Embed Size (px)

Citation preview

Christof Rühl, Group Chief Economist

January 2013

© BP 2013

Tight oil and shale gas: global implications

Global energy trends

- Characteristics

- Implications

Energy Outlook 2030

© BP 2013

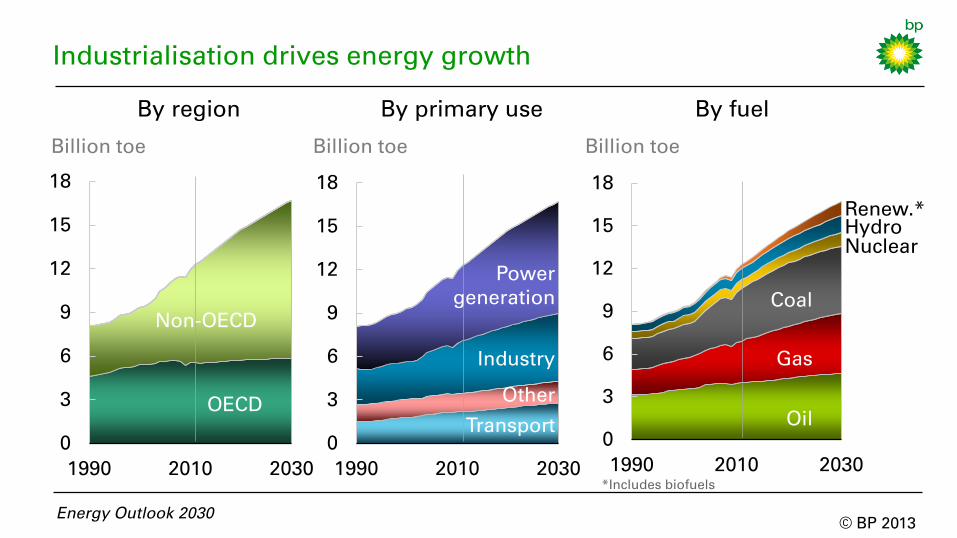

Industrialisation drives energy growth

OECD

Non-OECD

Billion toe

Energy Outlook 2030

0

3

6

9

12

15

18

1990 2010 2030

OECD

Non-OECD

0

3

6

9

12

15

18

1990 2010 2030

Other

Power

generation

Transport

By primary use By fuel By region

Oil

Coal

Gas

Billion toe Billion toe

Industry

0

3

6

9

12

15

18

1990 2010 2030

Hydro

Nuclear

Renew.*

Oil

Coal

Gas

*Includes biofuels

© BP 2013

Energy Outlook 2030

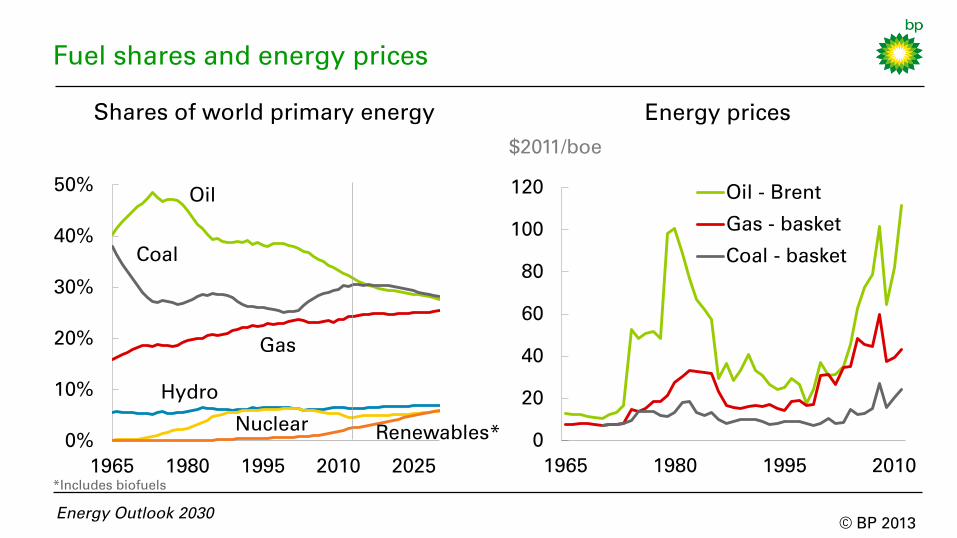

Shares of world primary energy

0%

10%

20%

30%

40%

50%

1965 1980 1995 2010 2025

Oil

Coal

Gas

Hydro

Nuclear Renewables*

*Includes biofuels

Fuel shares and energy prices

0

20

40

60

80

100

120

1965 1980 1995 2010

Oil - Brent

Gas - basket

Coal - basket

Energy prices

$2011/boe

© BP 2013

Energy Outlook 2030

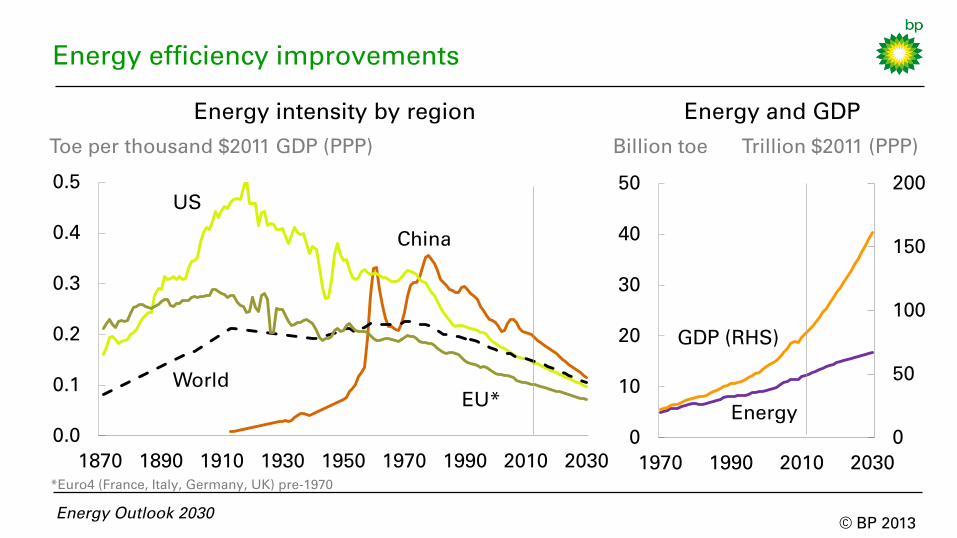

0.0

0.1

0.2

0.3

0.4

0.5

1870 1890 1910 1930 1950 1970 1990 2010 2030

Energy intensity by region

Toe per thousand $2011 GDP (PPP)

China

US

World

EU*

0

50

100

150

200

0

10

20

30

40

50

1970 1990 2010 2030

GDP (RHS)

Energy

Energy and GDP

Billion toe Trillion $2011 (PPP)

Energy efficiency improvements

*Euro4 (France, Italy, Germany, UK) pre-1970

© BP 2013

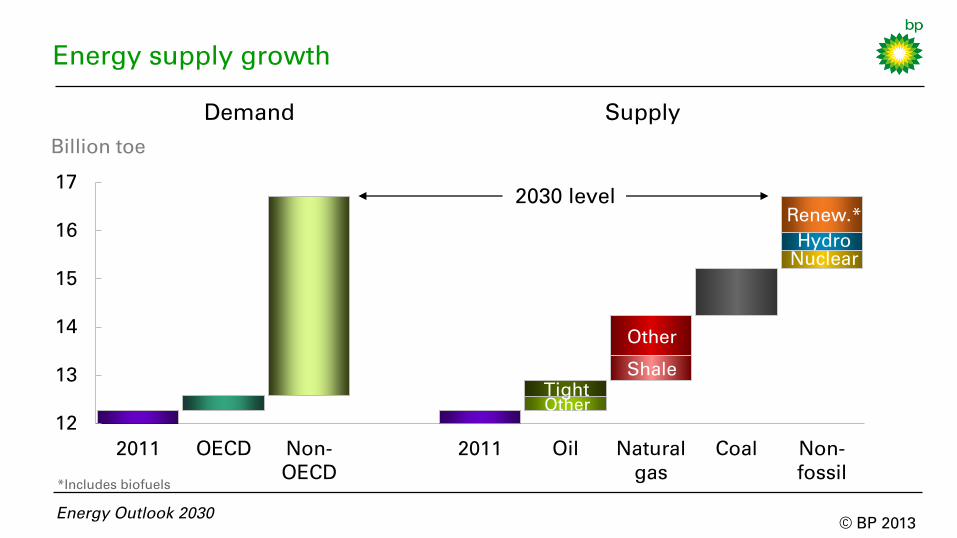

Energy supply growth

12

13

14

15

16

17

2011 OECD Non-

OECD

2011 Oil Natural

gas

Coal Non-

fossil

Demand Supply

Energy Outlook 2030

Tight

Other

Shale

Other

Nuclear

Hydro

Renew.*

Billion toe

2030 level

*Includes biofuels

© BP 2013

Tight oil and shale gas: global implications

Global energy trends

- Characteristics

- Implications

Energy Outlook 2030

© BP 2013

0

20

40

60

Asia P

acific

N. A

me

rica

S. &

C

.

Am

erica

Africa

Eu

ro

pe

&

Eu

ra

sia

Mid

dle

E

ast

Gas

Oil

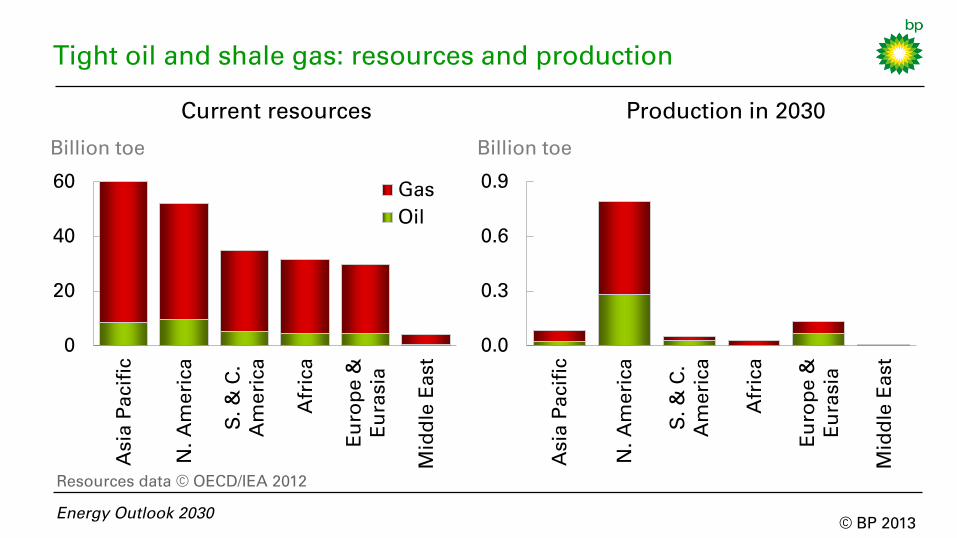

Tight oil and shale gas: resources and production

Billion toe

Current resources Production in 2030

Energy Outlook 2030

0.0

0.3

0.6

0.9

Asia P

acific

N. A

me

rica

S. &

C

.

Am

erica

Africa

Eu

ro

pe

&

Eu

ra

sia

Mid

dle

E

ast

Billion toe

Resources data © OECD/IEA 2012

© BP 2013

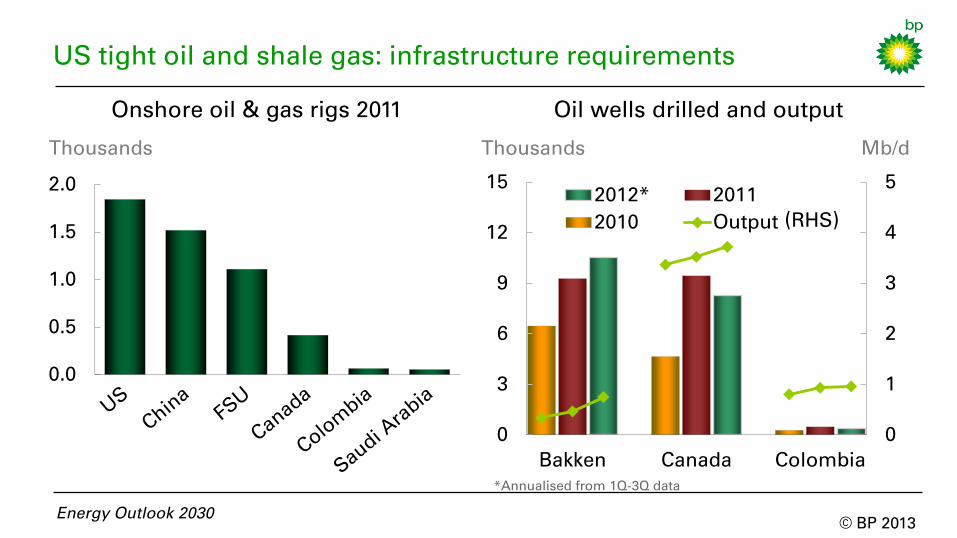

US tight oil and shale gas: infrastructure requirements

Onshore oil & gas rigs 2011

Thousands

Oil wells drilled and output

0

1

2

3

4

5

0

3

6

9

12

15

Bakken Canada Colombia

2012* 2011

2010 Output

Mb/d

Energy Outlook 2030

(RHS)

0.0

0.5

1.0

1.5

2.0

Thousands

*Annualised from 1Q-3Q data

© BP 2013

0%

2%

4%

6%

8%

10%

0

2

4

6

8

10

2000 2010 2020 2030

China

Russia

S. America

N. America

Liquids supply by type

30%

45%

0

15

30

45

60

75

90

105

1990 2000 2010 2020 2030

OPEC NGLs

OPEC crude

Biofuels

Oil sands

Tight oil

Other non-OPEC

Mb/d

NGLs

OPEC share (RHS)

Global supply growth and tight oil

Energy Outlook 2030

Tight oil output

% of total

(RHS)

Mb/d

© BP 2013

Global supply growth and shale gas

Energy Outlook 2030

Bcf/d

Gas production by type and region

0

100

200

300

400

500

1990 2000 2010 2020 2030

Non-OECD other

Non-OECD shale

OECD shale

OECD other

0%

6%

12%

18%

0

20

40

60

80

1990 2000 2010 2020 2030

RoW

China

Europe & Eurasia

Canada & Mexico

US

Shale gas production

Bcf/d

% of total (RHS)

© BP 2013

Tight oil and shale gas uncertainties

Share of global supply

growth

0

2

4

6

8

10

2010 2020 2030

Range

BP

Range of tight oil forecasts

(excludes NGLs)

Mb/d

Energy Outlook 2030

0%

25%

50%

75%

2000-10 2010-20 2020-30

Shale gas

Tight oil

0

20

40

60

80

100

120

2010 2020 2030

Range

BP

Bcf/d

Range of shale gas

forecasts

© BP 2013

Tight oil and shale gas: global implications

Global energy trends

- Characteristics

- Implications

Energy Outlook 2030

© BP 2013

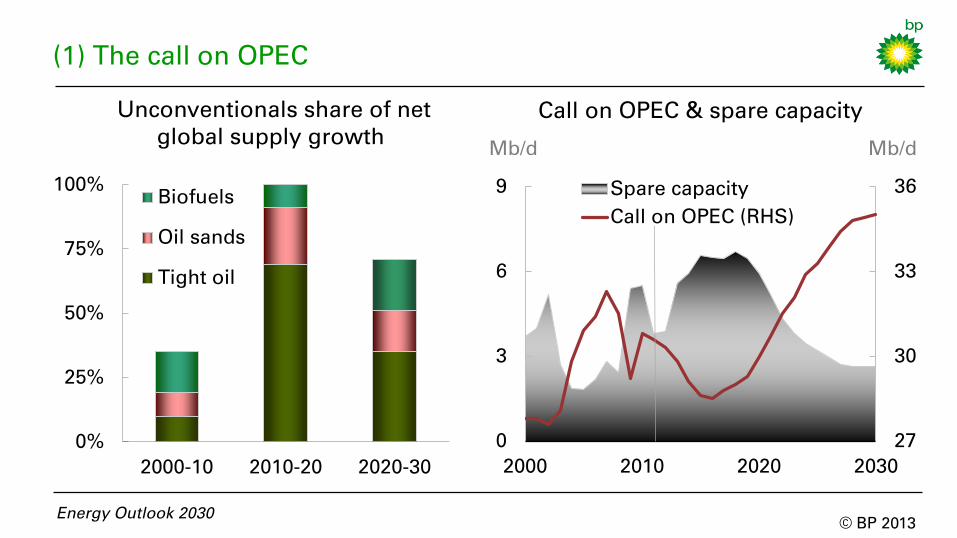

27

30

33

36

0

3

6

9

2000 2010 2020 2030

Spare capacity

Call on OPEC (RHS)

(1) The call on OPEC

Mb/d

Call on OPEC & spare capacity

Mb/d

Unconventionals share of net

global supply growth

0%

25%

50%

75%

100%

2000-10 2010-20 2020-30

Biofuels

Oil sands

Tight oil

Energy Outlook 2030

© BP 2013

0%

50%

(2) Oil and gas: reserves and production

2011 reserves

2030 output

% share of global total

Key:

Europe

N. America

S. & C. America Africa

Middle East

FSU

Asia Pacific

Energy Outlook 2030

Net exporters 2011

Net importers 2011

© BP 2013

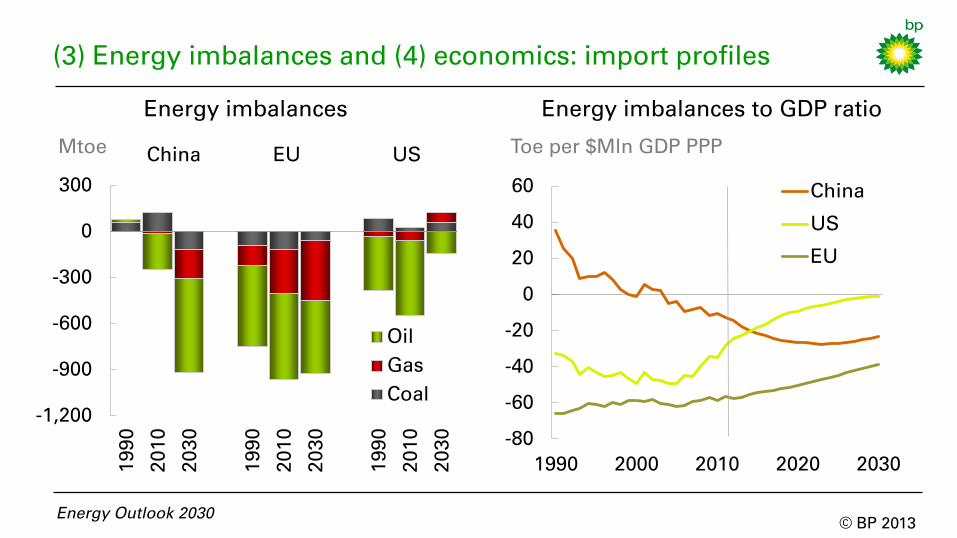

-80

-60

-40

-20

0

20

40

60

1990 2000 2010 2020 2030

China

US

EU

Energy imbalances to GDP ratio

Energy Outlook 2030

Energy imbalances

China EU US

-1,200

-900

-600

-300

0

300

199

0

201

0

203

0

199

0

201

0

203

0

199

0

201

0

203

0

Oil

Gas

Coal

Mtoe Toe per $Mln GDP PPP

(3) Energy imbalances and (4) economics: import profiles

© BP 2013

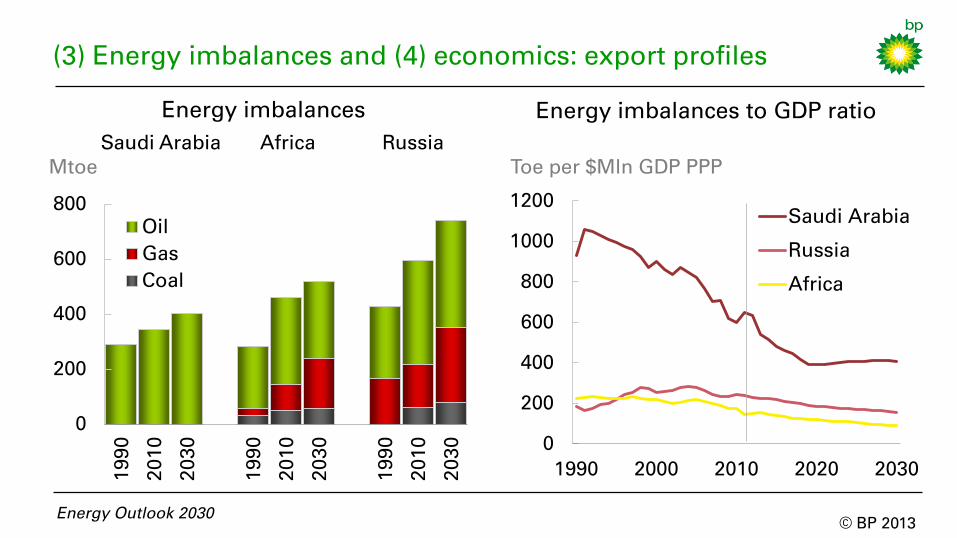

0

200

400

600

800

1000

1200

1990 2000 2010 2020 2030

Saudi Arabia

Russia

Africa

Energy imbalances to GDP ratio

Energy Outlook 2030

Energy imbalances

Saudi Arabia Africa Russia

0

200

400

600

800

199

0

201

0

203

0

199

0

201

0

203

0

199

0

201

0

203

0

Oil

Gas

Coal

Mtoe Toe per $Mln GDP PPP

(3) Energy imbalances and (4) economics: export profiles

© BP 2013

Oil

Gas

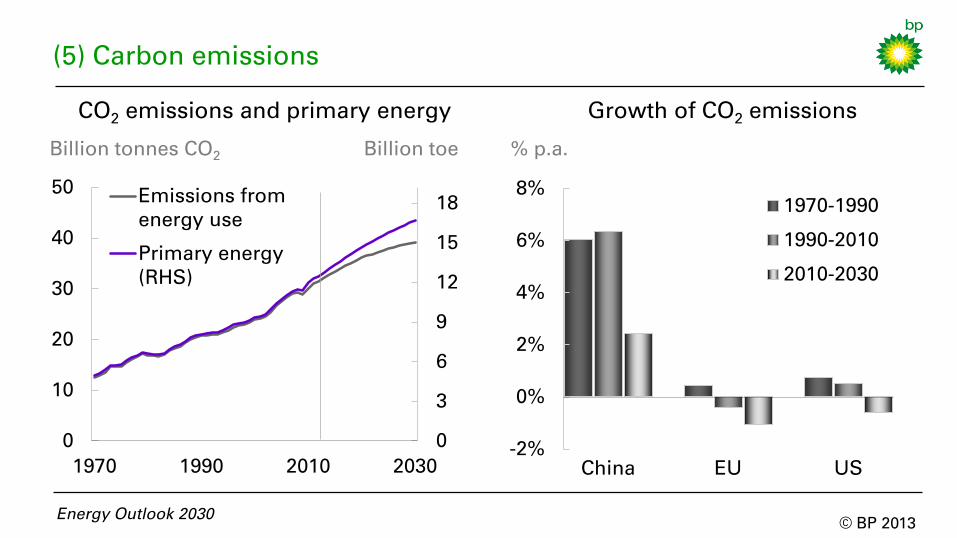

CO2 emissions and primary energy

Billion tonnes CO2

Energy Outlook 2030

Growth of CO2 emissions

% p.a.

0

3

6

9

12

15

18

0

10

20

30

40

50

1970 1990 2010 2030

Emissions from

energy use

Primary energy

(RHS)

Billion toe

-2%

0%

2%

4%

6%

8%

China EU US

1970-1990

1990-2010

2010-2030

(5) Carbon emissions

© BP 2013

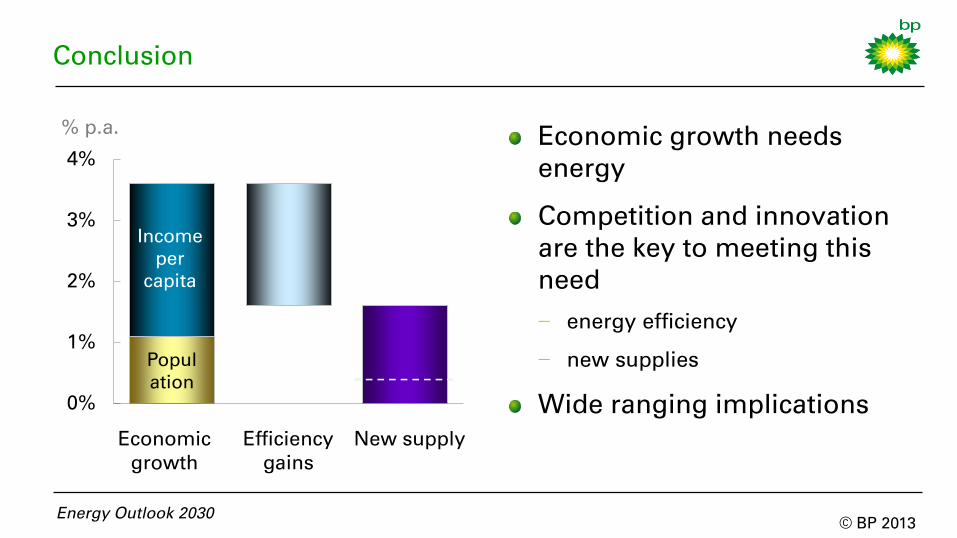

Conclusion

0%

1%

2%

3%

4%

Popul

ation

Income

per

capita

Economic

growth

Efficiency

gains

New supply

% p.a. Economic growth needs

energy

Competition and innovation

are the key to meeting this

need

− energy efficiency

− new supplies

Wide ranging implications

Energy Outlook 2030

January 2013

© BP 2013

Energy Outlook 2030

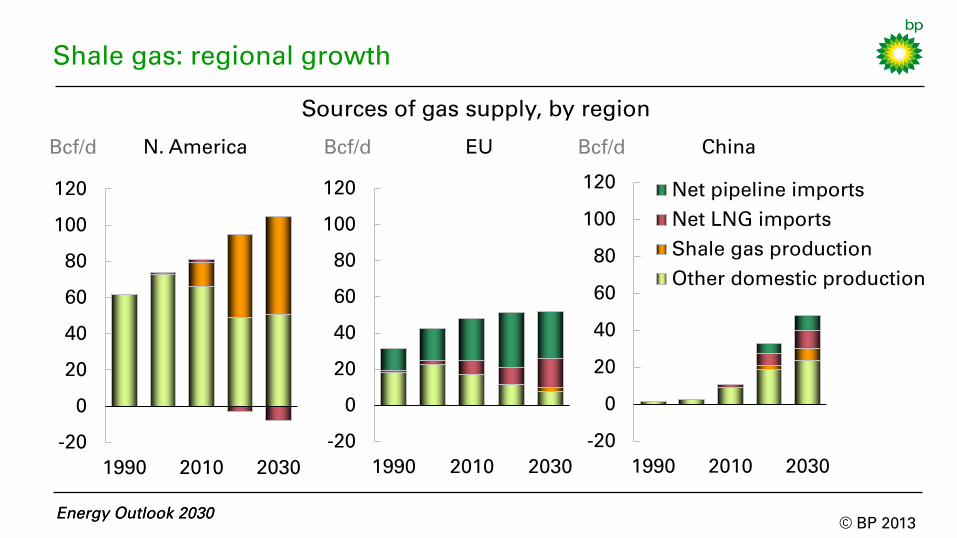

-20

0

20

40

60

80

100

120

1990 2010 2030

Net pipeline imports

Net LNG imports

Shale gas production

Other domestic production

Energy Outlook 2030

Shale gas: regional growth

Bcf/d China Bcf/d N. America Bcf/d EU

Sources of gas supply, by region

-20

0

20

40

60

80

100

120

1990 2010 2030

-20

0

20

40

60

80

100

120

1990 2010 2030

© BP 2013

Gas trade and market integration

Energy Outlook 2030

0%

5%

10%

15%

20%

0

20

40

60

80

1990 2000 2010 2020 2030

LNG

Bcf/d

LNG exports

% of total

consumption

(RHS)

LNG diversification

0

2

4

6

8

10

1991 1996 2001 2006 2011

Suppliers per importer

Customers per exporter