Embed Size (px)

Citation preview

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 1

2013 CONGREGATIONAL ECONOMIC IMPACT STUDY

THE RECESSION &

ITS IMPLICATIONS FOR CONGREGATIONAL LIFE

PRESENTED BY WILLIAM G. ENRIGHT

1

Lake Institute on Faith & Giving IU Lilly Family School of Philanthropy

2

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 2

2013 CONGREGATIONAL ECONOMIC IMPACT STUDY

(CEIS)

In partnership with Alban Institute NACBA Indianapolis Center for Congregations Maximum Generosity

3 www.philanthropy.iupui.edu/congregational-economic-impact-study

Respondents by denomination type

4

2013 CEIS Demographics

Denomination Percent Mainline Protestant 60.8%

Evangelical Protestant 24.9%

Other 9.2%

Jewish 2.4%

Catholic 1.1%

Prefer Not to Say/Not Selected 1.1%

Historically Black Protestant 0.6%

Page 46 – Table 8

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 3

By highest percentages reported:

37% of congregations established between 1801-1900

48% suburban

37% have average age of congregants between 55-64

33% have average AGI of congregants of $40K-$60K

37% have average number of people attending weekend services at 101-250 people, followed by 35% at 0-100. 2% are considered mega-churches at 2000+

5

2013 CEIS Demographics

Congregations are recovering from the worst of the recession.

Congregations are not keeping pace with inflation.

Gift size and number of donors are the drivers for fundraising success.

Congregations where the pastor aware if giving patterns do better.

Congregations with younger attendees do better.

Most congregations offer some type of electronic giving.

6

2013 CEIS Key Findings

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 4

Percentage of Congregations Reporting on How They Felt They Weathered the Great Recession

2013 CEIS Weathering the Great Recession

10.3%

63.6%

9.9%

1.1%

13.1%

1.6%

0.5%

Very well

Well

Poorly

Very poorly

Too soon to tell

Don't know

Prefer not to answer

7

Page 14 – Figure 1

28.1%

37.4%

32.7%

1.6% 0.3%

Improved Stayed about the same

Worsened Don't know Prefer not to answer

Percentage of Congregations Reporting Changes in Congregational Finances Since the Worst of the Recession

2013 CEIS Changes in Congregational Finances

8

Page 15 – Figure 2

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 5

2013 CEIS Changes in Revenues

Percentage of Congregations Reporting Changes in Revenues Between 2007 and 2011, Compared with Inflation

16.8%

22.6%

52.0%

8.4%

0.3%

Revenues were ahead of

inflation

Revenues kept pace with inflation

Revenues did not keep pace with inflation

Don't know Prefer not to answer

9

Page 16 – Figure 3

Percentage of Congregations Reporting Changes in Weekly Attendance Following the Recession

2013 CEIS Changes in Weekly Attendance

4.5%

20.2%

38.1%

28.8%

7.1%

1.0%

0.3%

Increased significantly

Increased slightly

Stayed about the same

Declined slightly

Declined significantly

Don't know

Prefer not to answer

10

Page 18 – Figure 5

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 6

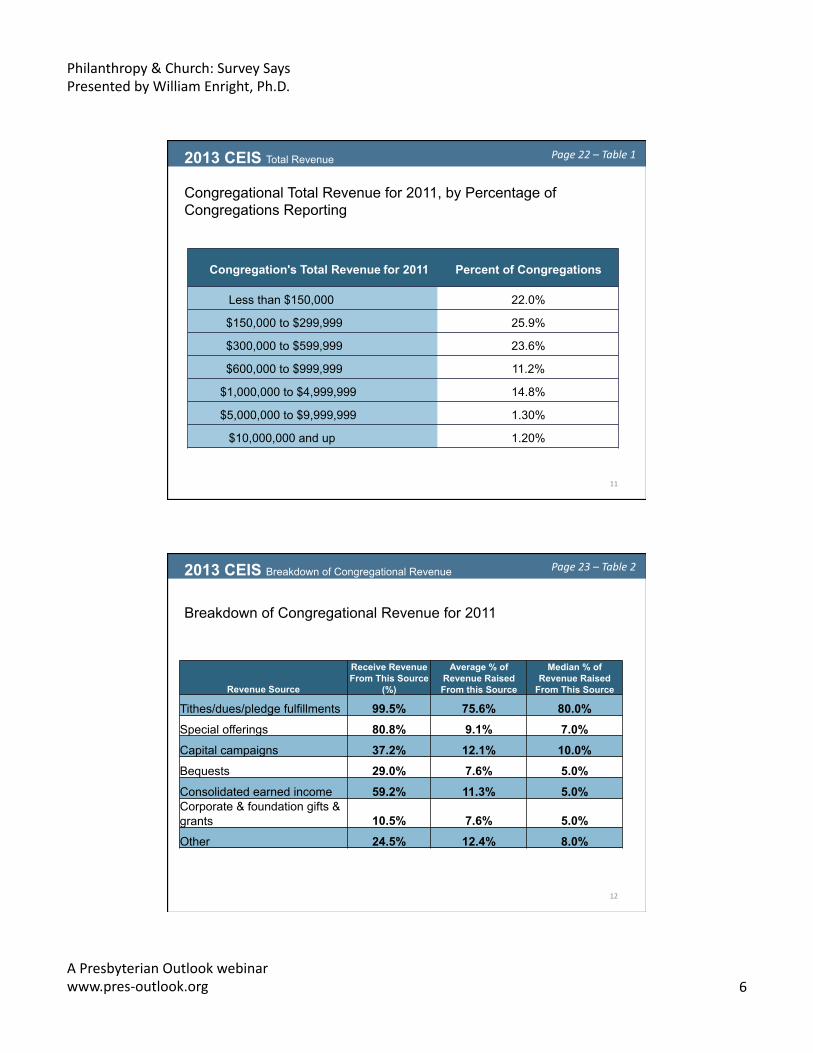

Congregation's Total Revenue for 2011 Percent of Congregations

Less than $150,000 22.0%

$150,000 to $299,999 25.9%

$300,000 to $599,999 23.6%

$600,000 to $999,999 11.2%

$1,000,000 to $4,999,999 14.8%

$5,000,000 to $9,999,999 1.30%

$10,000,000 and up 1.20%

Congregational Total Revenue for 2011, by Percentage of Congregations Reporting

2013 CEIS Total Revenue

11

Page 22 – Table 1

Breakdown of Congregational Revenue for 2011

2013 CEIS Breakdown of Congregational Revenue

12

Revenue Source

Receive Revenue From This Source

(%)

Average % of Revenue Raised From this Source

Median % of Revenue Raised

From This Source

Tithes/dues/pledge fulfillments 99.5% 75.6% 80.0%

Special offerings 80.8% 9.1% 7.0%

Capital campaigns 37.2% 12.1% 10.0%

Bequests 29.0% 7.6% 5.0%

Consolidated earned income 59.2% 11.3% 5.0% Corporate & foundation gifts & grants 10.5% 7.6% 5.0%

Other 24.5% 12.4% 8.0%

Page 23 – Table 2

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 7

Percentage of Congregations Reporting a Change in Overall Pledges or Dues Payments Received Between 2010 and 2011

2013 CEIS Change in Pledges/Payments Received

39.8%

31.1%

22.1%

5.0% 2.0%

Increased Stayed about the same

Decreased Don't know Prefer not to answer

13

Page 24 – Figure 6

Percentage of Congregations Reporting on Clergy’s Awareness of Contributions Received

2013 CEIS Clergy Awareness

44.7 49.3

5.0 1.0

0

10

20

30

40

50

60

Yes No Don't know Prefer not to answer

14

Page 26 – Figure 8

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 8

Percentage of Congregations Reporting a Change in Overall Fundraising Receipts Between 2010 and 2011

2013 CEIS Change in Fundraising Receipts

49.8%

24.1% 21.6%

4.3% 0.3%

Increased Stayed the same

Decreased Don't know Prefer not to answer

15

Page 28 – Figure 9

Factors Respondents Attributed to Increases & Decreases in 2011 Fundraising Results, by Percentage of Congregations Reporting

2013 CEIS Factors Attributed to Increases and Decreases

16

Among those reporting an increase in fundraising: Percent Higher average gifts 53.7% More donors 41.9% Other 23.6% Unexpected bequest or estate gifts 16.2% Unexpected cash gifts 15.4% Expected bequest or estate gifts 2.6%

Among those reporting a decrease in fundraising: Percent Fewer donors 69.0% Lower average gifts 47.8% Other 25.8% Unfulfilled pledges 24.6% Unexpected loss of large gift 14.8%

Page 31 – Table 3

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 9

Percentage of Congregations Reporting Changes in the Budget for 2012, Compared with 2011

2013 CEIS Changes in the Budget

48.9%

24.3% 25.6%

1.0% 0.2%

Increased Stayed the Same

Decreased Don't know Prefer not to answer

17

Page 35 – Figure 12

Percentage of Congregations Reporting Budget Allocation Adjustments for 2012, Compared with 2011

2013 CEIS Budget Allocations

18

Budget Allocation Adjustments Percent of Congregations

Making Increases Percent of Congregations

Making Reductions Salaries 34.2% 13.2% Outreach programs 23.0% 11.7% Revenue-generating activities 18.7% 3.8% Missions activities 18.6% 11.6% Internal programs 16.7% 33.4% Charitable organization support 16.2% 20.3% Staffing 15.5% 25.6% Building maintenance 14.5% 34.7% Employee benefits 9.3% 9.5% Brick-and-mortar projects 9.1% 16.3% Congregational assets 3.5% 4.1%

Page 36 – Table 5

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 10

Number of Employees Part-time Full-time

0 5.2% 5.8%

1 10.6% 37.8%

2 13.9% 15.9%

3 18.2% 10.6%

4 or more 52.1% 29.8%

Paid Congregational Staff Employed in 2011, by Percentage of Congregations Reporting

2013 CEIS Congregational Staff

19

Page 37 – Table 6

Changes in Congregations’ Approaches to Philanthropic Education in Recent Years, by Percentage of Congregations Reporting

2013 CEIS Philanthropic Education

1.9%

3.4% 47.0%

28.3%

13.4%

5.7%

0.3%

Significantly less than prior to the recession

Slightly less than prior to the recession

About the same as prior to the recession

Slightly more than prior to the recession

Significantly more than prior to the recession

Don't know

Prefer not to answer

20

Page 38 – Figure 13

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 11

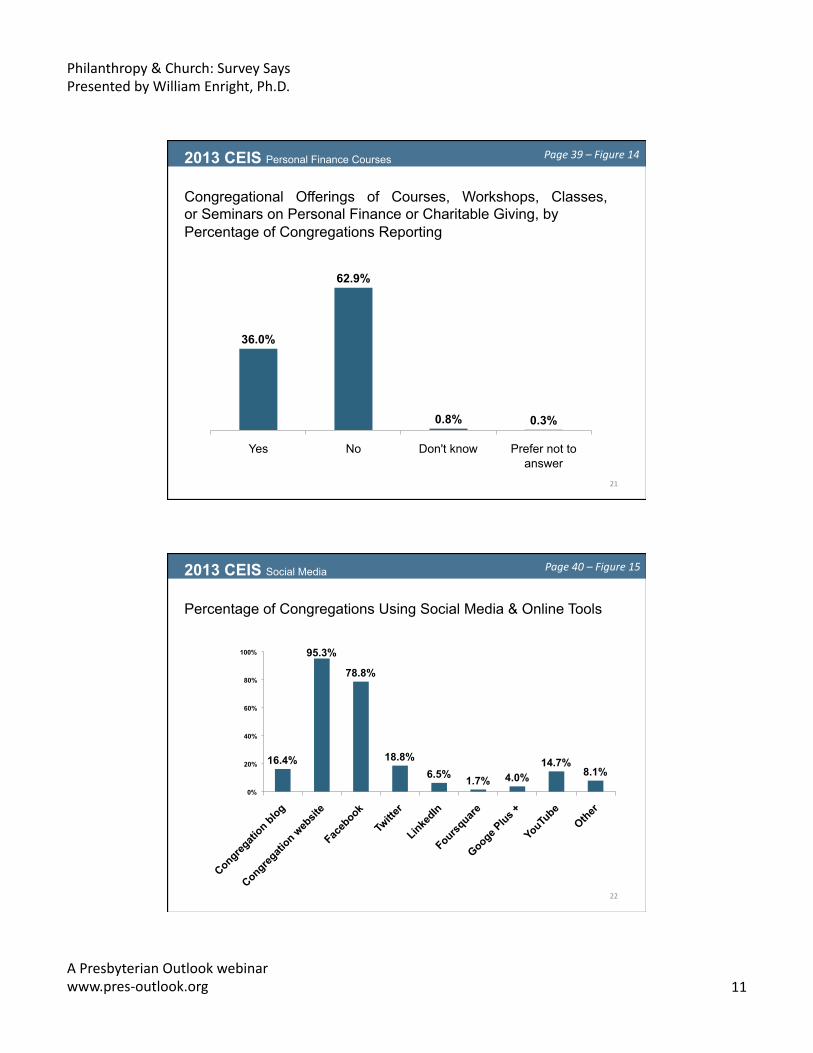

Congregational Offerings of Courses, Workshops, Classes, or Seminars on Personal Finance or Charitable Giving, by Percentage of Congregations Reporting

2013 CEIS Personal Finance Courses

36.0%

62.9%

0.8% 0.3%

Yes No Don't know Prefer not to answer

21

Page 39 – Figure 14

Percentage of Congregations Using Social Media & Online Tools

2013 CEIS Social Media

16.4%

95.3%

78.8%

18.8% 6.5% 1.7% 4.0%

14.7% 8.1%

0%

20%

40%

60%

80%

100%

22

Page 40 – Figure 15

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 12

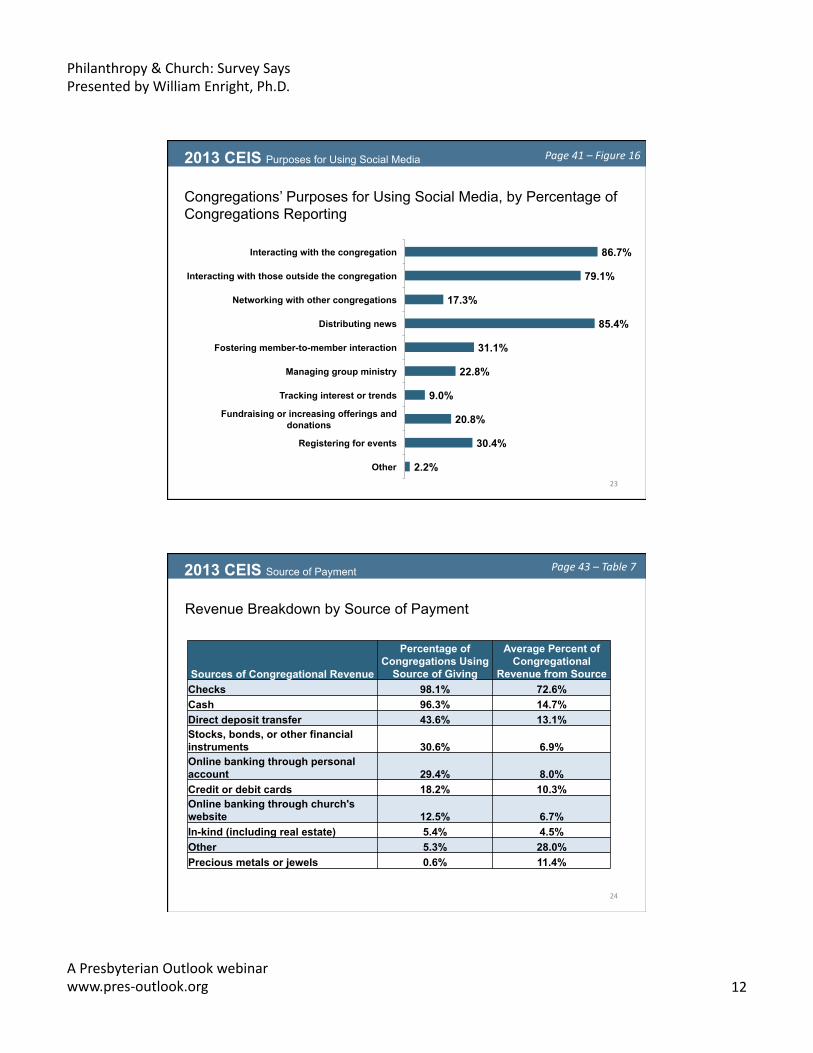

Congregations’ Purposes for Using Social Media, by Percentage of Congregations Reporting

2013 CEIS Purposes for Using Social Media

86.7%

79.1%

17.3%

85.4%

31.1%

22.8%

9.0%

20.8%

30.4%

2.2%

Interacting with the congregation

Interacting with those outside the congregation

Networking with other congregations

Distributing news

Fostering member-to-member interaction

Managing group ministry

Tracking interest or trends

Fundraising or increasing offerings and donations

Registering for events

Other 23

Page 41 – Figure 16

Revenue Breakdown by Source of Payment

2013 CEIS Source of Payment

24

Sources of Congregational Revenue

Percentage of Congregations Using

Source of Giving

Average Percent of Congregational

Revenue from Source Checks 98.1% 72.6% Cash 96.3% 14.7% Direct deposit transfer 43.6% 13.1% Stocks, bonds, or other financial instruments 30.6% 6.9% Online banking through personal account 29.4% 8.0% Credit or debit cards 18.2% 10.3% Online banking through church's website 12.5% 6.7% In-kind (including real estate) 5.4% 4.5% Other 5.3% 28.0% Precious metals or jewels 0.6% 11.4%

Page 43 – Table 7

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 13

Average Income of Congregants, by Percentage of Congregations Reporting

Average Adjusted Gross Income of Families Within

Congregation Percentage

$40,000 or less 10.5%

$40,001 to $60,000 32.7%

$60,001 to $80,000 29.3%

$80,001 or more 15.8%

Don't know 11.2%

Prefer not to answer 0.5%

2013 CEIS Average Income of Congregants

25

Page 50 – Table 12

Average Number of People Attending Typical Weekend Services

2013 CEIS Attendance

26

Average Number of People Attending Weekend Services Percentage

0 to 100 people 34.8%

101 to 250 people 36.9%

251 to 500 people 16.0%

501 to 1000 people 6.9%

1001 to 2000 people 3.1%

2000 people or more 1.8%

Don't know 0.4%

Page 51 – Table 13

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 14

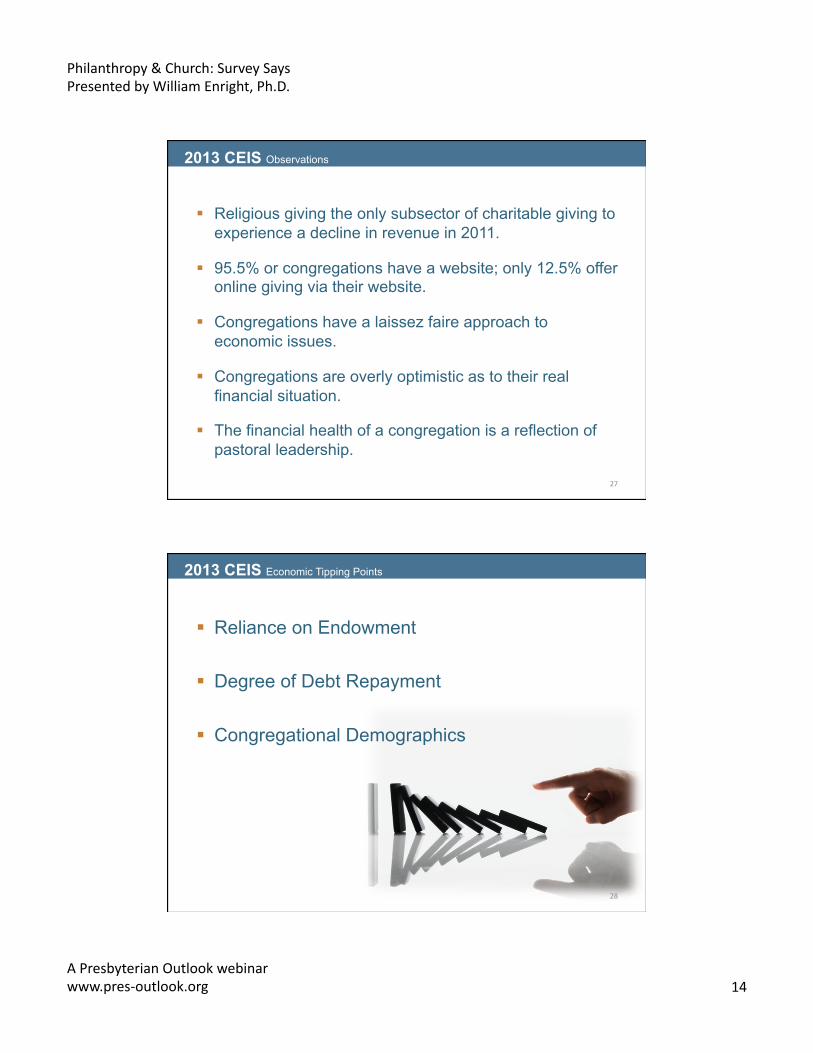

Religious giving the only subsector of charitable giving to experience a decline in revenue in 2011.

95.5% or congregations have a website; only 12.5% offer online giving via their website.

Congregations have a laissez faire approach to economic issues.

Congregations are overly optimistic as to their real financial situation.

The financial health of a congregation is a reflection of pastoral leadership.

27

2013 CEIS Observations

Reliance on Endowment

Degree of Debt Repayment

Congregational Demographics

28

2013 CEIS Economic Tipping Points

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 15

1. Mainline Protestant & Jewish congregations are more likely to have an annual pledge campaign and an endowment.

2. Evangelical congregations are more likely to offer courses in personal financial management.

“Differences in institutionalized practices are theological differences.” Mark Chaves

29

2013 CEIS Theology & Giving Practices

A theological footprint shapes giving practices

30

2013 CEIS The Religious Language Conundrum

The Language of Obligation

The Language of Reciprocity

The Language of Gratitude

How Does Theology Shape the Practice of Giving?

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 16

“The Christian life cannot have obligation as its deepest root. The life of faith is entirely responsive, springing from gratitude rather than duty.” Sondra Wheeler

“When we understand the grace we’ve received, we are able to turn outward in gratitude and generosity.” Christine D. Pohl

31

2013 CEIS Faith, Money & Giving

DONOR SENSITIVITY FUTURE CHALLENGES OF RELIGIOUS GIVING

32

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 17

Increased competition for the Almighty’s Dollar

Religious market share declining

The challenges of an uncertain economy

Donor’s increasing philanthropic savvy

Religion must learn to make its case/tell its story

Church must change its dialogue on money

33

Donor Sensitivity The New World of Religious Giving

DONOR SENSITIVITY Congregations and Social Media

95.3% of congregations have a website

79.8% of congregations use Facebook

80% of church attendees use email and the web.

Only 25% of attendees use it relative to their church.

“Religion is for the most part an insignificant participant in social media.”

Scott Thumma

2013 CEIS Report, Indiana University Lilly Family School of Philanthropy Third Annual Biennial Conference on Religion and American Culture, June 2013

34

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 18

1. What is your mission; what do you do?

2. Who are the people you serve; what needs do you address?

3. Are you in debt? If so, how are you addressing your debt?

4. What is your impact on your immediate community?

5. What programs and missions do you fund?

6. Do you have a strategic plan and goals for the future?

7. What does success look like in your congregation?

35

Donor Sensitivity: What Donors Want to Know

1. Why do you exist?

2. How do you behave?

3. What do you do?

4. What is important to you right now?

5. What does tomorrow look like?

6. What must you do now?

36

Donor Sensitivity Questions to Clarify your Organization’s Vision

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 19

NURTURING A CULTURE OF

GENEROSITY

37

CULTURE OF GENEROSITY Organizational Structure of Generosity

Keys to Building an Organizational Structure of Generosity

ATTITUDE: How does leadership feel about fundraising as a core

value?

ADVOCACY: How do your members & donors understand and

articulate your mission?

ACTION: How do you engage your staff in nurturing generosity? What steps do you need to take in building an

organizational culture of generosity?

38

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 20

CULTURE OF GENEROSITY Three Dimensions

Organizational Culture is Three-Dimensional

ARTIFACTS: The visible organizational structures and processes

ESPOUSED BELIEFS & VALUES: Organizational strategies, goal, philosophies, tenets

of faith

UNDERLYING ASSUMPTIONS: The unconscious, presumed beliefs, feelings,

perceptions

Edgar Schein: Organizational Culture and Leadership. 39

CULTURE OF GENEROSITY Four Frames

Four Frames of an Organization

1. STRUCTURAL FRAME: Organizational goals, roles, relationships.

2. HUMAN RESOURCE FRAME: People, their needs, feelings, prejudices, skills, limitations

3. POLITICAL FRAME: Areas where subjective interest groups vie for power & the use of resources.

4. SYMBOLIC FRAME: Organizational cultures: rituals, ceremonies, stories, myths, policies, heroes.

L. G. Boleman and T.E. Deal, Reframing Organization 40

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 21

THE WHY AND HOW

OF CHANGE

41

WHY & HOW Why Change?

Reasons for Strategic Change Initiatives

To improve and/or stabilize performance

To adapt to changes in the external environment & position an organization for the future

42

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 22

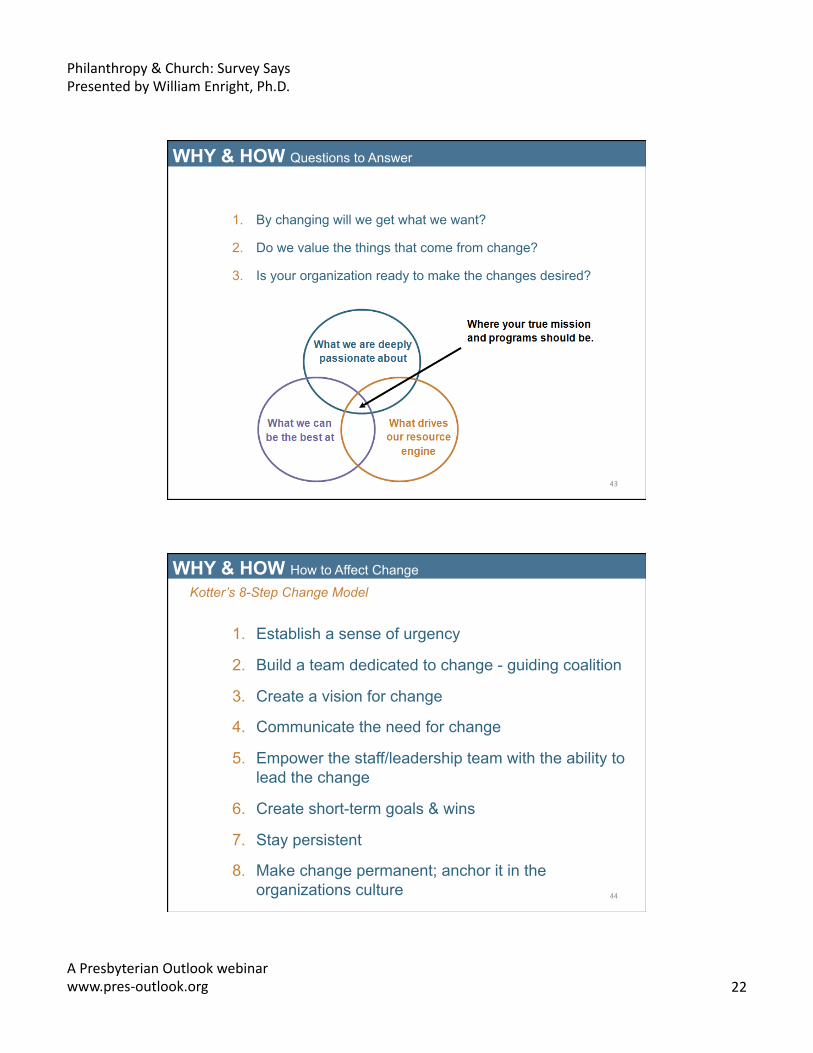

WHY & HOW Questions to Answer

1. By changing will we get what we want?

2. Do we value the things that come from change?

3. Is your organization ready to make the changes desired?

43

WHY & HOW How to Affect Change

Kotter’s 8-Step Change Model

1. Establish a sense of urgency

2. Build a team dedicated to change - guiding coalition

3. Create a vision for change

4. Communicate the need for change

5. Empower the staff/leadership team with the ability to lead the change

6. Create short-term goals & wins

7. Stay persistent

8. Make change permanent; anchor it in the organizations culture 44

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 23

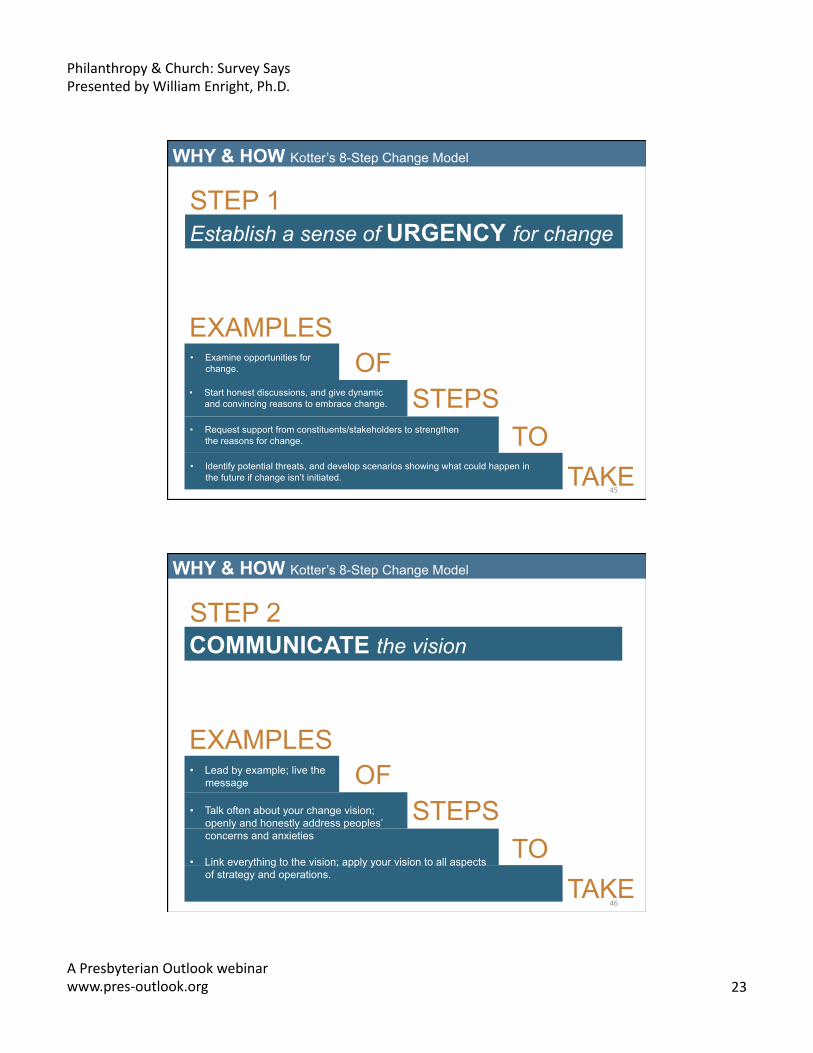

WHY & HOW Kotter’s 8-Step Change Model

STEP 1

Establish a sense of URGENCY for change

TAKE

• Start honest discussions, and give dynamic and convincing reasons to embrace change.

• Request support from constituents/stakeholders to strengthen the reasons for change.

• Identify potential threats, and develop scenarios showing what could happen in the future if change isn’t initiated.

EXAMPLES

STEPS

• Examine opportunities for change.

TO

OF

45

WHY & HOW Kotter’s 8-Step Change Model

STEP 2

COMMUNICATE the vision

TAKE

• Talk often about your change vision; openly and honestly address peoples’ concerns and anxieties

• Link everything to the vision; apply your vision to all aspects of strategy and operations.

EXAMPLES

STEPS

• Lead by example; live the message

TO

OF

46

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 24

WHY & HOW Kotter’s 8-Step Change Model

STEP 3

TAKE

• Include the change ideals and values when hiring and training new staff.

• Publicly recognize key members of your original change team, and make sure others recognize and remember their contributions.

• Create plans to replace key leaders of change as they move on to ensure their legacy is not lost or forgotten.

EXAMPLES

STEPS

• Constantly talk about progress and success stories to inspire others.

TO

OF

Make the change PERMANENT anchor it in the organiza>on’s culture

47

Get the message right

Be personal and specific

Tell your story with passion

Be financially accountable

Create big giving opportunities

Celebrate your successes

WHY & HOW Putting Generosity into Practice

48

Philanthropy & Church: Survey Says Presented by William Enright, Ph.D.

A Presbyterian Outlook webinar www.pres-‐outlook.org 25

REFLECT • DISCUSS • CONNECT

Connect with Lake Institute on Faith & Giving

EMAIL: [email protected]

PHONE: 317-278-8998

WEBSITE: www.philanthropy.iupui.edu/lake-institute

TWITTER: @LakeInstitute

49