Embed Size (px)

Citation preview

JAPANESE REALITIES: CHALLENGES TO MACROECONOMIC THEORY

Japan has been mired in a series of recessions for more than a decade.Incumbent prime minister, Junichiro Koizumi, a charismatic reformer who won election in 2001, pledged to forge ahead with reform, even if itshould require short-term hardship. Japan’s economy continues to struggle,however, and the prime minister’s popularity has been in decline. Criticspoint to Koizumi’s failure to deliver substantive reform thus far in his tenure.Koizumi now stands to make the most important appointment of his career,selecting a new governor for the Bank of Japan. He has stressed that the newappointee will be a “strong deflation fighter”. This has fueled speculation that he may select someone with a radical approach to monetary policy. Will Koizumi choose a “maverick” or continue to follow the conservative path he has taken so far? The speculation surrounding the selection highlightsthe continuing controversy regarding the appropriate strategy for combatingJapan’s recession. What economic and policy models explain Japan’s continuedeconomic stagnation? What is the appropriate “cure”? This symposium exploresthe relevance of several macroeconomic models and attempts to reconcile theory with appropriate policy prescriptions, both economic and political.

On 28 January 2003, the Center on Japanese Economy and Business ofColumbia University and The Mitsui USA Foundation sponsored a symposiumfocusing on the theoretical approaches of macroeconomics to Japan’s recession.Dr. Robert Feldman, Chief Economist and Managing Director of MorganStanley Japan, Ltd., was joined in his remarks by several University facultymembers. This report represents an excerpt of the symposium, accompaniedby highlights of exchanges with the audience that day.

CENTER ON JAPANESE

ECONOMY AND BUSINESS

SPONSORED BY THE MITSUI USA FOUNDATION

28 JANUARY 2003

ROBERT FELDMANChief Economist andManaging Director, Morgan Stanley Japan, Ltd.

We are dealing with a period in Japanese

history where much hasgone wrong for policy reasons and it’s easy to be terribly cynical and pessimistic about what’sgoing on there. However, I think if we go back tothinking about the modelswe use to explain Japan,there are many differentways where we can seeJapan coming back. Thereis also a lot of evidencethat it has done a numberof things that would bringabout that solution. Othermodels suggest to us thatthings actually can go inthe right direction if we getthe policies right and if thebusiness community worksproperly. I would like tospend the first few minutestalking about some economicmodels, what’s going on,and discussing the evidencein favor or against them.Then, I would like to discussa number of policy models,

because what’s going on inthe economy is one thing.Formulating policies andimplementing them is acompletely separate set oftheoretical considerations.The inspiration for thisapproach comes from aquotation I used in my1986 book. I received thequote from a person at theBank of Japan who readthrough all of Keynes’s works.It’s from a lovely letter of 4 July 1938: “Economics isthe science of thinking interms of models joined tothe art of choosing modelsthat are relevant in thecontemporary world.” That’sprecisely the issue we facewith Japan right now.

It has been fascinatingto watch over the last twoor three years the hugespectrum of pieces of adviceor models that have beenprescribed. I would saythat there are really fourcommands that differentgroups advise. One is printmoney. If you print enoughmoney the inflation willstop and everything will be okay. The second com-mand is spend. This is theapproach taken by the fiscalexpansionists who believethat if we spend enoughgovernment money then thedemand curve will moveoutward, the gap betweendemand and supply will be filled, inflation will stopand everything will be okay.The third is a group I callthe structuralists who say“Restructure!” This meansthere’s a demand-supply

gap, but the way you workon that is by shrinking theexcess supply rather thantrying to create demandenough to absorb supplythat we don’t really need.Would you really want the government to spendenough money to supportthe steel industry in Japan,to encourage them to pro-duce the whole 110 milliontons that they could pro-duce? Probably not. Theidea here is to get to workon the economic structure,eliminate excess supply andthen things will be okay,and this has labor marketimplications as well. Thefourth is the command ofreallocation, which is some-what similar to the structuralcommand, but has muchmore to do with trade theorythan it does with standardmacroeconomic theory.

There is a lot of talkthese days about how Chinais causing deflation aroundthe world. It is certainlytrue that increases in sup-ply from China reducedthe price of a huge numberof goods everywhere. I dolittle surveys on this and itturns out that the curbsideprice of an umbrella on arainy day is now the samein New York and Tokyo incontrast to ten years whenit was terribly outrageousin Tokyo. Now, you canwalk into any conveniencestore in Tokyo on a rainyday and get a very nice, fullyoperational umbrella thatwill last more than one usefor 600 yen or less, whereas

If we go back to thinking aboutthe models we useto explain Japan,there are manydifferent wayswhere we can

see Japan coming back.

—Robert Feldman

2 Japanese Realities: Challenges to Macroeconomic Theory

ten years ago that wouldhave cost you at least 1000yen, probably more. Soyes, China is producing alot. Does that necessarilymean China is the sourceof deflation? The answer isno. If the countries that arerecipients of these low-priced products from Chinawere able to reallocate thelabor from those industriesinto higher value-addedactivities quickly, then wageswould not have to fall. Therewould not be much unem-ployment, only short-term,transitional unemployment,and there would be nodeflation. What’s actuallyhappened is that countriesaround the world have not been able to adjust asquickly as they need to andtherefore we’re faced withexcess supply situations,particularly with excess orimmobile labor and that isthe source of deflation.

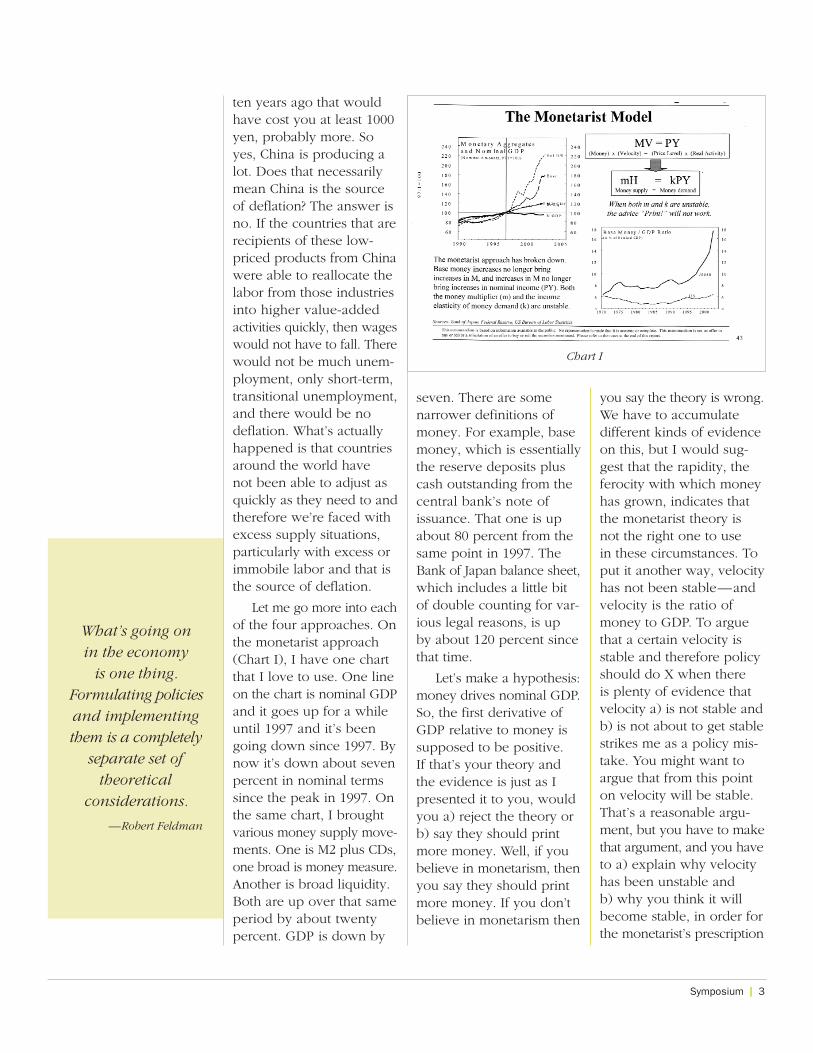

Let me go more into eachof the four approaches. Onthe monetarist approach(Chart I), I have one chartthat I love to use. One lineon the chart is nominal GDPand it goes up for a whileuntil 1997 and it’s beengoing down since 1997. Bynow it’s down about sevenpercent in nominal termssince the peak in 1997. Onthe same chart, I broughtvarious money supply move-ments. One is M2 plus CDs,one broad is money measure.Another is broad liquidity.Both are up over that sameperiod by about twentypercent. GDP is down by

seven. There are some narrower definitions ofmoney. For example, basemoney, which is essentiallythe reserve deposits pluscash outstanding from thecentral bank’s note ofissuance. That one is upabout 80 percent from thesame point in 1997. TheBank of Japan balance sheet,which includes a little bitof double counting for var-ious legal reasons, is up by about 120 percent sincethat time.

Let’s make a hypothesis:money drives nominal GDP.So, the first derivative ofGDP relative to money issupposed to be positive. If that’s your theory andthe evidence is just as Ipresented it to you, wouldyou a) reject the theory orb) say they should printmore money. Well, if youbelieve in monetarism, thenyou say they should printmore money. If you don’tbelieve in monetarism then

you say the theory is wrong.We have to accumulate different kinds of evidenceon this, but I would sug-gest that the rapidity, theferocity with which moneyhas grown, indicates thatthe monetarist theory isnot the right one to use in these circumstances. Toput it another way, velocityhas not been stable—andvelocity is the ratio ofmoney to GDP. To arguethat a certain velocity isstable and therefore policyshould do X when there is plenty of evidence thatvelocity a) is not stable andb) is not about to get stablestrikes me as a policy mis-take. You might want toargue that from this pointon velocity will be stable.That’s a reasonable argu-ment, but you have to makethat argument, and you haveto a) explain why velocityhas been unstable and b) why you think it willbecome stable, in order forthe monetarist’s prescription

What’s going on in the economy

is one thing.Formulating policiesand implementingthem is a completely

separate set of theoretical

considerations.

—Robert Feldman

Symposium 3

Chart I

to be correct. This is whatyou gain by working withtheoretical framework. Youknow what you have toexplain. That doesn’t nec-essarily mean monetarismis the wrong theory, but itmeans you’ve got some realwork to do. I don’t like thatapproach, because I thinkit’s inconsistent with theevidence.

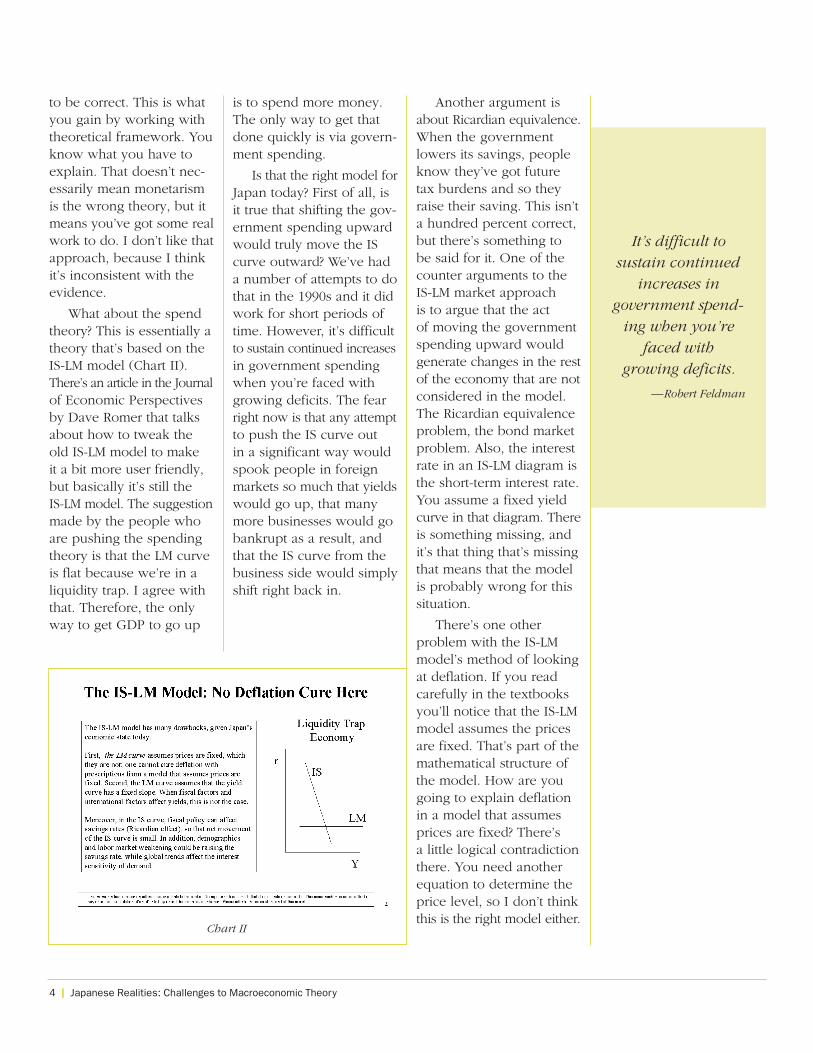

What about the spendtheory? This is essentially atheory that’s based on theIS-LM model (Chart II).There’s an article in the Journalof Economic Perspectivesby Dave Romer that talksabout how to tweak theold IS-LM model to make it a bit more user friendly,but basically it’s still the IS-LM model. The suggestionmade by the people whoare pushing the spendingtheory is that the LM curveis flat because we’re in aliquidity trap. I agree withthat. Therefore, the onlyway to get GDP to go up

is to spend more money.The only way to get thatdone quickly is via govern-ment spending.

Is that the right model forJapan today? First of all, isit true that shifting the gov-ernment spending upwardwould truly move the IScurve outward? We’ve hada number of attempts to dothat in the 1990s and it didwork for short periods oftime. However, it’s difficultto sustain continued increasesin government spendingwhen you’re faced withgrowing deficits. The fearright now is that any attemptto push the IS curve out in a significant way wouldspook people in foreignmarkets so much that yieldswould go up, that manymore businesses would gobankrupt as a result, andthat the IS curve from thebusiness side would simplyshift right back in.

Another argument isabout Ricardian equivalence.When the governmentlowers its savings, peopleknow they’ve got futuretax burdens and so theyraise their saving. This isn’ta hundred percent correct,but there’s something to be said for it. One of thecounter arguments to theIS-LM market approach is to argue that the act of moving the governmentspending upward wouldgenerate changes in the restof the economy that are notconsidered in the model.The Ricardian equivalenceproblem, the bond marketproblem. Also, the interestrate in an IS-LM diagram isthe short-term interest rate.You assume a fixed yieldcurve in that diagram. Thereis something missing, andit’s that thing that’s missingthat means that the modelis probably wrong for thissituation.

There’s one other problem with the IS-LMmodel’s method of lookingat deflation. If you readcarefully in the textbooksyou’ll notice that the IS-LMmodel assumes the pricesare fixed. That’s part of themathematical structure ofthe model. How are yougoing to explain deflationin a model that assumesprices are fixed? There’s a little logical contradictionthere. You need anotherequation to determine theprice level, so I don’t thinkthis is the right model either.

It’s difficult to sustain continued

increases in government spend-

ing when you’refaced with

growing deficits.

—Robert Feldman

4 Japanese Realities: Challenges to Macroeconomic Theory

Chart II

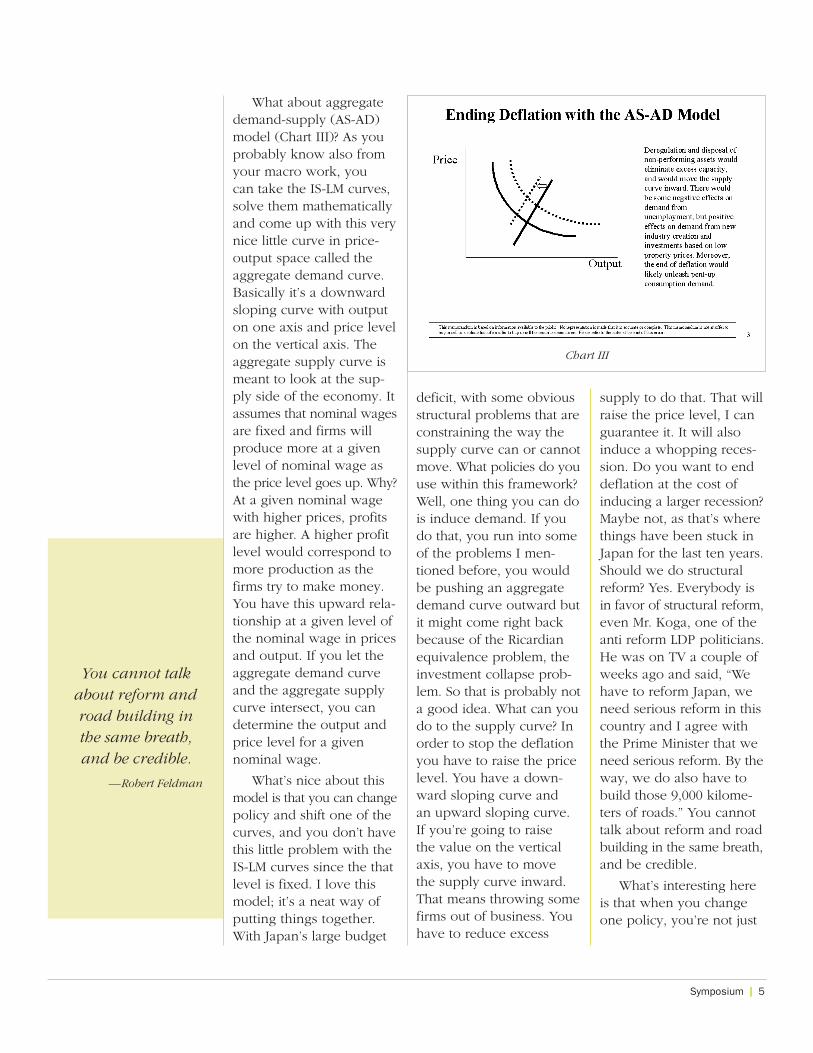

What about aggregatedemand-supply (AS-AD)model (Chart III)? As youprobably know also fromyour macro work, you can take the IS-LM curves,solve them mathematicallyand come up with this verynice little curve in price-output space called theaggregate demand curve.Basically it’s a downwardsloping curve with outputon one axis and price levelon the vertical axis. Theaggregate supply curve ismeant to look at the sup-ply side of the economy. Itassumes that nominal wagesare fixed and firms willproduce more at a givenlevel of nominal wage asthe price level goes up. Why?At a given nominal wagewith higher prices, profitsare higher. A higher profitlevel would correspond tomore production as thefirms try to make money.You have this upward rela-tionship at a given level ofthe nominal wage in pricesand output. If you let theaggregate demand curveand the aggregate supplycurve intersect, you candetermine the output andprice level for a givennominal wage.

What’s nice about thismodel is that you can changepolicy and shift one of thecurves, and you don’t havethis little problem with theIS-LM curves since the thatlevel is fixed. I love thismodel; it’s a neat way ofputting things together.With Japan’s large budget

deficit, with some obviousstructural problems that areconstraining the way thesupply curve can or cannotmove. What policies do youuse within this framework?Well, one thing you can dois induce demand. If youdo that, you run into someof the problems I men-tioned before, you wouldbe pushing an aggregatedemand curve outward butit might come right backbecause of the Ricardianequivalence problem, theinvestment collapse prob-lem. So that is probably nota good idea. What can youdo to the supply curve? Inorder to stop the deflationyou have to raise the pricelevel. You have a down-ward sloping curve and an upward sloping curve.If you’re going to raise the value on the verticalaxis, you have to move the supply curve inward.That means throwing somefirms out of business. Youhave to reduce excess

supply to do that. That willraise the price level, I canguarantee it. It will alsoinduce a whopping reces-sion. Do you want to enddeflation at the cost ofinducing a larger recession?Maybe not, as that’s wherethings have been stuck inJapan for the last ten years.Should we do structuralreform? Yes. Everybody isin favor of structural reform,even Mr. Koga, one of theanti reform LDP politicians.He was on TV a couple ofweeks ago and said, “Wehave to reform Japan, weneed serious reform in thiscountry and I agree withthe Prime Minister that weneed serious reform. By theway, we do also have tobuild those 9,000 kilome-ters of roads.” You cannottalk about reform and roadbuilding in the same breath,and be credible.

What’s interesting hereis that when you changeone policy, you’re not just

You cannot talkabout reform androad building inthe same breath,and be credible.

—Robert Feldman

Symposium 5

Chart III

moving one curve. Typicallywe think of fiscal policy asmoving the demand curvebut nothing else. That’s notnecessarily true. You mightbe able, with certain struc-tural policies, to move thesupply curve inward as wehave to do by eliminatingexcess capacity, but therecan also be some changesthat would move the aggre-gate demand curve outward.What do I mean? Say youtake a structural reformpolicy that ends up sellinga lot of land. You push abunch of weak, probablybankrupt constructioncompanies into liquidation,and you sell the land at avery low price—you havea fire sale. What happensto the people who buy that land? Do they sit on it?Typically they’re going todo something with it. Therehave been cases of this inother countries where thepeople who buy the assetsat very good prices typi-cally have projects in mind.They build new buildings,they have new venturesand that generates demandin the economy.

William Seidman, who was the head of the Resolution TrustCorporation in the U.S.(the agency that liquidatedall the bad debt from theS&L crisis), told us abouthis experience in Texas.When he first went toTexas, he needed a body-guard because he wasgoing to sell land, and the people who owned the

land didn’t want to see theprice go down. He cameback a year later and hewas a magnificent herobecause he sold the land.The reason people lovedhim is that after he madethe first auction at a verylow price, he eliminatedsome of the inventoryoverhang in the land mar-ket. When the inventoryoverhang starts goingdown the guys who areleft in the market knowthat they’ve got to startbuying pretty soon or theprices are going to startgoing up on them. Theminute he started sellingland and we saw thetrough, then the landprices started going up.His first auction in July1991 in Houston fetchedabout twenty cents on thedollar. A year later it wassixty cents on the dollarand by the time the RTCwound up, they were get-ting above par on the landthat they sold. The pointI’m trying to make here isthat policies that appear tobe supply reducing canalso have positive effectson the demand side.

There are a few otherthings you can do. Thereare structural reform poli-cies, such as the specialeconomics zone idea thatthey’ve got going rightnow in the government inJapan, which is a prettygood one. We don’t usu-ally think of structuralreform as the way to createdemand but, in this case, it

would be. The point I’mtrying to make here is thatwe have to be a little moreflexible in the way we thinkabout policies. A singlepolicy is not necessarilyonly a demand side oronly a supply side policy.We have to get some kindof a sense of the balancebetween the two if we’regoing to look at how itaffects deflation. The hardpart of this is there’s not a lot of empirical evidencethat the AS-AD frameworkwould have the beneficialeffects that I’m talking about.There have been a coupleof little papers using somevery advanced techniquesto try to detect relativedemand and supply sideeffects from say monetarypolicy, but the techniquesare very advanced andthey’re a little bit dicey. I’m sure the guys whowere doing them werevery bright, but that does-n’t mean that the resultsare reliable. AS-AD is agreat theory and you cando a lot with it, but theevidence that it wouldreally work is not so strong.You just have to hold yourbreath and do it.

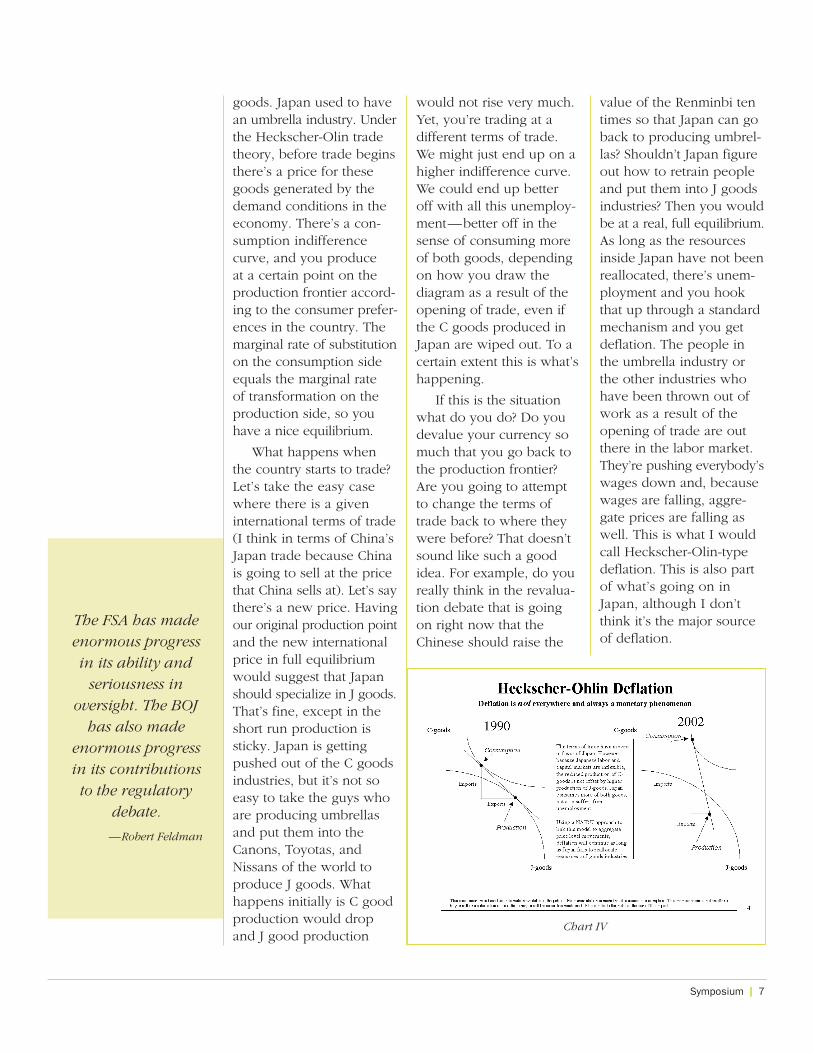

The final approach I’dlike to talk about is a tradeapproach, what I call theHeckscher-Olin model ofdeflation and trade (ChartIV). Let’s have two goods.We’ll call them “C” goodsand “J” goods. J goods arecapital intensive; C goodsare labor intensive. Japanproduces most kinds of

We have to be a little more flexible

in the way we thinkabout policies.

A single policy isnot necessarilyonly a demandside or only a

supply side policy.

—Robert Feldman

6 Japanese Realities: Challenges to Macroeconomic Theory

goods. Japan used to havean umbrella industry. Underthe Heckscher-Olin tradetheory, before trade beginsthere’s a price for thesegoods generated by thedemand conditions in theeconomy. There’s a con-sumption indifferencecurve, and you produce at a certain point on theproduction frontier accord-ing to the consumer prefer-ences in the country. Themarginal rate of substitutionon the consumption sideequals the marginal rate of transformation on theproduction side, so youhave a nice equilibrium.

What happens whenthe country starts to trade?Let’s take the easy casewhere there is a giveninternational terms of trade(I think in terms of China’sJapan trade because Chinais going to sell at the pricethat China sells at). Let’s saythere’s a new price. Havingour original production pointand the new internationalprice in full equilibriumwould suggest that Japanshould specialize in J goods.That’s fine, except in theshort run production issticky. Japan is gettingpushed out of the C goodsindustries, but it’s not soeasy to take the guys whoare producing umbrellasand put them into theCanons, Toyotas, andNissans of the world toproduce J goods. Whathappens initially is C goodproduction would dropand J good production

would not rise very much.Yet, you’re trading at a different terms of trade. We might just end up on ahigher indifference curve.We could end up better off with all this unemploy-ment—better off in thesense of consuming moreof both goods, dependingon how you draw the diagram as a result of theopening of trade, even ifthe C goods produced inJapan are wiped out. To acertain extent this is what’shappening.

If this is the situationwhat do you do? Do youdevalue your currency somuch that you go back tothe production frontier?Are you going to attemptto change the terms oftrade back to where theywere before? That doesn’tsound like such a goodidea. For example, do youreally think in the revalua-tion debate that is goingon right now that theChinese should raise the

value of the Renminbi tentimes so that Japan can goback to producing umbrel-las? Shouldn’t Japan figureout how to retrain peopleand put them into J goodsindustries? Then you wouldbe at a real, full equilibrium.As long as the resourcesinside Japan have not beenreallocated, there’s unem-ployment and you hookthat up through a standardmechanism and you getdeflation. The people inthe umbrella industry orthe other industries whohave been thrown out ofwork as a result of theopening of trade are outthere in the labor market.They’re pushing everybody’swages down and, becausewages are falling, aggre-gate prices are falling aswell. This is what I wouldcall Heckscher-Olin-typedeflation. This is also partof what’s going on inJapan, although I don’tthink it’s the major sourceof deflation.

The FSA has madeenormous progressin its ability and

seriousness in oversight. The BOJ

has also madeenormous progressin its contributionsto the regulatory

debate.

—Robert Feldman

Symposium 7

Chart IV

POLITICAL ECONOMY MODELS

Iwant to go a little bitinto some of the political

economy models that havebeen very helpful in think-ing about the situation inJapan. One is the prisoner’sdilemma. I’ve been tryingto analyze the relationshipbetween the Bank of Japanand the Financial ServicesAgency in terms of pris-oner’s dilemma. For a longtime there was a lot of badblood between the minis-ter of finance in the FSAon one side and the Bankof Japan on the other. Now,they are getting along okay,but there was an incidentthat triggered a lot of badblood in 1997, which wasthe bankruptcy of Yamaichi.At that time, the Ministry ofFinance, which is responsi-ble for the regulatoryfunction, knew they had a problem on their handswith Yamaichi. They wentto the Bank of Japan andsaid, “It’s okay, lend it somemoney, give them somespecial lending and it willrevive. You can trust usthat it’s okay to make theseloans.” Well, it wasn’t okay.Moreover, from the storiesI’ve heard at least, the MOFknew that it wasn’t okayand when it came time for the BOJ to go back tothem and say, “Look, youtold us it was okay, but it wasn’t. Why don’t youmake good the losses thatwe incurred on this?” theMOF response, so the storygoes, was “No, you made

the loan.” There was nowillingness to take respon-sibility for poor oversight.That makes it difficult tohave a quiet conversation,and things went downhillafter that. They are betternow. The FSA has madeenormous progress in itsability and seriousness inoversight. The BOJ has alsomade enormous progressin its contributions to theregulatory debate. The BOJmade some mistakes. TheAugust 2000 rate hike bythe Bank of Japan was aterrible mistake, and sothere is plenty of reasonfor people to argue witheach other about what wasgoing on. Look at this as a prisoner’s dilemma situa-tion simply because bothsides would like to do theright thing, but they won’tdo the right thing becausethe other guy has also gotto do the right thing inorder for the whole thingto succeed. If I do the rightthing and the other guydoesn’t, then I lose and hewins. Therefore, I’m notgoing to do the right thinguntil I’m sure he’s going todo the right thing, but he’snot going to tell me he’sgoing to do the right thingbecause he doesn’t knowif I’m going to do the rightthing.

What kind of strategydo you want to adopt in a prisoner’s dilemma gamein order to get a string of success? There’s somebrilliant work by a mathe-matician/political scientist

at the University of Michigannamed Axelrod. Axelrodposed an iterated prisoner’sdilemma, and he got math-ematicians from around theworld to submit strategiesthat they thought would be successful in such agame. The one that wonthe first round of the con-test was submitted by anacademic in Canada,Anatole Rappaport, whosubmitted a very simple tit-for-tat strategy. It involvescooperating on the firstmove and then, on everymove after that, you dowhat the other guy did onthe previous move. Thus,the other guy figures outthat if he does somethingbad, he’s going to get hitthe next time and so hedoes something good. Itturns out that this is thestrategy that won the firstround of the contest.

Axelrod published the results and said, “Let’shave a second round ofthe tournament.” Rappaportsubmitted exactly the samestrategy, and he won again.I think that what has beengoing on between the BOJand the FSA (and betweenother parts of the govern-ment as well) is a badequilibrium, tit-for-tat iter-ated prisoner’s dilemma.How do you break thatcycle? You have a littlecoordination. The essenceof the prisoner’s dilemmagame is that these guys aresitting in separate cells andcan’t talk to each other. Ifsomebody can get them to

Risk appetite needs to be

encouraged bynegative incentives.

—Robert Feldman

8 Japanese Realities: Challenges to Macroeconomic Theory

talk to each other andcooperate then you shouldget out of this bad equilib-rium. This is precisely whatPrime Minister Koizumi didwhen he a) forced the FSAinto the special inspections,and b) appointed Takenakaas the FSA Minister. It’smuch easier for them tocooperate. It’s not perfect,There are some at the BOJwho don’t like the wayTakenaka is talking aboutinflation targeting; they’removing away from thatanyway, but it is much eas-ier and Koizumi has cometo play a coordinating role.At his press conference on September 30th whenhe changed the cabinet,Koizumi repeatedly empha-sized that the FSA and BOJshould work together. Herepeated that admonitionfive times during the courseof the press conference. I suggest this is a prettygood model.

There are two moremodels I want to mention.One is the CRIC (Crisis-Response-Improvement-Complacency) Cycle, whichis a Morgan Stanley inven-tion. It started out as a wayto convince New York notto downsize the Tokyooperation in 1997. Whenthe BOJ and the Ministry of Finance were arguingabout Yamaichi, our man-agement in New York wassaying, “Things out theredon’t look so good. We justlost a couple of big banks,we just lost a big securitiesfirm, the economy doesn’t

look so hot, we just had the Asian crisis, let’sdownsize the office.” Themanaging directors in Tokyogathered and said, “No, wedon’t like that idea. This isour opportunity to expandthe business, because thereare a lot of things we cando to contribute to Japanto help out tremendouslyin this kind of environ-ment. We shouldn’t bedownsizing. We should be upsizing.” How do youmake that case to theseguys in New York? TheTokyo group had an inter-nal conference and cameup with a set of axes todescribe what they weregetting at. The vertical axisis growth, and the horizon-tal axis is reform. Whatkind of combination ofgrowth and reform are wegoing to have? What kindof business plan should we have? The idea in 1997was, “We have low growth,we have slow reform. Thisis not a good position.However, Japan will reactand, because of their reac-tions, they will do the rightthings and we will end upwith high growth and highreform. There’s a tremen-dous business chance inthis transition process. Youshould raise the resourceswe have in Tokyo.” Itworked. At the end of1997, the office was 600people. Three years later itwas 1,400. We made a lotof money in the process.

The CRIC cycle emergedas follows. I came to the

firm in early 1998, inheritedthe axes and, while walkingdown the street past theImperial Palace one day,an idea popped into myhead: “We haven’t gonefrom point A to point B. In the last ten, fifteen years,we’ve been going in circles.We’ve gone from crisis toresponse, to improvement,to complacency. Guesswhat happens after com-placency? You go rightback into crisis. This is notat all unique to Japan. Quitethe contrary—you canexplain many things aboutpolicy in the United Statesand in developing coun-tries through a crisis likethis. Why does it exist?

Who’s heard of a hogcycle in microeconomics?In the 1930s, for a numberof agricultural products, itwas observed that priceshad a tendency to fluctuatea lot. This meant that if theprice of hogs was high oneyear, everybody said, “Hey,let’s raise hogs.” Then a yearor two later the price ofhogs was very low becauseeverybody was bringingthem to the market, andthere was oversupply.Everybody says “Ah, forgetthis, I’m out of this busi-ness.” A couple of yearslater they are right back upagain. You have this cycleof supply versus demandthat generated huge pricefluctuations. The key tothis is that there is a lagbetween supply anddemand. Demand is con-temporaneous. Demand

I contend that this CRIC Cycle

has been animportant way

to explain what’shappened in Japan

over the last ten or twelve years.

—Robert Feldman

Symposium 9

today is high, then pricesare low. Demand today is low and prices are high.Very simple, normal con-temporaneous demandcurve. Supply takes time.As a U.S. AgricultureDepartment official oncesaid, “It takes two years to raise a 24-month heifer.”The lag between demandand supply is what gener-ates the cycle. That’s whatis interesting about hogcycle.

Let’s think about reformpolicy. We know that there’sa lag between the imple-mentation of reform and its effect on the economy.Sometimes it’s relativelyquick. In 1994, Japanderegulated the ownershipof mobile telephones. Untilthat point, if you wanted amobile phone you had torent one from NTT. Themarket didn’t expand verymuch because NTT wasn’tinterested in mobile phones.Then, the governmentderegulated it. It took a little time for deregulationto take effect, but when itdid by about 1996, it hadan explosive effect. Thepolicy response curve is alittle different. If the stockmarket goes down, peopleget scared and they dosomething. That’s prettyquick. Or, if the economyis sliding, then you tend toreact pretty quickly. I’mcontending here that thepolicy response line—wherethe better the economy is, the less response youget—is contemporaneous,

and the response of theeconomy to deregulation islonger term. I’ve got my lag.

This is a hog cycle inpolicy. The economy doesbetter, people get compla-cent. They don’t have todo too much. The stockmarket is high. We don’tneed too much more. Youdon’t have to do too muchreform. The stock marketgoes down or the econ-omy gets weak and “Oh,now we have to do some-thing.” It is not necessarilyreform, sometimes it’s thebig fiscal package. The pointis that the policy responseis quick; the economicresponse is slow and thatgenerates a CRIC cycle.That is why we have it.

I contend that this CRICCycle has been an impor-tant way to explain whathas happened in Japanover the last ten or twelveyears. We have gone througha number of them. I wouldalso contend that they’vegotten shorter over the lastcouple of years. In fact, thefirst economic sort of pol-icy plan that Koizumi putout in June reflects this.One of the phrases inthere is that we have to“reform the process ofreform,” and what thatmeans is moving the policyresponse curve outward.That’s going to speed upthe cycle. I would claimright now, although mycolleagues in some casesdisagree with me on this,that we have a faster CRIC

cycle, probably a narrowerone, and that things areactually getting a little bitbetter in that respect.

Japan’s dilemma isthat they’ve got lotsof savings that theworld can use butthere isn’t a mech-anism to get them

into the rest of the world.

—Hugh Patrick

10 Japanese Realities: Challenges to Macroeconomic Theory

Symposium 11

Discussion

HUGH PATRICKDirector, Center on JapaneseEconomy and Business

Ithink we all agree thatthe fundamental prob-

lem for Japan is lack ofaggregate demand and, asDr. Feldman has explained,essentially there are twoways of dealing with that.One is to try to stimulatedemand through fiscal andmonetary measures. Theother is to try to handle the problems of excesssupply by structural reform,liquidation of insolventcompanies, freeing upresources that are now usedinefficiently into more effi-cient uses. This will have asupply contracting effect inthe short run, but will havea supply enhancing effectin the longer run. If we ask,“Why is there inadequatedemand at the aggregatelevel?” we’re really askingthe question, “Why is thedomestic savings rate higherthan the domestic invest-ment rate?” That’s what the standard macro-model

stresses. It also says that oneway to handle this is toexport your savings. Whatdo we mean by “exporting”savings”? We mean that a country runs a larger current account surplus,and, probably, to do that acountry has to cut its prices,and that is usually done byhaving the exchange ratedepreciate.

If you are Singapore,you can run a currentaccount surplus that is ten to fifteen percent ofGDP and nobody cares.Why? You’re small; it has a negligible impact. If youare a large economy in the19th century, say England,you can run a currentaccount surplus of ten per-cent of GDP because youcontrol a lot of colonies. If you are a large economyin the late 1990s, you don’thave that degree of politi-cal freedom. If a countrystarts to run a larger cur-rent account surplus whatthis means is that somecountries are absorbingadditional imports from,say Japan, and that leadsto a political reaction andretaliation by the importingcountries. The only retalia-tion that really counts comesfrom the United States andthe European Union.

Japan’s dilemma is thatthey generate lots of sav-ings that the world can usebut there isn’t a mechanismto get them into the rest of the world, because thecounterpart of exporting

the savings is exporting alot of goods and services.Japan is a large economyand because the gapbetween domestic and savings and investment is so large the net exportgrowth is internationallyunacceptable politically.This is another dimensionof the economic policymodels which say thateven though it would liketo, Japan could not simplyhave the exchange ratedepreciate enough to gen-erate sufficient aggregatedemand and at the sametime not face retaliation.We’re talking about anexchange rate some peo-ple say should be 180 yenor 200 yen to the dollar.We don’t know what it isprecisely, but we do knowthat it’s far more than theUnited States would accept.That’s a terrible dilemmafor Japan.

One might say in theintermediate run, the ques-tion is whether businessinvestment demand isgood enough to sustaineconomic growth in Japanat the rate that would allowJapan to achieve two tothree percent growth ayear? Two to three percenta year growth doesn’trequire business invest-ment of fifteen percent. It requires much less, if it’sgoing to be used efficiently.Indeed, part of Dr. Feldman’swork in the past pointedout the return on assetshas declined so much overthe last twenty years in

The real problemnow is not

the household savings rate, it’s

the corporate savings rate.

—Hugh Patrick

Japan, and that suggeststhat business investmentopportunities really arequite limited in Japan. Partof those business invest-ment opportunities may be precluded by variousforms of regulation and thelack of ability to enter newmarkets within Japan. Ifyou believe that structuralreform is important, youwould say what Japanshould do is deregulateand reduce barriers so asto make it easier for firmsto enter new markets. Thatis the essence of the struc-turalist argument and it ofcourse has a lot of validity.

In the intermediate run,Japan also ought to reduceits private savings rate. Thequestion is how do you dothat. Everybody points tothe fact that householdsavings are so incrediblyhigh in Japan. Well, the

reality is that the Japanesehousehold savings rateshave declined graduallyfrom their peak in the mid-1970s. They flattened outduring the 1990s and beganto decline again recently.The real problem now isnot the household savingsrate, it’s the corporate savingsrate, because companiesare saving money to payoff debts and because theydon’t want to distributetheir profits as increaseddividends any more thanthey do in the United States.Last year, for the first time,the corporate sector was anet saver, saving more thanit invested. That’s a majortransformation.

How could policymakersget the Japanese economyto save less? One way mightbe to look precisely at corporate savings behavior,corporate profitability.

We don’t want to harmprofitability; we want firmsto be efficient and prof-itable. One policy might be to say that all dividendsthat are paid by companieswould come out of pretaxincome and would not betaxed. That would be anincentive for companies to distribute profits andsome of that would go into households and beconsumed. That might bean intermediate measure.

Typically, economistslike to think of “either thisor that”. Japan is in suchan unprecedentedly badsituation, one which wereally don’t know how to solve, but you have tomove forward on all fronts.I believe Japanese policy-makers should do everything.There should be monetarystimulus. I don’t think thatit’s going to likely lead tomuch increase in demand,but you have to try that. Ibelieve in the short run infurther fiscal stimulus toboot-start the economyand get it going again. Ialso believe in the impor-tance of structural reformsto free up resources, real-locate them and get to abetter growth situation.Japan needs to move for-ward on all these fronts.Then the question comesto the political economyproblems. It seems to methat the great strength ofeconomics is that we’reconcerned at the macrolevel about the optimal,full use of resources. At

Last year, for the first time,

the corporate sectorwas a net saver,

saving more than investors.That’s a majortransformation.

—Hugh Patrick

12 Japanese Realities: Challenges to Macroeconomic Theory

Left to right: David Weinstein, Carl S. Shoup Professor of theJapanese Economy, Department of Economics and AssociateDirector for Research, Center on Japanese Economy and Business;Janet Garland, Program Administrator, The Mitsui USA Foundation;Robert Feldman, Chief Economist and Managing Director,Morgan Stanley Japan, Ltd; Professor Hugh Patrick, Director,Center on Japanese Economy and Business

the micro level, we’re concerned about the efficientuse of resources. We’re notconcerned about the distri-butional effects of policiesdesigned to achieve full andefficient use of resources.An optimal policy is goingto create net winners forsociety, but within thatthere are going to be los-ers. Political scientists areconcerned about distribu-tion and how that works. It works through the politi-cal process of a democracyas well as through the marketplace. It’s the loserswho tend to have organizedand concentrated politicalpower; it’s the farmers, it’s the workers for NTT, ahighly effective union, it’sthe industrialists in thoseindustries that are no longercompetitive. All countrieshave these distributionalissues.

Part of the politicaleconomy gain is how toconstruct payoffs that ade-quately compensate, or atleast seem to compensatethe losers? For instance, in agriculture Japan couldfairly easily move to a sys-tem of world market priceswith zero tariffs if it wouldguarantee that all farmfamilies today would main-tain a middle class incomeand do that until the farm-ers die. That is a long runpolicy to solve the agricul-tural problem. It would be much cheaper if reformwere done now; we wouldend up with a more effi-cient resource allocation.

It’s very hard to come upwith those kinds of ideasin a political environmentwhere short-term paincounts much more thanlong-term gain. That seemsto be the political gridlockthat Japan is in, and insome sense, that politicalgridlock is the FeldmanCrisis-Response-Improvement-Complacency Model. Itreminds me of the literatureon why developing coun-tries would never develop.Decades ago, it was calleda “low level equilibriumtrap.” The idea was that therewould be a cycle in whichlow-income economieswould grow, would seetheir populations grow and that would eat up thegrowth and you go back toa low per capita income—a Malthusian argument.

Japan is in a high levelequilibrium trap and thequestion is, how can theresponses and the improve-ments be made sufficientlystrong to overcome theinevitable complacency, so that rather than return-ing to the same level, theeconomy goes upwardover time to improvedvariations of this cycle?What you need is not onlythe cyclical theory, but along run theory of how tomove this process forward.

DAVID WEINSTEINCarl S. Shoup Professor of the Japanese Economy,Department of Economics;Associate Director forResearch, Center on JapaneseEconomy and Business

This year I am at theFederal Reserve Bank

and there has been plentyof discussion about thenormative question of whatshould happen. One of thequestions that I always liketo ask is the positive ques-tion of what will happen.It strikes me that one ofthe driving variables that isgoing to force everythingto move, which we did nottalk about that much, is thedeficit. The deficit is bal-looning at a rate of tenpercent of GDP per year,and ultimately that is goingto be solved either throughhigher taxes, lower spend-ing or monetization. Thequestion is what is going todrive the equilibrium—willyou end up with inflation?What is your forecast? Infive years from now whereis the economy going to be?

One of the drivingvariables that isgoing to force

everything to move... is the deficit.

—David Weinstein

Symposium 13

Feldman: There will notbe an outright monetiza-tion because that is essen-tially an inflation tax. Thereason I say it’s unlikely tohappen is that the votingdemographics would argueagainst it. The old peopleown all the money. That’strue in the United States as well. They also, by far,have the heaviest voterturnout. If the people whohave the heaviest voterturnout are the ones whohave the biggest interest innot seeing an inflationaryresult, they will probablyvote in that fashion. Mysense is the political incen-tives for the monetizationsolution are probablyweaker in Japan than theyare anywhere else.

That does leave us witha question of what the peo-ple are going to vote for.I’ve done a few calcula-tions and I go around andask large Japanese audiencesto make some decisions on the basis of some fiscalcalculations. I just did thisa couple of days ago. Thecalculation is very simple.If we’re not going to havemonetization, that leavesus with two choices. Wecan either raise taxes orcut spending. If we aregoing eliminate the deficitand stabilize the ratio ofdebt to GDP, we wouldneed a swing in the fiscaldeficit of approximately 50 trillion yen, the otherso-called primary surplus.That’s ten percent of GDP.How are we going to do

this? Are we going to do it via 50 percent spendingcuts, 50 percent tax hikes?Are we going to do it via60 percent spending cuts,40 percent tax hikes; 70percent spending cuts, 30 percent tax hikes, etc.?What’s the breakdown? Bythe way, if we eliminatedall public works, includingnot building any roads oreven fixing the old ones,you would raise a little morethan half of the necessaryfunds. If you’re going totake out spending, youhave to take out corrup-tion, and you have to hitmedical care, pensions, andall kinds of other items. Itturns out that every place Ihave asked this to Japaneseaudiences, they vote for70/30 very strongly. Theyare saying, “We don’t mindif our taxes go up, but wedon’t want the taxes to goup until the spending iscut.” That’s the message,and I think that is preciselythe message that this par-ticular administration hastried to push forward.

We now have the anti-reform guys out with theirnew study on alternativesto the Koizumi program.That’s okay, we need allthe ideas we can get. Theiridea is we need more wel-fare spending and roads.How are you going toaddress this deficit issue ifyou’re going to do all thatspending? They don’t talkabout that. Moreover, it’scompletely out of sympa-thy with what the people

are thinking right now. My sense is that over time,with election results com-ing in (and Japan has amore vibrant democracytoday than in the past), Ithink the voters are makingtheir opinions very clear.Politicians do what the vot-ers tell them because theyknow that if they don’t, theyget thrown out and that ismore true today than it’sbeen in the past. Over timewe will end up with a verylarge decrease of publicworks spending. We willlook at some constraintson pension payouts, con-straints on medical payouts,better information sharing,and wholesale deregula-tion in order to lower thecosts of doing business.Are we going to need a fiscal crisis with a sharpspike in volume before thathappens? It might have tohappen that way—that’smy best guess.

Q: Is there a good economicmodel that explains howto raise people’s riskappetite?

Feldman: I don’t know ofany economic models thattell how to change a riskappetite. All I remember ispeople assuming that thereis a risk aversion coeffi-cient that individuals haveand that’s it. So I can’tgive you an economic theory answer to the ques-tion, but I can give you an answer that comes froma friend of mine who isactually a Japan economist

We’ve got to weanpeople away fromthe notion that the

government isalways going to be

there to makewhole anybody

who loses from anyprocess. It’s bad

education.

—Robert Feldman

14 Japanese Realities: Challenges to Macroeconomic Theory

scholar, Serguey Braguinsky.I first met Serguey in 1990in Japan. I said it’s absolutelyastonishing what theRussians accomplishedduring the Soviet era in onesense, because you had allthese magnificent achieve-ments in space, science,computer science andmathematics, just amazingachievements in a systemthat had absolutely noincentive whatsoever forpeople to achieve. If youdo something good yougot nothing. Why did theydo all these great things?His answer was, “If thenegative incentives arestrong enough people will perform.”

I think risk appetiteneeds to be encouraged by negative incentives. If you give everybody along-term, complete guar-antee on the value of theirdeposits in a bank, even at zero interest rate, whyshould they bother takingany risk? It was only whenthe first tier of the depositguarantees was removed,almost two years, that peo-ple began to take a littlebit more risk in their port-folios. There was a bigrush into Tokyo of moneyfrom other regions. Richpeople from outside Tokyospent a lot of money buy-ing high-end condominiumsin Tokyo and in some otherprojects around town. Whathappened was very simple.Initially, they had a low-risk,low-return of deposit onone hand and a high-risk,

high-return real estateinvestment on the other.Because of their risk appetitethey decided to stay withthe low-risk, low-returnasset, particularly becauseyou never really know whatyou’re buying when youbuy real estate. With theremoval of full depositinsurance they were thenfaced with a choice betweena different set of character-istics. You still had thehigh-return, high-risk assetin the real estate marketbut then you had a high-risk, low-return bankdeposit. That’s a negativeincentive. So they boughtcondominiums. Don’t be so nice. We have towean people away fromthe notion that the govern-ment is always going to bethere to make whole any-body who loses from anyprocess. It is bad education.

The better capitalized the

financial system,the more willing

people will be to take risks on

foreign assets andthat’s when the Yen will start to weaken.

—Robert Feldman

Symposium 15

Robert Feldman, Chief Economist and Managing Director,Morgan Stanley Japan, Ltd

EDITOR

Joshua Safier

Associate Director

Center on

Japanese Economy and Business

ASSOCIATE EDITOR

Dr. Tomoko Sugiyama

Program Consultant

Center on

Japanese Economy and Business

PHOTOGRAPHY

Joseph Piniero

DESIGN/PRODUCTION

Melanie Conty

CENTER ON JAPANESE

ECONOMY AND BUSINESS

Columbia Business School

321 Uris Hall

Mail Code 9155

3022 Broadway

New York, NY 10027

Phone: (212) 854-3976

Fax: (212) 678-6958

Email: [email protected]

http://www.gsb.columbia.edu/japan