Embed Size (px)

Citation preview

J. Sagar Associatesadvocates & solicitors

Delhi | Gurgaon | Mumbai | Bangalore | Hyderabad

Legal Due Diligence:The Overlooked Cornerstone

Due Diligence: The Big Picture

Due Diligence

Due Diligence can be categorized into:

Business or Strategic Due Diligence

Legal Due Diligence

Business Due Diligence: The Role of Lawyer

In business due diligence, the client determines its objectives in pursuing the transactions and indentifies potential targets

Attorneys can bring valuable experience and acumen at the planning stage and can improve the transaction plan by highlighting the legal issues that might arise at a later stage

Involving legal expertise at the planning stage can relay early warning and reduce the cost of legal diligence and emergency planning in a later acquisition / financing process

The Purpose

To help buyer to formulate its bid to decide on pursuing the transaction

To supplement representations/ warranties/ indemnities, especially when the representations and warranties expire at closing and when creditworthiness of the indemnification is suspect

To confirm the investment decision: Due diligence helps to determine wisdom of the acquisition. It also minimizes (but does not eliminate) the risk that the business is not as understood

To prepare better documentation. Due diligence allows a better ability to negotiate appropriate purchase price adjustments or adjustments to other terms of the purchase contract. Appropriate representations, warranties and other terms and conditions can be better customized

To determine whether closing conditions have been met

To establish an "innocent purchaser" defense to certain situations (Requires appropriate inquiry consistent with good commercial or customary practice)

The Purpose

To establish "reasonable prudence" or "justifiable reliance" conditionsto recover on action for fraud

To prepare buyer to run the business post-closing.

Due Diligence is not a substitute for Representation/Warranties or for that matter Indemnities.

The Purpose

Organizing Due Diligence

Determine the respective roles of the experts: Lawyers Accountants Environmental engineers Insurance specialists Consultants Investment bankers Others

Organizing Due Diligence

Legal specialties to be represented on the diligence team: Corporate lawyers Litigators Environmental lawyers Intellectual property lawyers Others

Organizing Due Diligence

Customize the diligence. Understand the business being acquired/transaction being pursued: Need to educate the diligence team about the

company and transaction Understand the legal, regulatory, and business risks

• Distinguish between the purposes of acquisition diligence (substantive) versus public offering diligence (disclosure and due diligence defense) The due diligence in a financing transaction would

focus on adequacy of security package Similarly, the extent of diligence will vary depending

on whether the target is public / private or whether the transaction is private equity investment or PIPE transaction

Due Diligence: Goals and Themes

Understand the Seller’s Business Emphasize on comprehensive, realistic

understanding of the targets business Uncover the hidden liabilities and risks Review the filings for listed companies in the

public domain

Evaluate the Deal Inject a degree of reality in the deal and test

the assumption underlying the projections and search for mechanisations behind the financial statements

Due Diligence: Goals and Themes

Deal Structure and Documentation Facts and issues discovered in due diligence

have significant impact on deal structure and documentation

Representation, Indemnities and Closing Conditions

Red Flags Finding any deal breakers is important part

of any due diligence exercise Similarly, deal negotiators play an important

role in negotiation process

Due Diligence: Goals and Themes

Due Diligence and Sellers Perspective Due diligence is not only a buyers task – Seller also has a

great deal to learn from it The process of building data room or assembling or

reviewing materials for distribution creates invaluable opportunity to examine the strengths and weaknesses of the business

If deal goes through, the enhanced view will allow seller to get the best bargain (price, financing etc) in future

If deal does not go through- helps management focus on weaknesses which demand improvement prior to another effort for the transaction

Prepares management for recommending the deal to the shareholders

Disclosure by the Seller act as qualification to the representation and warranties

Key Legal Diligence Areas

Corporate and Secretarial Approvals and Licenses Litigation Environmental Government regulation/compliance Material contracts HR and Industrial law compliance Transactions with affiliates

Key Legal Diligence Areas

Intellectual property Foreign operations

Due Diligence: The Nuts and Bolts

Due Diligence - The Nuts and Bolts

Due Diligence demands a dynamic and creative approach

What is required of due diligence will depend on the goals of the client, the industry, the timetable, the structure of the deal, the culture of the corporations, and the personalities of the players, among other things

If the due diligence process is not adapted carefully and thoughtfully to each deal, the transaction is likely to prove less profitable and successful than expected

Due Diligence - The Nuts and Bolts

Areas of focus should include: Corporate Governance & Key Approvals

verify the certificate of incorporation & articles of association

does the charter require special shareholder approval for the contemplated transaction?

are the minute books complete and the necessary board approval documented?

are shares properly authorized and issued? Will the change in control or transfer of asset

require fresh approvals under various laws?

Due Diligence - The Nuts and Bolts

Management Financial

who take the accounts receivable and credit lines?

are consents and/or guarantees needed?

are defaults in loan documents triggered by a change in control or sale of assets?

Due Diligence - The Nuts and Bolts

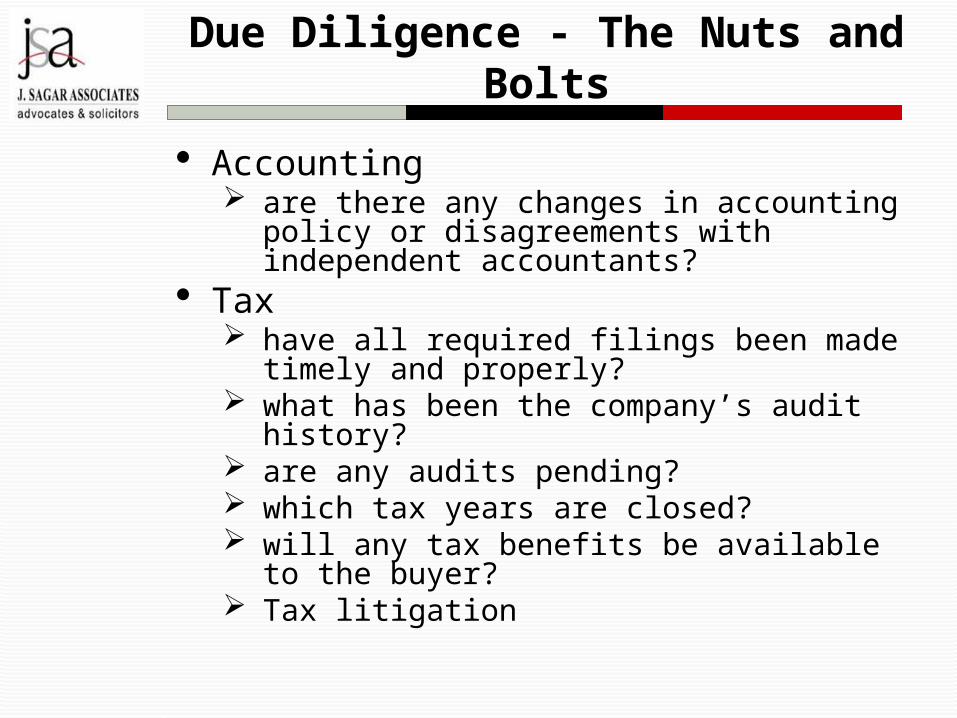

Accounting are there any changes in accounting policy

or disagreements with independent accountants?

Tax have all required filings been made timely

and properly? what has been the company’s audit history? are any audits pending? which tax years are closed? will any tax benefits be available to the

buyer? Tax litigation

Due Diligence - The Nuts and Bolts

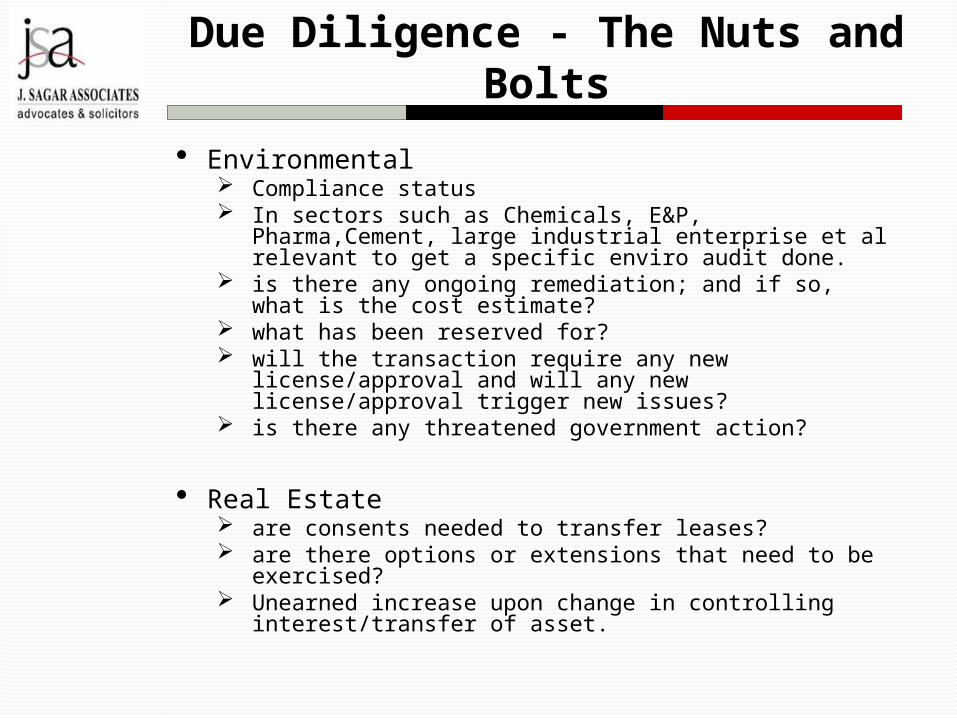

Environmental Compliance status In sectors such as Chemicals, E&P, Pharma,Cement,

large industrial enterprise et al relevant to get a specific enviro audit done.

is there any ongoing remediation; and if so, what is the cost estimate?

what has been reserved for? will the transaction require any new license/approval and

will any new license/approval trigger new issues? is there any threatened government action?

Real Estate are consents needed to transfer leases? are there options or extensions that need to be exercised? Unearned increase upon change in controlling

interest/transfer of asset.

Due Diligence - The Nuts and Bolts

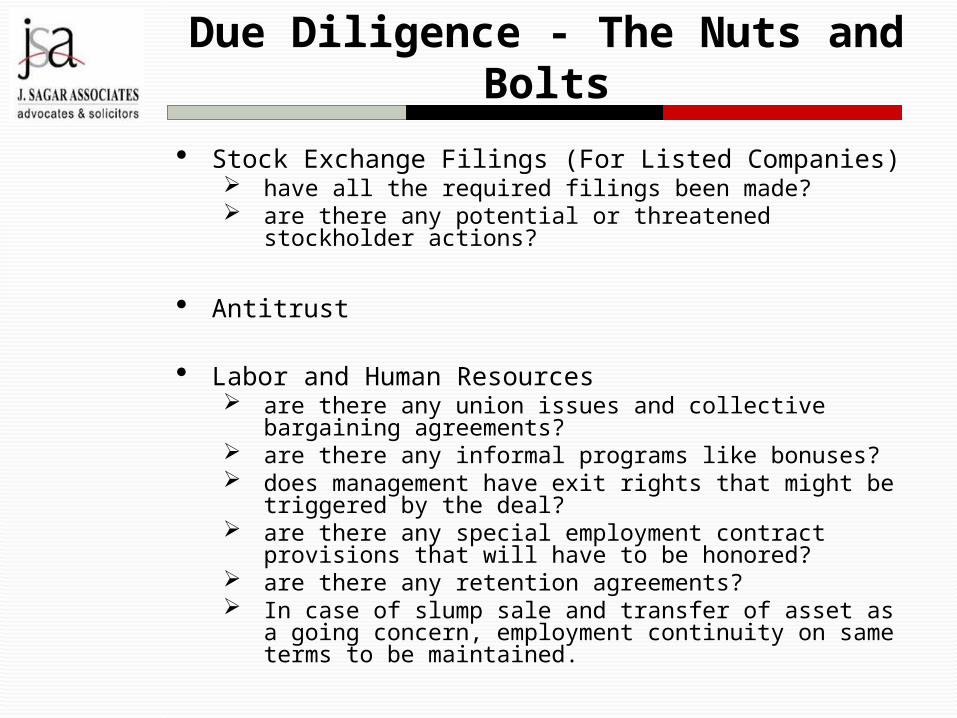

Stock Exchange Filings (For Listed Companies) have all the required filings been made? are there any potential or threatened stockholder actions?

Antitrust

Labor and Human Resources are there any union issues and collective bargaining

agreements? are there any informal programs like bonuses? does management have exit rights that might be triggered

by the deal? are there any special employment contract provisions that

will have to be honored? are there any retention agreements? In case of slump sale and transfer of asset as a going

concern, employment continuity on same terms to be maintained.

Due Diligence - The Nuts and Bolts

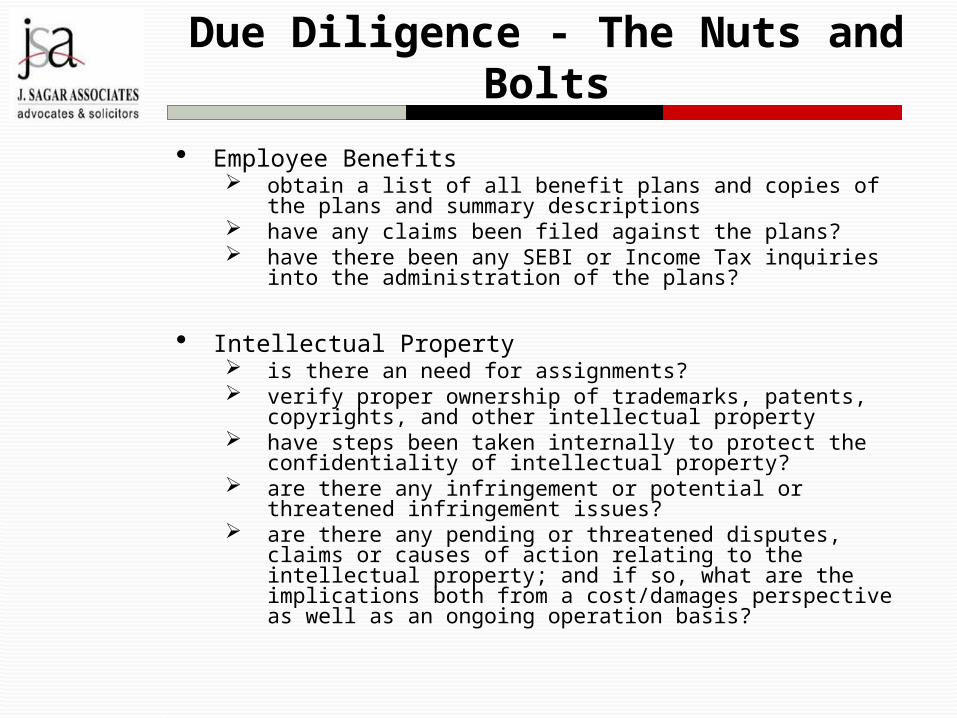

Employee Benefits obtain a list of all benefit plans and copies of the plans and

summary descriptions have any claims been filed against the plans? have there been any SEBI or Income Tax inquiries into the

administration of the plans?

Intellectual Property is there an need for assignments? verify proper ownership of trademarks, patents, copyrights, and

other intellectual property have steps been taken internally to protect the confidentiality of

intellectual property? are there any infringement or potential or threatened infringement

issues? are there any pending or threatened disputes, claims or causes of

action relating to the intellectual property; and if so, what are the implications both from a cost/damages perspective as well as an ongoing operation basis?

Due Diligence - The Nuts and Bolts

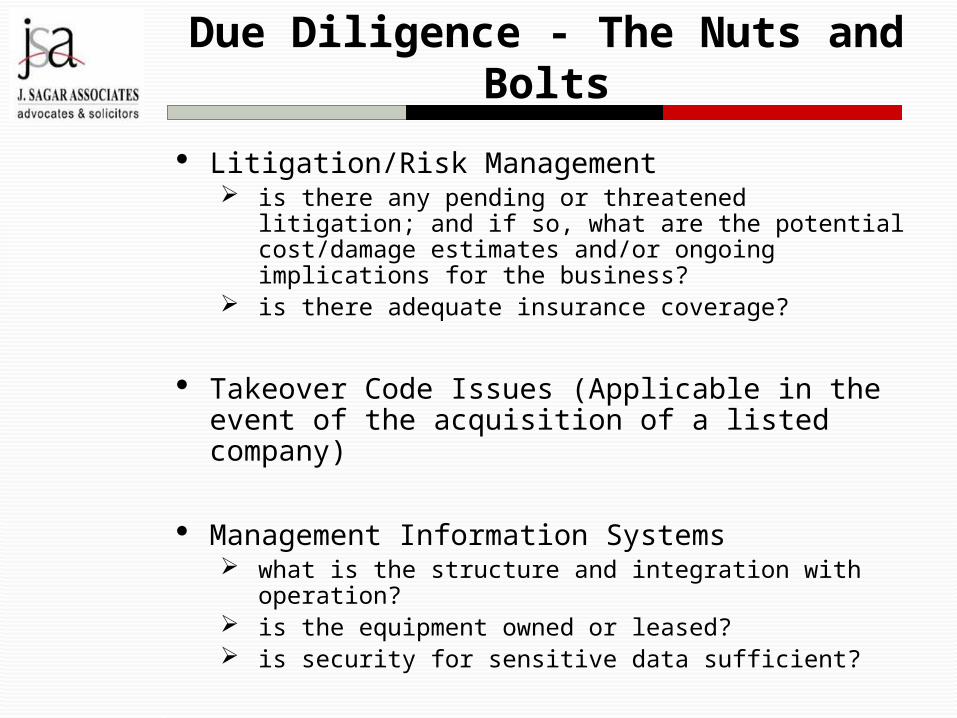

Litigation/Risk Management is there any pending or threatened litigation; and if so,

what are the potential cost/damage estimates and/or ongoing implications for the business?

is there adequate insurance coverage?

Takeover Code Issues (Applicable in the event of the acquisition of a listed company)

Management Information Systems what is the structure and integration with operation? is the equipment owned or leased? is security for sensitive data sufficient?

Due Diligence - The Nuts and Bolts

Manufacturing/Production/ Operations

Research and Development past and present plans is research and development done internally

or externally? what are the costs and expenses of R&D?

Marketing evaluate how products and services are

marketed geographic sales is the business seasonal or cyclical?

Due Diligence – Transaction Specific Issues

Public Company Deals Have benefit of reliable public information

(BSE/NSE/other stock exchange filings). The first step in due diligence has to be extensive review of public information

Strict confidentiality has to be maintained in the due diligence process because of “insider trading” and “price sensitive information” issues under Securities Exchange Board of India (Prohibition of Insider Trading) Regulations, 1992

Access to dataroom and outflow of information has to be controlled by setting up dataroom rules to monitor outflow of information.

Lawyers/consultants/advisors conducting due diligence customarily asked to sign confidentiality agreements.

Due Diligence – Transaction Specific Issues

Public Company Deals The core group of the company personnel have

to be apprised about the sensitivity of the transaction

The purpose of a M&A due diligence is substantive and the objective is to identify deal breakers, deal negotiators and value depletors

The presence of public shareholders expectations means that the deals are more standardised

In addition, the public company deals may trigger the Takeover Code and diligence team also needs to prepare for filing of Letters of Offer/Public Announcement documents with SEBI

Due Diligence – Transaction Specific Issues

Private Company Deals In private company deals there no stock

exchange filing(s) or reliable public information In private company deals, you have to rely on

representations, warranties and due diligence only

Recourse to Seller is available for the breach of representation and warranties

As SEBI regulations are not applicable, it can be done quietly in private

Private deals involve more variations and individual negotiations

Break down of private deal is not as catastrophic as public deals

Due Diligence – Transaction Specific Issues

PIPE Transactions (Private Investment in Public Enterprise)

A public listed company cannot communicate any undisclosed price sensitive information to any person under SEBI Regulations

If listed company communicates any undisclosed price sensitive information to the private investor, the private investor would qualify to be an 'insider' in accordance with the provisions of regulation 2(e) of the SEBI Insider Trading Regulations

Such private investor cannot therefore deal in the securities of such public limited company on the basis of such price sensitive information which is disclosed by the listed company under section 15G of the SEBI Act and regulation 3 of the SEBI Insider Trading Regulations

The investors / listed companies generally adopt one or more of the following methods to achieve the above objective without contravening SEBI Regulations

Due Diligence – Transaction Specific Issues

Rakesh Agarwal v. SEBI – Securities Appellate Tribunal• The appeal was against the order dated 10. 6.2001 of Chairman, SEBI against Shri Rakesh

Agarwal, directing – (i) Rakesh Agarwal to deposit Rs.17,00,000 each with Investor Protection Funds of The Stock

Exchange, Mumbai and National Stock Exchange to compensate any Investor who may make any claim aggrieved with the sale of shares of ABS Industries to Shri I.P. Kedia during the period 9.9.96 to 1.10.96;

– (ii) SEBI to initiate prosecution under Section 24 of the SEBI Act; and

– (iii) SEBI to initiate adjudication proceedings under Section 15I read with Section 15G of the SEBI Act.

Facts: Rakesh Agarwal was the Managing Director of ABS Industries Ltd. (ABS), a company incorporated under the Companies Act, 1956. ABS was subsequently acquired by Bayer AG. (Bayer), a company registered in Germany. Bayer acquired controlling stake in ABS Industries Ltd by acquiring 55,80,000 shares @ Rs.70/ - per share in a preferential allotment made by ABS Industries Ltd. and 20% shares from existing shareholders @ Rs.80/- per share in a public offer.

– Allegations were made regarding insider trading in purchase of shares of ABS Industries Ltd prior to announcement by Bayer of acquiring controlling stake in the company. SEBI conducted an investigation into the matter and found that prior to the announcement of the acquisition, the appellant through his brother in law, Shri I.P. Kedia had purchased shares of ABS from the market and tendered the said shares in the open offer made by Bayer thereby making a substantial profit.

Due Diligence – Transaction Specific Issues

The appellant being the Managing Director of ABS and having been involved in the negotiations had access to unpublished price sensitive information. Further he was also an insider as far as ABS is concerned. By dealing in the shares of ABS through his brother-in-law while the information regarding the acquisition of 51% stake by Bayer was not public, the appellant had acted in violation of Regulation 3 and 4 of the Insider Trading Regulations.

Order: The SAT in its order dated 3.11.2003 allowed the appeal finding that the appellant was not guilty of Insider Trading. The tribunal held that the that merger was a price sensitive information; that merger of Bayer with ABS Industries was price sensitive and unpublished; that Rakesh Agrawal an ‘insider’ and that he had purchased the shares of ABS on the basis of unpublished price sensitive information. However, the tribunal held that since Rakesh Agrawal acted in the interest of the company he cannot be considered to have violated the Insider Trading Regulations. The tribunal also held that although Rakesh Agrawal had made profit out of the transactions but it was only incidental to the cause of the interest of the company.

– The tribunal held that although it is true that Regulations 3 and 4 of the SEBI (Prohibition of Insider Trading) Regulations, 1992 are per se pure vanilla sections without specific mention of the requirement of the motive or intention, if read with the objective of prohibiting insider trading it becomes clear that motive is built in and the insider trading without establishing the motive factor is not punishable. It found that if it is established that the person who had indulged in insider trading had no intention of gaining any unfair advantage, the charge of insider trading warranting penalty can not be sustained against him In view of the above, the Tribunal allowed the appeal.

Due Diligence – Transaction Specific Issues

Result: SEBI appealed to the Supreme Court of India against the order of SAT and the Supreme Court admitted the appeal. Soon thereafter, SEBI notified a circular dated April 20, 2007, whereby the parties could settle disputes with SEBI on the basis of the consent terms. The apex court in its order dated January 23, 2008, disposed off the matter on the basis of the consent terms without deciding the issue on merits.

Conclusion: No definitive ruling by the Supreme Court and therefore, all we can do is rely on the decision of the SAT to protect the company and its officers disclosing unpublished price sensitive information to potential investors in a preferential allotment.

Due Diligence – Transaction Specific Issues

PIPE Transactions (Private Investment in Public Enterprise)

Management of public limited company authorizes certain reputed firm of auditors and legal counsels to conduct a due diligence over the listed company as part of the compliance obligation.

Pursuant to the due diligence, the company may disclose to the investors and to the public that the that the auditors/legal counsel are satisfied with the state of affairs after the due diligence exercise.

– If the auditor/ legal counsels have raised certain concerns or issues upon the conduct of the due diligence, they may be requested to prepare an 'exceptions report'.

– In the event, that some of the issues raised by auditors are not resolved, the public limited company may choose to disclose such parts of 'exceptions report' to the public and to the private investor.

Due Diligence – Transaction Specific Issues

Initial Public Offering (IPO) Due diligence for initial public offering is undertaken to provide

adequate disclosure to public to take an informed decision. The due diligence should cover the required disclosures and

eligibility requirements for listing under the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009

Due diligence also focuses on drafting of offer documents to be filed with SEBI

Adequate disclosure to the public, SEBI and stock exchanges would provide protection against allegation(s) of fraud in future

IPO’s involve an international wrap under Rule 144A and Regulation S of the Securities Act of 1933 of United States

Due diligence extremely important to provide protection against the anti fraud provision 10-b-5 of Securities Exchange Act of 1934 of United States

Due diligence also becomes important to show that the board has taken an informed decision and has complied with its fiduciary duties

Due Diligence – Transaction Specific Issues

Project Finance Transaction Due diligence for project finance transaction primarily focuses on

the feasibility of the transaction structure and the adequacy of the security package

Title to asset, which are subject matter of security.

The due diligence exercise should focus on the consents/approvals required for creation of charge over the assets to be secured

It is important for due diligence team to highlight the approvals/consents required for enforcement of the charge or the complications that may arise at the stage of enforcement of charge (like triggering of change of control provision, ROFO, ROFR etc)

Due diligence exercise should also verify if there are any other charges on the assets In the event, the borrower or the lender is an offshore company, the implications arising under FEMA should also be analysed and discussed at the due diligence stage

Due Diligence – Sector Specific Issues

E&P Sector Review the Production Sharing Contract (PSC)

entered by the participants with the Government of India

Check with the company/participant for compliance with the terms and conditions of the PSC including:• Operating Committee Resolutions • Management Committee Resolutions • Work Programme and Budgets

Ensure that the transaction (financing/farm in/farm out) does not trigger the “assignment provision” arising out of change in control provisions of the PSC

Due Diligence – Sector Specific Issues

Review the Joint Operating Agreement to determine: the rights and obligations of the participants determine the ROFO/ROFR provisions arising out of

change of control/transfer of participating interest any other restrictive covenants

Review the Petroleum Exploration License/Petroleum Mining Lease to determine any restrictive covenants

Review the construction contracts for change in control provisions

Review the crude offtake agreements/gas sale and purchase agreements for term and termination provision/quality/quantity/pricing and change in control provisions

contd…

Due Diligence – Sector Specific Issues

Telecom Sector

FDI Issue Structuring - FDI cap of 74% (49% under automatic

route, above 49% requires FIPB approval) Composition of the Board The majority of directors on the board including

Chairman, Managing Director and CEO have to be Indian citizens (enforced through licensing agreement of the DOT)

CTO/CFO are also required to be resident Indian citizens However, if Chairman, MD, CEO and CFO is held by

foreign national, prior security clearance from MHA

Due Diligence – Sector Specific Issues

Licence/Regulatory Regime Telecom operators and must act in accordance with their

respective telecom licences issued by the DoT Due Diligence must ensure that the operator is complying

with the terms of the licensing condition and security clearance

Prior approval of DOT required for change in shareholding pattern

In addition, it must comply with the following regulatory regime:

– Spectrum/Frequency allocation (WPC and SACFA);

– Interconnect arrangement (as per Interconnect Regulation); and compliance under TRAI Act

Review of compliance with Interconnect Agreements

contd…

Due Diligence – Transaction Specific Issues

Electricity – DISCOMs as an example

Final Thought

Envision Due Diligence as link between vision & reality of a great deal

Go beyond the details and make due diligence process as an integral part of the Corporate Strategy

![[Guildbook] Solicitors](https://img.pdfslide.us/doc/110x75/577cdbad1a28ab9e78a8c837/guildbook-solicitors.jpg)