Embed Size (px)

Citation preview

Ivan PerkovicHead of Economic Research

Economy Update

Economic Analysis, Market Intelligence & Evaluation – where it is all going?

June 2011

Business Support Briefing Session

Overview

1. Economy Update– Output– Prices and inflation– Labour market – Confidence– Outlook– Key challenges ahead

2. SEEDA Economic Analysis, Market Intelligence and Evaluation– What we did and – Where it is all going

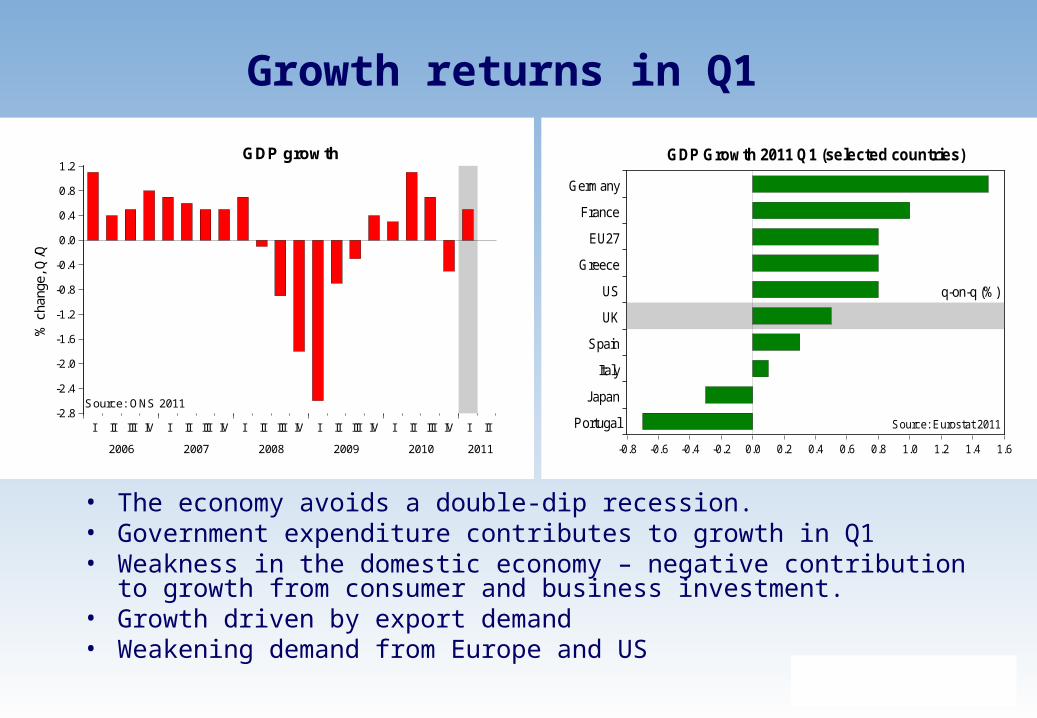

• The economy avoids a double-dip recession. • Government expenditure contributes to growth in Q1• Weakness in the domestic economy – negative contribution to growth

from consumer and business investment.• Growth driven by export demand• Weakening demand from Europe and US

Growth returns in Q1

-2.8

-2.4

-2.0

-1.6

-1.2

-0.8

-0.4

0.0

0.4

0.8

1.2

I II III IV I II III IV I II III IV I II III IV I II III IV I II

2006 2007 2008 2009 2010 2011

GDP growth

% c

hang

e, Q

/Q

Source: ONS 2011

-0.8 -0.6 -0.4 -0.2 0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6

Germany

France

EU27

Greece

US

UK

Spain

Italy

Japan

Portugal

GDP Growth 2011 Q1 (selected countries)

Source: Eurostat 2011

q-on-q (%)

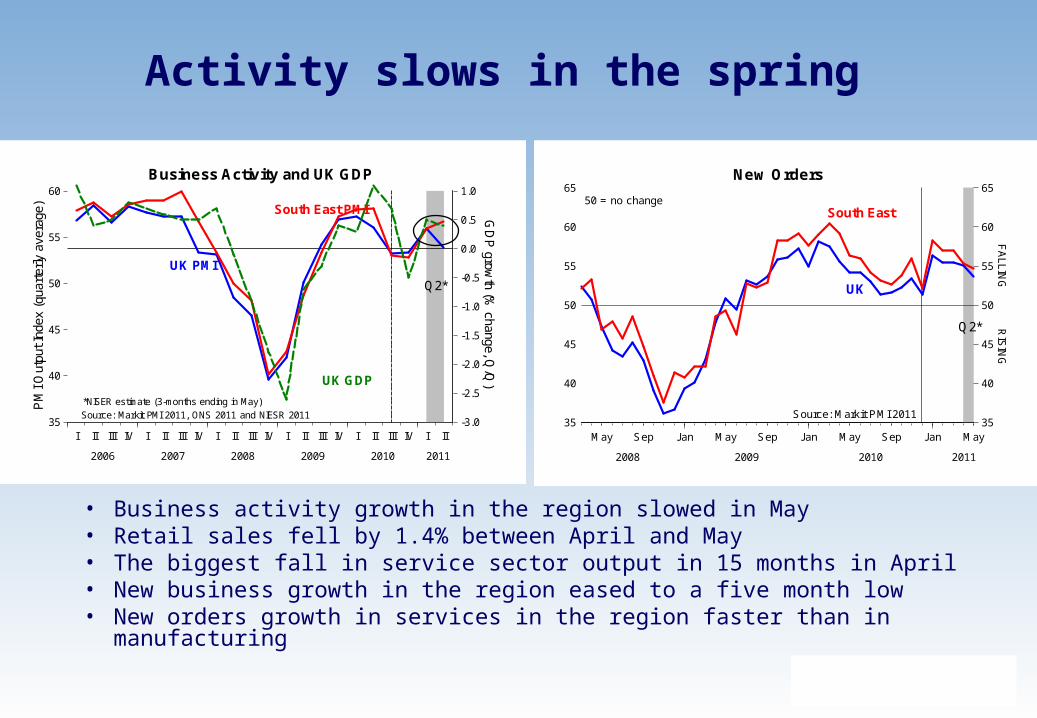

• Business activity growth in the region slowed in May• Retail sales fell by 1.4% between April and May• The biggest fall in service sector output in 15 months in April• New business growth in the region eased to a five month low• New orders growth in services in the region faster than in manufacturing

Activity slows in the spring

35

40

45

50

55

60

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

I II III IV I II III IV I II III IV I II III IV I II III IV I II

2006 2007 2008 2009 2010 2011

UK GDP

South East PMI

UK PMI

PM

I Out

put I

ndex

(qu

arte

rly a

vera

ge)

GD

P grow

th (% change, Q

/Q)

Business Activity and UK GDP

Source: Markit PMI 2011, ONS 2011 and NIESR 2011

Q2*

*NISER estimate (3-months ending in May)

35

40

45

50

55

60

65

35

40

45

50

55

60

65

May Sep Jan May Sep Jan May Sep Jan May

2008 2009 2010 2011

FA

LLING

RIS

ING

50 = no change

New Orders

South East

UK

Source: Markit PMI 2011

Q2*

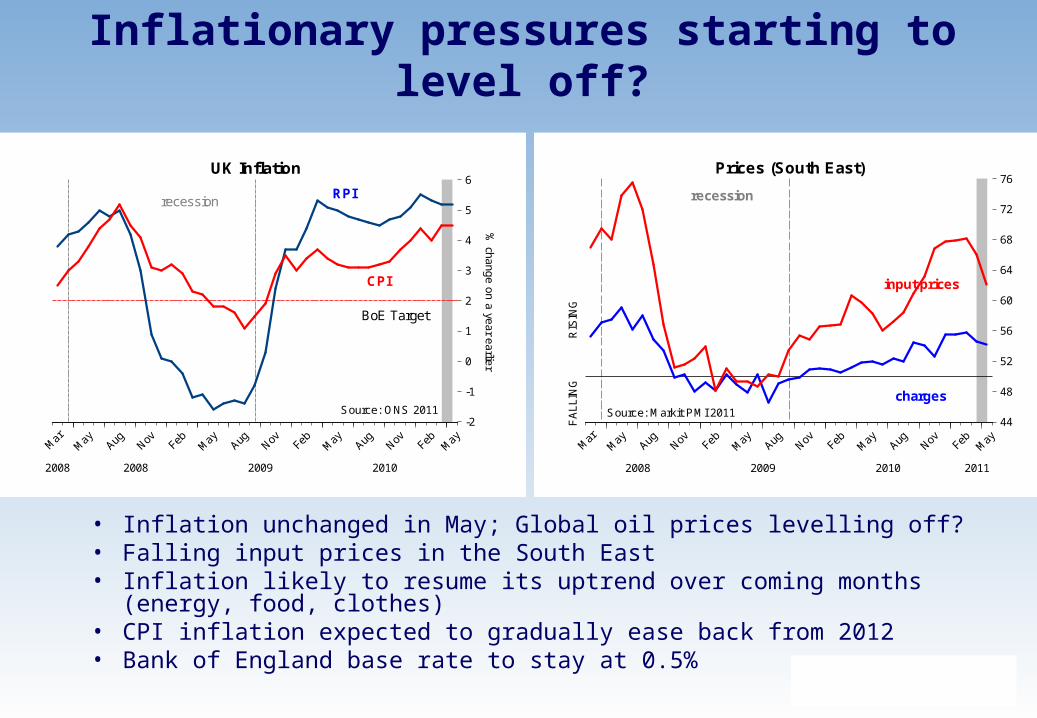

• Inflation unchanged in May; Global oil prices levelling off?• Falling input prices in the South East • Inflation likely to resume its uptrend over coming months (energy, food,

clothes)• CPI inflation expected to gradually ease back from 2012• Bank of England base rate to stay at 0.5%

Inflationary pressures starting to level off?

-2

-1

0

1

2

3

4

5

6

-2

-1

0

1

2

3

4

5

6

Mar

May Aug Nov Feb M

ay Aug Nov Feb May Aug Nov Feb M

ay

2008 2008 2009 2010

% ch

an

ge

on

a ye

ar e

arlie

r

Source: ONS 2011

RPI

CPI

UK Inflation

BoE Target

recession

44

48

52

56

60

64

68

72

76

44

48

52

56

60

64

68

72

76

Mar

May Aug Nov Feb M

ay Aug Nov Feb May Aug Nov Feb M

ay

2008 2009 2010 2011

Prices (South East)

FA

LL

ING

RIS

ING

input prices

charges

recession

Source: Markit PMI 2011

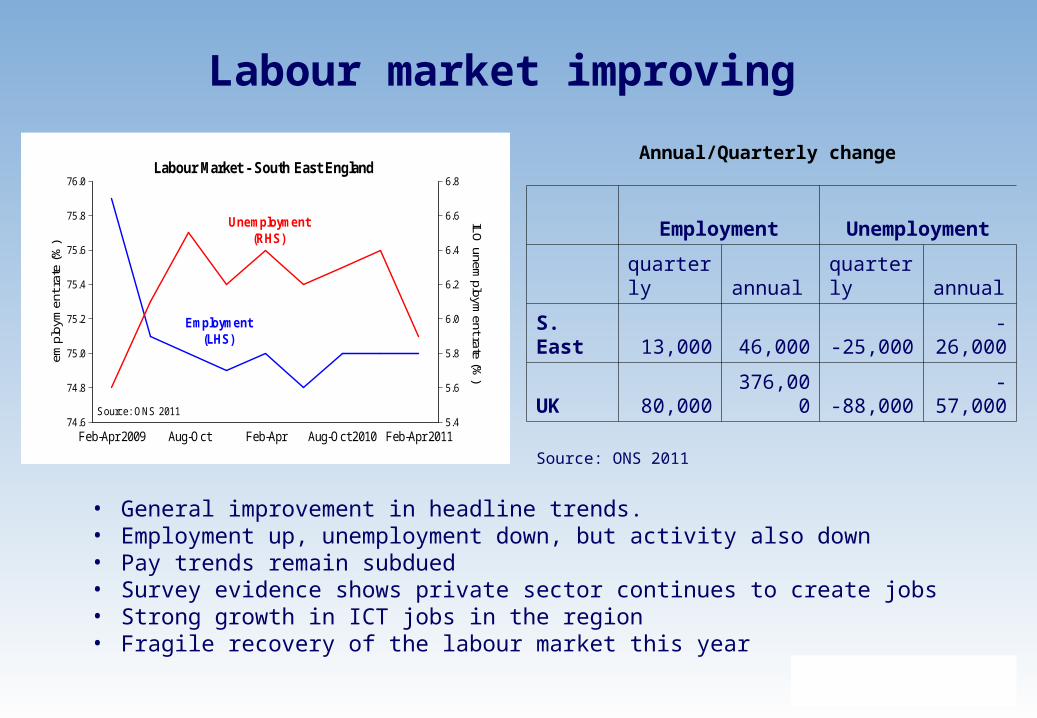

Labour market improving

• General improvement in headline trends.• Employment up, unemployment down, but activity also down • Pay trends remain subdued• Survey evidence shows private sector continues to create jobs• Strong growth in ICT jobs in the region• Fragile recovery of the labour market this year

74.6

74.8

75.0

75.2

75.4

75.6

75.8

76.0

5.4

5.6

5.8

6.0

6.2

6.4

6.6

6.8

Feb-Apr 2009 Aug-Oct Feb-Apr Aug-Oct 2010 Feb-Apr 2011

Employment(LHS)

Unemployment(RHS)

Labour Market - South East England

Source: ONS 2011

empl

oym

ent r

ate

(%)

ILO unem

ployment rate (%

)

Employment Unemployment

quarterly annual quarterly annual

S. East 13,000 46,000 -25,000 -26,000

UK 80,000 376,000 -88,000 -57,000

Source: ONS 2011

Annual/Quarterly change

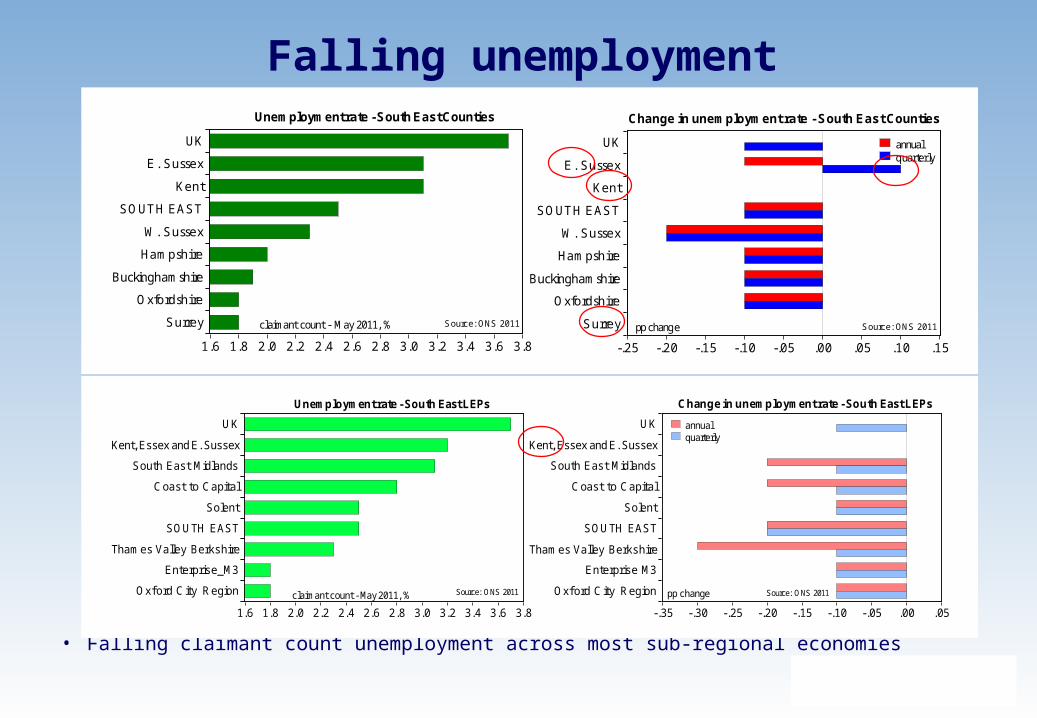

• Falling claimant count unemployment across most sub-regional economies

Falling unemployment

1.6 1.8 2.0 2.2 2.4 2.6 2.8 3.0 3.2 3.4 3.6 3.8

UK

E. Sussex

Kent

SOUTH EAST

W. Sussex

Hampshire

Buckinghamshire

Oxfordshire

Surrey Source: ONS 2011

Unemployment rate - South East Counties

claimant count - May 2011, %

-.25 -.20 -.15 -.10 -.05 .00 .05 .10 .15

UK

E. Sussex

Kent

SOUTH EAST

W. Sussex

Hampshire

Buckinghamshire

Oxfordshire

Surrey

annualquarterly

pp change Source: ONS 2011

Change in unemployment rate - South East Counties

1.6 1.8 2.0 2.2 2.4 2.6 2.8 3.0 3.2 3.4 3.6 3.8

UK

Kent, Essex and E. Sussex

South East Midlands

Coast to Capital

Solent

SOUTH EAST

Thames Valley Berkshire

Enterprise_M3

Oxf ord City Region Source: ONS 2011claimant count - May 2011, %

-.35 -.30 -.25 -.20 -.15 -.10 -.05 .00 .05

UK

Kent, Essex and E. Sussex

South East Midlands

Coast to Capital

Solent

SOUTH EAST

Thames Valley Berkshire

Enterprise M3

Oxf ord City Region

annualquarterly

Change in unemployment rate - South East LEPs

Source: ONS 2011pp change

Unemployment rate - South East LEPs

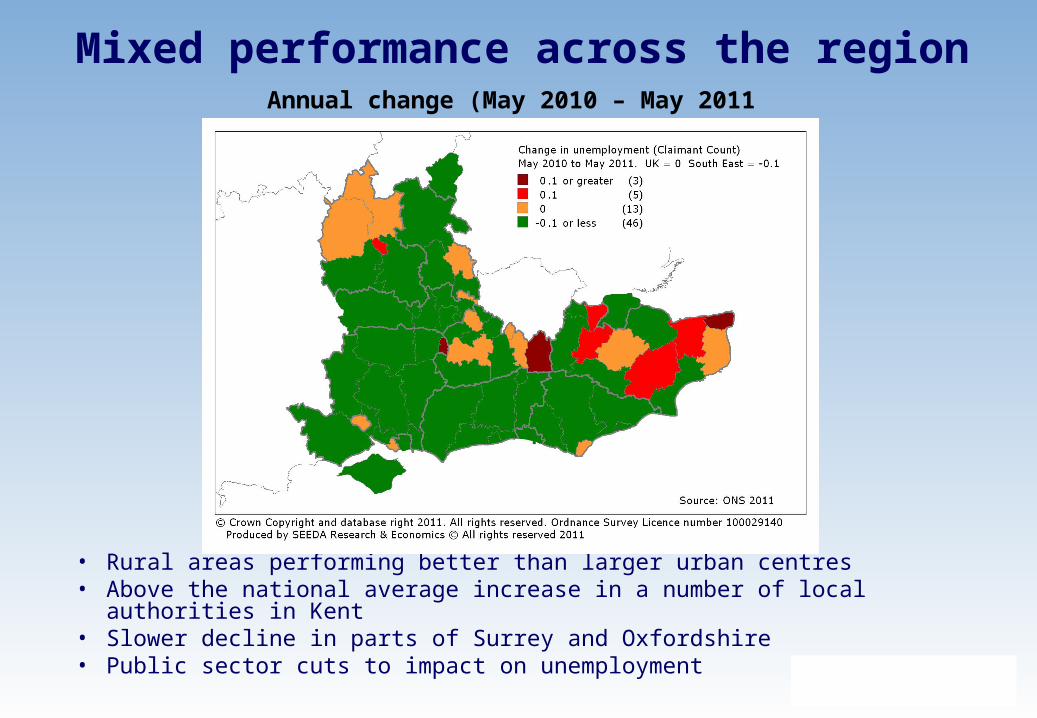

• Rural areas performing better than larger urban centres• Above the national average increase in a number of local authorities in Kent• Slower decline in parts of Surrey and Oxfordshire• Public sector cuts to impact on unemployment

Mixed performance across the regionAnnual change (May 2010 – May 2011

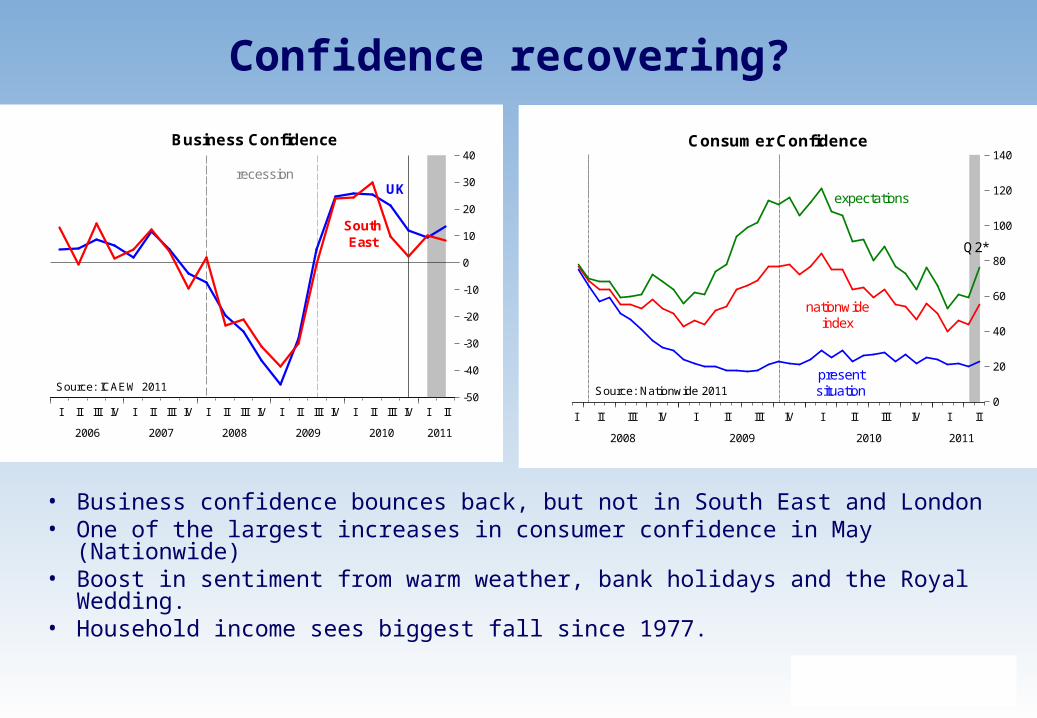

• Business confidence bounces back, but not in South East and London• One of the largest increases in consumer confidence in May (Nationwide)• Boost in sentiment from warm weather, bank holidays and the Royal

Wedding.• Household income sees biggest fall since 1977.

Confidence recovering?

-50

-40

-30

-20

-10

0

10

20

30

40

-50

-40

-30

-20

-10

0

10

20

30

40

I II III IV I II III IV I II III IV I II III IV I II III IV I II

2006 2007 2008 2009 2010 2011

SouthEast

UK

Business Confidence

Source: ICAEW 2011

recession

0

20

40

60

80

100

120

140

0

20

40

60

80

100

120

140

I II III IV I II III IV I II III IV I II

2008 2009 2010 2011

nationwideindex

presentsituation

expectations

Q2*

Consumer Confidence

Source: Nationwide 2011

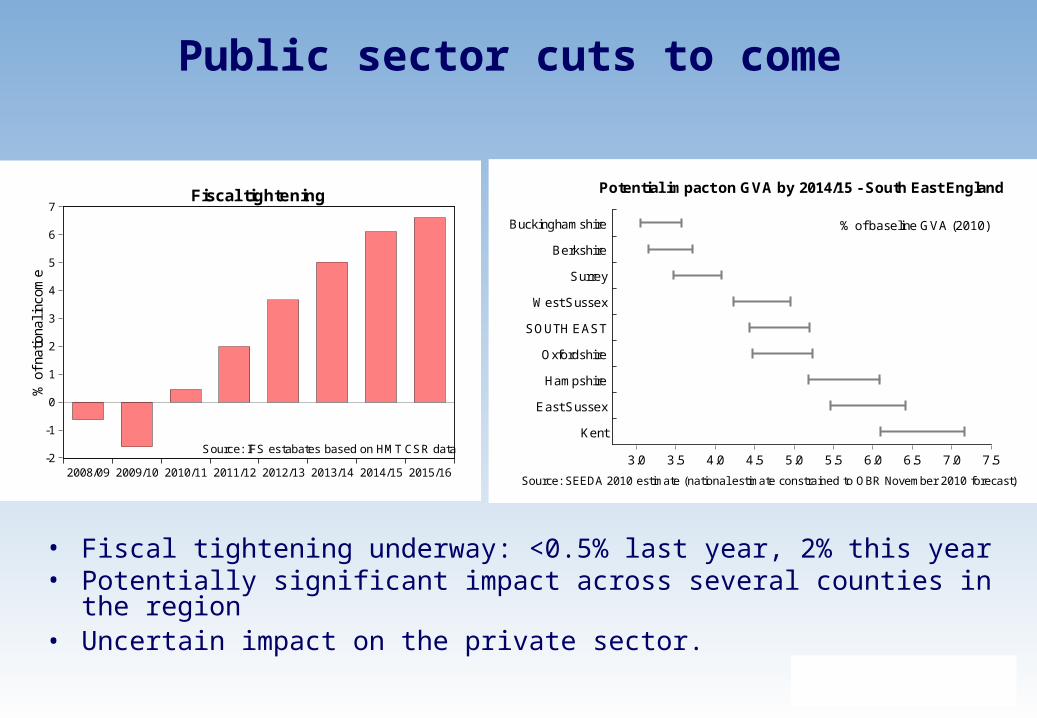

• Fiscal tightening underway: <0.5% last year, 2% this year• Potentially significant impact across several counties in the region • Uncertain impact on the private sector.

Public sector cuts to come

-2

-1

0

1

2

3

4

5

6

7

2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16

% o

f nat

iona

l inc

ome

Fiscal tightening

Source: IFS estabates based on HMT CSR data3.0 3.5 4.0 4.5 5.0 5.5 6.0 6.5 7.0 7.5

Buckinghamshire

Berkshire

Surrey

West Sussex

SOUTH EAST

Oxfordshire

Hampshire

East Sussex

Kent

% of baseline GVA (2010)

Source: SEEDA 2010 estimate (national estimate constrained to OBR November 2010 forecast)

Potential impact on GVA by 2014/15 - South East England

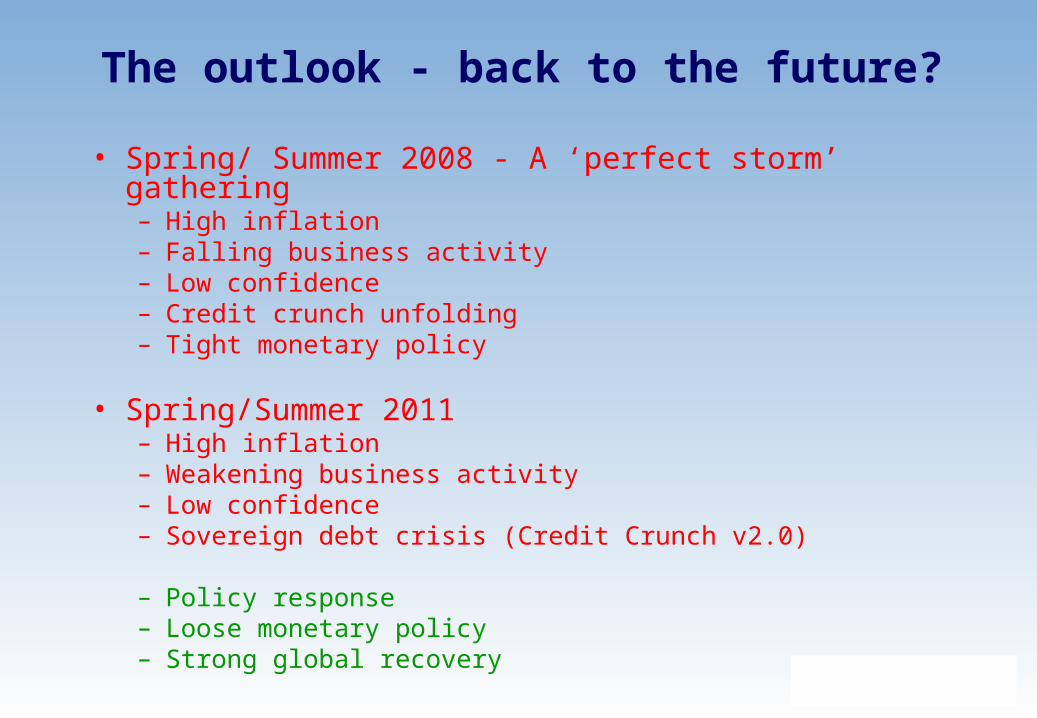

The outlook - back to the future?

• Spring/ Summer 2008 - A ‘perfect storm’ gathering– High inflation– Falling business activity– Low confidence– Credit crunch unfolding– Tight monetary policy

• Spring/Summer 2011– High inflation– Weakening business activity– Low confidence– Sovereign debt crisis (Credit Crunch v2.0)

– Policy response– Loose monetary policy– Strong global recovery

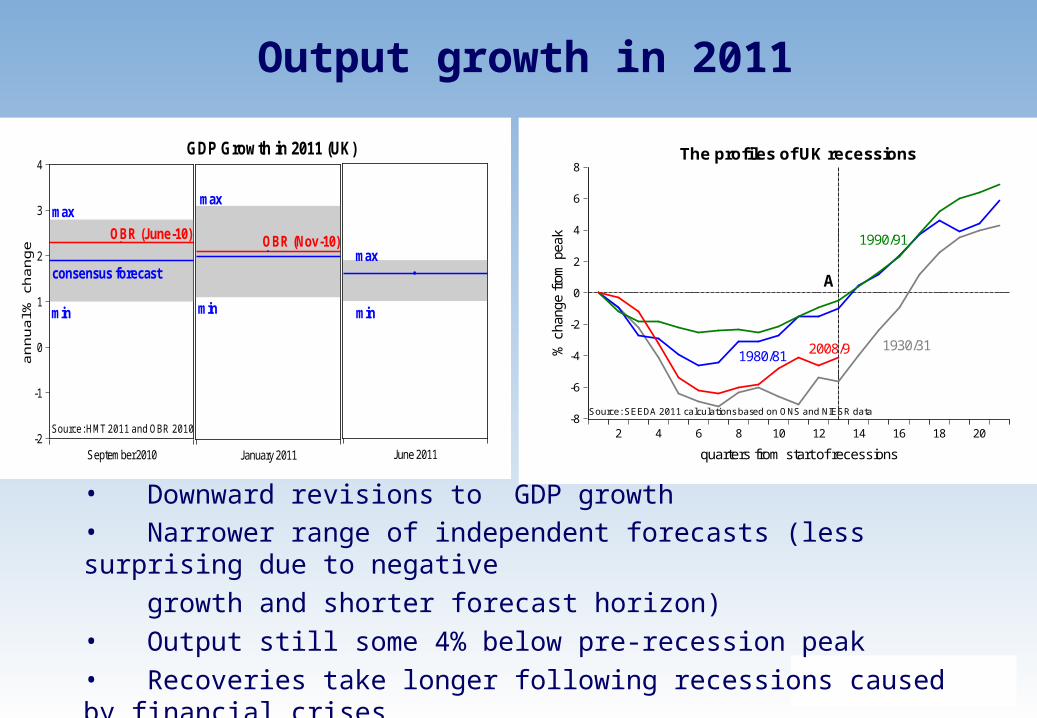

Output growth in 2011

• Downward revisions to GDP growth• Narrower range of independent forecasts (less surprising due to negative

growth and shorter forecast horizon)• Output still some 4% below pre-recession peak• Recoveries take longer following recessions caused by financial crises

-2

-1

0

1

2

3

4

September 2010

max

min

consensus forecast

OBR (June-10)

January 2011

OBR (Nov-10)

max

min

June 2011

max

min

GDP Growth in 2011 (UK)

an

nu

al %

ch

an

ge

Source: HMT 2011 and OBR 2010-8

-6

-4

-2

0

2

4

6

8

2 4 6 8 10 12 14 16 18 20

1930/312008/91980/81

1990/91

The profiles of UK recessions

quarters from start of recessions

Source: SEEDA 2011 calculations based on ONS and NIESR data

% c

hang

e fr

om p

eak

A

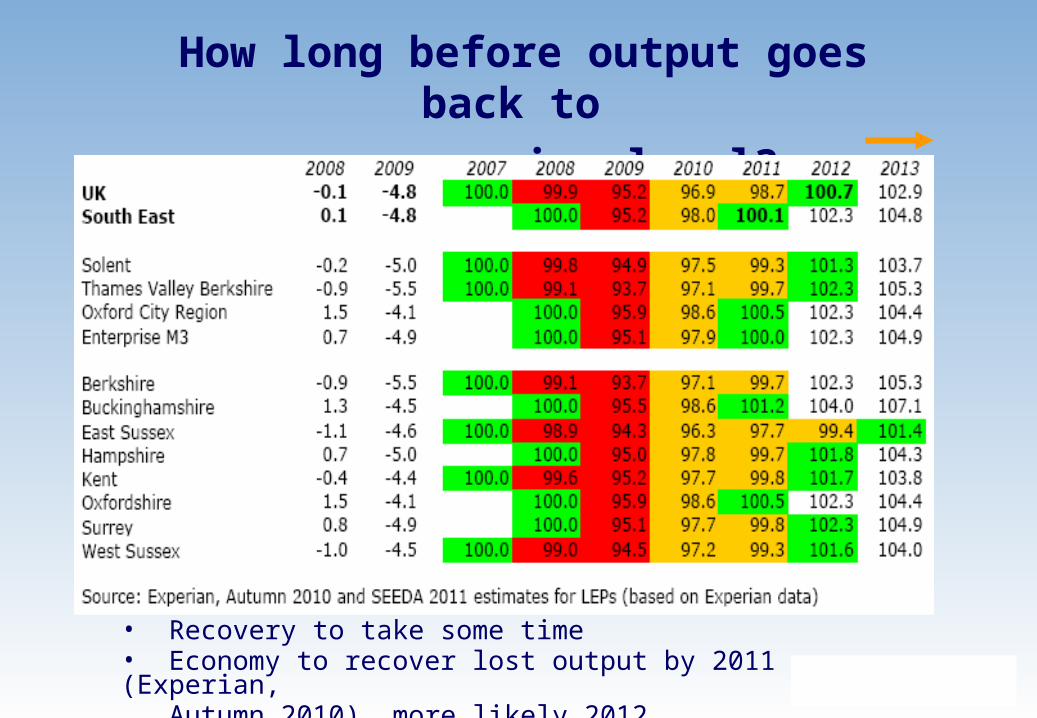

How long before output goes back to

pre-recession level?

• Recovery to take some time• Economy to recover lost output by 2011 (Experian, Autumn 2010), more likely 2012.

Key challenges ahead

• Sovereign debt crisis and possibility of the Credit Crunch v2.0

• Slowdown in demand from US and Eurozone economies

• Business investment fails to materialise

• Tighter monetary policy (when it arrives) and its impact on the housing market

• Consumer spending ~2/3 of demand. How will UK consumer react?

Economic Analysis, Market Intelligence & Evaluation

What we did and where it is all going?

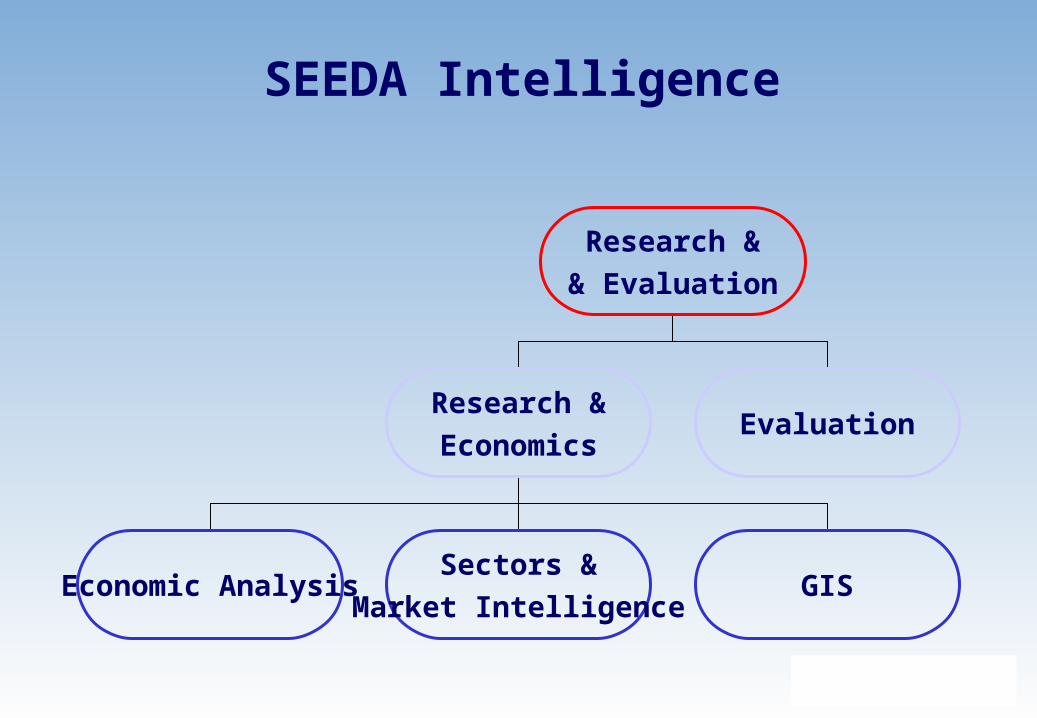

SEEDA Intelligence

Research &

& Evaluation

Research &

EconomicsEvaluation

Economic AnalysisSectors &

Market IntelligenceGIS

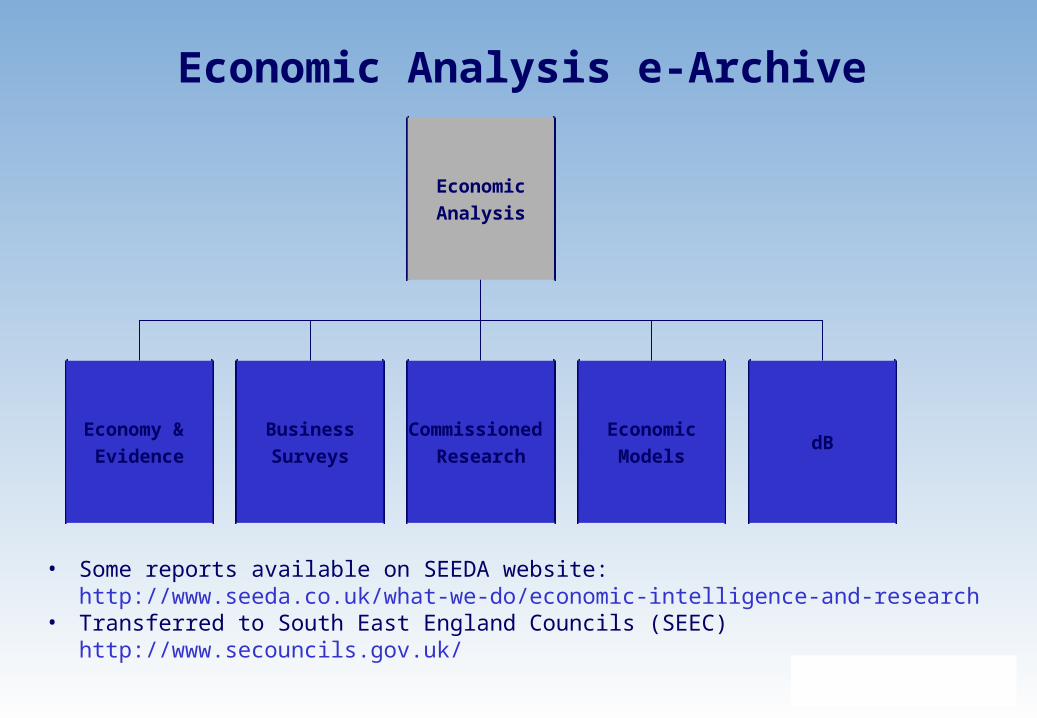

Economic Analysis e-Archive

Economic

Analysis

Economy &

Evidence

Business

Surveys

Commissioned

ResearchdB

Economic

Models

• Some reports available on SEEDA website:http://www.seeda.co.uk/what-we-do/economic-intelligence-and-research

• Transferred to South East England Councils (SEEC)http://www.secouncils.gov.uk/

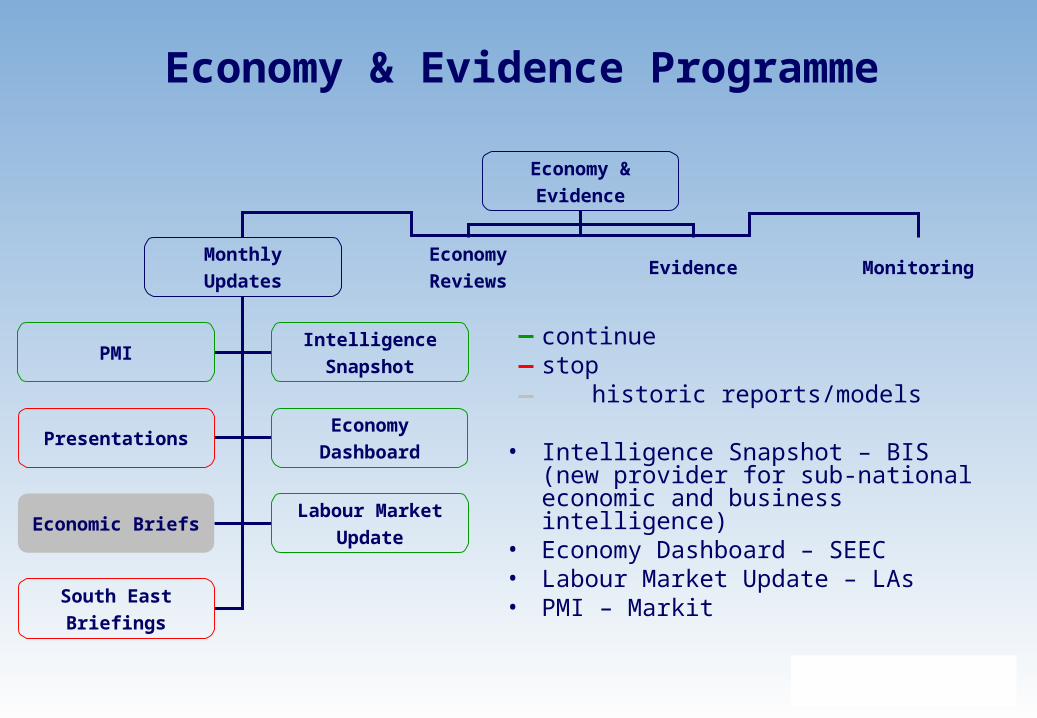

Economy & Evidence Programme

Economy &

Evidence

Monthly

Updates

Economy

ReviewsEvidence Monitoring

PMIIntelligence

Snapshot

PresentationsEconomy

Dashboard

Economic BriefsLabour Market

Update

South East

Briefings

continue stop historic reports/models

• Intelligence Snapshot – BIS (new provider for sub-national economic and business intelligence)

• Economy Dashboard – SEEC• Labour Market Update – LAs• PMI – Markit

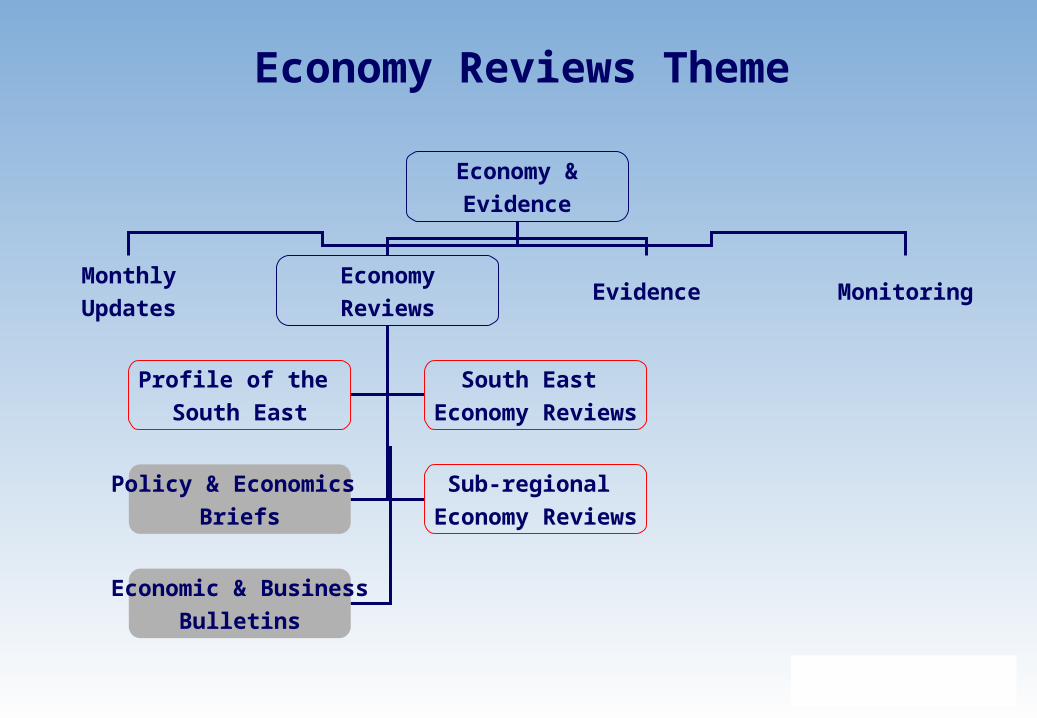

Economy Reviews Theme

Economy &

Evidence

Monthly

Updates

Economy

ReviewsEvidence Monitoring

Profile of the

South East

South East

Economy Reviews

Policy & Economics

Briefs

Sub-regional

Economy Reviews

Economic & Business

Bulletins

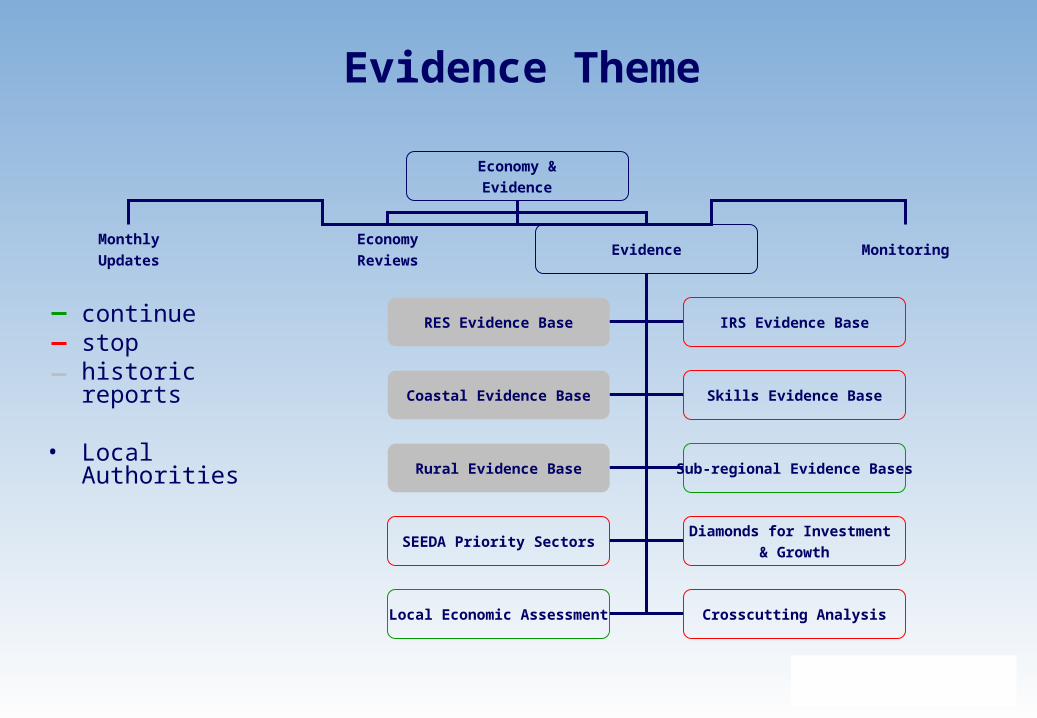

Evidence Theme

Economy &

Evidence

Monthly

Updates

Economy

ReviewsEvidence Monitoring

RES Evidence Base IRS Evidence Base

Coastal Evidence Base Skills Evidence Base

Rural Evidence Base Sub-regional Evidence Bases

SEEDA Priority SectorsDiamonds for Investment

& Growth

Local Economic Assessment Crosscutting Analysis

continue stop

historic reports

• Local Authorities

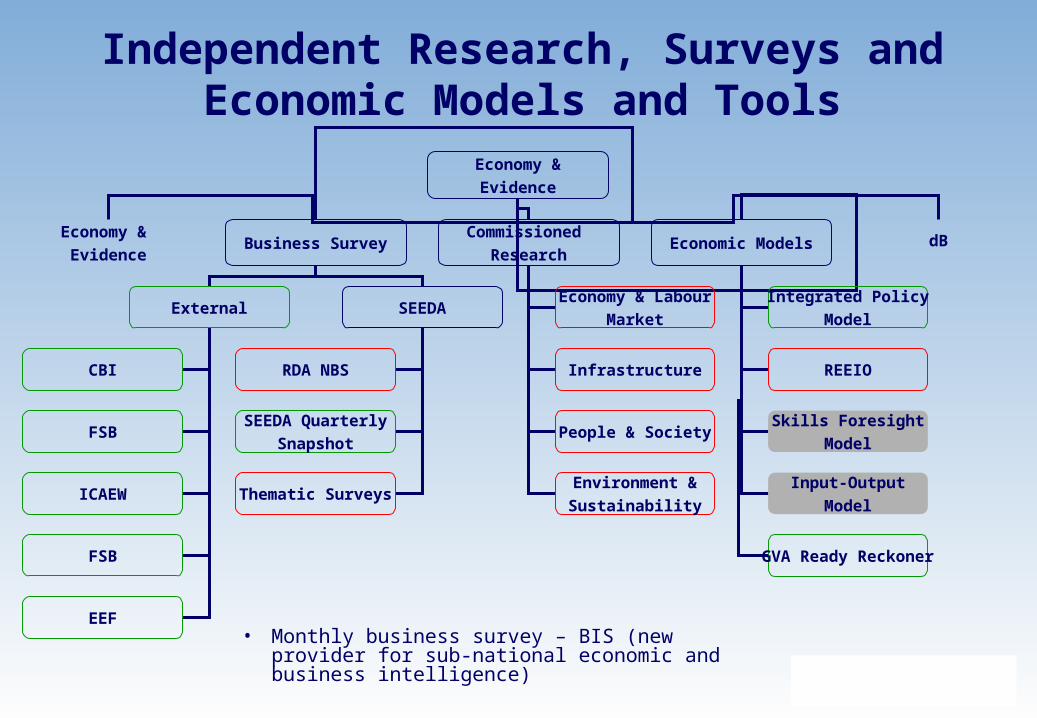

Independent Research, Surveys and Economic Models and Tools

Economy &

Evidence

Economy &

EvidenceBusiness Survey

Commissioned

ResearchEconomic Models dB

External SEEDA

CBI

FSB

ICAEW

FSB

EEF

RDA NBS

SEEDA Quarterly

Snapshot

Economy & Labour

Market

Infrastructure

Thematic Surveys

People & Society

Environment &

Sustainability

Integrated Policy

Model

REEIO

Skills Foresight

Model

Input-Output

Model

GVA Ready Reckoner

• Monthly business survey – BIS (new provider for sub-national economic and business intelligence)

Sectors & Market Intelligence

• Sector-related material• Regional/sub-regional propositions• Business support, access to finance and regional profile

guides• Performance Monitors

• Transferred to the new provider PA Consulting and UKTI:

http://www.ukti.gov.uk

http://www.paconsulting.co.uk/

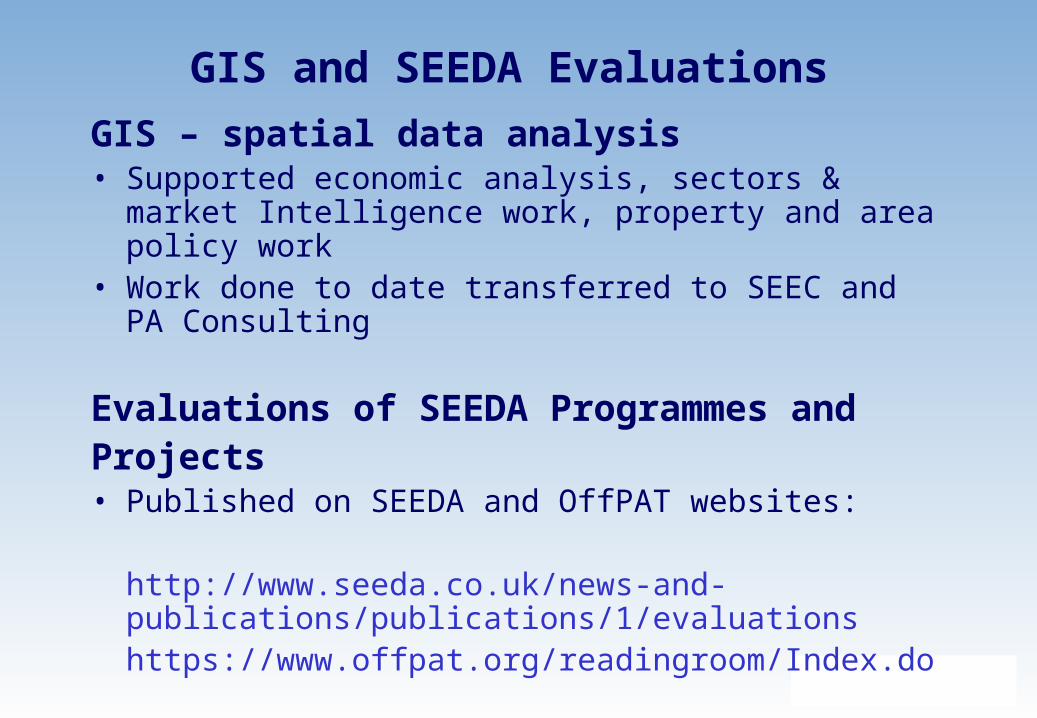

GIS and SEEDA Evaluations

GIS – spatial data analysis• Supported economic analysis, sectors & market

Intelligence work, property and area policy work• Work done to date transferred to SEEC and PA

Consulting

Evaluations of SEEDA Programmes andProjects• Published on SEEDA and OffPAT websites:

http://www.seeda.co.uk/news-and-publications/publications/1/evaluationshttps://www.offpat.org/readingroom/Index.do

Thank you

SEEDA Research & Economics

Email: [email protected]

www: http://www.seeda.co.uk/what-we-do/economic-intelligence-and-research