Embed Size (px)

Citation preview

JagoInvestor Book review - TheWealthWisherPosted by TheWealthWisher on Feb 25, 2012 in Product Reviews | 20 commentsbook reviews

28

Share

I have had the pleasure of reading theJagoInvestor book that has been out in the market for a month now. Written by Manish Chauhan, a personal fellow blogger and a friend, I could not help writing a review on the book.I remember when I was in my teens, I used to finish the Alistair MacLeans and James Hadley Chases in one sitting of a couple of hours. Though I have grown old and juggle multiple things in a day, the book was so captivating that I knocked it off in two sittings. So you know what is coming next ?

JagoInvestor Book, chapter by chapterLike me, Manish comes from an IT background and left his full time job to change people’s relationship with money. The book is an attempt at that.The subject of the book is basic personal finance and principles of financial planning. In that sense, it is a must read for every new beginner. I recommend that experts on personal finance also grab this book, here is why.Chapter 1, “Burning the Jungle” is an absolute stunner. One could never have imagined how the power of compounding can be looked at in different ways. Manish presents various inferences that will give a whole new perspective to things you already knew but never stretched your imagination further to explore. Therein lies the difference between the author and others.Chapter 2, “Have you protected your garden” is all about insurance. The questionnaire that Manish uses while coaching his clients is very interesting and I am sure, enough to drive home the point to investors who don’t have enough life insurance and think they don’t need it. A ready reckoner of how much insurance one needs at 6%, 8% and 10% inflation and various returns is helpful as well.Chapter 3, “Get, set, goal” is all about goal based investing. Manish has used different terminologies for must-have and good-to-have goals – committed goals, interested goals, outcome goals and process goals. Impressive, I must admit. You also clarify here what SMART goals are – Specific, Measurable, Attainable, Relevant, Time-Based.Chapter 4,”Busting your myths about money” is to drive home the point that equity is not risky in the long term but is in the short term while debt is safe in the short term and thatreturns from stocks can get you the riches you desire but only in the long term. Manish uses some interesting Sensex data to prove this point – this is where you will spend ample time trying to understand the analysis. Worth the time.Chapter 4 also talks about asset allocation and rebalancing.Chapter 5, “Change your relationship with money” is all about your attitude towards money and how your own money behavior can get things going for you. Manish says that you are a movie star in your life’s financial film and only you can make it 9 stars out of 10.Chapter 6, “Simplifying your financial life” is one of the most practical chapters with to do things that everyone will find useful. Manish shows how documents can be managed using technology and automation. Watch the 6 commitments at the end of the chapter.Chapter 7, “10 things to do to make your financial life awesome” is essentially a laundry list of things you need to do right in your financial life. Each one of those 10 things is essential to understand and implement.

Should you buy the JagoInvestor Book ?Firstly, Manish’s style of writing is simplicity. That helps everyone understand each chapter easily. While it is simple, the writing style is rich.Secondly, every chapter is followed up with an action plan, which in my mind if you follow, you would have already begun on the journey of financial freedom.Thirdly, needless to say, the book is studded with stories and quantitative examples that make your reading and understanding both enjoyable. In a very subtle way, Manish starts with a story, moves to examples and drives home the point. The flow is so easy going that you get the point the author is intending to make.So for every investor who wants to start learning about personal finance, JagoInvestor book is a must. This book will lay the foundation of strong financial habits as soon as you read it (which we inculcate very late in life) – read it now to take advantage of early investing.The book also has nice graphics at appropriate places to help the readers understand the topic being discussed.At Rs 374, you are getting a kick start to your financial life – why miss the JagoInvestor book ? In case you need a free copy, try this.For some folks who were pointing out in social media that there are mistakes in calculations, well, why not appreciate a mammoth attempt by a youngster to write a book instead of trying to find faults.Well written Manish, my best wishes with you always. Keep up the good work !PS : I am not an affiliate for the JagoInvestor book. I don’t get anything if you buy ! It’s you who gets a new life !

36 Personal Finance Resources to make you a smart investor - TheWealthWisherPosted by TheWealthWisher on Jan 30, 2012 in Investing | 38 commentsinvesting tips

12

Share

If you are scouring for personal finance resources or guides to learn about financial planning in India, go no further. We bring to you the complete list that will make you walk and eventually run ! Personally, the personal finance landscape is changing so fast in India that I am amazed at what one wants to keep his or her eyes on.But that’s the fun in life – keep catching up or be abreast of the latest happenings and that is how you can learn. So let me jump straight away into the complete list. Note that I had done the The Ultimate Listing of Personal Finance Learning Sites last year but a lot of them have not become defunct so the below will help everyone.

If you think there are some gems out there which I have missed, please add it to the comments section and I will update the article.

Best Personal Finance Resources – Magazines1. Outlook Money - If you haven’t subscribed to this yet, you are missing participating in the treasure hunt which scores of other readers have already joined. While the fortnightly issue is here, the digital weekly version has enough to keep you busy for an hour over the weekend. Now you know where my Sunday goes ! At a 1 year subscription of Rs 599, 2 years at Rs 999 and 3 years at Rs 1399, it would be a shame not to have this in your kitty.2. Economic Times Wealth - Just a year old into circulation, Economic Times Wealth is, in my opinion, giving a tough competition to Outlook Money. I like the presentation and articles that come out each Monday. If you are missing on the hard copy, read all articles online.3. Money Today - Once a monthly bundle of absolute joy is what I call Money Today. The 1 year subscription is for Rs 500 and 3 year is for Rs 1500. Not to be missed.4. Money Life - This personal finance resource is different in the sense that it takes most of the awareness issues for the investors head on with regulators. “Know Whats Coming” is it’s tag line. Is it yours as well ?

Best Online Personal Finance Resources – Articles5. Business Today Money - Basic and advanced articles from Business Today house. Top notch.6. Rediff Business Personal Finance - A plethora of articles from Rediff. Go check the archives as well.7. Rediff GetAhead Personal Finance - Basic and advanced articles for beginners. Don’t miss the archives.8. Yahoo Finance - Coming from the Yahoo stable (never mind their top management reshuffle every now and then), this is top class.9. Economic Times Personal Finance - The Economic Times is probably one of the best dailies on economy and personal finance. Breaking news are a differentiating feature.10. Indian Express Money - Articles here are both basic and advanced.11. LiveMint Money - The personal finance and economy authored editorials are very very good.12. Money Life Personal Finance - As good as the magazine at point no 4 above.

Miscellaneous Personal Finance Resources13. ValueResearchOnline - The one and only place where you can do everything on mutual funds.14. MoneyControl - A portal with everything an investor would want to check out – heavy on the stock market.15. BankBazaar - The all loan junction. Check out the blog articles as well.16. MyInsuranceClub – One stop shop for insurance news, articles, videos and product reviews.

Blogs from India17. JagoInvestor - Read how Manish Chauhan is changing your relationship with money.18. RaagVamdatt - Lying low of late, still a store house of power packed articles.19. TFL Guide - Hemant Beniwal writes about financial planning, product reviews and much more.20. PersonalFinance201 - Ranjam Verma blogs about basic and advanced personal finance topics.21. OneMint - Manshu writes about personal finance and the economy as a whole.22.CapitalMind - Deepak Shenoy talks about money, markets and trading.23. PPFAS Blog - When somethings belong to Parag Parikh, wake up and take stock !24. InvestmentYogi - Nice practical guides on investing in India.25. Subramoney.com – PV Subramanyam’s must follow blog on personal finance.

Blogs from around the world26. Moolanomy - Very nice generic articles about income, expense and debt management.27. Mint Blog - Though a lot of articles might not be related to Indian investing, the others are chic and awesome.28. MotleyFool - I like the 60 second guides here.29. TheDigeratiLife - One of my favorites for a very long time now.30. GetRichSlowly - Meticulous and very detailed articles about investing in the US.31. I Will Teach You to be Rich - Ramit Sethi teaches you how to be rich.32. The Smarter Wallet – Money tips to help you live smarter.

Personal Finance TV programmes33. The Financial Planner on Bloomberg UTV- A show that helps you to understand about various aspects of equity markets, mutual funds and other investment categories.34. Smart Money on Bloomberg UTV - A show that tells you how to make your money work for you.35. Talk Funds on Bloomberg UTV - A mutual fund show.36. Your Money on CNBC Awaaz - This show discusses insurance, stocks, mutual funds with queries from investors.Your turn now dear readers, did I miss any personal finance resources ?

Sir John Templeton’s 16 rules for investment success - TheWealthWisherPosted by TheWealthWisher on Jan 20, 2012 in Investing | 22 commentsinvesting tips

5

Share

I stumbled upon this document which talks about Sir John Templeton’s 16 rules for investment success. It was such a basic and nice reading that I was prompted to write down this article with my tits and bits thrown in. Sir John Templeton was an investor andmutual fund pioneer who became a billionaire by pioneering the use of globally diversifiedmutual funds .Templeton started his Wall Street career in 1937 and went on to create some of the world’s largest and most successful international investment funds. Called by Money magazine “arguably the greatest global stock picker of the century” (January 1999), he sold the Templeton Funds in 1992 to the Franklin Group for $440 million.Here is his wisdom. While his rules were more relevant to the stock market, my commentary is more generic.

1. Invest for maximum total returnWhat Sir John means by this statement is that one needs to look at the REAL return on his investments.For example, if you park your money in a FD which is promising 9% rate of return, then 9% is not the actual returns you made on it as inflation reduces your purchasing power. While most of the readers are aware of what inflation means, there is taxes as well that eat into your returns.So before you jump with joy at the inference of having made 9% on your FD, remember that taxes and inflation need to be taken into account.There is only one place to invest to tackle the rising inflation and that’s the stock market.

2. Invest – do not trade or speculateThis is so basic. So so basic. I keep saying from my articles – the average investor who believes in long term investing will make same or more money than the one who is actively looking at the ticker, has his heart in his mouth and makes less money trading many times and loses all of it at one go.Keep in mind the wise words of Lucien Hooper, a Wall Street legend:“What always impresses me,” he wrote,“is how much better the relaxed, long-term owners of stock do with their portfolios than the traders do with their switching of inventory. The relaxed investor is usually better informed and more understanding of essential values; he is more patient and less emotional; he pays smaller capital gains taxes; he does not incur unnecessary brokerage commissions; and he avoids behaving like Cassius by ‘thinking too much.’”

3. Remain flexible and open minded about investment typesThis is a nice one as well. Sir John means to say that at some point of the year, there will be aninvestment avenues that will become very famous among investors. However, as Change is the only constant, it will consistently never be famous.

Sir John Templeton

At some point of time, investors will take fancy to some other avenue.For example, right now, investors are lapping up long term debt funds as the interest rate cycle is going to reverse.While sometimes stocks will catch one’s fancy, at other times they wont (2011, anyone?). So one needs to remain flexible and move among different asset classes.

4. Buy Low

This is a master stroke. It is so simple in understanding but hardly anyone ever executes it.For a moment pause here and ask yourself whether in 2011 you were buying the blue chip stocks when the entire Indian stock market was on sale. Not many will say yes.Advice will be given out and investors will read it but never execute. The reason is simple – fear of making losses when things are going down over powers your basic reasoning of buying when everyone is running away.As Benjamin Graham put it – “Buy when most people…including experts…are pessimistic, and sell when they are actively optimistic.”

5. When buying stocks, search for bargains among quality stocksSelf explanatory!

6. Buy value, not market trends or the economic outlookIf you belong to the section of people who look at how up Sensex or the Nifty is headed and then buy (say) Infosys, then this is for you. One needs to buy Infosys because the company is good and rich in valuation. You cannot buy it because the overall market is going up.The inference here is that the stock market is driven by the individual stocks that are its constituents. Stocks drive the stock market, the stock market does not drive the stocks!

7. DiversifyThis and the next point are self explanatory.

8. Do your homework or hire experts9. Monitor your investments aggressivelyActive management of your portfolio is any day better than passive management. Be it stocks, mutual funds, fixed income instruments or even cash – the products do not stay awesome for the rest of their lives.You need to get rid of stocks every quarter should their performance go down and mutual funds needs to match up to their benchmarks and peers otherwise they need to be weeded out.All products need monitoring – the more you do the better but this cannot come at the risk of impacting your daily work.

10. Don’t panicThere are times when each one of us has made mistakes with our investments. To err is human so we will make mistakes even in the future.But the point is when the mistake happens, do not panic.So if you did not sell your stocks in the end of 2010 before the stock market nose dived in 2011, why did you sell all of it in 2011 when the stock market was already down? This meant losses for you.Tie this back to the point earlier on Buy Low and you will realize that this rule of “Don’t panic” would have helped you immensely to lie low in 2011 and you would have probably invested more in equity for the long term.In 2011, we all should have stayed calm and invested in equity more.

11. Learn from your mistakesSir John says that the biggest difference between people who are successful and those who are not is that the former have learnt from their mistakes.It does not make sense to fret about mistakes and brood on them, does it ? Many people stop investing in mutual funds or stocks after having burnt their fingers. The mistake they made was to invest in the wrong way (buying too high; going with IPOs; investing in NFOs; investing one time and forgetting to name a few).Once they burnt their fingers, some investors stopped investing completely. Now that is the biggest mistake, says Sir John.

12. Begin with a PrayerA prayer will give you more confidence in anything that you do – simple and lucid.

13. Outperforming the market is difficultSir John says “The challenge is not simply making better investment decisions than the average investor. The real challenge is making investment decisions that are better than those of the professionals who manage the big institutions.”Now that is difficult. As an investor, are you happy with the returns that the market is offering or do you want more?If it’s the former, investing in index funds will satisfy you, if it’s the latter, then professionally managed diversified equity funds might be your answer. Of course, there is no guarantee that the latter is necessarily going to return you more than the market.

14. An investor who has all the answers does not even understand all the questionsRemember the gurus of the stock markets who come on TV and predict where the market will go ? Well they are seldom right.The biggest challenge with investing is that an investor might master himself on all existing principles, rules, tips and tricks, best practices and be ready to invest. However, he can never master how he will react to the changing economic and investment situation around him.That is a learning process he will go through all his life – everyone does!

So be wary of people who say they know everything.

15. There is no free lunch everIn India’s context, your dad’s good friend sells you LIC policies not because it’s the best product for you but because he earns commissions; the IPOs that are launched promise you a killing on the day of listing but not everyone who invested can keep making that mad money; life insurance agents make financial plans for you with the only investment products as policies that they can sell.There is no free lunch and everyone has a motive in mind. Be wary.

16. Do not be fearful or negative too oftenWe will have our own fair share of scams and market crashes but remember that over a long period of time, the economy of our country is still good. We might be behind China but we are way ahead of others.Our politicians might be pocketing the taxes we pay but some went behind bars to set a precedent in this country which should improve things.Hang in there for a long term and all of us are sure to be rewarded. Be positive.Thoughts, readers ?

Opening a 2nd bank account gets easier -TheWealthWisherPosted by TheWealthWisher on Jan 5, 2012 in Personal Finance News | 20 commentsbanking news

0

Share

The Know Your Customer (KYC) guidelines for opening a new bank account when you move to a new city (or otherwise) is now made simpler.The Indian banks have decided that if an individual already has a bank account with any bank, then they will use that as a proof of residence for opening a new account for the same individual, in the same city or in any other city. The person will need to provide a bank statement as a proof for the same.It must be noted that the individual still needs to provide an identity proof for opening the new bank account.This is welcome news for everyone as, of late the Reserve Bank of India had conveyed its displeasure to banks saying that customers were complaining that when individuals moved to new cities and wanted to open new accounts, the proof of residence was becoming a bottleneck for them and causing a lot of grievance. So they were filling up lengthy forms once again to open their accounts.Now that the banks will talk to each other to establish a person’s residence proof for a new bank account, a lot of complaints coming to RBI will be taken care of.Our observation is that though it is very important to establish a person’s identity and follow stringent KYC norms, it cannot happen at the cost of the customer’s discomfort. It is the banks and RBI’s responsibility to not open undesirable accounts, but as the above path breaking ruling indicates, there are solutions out there that can be intelligently tapped into.

5 personal financial milestones before 30 -TheWealthWisherPosted by TheWealthWisher on Dec 1, 2011 in Investing | 37 commentsinvestment musings

10

Share

In India, generally a person starts earning between the ages of 22-24 depending on what kind of education he is after in college. So that gives the person 8-10 years before he hits the age 30. What do you think one should achieve in life by the age of 30 ? No, I am not taking about those naughty random thoughts that are crossing your mind now, my subject here has to do with personal financial milestones only.Here is a list I would consider as my financial milestones before 30.

Open a DEMAT accountThe power of compounding works best when you start early. And it works best for long term investing. Long term investing is all about putting your money in the those investment avenues which will earn you the most with the least possible risk.Over a large period of time, equity investments have returned the most. So open a DEMAT account as soon as possible and start investing money. Now be aware of the fact that this is possibly the time when most people get carried away with direct stock investing. Dabbing your hands in the stock markets is not a bad thing but if you end up being a day trader, God bless you.And if you don’t care about this blessing for a moment, then put aside some money which you are ready to lose in the stock markets and invest the rest in equity via systematic investment planning of mutual funds. If like a spoilt child you still want to go for direct stocks, try SIP in stocks for higher returns.I consider this a very important financial milestones before 30.

Save enough for a rainy dayStarting with your first pay check, save a little amount of money each month that can be used in case of emergencies. In personal finance parlance, that is called an emergency fund.When you start your career, your earnings are a pittance so trying to form this fund might be a bit challenging because you need to save little by little over a period of some months. But that is exactly what teaches you to be patient and inculcates the habit of saving your money systematically.Many young professionals are generally in probation for a year of service when they start their career. If at this time, the economy forces a job loss, your emergency fund can come handy then. This is perhaps the most important financial milestones before 30 or for that matter any age !

Don’t sign up for credit cardsAfter college, this is probably the first time you get paid for working. Once you realize the power of a fat wallet on the 30th of each month, it’s easy to get carried away to spend it on things you always wanted to. While spending is fine and it is important to differentiate between needs and wants, don’t do the spends via credit cards.Be aware of what credit card debts can lead you to. Use debit cards and cash to the best of your abilities but keep the credit card companies far far away. So your financial milestones before 30 here is not to have credit cards !Honestly, credit cards are not bad but I would advise one to look at them after 30.

Build a budget sheet for yourselfThis might not sound like a milestone but the fact that no one does it makes it a target to be achieved. No one wants to be burdened by the boring task of estimating how much one would spend on groceries, entertainment and other lifestyle expenses.But if you don’t plan now, you might falter later. The best habits in life are started early and it’s never too late.So if you do create a budget for yourself, pat yourself on your back because you are among those few people who will know how much more you are spending against the baseline you have set for yourself. Most people fail here so keep pushing yourself till you get down to doing it.

Chalk out your targetsSimply put, document your financial goals which you want to achieve by 30. If you think for a moment, by 30 you will definitely want to get married and then probably buy yourself a house.Marriage costs are not cheap these days and the 20% down-payment for an apartment is not a small amount either. So run through the exercise of knowing how much money you need to aim for and how much money you need to invest each month to get to these goals. Don’t forget the inflation monster when you strategize this goal based investing.If you invest smartly, you might end up buying an apartment of your choice with your local earnings. There are many lucky individuals who make international trips, earn quick bucks and invest in property. Even if you don’t belong to this lucky group, you can still achieve your goals with smart investing.And as far as marriage is concerned, it will happen and you will go broke !

How do I know that my financial planner is certified ? - TheWealthWisherPosted by TheWealthWisher on Nov 27, 2011 in Financial Planning | 10 commentsfinancial planner

3

Share

This might look a very odd topic to write on but I picked up the subject of writing aboutcertified financial planners in India after some personal experiences and those of my peers as well. The need of financial planning is a very vast one and many investors still do not know the difference between investment advisors, insurance agents, relationship managers and financial planners. Obviously, not all of them can meet your needs of comprehensive financial planning.I personally think that when investors ask for a financial planner, they ought to ask for a certified one. But do investors know what that means, what to ask for and why and how to check for the certification ?

The CERTIFIED FINANCIAL PLANNERCM India tagWell, first things first, around 75% of my clients have never asked whether I am certified or not. The few that have, have no clue what and where this certification is from and what it means. The same is the observation of my peer financial planners as well.So the question I ask is, if that is the case, do I need to be certified to be thriving in this business ? The answer is actually no. You do not need to be certified to do good business as there are very few people asking for it. So why be certified in the first place ?That is where the importance of the CERTIFIED FINANCIAL PLANNERCM tag comes in.The CERTIFIED FINANCIAL PLANNERCM certification is a mark of excellence granted to individuals who meet stringent standards of education, examination, experience and ethics. It is the most prestigious and internationally accepted Financial Planning qualification recognized and respected by the global financial community.In India, FPSB India (Financial Planning Standards Board India) is the principal licensing body that awards CFPCM Certification in India. No other body is authorized to award this certification. There is also no other certification that can meet the purpose that certified financial planners in India cater to – that of making a holistic and comprehensive financial plan for an investor.Another thing to note is that FPSB India authorizes financial planners to use the certification tag for only a year. The renewal is based on continuous education where the financial planner is expected to keep upto speed in the financial planning domain by undertaking activities like submission of articles, speaking assignments, attending seminars and events, undertaking quizzes, attaining certifications & qualifications and many more.There are many financial planners in India who were certified once upon a time but have not renewed their certification with FPSB India, so they cannot use the CERTIFIED FINANCIAL PLANNERCM tag anymore. I think that does not make them any less competent. They could be as good as any certified financial planner.But yes, you are in the best hands if you go with a planner who is currently a CERTIFIED FINANCIAL PLANNERCM .If you compare this for a moment with what insurance agents, relationship managers and investment advisors go through you will realize that Certified Financial Planners in India have the most rigorous curriculum right throughout their career. This is what makes them different and the best in the field to do financial planning.

How to verify whether your financial planner is certified ?Use the below steps to check whether your financial planner holds the CERTIFIED FINANCIAL PLANNERCM certification.1. Go to The FPSB India website – http://www.fpsbindia.org/2. Click on the “CFP Certificant” link on the main navigation bar.3. You can simply search for a certified financial planner in India by three categories presented to you.Search by Name/CompanySearch by City/StateSearch by Nature of Employment

4. It is always wise to make sure that you search for your financial planners name by using at least two categories of search before you decide to drop the poor chap. If you use the city based search, you can find all certified financial planners in that city.This is how the snapshot will look like for a typical search -

You can also ask for a Certification ID card that financial planners should carry for a quick proof of the fact that they are certified. It will bear their registration number, their name and validity till when they can use the CERTIFIED FINANCIAL PLANNERCM tag.So next time you go searching for a financial planner, make sure you check whether he is certified or not. It is like going to a doctor or a quack. You really need to differentiate between who will open your bowels, don’t you ?Has anyone done this before signing up for their planner ?

How to choose a good life insurance agent ? -TheWealthWisherPosted by TheWealthWisher on Oct 14, 2011 in Insurance | 1 commentbasics of life insurance

0

Share

Choosing a good life insurance agent is like buying onions and potatoes these days – they cause a hole in your pocket and more often than not, they are not upto the mark. If you want to get your dish right, you need to select your veggies carefully – similarly, if you want to get your financial planning right, you need to select the right life insuranceproduct among the different types of life insurance policies available.And only one person can help you do that. That is your life insurance agent.Most of us have been associated with life insurance agents or life insurance advisors through our parents who forced us to pick up an LIC policy because the advisor was their friend. We did not choose the life insurance agent ourselves then. But you can do so now.Use the below tick in the box approach to choose a good life insurance agent.

How does he sell you a policy ?Most agents glibly ask the investor how much premium they can afford and then offer a policy to match the premium. That is the worst way to sell an insurance product. Check whether your life advisor asks for your needs. If he puts forth questions like how much insurance you already have, how much do you need to spend on your children’s education and marriage or how much money do you need to retire, then he is going down the right path.The advisor needs to ensure that your goal based investing approach matches the maturity of the products so that your needs are taken care of.

Is he armed with tools and calculators ?Using thumb rules to find out how much life insurance you need is acceptable but he ought to devote sometime with his tools and calculators to do some number juggling to justify the numbers.Remember, if you end up taking a huge life insurance, you are paying more money in the form of premiums which could be put to better use and if you are taking less cover, then you could possibly be under insured.Make sure you get it right.

Does he make your products churn ?Good life advisors will not ask you to sell your current policies and take new ones. If this happens, be wary and ask questions.Insurance is not an investment avenue which you get in and get out of every alternate year.He must be appreciative or disapproving of the products you have and he should ideally suggest you check with your financial planner whether the products should be retained or moved out of your portfolio but he should not be pushing you to get out of them now so that he can sell his.If you have taken insurance clubbed with investments (non term plans), remember you need to stick around for a long time as these are long term products. Churning is bad.

Does he utter the word TERM PLAN ?Remember that life advisors earn commissions on the product they sell, so they will want you to buy the ones that fetch them the most money. And term plans just don’t do that. So life advisors seldom speak about it.They will want you to purchase Unit Linked Insurance Plans (ULIPs), endowment plans, money back plans or pension plans where the cut is comparatively larger.You have chosen a good life insurance agent if he sells you term plans or explains why you do not need them.

Other points to noteNeedless to say, a good life advisor is one who knows about the products in the industry and how they compare to each other. Your agent must know why the other products are not good to have and why his is the best – a simple answer that it belongs to the Reliance brand will not fly.Check whether he is involved with you while he fills in the application forms. If he is skipping critical details and ticking all the “No” and “N/A”s in the form, then he is probably a less informed individual who does not understand the significance of what incorrect data could lead to.A good advisor is one who checks how much cover you already have and how much you need more and then plans for it.Be extra careful of fly by night agents who vanish within a year or less. You will be left stranded trying to reach out to the new ones who will anyway be reluctant to serve you as they might be earning a pittance or nothing in continuing to serve you.Chose a good life insurance agent who can be your guide and friend at the same time.You will need to search a lot because most of the potatoes and onions are rotten and the ones that are good are few and far between.

7 stock investing secrets of Warren Buffett -TheWealthWisherPosted by TheWealthWisher on Apr 17, 2011 in Stocks | 2 commentsstock market tips

2

Share

Warren Buffett is acknowledged by investors around the world as the world’s best investor. There are certain guidelines he has adopted while investing in businesses and companies and he has been very generous to let these guidelines be known to the general public. It is a different story that though everyone knows his principles and methodologies, very few actually adopt and execute them. We look at 7 such secrets that Warren Buffet has implemented.

Secret #1: Invest in quality businesses, not stock symbolsMost of the small time investors and even educated ones for that matter, look at the historical performance of a stock to conclude how much money they can make. Sitting back and hoping for a northward movement of the stock you buy is designed to fail. The stock after all belongs to a company and if that company is sick, so is your investment.Warren Buffett refers to this as trying to play bridge without looking at the cards. Instead, Warren Buffet suggests investing in sound companies that will grow over a period of time and will be able to thwart off challenges from peer companies.Technical and fundamental analysis are a science and how to choose quality businesses to make money is still a hot favourite pastime for many today. Buy sound companies whose stock will grow healthily over a period of time, not just stock symbols.

Secret #2: Don’t invest for ten minutes if you’re not prepared to invest for ten years

Simply put, this amounts to long term investing. Warren Buffer says that the real value of a good company is unlocked over a extended period of time and not really over a short one. So he suggests investing in a company possibly for the entire life term.One could possibly end up buying a good company stock at a higher price in the short term but over a long period of time, the market will present many opportunities to buy that stock cheap.The exciting thing about long term investing is that you are bound to beat the fluctuating market. Don’t buy stocks to make a profit in the short term.

Secret #3: Scan thousands of stocks looking for screaming bargainsWarren Buffet is known to look into annual and quarterly reports of thousands and thousand of companies to find the real bargain. He doesn’t use a computer or a calculator they say and is able to remember details about companies that others don’t.His intent to look at so many stocks is not to find a company doing just average earnings, instead he looks for investments that are a steal by a huge margin.

Secret #4: Calculate how well management is using the money they haveWarren Buffet looks for companies with good returns on equity while employing little or no debt. This is measured by two ratios called return on equity and return on capital.The measurement of return on equity and capital is a direct indication of how the businesses are run by the management of the company.If you want your stocks to perform well, the company has to perform well as well and for that the management has to use equity and capital wisely. Keep track of money usage by the management of the firm.

Secret #5: Stay away from “glitter” stocksMore often than not, you will find stocks on the Sensex that will catch your fancy for having a high trading volume or a wild fluctuation in its price over a day or week or month.Studies have shown that most of the investors put their hard earned money is such stocks and lose more than they would had they put in normal stocks that were not grabbing the headlines.In Buffet’s words – “Most people get interested in stocks when everyone else is. The time to get interested is when no one else is. You can’t buy what is popular and do well.”Stay away from the headline making stocks.

Secret #6: Calculate how much money you will make, not whether the stock is undervalued or overvalued according to some academic modelThere are many models available to find out the actual worth of a stock and whether it is over valued or under valued. But remember that none of these can be relied upon. They can work sometimes and they will fail sometimes but they will not consistently succeed. Using any model does not guarantee that you will end up making money on the stock.It is because of these reasons that Warren Buffett focuses on expected return from the stock, not whether the company is undervalued or overvalued. He aims for a minimum 10%, anything above that is a bonus.

Secret #7: Remove the weeds and water the flowers — not the other way aroundMost of the investors will want to cash out when the market price of their stock goes a few notches higher than their purchase price. In case the stock price goes below their purchase price, they will want to hold on with the hope that the price will eventually go up.

Studies have shown that investors would be better off selling their losers and keeping their winners and not the other way around. This is what is referred to as “remove the weeds and water the flowers, not the other way around” . There are exceptions to this but the general idea can work wonders.Are you aware of any more stock investing tips that Warren Buffet uses ?

Cost inflation index table - TheWealthWisherPosted by TheWealthWisher on Apr 6, 2011 in Quick Reckoners | 2 commentsmisc

1

Share

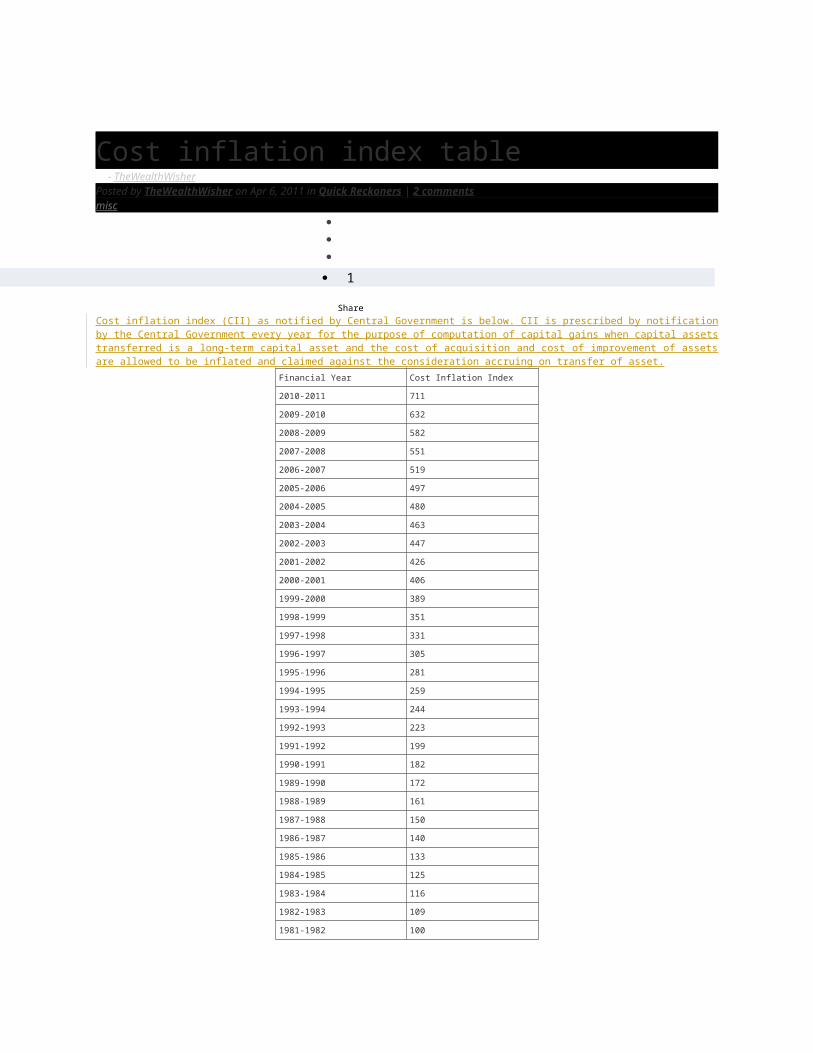

Cost inflation index (CII) as notified by Central Government is below. CII is prescribed by notification by the Central Government every year for the purpose of computation of capital gains when capital assets transferred is a long-term capital asset and the cost of acquisition and cost of improvement of assets are allowed to be inflated and claimed against the consideration accruing on transfer of asset.

Financial Year Cost Inflation Index

2010-2011 711

2009-2010 632

2008-2009 582

2007-2008 551

2006-2007 519

2005-2006 497

2004-2005 480

2003-2004 463

2002-2003 447

2001-2002 426

2000-2001 406

1999-2000 389

1998-1999 351

1997-1998 331

1996-1997 305

1995-1996 281

1994-1995 259

1993-1994 244

1992-1993 223

1991-1992 199

1990-1991 182

1989-1990 172

1988-1989 161

1987-1988 150

1986-1987 140

1985-1986 133

1984-1985 125

1983-1984 116

1982-1983 109

1981-1982 100

4 ways to diversify your investment portfolio -TheWealthWisher

Posted by TheWealthWisher on Apr 10, 2011 in Investing | 0 commentsinvesting tips

0

Share

Your investment portfolio is your base to a future of healthy financial planning. If you go wrong with your investments, you will need time and acumen to bring yourself back to a healthy state of finances. One of the key ingredients towards a healthy portfolio is diversification. Let us take a peek on how you can use diversification for your investment portfolio.

What is diversification ?Diversification is defined as spreading of your investments across different parameters to reduce risk. These parameters could endanger your portfolio and reduce its return – your proactive measures to reduce its impact is defined as diversification.Diversification is not a solution to all investment portfolio woes. It is a mechanism by which the impact of the risk is reduced, if not eliminated. So if the risk were to materialize, then diversification would ensure that part of your portfolio is impacted by the risk while part of it is not. This balances your portfolio.

4 methods to achieve diversification1. Do not put all your eggs in one basketThe line itself is self explanatory. You should not invest all hard earned money in just one investment class. There are so many investment avenues available. Your money should be spread across all.So you should dab your hands with equity, debt, real estate or gold. However, you cannot have all your money into just one investment class, say equity. If the equity markets were to tank, yourpersonal net worth would get eroded since all your money was in equity.When one asset class under performs, others in the portfolio will over perform. This ensures that decrease in value in one asset class does not decrease your portfolio value to a great degree as the other asset classes have over performed.Spreading your monies across different asset classes ensures that non performance of one asset class does not hurt the overall return of the portfolio and achieves diversification.

2. Spread your investment across different timezones to ensure diversificationIf you follow goal based investing, then this will come as a result automatically. Your short term goals will mature within 2-3 years while long term goals will ensure that you keep investing for the long term.

However, for all your short term or long term goals, keep the maturity proceeds over different time periods. This ensures that your investments are spread across large time periods and do not suffer from adverse impacts which happen on and off.Also note that you should not have a lump-sum of maturity money come to you once in the year when you require the money. Stagger that maturity across different months of the year when money is needed.This ensures that you can take care of adverse impacts if it were to happen in some months of the year.Supposed you needed Rs 5 lakhs 3 years from now. If your maturity of 5 lakhs is going to come via a close ended fund or tax saving mutual fund and that mutual fund tanks in the final year when you need the money (third year), then you have little choice. But if you were to spread this across different mutual funds, some debt and some equity, which mature in different months 3 years from now, then adverse impact to one mutual fund would not impact the others. Your diversification is better off here.

3. Buy across different fund houses for better diversificationEach year, you should sit down and calculate how much percentage of your portfolio money is parked with a particular mutual fund house. Over exposure to a single one could be dangerous.One tends to invest with a particular fund house either because their processes are good; or because they have a star fund manager aboard or because you simply like the fund house. But fund managers could quit and processes could go awry.Remember that if you have invested a substantial portion of your portfolio with a particular fund house and it does not do well one year, your returns will suffer.Spread your money across different fund houses so that you can benefit from their different processes and methodology – this is diversification at play !.

4. Intra diversify your investmentsThis one could be missed very easily but is equally important. When you buy into equity or debt, achieve diversification using different parameters. Some quick examples could be :

1. Make sure you diversify across different sectors of the industry.2. Make sure you have substantial spread between large caps, small caps and mid caps.3. Spread money across different debt instruments – gilts or corporate bonds for example.4. Go for balanced funds, tax saving funds (ELSS) or monthly income plans and not just equity diversified funds.

Last WordDiversification is the most basic yet important tool in an intelligent investors hand. If used correctly along with asset allocation, it can be a powerful tool to flaunt and one of the best ways to achieve safe returns on your investment portfolio.

Real estate or stocks ? - TheWealthWisherPosted by TheWealthWisher on Nov 15, 2010 in Investing | 6 commentsinvestment comparison

0

Share

The choice of investing in real estate orstocks is driven by many factors, bordering from emotional indulgence to pure gamble. Where to invest between these investment avenues is an answer you will need to find depending on some factors in your financial planning process , namely asset allocation, future financial goals and risk taking capability. Let us do a quick run down on the perceptions investors have when investing in real estate or stocks.Investors find real estate tangible – the can see it with their own eyes. This offers a very comforting feeling to investors – they think they can see what they are buying. This gives them a sense of security. Between real estate or stocks, the former is something which the investor comprehends better. Or so it seems.Real estate also has a very emotional angle attached to it. Indians generally buy a house to live in. Owning a house was a very ambitious and once in a lifetime event for parents of the earlier generation, so owning a house today is a goal for almost every investor. It’s a decision supported by the elders in the family very strongly irrespective of whether they understand the pros and cons of investing in real estate or stocks or for that matter any investment class.There have been innumerable stories of how people made tons of money by buying real estate in the early 2000s. It’s true that the real estate boom in India made many a middle class person rich as far as home equity is concerned. Going by these stories, every one thinks they still can make a killing by investing in real estate. Coupled with the price appreciation is the fact, or maybe a notion that a consistent rental income can be easily got from a property. For these reasons, between real estate or stocks, the middle class investor chooses the former.Time for a reality check. !Firstly, the property market in India sucks. There are no regulations in place and builders are making hay duping investors. The correct price of an apartment can/is never known. The correct price unfortunately comes to be the price which builders and real estate agents drive as sales in a vicinity. But that might not be the right price. Its the builders who give the notion that the market is stable and that it will only rise. Gullible investors believe them and are rest assured that their investment is safe. They feel safe with their money invested in properties.Secondly, like all other asset classes, property also has its ups and down. Its not true that it will only go up. Remember the 2008 2009 property slowdown ? If you happen to catch real estate at the upper end of the sine curve, it will be a long time before you can recover after a slump. And remember, the property market is not a liquid one. If you want to liquidate during a slump, it’s not going to be easy.

Which makes us move our focus to equities amidst this real estate or stocks discussion.

The stock ticker is every investors nightmare. Every fluctuation can make his investment go up or down. It’s this visible fluctuation of his net-worth that makes the investor stay away form the stock market. Over a short period of time, the stock market could cause a few heart attacks but over a long period of time, it’s the winner. But many investors don’t know that and they think the stock market is a gamble den. It sure is, only over a small period of time though. Investors focus on too many stock news and get carried away by the greed of short term profits. It is the uncertainty of stocks over a short period of time that makes them wary. Investors who love property between real estate or stocks do so very for this reason.But investors forget the advantages with stocks. Stocks are very liquid and can be bought in small amounts of money. Between real estate or stocks, it is very obvious that you can achieve diversification with the latter more easily than the former.If investors choose the right stocks or take the systematic investment planning route of mutual funds, they can be rest assured that they will reap riches from the stock market.Take a look at what the Indian market has offered between real estate and stocks.

As you can see, equity is the winner while property is not much behind.So what should investors do – should they invest in real estate or stocks ?Invest in these two asset classes depending on your asset allocation. You cannot miss out on real estate – the famed Peter Lynch said that the first investment one should make is invest in a house. So by all means, indulge yourself.It is generally advised that a person should not have more than 45% of his networth in real estate. Of the rest, follow the (100-x) thumbrule to invest in equity and debt.

That’s as good as it gets between real estate or stocks. Whats your take ?

The Ultimate Listing of Personal Finance Learning Sites - TheWealthWisherPosted by TheWealthWisher on Nov 9, 2010 in Investing | 16 commentsinvesting tips

0

Share

My reader Ravi asked me “Can you please suggest me some good books for knowing the basics of investment and finance in India ? I want to be aware of must needed financial terms and plans.”. This compilation is an offshoot of the comment above. Why spend on books to learn personal finance when the Internet can offer everything ? I present the ultimate guide to personal finance sites which you can use to learn about financial planning basics.I am also suggesting the order in which you take to reading these if you are a beginner.

MagazinesStart with one magazine from the list below. The first two are gems.

1. Outlook Money – Should be on top of your list if you are eager to start reading.2. MoneyToday Magazine – Monthly magazine with loads of learnings.3. MoneyLife Personal Finance – Another magazine for you to kill your time.4. BusinessToday Money – Very compact articles from the financial world.

Ultimate Listing for Personal Finance Sites

WebsitesGet to any of the below on-line portals next to enhance your learning.

1. Rediff.com Business Personal Finance – Plethora of articles. You will run short of time to read. Basic stuff.2. Rediff.com GetAhead Personal Finance – Ditto as above.3. Yahoo Finance – Great repository for beginners and advanced readers.4. The Motley Fool – Though US based, most of the articles can be applied locally.5. MintBlog - Again, this is US based, but a great place for learning.

On-line NewspapersI think this is optional for beginners. Take to it if you are twiddling your thumb.

1. Economic Times Personal Finance – You can expect the best from the experts. Must read.2. LiveMint.com Personal Finance – News from the finance world as and when it happens.3. IndianExpress Money – Simple and short snippet articles on personal finance.4. BusinessStandard Banking – Heavy on banking and economy.

Niche SitesNiche sites for mutual funds and stocks. Now there are many more such sites and I can say these are the ones that will meet all your objectives. So don’t waste time anywhere else.

1. ValueResearchOnline - The comprehensive guide to Mutual Funds in India.2. MoneyControl - Great place with step by step guides on all aspects of personal finance.

Blogs from IndiaApart from the websites, there are blogs out there to teach you the basics as well – the basic advantage is you can talk via comments to the blogger and other readers to make your learning more interactive. Here is the listing, in no order of priority at all ! Some might tend to lean more towards the stock market while others might be a mish-mash of your expectations, so take your pick.

1. InvestmentYogi Articles 2. JagoInvestor 3. RaagVamdatt 4. RanjanVerma 5. Subramoney 6. TheFinancialLiterates 7. OneMint 8. TipBlog 9. Squamble 10. MyJourneyToBillionaireClub 11. CapitalMind 12. TheMoneyQuest

Blogs from around the worldThere are tons and tons of them out there and I cannot jot down all because I don’t follow all of them myself. But here is the three I follow and I can assure you that you don’t need to look beyond these !

1. Moolanmony 2. The Digerati Life 3. Get Rich Slowly

Financial Calculators

And if you need to use calculators to check how deep in trouble you are financially, go for the below.1. MoneyControl - Lots of calculators across all areas of personal finance.2. PersonalFn -Some basic calculators offered.3. InvestmentYogi - Amazing number of calculators to use.4. JagoInvestor Calculators – A good bunch of easy to use calculators with examples.5. BankBazaar Calculators – Another site with decent calculators in the offing.

Now get started !

How many insurance policies should you have ? -TheWealthWisherPosted by TheWealthWisher on Oct 28, 2010 in Insurance | 7 commentsbasics of insurance

1

Share

This is in continuation of my “How Many” series articles. The topic this time is how many insurance policies should one have ? While we did touch upon must have insurance policies for an investor in his overall financial planning, what might confuse the investor is how many such insurance policies should he totally have. If you are not aware of this number, you could get loaded with innumerable junk policies which could hurt your overall financial health. Let us go step by step to get to the magical figure.

Life InsuranceHaving understood the basic premise that insurance is meant only for protection and not for investment, the obvious conclusion an intelligent investor will make is to take term insurance. That makes our count of number of insurance policies as 1. How many such term insurance policies should you buy ? Generally, this is driven by the life stage events of a person. The first life insurance policy a person should buy is when he gets a job. The second policy can be bought when he gets married. The third, when he has a kid. Going by this, our count now becomes a minimum 3. You could even make this four, but then the more policies you take, the more tracking you need to do of when premiums need to be paid. Don’t go beyond 5 by any means.

Remember that if you have bought children’s plan and Unit Linked Insurance Plans or ULIPs as well, the total count should not extend beyond 5. Don’t buy ULIPs, endowment plans, moneyback plans if you possibly can. The conclusion here is that the total life insurance policies should ideally not cross 5.It is generally advised that life insurance should be taken from more than one insurance company. Let us see why. Suppose you have taken term insurance from just one insurer and on your demise, the claim is challenged in court due to some reasons. If there is no payout eventually, your family will be left with no money – this would defeat the basic purpose of why you paid premiums to an insurer to cover your life. In order to reduce this risk of claim rejection, it is advised that you spread your risk by taking insurance from more than one insurer.Make sure that your 5 life insurance policies (or minimum 3 as explained above) are spread evenly across different insurers.

General InsuranceAmong the general insurance policies, a health insurance policy is a must. This is same as mediclaim.An investor must also take a personal accident insurance policy.Over and above these two, there is critical illness that a person can take optionally. Financial planners generally

recommend such products as must have. Assuming you go for this, our count now becomes minimum 6 and maximum 8.Now, unfortunately you do have more assets you want to protect. You want to drive your own vehicle and live in your own house. Well, there are policies you must have for those too. The motor insurance is mandatory for the vehicle you drive so there is no escape here. Our count just increased.If you stay in your house, you might decline to take insurance for loss of belongings in your house or for structural damages to your house. If you think for a moment, the house is more precious and expensive than your motor, yet you took motor insurance because it is mandatory in India. What if there is a fire in your house or an earthquake damages the structure of your house. Home insurance is an important protection that all investors must have. I will take the liberty to increase the count yet again.Now we could go on and on and add another protection policy which pays the outstanding loan (on your demise) that you have taken on your house. But for the moment let’s assume that the life insurance plans will cover such needs.The count stands at 8 minimum and 10 maximum.So there you have it. I think it’s challenging enough to track 8 insurance policies year on year. You could argue that you can club in the health and critical illness covers with a ULIP and make the count come down. Remember, finance is simple and you should buy products which are simple as well. Its generally advised to buy life, health and critical illness plans separately.Keep the following things in mind :

Start young and invest regularly - TheWealthWisherPosted by TheWealthWisher on May 23, 2010 in Financial Planning | 5 commentsbeginner saving

2

Share

What would you think if you were fifty years of age, had a doting daughter and a SNOB son; had happily met their whims and fancies always as both of them were addicted to the latest gizmos and trends out there in the street and therefore you really never saved your money ever, leave alone invest it and are now suddenly faced with the daunting task of coughing up fifty lakhs for your daughters higher education in the US.Fact of the matter is, there are a lot of investors out there who find themselves in the same position – those who never saved for such a goal in one’s life. But even if one had, how soon should one start? 5 years before the money was needed? 10 or 15?Finance pundits will tell you, the earlier, the better.

Let us take an example.Suppose Mr Wise-Saver is 30 years old and decides to save till he works (say 60 years of age). However, he can only invest Rs 10,000 each year.On the contrary, Mr Movie-Goer can save more but hasn’t really started till he reaches age 45. With 15 more years to go before retirement, he realizes he has to rack up money. He decides to put in Rs 20,000 each year, double of what Mr Wise-Saver puts in.Lastly we have Mr Gone-Case, who doesn’t really care about saving – he wakes up at age 55 and thinks that investing Rs 40,000 each year will do him good. Let’s compare what each person will get at age 60.

Mr Wise-Saver puts in Rs 10,000 each year for 30

years

Mr Movie-Goer puts in Rs 20,000 each year for 15 years

Mr Gone-Case puts in Rs 40,000 each year for 5 years

Yr. No. Monies Yr. No. Monies Yr. No. Monies

1 10,000 1 20,000 1 40,000

2 21,500 2 43,000 2 86,000

3 34,725 3 69,450 3 138,900

4 49,934 4 99,868 4 199,735

5 67,424 5 134,848 5 269,695

6 87,537 6 175,075

7 110,668 7 221,336

8 137,268 8 274,536

9 167,858 9 335,717

10 203,037 10 406,074

11 243,493 11 486,986

12 290,017 12 580,033

13 343,519 13 687,038

14 405,047 14 810,094

15 475,804 15 951,608

16 557,175

17 650,751

18 758,364

19 882,118

20 1,024,436

21 1,188,101

22 1,376,316

23 1,592,764

24 1,841,678

25 2,127,930

26 2,457,120

27 2,835,688

28 3,271,041

29 3,771,697

30 4,347,451

Assumed Rate of Return is 15% each year.As shown above, Mr Wise-Saver will end up with Rs 43 lakhs while Mr Movie-Goer will get Rs 9.5 lakhs even though he has doubled the investment as compared to Mr Wise-Saver. However hard Mr Gone-Case tries, he will have the least even though he invests four times of what Mr Wise-Saver puts in !Working behind generating this huge amount of money over such a long period of time is a wonder called compounding.The power of compounding works its magic over a long duration of time and produces massive wealth.

It’s imperative that each of us start investing our money as early as we can, possibly in the early twenties. Waiting for a day, when we think we will earn enough to save and invest will never come – with an increased earning capacity comes an increased living expense. This is a vicious cycle every investor needs to get out of.So start now with whatever little you have !

What is your definition of wealth ? - TheWealthWisherPosted by TheWealthWisher on May 21, 2010 in Investing | 1 commentinvestment musings

0

Share

How do we define wealth ? If we plan to be wealthy, what do we mean by that? When will we call ourselves wealthy? Like everything in life, this question ought to have an answer – we need to know when to make that call.For a poor individual, living in a pukka house and sending his children to good schools could be the definition of wealth; for a middle class person, driving a classy sedan and living in a bungalow could be the definition.Does our definition of wealth stay constant ? Having a small car and a small house could make us wealthy; once we attain that, we look to buy a bigger car and a bigger house. Will acquiring these make us wealthy? The way life is, its sure to thrown in a few problems of its own and skew our definition of wealth. It leaves us asking for more.

Whatever be the meaning, its quite clear that : Without such a measure, it will be akin to standing at a shooting range and aiming with a rifle – only to find that the mark is missing.

By Salvatore Vuono from freedigitalphotos.net

I define wealth as the amount of money that can make me and my family live comfortably today and tomorrow and which won’t make me ask for more. You could argue that “live comfortably” is a very subjective view. I agree. And I won’t argue. That’s why it’s my view!The definition of wealth is different for different individuals.Every investor needs to first measure what his definition is. And then aim to get to it.

All those who have set out to get rich need to know when they can call themselves rich. Without such a target, one is a blind man in a blind world.Here’s wishing everyone wealth which can make them happy forever.

HDFC Top 200 mutual fund review : stellar performance. - TheWealthWisher

Posted by TheWealthWisher on Aug 13, 2010 in Product Reviews | 40 commentsmutual fund reviews

3

Share

HDFC Top 200 is one mutual fund you cannot give a miss. Coming from the stable of HDFC Fund house, its no surprise that this fund has performed consistently over the years. HDFC fund house has some of the best mutual funds to its credit.If you do not have this in your portfolio, you might want to take a hard look at replacing one that you have with HDC Top 200.Lets take a peek into the performance of HDFC Top 200 mutual fund.Post updated in Dec 2010 to reflect current review status.

Objective of HDFC Top 200Launched in September 1996, the fund is an equity diversified open ended mutual fund with a large cap bias. It is bench marked against BSE 200.HDFC Top 200 objectives state “The scheme seeks capital appreciation and would invest up to 90 per cent in equity and the remaining in debt instruments. Also, the stocks would be drawn from the companies in the BSE 200 Index as well as 200 largest capitalized companies in India“. The fund manager does retain the ability to invest in companies that are unlisted but which are still in the BSE top 200 by market capitalization.HDFC Top 200 carries a below average risk profile while its returns are high.

Details of HDFC Top 200

NAV : 221.454 (Dec 27th 2010) Launch Date : September 1996 Return since launch : around 26% Net Assets : Rs 9,069 crore Entry Load : Nil Exit Load : 1% id redeemed within a year and nil if redeemed after year. Minimum Application Amount : Rs 5,000/- for new investors and Rs 1,000/- for existing ones. Options : Growth and Dividend / SIP Risk : Below Average Return : Very High Benchmark : BSE 200

Performance of HDFC Top 200Here is what HDFC Top 200 mutual fund would have returned to you had you invested Rs 1,000/- each month in the time periods shown. Note that the annualized returns of HDFC Top 200 are beating the benchmark returns hand down.SIP Investments Since Inception 10 Year 5 Year 3 Year 1 Year

Total Amount Invested (Rs.) 170,000 120,000 60,000 36,000 12,000

Market Value as on November 30, 2010 (Rs.)

1,651,330.27 715,521.60 109,175.33 58,537.24 13,843.56

Returns (Annualized)*(%) 28.58% 33.54% 24.19% 34.23% 29.76%

Benchmark Returns (Annualized)(%) 18.33% 22.23% 15.39% 23.18% 17.22%

If you happen to look at the annual returns, they are mind boggling as well. Except for 2006, it has beaten its benchmark each and every year. 2009 2008 2007 2006 2005

Fund Returns 94.46 -45.35 54.46 37.44 55.25

S&P CNX Nifty 75.76 -51.79 54.77 39.83 36.34

Sensex 81.03 -52.45 47.15 46.70 42.33

PortfolioThe portfolio concentration as of Nov 2010 was 95% equities and 5% debt.Large Cap makes up around 15% of holdings while the rest 85% is Large cap. The large caps are predominantly index stocks and blue chips like Stats Bank of India, Infosys Technologies and ICICI Bank.The top 3 holdings make up around 50% of portfolio concentration while the top 10 make up around 43%.

Comparison with other fundsWhen compared to its peers (comparison on a large cap basis only), say DSPBR Top 100 and Birla Sun Life Frontline Equity, HDFC Top 200 seems to have taken a bit of risk to get the returns. Note that if you compare it with other large cap mutual funds, it might turn out to be less risky – I have provided comparison with only two mutual funds.

Fund NameStandard Deviation

Sharpe Ratio

DSPBR Top 100 28.69 0.19

Birla Sun Life Frontline Equity 35.88 0.07

HDFC Top 200 32.3 0.37

As far as the Sharpe ratio is concerned, HDFC Top 200 seems to do the best. Sharpe Ratio is defined as the returns delivered by the fund, per unit of risk borne. In the comparison shown, Birla Sun Life Frontline Equity seems to be doing the worst while HDFC Top 200 is doing the best.

Who is HDFC Top 200 mutual fund for ?Its best suited for low risk averse investors who want steady yet near guarantee returns. The fund has beaten its benchmark in all the years except in 2006. With a return of around 26% since launch, it has proved it is dependable and consistent. In the market crash of 2008, HDFC Top 200 lost around 45% only, which was less than the category average and BSE 200. In 2009, the fund was back with a bang and established its clout among the best performing funds.

Why buy HDFC Top 200 mutual fund ?You hardly get a stalwart return of 26% year on year.Prashant Jain, the fund manager has been at the helm of affairs for straight 8 years, which goes to show what a good fund manager can accomplish for a mutual fund.HDFC Top 200 comes from a fund house which is known for its process driven approach to investments. Given the consistent good returns over a long period of time, investors should not give this a miss if it suits their risk and return appetite.Go for HDFC Top 200. It’s a must have in every portfolio.

Facts to consider before buying health insurance -TheWealthWisherPosted by TheWealthWisher on May 29, 2010 in Insurance | 6 commentshealth insurance

0

Share

Buying health insurance in India needs to be a careful task. There have been incidents of painful moments investors have gone through at the time of hospitalizations and claims with the insurance company refusing to reimburse the actual expenses incurred. In order to avoid hassles like these, one needs to keep in mind the following points before zeroing down on health insurance. Let the buyer be aware is the policy as far as health insurance goes.

1. Where do I buy my health insurance policy from – general insurance or life insurance companies ?Life insurance companies are more focussed on providing insurance (or rather investment in today’s world of mis-selling !!!) for life, so health insurance is not a central point of business for them. Would you go to your neighbourhood grocery store and buy loads of vegetables with the expectation that they will be green, leafy and fresh ? If you want to buy fresh vegetables, you would rather go to “sabzi mandi”. Keep insurance simple – buy health insurance from general insurance firms. Note that if you were to buy it from life insurance companies, the charges would be slightly more.

2. Which general insurance companies should I look at ?The ones that will pay your claim always ! But of course, you do not know that in advance. So check the claim settlement records of the company. Ask the agent selling you the policy for these details. You might not get anywhere to begin with but make sure you check thoroughly before you buy – many health insurance companies are still trying to break even and are suffering heavy losses. Also check for the solvency margin of the company – you do not want your insurer going bust within months of buying your policy especially if you are old aged.

3. Who is the TPA (Third Party Administrator)?Check out who the TPA is and enquire about what it has to offer. Many TPAs might not cover the hospitals which you are looking at for future hospitalizations. So check with the TPA to see which all hospitals they cover. You interaction during and after hospitalization is with the TPA for claim settlement, so make sure you know the people you will be dealing with in your time of crisis.These are some of the most critical aspects to be kept in mind when taking health insurance.