Embed Size (px)

Citation preview

2018 It’s Not Getting Any Easier

Disclosure StatementPAST PERFORMANCE IS NOT INDICATIVE OF FUTURE

RESULTS. THERE IS SUBSTANTIAL RISK OF LOSS INVOLVED IN TRADING FUTURES AND OPTIONS WHICH MAY NOT BE SUITABLE

FOR EVERYONE. HOWEVER, THE RISK INVOLVED WITH PURCHASING OPTIONS IS LIMITED TO THE PREMIUM PAID PLUS

TRANSACTION COSTS. THIS MATERIAL HAS BEEN PREPARED BY A SALES OR TRADING EMPLOYEE OR AGENT OF AGWEST AND IS A

SOLICITATION FOR ENTERING INTO A DERIVATIVES TRANSACTION. THIS MATERIAL IS NOT A RESEARCH REPORT

PREPARED BY AGWEST. IF YOU ARE NOT AN EXPERIENCED USER OF THE DERIVATIVES MARKETS, CAPABLE OF MAKING

INDEPENDENT TRADING DECISIONS, THEN YOU SHOULD NOT RELY SOLELY ON THIS COMMUNICATION IN MAKING TRADING DECISIONS.

Topics Include

2017 Crop Size

Grain Sorghum Basis

China

Grains &Oilseeds

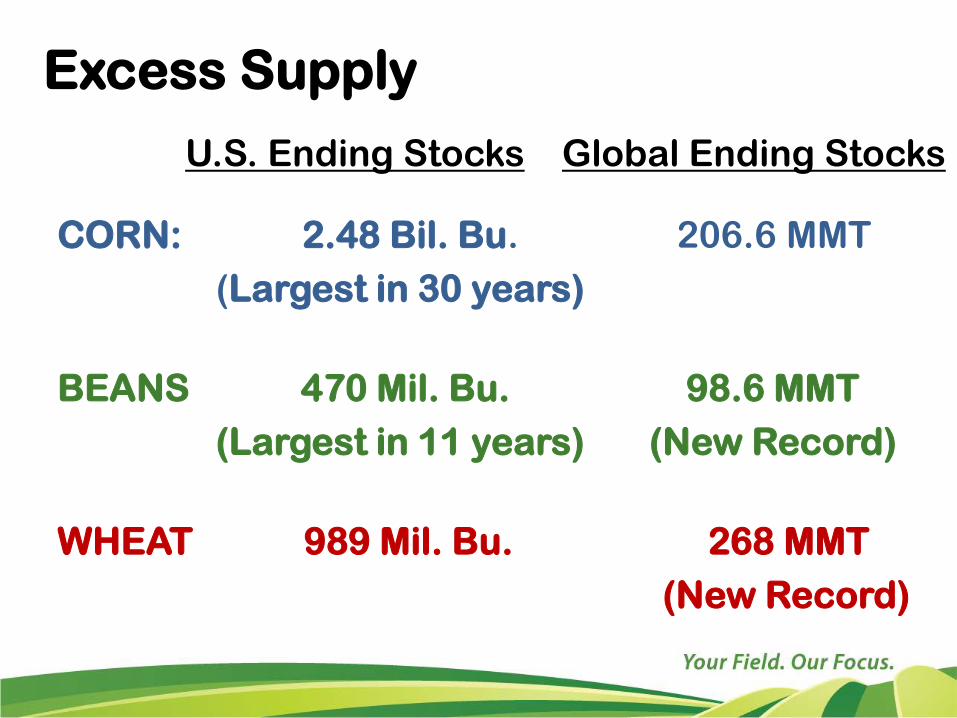

Excess Supply

U.S. Ending Stocks Global Ending Stocks

CORN: 2.48 Bil. Bu. 206.6 MMT(Largest in 30 years)

BEANS 470 Mil. Bu. 98.6 MMT(Largest in 11 years) (New Record)

WHEAT 989 Mil. Bu. 268 MMT(New Record)

The Facts:

Global over-capacity continues to be a problem

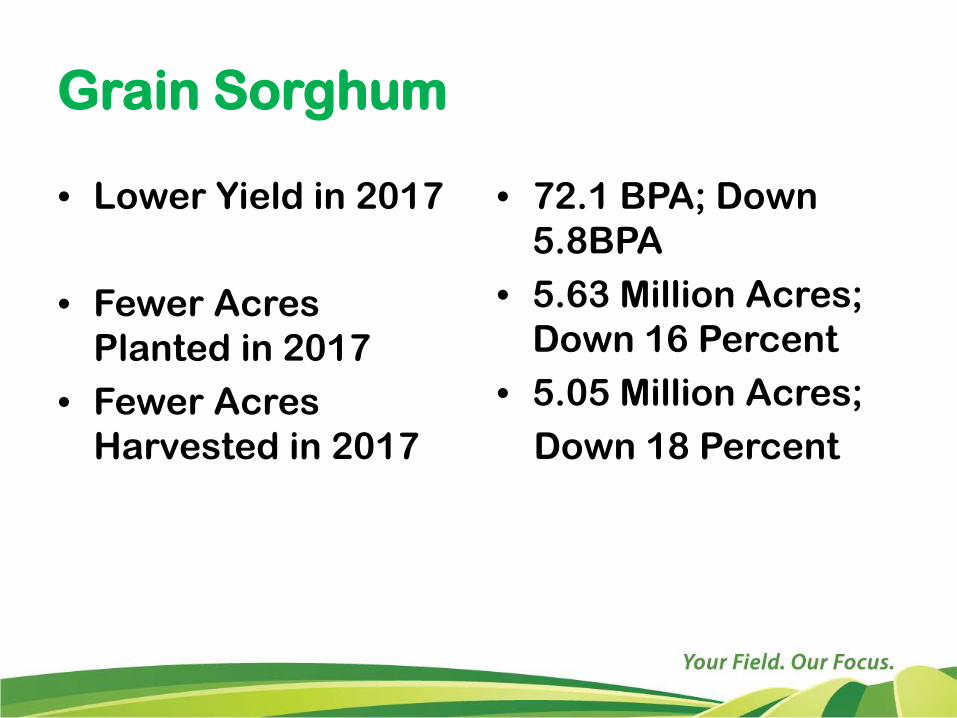

Grain Sorghum

• Lower Yield in 2017

• Fewer Acres Planted in 2017

• Fewer Acres Harvested in 2017

• 72.1 BPA; Down 5.8BPA

• 5.63 Million Acres; Down 16 Percent

• 5.05 Million Acres;Down 18 Percent

China

Began importing Grain Sorghum aggressively in 2017

Basis levels in Nebraska improved during the growing season reflecting this demand lifting grain sorghum values over corn in many places

2018 Grain Sorghum

Drought conditions are prevalent across a wide section of the plains

Wheat crop condition ratings are very low

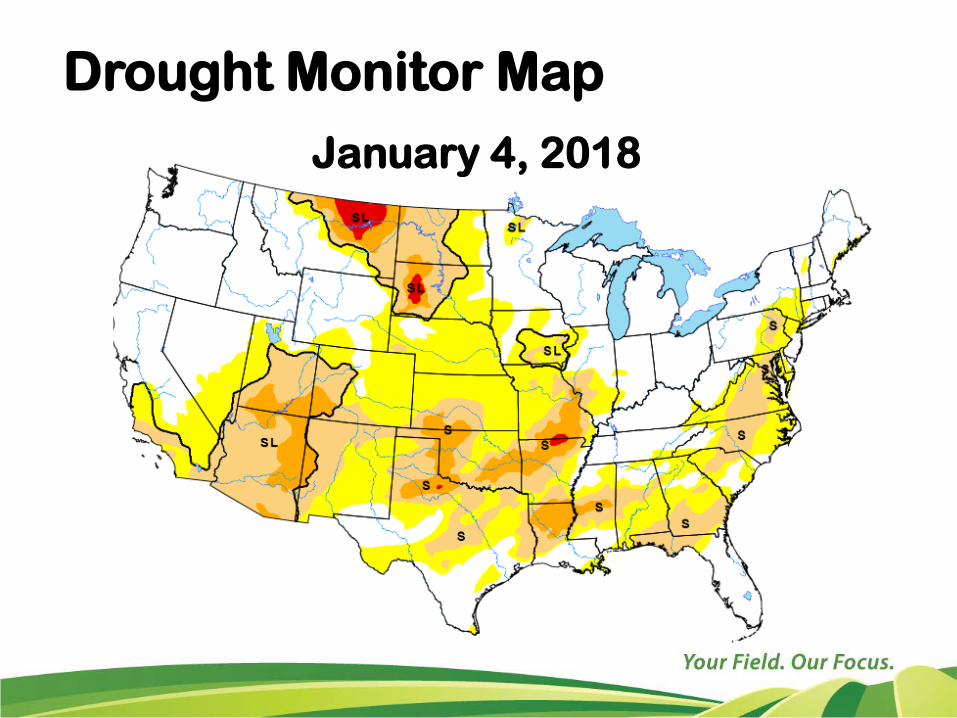

Drought Monitor Map

January 4, 2018

2018 Grain Sorghum

Basis levels are at historically good levels for 2018 new crop bids

Does NOT mean that basis levels have to narrow or widen

China is unpredictable.

2018 Grain Sorghum

Corn price is used to determine futures price of Grain Sorghum contract

Corn is burdened with largest stocks in 30 years

Corn price may be the most limiting factor in Sorghum pricing; Basis will do the rest

Your Turn

QuestionsComments

Arguments

Relationships

Thank You!

19 Years of Building Relationships

Thank You!

130 Referral ClientsIn 2017

44 From Lenders

DeWalt Tools

Yeti Cooler

Our 90 second advertisement

Producer tested since 2002

TOGETHER we design YOUR marketing plan, and then WE make it happen

NOT a Program!

Completely individualized

Blue sheet for more information

What We Will Cover

Cattle

Grains & oilseeds

It’s not getting any easier(Can we improve)

For those looking for help(We will send you home with a challenge)

Livestock Markets

Profits in all sectors – except for me

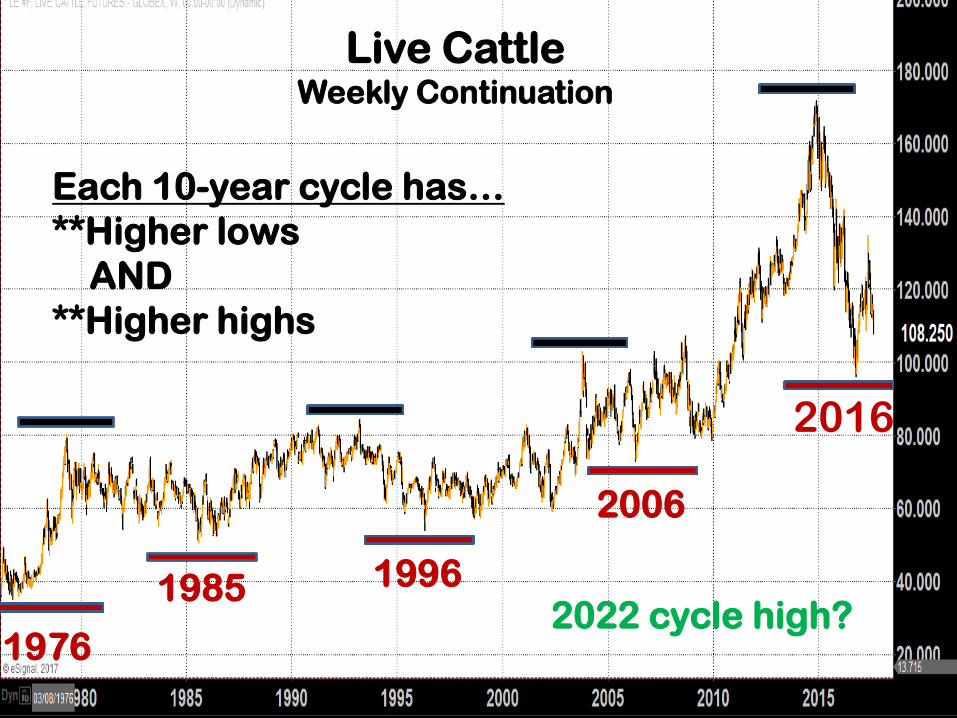

Is the “10-year” cycle low in place?(pegged for 2016)

Final confirmation of low will come with a change in market trend

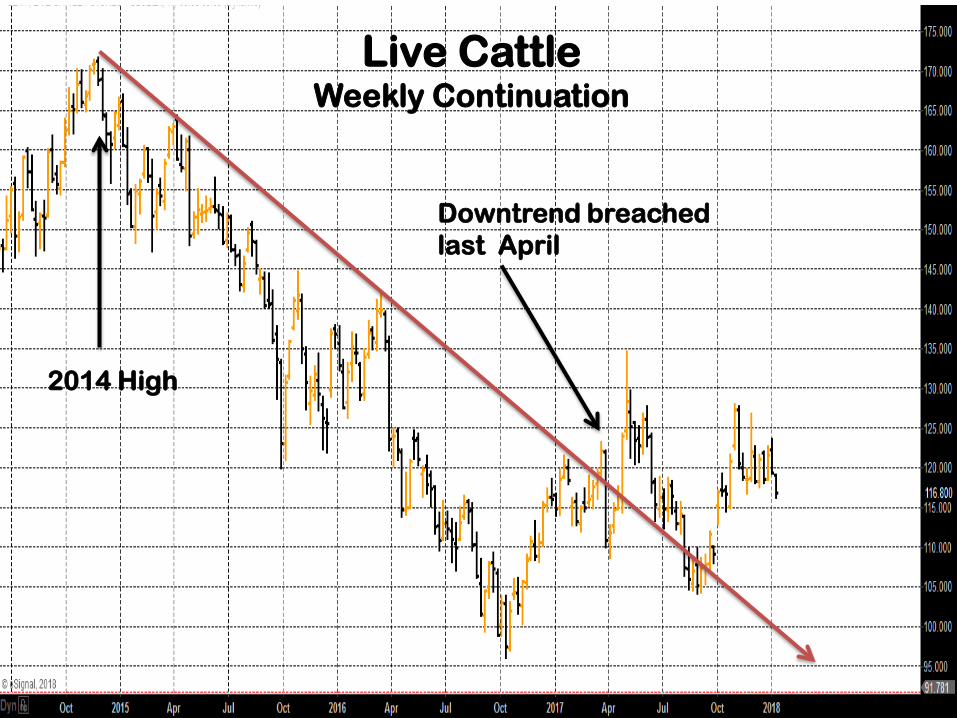

Cattle

Live CattleWeekly Continuation

2014 High

Downtrend breached last April

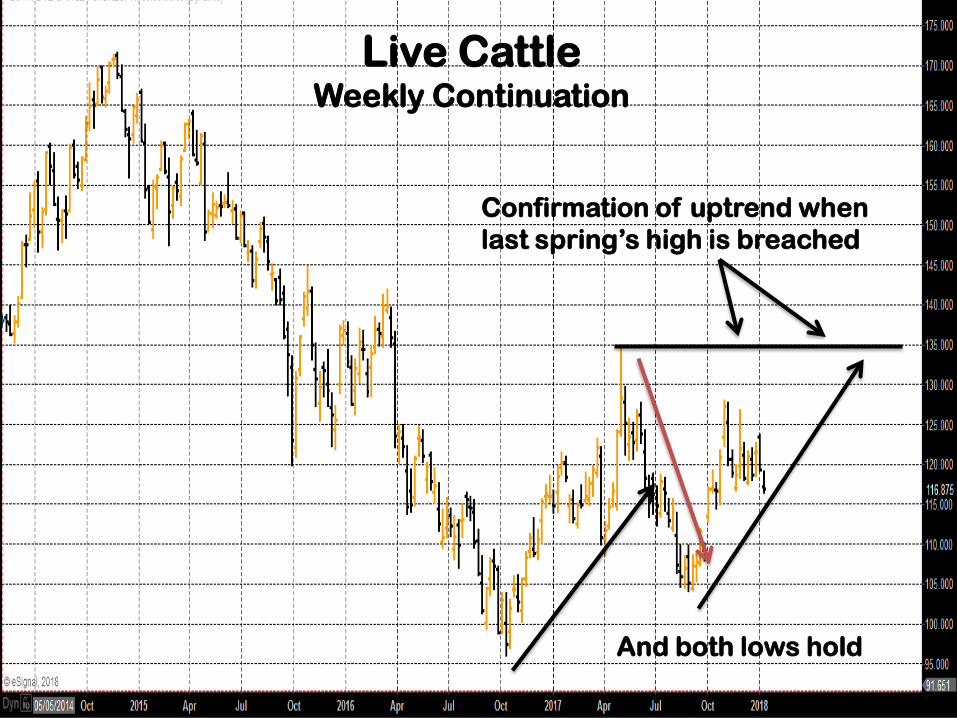

Live CattleWeekly Continuation

Confirmation of uptrend whenlast spring’s high is breached

And both lows hold

1976

1985 1996

2006

2016

Live CattleWeekly Continuation

Each 10-year cycle has…**Higher lows

AND**Higher highs

2022 cycle high?

10-Year Cycle

Timing is here for years of good results

IMPORTANT -- This DOES NOT mean the cattle market goes straight up

Corrections during the upswing of the cycle do happen

Proactively Avoid the DipsWe can’t wait them out!

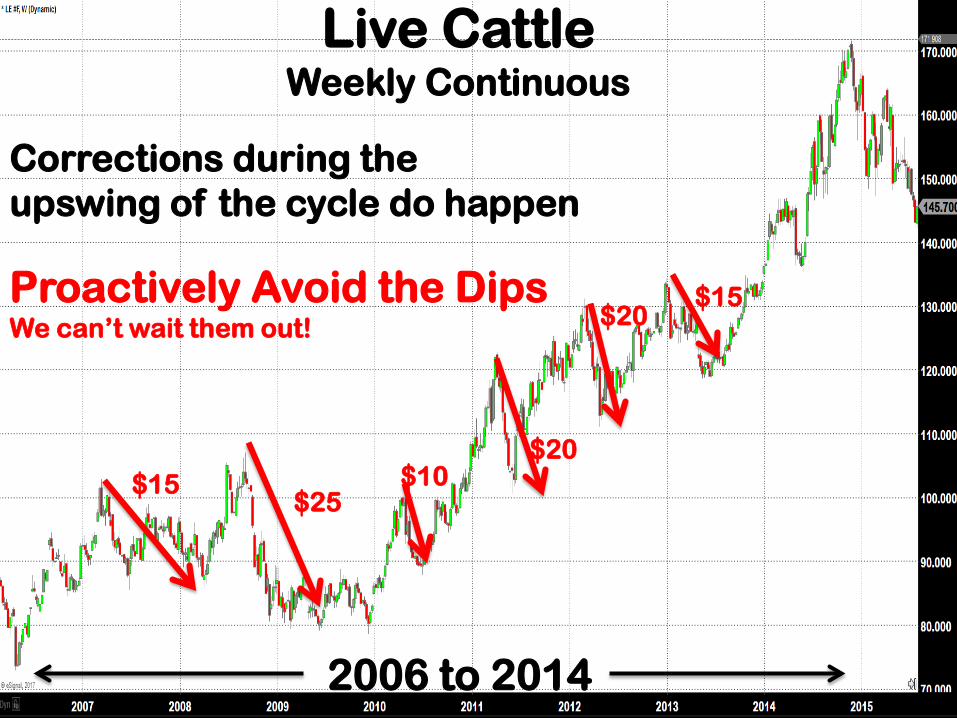

Live CattleWeekly Continuous

$15$25

$10$20

$20$15

2006 to 2014

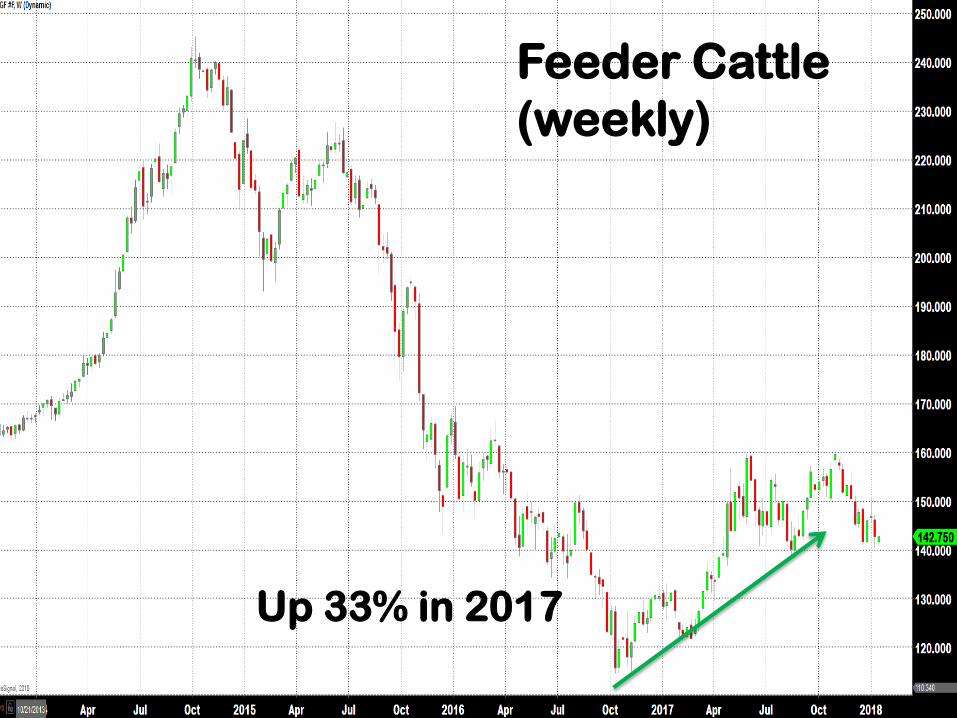

Feeder Cattle (weekly)

Up 33% in 2017

FeedersWeekly Cont.

New Range: Driven by Fat Cattle

$90 - $120 Range

$120 - $160 Range

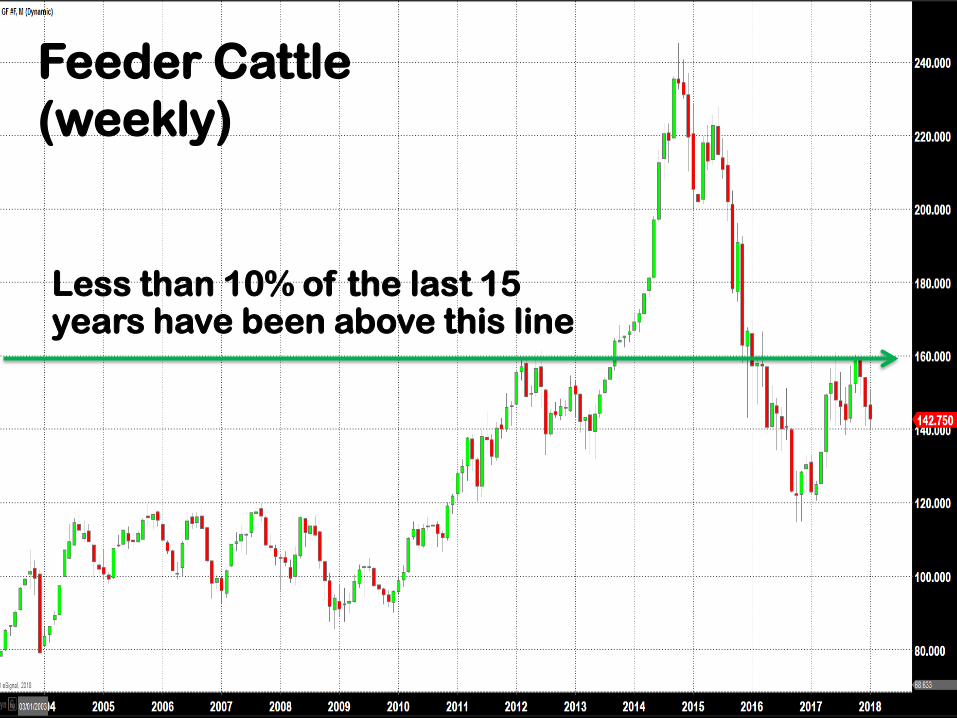

Feeder Cattle (weekly)

Less than 10% of the last 15 years have been above this line

Avoiding Pain During Corrections

Markets go up and then they go down

Opportunity comes and then it goes

We buy calves based on profits, why don’t we sell them that way also?

Striving for Consistency in Profitability

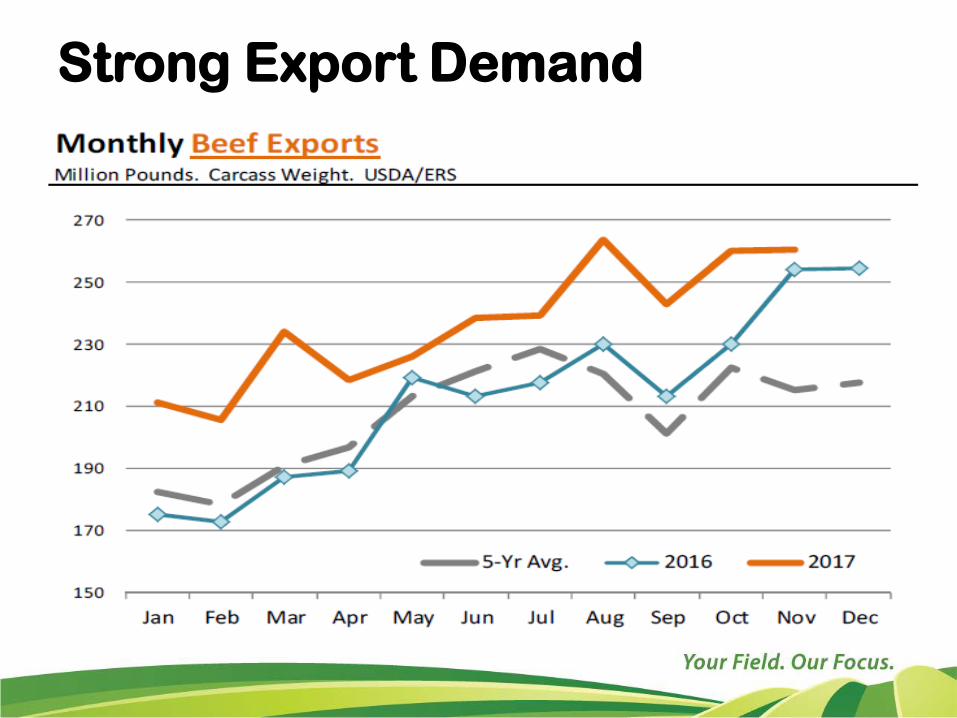

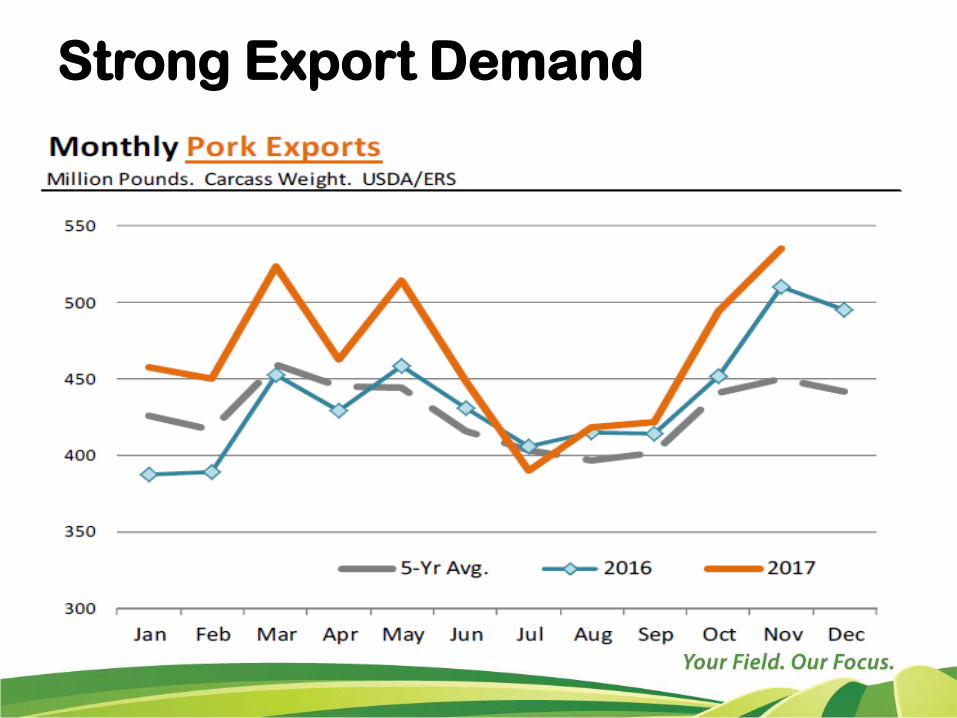

Healthy Market

Strong Export Demand

Strong Export Demand

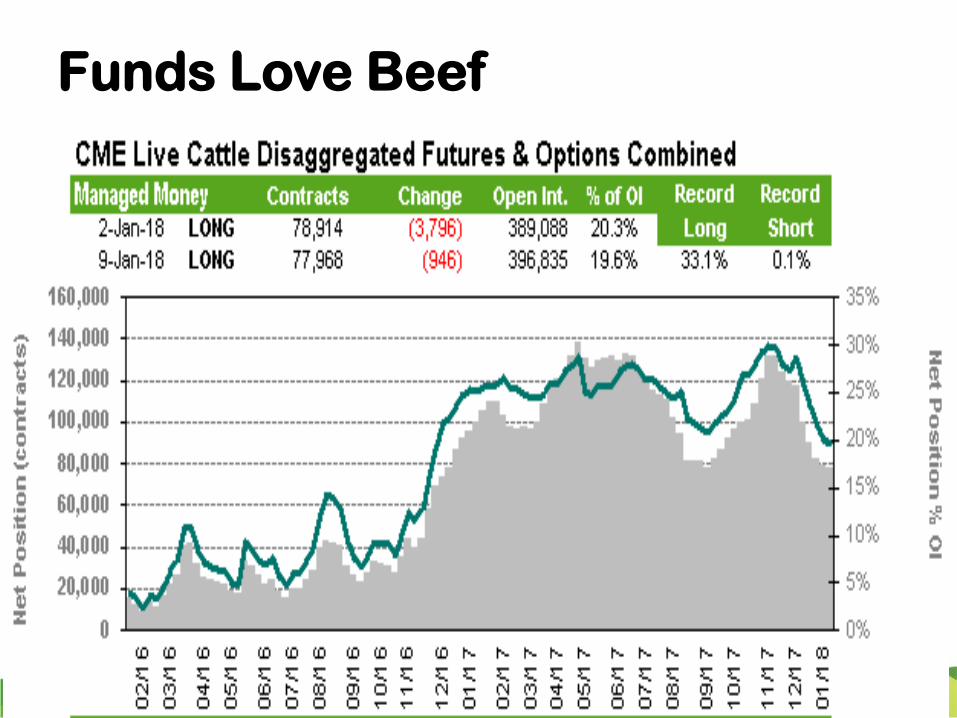

Funds Love Beef

Funds love Pork even more!

Taps for the Grain Markets

Most important

Ma

rke

t S

tru

ctu

re

Market Drivers In 2018

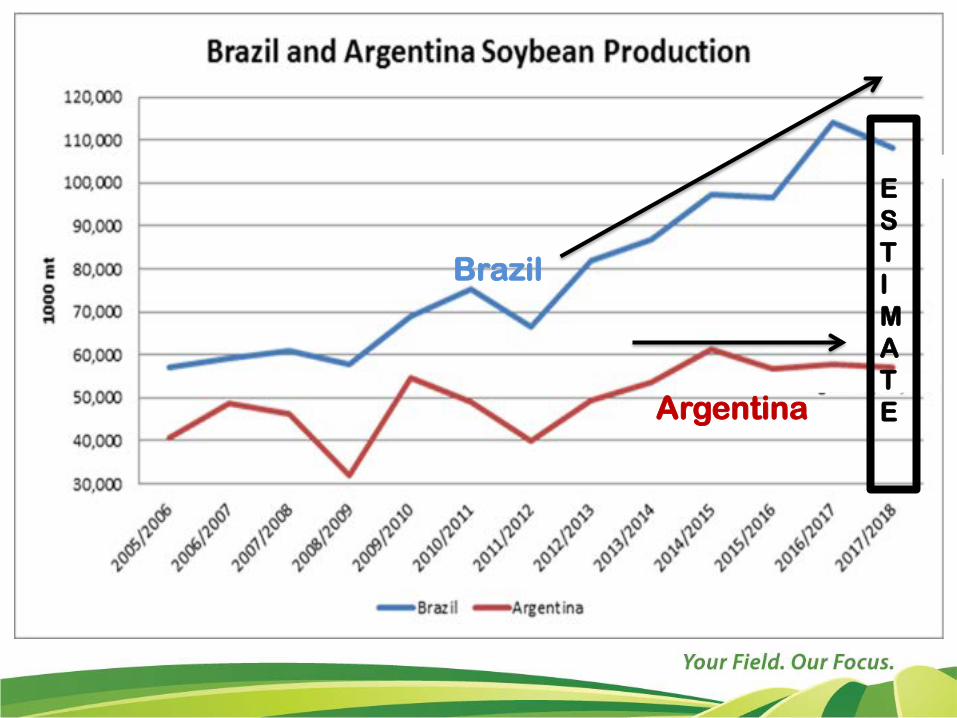

Key Drivers in ’18

South American productionFirst crop good but delayed and could push

second corn crop back7.8% in production

Brazil

Argentina

ESTIMATE

Lagging Exports

So far in the marketing year…

Corn exports are 25% behind last year compared to the USDA estimate of down 16% for the marketing year

Lagging Exports

So far in the marketing year…

Soybeans exports are 14% behind last year while USDA is estimating a 3% increase for the marketing year

Lagging Exports

So far in the marketing year…

Wheat exports are 8% behind last year with USDA estimating this marketing year to be down 5%

Key Drivers in ’18

South American production

U.S. weather

Exports

Funds (Where are they when we need them?)

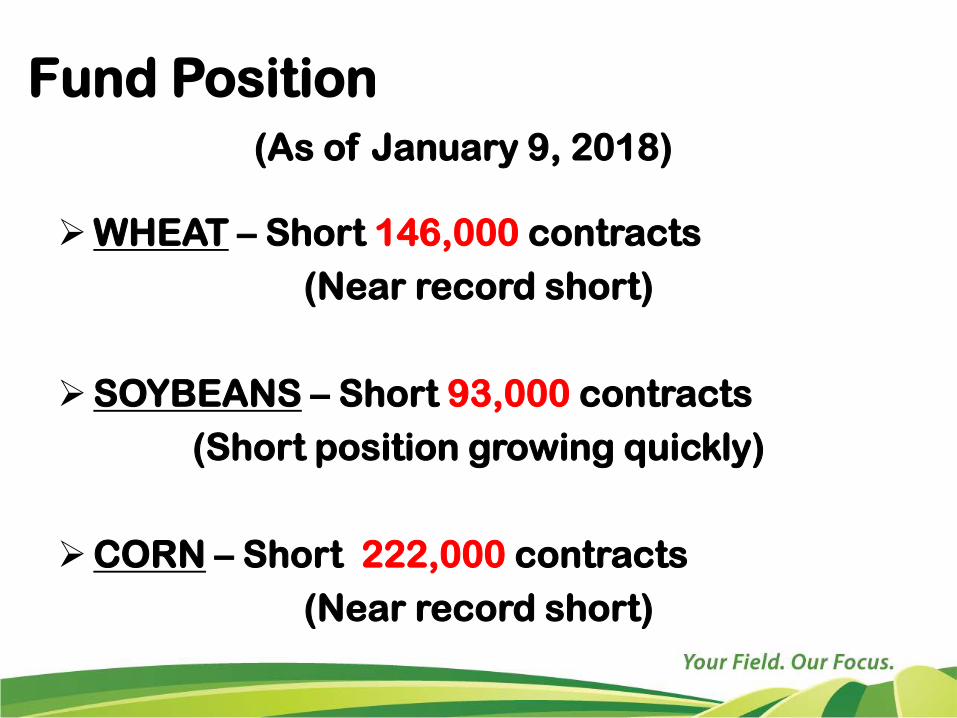

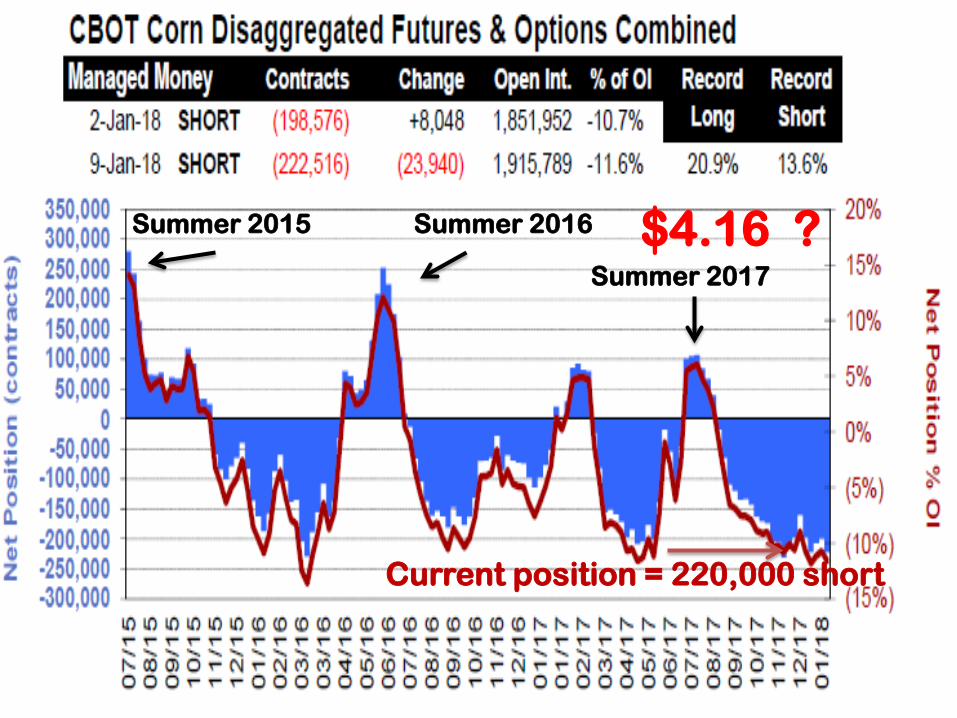

Fund Position (As of January 9, 2018)

WHEAT – Short 146,000 contracts (Near record short)

SOYBEANS – Short 93,000 contracts(Short position growing quickly)

CORN – Short 222,000 contracts(Near record short)

Summer 2015 Summer 2016

Summer 2017

Current position = 220,000 short

$4.16 ?

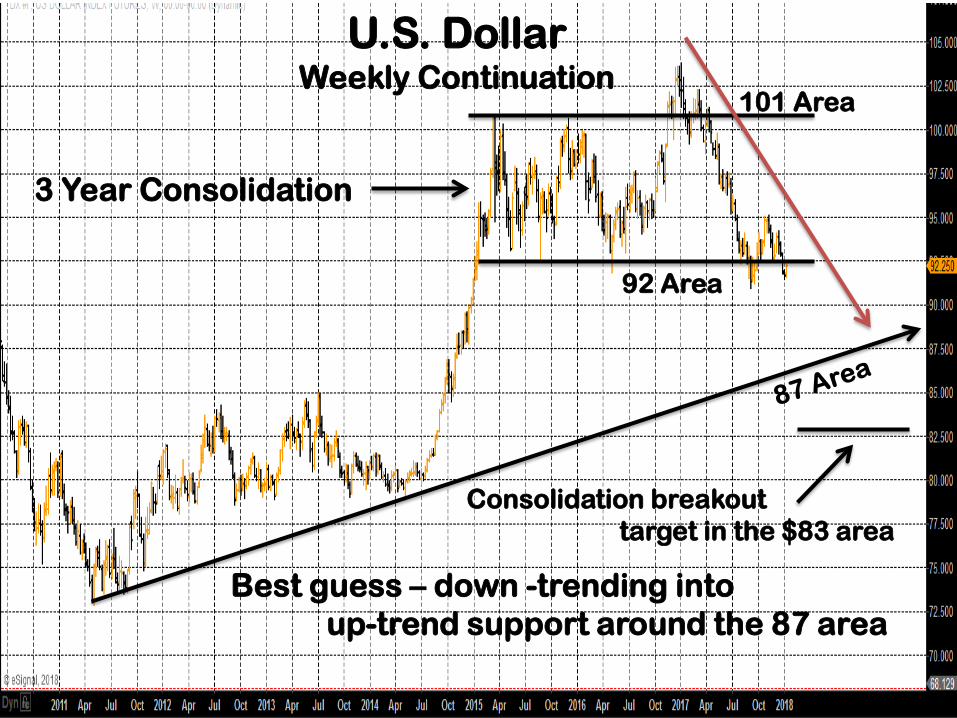

U.S. DollarWeekly Continuation

101 Area

92 Area

Best guess – down -trending into up-trend support around the 87 area

3 Year Consolidation

Consolidation breakouttarget in the $83 area

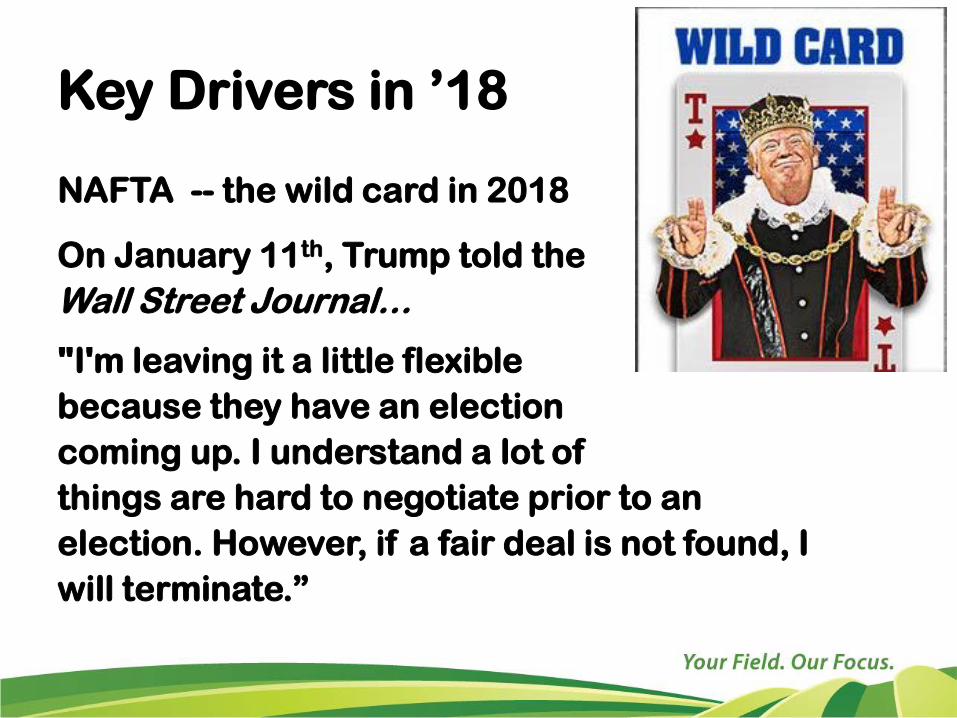

Key Drivers in ’18

NAFTA -- the wild card in 2018

On January 11th, Trump told theWall Street Journal…

"I'm leaving it a little flexible because they have an election coming up. I understand a lot of things are hard to negotiate prior to anelection. However, if a fair deal is not found, Iwill terminate.”

Production Overcapacity

From 2000 to 2016

CORN:*Global acreage up 32%*Global yield per acre up 30%

SOYBEANS:*Global acreage up 69%*Global yield per acre up 24%

Acreage + Technology = Overcapacity

Recognizing The Problem

Production capacity is HUGE EXCESS supply globally

Small windows of time to make good things happen

U.S. producer has shown a tendency of…*Marketing complacency

AND*Kicking the can down the road

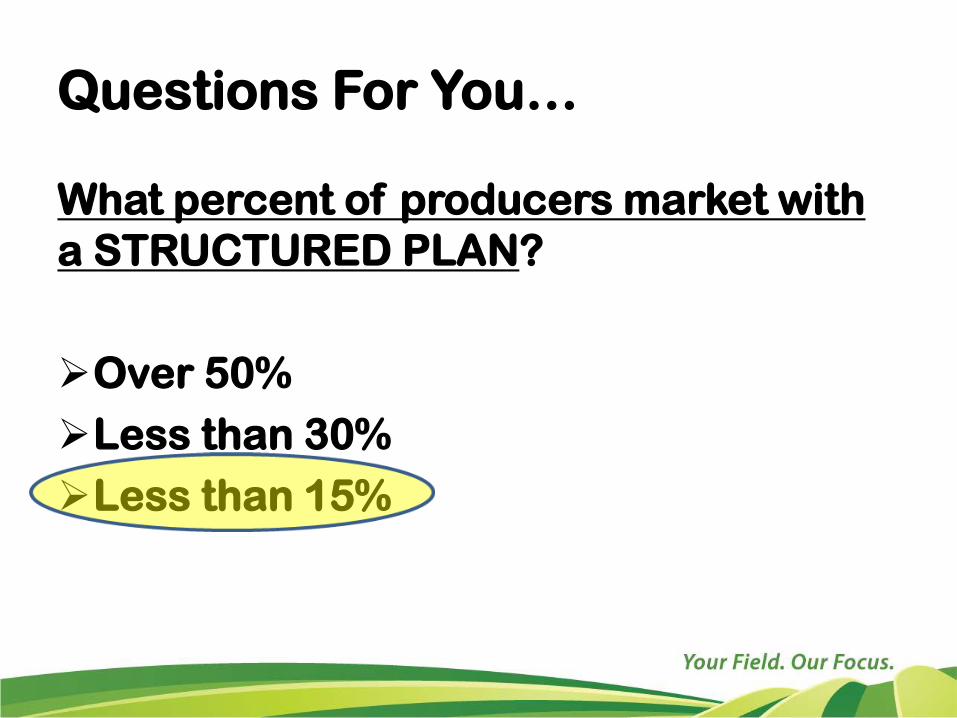

Questions For You…

What percent of producers market with a STRUCTURED PLAN?

Over 50%Less than 30%Less than 15%

Questions For You…

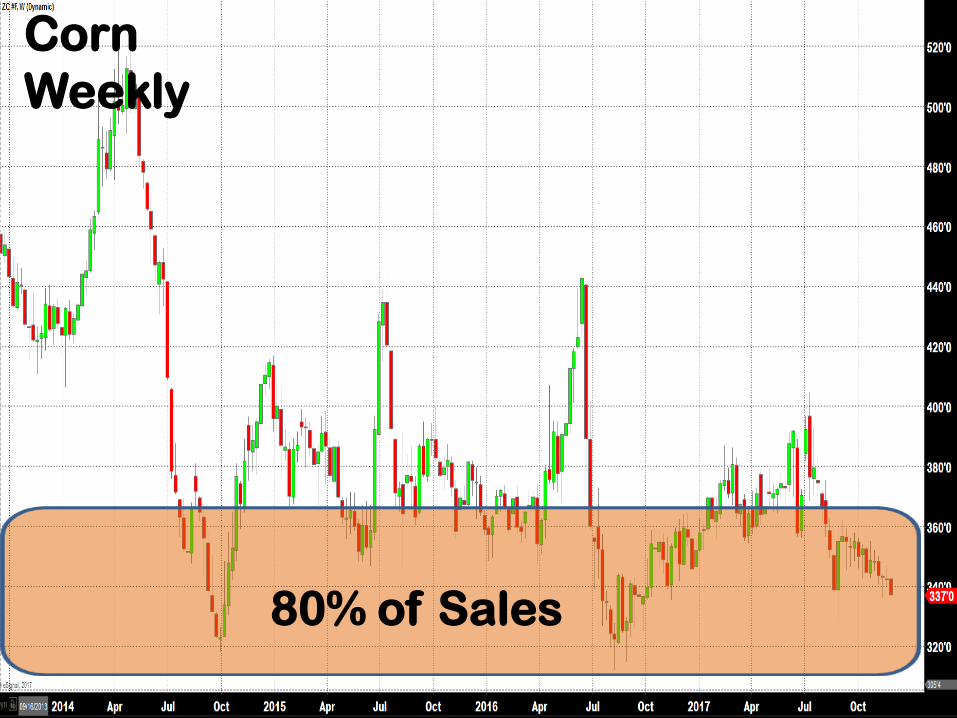

How much grain gets sold in the bottom 1/3 of the market each year?

• 20%• 40%• 60%• 80%

Source: Cargill

CornWeekly

80% of Sales

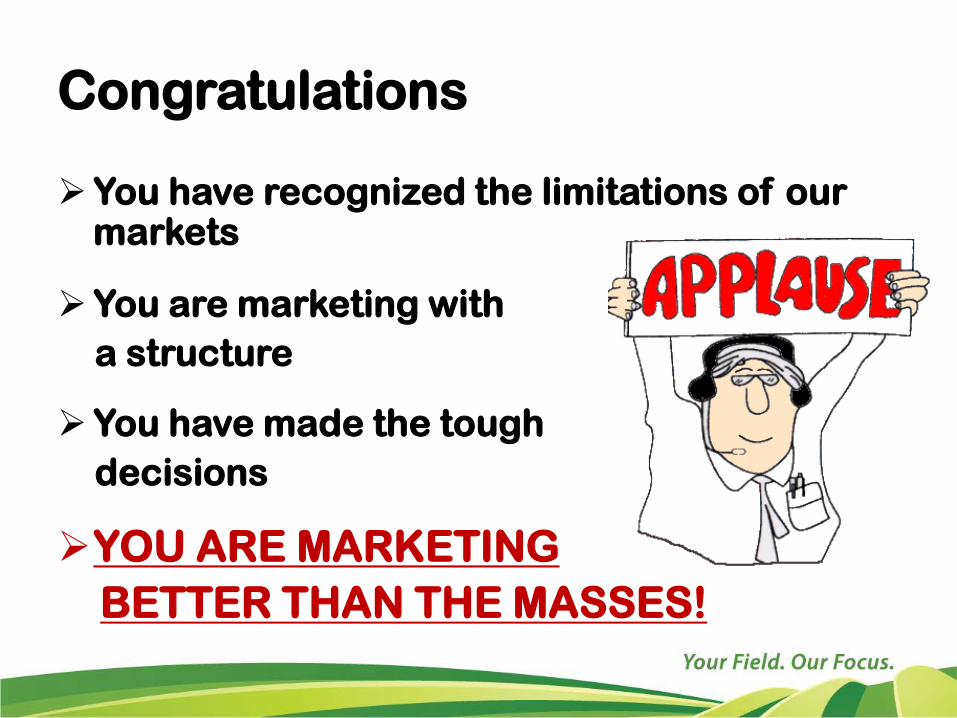

Congratulations

You have recognized the limitations of our markets

You are marketing witha structure

You have made the tough decisions

YOU ARE MARKETING BETTER THAN THE MASSES!

Question…Is There Room To Improve?

Is There Room To Improve?

We CANNOT improve the markets… they are what they are

BUT

We CAN improve how we go about marketing

What Makes Marketing So Difficult

SOLID DISCIPLINE is required

EMOTIONS can completely derail discipline

It is HUMAN NATURE – we all have emotions

EACH OF US, EVERY YEAR can work to improve our discipline and ability to keep emotions in check

What Makes Marketing So Difficult

Robert Plutchink’s theory – 8 basic emotionsHere are 5 of the 8

FEARANTICIPATIONJOYSURPRISEANGER

What Makes Marketing So Difficult

Robert Plutchink’s theory – 8 basic emotionsHere are 5 of the 8

FEAR of selling too soon – missing an opportunityANTICIPATION of better prices comingJOY when markets are moving higherSURPRISE when markets drop quickly ANGER when the markets have it all wrong

EMOTIONS screw up sound marketing!

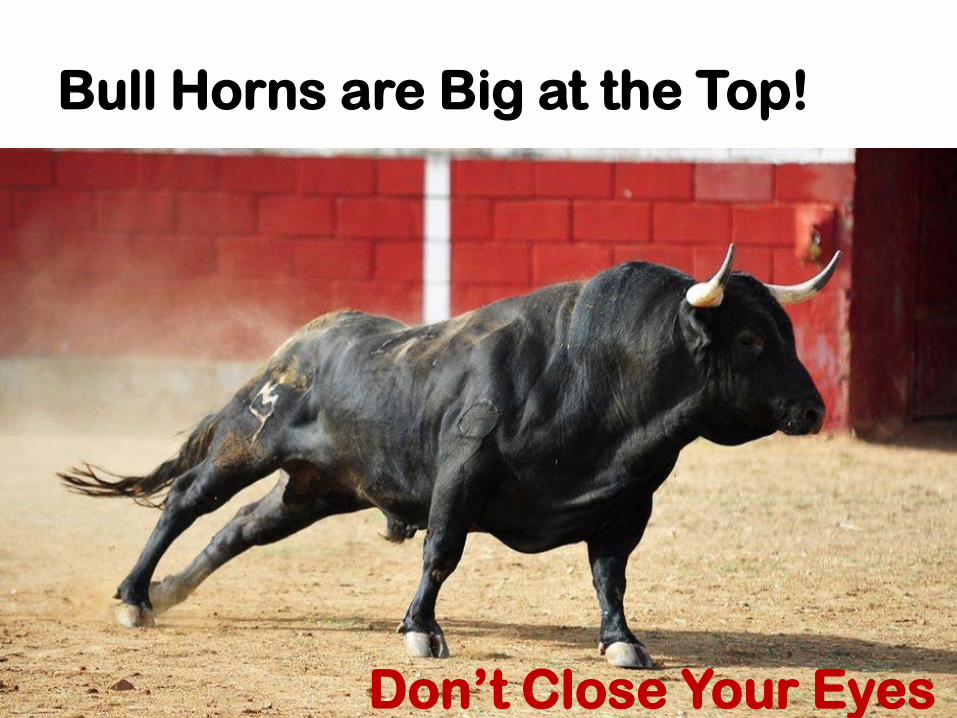

Bull Horns are Big at the Top!

Don’t Close Your Eyes

When Emotions Take Over

At Times…Even The Best Marketers Second Guess Their Plans

Do any of these adjustments ring a bell?

Adjust sales targetsCancel sales targets -- (Cancel when close)Lift hedges before sales are made

When Emotions Take Over

Three of our TOP TEN Rules speak directly to keeping emotions in check

Rules #6 - #9 - #10

Keeping Emotions In Check

Marketing Rule #6

Discipline is necessary for successful marketing – emotionally driven decisions are often poor decisions

Keeping Emotions In CheckSteps for improvement…

Acknowledgement – the first and most important step

Accountability – ask your broker to be honest with you and call a spade a spade when you want to stray from the structure of your plan

Let others know you are working on improving in this area – spouse, partners and lenders

Keeping Emotions In Check

Recognize your emotional triggers…

Ahead of major reports?When weather forecasts turn ugly?When your backyard is suffering?When analysts on TV or radio start getting

bullish?When it seems like you’re the only one

selling anything?

Keeping Emotions In Check

Change the narrative -- both to yourself and to others

STOP SAYING

I’m the world’s worst at marketing I really messed that up I was asleep on the trigger I don’t know enough

*These are not Badges of Honor*

Keeping Emotions In Check

Change the narrative -- both to yourself and to others

START SAYING

I have a plan, and I will follow through I am a disciplined individual I can’t control the markets but can control how I

market

Keeping Emotions In Check

Marketing Rule #9

Every good plan includes contingency plans in case of a major market-changing event

Keeping Emotions In Check

Something will happen and market structures will change

***Could it be this year… ***Will it be 5 years from now…

Keeping Emotions In Check

Contingency Plans – “Tools to Use”

Deploy a “call” option strategy against sales above 50% of APH production

Remain open on 50% of your APH bushels

“Calls” provide confidence to keep selling

A replacement strategy can curb the fear of selling too much too early!

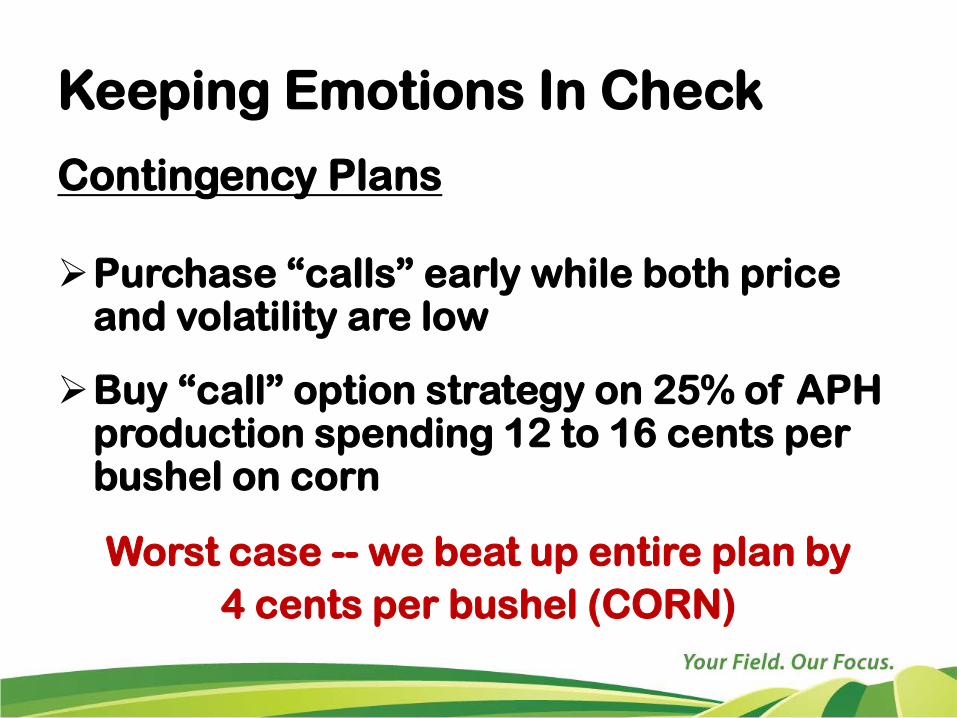

Keeping Emotions In Check

Contingency Plans

Purchase “calls” early while both price and volatility are low

Buy “call” option strategy on 25% of APH production spending 12 to 16 cents per bushel on corn

Worst case -- we beat up entire plan by 4 cents per bushel (CORN)

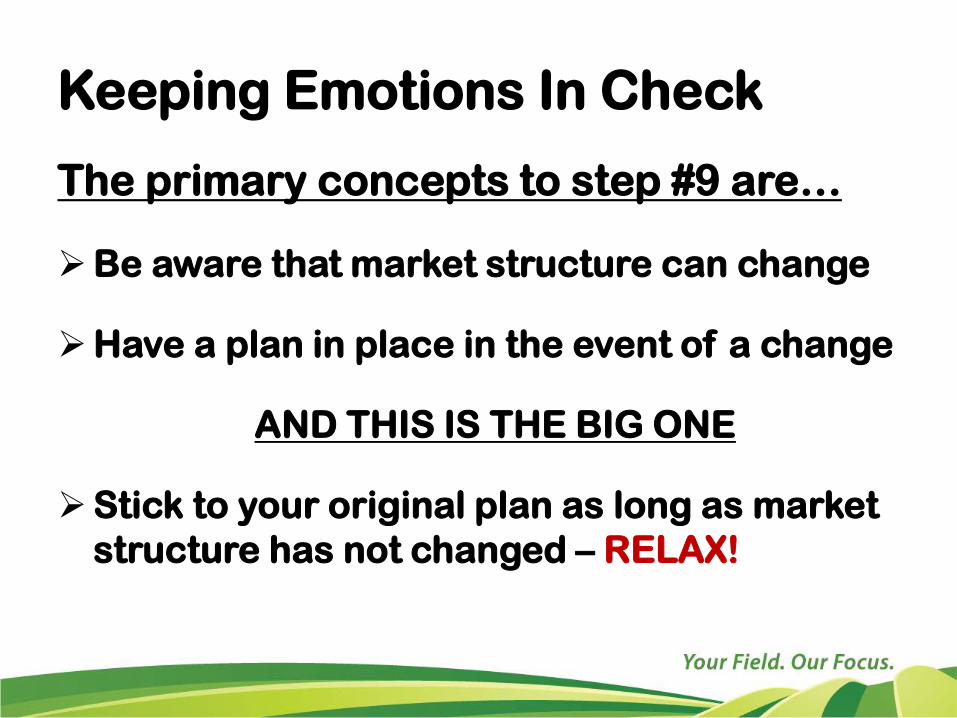

Keeping Emotions In Check

The primary concepts to step #9 are…

Be aware that market structure can change

Have a plan in place in the event of a change

AND THIS IS THE BIG ONE

Stick to your original plan as long as market structure has not changed – RELAX!

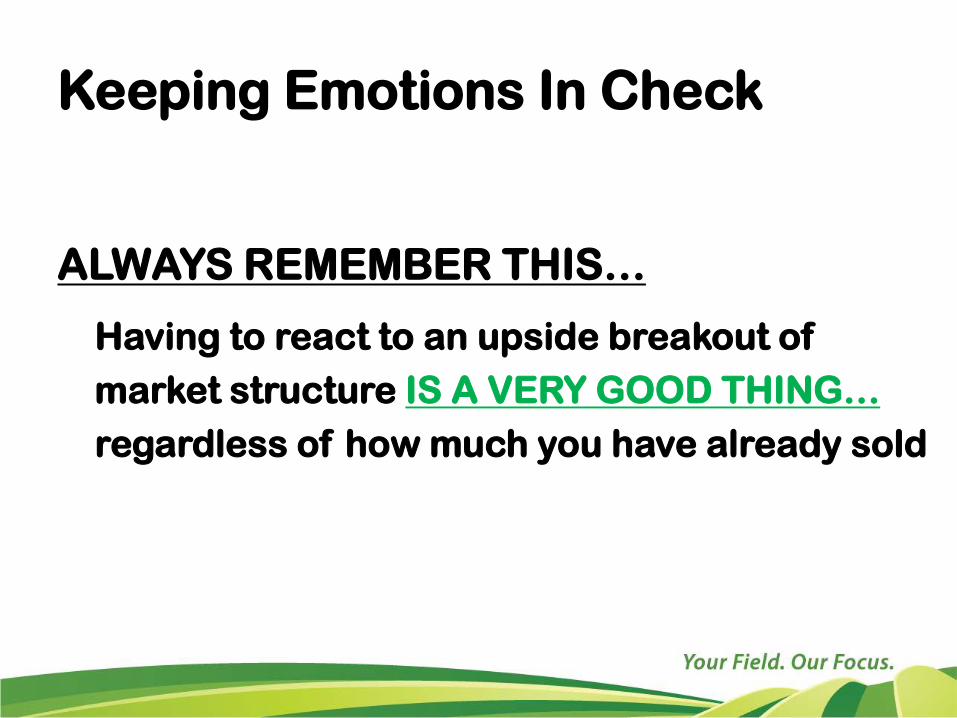

Keeping Emotions In Check

ALWAYS REMEMBER THIS…

Having to react to an upside breakout ofmarket structure IS A VERY GOOD THING…regardless of how much you have already sold

Keeping Emotions In Check

Marketing Rule #10

Perfection in marketing is undefinable and therefore unachievable— Marketing plan success should be gauged against individual goals rather than Chicago price action

Keeping Emotions In Check

Rule #10 is all about…

Staying focused on meeting YOUR goals

Understand that meeting goals represents a MAJOR WIN

CELEBRATE YOUR WINS!

Striving to improve is importantbecause…

Marketing IS NOTgetting any easier!

SoybeansWeekly Continuation

If downtrend holds,we may have already seen the annual high…

Market Structure

2018 Soybean Risk And Hedge Directive

Potential price risk in 2018 = $8.44 futures(2015 low)

You currently own $10.00 November “puts” on all unsold production

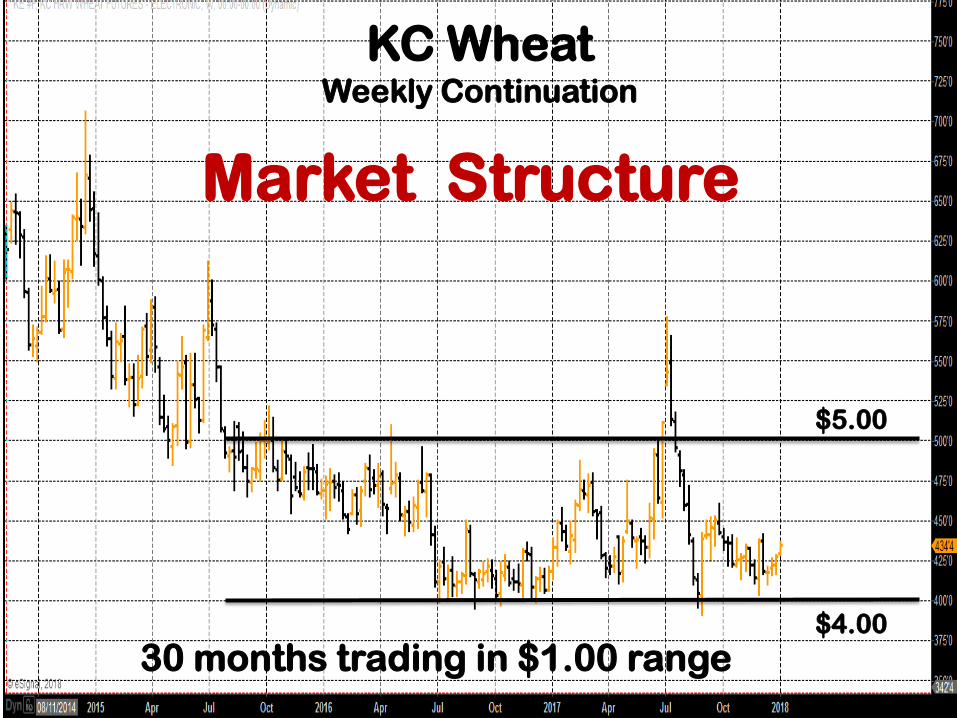

KC WheatWeekly Continuation

$5.00

$4.0030 months trading in $1.00 range

Market Structure

2018 KC Wheat Risk And Hedge Directive

Potential price risk in 2018 = $3.90 futures(2015 low)

You should have order in place to buy…$5.20 September “puts” at 30 cents

on 40% of APH production

$4.50

$3.00

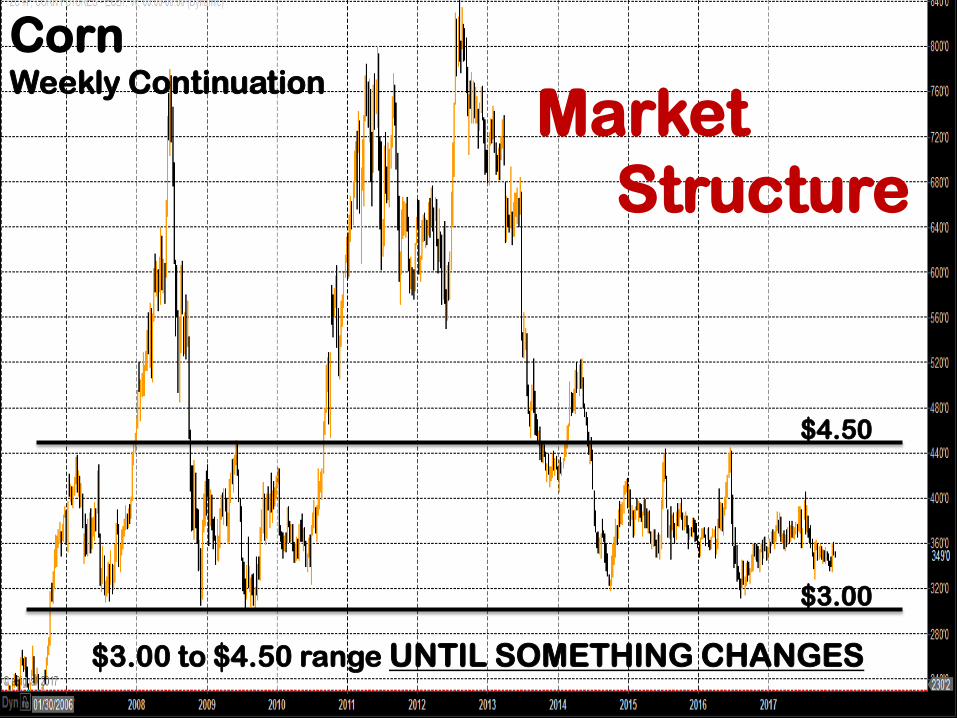

$3.00 to $4.50 range UNTIL SOMETHING CHANGES

Market Structure

CornWeekly Continuation

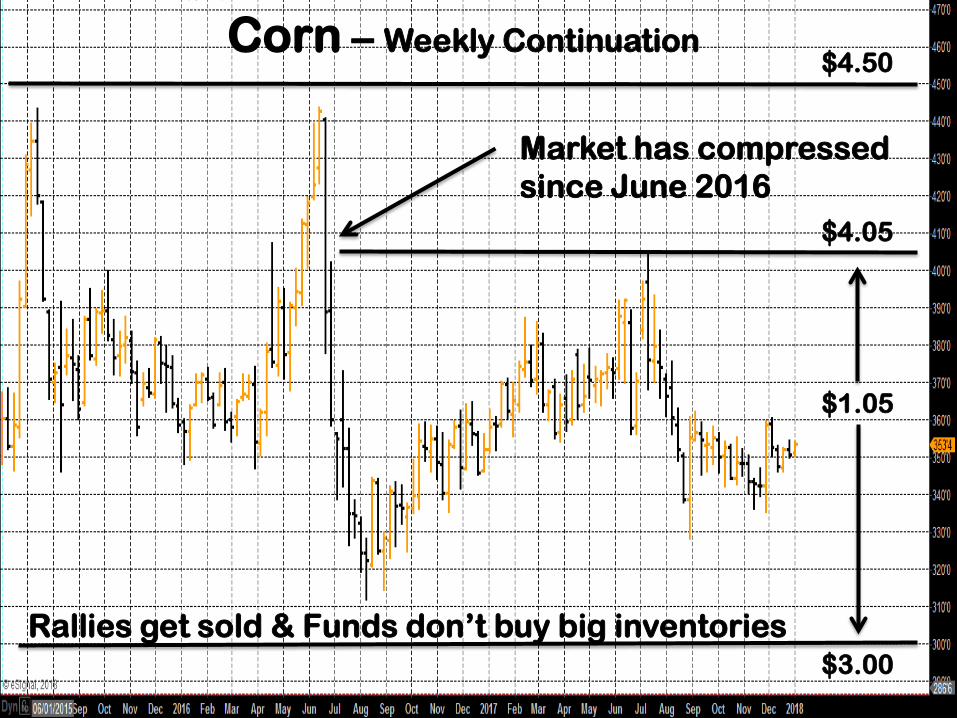

Corn – Weekly Continuation$4.50

$4.05

Market has compressedsince June 2016

$3.00

$1.05

Rallies get sold & Funds don’t buy big inventories

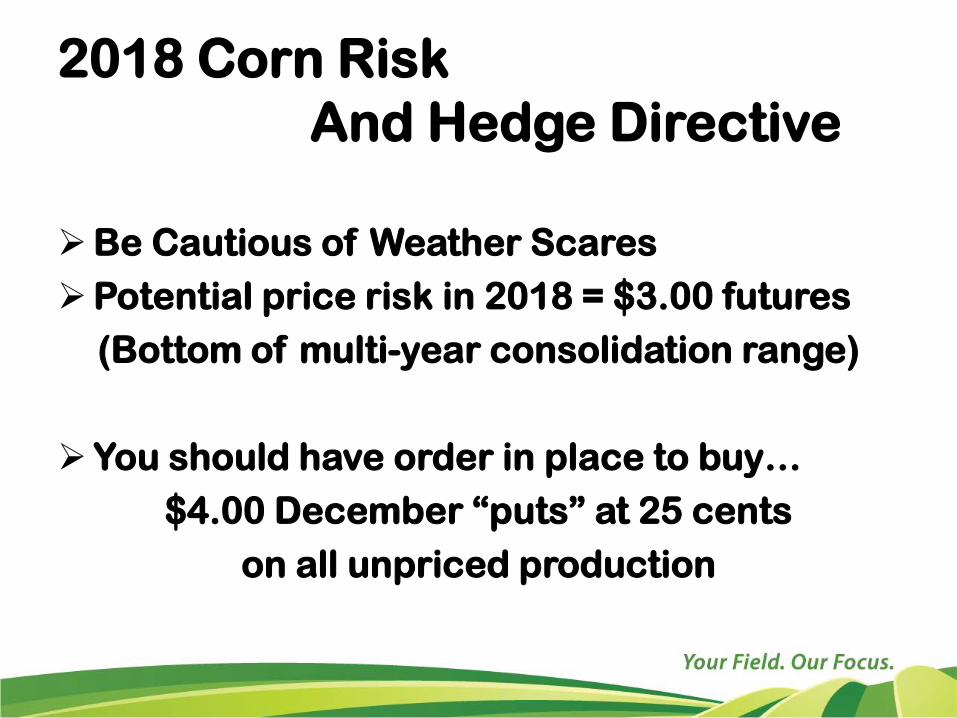

2018 Corn Risk And Hedge Directive

Be Cautious of Weather ScaresPotential price risk in 2018 = $3.00 futures

(Bottom of multi-year consolidation range)

You should have order in place to buy…$4.00 December “puts” at 25 cents

on all unpriced production

Seriously –

Marketing has become more difficult in these low-price, compressed trading ranges

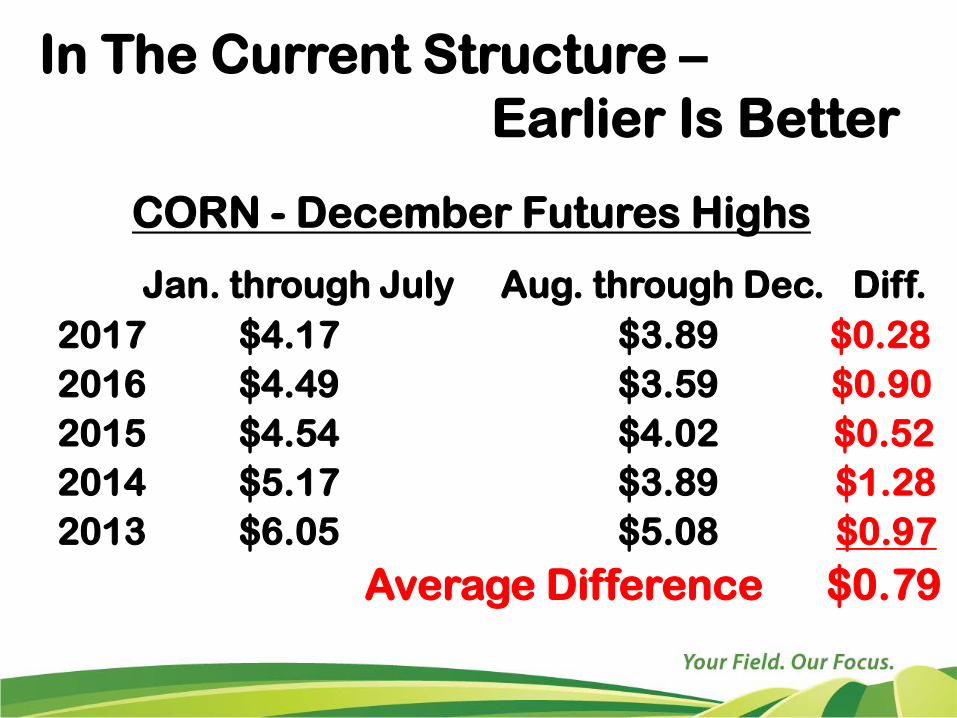

In The Current Structure –Earlier Is Better

CORN - December Futures Highs

Jan. through July Aug. through Dec. Diff.2017 $4.17 $3.89 $0.28 2016 $4.49 $3.59 $0.902015 $4.54 $4.02 $0.522014 $5.17 $3.89 $1.282013 $6.05 $5.08 $0.97

Average Difference $0.79

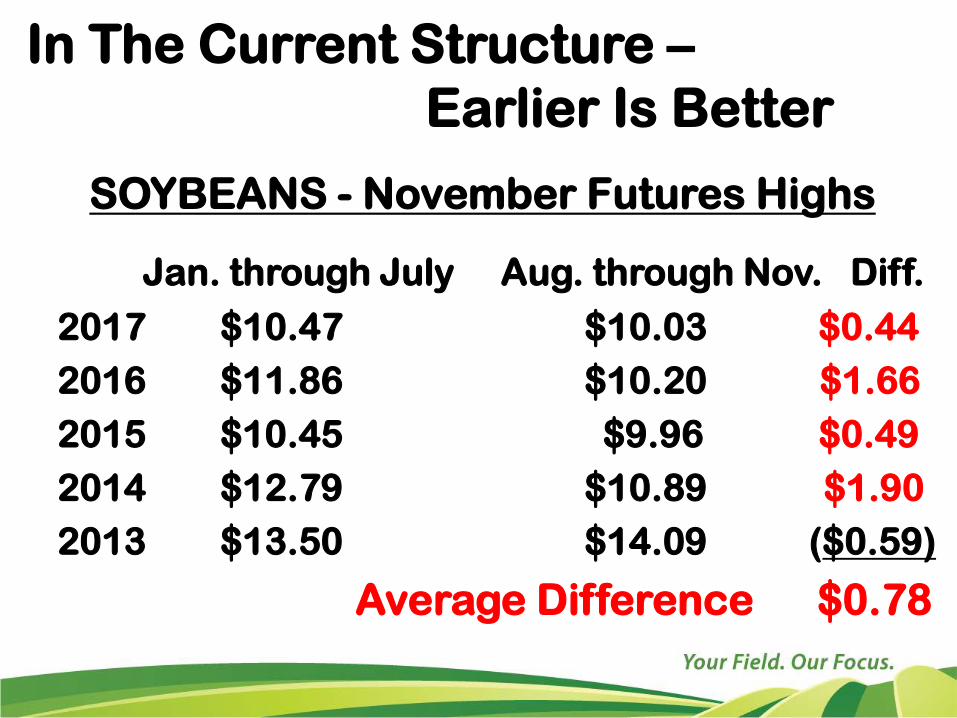

In The Current Structure –Earlier Is Better

SOYBEANS - November Futures Highs

Jan. through July Aug. through Nov. Diff.

2017 $10.47 $10.03 $0.442016 $11.86 $10.20 $1.662015 $10.45 $9.96 $0.492014 $12.79 $10.89 $1.902013 $13.50 $14.09 ($0.59)

Average Difference $0.78

2018 Sales Targets

Fundamentals and structure argue for more aggressive sales percentages at lower prices

Can we be more aggressive in 2018?

What tools can help you?

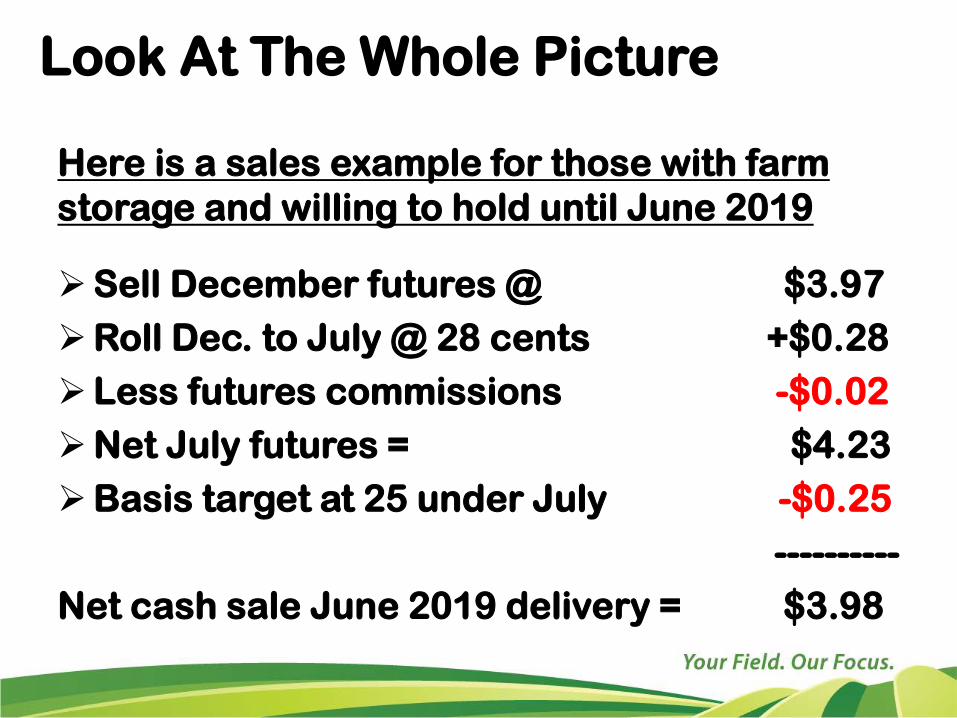

Look At The Whole Picture

Here is a sales example for those with farm storage and willing to hold until June 2019

Sell December futures @ $3.97Roll Dec. to July @ 28 cents +$0.28Less futures commissions -$0.02Net July futures = $4.23Basis target at 25 under July -$0.25

----------Net cash sale June 2019 delivery = $3.98

For Our Visitors

A Challenge For You

“A call to action”

Questions For YOU!

Discuss with your spouse, partners and your lender…

What are your needs and wants?

How important is production marketing in getting these?

Are you interested in a structured approach to production marketing?

Your Marketing Partners

Thank You From Our Entire Team!

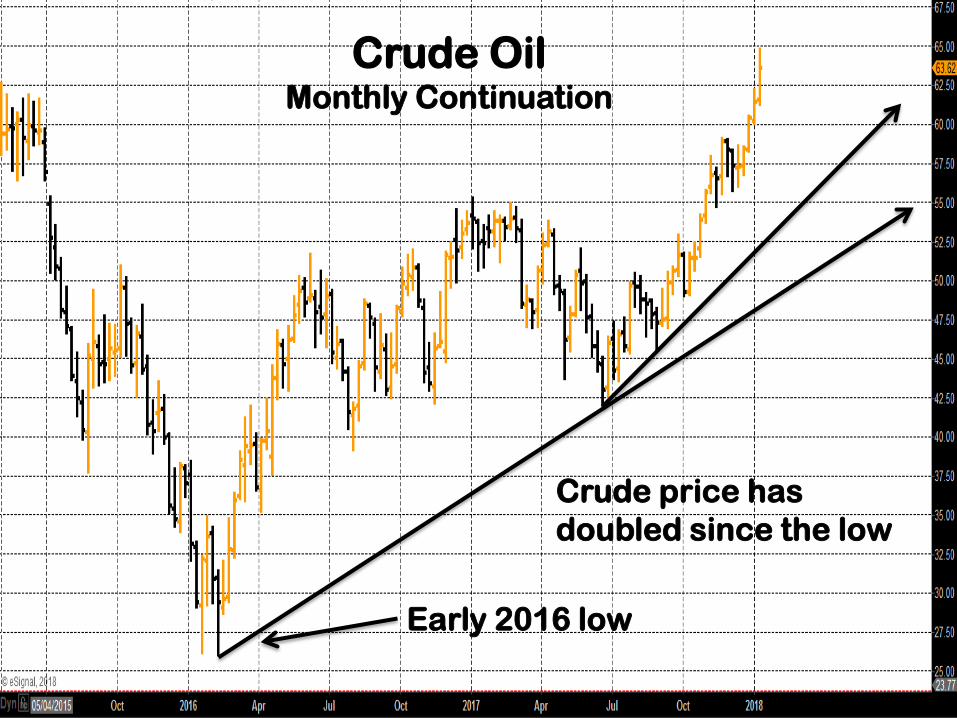

Crude Oil Monthly Continuation

Early 2016 low

Crude price has doubled since the low

Blue = Corn Monthly Cont.Red = Crude Monthly Cont.

1995 to Current

Introducing

Enhancing relationships across 5 states

Customer relationships

Over 1,000 ag related professionals who receive our weekly market commentary

Trusted awareness thru a network of the right folks in ag

Structure of AgWest Land Brokers

Partners with George Clift, Amarillo TX

Jeff Moon is heading up the ALB initiative

Aggressively developing a network of AgWest Land agents

Why would you use AgWest Land Brokers?

Both buyers and sellers will benefit from the network of relationships

ALB will operate with the same ethical standards and integrity as we have from the beginning

Stay In Touch

Website – www.agwestland.com

Sign up for new listing alerts

Sign up for “New Listing” alerts

Stay In Touch

Website – www.agwestland.com

Sign up for new listing alerts

Let your AgWest representative know your land needs

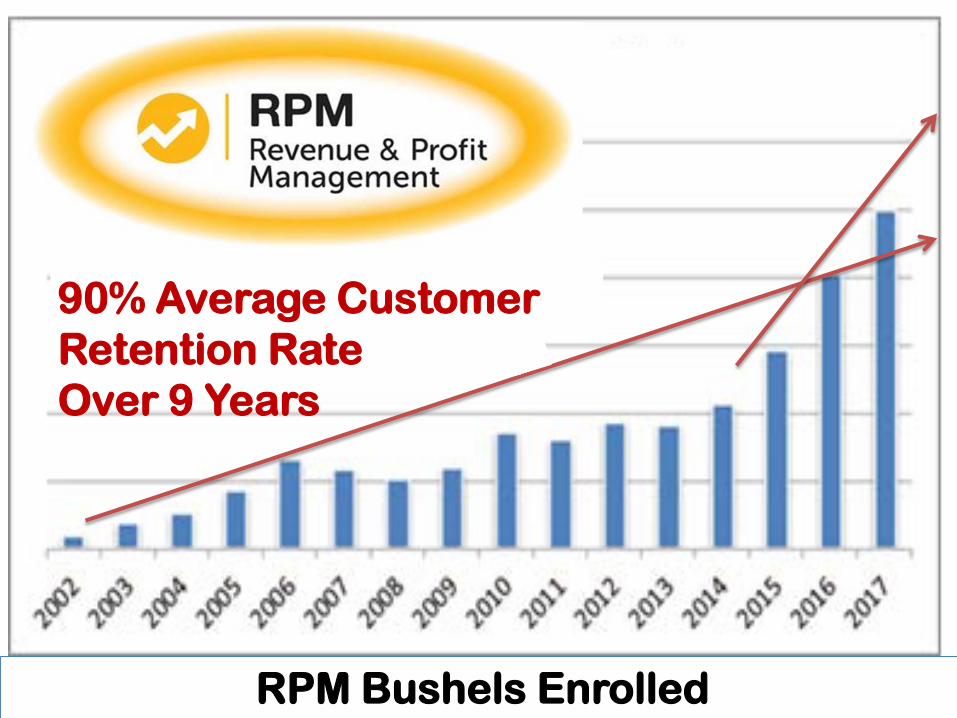

RPM Bushels Enrolled

90% Average Customer Retention Rate Over 9 Years

There are 2 phases to MARKETING PLANNINGA C T I O N

Emotions can derail a good plan

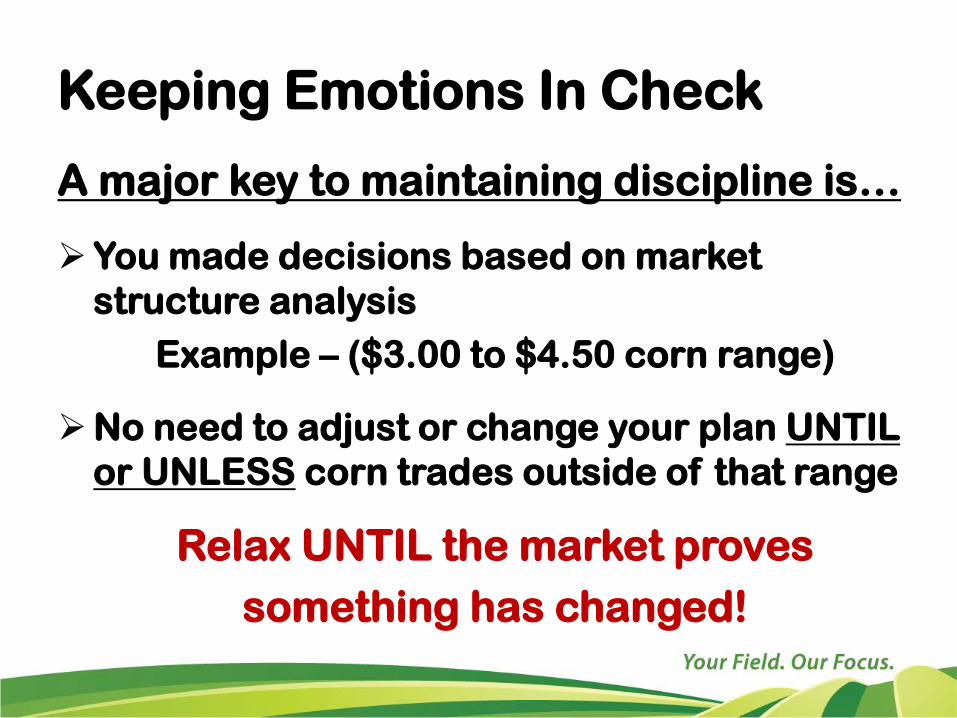

Keeping Emotions In Check

A major key to maintaining discipline is…

You made decisions based on market structure analysis

Example – ($3.00 to $4.50 corn range)

No need to adjust or change your plan UNTILor UNLESS corn trades outside of that range

Relax UNTIL the market proves something has changed!

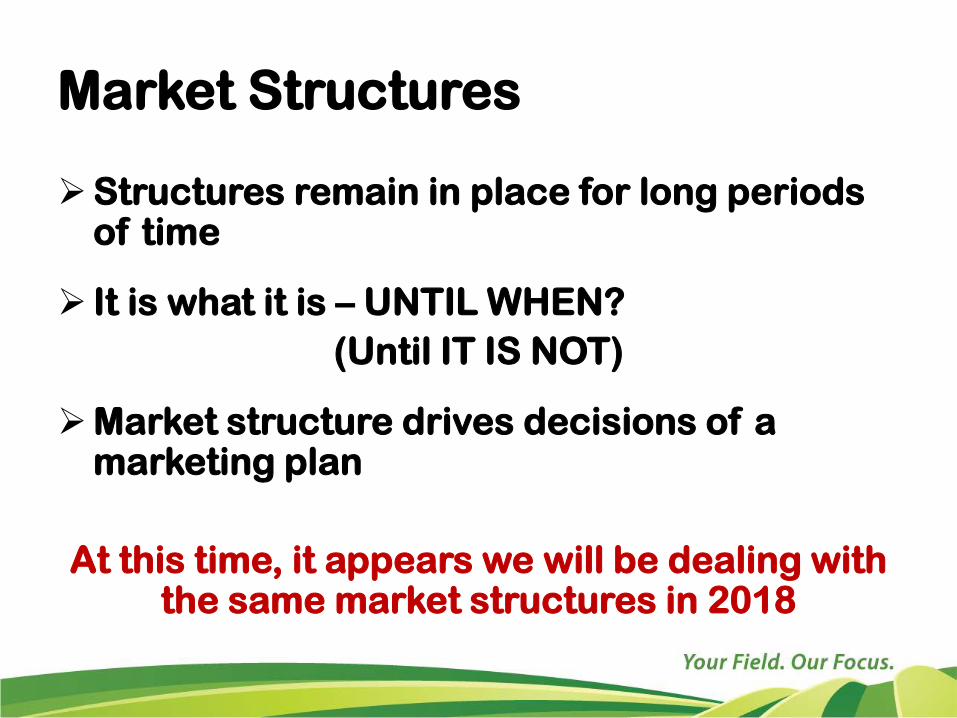

Market Structures

Structures remain in place for long periods of time

It is what it is – UNTIL WHEN?(Until IT IS NOT)

Market structure drives decisions of a marketing plan

At this time, it appears we will be dealing with the same market structures in 2018

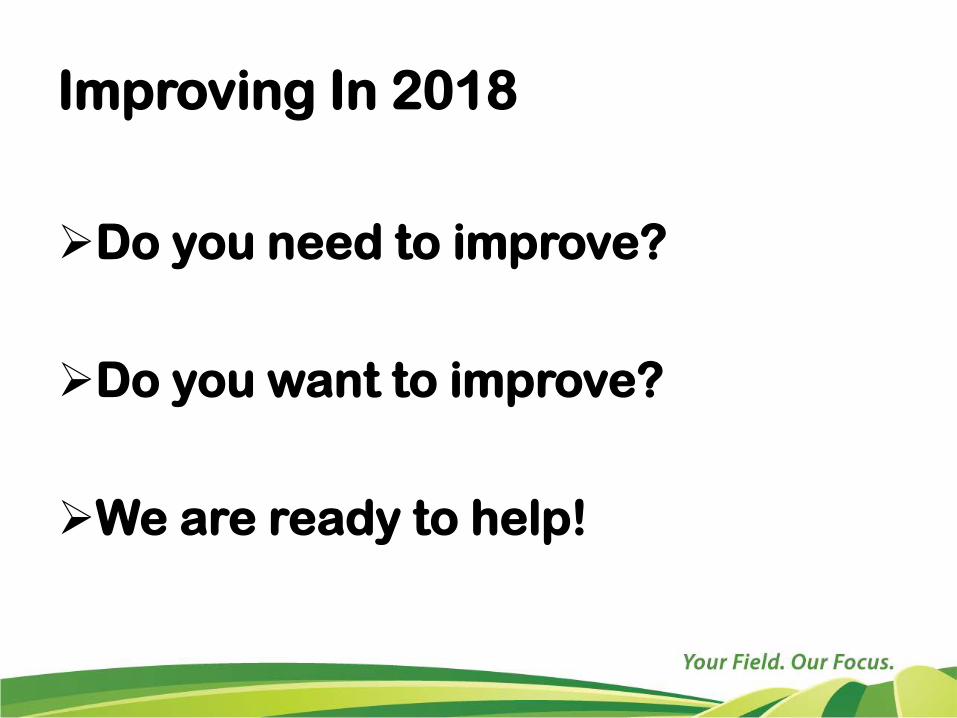

Improving In 2018

Do you need to improve?

Do you want to improve?

We are ready to help!

Questions For YOU!

Discuss with your spouse, partners and your lender…

Are you satisfied with your current marketing results?

What is your marketing philosophy… do you have a marketing philosophy?

Questions For YOU!

Discuss with your spouse, partners and your lender…

If your marketing needs improvement, what steps need to be taken?

Are you ready for a marketing partner?

We would appreciate the opportunity to be on your short list of choices!