Embed Size (px)

Citation preview

Infrastructure September 9, 2014

ITD Cementation

Bloomberg: ITCE IN Reuters: ITCM.BO

Not Rated

Institutional Equities

India Research

MANAGEMENT MEET

Recommendation

CMP: Rs434

Click here to enter text.

Stock Information Market Cap. (Rs bn / US$ mn) 05/83

52-week High/Low (Rs) 449/114

3m ADV (Rs mn /US$ mn) 10 /0.2

Beta 1.0

Sensex/ Nifty 27,320/8,174

Share outstanding (mn) 12

Stock Performance (%) 1M 3M 12M YTD

Absolute 30.5 62.5 165.7 210.3

Rel. to Sensex 21.0 51.0 87.4 140.4

Performance

Source: Bloomberg

Analysts Contact Parikshit Kandpal

022 6184 4311

Click here to enter text. Click here to enter text. Click here to enter text.

30 130 230 330 430 530

15,000 17,000 19,000 21,000 23,000 25,000 27,000 29,000

Sep

-13

Oct

-13

No

v-1

3

Jan

-14

Feb

-14

Mar

-14

May

-14

Jun

-14

Jul-

14

Sep

-14

Sensex (LHS) ITD Cem (RHS)

A niche player – awaiting turnaround ITD Cementation (ITDC) is a niche player in the Indian EPC context with a

focus on complex yet differentiated segments. Having burnt its finger on

road EPC projects over 2002-12 period, ITDC is awaiting major turnaround.

This shall be achieved by QIP share dilution of Rs1.4bn (already raised –

Sep-14) and pending claims settlements with NHAI of Rs2bn. Presence in

high growth segments, potential margins expansion and robust project

pipeline remain key re-rating triggers. ITDC may be a CUB in the Indian

EPC markets but time is ripe to come out of past and build for future.

Strong diversified presence – complexity key differentiator ITDC is a subsidiary of the Thailand-based Italian -Thai Development Public

Company Ltd. (ITD) and is well entrenched in the construction of marine

works, highways & bridges, metros, airports, hydro-tunneling, dams &

canals, water & sewage, industrial structures and specialist foundation

engineering projects. ITD parent holds ~51.6% stake (post QIP dilution

during Sep-14) in the Indian company and has been at the forefront of

bringing Pre-qualification by Jointly bidding for the Indian Projects where

the Indian company’s qualification was insufficient. The complexities of

project undertaken by the company is also its key competitive strength.

NHAI claim settlement – equity dilution to strengthen BS ITDC is a focused player in the EPC segment and has consciously stayed

away from bidding for the BOT projects. Earlier road EPC project undertaken

by company resulted in ~Rs9.8bn of costs overruns which has largely been

absorbed in books. ITDC has presented 25% of the NHAI claims for awards

and is awaiting One time settlement (OTS). Going forward the focus will be

on debt reduction from current levels of Rs8.4bn (of this Rs3bn is disputed

with NHAI and ITD expects to receive about Rs2bn as one time settlement).

Current D/E is 2x which post OTS and QIP (Rs1.4bn) will come down to 0.8x.

Current order book 3.3x CY13 revenue – lends visibility to growth ITDC has current order book of Rs38.2bn, LOI of Rs7.3bn and L1 status of

Rs6.8bn this is ~3.3x CY13 revenue. Going forward the strong project pipeline

in Metro, Water network upgradation, Marine and River cleaning remains

key opportunity. Pick up in private Capex shall more or else augment order

misses on Road EPC segment, where ITDC won’t be participating in future.

Key Financial - Consolidated

Y/E Dec (Rs mn) CY10 CY11 CY12 CY13

Operating income 14,622 17,122 16,709 15,841

EBITDA 1,404 1,668 2,112 1,625

EBIDTA margins % 9.6 9.7 12.6 10.3

Net profit 94 226 220 93

EPS (Rs) 6.0 14.5 14.2 6.0

RoCE (%) 12.8 14.0 16.2 14.0

RoE (%) 2.6 6.1 5.6 2.3

Source: Company, Karvy Institutional Research

2

9th September 2014

ITD Cementation Ltd.

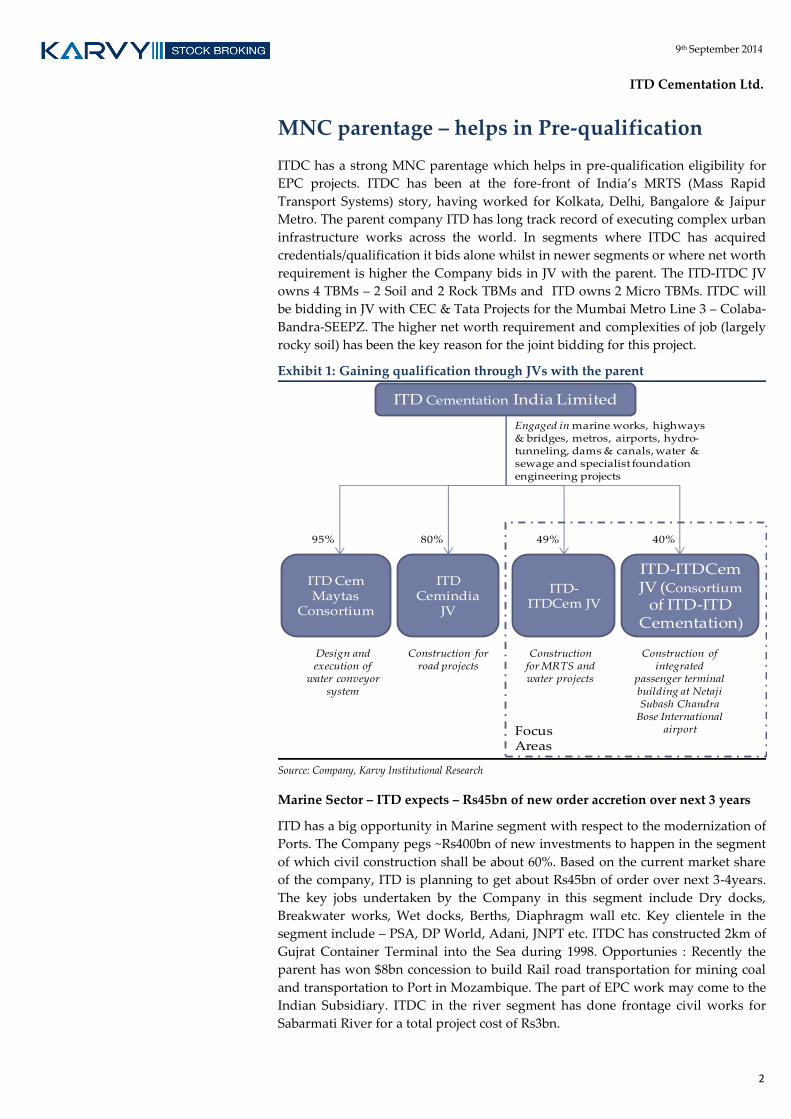

MNC parentage – helps in Pre-qualification

ITDC has a strong MNC parentage which helps in pre-qualification eligibility for

EPC projects. ITDC has been at the fore-front of India’s MRTS (Mass Rapid

Transport Systems) story, having worked for Kolkata, Delhi, Bangalore & Jaipur

Metro. The parent company ITD has long track record of executing complex urban

infrastructure works across the world. In segments where ITDC has acquired

credentials/qualification it bids alone whilst in newer segments or where net worth

requirement is higher the Company bids in JV with the parent. The ITD-ITDC JV

owns 4 TBMs – 2 Soil and 2 Rock TBMs and ITD owns 2 Micro TBMs. ITDC will

be bidding in JV with CEC & Tata Projects for the Mumbai Metro Line 3 – Colaba-

Bandra-SEEPZ. The higher net worth requirement and complexities of job (largely

rocky soil) has been the key reason for the joint bidding for this project.

Exhibit 1: Gaining qualification through JVs with the parent

Source: Company, Karvy Institutional Research

Marine Sector – ITD expects – Rs45bn of new order accretion over next 3 years

ITD has a big opportunity in Marine segment with respect to the modernization of

Ports. The Company pegs ~Rs400bn of new investments to happen in the segment

of which civil construction shall be about 60%. Based on the current market share

of the company, ITD is planning to get about Rs45bn of order over next 3-4years.

The key jobs undertaken by the Company in this segment include Dry docks,

Breakwater works, Wet docks, Berths, Diaphragm wall etc. Key clientele in the

segment include – PSA, DP World, Adani, JNPT etc. ITDC has constructed 2km of

Gujrat Container Terminal into the Sea during 1998. Opportunies : Recently the

parent has won $8bn concession to build Rail road transportation for mining coal

and transportation to Port in Mozambique. The part of EPC work may come to the

Indian Subsidiary. ITDC in the river segment has done frontage civil works for

Sabarmati River for a total project cost of Rs3bn.

ITD Cementation India Limited

ITD Cemindia

JV

ITD-ITDCem JV

ITD-ITDCem JV (Consortium

of ITD-ITD Cementation)

80% 49% 40%

Engaged in marine works, highways & bridges, metros, airports, hydro-tunneling, dams & canals, water & sewage and specialist foundation engineering projects

Construction of integrated

passenger terminal building at NetajiSubash Chandra

Bose International airport

Construction for MRTS and water projects

Construction for road projects

ITD Cem Maytas

Consortium

Design and execution of

water conveyor system

95%

FocusAreas

3

9th September 2014

ITD Cementation Ltd.

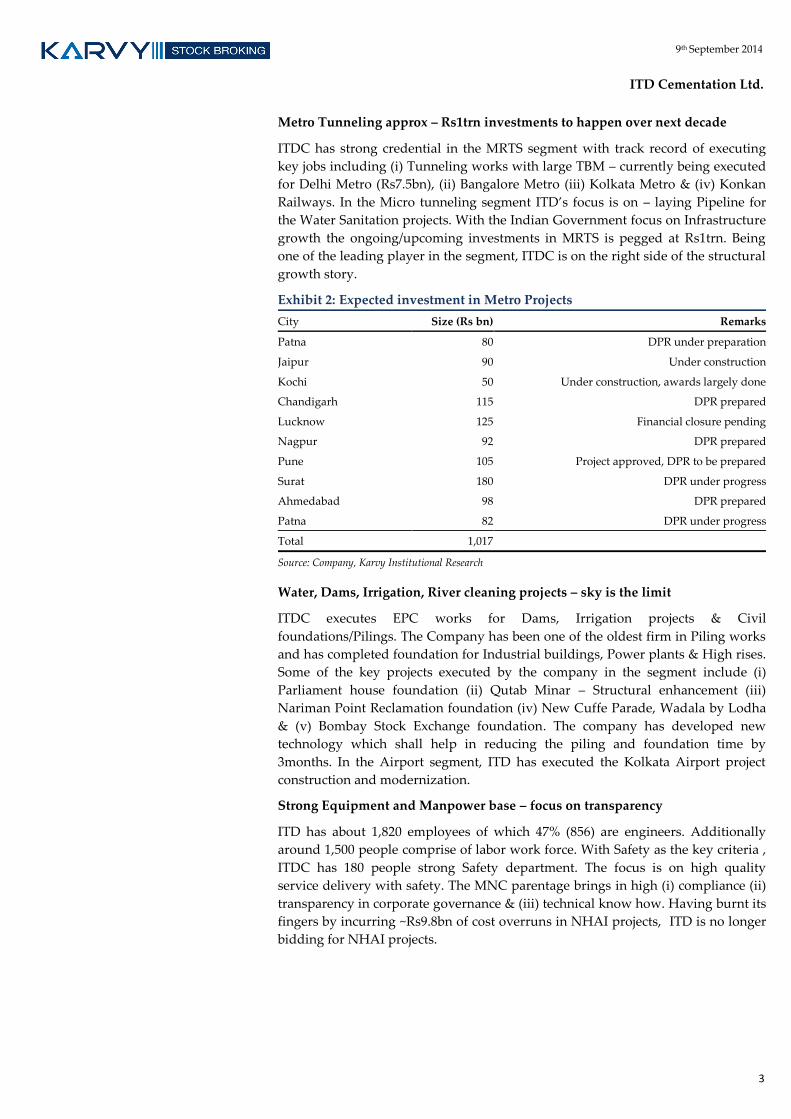

Metro Tunneling approx – Rs1trn investments to happen over next decade

ITDC has strong credential in the MRTS segment with track record of executing

key jobs including (i) Tunneling works with large TBM – currently being executed

for Delhi Metro (Rs7.5bn), (ii) Bangalore Metro (iii) Kolkata Metro & (iv) Konkan

Railways. In the Micro tunneling segment ITD’s focus is on – laying Pipeline for

the Water Sanitation projects. With the Indian Government focus on Infrastructure

growth the ongoing/upcoming investments in MRTS is pegged at Rs1trn. Being

one of the leading player in the segment, ITDC is on the right side of the structural

growth story.

Exhibit 2: Expected investment in Metro Projects

City Size (Rs bn) Remarks

Patna 80 DPR under preparation

Jaipur 90 Under construction

Kochi 50 Under construction, awards largely done

Chandigarh 115 DPR prepared

Lucknow 125 Financial closure pending

Nagpur 92 DPR prepared

Pune 105 Project approved, DPR to be prepared

Surat 180 DPR under progress

Ahmedabad 98 DPR prepared

Patna 82 DPR under progress

Total 1,017

Source: Company, Karvy Institutional Research

Water, Dams, Irrigation, River cleaning projects – sky is the limit

ITDC executes EPC works for Dams, Irrigation projects & Civil

foundations/Pilings. The Company has been one of the oldest firm in Piling works

and has completed foundation for Industrial buildings, Power plants & High rises.

Some of the key projects executed by the company in the segment include (i)

Parliament house foundation (ii) Qutab Minar – Structural enhancement (iii)

Nariman Point Reclamation foundation (iv) New Cuffe Parade, Wadala by Lodha

& (v) Bombay Stock Exchange foundation. The company has developed new

technology which shall help in reducing the piling and foundation time by

3months. In the Airport segment, ITD has executed the Kolkata Airport project

construction and modernization.

Strong Equipment and Manpower base – focus on transparency

ITD has about 1,820 employees of which 47% (856) are engineers. Additionally

around 1,500 people comprise of labor work force. With Safety as the key criteria ,

ITDC has 180 people strong Safety department. The focus is on high quality

service delivery with safety. The MNC parentage brings in high (i) compliance (ii)

transparency in corporate governance & (iii) technical know how. Having burnt its

fingers by incurring ~Rs9.8bn of cost overruns in NHAI projects, ITD is no longer

bidding for NHAI projects.

4

9th September 2014

ITD Cementation Ltd.

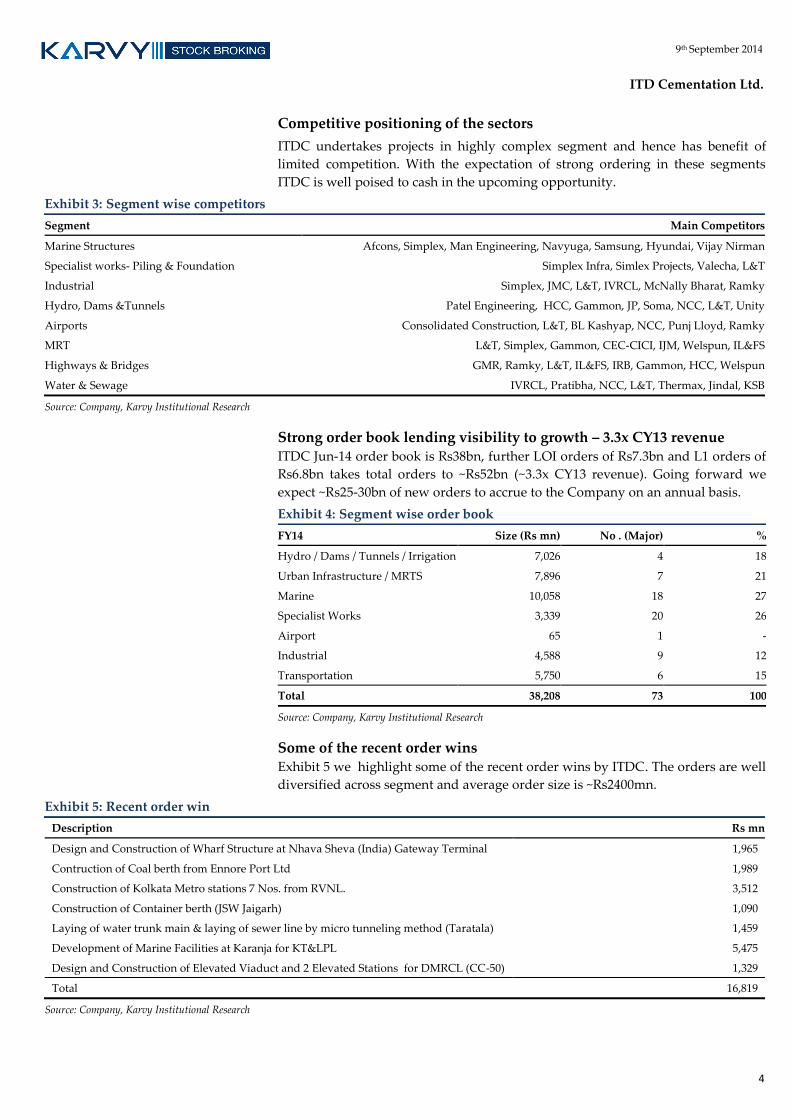

Competitive positioning of the sectors

ITDC undertakes projects in highly complex segment and hence has benefit of

limited competition. With the expectation of strong ordering in these segments

ITDC is well poised to cash in the upcoming opportunity.

Exhibit 3: Segment wise competitors

Segment Main Competitors

Marine Structures Afcons, Simplex, Man Engineering, Navyuga, Samsung, Hyundai, Vijay Nirman

Specialist works- Piling & Foundation Simplex Infra, Simlex Projects, Valecha, L&T

Industrial Simplex, JMC, L&T, IVRCL, McNally Bharat, Ramky

Hydro, Dams &Tunnels Patel Engineering, HCC, Gammon, JP, Soma, NCC, L&T, Unity

Airports Consolidated Construction, L&T, BL Kashyap, NCC, Punj Lloyd, Ramky

MRT L&T, Simplex, Gammon, CEC-CICI, IJM, Welspun, IL&FS

Highways & Bridges GMR, Ramky, L&T, IL&FS, IRB, Gammon, HCC, Welspun

Water & Sewage IVRCL, Pratibha, NCC, L&T, Thermax, Jindal, KSB

Source: Company, Karvy Institutional Research

Strong order book lending visibility to growth – 3.3x CY13 revenue ITDC Jun-14 order book is Rs38bn, further LOI orders of Rs7.3bn and L1 orders of

Rs6.8bn takes total orders to ~Rs52bn (~3.3x CY13 revenue). Going forward we

expect ~Rs25-30bn of new orders to accrue to the Company on an annual basis.

Exhibit 4: Segment wise order book

FY14 Size (Rs mn) No . (Major) %

Hydro / Dams / Tunnels / Irrigation 7,026 4 18

Urban Infrastructure / MRTS 7,896 7 21

Marine 10,058 18 27

Specialist Works 3,339 20 26

Airport 65 1 -

Industrial 4,588 9 12

Transportation 5,750 6 15

Total 38,208 73 100

Source: Company, Karvy Institutional Research

Some of the recent order wins Exhibit 5 we highlight some of the recent order wins by ITDC. The orders are well

diversified across segment and average order size is ~Rs2400mn.

Exhibit 5: Recent order win

Description Rs mn

Design and Construction of Wharf Structure at Nhava Sheva (India) Gateway Terminal 1,965

Contruction of Coal berth from Ennore Port Ltd 1,989

Construction of Kolkata Metro stations 7 Nos. from RVNL. 3,512

Construction of Container berth (JSW Jaigarh) 1,090

Laying of water trunk main & laying of sewer line by micro tunneling method (Taratala) 1,459

Development of Marine Facilities at Karanja for KT&LPL 5,475

Design and Construction of Elevated Viaduct and 2 Elevated Stations for DMRCL (CC-50) 1,329

Total 16,819

Source: Company, Karvy Institutional Research

5

9th September 2014

ITD Cementation Ltd.

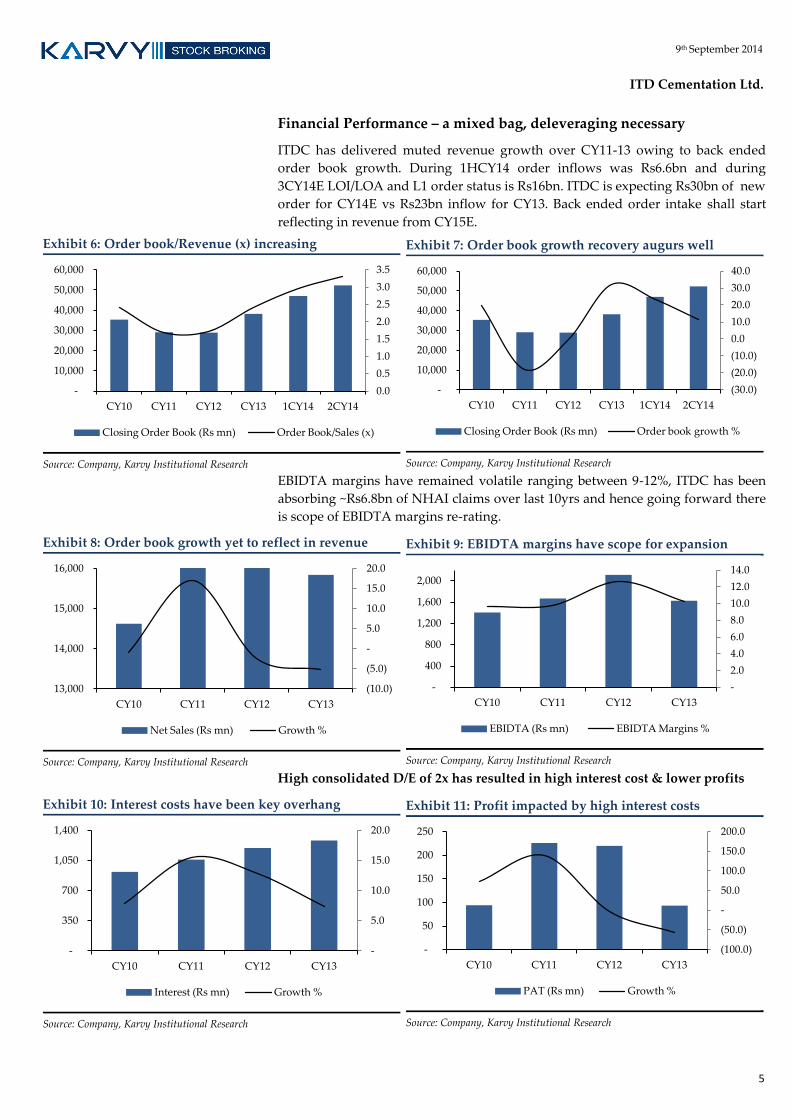

Financial Performance – a mixed bag, deleveraging necessary

ITDC has delivered muted revenue growth over CY11-13 owing to back ended

order book growth. During 1HCY14 order inflows was Rs6.6bn and during

3CY14E LOI/LOA and L1 order status is Rs16bn. ITDC is expecting Rs30bn of new

order for CY14E vs Rs23bn inflow for CY13. Back ended order intake shall start

reflecting in revenue from CY15E.

Exhibit 6: Order book/Revenue (x) increasing

Source: Company, Karvy Institutional Research

Exhibit 7: Order book growth recovery augurs well

Source: Company, Karvy Institutional Research

EBIDTA margins have remained volatile ranging between 9-12%, ITDC has been

absorbing ~Rs6.8bn of NHAI claims over last 10yrs and hence going forward there

is scope of EBIDTA margins re-rating.

Exhibit 8: Order book growth yet to reflect in revenue

Source: Company, Karvy Institutional Research

Exhibit 9: EBIDTA margins have scope for expansion

Source: Company, Karvy Institutional Research

High consolidated D/E of 2x has resulted in high interest cost & lower profits

Exhibit 10: Interest costs have been key overhang

Source: Company, Karvy Institutional Research

Exhibit 11: Profit impacted by high interest costs

Source: Company, Karvy Institutional Research

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

-

10,000

20,000

30,000

40,000

50,000

60,000

CY10 CY11 CY12 CY13 1CY14 2CY14

Closing Order Book (Rs mn) Order Book/Sales (x)

(30.0)

(20.0)

(10.0)

0.0

10.0

20.0

30.0

40.0

-

10,000

20,000

30,000

40,000

50,000

60,000

CY10 CY11 CY12 CY13 1CY14 2CY14

Closing Order Book (Rs mn) Order book growth %

(10.0)

(5.0)

-

5.0

10.0

15.0

20.0

13,000

14,000

15,000

16,000

CY10 CY11 CY12 CY13

Net Sales (Rs mn) Growth %

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

-

400

800

1,200

1,600

2,000

CY10 CY11 CY12 CY13

EBIDTA (Rs mn) EBIDTA Margins %

-

5.0

10.0

15.0

20.0

-

350

700

1,050

1,400

CY10 CY11 CY12 CY13

Interest (Rs mn) Growth %

(100.0)

(50.0)

-

50.0

100.0

150.0

200.0

-

50

100

150

200

250

CY10 CY11 CY12 CY13

PAT (Rs mn) Growth %

6

9th September 2014

ITD Cementation Ltd.

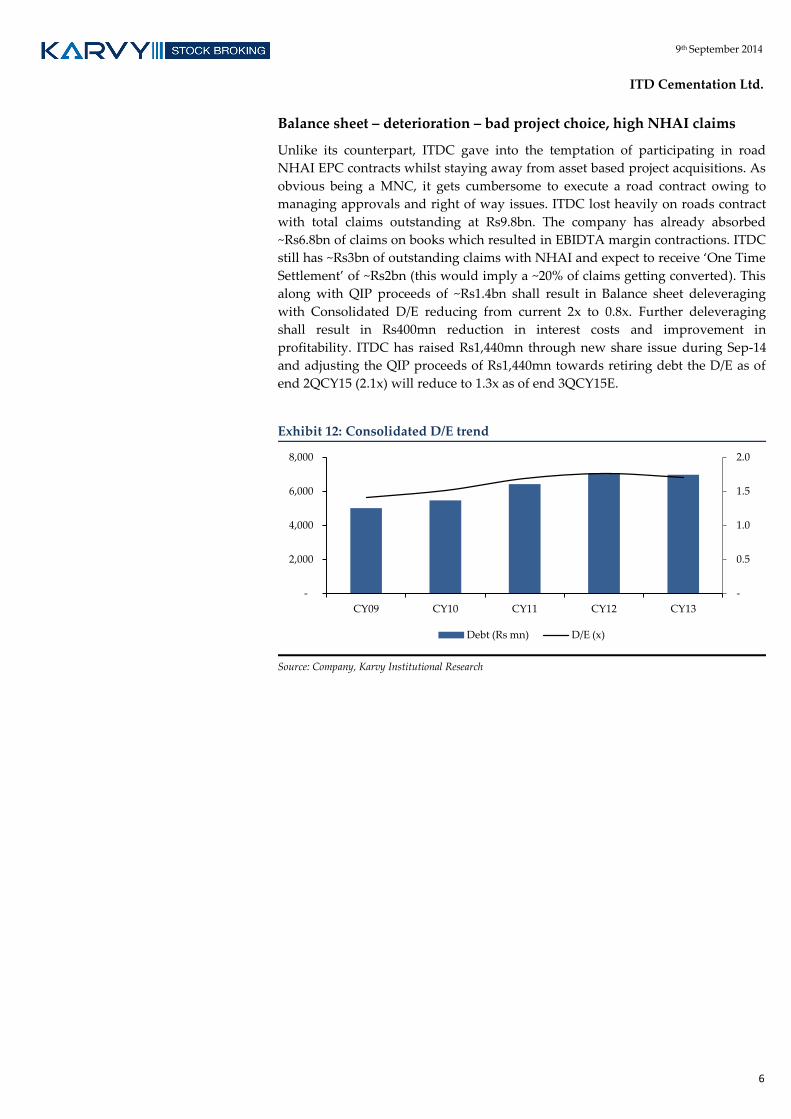

Balance sheet – deterioration – bad project choice, high NHAI claims

Unlike its counterpart, ITDC gave into the temptation of participating in road

NHAI EPC contracts whilst staying away from asset based project acquisitions. As

obvious being a MNC, it gets cumbersome to execute a road contract owing to

managing approvals and right of way issues. ITDC lost heavily on roads contract

with total claims outstanding at Rs9.8bn. The company has already absorbed

~Rs6.8bn of claims on books which resulted in EBIDTA margin contractions. ITDC

still has ~Rs3bn of outstanding claims with NHAI and expect to receive ‘One Time

Settlement’ of ~Rs2bn (this would imply a ~20% of claims getting converted). This

along with QIP proceeds of ~Rs1.4bn shall result in Balance sheet deleveraging

with Consolidated D/E reducing from current 2x to 0.8x. Further deleveraging

shall result in Rs400mn reduction in interest costs and improvement in

profitability. ITDC has raised Rs1,440mn through new share issue during Sep-14

and adjusting the QIP proceeds of Rs1,440mn towards retiring debt the D/E as of

end 2QCY15 (2.1x) will reduce to 1.3x as of end 3QCY15E.

Exhibit 12: Consolidated D/E trend

Source: Company, Karvy Institutional Research

-

0.5

1.0

1.5

2.0

-

2,000

4,000

6,000

8,000

CY09 CY10 CY11 CY12 CY13

Debt (Rs mn) D/E (x)

7

9th September 2014

ITD Cementation Ltd.

Financials - Consolidated

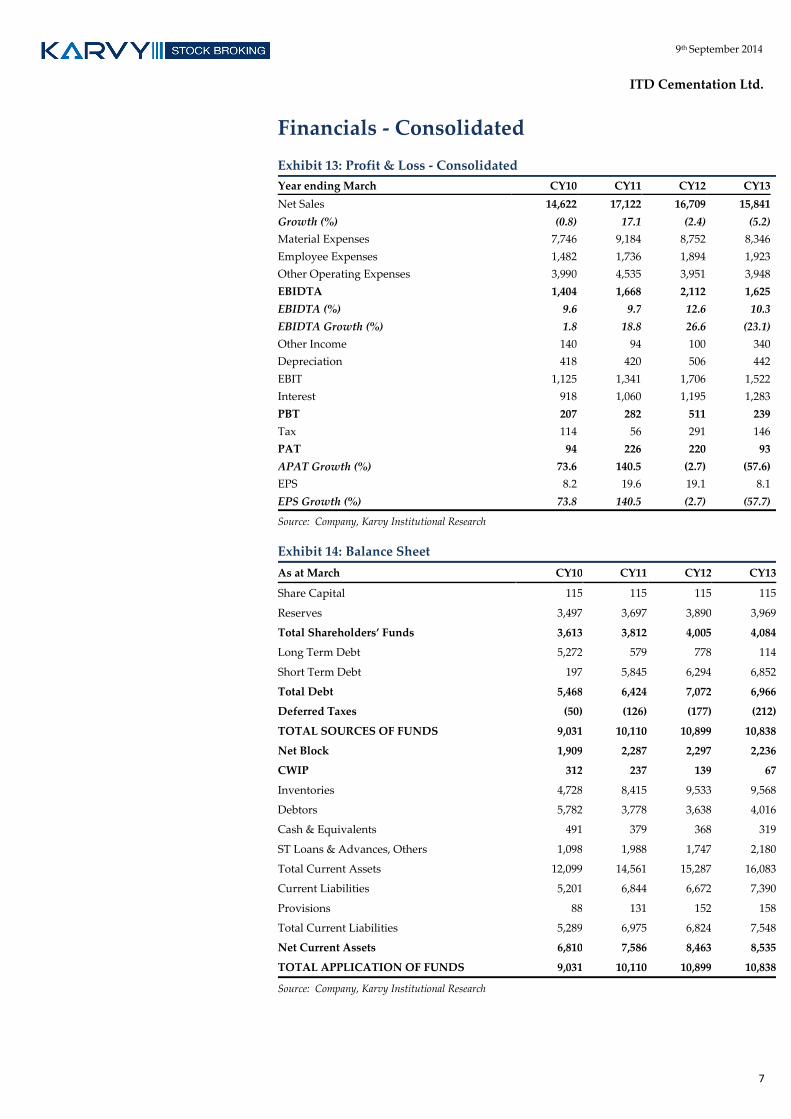

Exhibit 13: Profit & Loss - Consolidated

Year ending March CY10 CY11 CY12 CY13

Net Sales 14,622 17,122 16,709 15,841

Growth (%) (0.8) 17.1 (2.4) (5.2)

Material Expenses 7,746 9,184 8,752 8,346

Employee Expenses 1,482 1,736 1,894 1,923

Other Operating Expenses 3,990 4,535 3,951 3,948

EBIDTA 1,404 1,668 2,112 1,625

EBIDTA (%) 9.6 9.7 12.6 10.3

EBIDTA Growth (%) 1.8 18.8 26.6 (23.1)

Other Income 140 94 100 340

Depreciation 418 420 506 442

EBIT 1,125 1,341 1,706 1,522

Interest 918 1,060 1,195 1,283

PBT 207 282 511 239

Tax 114 56 291 146

PAT 94 226 220 93

APAT Growth (%) 73.6 140.5 (2.7) (57.6)

EPS 8.2 19.6 19.1 8.1

EPS Growth (%) 73.8 140.5 (2.7) (57.7)

Source: Company, Karvy Institutional Research

Exhibit 14: Balance Sheet

As at March CY10 CY11 CY12 CY13

Share Capital 115 115 115 115

Reserves 3,497 3,697 3,890 3,969

Total Shareholders’ Funds 3,613 3,812 4,005 4,084

Long Term Debt 5,272 579 778 114

Short Term Debt 197 5,845 6,294 6,852

Total Debt 5,468 6,424 7,072 6,966

Deferred Taxes (50) (126) (177) (212)

TOTAL SOURCES OF FUNDS 9,031 10,110 10,899 10,838

Net Block 1,909 2,287 2,297 2,236

CWIP 312 237 139 67

Inventories 4,728 8,415 9,533 9,568

Debtors 5,782 3,778 3,638 4,016

Cash & Equivalents 491 379 368 319

ST Loans & Advances, Others 1,098 1,988 1,747 2,180

Total Current Assets 12,099 14,561 15,287 16,083

Current Liabilities 5,201 6,844 6,672 7,390

Provisions 88 131 152 158

Total Current Liabilities 5,289 6,975 6,824 7,548

Net Current Assets 6,810 7,586 8,463 8,535

TOTAL APPLICATION OF FUNDS 9,031 10,110 10,899 10,838

Source: Company, Karvy Institutional Research

8

9th September 2014

ITD Cementation Ltd.

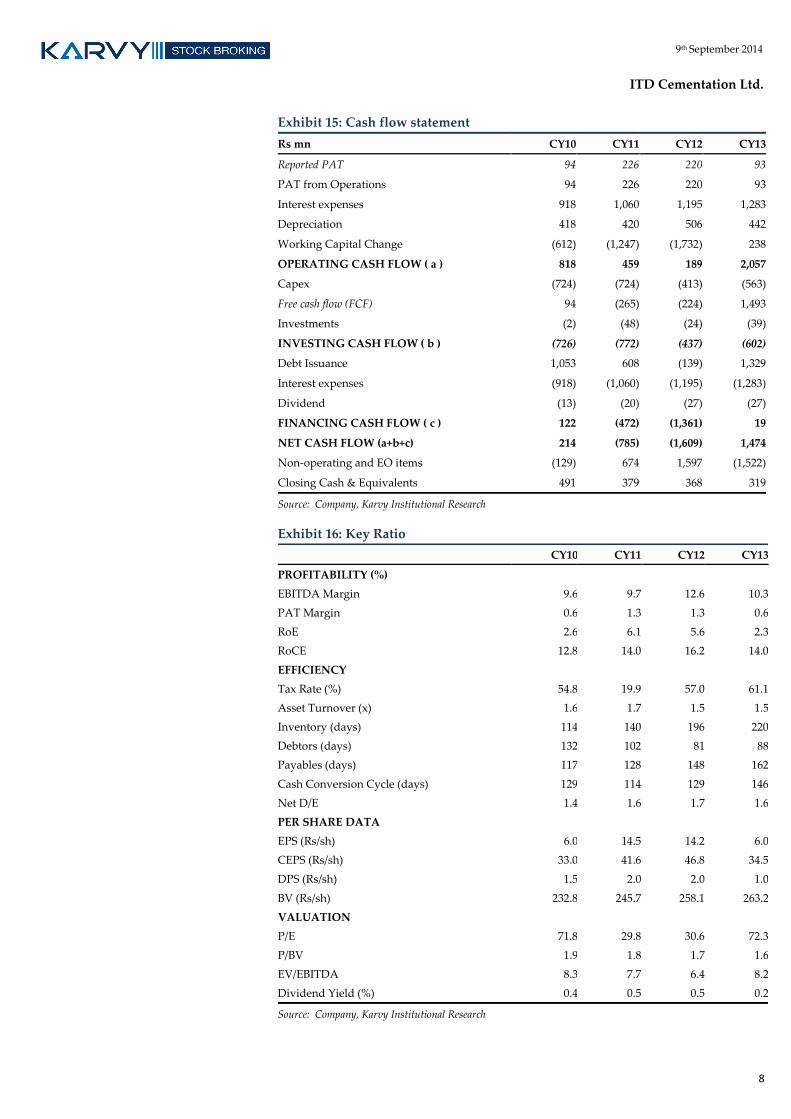

Exhibit 15: Cash flow statement

Rs mn CY10 CY11 CY12 CY13

Reported PAT 94 226 220 93

PAT from Operations 94 226 220 93

Interest expenses 918 1,060 1,195 1,283

Depreciation 418 420 506 442

Working Capital Change (612) (1,247) (1,732) 238

OPERATING CASH FLOW ( a ) 818 459 189 2,057

Capex (724) (724) (413) (563)

Free cash flow (FCF) 94 (265) (224) 1,493

Investments (2) (48) (24) (39)

INVESTING CASH FLOW ( b ) (726) (772) (437) (602)

Debt Issuance 1,053 608 (139) 1,329

Interest expenses (918) (1,060) (1,195) (1,283)

Dividend (13) (20) (27) (27)

FINANCING CASH FLOW ( c ) 122 (472) (1,361) 19

NET CASH FLOW (a+b+c) 214 (785) (1,609) 1,474

Non-operating and EO items (129) 674 1,597 (1,522)

Closing Cash & Equivalents 491 379 368 319

Source: Company, Karvy Institutional Research

Exhibit 16: Key Ratio

CY10 CY11 CY12 CY13

PROFITABILITY (%)

EBITDA Margin 9.6 9.7 12.6 10.3

PAT Margin 0.6 1.3 1.3 0.6

RoE 2.6 6.1 5.6 2.3

RoCE 12.8 14.0 16.2 14.0

EFFICIENCY

Tax Rate (%) 54.8 19.9 57.0 61.1

Asset Turnover (x) 1.6 1.7 1.5 1.5

Inventory (days) 114 140 196 220

Debtors (days) 132 102 81 88

Payables (days) 117 128 148 162

Cash Conversion Cycle (days) 129 114 129 146

Net D/E 1.4 1.6 1.7 1.6

PER SHARE DATA

EPS (Rs/sh) 6.0 14.5 14.2 6.0

CEPS (Rs/sh) 33.0 41.6 46.8 34.5

DPS (Rs/sh) 1.5 2.0 2.0 1.0

BV (Rs/sh) 232.8 245.7 258.1 263.2

VALUATION

P/E 71.8 29.8 30.6 72.3

P/BV 1.9 1.8 1.7 1.6

EV/EBITDA 8.3 7.7 6.4 8.2

Dividend Yield (%) 0.4 0.5 0.5 0.2

Source: Company, Karvy Institutional Research

Institutional Equities Team Rahul Sharma

Head – Institutional Equities /

Research / Pharma +91-22 61844310/01 [email protected]

Gurdarshan Singh Kharbanda Head - Sales-Trading +91-22 61844368/69 [email protected]

INSTITUTIONAL RESEARCH

Analysts Industry / Sector Desk Phone Email ID

Mitul Shah Automobiles/Auto Ancillary +91-22 61844312 [email protected]

Parikshit Kandpal Infra / Real Estate / Strategy/Consumer +91-22 61844311 [email protected]

Rajesh Kumar Ravi Cement/ Logistics/ Paints +91-22 61844313 [email protected]

Rupesh Sankhe Power/Capital Goods +91-22 61844315 [email protected]

Asutosh Mishra Banking & Finance +91-22-61844329 [email protected]

Vinesh Vala Research Associate +91 22 61844325 [email protected]

Rajesh Mudaliar Research Associate +91 22 61844322 [email protected]

INSTITUTIONAL SALES

Celine Dsouza Sales +91 22 61844341 [email protected]

Edelbert Dcosta Sales +91 22 61844344 [email protected]

INSTITUTIONAL SALES TRADING & DEALING

Aashish Parekh Institutional Sales/Trading/ Dealing +91-22 61844361 [email protected]

Prashant Oza Institutional Sales/Trading/ Dealing +91-22 61844370 /71 [email protected]

Pratik Sanghvi Institutional Sales/Trading/ Dealing +91-22 61844366 /67 [email protected]

For further enquiries please contact:

Tel: +91-22-6184 4300

Disclosures Appendix

Analyst certification

The following analyst(s), who is (are) primarily responsible for this report, certify (ies) that the views expressed

herein accurately reflect his (their) personal view(s) about the subject security (ies) and issuer(s) and that no part of

his (their) compensation was, is or will be directly or indirectly related to the specific recommendation(s) or views

contained in this research report.

Disclaimer

The information and views presented in this report are prepared by Karvy Stock Broking Limited. The information

contained herein is based on our analysis and upon sources that we consider reliable. We, however, do not vouch for

the accuracy or the completeness thereof. This material is for personal information and we are not responsible for any

loss incurred based upon it. The investments discussed or recommended in this report may not be suitable for all

investors. Investors must make their own investment decisions based on their specific investment objectives and

financial position and using such independent advice, as they believe necessary. While acting upon any information

or analysis mentioned in this report, investors may please note that neither Karvy nor Karvy Stock Broking nor any

person connected with any associate companies of Karvy accepts any liability arising from the use of this information

and views mentioned in this document.

The author, directors and other employees of Karvy and its affiliates may hold long or short positions in the above

mentioned companies from time to time. Every employee of Karvy and its associate companies are required to

disclose their individual stock holdings and details of trades, if any, that they undertake. The team rendering

corporate analysis and investment recommendations are restricted in purchasing/selling of shares or other securities

till such a time this recommendation has either been displayed or has been forwarded to clients of Karvy. All

employees are further restricted to place orders only through Karvy Stock Broking Ltd. This report is intended for a

restricted audience and we are not soliciting any action based on it. Neither the information nor any opinion

expressed herein constitutes an offer or an invitation to make an offer, to buy or sell any securities, or any options,

futures nor other derivatives related to such securities.

Karvy Stock Broking Limited Institutional Equities

Office No. 701, 7th Floor, Hallmark Business Plaza, Opp.-Gurunanak Hospital, Mumbai 400 051 Regd Off : 46, Road No 4, Street No 1, Banjara Hills, Hyderabad – 500 034.

Karvy Stock Broking Research is also available on: Bloomberg - KRVY <GO>, Thomson Publisher & Reuters.

Stock Ratings Absolute Returns Buy : > 15% Hold : 5 - 15% Sell : < 5%