Embed Size (px)

Citation preview

ANALYST BRIEFING

11 May 2012

1Q12 Performance Result

Disclaimer

2

The views expressed here contain information derived from publicly available sources that have not been independently verified. No representation or warranty is made as to the accuracy, completeness or reliability of the information. Any forward looking

information in this presentation has been prepared on the basis of a number of assumptions which may prove to be incorrect. This presentation should not be relied upon as a recommendation or forecast by PT.Indo Tambangraya Megah Tbk. Nothing in this release should be construed as either an offer to buy or sell or a solicitation of

an offer to buy or sell shares in any jurisdiction

Agenda

3

1. Introduction

2. Operational Review

3. Commercial Review

4. Financial Review

Appendices

Disclaimer

4

Agenda

(a) Highlights of 1Q12 Results

(b) Board of Management

1. Introduction

5

Highlights of 1Q12 Results

Unit: USD Million

Total Revenue

Gross Profit Margin

EBIT

Net Income

ASP (USD/ton)

Q-Q

(21%)

(3%)

(23%)

(33%)

(2%)

1Q12

578

36%

169

124

$101.1

y-y

+23%

+4%

+44%

+31%

+16%

Coal Sales: 5.7 MtDown 1.4 Mt

-20% Q-QUp 0.2 Mt

+4% y-y

1Q11

468

32%

117

95

$87.3

4Q11

733

39%

220

185

$103.1

6

Somyot RuchirawatCommissioner

Rudijanto BoentoroCommissioner

Ir. Lukmanul Hakim, MMCommissioner

Prof. DR. Djisman S.SimandjuntakIndependent Commissioner

Ibrahim Yusuf

President Commissioner &Independent Commissioner

Somruedee ChaimongkolCommissioner

Board of Commissioners

Previously held the position as President Director (2001-2012)

2012 Board of Directors

7

Hartono WidjajaDirector

Leksono PoerantoDirector

Edward Manurung SE, MBADirector

Pongsak ThongampaiPresident Director

Sean Trehane PellowDirector

Previously held the position as Operational Director (2003-2012)

Also holds the position as President Director of PT Kitadin (2009-now)

Also holds the position as BontangOperation Group Head (2011-now)

Disclaimer

8

Agenda

2. Operational Review

(a) ITM Group Operations

(b) Indicative Output Targets

(c) Mine by Mine Operations

ITM Group Operations

9

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12E

Units: Million Ton

QUARTERLY OUTPUT

5.2

5.8

6.77.2

5.7

6.8

Indominco

Trubaindo

Bharinto

Kitadin

Jorong

East Kalimantan

Bunyut Port

Balikpapan

Palangkaraya

Banjarmasin

Central Kalimantan

South Kalimantan

KITADIN-EMBALUT

0.7 Mt

INDOMINCO 15.0 Mt

TRUBAINDO 7.1 Mt

BHARINTO0.7 Mt

JORONG 1.0 Mt

Samarinda

Jorong Port

Bontang Coal Terminal

Captive coal-fired power

project

KITADINTANDUNG MAYANG2.7 Mt

2012 Target: 27mt2012 OUTPUT TARGET

Indicative output targets*

10

0

5

10

15

20

25

30

35

40

2008 2009 2010 2011 2012E 2013E 2014E 2015E

Indominco

Trubaindo

Bharinto

Kitadin

* Not including inorganic growth.** These finished coal output targets are indicative only and may subject to change.

Jorong

Units: Million Ton

MAJOR QUARTERLY UPDATES

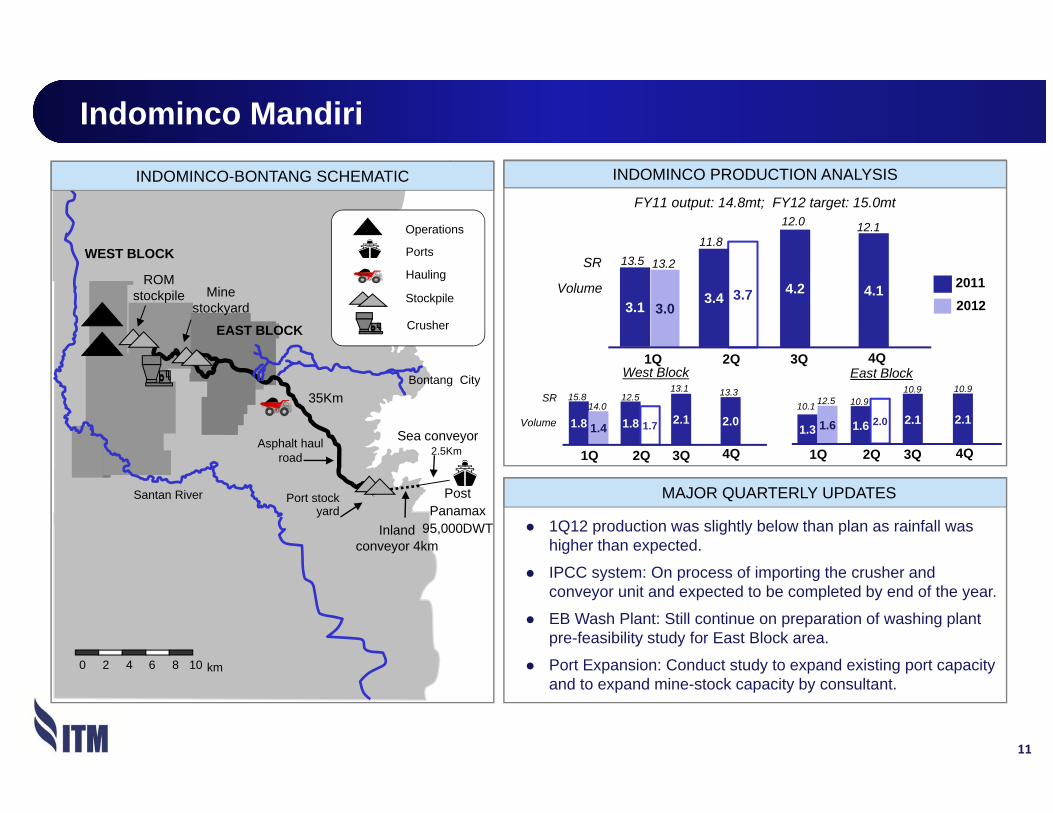

Indominco Mandiri

11

3.7

EAST BLOCK

Santan River Port stock yard

Bontang City

Asphalt haul road 2.5Km

35Km

Sea conveyor

Mine stockyard

Inland conveyor 4km

0 106 82 km4

WEST BLOCK

Operations

Stockpile

Ports

Hauling

Crusher

ROM stockpile

INDOMINCO-BONTANG SCHEMATIC

Post Panamax

95,000DWT

INDOMINCO PRODUCTION ANALYSIS

3.1 3.4 4.2 4.1

1Q 2Q 3Q 4Q

20112012

SR 13.511.8

12.0 12.1

West Block

1.8 1.8 2.1 2.0

1Q 2Q 3Q 4Q

East Block

1.3 1.6 2.1 2.1

1Q 2Q 3Q 4Q

SR 15.8 12.513.1 13.3

10.1 10.910.9 10.9

Volume

FY11 output: 14.8mt; FY12 target: 15.0mt

Volume

3.0

13.2

1.7 2.01.4 1.614.0 12.5

1Q12 production was slightly below than plan as rainfall was higher than expected.

IPCC system: On process of importing the crusher and conveyor unit and expected to be completed by end of the year.

EB Wash Plant: Still continue on preparation of washing plant pre-feasibility study for East Block area.

Port Expansion: Conduct study to expand existing port capacity and to expand mine-stock capacity by consultant.

Trubaindo and Bharinto

12

Mahakam River

Operation

Stockpile

Hauling

Barge Port

Crusher

South Block 1(Dayak Besar)

North Block

40kmMine to port

KedangpahuRiver

ROM stockpile

BunyutPort

0 10 2515 205 km

Product coal conveyor, stacking,

stockpile

TRUBAINDO-BHARINTO SCHEMATIC

EAST KALIMANTAN

Bharinto 60km south west of

TrubaindoNorth Block

South Block 2(Biangan)

PT. BHARINTO

PT. TRUBAINDO

TRUBAINDO PRODUCTION ANALYSIS

1.5 1.7 1.7 1.8 2.1

1Q 2Q 3Q 4Q

SR : 10.0 11.9 14.1

12.4FY11 output: 7.1mt; FY12 target: 7.1mt

20112012Volume :

BHARINTO PRODUCTION ANALYSIS

1Q 2Q 3Q 4Q

FY12 target: 0.7mt

Volume : 0.0 0.0 0.0 0.00.1

20112012

1.8

13.4

0.0

Trubaindo: 1Q12 production was slightly higher than plan due to additional stock from ROM stockyard.

Bharinto: Coal production already commenced since April 2012.Coal hauling and coal crushing activities already commenced since 1st week of May 2012.

MAJOR QUARTERLY UPDATES

TRUBAINDO PRODUCTION ANALYSIS

Kitadin Embalut and Td.Mayang

13

Balikpapan

MahakamRiver Samarinda to Muara Berau

Bontang city

EMBALUT

Embalut Port

to Muara Jawa

ROM stockpile

Operations

Stockpile

Ports

Hauling

Crusher

0 106 82 km4

5km Mine to port

TD. MAYANG

EAST KALIMANTAN

IMM EB

KITADIN SCHEMATIC

IMM WB

Bontang Port

EMBALUT PRODUCTION ANALYSIS

0.3 0.3 0.3 0.4

1Q 2Q 3Q 4Q

SR : 8.9 8.7 11.2 11.5FY11 output: 1.3mt; FY12 target: 0.7mt

Volume :

TD.MAYANG PRODUCTION ANALYSIS

1Q 2Q 3Q 4Q

Volume :0.0 0.0 0.0

0.3

FY11 output: 0.4mt; FY12 target: 2.7mt

20112012

201120120.40.5

15.1SR :

0.3

12.1

0.6

15.1

Kitadin Embalut: 1Q12 production achieved slightly higher than plan due to normal weather condition and good support from mining contractor.

Kitadin Tandung Mayang:1Q12 production achieved according to plan as most of the mining equipment has already put in place.Expect 2.7mt production for the full year of 2012.

MAJOR QUARTERLY UPDATES

Jorong

14

Coal terminal

Jorong

Pelaihari

Pacific Ocean

Haul road

Operations

Stockpile

Hauling

Barge Port

0 10 2515 205 km

20km

JORONG SCHEMATIC JORONG PRODUCTION ANALYSIS

0.3 0.3

1Q 2Q 3Q 4Q

SR :

FY11 output: 1.4mt; FY12 target: 1.0mt

8.6

Volume : 0.4

8.6

0.4

8.6

201120120.3

8.6

0.3

8.6

1Q12 production achieved slightly above target due to better weather condition.

Annual production output will be maintained at around 1.0mt due to limited reserves.

MAJOR QUARTERLY UPDATES

Disclaimer

15

Agenda

3. Commercial Review

(a) Long-term Coal Market Analysis

(b) Coal Market Update

(c) ITM Coal Sales

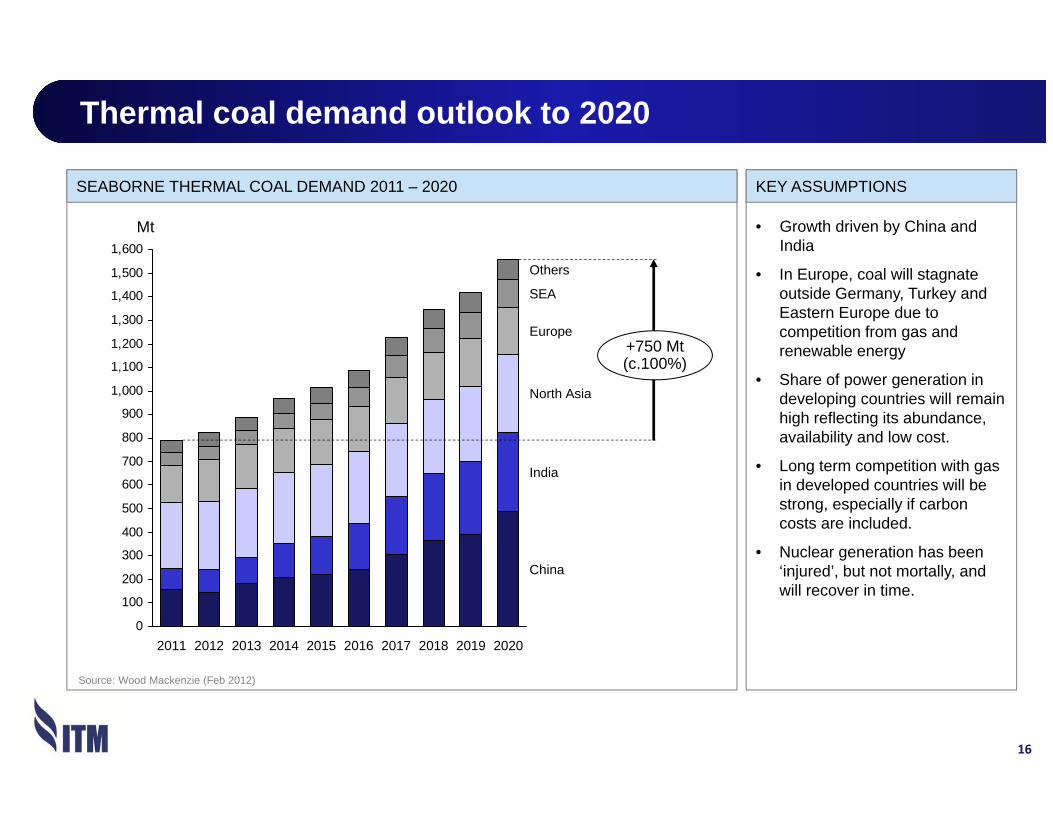

Thermal coal demand outlook to 2020

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

+750 Mt(c.100%)

China

India

North Asia

Europe

SEA

Others

2020201920182017201620152014201320122011

Source: Wood Mackenzie (Feb 2012)

Unit: MtSEABORNE THERMAL COAL DEMAND 2011 – 2020 KEY ASSUMPTIONS

• Growth driven by China and India

• In Europe, coal will stagnate outside Germany, Turkey and Eastern Europe due to competition from gas and renewable energy

• Share of power generation in developing countries will remain high reflecting its abundance, availability and low cost.

• Long term competition with gas in developed countries will be strong, especially if carbon costs are included.

• Nuclear generation has been ‘injured’, but not mortally, and will recover in time.

Mt

16

17

Key dynamics affecting long term Asian thermal coal marketIS

SU

ES

GOVERNMENT POLICY

DEMAND ELASTICITY

NUCLEAR GAS FREIGHTMACRO-ECONOMICS

+++

--

-

++

---

NE

T IM

PAC

T ?

+

• Developing countries growth

• EU debt risks

• Credit issues

• Exchange rate risks

• China: price cap

• India: nuclear policy, coal tax, environmental

• Indonesia: DMO, export tax, foreign % limits

• Australia: MRRT, carbon tax

• S.Africa: mining law, tax policy

• Demand-side management and new tech

• Japan: target to reduce energy consumption 7% by 2030

• China: target to reduce energy (by 16%) and carbon (by 17%) intensity by 2015

• Aftermath of Fukushima: delays, cancellations

• Japan: closed (c. 90 Mtce*) but how much will come back ?

• Taiwan: cap ?

• China and India diversification of supply security ?

• US: low gas price; availability of domestic coal

• China: shale gas; Russian and Burma pipelines

• Gas price in Asia linked to oil price: not competitive with coal (LNG delink ?)

• Low freight rates now

• Will rise

• Rise will limit Columbia, US and some South Africa exports to Asia

Development time lags

Medium term Time lags if recover

Time lags Short to medium term

* Million tonne of coal equivalent (based on 6,700 kcal/kg GAD)

18

Long term thermal demand and supply outlook 2011 – 2015

Source: Wood Mackenzie, Company

Change in supply (Mt)

Change in demand (Mt)

+112+75

+65 +15

+40

+20

+15REST OF WORLD

NORTHEAST ASIA

SOUTHEAST ASIA

CHINA

INDIA

EUROPE

+90+25

+40+80

- 5

COLOMBIA

SOUTH AFRICA

INDONESIA

AUSTRALIA

Total Change +230Mt

19

Long term thermal demand and supply outlook 2011 – 2020

Source: Wood Mackenzie, Company

+30

+320

+245

+45 NORTHEAST ASIA

SOUTHEAST ASIA+65

+45

Change in supply (Mt)

Change in demand (Mt)

REST OF WORLD

INDIA

CHINA

EUROPE

+290

+265

+65

+20

+30

+30

+60- 10

AUSTRALIA

INDONESIA

SOUTH AFRICA

MOZAMBIQUECOLOMBIA

USA

Total change +750Mt

20

New thermal coal supply considerations for Asian market

* Low Rank Coal or LRC (CV less than 4,500 kcal/kg GAR); note that Indonesian government defines as coal with CV less than 4,200 kcal/kg GAR)Source: Wood Mackenzie, Company

Change in supply (Mt)

QUALITY: Downward shift in coal quality. LRC* is forecast to have the fastest production growth and accounts for 50% of Indonesia’s marketable reserves

INFRASTRUCTURE: Required rail in the longer term (Sumatra, Central Kalimantan)

POLICY: Tax, DMO, etc.

INFRASTRUCTURE: Require commitment of production and infrastructure expansion (Surat, Galilee)

POLICY: Policy constraints delay timetables.

FREIGHT: Low competitiveness in Asia due to substantial freight disadvantage to Australia and Indonesia.

INFRASTRUCTURE: Require major logistic infrastructure improvement and commitments (esp. from growth markets like China and India)

COST: Cannot out compete Indonesian margins

FREIGHT: Low competitiveness in Asia esp. from east coast

POLICY: Environmental.

DOMESTIC COAL. QUALITY / COST: New production is lower CV while replacement production costs rising relatively quickly

AUSTRALIA

INDONESIA

CHINA

COLOMBIA

USA

21

Focus on Australian and Indonesian supply analysis

AUSTRALIA (40% of supply growth 2011 – 2020) INDONESIA (35% of supply growth 2011 – 2020)

0

50

100

150

200

250

Surat

SydneyGalileeGunnedahOthers

Identified vsunidentified

Required supply growth

Source: Wood Mackenzie, Company

Unidentified

0

50

100

150

200

250

BaritoE. KaliMahakamSumatraOthers

Identified vsunidentified

Required supply growth

Source: Wood Mackenzie, Company

• Requires additional supply for medium and long term needs• Reliance on Sydney basin in the short term and Surat in the

longer term• Surat and Galilee require new infrastructure• Environmental sensitivities and challenges

• Limited large scale projects in pipeline• More than half of identified supply is low ranked coal (LRC)• Environmental and policy constraints

Unidentified

Mt Mt

22

Seaborne thermal coal cost curve analysis

2012 CV ADJUSTED COST CURVE (6,322 GAR) 2020 CV ADJUSTED COST CURVE (6,322 GAR) ?

0

10

20

30

40

50

60

70

80

90

0 200 400 600 800CUMULATIVE SUPPLY (Mt)

Vietnam

Indonesia

Colombia

S.Africa Australia

RussiaChina

US

• Higher stripping ratio, lower quality, depleting reserves for current capacity

• Lower quality, higher-cost production for future capacity

• Indonesia continues to be competitive in Asia

• Australia less competitive due to stronger A$

• Columbia / US to Asia depends on low freight rate

CUMULATIVE SUPPLY (Mt)

0 100 200 300 400 500 600 700 800 9001,000 1,500

50

100

150

200

2012

20202020

DEMAND

???

$/t$/t

~$6/t

~$5/t

Source: Wood Mackenzie, Company Source: Wood Mackenzie, Company

23

Prices must rise to support cost of new capacity

ILLUSTRATIVE INCENTIVE PRICES FOR NEW COAL PROJECTS ($/t)INCENTIVE COAL PRICES FOR NEW COAL PROJECTS COMMENTS

Source: Wood Mackenzie, AWR Lloyd analysis

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

Min

Avg.*

Max

APPALACHIAUS

SURATAUSTRALIA

ILLINOISUS

LRC**INDONESIA

GALILEEAUSTRALIA

CV ADJUSTED FOB CASH COST

CAPITAL FOR RAIL,

PORT?CAPITAL

FOR LOGISTICS?

QUALITY, FREIGHT

DIFFERENTIAL?

CAPITAL

2012$/t

* Capacity weighted average** Low Rank Coal or LRC (CV less than 4,500 kcal/kg GAR); note that Indonesian government defines as coal with CV less than 4,200 kcal/kg GAR

• Most new projects are yesterday’s “undesirable projects” due to:

• Poorer quality

• Costly and difficult logistics

• More challenging policy issues

• Prices will have to be high enough to incentivize development of these projects

24

The trend to lower quality and higher cost coal supply

ESTIMATED PORTION OF LOW RANK COAL IN LONG TERM INDONESIAN SUPPLY COMMENTS

85%

LRC*

15% 25%

49%

Potential LRC*26%

300Mt 570 Mt

REQUIRED CAPACITY

2012 2020

Source: Wood Mackenzie, Company

* Low Rank Coal or LRC (CV less than 4,500 kcal/kg GAR); note that Indonesian government defines as coal with CV less than 4,200 kcal/kg GAR

SUPPLY

• Flat output for mid and high cvcoal

• Significant portion of new capacity could be LRC

• More blending of mid CV with LRC to improve attractiveness of LRC

BUYERS

• Need to be flexible and can be more flexible

• Blending for cost and quality

• High CV segment tighter requiring adjustments to purchase policy and coal handling

25

1Q 2012 seaborne thermal coal market drivers

WEATHER CHINESE DEMAND OTHER DRIVERS

• Indonesia wet season was normal. Stocks starting to build as rains lessen.

• Chinese winter was normal followed by water shortages.

• Australian storms/floods damage has been limited.

• GDP growth declining but still relatively good at 8.2%*

• Coal production increased beyond demand increase, but again levels vary by region.

• Imports in 1Q, double 1Q 2011, but 75% of 4Q 2011.

• Policy uncertainty affecting confidence.

• Downward trend in sentiment.

• Uncertainty impacting forecasts due to European debt concerns, Middle East/N. Africa unrest, and exchange rate trends.

• Rate/timing of Chinese import increase – a question?

• Can U.S.A. continue to sell below cost?

• Gas prices reverse to coal’s disadvantage, while short term USA diverts coal to export.

• 2012 world growth forecast 2.2% (Prev. 2.0%); Asian growth forecast 6.5% (Prev. 6.0%)

ASP held up well in 1Q 2012.

Some pressure from weaker market prices, and product mix should cap ASP improvement in 2Q-4Q 2012.

ITM remains protected by relatively high ‘sold with price’ status (+62%) and hedge status (+7%).

26

ITM ASP VS BENCHMARK PRICES COMMENTS

0

20

40

60

80

100

120

140

160

180

200

Mar

-07

Jun-

07

Sep

-07

Dec

-07

Mar

-08

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

Mar

-11

Jun-

11

Sep

-11

Dec

-11

Mar

-12

Monthly BJIQuarterly BJIQuarterly Banpu Indonesia ASP

Unit: $/t

ITM ASPs vs seaborne thermal coal benchmark prices

Monthly NEXQuarterly NEXQuarterly ASP

ASP 1Q12 $101.1/tASP FY10 $97.1/t

NEX* May 03, 2012$101.0

Indicative 2012 Coal Sales

Coal sales contract and pricing status CommentCoal sales contract and pricing status

Contract Status Price Status

Contracted Fixed

Index

TARGET SALES 2012: 27 Mt

UncontractedUnpriced

Unsold

90%

10%

62%

24%4%

10%

Mostly insulated from market weakness (including hedged tonnes, 70% of sales)

27

28

ITM coal sales 1Q12

COAL SALES BREAKDOWN BY DESTINATION 1Q12 (Mt) COAL SALES 1Q12

Total Coal Sales: 5.7 Mt

31%

16%

10%

9%

9%

7%

5%

5%3%

3% 2%

Japan

China

Taiwan

S Korea

Italy

Thailand

Philippines

Hong KongIndia

Indonesia

JAPAN0.9 Mt

PHILIPPINES0.4 Mt

THAILAND0.5 MtINDIA

0.2 Mt

HK0.2 Mt

S KOREA0.3 Mt

CHINA1.8 Mt

TAIWAN0.5 Mt

ITALY0.3 Mt

1.5

INDONESIA0.6 Mt

MALAYSIA0.1 Mt

Malaysia

29

COAL SALES BREAKDOWN BY DESTINATION 2012e (Mt) COAL SALES 2012e

Total Coal Sales: 27.0 Mt

20%

18%

11%9%

8%

7%

6%

6%

4%2%

2% 5%

Japan

China

Taiwan

S Korea

Italy

Thailand

Philippines

Hong Kong

India

Indonesia

JAPAN4.9 Mt

PHILIPPINES1.6 Mt

THAILAND1.9 MtINDIA

2.2 Mt

HK0.6 Mt

S KOREA1.2 Mt

CHINA5.5 Mt

TAIWAN2.5 Mt

ITALY1.7 Mt

1.5

INDONESIA3.0 Mt

MALAYSIA0.5 Mt

Malaysia

ITM coal sales 2012e

Others

OTHERS 1.4 Mt

Disclaimer

30

Agenda

4. Financial Review

(a) Performance Results

(b) Cash Cost

(c) Capital Expenditure

Sales Revenue

31

1Q11 2Q11 3Q11 4Q11 1Q12

1Q11 2Q11 3Q11 4Q11 1Q12

Units: Million Ton

SALES VOLUME

Units: USD/Ton

AVERAGE SELLING PRICE

Units: USD Million

REVENUE* GROWTH

1Q11 2Q11 3Q11 4Q11 1Q12

5.5 5.2

6.8 7.1

97.4

87.3

98.4

103.1

1Q11 2Q11 3Q11 4Q11 1Q12

466500

675

729

5.7

101.1

575

+5% YoY-18% QoQ

+16% YoY-2% QoQ

+23% YoY-21% QoQ

Indominco

Trubaindo

Kitadin

Jorong

* excluding port revenue

1Q11 2Q11 3Q11 4Q11 1Q12

Average Cost

32

Units: US$/Ltr

FUEL PRICE

STRIP RATIO

Units: US$/Ton

TOTAL CASH COST

58.564.6

70.2 71.068.5

1Q11 2Q11 3Q11 4Q11 1Q12 1Q11 2Q11 3Q11 4Q11 1Q12

Units: US$/Ton

CASH PRODUCTION COST

1Q11 2Q11 3Q11 4Q11 1Q12

41.545.3

49.3 48.0 51.9

0.93

1.10 1.05 1.03 1.07

11.911.4

12.3 12.213.1

*Total cash cost including royalty and SG&ASource: Pertamina

Average Gross Margin

33

* COGS included royalty

Units: USD million

ITM Consolidated Indominco Trubaindo Kitadin Jorong1Q11

468

33%

364

22%

164

28%

37%44

18%

19

13%4Q11

733

39%

512

28%

242

38%

93

46%38

17%

Total Revenue

GPM* (%)

1Q12

578

36%

28%

341

27%

228

35%

83

42% 23

18%1Q11 4Q11 1Q12 1Q11 4Q11 1Q12 1Q11 4Q11 1Q12 1Q11 4Q11 1Q12

EBITDA

34

Units: USD million CONSOLIDATED

MINE BY MINE

*COGS = Prod cost + Transport cost + Inv. movement

Revenue4Q111Q11 1Q12

234.6

COGS SellingRoyalty Admin

131.7

71.6

47.0

10.61.9

Indominco Trubaindo1Q11

Kitadin Jorong4Q11

125.6

65.544.3

3.7

1Q12

88.0

64.5

34.8

3.2

Units: USD million

1Q11 4Q11 1Q12 1Q11 4Q11 1Q12 1Q11 4Q11 1Q12

183.8

+55.6+0.2

+25.5

Royalty decreased with revenues

Lower sales volume and ASP

+40% YoY-21% QoQ

(155.2)

+23.1

Net Income

35

4Q11 1Q12OthersEBIT IncomeTax

DerivativeTransactions

FOREXNet Fin.Charges

1Q11

CONSOLIDATED

MINE BY MINE

Units: USD million

95.2

184.9

124.5

55.2

5.4

33.0

(0.4)

Indominco Trubaindo JorongKitadin

116.9

30.145.7

(7.8)

61.442.5

23.3

1Q11 4Q11 1Q12 1Q11 4Q11 1Q12 1Q11 4Q11 1Q12 1Q11 4Q11 1Q12

Units: USD million

(0.6)

Derivative gain/loss

+31% YoY-33% QoQ(50.6)

+1.0

(0.9)(10.3) (12.1)

+12.5

Lower sales volume and ASP

Balance Sheet

36

Net Gearing (%)

Net D/E (times)

(0.34)

(34%)

(Units: USD million)CASH POSITION

2008

222

(Units: USD million)

DEBT POSITION

2008

11

55

2009

429

(0.47)

(44%)

2009

2011

612

0

2011

(0.57)

(57%)

295

2010

0

2010

(0.41)

(41%)

2008 2009 20112010

771

1Q12

0

1Q12

(0.64)

(64%)

1Q12

2012 Capital Expenditure Plan: USD 209 mln

37

Units: USD million

Indominco

Trubaindo

Bharinto

Kitadin

Jorong

ITM Consolidated

5

Realized up to Mar’12

2012 major Capex plan

108

80

9

209

1

6

13

2

1

Note: Total capex plan including Jakarta office

5

1

Disclaimer

38

Question & Answer

Disclaimer

39

Agenda

Appendices

ITM Structure and History

40

ITMG

65.00%

Indominco Trubaindo Bharinto Jorong

PT Indominco Mandiri

(CCOW Gen.I)

PT Trubaindo Coal Mining

(CCOW Gen II)

PT Kitadin-Embalut

(KP)

PT Bharinto Ekatama

(CCOW Gen III)

PT Jorong Barutama Greston

(CCOW Gen II)

50.00%

PT Indo Tambangraya Megah Tbk.

Banpu Minerals (Singapore) Pte Ltd

99.99% 99.99% 99.99%99.99% 99.67%

174 Mt

695 MtResources

Reserves102 Mt

327 MtResources

Reserves13 Mt

150 MtResources

Reserves112 Mt

298 MtResources

Reserves6 Mt

144 MtResources

Reserves

Banpu Minerals Co.Ltd

Reserves 411* Mt

Resources 1,627* Mt

BMS

99.99%

BMC

Banpu PCLBanpu

Public35.00%

Kitadin

PT Kitadin-Td.Mayang

(KP)

10 Mt13 Mt

Resources

Reserves

BCI50.00%

100.00%Banpu Coal

Investment Co.Ltd

Note: * Updated Coal Resources and Reserves as of 31 Mar 2012

East Kalimantan East Kalimantan South KalimantanEast KalimantanEast / Central Kalimantan

INDONESIAN STOCK EXCHANGEIPO 18th Dec 2007

6,500-7,300 kcal/kg6,000-6,300 kcal/kg 5,800 kcal/kg6,400-6,800 kcal/kg 6,700 kcal/kg 5,300 kcal/kg

Coal Resources and Reserves (as of 31 Mar 2012)

41

Indominco

Kitadin-Td.Mayang

Jorong

Trubaindo

W.Block

E.Block

242 Mt

26 Mt

453 Mt

151 Mt

14Mt

144 Mt

5Mt

327 Mt

100 Mt

298 Mt

112 Mt

12Mt

RESOURCES

RESERVES

Kitadin-Embalut

Total Reserves: 411 Mt

Total Resources: 1,627 Mt

145 Mt

9Mt

Bharinto

Note: * Updated Coal Resources and Reserves as of 31 Mar 2012 based on estimates prepared by Competent Persons (consider suitably experienced under the JORC Code)in 31 Dec 2010 and deducted from coal sales volume in 1Q12

42

Income Statement

Unit: US$ thousand 1Q12 4Q11 1Q11 QoQ% YoY%

Net Sales 577,955 733,123 468,330 -21% 23%Gross Profit 209,207 285,596 152,077 -27% 38%GPM 36% 39% 32%SG&A (40,025) (65,788) (34,646) EBIT 169,182 219,808 117,431 -23% 44%EBIT Margin 29% 30% 25%EBITDA 183,851 232,773 131,754 -21% 40%EBITDA Margin 32% 32% 28%Net Interest Income / (Expenses) 3,028 2,035 255 FX Gain / (Loss) (2,138) (1,222) 3,187 Derivative Gain / (Loss) 26,916 37,180 9,497 Others (21,492) (9,346) (3,379) Profit Before Tax 175,496 248,455 126,991 -29% 38%Income Tax (50,999) (63,539) (31,765) Net Income 124,497 184,916 95,226 -33% 31%Net Income Margin 22% 25% 20%