Embed Size (px)

Citation preview

Jarir Marketing Company

Reinstating Coverage

Hold 12-Month Target Price SAR 212.00

Unique Retail Proposition

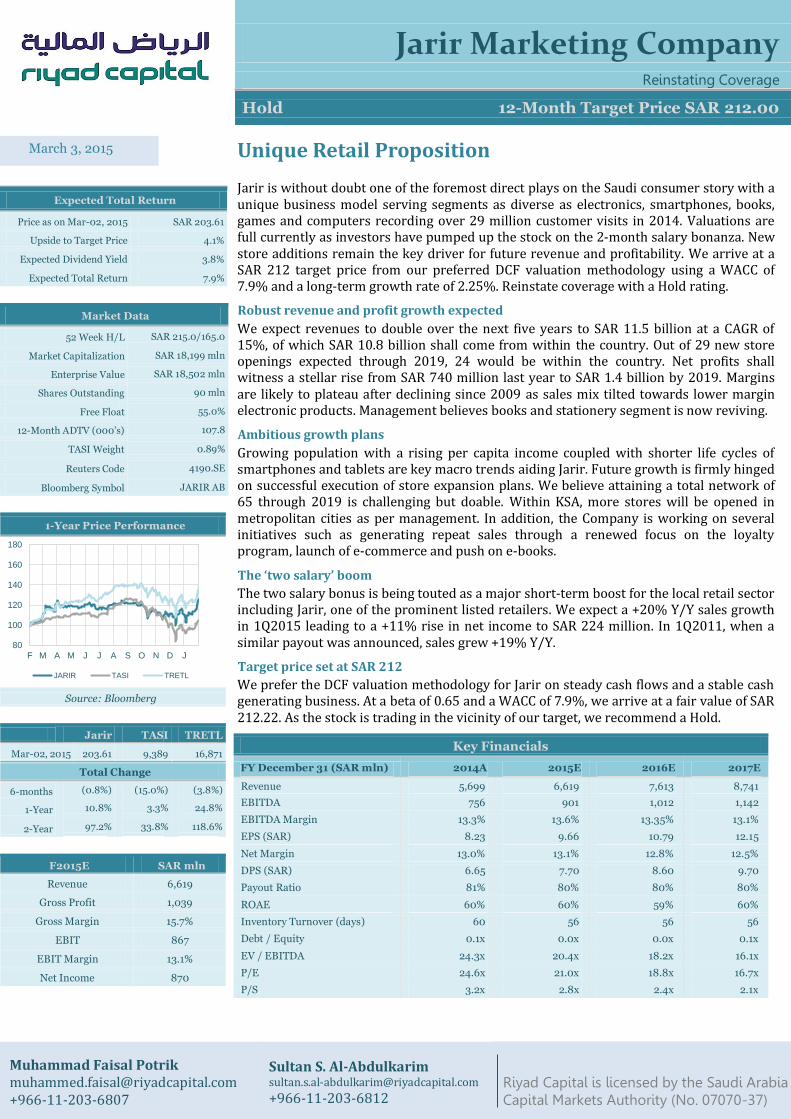

Jarir is without doubt one of the foremost direct plays on the Saudi consumer story with a unique business model serving segments as diverse as electronics, smartphones, books, games and computers recording over 29 million customer visits in 2014. Valuations are full currently as investors have pumped up the stock on the 2-month salary bonanza. New store additions remain the key driver for future revenue and profitability. We arrive at a SAR 212 target price from our preferred DCF valuation methodology using a WACC of 7.9% and a long-term growth rate of 2.25%. Reinstate coverage with a Hold rating.

Robust revenue and profit growth expected

We expect revenues to double over the next five years to SAR 11.5 billion at a CAGR of 15%, of which SAR 10.8 billion shall come from within the country. Out of 29 new store openings expected through 2019, 24 would be within the country. Net profits shall witness a stellar rise from SAR 740 million last year to SAR 1.4 billion by 2019. Margins are likely to plateau after declining since 2009 as sales mix tilted towards lower margin electronic products. Management believes books and stationery segment is now reviving.

Ambitious growth plans

Growing population with a rising per capita income coupled with shorter life cycles of smartphones and tablets are key macro trends aiding Jarir. Future growth is firmly hinged on successful execution of store expansion plans. We believe attaining a total network of 65 through 2019 is challenging but doable. Within KSA, more stores will be opened in metropolitan cities as per management. In addition, the Company is working on several initiatives such as generating repeat sales through a renewed focus on the loyalty program, launch of e-commerce and push on e-books.

The ‘two salary’ boom

The two salary bonus is being touted as a major short-term boost for the local retail sector including Jarir, one of the prominent listed retailers. We expect a +20% Y/Y sales growth in 1Q2015 leading to a +11% rise in net income to SAR 224 million. In 1Q2011, when a similar payout was announced, sales grew +19% Y/Y.

Target price set at SAR 212

We prefer the DCF valuation methodology for Jarir on steady cash flows and a stable cash generating business. At a beta of 0.65 and a WACC of 7.9%, we arrive at a fair value of SAR 212.22. As the stock is trading in the vicinity of our target, we recommend a Hold.

Key Financials

FY December 31 (SAR mln) 2014A 2015E 2016E 2017E

Revenue 5,699 6,619 7,613 8,741

EBITDA 756 901 1,012 1,142

EBITDA Margin 13.3% 13.6% 13.35% 13.1%

EPS (SAR) 8.23 9.66 10.79 12.15

Net Margin 13.0% 13.1% 12.8% 12.5%

DPS (SAR) 6.65 7.70 8.60 9.70

Payout Ratio 81% 80% 80% 80%

ROAE 60% 60% 59% 60%

Inventory Turnover (days) 60 56 56 56

Debt / Equity 0.1x 0.0x 0.0x 0.1x

EV / EBITDA 24.3x 20.4x 18.2x 16.1x

P/E 24.6x 21.0x 18.8x 16.7x

P/S 3.2x 2.8x 2.4x 2.1x

March 3, 2015

Expected Total Return

Price as on Mar-02, 2015 SAR 203.61

Upside to Target Price 4.1%

Expected Dividend Yield 3.8%

Expected Total Return 7.9%

Market Data

52 Week H/L SAR 215.0/165.0

Market Capitalization SAR 18,199 mln

Enterprise Value SAR 18,502 mln

Shares Outstanding 90 mln

Free Float 55.0%

12-Month ADTV (000’s) 107.8

TASI Weight 0.89%

Reuters Code 4190.SE

Bloomberg Symbol JARIR AB

1-Year Price Performance

Source: Bloomberg

Jarir TASI TRETL

Mar-02, 2015 203.61 9,389 16,871

Total Change

6-months (0.8%)

(15.0%)

(3.8%)

1-Year 10.8%

3.3%

24.8%

2-Year 97.2%

33.8%

118.6%

F2015E SAR mln

Revenue 6,619

Gross Profit 1,039

Gross Margin 15.7%

EBIT 867

EBIT Margin 13.1%

Net Income 870

80

100

120

140

160

180

F M A M J J A S O N D J

JARIR TASI TRETL

Muhammad Faisal Potrik [email protected] +966-11-203-6807

Sultan S. Al-Abdulkarim [email protected]

+966-11-203-6812 Riyad Capital is licensed by the Saudi Arabia Capital Markets Authority (No. 07070-37)

Jarir Marketing Company

Reinstating Coverage

March 3, 2015 | 2

Reinstating Coverage

We reinstate coverage on Jarir Marketing Company (Jarir) with a Hold rating and a SAR

212 target price. Presented below is a recap of the year 2014, our expectations for the

Company going forward as well as our 1Q2015 forecasts.

Recap of 2014

4Q positively surprises

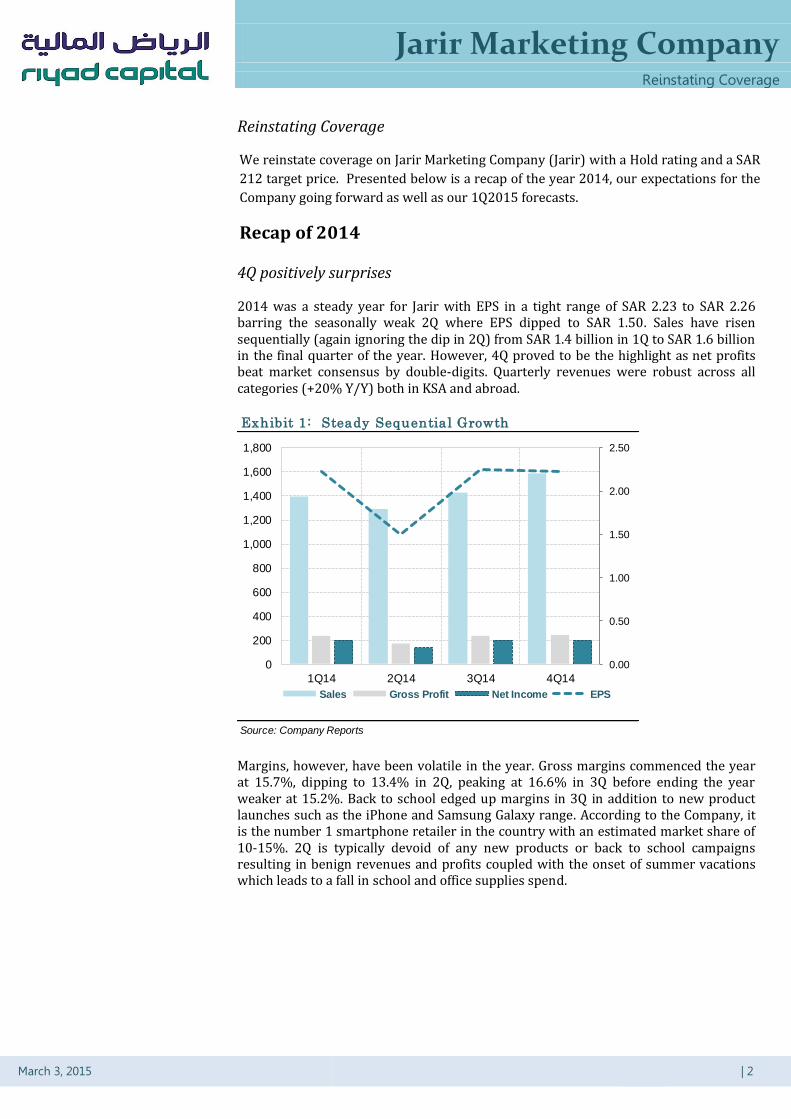

2014 was a steady year for Jarir with EPS in a tight range of SAR 2.23 to SAR 2.26 barring the seasonally weak 2Q where EPS dipped to SAR 1.50. Sales have risen sequentially (again ignoring the dip in 2Q) from SAR 1.4 billion in 1Q to SAR 1.6 billion in the final quarter of the year. However, 4Q proved to be the highlight as net profits beat market consensus by double-digits. Quarterly revenues were robust across all categories (+20% Y/Y) both in KSA and abroad.

Margins, however, have been volatile in the year. Gross margins commenced the year at 15.7%, dipping to 13.4% in 2Q, peaking at 16.6% in 3Q before ending the year weaker at 15.2%. Back to school edged up margins in 3Q in addition to new product launches such as the iPhone and Samsung Galaxy range. According to the Company, it is the number 1 smartphone retailer in the country with an estimated market share of 10-15%. 2Q is typically devoid of any new products or back to school campaigns resulting in benign revenues and profits coupled with the onset of summer vacations which leads to a fall in school and office supplies spend.

Exhibit 1: Steady Sequential Growth

Source: Company Reports

0.00

0.50

1.00

1.50

2.00

2.50

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

1Q14 2Q14 3Q14 4Q14

Sales Gross Profit Net Income EPS

Jarir Marketing Company

Reinstating Coverage

March 3, 2015 | 3

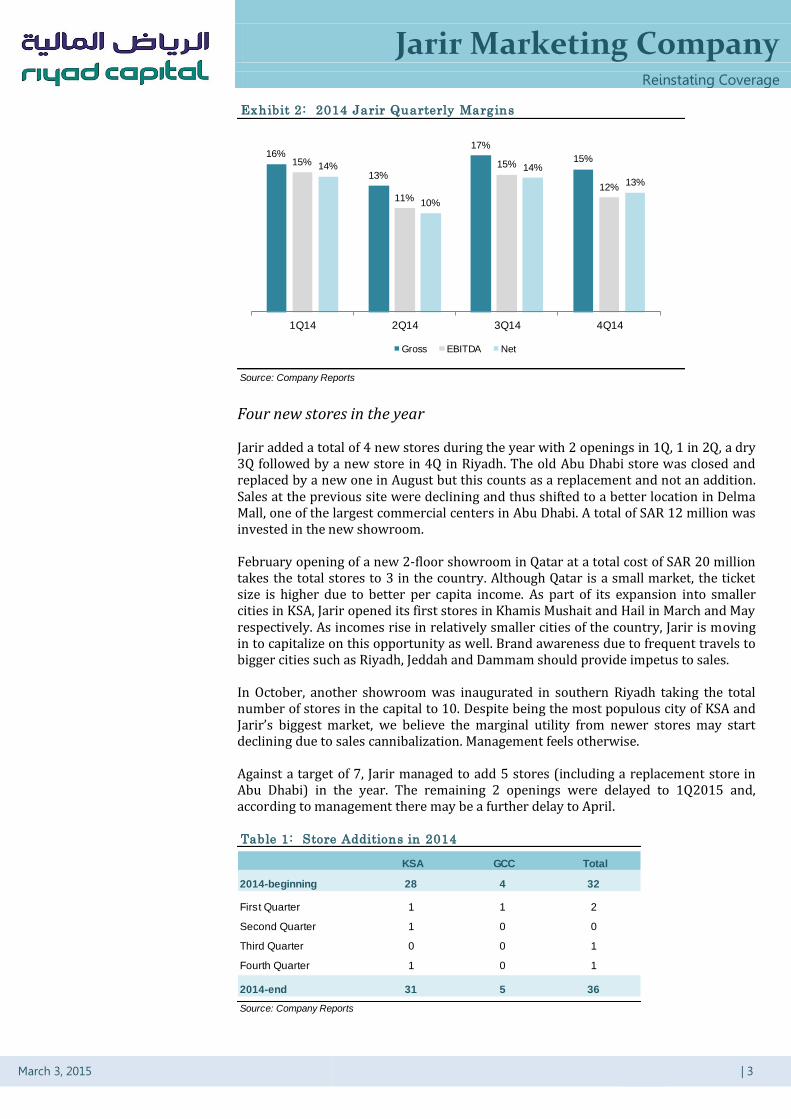

Four new stores in the year

Jarir added a total of 4 new stores during the year with 2 openings in 1Q, 1 in 2Q, a dry 3Q followed by a new store in 4Q in Riyadh. The old Abu Dhabi store was closed and replaced by a new one in August but this counts as a replacement and not an addition. Sales at the previous site were declining and thus shifted to a better location in Delma Mall, one of the largest commercial centers in Abu Dhabi. A total of SAR 12 million was invested in the new showroom.

February opening of a new 2-floor showroom in Qatar at a total cost of SAR 20 million takes the total stores to 3 in the country. Although Qatar is a small market, the ticket size is higher due to better per capita income. As part of its expansion into smaller cities in KSA, Jarir opened its first stores in Khamis Mushait and Hail in March and May respectively. As incomes rise in relatively smaller cities of the country, Jarir is moving in to capitalize on this opportunity as well. Brand awareness due to frequent travels to bigger cities such as Riyadh, Jeddah and Dammam should provide impetus to sales.

In October, another showroom was inaugurated in southern Riyadh taking the total number of stores in the capital to 10. Despite being the most populous city of KSA and Jarir’s biggest market, we believe the marginal utility from newer stores may start declining due to sales cannibalization. Management feels otherwise.

Against a target of 7, Jarir managed to add 5 stores (including a replacement store in Abu Dhabi) in the year. The remaining 2 openings were delayed to 1Q2015 and, according to management there may be a further delay to April.

Exhibit 2: 2014 Jarir Quarterly Margins

Source: Company Reports

16%

13%

17%

15%15%

11%

15%

12%

14%

10%

14%

13%

1Q14 2Q14 3Q14 4Q14

Gross EBITDA Net

Table 1: Store Additions in 2014

KSA GCC Total

2014-beginning 28 4 32

First Quarter 1 1 2

Second Quarter 1 0 0

Third Quarter 0 0 1

Fourth Quarter 1 0 1

2014-end 31 5 36

Source: Company Reports

Jarir Marketing Company

Reinstating Coverage

March 3, 2015 | 4

Salaries rise in line with revenues

2014 has seen a +9.3% rise in salary expense to SAR 104.5 million (included in G&A and S&M). Salary portion of cost of goods sold is not available. While a majority of the rise can be attributed to rising headcount as new showrooms are opened, there is an effort to increase Saudi Nationals, for which an additional cost has to be borne due to higher wages. Jarir has put the current Saudization rate at 35%+ exceeding the 30% requirement by law and plans to increase this going forward. As an example, Saudis comprise 45% of the workforce at the latest store opened in Riyadh in October, according to management. As a percentage of revenues, salary expense has fallen from 2.3% in 2009 to a steady 1.8% for the last three years.

As the Company pushes the proportion of Saudis in its workforce towards 45%, likely through new store openings, we expect salary expense to rise as a percentage of sales to close in on 2% over the next few years.

Exhibit 3: Salaries & Benefits (SAR mln)

Source: Company Reports

2.3%

2.2%2.0%

1.8% 1.8% 1.8%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

-

20

40

60

80

100

120

2009 2010 2011 2012 2013 2014

Salaries & Benefits As %age of Sales

Jarir Marketing Company

Reinstating Coverage

March 3, 2015 | 5

Future Outlook

Revenues to double in five years

We forecast revenues to double from SAR 5.7 billion in 2014 to SAR 11.5 billion through 2019. Sales growth is estimated to be higher (16.1%) in the ongoing year on the back of greater spending power as the two salary bonus is disbursed leading to higher spend on consumer items such as electronics, mobile phones, tablets and laptop computers. Between 2016 and 2019, we believe revenue growth will be in a range of 14.5% to 15.0%. One reason for slower revenue growth in 2014 (9%) was slackening in new store openings, 2 less than targeted.

As illustrated in Exhibit 4 below, wholesale revenues (to corporates and businesses) comprised only 8% of total sales in 2014 and this is likely to fall further to 6% by 2019. While Jarir has good corporate customers (such as banks, telecoms and other multinationals), demand for office supplies is not very strong vis-à-vis retail demand. There are no sales of mobile phones or computers to the corporate market. Margins are higher in this segment and any gains beyond expectations have the potential to expand profitability. Furthermore, continued addition of brick and mortar stores at a higher pace naturally enhances the share of the retail segment.

Sales within KSA comprise the overwhelming majority of total revenues. On average, 92% of total sales came from within the Kingdom in the last five years, which we expect to rise to 94% in the next five years. This is a direct result of geographical make-up of current outlets and expected opening of new stores.

We estimate KSA revenues to rise from SAR 5.2 billion last year to SAR 8.2 billion by 2017 at a CAGR of 15.8% while GCC sales are expected to increase from SAR 450 million to SAR 580 million for the same period at a CAGR of 8.8%.

Exhibit 4: Sales Projections (SAR mln)

Source: Company Reports, Riyad Capital

4,634

5,2435,699

6,619

7,613

8,741

10,009

11,463

12%

13%

9%

16%

15% 15%

15% 15%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

2012 2013 2014 2015E 2016E 2017E 2018E 2019E

Wholesale Retail Y/Y Growth

Jarir Marketing Company

Reinstating Coverage

March 3, 2015 | 6

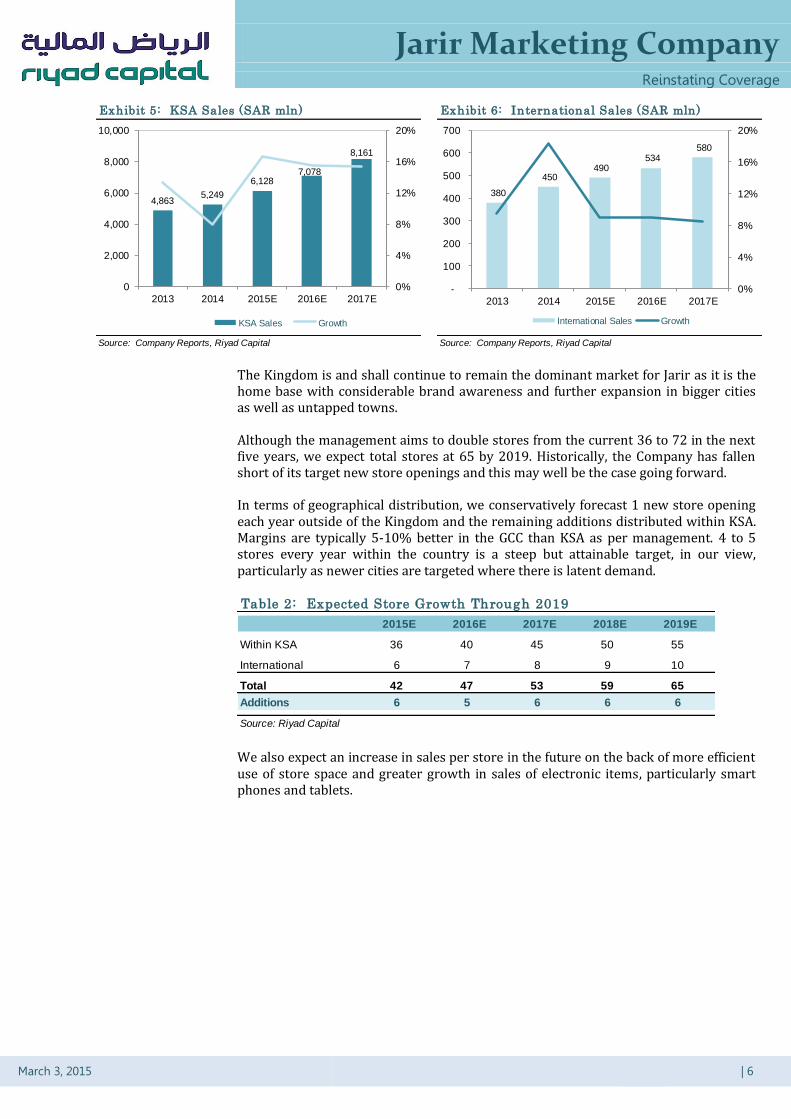

The Kingdom is and shall continue to remain the dominant market for Jarir as it is the home base with considerable brand awareness and further expansion in bigger cities as well as untapped towns.

Although the management aims to double stores from the current 36 to 72 in the next five years, we expect total stores at 65 by 2019. Historically, the Company has fallen short of its target new store openings and this may well be the case going forward.

In terms of geographical distribution, we conservatively forecast 1 new store opening each year outside of the Kingdom and the remaining additions distributed within KSA. Margins are typically 5-10% better in the GCC than KSA as per management. 4 to 5 stores every year within the country is a steep but attainable target, in our view, particularly as newer cities are targeted where there is latent demand.

We also expect an increase in sales per store in the future on the back of more efficient use of store space and greater growth in sales of electronic items, particularly smart phones and tablets.

Exhibit 5: KSA Sales (SAR mln) Exhibit 6: International Sales (SAR mln)

Source: Company Reports, Riyad Capital Source: Company Reports, Riyad Capital

4,8635,249

6,1287,078

8,161

0

2,000

4,000

6,000

8,000

10,000

2013 2014 2015E 2016E 2017E

0%

4%

8%

12%

16%

20%

KSA Sales Growth

380

450 490

534 580

-

100

200

300

400

500

600

700

2013 2014 2015E 2016E 2017E

0%

4%

8%

12%

16%

20%

International Sales Growth

Table 2: Expected Store Growth Through 2019

2015E 2016E 2017E 2018E 2019E

Within KSA 36 40 45 50 55

International 6 7 8 9 10

Total 42 47 53 59 65

Additions 6 5 6 6 6

Source: Riyad Capital

Jarir Marketing Company

Reinstating Coverage

March 3, 2015 | 7

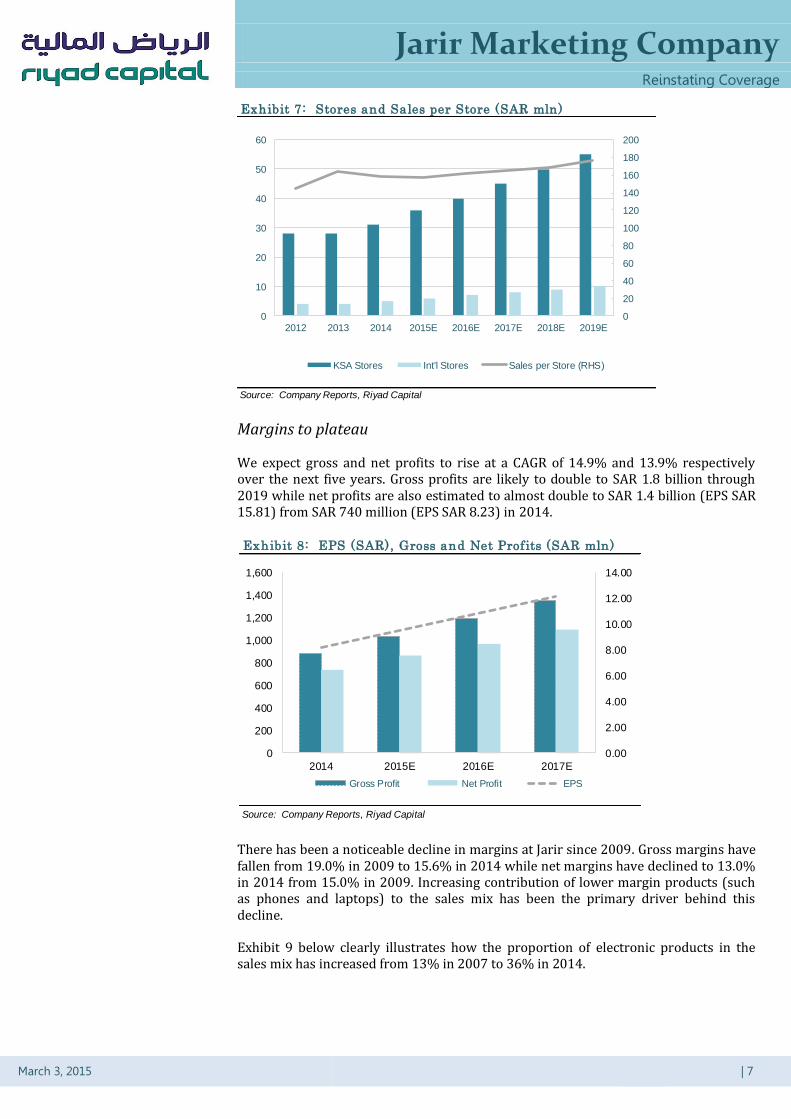

Margins to plateau

We expect gross and net profits to rise at a CAGR of 14.9% and 13.9% respectively over the next five years. Gross profits are likely to double to SAR 1.8 billion through 2019 while net profits are also estimated to almost double to SAR 1.4 billion (EPS SAR 15.81) from SAR 740 million (EPS SAR 8.23) in 2014.

There has been a noticeable decline in margins at Jarir since 2009. Gross margins have fallen from 19.0% in 2009 to 15.6% in 2014 while net margins have declined to 13.0% in 2014 from 15.0% in 2009. Increasing contribution of lower margin products (such as phones and laptops) to the sales mix has been the primary driver behind this decline.

Exhibit 9 below clearly illustrates how the proportion of electronic products in the sales mix has increased from 13% in 2007 to 36% in 2014.

Exhibit 7: Stores and Sales per Store (SAR mln)

Source: Company Reports, Riyad Capital

0

20

40

60

80

100

120

140

160

180

200

0

10

20

30

40

50

60

2012 2013 2014 2015E 2016E 2017E 2018E 2019E

KSA Stores Int'l Stores Sales per Store (RHS)

Exhibit 8: EPS (SAR), Gross and Net Profits (SAR mln)

Source: Company Reports, Riyad Capital

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

0

200

400

600

800

1,000

1,200

1,400

1,600

2014 2015E 2016E 2017E

Gross Profit Net Profit EPS

Jarir Marketing Company

Reinstating Coverage

March 3, 2015 | 8

Going forward, we expect margins to stabilize with average gross margins expected at 15.6% through 2019 similar to 2014. According to management, the tilt towards electronics in the sales mix is now changing and there is a revival of stationery and books, which accrue higher margins. We believe net margins may continue to slightly suffer averaging 12.6% through 2019 versus 13.0% in 2014. Stagnant other income and higher variable costs are likely to be the culprit.

We have conducted a comparative margin analysis of Jarir’s peers at a local, regional and international level. Within the Kingdom, Extra is the closest peer although it only deals in electronics, where margins are lower as evident by 3% net margins.

Barnes and Noble is the largest retail bookseller in the United States and the leading retailer of content, digital media and educational products and is a good benchmark for Jarir. While gross margins are substantially higher than Jarir, they slim down very close to zero as we come down to the net level versus a minor decline from 16% to 13% for Jarir.

Exhibit 9: Changing Product Mix 2007-2014

Source: Company Reports

Computers &

Peripherals40%

Electronics13%

Other Products

47%

Computers & Peripherals

26%

Electronics36%

Other Products

38%

Exhibit 10: Gross, EBITDA and Net Margins (%)

Source: Company Reports, Riyad Capital

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11

EU UK US Japan

15.6% 15.7% 15.7% 15.5%

13.3% 13.5% 13.3% 13.1%13.0% 13.0% 12.8% 12.5%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2014 2015E 2016E 2017E

Gross EBITDA Net

Jarir Marketing Company

Reinstating Coverage

March 3, 2015 | 9

Expect stable dividend payout

Jarir has historically maintained a dividend payout ratio close to 80%. We do not expect this to change going forward as the major shareholder appears inclined towards a steady and high payout ratio. In nominal terms, DPS is forecasted to rise from SAR 6.65 in 2014 to SAR 11.10 by 2018. As a result, a dividend yield of 3.8% for 2015 rising to over 5.0% on 2018 estimates appears quite attractive for a retail stock.

Management believes if there are no additional cash requirements, there may be an increase in payout beyond 80%. Although this is good news for minority investors, it also points towards lack of opportunities to earn attractive returns on excess retained cash.

Strategy and competitors

Jarir has two main competitors locally, Extra (electronics segment) and Obeikan (books, office supplies and school supplies). Much like Jarir, Obeikan has more than 30

Table 3: Margin Comparison

Company Country Gross EBITDA EBIT Net

BEST BUY CO INC US 23% 4% 3% 2%

OFFICE DEPOT INC US 23% (0%) (2%) (3%)

RADIOSHACK CORP US 34% NA NA NA

BARNES & NOBLE INC US 29% 5% 1% 0%

WH SMITH GB 57% 13% 10% 8%

UNITED ELECTRONICS (EXTRA) KSA 17% 5% 3% 3%

AL MEERA CONSUMER GOODS CO QT 16% 13% 5% 12%

JARIR MARKETING CO KSA 16% 13% 13% 13%

AVERAGE (Excl. Jarir) 28% 8% 5% 6%

Source: Bloomberg, Riyad Capital

Margins

Exhibit 11: Enticing Dividend Yield

Source: Company Reports, Riyad Capital

6.65

7.70

8.60

9.70

11.10

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2014 2015E 2016E 2017E 2018E

DPS Dividend Payout Dividend Yield

Jarir Marketing Company

Reinstating Coverage

March 3, 2015 | 10

bookstores within the country. However, it is considerably less known due to its limited product offering as well as no presence outside the Kingdom.

Extra has a much wider presence within KSA and is a known retailer of a full range of electronic items. While Jarir largely deals in mobile phones, laptops, tablets and computer accessories, Extra has the full range including TVs, Fridges, Washing Machines and other products. This low margin business has been further penetrated by hypermarkets offering electronic items at even lower prices but with limited product range and little or no customer service.

Given market dynamics in the country, Jarir has tried to position itself as a superior and premium retailer offering a better buying experience and enhanced customer service. Business is cyclical, getting a boost from back-to-school and launch of newer electronic devices such as smartphones. Within KSA, management expects to continue expanding in metropolitan cities such as Riyadh and Jeddah due to continued migration to these cities and a rise in average household income as number of women in the workforce rise increasing the total household income.

Jarir is still a very much family owned and managed business. Top executive positions and roles are held by the Alagil brothers who have decades of experience. However, with the passage of time, independent management and/or the younger generation from within the family may come in which can give a new direction to the business.

The management has been working on several new initiatives:

1. A brand manager has been appointed for the loyalty cards so as to increase

members and generate higher repeat sales.

2. Enhancement in the Company’s ROCO brand, which primarily produces office

and school supplies.

3. E-books have been launched but it is not expected to impact bottomline for

another 3 years.

4. Complete revision of the sales catalogue.

5. Launching of e-commerce in 2H 2015. However, this is unlikely to generate any

material sales given share of e-commerce in Dubai is less than 1% at present.

6. Emphasis on social media and a push to increase subscribers at its Facebook

page and number of followers on Twitter.

Jarir Marketing Company

Reinstating Coverage

March 3, 2015 | 11

1Q 2015 Expectations

Given the two salaries bonus granted to government employees and many private sector companies, there is widespread expectation that retailers would be one of the prime beneficiaries of this additional money in the system. While we expect only a marginal positive impact on book sales at Jarir, there is likely to be a much greater rise in sales of smart phones, tablets, gaming consoles and laptops along with their accessories. These are the products most in demand at present. This is similar to what happened in 2011 when a government payout was announced.

Resultantly, we are anticipating a +20% Y/Y rise in revenues to SAR 1.68 billion for 1Q2015 driven by incremental sales as consumers spend the additional money in their pockets. Majority of the revenues (93%) are forecasted to accrue from the Retail segment. Dissecting by geographic contribution, SAR 1.57 billion of the total revenues are likely to come from within KSA.

Although gross margins dipped in 4Q2014 to 15.2%, we expect them to improve to 15.9%. However, EBITDA and net margins are forecasted to remain weaker this quarter over the similar quarter last year as sales composition is likely to be tilted towards lower margin products. Exhibit 11 below illustrates margin expectations.

Table 4: Sales Composition

SAR (mln) 1Q2015E 1Q2014 4Q2014

KSA 1,569 1,297 1,457

International 111 102 127

Total Sales 1,681 1,399 1,584

Retail 1,563 1,275 1,492

Wholesale 118 124 92

Source: Company Reports, Riyad Capital

Table 5: 1Q 2015 Forecasts (SAR mln)

1Q15E 1Q14 Y/Y 4Q14 Q/Q

Revenues 1,681 1,399 20% 1,584 6%

Cost of Sales 1,413 1,164 21% 1,344 5%

Gross Profit 267 235 14% 240 11%

EBITDA 232 207 12% 193 20%

EBIT 224 200 12% 193 16%

Net Income 224 201 11% 201 12%

EPS (SAR) 2.49 2.24 11% 2.23 12%

Source: Company Reports, Riyad Capital

Jarir Marketing Company

Reinstating Coverage

March 3, 2015 | 12

Exhibit 11: Quarterly Margin Comparison (%)

Source: Company Reports, Riyad Capital

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

1Q10 2Q10 3Q10 4Q10 1Q11 2Q11

EU UK US Japan

15.7%15.2%

15.9%

14.8%

12.2%

13.8%14.4%

12.7%13.3%

1Q14 4Q14 1Q15E

Gross EBITDA Net

Jarir Marketing Company

Reinstating Coverage

March 3, 2015 | 13

Valuation and Recommendation

Given steady cash flows and a stable cash generating business, we have used Discount Cash Flows (DCF) as our preferred valuation methodology. We have assumed a long-term growth rate of 2.25% and our standard risk free rate assumption of 3.9% for KSA. Beta assumption of 0.65 is lower than 0.71 Bloomberg calculation. Very low debt levels (3% of capital) means that a 7.9% WACC is very close to 8.0% cost of equity for the Company. Using 18.2x terminal multiple and discounting free cash flows through 2019, we arrive at our fair value of SAR 212.22. Table 6 below details the DCF valuation.

The table below details the sensitivity of the fair value to a range of long-term growth rates between 2.00% and 2.75% and a WACC estimate of between 6.5% and 9.0%.

As a cross‐check we carried out a Dividend Discount Model (DDM) valuation as Jarir has sustained a consistent dividend payout. The average payout of 80% over the last three years is expected to be maintained over the next five. At a long-term growth rate of 2.25%, cost of equity at 8.0% and a terminal multiple of 17.9x, we derive a fair value of SAR 201.78, lower than the DCF based fair value.

Table 6: DCF Valuation

SAR (mln) 2016E 2017E 2018E 2019E

LT growth rate 2.25% EBIT 974 1,101 1,261 1444

Risk-free rate 3.9% + Depreciation 37 40 44 47

Equity risk premium 6.25% - Zakat 29 34 43 49

Beta 0.65 - Capex 93 98 105 111

CoE 8.0% - Working Capital Changes 85 146 137 148

CoD 5.2% Free Cash Flow 805 863 1,020 1,184

Equity (% of capital) 97%

Debt (% of capital) 3% PV of FCF 746 742 813 874

WACC 7.9% Terminal value 21,528

Terminal Multiple 18.2x Discounted TV 15,898

Total Firm Value 19,073

Net Debt -27

Equity Value 19,100

Shares Outstanding 90

Per Share Fair Value 212.22

Source: Riyad Capital

Assumptions

Table 7: Sensitivity Analysis

2.00% 2.25% 2.50% 2.75%

6.5% 269 283 299 317

7.0% 241 252 265 279

7.9% 204 212 221 230

8.5% 184 190 197 205

9.0% 170 176 182 188

Source: Riyad Capital

Long-term growth rate

WA

CC

Jarir Marketing Company

Reinstating Coverage

March 3, 2015 | 14

Comparative multiples

We have compared Jarir to global, regional and local companies in order to assess relative valuation multiples. Best Buy, Barnes & Noble and WH Smith are some of the comparable companies.

As there is no direct listed competitor for Jarir in the Saudi market, we have compared against closest peers such as Extra and retail names including Savola, Almarai and Alhokair. We believe investors would apply similar multiples to companies in the retail segment. Although their products and business models vary, they are in effect targeting the same retail consumer pool in KSA.

On 2015E EV/EBITDA, Jarir appears more expensive than the group average and most

of its peers. However, on a forward P/E basis, the Company trades at 21.0x versus a

group average of 26.1x. Within KSA, Almarai and Alhokair are pricier than Jarir but

Extra, Alothaim and Savola trade at more attractive P/E.

Table 8: DDM Valuation

2015E 2016E 2017E 2018E 2019E

DPS 7.70 8.60 9.70 11.10 12.70

Discount factor 0.926 0.858 0.795 0.736

Discounted DPS 7.97 8.32 8.82 9.35

Terminal multiple 17.9x

Terminal value 227.32

Discounted TV 167.32

Fair value per share 201.78

Source: Riyad Capital

Table 9: Valuation Comparison

Market Cap

Company Country (SAR mln) TTM 2015E TTM 2015E TTM 2015E

BEST BUY CO INC US 51,689 7.0x 5.8x 17.0x 16.0x 0.3x 0.3x

OFFICE DEPOT INC US 19,364 NA 8.6x NA 51.6x 0.1x 0.3x

RADIOSHACK CORP US 97 NA NA NA NA 0.1x NA

BARNES & NOBLE INC US 5,571 6.4x 5.5x NA 47.6x 0.1x 0.2x

SAVOLA KSA 41,517 22.5x 16.0x 20.2x 18.3x 1.2x 1.5x

ALMARAI CO KSA 49,314 17.3x 16.1x 29.9x 24.1x 3.0x 3.9x

WH SMITH PLC GB 8,842 10.0x 9.4x 17.1x 15.4x NA 1.3x

FAWAZ ALHOKAIR KSA 22,594 24.7x 21.6x 28.5x 26.5x 2.7x 3.4x

ABDULLAH AL OTHAIM MARKETS KSA 4,875 16.2x 14.9x 22.7x 19.4x 0.6x 0.9x

AL MEERA CONSUMER GOODS QT 4,430 NA 22.1x 15.9x 26.1x 1.1x 1.9x

UNITED ELECTRONICS (EXTRA) KSA 2,912 17.0x 12.3x 24.1x 15.8x 0.9x 0.8x

AVERAGE 15.1x 13.2x 21.9x 26.1x 1.0x 1.5x

JARIR MARKETING CO KSA 18,180 24.3x 20.4x 24.6x 21.0x 3.2x 2.8x

Source: Bloomberg, Riyad Capital

EV / EBITDA P / E P / S

Jarir Marketing Company

Reinstating Coverage

March 3, 2015 | 15

Recommendation

We reinstate coverage on Jarir Marketing Company with a 2015-end target price of

SAR 212.00 representing 20.4x 2015E EV/EBITDA and 21.0x P/E. With stock price

close to our target, we recommend a Hold.

Growing population with a rising per capita income shall ensure more disposable

income with the Saudi consumer. Books and stationery segment will benefit from more

children in school and better education levels while increased connectivity and shorter

life cycles of products such as smartphones and tablets shall provide an impetus to

electronic sales.

We view the execution of store expansion targets in the next five years as critical to the

Company’s future growth. We believe getting to 65 stores by 2019 would be good

enough generating average sales growth of 15% per annum.

Jarir Marketing Company

Reinstating Coverage

March 3, 2015 | 16

Summary Financials

Table 10: Jarir Summary Financials

Income Statement (SAR mln) 2014 2015E 2016E 2017E Cash Flows (SAR mln) 2014 2015E 2016E 2017E

Total Sales 5,699 6,619 7,613 8,741 Pre-Zakat Income 766 898 1,005 1,131

Cost of Sales 4,812 5,579 6,417 7,386 Depreciation 31 34 37 40

Gross Profit 886 1,039 1,195 1,355 Other Adjustments 12 (130) (65) (195)

S,G &A Expenses 160 172 221 253 Cash from operations 809 803 977 977

EBIT 727 867 974 1,101 Additions to Fixed Assets (85) (47) (93) (98)

Financial Charges 5 2 3 4 Other Items 1 (39) 1 1

Net Income 740 869 971 1,093 Cash from investing activities (84) (86) (92) (97)

Shares Outstanding (mln) 90 90 90 90 Due to Banks (125) (75) 25 25

EPS 8.23 9.66 10.79 12.15 Dividends Paid (558) (693) (774) (873)

DPS 6.65 7.70 8.60 9.70 Cash from financing activities (683) (768) (749) (848)

EBITDA 756 901 1,012 1,142 Cash at year end 128 77 213 244

Balance Sheet (SAR mln) 2014 2015E 2016E 2017E Ratios 2014 2015E 2016E 2017E

Assets Growth (YoY)

Cash & Equivalents 128 77 213 244 Total Sales 9% 16% 15% 15%

Recievables 204 290 333 383 KSA Sales 9% 17% 16% 15%

Inventories 817 907 1,043 1,232 International Sales 18% 9% 9% 9%

Total Current Assets 1,381 1,472 1,817 2,122 Gross Profit 12% 17% 15% 13%

Fixed Assets 1,048 1,101 1,156 1,214 General & Admin 8% 4% 31% 15%

Total non-Current Assets 1,081 1,134 1,189 1,247 Selling & Distribution 11% 13% 25% 15%

Total Assets 2,462 2,606 3,006 3,370 EBITDA 13% 19% 12% 13%

EBIT 12% 19% 12% 13%

Liabilities & Equity Net Income 13% 17% 12% 13%

Payables 711 734 842 951 Margins

Accrued Expenses 86 106 122 140 Gross 16% 16% 16% 16%

Total Current Liabilities 950 911 1,073 1,175 EBITDA 13% 14% 13% 13%

Long Term Debt 25 25 50 75 Net Margins 13% 13% 13% 13%

Total Non-current Liab 158 163 205 246 Others

Total Liabilities 1,107 1,074 1,278 1,421 EPS 8.23 9.66 10.79 12.15

Price to Earnings 24.6x 21.0x 18.8x 16.7x

Share Capital 900 900 900 900 Book Value per share 15.1x 17.0x 19.2x 21.7x

Retained Earnings 316 405 505 642 DPS 6.65 7.70 8.60 9.70

Total Equity 1,355 1,531 1,729 1,949 Dividend Payout 81% 80% 80% 80%

Total Liab & Equity 2,462 2,606 3,006 3,370 Dividend Yield 3.3% 3.8% 4.2% 4.8%

Source: Company Reports, Riyad Capital

Riyad Capital is licensed by the Saudi Arabia Capital Markets Authority (No. 07070-37)

Stock Rating

Strong Buy Buy Hold Sell Not Rated

Expected Total Return

≥ 25%

Expected Total Return

≥ 15%

Expected Total Return

< 15% Overvalued

Under Review/

Restricted

Head Office Riyad Capital P.O. Box 21116 Riyadh 11475 Saudi Arabia Phone 800 124 0010 Website www.riyadcapital.com Email [email protected]

Disclaimer

This research document is prepared for the use of clients of Riyad Capital and may not be redistributed, retransmitted or

disclosed, in whole or in part, or in any form or manner, without the express written consent of Riyad Capital. Receipt and

review of this research document constitute your agreement not to redistribute, retransmit, or disclose to others the

contents, opinions, conclusion, or information contained in this document prior to public disclosure of such information by

Riyad Capital. The information herein was obtained from various public sources believed to be reliable but we do not

guarantee its accuracy. Riyad Capital make no representations or warranties whatsoever as to the data and information

provided and Riyad Capital do not represent that the information content of this document is complete or free from any

error. This research document provides general information only. Neither the information nor any opinion expressed

constitutes an offer or an invitation to make an offer, to buy or sell any securities or other investment products related to

such securities or investments. It is not intended to provide personal investment advice and it does not take into account

the specific investment objectives, financial situation and the particular needs of any specific person who may receive this

document.

Investors should seek financial, legal or tax advice regarding the appropriateness of investing in any securities, other

investment or investment strategies discussed or recommended in this document and should understand that statements

regarding future prospects may not be realized. Investors should note that income from such securities or other

investments, if any, may fluctuate and that the price or value of such securities and investments may rise or fall.

Accordingly, investors may receive back less than originally invested. Riyad Capital or its officers or one or more of its

affiliates (including research analysts) may have a financial interest in securities of the issuer(s) or related investments.

Riyad Capital shall not be liable for any loss or damages that may arise, directly or indirectly, from any use of the

information contained in this research document. This research document is subject to change without prior notice.”