Embed Size (px)

Citation preview

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 1/43

Acknowledgements We extend our gratitude to BCIDS to give us the opportunity to research into the

Japan’s current crisis and its impact on the world

We thank our guide, Mrs Karishma Chawla for supporting us with the project and

providing us with critical insight into the topic and its direction.

We are grateful to the various people working in various financial institutions for

helping us acquire reports and research material which helped us add value to this

report.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 2/43

Japan Earthquake – 2011

1

Dedications

We dedicate this report to the people of Japan who have suffered from the terrible

calamity that shook their nation and also to those who are struggling to put their

lives back to normal.

We further make this dedication to our family and friends who have always

supported us through our education and other endeavors and always wished for our

success.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 3/43

What hit the Country – What the Country hit

2

Table of ContentsOverview .................................................................................................................................. 4

Introduction .............................................................................................................................

Risk and Risk Management ............................................................................................... 6

The 2011 Tōhoku Earthquake and its causes ......................................................... 7

The Japanese Economy .......................................................................................... 8

The 1995 Kobe Earthquake and its impact on the economy of Japan ................. 9

The impact on the economy of Japan of the 2011 Tohoku Earthquake ........... 9

The Japanese Stock Market ..............................................................................................10

Impact of the 1995 Kobe earthquake on Tokyo Stock Exchange .................................... 10

Impact of the 2011 Tohoku earthquake on Tokyo Stock Exchange ................................. 11

Forecast for the Nikkei 225 after the 2011 Tohoku Earthquake ..................................... 12

Impact on the Indian Markets ......................................................................................... 12

Comparison between BSE Sensex and Nikkei 225 .......................................................... 12

Impact of the earthquake on Insurance........................................................................14

Estimates of loss to insurance companies ....................................................................... 15

Losses incurred to the residential sector ..................................................................... 15

Losses incurred from loss of life .................................................................................. 16

Losses incurred from loss at sea and sea vessels ......................................................... 16

Losses incurred from loss to vehicles .......................................................................... 16

Losses incurred to international insurers .................................................................... 16

Impact on Japan’s currency –the Yen ...........................................................................18

Shift to Gold Exchange Standard ................................................................................. 18

Fixed value of the Yen to the US dollar and introduction to floating exchange rates . 18

Highly volatile decade for the Yen (1970 – 1980) ....................................................... 18

Weakening Yen (1980 – 1985) ..................................................................................... 19

Impact of Plaza Accord ................................................................................................ 19

Twin Disaster – Japanese Asset bubble and Kobe Earthquake .................................. 19

Deflation trap (2000 – 2007), US Crisis and Tohoku Earthquake 2011 ..................... 19

The Tohoku Sendai Earthquake and Tsunami ..................................................... 20

Japanese Yen fuelled by Earthquake ................................................................ 20

Dollar hits all time low against earthquake ...................................................... 21

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 4/43

Japan Earthquake – 2011

3

What drove the Yen’s strength?........................................................................ 21

Difference with Yen strengthening following Kobe earthquake in 1995 ............ 22

Yen stabilizes after hitting record high ..................................................................... 23

What next for the Yen ............................................................................................ 24

Impact of Earthquake on commodity ........................................................................... 26

Impact of 2011 earthquake on steel and base metals .......................................... 26

Production impact on steel ............................................................................... 26

Consumption impact on steel ........................................................................... 27

Impact on iron ore and coking coal .................................................................. 27

Would Indian steel benefit from the crisis?...................................................... 28

Impact on base metals ...................................................................................... 28

Impact on crude oil ........................................................................................... 29

Impact on Liquid Natural Gas .......................................................................... 30

Impact on construction materials ..................................................................... 31

Impact on information technology ................................................................... 32

Impact of Japan’s Import and Export........................................................................... 34

Annexure I – Japan’s stock market post Kobe 1995..................................................35

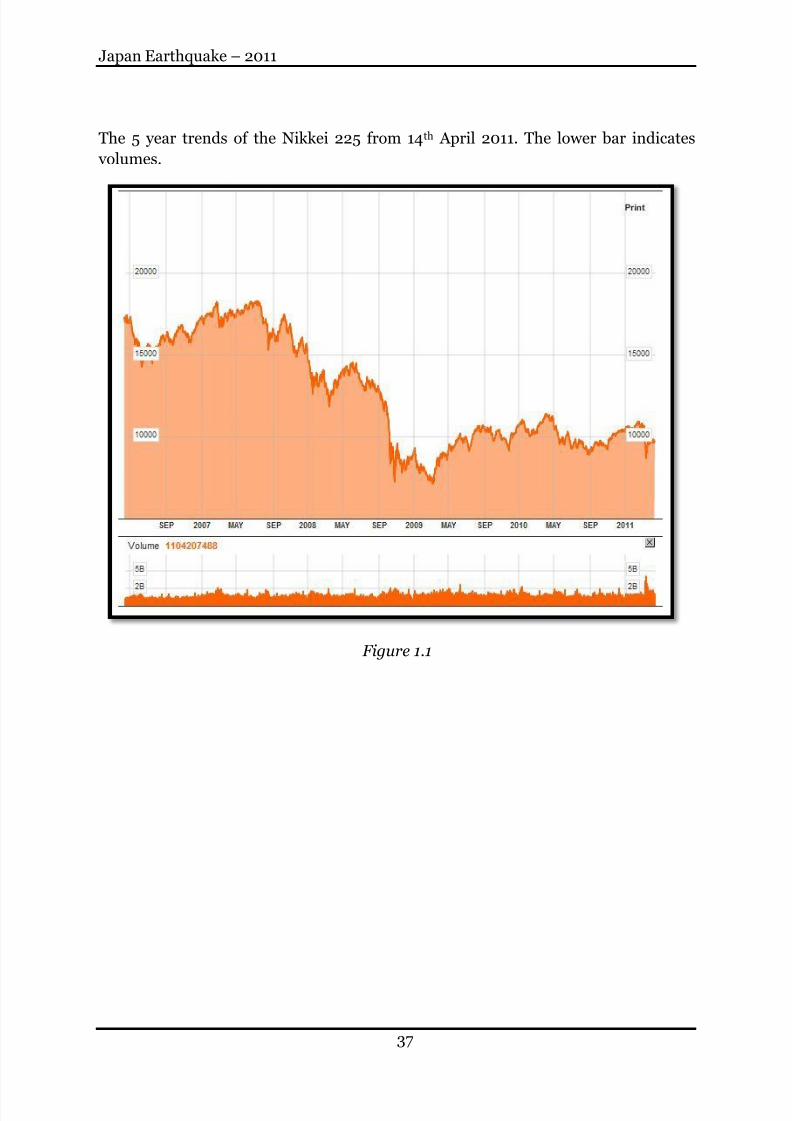

Annexure II – Trends of Nikkei 225 .............................................................................. 36

Annexure III – Trends of BSE Sensex........................................................................... 38

Annexure IV – Japanese Yen charts and graphs........................................................39

Bibliography .........................................................................................................................41

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 5/43

What hit the Country – What the Country hit

4

Overview Japan is one of the more influential countries in the world. With its participation in

the G - 20 and the ASEAN, it influences a lot of the world trade. It is one of the few

countries in the world that has a positive balance of payments.

Given that, it is also a country prone to natural calamities due to its geographical

positioning. Japan has faced many earthquakes in the past but the 2011 Tohoku

earthquake has been the most impactful and most damaging of them all – not only in

terms of loss to property and lives but also the economic loss in terms of trade,

equity markets, loss to insurance and impact on the commodity that the country

produces and trades.

This report seeks to study the impact of the earthquake from the perspective of

Markets, insurance, currency, commodity and trade.

The equity markets of Japan are known to be the most affected with a declining

returns on investment since the property and stock market bubble in the late 1980’s.

Although this can be attributed more to fundamental factors like deflation, many

stocks are still struggling to find equilibrium even 16 years after the 1995 Kobe

earthquake. From the FII front, Japan was one of the few countries in the world and

the only Asian country that was able to attract large FIIs in the first two months of

the last quarter of FY2010 ($2.2bn), but the earthquake’s devastating impact led the

FIIs to withdraw from these markets and find newer markets, therefore, other Asian

markets saw an increase in the FIIs in the month of March. It can be said fromprevious observations made during the 1995 Kobe earthquake (however, there was

the bank crisis also prevailing at that time in Japan) that the markets see a short

term impact due to sentiments and temporary disabled production in the economy,

in the medium term markets will show a bounce back and within one and a half years

from the 2011 Tohoku earthquake, after the production and consumption come to

normal, the markets will show significant returns. In conclusion, investors find an

opportunity in such markets and although the country of Japan is going through the

worst crisis in its history, there is still hope for growth in the years to come.

Insurance is another sector that took a major impact. Although WB estimates are

that $235bn will be the damages to Japan, insurers are estimating that the insured

losses will be around $20bn to $45bn. The government of Japan in its Earthquake

insurance sharing scheme has neatly organized the insurance to be paid by the two

parties apart from itself –the Japanese Earthquake reinsurer company and the non-

life insurers. The impact on the insurance companies is not going to be significant as

insurers are observed to maintain within themselves very strict standards of capital

adequacy and take into account events of this nature. It was observed that the limit of

capital with the insurance agencies was 5 times the prescribed amount and that some

companies had reserves of $90bn while the total for the industry exceeded $134bn.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 6/43

Japan Earthquake – 2011

5

International agencies did not have a large exposure and damage to them was limited

to around $1.5bn.

The Yen showed strong appreciation after the earthquake of 1.3% to the US dollar.

Although one might expect that a currency might show signs of weakening after an

event of such magnitude, the Japanese Yen became stronger. The main reason forthis is that many Japanese nationals living abroad started to repatriate money into

the Japanese economy increasing the demand for Yen. Another reason was that the

Japanese are famous for selling asset abroad in case their own country requires it.

These assets are usually held in the form of land and property or bonds in different

countries which were liquidated and brought back into the country.

The commodity market for Japan looked stable, although the production has been

impacted and consumption is expected to rise as replacement and reconstruction

demands will rise. Coincidently the oil prices have risen, although there will be an

increased demand in oil and petroleum from Japan to generate power to make up for

the loss in capacity due to the loss of the nuclear power plants, a lot of the increase in

price can be attributed to the OPEC and the Chinese refineries shutting down. The

impact on LNG however is a different story as it is anticipated that 40% of the loss of

capacity will be fuelled by production of energy using LNG and prices have seen a

spike and expected to remain there for atleast another 3 months or till the time

Japan does not regain energy production capacity. Steel and base metals have seen a

sharp spike due to demand from reconstruction looming and iron ore and coking

coal also have seen the same. Cement will not be affected as Japan has the capacity to

increase the production as seen from the 2008 earthquake and also can reduce theexports to further meet internal demand, however an impact can be felt on countries

that have small domestic markets for cement and are dependent n Japan for exports.

Finished goods like the personal computer and TV panels are expected to see some

impact in the short run as the production capacity of many Japanese companies is

hindered due to lack of power, in the medium term the market still looks favorable

for the other Asian countries such as Korea and Taiwan, but in the long run again

replacement demand will help the economy and industry pick up.

On trade the Japanese economy is mainly dependent on China for imports and US

for exports. Other trading partners also play an important role s Japan has very poorraw material resource, but have technology and quality of finished goods. The impact

on trade is going to be short lived and only till the time infrastructure is going to be

restored as many countries are dependent on information technology that Japan

offers and Japan is dependent on other countries or resources.

In conclusion the impact will affect the global economy only in the short run and as

the Japanese economy restores its infrastructure and as demand will pick up, trade,

and the markets will reach the equilibrium much faster.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 7/43

What hit the Country – What the Country hit

6

IntroductionRisk and risk management

Risk as the dictionary defines it is – ―the exposure to the chance of injury or loss; a

hazard or danger...‖ (Dictionary.com). Many different industries follow different

more specific definitions of risk more suited to their field of operation; however, the

essence of the term is the same. There are many different types of risks and each one

of them is treated differently.

Below is a list of types of risks that a business faces on a day to day basis. This list

only comprises of 9 types of risks, however, in reality there are many other risks that

exist. (withRisk, 2008):-

i. Strategic Risks (for example a competitor coming on to the market);

ii. Compliance Risks (for example the introduction of new health and safety

legislation);

iii. Financial Risks (for example non-payment by a customer or increased interest

charges on a business loan);

iv. Operational Risks (for example the breakdown of key equipment);

v. Environmental Risks (like disasters);

vi. Employee Risks (supplying necessary number of employees, safety and health

issues);

vii. Political and Economic (instable political status in foreign markets you export

goods to.);

ix. Planning Risks (sometimes the work requirement and specification

may change and all the work would be planned again.)

These are only a few types of risks that exist in an environment. However, they are

the most significant ones as far as a business organization is concerned; the risks that

affect a country are slightly different.

Countries operate in an environment that is governed mainly by international trade,exchange rates, the political stability of the countries of the world and diplomatic

relations with the outside world.

Given that; countries are more exposed to risks such as:-

i. Trade risk

ii. Foreign exchange rate risk

iii. Political and economic risk

iv. Environmental risk

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 8/43

Japan Earthquake – 2011

7

Although the risks faced by the countries are similar, their magnitude and effect on

the economy and other economies can be different. For e.g. the Foreign exchange

rate would impact a business as an appreciation of the foreign currency would make

the exported commodity more expensive and affect demand, however, from the

countries point of view it would mean that their country’s demand for goods falls

affecting their balance of payments.

Exposure to risk therefore can be hazardous to the overall health of the economy.

Understanding risk and controlling it is therefore detrimental. Many techniques of

counteracting the risk and controlling losses from it have been designed under the

banner Risk Management .

Risk management is the process of identification, analysis and either acceptance or

mitigation of uncertainty or chance of loss. Essentially, risk management occurs

anytime when an entity analyzes and attempts to quantify the potential for losses for

a given occurrence and then takes the appropriate action (or inaction). Inadequate

risk management can result in severe consequences for companies, Nations as well as

individuals. For example, the recession that began in 2008 was largely caused by the

loose credit risk management of financial firms. (Investopedia, 2010)

There are numerous risk management techniques that are practiced and new ones

are designed on a regular basis to tackle risks that are newly being identified – such

as the Information systems risk management techniques – with the growing

dependence on technology and information systems.

The 2011 Tōhoku Earthquake and its causes

The 2011 Tōhoku earthquake and tsunami, literally "Eastern Japan Great was caused

by a 9.0-magnitude undersea megathrust earthquake off the coast of Japan that

occurred at 14:46 JST (05:46 UTC) on Friday, 11 March 2011. The epicenter was

approximately 72 km (45 mi) east of the Oshika Peninsula of Tōhoku, with the

hypocenter at an underwater depth of approximately 32 km (19.9 mi). On 1 April

2011, the Japanese government named the disaster resulting from the earthquake

and tsunami the "Great Eastern Japan Earthquake".

The earthquake triggered extremely destructive tsunami waves of up to 37.9 meters

(124 ft) that struck Japan minutes after the quake, in some cases traveling up to

10 km (6 mi) inland, with smaller waves reaching many other countries after several

hours. Tsunami warnings were issued and evacuations ordered along Japan's Pacific

coast and at least 20 other countries, including the entire Pacific coast of the

Americas.

The Japanese National Police Agency has confirmed 13,219 deaths, 4,742 injured and

14,274 people missing across eighteen prefectures, as well as over 125,000 buildings

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 9/43

What hit the Country – What the Country hit

8

damaged or destroyed. The earthquake and tsunami caused extensive and severe

structural damage in Japan, including heavy damage to roads and railways as well as

fires in many areas, and a dam collapse. Around 4.4 million households in

northeastern Japan were left without electricity and 1.5 million without water. Many

electrical generators were taken down, and at least three nuclear reactors suffered

explosions due to hydrogen gas that had built up within their outer containment

buildings after cooling system failure. On 18 March, Yukiya Amano—the head of the

International Atomic Energy Agency —described the crisis as "extremely serious."

Residents within a 20 km (12 mi) radius of the Fukushima I Nuclear Power Plant and

a 10 km (6 mi) radius of the Fukushima II Nuclear Power Plant were evacuated. In

addition, the U.S. recommended that its citizens evacuate up to 80 km (50 mi) of the

plant.

Estimates of the Tōhoku earthquake's magnitude make it the most powerful known

earthquake to have hit Japan, and one of the five most powerful earthquakes in the world overall since modern record-keeping began in 1900. Japanese Prime Minister

Naoto Kan said, "In the 65 years after the end of World War II, this is the toughest

and the most difficult crisis for Japan.‖ The earthquake moved Honshu 2.4 m (7.9 ft)

east and shifted the Earth on its axis by almost 10 cm (3.9 in). Early estimates placed

insured losses from the earthquake alone at US$14.5 to $34.6 billion. The Bank of

Japan offered ¥15 trillion (US$183 billion) to the banking system on 14 March in an

effort to normalize market conditions. On 21 March, the World Bank estimated

damage between US$122 billion and $235 billion. Japan's government said the cost

of the earthquake and tsunami that devastated the northeast could reach $309

billion, making it the world's most expensive natural disaster on record. (Wikipedia,

2011)

The Japanese Economy

Japan’s economy can be characterized as highly industrialized and a free market

economy. The nation plays a competitive role in international trade, although

productivity is quite low in protected areas, including agriculture, services and

distribution. (Economy Watch, 2010) However, it is the third largest economy in the world – only after the United States of America and China. Most of its export goods

consist of cars, electronic devices and computers. Its trading partners for export are

USA, China, South Korea, Taiwan and Honk Kong. Japan is dependent on imports

for goods such as raw materials such as oil, foodstuffs and wood imported from

China, followed by the USA, Australia, Saudi Arabia, South Korea, Indonesia and the

United Arab Emirates.

The major industries prevalent in Japan are manufacturing; construction;

distribution; real estate; services; and communication are Japan's major industries

today. Agriculture makes up only about two percent of the GNP. Most important

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 10/43

Japan Earthquake – 2011

9

agricultural product is rice. Resources of raw materials are very limited and the

mining industry rather small. (JapanGuide.com, 2011). Japan is one of the few

countries in the world that has a positive balance of payments - i.e. the component of

exports in much higher in Japan than it imports.

The 1995 Kobe Earthquake and its impact on the economy of

Japan

Japan is in a geographically perilous area and faces the risk of earthquakes

frequently exposing it to the environmental risk factor more than most other

countries. The 1995 Kobe earthquake killed 6,500 people and caused a damage of

¥10bn which was 2.5% of the GDP of the country during the time. Apart from the loss

of life and financial impact, the country saw a loss in value of 25% from the stock

market over the next six months. From a currency perspective, the Yen appreciated by 20% relative to the US Dollar in the following three months as local Japanese

investors sold foreign assets to fund domestic reconstruction (McCafferty, et al.,

2011). However, data also suggests that in the year before the Kobe earthquake the

GDP of the country had expanded by 0.9% however, the following year saw a growth

of 2.5% as reconstruction efforts contributed greatly to the economy. However, one

cannot ignore the destruction of the pre-existing assets (Morris, 2011).

The impact on the Japanese economy of the 2011 Tōhoku

Earthquake

The damage from the three most important prefecture affected by the earthquake

and tsunami – the nuclear reactors Miyagi, Fukushima and Iwate – account for

nearly 4% of Japan’s 2007 GDP. The damage in Tokyo alone accounts for nearly 18%

of the GDP. The impact is not only extended to the financial loss but an impact will

also be seen on automakers, consumer goods and IT manufacturers who will suffer

losses also due the time period it will take to for operations to come back to its

original state (Morris, 2011).

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 11/43

What hit the Country – What the Country hit

10

The Japanese stock markets

The Nikkei 225 more commonly called the Nikkei , the Nikkei index , or the Nikkei

Stock Average, is a stock market index for the Tokyo Stock Exchange (TSE). It has

been calculated daily by the Nihon Keizai Shimbun (Nikkei) newspaper since 1950. It

is a price-weighted average (the unit is yen), and the components are reviewed once a

year. Currently, the Nikkei is the most widely quoted average of Japanese equities,

similar to the Dow Jones Industrial Average. In fact, it was known as the "Nikkei

Dow Jones Stock Average" from 1975 to 1985. The Nikkei 225 began to be calculated

on September 7, 1950, retroactively calculated back to May 16, 1949. Since January

2010 the index is updated every 15 seconds during trading sessions. (Wikipedia,

2011)

The Japanese stock market has seen a decline in the returns from stocks and bondssince the 1989 equity bubble burst. Today the returns on the Japanese stocks are just

above 1.75% and the Japanese bond markets are giving a return of just over 0%

which is almost negligible, this in comparison to the 8% returns that both the

markets gave is a significant drop.

Apart from the impact from the earthquakes, the main reason for the decrease in the

return is attributed to deflation in the economy (Morris, 2011).

The currency was seen becoming weaker compared to the dollar, this could be a

positive sign for the stock markets of Japan. The markets have already startedshowing signs of positive movement as the Nikkei 225 is rising at a steady rate. The

depreciated Yen and the fallen stock prices can be viewed highly beneficial for the

foreign investor. This lays down foundation for large foreign investment in the

country which will help the Nikkei 225 come back to the pre-earthquake levels.

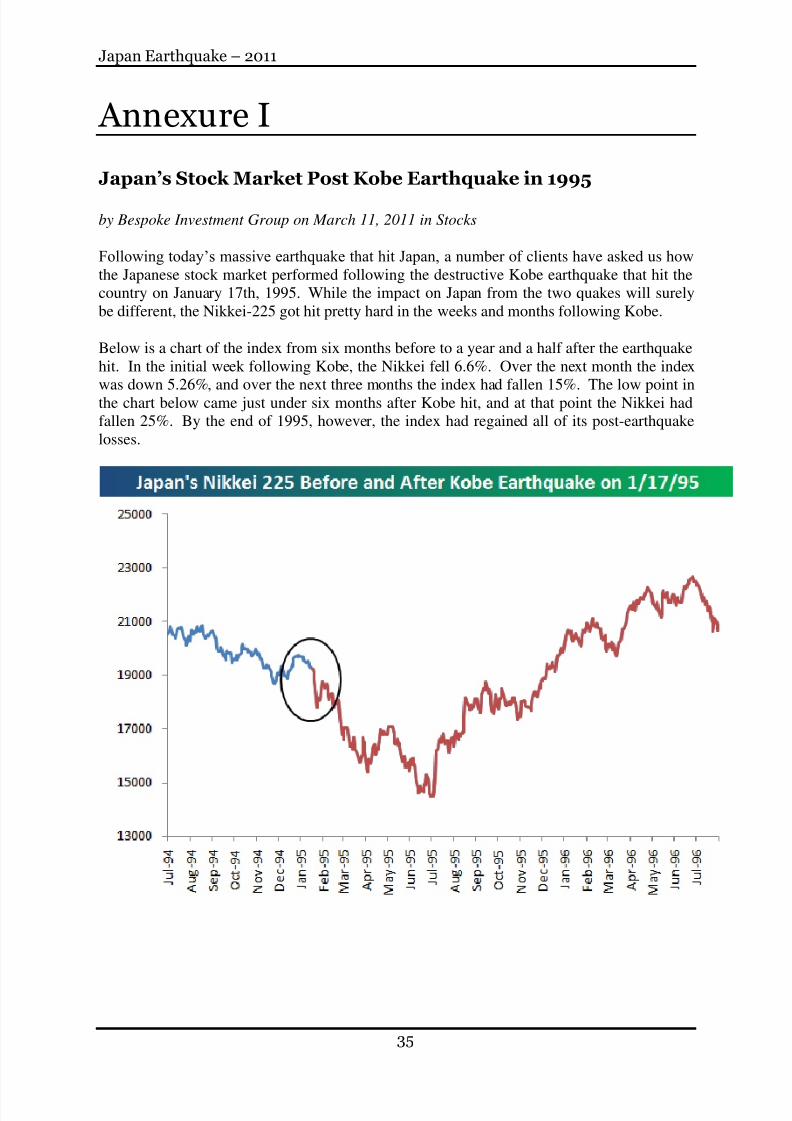

Impact of the 1995 Kobe Earthquake on Tokyo Stock Exchange

The 1995 Kobe Earthquake was the last major earthquake that caused significant

damage to the country of Japan. Nikkei 225 saw a fall of 1000 points on the day of

the earthquake. The trend that was observed was that the Nikkei 225 fell by 6.6% in

the initial week from the Kobe Earthquake which occurred on 17th January 1995,

before the fall the Nikkei was around the 19600 points mark. Over the next month

the index saw a further drop of 5.6%, and over the next three months saw a 15% drop

in the index. However, the lowest point was seen at the end of six months when the

Nikkei 225 fell by 25% from the day the earthquake had occurred; despite this the

market recovered well after July of 1995 and closed higher than the Index closing

before the earthquake took place by July 1996. (Bespoke Investment Group, 2011)

(Refer Annexure I).

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 12/43

Japan Earthquake – 2011

11

The initial decline in the market index in January 1995 was attributed to the Kobe

Earthquake, however, the further decline seen through the year was also because

Japan’s Banks were facing a crisis in the form of a wave of non-performing loans.

Even though the government had tried to recapitalize the banks, it was seen as

heavily inadequate (Brooks, 2011).

The impact of the 2011 Tōhoku Earthquake on Tokyo Stock

Exchange

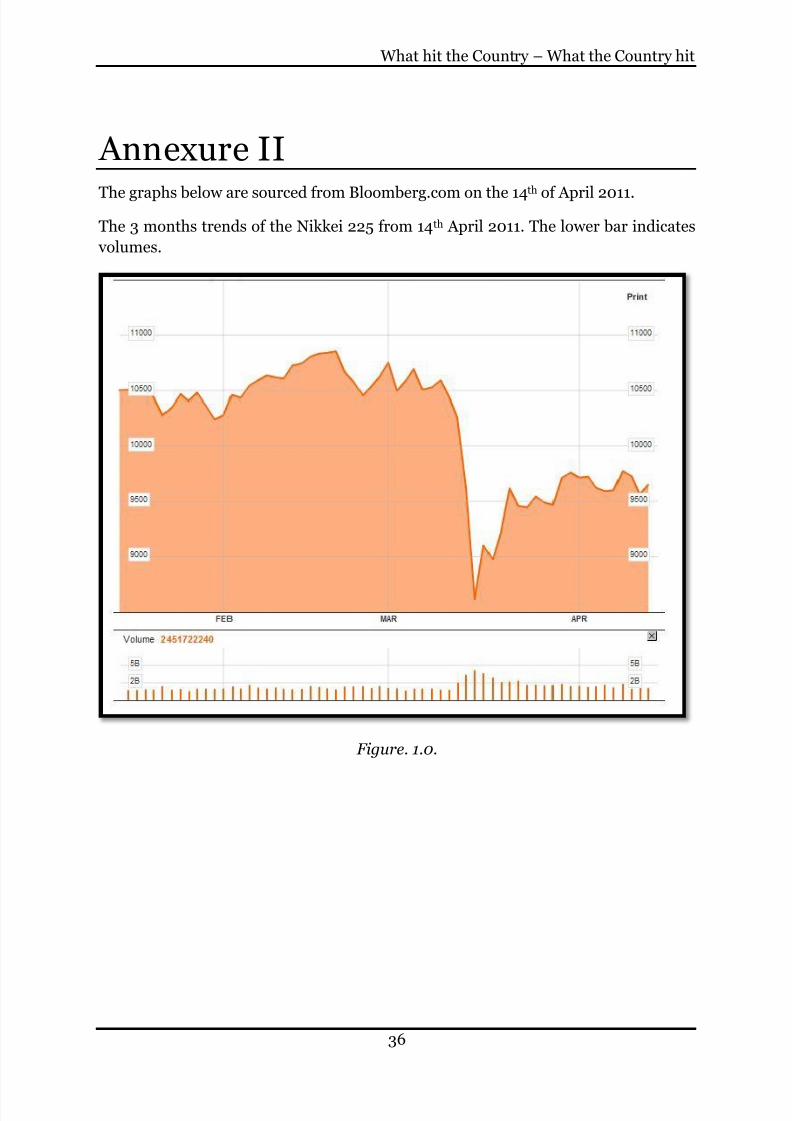

Past data suggests that the Nikkei 225 was looking good since November 2010. It had

risen from 9200 to 10600 – a return of 15.7% over 5 months. However, the news of

an earthquake had great impact on the Nikkei 225, two days prior to the earthquake

the Nikkei 225 fell from 10600 to 8600 within 2 days after the event; a negative

return of 18.9% over one week.

This can be attributed to the large sell volumes seen in the days following the

earthquake. From trend analysis of the Nikkei 225, it is observable that the total

trade volumes had increased to over 250% from the average trade volumes over the

past 5 years. This is indicative of the fact that many foreign and domestic investors

were exiting the market – foreign ones in anticipation of the markets drastically

falling and domestic entities removing their money to fund the damage that was

incurred and to aid in the rebuilding efforts (Refer Annexure II).

Comparison between the situation of Japan after theearthquakes

Given that the 1995 Kobe earthquake and the 2011 Tōhoku earthquake let a large

impact on the Japanese economy, there is no contention that the Tōhoku earthquake

was far more devastating to the economy and is the cause for the largest damage

caused to any nation due to a natural calamity. However, the situation of Japan when

the Kobe earthquake hit in 1995 and the Tōhoku earthquake of 2011 is very different.

One of the most significant differences is that the banking sector of Japan today in

not going through a crisis like it was in 1995.

Another difference is that the extent of impact on the Nikkei was far more adverse in

the 2011 Tōhoku earthquake than the 1995 Kobe earthquake, this can be inferred by

looking at the fall in the index. In 1995, Nikkei 225 fell by 25% over a 6 month period

whereas in 2011, the Nikkei fell by almost 19% in just 4 days after the 2011 Tōhoku

earthquake.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 13/43

What hit the Country – What the Country hit

12

Forecast for the Nikkei 225 after the 2011 Tōhoku Earthquake

Japan was the only Asian country that was able to attract FIIs1 estimated at $2.2bn.

In the initial days of the 2011 earthquake, FII flows out of Japan were seen to rise.

This is backed up by the fact that other Asian markets saw a turnaround in the

amount of FII flows in their respective countries. For example, India witnessed an

FII outflow of $2bn in the months of January 2011 and February 2011, however, in

March, India saw an FII flow of $304.6mn. However, this increase in FII cannot be

totally contributed to the calamity, the extent of increase in FII flows to India are

indicatives of the foreign institutes looking for other than Japan markets.

This could change very rapidly as the currency and market conditions of Japan seem

favorable for foreign investors to invest in the markets.

Going by the trends that previous data for 1995 Kobe earthquake suggests, the

Japanese economy showed a turnaround the stock prices rose almost a year and a

half after the Kobe earthquake, then again the economy was going through a problem

in the banking sector. Given that the economy is not suffering from any fundamental

issues with the financial system and that the deflation in the market is decreasing,

the outlook of the market is positive and investors will be keen to look at the

Japanese markets in the near future.

Impact on the Indian Markets

To better understand the impact of the Japanese earthquake on the Indian stock

markets, it is important to understand what the index is. The index is a weighted

average of selected stocks from different sectors industry. What needs to be observed

is which stocks that comprise of the index have exposure to Japan. In the Indian

context, the major sectors that have any sort of exposure are the Automobile and

Information Technology (Equitymaster, 2011).

Given that the operations in Japan are not permanently disabled, however, it is

estimated that Japanese Auto makers are going to take some time to recover theirproduction back to normal. This could have some impact on the share prices of the

auto makers. However, since most of the Japanese companies have production

facilities outside Japan, this fall in prices could only be sentimental as effect in sales

would not be significant and the Indian markets will not see a long term impact on

the index.

Although the there are certain assessments of the future of the global and Indian

stock markets, a fair assessment cannot be made as the extent of damage has not

1 Foreign Institutional Investors: An investor or investment fund that is from or registered in a country outside of the one in which it is currently investing.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 14/43

Japan Earthquake – 2011

13

completely come into view. But, one thing is sure that the extent of the damage is

substantially large and the impact on the markets in the short term is inevitable.

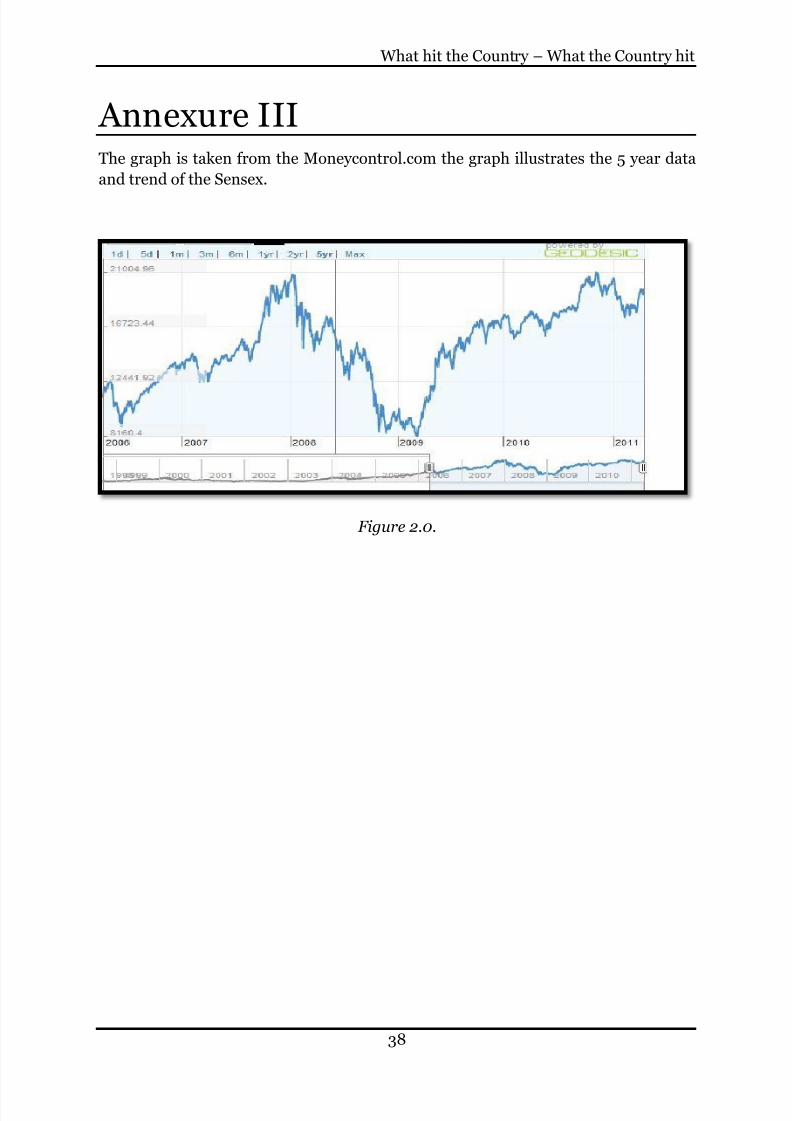

Comparison between the BSE Sensex and the TSE Nikkei 225

From the past trends of the market, it can be observed in 2007 and 2008 the Sensex

and the Nikkei 225 have seen growth in the years, however, the trend shows that in

2009 the Nikkei and the Sensex had fallen dramatically as a result of the credit crisis

that prevailed in the period. However, the Sensex had recovered within 18 months

and so did the Nikkei but the extent to which the Nikkei increased was less due to the

prevailing deflation at the time. Although trends are similar, it does not indicate any

dependence as the trend was observed in markets all over the world (Refer Annexure

III).

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 15/43

What hit the Country – What the Country hit

14

Impact of the earthquake onInsurance

Japan being in an earthquake prone region has developed an earthquake insurancesharing scheme. The main participants in the scheme are the Japanese government,

the Japanese earthquake reinsurance company (JER) and the non-life insurers. The

scheme is divided into slabs on the basis of the value of the damaged caused. The

JER is to cover any losses up to the extent of $1.4bn or ¥0.115tn, the next slab is

$23.5bn or ¥1.1925tn of which 50% is to be borne by the government and the

remaining 50% is to be shared by the non-life insurers and the JER in a defined

proportion. The third slab is $45.3bn or ¥3.712tn of which 95% losses are borne by

the government and 5% losses by the non-life insurers. The last slab is the $67.1bn or

¥5.500tn in losses of which again the government bares 95% of the losses and the

JER bares 5% of the losses (Tower Watson, 2011).

The cover on the losses is provided by non-life and co-operative insurers, the

Standard property policies offered by non-life insurers exclude earthquake risk.

Residential earthquake insurance (residential EQ) coverage and extended cover to

the commercial market are offered as optional coverage. For a residential EQ policy

offered by non-life insurers, the amount of coverage is typically selected by the

insured to be between 30% and 50% of the fire limit of coverage, with a maximum

limit of ¥50 million for the building and ¥10 million for its contents. By contrast, the

standard property policy offered by Zenkyoren – the leading non-life insuranceprovider – does not exclude earthquake risk.

Residential EQ coverage was first established in 1964 following a large earthquake in

Niigata, in northern Japan. Until 1995’s Kobe earthquake, the penetration ratio of

residential EQ on policies issued by non-life insurers had been less than 10% of

households. After the Kobe event, the penetration rate increased to the current rate

of 22% of households. Combined with the EQ coverage issued by the co-op insurers,

roughly half of all households in Japan carry EQ coverage. However, even when

covered, the insured typically participates significantly in the exposure. The

commercial property market is mainly covered by local non-life insurers. Earthquakeinsurance is written as an extended coverage endorsement to an ordinary fire policy

and is offered to selected large corporations. (Tower Watson, 2011)

Given the high natural catastrophe risk present in this part of the world, solvency

regulation of Japanese non-life insurance companies includes a solvency margin

requirement specific to catastrophes. Currently, the required solvency margin for

catastrophe risk is defined as the larger of the loss arising from a repeat of the Kanto/

Tokyo earthquake of 1923, which is deemed equivalent to a one-in-200-year event,

and the Isewan Typhoon of 1959, which is deemed equivalent to a one-in-70-year

event. Japanese insurers have a long track record of providing a high level of security

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 16/43

Japan Earthquake – 2011

15

to their policyholders. For example; the combined available solvency margins for the

three largest non-life insurance groups in Japan, Tokio Marine Group, NKSJ Group

and MS&AD Group, exceeded US$120 billion as of March 2010. The total is

equivalent to four times the required risk solvency margin of these carriers, inclusive

of catastrophe risks. Zenkyoren has a solvency margin of US$90 billion, representing

almost five times its required solvency margin. Based on the large market share of

these three non-life groups (90% of the market share of non-life premiums,

excluding the co-ops) and some of the largest co-ops (Zenkyoren in particular), This

indicates that Japanese industry’s capitalization will be sufficient to withstand the

estimates of insured losses from this recent disaster.

Estimates of loss to insurance companies

Although the extent of the damage to the country of Japan was estimated at $235bn by the World bank just 10 days after the earthquake, the estimates of the insured

losses are around $20bn to $45bn (Tower Watson, 2011), this implies that the

insured property and life that was damaged is between 8% to 18% of the total losses

due to the earthquake in excess of the damage cause to the 4 nuclear power station of

the 17 that Japan has. The impact was seen throughout all the arms of insurances i.e.

Fire insurance (that covers residential and commercial property), Life, Auto, Marine.

There was an impact on the international insurance companies as well.

Losses incurred to the residential sector

The estimate of insured losses to residential properties from the combination of the

earthquake and the ensuing tsunami is US$9.5 billion to US$21.9 billion, based on

the assumption that approximately half of the population affected by these events

currently purchases earthquake insurance.

It is important to note that the co-ops, including Zenkyoren, follow a different set of

regulations from those that apply to insurance companies in Japan. In particular,

they do not share their EQ exposures with the JER. Zenkyoren has purchased an

excess of loss program2 from the international reinsurance markets that is said to beone of the largest programs in the world. It is believed that Zenkyoren’s catastrophe

reinsurance coverage is approximately US$8 billion excess of US$3.3 billion,

bringing our ground-up loss estimate for Zenkyoren to between US$3.5 billion and

US$8.5 billion. The loss estimates assume Zenkyoren holds a 60% market share of

the total co-op market (Tower Watson, 2011).

2 This is a type of treaty reinsurance where the reinsurer covers all the insurance contracts with theinsurer that are defined under a specific contract.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 17/43

What hit the Country – What the Country hit

16

Losses incurred to the commercial sector

The estimate of the insured losses to commercial properties from the combination of

the earthquake and the ensuing tsunami is US$4.7 billion to US$11 billion. This

estimate is based on the assumption that the industry losses will be split two-thirds

to residential and one-third to commercial properties (Tower Watson, 2011).

Losses incurred from loss of Li fe

Because of the tremendous loss of life, life insurers face increased death, accident

and health claims. Life insurance coverage in Japan is relatively straightforward,

with one exception. An accidental death benefit rider, typically double the death

benefit, is excluded by contract in the event of an earthquake. However, in

accordance with local customs and concern for insureds’ families, the Japanese life

insurance industry has announced that the earthquake exclusion will not be enforced

for this event and that payments arising from the accidental death benefit coverage

will be made. The current estimate of the losses to life insurers is US$3.0 billion to

US$4.9 billion.

This estimate does not contemplate any scenario where there is a significant release

of radioactive material from the stricken Fukushima power plant, which could cause

significant health and mortality issues (Tower Watson, 2011).

Losses incurred from loss at sea and sea vessels

The ensuing tsunamis tossed many large ships aground along with many smaller

commercial and personal vessels. Losses to port facilities were also extensive. The

estimate of the marine losses related to the event is US$1.1 billion to US$1.5 billion

(Tower Watson, 2011).

Losses incurred from loss to vehicles

Many thousands of cars were flooded due to the tsunamis. The estimate of the losses

to auto insurers is US$0.2 billion to US$0.7 billion (Tower Watson, 2011).

Losses incurred to international insurers

The estimated loss to international insurers is US$1.5 billion to US$5.0 billion. One

of the most uncertain elements of this catastrophe is the insured loss associated with

large international (non-Japanese) corporations. These companies will be primarily

insured by major international insurers. Insurance protections often include time

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 18/43

Japan Earthquake – 2011

17

element coverages such as business interruption, extra expense and contingent

business interruption (CBI) cover when suppliers can’t supply needed production

materials to customers. The CBI element is particularly difficult to estimate because

the financial effects of supply-chain interruption will not be known for some time.

The policy terms and conditions for time element coverages also vary considerably

from company to company.

While this estimate does include some level of losses from these types of coverages,

The range of potential outcomes for this portion of the insured loss is very wide. But

the time element coverages will likely account for a significant portion of the impact

on the international reinsurance market. This business is more heavily reinsured in

both the treaty 3 and facultative4 markets, which operate, respectively, by contract

and the prerogative of the reinsurer’s appetite for risk. The level of uncertainty

surrounding the earthquake’s impact on the international reinsurance market is

disproportionately influenced by time element coverage obligations.

To sum up, the loss to the insurance industry can attributed to 47.5% loss from

residential, 23.5% from commercial 15% from life, 5.5% from Marine, 1% from Auto

and 7.5% of losses to the international insurer.

3 Treaty Reinsurance is a method of reinsurance requiring the insurer and the reinsurer to formulate and execute a reinsurancecontract. The reinsurer then covers all the insurance policies coming within the scope of that contract. There are two basicmethods of treaty reinsurance: Quota Share Treaty Reinsurance, and Excess of Loss Treaty Reinsurance.

4 Facultative reinsurance, the ceding company cedes and the reinsurer assumes all or part of the risk assumed by a particular

specified insurance policy. Facultative reinsurance is negotiated separately for each insurance contract that is reinsured.Facultative reinsurance normally is purchased by ceding companies for individual risks not covered by their reinsurancetreaties, for amounts in excess of the monetary limits of their reinsurance treaties and for unusual risks

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 19/43

What hit the Country – What the Country hit

18

Impact on Japan’s currency – The YenThe Japanese yen (sign: ¥; code: JPY) is the official currency of Japan. It is the third

most-traded currency in the foreign exchange market after the United States dollar

and the euro. It is also widely used as a reserve currency after the U.S. dollar, theeuro and the pound sterling.

Shift to Gold Exchange Standard

Following the silver devaluation of 1873, Japan adhered to a gold standard, and by

the year 1897 the yen was worth only about US$0.50. In that year, Japan adopted a

gold exchange standard and hence froze the value of the yen at $0.50.

Fixed value of the Yen to the US dollar & Introduction to Floating Exchange Rates

The yen lost most of its value during and after World War II. After a period of

instability, in 1949, the value of the yen was fixed at ¥360 per US$1 through a United

States plan, which was part of the Bretton Woods System, to stabilize prices in the

Japanese economy. That exchange rate was maintained until 1971, when the United

States abandoned the gold standard, which had been a key element of the Bretton

Woods System5, setting in motion, changes that eventually led to floating exchange

rates in 1973.

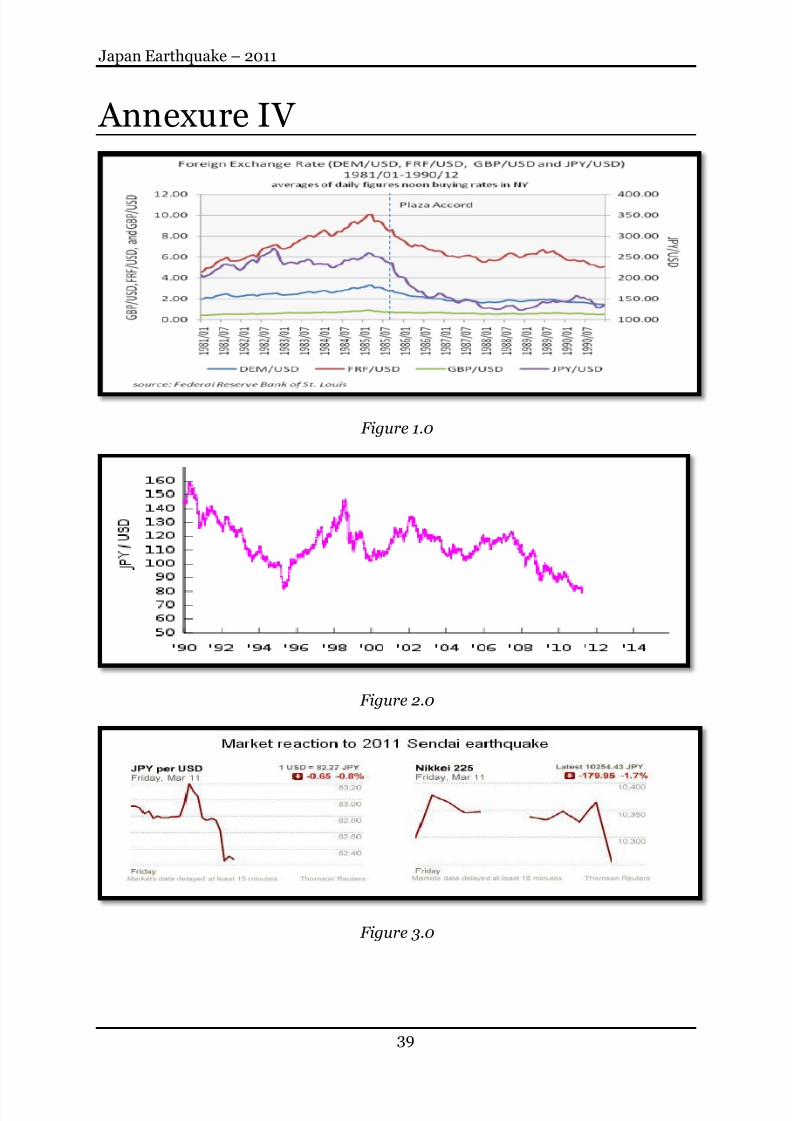

Highly Volatile Decade for Yen (1970-1980)

Floating exchange rates brought the yen to 271 per US$ from 308 yen per US$ in

1971, hurting the export growth as Japanese products became less competitive, even

though the Japanese Government tried to intervene in Forex market. After the 1973

Oil Crisis, the Yen depreciated & was in the range 290-300 per US$ from 1974-1976.

But due to trade surpluses in late 1970’s, the yen appreciated very strongly to 211 per

US$. But this appreciation was affected again due to 2nd Oil Crisis in 1979, which

weakened the yen to 227 per US$ in 1980 (Refer Annexure IV, Fig 1.0).

5 The Bretton Woods system of monetary management established the rules for commercial and financial relations among the world's major industrial states in the mid 20th century. The Bretton Woods system was the first example of a fully negotiated

monetary order intended to govern monetary relations among independent nation-states.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 20/43

Japan Earthquake – 2011

19

Weakening Yen (1980-85)

Though there was re-emergence of Trade surpluses in early 80’s, the yen remained

low at 221 per US$ in 1981. This lowered further due to large capital outflow from

Japan, from 1981-1985, to USA, as the interest rates in USA rose to new heights, than

the Japanese rates. This caused high supply of yen in Forex market, weakening it to

239 per US$ in 1985. But this also helped in promoting the rapid rise in Japanese

trade surpluses (Refer Annexure IV, Fig 1.0).

Impact of Plaza Accord

In 1985 a dramatic change began. Finance officials from major nations signed an

agreement (the Plaza Accord6) stating that the dollar was overvalued (and, therefore,

the yen undervalued). This agreement, and shifting supply and demand pressures in

the markets, led to a rapid rise in the value of the yen. From its average of ¥239 per

US$1 in 1985, the yen rose to a peak of ¥128 in 1988, virtually doubling its value

relative to the dollar. At the end of the decade, Yen stood at around ¥145 per US$.

Japan had entered the stage of depression (Refer Annexure IV, Fig 1.0).

Twin Disaster – Japanese Asset Bubble & Kobe Earthquake

The Japanese asset price bubble was an economic bubble in Japan from 1986 to1991, in which real estate and stock prices greatly inflated. This caused deflation in

Japan (which is still present). Yen depreciated a bit, in early months of 1990 but after

1991 it started strengthening & hit the strongest in 1995, due to the Kobe earthquake,

falling to 79.75 yen per dollar. The fall was due to the repatriating of funds by

Japanese people & also Mexican Peso Crisis. In the late 1990s, the yen retreated from

its extraordinary 1995 high, with the fairly wide fluctuations, getting extremely weak,

144 yen per US$ in August 1998 & standing at 102 yen per US$ in December 1999

(Refer Annexure IV, fig 2.0)

Deflation Trap (2000-2007) , US Crisis 2008 & Tohuku Earthquake 2011

The combination of an overvalued yen and the aftermath of collapsed asset bubbles

previous 5 years, forced Japan's economy into a deflationary slump from which it has

yet to fully recover. The yen started weakening till February 2002 to 133 yen per

US$, when the Bubble economy burst effect had come to an end. As Japan was about

6 The Plaza Accord or Plaza Agreement was an agreement between the governments of France, West Germany, Japan, theUnited States, and the United Kingdom, to depreciate the U.S. dollar in relation to the Japanese yen and German Deutsche

Mark by intervening in currency markets. The five governments signed the accord on September 22, 1985 at the Plaza Hotelin New York City.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 21/43

What hit the Country – What the Country hit

20

to get back to its feet, from 2003-2006, when the yen touched 103 yen per US$, it

was struck badly by the US sub-prime crisis in December 2007, when the yen

strengthened to 90 yen per US$ in early 2009. In that year, the yen had shown

fluctuations in the around 95 yen per US$; till late 2009 when the Japanese yen

again appreciated against the dollar falling lower than 90 yen per US$ mid 2010 &

later stabilizing around 83 yen per US$ in February 2011.

The Tohoku-Sendai Earthquake & Tsunami

The 2011 Tohuku earthquake and tsunami, officially named the Great East Japan

Earthquake, was caused by a 9.0-magnitude undersea megathrust earthquake off the

coast of Japan that occurred at 14:46 JST on Friday, 11 March 2011.

Japan's biggest earthquake in 140 years pushed global stocks and commodities

markets lower. But guess what went up? The Yen.

Japanese Yen fueled by earthquake

The Japanese Yen advanced on Friday 11th after a massive tsunami-including

earthquake hit Japan, killing hundreds. It was the biggest ever earthquake to hit

Japan.

The Japanese currency took a brief dip but then quickly turned higher against all 16

of its major counterparts. The reason? It still had safe-haven status, and there was

speculation that overseas Japanese were repatriating large amounts of the currency.The U.S. dollar slid 1.3% against the Japanese currency at 81.876 yen.

"You would expect any catastrophic event would have a negative impact on the

victim's currency," Chuck Butler, president of Everbank World Markets, "But this

natural disaster has caused these Japanese investors to bring their currency back

home, as they fear they will need it to help rebuild."

Over the years, Japanese investors have been investing their savings in foreign

markets, including the higher-yielding currencies of New Zealand and Australia,

given the near-zero interest rates in their home country. But the magnitude of theearthquake's devastation was helping to reverse this trend.

Risk modeller AIR Worldwide said that insured losses could be $14.5bn to $35bn,

which excludes some pretty devastating tsunami effects. So there were to be inflows

from (largely European) reinsurers. Meanwhile Japan’s domestic insurers w ere

probably expected to liquidate some of their assets to make payments too. These two

combined meant more yen inflows.

Still, there was watchfulness that the yen's appreciation will likely be short-term, and

longer-term investors should avoid the Japanese currency.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 22/43

Japan Earthquake – 2011

21

The economy had actually benefited from this disaster in the short run as there was

fiscal stimulus from reconstruction. But Japan's budget deficits were already close to

10% of GDP, and this additional spending only added to the problem, facing the

Japan's aging population (The Street, 2011) (Refer Annexure IV, fig 3.0).

Dollar hits al l-time low against Yen

The dollar hit an all-time low against a strengthening Japanese yen on 16th, as global

uncertainty and the prospect of more cash flowing into Japan pushed its currency

higher.

The dollar fell as low as 76.54 against the yen in late trading on that day, dipping

under the previous all-time low of 79.75 set in April 1995.

Despite the nation's turmoil, the yen has long been a haven for risk-averse investors.Japanese corporations were also expected to repatriate vast amounts of capital. The

repatriation effect is that Japanese companies and households sell foreign assets to

cover needs at home. These holdings are mostly bonds of countries such as Brazil,

South Africa, Australia, or New Zealand with temptingly high interest rates. They

hold $50bn of bonds issued in Brazilian real and $27bn of "Uridashi"7 bonds in

Australia. The reversal of funds was expected to be swift. Japanese authorities soon

expected to intervene in currency markets to arrest the yen's appreciation. The BoJ

had immediately yet secretly injected $183 billion into the financial system in a move

to provide liquidity, on 14th March (CNN Money, 2011) (Refer Annexure IV, fig, 4.0).

What drove the yen's strength?

If you believe the Japanese government, it is all down to speculators, but there were

constant rumors that the yen's record high against the dollar on 17th April’s-day

trading was due to the repatriation of funds, mostly by insurance firms. What is not

in doubt is the remarkable rise of the yen after the dollar plunged to an all-time low

of 76.25 yen by the close of the US market. The question was why?

The markets were moved by a consensus view that Japanese institutions, particularly insurance companies, would repatriate assets into yen to meet their obligations

denominated in the currency. Ana Armstrong of Distinction Asset Management

wrote: "Japanese investors are selling overseas assets to bring home funds, and

insurance companies buy yen to meet obligations and foreign aid packages have all

increased short term demand for yen."

7 An Uridashi bond is a bond denominated in a foreign currency and sold directly to Japanese household investors. An Uridashi

bond is normally issued in high-yielding currencies such as New Zealand Dollars or Australian Dollars in order to give the

investor a higher return than the historically low domestic interest rate in Japan.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 23/43

What hit the Country – What the Country hit

22

The Japanese government moved fast to shoot this, with officials saying that

speculators were to blame and that there was "no evidence" of funds repatriating

assets.

That remains to be seen, but analysts expected an announcement on intervention in

the currency to mitigate the strength after a G7 (Group of 7 Industrial Nations:

Canada, France, Germany, Italy, Japan, UK & USA) meeting on the Japan situation.

It was noted that the situation was finely balanced, as while a stronger currency hurts

exports, it might help bring the costs of reconstruction and energy down.

Either way, while traders feast on the volatility in the markets, the disaster in Japan

has affected risk appetite dramatically.

But what we saw here is a function of ultra-leveraged hedge funds loosening their

carry trades8. If you borrowed yen and invested in higher-yielding currencies like the

Australian dollar or the South African rand, you made lots of money so long as the

rate of appreciation of the yen was lower than the interest rate you were getting in

the target currency. But when the yen starts to appreciate dramatically, you get

margin calls, which force you to buy a lot of yen in an illiquid market, which in turn

drives the yen up even further, which in turn not only increases the size of your

margin call but also triggers a large number of stop-loss orders and other FX options.

The result has been massive.

Difference with Yen strengthening following Kobe earthquake

in 1995

That earthquake, known in the US as the "Kobe Earthquake" and officially in Japan

as "The Great Hanshin-Awaji Earthquake Disaster," measured 6.8 in magnitude. The

energy released by Sendai quake was some 200 times that released by the Kobe

quake. Unlike the Kobe quake, the Tohoku quake was centered offshore, generating

the tsunami (Morris, 2011) (Refer Annexure IV, Fig 5.0).

The Kobe quake struck at Japan's industrial heartland. The affected regions

accounted for 12.4% of Japan's GDP in 1995. The five prefectures most affected by

the Tohoku quake are not as industrialized as the Kobe quake region. They accountfor about 7.8% of GDP.

The question now arises is how the latest disaster would be compared with the Kobe

earthquake in 1995.

8 The "carry trade" is basically an interest arbitrage speculation. Investors (speculators) borrow money in a country with low

interest rates, and then invest that borrowed money overseas in countries that pay higher interest rates. The risk, obviously, is

that the currency exchange rates may change. If the value of the Japanese Yen were to suddenly appreciate, then the amount

you owe (account payable) would grow, meaning that you would suddenly owe more money than you anticipated. On the

other hand, the currency that you invested in might suddenly depreciate, making your gain smaller.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 24/43

Japan Earthquake – 2011

23

The yen was on a tear at the time of the Kobe earthquake. It had already rallied from

just over 160 yen per dollar in 1990 to 99 yen at the end of 1994. The day before the

disaster, the yen had closed around 98.40 per dollar. It fell on the day of the quake to

99.11 and the following day to 99.69. The yen strengthened 20% against the U.S

dollar to turn down in April 1995, 3 months after the earthquake. USD/JPY

ultimately broke below 80 to a record low to 79.75 yen/$.

The reason for the appreciation, at first was, individuals and companies began to

repatriate some of their foreign holdings. It was more an indirect result of the

Mexican peso crisis & trade tensions with the United States were also a factor behind

the yen's rise. The yen reached a monthly high of 83.7 per USD by April, 1995 & then

to 79.75 per USD in and then began to depreciate sharply reaching 144.87 to the

dollar by August, 1998. The stock market immediately fell sharply, and continued to

fall until mid year, after which it had a good rise to June, 1997.

However, the main driver of the strong yen in 1995 wasn’t flow triggered by the

earthquake. A sharp increase in US interest rates in 1994 led to crisis in Mexico and

uncertainty in the dollar. In Japan, risk tolerance declined, and because US-Japan

trade negotiations were in their final stages, there were strong underlying concerns

about yen appreciation. In addition, life insurers and other Japanese entities

accelerated the hedging and selling of assets denominated in foreign currencies (also

owing to accounting issues; insurance companies had to record their mark-to-market

losses once the losses exceeded 15% and they rushed to sell foreign bonds before the

losses exceeded 15%), contributing to the yen’s sharp appreciation between the

earthquake and the end-March book-closing period. The BOJ lowered interest ratesin April 1995 in response to the strong yen.

When we compare the Kobe quake with the recent Tohuku quake, the economies of

Iwate, Miyagi and Fukushima regions that have been affected most seriously this

time account for 4-5% of Japan’s GDP, as compared to 2.5% of the Hyogo region

economy that was devastated by the Kobe earthquake in 1995. Now the damages to

infrastructure in the latest earthquake are more widespread owing to the effect of the

tsunamis, which also aggravated the human toll. Economists thus expected the short-

term economic effect this time to exceed that in 1995, which strengthened the yen by

making investors less likely to take risk.

Yen stabilizes after hitting record high

The dollar strengthened against the Japanese yen Thursday 16th ahead of a

conference call of G-7 finance ministers that was the first step towards intervention

by Japanese authorities in currency markets.

The call came after twin natural disasters pushed the yen to a record high against the

dollar, and fears over the country’s unf olding nuclear crisis continue to spook investors.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 25/43

What hit the Country – What the Country hit

24

On Wednesday 16th, the dollar fell as low as 76.54 against the yen in late trading,

dipping under the previous all-time low of 79.75 set in April 1995. By Thursday

afternoon, the dollar had stabilized around 79 versus the yen.

Reports published in advance of the conference call speculated that finance ministers

would voice a measure of support for Japanese efforts to weaken the yen.

For an economy facing a tough road ahead, a weaker currency would be a good thing.

Japan is an exporting nation and needs an undervalued currency to stimulate exports

and to fight persistent deflationary pressures. A stronger home currency will make

Japanese goods more expensive in overseas markets, to the disadvantage of Japan’s

manufacturing industry (CNN Money, 2011) (Refer Annexure IV, Fig 6.0).

What next for Yen?

The Yen had strengthened by more than 1 per cent against the dollar in the

immediate aftermath of the earthquake, but it’s been ticking back down. After the G7

intervened in Forex markets in the 3rd week of March, the Yen fell dramatically. But

at the end of the 1st week of April, however, the Yen has stabilized and is now starting

to claw back some of its losses. Also Yen weakness throughout that week was most

likely speculative JPY-selling from overseas investors. When Japanese corporate and

investors start buying back JPY to cut back their foreign risk positions, these JPY

short positions are likely to be unwound. That week’s USD/JPY’s rally was driven by

―JPY weakness‖, not USD strength — in fact, USD actually softened in trade-

weighted terms 9 over the period. Thus USD/JPY appreciation led only by JPY

weakness does not last long.

One has to wonder: is the Yen heading back towards record highs or will it wear out

soon and resume its decline?

There has been a tremendous influence to the G7, since the Yen fell by a whopping

5% following its intervention. Thus, investors are confident that the G7 won’t let the

yen go below 80 versus the dollar again.

However, it would be virtually impossible for the G7 to single-handedly lower the Yen. That’s because the Yen holdings of G7 Central Banks are absolutely small. For

example, the Fed holds only $14 Billion in Yen-denominated assets (compared to the

Bank of Japan’s $800+ Billion in Dollar assets), of which it deployed only $600

million towards the Yen intervention effort. Even if the Bank of Japan was secretly

involved (by printing money and advancing it to other Central Banks), its efforts

would still pale in comparison to overall Yen exchanges. Trading in the USD/JPY

pair alone accounts for an estimated $570 Billion per day. Thus, given the minute

9 an economic instrument used by economies to compare their exchange rate against those of their major trading partners

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 26/43

Japan Earthquake – 2011

25

amounts in question, it would be unworkable for the Central Banks alone to move the

Yen.

Foreign institutional interest in Yen assets – which initially surged as investors dived

in, following the 20% drop in the Nikkei 225 average – has probably worn out. The

Bank of Japan will probably continue to flood the markets with Yen, and theGovernment of Japan will need to issue a large amount of debt in order to pay for the

rebuilding effort. Given Japan’s already weak fiscal situation, it seems unlikely that it

can count on foreign sources of funding. Japan's debt burden currently stands at 200

percent of its gross domestic product, compared with about 85 percent when Kobe

struck. Japan will also be "tempted" to print money to pay for the reconstruction bill.

But concerns about inflation and higher interest rates will likely limit that option too,

noting that higher interest rates would have negative consequences given the

country's massive debt burden.

In nominal terms the currency today is just past its 1995 high of JPY83 per dollar,

but this overstates the currency’s strength. On a real, trade-weighted basis the yen is

still 36% below the 1995 peak. This suggests that there is more room for the currency

to continue appreciating, even though the headline exchange rate is already at new

highs and governments have been intervening to manage it. In the meantime, the

yen’s (real) relative weakness should continue to benefit Japanese exporters

(Fxstreet, 2011).

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 27/43

What hit the Country – What the Country hit

26

Impact of the Earthquake oncommodity

The balance of payments is an account of the exports and imports of a country. A positive balance of payment implies that the exports are more than the imports of

that country, and is a favorable scenario for a country. Japan is one of the few

countries in the world with a positive balance of payments. The export value of Japan

exceeded its import value by nearly 10% in FY 2011 (Ministry of Finance, Japan,

2011).

The main export and import commodities of Japan and its trading partners are

discussed previously. The question that arises is what commodities are most affected

by this crisis. Although many commodities were affected, this report will see the

impact on steel and base metals; oil, petroleum and Liquid Natural Gas (LNG); andnon-coking coal.

Impact of the 2011 earthquake on steel and base metals

Japan accounts for 7.8% of production and 4.6% of consumption in Steel & less than

10% of global exports.

Production Impact on steel

In CY10, Japan produced 110mt of crude steel and is forecast to produce 121mt in

CY11. Japan accounts for more than 10% of global ordinary steel exports accounting

for 29 mt of ordinary steel and 43mt including specialty steel. The natural disaster

will hinder the forecast 10% growth in production for CY11.

Production will be mainly affected due to shortage in power. According to Platts, as

of 14th March, only two steel mills (Sumitomo’s Kashima and Nippon’s Kamaishi)

had suspended work. While the direct impact from production cuts in these two

plants might not be significant, however, many steelmakers in Japan would have tocut or reduce production due to power rationing by the government. That said, the

reduced production would only trigger increased capacity utilization elsewhere, since

foremost the World has more than 20% capacity lying idle and that it ideally takes

only 3 months to restart a blast furnace.

In totality, hot rolled coil could see near term spikes, due to sudden decrease in

Japanese steel production, caused due to the crisis. But it will moderate in a two to

three months, once the capacity in other parts of the world starts coming online.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 28/43

Japan Earthquake – 2011

27

Consumption Impact on steel

Currently the pre-calamity Japanese consumption of steel is forecast to be 65mt in

CY11 i.e. around a 5% increase from 62mt in previous year. The major setback in

steel consumption would emerge from the automobile industry. Many car makers

including Suzuki motor, Mitsubishi motors, Toyota etc. announced plans to halt

production temporarily.

These cuts will not lead to a surplus in global steel market, since Japan accounts for

less than 1% of global imports. However, consumption could surprise positively once

rebuilding commences and the auto manufacturers start operating at normal rates.

Also majority of the reconstruction may be happening towards the latter half of CY11.

Thus steel raw materials could see correction in spot prices, however recovering and

possibly increasing in the next three months.

Impact on iron ore and coking coal

Iron ore and coking coal are the most essential components of steel. Japan accounts

for 13% of global iron ore imports and 22% of coking coal imports.

While traditionally Japan has been the price negotiator for iron ore and coking coal

with the big miners, the trend has been slowly undergoing a shift to Chinese steel

makers directly negotiating with the miners and two, frequency of prices movingfrom annual to quarterly and now possibly monthly contracts (with BHP talking

about a large spot market by year 2012 – BHP increased offer price by 21% to

US$188 to some Chinese steel makers). For these reasons the Japanese steel makers’

importance as price setters as reduced.

The impact on steel, due to crisis has helped to avoid major impacts of both its raw

materials. Production halts or reduced production due to power shortage will lead to

more availability of steel raw materials on spot market for a short period, which

could see a slight correction for both the raw materials (iron ore & coking coal) over

the next couple of months. According to Platts, some Japanese steel makers coulddeclare force measures on coal purchases.

In the medium term, both the raw materials could be positively impacted due to

increased capacity utilization in anticipation of an increase in Japanese steel demand

once it starts rebuilding the affected areas.

Therefore one can anticipate chances of increased imports of Iron Ore by the Korean

and Chinese firms due to increased steel capacity utilization; and secondly, the big

four suppliers of coking coal might be forced to sell small volumes in the spot market.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 29/43

What hit the Country – What the Country hit

28

One of them, Anglo settled for US$330 for German creek coal for Q2 CY11. BHP also

spoke of creating a liquid spot market over the next 12 months.

Would Indian steel benefit from the crisis?

Most of the steel that Japan exports are high end value added steel – the segment in

which India is fairly deficient. Therefore chances of any Indian companies getting

affected or directly taking advantage of this short term crisis are very less. The

Korean steel makers could be the major beneficiaries. However, any movement

towards the monthly pricing system by the steelmakers, could lead to a short term

gains from rising HRC prices.

Impact on Base metals

Apart from steel Japan is also a large consumer of Copper, Aluminum, and Zinc.

Japan consumes 4% to 5% of the total global production of the three metals;

however, the production capacity of Japan is 7% for copper and 4% to 5% of Zinc

which is not sufficient for the country. And due to the lack of natural raw materials in

the country, these base metals have to be imported.

Chances of base metals getting impacted to a large extent is less, even after shut

downs by Japanese factories would lead to a temporary drop in base metal demand,

since the percentage of Japanese consumption is only in the range of 4-5% of global

demand in the Copper-aluminum-zinc space.

However Japan is one of the largest importers of copper concentrate with an import

of 5.4mt in CY10. In the event of a prolonged halt in copper smelters, the imports

could be diverted elsewhere, thus leading to a temporary relief in the extremely tight

copper concentrate market. While copper concentrate market could slightly ease,

refined copper will tighten further, due to production halts in some Japanese copper

smelters. On 14th March, a total of 378kt of smelting capacity was offline.

Lead could be a major gainer on the back of increased battery demand for power

backups. Its price has shown a 3.9% increase.

On a medium term, the Japanese consumption of metals, there will increase and

surpass the estimated demand for CY11 and CY12 due to rebuilding of lost property

and infrastructure and replacement of lost goods. There will be a positive revision of

consumption over the next year to year and a half.

A further insight into the base metal exchanges like the London Metal Exchange

(LME) and India’s commodity exchange MCX give a glimpse into the current trade

prices and the impact of the Japan crisis.

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 30/43

Japan Earthquake – 2011

29

The foremost observation is that the concern about the nuclear crisis in Japan and

lower equity markets, base metal prices are expected to remain under pressure.

Aluminium prices ended lower by 0.8 percent on LME and half a percent on MCX

thereby underperforming the base metal pack. Aluminium stocks on London Metal

Exchange witnessed draw-down of 4,250 tonnes thereby marking fourth consecutivedecline. On the fundamental front, reports indicated that China has halted plans to

build new aluminium plants in the country to tackle serious over-capacity in the

industry.

Copper stocks on London Metal Exchange witnessed build-up of 1,525 tonnes

thereby marking third consecutive increase. On the fundamental front, copper

imports climbed by 29 percent in March to 304,299 tonnes. However on a year-on-

year basis, it declined by 33 percent.

Lead stocks on London Metal Exchange witnessed draw-down of 975 tonnes thereby

marking sixth consecutive decline. Open interest also declined along with increase in

prices by half a percent indicating unwinding of positions.

Nickel prices on LME ended higher by 0.4 percent while the gains on MCX were

more than a percent. Nickel stocks on London Metal Exchange witnessed draw-

downs of 234 tonnes thereby marking sixth consecutive decline.

Zinc stocks witnessed draw-down of a modest 300 tonnes from London Metal

Exchange as against increase of 1,150 tonnes on the previous day. After declining to

$10/tonne, the basis has moved back to average levels of $20/tonne thereby givingno clear indication about future price movement. Open interest however declined by

nearly 10 percent indicating unwinding of positions at higher levels (Commodity

Online, 2011).

To summarize, the commodity market also reacted to the crisis and base metal prices

of Copper, Aluminum and Zinc – the three most demanded metal in Japan – saw a

hit in prices, whereas Nickel and Lead saw trade according to the market dynamics.

Impact on Crude Oil

Japan imports 1.6% of world demand of crude oil. Based on the U.S. EIA data, Japan

imported 4.7 million barrels a day (bpd) in 2009, with total oil refining capacity of

4.6 million bpd at 29 facilities as of January 2010. According to Reuters, the six

refineries that are shut down have a total capacity of 1.40 million barrels per day

(bpd). That's about 1.6% of the 89.3 million bbl/d global 2011 product demand

forecast by the International Energy Agency (IEA).

7/29/2019 Japan Crisis_Final Draft

http://slidepdf.com/reader/full/japan-crisisfinal-draft 31/43