Embed Size (px)

Citation preview

ITEM NO. 1-A

Confirmation and signing of the minutes of last Council’s Meeting No.

10/2001-2002 held on 28.1.2002 AT 11-00 A.M. (See pages 2 - 11) at Committee

Room, Palika Kendra, NDMC.

COUNCIL’S DECISION

Confirmed subject to the modification that the following be further added in the minutes relating to item No. 3(xv) “the qualification prescribed as ‘advance diploma of National Fire Service College, Nagpur for the post of Asstt. Fire Officer shall be substituted with “Station Officer Course from NFSC, Nagpur or equivalent as per R.Rs for the equivalent post in Delhi Fire Service.”

1

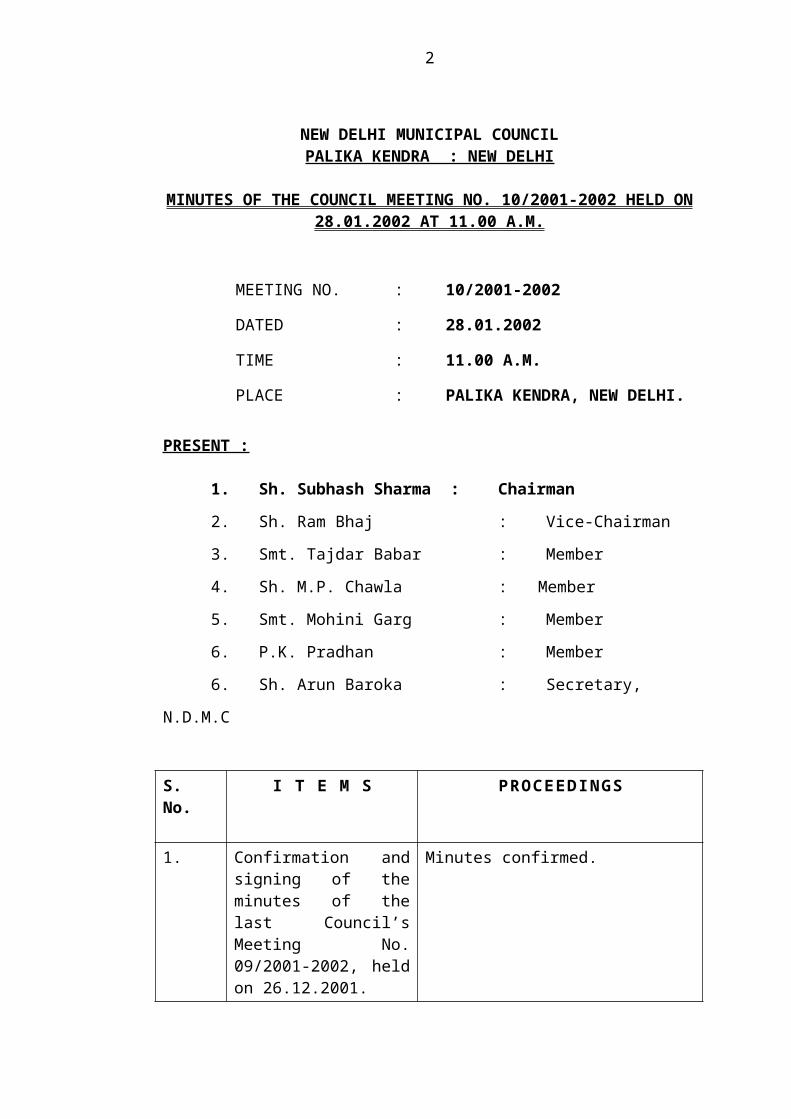

NEW DELHI MUNICIPAL COUNCILPALIKA KENDRA : NEW DELHI

MINUTES OF THE COUNCIL MEETING NO. 10/2001-2002 HELD ON 28.01.2002 AT 11.00 A.M.

MEETING NO. : 10/2001-2002

DATED : 28.01.2002

TIME : 11.00 A.M.

PLACE : PALIKA KENDRA, NEW DELHI.

PRESENT :

1. Sh. Subhash Sharma : Chairman

2. Sh. Ram Bhaj : Vice-Chairman

3. Smt. Tajdar Babar : Member

4. Sh. M.P. Chawla : Member

5. Smt. Mohini Garg : Member

6. P.K. Pradhan : Member

6. Sh. Arun Baroka : Secretary, N.D.M.C

S. No. I T E M S PROCEEDINGS

1. Confirmation and signing of the minutes of the last Council’s Meeting No. 09/2001-2002, held on 26.12.2001.

Minutes confirmed.

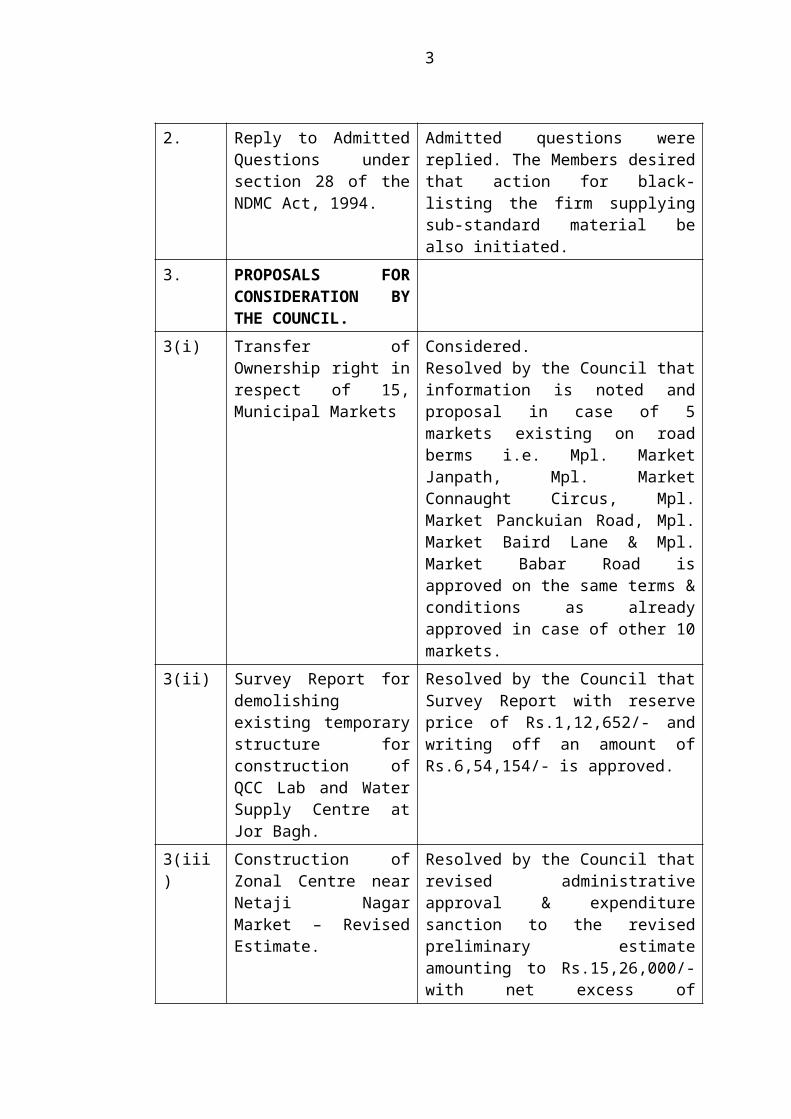

2. Reply to Admitted Questions under section 28 of the NDMC Act, 1994.

Admitted questions were replied. The Members desired that action for black-listing the firm supplying sub-standard material be also initiated.

3. PROPOSALS FOR CONSIDERATION BY THE COUNCIL.

3(i) Transfer of Ownership right in respect of 15, Municipal Markets

Considered.Resolved by the Council that information is noted and proposal in case of 5 markets existing on road berms i.e. Mpl. Market

2

Janpath, Mpl. Market Connaught Circus, Mpl. Market Panckuian Road, Mpl. Market Baird Lane & Mpl. Market Babar Road is approved on the same terms & conditions as already approved in case of other 10 markets.

3(ii) Survey Report for demolishing existing temporary structure for construction of QCC Lab and Water Supply Centre at Jor Bagh.

Resolved by the Council that Survey Report with reserve price of Rs.1,12,652/- and writing off an amount of Rs.6,54,154/- is approved.

3(iii) Construction of Zonal Centre near Netaji Nagar Market – Revised Estimate.

Resolved by the Council that revised administrative approval & expenditure sanction to the revised preliminary estimate amounting to Rs.15,26,000/- with net excess of Rs.7,13,000/- is accorded.

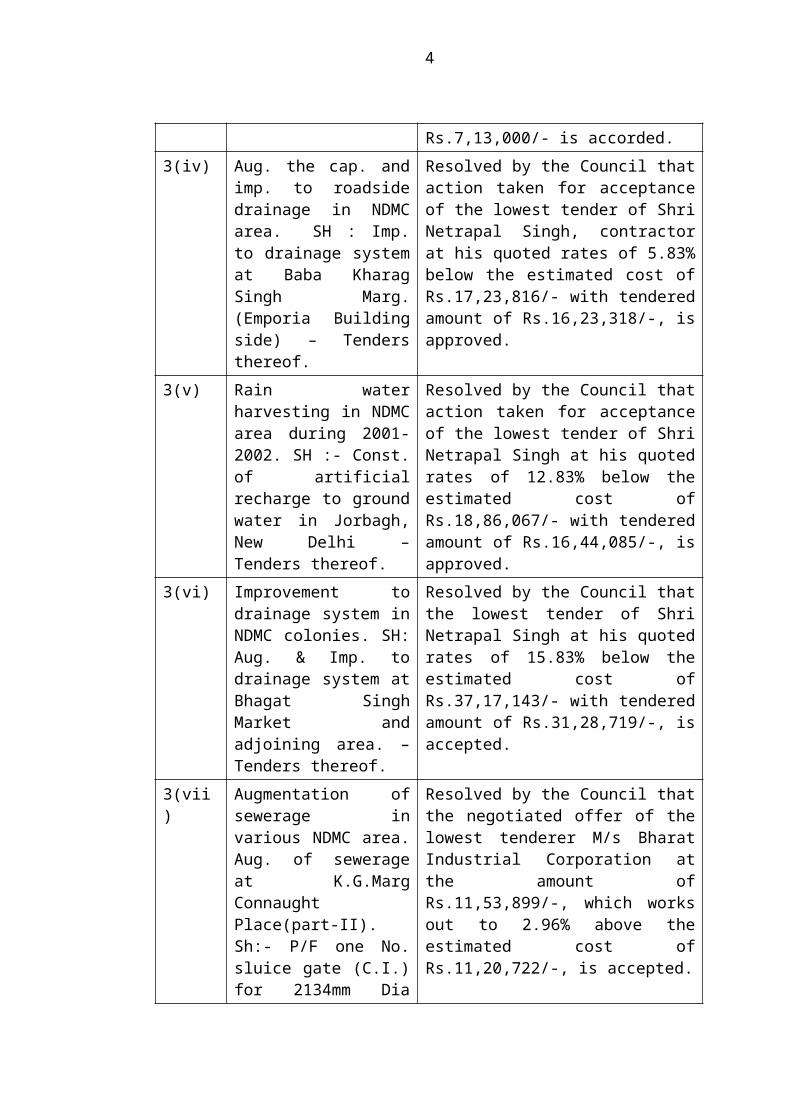

3(iv) Aug. the cap. and imp. to roadside drainage in NDMC area. SH : Imp. to drainage system at Baba Kharag Singh Marg. (Emporia Building side) – Tenders thereof.

Resolved by the Council that action taken for acceptance of the lowest tender of Shri Netrapal Singh, contractor at his quoted rates of 5.83% below the estimated cost of Rs.17,23,816/- with tendered amount of Rs.16,23,318/-, is approved.

3(v) Rain water harvesting in NDMC area during 2001-2002. SH :- Const. of artificial recharge to ground water in Jorbagh, New Delhi – Tenders thereof.

Resolved by the Council that action taken for acceptance of the lowest tender of Shri Netrapal Singh at his quoted rates of 12.83% below the estimated cost of Rs.18,86,067/- with tendered amount of Rs.16,44,085/-, is approved.

3(vi) Improvement to drainage system in NDMC colonies. SH: Aug. & Imp. to drainage system at Bhagat Singh Market and adjoining area. – Tenders thereof.

Resolved by the Council that the lowest tender of Shri Netrapal Singh at his quoted rates of 15.83% below the estimated cost of Rs.37,17,143/- with tendered amount of Rs.31,28,719/-, is accepted.

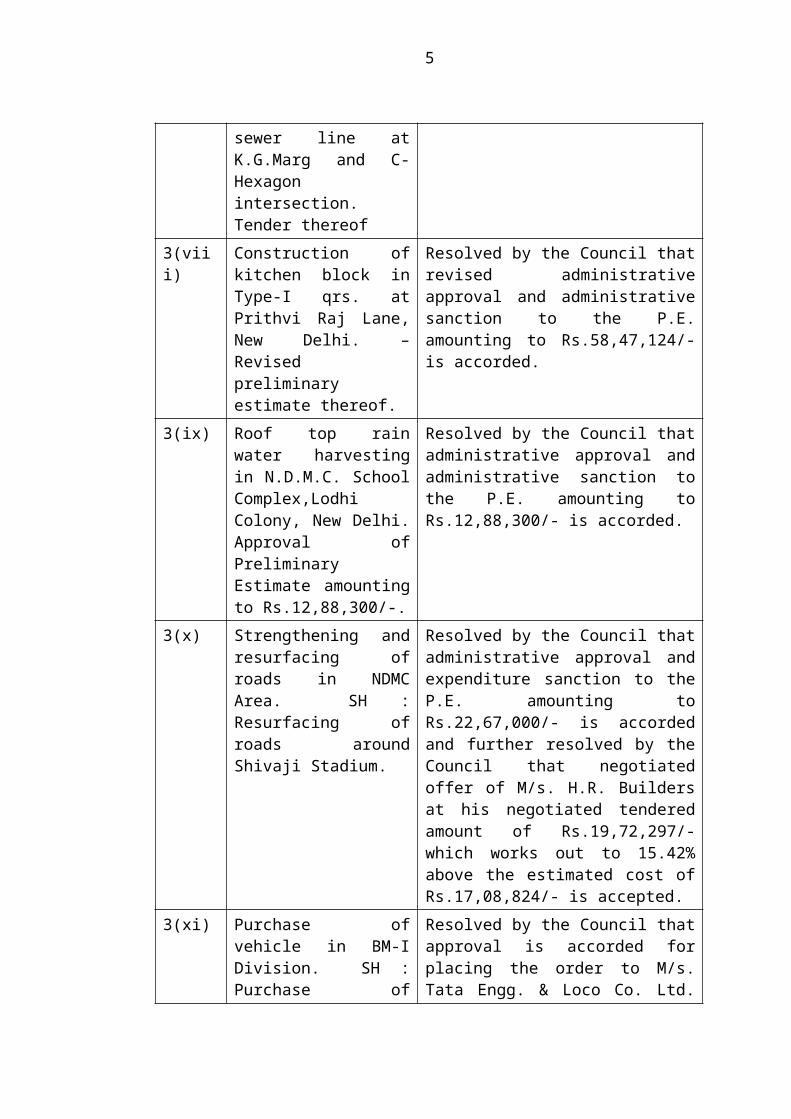

3(vii) Augmentation of sewerage in various NDMC area. Aug. of sewerage at K.G.Marg Connaught Place(part-II). Sh:- P/F one No. sluice gate (C.I.) for 2134mm Dia sewer line at

Resolved by the Council that the negotiated offer of the lowest tenderer M/s Bharat Industrial Corporation at the amount of Rs.11,53,899/-, which works out to 2.96% above the estimated cost of Rs.11,20,722/-, is accepted.

3

K.G.Marg and C-Hexagon intersection. Tender thereof

3(viii) Construction of kitchen block in Type-I qrs. at Prithvi Raj Lane, New Delhi. – Revised preliminary estimate thereof.

Resolved by the Council that revised administrative approval and administrative sanction to the P.E. amounting to Rs.58,47,124/- is accorded.

3(ix) Roof top rain water harvesting in N.D.M.C. School Complex,Lodhi Colony, New Delhi. Approval of Preliminary Estimate amounting to Rs.12,88,300/-.

Resolved by the Council that administrative approval and administrative sanction to the P.E. amounting to Rs.12,88,300/- is accorded.

3(x) Strengthening and resurfacing of roads in NDMC Area. SH : Resurfacing of roads around Shivaji Stadium.

Resolved by the Council that administrative approval and expenditure sanction to the P.E. amounting to Rs.22,67,000/- is accorded and further resolved by the Council that negotiated offer of M/s. H.R. Builders at his negotiated tendered amount of Rs.19,72,297/- which works out to 15.42% above the estimated cost of Rs.17,08,824/- is accepted.

3(xi) Purchase of vehicle in BM-I Division. SH : Purchase of tempoes in BM-I Division during 2000-01.

Resolved by the Council that approval is accorded for placing the order to M/s. Tata Engg. & Loco Co. Ltd. amounting to Rs.14,63,512.70 for purchase of two nos. tempoes Tata Model SFC-407/31 CLB & One No. truck Tata Model SFA 709/38 Box type Tipper.

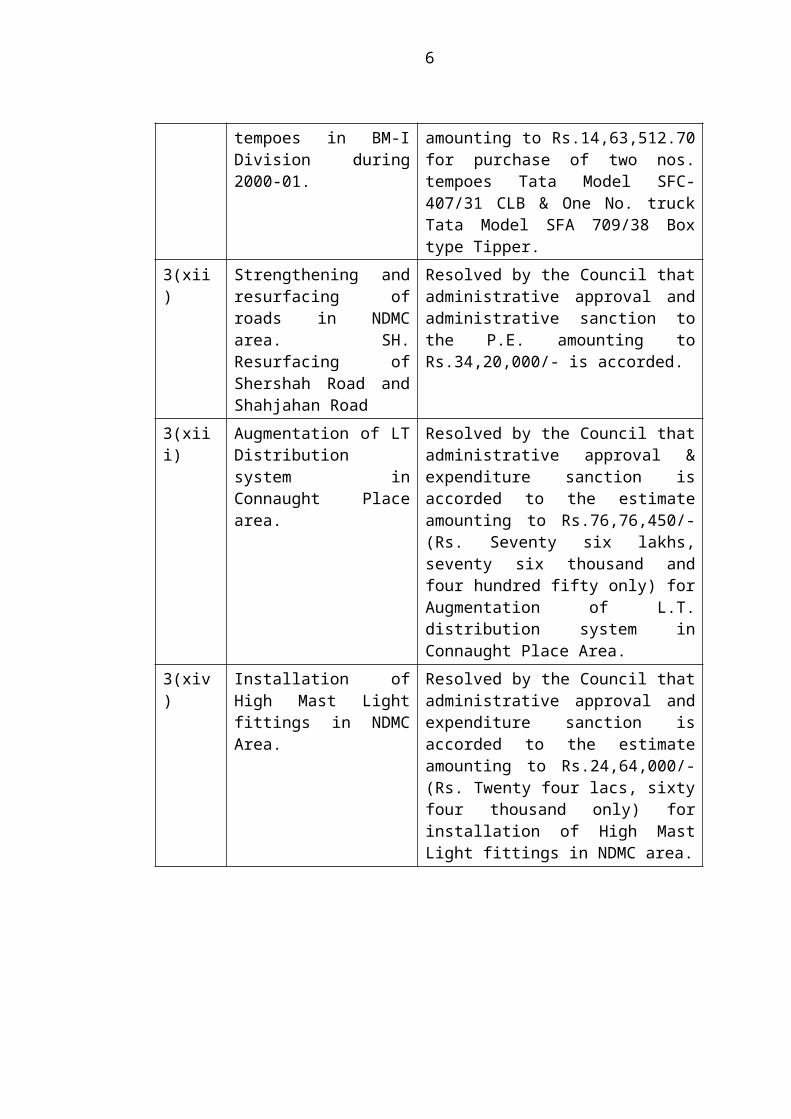

3(xii) Strengthening and resurfacing of roads in NDMC area. SH. Resurfacing of Shershah Road and Shahjahan Road

Resolved by the Council that administrative approval and administrative sanction to the P.E. amounting to Rs.34,20,000/- is accorded.

3(xiii) Augmentation of LT Distribution system in Connaught Place area.

Resolved by the Council that administrative approval & expenditure sanction is accorded to the estimate amounting to Rs.76,76,450/- (Rs. Seventy six lakhs, seventy six thousand and four hundred fifty only) for Augmentation of L.T. distribution system in Connaught Place Area.

4

3(xiv) Installation of High Mast Light fittings in NDMC Area.

Resolved by the Council that administrative approval and expenditure sanction is accorded to the estimate amounting to Rs.24,64,000/- (Rs. Twenty four lacs, sixty four thousand only) for installation of High Mast Light fittings in NDMC area.

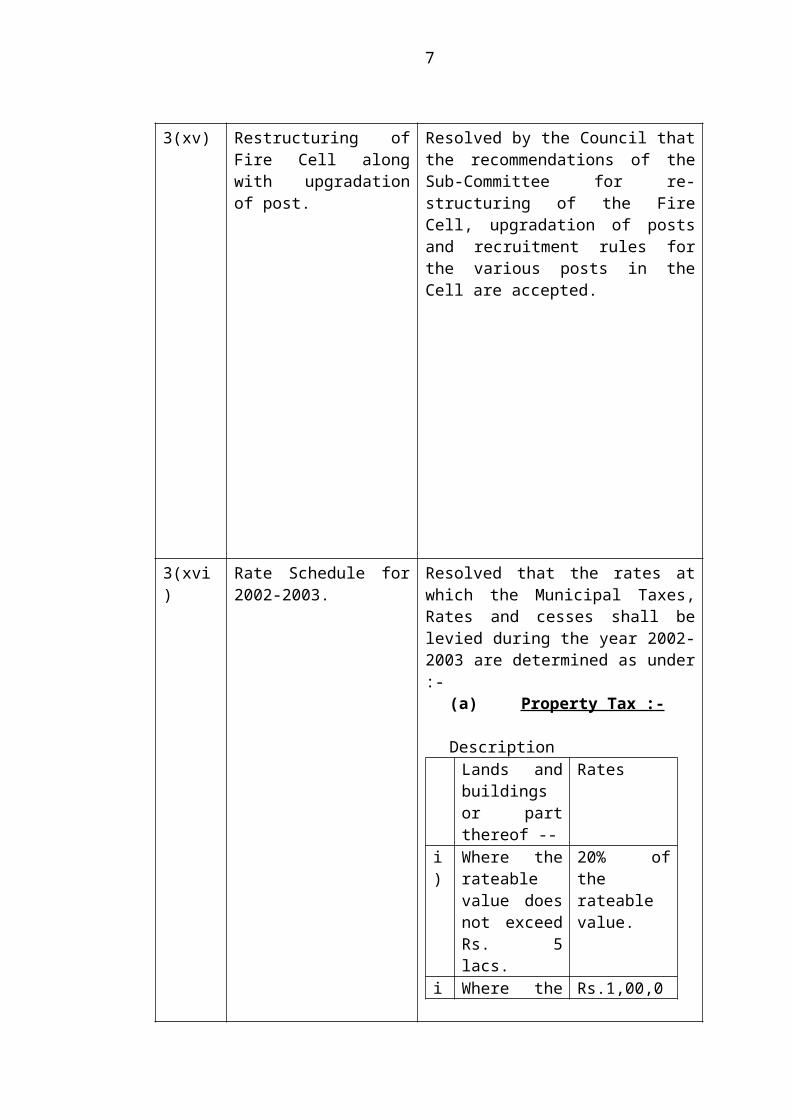

3(xv) Restructuring of Fire Cell along with upgradation of post.

Resolved by the Council that the recommendations of the Sub-Committee for re-structuring of the Fire Cell, upgradation of posts and recruitment rules for the various posts in the Cell are accepted.

3(xvi) Rate Schedule for 2002-2003.

Resolved that the rates at which the Municipal Taxes, Rates and cesses shall be levied during the year 2002-2003 are determined as under :-

(a) Property Tax :-

DescriptionLands and buildings or part thereof --

Rates

i) Where the rateable value does not exceed Rs. 5 lacs.

20% of the rateable value.

ii) Where the rateable value

Rs.1,00,000/- plus 30% of

5

exceeds Rs. 5 lacs.

the amount by which the rateable value exceeds Rs. 5 lacs.

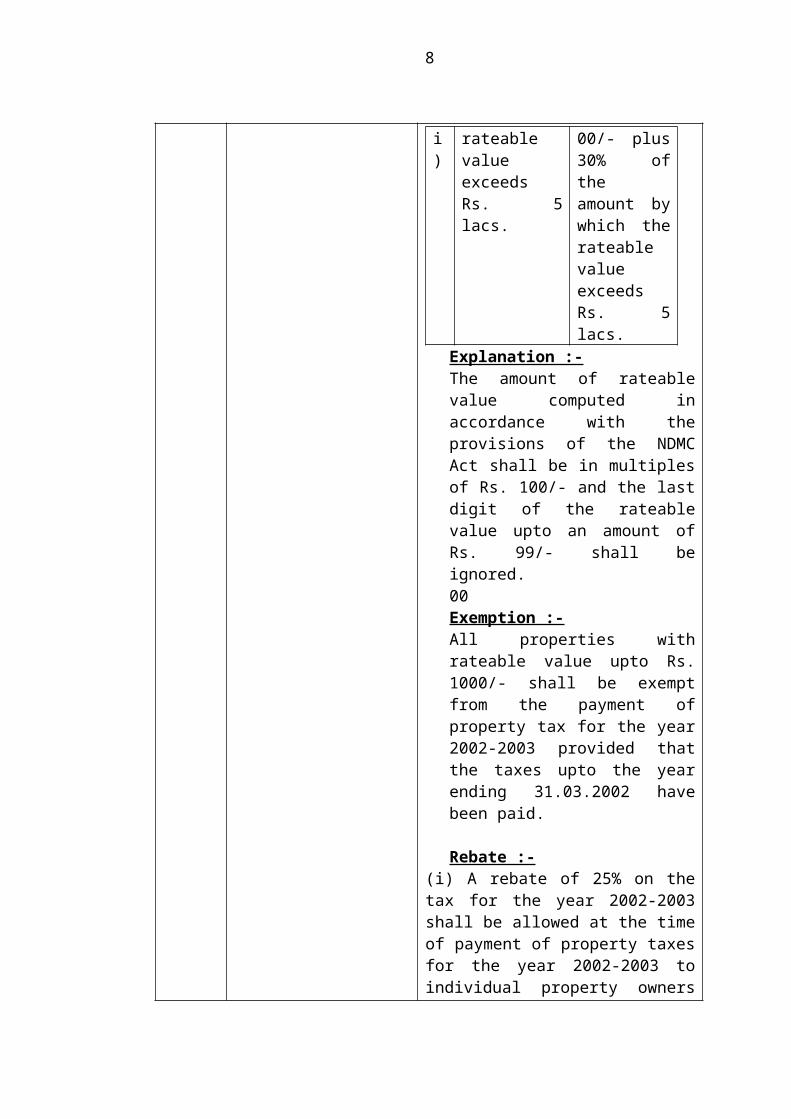

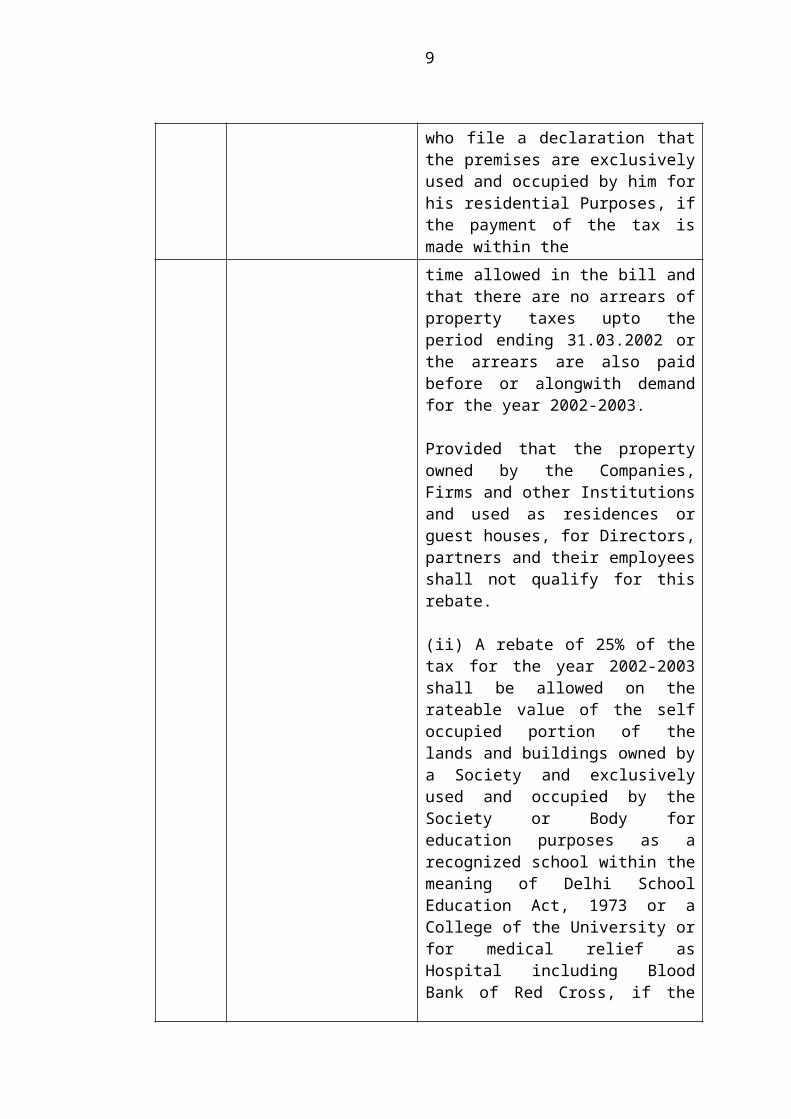

Explanation :-The amount of rateable value computed in accordance with the provisions of the NDMC Act shall be in multiples of Rs. 100/- and the last digit of the rateable value upto an amount of Rs. 99/- shall be ignored.00Exemption :-All properties with rateable value upto Rs. 1000/- shall be exempt from the payment of property tax for the year 2002-2003 provided that the taxes upto the year ending 31.03.2002 have been paid.

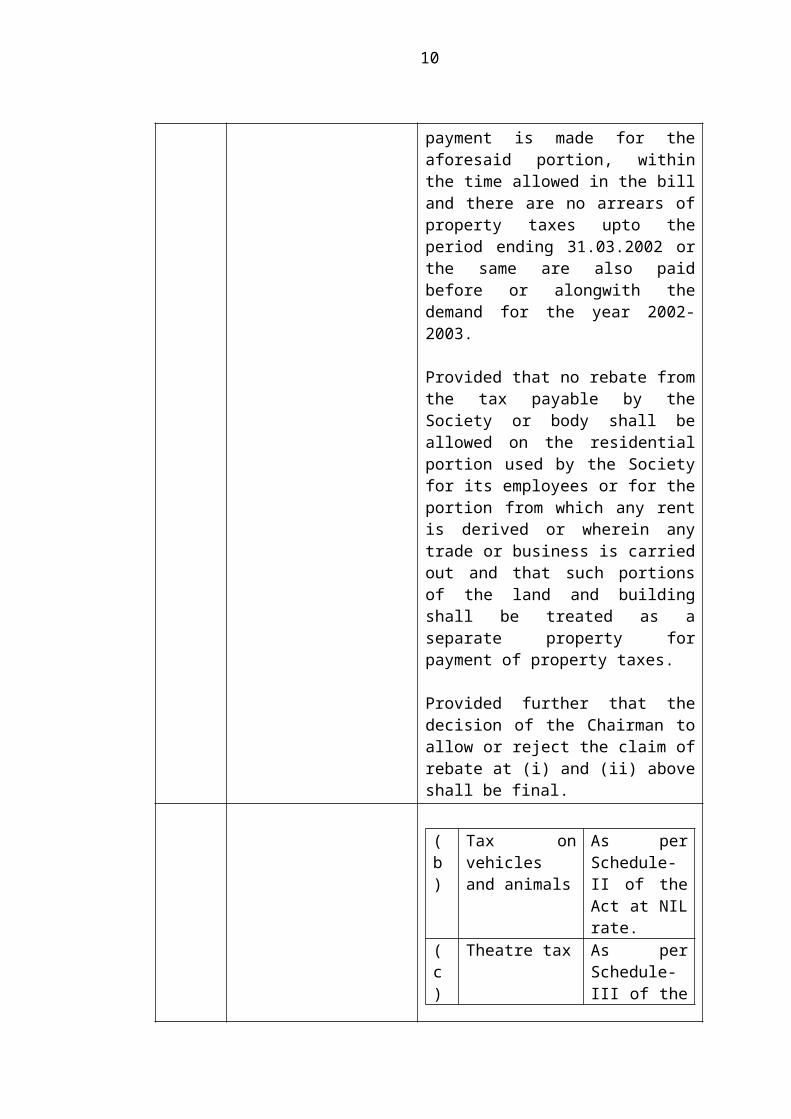

Rebate :-(i) A rebate of 25% on the tax for the year 2002-2003 shall be allowed at the time of payment of property taxes for the year 2002-2003 to individual property owners who file a declaration that the premises are exclusively used and occupied by him for his residential Purposes, if the payment of the tax is made within the

6

time allowed in the bill and that there are no arrears of property taxes upto the period ending 31.03.2002 or the arrears are also paid before or alongwith demand for the year 2002-2003.

Provided that the property owned by the Companies, Firms and other Institutions and used as residences or guest houses, for Directors, partners and their employees shall not qualify for this rebate.

(ii) A rebate of 25% of the tax for the year 2002-2003 shall be allowed on the rateable value of the self occupied portion of the lands and buildings owned by a Society and exclusively used and occupied by the Society or Body for education purposes as a recognized school within the meaning of Delhi School Education Act, 1973 or a College of the University or for medical relief as Hospital including Blood Bank of Red Cross, if the payment is made for the aforesaid portion, within the time allowed in the bill and there are no arrears of property taxes upto the period ending 31.03.2002 or the same are also paid before or alongwith the demand for the year 2002-2003.

Provided that no rebate from the tax payable by the Society or body shall be allowed on the residential portion used by the Society for its employees or for the portion from which any rent is derived or wherein any trade or business is carried out and that such portions of the land and building shall be treated as a separate property for payment of property taxes.

Provided further that the decision of the Chairman to allow or reject the claim of rebate at (i) and (ii) above shall be final.

7

(b) Tax on vehicles and animals

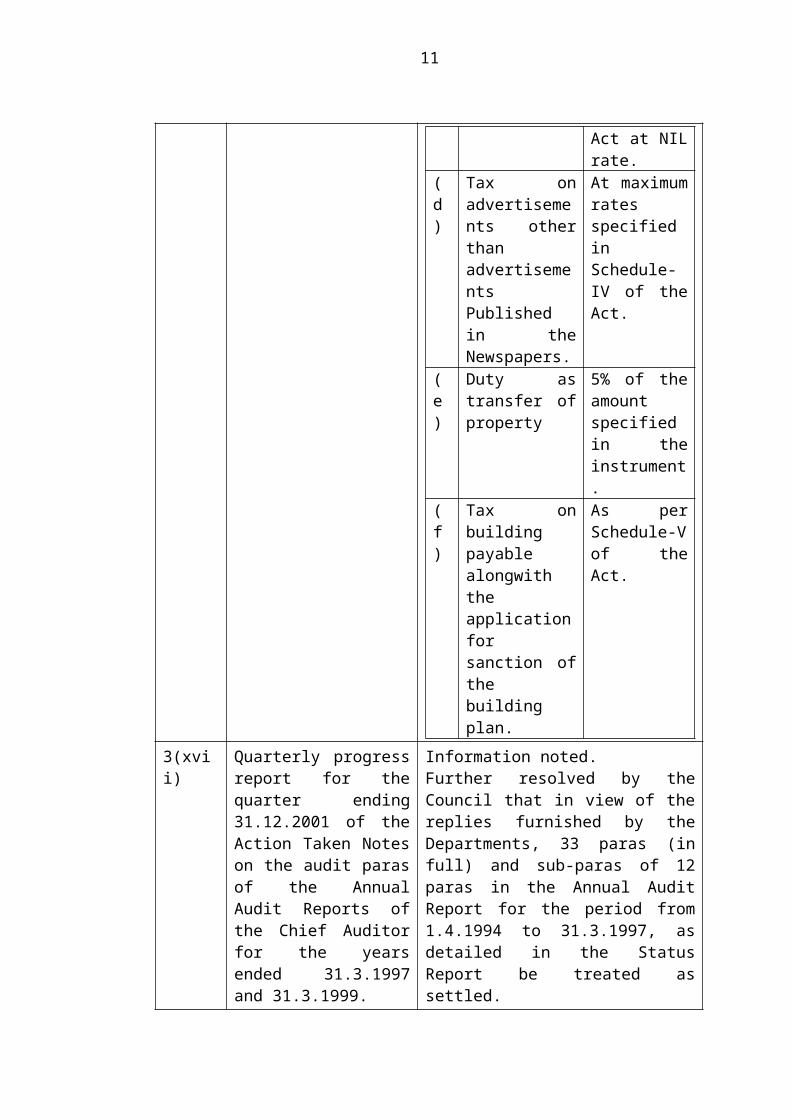

As per Schedule-II of the Act at NIL rate.

(c) Theatre tax As per Schedule-III of the Act at NIL rate.

(d) Tax on advertisements other than advertisements Published in the Newspapers.

At maximum rates specified in Schedule-IV of the Act.

(e) Duty as transfer of property

5% of the amount specified in the instrument.

(f) Tax on building payable alongwith the application for sanction of the building plan.

As per Schedule-V of the Act.

3(xvii) Quarterly progress report for the quarter ending 31.12.2001 of the Action Taken Notes on the audit paras of the Annual Audit Reports of the Chief Auditor for the years ended 31.3.1997 and 31.3.1999.

Information noted.Further resolved by the Council that in view of the replies furnished by the Departments, 33 paras (in full) and sub-paras of 12 paras in the Annual Audit Report for the period from 1.4.1994 to 31.3.1997, as detailed in the Status Report be treated as settled.

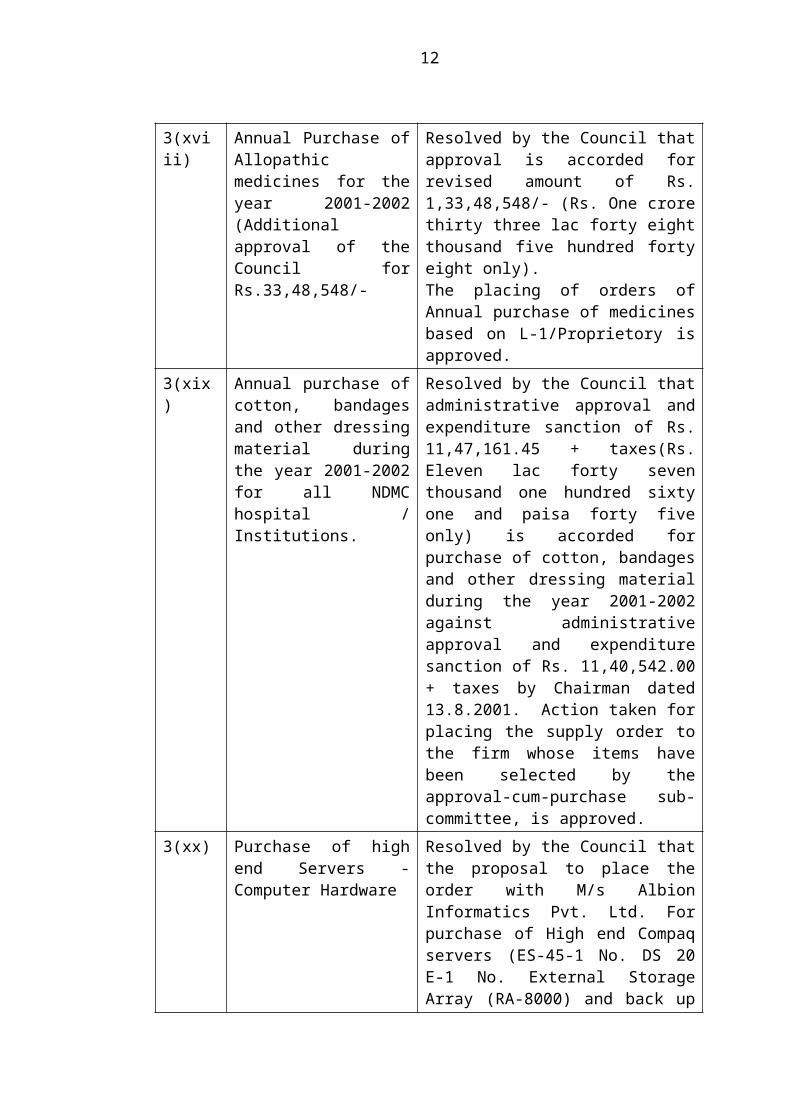

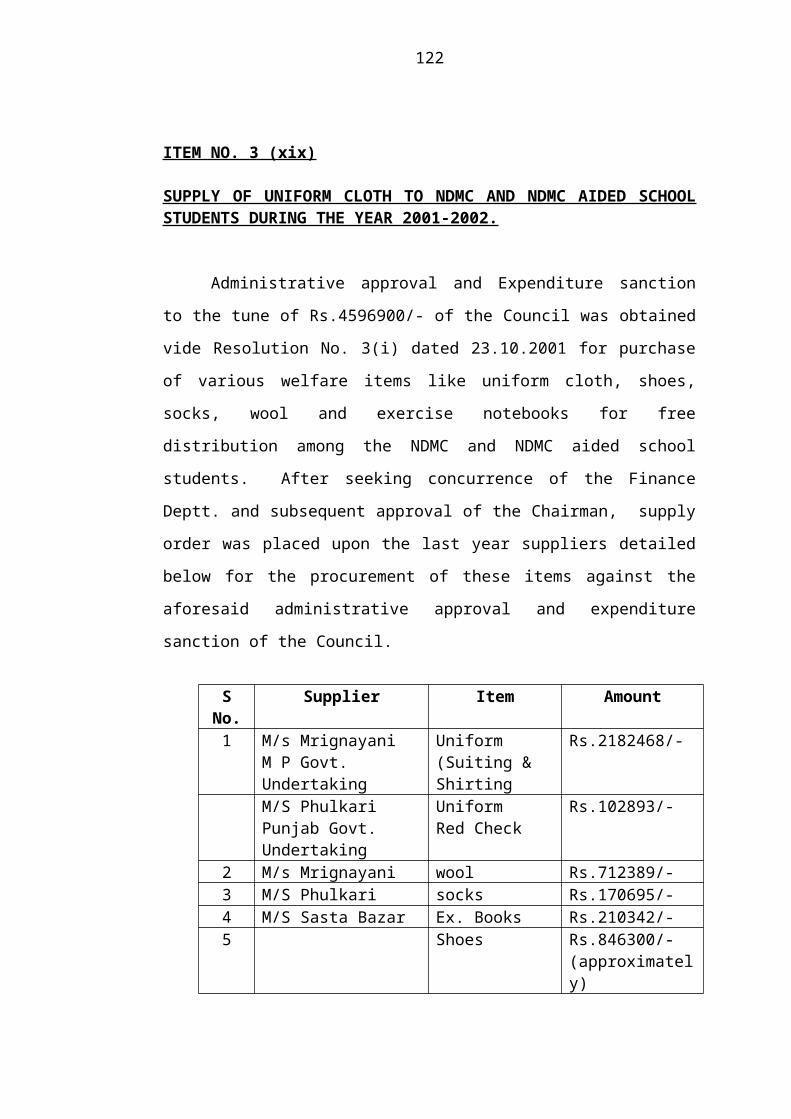

3(xviii) Annual Purchase of Allopathic medicines for the year 2001-2002 (Additional approval of the Council for Rs.33,48,548/-

Resolved by the Council that approval is accorded for revised amount of Rs. 1,33,48,548/- (Rs. One crore thirty three lac forty eight thousand five hundred forty eight only).The placing of orders of Annual purchase of medicines based on L-1/Proprietory is approved.

3(xix) Annual purchase of cotton, bandages and other dressing material during the year 2001-2002 for all NDMC hospital / Institutions.

Resolved by the Council that administrative approval and expenditure sanction of Rs. 11,47,161.45 + taxes(Rs. Eleven lac forty seven thousand one hundred sixty one and paisa forty five only) is accorded for purchase of cotton,

8

bandages and other dressing material during the year 2001-2002 against administrative approval and expenditure sanction of Rs. 11,40,542.00 + taxes by Chairman dated 13.8.2001. Action taken for placing the supply order to the firm whose items have been selected by the approval-cum-purchase sub-committee, is approved.

3(xx) Purchase of high end Servers - Computer Hardware

Resolved by the Council that the proposal to place the order with M/s Albion Informatics Pvt. Ltd. For purchase of High end Compaq servers (ES-45-1 No. DS 20 E-1 No. External Storage Array (RA-8000) and back up devise (MSL-5026 SL)- one each and clustering solution) at a negotiated cost of Rs.75,18,675/- (Rs. Seventy five lakhs eighteen thousand six hundred seventy five only) inclusive of all taxes.

3(xxi) Grant of Electricity allowance to all employees of NDMC in lieu of concessional electricity tariff.

Postponed for re-examination.

3(xxii) Write off of Council loss amounting to Rs. 9060/-.

Resolved by the Council that loss of Rs.9060/- on account of lost mobile phone is written off. It was further decided that in future, the officers concerned will be personally responsible for the safe custody of mobile phones.

3(xxiii) Amalgamation / Merger of the post of Supdt. (T) with the post of Junior Engineer (Electric).

Resolved by the Council that the proposal regarding merger of the existing cadre strength of Supdt.(T) i.e. 49 in the scale of Rs.6000-10800 to the post of JE(E) in the scale of Rs.5500-9875 is approved. It is further resolved that the existing incumbents against the post of Supdt.(T) shall be allowed to retain their existing pay scales as personal to them till they vacate the post.

3(xxiv) Contract/Schemes involving an expenditure of Rs. 1.00 Lac but not exceeding Rs. 10.00 Lacs.

Information noted.

3(xxv) Action Taken Report on Information noted.

9

the status of ongoing schemes/works approved by the Council.

3(xxvi) Action Taken Report on the Resolutions / decision taken.

Information noted.

3(xxvii) Revision of charges of Shivaji Stadium.

Resolved by the Council that the charges of Shivaji Stadium be revised, as proposed with effect from 24.10.2001. It was also decided that only condition No. 11 be amended as proposed.It was also accepted that the word ‘clause’ in the second line of p. 207 of the agenda be substituted by the word ‘condition’ being a typographical error. It was also decided that it should be ensured that nobody is allowed to use the office space permanently.

3(xxviii) Establishing 33 KV Indoor S/S at the place of old 33 KV Substation, Connaught Place and Augmentation of its transformer capacity.

Resolved by the Council that administrative approval and expenditure sanction is accorded to the estimate amounting to Rs.495.13 lacs (Gross) and Rs. 494.29 lacs (Net) chargeable to head of A/Cs E.4.1 and E-3 as explained in the preamble.

3(xxix) Duty on transfer of property and method of assessment thereto – Amendment in section-93 of NDMC Act, 1994.

Resolved by the Council that the Ministry of Home Affairs may be requested for amendment in section-93 of the NDMC Act, 1994 as proposed in the Preamble.

3(xxx) A Policy regarding conversion of TMR workers as on 31.12.98 into RMR on the basis of data collected from the various Deptts.

Chairman will discuss with the Vice-Chairperson and Members of the Council and decide.

3(xxxi) NAMING OF ROAD in Sarojini Nagar or any other suitable road in honour of the Khazak poet and philosopher ‘Abai’.

Resolved by the Council that one of the un-named cross roads in Chankya Puri be named as ‘Abai’ Marg in honour of the Khazak poet and philosopher. It was further decided that C.E.(C-II) may identify the Cross Road and furnish a sketch map of the proposed road so that the Ministry of External Affairs is informed accordingly.

3(xxxii) Action Taken Report Considered.

10

against M/s Bharat hotels Ltd. (Inter-continental) & CJ International Hotels Ltd. (Le-meridian) as resolved in the Council Meeting against item no. 3(xxiii) dt. 29.05.98.

Noted for information.

SECRETARY CHAIRMAN

11

ITEM NO. 2

REPLY TO ADMITTED QUESTIONS UNDER SECTION 28 OF THE NDMC ACT, 1994.

COUNCIL’S DECISION

Sh. M.P. Chawla who had submitted two questions desired that the questions be taken up in the next Council Meeting.

ITEM NO. 3

PROPOSALS FOR CONSIDERATION BY THE COUNCIL.

Contd……

12

ITEM NO. 3 (i)

INSTALLATION OF MUSICAL DANCING FOUNTAIN IN THE PARK ADJACENT TO BANGLA SAHIB GURDWARA.

During a meeting in the chamber of Chairman, NDMC attended by Smt.

Rita Kumar, O.S.D. to Chief Minister, Delhi and other senior officers on

28.11.2001, it was decided to give a face lift to the park adjacent to Bangla Sahib

Gurdwara, visited by a large section of people, by providing a musical dancing

fountain which can also respond to the live devotional music. In order to finalise

the proposal, a meeting has again held in the chamber of Chairman on 03.12.2001

attended by F.A., CE(E), CE©II, C.A. and Director (Hort.) when it was felt that

musical fountain and high mast light be commissioned before Baisakhi i.e. 13 th of

April, 2002.

Accordingly, an estimate amounting to Rs.38.27 lacs has been framed

inclusive of civil cost after having budgetary offer from the agency, who had

installed a similar musical fountain on behalf of Amritsar Municipal Corporn.

Proposed fountain shall be rectangular one with hybrid design having auto-

sensing for live devotional music as well as water formations for pre-programmed

recorded music. Besides having the musical fountain in the center, two static

fountains on each sides will also be provided, which will operate even when

musical fountain is not running.

The expenditure will be chargeable to the Head D-4-4-10 having a

provision of Rs.50.00 lacs during 2001-2002. Finance has already concurred in the

estimate vide their Diary No.D-260/FA, dtd. 01.02.2002 with certain observations,

which are replied as under:-

1. Adequate funds are available under the Head D-4-4-10.

2. The park belongs to NDMC and same is also being maintained by the

NDMC.

3. CE(Civil) will be informed about the civil work after the sanction of

estimate.

13

4. Certified that installation of musical dancing fountain does not

tentamount to promote or favour any religious sect, as the same is being

installed in the NDMC Park.

With the approval of Chairman dated 11.02.2002, further action for inviting

tenders has been initiated.

Remarks of Chief Engineer (E) :

The case is laid before the Council for according administrative approval

and expenditure sanction to the estimate amounting to Rs.38,27,000/- (Rupees

Thirty eight lacs and twenty seven thousand only) for ` Installation of musical

dancing fountain in the park adjacent to Bangla Sahib Gurdwara`.

COUNCIL’S DECISION

Deferred.

14

ITEM NO. 3 (ii)

MEDICAL BENEFITS FOR RETIRED EMPLOYEES OF NDMC.

The Council, vide Resolution No. 3(ix) dated 26.9.97 approved the above scheme. In this scheme, only retired employees and his/her spouse is entitled for these facilities and the family pensioners are also covered. THE scheme is optional and the retired employee for joining the scheme is required to pay one time lump sum contribution, equivalent to the last pay drawn.

The retired employees joining the scheme are entitled to draw medical facilities from NDMC institutions at part with those applicable to serving employees. The employees residing outside NDMC limits or falling ill outside NDMC area are governed by the provisions of CS (Medical Attendance) Rules.

The retiring employees have to submit their option for joining or not joining the scheme, while submitting the papers for settlement of provident funds etc. The employees who had already retired at the commencement of the scheme or in case of unfortunate death of a retired employee, the family pensioner could opt for the scheme within six months. Secretary and the Chairman are empowered to permit any ex-employee for joining the scheme in relaxation of the eligibility period.

Some of the retired employees are requesting now for joining the scheme, informing that they were not aware of the scheme approved by the Council. It appears that wide publicity of the scheme was not made and all the retired employees could not opt for the scheme. The retired employees who are not covered under the said scheme and are not availing OPD facility from NDMC Hospitals/Dispensaries are getting Rs. 100/- p.m. for OPD treatment on the pattern of the Govt. of India.

The Chairman has seen the case.

The case is laid before the Council for approving wide publicity of the Scheme for the benefit of the retired employees and give them option for becoming the Member of the scheme on the terms and conditions already decided.

COUNCIL’S DECISION

Resolved by the Council that wide publicity of Medical Scheme for retired employees be given so that they may give option for becoming members of the scheme.

15

ITEM NO. 3 (iii)

CONSTITUTION OF COMMITTEE FOR FIXING THE TARIFF FOR SUPPLY OF ELECTRICITY AND FILTERED WATER IN NDMC AREA UNDER SECTION 9 OF NDMC ACT 1994.

1. NDMC had been adopting the tariff schedule of Delhi Vidyut Board and

Delhi Jal Board from time to time in compliance of instructions given by the

ministry of Home Affairs vide minutes of the meeting held in the room of Home

Secretary on 26.3.76 to maintain parity of tariff for consumers in MCD and

NDMC area.

2. The Delhi Electricity Regulatory Commission passed orders on petition

No.1/2001 in the matter of annual revenue requirement for the financial year 2001-

02 for Delhi Vidyut Board on 23.5.2001 thereby fixing the tariff chargeable from

various categories of consumers by DVB. A proposal to adopt tariff schedule of

DVB mutatis-mutandis was laid before the Council vide Item No.3 (i) dated

16.6.2001 but the item could not be taken up. The Council vide Reso.No.3 (i)

dated 17.7.2001 considered the proposals and fixed the revised electricity tariff for

consumers in NDMC area as contained in Annexure ‘B’ to the Agendum which is

equivalent to the tariff prevailing in MCD area with the stipulation that in case of

any adjustment later on in the notified tariff by DERC/DVB, the tariff applicable to

consumers in NDMC area will also be amended accordingly. As per procedure in

vogue a public notice was given in the newspapers notifying the revised tariff and

as such the revised tariff in NDMC area has become effective from 22.8.2001 only

whereas the corresponding increase in tariff in DVB area was given effect from

1.6.2001, i.e., 7 days after the publication of orders of DERC.

3. Since the procedure for implementation of revised tariff in NDMC area

took more than 2 months thereby resulting in financial loss to NDMC legal opinion

was sought on the issue whether revision of rate could be made effective from a

retrospective date by giving a public notice to this effect. Legal Adviser has

opined that the Council may constitute a Committee under Section 9 of the NDMC

Act, which may be authorized to take immediate decision whenever a revision is

16

required in electricity tariff to avoid any further delay, as the decision of such

committee will be deemed to be a decision of the Council. He has also opined that

one month’s notice for implementing the revised tariff was not a statutory

requirement under the Indian Electricity Act 1910 and such a notice is required

only when method of charging is to be changed. Further Section 200 of the

NDMC Act 1994 empowers NDMC to determine/levy charges for the supply of

energy in NDMC area. Similar provision for fixing tariff for filtered water supply

exists under Section 64 of the NDMC Act.

4. Section 9 of the NDMC Act is reproduced as under: -

9(1) The Council may constitute as many committees as it thinks fit for the

exercise of any power or discharge of any function which the Council may by

resolution delegate to them or for inquiring into, reporting or advising upon any

matter which the Council may refer to them.

(2) Any such committee shall consist of members of the Council only: Provided

that a committee may, with the sanction of the Council, co-opt not more than two

persons who are not members of the Council, but who in the opinion of the

Council possesses special qualifications for serving on such committee.

(3) Each committee constituted under this section shall be presided by the

Chairperson of the Council.

(4) Any matter relating to committee constituted under this section, not expressly

provided in this Act may be provided by regulations made in this behalf.

5. It is, therefore, proposed that a Committee consisting of at least two

members of the Council and two senior officers of the Council to be nominated by

the Chairman may be constituted under the chairmanship of Chairperson NDMC

under Section 9 of the NDMC Act., and authorised to fix the tariff chargeable for

filtered water supply and electricity in NDMC area in terms of provisions of

Section 64 and Section 200 of NDMC Act as and when tariff prevailing in MCD

area is revised by DJB and DVB respectively. Such revised tariff can be

implemented immediately to avoid loss of revenue to the Council and the

17

procedure of giving one month’s notice to the consumers in NDMC area may also

be dispensed with.

6. Finance has seen the case and concurred in the proposal vide their Diary

No. 147 dated 30.1.2002.

7. Chairman has seen the case and has nominated Sh. B.M. Sukhija, C.E. (E-

II) and Sh. S.C. Basuroy, C. E. ( C ) to be the members of the Committee

for fixing the tariff..

8. The case is laid before the Council for approval of the proposal contained

in para 5 above.

COUNCIL’S DECISION

Resolved by the Council that the proposal contained in para 5 is approved. Further resolved that the Chairman, NDMC will preside over the Committee, and the Committee shall have the following members :-

1. Smt. Tajdar Babar, Member, NDMC.2. Sh. Mahendra Chawla, Member, NDMC.3. Sh. B.M. Sukhija, Chief Engineer (E-II).4. Sh. S.C. Basuroy, Chief Engineer (Civil).

18

ITEM NO. 3 (iv)

CHANAKYA CINEMA COMPLEX.

Matter regarding the Estate Policy / Guidelines for dealing with Estate

Matters was brought before the Council in its meeting held on 30th August 2000 as

an item no. 3 (xxi) wherein, the Council resolved inter-alia that on expiry of

present term of licenses of Hotels/Cinemas and other similar complexes, the

licenses shall not be renewed. The fresh licence shall be as per the provisions of

section 141 of NDMC Act, 1994. Copy of the Resolutions is enclosed at Annexure

(See pages 22 – 24).

2. Chanakya Cinema Complex is located in Chanakya Puri area and is a part

of land parcel where other prestigious building such as Akbar Bhawan etc. are

located. Licence was given for running a cinema to M/s Aggarwal and Modi

Enterprises (Cinema Project) Pvt. Ltd. on tender basis being highest bidder and the

licence deed was executed on 16.9.70 which was renewed time to time and finally

expired on 30.9.2000 with flux of time. The licence fee last paid was Rs. 15.15 lacs

per annum, NDMC could not take action immediately as stay was operating

against NDMC as passed by High Court of Delhi in Writ Petition No.3244/92

which was vacated by the Hon’ble Court on 24.5.2001 only in CM No.1044/2001

in CW 3244/92. While vacating the stay, the Hon’ble Court passed the following

orders:-

The Petitioner in the writ petition seeks renewal of the lease for the period

1st Oct. 1990 to 30th Sept. 2000 in respect of Chanakya Cinema. This period has

come to an end. The interim order dated 21st Sept. 1992 cannot ensure beyond 30th

Sept. 2000. Therefore the interim order dated 21st September 1992 is hereby

vacated.

This order will not prevent the NDMC from considering the proposals of

the Petitioner dated 5th April 2000 and 15th March 2001. The application is

accordingly disposed off.

3. The Chairman, NDMC , considered the representation as per the above

observation of the Court. Since the stay was vacated only in May 2001, and the

contents of the representation were examined by the Chief Architect, it was almost

19

nearer to one year when the complex remained without any valid licensee. The

matter was placed before the Council in its meeting held on 28 th August 2001 for

guidance in the matter in interest of revenue as it was in variation of resolution

passed by the Council on 30th August 2000. Preamble of the proposal is attached at

Annexure (See pages 25 – 28) .

4. A draft minutes of the Resolution was put up before the Council in its

meeting held on 25th September 2001 when the Council did not confirm the

minutes and decided to defer it and case to be reviewed by the Council again.

Thus, the position remained as it was, as resolution did not sail. Chairman

considered the representations of Chanakya Cinema afresh in view of the

observations of Hon’ble High Court of Delhi and gave personal hearing to the

representatives of M/sAggarwal and Modi Enterprises (Cinema Project) Pvt. Ltd.

After hearing them, Chairman passed the orders on 13.11.2001 in view of the

guidelines/policy/ resolution dated 30.8.2000 and concluded that there is no merit

in the representation submitted by the Company. The status of the company since

1.10.2000 is that of unauthorized occupant. He also ordered that they would hand

over the vacant possession by 28th February 2002 after removing all the belongings

etc as per terms of the licence, subject to further conditions that for the intervening

period, they will pay damages Rs. 15.15 lacs per annum and further they will

submit an undertaking to the above effect within 15 days that they would vacate by

the above said date. On the event of failure to vacate and give the undertaking, M/s

Aggarwal and Modi Enterprises (Cinema Project) Pvt. Ltd. and other sub-licensees

shall become liable to vacate the cinema complex forthwith and in that case

NDMC will take such other action as may be permissible to them in accordance

with the Law besides claiming the damages from 1.10.2000 till such time it is

vacated as per market rate by approaching to the appropriate authority. Copy of the

order enclosed at Annexure (See pages 29 – 32).

5. However, the occupant company though responded to the order of the

Chairman but did not agree to the above orders. Thereafter, a notice was issued by

the Estate Department on 22.1.2002 giving 10 days time to give vacant possession

to all concerned, including the sub-licensee. Sub-licensee though responded but the

unauthorized occupant M/s Aggarwal and Modi Enterprises (Cinema Project) Pvt.

20

Ltd., however, filed the writ petition in High Court of Delhi against the orders of

Chairman dated 13.11.2001. The case came-up for hearing on 12 February 2002,

which was adjourned, to 18th February 2002 for filing the affidavit on behalf of

NDMC. Now, it is listed on 27th February 2002.

The Chairman has seen the case.

In view of decision taken by the Council in its meeting held on 25 th

September 2001, the action was taken by the Chairman as stated in para 4 above

which is in conformity with the guidelines issued by Council vide its Resolution

dated 30th August 2000 and it is for information and approval of the Council.

COUNCIL’S DECISION

Resolved by the Council that information as given in para – 4 is approved.

21

ANNEXURE

22

ANNEXURTE

23

ANNEUXRE

24

ANNEXURE

25

ANNEXURE

26

ANNEXURE

27

ANNEUXRE

28

ANNEUXRE

29

ANNEUXRE

30

ANNEXURE

31

ANNEUXRUER

32

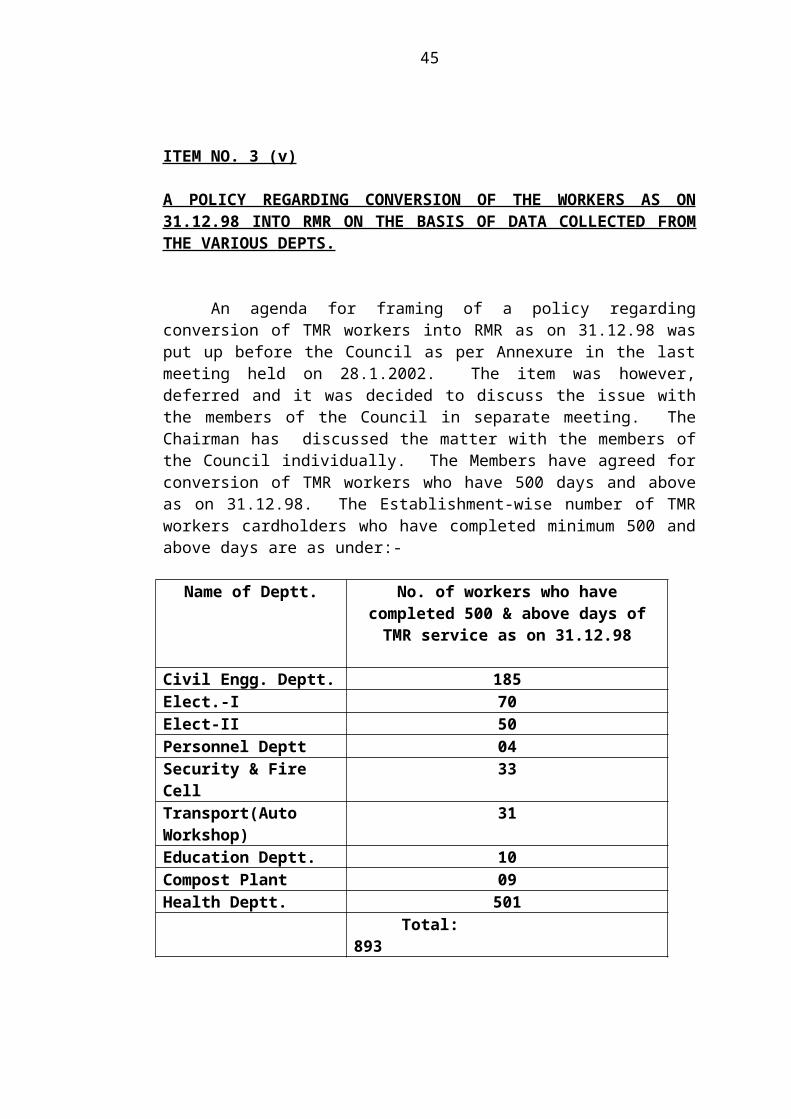

ITEM NO. 3 (v)

A POLICY REGARDING CONVERSION OF THE WORKERS AS ON 31.12.98 INTO RMR ON THE BASIS OF DATA COLLECTED FROM THE VARIOUS DEPTS.

An agenda for framing of a policy regarding conversion of TMR workers into RMR as on 31.12.98 was put up before the Council as per Annexure in the last meeting held on 28.1.2002. The item was however, deferred and it was decided to discuss the issue with the members of the Council in separate meeting. The Chairman has discussed the matter with the members of the Council individually. The Members have agreed for conversion of TMR workers who have 500 days and above as on 31.12.98. The Establishment-wise number of TMR workers cardholders who have completed minimum 500 and above days are as under:-

Name of Deptt. No. of workers who have completed 500 & above days of TMR service as on 31.12.98

Civil Engg. Deptt. 185Elect.-I 70Elect-II 50Personnel Deptt 04Security & Fire Cell 33Transport(Auto Workshop)

31

Education Deptt. 10Compost Plant 09Health Deptt. 501

Total: 893

The number of eligible TMR worker is, however, tentative and may increase on account of receipt of objections later and their verification regarding number of days actually served in the concerned Departments.

The Chairman has seen the case.

The matter is accordingly placed before the Council for formal approval of the proposal regarding 500 & above days as the criteria for conversion of TMR into RMR as on 31.12.98.

COUNCIL’S DECISION

Resolved by the Council that the proposal regarding 500 & above days as the criteria for conversion of TMR into RMR as on 31.12.98 is approved.

33

ITEM NO. 3 (vi)

NAMING OF ROAD AFTER THE NAME OF “RAJMATA SCINDIA ROAD”.

Sh. Ram Bhaj, Vice-Chairman, N.D.M.C has proposed to rename the “I”

Avenue Road, Sarojini Nagar, New Delhi after the name of “RAJMATA

SCINDIA” Road.

Rajmata Scindia was a prominent leader, renowned social worker who

devoted her whole life for the betterment of the poor people.

Chairman, NDMC has seen and approved the proposal to be placed before

the Council.

The proposal is accordingly placed before the Council for its

consideration/approval.

COUNCIL’S DECISION

Resolved by the Council that the proposal regarding re-naming of I-Avenue Road in Sarojini Nagar as Rajmata Vijayraje Scindia Marg is approved.

34

ITEM NO. 3 (vii)

NAMING OF ROAD AFTER THE NAME OF LATE SHRI MADHAV RAO SCINDIA.

Sh. Ramakant Goswami, Parliamentary Secretary to Chief Minister, Delhi

has proposed / requested that a road amongst the following roads be named after

the name of “MADHAV RAO SCINDIA”.

1. Willington Crescent.

2. Vinay Marg.

3. Dalhousie Road.

C.E. (C-II) has proposed that Canning Road may be renamed as Madhav

Rao Scindia Road. The Canning Road starts from Ferozshah Road and after

crossing K.G. Marg joins Copernicus Marg.

Chairman, NDMC has seen the case and approved the proposal to be placed

before the Council.

The proposal is accordingly placed before the Council for its

consideration/approval.

COUNCIL’S DECISION

Resolved by the Council that the proposal regarding re-naming of Canning Road as Madhavrao Scindia Marg is approved.

35

ITEM NO. 3 (viii)

NAMING OF SERVICE LANE FROM BARAT GHAR, PESHWA ROAD ENDING AT MANDIR MARG AFTER THE NAME OF SHAHEED MATBAR SINGH NEGI MARG.

The Chairman, Rajya Sabha has recommended that the Service lane from

barat Ghar, Peshwa Road ending at Mandir Marg be named after the name of

Shaheed Matbar Singh Negi Marg.

Sh. Negi was Security Assistant in Rajya Sabha who sacrificed his life

combating terrorists during terrorist attack on Parliament on 13th December, 2001.

CE(C-II) has informed that the Service lane from Barat Ghar, Peshwa Road

ending at Mandir Marg is un-named. NDMC can name the un-named roads in its

jurisdiction.

Chairman, NDMC has seen the case and approved the proposal to be placed

before the Council.

The proposal is accordingly placed before the Council for its

consideration/approval.

COUNCIL’S DECISION

Resolved by the Council that the proposal regarding naming of the Service Lane from Barat Ghar Peshwa Road ending at Mandir Marg as Shaheed Matwar Singh Negi Marg is approved.

36

ITEM NO. 3 (ix)

AUGMENTATION OF SEWERAGE IN VARIOUS NDMC AREA. SH : LAYING OF DIVERSION LINE OF 250-300-400-450 MM DIA FOR AUGMENTING THE SEWERAGE SYSTEM OF A PART OF LAXMI BAI NAGAR – LAYING OF BRANCH SEWER LINE.-TENDER THEREOF-

Administrative approval and expenditure sanction for the above cited work

was accorded by the Council vide Reso. No. 3 (VII) dated 25.9.1998 for Rs.

30,44,200/-. The technical sanction and NIT for the above noted sub-head of the

work were approved by CE(C-I) for Rs. 15, 48,900/- and Rs. 15,03,735/-

respectively. Accordingly percentage rate sealed tenders were invited by fixing

dates of sale and receipt of tenders 14.8.2001 and 16.8.2001 respectively giving

wide publicity in the leading newspapers. M/s Duaba Construction Co. emerged

out as the lowest tenderer @ 27.27 % above the estimated cost of Rs. 15,03,735/-.

The tendered amount worked out to Rs. 19,13,804/-. The lowest tender was

rejected on the ground that all the four tenderers had polled themselves in favour of

M/s Duaba Construction Co. and quoted higher rates with respect to the trend of

similar works having been awarded below the estimated cost. The rejection of

tender was concurred in by the Finance and approved by the Chairman, NDMC.

Accordingly with the approval of Chairman, the tenders were recalled fixing dates

of sale and opening/receipt of tenders as 7.11.2001 and 9.11.2001 respectively by

giving wide publicity in the leading newspapers. In response to this second call of

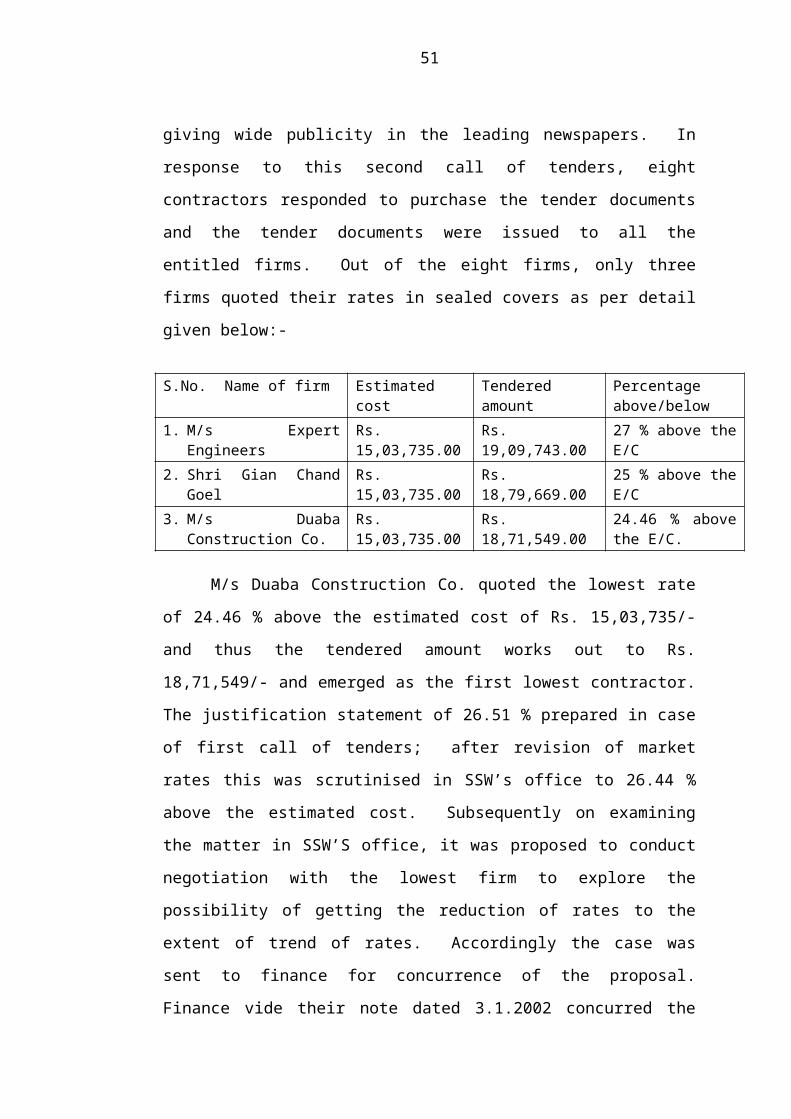

tenders, eight contractors responded to purchase the tender documents and the

tender documents were issued to all the entitled firms. Out of the eight firms, only

three firms quoted their rates in sealed covers as per detail given below:-

S.No. Name of firm Estimated cost Tendered amount Percentage above/below

1. M/s Expert Engineers Rs. 15,03,735.00 Rs. 19,09,743.00 27 % above the E/C2. Shri Gian Chand Goel Rs. 15,03,735.00 Rs. 18,79,669.00 25 % above the E/C3. M/s Duaba Construction

Co.Rs. 15,03,735.00 Rs. 18,71,549.00 24.46 % above the

E/C.

M/s Duaba Construction Co. quoted the lowest rate of 24.46 % above the

estimated cost of Rs. 15,03,735/- and thus the tendered amount works out to Rs.

18,71,549/- and emerged as the first lowest contractor. The justification statement

37

of 26.51 % prepared in case of first call of tenders; after revision of market rates

this was scrutinised in SSW’s office to 26.44 % above the estimated cost.

Subsequently on examining the matter in SSW’S office, it was proposed to

conduct negotiation with the lowest firm to explore the possibility of getting the

reduction of rates to the extent of trend of rates. Accordingly the case was sent to

finance for concurrence of the proposal. Finance vide their note dated 3.1.2002

concurred the proposal for conducting negotiation with the lowest tenderer:-

“Though the lowest quoted rates are still on very much higher side than the trend of rates but considering that this is the second call of tenders, we concur in the proposal of the department to conduct negotiation with the lowest contractor, M/s Duaba Construction Co. for getting reduction in their rates to the extent of the trend of rates.”

Consequent upon the concurrence of the Finance, the case was put up to

Chairman, for approval to conduct negotiation with the contractor. With the prior

approval of Chairman dated 9.1.2002, the negotiation was conducted with the

lowest contractor, M/s Duaba Construction Co. by the Negotiation Sub-Committee

under the Chairmanship of EE(C-I). After detailed discussion, the firm, as a

gesture of goodwill offered to reduce their rates from 24.46 % above to 18 %

above the E.C. which is 8.44 % below the justified rates. Negotiation Sub-

Committee have recommended negotiated offer of lowest tenderer M/s Duaba

Construction Co. at 18 % above the estimated cost with a tendered amount of Rs.

17,74,407 be accepted. The firm has confirmed their negotiated offer vide their

letter dated 21.1.2002.

The Chairman has seen the case.

CE(C-I)’s remarks :-

The case is placed before the Council for consideration and approval of negotiated offer of M/s Duaba Construction Co. at 18% above the estimated cost of Rs. 15,03,735/- with the tendered amount of Rs.17,74,407/-. The negotiated offer letter shall form part of the agreement.

COUNCIL’S DECISION

Resolved by the Council that the negotiated offer of the lowest tenderer M/s Duaba Construction Co. at 18% above the estimated cost of Rs.15,03,735/- with the tendered amount of Rs.17,74,407/- is accepted.

38

ITEM NO. 3 (x)

STRENGTHENING OF EXISTING MECHANICAL COMPOST PLANT AT OKHLA. SH : FABRICATION OF A WATER TENDER WITH FACILITY FOR FIRE EXTINGUISHER ALONGWITH ALLIED ARRANGEMENTS.

There has been number of fire incidents at the Compost Plant specially

during summer seasons due to dry horticulture waste, for which the Department

has also to take stringent measures to segregate the waste from the fire place with

the help of loaders & machinery available at the compost plant. The requisition of

fire tenders are also invariably sought & immediate action for extinguishing the

fire & later on being the fire in the waste, every possibility of spreading the fire

still exists. During one of the incidents of fire, Secretary, CE(E), CE(C )-II , Fire

Officer & other Senior Officers, the matter was discussed by the Officers of the

DFS at the site & desired that NDMC should have there own water tenders with

the facility for fire extinguishers so that immediate steps are taken to control the

fire so as to avoid any loss of life & properties at the Compost Plant. Accordingly,

Chairman vide his order dated 16.2.1996 approved the proposal for one water

tanker after having concurred in the proposal by FA vide Dy. No.D-534/FA dated

15.2.96.

Later on, in a meeting held in the Chamber of Secretary, NDMC on 6.7.99,

it was interalia decided that one Ashok Leyland Comet Chassis purchased in the

year 1994 and lying at Okhla Workshop be utilised for fabrication of the said fire

tender. Since the chassis is not meeting the latest norms of the STA as per the

judgement of the Supreme Court, accordingly, a detailed note dated 22.8.2001 was

sent by TC/CSO clarifying all the position & the requirement of the said fire tender

as well as the present status of the case which was approved by the Chairman vide

his order dated 25.8.2001 as under:-

1. To purchase a new chassis from Ashok Leyland on DGS&D rate contract

for fabrication of Fire tender.

39

2. The existing chassis lying at Okhla Workshop, may be converted into a

Tractor Trolley for the use of Transportation of material within the

Compost Plant.

In view of the above, an estimate amounting to Rs.13,71,627/- has been

prepared for the purchase and fabrication of water tender for the Compost Plant

with the facility for fire extinguisher alongwith allied arrangements and sent to

finance for its concurrence. Finance vide their Dy.No.D-121/FA dated 5.2.2002

concurred in the proposal subject to certain observations which are clarified as

under:-

1. Sufficient funds are available under the Head D.4.4.13 wherein a budget

provision of Rs.100.00 lacs exists during 2001-2002.

2. It is certified that the information submitted is correct.

3. CE(E) has signed.

4. The chassis will be purchased on the DGS&D rate contract meeting the

EURO-II/latest norms on the rates applicable at the time of placing the

order meeting with our delivery schedule.

Chairman has seen.

CE(E)’s remarks

The case is laid before the Council as per the following:-

a) To accord administrative approval & expenditure sanction for

Rs.13,71,627/-(Rs. Thirteen lacs seventy one thousand six hundred &

twenty seven only) for the purchase & fabrication of water tender for the

Compost plant with the facility for fire extinguishers alongwith allied

arrangements.

b) To purchase one chassis borne on DGS&D rate contract meeting EURO-

II/latest norms & delivery period on the rates applicable at the time of

delivery by making advance payment as per their conditions.

COUNCIL’S DECISION

Resolved by the Council that administrative approval & expenditure sanction is accorded to (a) & (b) above.

40

ITEM NO. 3 (xi)

PURCHASE OF 11KV HT XLPE CABLE OF SIZE 3X150 SQ.MM & 3X300 SQ.MM DULY ISI MARKED.

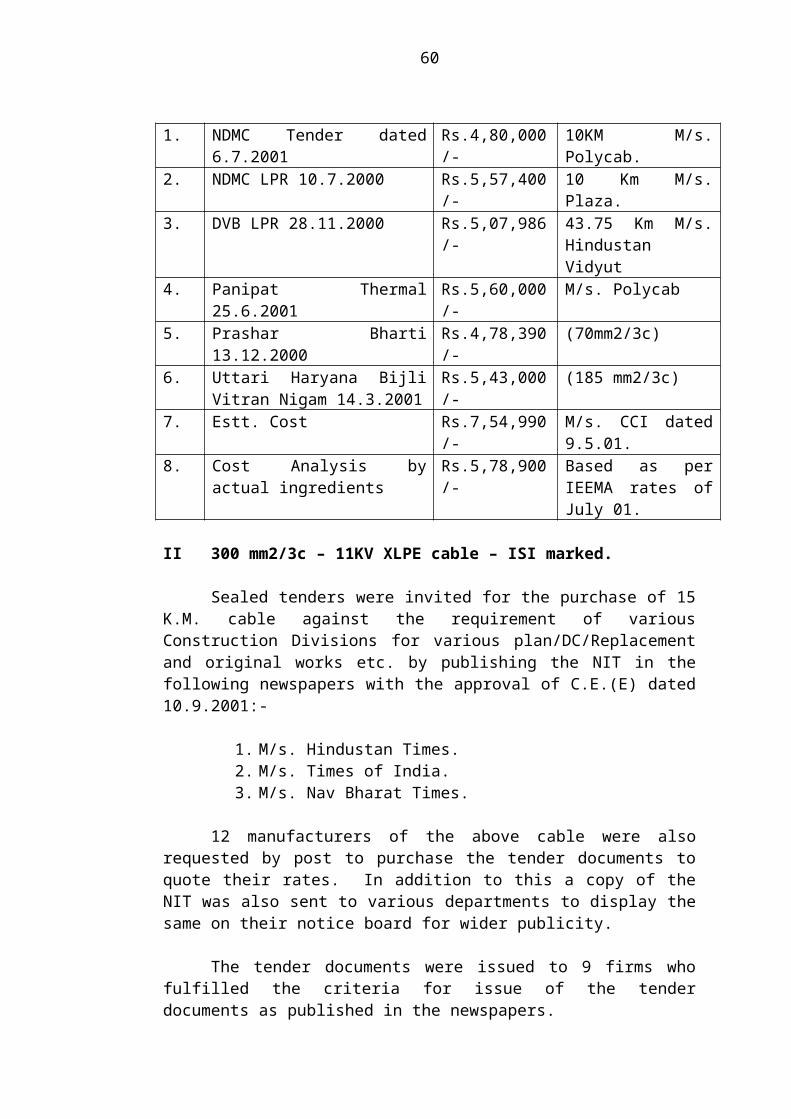

1. 150 mm2/3c – 11kv – XLPE cable – ISI marked.

Sealed tenders were invited for the purchase of the 10 K.M. cable against the requirement of various Construction Divisions for various plan/DC/Replacement and original works etc. by publishing the NIT in the following newspapers with the approval of C.E.(E) dated 11.5.2001:-

1. M/s. Hindustan Times.2. M/s. Times of India.3. M/s. Nav Bharat Times.

13 manufacturers of the above cable were also requested by post to purchase the tender documents to quote their rates. In addition to this a copy of the NIT was also sent to various departments to display the same on their notice board for wider publicity.

The tender documents were issued to 11 firms who fulfilled the criteria for issue of the tender documents as published in the newspapers.

The tender box was opened on the due date i.e. on 6.7.2001 and in all 8 firms responded to our tender enquiry. All the firms except M/s. Fort Gloster, M/s Nicco Corporation Ltd & M/s. RPG Cables Ltd. had mentioned about the deposit of earnest money on their envelop. As such the Ist cover only of 5 eligible tenders were opened in presence of the representatives of various firms who choose to be present. The IInd cover was opened subsequently on 13.09.2001 with the approval of C.E.(E).

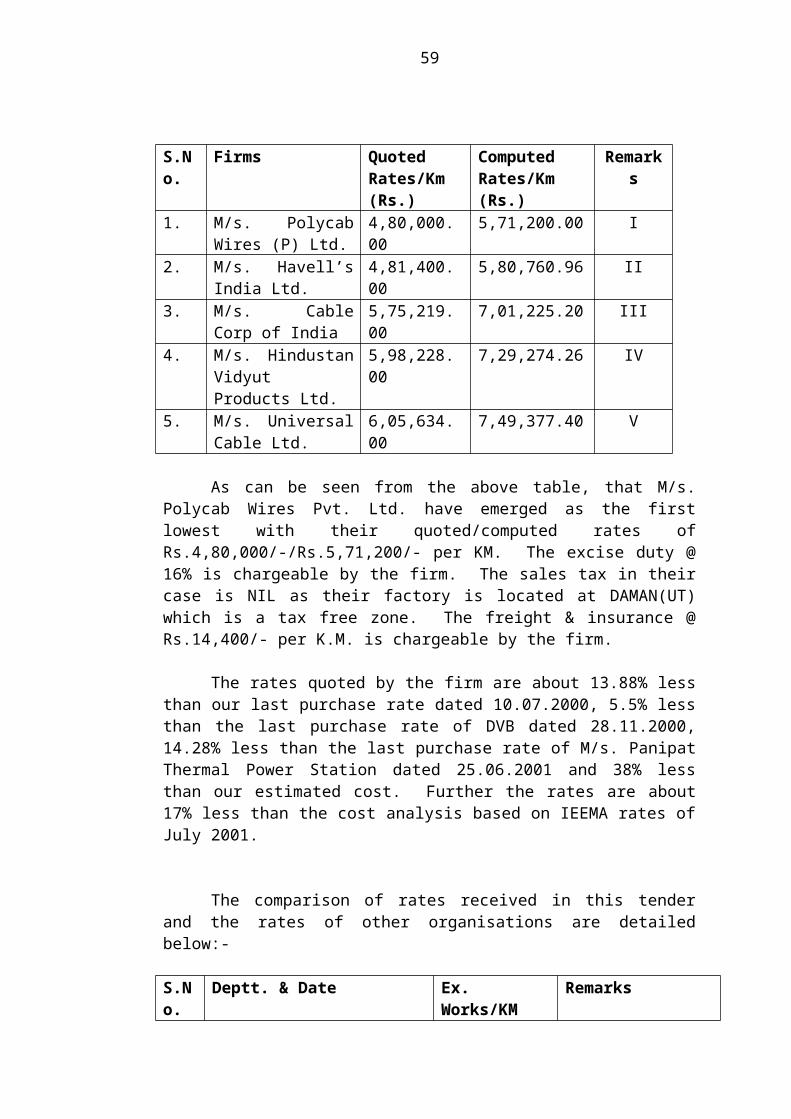

The quoted/computed rates of various firms are as under:-

S.No. Firms Quoted Rates/Km (Rs.)

Computed Rates/Km (Rs.)

Remarks

1. M/s. Polycab Wires (P) Ltd.

4,80,000.00 5,71,200.00 I

2. M/s. Havell’s India Ltd.

4,81,400.00 5,80,760.96 II

3. M/s. Cable Corp of India

5,75,219.00 7,01,225.20 III

4. M/s. Hindustan Vidyut Products Ltd.

5,98,228.00 7,29,274.26 IV

5. M/s. Universal Cable Ltd.

6,05,634.00 7,49,377.40 V

41

As can be seen from the above table, that M/s. Polycab Wires Pvt. Ltd. have emerged as the first lowest with their quoted/computed rates of Rs.4,80,000/-/Rs.5,71,200/- per KM. The excise duty @ 16% is chargeable by the firm. The sales tax in their case is NIL as their factory is located at DAMAN(UT) which is a tax free zone. The freight & insurance @ Rs.14,400/- per K.M. is chargeable by the firm.

The rates quoted by the firm are about 13.88% less than our last purchase rate dated 10.07.2000, 5.5% less than the last purchase rate of DVB dated 28.11.2000, 14.28% less than the last purchase rate of M/s. Panipat Thermal Power Station dated 25.06.2001 and 38% less than our estimated cost. Further the rates are about 17% less than the cost analysis based on IEEMA rates of July 2001.

The comparison of rates received in this tender and the rates of other organisations are detailed below:-

S.No.

Deptt. & Date Ex. Works/KM Remarks

1. NDMC Tender dated 6.7.2001 Rs.4,80,000/- 10KM M/s. Polycab.2. NDMC LPR 10.7.2000 Rs.5,57,400/- 10 Km M/s. Plaza.3. DVB LPR 28.11.2000 Rs.5,07,986/- 43.75 Km M/s.

Hindustan Vidyut 4. Panipat Thermal 25.6.2001 Rs.5,60,000/- M/s. Polycab5. Prashar Bharti 13.12.2000 Rs.4,78,390/- (70mm2/3c) 6. Uttari Haryana Bijli Vitran

Nigam 14.3.2001Rs.5,43,000/- (185 mm2/3c)

7. Estt. Cost Rs.7,54,990/- M/s. CCI dated 9.5.01.8. Cost Analysis by actual

ingredients Rs.5,78,900/- Based as per IEEMA

rates of July 01.

II 300 mm2/3c – 11KV XLPE cable – ISI marked.

Sealed tenders were invited for the purchase of 15 K.M. cable against the requirement of various Construction Divisions for various plan/DC/Replacement and original works etc. by publishing the NIT in the following newspapers with the approval of C.E.(E) dated 10.9.2001:-

1. M/s. Hindustan Times.2. M/s. Times of India.3. M/s. Nav Bharat Times.

12 manufacturers of the above cable were also requested by post to purchase the tender documents to quote their rates. In addition to this a copy of the NIT was also sent to various departments to display the same on their notice board for wider publicity.

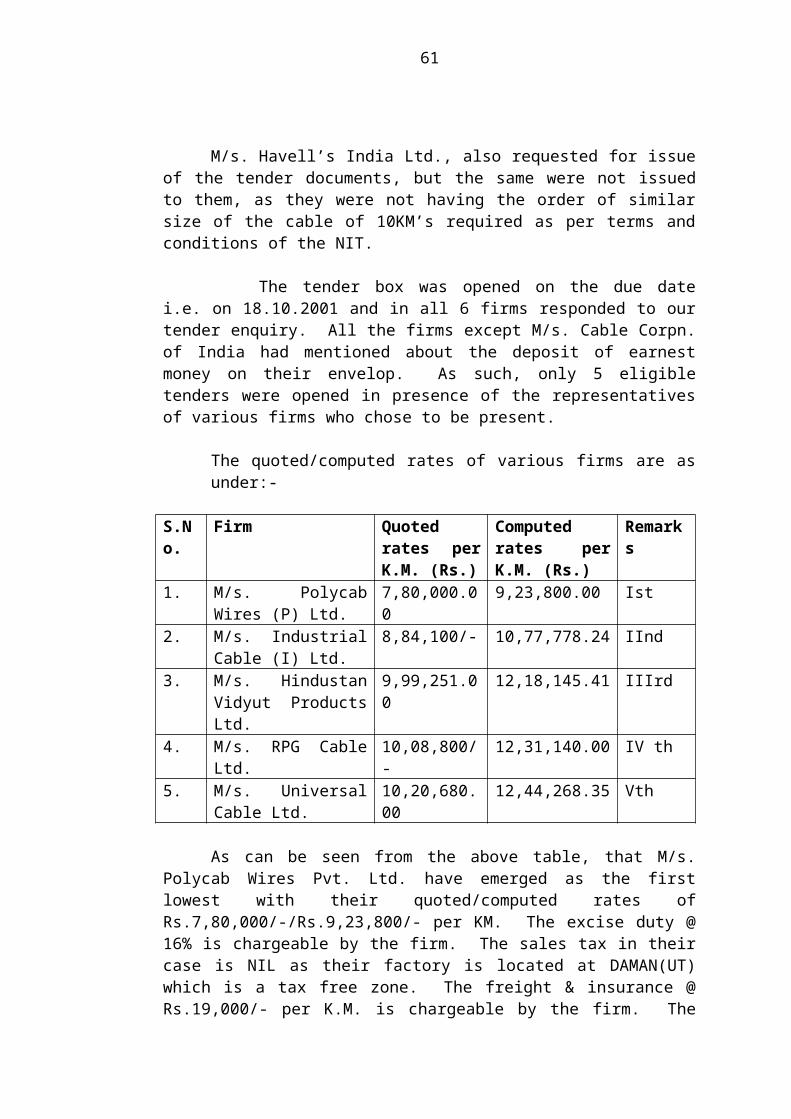

42

The tender documents were issued to 9 firms who fulfilled the criteria for issue of the tender documents as published in the newspapers.

M/s. Havell’s India Ltd., also requested for issue of the tender documents, but the same were not issued to them, as they were not having the order of similar size of the cable of 10KM’s required as per terms and conditions of the NIT.

The tender box was opened on the due date i.e. on 18.10.2001 and in all 6 firms responded to our tender enquiry. All the firms except M/s. Cable Corpn. of India had mentioned about the deposit of earnest money on their envelop. As such, only 5 eligible tenders were opened in presence of the representatives of various firms who chose to be present.

The quoted/computed rates of various firms are as under:-

S.No. Firm Quoted rates per K.M. (Rs.)

Computed rates per K.M. (Rs.)

Remarks

1. M/s. Polycab Wires (P) Ltd.

7,80,000.00 9,23,800.00 Ist

2. M/s. Industrial Cable (I) Ltd.

8,84,100/- 10,77,778.24 IInd

3. M/s. Hindustan Vidyut Products Ltd.

9,99,251.00 12,18,145.41 IIIrd

4. M/s. RPG Cable Ltd. 10,08,800/- 12,31,140.00 IV th5. M/s. Universal Cable

Ltd.10,20,680.00 12,44,268.35 Vth

As can be seen from the above table, that M/s. Polycab Wires Pvt. Ltd. have emerged as the first lowest with their quoted/computed rates of Rs.7,80,000/-/Rs.9,23,800/- per KM. The excise duty @ 16% is chargeable by the firm. The sales tax in their case is NIL as their factory is located at DAMAN(UT) which is a tax free zone. The freight & insurance @ Rs.19,000/- per K.M. is chargeable by the firm. The firm has agreed to all our terms and conditions as per NIT.

The rates quoted by the firm are about 12.8% less than our last purchase rates dated 31.08.2000, 9.3% less than the last purchase rate of DVB dated 22.1.2001, 21.73% less than the last purchase rate of M/s. TATA dated 31.01.2001 and 12.3% less than the last purchase rates of M/s. Panipat Thermal Power Station dated 25.6.2001. Their rates are 31.63% less than the estimated cost and 46% less than the price list of the firm. The justified rates have also been worked out by taking actual weight of the various ingredients and the rates of IEEMA circular of August 2001 and the rates received are 15.2% less than our justified rates. The comparison of rates received in this tender and the rates of other organisations are detailed below:-

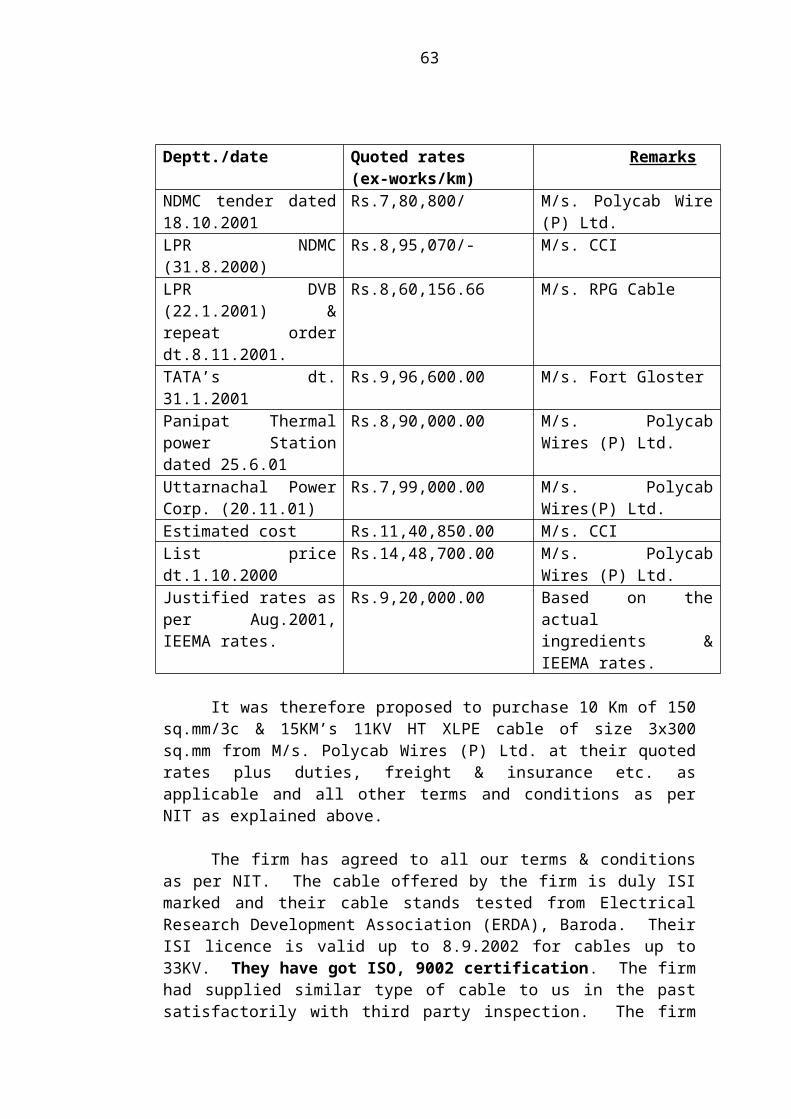

43

Deptt./date Quoted rates (ex-works/km)

Remarks

NDMC tender dated 18.10.2001

Rs.7,80,800/ M/s. Polycab Wire (P) Ltd.

LPR NDMC (31.8.2000) Rs.8,95,070/- M/s. CCILPR DVB (22.1.2001) & repeat order dt.8.11.2001.

Rs.8,60,156.66 M/s. RPG Cable

TATA’s dt. 31.1.2001 Rs.9,96,600.00 M/s. Fort GlosterPanipat Thermal power Station dated 25.6.01

Rs.8,90,000.00 M/s. Polycab Wires (P) Ltd.

Uttarnachal Power Corp. (20.11.01)

Rs.7,99,000.00 M/s. Polycab Wires(P) Ltd.

Estimated cost Rs.11,40,850.00 M/s. CCIList price dt.1.10.2000 Rs.14,48,700.00 M/s. Polycab Wires (P)

Ltd.Justified rates as per Aug.2001, IEEMA rates.

Rs.9,20,000.00 Based on the actual ingredients & IEEMA rates.

It was therefore proposed to purchase 10 Km of 150 sq.mm/3c & 15KM’s 11KV HT XLPE cable of size 3x300 sq.mm from M/s. Polycab Wires (P) Ltd. at their quoted rates plus duties, freight & insurance etc. as applicable and all other terms and conditions as per NIT as explained above.

The firm has agreed to all our terms & conditions as per NIT. The cable offered by the firm is duly ISI marked and their cable stands tested from Electrical Research Development Association (ERDA), Baroda. Their ISI licence is valid up to 8.9.2002 for cables up to 33KV. They have got ISO, 9002 certification. The firm had supplied similar type of cable to us in the past satisfactorily with third party inspection. The firm had also supplied the cables to various departments such as IOCL, HPCL, ACC, ABB, BHEL, Prashar Bharti, Crompton, L&T, Airport Authority, Railways, Panipat Thermal Power Station and Haryana State etc. The firm is considered technically and financially capable to execute the order.

The Finance vide their diary No.4029 dt. 7.1.2002 & No.1 dated 16.1.2002 concurred in the above two proposal of the department for the purchase of 300 sq.mm & 150 sq.mm from M/s. Polycab Wires (P) Ltd., the lowest firm.

Meanwhile an unsigned representation was given to Chairman by one of the unsuccessful tenderer wherein they advocated that the cable manufactured by them with nitrogen cure method is superior. They further requested that the process mentioned in the NITs of DVB should be followed. Chairman appointed a technical committee to go into the aspect and to make technical evaluation.

In this regard, it is to mention that we are procuring cable as per ISS 7098 (part-II) duly ISI marked. The ISS does not specify the method of manufacture of

44

cable. The international code IEC-502 also does not specify the method but insist that the cable manufactured should meet the various test requirements prescribed in these standards i.e. ISS 7098 (part-II). We have been rightly following the same in the past tenders and as well as in the instant tender & cables procured in the past have been working satisfactorily.

As per the reports available from Central Electricity Authority, Indian Institute Technology, Delhi, Central Power Research Institute, Banglore, both the processes i.e. “ SIOPLAS” & Nitrogen cure are equivalent technically. M/s. Associated Electrical Industries Ltd., U.K. has also stated the same.

Of late DVB had mentioned dry cure process in their specification and some of the firms have gone to the Court & final decision of the Court is to come on 22.03.2002. The above aspect of comparison of both the methods has been dealt with on the file at length.

Since it was neither feasible nor advisable to change the specifications of present tenders under finalisation, it was decided with approval of Chairman that present tender be finalised but for the tenders to be floated in future, the Technical Committee shall take a view & shall submit the report after the decision of the Court on 22.03.2002 is known. However, the quantity has been curtailed to meet the immediate essential requirement.

The requirement of the cable is extremely urgent as the same is required for various Govt. utilities, Embassies, Hospitals and High Courts etc. The case was submitted to the Chairperson for consideration to procure the bare minimum requirement of cable of 150 sq.mm and 300 sq.mm cable. The case was again examined by Finance Dept.

Finance vide their diary No.484 dated 18.2.2002 with the approval of Chairperson, have finally concurred in the proposal of the Dept. to procure 10 K.M. of 300 sq.mm instead of 15 K.M. and 8 K.M. of 150 sq.mm instead of 10 K.M. of cable put to tender subject to conditions which are clarified as under:-

1. Funds are available against sanctioned estimates.2. The report of technical committee nominated by the Chairman shall be

submitted before inviting tenders for future purchase of the cables.

It is, therefore, proposed to purchase 8 K.M. 150 sq.mm 3 core and 10 K.M. of 300 sq.mm of 3 core 11KV XLPE cable from M/s. Polycab Wires (P) Ltd. at their quoted rates and other terms and conditions as detailed below:-

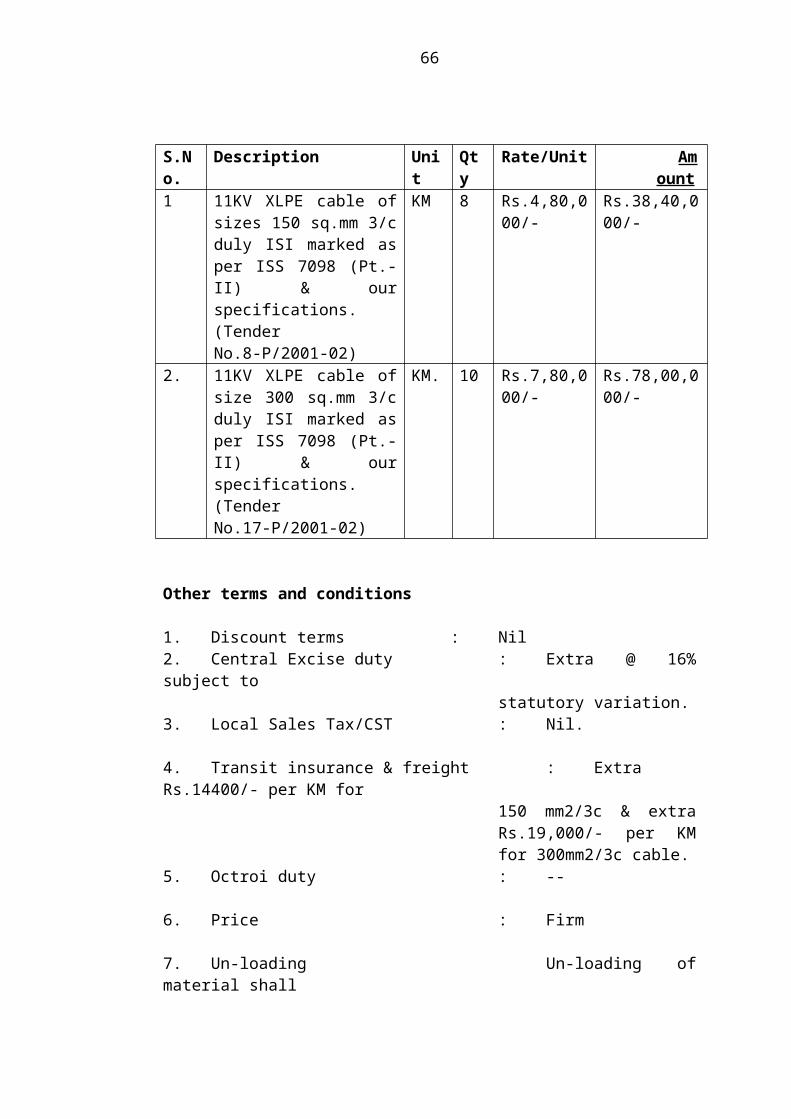

S.No. Description Unit Qty Rate/Unit Amount

1 11KV XLPE cable of sizes 150 sq.mm 3/c duly ISI marked as per ISS 7098 (Pt.-II) & our specifications. (Tender No.8-P/2001-02)

KM 8 Rs.4,80,000/- Rs.38,40,000/-

45

2. 11KV XLPE cable of size 300 sq.mm 3/c duly ISI marked as per ISS 7098 (Pt.-II) & our specifications. (Tender No.17-P/2001-02)

KM. 10 Rs.7,80,000/- Rs.78,00,000/-

Other terms and conditions

1. Discount terms : Nil2. Central Excise duty : Extra @ 16% subject to

statutory variation.3. Local Sales Tax/CST : Nil.

4. Transit insurance & freight : Extra Rs.14400/- per KM for 150 mm2/3c & extra Rs.19,000/- per KM for 300mm2/3c cable.

5. Octroi duty : --

6. Price : Firm

7. Un-loading Un-loading of material shall be firm’s responsibility.

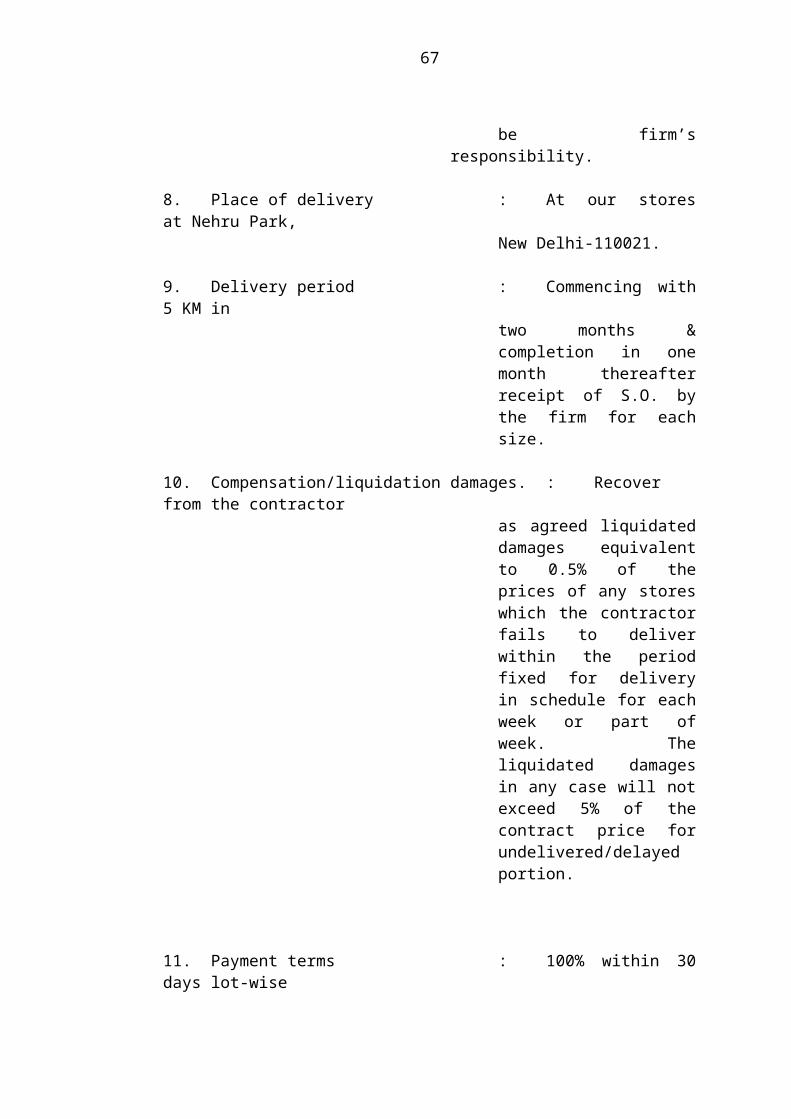

8. Place of delivery : At our stores at Nehru Park, New Delhi-110021.

9. Delivery period : Commencing with 5 KM in two months & completion in one month thereafter receipt of S.O. by the firm for each size.

10. Compensation/liquidation damages. : Recover from the contractor as agreed liquidated damages equivalent to 0.5% of the prices of any stores which the contractor fails to deliver within the period fixed for delivery in schedule for each week or part of week. The liquidated damages in any case will not exceed 5% of the contract price for undelivered/delayed portion.

46

11. Payment terms : 100% within 30 days lot-wise after receipt of material in good condition duly inspected and submission of bills.

12. Performance guarantee : A bank guarantee amounting to 2% of the total value of order (inclusive of taxes & duties) valid up to guarantee period shall be furnished by the firm as performance guarantee.

13. Risk purchase : The department reserves the right to make risk purchase if firm fails to comply with the contractual obligations.

14. Inspection : Through DGS&D/RITES/By our engineers at our cost. The date of which the material is offered for inspection shall be taken as the date of delivery.

15. Agreement : The firm will be required to execute an agreement within 10 days of receipt of the order on Rs.50/- non-judicial stamp paper to be procured by the firm failing which the supply order is liable to be rejected and amount of deposit made by the firm towards the earnest money shall be forfeited.

16. Arbitration : In case of any dispute, the matter shall be referred to the Sole Arbitrator, appointed by the Chairperson, NDMC.

17. Jurisdiction : In case of any legal dispute the venue shall be New Delhi Courts.

18. Guarantee : 12 months from the date of commissioning or 18 months from the date of delivery

47

whichever is earlier against manufacturing defects.

19. Additional quantity : The dept. reserves its right to place order for additional quantity up to 25% at the rates accepted within delivery period or mutually agreed subsequently with the approval of C.E.(E)

20. Other terms & conditions : As per our NIT.

21. Validity : 28.02.2002.

Chairman has seen.

C.E.(E) remarks:

The case is laid before the Council to accord approval for the purchase of 8 K.M. of 11KV XLPE cable 150mm2/3c at a total cost of Rs.38,40,000/- & 10 K.M. of 300mm2/3c 11KV XLPE cable at a total cost of Rs.78,00,000/- from M/s. Polycab Wires (P) Ltd., plus duties, freight & insurance etc. etc. as applicable and all other terms and conditions as above as concurred in by Finance and to accord expenditure sanction of the same amount.

COUNCIL’S DECISION

Resolved by the Council that approval is accorded for the purchase of 8KM of XLPE 150mm 2/3c at a cost of Rs.38,40,000/- (Rs. Thirty eight lacs & forty thousand only) & 10 KM of 300 mm 2/3c XLPE cable at the cost of Rs.78,00,000/- (Rs. Seventy eight lacs) from M/s Polycab Wires (P) Ltd. in respect of the above two tenders plus duties, freight & Insurance etc. etc. as applicable and as per the terms & conditions mentioned above and expenditure sanction of the same amount is also accorded.

48

ITEM NO. 3 (xii)

AUGMENTATION OF SUBSTASTION CAPACITY AND REPLACEMENT OF HT/LT SWITCHGEAR AT SUBSTATION ANSARI NAGAR (EAST).

Power demand of Ansari Nagar (E) and (West) has increased considerably

and the existing system is not capable of meeting the power demand of this area.

In order to cope up with the increasing power demand, it has been proposed to

augment the substation capacity from 1x1000 KVA (+) 1x500 KVA to 2x1000

KVA. Further HT feed from Safdarjung Hospital to Ansari Nagar (East) via

Ansari Nagar (West) of 70 sq.mm has been proposed to be augmented by HT feed

of 300 sq.mm.

Further it has been proposed to replace the existing old and obsolete HT

and LT switchgear at Ansari Nagar (E). The same have served forty years of its

useful life against the prescribed life of twenty five years and are giving frequent

problems. Necessary credit has been afforded to ht estimate.

Accordingly, an estimate amounting to Rs.33,96,500/- Gross and

Rs.33,92,500/-Net has been framed for Augmentation of substation capacity and

HT feed. The expenditure will be chargeable to the Budget Head E-4-1 plan works

having provision of Rs.400.00 lacs during 2001-2002.

Estimate amounting to Rs. 16,58,500/- Gross and Rs.16,37,000/- net has

been framed against the Budget Head E-3 Replacement, having provision of

Rs.392.00 lacs during 2001-2002.

Finance has concurred in the case vide their Diary No. D-3707/FA,, dtd.

04.02.2002 with certain observations which are replied as under:-

1. Adequate funds are available under the Head E-4-1 and kE-3.

(Expenditure incurred on E-4-1 up to December is Rs.181.00 lacs

against budget provision of Rs.431.00 lacs. Expenditure incurred on

49

E-3 up to December, 2001 is Rs.78.00 lacs against Budget estimate of

Rs.145.00 lacs

2. Certified that the information/data provided in the estimate are correct.

3. The existing transformer of 500 KVA, proposed to be replaced with

1000 KVA alternate use of the same will be considered.

The Chairman has seen the case.

Remarks of Chief Engineer(E) :

The case is laid before the Council for according administrative approval

and expenditure sanction to the estimate:-

1. for Augmentation of transformer capacity and HT cable amounting to

Rs.33,96,500/- gross and Rs.33,92,500/- net (Rupees thirty three lacs,

ninty six thousand and five hundred only, gross and Rupees Thirty three

lacs ninty two thousand and five hundred only, net)

2. for Replacement of HT/LT switchgear amounting to Rs.16,58,500/-

Gross and Rs. 16,37,000/- Net (Rupees sixteen lacs fifty eight thousand

and five hundred only, Gross and Rupees Sixteen lacs, thirty seven

thousand only, Net).

COUNCIL’S DECISION

Resolved by the Council that administrative approval and expenditure sanction is accorded to the estimate :-

1. Augmentation of transformer capacity and HT cable amounting to Rs.33,96,500/- Gross & Rs.33,92,500/- Net (Rs.Thirty three lacs ninty six thousand and five hundred only, Gross and Rs. Thirty three lacs ninety two thousand and five hundred only net).

2. Replacement of HT/LT Switchgear amounting to Rs.16,58,500/- Gross and Rs.16,37,000/- Net (Rs. Sixteen lacs fifty eight thousand and five hundred only, Gross and Rs. Sixteen lacs, thrity seven thousand only, Net).

50

ITEM NO. 3 (xiii)

PROVIDING HIGH MAST LIGHT FITTINGS AT THE CROSSING OF PT.PANT MARG-TALKATORA ROAD AND NEAR BUS TERMINAL AT CHURCH ROAD.

During a meeting held at the residence of Chief Minister, Delhi on dated

11.01.2001, it was proposed to provide high mast light fittings at the following

places:-

(i) On all the radial roads entries from C-Hexagon outer (9 Nos).

(ii) Round about at Central Secretariat North Block near Church Road.

(iii) Crossing of Pt. Pant Marg-Talkatora Road.

Chairman, NDMC has accorded approval in principle to the above proposal

on dated 31.01.2001.

Since the area was under the jurisdiction of Central Vista Committee, the

matter was referred to the Secretary, Central Vista Committee and it was decided

in the meeting of Central Vista Committee held on dated 11.07.2001 that high

mast light fittings may be installed in round about at the crossing of Pt. Pant

Marg-Talkatora Road and near bus terminal at Church Road. However, it was

mentioned that the proposals for providing high mast light fittings at all the radial

entries, C-Hexagan, India Gate should be put up again, after detail study.

Accordingly, an estimate amounting to Rs.11,10,500/- was framed for

installation of 2 Nos. thirty meters high mast with 16 Nos. luminaries combined

with narrow/broad beam light fittings and control panel for conservation of energy.

The expenditure is chargeable to the Head G-1-3 ROAD SECTOR with a

provision of Rs.100.00 lacs during 2001-2002.

Finance has concurred in the case vide their Diary No.D-44/FA, dtd.11-02-

2002 with certain observations, which are replied as under:-

51

1. Adequate funds are available under the Head G-1-3. The expenditure up

to January, 2002 is Rs.38.83 lacs against the provision of Rs.100.00

lacs.

2. It is ensured that all sanctioned similar proposals will be consolidated

to achieve competitive rates.

The Chairman has seen the case.

Remarks of Chief Engineer(Electric) :

The case is laid before the Council for according administrative approval

and expenditure sanction to the estimate amounting toRs.11,10,500/- (Rupees

Eleven lacs, ten thousand and five hundred only) for Providing high mast light

fittings at the crossing of Pt. Pant Marg -Talkatora Road and near bus

terminal at Church Road.

COUNCIL’S DECISION

Resolved by the Council that administrative approval and expenditure sanction is accorded to the estimate amounting to Rs.11,10,500/- (Rs. Eleven lacs, ten thousand and five hundred only) for providing High Mast light fittings at the crossing of Pt. Pant Marg – Talkatora Road & near bus terminus at Church Road.

52

ITEM NO. 3 (xiv)

ESTIMATE FOR PURCHASE OF ENERGY METERS AGAINST THE HEAD E-3 (DEPRECIATION RESERVE FUND).

The energy meters at the consumers premises are installed and replaced by

NDMC and the consumers pay the rent of the energy meters. Earlier, 14484 Nos.

energy meters were surveyed off by the Special Officer, NDMC on 24.12.94 after

due concurrence of the Finance. Surveyed off energy meters were to be replaced in

a phased manner. Accordingly, an estimate for 2568 nos. energy meters was got

sanctioned in the year 1996-97. These energy meters have since been procured

and utilized. In the second phase, an estimate for purchase of 4725 nos. energy

meters has been sanctioned in the year 2000-2001. The case is under process for

procurement of these energy meters. Now, in third and final phase, an estimate for

purchase of 7191 nos. Induction type single phase energy meters of various

capacities amounting to Rs. 82,37,000/- has been framed. Finance Department

have concurred in the estimate vide their Dy. No. FA-90/R dated 29.1.2002

subject to the following conditions:-

1. Correctness of the information submitted by the Department.

2. Certification that the expenditure will be met for this purpose only under

the available budget provisions.

3. Adoption of proper tendering procedure laid down under rules/regulations.

4. Approval of the competent authority.

Department’s clarifications:-1. Certified that the information submitted by the Department is correct.

2. Certified that the expenditure will be met out of the available budget

provisions for this purpose.

3. Proper tendering procedure for procurement laid down under rules/regulations

shall be followed.

4. The case is laid before the Council for necessary approval.

53

The expenditure shall be charged to head of account E-3 (Depreciation

Reserve Fund).

The Chairman has seen the case.

CE(E)-II’s Remarks:-

The case is laid before the Council for according administrative approval

and expenditure sanction to the estimate for purchase of 7191 nos. Induction type

single phase energy meters amounting to Rs. 82,37,000/- for replacement of

energy meters in NDMC area.

COUNCIL’S DECISION

Resolved by the Council that administrative approval and expenditure sanction to the estimate amounting to Rs.82,37,000/- for replacement of energy meters is accorded.

54

ITEM NO. 3 (xv)

CHARGES OF SUR-TAAL OPEN AIR THEATRE AT TALKATORA GARDEN.

NDMC has started Sur-Taal Open Air Theatre at Talkatora Garden for

organising Classical dance performances with the approval of the Chairman. To

make the best optimum use of the Theatre, it was also decided to provided it on

hire to different organizations for similar programmes.

The following charges & attached terms & conditions were proposed :-

a) Booking charges for programme for Classical dance/Music, Kavi Sammelan/Literary and theatre activities Rs. 5,000/- per dayby Regd. Association.

b) Booking for school/college Functions Rs. 1,000/- per dayc) Security Deposit (By Bank Draft) Rs. 5,000/-

(Refundable)

Head of A/c : D IX A Income Indoor Stadium

Proposed Terms & Conditions of Sur-Taal Open Air Theatre is appended at Annexure (See pages 56 – 57).

Finance Deptt. has also concurred the proposal & Chairman has approved the charges vide orders dt. 26-9-01.

The Chairman has seen the case.

The case is laid before the Council for information and approval.

COUNCIL’S DECISION

Resolved by the Council that the charges proposed by the Department in Para 2 (a, b and c) alongwith the terms & conditions are approved. Further, it resolved that exemption/reduction of charges would be granted by the Chairman on a case to case basis, depending on the merits of each case.

55

ANNEUXRE

56

ANNEUXRE

57

ITEM NO. 3 (xvi)

INVESTMENT OF PENSION FUND (CORPUS) IN STATE BANK OF INDIA.

NDMC disburses pension to its retired employees directly from its treasury

as also through the network of State Bank of India (SBI) branches in different parts

of the country. In the current year’s budget, out a provision of Rs 32 crore for

payment of pension, about Rs 18 crore is presently being disbursed through SBI.

In pursuance of an informal agreement between SBI and NDMC in 1991, SBI had

not been charging any fees for the services rendered on disbursement of pension

until the year 2000, in consideration of NDMC having agreed to maintain a

minimum balance of Rs 15 crore as fixed deposit with SBI.

2. In spite of the fact that the deposits with SBI have since risen to about Rs

178 crore, the bank started debiting NDMC’s account by about of Rs 3 lakh a

month from January 2001 as service charges @ 2.5% of the amount of pension

disbursed by it. As the unilateral action of SBI was contrary to the agreement,

NDMC communicated its objection to SBI. Following latter’s expression of

inability to waive the recovery of service charge, the Financial Advisor took a

meeting with the SBI authorities on 7th November 2001. Minutes of the meeting is

at Annexure (See pages 61 – 64). The burden of SBI’s argument was that,

initially, the scheme was only for Delhi/New Delhi branches, which was latter

extended to branches of SBI all over India. As the cost of service has substantially

increased over the years, it is no longer in a position to provide such free service to

NDMC. With the passage of time, the number of pensioners has gone up, resulting

in increase in the volume of transactions as also amount of pension disbursement.

The work has increased manifolds and so is the cost of service; hence, the levy of

service charges. On disbursement of Rs 18 crore, the service charges works out to

Rs 45 lakh in a year. Service charges will increase in proportion to the increase in

the amount of pension disbursement.

3. In the circumstances, NDMC has the option to either (i) look for another

bank that may offer such service at less cost or; (ii) pay the service charges to SBI.

The former option would pose difficulties to old pensioners in locating and

opening their pension accounts in new branches of another pension disbursing

58

bank as also to NDMC in ensuring a regular reconciliation of accounts with the

new pension disbursing bank. Bank rates received during the last three occasions

are placed at Annexure (See page 65). It may be seen from the “Cost Analysis of

Rates” that, from amongst the Public Sector Banks on NDMC’s panel, only Bank

of Maharashtra had quoted 00.25% more than other banks. However, the level of

investment in the Bank of Maharashtra is already too high vis-à-vis other

empanelled banks and since the Public Sector Banks are likely to be disinvested as

per budget speech 2000-01 of the Finance Minister and newspaper report of TOI

dated 17/11/2000 as per Annexure (See pages 66- 68), it would be advisable to

make the NDMC’s portfolio of investment as much diversified as possible.

Although SBI which is the principal banker of NDMC, has started charging 2.5%

of the amount of pension disbursement by way of service charges for disbursement

of pension which works out to Rs 45 lakh per annum for the current fiscal, the Cost

Analysis of Rates would show that it would still be desirable to disburse pension

through SBI especially in view of Sections 45 and 52 of the NDMC Act, 1994.

According to Section 52, surplus money standing at the credit of the New Delhi

Municipal Fund shall be deposited with SBI or in such scheduled banks as the

Council may select. Pension is in the nature of deferred wages and is a committed

liability of NDMC for its retired employees. As it is a committed liability, the

corpus of Pension Fund cannot be regarded as surplus money. It is also not a free

reserve because the entire corpus is meant to exclusively service NDMC’s liability

towards its retired employees. Hence, the rationale for creation of a separate

Pension Fund.

4. According to guidelines issues by the Department of Public Enterprises of

the Central Government on investment of funds by PSUs, safety of funds takes

precedence over returns. Taking cue from the Act and the said guidelines, parking

of Pension Fund in SBI appears to be a safer course of action. In the November

2001 issue of CRISIL’s Rating List, SBI has been rated AAA and P1+. AAA

denotes highest degree of certainty regarding timely payment of financial

obligations on the instrument as per Annexure (See page 69 – 72) . Any

adverse changes in circumstance are most unlikely to affect the payment on the

instrument. January 2002 issue of ICRA’s Rating Update ranks SBI as LAAA in

the long term and A1+ in the short term. LAAA denotes highest safety

59

(Annexure (See pages 73 - 74). It indicates a fundamentally strong position in

which risk factors are negligible. It further states that adverse circumstances are

not likely to affect the timely payment of principal and interest as per terms. A1+

also denotes highest safety where timely payment of debt/obligation is best.

5. Given the fact that safety of Pension Fund is of paramount importance, it is proposed that the entire corpus of Pension Fund of NDMC should be parked in SBI by opening a separate Pension Account of NDMC. The interest on the funds so parked would be credited to the Pension Fund and all pension payments would be debited to the said account. In a meeting held with the officers of SBI in November 2001, SBI tentatively agreed to waive service charges if NDMC raised its deposits from Rs 178 crore to Rs 300 crore. Minutes of the meeting are enclosed as Annexure VII. This was also indicated in SBI’s letter No. NDMB/INST/2001/6436 dated 31.10.2001 (Annexure (See page 75). Since raising investment of funds from the present Rs 178 crore to Rs 300 crore would take time, because it is dependent on the maturity of the NDMC’s FDRs in different banks which would mature at different points of time, SBI has been requested to allow NDMC some time to bring the level of investment to Rs. 300 crore. 6. For maintaining a diversified portfolio of NDMC’s investment, it is also proposed that NDMC may invest 50% of its maturity proceeds of FDRs/surplus funds in SBI the credit of NDMC’s Pension Fund and the balance may be parked in empanelled banks as per the Council’s guidelines.7. In anticipation of Council’s approval to the above proposal, a sum of Rs 49 crore has since been invested in SBI’s fixed deposits raising NDMC’s investment in SBI to Rs 227 crore. Council is requested to approve the proposal for investment of Pension Fund in SBI into a corpus of Rs 300 crore representing Pension Fund. Council is further requested to approve the proposal at para 6 above regarding pattern of investment.8. The case is accordingly laid before the Council.

COUNCIL’S DECISION

Resolved by the Council that proposal for creation of Pension Fund (Corpus) and investment of Pension Fund in State Bank of India, Main Branch, Sansad Marg, is approved.

The Council has further directed to review the investment policy in the background of disinvestments of nationalized banks to include financially sound banks in CBD area of NDMC.

60

Minutes of the Meeting with Officers of the State Bank of India, New Delhi Main Branch, Parliament Street, New Delhi held in the chamber of

Financial Adviser on 7 th November 2001.

The following were present:

N.D.M.C

1.Shri T.K. Sanyal, Financial Advisor (In Chair)