Embed Size (px)

Citation preview

It’s a new world!Health Care Changes and the ACA

2

• MHC – Who we are• Understanding the Problem• Understanding the Affordable Care

Act• Understanding Insurance Exchanges• Moving Forward

Today’s Agenda

Montana Health CO-OP: Who We Are

4

Who is MHC?

• Member-operated health CO-OP• Non-profit organization• Home-grown (Helena-based)• Funded via federal start-up loans• CO-OPs currently approved in 24

states• Offering products via the Health

Insurance Exchange

Health Care: Understanding the Problem

6

Health Care Problems

• Insurance Situation• 50 million uninsured Americans• 200,000 uninsured Montanans• Premiums double in last 10 years• 62% of all bankruptcies medically-related

7

Health Care Problems

Insurance Situation• Coverage isn’t comprehensive• Affordability• Emphasis on group/employer-provided

insurance.• Pre-existing condition clause• Fear of losing coverage with job

loss/change• Insurance denied if no continuity of

coverage

Health Insurance Exchanges & the ACA

9

Health Insurance Exchanges

Internet-based marketplaces to shop for and buy health insurance

• Compare apples to apples (tiers of coverage)• Determine eligibility for premium subsidies• Plans on the exchange must offer Essential Health Benefits• 278,000 Montanans could get insurance via the Exchange• Congress and their staff will get insurance from the

Exchange

Exchange = Marketplace

10

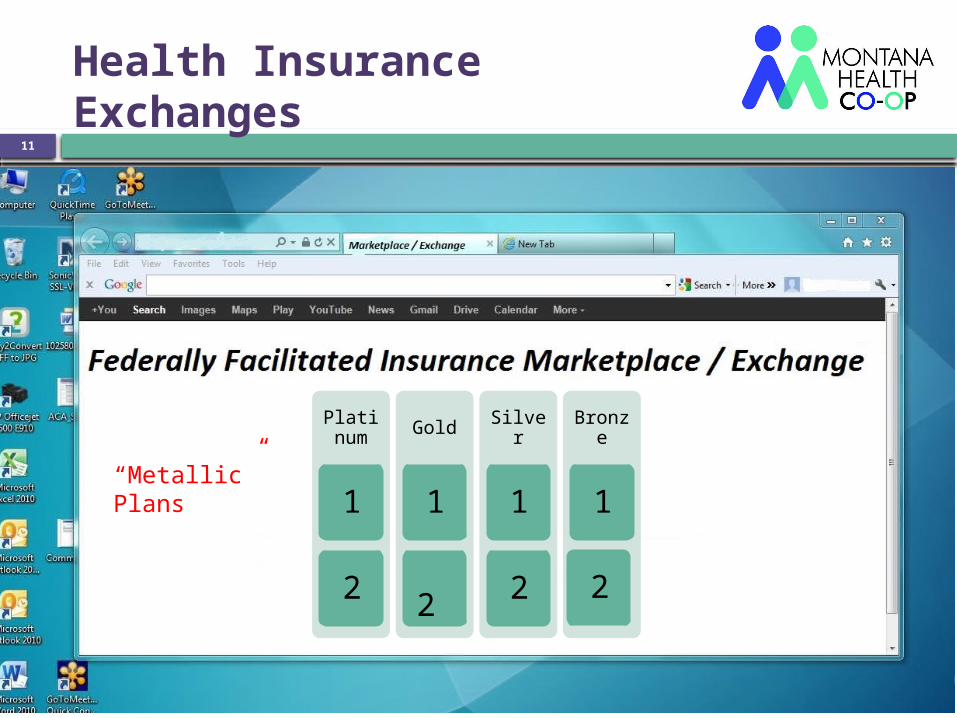

Health Insurance Exchanges

11

Health Insurance Exchanges

Platinum

1

2

Gold

1

22

Silver

1

2

Bronze

1

2

“Metallic” Plans

Solutions

• Open Enrollment/Guaranteed Coverage

12

Gold Silver Bronze$750 Deductible $2,000 Deductible $4,000 Deductible

80/20 70/30 60/40

ACA Subsidies

For qualifying individuals and families without employer-based insurance. Subsidies are not for those receiving Medicare.

Starting in 2014

• Subsidies (advanceable tax credits) to offset monthly premiums for those with income between 100-400% of the Federal Poverty Level (FPL).

• 65% of Montana families have incomes below 340% of the FPL.

13

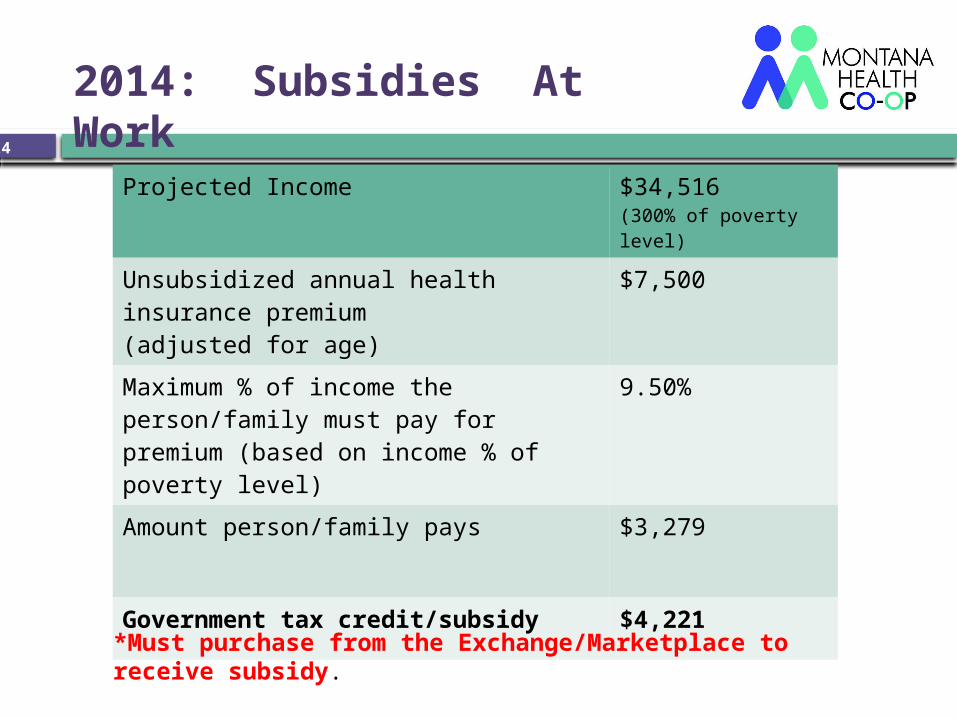

Projected Income $34,516 (300% of poverty level)

Unsubsidized annual health insurance premium (adjusted for age)

$7,500

Maximum % of income the person/family must pay for premium (based on income % of poverty level)

9.50%

Amount person/family pays $3,279

Government tax credit/subsidy $4,221

2014: Subsidies At Work14

*Must purchase from the Exchange/Marketplace to receive subsidy.

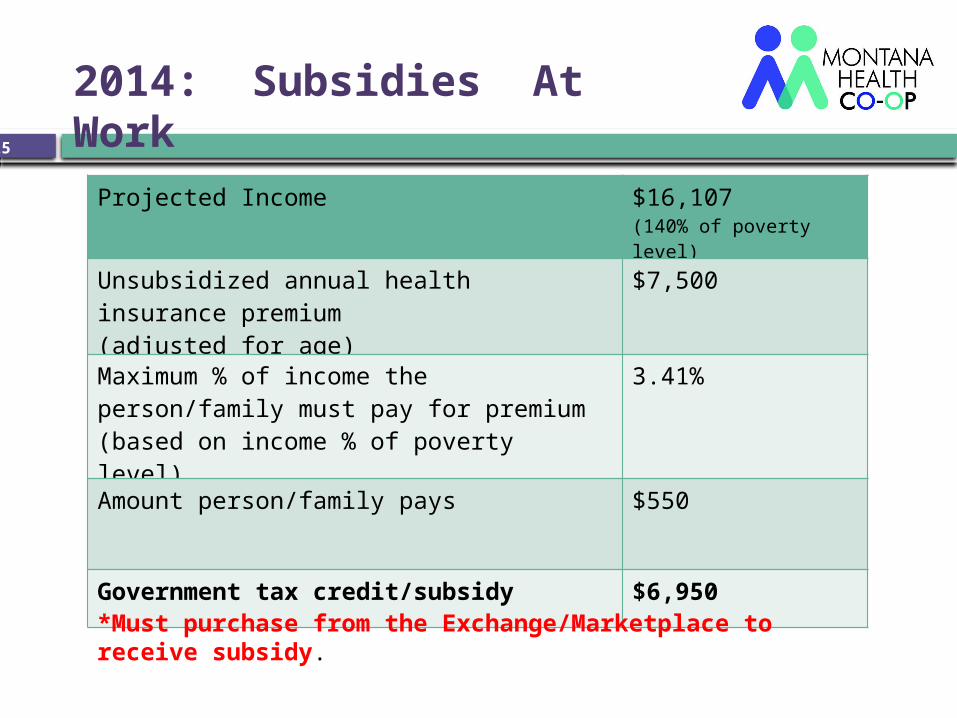

2014: Subsidies At Work15

Projected Income $16,107 (140% of poverty level)

Unsubsidized annual health insurance premium (adjusted for age)

$7,500

Maximum % of income the person/family must pay for premium (based on income % of poverty level)

3.41%

Amount person/family pays $550

Government tax credit/subsidy $6,950

*Must purchase from the Exchange/Marketplace to receive subsidy.

Subsidies At Work16

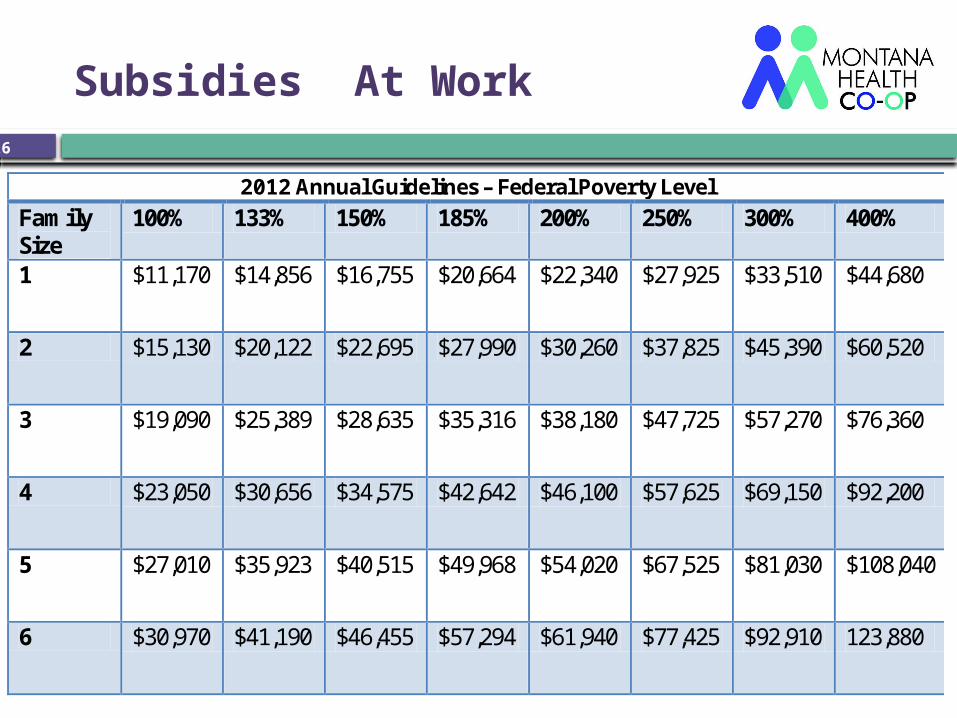

2012 Annual Guidelines – Federal Poverty Level

Family Size

100% 133% 150% 185% 200% 250% 300% 400%

1 $11,170 $14,856 $16,755 $20,664 $22,340 $27,925 $33,510 $44,680

2 $15,130 $20,122 $22,695 $27,990 $30,260 $37,825 $45,390 $60,520

3 $19,090 $25,389 $28,635 $35,316 $38,180 $47,725 $57,270 $76,360

4 $23,050 $30,656 $34,575 $42,642 $46,100 $57,625 $69,150 $92,200

5 $27,010 $35,923 $40,515 $49,968 $54,020 $67,525 $81,030 $108,040

6 $30,970 $41,190 $46,455 $57,294 $61,940 $77,425 $92,910 123,880

ACA Subsidies

Subsides will ensure qualifying households pay no more than a specific percentage of income on premiums:

Percentage of household income is a sliding scale based on the Federal poverty level (FPL) of the family involved:

• Up to 133% FPL: 2% of income• 133-150% FPL: 3.0% – 4.0% of income• 150-200% FPL: 4.0% – 6.3% of income• 200-250% FPL: 6.3% – 8.05% of income• 250-300% FPL: 8.05% – 9.5% of income• 300-400% FPL: Capped to 9.5% of income

Source: (PPACA §§ 1401, 10105; HCERA § 1001; IRC § 36B)

17

ACA Catch-22

What is affordable?

Employers: W-2, Box 1 9.5% of salary

Employees: 1040, MAGI, 9.5% of income

IRS: 8% of household income

18

Understanding the Affordable Care Act (ACA)

Affordable Care Act (ACA)

20

Signed into law March 2010

• Expand Medicaid• Encourage employers to offer health insurance.• Provide premium subsidies • Establish health insurance exchanges• Strengthen consumer protections• Impose protections to guard against

unreasonable rate increases.• Encourage primary and preventive care.• Mandate insurance for everyone.

Affordable Care Act (ACA)

Insurance companies cannot:

• Put a lifetime cap on how much they will pay• Cancel coverage by finding a paperwork

error.• Deny coverage based on pre-existing

conditions• Charge women more for coverage

21

Affordable Care Act (ACA)

Making Health Care AffordablePreventative services are free

• Cancer screenings: mammograms & colonoscopies• Vaccinations: flu, mumps & measles• Blood pressure and cholesterol screenings• Tobacco cessation counseling• Depression screening• And more…

22

Affordable Care Act (ACA)

Making Health Care AffordableThe 80/20 Rule

Before…insurance companies spent as much as 40 cents of every premium dollar on overhead, marketing and salaries.

Now…they must spend 80 cents of your premium dollar on your health care or on improvements to care. If they don’t, they must repay the money.

23

24

2014: Changes for Employers

Small employers offering health insurance…

• with 25 or fewer full-time employees • that have average wages under $50K

…are eligible for small business tax credit of 35 percent (increasing to 50% by 2014).

25

2014: Changes for Employers

Businesses with less than 50 full-time employees are exempt from having to offer health insurance to workers.

97% of Montana business have fewer than 50 full-time employees.

80% of Montana employers have fewer than 10 workers.

26

2014: Changes for Employers

Penalties for large companies (50+ workers):

Not offering minimum essential benefit coverage -- $2,000 per full-time worker (subtracts first 30 full-time workers)

Not offering affordable coverage – lesser of $3,000 per full-time employee receiving a subsidy or $2,000 per full-time employee

Excellent Summary:http://laborcenter.berkeley.edu/healthpolicy /“Summary of Provisions Affecting Employer-Sponsored Insurance”

27

Penalties for the Uninsured

2015: Insurers mail a Notice of Insurance (similar to W-2) for taxes.

Income too low to file a federal tax return? Penalties are not meant for you.

2014– $95 per adult and $47.50 per child, up to a family maximum of $285 or 1 percent of family income, whichever is greater

Moving Forward

• Stay informed: Medicaid expansion dead?Will other insurers participate on the exchange?Consider the paradigm shift from group coverage to

individual coverage.Do we have ample primary care physicians?Expect a dramatic change in the health care market.Anticipate the possibility of an insurance shift

(354,000 Montanans may see an insurance change).Know that there will be fine-tuning and clarification

of the ACA.See: www.healthcare.gov

Making the New Laws Work for Montana 29