Embed Size (px)

Citation preview

January 3, 2003

Kevin RakinKevin RakinPresident and Chief Executive OfficerPresident and Chief Executive Officer

Kevin RakinKevin RakinPresident and Chief Executive OfficerPresident and Chief Executive Officer

Economic SummitEconomic Summit

andand

Outlook 2003Outlook 2003

CT'S Bioscience Cluster Continues CT'S Bioscience Cluster Continues to Have Impressive Economic Impact….to Have Impressive Economic Impact….

• Connecticut biotechnology companies raised nearly $557M in private and public capital in 2001

• Total 2001 R&D investments of $3.6B including biotechnology R&D of $277M • Employment level in 2001 increased to 16,500 jobs with average R&D annual salary at ~ $63,000

Seventh Annual Economic Report of Connecticut United for Research Excellence (CURE), Connecticut's BioScience Cluster

Results from the Biotechnology Sector….Results from the Biotechnology Sector….

> 325M people worldwide have been helped by >130 drugs and vaccines (U.S. FDA approved)

70 % of medicines on the market were approved in the last 6 yrs

> 350 drug products and vaccines currently in clinical trials for > 200 diseases, incl. cancers, Alzheimer's disease, heart disease, diabetes, multiple sclerosis, AIDS and arthritis

Biotechnology is responsible for hundreds of medical diagnostic tests

Source: BIO

Total 1,457 (342 are publicly held)

Total value $224B as of early May 2002

Have > tripled in size since 1992, with revenues increasing from $8B in 1992 to $27.6B in 2001

Currently employ 179,000 people; that's more than those employed by the toy and sporting goods industries

Spent $15.6B on R&D in 2001

Source: BIO

Some Interesting Statistics…Some Interesting Statistics…

US Biotech Companies

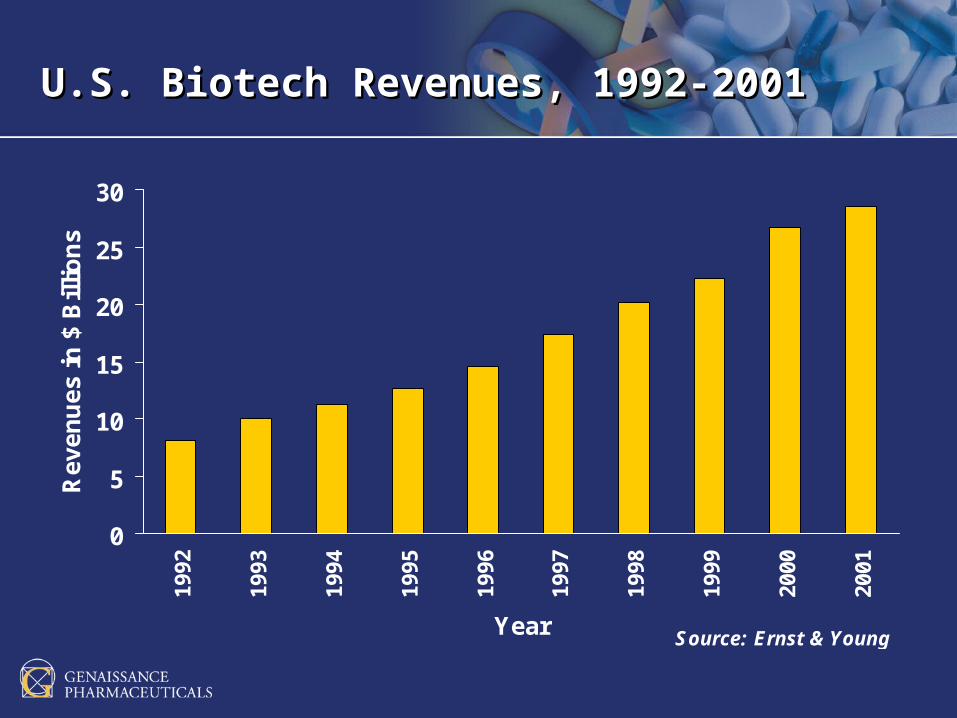

U.S. Biotech Revenues, 1992-2001U.S. Biotech Revenues, 1992-2001

0

5

10

15

20

25

3019

92

1993

1994

1995

1996

1997

1998

1999

2000

2001

Year

Re

ve

nu

es

in

$ B

illi

on

s

Source: Ernst & Young

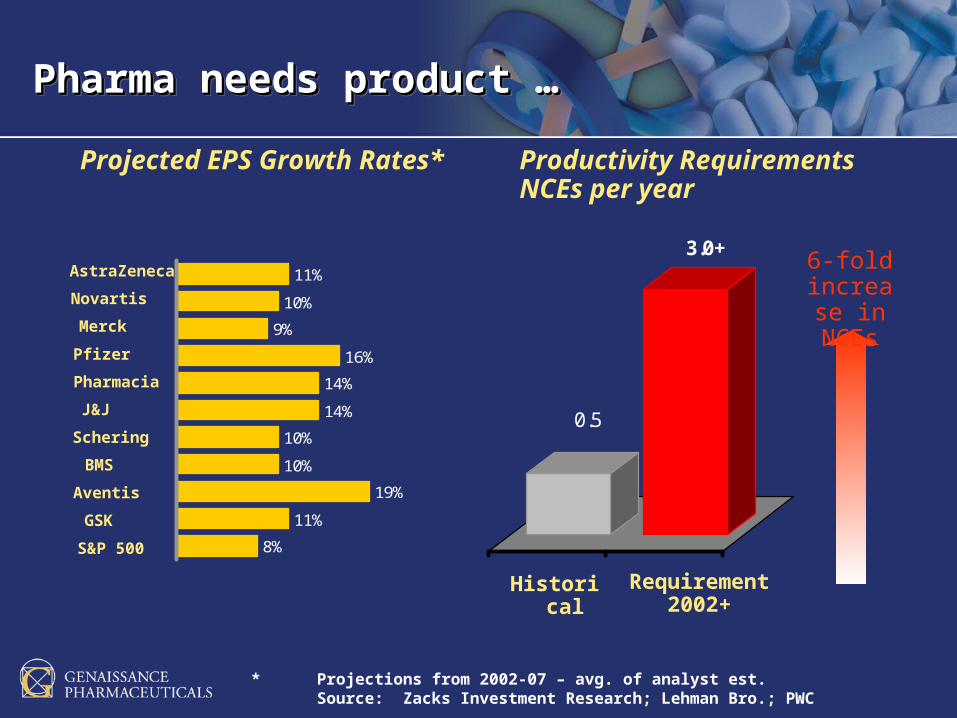

* Projections from 2002-07 – avg. of analyst est.Source:Zacks Investment Research; Lehman Bro.; PWC

Projected EPS Growth Rates*

10%

9%

16%

14%

10%

10%

19%

11%

8%

14%

11%

Productivity RequirementsNCEs per year

0.5

3.0+

Historical Requirement 2002+

6-fold increase in NCEs

Pharma needs product …Pharma needs product …Pharma needs product …Pharma needs product …

Pfizer

Pharmacia

Schering

Aventis

J&J

BMS

Merck

Novartis

AstraZeneca

GSK

S&P 500

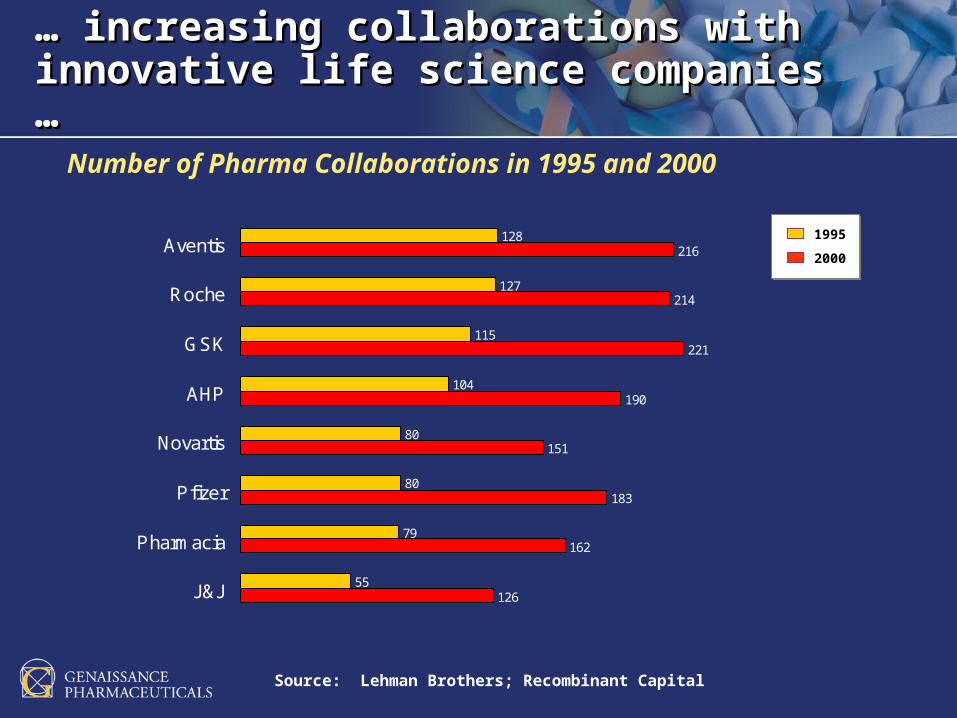

… … increasing collaborations with increasing collaborations with innovative life science companies …innovative life science companies …

Source: Lehman Brothers; Recombinant Capital

Number of Pharma Collaborations in 1995 and 2000

128

127

115

104

80

80

79

55

216

214

221

190

151

183

162

126

Aventis

Roche

GSK

AHP

Novartis

Pfizer

Pharmacia

J&J

1995

2000

Source:Signals (Recombinant Capital)

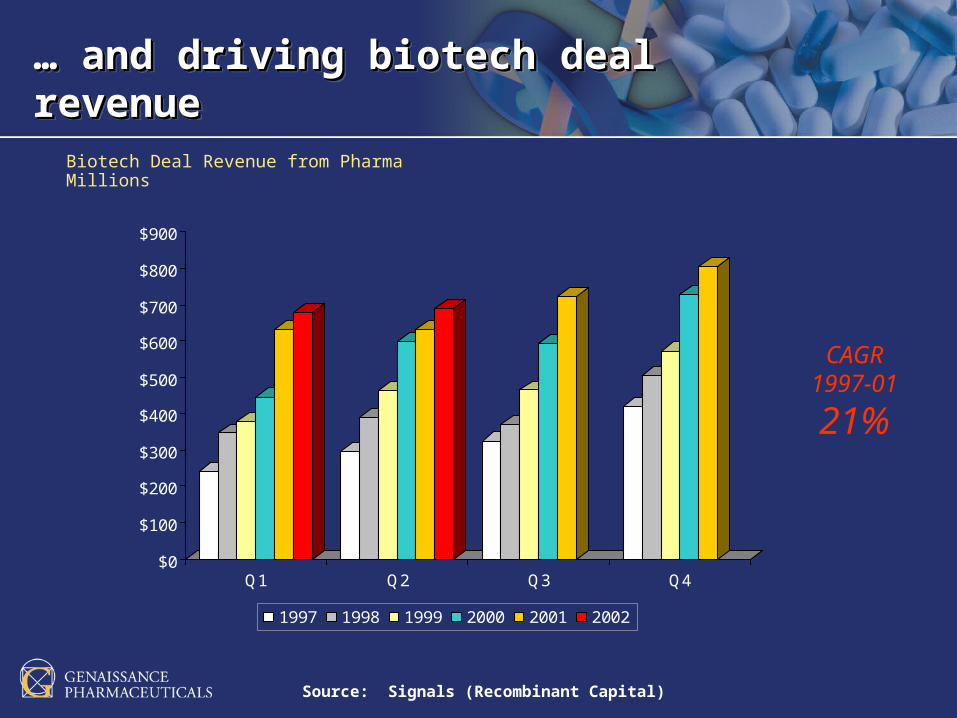

… … and driving biotech deal revenueand driving biotech deal revenue… … and driving biotech deal revenueand driving biotech deal revenue

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

Q1 Q2 Q3 Q4

1997 1998 1999 2000 2001 2002

Biotech Deal Revenue from PharmaMillions

CAGR1997-01

21%

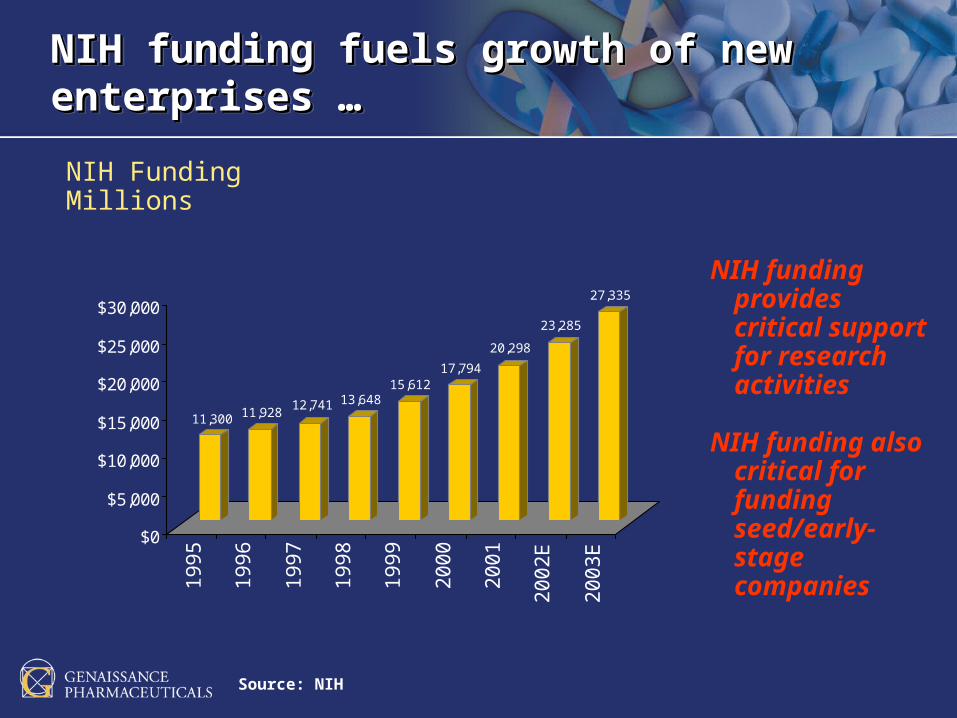

Source: NIH

NIH FundingMillions

NIH funding provides critical support for research activities

NIH funding also critical for funding seed/early-stage companies

NIH funding fuels growth of new enterprises …NIH funding fuels growth of new enterprises …NIH funding fuels growth of new enterprises …NIH funding fuels growth of new enterprises …

11,300 11,92812,741 13,648

15,61217,794

20,298

23,285

27,335

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

E

20

03

E

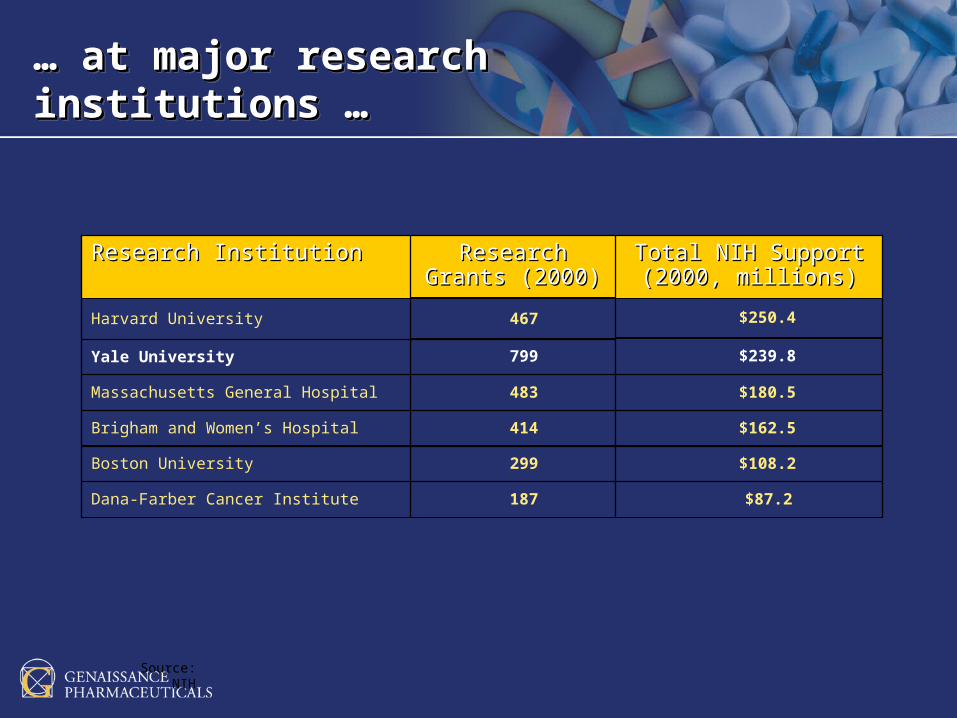

$87.2187Dana-Farber Cancer Institute

$108.2299Boston University

$162.5414Brigham and Women’s Hospital

$180.5483Massachusetts General Hospital

$250.4467Harvard University

Total NIH Support Total NIH Support (2000, millions)(2000, millions)

Research Grants Research Grants (2000)(2000)

Research InstitutionResearch Institution

… … at major research institutions …at major research institutions …… … at major research institutions …at major research institutions …

Source:NIH

Yale University $239.8799

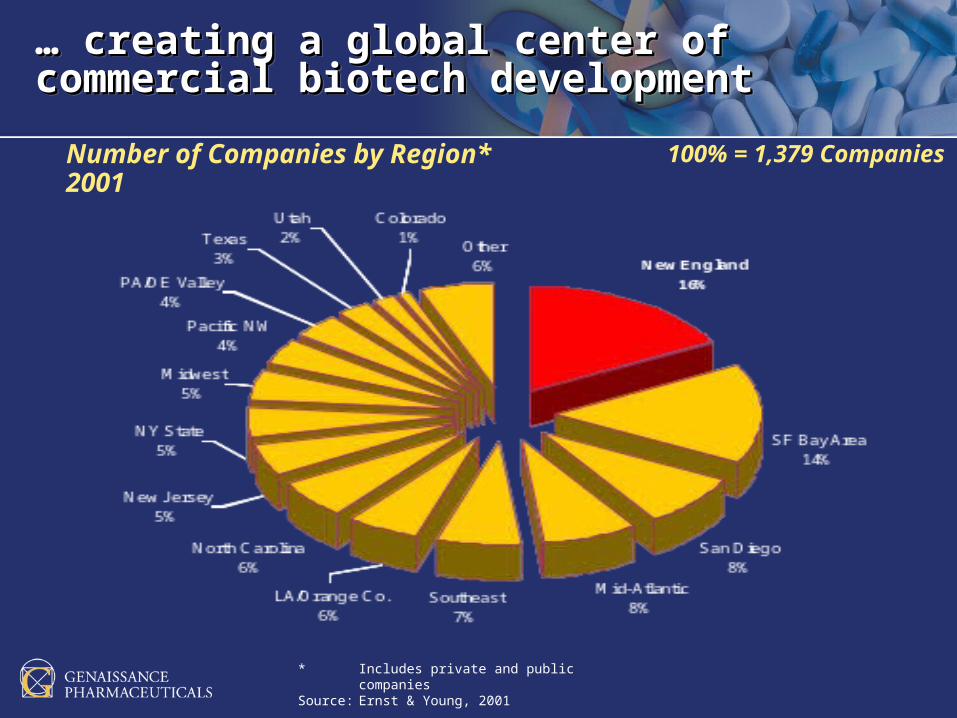

* Includes private and public companiesSource: Ernst & Young, 2001

… … creating a global center of creating a global center of commercial biotech developmentcommercial biotech development… … creating a global center of creating a global center of commercial biotech developmentcommercial biotech development

Number of Companies by Region*2001

100% = 1,379 Companies

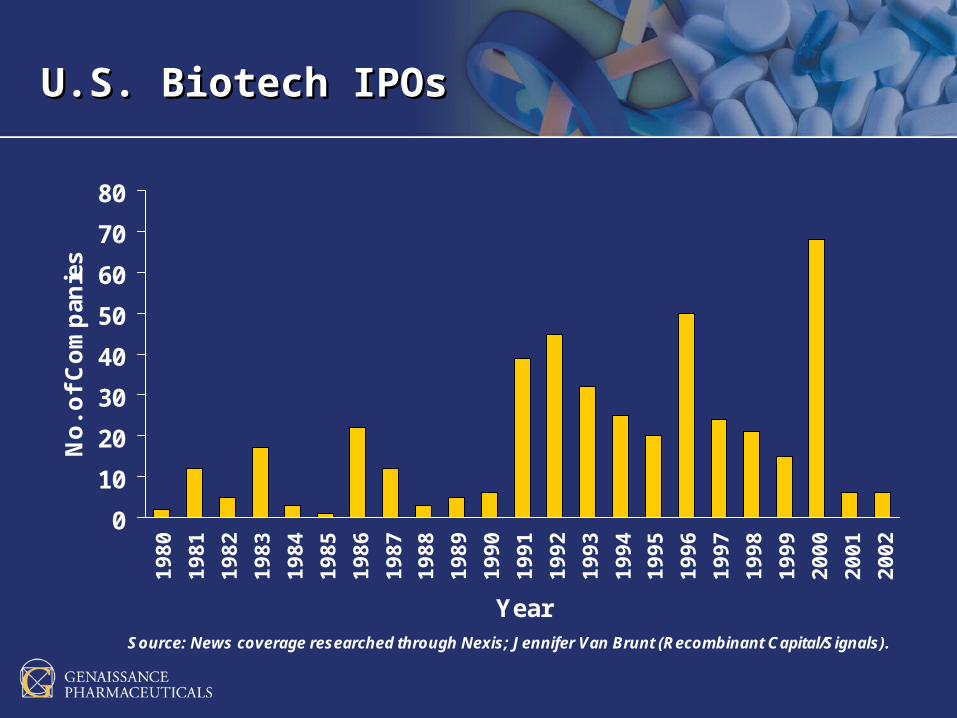

U.S. Biotech IPOsU.S. Biotech IPOs

0

10

20

30

40

50

60

70

801

98

0

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

Year

No

. o

f C

om

pan

ies

Source: News coverage researched through Nexis; Jennifer Van Brunt (Recombinant Capital/Signals).

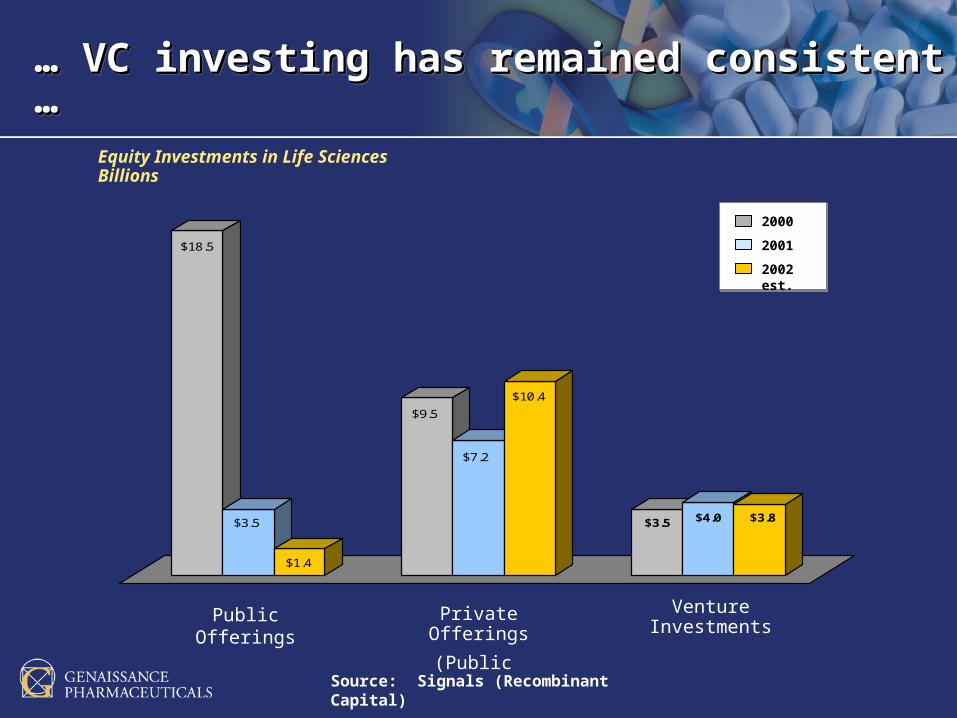

$18.5

$3.5

$1.4

$9.5

$7.2

$10.4

$3.5 $4.0 $3.8

Public Offerings

(Public Companies)

Private Offerings

(Public

Companies)

Venture Investments

(Private Companies)

2000

2001

2002 est.

Source: Signals (Recombinant Capital)

… … VC investing has remained consistent …VC investing has remained consistent …… … VC investing has remained consistent …VC investing has remained consistent …

Equity Investments in Life Sciences Billions

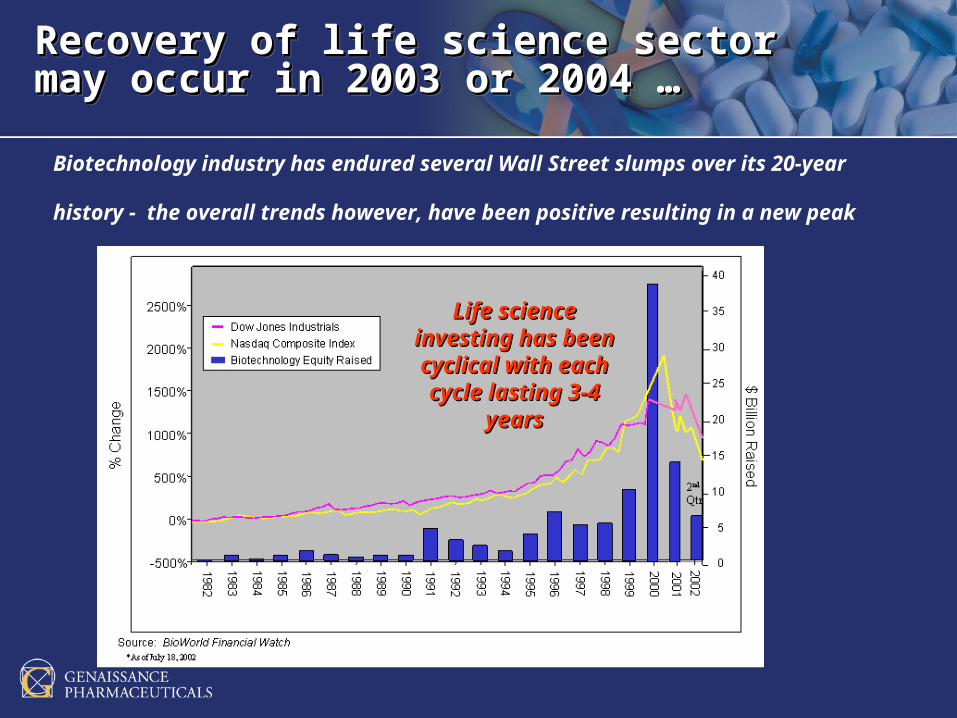

Recovery of life science sectorRecovery of life science sectormay occur in 2003 or 2004 …may occur in 2003 or 2004 …Recovery of life science sectorRecovery of life science sectormay occur in 2003 or 2004 …may occur in 2003 or 2004 …

Life science Life science investing has been investing has been cyclical with each cyclical with each cycle lasting 3-4 cycle lasting 3-4

yearsyears

Biotechnology industry has endured several Wall Street slumps over its 20-year

history - the overall trends however, have been positive resulting in a new peak

In SummaryIn Summary

The biotech sector is a major U.S. industry

Cluster has critical mass in Connnecticut

Drivers exist for continued growth:– Pharma needs biotech for new products and revenue growth– NIH Funding fuels early stage research– Private Investment in the biotech sector continues

Capital markets should improve 2003/04:– Emerging from bottom of the cycle– Companies are becoming more commercially oriented

From Genomics From Genomics to Drugsto Drugs

Personalized Medicine Personalized Medicine From Genomics™From Genomics™