Embed Size (px)

Citation preview

Marshall Terry COO/CCO of Rotation Capital Management, L.P.

Rotation Capital Management, L.P., 2015

2014

Solving the Issues Facing Hedge Fund Managers Today: The Role of the Hedge Fund COO and Co-Sourcing

2 | P a g e

INTRODUCTION:

The capital raising environment for hedge funds is as challenging as ever, and

hedge funds that are looking to attract institutional investors (currently the largest source

of investor dollars) will have to develop the institutional qualities that institutional

investors are looking for. The regulatory environment is also more onerous than ever, and a

hedge fund that is of institutional quality will be in a better position to successfully

navigate the ever increasing regulatory burdens.

The term “institutional quality” is used to describe a hedge fund (and the hedge

fund manager (“HFM”) that manages the hedge fund) that has a mix of characteristics that

institutional investors require before making an allocation. These characteristics include: (i)

a well-developed investment management infrastructure; (ii) a robust compliance regime;

(iii) well documented policies and procedures; (iv) a robust operational platform that meets

international standards; (v) top service providers; and (vi) a strong risk management

program.

Investors will use the operational due diligence (“ODD”) process at the beginning

(and during the life of the relationship) to determine whether a hedge fund is of

institutional quality. Similarly, regulators will use the exam process to determine whether

a HFM has the correct processes and controls in place to manage the associated risks in

running their business and to ensure that the hedge fund is compliant with the relevant

regulatory rules of the jurisdictions in which they are domiciled and transact in.1 The failure

to pass either of these tests will significantly inhibit the HFM’s ability to raise capital. Thus,

one of the most important responsibilities of the HFM is to ensure that it can effectively

1 Some of the regulatory regimes that hedge funds are currently subject to are as follows: (i) in the United States hedge funds are subject to the rules defined in the Securities Acts of 1933 and 1934, the Investment Company Act of 1940, the Investment Advisers Act of 1940 (the “Advisers Act”), and, in some cases, the Commodity Exchange Act; and (ii) in Europe hedge funds are subject to the rules recently codified in the Directive on Alternative Investment Fund Managers (“AIFMD”). Similar type regulations are developing in Asia as well.

3 | P a g e

and efficiently meet the requirements imposed on it by investors (the continuing ODD

process) and regulators (the inevitable exam process).

A BROADER LOOK AT THE ISSUES FACING HFMS TODAY:

Since the financial crisis of 2008-09 (which lead to the recent passage of the Dodd-

Frank Act and the European Directive on Alternative Investment Fund Managers) and the

exposure of the Madoff fraud case (collectively, the “Financial Crisis”), the barriers to

setting up a hedge fund are substantially higher and more burdensome than in the past,

where both a strong pedigree and track record almost always assured a robust capital

raising environment. The two main barriers to entry, which are inversely related to each

other, are: (i) substantially increased costs of doing business; and (ii) a decrease in

operating capital.

The first barrier to entry (increased costs) is the result of the increased investor and

regulatory demands post the Financial Crisis: the cost of managing a hedge fund has been

growing more quickly than hedge fund revenues.2 For instance, the current state of

regulatory affairs (it is now more likely than ever that a HFM will be subject to a regulatory

exam) and investor due diligence and transparency demands have created a challenging

and expensive environment in which to manage a hedge fund. As a result of these

increasing demands, new and established HFMs need to develop institutional quality

infrastructure if they want to grow and attract new monies. Not surprisingly, it can cost a

significant amount of money and take a great deal of time to develop an institutional

quality infrastructure. For instance, according to a recent hedge fund expense survey

conducted by Citi Prime Finance, HFMs need $375 million of assets under management

(“AuM”) in order to break even and survive off management fees alone.3 Similarly, KPMG

recently estimated that the small HFM spends on average $750,000 in support of their

2 Ernst & Young, Global Hedge Fund and Investor Survey 2012, 2012 3 Citi Prime Services, 2013 Business Expense Benchmark Survey, November 2013.

4 | P a g e

compliance programs.4 The following is an outline of the major expenses that a HFM will

have to manage.

HFM EXPENSES

START-UP ONGOING Legal- Org Docs Salaries Consulting Payroll Tax Office Furniture Health Benefits IT Hardware Legal IT Infrastructure Tax Office Expenses Rent Expense Capital Raising IT Infrastructure and Support

Regulatory

Compliance

Marketing Expenses

Bloomberg

Office Equipment and Supplies

Insurance

OMS/PMS

Accounting/Risk System

D&O/E&O

FUND EXPENSES START-UP ONGOING ST Legal- Org Docs Administration Expenses Legal- Acct Opening Docs (PB, ISDA, etc.) Board of Directors Expenses (if applicable)

Registered Office Expense

Audit/Tax Expense

Legal

Consulting

Research

PB/Bank Fees

D&O/E&O

Financial Statements/Investor Reporting

Accounting/Risk systems (if applicable)

4 KPMG, AIMA and MFA, The Cost of Compliance, October 2013.

5 | P a g e

Unfortunately for HFMs, increased costs not only act as a barrier to entry, but they

have also resulted in a significant number of HFM liquidations during and since the

Financial Crisis. For instance, as the demands associated with investor ODD and regulatory

requests have increased, so have the associated expenses. HFMs that have not been able to

adjust for these increased expenses have been forced to liquidate even when performance

has been positive.5

The second barrier to entry (decreased operating budget) is directly related to the

rapid institutionalization of the hedge fund industry over the course of the last few years.

This institutionalization has resulted in a bias in favor of large hedge funds among

institutional investors.6 One of the reasons for this bias is the perception that larger more

established hedge funds are safer and less prone to operational risk. As a result of this

belief, institutional investors are reluctant to invest in smaller HFMs. Institutional investors

are more comfortable investing in the largest hedge funds, because they believe the

operational risk is significantly mitigated by the institutional infrastructure that they have

developed over many years: “Investors have become more educated and more paranoid

since the 2008 crash; they gravitate toward the perception of safety in large hedge funds

that boast long track records.”7 Not surprisingly, it has become much harder for smaller

HFMs to raise assets. Further compounding the problem is the fact that the fees HFMs are

able to charge their investors are being compressed.8 Because of the reduction of fees and

AuM, the amount of capital an emerging or smaller HFM has at its disposal to develop an

institutional quality infrastructure has (in most instances) significantly diminished.

5 The Economist, Hedge Fund Closures: Quitting While They’re Behind, February 18, 2012; Wells Fargo, The Business of Running a Hedge Fund, February 2011. 6 Various studies suggest that iinstitutional investors seem to favor HFMs with an AuM of $5 billion or more. Institutional Investor, Size Matters to Hedge Fund Investors, September 16, 2010. 7 Barron’s, How to Build a Hedge Fund, Saturday, May 25, 2013. 8 Only 42% of single-manager hedge funds are still charging the industry standard “two-and-twenty.” Preqin, 2011, Preqin Global Investor report Hedge Funds, 2011.

6 | P a g e

Similar to the case with increased costs, declining revenues can also lead to a HFM

liquidation event even when returns have been positive. For instance, throughout and

immediately following the carnage inflicted on the hedge fund industry during the

Financial Crisis, many hedge fund managers were forced to liquidate not because they had

the worst performance among their peers, but because they suffered from large investor

redemptions as a result of the “ATM effect”: many investors saw these HFMs as a source of

much need cash to cover for other investments they made with other HFMs that were

suffering larger loses and instituting gates and other restrictive measures. As their AuM

decreased, HFMs that had built their infrastructures based on a traditional fixed cost model

found themselves in a position where the cost of running their business was greater than

the revenue they were producing from the fees they were collecting.9 This situation was

significantly exacerbated for those HFMs that were relying on both management and

incentive fees to pay their expenses.

In the post Financial Crisis era, a HFM will need to develop a business model that

allows it to operate in a manner where the majority of its expenses are variable in structure

and where it can ramp up or scale down its infrastructure as revenues change without

increasing operational risk and economic soundness. It is also critical that this new

business model allow a HFM to do so within the limits of it management fees. HFMs that

do so will be in a better position to survive during periods of contracting revenues (reduced

AuM and fees) and will have a higher rate of survival in the long term. “While performance

and AuM growth are still important levers in the hedge fund business model, they are no

longer foregone conclusions and are not wholly controlled by the hedge fund manager.

Expenses are the only lever the manager can reliably control.”10

In today’s environment, where the costs of running a hedge fund are increasing

dramatically and the average AuM and fees collected are significantly less than they used

to be, HFMs are being forced to do more with less. This reality is not likely to change any

9 Citi Prime Services, Hedge Fund 3.0: A Flexible Operating Model for Building, Managing or Launching a State-of-the-Art Firm, 2011. 1010 Wells Fargo, February 2011.

7 | P a g e

time soon, as the demands associated with compliance, regulatory reporting, and investor

transparency and due diligence will only continue to grow more demanding and

complicated. The HFM will need to find new ways to develop and run their businesses to

meet these increased demands.

Most often it is the responsibility of the HFM’s Chief Operating Officer (“COO”) to

solve for these demands and to develop the institutional quality infrastructure that

investors and regulators require. In the past, this was most often accomplished by hiring a

large number of internal operational staff in coordination with the development of

proprietary technology. However, for the reasons discussed above, this model is no longer

realistic or viable for most HFMs. Thus, the HFM and its COO will need to develop a

different business model to solve for the aforementioned problems. This business model

will need to be multidimensional, will rely on both internal and external resources, and

should be based primarily on a variable cost structure with expenses not exceeding

management fees. A COO that understands these complexities and changing dynamics will

be best positioned to design, implement and manage the institutional quality infrastructure

that today’s hedge fund investors and regulators expect from a HFM in an efficient and

economically prudent manner.

WHAT IS INSTITUTIONAL QUALITY INFRASTRUCTURE AND WHY

IS IT IMPORTANT?

In order to satisfy investors and regulators ongoing expectations for institutional

quality, the HFM must be able to illustrate that it can effectively and efficiently run the

business side of the organization: middle and back office operations; technology

development and maintenance; legal and compliance; finance and accounting; trading;

marketing; human resources; and facilities. Only through the development of an

institutional quality infrastructure will a HFM be able to illustrate to investors and

8 | P a g e

regulators that it has the ability and know-how to manage these functions and the

associated business and operational risks. Institutional quality infrastructure is the

combination and interaction of the following three elements that facilitate and ensure a

robust hedge fund operation: (i) process; (ii) people (knowledge and personnel); and (iii)

technology.

1) PROCESS:

In order to respond to the demands of institutional investors and to be in

compliance with the Advisers Act and other regulatory initiatives, HFMs must develop

and monitor their processes and controls. Most often this is done via the drafting and

implementation of robust policies and procedures across the various functional areas

described above. Strong policies and procedures, among other things, reduce the

reliance on individuals, which in turn, reduces the potential for control failures and key

man risk while also giving investors and regulators greater comfort. Thus, strong

processes and controls will enhance the ability of HFMs to manage operations, satisfy

responsibilities to investors, comply with the applicable regulations and address

unexpected market events.

It is the job of the COO to oversee the drafting, implementation and monitoring of

the HFM’s policies and procedures. The following is a list of some of the policies and

procedures that the HFM will need to have in place in order to demonstrate an

institutional quality infrastructure: valuation; cash management; compliance and code

of ethics; trade errors; insider trading; information security program11; counterparty

monitoring and best execution; corporate action and proxy voting; know your client

(KYC); anti-money laundering (AML); and business continuity and disaster recovery.

11 A robust information security program includes the following policies: IT Acceptable Usage Policy; Data Destruction Policy: Information Security and Cyber-Security Policy; and Incident Response Policy.

9 | P a g e

While HFMs should look to and understand best practices when drafting their

policies and procedures, they will most likely need to customize their policies and

procedures to reflect how they run their business – “one size does not fit all”.12 For

instance, the HFM should not adopt an off-the-rack compliance manual. Adopting

generic compliance policies and procedures without undergoing a thorough review of

operational practices will most likely result in policies and procedures that are overly

burdensome, impossible to implement or result in non-compliance with the adopted

rules. Furthermore, policies and procedures that appear ill-suited or ineffective may

lead the regulatory staff and a prospective investor to conclude that a strong culture of

compliance and/or operational soundness is not a priority of the HFM. Such a

conclusion will both significantly increase the chance of a regulatory exam and

decrease the likelihood of an investment by a prospective investor

It is also important to note that the drafting and implementing of a firm’s policies

and procedures is not a one-time exercise. It is the responsibility of the COO to ensure

that they are routinely tested and updated as needed. Specifically, the HFM will need

to test its policies and procedures periodically (at least annually) to make sure they are

effective and that it continues to be in compliance with the Advisers Act and other

regulatory directives.

2) PEOPLE:

Prior to the Financial Crisis, it was common for a HFM to have a large internal staff

managed by multiple C-level executives (e.g., COO, CFO, GC, CCO, CTO, CRO, CISO, etc.)

to support these functions. This is still the case for many large HFMs that have

significant operating budgets. In contrast, in today’s reality of decreasing budgets, it is

not economically possible for the majority of small and mid-size HFMs to have a large

in house staff and multiple C-level executives to perform and manage the above

12 Managed Funds Association, Sound Practices for Hedge Fund Managers, 2009 Edition.

10 | P a g e

referenced functions. However, in order to develop and support an institutional quality

infrastructure, the HFM will still have to acquire the knowledge and solve for the

responsibilities mentioned above.

It is the job of the COO to solve for this staffing and knowledge issue. In order to

effectively solve for this, the COO will need to perform an internal gap analysis to

determine where within the firm there are internal deficiencies in both knowledge and

man power. Only after this has been accomplished can the COO look externally to

service providers to solve for the deficiencies discovered during the gap analysis. It is

important to recognize that internal deficiencies in skill-set or resources are not

necessarily perceived as a negative by either investors or regulators, as long as the HFM

recognizes them and finds a way to effectively and efficiently solve and manage for

them. By contrast, not recognizing and solving for such deficiencies will likely create

significant issues with investors and regulators. By strengthening their human

resources frameworks, HFMs will not only satisfy investors’ and regulators’ ever-

expanding requirements, but also enhance the effectiveness of their control

environments, the formality of their process and their capacity for growth.

3) TECHNOLOGY:

The need for HFMs to select best of breed technology that is both scalable and

robust in design and functionality has become more important than ever, as they

struggle to meet the technological challenges of increased regulatory compliance and

investor demand for detailed reports. The old way of deploying technology for a

specific purpose and pulling data from multiple systems is inefficient and not easily

scalable. This approach results in duplication of effort and requests, which adds further

costs to the HFM. It also guarantees the continued existence of functional systems and

data silos, preventing HFMs from re-using data held in various repositories across the

firm. Notwithstanding, and perhaps most importantly, the old model is cost-prohibitive

for most small to mid-size HFMs.

11 | P a g e

In order to avoid these issues in today’s competitive environment, HFMs need to take

an enterprise-wide and holistic approach to reviewing their data and technology. The right

technology infrastructure enables HFMs to generate and analyze data quickly, while using

fewer people and reducing the scope for error and inconsistencies. The technology needs

to be flexible and scalable as the business grows and contracts, and must mesh with other

systems to add value and scalability to risk management and middle office and back office

infrastructure. Addressing such technology infrastructure is the COO’s responsibility and

must be part of any firm’s future growth strategy, as it will begin to allow the HFM to

become more efficient and effectively do more with less.

Unfortunately, even the best technology solution cannot solve all of the problems

facing the average HFM today. Knowledge of specific subject matter is also critical. In order

to acquire this knowledge on a limited budget, the HFM will need to establish strong

relationships with best of breed service providers, as this will ensure that they maximize

the power of the technology.

The investment in the development of an institutional quality infrastructure is not a

discretionary buy for a HFM, as the cost of not doing so can be catastrophic and inhibiting

to asset raising and long term business development: “as a hedge fund, if you don't have

the right systems, infrastructure, controls, and back-office functions administered by third

parties, you don't get funded…[a]nd you're out of business.”13 The role that an institutional

quality infrastructure plays in the investment decision making process is further

exemplified in a recent Goldman Sachs investor survey, which states that operational

robustness ranked as equal to track record as the most important factor.14 Also, according

to PAAMCO, their ODD team holds emerging and smaller managers to the same standards

as they do to larger, more established managers, and they will not invest in HFMs that do

not have operational sophistication.15 Finally, a recent ODD survey authored by Deutsche

13 Barron’s, Ray Nolte: A Clearer Window Into Hedge Funds, July 19, 2014. 14 Goldman Sachs Prime Brokerage, Twelfth Annual Hedge Fund Investor Survey 2012, 2012. 15 PAAMCO Viewpoint, The Challenge of Operational Due Diligence on Emerging Managers, Joshua M. Barlow, Associate Director, March 2013.

12 | P a g e

Bank AG found that 70% of the ODD teams interviewed for the survey stated that they now

have explicit veto authority, and that such authority was exercised in almost 10% of the

manager reviews conducted by the respondents to the survey.16 Furthermore, 63% of the

investor respondents will not reconsider investing in a fund that their ODD team has

previously vetoed.17 The survey also states that the trend is for more frequent, more

exhaustive and more comprehensive reviews.

A NEW BUSINESS MODEL:

The traditional business model of developing the needed technology and employing a

large staff to manage it internally to solve for the increased investor and regulatory

demands no longer represents a viable option for most HFMs because of the cost

associated with this model. Similarly, the traditional outsourced or consultant-based model

is also no longer a viable model, because HFMs in today’s world are accountable for every

aspect of their business to both investors and regulators. HFMs need to understand how

their systems work and be able to articulate this to regulators, investors and prospective

investors: the control and ultimate responsibility for all output and decisions remain with

the HFM.

The developing business practice of co-sourcing represents a viable operating model

for most HFMs. Co-sourcing is a practice of service in a business where a service is

performed by staff inside an organization and also by an external service provider. It may

focus on one or more aspects of the internal operational functions of a hedge fund. One of

major advantages of co-sourcing versus outsourcing is that it can reduce risks by bringing

transparency, clarity and better control over the processes outsourced, as the HFM’s specific

policies and procedures can be conveyed and followed. The following chart details some of

the major advantages of co-sourcing over the traditional outsourcing model

16 Deutsche Bank AG, Hedge Fund Consulting Group, Second Annual Operational Due Diligence Survey, Summer 2013. 17 Deutsche Bank AG, Summer 2013.

13 | P a g e

CO- SOURCING OUTSOURCING

CONTROL

The HFM has a dedicated team at the service provider which allows for better control of

resources and output

Non-dedicated team at service provider means the HFM has significantly less control over

resources and output

PROCESS &

PROCEDURES

The HFM’s policies and procedures are followed and

adhered to by the service provider

The service provider follows it own policies and procedures which make it difficult for the

HFM to implement and enforce its policies and procedures

QUALITY

Control over policies and procedures and dedicated team

ensures predictability of workflow and quality and

timeliness of output

Lack of control or input over policies and procedures and team members reduces the

predictability of workflow and quality and timeliness of output

OWNERSHIP &

ACCOUNTABILITY

The HFM and the service provider form a partnership

which builds an overall sense of ownership and

accountability for successes as well as failures

The lack of a strong partnership creates a ownership void and

nominal accountability

KNOWLEDGE

The HFM gathers and retains the knowledge, which can be leveraged and disseminated

within its organization

The service provider (and not the HFM) is the main recipient of the HFM’s organizational knowledge,

and although the transfer of knowledge is possible the

transfer of tacit knowledge is difficult

14 | P a g e

Co-sourcing is about building a partnership with each service and technology provider.

The provider’s team becomes an extension of the HFM’s own staff, rather than acting as a

completely separate entity, which establishes accountability and ownership on the part of

the provider, and an open dialogue and collaboration between the provider and the HFM.

The co-sourcing model emphasizes the involvement of both parties while allowing a firm

to take advantage of best-of-breed technology and the specialized knowledge that its

service providers offer. This access can be acquired at a fraction of a cost of trying to

maintain and build the technology in house and employing teams of relevant subject

matter experts. The following chart and schematic are designed to illustrate what roles

and responsibilities can be co-sourced and how the interaction between the HFM and

service providers works and how the relevant data is shared and processed in the co-

sourcing model.

IN-HOUSE

CO-SOURCE

FUNCTIONAL

AREA FUNCTION PROCESS

PEOPLE / KNOWLEDGE

TECHNOLOGY

FRONT OFFICE:

Trading

Portfolio Management: making decisions about

investment mix and policy, matching investments to

objectives, asset allocation for individuals and

institutions, and balancing risk against performance.

Codified in the firm's constitutional

documents Portfolio Manager

Vendor supported EMS/OMS that has the firm's trading rules and limits programmed into

the system

Pre-Trade Compliance:

involves the management, monitoring and observance

of trading guidelines

Codified in the firm's pre-trade and best

execution policies and procedures

PM, COO and internal staff

MIDDLE OFFICE: Trade Affirmation

Internal staff and

15 | P a g e

Affirming all trade details

with all relevant counterparties on trade

date

Codified in the firm's operational policies and procedures and in the

service level agreements with its

relevant vendors

external staff (Administrator, vendor

managed services solutions, etc.)

A post trade solution that assists in the

affirmation of a trade between counterparties

on trade date via the matching and real time communication of trade

details

Treasury

Cash management and

liquidity risk: The management of the firm’s

cash to ensure the liquidity and maximization of the

firm's cash balances

Codified in the firm's operational policies and procedures and in the

service level agreements with its

relevant vendors

Internal staff and external staff

(Administrator, vendor managed services

solutions, etc.)

A technology solution that provides a user

with a single vantage point to discern,

analyze and optimize rates and cash balances

across all counterparties.

Collateral management and counterparty risk: involves

the monitoring of all aspects of the collateral management function

including collateral valuation, position

valuation, margin calls, response to margin calls and collateral movement

Codified in the firm's operational policies and procedures and in the

service level agreements with its

relevant vendors

Internal staff and external staff

(Administrator, vendor managed services

solutions, etc.)

A rules based technology solution

that provides an overview of: (i)

collateral, collateral values and market positions; and (ii)

processing workflows that include margin calls, response to

margin calls, dispute management, and

collateral reconciliations

Market Risk Management

Codified in the firm's operational policies and procedures and in the

service level agreements with its

relevant vendors

Internal staff and external staff

(Administrator, vendor managed services

solutions, etc.)

A solution that provides market exposures and sensitivities across a

broad range of instruments including, commodities, equities,

fixed income, FX, mortgages and

structured credit, using multiple Value at Risk (VaR) methodologies and flexible stress-

testing.

The management of the financial risk brought about from changes in the market

price of investments

Trade support/settlement

16 | P a g e

Process of monitoring, confirming and resolving

any trade, position or payment break with a

counterparty

Codified in the firm's operational policies and procedures and in the

service level agreements with its

relevant vendors

Internal staff and external staff

(Administrator, vendor managed services

solutions, etc.)

System to help monitor, confirm and resolve any

trade, position or payment breaks with a

counterparty

BACK OFFICE: Asset Servicing

Includes collecting dividends and interest payments, processing corporate actions and

applying for tax relief from foreign governments

Codified in the firm's proxy/corporate actions policies and procedures

Internal staff and external staff

(Administrator, vendor managed services

solutions, etc.)

An automated, rules-based workflow

solution that captures, scrubs and validates

corporate actions, proxy events and other

related activities and security related data

across a large variety of market data vendors

Accounting

Codified in the firm's PPM, valuation and

operational policies and procedures

Internal staff and external staff

(Administrator, vendor managed services

solutions, etc.)

General ledger and/or portfolio management

system

Portfolio accounting:

accounting for the firm's holdings and transactions

NAV calculation: calculation of the daily, monthly and annual net asset value of

the fund

Investor accounting and

allocation reporting: calculate and report on the

fund’s limited partners’ capital allocations of calls,

distributions, gains and losses, and management

fees

Codified in the firm's PPM and subscription

agreement

Investor allocation system

Reconciliations

Daily reconciliation of cash and positions with the

firm's prime brokers and custodians

Codified in the firm's operational policies and procedures and in the

service level agreements with its

relevant vendors

Internal staff and external staff

(Administrator, vendor managed services

solutions, etc.)

T+1 reconciliation engine that reconciles

the firm's cash and positions

ORGANIZATIONAL: Marketing

17 | P a g e

Responsible for the marketing of the firm to

prospective investors

Codified in the firm's operational policies and

procedures and compliance manual and the fund documentation

Internal staff and third party placement agent

CRM solution that allows a firm to manage

its client and partner activities, investment

documentation, research materials and e-mail communications in one central database

Investor Service/Reporting

Responsible for answering investors request for fund

information and for handling investor subscriptions and

redemptions

Codified in the firm's operational policies and

procedures and compliance manual and the fund documentation

Internal Staff

Investor relationship management database that allows the firm to

track, report and communicate on its

investor account activity, liquidity and

performance data

Legal

Internal staff and external staff (Legal

Counsel)

Datahub that captures both the key terms found in the firm's

offering documentation and portfolio of

financial and legal documentation

(including the firm's ISDA, repo and PB docs)

Fund documentation: the

drafting an updating of the fund's constitutional and

offering documents.

Codified in the firm's constitutional

documents

Trading documentation: ensure that the firms

trading documents (PB, ISDA, repo, bank debt, private equity, etc.) are consistent with firm's

mandates and the terms of the document consistent

with best practice and across document type.

Codified in the firm's operational and risk

policies and procedures and the funds constitutional

documentation

Tax

Codified in the firm's constitutional

documents

CFO, COO and external tax counsel

Vendor suppoted tax software

Includes strategies for

optimal onshore and offshore fund structure,

preparation of federal, state and local fund income tax

returns, preparation of Schedule K-1s, reporting to

meet US filings requirements and US tax

reporting obligations, preparation of PFIC

Statements, UBTI and FBAR reporting

Compliance Codified in the firm's CCO, COO, CFO, internal

18 | P a g e

compliance manual and operational policies and

procedures

staff and external consultants

Regulatory reporting: responsible for the

monitoring and production of all regulatory reports

including: i) SEC forms ADV Part 1 and 2, 13F, 13G, 13H and PF; ii) CFTC Form CPO-PQR; iii) IRS FATCA, FBAR and FIN 48; iv) AIFMD and

other international regulatory reporting

requirements

Datahub that allows for a holistic and

centralized regulatory reporting engine.

Compliance monitoring and

training: ensure that all employees are compliant

with the firm's compliance manual and that they are routinely updated on all

compliance related matters. Also includes personal

trade monitoring.

Private cloud based platform that fully

automates the firm's compliance program in one centralized system. Dashboards and flexible

reporting enable easy compliance with

changing regulatory reporting requirements.

Human Resources

Codified in the firm's employment manual,

code of ethics and compliance manual

COO,CCO, internal staff and external HR staff

Private cloud based platform that provides a secure environment for

managing HR issues, such as health and

benefit plan enrollment forms, payroll

processing, employee business and employment

information, etc.

Payroll/Benefits: payroll

preparation and disbursement, tax reporting and the administration of

the firm's benefits and health plans

Human resources

management: administration of issues

such as hiring, terminations, and employment relations

issues

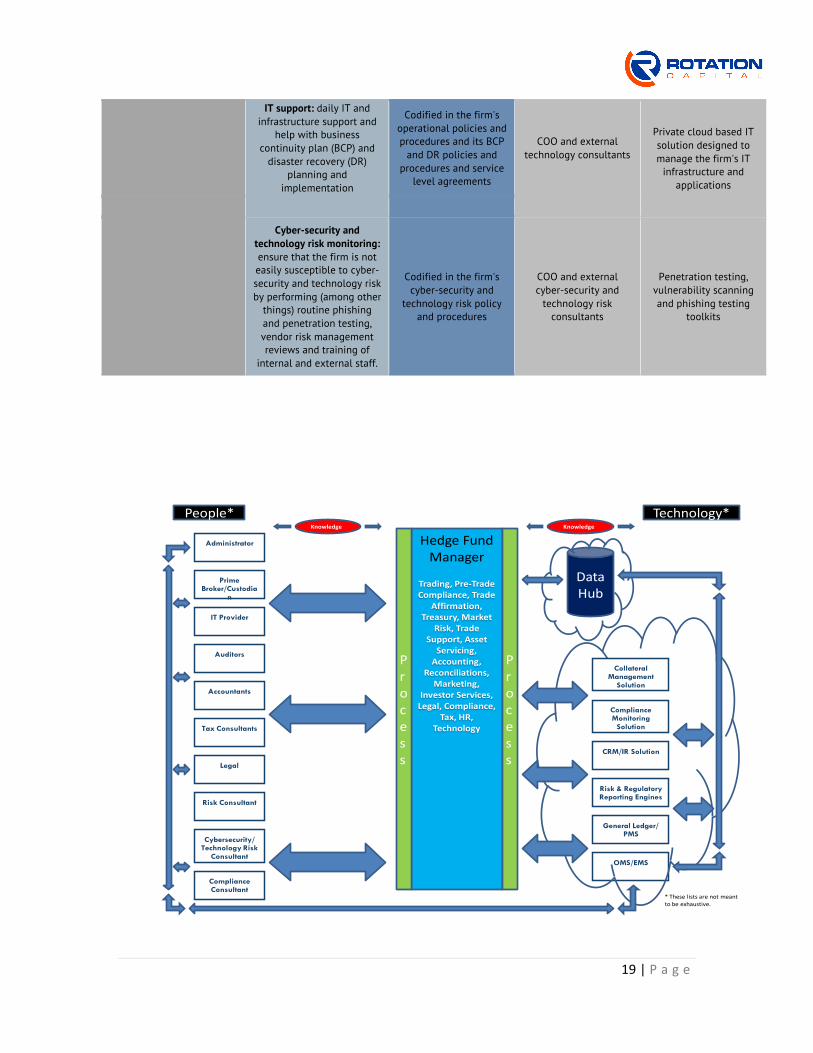

Technology

19 | P a g e

IT support: daily IT and infrastructure support and

help with business continuity plan (BCP) and

disaster recovery (DR) planning and

implementation

Codified in the firm's operational policies and procedures and its BCP

and DR policies and procedures and service

level agreements

COO and external technology consultants

Private cloud based IT solution designed to manage the firm's IT

infrastructure and applications

Cyber-security and

technology risk monitoring: ensure that the firm is not easily susceptible to cyber-security and technology risk by performing (among other

things) routine phishing and penetration testing, vendor risk management reviews and training of

internal and external staff.

Codified in the firm's cyber-security and

technology risk policy and procedures

COO and external cyber-security and

technology risk consultants

Penetration testing, vulnerability scanning and phishing testing

toolkits

Process

Process

Hedge Fund Manager

Trading, Pre-‐Trade Compliance, Trade

Affirmation, Treasury, Market

Risk, Trade Support, Asset Servicing, Accounting,

Reconciliations, Marketing,

Investor Services, Legal, Compliance,

Tax, HR, Technology

IT Provider

Knowledge

Auditors

Accountants

Tax Consultants

Legal

Risk Consultant

Compliance Consultant

Cybersecurity/ Technology Risk

Consultant

Prime Broker/Custodia

n

Administrator

People* Technology*

OMS/EMS

Knowledge

General Ledger/ PMS

CRM/IR Solution

Compliance Monitoring

Solution

Risk & Regulatory Reporting Engines

DataHub

Collateral Management

Solution

* These lists are not meant to be exhaustive.

20 | P a g e

Expense management is another benefit of the co-sourcing model. For instance,

through the use of a co-sourced model, a HFM can reduce its fixed expenses by shifting

the burden of managing many high-expense activities (technology development, staffing,

etc.) from its own P&L to a third party service provider. This model is more cost-efficient

and flexible, as it can be scaled up or down depending on the fund’s performance, AuM and

business needs without increasing operational risk. This model also takes advantage of

economies of scale, which allows a HFM to be nimble and enables it to adapt quicker as

opportunities arise.

21 | P a g e

CONCLUSION:

In order for an HFM to attract monies from institutional investors or perform

successfully during the inevitable regulatory exam, an HFM must possess the institutional

qualities and infrastructure that investors and regulators are looking for. Institutional

quality infrastructure is a combination of process, people (knowledge and personnel) and

technology. It is the job of the HFM’s COO to develop a business plan that successfully

integrates these three components in a cost effective and efficient manner. If implemented

correctly, the business plan will lead to the development of an institutional quality

infrastructure that can handle both investor ODD requests and regulatory scrutiny. The

emerging business model known as “co-sourcing”, which is based in part on the

development of strategic partnerships with service providers that possess the needed

specialized knowledge and best of breed technology, enables an HFM to develop

institutional quality infrastructure in a cost efficient and economically responsible manner

by shifting from a predominately fixed cost base model to a variable cost base model. It is

a way for the HFM to solve for the problem of having to do “more with less” and helps to

overcome the significant barriers to entry of increasing costs and decreasing budgets facing

the majority of HFMs today.