Embed Size (px)

Citation preview

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 1/38

FEBRUARY 2006

Lakshmi Nambiar, Senior Associate

(+91) 80 5152 4088

Sector Report : IT IndustryMid-Caps: The Untold Story

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 2/38

+ Strong Growth Driven By Structural Shifts In Global IT Industry:

The Indian IT industry is witnessing rapid growth as leading Indian IT

companies globalize their operations, IT multinationals enhance their offshore

presence and as players move up the value chain, offering services like design

conceptualization and implementation, product co-development and IT

infrastructure management.

+ Emergence Of Mid-Caps:

After going through a turbulent phase during the IT industry slowdownbetween 2001-2003, Mid-Caps have emerged larger and stronger. Mid-Caps

have taken bolder strategic decisions than Large-Caps, and have benefited by

them. Based on these strategies, Mid-Caps can be classified into four categories

Niche Service Providers, Multi-Domain Players, Consolidators, and

Solutions/Product Providers.

+ Drivers Of Mid-Cap Growth:

A three-year Compounded Annual Growth Rate (CAGR) analysis of Market Cap

of Mid-Cap companies, post the IT industry slowdown, indicates that

companies with a clear differentiated strategy have performed extremely well.

The strategies include one or a combination of the following - focusing on

intellectual property related products and services, developing leadership along

fast-growing niche markets, focusing on under-served markets and acquiring

strategically.

+ Differentiated Mid-Caps - A Compelling Proposition:

Mid-Cap Market Cap has grown dramatically compared to those of Large-Caps.

The difference is more compelling in the case of the Top 10 performing Mid-Cap

companies who have adopted a differentiated strategy and whose revenue

growth exceeds that of Large-Caps at comparable levels of profitability. The

median three-year CAGR in Market Cap (2002-2005) for Large-Caps was 32%,

compared with 37% for Mid-Caps and 65% for the top 10 performing Mid-Cap

companies.

+ The Road Ahead:

Going forward, we expect the Mid-Cap landscape to be action-packed, with a

number of mergers, acquisitions, private equity plays and public market

offerings, as companies try to move to the next level and fill the void between

the Large-Cap and the Mid-Cap players. (Revenues of the largest Mid-Cap player

in India are less than USD 200 million.) Also, as the level of risk capital available

increases over the next couple of years, we expect more product-centric

companies to grow into the Mid-Cap segment.

Sector Report : IT Industry

Mid-Caps: The Untold Story

Industry Coverage

Lakshmi Nambiar, Senior Associate

(+91) 80 5152 4088

Recent Reports- BPO opportunities in the US Residential

Mortgage Market

- Bioinfomatics

- Analysis of the Non-voice Back Office

Market in India

-The Indian Semiconductor Sector

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 3/38

Table of Contents

List of Exhibits

Executive Summary 01

The Indian IT Industry: A Snapshot 03

Mid-Caps: An Evolution 05

Mid-Caps: Building Market Competitiveness 06

Mid-Caps: Drivers for Growth 09

Differentiated Mid-caps: A Compelling Value Proposition 15

Mid-Caps: The Road Ahead 17

Appendix A: Company Specific Strategy of Top Ten Performers 18

Appendix B: Financials, Growth & Margins and Valuation Analysis 29

Exhibit 1: Indian IT Software and Services Revenues 03

Exhibit 2: Global Delivery Centers for Infosys, Satyam, TCS and Wipro 03

Exhibit 3: IT IPO's in Calendar Year 2005 07

Exhibit 4: Overview of Mid-Cap Landscape 07-08Exhibit 5: Market Cap CAGR Comparison for Mid-Cap Companies 09

Exhibit 6: Strategies of Top Performers 10

Exhibit 7: Emerging Service Offerings for Products 12

Exhibit 8: Acquisitions by Mid-Cap Companies in the Last Twelve Months 13-14

Exhibit 9: Market Cap CAGR for Large-Cap, Mid-Cap and the Top Performers 15

Exhibit 10: Median EBITDA and PAT Comparison 15

Exhibit 11: Median PAT Margin Comparison 15

Exhibit 12: Median Market Cap/Sales comparison 16

Exhibit 13: Median Market Cap/EBITDA Comparison 16

Exhibit 14: Median Market Cap/PAT Comparison 16

Exhibit 15: Private Companies That Might Go Public In The Near Future 17

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 4/38

Emergence of the Indian IT Multinational

Recognizing the impending competition from multinational IT

companies, large Indian IT companies have aggressively

expanded their global footprint over the last few years. They

now offer a Global Delivery Model (GDM) that enables them

to service diverse needs of their clients more effectively than a

“one-size-fits-all” approach. This will also help them hedge

their risks against rapid wage escalation in India and the

growth of other geographies like China and Eastern Europe as

more cost-competitive delivery options. Exhibit 2 illustrates

the emergence of the Indian IT multinational.

Global IT Vendors Embracing India

Indian companies face stiff competition from global IT

vendors (Accenture, IBM, EDS, Cap Gemini) who are

aggressively developing and enhancing their offshore delivery

capability. They are doing this through both organic growth

headcount as well selective strategic acquisitions. For

example, Accenture announced plans to increase its3headcount in India to 22,500 employees in fiscal year 2005 , a

growth of almost 50%.

Furthermore, global IT firms have started taking a long-term

strategic view on the Indian market to position themselves

well for the expected growth in the domestic IT market. IBM's

acquisition of Network Solutions, which provides it an entry

into the domestic IT Infrastructure Management business,

illustrates this early trend. This will create additional pressurefor Indian IT companies on their home turf, a market many

have neglected due to low revenue realizations.

The story of Indian IT Large-Caps is that of relentless

execution, supported by a strong global structural shift in1the IT industry, whereas that of the Indian IT Mid-Caps is

that of bold choices.

In this section, we take a brief snapshot of the Indian IT

industry.

It is a commonly accepted fact that the Indian IT industry

has leveraged offshore delivery capability to position India

as the 'go-to' IT destination in the world. This is evident in

the industry's double-digit growth rate, which validates the

compelling economics of offshore outsourcing.

As the industry assumed a larger scale, many predicted a

slowdown. However, the past year has proved to be a

watershed, as the industry has not only maintained itsmomentum for growth, but has also accelerated it. National

Association of Software and Service Companies (NASSCOM),

the premier Indian IT industry body, has estimated that the

Indian IT and BPO industry recorded revenues of USD 222billion in fiscal year 2005 (ending March 2005) . This

translates into a 32% growth, the highest since 2001, as

illustrated in Exhibit 1. This growth is underlined by certain

long-term structural shifts in the global IT outsourcing

industry as outlined below.

The Indian IT Industry: A Snapshot

Exhibit 1: Indian IT Software & Services Revenues

5

(US $ Billion)

FY04 FY05 FY06 (E)

30

25

20

15

10

0

3.6

3.9

5.2

12

4.8

9.2

15.2

7.3

6.0

ITES-BPO Exports IT Software & Services Exports Domestic Market

Exhibit 1: Indian IT Software & Services Revenues

Source: NASSCOM 2005 Report

Source: Avendus Research

Exhibit 2: Global Delivery Centers for Infosys, Satyam, TCS & Wipro

Infosys TCS SatyamWipro

1For the purpose of this report, we have segmented publicly listed Indian IT companies (comprising software services, products and training companies)

based on their market caps as follows:! Large-Caps : Companies with market cap of more than USD 1 billion! Mid-Caps: Companies with market cap between USD 100 million and USD 1 billion! Small-Caps: Companies with market cap of less than USD 100 million

Market Cap used to segment these companies is the 30-day trailing average as of December 30, 2005.

Besides listed companies, we expect several private companies to enter the mid-cap universe over the next couple of years through an IPO. Our analysis does not cover these companies,

though we have included a brief section on them in the report.2As per Nasscom 2005 Report

3Source: Financial Express: India is Accenture's Flagship Global Delivery Center - September 13, 2005

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 5/38

Scale And Offshore Leadership Is Enabling Indian IT Vendors

To Compete With MNCs For Large Global Projects

The year 2005 has seen leading Indian IT companies

breaking the glass ceiling and competing successfully with

IT multinational companies for large global projects. Two

factors have made this possible:

a. Offshore outsourcing of IT requirements has

assumed strategic importance for large global

corporations owing to its compelling cost-quality

equation.

b. Leading Indian IT companies have developed an

excellent track record and assumed a leadership

position for offshore delivery, making them 'go-to'

players for a company's offshore outsourcing

requirements. In addition, they have attained alevel of scale that enables them to compete

effectively for large multi-year IT contracts,

business that was previously ring-fenced by large

IT multinational companies.

Some examples of this trend include ABN Amro awarding a

USD 400 million, five-year contract to TCS, Infosys and Patni

for outsourcing of IT infrastructure, application support and4application development . More recently, General Motors

awarded Wipro a five-year contract that was valued at5around USD 300 million .

The significance of these contracts goes beyond size and

quality. It indicates an emerging trend towards unbundling

of large multi-year outsourcing contracts and distribution to

multiple vendors as opposed to the hitherto single-vendor

norm. This further increases the eligibility of Indian offshore

majors.

Movement up the Value Chain

Today, India as an offshore destination for IT services offers

more than just a cost proposition. Its demonstrated track

record of delivering global quality at low cost has enabled

the Indian IT industry to transition from being a lower-end

application development and maintenance services

provider to offering higher-end critical services like design

conceptualization and implementation, product co-

development and IT infrastructure management. This

validates the maturing of the Indian IT industry as a

provider of high-productivity, quality-driven services.

4Source: Company Website

5Source: Company Website

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 6/38

The IT industry has undergone significant changes as result

of the slowdown in the US economy in 2001. The sharp fall

in industry growth affected all IT companies adversely but

Mid-Caps were among the worst affected. In the last five

years, some companies (like DSQ, Pentafour and Silverline)

disappeared from the Mid-Cap IT landscape in India, while

some entirely new players emerged like Geodesic. Several

others took bold decisions and reorganized themselves

around strategies that could help them differentiate and

grow in highly dynamic and difficult market conditions.

Our analysis led us to classifying stages in the evolution of

Mid-Caps over the last five years into three distinct phases.

Phase 1: Unbridled Growth

Prior to the slowdown in the US economy in 2001, the

Indian IT sector enjoyed a phenomenal growth rate of morethan 60%. The scorching pace of growth was first led by the

Y2K wave, which was immediately followed by the Internet

hysteria.

With no demand constraints, medium-sized companies

adopted a carpet- bombing approach, claiming to offer

services in every vertical, technology or business practice.

These companies were also exposed to high customer

concentration and the US as the primary market for growth.

Lastly, the relative lack of competitive market pressure

made companies lose focus on creating differentiation and

on developing their sales capability.

Customers, on the other hand, adopted a diversified vendor

selection strategy by selecting different offshore suppliers

for each division. While this provided a large number of

projects for Mid-Cap vendors, revenues were mainly time-

bound, owing to their project-based nature. Coupled with

concentration of business around a few large clients left

Mid-Caps highly vulnerable to several business risks.

Phase 2: Challenged Growth

Phase 1 came to an abrupt halt with the slowdown in the

US economy in 2001, which severely affected the fortunes

of Indian companies and exposed the limitations of the

Indian model. This phase was characterized by:

+ Decline in the Industry Growth Rate: As customers in

the US started cutting back IT budgets, overall industry

growth fell from more than 60 per cent year-on-year to

around 35-40 per cent.

+ Margin Pressures and Increased Competition: Companies

faced margin pressures and gross profit growth reduced

dramatically as customers stopped being relationship-

oriented and began re-negotiating billing rates. As

customers threatened to withdraw future prospects if

billing rates were not brought down, companies were

forced to compete on price. Mid-Caps were the worst

affected because more often than not, larger companies

not only succumbed to pricing pressures but also started

competing for the smallest deals - mainly because

economies of scale allowed them to take a long-term

view of the customer relationship.

+ Business Model Challenges: Mid-Cap companies were

further challenged because more than 50% of their

revenues came from on-site work, which was under

severe pressure in terms of both volume and pricing. Insome cases, companies with high client concentration

saw a dramatic decline in revenues and profits due to a

loss of one customer.

Faced with the threat of being squeezed out of business, Mid-

Cap companies responded by streamlining operations and

devising strategies that helped them differentiate themselves,

which in turn, helped them survive and grow in a highly

dynamic market condition.

Phase 3: Focused Growth

By the end of 2003, the US economy started its path to

recovery and the third phase of the offshore outsourcing era

had begun. Large-Cap players scaled their business

dramatically by developing capabilities across multiple

verticals. Mid-Caps, on the other hand, focused on developin

a strong niche focus. This phase also witnessed the evolution

of new areas of outsourcing like product engineering services,

IT infrastructure management and software testing services.

Meanwhile, customers re-oriented their IT outsourcing

strategy by consolidating their vendor base and tightening the

norms for new vendor selection. These changes implied that

only large vendors or medium-sized companies with

specialization were positioned for growth.

In this report, we have tried to look at how Mid-Caps have

overcome the lack of scale leadership by adopting distinct

strategies in order to survive and thrive in a rapidly evolving IT

industry.

Mid-Caps : An Evolution

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 7/38

Mid-Caps : Building Market Competitiveness

The existing Large-Caps broke away from the pack in the

late 1990s to emerge as dominant market leaders. Around

this time, the rest of the Indian IT industry was highly

fragmented, with certain sources estimating that there

were more than 2,000 IT companies. In an industry where

scale came from qualifying for larger projects, which, in

turn, were awarded primarily to larger companies,

companies other than the market leaders were clearly

challenged for growth. As described in the previous section,

some of these companies focused on building strong niche

or domain differentiation to compete effectively. In this

section, we take a deeper look at some of these companies

and the strategies that have helped them survive and

thrive.

The publicly listed Mid-Cap landscape in India includes 23

companies with a cumulative Market Cap of USD 4.6 billion(based on a 30-day trailing average as of December 30,

2005). Exhibit 4 provides a summary listing of these

companies.

While the Mid-Caps constitute a fairly diverse universe, our

analysis provided insights that helped us classify them into

the following categories, based on the strategy they have

adopted to differentiate themselves:

1. Niche Service Providers: Some companies, such as

Aztec, and Hexaware, have diligently focused on developing

their capability around a specific niche with a goal to build aleadership position in that segment. For example,

Hexaware's positioning as a leading offshore ERP vendor

has helped it compete effectively with Large-Caps for large

ERP contracts.

2. Multi-Domain Players: This segment constitutes

companies that have achieved more than USD 50 million in

revenues by building capabilities across multiple domains.

Examples include companies such as KPIT Cummins, Mastek

and Zensar. While it is difficult to pinpoint a common

strategy adopted by these players, companies that have

developed a strong capability in a couple of high-growth

verticals and in some cases, a leadership position in one,

clearly stand out from the rest. For example, KPIT Cummins

enjoys a significant differentiation in the market owing to

its established track record in executing moderate-sized

manufacturing-related IT projects.

3. Consolidators: There seems to be an emerging segment

of players that are adopting a highly inorganic approach to

growing their businesses. Scandent Solutions is among the

first few that has relied largely on equal-sized mergers and

significant acquisitions to grow its business. Its merger with

SSI Technologies enabled the formation of a company that

leapfrogged into the Mid-Cap segment.

4. Solution/Product Providers: The surprise package from

our analysis was the product and solution providers. These

include companies such as Cranes Software, Geodesic and

Polaris, which have grown largely through a product-led

strategy. These companies seem to have defined their target

product/solution segments early and have aligned their

execution around this focus. One of the players, Cranes

Software, has acquired companies globally in a highly

methodical manner with a clear goal of enhancing its product

portfolio in the scientific products market.

In addition, there are a few other companies such as Sasken

and 3i Infotech that have listed their stocks on the capital

markets recently and are new additions to the Mid-Cap sector.

They have not been included in our analysis of Top Performing

Mid-Caps due to an inadequate track record of their stocks,

post listing.

Also, there are several privately held companies waiting to

break into the Mid-Cap segment. Amongst these, MindTree

Consulting and Caritor have witnessed significant growth in

recent times. While the former has positioned itself as one o

the only offshore vendors providing high-end systemsarchitecting capability, the latter has leveraged a couple of

large client relationships to build a USD 100 million+ revenue

company. Citigroup Venture Corporation (“CVC”) has recently

invested into the company.

We believe many more private companies will go public in the

next 24 months, thereby enhancing the depth of the Mid-Cap

sector. Calendar year 2005 saw nine IT companies list on the

Indian capital markets, the highest number after the Internet

hysteria in 1999-2000. Exhibit 3 lists all companies that went

public in 2005. For these companies, the median Market Cap

to-sales multiple was 2.85x and the Market Cap-to-earnings

multiple was 27.1x.

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 8/38

3i infotechwww.3i-infotech.com

Company Segment Key Focus Area Market Cap Revenue(TTM)

EBITDA(TTM)

Aftek Infosyswww.aftek.com

Aptech Ltd.www.aptech-worldwide.com

Aztec Software &Technology Serviceswww.aztek.com

Cranes Softwarewww.cranessoftware.com

Geodesic InformationSystemswww.geodesiconline.com

Product/Solution Provider

Product/Solution Provider

Niche Service Provider

Niche Service Provider(Product-Centric Services)

Product/Solution Provider

Product/Solution Provider

IT services company focused on BFSI,manufacturing, retail anddistribution space

Product cum services companyin the embedded space

IT training company

Product engineering company

Product-centric company inscientific and engineering space

Product company in thecommunication and collaborationspace

189

217

115

166

268

299

85

51

27

40

44

17

17

19

(5)

9

28

10

Exhibit 4: Overview of Mid-Cap Landscape

Continued on the next paMarket Cap is a 30-day trailing average, as on December 30, 2005.All figures in USD MillionSource: Avendus Estimates, CMIE Database, Company Annual Reports

*Revenue and PAT are for fiscal year prior to listingMarket Cap, Revenue, PAT in USD MillionSource: Avendus Estimates, CMIE Database

Change SinceListing as on

30 Dec 05

Company IssueOpening

Date

CapitalRaised

Revenue* PAT* MarketCap

MarketCap/Sales

Market/PAT

MarketCap

MarketCap/Sales

MarketCap/PAT

3i Infotech Apr-05 51.1 3.9 110.8 1.7 28.3 225.0 3.4 57.4 103%64.9

PrithviInformationSystems

Nov-05 30.0 6.3 113.4 1.7 17.8 136.0 2.0 21.6 21%67.8

Saksoft Mar-05 1.7 1.3 28.2 6.8 22.2 29.0 7.1 23.0 4%4.1

FCS Software Sep-05 3.9 2.5 55.7 2.9 27.1 34.0 1.8 16.6 -39%18.8

AurionproSolutions

Oct-05 6.0 0.5 25.6 13.4 48.5 23.0 12.0 43.6 -10%1.9

Paradyne Info Nov-05 3.1 1.1 18.2 1.2 16.4 19.0 1.2 16.9 4%15.2

CompulinkSystems

Dec-05 6.0 0.8 16.8 5.9 21 16.0 5.7 20.3 -3%2.8

KernexMicrosystems

Dec-05 22.0 2.0 87.1 7.5 43.7 78.0 6.6 38.9 -11%11.7

As on Listing As on December 30, 2005

Mid-Cap

Small-Cap

Exhibit 3: IT IPO’s in Calendar Year 2005

Sasken Sep-05 28.9 4.8 284.0 5.3 56.1 232.0 4.3 48.3 -18%53.3

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 9/38

Company Segment Key Focus Area Market Cap Revenue(TTM)

EBITDA(TTM)

Geometric Software

www.geometricsoftware.com

Hexaware Technologieswww.hexaware.com

iGATE Gobal Solutionswww.igate.com

Infotech Enterpriseswww.infotechsw.com

KPIT Cummins Infosystemswww.kpitcummins.com

Mastekwww.mastek.com

Mphasis BFLwww.mphasis.com

NIIT Ltdwww.niit.com

NIIT Technologieswww.niit.com/tech

Nucleus Software Exportswww.nucleussoftware.com

Polaris Software Labwww.polaris.co.in

Rolta Indiawww.rolta.com

Sasken CommunicationTechnologieswww.sasken.com

Scandent SolutionsCorporationwww.scandentgroup.com

Subex Systemswww.subexgroup.com

Visualsoft Technologieswww.visualsoft-tech.com

Niche Service Provider

(Product-Centric Services)

Niche Service Provider

Multi- Domain Player

Niche Service Provider

Multi-domain Player

Multi-domain Player

Multi-domain Player

Niche Service Provider

Multi-domain Player

Product/Solution Provider

Product/Solution Provider

Niche Service Provider

Consolidator

Product/Solution Provider

Product/Solution Provider

Niche Service Provider

Multi-domain Player

PLM software company

IT services company focused onairlines, HR IT, peoplesoft,insurance, testing and Assetmanagement solutions

IT services company focused on BFSIspace

IT services company focused on GIS,engineering design space

IT services company focused on BFSI,manufacturing space

IT services company focused on BFSI,telecom, education and governmentspace

IT services company focused onfinancial services, retail, logistics,transportation, technologyand healthcare space

IT training company

IT services company focused onfinance, retail, transport andmanufacturing space

Product company focused on BFSIspace

Product-cum-services companyin BFSI space

IT services company in engineeringservices, GIS and eSolutions space

135

314

158

158

111

168

528

127

140

138

290

288

235

136

186

106

100

47

147

129

71

65

140

199

92

109

30

183

88

51

71

37

41

78

11

23

13

14

8

24

49

11

22

11

18

41

6

12

11

9

13Zensar Technologieswww.zensar.com

IT services company focused onTelecom space

IT services company focused onmanufacturing, government, BFSIspace

Product company focused ontelecommunications space

Software solutions and productdevelopment company focusedon BFSI, retail and manufacturingspace

IT services and BPO company

Market Cap is a 30-day trailing average, as on December 30, 2005.All figures in USD MillionSource: Avendus Estimates, CMIE Database, Company Annual Reports

Exhibit 4: Overview of Mid-Cap Landscape

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 10/38

All Mid-Caps listed in the previous section are survivors of

the economic downturn witnessed during 2000-2002.

These companies have followed multiple growth strategies

but in most cases, it has been around a single foundation of

consolidation, niche services focus, product/solutions focus

or domain differentiation. In this section, we try to answer

the following questions:

+ Which are the top-performing Mid-Cap companies?

+ What is common among these top-performing

companies?

+ What lessons can be drawn from these top-performing

companies?

Top Performers

We have used Market Cap to compare the performance of

these companies. Our analysis excludes companies thathave recently listed on the capital markets, such 3i Infotech

and Sasken. We believe Market Cap is the most appropriate

metric for comparing companies as it takes into account

both, its past track record and future expectation of growth.

We have selected 10 companies that have outperformed

others, based on a three-year CAGR in their Market Cap.

This period provides a fair measure of the companies'

capabilities as it captures efforts made by them to deal with

extremely challenging market dynamics. The list of the top

ten companies is provided in Exhibit 5 (these companies

shall be referred to as “Top Performers” in the rest of the

report).

We have compiled the strategies adopted by each of the Top

Performers in Exhibit 6. Further details on each company

and their strategies are provided in the Appendix 1 to the

report.

As observed in Exhibit 6, five out of the Top Performers are

product companies, two are product-centric services

companies, two are niche services companies and one is a

multi domain player.

This data, in conjunction with an in-depth study of each

company, reveals some critical strategies adopted by most

of the Top Performers.

Strategy #1: Build a Product Either Your Own or Somebody

Else's

In the world of IT services companies, product-related

Mid-Caps : Drivers for Growth

companies seem to be positioned well for growth.

Companies such as Cranes, Geodesic, Nucleus, Subex and 3i

Infotech have demonstrated the ability of Indian companies

developing software products that have global applicability.

The capital markets have rewarded these companies with

attractive valuations that factor in the economics of product

plays.

Company Name

Geodesic

Cranes Software

HexawareTechnologies

Subex Systems

Aptech

K P I T CumminsInfosystems

Nucleus Software

Aftek Infosys

Aztec Software

GeometricSoftware Solutions

Mphasis B F L

ZensarTechnologies

InfotechEnterprises

Igate GlobalSolutions

Rolta India

Polaris SoftwareLab

Mastek

VisualsoftTechnologies

NIIT

3i Infotech

NIITTechnologies

Sasken

ScandentSolutions

2-yr CAGR inMarket Cap

268%

125%

84%

107%

62%

66%

149%

73%

132%

60%

22%

45%

57%

24%

33%

14%

10%

-8%

-11%

NA

NA

NA

NA

1yr CAGR inMarket Cap

353%

93%

44%

116%

63%

34%

248%

65%

240%

82%

0%

60%

122%

1%

70%

-23%

42%

4%

3%

NA

-5%

NA

-5%

3-yr CAGR inMarket Cap

211%

128%

125%

99%

68%

62%

62%

50%

45%

37%

32%

20%

12%

11%

6%

5%

4%

-10%

NA

NA

NA

NA

NA

All figures in USD MillionSource: Avendus Estimates, CMIE Database

Exhibit 5: Market Cap CAGR Comparison for Mid-Cap Companies

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 11/38

Geodesic InformationSystems Ltd.

Communication andcollaboration

Product/Solution Provider , Focused on the instant messaging space, Focused on constantly innovating product lines: Mundu,

its flagship product is the number 1 interoperable instantmessenger in the world

, Did three acquisitions in 2005 in technology companiesthat added to Geodesic's product range andfunctionality.

Cranes Software Intl. Ltd. Scientific and engineering Product/Solution Provider , Acquisition of under valued products, Enhancement of these products by leveraging the Indian

development center, Cross sell these products to their existing and new user

base, Acquired one company in 2005

IT Training Niche Service Provider , Focused exclusively on training from 2001

, Established a very strong brand- Second largest Indian ITtraining company.

, Focused on international Markets like China, Africa,Bangladesh, Latin America and Vietnam

, Focused on forming alliances with education institutes aswell as corporate for IT training

Aptech Ltd.

K P I T Cummins InfosystemsLtd.

BFSI, Manufacturing Multi-domain player , Focused on the verticals and domains includingadvanced technology solutions, information risk

, Focused on mining a few clientsmanagement andcontrol, SAP and BPO.

, Acquired two companies in 2005 in order to expand

its presence in the French market and add businessintelligence as a domain

Company Name Vertical Profile Strategy

Aztec Software & TechnologyServices

Technology Niche Service Provider(Product-Centric Services)

, Focused on Product Engineering.

, Strong focus on Technology.

, Select clients and annuity focus.

, Acquired Disha Technologies, a testing company tofacilitate rapid Product Development

Geometric Software SolutionsCo. Ltd.

Primarily Manufacturing Niche Service Provider(Product-Centric Services)

, Focused on Product Lifecycle Management.

, Used Intellectual Property effectively to differentiateitself.

, Has been expanding service offerings around the PLMspace.

, Started focusing on products with the launch of

Embedded Product/Solution Provider , Strong focus on the Embedded space., Following a product cum services strategy., Effective use of alliances to tap clients.

, Strong focus on inorganic growth with the acquisition of Arexera in 2003 to enter the European markets and V-Soft

Aftek Infosys Ltd.

Exhibit 6: Strategies of Top Performers

Source: Avendus Research

Airlines,HR IT, Peoplesoft,Insurance and morerecently testing and AssetManagement Solutions

Niche Service Provider , Identifying undeserved but scalable markets, and thenmaking substantial investment upfront to create marketleadership status

, Focus on niche segments like Airline, HR, Peoplesoft

, Focus on emerging & underserved markets in Europespecifically Germany

, Focus on client mining

Hexaware Technologies Ltd.

Telecom Product/Solution Provider , Focused on the fraud management and revenuemaximization space

, Focused initially on emerging markets and later entereddeveloped markets

Subex Systems Ltd.

BFSI Product/Solution Provider , Focused on niche segments like cash management andretail lending.

, Focused on untapped markets like Asia, Philippines andJapan in particular, Middle East and Europe.

, Focused on investment in IP creation and new productofferings

Nucleus Software Exports Ltd.

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 12/38

Refer the inset box for a profile of Subex, one of the top

performers that have adopted a product- focused strategy.

We expect more companies with a product-focused strategy

to access the public markets in coming years. According to a

recent NASSCOM report, the

products and technology

services market in India is

expected to grow to USD 8

billion by 2008.

Another rapidly growing

opportunity is the creation of

offshore players dedicated to

providing intellectual property

related services to technology or

manufacturing companies

globally. Aztec Software is anexample of a company that

provides outsourced product

development and software

testing services to Independent

Software Vendors (ISVs). A similar opportunity exists in

Engineering Design Services that help companies manage

their product lifecycles more effectively. Exhibit 7 highlights

each of these opportunities in more detail.

Strategy #2: Focus on A Fast-Growing Niche And Strive For

Global Leadership

Positioning, focus and leadership (actual and perceived) goa long way towards helping win customers. It does wonders

for your Market Cap as well. There was a time in the Indian

IT markets when being focused on financial services was

considered a niche. That is no longer true. In today's context,

a financial services niche implies focusing on something

more specific, such as Fixed Income Capital Markets.

Hexaware has leveraged its HR IT niche positioning to get

long-term contracts from large clients, whereas Subex has

kept redefining its telecom focus to define a niche where it

can claim to have a global leadership position.

Strategy #3: Target Under-Served Markets

Mid-Cap companies are also following a strategy of

exploring new markets to not only insulate themselves

against over-dependence on the US market, but to also

shield themselves from head-on competition with the

Large-Caps. Though the US will remain a dominant market

for software exporting, these companies are focusing on

expanding into newer geographies such as Middle East, Asia

and Latin America. For example, 3i Infotech Limited, a

software products company, is believed to achieve almost 25-

30% of its growth from emerging

markets like Central Asia, East

Asia and the Middle East.

When talking of under-served

markets, we need to take stock of

a latent opportunity right at our

doorstep. Some companies are

focusing on the Indian domestic

IT market that NASSCOM projects

will grow to USD 6 billion by

2006, a CAGR of 25%. While this

may seem lower when comparedto exports, we can expect the

domestic IT market to get a fillip

with increased penetration of

broadband, increased

investments in e-Governance projects, progressive

deregulation, etc. With this expectation, companies are

increasing their focus on the domestic market, especially in

emerging sectors such as retail, logistics, telecommunications

and SMEs. Companies such as Nucleus Software have a long

track record of serving the Indian market.

Strategy #4: Leverage Acquisitions, StrategicallyAcquisitions have been used fairly aggressively by the Mid-

Cap segment, as can be seen in Exhibit 8. While the jury is still

out on the success or failure of these acquisitions, Mid-Caps

have demonstrated the ability to leverage acquisitions to

complement their existing capabilities.

SUBEX: An Indian Software Product Company

Subex offers products focused on niches within the

telecom sector. The company identified an

opportunity in the fraud management and revenue

maximization solutions for telecom operators. A

survey conducted by Communications Fraud Control

Association (CFCA) estimated annual telecom fraud

losses to be in the range of USD 35-40 billion.

However, only 27% of operators currently use

'Revenue Maximization' solutions. Subex is among

the few product companies globally that has

developed solutions targeting this opportunity, afeat acknowledged by a 100% CAGR in their Market

Cap over the last three years.

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 13/38

Engineering Design Services

, Engineering services are those that augment or manage processes that are associated with the creation of a product or service, as wellas those associated with maximizing the life span and optimizing the yield associated with a product or asset.

, This not only includes design elements of the product or service itself, but also encompasses the infrastructure, equipment andprocesses engaged in manufacturing or delivering them.

Current slow down in the global automotive andaerospace sectors has increased the need for low costvendors for design services

Focused engineering design players:Infotech Enterprises, Rolta India, Geometric, OnwardTechnologies, KLG Systel, Hero Global Design, Axis/IT&T, Plexion& Quest

Market Size

The worldwide marketfor outsourcedengineering designservices is estimated tobe $12.4 billion in 2006.Source: IDC

Offshoring engineering design and services translateinto:

Market Drivers Service Providers

Captive MNCs:Bechtel, Ford, Daimler Chrysler, GM, Caterpillar

Large players with engineering design capabilities:TCS (recently signed a deal with Ferrari), Infosys (recently signeda deal with Airbus), Wipro, Satyam, NIIT, HCL Tech

25%-30% reduction in engineering cycle time

30%-40% reduction in cost

20%-30% increase in production efficiency(productivity and quality)

15%-20% reduction in maintenance cost(Source:Dataquest)

Lack of skilled manpower/bandwidth within OEMs tocater to their design needs in-house

Faster time to market- a critical factor in fluctuatingbusiness trends in sectors like automotives

Offshore Product Development (OPD)

, OPD is a term that refers to outsourcing pieces of ISV's product development functions to a specialist, A number of global ISV's like Siebel, Hyperion, BMC software and Autodesk are leveraging this model. partner.

, Increasing cost pressures, Need to shorten the time-to-market cycle, Failed attempt by some ISV's to set up captive, Significant traction in startups with many venture

capitalists specifically asking for an 'India plan'.centers in India due to issues with managing scaleand operations and keeping their team motivated

, Example: US$ 18 million investment byNorwest Capital Partners into Pune basedPersistent Systems.

Market Size

The Indian OPDmarket is estimated togrow to $8-11 billion by2008Source Nasscom

Market Drivers Service Providers

, Mid-Cap companies: Aztec software, Visualsoft

, Small Cap & Private Companies: Sonata Software,Symphony Services, Virtusa, ISG Novasoft, CybernetSoftware Systems, Aditi Software and PersistentSystems.

, Large-Caps: TCS, Infosys, Wipro

Outsourced Testing Service

Cost arbitrage

Increased need for rigor and transparency to the testingand defect reporting ocess of the software productdevelopment life cycle.

Stringent compliance norms set by regulatory bodies inUS and Europe for the banking, financial, insurance andhealthcare sectors, are also driving ISVs to outsourcetesting services

Pure play testing companies: Applabs (now merged withVisualsoft), Disha Technologies (now merged withAztec),ThinkSoft, RelQ and Ready Test Go

Market Size

The size of the Indiantesting market isestimated at $300million (CY05) and isprojected to grow to $1billion by the year 2007 Source Meta Group Time to market is becoming a key for ISVs to

differentiate from each other and capitalize on theearly mover advantage.

Market Drivers Service Providers

Large Players: Infosys, Wipro, TCS, Satyam, Cognizant, HCLTechnologies, Headstrong, Keane, Patni operate in this space. .

, This refers to quality assurance (QA) service outsourcing functions

, Globally companies endeavor to have a ratio of 3:1 between developers and QA professionals and therefore providing for a huge

market opportunity., Outsourced testing services includes services like white-box, black-box, functionality, compatibility, and stress testing

Exhibit 7: Emerging Service Offerings for Products

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 14/38

Continued on the next page

Dec-05 Geodesic Engage Solutions In line with the company's plan to makestrategic investments in technology

companies, that possess innovative ideas thatcan be integrated with the company'sexisting suit of products.

Nov-05 MBT Axes Technologies Bridge a gap in MBT's service offerings to theTelecom Equipment Manufacturers (TEM)segment of the telecom market.

Augment MBT's offerings in productengineering and enhance capabilities toprovide solutions to telecom service providers.

Strengthen MBT's delivery capabilities.

Nov-05 KPIT Cummins Pivolis Gateway to France (with large manufacturing& banking companies, KPIT's focus areas), a

new geographyfor KPIT.

Strengthen presence in BFSI segment.

Nov-05 Geodesic PicoPeta Simputers Provides Geodesic with new value addedproduct offerings by combining its instantmessaging platform with PicoPeta's Simputersand its complementary universal messagingsystem.

Leverage on PicoPeta's understanding of acomplete product for the local market with itsglobal product presence, in order to enableeffective cross selling of products andsolutions.

Nov-05 3i Infotech SDG SoftwareTechnologies

Acquisition of new products in banking(Anti Money Laundering) and capital markets(Fraud Management), erstwhile missing in thecompany's array of products.

Nov-05 KPIT Cummins SolvCentral.com Strengthen domain focus on BI by creating anew line of business (LoB).

Establish presence in new geographicarea - Washington DC.

Oct-05 Geodesic Clangula IT AB NA

Oct-05 Mastek Entegram Access to strong client base(Fortune 500 companies).

Sep-05 3i Infotech Innovative BusinessSolutions

Enhance company's niche consulting skills inEAI, BI and IT security.

Augment geographic reach to US

Credible customer base acquisition.

Aug-05 Aftek Infosys V-Soft Inc Enhance its footprint in the professionalservices arena in USA.

NA

54

2

7

NA

2

NA

2

4

4

Date Acquirer Target Deal Value Purpose/Outcome of Transaction

Exhibit 8: Acquisitions by Mid-Cap Companies in the Last Twelve Months

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 15/38

Jul-05 Scandent Solutions BWH France Entry into the French market.

Jun-05 Caritor Idgo Group Provides consulting to telecom and financialsverticals.

Entry into the Paris market.

May-05 MindtreeConsulting

Linc Software Provides expertise in the areas of applicationdevelopment and maintenance domains forIBM Mid-range systems- An importantcomponent in the growth strategy laid downMindtree.

May-05 Cranes Software Engineering MechanicsResearch CorporationIndia Operations

Provides consulting services and customizedsoftware in the field of computer aidedengineering.

May-05 Mphasis BFL Eldorado Computing Make a foray into the booming healthcareinsurance and payment processing business.

Strengthen presence in the US market.

Date Acquirer Target Deal Value Purpose/Outcome of Transaction

Mar-05 InfotechEnterprises

Tele Atlas India Pvt Ltd Strategic acquisition to see definitive inflow of revenue by ensuring a minimum amount of business to be carried out in the next 3 years.Structured to provide financial aid to TeleAtlas's large order book execution.

Feb-05 Mphasis BFL Princeton Consulting Add niche consultancy services focused onproviding customer management solutions;depth to existing service offerings.

Acquisition used as a route to scale operations(buy vs build model).

Jan-05 GeometricSoftware

Tecsoft Inc& Cimitronics Inc

NA

NA

4

NA

NA

17

2

8

2

All Figures in USD MillionSource: Avendus Estimates, Company Press Releases

Exhibit 8: Acquisitions by Mid-Cap Companies in the Last Twelve Months

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 16/38

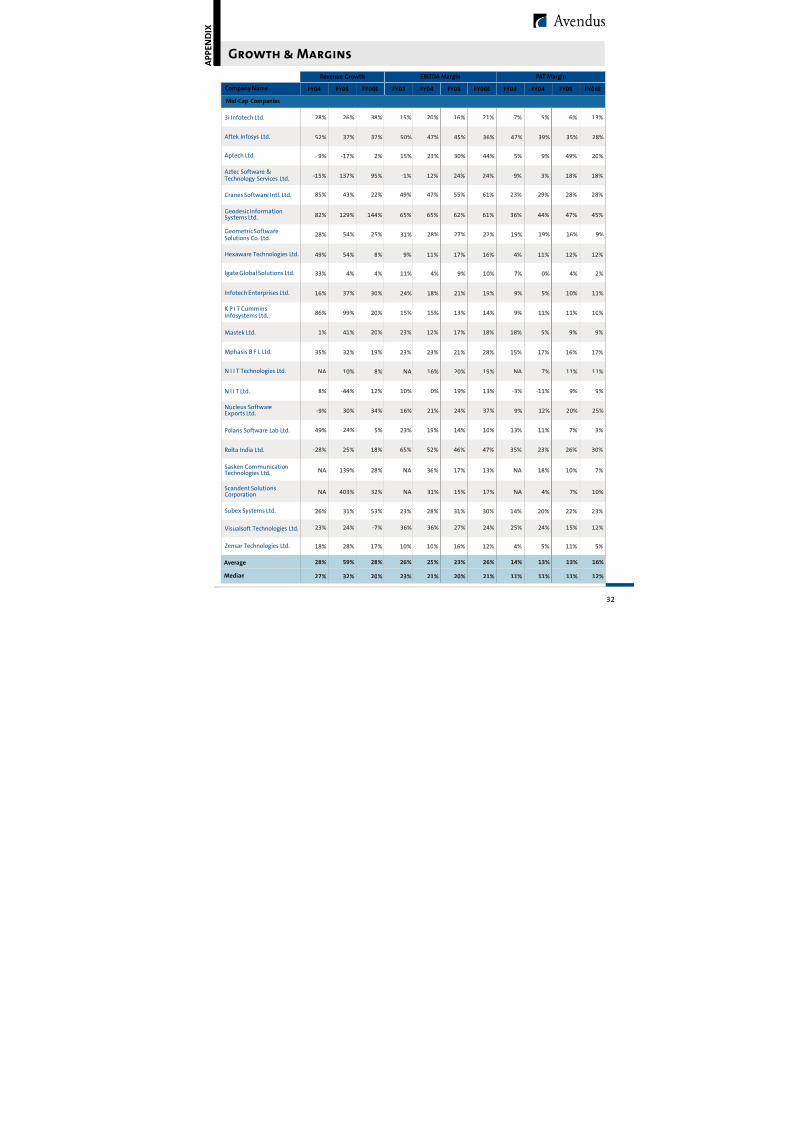

What is important to note is that the Top Performers, with

median EBITDA margins of 26% and median PAT margins of

19% (for fiscal year ending March 31, 2005), were

comparable to the profitability levels of the Large-Caps

whose median EBITDA margins were 27% and PAT margins

were 20%, as illustrated in Exhibit 10 and 11.

As discussed in previous sections, Mid-Caps have followed a

different strategy, as compared with Large-Caps. While Large-

Caps have focused on building global delivery capability to

service large multi-year outsourcing engagements, Mid-Caps

have primarily focused on developing their competence

around niche areas for growth. Our analysis shows that

though Mid-Cap Market Cap has grown dramatically

compared to those of Large-Caps, they are relatively

undervalued as compared to Large-Caps. The difference is

more telling in the case of our Top Performers, whose revenue

growth rates exceed Large-Caps at comparable levels of

profitability.

Mid-Caps Have Outperformed Large-Caps in Market Cap

Growth

Contrary to the common perception, the Mid-Caps have

shown stronger growth in their Market Cap than the Large-Caps. We compared the 365-day trailing average Market Cap

(as of December 30, 2005) of all Mid-Caps and Large-Caps over

the last three years. Mid-Caps performed better than Large-

Caps for all three years.

The median three-year CAGR in Market Cap for Large-Caps

was 32%, compared with 37% for Mid-Caps and 65% for the

Top Performers. Mid-Caps have also outperformed Large-Caps

in terms of growth rates of both two-year and one-year

Market Cap, as illustrated in Exhibit 9.

Top Performers Beat Large-Caps in Terms of Revenue Growth,

at Comparable Margins

Mid-Cap companies as a whole have increased their revenue

in the last three years (2003-2005) at a CAGR of 31%.

However, our Top Performers have done better, growing at an

impressive 40%. This growth is better than that of Large-Caps,

who are growing at a CAGR of 36%.

Differentiated Mid-caps: A Compelling Value Proposition

Exhibit 9: Market Cap CAGR for Large-Cap, Mid-Cap

& the Top Performers

3 year CAGR 2 year CAGR 1 year CAGR

100%

80%

60%

40%

20%

0

65%

32%

37%

88%

62%

35%

95%

60%

47%

Median Mid-Cap Median Top Ten Players Median Large-Cap

Market Cap is the 365-day trailing average (as of December 30, 2005)Source: Avendus Research, CMIE Database

FY 03

25%

20%

15%

10%

5%

Median Mid-Cap Median Top Ten Players Median Large-Cap

Exhibit 11: Median PAT Margin Comparison

FY 04 FY 05 FY06(E)

11%

12%

20%

11%

15%

21%

11%

19%

12%

20%

19% 20%

Exhibit 10: Median EBITDA Margin Comparison

FY 03

35%

30%

25%

20%

15%

Median Mid-Cap Median Top Ten Players Median Large-Cap

FY 04 FY 05 FY06(E)

19%

23%

27%

21%

25%

27%

33%

20%

26%21%

26%25%

Source: Avendus Research, CMIE Database

Source: Avendus Research, CMIE Database

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 17/38

Large-Caps Are Still Trading At a Significant Valuation

Premium

For the trailing twelve months (ending December 30, 2005),

the Mid-Caps had a Market Cap/Sales, Market Cap/EBITDA

and Market Cap/PAT of 2.58x, 11.12x and 18.00x respectively.

As expected, the Mid-Caps are trading at lower multiples than

Large-Caps as illustrated in Exhibits 12, 13 and 14.

Based on the above facts, we believe there is a strong case to

be made for investing in Mid-Caps that have demonstrated

the ability to differentiate themselves in a market dominated

by the Large-Caps.

Exhibit 13: Median Market Cap/EBITDA Comparison

Exhibit 12: Median Market Cap/Sales Comparison

FY 03

5.00

4.00

3.00

2.00

1.00

0

Median Mid-Cap Median Top Ten Players Median Large-Cap

6.00

FY 04 FY 05 TTM

1.20

1.61

4.01

1.75

1.86

3.775.68

1.57

2.112.58

4.233.96

FY 03

15.00

12.00

9.00

6.00

3.00

0

24.00

FY 04 FY 05 TTM

21.00

18.00

27.00

6.45

6.98 7.73

12.45

7.68

6.617.09

11.12

13.26

14.22 13.96

24.13

Median Mid-Cap Median Top Ten Players Median Large-Cap

Source: Avendus Research, CMIE Database

Source: Avendus Research, CMIE Database

FY 03

20.00

16.00

12.00

8.00

4.00

0

Exhibit 14: Median Market Cap/PAT Comparison

32.00

FY 04 FY 05 TTM

28.00

24.00

36.00

13.02

11.22

21.48

Median Mid-Cap Median Top Ten Players Median Large-Cap

19.21

11.11

10.08

10.09

11.06

18.03

31.18

20.12

18.00

Source: Avendus Research, CMIE Database

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 18/38

Going forward, we expect the Mid-Cap landscape to be

action-packed with a number of mergers, acquisitions,

private equity plays and public market offerings as

companies try to move to the next level and fill the void

between the Large-Cap and the Mid-Cap players as the

revenues of the largest Mid-Cap player in India are less than

USD 200 million.

If we allow ourselves the liberty to indulge in some crystal

gazing, we expect the Mid-Cap segment to witness the

following:

+ As mentioned above, there is a huge gap between the

Large and Mid-Cap players today in terms of their

revenue base. This has created a unique market

opportunity for Mid-Caps to fill this void as clients look

for a second bracket of companies to outsource their

services rather than largely depend on the few Large-

Caps who are growing larger by the day. Mid-Caps will

adopt different approaches to exploit this opportunity.

The Niche Service Providers will continue to

specialize and gain scale to become global leaders in

their areas of focus. This will be facilitated by private

equity and venture capital firms looking to

participate in the next wave of opportunity in the

Indian IT industry. An early indicator of this is the

$18.8 million investment by Norwest Venture

Partners and Gabriel Venture Partners in Persistent6Systems .

Some of the multi-domain players with strong

capability in a couple of high-growth verticals, and

possibly a leadership position in one or more, will be

well positioned to grow rapidly. In these cases too,

we can expect private equity firms to provide the

capital for expansion through organic or inorganic

means.

We could see large global buy-out funds provide the

capital to successful managers to build companies

through the consolidator strategy, which relies on

equal-sized mergers or significant acquisitions in

order to leapfrog to a certain level of scale. However,

we would like to add a word of caution here because

the success of this strategy remains to be proven.

The biggest challenge in executing this strategy

would come from integrating cultures of

predominantly human capital-driven businesses.

+ Considering the outlook that several early stage India-

focused funds are expected to be raised in 2006, we

should expect to see the emergence and growth of

product companies over the next three-five years. The

+

+

+

last couple of years has witnessed a strong show of

interest by global venture capitalists that have invested

in product companies in India. This includes investments

by Nokia Growth Partners and Nortel in Sasken, Bank of

America in Ittiam and Battery Ventures and Intel Capital

in Tejas Networks.

+ We expect weaker Mid-Cap companies that are unable to

develop strong differentiation to get acquired by large IT

multinationals like EDS, Accenture, Cap Gemini, etc, who

are constantly looking for inorganic opportunities to

enhance their offshore presence.

+ We expect a number of new entrants to the publicly

listed Mid-Cap landscape through IPOs in 2006. Calendar

year 2005 saw a number of IT services companies access

the Indian capital markets but most of these companieswould be categorized as Small-Cap, except for 3i Infotech

Sasken and Prithvi Information Systems. Year 2006

promises to be different, with a number of sizeable

private companies looking to go public. The companies

we expect to go public in the next 12-18 months are

illustrated in Exhibit 15.

Mid-Caps : The Road Ahead

Source: Avendus Estimates, Industry Reports

Company Profile

Mindtree ConsultingIT service provider focused on Travel and Leisure,Manufacturing, BFSI, Hi-Tech andPharmaceutical verticals.

L&T InfotechIT services provider focused on Manufacturing,BFSI and Communications and Embeddedspace.

Infinite IT service provider focused on Telecom, Utilities,Healthcare and Government verticals.

CaritorIT service provider focused on Financial Services,Telecommunications, Retail, Manufacturing and

Public Sector.

CorpusIT service provider in the Telecommunicationand BFSI space.

Persistent Software product development.

Mahindra British Telecom Telecom-focused IT service provider.

6

Source: Norwest Venture Partners Press Release

Exhibit 15: Private Companies that might Go Public In the Near Future

Mid-Cap companies will continue the inorganic route to buildon their service offerings or domain expertise. We believe that

a number of Mid-Caps might look at adding scale and

accelerating growth by acquiring a front-end company in the

US. This strategy should enable them to get a global scale

rapidly.

In conclusion, we recommend a close look at Mid-Cap

companies that have invested in prior years to build a strong

differentiation in the market. We may just be at the thresho

of the next big IT wave.

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 19/38

Appendix A :

Company Specific Strategy of Top Ten Performers

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 20/38

APPENDIX

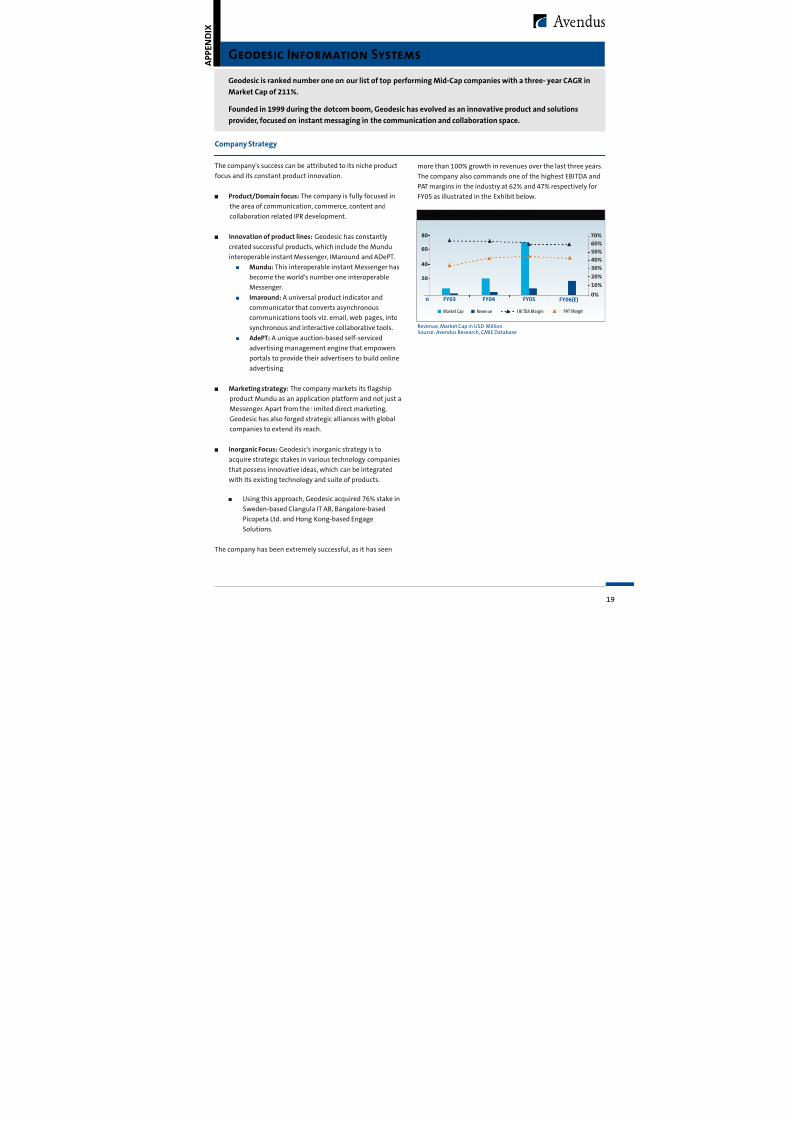

Geodesic is ranked number one on our list of top performing Mid-Cap companies with a three- year CAGR in

Market Cap of 211%.

Founded in 1999 during the dotcom boom, Geodesic has evolved as an innovative product and solutions

provider, focused on instant messaging in the communication and collaboration space.

Geodesic Information Systems

Company Strategy

+

+

+

The company's success can be attributed to its niche product

focus and its constant product innovation.

+ Product/Domain focus: The company is fully focused in

the area of communication, commerce, content and

collaboration related IPR development.

+ Innovation of product lines: Geodesic has constantlycreated successful products, which include the Mundu

interoperable instant Messenger, IMaround and ADePT.

Mundu: This interoperable instant Messenger has

become the world's number one interoperable

Messenger.

Imaround: A universal product indicator and

communicator that converts asynchronous

communications tools viz. email, web pages, into

synchronous and interactive collaborative tools.

AdePT: A unique auction-based self-serviced

advertising management engine that empowers

portals to provide their advertisers to build online

advertising.

+ Marketing strategy: The company markets its flagship

product Mundu as an application platform and not just a

Messenger. Apart from the l imited direct marketing,

Geodesic has also forged strategic alliances with global

companies to extend its reach.

+ Inorganic Focus: Geodesic's inorganic strategy is to

acquire strategic stakes in various technology companies

that possess innovative ideas, which can be integrated

with its existing technology and suite of products.

+ Using this approach, Geodesic acquired 76% stake in

Sweden-based Clangula IT AB, Bangalore-based

Picopeta Ltd. and Hong Kong-based Engage

Solutions.

The company has been extremely successful, as it has seen

more than 100% growth in revenues over the last three years.

The company also commands one of the highest EBITDA and

PAT margins in the industry at 62% and 47% respectively for

FY05 as illustrated in the Exhibit below.

FY03 FY04 FY05

20

00%

FY06(E)

40

60

80

10%

20%

30%

40%

50%

60%70%

Market Cap Reven ue EBI TDA Margin PAT Margin

Revenue, Market Cap in USD MillionSource: Avendus Research, CMIE Database

Exhibit A: Geodesic Financial Performance

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 21/38

Cranes Software International is ranked number two on our list of top performing Mid-Cap companies with

a three-year CAGR in Market Cap of 128%.

Founded in 1991, Cranes Software began business as a distributor of scientific and mathematical software

products from Mathworks Inc.,USA. In the late 1990's, the company also got into the training business. As adistributor, the company was focused on the domestic sector and established relationships with leading

global technology players and gained tremendous domain experience. However, the company did not own

any IPR. In 2001, the company changed its strategy and initiated its foray into software IPR through the

acquisition of a number of products. This strategy has paid off as the company has expanded over ten times

in the last four years.

Cranes Software International

Exhibit B : Cranes Financial Performance

Company Strategy

Since 2001, the company has followed a clear strategy of

acquiring under-valued products and then enhancing them byleveraging its Indian development center and then cross-

selling these products to its existing and new user base.

+ Acquisition: Acquisitions have been an integral part of

the company's strategy. It has acquired under-valued

products with demonstrated technical capabilities and a

strong brand among the user segments. It acquired AISN

Software along with its market-leading software

products (2000), SYSTAT and Sigma product line from

SPSS Inc (2001, 2004), and Engineering Mechanics

Research Corporation, the developer of the NISA family of

FEA programs and a pioneer in the field of ComputerAided Engineering Software (2005). With these

acquisitions, the company acquired a cumulative user

base of 350,000, which included customers like Merck,

Eli Lilly, Pfizer and NASA.

+ Enhancement: The company enhances product lines by

setting a clear product development roadmap and by

leveraging its domain expertise and the India

development center.

+ Expansion: Once the product is enhanced with added

capabilities, the company leverages its global presenceand 38 offices to sell. It also optimizes opportunities by

significantly cross-selling to existing and new users.

That the company's strategy has been successful can be seen

from a CAGR in revenue of 84% over the last five years. The

growth has been driven by product business, which

contributes 80% of its current revenues. (The rest of the 20%

in revenue is derived from the distribution of products and

from training on scientific software products.) The company

APPENDIX

FY03 FY04 FY0500%

FY06(E)

50

100

150

10%

20%

30%

40%

50%

60%

70%

Market Cap Revenue EBITDA Margin PAT Margin

Revenue, Market Cap in USD millionSource: Avendus Research, CMIE Database

delivered high EBITDA and PAT margins at 55% and 28%

respectively for FY05 as illustrated in the Exhibit below.

Exhibit B: Cranes Financial Performance

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 22/38

APPENDIX

Hexaware is ranked number three on our list of top performing Mid-Cap companies with a three-year CAGR in

Market Cap of 125%.

Founded in 1990, Hexaware operated independently till 2001 when it merged with the software division of

Aptech. This merged entity later de-merged from the training arm and subsequently went public. Hexawareprovides software services to organizations in the banking and financial, healthcare, airlines, insurance,

transportation and hospitality sectors. The company focuses primarily on marketing three technology practices

- PeopleSoft Services, Application Management Solutions and e-Solutions. Hexaware also offers offshore R&D

solutions practice comprising embedded software, chip development and testing services.

Hexaware Technologies Ltd.

Company Strategy

Hexaware has followed a strategy of identifying under-served

but scalable markets and making substantial upfront

investment to create market leadership status in these focus

areas.

+ Niche Focus: Hexaware differentiated itself by focusing

on niche areas such as ERP Offshoring, HR IT and the

airline industry. More recently, they have been trying to

make a mark in the testing and asset management

solutions space as well.

+ Expanding into under-served markets: Hexaware has

established a leadership position in the German market

and has also expanded their global footprint in the

Australian and Netherlands market. This is in line withtheir strategy to make a mark in relatively under-served

markets and create market leadership.

+ Alliances: The company has managed to form alliances

with partners who serve Fortune 500 clients, including

PeopleSoft, IBM, Unisys, and Valtech.

+ Client Mining: There is a clear focus on mining the top 35

accounts of the company who contribute close to 80% of

the revenues. Hexaware has been able to achieve

significant growth by purely by focusing on their top

customers.

Since Oracle's acquisition of PeopleSoft, there has been a

slowdown in outsourcing from this platform, which has

resulted in the poor performance of the Hexaware scrip in the

last year. However the release of PeopleSoft version 8.9 by

Oracle has seen a regaining of confidence among PeopleSoft

users, especially in North America, leading to a revival in the

PeopleSoft market. Also, Hexaware is simultaneously trying to

expand its portfolio in the ERP space. They have 14 clients

using systems other than PeopleSoft in this space. Hexaware

is making a conscious effort to de-risk its business from only

one or two services, by bringing in services like asset

management, testing services and leasing.

The company has seen 41% growth in revenues over the last

three years and its EBITDA and PAT margins were recorded at

17% and 12% respectively for FY05 as illustrated in the Exhibit

below.

Exhibit C : Hexaware Financial Performance

Market Cap Revenue EBITDA Margin PAT Margin

FY03 FY04 FY0500%

FY06(E)

100

200

300

5%

10%

15%

20%

Revenue, Market Cap in USD MillionSource: Avendus Research, CMIE Database

Exhibit C: Hexaware Financial Performance

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 23/38

Subex is ranked number four on our list of best performing Mid-Cap companies with a three-year CAGR in

Market Cap of 99%.

Subex was established in 1992 as a telecom hardware system integrator. In 1998 they diversified into

software development and started focusing on developing products in the fraud management and revenuemaximization space. Its clear focus on the telecom vertical and the domains within it has enabled the

company to emerge as the number 1 player in this space.

Subex Systems Ltd.

Company Strategy

Subex's organic strategy has been three-fold -- domain focus,

product focus and market focus.

+ Domain Focus: Subex has not only been focused on the

telecom vertical but within it on the fraud management

and revenue maximization space. This has helped the

company emerge as a leader in this space.

+ Product Focus: Since inception, Subex has been focusing

on developing products in its specialized domain.

Towards this end, Subex has developed Ranger, a fraud

management software and INcharge, a revenue

assurance system. The company derives 36% of their

revenue from the product business.

+ Developing Markets Focus: Subex follows a unique

strategy of focusing initially on the developing markets

in order to a build a good client list. With an availability

of an excellent reference base and suite of products, the

company later enters the developed markets.

+ Inorganic Focus: Subex has launched a proactive

acquisition program in order to fill gaps in its technology

offerings and also expand its geographical reach.

+ Subex acquired IVth Generation Inc, USA in 2000 and

Magardi Inc, Canada in 2001. In 2004, Subex

acquired Alcatel's Fraud Management Group and

Lightbridge's Fraud Centurion, making it the largestfraud management system vendor in the world.

The company has seen 34% growth in revenues over the last

three years, testimony to the success of its strategy. It also

commands high EBITDA and PAT margins at 31% and 22%

respectively for FY05 as illustrated in Exhibit F.

APPENDIX

FY03 FY04 FY0500%

FY06(E)

40

60

80

5%

10%

25%

35%

20

15%

20%

30%

Market Cap Revenue EBITDA Margin PAT Margin

Revenue, Market Cap in USD MillionSource: Avendus Research, CMIE Database

Exhibit D: Subex Financial Performance

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 24/38

APPENDIX

Aptech is ranked number five on our list of top performing Mid-Cap companies with a three-year CAGR in

Market Cap of 68%.

Aptech commenced its IT education and training business in 1986. Since its inception, the company has been

successfully addressing business opportunities in the retail training and education segment in informationtechnology, multimedia and soft skills. In 1998, with the slowdown in the domestic education and training

markets, Aptech expanded its portfolio to include software exports, ERP and knowledge management.

However, in 2001, Aptech Limited de-merged the Training and Software businesses as these markets had

different customer and growth profiles, as well as target markets. The training arm became Aptech Ltd.

Aptech Ltd.

Company Strategy

+ Training focus: Aptech has been traditionally an IT

training company till they entered the software services

space in 1998. However, with the de-merger in 2001, the

company has focused exclusively on training.

+ Brand Buiding: Thanks to the customer-centricity of the

training business, the company realized early on the need

to spend time and money on brand- building. This

strategy has paid off immensely for the company as they

have emerged as the second-largest Indian IT training

company.

+ Global Markets: Since its first foray into the Bahrain

market in 1993, the international business has grown

exponentially. Aptech has been aggressively expandingits international business. It now has training centers in

China, Africa, Bangladesh, Latin America and Vietnam.

Aptech has maintained leadership position in China,

Bangladesh and Nigeria.

+ Alliances: Aptech has formed alliances with education

institutes as well as corporates for IT training. On the

education institutions front, they have formed

collaborative alliances with Southern Cross University -

Australia, Beijing University - China, IIT - Allahabad and

Sikkim Manipal University - Mangalore. Corporate

training is focused only on IT and non-IT Fortune 500companies in developed countries.

However, the company has not done very well in terms of top

and bottom line growth in the past few years. We believe that

Aptech has done well on the indices because of its distinct

position in the Indian IT training industry and the future

global opportunity.

FY03 FY04 FY05

10

0-60%

FY06(E)

20

30

40

-40%

-20%

0%

20%

40%

60%

Market Cap Revenue EBITDA Margin PAT Margin

Revenue, Market Cap in USD MillionSource: Avendus Research, CMIE Database

Exhibit E: Aptech Financial Performance

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 25/38

FY03 FY04 FY05

20

00%

FY06(E)

40

60

80

5%

10%

15%

20%

Market Cap Revenue EBITDA Margin PAT Margin

Revenue, Market Cap in USD MillionSource: Avendus Research, CMIE Database

APPENDIX

KPIT Cummins Infosystems is ranked number six on our list of best performing companies with a three-year

CAGR in Market Cap of 62%.

KPIT Infosystems, incorporated in 1991, was focused on providing software services to the Financials Services

and Manufacturing Verticals. The promoters started with these two verticals because of their accountingbackgrounds, and the fact that the company was based in Pune - a strong manufacturing hub. In 2002, KPIT

merged with Cummins Infotech, a captive IT service unit for Cummins group. This merger provided greater

stability to the combined entity's earnings stream and a stronger presence in the market for the

manufacturing vertical. Recently Lehman Brothers acquired an 8% stake in company.

K P I T Cummins Infosystems.

Company Strategy

Inorganic Focus:

Since its inception, KPIT's strategy has been to be vertical and

domain- focused, as well as focused on client relationships for

growth.

+ Vertical and Domain-Focused: The company has not only

been vertically focused in the BFSI and manufacturing

but also domain-focused in advanced technology

solutions, information risk management and control, SAP

and BPO. Its exclusive focus on these verticals as well in

these segments has helped the company create a niche

in this space and grow rapidly.

+ Focus on strengthening client relationships: With only 24

active clients as of March 2005, its STAR customer

approach of focusing on a few clients has helped thecompany mine client relationships better. It has focused

only on a few clients as it aspires to be the number one

vendor of choice for at least five of its top 10 clients.

+ KPIT's acquisitive strategy has been

either to fulfill gaps in service offerings or to expand

service offerings or to enter new geographies.

+ Following this strategy, KPIT expanded its service

offering and added Business Intelligence expertise

through the acquisition of SolvCentral, and

established a stronger foothold in the French marketthrough the acquisition of Pivolis. These acquisitions

are also an effort to bring down the proportion of

revenue from Cummins.

The company has been extremely successful at its strategy, as

can be seen from its more than 62% growth in revenues over

the last three years. The company has seen a decrease in its

margin over the last year and recorded EBITDA and PAT

margins of 13% and 11% respectively for FY05 as illustrated in

the Exhibit below.

Exhibit F : KPIT Financial Performance

8/7/2019 IT_Mid_Caps_The_Untold_Story

http://slidepdf.com/reader/full/itmidcapstheuntoldstory 26/38

APPENDIX

Nucleus Software is ranked number seven on our list of top performing Mid-Cap companies with a three-year

CAGR in Market Cap of 62%.

Incorporated in 1989, Nucleus Software provides products and solutions to the Banking and Financial Services

industry. For long, Banking and Financial Services have been one of the most competitive segments in theindustry. However, Nucleus' strong domain knowledge, constant investment in IP creation, focus on niche

segments within the banking sector and efforts towards exploring untapped geographies have paid off. The

company has seen a 250% year-on-year increase in Market Cap and is well poised to leap into the next level of

growth through its distinctive strategy.

Nucleus Software Exports Ltd.

Company Strategy

Nucleus has been providing customized solutions to the

banking sector since its inception. The company's flagship

'FinnOne' suite of products has been competing with larger

peers such as Infosys' 'Finnacle' and i-Flex's 'Flexcube' for some

time now. In order to avoid being squeezed by these larger