET DIGEST 2013-14

The Bill proposes an amendment to equate the powers of Board and Chief Commissioner regarding posting of Inland Revenue Officer to monitor production, sales of taxable goods and stock position of registered person. Monitoring or Tracking by Electronic or Other Means [Section 40C] The Bill proposes to insert a new section to provide legal powers for monitoring or tracking by electronic or other means of productions, sales, clearances, stocks etc. of any registered person or class of persons etc. Appeals [Section 45B(1A)] The Bill proposes to insert a new sub-section to allow Commissioner (Appeals) to grant stay of thirty days in aggregate to relax taxpayer from undue hardship in payment of tax to be recovered. Rectification of Mistake [Section 57] The Bill proposes to substitute section 57 to harmonize the concept of rectification of mistake in lines of Income Tax Ordinance, 2001. Reward to Inland Revenue Officers and Officials [Section 72C] The Bill proposes to insert a new section to provide cash rewards to officials of Inland Revenue for their meritorious conduct in full or partial realization of sales tax and other taxes from cases of concealment or evasion of sales tax and other taxes.

J.A.S.B. & Associates Chartered Accountants

39

BUDGET DIGEST 2013-14

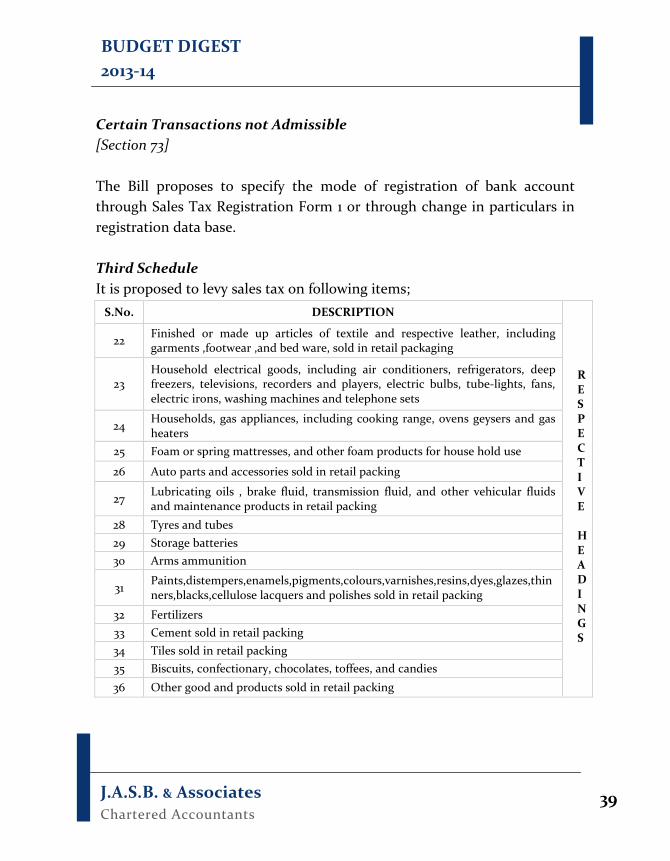

Certain Transactions not Admissible [Section 73] The Bill proposes to specify the mode of registration of bank account through Sales Tax Registration Form 1 or through change in particulars in registration data base. Third Schedule It is proposed to levy sales tax on following items;

S.No. DESCRIPTION

RESPECTIVE HEADINGS

22 Finished or made up articles of textile and respective leather, including garments ,footwear ,and bed ware, sold in retail packaging

23 Household electrical goods, including air conditioners, refrigerators, deep freezers, televisions, recorders and players, electric bulbs, tube-lights, fans, electric irons, washing machines and telephone sets

24 Households, gas appliances, including cooking range, ovens geysers and gas heaters

25 Foam or spring mattresses, and other foam products for house hold use

26 Auto parts and accessories sold in retail packing

27 Lubricating oils , brake fluid, transmission fluid, and other vehicular fluids and maintenance products in retail packing

28 Tyres and tubes 29 Storage batteries 30 Arms ammunition

31 Paints,distempers,enamels,pigments,colours,varnishes,resins,dyes,glazes,thinners,blacks,cellulose lacquers and polishes sold in retail packing

32 Fertilizers 33 Cement sold in retail packing 34 Tiles sold in retail packing 35 Biscuits, confectionary, chocolates, toffees, and candies 36 Other good and products sold in retail packing

J.A.S.B. & Associates Chartered Accountants

40

BUDGET DIGEST 2013-14

Sixth Schedule Milk Preparations etc. [Serial No. 25, Table-1(Import or Supplies] The Bill seeks to omit Serial No. 25 from Table 1 to Sixth Schedule to withdraw exemption of sales tax on milk preparations obtained by replacing one or more constituents of milk by another substance. Local Supplies against International Tenders [Serial No. 12, Table-2 (Local supplies only)] The Bill seeks to omit Serial No. 12 from Table 2 to Sixth Schedule to withdraw exemption of sales tax on local supplies against International Tenders. Rescinded Notifications [SRO 500(I)/2013] With effect from June 13, 2013 various notifications have been rescinded. In addition to notifications presented in table, SRO 172(I)/2006 dated 24th February 2006, SRO 200 & 201 (I)/2011 dated 14th March 2011 are also rescinded.

J.A.S.B. & Associates Chartered Accountants

41

BUDGET DIGEST 2013-14

SROS DESCRIPTION

646(I)/2005 30th June 2005

Application of zero rating on supply of Hydrogen, Nitrogen and Helium produced by BOC to M/s Pakistan PTA Limited, Port Qasim.

863(I)/2007 24th August,2007

Charging of zero per cent on raw materials, sub-components, components, sub-assemblies and assemblies imported or purchased locally for the manufacture of dairy products and office /school supplies.

160(I)/2010 10th March 2010

Exemption of whole of the amount of default surcharge and penalties payable by a registered person located in districts of Hangu, Bannu, Tank, Kohat, Chitral, Charsadda, Peshawar, Dera Ismael Khan, Batagram, Lakki Marwat, Sawabi and Mardan against whom an amount of sales tax or federal excise duty is outstanding on account of any audit observation, audit report, show cause notice or any adjudication order or who has failed to pay any amount of sales tax or federal excise duty or claimed inadmissible input tax adjustment or refund or drawback due to any reason.

161(I)/2010 10th March 2010

Exemption of whole of the amount of additional duties and penalties payable by a registered person located in Agencies of Bajaur, Mohmand, Khyber, Orakzai, Kurrum, North Waziristan and South Waziristan against whom an amount of central excise duty is outstanding on account of any audit observation, audit report, show cause notice or any adjudication order or who has failed to pay any amount of central excise duty or claimed inadmissible refund or drawback due to any reason etc.

162(I)/2010 10th March 2010

Exemption of central excise duty leviable on goods produced or services rendered in the areas Bajaur Agency, Mohmand Agency, Khyber Agency, Orakzai Agency, Kurrum Agency, North Waziristan Agency and South Waziristan Agency

163(I)/2010 10th March 2010

Exemption of federal excise duty leviable on goods produced or services rendered in the areas Districts of Hangu, Bannu, Tank, Kohat and Chitral Districts of Charsadda, Peshawar, Dera Ismael Khan, Batagram, Lakki Marwat, Sawabi and Mardan

164(I)/2010 10th March 2010

Exemption sales tax leviable on supply of electricity by Peshawar Electric Supply Company or any other duly registered Electric Supply Company to manufacturing units (having industrial connections) whether registered or not, located in districts of Hangu, Bannu, Tank, Kohat, Chitral, Charsadda, Peshawar, Dera Ismael Khan, Batagram, Lakki Marwat, Sawabi and Mardan.

117(I)/2011 10th February 2011

Goods produced or manufactured in such areas, where the Sales Tax Act, 1990, is not applicable but are included in the Prime Minister’s Fiscal Relief to Rehabilitate the Economic Life in Khyber Pakhtunkhwa, FATA and PATA, namely, Bajaur Agency, Mohamand Agency, Khyber Agency, Orakzai Agency, Kurram Agency, North Waziristan Agency, South Waziristan Agency, Malakand Agency, District Swat, District Buner, District Shangla, District Upper Dir and District Lower Dir, shall be charged to fifty per cent of the rate leviable under sub-section (1) of section 3 of the Sales Tax Act, 1990, if supplied to a person in any area where the Sales Tax Act, 1990, is applicable.

180(I)/2011 5th March 2011

Sales tax shall be charged at the lower rate of fifty per cent of the rate leviable under sub-section (1) of the said section on the supplies made of goods, other than cement, sugar, beverages and cigarettes, by the registered persons located in districts of Hangu, Bannu, Tank, Kohat, Chitral, Charsadda, Peshawar, Dera Ismael Khan, Batagram, Lakki Marwat, Sawabi, Nowshera and Mardan.

J.A.S.B. & Associates Chartered Accountants

42

BUDGET DIGEST 2013-14

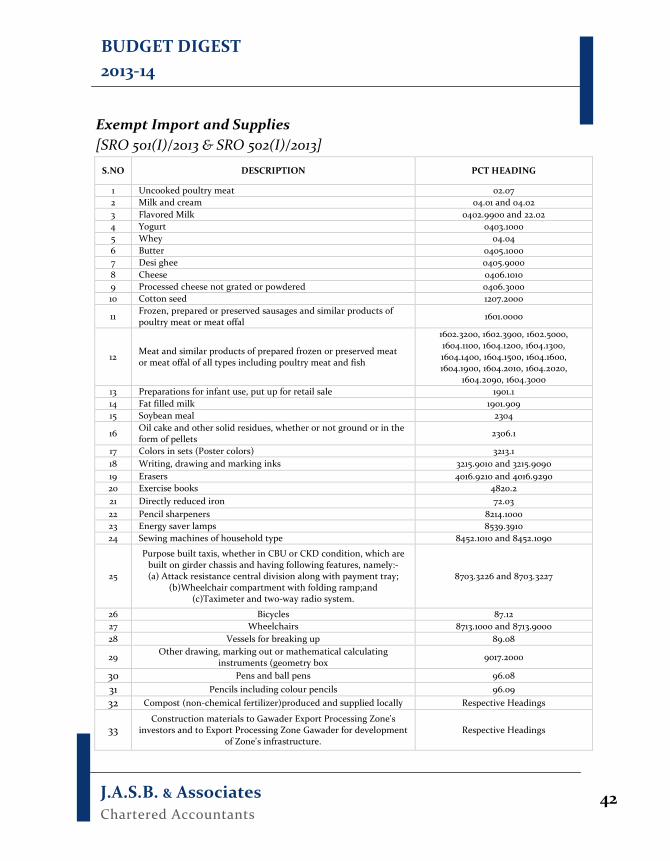

Exempt Import and Supplies [SRO 501(I)/2013 & SRO 502(I)/2013]

S.NO DESCRIPTION PCT HEADING

1 Uncooked poultry meat 02.07 2 Milk and cream 04.01 and 04.02 3 Flavored Milk 0402.9900 and 22.02 4 Yogurt 0403.1000 5 Whey 04.04 6 Butter 0405.1000 7 Desi ghee 0405.9000 8 Cheese 0406.1010 9 Processed cheese not grated or powdered 0406.3000 10 Cotton seed 1207.2000

11 Frozen, prepared or preserved sausages and similar products of poultry meat or meat offal 1601.0000

12 Meat and similar products of prepared frozen or preserved meat or meat offal of all types including poultry meat and fish

1602.3200, 1602.3900, 1602.5000, 1604.1100, 1604.1200, 1604.1300, 1604.1400, 1604.1500, 1604.1600, 1604.1900, 1604.2010, 1604.2020,

1604.2090, 1604.3000 13 Preparations for infant use, put up for retail sale 1901.1 14 Fat filled milk 1901.909 15 Soybean meal 2304

16 Oil cake and other solid residues, whether or not ground or in the form of pellets 2306.1

17 Colors in sets (Poster colors) 3213.1 18 Writing, drawing and marking inks 3215.9010 and 3215.9090 19 Erasers 4016.9210 and 4016.9290 20 Exercise books 4820.2 21 Directly reduced iron 72.03 22 Pencil sharpeners 8214.1000 23 Energy saver lamps 8539.3910 24 Sewing machines of household type 8452.1010 and 8452.1090

25

Purpose built taxis, whether in CBU or CKD condition, which are built on girder chassis and having following features, namely:- (a) Attack resistance central division along with payment tray;

(b)Wheelchair compartment with folding ramp;and (c)Taximeter and two-way radio system.

8703.3226 and 8703.3227

26 Bicycles 87.12 27 Wheelchairs 8713.1000 and 8713.9000 28 Vessels for breaking up 89.08

29 Other drawing, marking out or mathematical calculating instruments (geometry box 9017.2000

30 Pens and ball pens 96.08 31 Pencils including colour pencils 96.09 32 Compost (non-chemical fertilizer)produced and supplied locally Respective Headings

33 Construction materials to Gawader Export Processing Zone's

investors and to Export Processing Zone Gawader for development of Zone's infrastructure.

Respective Headings

J.A.S.B. & Associates Chartered Accountants

43

BUDGET DIGEST 2013-14

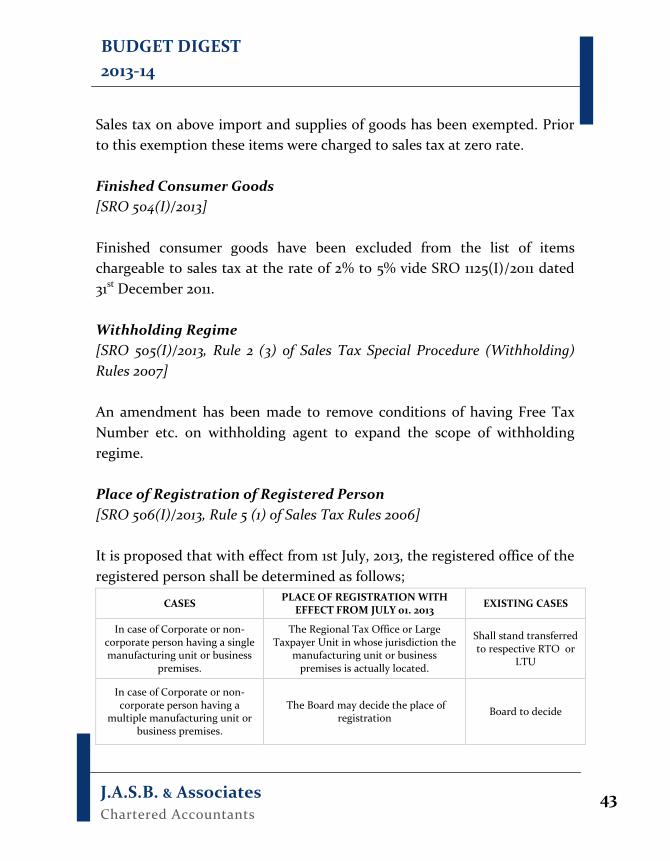

Sales tax on above import and supplies of goods has been exempted. Prior to this exemption these items were charged to sales tax at zero rate. Finished Consumer Goods [SRO 504(I)/2013] Finished consumer goods have been excluded from the list of items chargeable to sales tax at the rate of 2% to 5% vide SRO 1125(I)/2011 dated 31st December 2011. Withholding Regime [SRO 505(I)/2013, Rule 2 (3) of Sales Tax Special Procedure (Withholding) Rules 2007] An amendment has been made to remove conditions of having Free Tax Number etc. on withholding agent to expand the scope of withholding regime. Place of Registration of Registered Person [SRO 506(I)/2013, Rule 5 (1) of Sales Tax Rules 2006] It is proposed that with effect from 1st July, 2013, the registered office of the registered person shall be determined as follows;

CASES PLACE OF REGISTRATION WITH EFFECT FROM JULY 01. 2013 EXISTING CASES

In case of Corporate or non-corporate person having a single manufacturing unit or business

premises.

The Regional Tax Office or Large Taxpayer Unit in whose jurisdiction the

manufacturing unit or business premises is actually located.

Shall stand transferred to respective RTO or

LTU

In case of Corporate or non-corporate person having a

multiple manufacturing unit or business premises.

The Board may decide the place of registration Board to decide

J.A.S.B. & Associates Chartered Accountants

44

BUDGET DIGEST 2013-14

Extra Sales Tax on Supplies of Electric Power & Natural Gas [SRO 509(I)/2013, SRO 510(I)/2013 & Sales Tax Special Procedure Rules 2007] Extra sales tax at the rate of 5% shall be charged on unregistered or inactive taxpayers having industrial or commercial connections of electric power and gas having monthly bill in excess of Rs.15,000. Special procedures for collection and payment of extra tax on supplies of electric power and natural gas consumed by unregistered and inactive taxpayers has been framed and inserted as Chapter IVA in Sales Tax Special Procedure Rules 2007 to provide the legal cover.

J.A.S.B. & Associates Chartered Accountants

45

BUDGET DIGEST 2013-14

5. FEDERAL EXCISE DUTY Duties Specified in First Schedule to be Levied [Section 3 (3A)] The Bill proposes to insert a new sub-section (3A) to charge further duty at the rate of 2% of the excisable goods and services made to unregistered person. Records [Section 17(1)(da)] It is proposed to insert a new clause (da) to prescribe inward and outward gate passes and transport receipts as legal documents for the purposes of federal excise duty. Appeals to the Commissioner (Appeals) [Section 33(1A)] The Bill proposes to insert a new sub-section to allow Commissioner (Appeals) to grant stay of thirty days in aggregate to relax taxpayer from undue hardship in payment of tax to be recovered. Powers of Board or Commissioner to Pass Certain Orders [Section 35 (3)] An explanation is proposed to be inserted to declare that powers of the Board, Commissioner or Officer of Inland Revenue under section 35,45 and 46 are independent of powers of the Board, Commissioner or Officer of Inland Revenue under section 42B “Selection for the Audit by the Board”.

J.A.S.B. & Associates Chartered Accountants

46

BUDGET DIGEST 2013-14

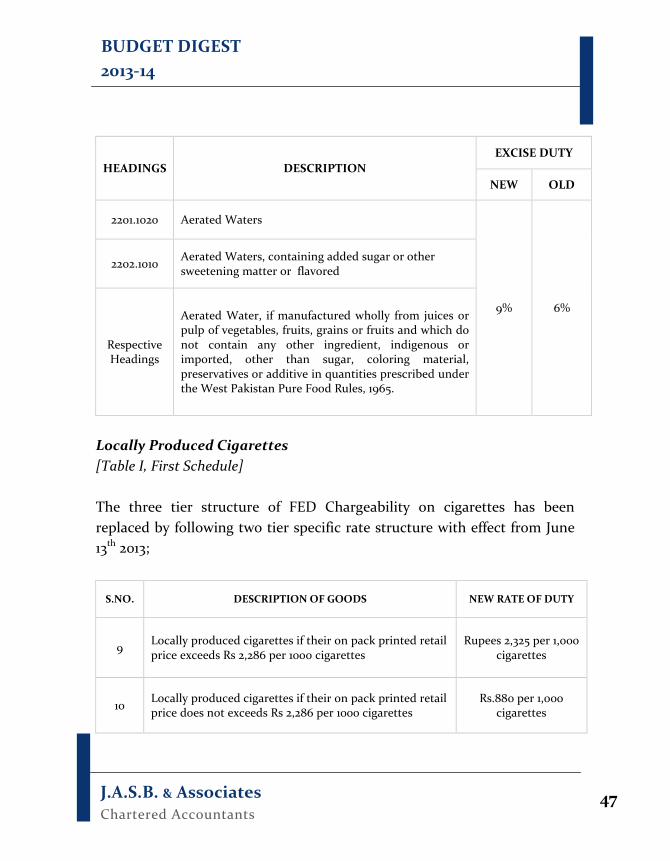

Reward to Inland Revenue Officers and Officials [Section 42C] The Bill proposes to insert a new section to provide cash rewards to officials of Inland Revenue for their meritorious conduct in full or partial realization of excise duty and other taxes from cases of concealment or evasion of excise duty and other taxes. Access to Records and Posting of Inland Revenue Staff [Section 45(2)] The Bill proposes an amendment to equate the powers of Board and Chief Commissioner regarding posting of Inland Revenue Officer to monitor production, removal or sale of goods and the stock position or the maintenance of records. Monitoring or Tracking by Electronic or Other Means [Section 45A] The Bill proposes to insert a new section to provide legal powers for monitoring or tracking by electronic or other means of productions, sales, clearances, stocks etc.of any registered person or class of persons etc. Aerated Water etc. [Table 1, First Schedule] The rate of Excise Duty is proposed to be increased from 6% to 9% on the retail price for the following items of aerated water;

J.A.S.B. & Associates Chartered Accountants

47

BUDGET DIGEST 2013-14

HEADINGS DESCRIPTION EXCISE DUTY

NEW OLD

2201.1020 Aerated Waters

9% 6%

2202.1010 Aerated Waters, containing added sugar or other sweetening matter or flavored

Respective Headings

Aerated Water, if manufactured wholly from juices or pulp of vegetables, fruits, grains or fruits and which do not contain any other ingredient, indigenous or imported, other than sugar, coloring material, preservatives or additive in quantities prescribed under the West Pakistan Pure Food Rules, 1965.

Locally Produced Cigarettes [Table I, First Schedule] The three tier structure of FED Chargeability on cigarettes has been replaced by following two tier specific rate structure with effect from June 13th 2013;

S.NO. DESCRIPTION OF GOODS NEW RATE OF DUTY

9 Locally produced cigarettes if their on pack printed retail price exceeds Rs 2,286 per 1000 cigarettes

Rupees 2,325 per 1,000 cigarettes

10 Locally produced cigarettes if their on pack printed retail price does not exceeds Rs 2,286 per 1000 cigarettes

Rs.880 per 1,000 cigarettes

J.A.S.B. & Associates Chartered Accountants

48

BUDGET DIGEST 2013-14

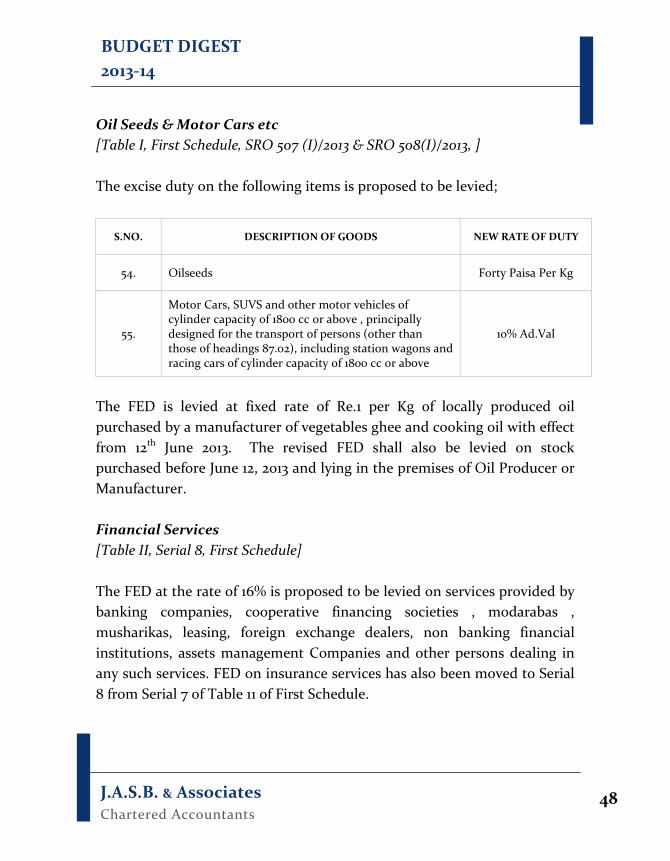

Oil Seeds & Motor Cars etc [Table I, First Schedule, SRO 507 (I)/2013 & SRO 508(I)/2013, ] The excise duty on the following items is proposed to be levied;

S.NO. DESCRIPTION OF GOODS NEW RATE OF DUTY

54. Oilseeds Forty Paisa Per Kg

55.

Motor Cars, SUVS and other motor vehicles of cylinder capacity of 1800 cc or above , principally designed for the transport of persons (other than those of headings 87.02), including station wagons and racing cars of cylinder capacity of 1800 cc or above

10% Ad.Val

The FED is levied at fixed rate of Re.1 per Kg of locally produced oil purchased by a manufacturer of vegetables ghee and cooking oil with effect from 12th June 2013. The revised FED shall also be levied on stock purchased before June 12, 2013 and lying in the premises of Oil Producer or Manufacturer. Financial Services [Table II, Serial 8, First Schedule] The FED at the rate of 16% is proposed to be levied on services provided by banking companies, cooperative financing societies , modarabas , musharikas, leasing, foreign exchange dealers, non banking financial institutions, assets management Companies and other persons dealing in any such services. FED on insurance services has also been moved to Serial 8 from Serial 7 of Table 11 of First Schedule.

J.A.S.B. & Associates Chartered Accountants

49

BUDGET DIGEST 2013-14

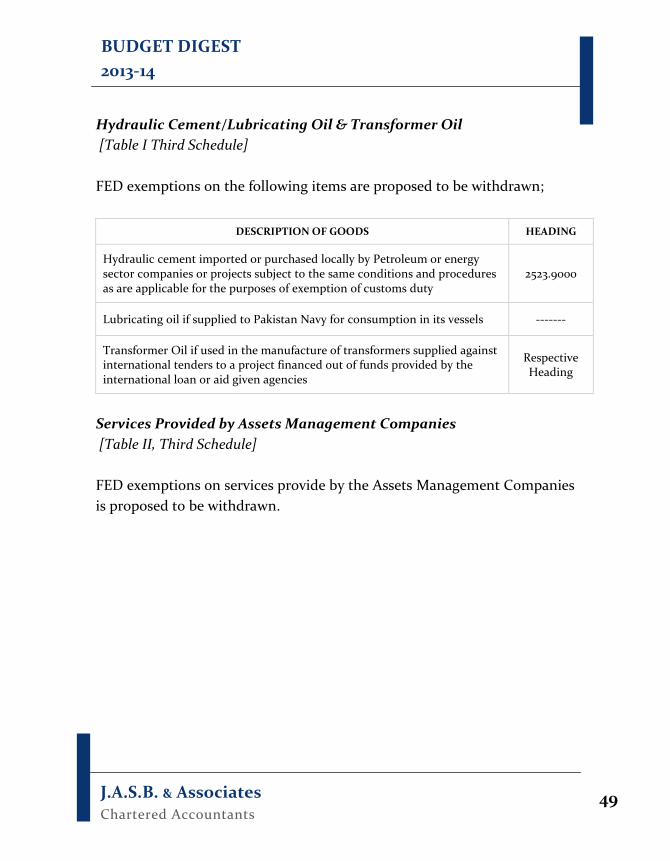

Hydraulic Cement/Lubricating Oil & Transformer Oil [Table I Third Schedule] FED exemptions on the following items are proposed to be withdrawn;

DESCRIPTION OF GOODS HEADING

Hydraulic cement imported or purchased locally by Petroleum or energy sector companies or projects subject to the same conditions and procedures as are applicable for the purposes of exemption of customs duty

2523.9000

Lubricating oil if supplied to Pakistan Navy for consumption in its vessels -------

Transformer Oil if used in the manufacture of transformers supplied against international tenders to a project financed out of funds provided by the international loan or aid given agencies

Respective Heading

Services Provided by Assets Management Companies [Table II, Third Schedule] FED exemptions on services provide by the Assets Management Companies is proposed to be withdrawn.

J.A.S.B. & Associates Chartered Accountants

50

BUDGET DIGEST 2013-14

6. CUSTOMS Goods Declaration [Section 2(la] Amendment is proposed in the definition of “Goods Declaration” to provide legal cover for filing of “Good Declaration” under Transshipment Rules for WeBOC (Web Based One Customs). Establishment of Directorate General of Input Output Co-efficient Organization [Section 3DDD] The bill proposes to form a new directorate as an administrative measure for better enforcement of enactment. The Directorate has as many Directors, Additional Directors, Deputy Directors, Assistant Directors and such other officers as the Board may appoint through notification in the official Gazette. Provision of Security and Accommodation at Customs -ports [Section 14-A] The Bill proposes to substitute section 14A to bind the custodian of goods and terminal handlers to provide at their own cost adequate security, accommodation for residential purposes, office, examination of goods, detention and storage of goods and for other departmental requirements etc. to Customs Authorities and to entertain the delay and detention certificates issued by the Customs and refund of demurrage charges.

J.A.S.B. & Associates Chartered Accountants

51

BUDGET DIGEST 2013-14

False Statement, Error etc [Section 32(4)] To rectify the earlier erroneous omission, the bill proposed to insert “or sub-section (3A)” in sub-section (4) of Section 32 to empowers the appropriate officer to determine payable amount on account of post clearance audit. Provisional Determination of Liability [Section 81] The Bill seeks to omit words “post-dated cheques” from Section 81 to facilitate Collectorates facing enforcement issues in encashment of post dated cheques (PDC) for improvement in government’s legitimate revenue. It is also proposed to replace the words “post dated cheques” with “pay order” in ‘Explanation’ of Section 81. Clearance for Home Consumption [Section 83(2)] It is proposed to omit reference of Section 80-A in Section 83(2) as it is meaningless since section 80-A has been omitted by Finance Act, 2005. Power of Adjudication [Section 179] The Bill proposes to insert a new proviso to fix jurisdiction and powers of officers in case of export of goods for the purposes of adjudication of customs in terms of FOB value and twice their respective limits.

J.A.S.B. & Associates Chartered Accountants

52

BUDGET DIGEST 2013-14

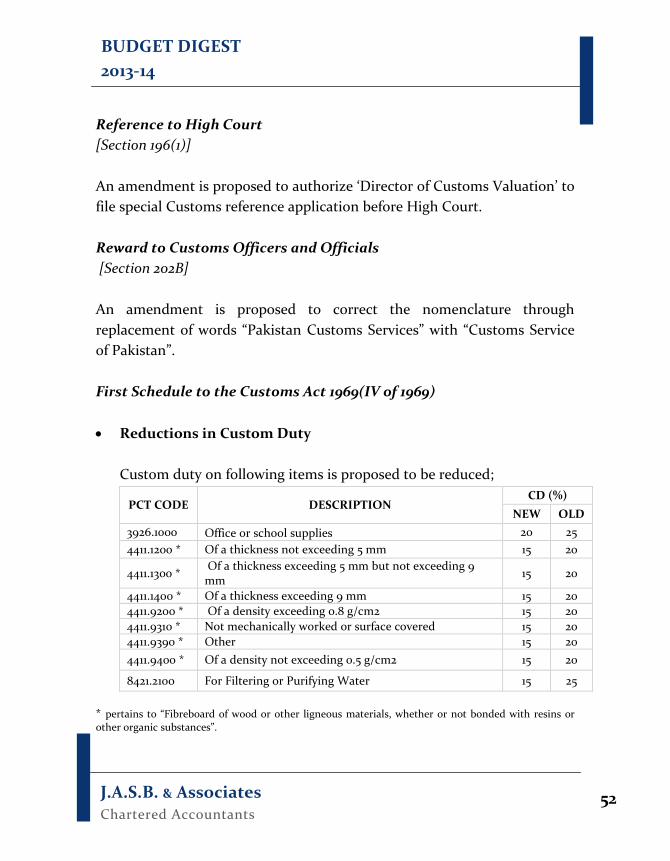

Reference to High Court [Section 196(1)] An amendment is proposed to authorize ‘Director of Customs Valuation’ to file special Customs reference application before High Court. Reward to Customs Officers and Officials [Section 202B] An amendment is proposed to correct the nomenclature through replacement of words “Pakistan Customs Services” with “Customs Service of Pakistan”. First Schedule to the Customs Act 1969(IV of 1969) • Reductions in Custom Duty

Custom duty on following items is proposed to be reduced;

PCT CODE DESCRIPTION CD (%)

NEW OLD 3926.1000 Office or school supplies 20 25 4411.1200 * Of a thickness not exceeding 5 mm 15 20

4411.1300 * Of a thickness exceeding 5 mm but not exceeding 9 mm 15 20

4411.1400 * Of a thickness exceeding 9 mm 15 20 4411.9200 * Of a density exceeding 0.8 g/cm2 15 20 4411.9310 * Not mechanically worked or surface covered 15 20 4411.9390 * Other 15 20 4411.9400 * Of a density not exceeding 0.5 g/cm2 15 20

8421.2100 For Filtering or Purifying Water 15 25 * pertains to “Fibreboard of wood or other ligneous materials, whether or not bonded with resins or other organic substances”.

J.A.S.B. & Associates Chartered Accountants

53

BUDGET DIGEST 2013-14

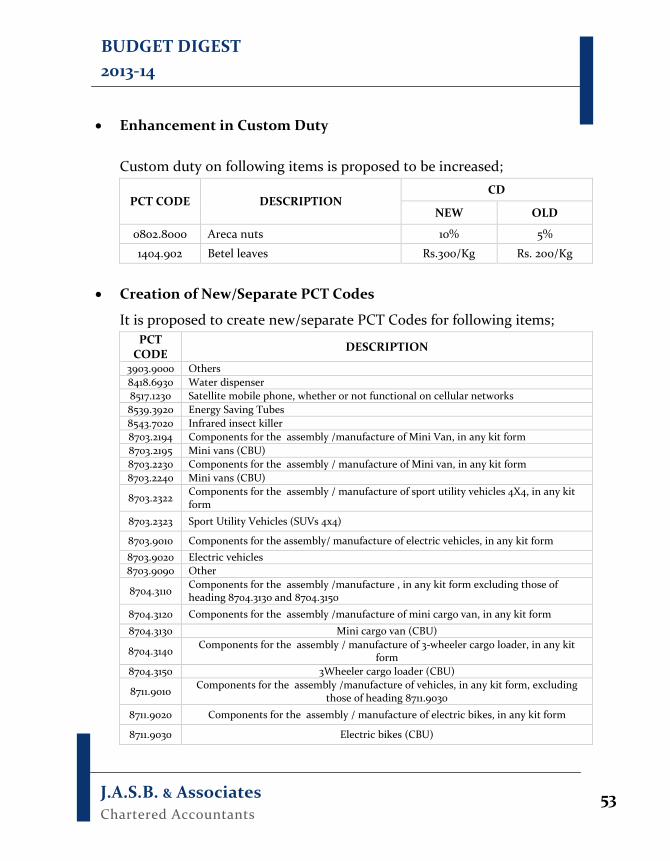

• Enhancement in Custom Duty

Custom duty on following items is proposed to be increased;

PCT CODE DESCRIPTION CD

NEW OLD

0802.8000 Areca nuts 10% 5%

1404.902 Betel leaves Rs.300/Kg Rs. 200/Kg

• Creation of New/Separate PCT Codes

It is proposed to create new/separate PCT Codes for following items; PCT

CODE DESCRIPTION

3903.9000 Others 8418.6930 Water dispenser 8517.1230 Satellite mobile phone, whether or not functional on cellular networks 8539.3920 Energy Saving Tubes 8543.7020 Infrared insect killer 8703.2194 Components for the assembly /manufacture of Mini Van, in any kit form 8703.2195 Mini vans (CBU) 8703.2230 Components for the assembly / manufacture of Mini van, in any kit form 8703.2240 Mini vans (CBU)

8703.2322 Components for the assembly / manufacture of sport utility vehicles 4X4, in any kit form

8703.2323 Sport Utility Vehicles (SUVs 4x4)

8703.9010 Components for the assembly/ manufacture of electric vehicles, in any kit form 8703.9020 Electric vehicles 8703.9090 Other

8704.3110 Components for the assembly /manufacture , in any kit form excluding those of heading 8704.3130 and 8704.3150

8704.3120 Components for the assembly /manufacture of mini cargo van, in any kit form 8704.3130 Mini cargo van (CBU)

8704.3140 Components for the assembly / manufacture of 3-wheeler cargo loader, in any kit form

8704.3150 3Wheeler cargo loader (CBU)

8711.9010 Components for the assembly /manufacture of vehicles, in any kit form, excluding those of heading 8711.9030

8711.9020 Components for the assembly / manufacture of electric bikes, in any kit form

8711.9030 Electric bikes (CBU)

J.A.S.B. & Associates Chartered Accountants

54

BUDGET DIGEST 2013-14

Notifications Notifications issued as part of Budget 2013-14 are effective from 13th June 2013. [SRO 495(I)/2013] Certain amendments has been made in SRO 655(I)/2006 dated 22nd June 2006 with respect to use of “Customs Computerized System” instead of “PaCCS or One Customs System” Changes in Concessionary Notification SRO 656(I)/2006) dated June 22, 2006 with respect to Components (sub-components , components assembly but excludes consumables) imported in any kit form and direct materials for assembly or manufacture of vehicles [SRO 496(I)/2013 &] Amendments have been made in the above said notification with respect to use of “Customs Computerized System” instead of “PaCCS or One Customs System”. Concessionary duty on the following items has been withdrawn where facility of assembly or manufacture under firm contract is used by importer

HS CODE DESCRIPTION CD (%)

NEW OLD

8703.2115 Auto Rickshaw (CBU) Components for assembly/manufacture in any kit form

50 20

8704.3150 3-Wheeler Cargo Loader (New Addition)

60 0

87.11 Motor Cycles Components for assembly/manufacture in any kit form

65 15

J.A.S.B. & Associates Chartered Accountants

55

BUDGET DIGEST 2013-14

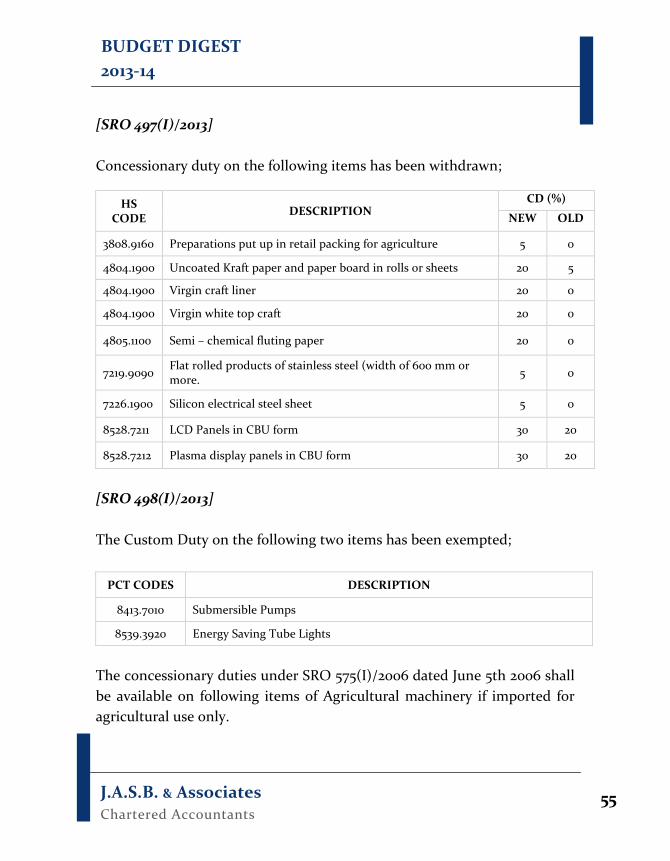

[SRO 497(I)/2013] Concessionary duty on the following items has been withdrawn;

HS CODE DESCRIPTION

CD (%)

NEW OLD

3808.9160 Preparations put up in retail packing for agriculture 5 0

4804.1900 Uncoated Kraft paper and paper board in rolls or sheets 20 5

4804.1900 Virgin craft liner 20 0

4804.1900 Virgin white top craft 20 0

4805.1100 Semi – chemical fluting paper 20 0

7219.9090 Flat rolled products of stainless steel (width of 600 mm or more. 5 0

7226.1900 Silicon electrical steel sheet 5 0

8528.7211 LCD Panels in CBU form 30 20

8528.7212 Plasma display panels in CBU form 30 20

[SRO 498(I)/2013] The Custom Duty on the following two items has been exempted;

PCT CODES DESCRIPTION

8413.7010 Submersible Pumps

8539.3920 Energy Saving Tube Lights

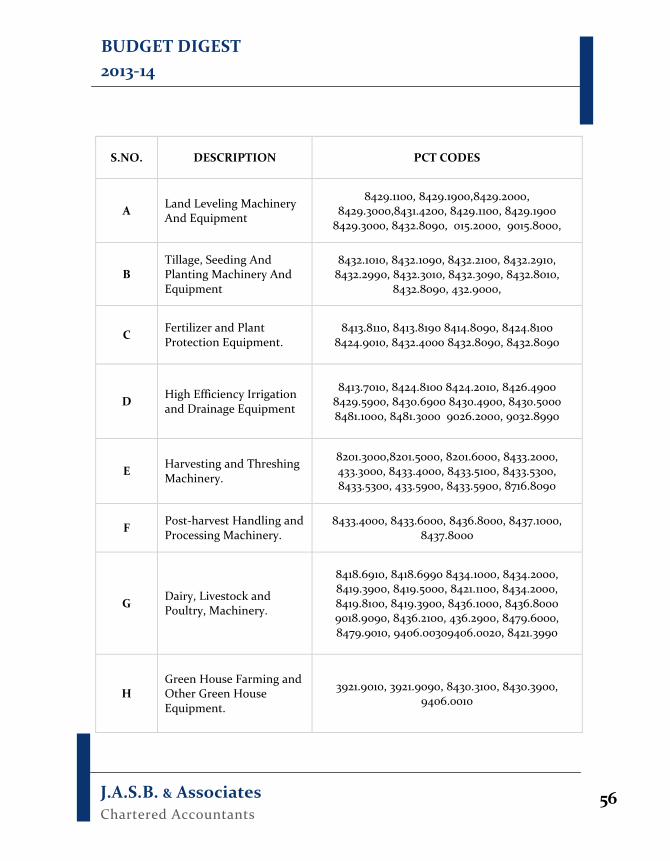

The concessionary duties under SRO 575(I)/2006 dated June 5th 2006 shall be available on following items of Agricultural machinery if imported for agricultural use only.

J.A.S.B. & Associates Chartered Accountants

56

BUDGET DIGEST 2013-14

S.NO. DESCRIPTION PCT CODES

A Land Leveling Machinery And Equipment

8429.1100, 8429.1900,8429.2000, 8429.3000,8431.4200, 8429.1100, 8429.1900

8429.3000, 8432.8090, 015.2000, 9015.8000,

B Tillage, Seeding And Planting Machinery And Equipment

8432.1010, 8432.1090, 8432.2100, 8432.2910, 8432.2990, 8432.3010, 8432.3090, 8432.8010,

8432.8090, 432.9000,

C Fertilizer and Plant Protection Equipment.

8413.8110, 8413.8190 8414.8090, 8424.8100 8424.9010, 8432.4000 8432.8090, 8432.8090

D High Efficiency Irrigation and Drainage Equipment

8413.7010, 8424.8100 8424.2010, 8426.4900 8429.5900, 8430.6900 8430.4900, 8430.5000 8481.1000, 8481.3000 9026.2000, 9032.8990

E Harvesting and Threshing Machinery.

8201.3000,8201.5000, 8201.6000, 8433.2000, 433.3000, 8433.4000, 8433.5100, 8433.5300, 8433.5300, 433.5900, 8433.5900, 8716.8090

F Post-harvest Handling and Processing Machinery.

8433.4000, 8433.6000, 8436.8000, 8437.1000, 8437.8000

G Dairy, Livestock and Poultry, Machinery.

8418.6910, 8418.6990 8434.1000, 8434.2000, 8419.3900, 8419.5000, 8421.1100, 8434.2000, 8419.8100, 8419.3900, 8436.1000, 8436.8000 9018.9090, 8436.2100, 436.2900, 8479.6000, 8479.9010, 9406.00309406.0020, 8421.3990

H Green House Farming and Other Green House Equipment.

3921.9010, 3921.9090, 8430.3100, 8430.3900, 9406.0010

J.A.S.B. & Associates Chartered Accountants

57

BUDGET DIGEST 2013-14

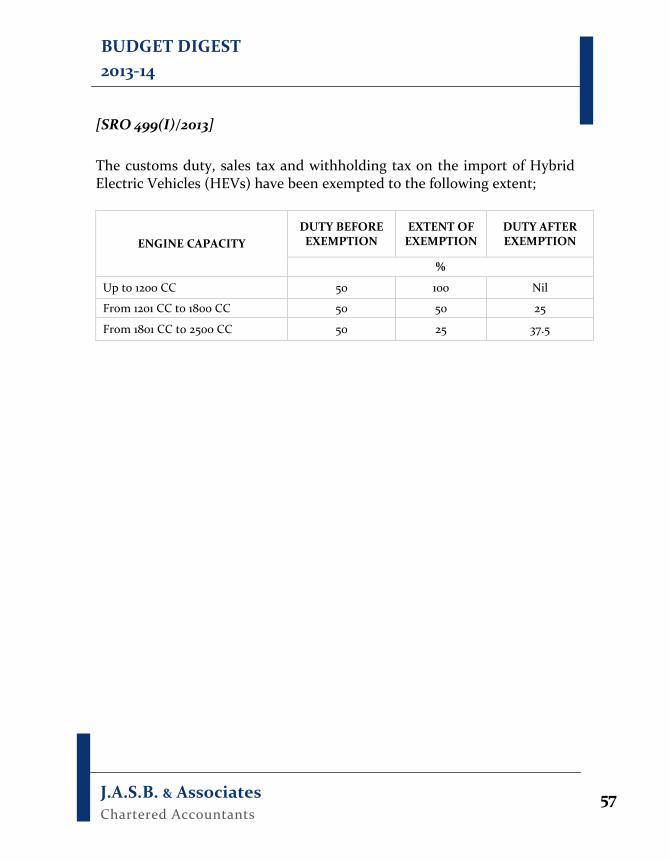

[SRO 499(I)/2013] The customs duty, sales tax and withholding tax on the import of Hybrid Electric Vehicles (HEVs) have been exempted to the following extent;

ENGINE CAPACITY DUTY BEFORE EXEMPTION

EXTENT OF EXEMPTION

DUTY AFTER EXEMPTION

%

Up to 1200 CC 50 100 Nil

From 1201 CC to 1800 CC 50 50 25

From 1801 CC to 2500 CC 50 25 37.5

J.A.S.B. & Associates Chartered Accountants

58

BUDGET DIGEST 2013-14

Working Notes

J.A.S.B. & Associates Chartered Accountants

59

BUDGET DIGEST 2013-14

J.A.S.B. & Associates Chartered Accountants

60

BUDGET DIGEST 2013-14