Embed Size (px)

DESCRIPTION

Presents an analysis of influence of code of ethics on decision making in business firms.

Citation preview

CODE OF ETHICS AMONG INDIAN BUSINESS FIRMS: A CROSS-SECTIONAL ANALYSIS OF ITS INCIDENCE, ROLE AND

COMPLIANCE

Sanjay K. Jain* and Anupama Mahajan**

The present paper is an attempt to fill this void in ethics literature. More specifically, the

paper aims at assessing incidence of code of ethics among Indian business firms, examining

With business organisations increasingly finding themselves confronted with ethical issues and dilemmas, concerns for codes of ethics have also intensified and so has the research interest in the field. The present paper reports results of a cross-sectional survey that the authors carried out to assess incidence of code of ethics among Indian business firms, examine managerial perceptions about the role of ethics as a source of ethical learning, likely influence of codes on employees’ thinking and behaviour and assess surveyed mangers’ perceptions about the reasons responsible for compliance and non-compliance of codes. Based on findings of the survey, managerial implications have been spelt out and directions for future researches in the area have been provided.

Ethics, of late, has become all pervasive and a matter of concern in all walks of human life.

And this is true of business also. In the wake of growing confrontation with ethical

dilemmas and increasing realization that “good ethics is good business”, business firms have

started looking for ways and means to build ethically strong organizations and inject a sense

of ethicality among their staff. Code of ethics represents one such effort. With growing

importance of code of ethics in the business world, researchers’ interest in the area has also

intensified over the last two decades or so. A number of researches have been carried out in

the past in several countries to examine the practices relating to use of code of ethics and

examine its influence on employees’ sensitivity to ethical issues and their proclivity to

behave ethically. Such researches are marked by their conspicuous absence in a developing

country like India (see, for example, Elankumaran, 2005; Jain and Mahajan, 2010).

* Professor of Marketing and International Business, Department of Commerce, Delhi School of Economics, University of

Delhi, Delhi - 110007, India. E-mail id: [email protected] ** Associate Professor, Bharati College, University of Delhi, Janak Puri, New Delhi 110056, India.

2

importance of code of ethics as a source of ethical learning, assessing its likely influence on

employees’ ethical thinking and behaviour, and investigating reasons responsible for

compliance and non-compliance of codes in the surveyed organizations. The data collected

through a survey of managers and owner-managers in Indian firms has been cross-classified

so as to ascertain whether the incidence and managerial perceptions about the role of code of

ethics and reasons responsible for compliance and non-compliance of codes differ across

different types of business firms.

The paper is divided into six sections. The first two sections are devoted to conceptual

overview of code of ethics and formulation of hypotheses that have been empirically tested

in the study. Research design used in the study is discussed next. Succeeding two sections

discuss the findings of the survey and its managerial and research implications.

CODE OF ETHICS: A CONCEPTUAL OVERVIEW Recent times have witnessed heightened interest in business ethics. As a result of

globalization and liberalisation, competition in the market has increased manifold and

pressures have started building up on business firms to behave sensibly and ethically. Both

the print and audio-visual media have become hyper active in publicizing scandalous

business deals and practices, resulting in initiation of criminal proceedings against the erring

firms and imposition of heavy penalties, boycotts of such companies by consumers and

considerable loss of goodwill in public minds. Bid-rigging in Japan, embezzlement and

bribery in China, fraud in Europe and massive lay-offs in the United States (Carroll and

Gannon, 1997), acid rains, Bhopal gas tragedy, pesticides in colas, germs in chocolates and

use of beef oil in French fries in India are some of the prominent media hyped instances of

unethical practices in business the world over. Having lost millions of dollars due to media

attacks, firms have come to realise that unethical practices, if discovered, can prove to be

disastrous to the financial and social standing of a business organisation (Jackson, 1996).

As of today, business firms have got highly awakened to the need of being proactive in

initiating steps to avoid negative publicity and consequent social and legal sanctions.

Management prudence demands that the business firms on their own become sensitive to

ethical issues and embody them in voluntary standards, without waiting for legal actions and

3

enactment of newer and stringent laws and regulations (Stark, 1993). Self-regulation has

always been advocated as a preferable solution to human problems and this holds true for

ethical problems too. It is this very sense of realization of the need for self regulation that

has been instrumental in formulation and adoption of codes of ethics among the business

firms, industries and associations (Adams, 2001; Schwartz, 2001; Murphy, 2002).

Simply speaking, codes of ethics are written statements of ethical principles and policies

that guide the people as to how to uphold high standards of behaviour in their dealing with

various internal and external stakeholders (Elankumaran, 2006; Stevens, 1999). Also

referred to as code of conduct, codes of practice, corporate credos, business conduct

guidelines, operating principles, staff handbooks or even as company objectives and mission

statements (Collins and Porras, 1997; Schlegelmilch and Houston, 1989, Schwartz, 2001);

code of ethics can be laid down at the individual firm level as well as at the levels of

industry and trade associations.

Code of ethics are in a way an effort on the part of business organisation to institutionalize

ethical values and standards to serve as a guide to its members in their dealings with various

stakeholders such as competitors, customers, suppliers, administrative authorities and

general public outside the organization as well as peers, subordinates and superiors within

the organization (Elankumaran, 2006; Weller, 1988). Codes of ethics cover a wide gamut of

ethical issues confronted in performing various business activities such as production,

marketing, research and development and human resource management. Organisations

create a code of ethics not only to guide their present and future actions, but also to signify

to the outside world that they care for and are concerned with ethics (Wotruba, 2001).

Code of Ethics: Review of Past Researches and Hypotheses Formulation A review of past studies as relevant to the objectives and issues under investigation in the

present study and formulation of hypotheses taken up for empirical testing in the present

research are as follows.

Incidence of Code of Ethics The early twentieth century saw the development of ‘codes of ethics’ for many professions,

including business. The idea of codes of ethics in business and the professions became

4

widely discussed and emerged as a subject of a special relevance in the early 1920s. Though

the codes are now prevalent around the world, especially among the large corporations; past

studies do point to variations present in incidence of code of ethics across countries. While

over 90 per cent of large corporations have been reported to be having code of ethics in the

United States, the corresponding percentage figures for Canada, the United Kingdom,

Germany and France are 86 per cent, 57 per cent, 51 per cent, and 37 per cent respectively

(Brooks, 1989; Schlegelmilch et al., 1989; Schlegelmilch and Langlois, 1990; Schwartz,

2002). Based on a small sample of 52 corporations, Elankumaran (2006) found 32

organisations to be having explicit and written codes of conduct in India. In addition to the

codes developed by the individual corporations, there also exist industry codes and

professional standards meant for particular type of firms and professions respectively.

In the wake of globalisation of economies and resulting pervasiveness of unethical behavior,

growing need is being increasingly felt for developing and implementing codes of ethics that

transcend national borders (Asgary and Mitschon, 2002). In a zest for global codes of

conduct, Rallapalli (1999) has gone to the extent of suggesting development of a global code

of marketing ethics and carried out a study to examine the feasibility and possible outcome

of such a global code.

Since not much information is available about the presence and use of codes of conduct in

India (e.g., Elankumaran, 2005; Jain and Mahajan, 2010), the present study is an attempt to

assess the incidence of code of ethics among different types of Indian business firms and

ascertain the extent to which the Indian firms make use of industry association codes.

Conceptual as well as past empirical studies, however, suggests that incidence of code of

ethics and use of industry association codes are likely to differ among firms of different

sizes and origins owing to different legal as well as perceptual requirements for a formal

mechanism of ensuring ethical corporate behaviour in these organizations (e.g., Batten et al.,

2008; Watson and Weaver, 2003). It is, therefore, hypothesised that:

H1a: Incidence of code of ethics differs across firms of different sizes (small vs. large) and origins (Indian vs. foreign).

H1b: Use of industry association code of ethics differs across firms of different sizes (small vs. large) and origins (Indian vs. foreign).

5

Role of Code of Ethics Firms attempt to develop and implement code of ethics with a view to enhance ethicality of

the corporate behaviour (e.g., Batten et al., 2008; Bowie, 1979; Skubik and Stening, 2008;

Watson and Weaver, 2003; Weller, 1988). Codes of conduct, if properly written and

communicated, can serve an educational role (e.g., Skubik and Stening, 2008). It is,

therefore, hypothesized that:

H2a: Code of ethics serves as a source of learning in business firms.

It is but natural to expect that the managerial staff and employees of the firms with their own

codes of conduct or following industry association codes are likely to be having greater

reliance on code of ethics as a source of learning than those who work in organizations that

do not have or follow such codes. Moreover, the persons working in firms of different sizes

(small vs. large) and origins (domestic vs. foreign) are likely to differ in their perception

about the importance of code of ethics as a source of learning, probably due to variations in

emphasis laid on ethical concerns across these types of organizations as well as in terms of

methods and approaches that they use in building ethical organizations (see, for example,

Batten et al., 2008; Watson and Weaver, 2003). It is, therefore, being hypothesized that:

H2b: Role of code of ethics as a source of learning differs across firms with and without codes, small and large firms, and Indian and foreign firms.

Code of ethics serves not only as a source of ethical learning, but also influences employees’

ethicality by way of sensitizing them to ethical issues faced by them in performing their jobs

and enhancing their proclivity to think and behave ethically (e.g., Batten et al., 2008; Bowie,

1979; Skubik and Stening, 2008; Watson and Weaver, 2003; Weller, 1988). Similar to the

reasoning put forward in respect of code of ethics serving as a source of ethical learning in

the preceding section, perceived effectiveness of code of ethics too is expected to vary

across different types of firms. The relevant hypotheses being taken up for empirical testing

in the study, therefore, are:

H3a: Code of ethics helps influencing employees thinking and behaviour.

H3b: Effectiveness of code of ethics in influencing employees thinking and behaviour differs across different types of firms.

6

Code of Ethics: Reasons for Compliance and Non-compliance Although a number of studies have been undertaken in the past to assess effectiveness of

codes in influencing ethical decision making, not much work has been done in respect of

compliance and non-compliance of codes (Weller, 1988). One such study was undertaken

by Ashkanasy et al. (2000) who found that compliance of code was primarily depended on

staff perception about the code being used by other persons in the organisation, while the

ethical tolerance (i.e., non-compliance) was based on personal values of the staff members.

Later, Schwartz (2001) in his study of relationship between codes and behavior concluded

that modified behaviour resulted merely due to the presence of a code of ethics. He also

identified a number of reasons (which he referred to as metaphors) to explain as to why

codes are complied or not complied with. In a recent study, Adam and Moore (2004) have

reported that informal methods used for implementing the codes are likely to yield greater

commitment than the formal methods.

Since any such knowledge about the reasons responsible for compliance and non-

compliance of codes can be greatly helpful in taking steps to ensure effective code

implementation in future, in the present study too it was decided to venture into exploration

of this aspect. Based on the frameworks adopted by Shwartz (2000) and other works in the

area, a few reasons were selected for assessing surveyed managers’ perceptions about the

factors that affect code compliance and non-compliance. Since variations can be expected to

be present across firms of different sizes and origins in respect of importance of reasons for

code implementation (e.g., Skubik and Stening, 2008; Watson and Weaver, 2003; Weller,

1988), it is hypothesised that:

H4a: Perceived importance of reasons responsible for code compliance differs across firms of different sizes and origins.

H4b: Perceived importance of reasons responsible for code non-compliance differs across firms of different sizes and origins.

RESEARCH DESIGN AND SAMPLE The present study is exploratory in nature. The necessary data have been gathered through a

survey of managers of various manufacturing organisations located in and around Delhi.

Convenience sampling method has been used to select the organisations. Managers of the

7

selected organisations were personally approached to elicit the needed information from

them. A structured non-disguised questionnaire has been employed to collect the primary

data. Based on review of ethics literature, various scale items were identified for use in the

questionnaire. The responses to various items were obtained using a on a 5-point Likert

scale. But before finalizing the questionnaire, it was thought appropriate to conduct a pilot

study. The draft questionnaire was pilot tested with a few executives. The potential for

systematic bias was minimized by asking a few knowledgeable individuals to assess the

content validity of the items prior to their inclusion in the questionnaire. Based on their

comments and observations, the draft questionnaire was modified to enhance its

understanding to the target respondents. Details about the individual scale items and

response formats used in the study are discussed in sections discussing findings of the study.

Managers or owner-managers of 400 firms were personally approached. Even after repeated

follow-ups, only a total of 210 duly filled-in questionnaires could be collected back, thus

constituting a 52.5 per cent response rate. Based on the number of persons employed in the

firms, the total sample was categorized into small and large firms. Firms employing 100 or

less workers were classified as small firms, and the rest were categorised as large firms.

The number of firms belonging to these two categories is 81 and 129 respectively. Of the

total 210 firms, while 146 are Indian firms, the rest of 64 are foreign firms for being either

multinational corporations or subsidiaries of foreign firms.

The collected data have been analysed using mean values and percentage figures.

Differences in mean scores have been tested through use of z-tests and t-tests. Cronbach

alpha values have been computed to assess reliability of the three multi-item scales used for

gauzing respondents’ perceptions about the influence of code of ethics on employees’

sensitivity to ethical issues, fostering ethical intentions and inducing ethical behaviour.

ANALYSIS AND RESULTS

Presence and Absence of Codes of Ethics in Surveyed Firms

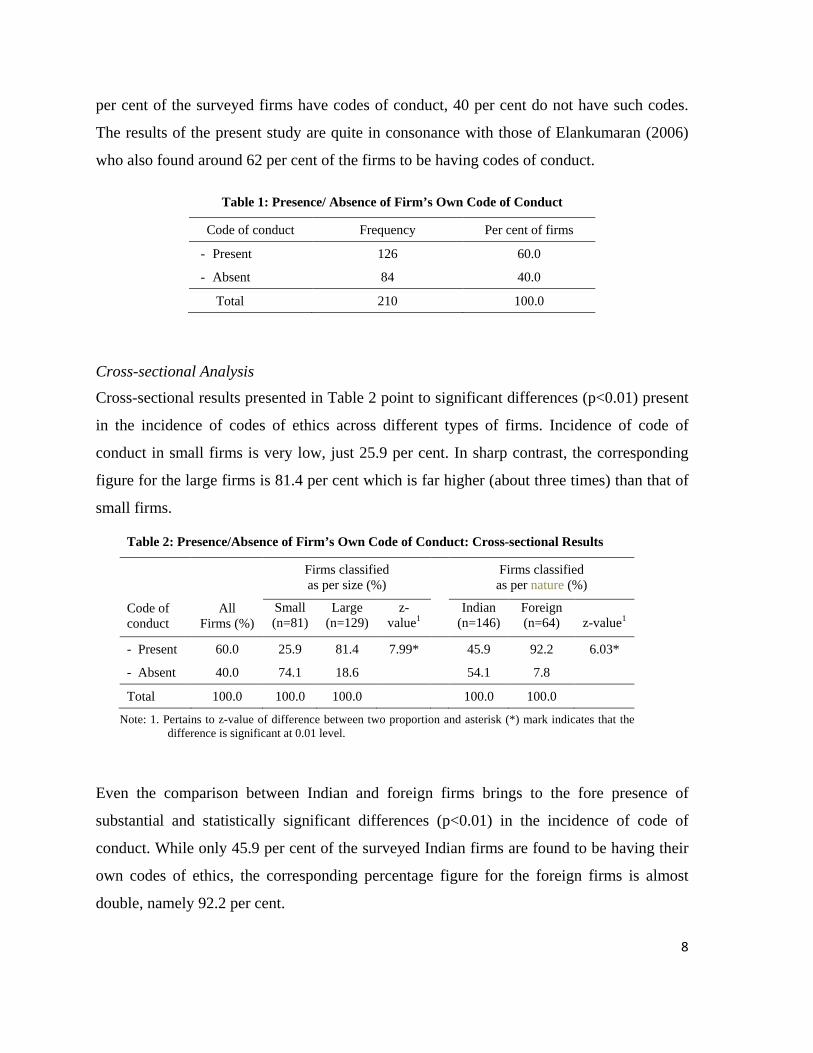

Overall Results Respondents were asked to report whether or not there existed code of conduct/ethics in

their firms. The survey results are summarized in Table 1. It can be observed that while 60

8

per cent of the surveyed firms have codes of conduct, 40 per cent do not have such codes.

The results of the present study are quite in consonance with those of Elankumaran (2006)

who also found around 62 per cent of the firms to be having codes of conduct.

Table 1: Presence/ Absence of Firm’s Own Code of Conduct

Code of conduct Frequency Per cent of firms

- Present 126 60.0

- Absent 84 40.0

Total 210 100.0

Cross-sectional Analysis Cross-sectional results presented in Table 2 point to significant differences (p<0.01) present

in the incidence of codes of ethics across different types of firms. Incidence of code of

conduct in small firms is very low, just 25.9 per cent. In sharp contrast, the corresponding

figure for the large firms is 81.4 per cent which is far higher (about three times) than that of

small firms.

Table 2: Presence/Absence of Firm’s Own Code of Conduct: Cross-sectional Results

Code of conduct

All Firms (%)

Firms classified as per size (%)

Firms classified as per nature (%)

Small (n=81)

Large (n=129)

z-value1

Indian (n=146)

Foreign (n=64)

z-value1

- Present 60.0 25.9 81.4 7.99* 45.9 92.2 6.03*

- Absent 40.0 74.1 18.6 54.1 7.8

Total 100.0 100.0 100.0 100.0 100.0

Note: 1. Pertains to z-value of difference between two proportion and asterisk (*) mark indicates that the difference is significant at 0.01 level.

Even the comparison between Indian and foreign firms brings to the fore presence of

substantial and statistically significant differences (p<0.01) in the incidence of code of

conduct. While only 45.9 per cent of the surveyed Indian firms are found to be having their

own codes of ethics, the corresponding percentage figure for the foreign firms is almost

double, namely 92.2 per cent.

9

The findings of the study thus lend ample support to the hypothesis that:

H1a: Incidence of code of ethics differs across firms of different sizes (small vs. large) and origins (Indian vs. foreign).

Use of Industry Association Code by Surveyed Firms

Overall Results Respondents were also asked to report whether their firms follow industry association codes

of conduct. Only 110 (i.e., 52.4 per cent) of total of 210 mangers/owners responded to this

query. As many as 47.6 per cent of the respondents did not provide response to this

question, implying thereby a high level of unawareness prevailing among the surveyed

managers/owner-managers about the use of codes of industry association codes by their

organisations. Such a high level of ignorance among the senior executives is something that

is highly disconcerting.

Responses obtained from 110 respondents were cross-classified to ascertain differences, if

any, existing among the surveyed firms. It can be observed from the results presented in

Table 3 that a great majority of the surveyed firms (i.e., 86.4 per cent) make use of the codes

developed by their industry associations.

Table 3: Use of Industry Association Code of Conduct

Industry code of conduct

Frequency

Per cent of firms

- Yes 95 86.4 - No 15 13.6

Total 110 100.0

Cross-sectional Analysis Cross-sectional results in respect of industry association codes are presented in Table 4 and

it can be observed that significant differences (p<0.01) exist across different types of firms

under investigation in the present study. As compared to small and Indian firms, it is the

large and foreign firms which report higher incidence of using industry codes.

Table 4: Use of Industry Association Code: Cross-sectional Results (N=110)

Code of conduct

All surveyed firms (%)

Firms classified as per size (%) Firms classified as per nature (%) Small (n=38)

Large (n=72)

z-value1

Indian (n=66)

Foreign (n=44)

z-value1

- Present 86.4 73.7 93.1 3.26* 78.8 97.7 2.70*

- Absent 13.6 26.3 6.9 21.2 2.3

Total 100.0 100.0 100.0 100.0 100.0

Note: 1. Pertains to z-value of difference between two proportion and asterisk (*) mark indicates that the difference is significant at 0.01 level.

The findings of the present study once again lend support to the hypothesis that: H1b: Use of industry association code of ethics differs across firms of different sizes (small vs. large) and

origins (Indian vs. foreign).

Code of Conduct: Perceptions about Its Role as a Source of Ethical Learning

Overall Results

Ethics literature posits code of ethics as a source of learning of ethical beliefs and behaviour

in the organization. Based on the past studies, a total of ten sources of learning (including

code of ethics) were identified and presented to the respondents for assessing their level of

agreement with each. A 5-point Likert scale ranging from ‘1= not at all’ to ‘5 = to full

extent’ was used for seeking their responses. The results are summarised in Table 5. It can

be observed that code of ethics in the opinion of respondents is not that important source a

learning as are other sources such as ‘observing direct supervisors’, ‘meetings with direct

supervisors regarding ethical issues’, ‘guidance from the seniors’, ‘observing other

employees’, ‘guiding the subordinates’ and’ training programmes based on ethical learning’.

The mean score for the code of ethics is 3.37, implying that the respondents only moderately

subscribe to the view that code of ethics is a source of learning. The results thus provide

only a marginal support to the hypothesis that: H2a: Code of ethics serves as a source of learning in business firms.

11

Table 5: Code of Ethics vs. Other Sources of Learning: Mean Perception Scores1

Source of learning

Mean score (n=210)

− Codes of ethics 3.37 − Ethics related training programmes 3.44 − Guidance from seniors 3.62 − Observing other employees 3.56 − Observing direct supervisors 3.79 − Meetings with direct supervisors regarding ethical issues 3.68 − Guiding the subordinates 3.50 − Participating in the meetings/seminars on ethical issues 3.31 − Reading or listening to Holy books 2.70 − Discussion on the ethical issues in the informal groups 3.23

Note: 1. A 5-point Likert scale ranging from ‘1= not at all’ to ‘5 = to full extent’ has been used for assessing respondents’ perceptions of importance of different sources of learning.

Cross-sectional Analysis An analysis of the survey results across different types of firms presents a somewhat

different picture. As can be observed from Table 6, respondents’ perception about the

importance of code of ethics does differs significantly between the firms with and without

codes (p<0.01). While the mean importance score for the firms with code of conduct is 3.57,

it is only 3.07 for the firms without code of ethics. In a similar vein, it can be observed that

respondents from the larger firms view code of ethics as a more important source than is the

case with the respondents from smaller firms (p<0.01). In a similar vein, it can be observed

that the perceived importance of the code of ethics as a source of ethical learning is

significantly higher (p<0.01) for the foreign firms than the Indian firms. Foreign firms have

a mean score of 3.81 which is significantly higher (p<0.01) than that of 3.18 for the Indian

firms. More effective communication and/or implementation of codes might be possibly the

reason underlying a more positive perception among the respondents about the code of

conduct as a source of learning in the foreign firms.

The above results thus fully corroborate our faith in the hypothesis that:

H2b: Role of code of ethics as a source of learning differs across firms with and without codes, small and large firms, and Indian and foreign firms.

Table 6: Perceived Role of Code of Ethics as a Source of Ethical Learning: Cross-sectional Results1

Overall mean score

(n=210)

Mean scores across firms with/ without code of ethics

Mean scores across size of firms

Mean scores across origin of firms

With code (n=126)

Without code

(n=84)

t-value

Small (n=81)

Large

(n=129)

t-value

Indian

(n=146)

Foreign (n=64)

t-value

Perceived role of code of conduct as a source of learning

3.37

3.57

3.11

2.70*

3.14

3.54

2.33**

3.20

3.81

3.39*

Notes: 1. A 5-point Likert scale ranging from ‘1= not at all’ to ‘5 = to full extent’ has been used for assessing respondents’ perceptions of importance of different sources of learning.

2. * indicates that the difference is significant at 0.01 level

Managerial Perception of Likely Influence of Code of Conduct on Employees Business firms set up their own codes or follow industry codes with the belief that such

codes will be not only make their employees more sensitive to ethical issues, but will also

induce them to think and act more ethically in discharge of their duties. Based on the past

studies, three dimensions of code influence were identified and these included: enhancing

sensitivity to ethical issues, fostering ethical intentions and inducing ethical behaviours.

Multi-item scales were developed to tap these dimensions. Opinions of the surveyed

mangers were obtained on a five-point Likert scale, ranging from ‘1= strongly disagree’’ to

‘5 = strongly agree’. The Cronbach-alpha coefficients for the three dimensions are found to

be 0.65, 0.61 and 0.72 respectively. Since the alpha values are not very high, mean scores

for individual scale items rather than composite scales have been computed and used in the

study. The aggregative and cross-sectional results of the study using these scale items are

analysed in the following two sub-sections

Overall Results Though mean scores for each of the items (excepting item 7) are above a value of 3.25

(signifying upper level of threshold of respondents’ indifference; see foot note to Table 7),

the scores are nonetheless too low to imply respondents’ high level of belief in the role of

code of ethics in significantly enhancing either employees’ sensitivity to ethical issues or

fostering ethical intentions and behaviours in them. In respect of item 7, a mean score of

3.21 signifies respondents’ slight disagreement with the assertion that presence of codes

13

tend to induce employees to report violation of ethical standards to their seniors. In general,

the results fail to lend much support to the hypothesis that:

H3a: Code of ethics helps influencing employees thinking and behaviour.

Table 7: Managerial Perceptions1 about Likely Influence of Code of Ethics on Employees’ Sensitivity to Ethical Issues, Intentions and Behaviours: Overall Mean Scores

Statement

Overall mean score2 (n=210)

Enhancing sensitivity to ethical issues 1. Codes make employees more sensitive to ethical issues. 3.49 2. Codes prompt a discussion on the ethical issues. 3.40

Fostering ethical intentions 3. A reading of code of ethics inspires an individual to behave ethically. 3.28 4. Codes increase ability to resist/ turndown unethical requests. 3.40 5. Fear of punishment provided for in the codes acts as a deterrent to unethical

behaviour. 3.45

Inducing ethical behaviour 6. Codes reduce unintentional violation. 3.38 7. Employees may report to the seniors about violation of codes. 3.21 8. A company’s support to codes can lead to high standards of ethical behaviour. 3.76 9. Codes bridge the gap between what employees believe in and what they do. 3.47

Notes: 1. A 5-point Likert scale ranging from ‘1= strongly disagree’’ to ‘5 = strongly agree’ has been used for assessing respondents’ perceptions of role of code of ethics in influencing employees’ sensitivity to ethical issues, intentions and behaviour.

2. For the purposes of analysis, while a score ranging from 2.75 to 3.25 has been considered as reflecting respondents’ ‘indifferent attitude’ towards the scale item in question; a score above 3.25 has been construed as reflecting respondents’ ‘agreement’ with the scale items in question. A score below 2.75 is, on the other hand, is treated as indicative of respondents’ ‘disagreement’ with the statement.

Cross-sectional Analysis Results presented in Table 8 show presence of statistically significant differences in mean

influence scores between the firms with and without codes of conduct for as many as seven

out of nine scale items, with managers from the former category in general exuding much

higher agreement with the positive role of codes in making their employees sensitive to

ethical issues and fostering ethicality in their intentions and behaviours. Items 2 and 9 (i.e.,

role of codes in prompting employees to discuss ethical issues and bridging the gap between

14

employees’ beliefs and behaviour) are the lone exceptions in respect of which no significant

differences are observable between the two types of firms. Even otherwise, relatively lower

mean scores point to just an average level of respondents’ agreement even with these two

scale items.

A comparison between small and large firms reveals significant differences in respect of

only four out of a total of nine items. Items 1, 3, 4 and 6 are the items in respect of which the

surveyed respondents from the large firms are more in agreement with the role of codes in

sensitising employees to ethical issues, inspiring them to behave ethically, fostering

resistance among them to turndown unethical requests and reducing unintentional violations

of the ethical norms.

Surprisingly, mean perception scores about the role of codes in respect of all the nine items

are found to be significantly different between Indian and foreign firms, with the

respondents from the latter conveying much higher agreement with the role of codes than is

the case with managers from Indian companies. While the mean scores for various possible

effects of code of conduct for foreign firms range from 3.64 to 4.02; the corresponding

range of mean scores for majority of the items for the Indian firms are quite low (i.e., just

3.01 to 3.33 for the eight out of nine items). Lower means scores amply imply either an

ambivalence or low level of perceived importance among the respondents about the

influence of codes on the employees. Item 8 is the only exception in respect of which Indian

respondents are found to be in agreement with the proposition that codes can lead to high

standards of high ethical behaviour among the employees provided that company support is

available for the implementation and enforcement of codes.

In overall terms, the results of the present study are largely in support of the hypothesis that:

H3b: Effectiveness of code of ethics in influencing employees thinking and behaviour differs across different types of firms.

Table 8: Managerial Perceptions1 about Likely Influence of Code of Ethics on Employees’ Sensitivity to Ethical Issues, Intentions and Behaviours: Cross-sectional Results

Statement

Overall mean score2

(n=210)

Mean scores2 across firms with/without code of ethics

Mean scores2 across size of firms

Mean scores across origin of firms

With code

(n=126)

Without code

(n=84)

t-value3

Small (n=81)

Large

(n=129)

t-value3

Indian

(n=146)

Foreign (n=64)

t-value

Enhancing sensitivity to ethical issues 1. Codes make you more sensitive to ethical

issues. 3.49 3.74 3.12 3.91* 3.11 3.73 3.87* 3.30 3.91 3.57*

2. Codes prompt a discussion on the ethical issues.

3.40 3.49 3.26 1.41 3.32 3.45 0.79 3.27 3.70 2.62*

Fostering ethical intentions 3. A reading of code of ethics inspires an

individual to behave ethically. 3.28 3.42 3.07 2.11** 3.05 3.43 2.27** 3.10 3.70 3.54*

4. Codes increase employees’ ability to resist turndown unethical requests.

3.40 3.64 3.04 3.64* 3.10 3.58 2.90* 3.18 3.89 4.16*

5. Fear of punishment provided for in the codes acts as a deterrent to unethical behaviour.

3.45 3.60 3.23 2.43** 3.31 3.54 1.46 3.35 3.69 2.02**

Inducing ethical behaviour 6. Codes reduce unintentional violation. 3.38 3.55 3.12 2.65* 3.16 3.52 2.18** 3.27 3.64 2.12** 7. Employees may report to the seniors about

violation of codes. 3.21 3.36 2.98 2.34** 3.05 3.30 1.59 3.01 3.66 3.86*

8. A company’s support to codes can lead to high standards of ethical behaviour.

3.76 3.91 3.52 2.58* 3.68 3.81 0.84 3.64 4.02 2.32**

9. Codes bridge the gap between what employees believe in and what they do.

3.47 3.58 3.31 1.69 3.30 3.58 1.78 3.33 3.78 2.74*

Notes: 1.A 5-point Likert scale ranging from ‘1= strongly disagree’’ to ‘5 = Strongly agree’ has been used for assessing respondents’ perceptions of role of code of ethics in influencing employees’ sensitivity to ethical issues, intentions and behaviour.

2. For the purposes of analysis, while a score ranging from 2.75 to 3.25 has been considered as reflecting respondents’ ‘indifferent attitude’ towards the scale item in question; a score above 3.25 has been construed as reflecting respondents’ ‘agreement’ with the scale items in question. A score below 2.75 is, on the other hand, is treated as indicative of respondents’ ‘disagreement’ with the statement.

3. * indicates that the difference is significant at 0.01 level ** indicates that the difference is significant at 0.05 level

Reasons for Compliance and Non-compliance of Codes

Presence of code by itself cannot guarantee ethical decision making in the organizations.

What is more crucial is effective implementation of the codes. Though there is a dearth of

empirical studies in the area, the limited research does point to certain reasons that lead to

compliance and non-compliance of codes in the organisation. The information about the

scale used in this context and findings of the survey in this connection are presented in the

succeeding two sub-sections. It may, however, be mentioned here that the discussion in the

following two sub-sections is based only on the responses received from the firms having

codes of conduct. The reason underlying the use of limited subset of sample is that the

respondents from the firms having codes of conduct are more likely to be in a position to

provide more valid information based on their first hand experiences with the

implementation of codes than their counterparts who are unlikely to be having such an

objective information and would be airing somewhat impressionistic information based

simply on their opinions and gut feelings.

Reasons Responsible for Code Compliance Overall Results For delving into an investigation of the reasons responsible for code compliance,

respondents from the firms having code of conduct were presented with a list of four

reasons, viz., ‘personal values’, ‘fear of losing job’ and ‘expectation of reward’ and ‘loyalty

to organisation’. These are the same reasons which Schwartz (2001) used in his study as

metaphors. The respondents were asked to state their level of agreement/ disagreement with

each of the metaphors.

The results are presented in Table 9 and it can be observed that mean scores for all the

statements are in the range of 3.56 to 3.95, implying respondents’ relatively high level of

respondents’ agreement with the four metaphors as being reasons responsible for code

compliance in the business organizations.

When analysed in terms of ranks, ‘personal value’ emerges as the top most reason, followed

by ‘expectation of reward’ and ‘loyalty to organisation’, and in that order. ‘Fear of losing

the job’ has received the lowest score. The analysis, thus, indicates that ‘personal values’

and ‘expectation of reward’ are the two most important reasons perceived by the Indian

17

managers/owners for code compliance in their organizations. Findings of the present study

to some extent are consistent with those of previous studies. While the study by Ashkanasy

et al. (2000) reported that the ethical tolerance in the organizations is based on ‘personal

values’, the study conducted by Baumhart (1961) found ‘reward’ as being an important

determinant of ethical behaviour.

Table 9: Perceptions1 of Indian Managers about Code Compliance: Overall Mean Scores Statement

Overall mean score2,3

(n=126)

1. One complies with the code because of his personal values. 3.95 (1) 2. Fear of losing the job for non-compliance makes one comply with the

code. 3.56 (4)

3. Organisations expect their employees to behave ethically and reward them accordingly.

3.87 (2)

4. Loyalty towards one’s organisation makes one adhere to the codes of ethics.

3.76 (3)

Notes: 1. A 5-point Likert scale ranging from ‘1= strongly disagree’’ to ‘5 = strongly agree’ has been used for assessing respondents’ perceptions of role of code of ethics in influencing employees’ sensitivity to ethical issues, intentions and behaviour.

2. Rank numbers have been given on the basis of mean scores. 3. For the purposes of analysis, while a score ranging from 2.75 to 3.25 has been considered as reflecting

respondents’ ‘indifferent attitude’ towards the scale item in question; a score above 3.25 has been construed as reflecting respondents’ ‘agreement’ with the scale items in question. A score below 2.75 is, on the other hand, is treated as indicative of respondents’ ‘disagreement’ with the statement.

Cross-sectional Analysis Data relating to reasons for code compliance were cross-analysed and the results are

summarised in Table 10. A perusal of the results reveal no significant differences in mean

scores assigned to different metaphors by the respondents of small and large firms. Exactly

same is the situation in respect of differences between the Indian and foreign firms. The

study findings thus fail to support the hypotheses:

H4a: Perceived importance of reasons responsible for code compliance differs across firms of different sizes and origins.

Table 10: Perceptions1 of Indian Managers about Reasons for Code Compliance: Cross-sectional Results

Statement

Overall mean

score2,3 (n=126)

Mean scores2,3 across size of firms

Mean scores2,3 across origin of firms

Small (n=21)

Large (n=105)

t-value4

Indian (n=67)

Foreign (n=59)

t-value4

1. One complies with the code because of his personal values.

3.95 (1) 3.95 (1) 3.95 (1) 0.00 4.02 (1) 3.88 (2) 0.70

2. Fear of losing the job for non-compliance makes one comply with the code.

3.56 (4) 3.48 (4) 3.57 (3) 0.39 3.42 (4) 3.71 (4) 1.38

3. Organisations expect their employees to behave ethically and reward them accordingly.

3.87 (2) 3.86 (2) 3.88 (2) 0.09 3.74 (2) 4.01 (1) 1.68

4. Loyalty towards one’s organisation makes one adhere to the codes of ethics.

3.76 (3) 3.95 (3) 3.72 (4) 1.01 3.75 (3) 3.78 (3) 0.18

Notes: 1. A 5-point Likert scale ranging from ‘1= strongly disagree’’ to ‘5 = strongly agree’ has been used for assessing respondents’ perceptions of role of code of ethics in influencing employees’ sensitivity to ethical issues, intentions and behaviour.

2. Rank numbers have been given on the basis of mean scores. 3. For the purposes of analysis, while a score ranging from 2.75 to 3.25 has been considered as reflecting respondents’ ‘indifferent attitude’

towards the scale item in question; a score above 3.25 has been construed as reflecting respondents’ ‘agreement’ with the scale items in question. A score below 2.75 is, on the other hand, is treated as indicative of respondents’ ‘disagreement’ with the statement.

4. None of the t-values is found to be significant (p<0.05).

Perceptions Regarding Reasons for Non-compliance of Codes

Overall Results A total of nine metaphors as used by Schwartz for examining non-compliance of codes were

employed in the present study after making necessary modifications in their wordings and

context so as to enhance their understandability to the respondents. Respondents were asked to

indicate their level of agreement with each of the metaphors on a 5-point Likert scale, ranging

from ‘5=strongly agree’ to ‘3= can’t say’ and ‘1=strongly disagree’.

The results reported in Table 11 show respondents’ agreement with metaphors 1, 4, 5, and 3 as

the possible reasons for non-compliance of codes. ‘Greed’ (item number 1) emerges as the most

important reason, followed by ‘seniors’ indifferent attitudes to ethical lapses’ (item 5), ‘feeling

of getting away with non-compliance’ (item 7) and ‘unhappiness with job/organization’ (item 3).

Respondents appear to be ambivalent with items 2, 3, 6 and 8. Respondents’ disagreement with

item 9 (i.e., ‘people find it more convenient to ignore codes’), on the other hand, implies that it is

not convenient for them to ignore the codes and thus non-comply with them.

Table 11: Perceptions1 of Indian Managers about Reasons for Code Non-compliance: Overall Mean Scores

Statement

Mean2,3 (n=126)

1. It is greed that makes people do a lot of wrong things and not comply with codes. 3.52 (1) 2. Codes are not followed by those having a strong desire to be the best. 3.02 (5) 3. Codes are violated by people who are not happy with their jobs/ organisations they work for. 2.90 (7) 4. People start resorting to unethical behaviour as acceptable behaviour as most others do it. 3.28 (4) 5. When people find the seniors indifferent to ethical lapses. 3.46 (2) 6. They sometimes think following codes strictly would not be in the best interest of company. 2.95 (6) 7. People think that they can get away with non-compliance easily. 3.36 (3) 8. People are ignorant about the existence of the code of conduct. 2.87 (8) 9. People find it more convenient to ignore codes. 2.71 (9)

Notes: 1. A 5-point Likert scale ranging from ‘1= strongly disagree’’ to ‘5 = strongly agree’ has been used for assessing respondents’ perceptions of role of code of ethics in influencing employees’ sensitivity to ethical issues, intentions and behaviour.

2. Rank numbers have been given on the basis of mean scores. 3. For the purposes of analysis, while a score ranging from 2.75 to 3.25 has been considered as reflecting respondents’

‘indifferent attitude’ towards the scale item in question; a score above 3.25 has been construed as reflecting respondents’ ‘agreement’ with the scale items in question. A score below 2.75 is, on the other hand, is treated as indicative of respondents’ ‘disagreement’ with the statement.

20

Cross-sectional Analysis Mean scores of the surveyed managers’ responses across different types of firms are presented in

Table 12. No significant differences are present in respect of mean scores between the small and

large firms. Almost similar is the situation in respect of responses obtained from the managers

from the Indian and foreign firms. Item 8 (i.e., ‘ignorance of the people about code of conduct')

is the only metaphor in respect of which the respondents from the two types of organizations

significantly differ (p<0.05), with respondents from the Indian firms reporting a higher degree of

ignorance of code as a plausible reason for the code non-compliance than is the case with their

counterparts from the foreign firms. The study findings thus in general fail to lend support to the

hypothesis that:

H4b: Perceived importance of reasons responsible for code non-compliance differs across firms of different sizes and origins.

CONCLUSIONS, DISCUSSION AND IMPLICATIONS

In view of dearth of researches in respect of incidence, role and compliance of code of conduct in

the country, the present study has been undertaken to assess the incidence code of conduct and

investigate its role and compliance among Indian business firms. Employing a structured-non-

disguised questionnaire, the necessary information was collected through a survey of managers

and owner-managers of 210 firms located in and around Delhi. A cross-sectional analysis was

performed on the collected data with a view to ascertain the extent to which different types of

firms differ in their incidence and perceptions about the role and compliance of code of conduct.

In respect of the incidence of code of ethics, survey finds only 60 per cent of the surveyed firms

to be having code of conduct. The incidence of code of conduct is significantly higher in large

and foreign firms (viz., 81.4 per cent and 92.2 per cent respectively) than is the case with the

small business organizations and Indian firms. Use of industry association code is found to be

high (86.4 per cent), but a caution is warranted here in view of high degree of non-response

present in respect of answer to this question. Managers of about 50 per cent of the firms have not

provided answer to this question.

Table 12: Perceptions1 of Indian Managers about Reasons for Code Non-compliance: Cross-sectional Results

Statement

Overall mean

score1,2

(n=126)

Mean scores2,3 across size of firms

Mean scores2, 3 across origin of firms

Small (n=21)

Large (n=105)

t-value4

Indian (n=67)

Foreign (n=59)

t-value4

1. It is greed that makes people do a lot of wrong things and not comply with codes.

3.52 (1) 3.86 (1) 3.46 (2) 1.40 3.64 (1) 3.39 (2) 1.17

2. Codes are not followed by those having a strong desire to be the best.

3.02 (5) 3.33 (3) 2.95 (5) 1.59 3.08 (6) 2.95 (6) 0.61

3. Codes are violated by people who are not happy with their jobs/ organisations they work for.

2.90 (7) 3.10 (7) 2.86 (7) 0.94 3.06 (7) 2.71 (8) 1.77

4. People start resorting to unethical behaviour as acceptable behaviour as most others do it.

3.28 (4) 3.14 (6) 3.31 (4) 0.62 3.45 (2) 3.09 (4) 1.76

5. When people find the seniors indifferent to ethical lapses.

3.46 (2) 3.38 (2) 3.48 (1) 0.40 3.42 (3.5) 3.51 (1) 0.40

6. They sometimes think following codes strictly would not be in the best interest of company.

2.95 (6) 3.19 (5) 2.90 (6) 0.97 2.91 (8) 3.00 (5) 0.42

7. People think that they can get away with non-compliance easily.

3.36 (3) 3.29 (4) 3.38 (3) 0.36 3.42 (3.5) 3.31 (3) 0.53

8. People are ignorant about the existence of the code of conduct.

2.87 (8) 3.00 (8) 2.85 (8) 0.54 3.09 (5) 2.63 (9) 2.20**

9. People find it more convenient to ignore codes. 2.71 (9) 2.52 (9) 2.75 (9) 0.80 2.59 (9) 2.85 (7) 1.21

Notes: 1. A 5-point Likert scale ranging from ‘1= strongly disagree’’ to ‘5 = strongly agree’ has been used for assessing respondents’ perceptions of role of code of ethics in influencing employees’ sensitivity to ethical issues, intentions and behaviour.

2. Rank numbers have been given on the basis of mean scores. 3. For the purposes of analysis, while a score ranging from 2.75 to 3.25 has been considered as reflecting respondents’ ‘indifferent attitude’ towards the scale item in

question; a score above 3.25 has been construed as reflecting respondents’ ‘agreement’ with the scale items in question. A score below 2.75 is, on the other hand, is treated as indicative of respondents’ ‘disagreement’ with the statement.

4. ** indicates that the difference is significant at 0.05 level.

Since code of conduct can play an important role in building ethical organizations, it is suggested

that more and more firms should be persuaded to go in for setting up their own codes of conduct.

Government support and directions can be of great help. If required, trade and industry

associations and regulatory bodies can make it mandatory for the firms (especially for those from

medium and large scale sectors) to establish their codes of conduct.

As per the perceptions of the surveyed respondents, code of ethics is only a marginally important

source of learning. Respondents view other sources such as observing behaviour of supervisors,

meetings with direct supervisors regarding ethical issues, ethics related training programmes and

guidance from seniors as more important sources of ethical learning than code of ethics. Across

the firm analyses reveal significant differences, with respondents from firms with code, large

corporate houses and foreign firms reporting much higher perceived importance than their

counter parts from firms without codes, small firms and foreign enterprises. Barring the case of

foreign firms, the surveyed executives only marginally of the view that codes of ethics serve as a

source of ethical learning.

Even in respect of influence of code on employees, respondents in general do not appear much

optimistic. They only marginally consider code of ethics to be helpful in improving employees’

sensitivity to ethical issues and fostering ethical intentions and behaviour in them. A cross-

sectional analysis of the responses, however, presents a different picture. Respondents from the

firms with codes, larger business organizations and foreign companies are in general found to be

holding significantly more positive opinion about the role of the code of conduct than the

respondents from organizations without codes, smaller firms and firms of Indian origin.

It seems that poor perceptions about the role of code of ethics as a source of learning and

influencer of employees’ intentions and behaviour have arisen due to lack of proper

communication and implementation of the codes in organizations in India. Even the

respondents’ in the present survey seems to be holding similar opinion. This is evident from their

agreement with the assertion that code of ethics can be helpful provided adequate support is

available from the top management in its implementation.

As regards code compliance, the surveyed executive report ‘personal values’ as the most

important reason for the compliance of code, followed by ‘expectation of reward’ and ‘loyalty to

organisation’. ‘Fear of losing job’ also turns out to be one of the factors. In respect of non-

23

compliance, ‘greed’, ‘seniors’ indifferent attitudes to ethical lapses’, ‘feeling of getting away

with non-compliance’ and ‘unhappiness with job/organization’ have been reported as the main

reasons responsible for non-observance of codes. An absence of significant differences in the

mean importance scores of these factors across different types of firm points to pervasive nature

of these reasons among the business firms in India.

The most obvious implication of the study findings in respect of this aspect as well as the one

examined in the preceding section is that the management need to be cognizant of these reasons

which hold true with all the types of organizations and make use of this information for

developing strategies for more effective implementation of codes in their organizations. Since

‘personal values has been reported as the most important determinant of code compliance, it is

imperative for the management of the companies in India to take steps to inculcate personal

values among the employees. Frequent holding of workshops and training programmes and

convening meetings with the employees can go a long way in injecting values of integrity and

honesty among the employees, thus ensuring more effective compliance of codes in future.

The finding in respect of expectation of reward points to the need for introducing a system of

employees’ ethical performance appraisal so that the ethically well performing employees get

suitably recognized and rewarded. Since fear of losing job also surfaces as one of the reasons

responsible for code compliance, a warning to the employees in clear terms that strict actions

(including a threat of termination from the job) will follow in case the employees fail to adhere

repeatedly to code of ethics. Setting up of ethical committees in the organizations for providing

guidance and advice to employees in matters of ethics and establishment of a system mechanism

to monitor code compliance can also help in allaying impressions from the minds of employees

that no one in the organisation is watching their behaviours and they can easily get away with

ethical lapses.

Organsiation loyalty and observance of behaviour of seniors have also been reported as the

reasons for code implementation. It will be in the fitness of the things that the management as a

long term measure strives for building a healthy organizational climate so that the employees

become more loyal to the organizations and thus start more zealously complying with codes. It is

equally imperative that the top management itself commits to adhere to codes of conduct and set

precedents for others to observe and follow their behaviour in respect of code compliance.

24

A few caveats about the limitations of the study are in order. The study is based on a relatively

small sample of firms located in and around Delhi. Non-probabilistic method used for selecting

the respondents is another limitation. The future studies making use of larger and nationally

more representative samples selected on the basis of stratified sampling method need to be

undertaken in future to arrive at more reliable and valid inferences.

Only incidence rather than contents, scope and designing of the codes has been examined in the

study. Domain, contents and drafting of the codes are equally important aspects (e.g., Batten et

al., 2008; Cressey and Moore, 1983; Carasco and Singh, 2003; Edmonson, 1990; Langlois and

Schlegelmilch, 1988, Murphy, 1995; White and Montagomery, 1980) and need to be investigated

in future studies for developing a complete knowledge base about the use and appropriateness of

code of ethics in the Indian context.

Code of conduct constitutes only one of the elements of the ethical management system. Unless

codes are properly communicated to both the internal and external stakeholders, supported by top

management commitment, and backed by training programmes in ethics and other elements of

ethical management system (such as appraisal of employees ethical performance, ethical

surveillance and monitoring committees, ethical audit, ethics guidance, compliance procedures

and counseling committees); codes of conduct on their own can do little in instilling ethical

beliefs and behaviours in the employees (e.g., Chakraborty, 2003; Elankumaran, 2006Laczniak

and Murphy, 1993; Murphy, 1995; Molander, 1987; Sethi, 2003; Svensson et al., 2009). Future

studies should take into account these other factors to arrive at a better picture about the role of

codes of conduct in building ethically sound organizations.

Last but not the least, use of experimental designs or vignette approach can be helpful in arriving

at more meaningful and valid inferences about the effect of code of conduct on the ethical beliefs

and behaviours in the organizations.

RERERENCES Adam, A. M. and D. R. Moore (2004), “The Methods Used to Implement an Ethical Code of Conduct and Employee

Attitude”, Journal of Business Ethics, 54, 225–244.

Asgary, N. and M. C. Mitschow (2002), “Toward a Model for International Business Ethics”, Journal of Business Ethics, 36, 239-246.

25

Ashkanasy, M. N., S. Falkus and V. J. Callan (2000), “Predictors of Ethical Code Use and Ethical Tolerance in the Public Sector”, Journal of Business Ethics, 25, 237-253.

Batten, J. A., R. S. Hettihewa and R. Mellor (2008),”Ethical Management Practices in Australia”, Global Business Review, 9(1), 1 -18.

Baumhart, R. (1961), ‘Problems in Review: How Ethical are Businessmen?”, Harvard Business Review, 39 (July-August), 6-9.

Bowie, N. E (1979), 'Business Codes of Ethics: Window Dressing or Legitimate Alternative to Government Regulation?”, in Beauchamp, T. L. and N. E. Bowie (eds.), Ethical Theory and Business, Englewood Cliffs, NJ: Prentice-Hall, Inc.

Brooks, L. J. (1989), “Corporate Code of Ethics”, Journal of Business Ethics, 8, 117.

Carasco, E.F. and J.B. Singh (2003), “The Content and Focus of the Codes of Ethics of the World’s Largest Trans-national Corporations”, Business and Society Review, 108 (1), 71–94.

Carroll, S. J. and M. J. Gannon (1997), Ethical Dimensions of International Management, New Delhi: Sage Publications.

Chakraborty, S.K. (2003), Against the Tide: The Philosophical Foundations of Modern Management, New Delhi: Oxford University Press.

Collins, P. J. and J. I. Porras (1997), Built to last-Successful Habits of Visionary Companies, San Francisco: Harper Business.

Cressey, D.R. and C.A. Moore (1983),”‘Managerial Values and Corporate Codes of Ethics”, California Manage-ment Review, 25 (1), 53–77.

Edmonson, W.F. (1990), A Code of Ethics: Do Corporate Executives and Employees Need It, Fulton, MS: Itawamba Community College Press.

Elankumaran, S. (2006), “Corporate Codes of Conduct in India: A Survey”, Journal of Human Values, 12 (1), 65-80.

Jain, S. K. and A. Mahajan (2010), “Marketing Ethics: An Investigation of the Ethicality of Beliefs and Behaviours of Managers in India”, Bhutan Journal of Business and Management, 1(1), forthcoming.

Jackson, J. (1996), An Introduction to Business Ethics, 1st ed., Blackwell Publishers.

Laczniak, G.R. and P.E. Murphy (1993), Ethical Marketing Decisions: The Higher Road, Boston: Allyn & Bacon.

Langlois, C.C. and B.B. Schlegelmilch (1998), “Do Corporate Codes of Ethics Reflect National Character? Evidence from Europe and the United States”, in B.B. Schlegelmilch, ed., Marketing Ethics: An International Perspective, pp. 356–74, London: International Thomson Business Press.

Molander, E. A. (1987), “A Paradigm for Design, Promulgation and Enforcement of Ethical Codes”, Journal of Business Ethics, 6, 619-631.

Murphy, P.E. (1995), “Corporate Ethics Statements: Current Status and Future Prospects”, Journal of Business Ethics, 14 (9), 727–40.

Murphy, P. E. (2002), “Marketing Ethics at the Millennium: Reviews, Reflections and Recommendations”, www. Patrick E. Murphy. 72 @ nd. edu.

Rallapalli, C. K. (1999), “A Paradigm for Development and Promulgation of a Global Code of Marketing Ethics”, Journal of Business Ethics, 18, 125-137.

Schlegelmilch, B. B. and J. E. Houston (1989), “Corporate Codes of Ethics in Large UK Companies: An Empirical Investigation of Use, Content and Attitudes”, European Journal of Marketing, 23, 7-23.

Schlegelmilch, B. B. and C. C. Langlois (1990), “Do Corporate Codes of Ethics in Large Reflect National Character? Evidence from Europe and United States”, Journal of International Business Studies, 519-539 as quoted in Schwartz 2001.

26

Schwartz, M. S. (2001), “The Nature of the Relationship between Corporate Codes of Ethics and Behaviour”, Journal of Business Ethics, 32, 247-262.

Schwartz, M. S. (2002) “A Code of Ethics for Corporate Code of Ethics”, Journal of Business Ethics, 41, 21-43.

Sethi, S. P. (2003), Setting Global Standards: Guidelines for Creating Codes of Conduct in Multinational Cor-porations, New Jersey: John Wiley.

Skubik, D. D. and Stenning, B. W. (2009), “What‘s in a Credo? A Critique of the Academy of Management’s Code of Ethical Conduct and Code of Ethics”, Journal of Business Ethics, 85, 515-523.

Stark, A. (1993), “What’s the Matter with Business ethics?”, Harvard Business Review, 38-46.

Stevens, B. (1999), “Communicating Ethical Values: A Study of Employee Perceptions”, Journal of Business Ethics, 20, 113-120.

Svensson, G., Wood, G., Singh, J., and Callaghan, M. (2009), “A Cross-cultural Construct of the Ethos of the Corporate Codes of Ethics: Australia, Canada and Sweden”, Business: Ethics: A European Review, 18 (3), 253-267.

Watson, S. and G.R. Weaver (2003), “How Internationalization Affects Corporate Ethics: Formal Structures and Informal Management Behavior”, Journal of International Management, 9(1), 75–93.

White, B.J. and B.R. Montgomery (1980), “Corporate Codes of Conduct’, California Management Review, 23 (2), 80–87.

Weller, S. (1988), “The Effectiveness of Corporate codes of Ethics”, Journal of Business Ethics, 7, 389-395.

Wotruba, T. R., B. Chonko and T. W. Loe (2001), “The Impact of Ethics Code Familiarity on Manager Behaviour”, Journal of Business Ethics, 33 (September), 59-69.