Embed Size (px)

Citation preview

TEMENOS NEWSThe Banking Software Company

Barrie Neill, Temenos, highlights areas to consider for success in mobile banking

Youthful mobilityExamining the association’s role in the future of banking

BIAN

• The road to Rome – Temenos Client Forum 2008 • Against the grain • Risky business • Online challenges • Wishes, buses and wise men • The three pillars of Islamic private banking • Database spotlight – on the bench

ISSUE 18 NOVEMBER 2008

Scaling new heights in retail bankingThe future of retail banking operations – reaching out for greater development and growth

TEMENOS HEADQUARTERS SA18 Place des PhilosophesCH-1205 GenevaSwitzerlandTel: +41 22 708 1150Fax: +41 22 708 1160www.temenos.com

©2008 TEMENOS HEADQUARTERS SA – all rights reserved. Warning: This document is protected by copyright law and international treaties. Unauthorised reproduction of this document, or any portion of it, may result in severe and criminal penalties, and will be prosecuted to the maximum extent possible under law.

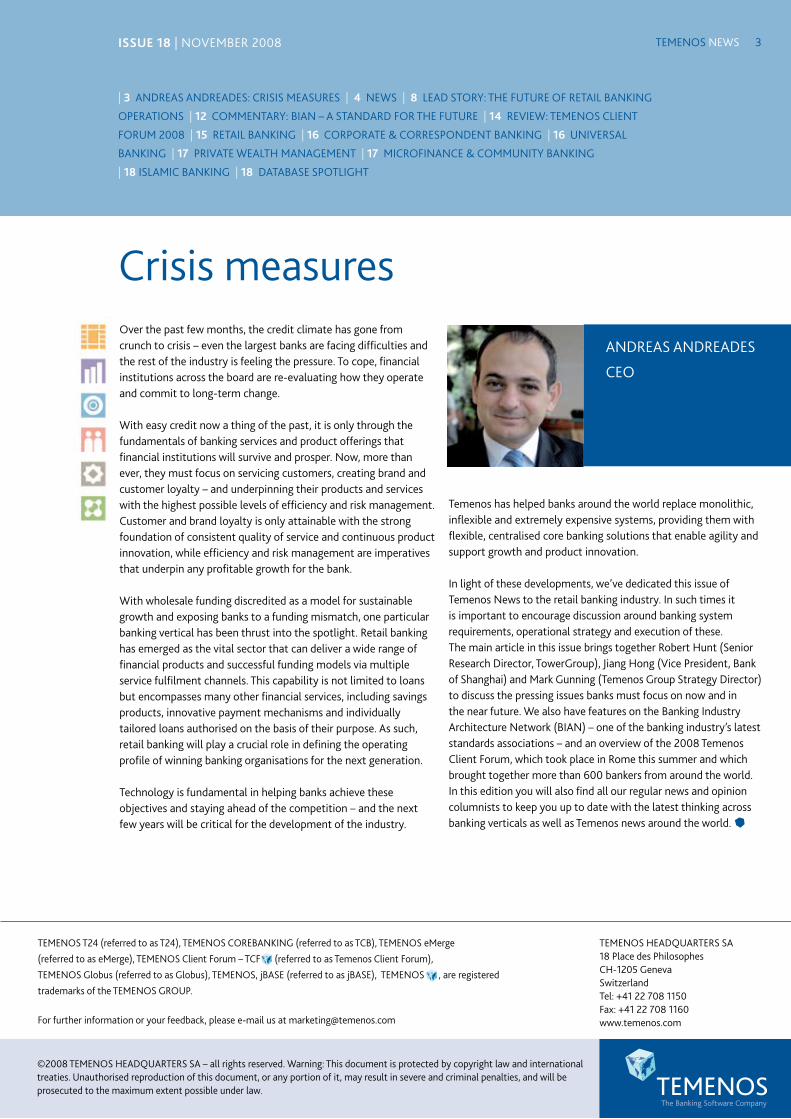

Over the past few months, the credit climate has gone from crunch to crisis – even the largest banks are facing difficulties and the rest of the industry is feeling the pressure. To cope, financial institutions across the board are re-evaluating how they operate and commit to long-term change.

With easy credit now a thing of the past, it is only through the fundamentals of banking services and product offerings that financial institutions will survive and prosper. Now, more than ever, they must focus on servicing customers, creating brand and customer loyalty – and underpinning their products and services with the highest possible levels of efficiency and risk management. Customer and brand loyalty is only attainable with the strong foundation of consistent quality of service and continuous product innovation, while efficiency and risk management are imperatives that underpin any profitable growth for the bank.

With wholesale funding discredited as a model for sustainable growth and exposing banks to a funding mismatch, one particular banking vertical has been thrust into the spotlight. Retail banking has emerged as the vital sector that can deliver a wide range of financial products and successful funding models via multiple service fulfilment channels. This capability is not limited to loans but encompasses many other financial services, including savings products, innovative payment mechanisms and individually tailored loans authorised on the basis of their purpose. As such, retail banking will play a crucial role in defining the operating profile of winning banking organisations for the next generation.

Technology is fundamental in helping banks achieve these objectives and staying ahead of the competition – and the next few years will be critical for the development of the industry.

Crisis measures

Temenos has helped banks around the world replace monolithic, inflexible and extremely expensive systems, providing them with flexible, centralised core banking solutions that enable agility and support growth and product innovation.

In light of these developments, we’ve dedicated this issue of Temenos News to the retail banking industry. In such times it is important to encourage discussion around banking system requirements, operational strategy and execution of these. The main article in this issue brings together Robert Hunt (Senior Research Director, TowerGroup), Jiang Hong (Vice President, Bank of Shanghai) and Mark Gunning (Temenos Group Strategy Director) to discuss the pressing issues banks must focus on now and in the near future. We also have features on the Banking Industry Architecture Network (BIAN) – one of the banking industry’s latest standards associations – and an overview of the 2008 Temenos Client Forum, which took place in Rome this summer and which brought together more than 600 bankers from around the world. In this edition you will also find all our regular news and opinion columnists to keep you up to date with the latest thinking across banking verticals as well as Temenos news around the world.

TEMENOS NEWS �

| 3 ANDREAS ANDREADES: CRISIS MEASURES | 4 NEWS | 8 LEAD STORY: THE FUTURE OF RETAIL BANKING

OPERATIONS | 12 COMMENTARY: BIAN – A STANDARD FOR THE FUTURE | 14 REVIEW: TEMENOS CLIENT

FORUM 2008 | 15 RETAIL BANKING | 16 CORPORATE & CORRESPONDENT BANKING | 16 UNIVERSAL

BANKING | 17 PRIVATE WEALTH MANAGEMENT | 17 MICROFINANCE & COMMUNITY BANKING

| 18 ISLAMIC BANKING | 18 DATABASE SPOTLIGHT

ANDREAS ANDREADES

CEO

TEMENOS T24 (referred to as T24), TEMENOS COREBANKING (referred to as TCB), TEMENOS eMerge

(referred to as eMerge), TEMENOS Client Forum – TCF (referred to as Temenos Client Forum),

TEMENOS Globus (referred to as Globus), TEMENOS, jBASE (referred to as jBASE), TEMENOS , are registered

trademarks of the TEMENOS GROUP.

For further information or your feedback, please e-mail us at [email protected]

ISSUE 18 | NOVEMBER 2008

TEMENOS NEWS4

“The acquisition underscores both our ambition and the potential for Temenos to lead the core banking software market over the long term.”Andreas Andreades, CEO, Temenos

Temenos has acquired software vendor Financial Objects. Andreas Andreades, Chief Executive Officer, Temenos, says: “The combination of Temenos and Financial Objects creates a group that is bigger, stronger and more profitable

Temenos acquires Financial Objectsand, therefore, better placed to take advantage of the significant market potential that exists for third-party core banking software.

“This is a value-enhancing deal for our shareholders – even before any cross-selling revenues, we expect the acquisition to materially enhance our 2009 earnings. Following on from the Informer acquisition in July and the Actis.BSP deal in 2007, we are demonstrating that we can and will continue to successfully complement strong organic growth without compromising shareholder value or losing focus. This underscores both our ambition and the potential for Temenos to lead the core banking software market over the long term.”

Bank of Shanghai goes live with TEMENOS T24 to support retail banking operations and 11 million accounts

Bank of Shanghai, one of the largest city commercial banks in China, has gone live with TEMENOS T24 (T24) across its entire retail banking operation in September 2008. T24 had already been supporting the bank’s corporate banking, trade finance and treasury divisions, and the system now supports approximately 11 million customer accounts, 245 branches and up to 2.5 million transactions per day.

Jiang Hong, Vice President, Bank of Shanghai comments: “This successful implementation signifies a pivotal point in the bank’s development. Our long-term business strategy is to become a truly international bank with global scope. T24’s scalability and open systems architecture will enable us to standardise our processes and manage more than 11 million customer accounts from one central point. It also provides us with unrivalled scalability to support our retail operations. The system’s rich functionality means we can deliver cutting-edge integrated product and services offerings to both existing and new markets.”

Votorantim Bank, a rapidly growing financial institution based in Brazil, has gone live with TEMENOS T24 (T24). T24 supports the bank’s international wealth management operations. The bank went live in March 2008 and represents Temenos’ first client in Brazil. Votorantim employed Temenos Professional Services including Temenos Application Management and jointly delivered a complete international wealth management system in just seven months. With T24, the bank plans to support its international treasury, asset management, private and lending

Votorantim Bank goes live with TEMENOS T24 Model Bank in just seven months

(cars and mortgages) operations. Reinaldo Lacerda, Wealth Manage-

ment and Product Director, Votorantim Bank, says: “With T24 supporting our business, we have the front-end capabilities, modular integration, asset management support and the scalabil-ity we need. We can now expand our customer base without increasing our costs or operational risk. We will also take advantage of the improved workflows and rapid deployment of new products enabled by T24 to help increase our competitive advantage and market share.”

TEMENOS NEWS 5

“We recognise that having the most robust technology capabilities possible will be a key driver in achieving our goals.”

JPMorgan, a full-service provider of cash management, trade finance, and treasury solutions, announced that it will make a US$�0 million technology investment to implement a centralised operating platform supporting expansion of the bank’s global treasury management and liquidity services businesses.

This core banking solution will bring uniformity to the firm’s product offerings, enable JPMorgan to offer a consistent set of services across the world, and use robust infrastructure to deliver richer data and real-time reporting to clients. Work has begun to deploy the platform with pilot schemes planned for later in 2008.

JPMorgan will work with Temenos, a global provider of banking software systems, to implement the platform. In addition to this US$�0 million commitment, the firm will make additional significant technology investments to support international expansion.

Sue Webb, Executive Vice President, Global Core Cash Management, JPMorgan Treasury Services, says:

JPMorgan commits US$�0 million to implement central platform for global services

“The global marketplace is where we expect to see significant growth in our business, and we recognise that having the most robust technology capabilities possible will be a key driver in achieving our goals. We are making a significant investment in our technology to support our clients’ businesses around the world. Working with an industry-leading software provider such as Temenos will enable us to meet our clients’ evolving needs, regardless of where they do business.”

An Binh Commercial Joint Stock Bank (ABBANK), one of Vietnam’s largest joint-stock banks by chartered capital, has become the seventh client in the country to go live with TEMENOS T24 (T24). T24 now provides the bank with centralised core banking across its retail and corporate banking operations in 57 branches and is helping the bank to launch a range of new delivery channels, including ATM and internet banking.

ABBANK implemented T24 Model Bank to reduce its implementation time and costs, minimise customisation and lower project risk. Nguyen Hung Manh, Vice Chairman of ABBANK, says: “Because T24 Model Bank is a proven technology, we have been able to benefit from a fast, low-risk implementation. We are now ready with a platform that will support the bank as it launches new delivery channels to help us achieve rapid business growth over the next two years.”

An Binh Bank goes live with TEMENOS T24 Model Bank in 57 branches

Al Wasatah Al Maliah, a newly established Islamic brokerage and investment house, has become the first non-bank-backed financial investment services company in the Kingdom of Saudi Arabia to implement TEMENOS T24 (T24). Al Wasatah Al Maliah signed with Temenos in February 2008 with a go live date scheduled for mid-2008. T24 will support all the company’s operations in Saudi Arabia and the Gulf Corporation Council (GCC) states.

Al Wasatah Al Maliah selects TEMENOS T24 Model Bank to support new e-brokerage

Bassam Bin Gheshian, Chief Operating Officer, Al Wasatah Al Maliah, says: “Our aim is to become a leader in the Islamic e-brokerage sector. We chose Temenos because we feel that it delivers the best technology on the market. T24 Model Bank will help us position our products and services in a way that will make them convenient and readily available to all investors. This is a crucial part of our commitment to nurturing our clients with a view to helping them develop into well-informed, profitable investors.”

Sue Webb, Executive Vice President,

Global Core Cash Management,

JPMorgan Treasury Services

TEMENOS NEWS6

“A critical element in our decision to implement T24 was the oppor-tunity to have Metavante host the application and integrate it with the broader set of services Metavante currently provides the bank.”

Frank Trotter, President, EverBank Direct

EverBank Financial Corporation, a Metavante core processing client, has selected TEMENOS T24 (T24) to support its World Markets division. The deal represents the first T24 opportunity resulting from the extended Metavante–Temenos strategic marketing alliance announced on �1 July 2008.

T24 will be implemented and hosted by Metavante and will support the bank’s World Markets global trading (including foreign exchange) and commodities operations. T24 will replace several in-house systems and support the continued development and delivery of innovative multi-currency and metals-based products and services. Frank Trotter, President, EverBank Direct, says: “We needed a system that would fully support our growth objectives. A critical element in our decision to implement T24 was the opportunity to have Metavante host the application and integrate it with the broader set of services Metavante currently provides the bank.”

Andreas Andreades, CEO, Temenos, says: “As the first contract under our joint T24 marketing agreement with Metavante, this is a very exciting development.”

Temenos and Metavante sign EverBank as first joint T24 marketing client

Following impressive growth in Central & Eastern Europe, we have enhanced our regional capabilities. Customers and prospects will now be supported by an expanded sales and pre-sales team, boosted by a number of new joiners following the acquisition of Informer Group in the region. We are also equipped to provide training facilities and courses for existing and prospective customers on all T24 modules.

Temenos expands capabilities in Central & Eastern Europe

To support this growth and future plans Temenos Greece has relocated to a new office in the heart of Athens’ business district. This large, highly-equipped office already provides a base to our sales, pre-sales, services, finance and support functions. Additionally, our Sofia office has been fully operational from 1 September 2008 and we now also have another office in Bucharest.

Temenos acquires Informer Group assetsTemenos has signed an agreement to acquire the core banking assets of Informer Group for US$40.� million in cash and shares. The transaction is expected to be accretive to adjusted EPS by US$0.02 in 2008 and by US$0.08 in 2009.

Informer SA, a listed provider of software and services for core banking, has been an authorised licensor and systems integrator for Temenos in Greece, Eastern Europe, the Balkans and the Middle East since 1995. Through the acquisition, Temenos will gain an expanded footprint in these markets and also immediate entry into Romania and Egypt, where Informer already has an established presence.

Metavante Technologies, Inc. and Temenos have expanded the strategic alliance previously announced in March 2007, and have begun the joint marketing of TEMENOS T24 (T24) to foreign financial institutions in the US. The highly specialised international institutions will benefit from Metavante’s extensive US banking knowledge and over 40 years’ experience in the US banking industry as well as gain access to T24, the internationally recognised market leader of global banking systems. Metavante will provide T24 in an outsourced environment, along with providing integration, implementation and support services,

Metavante and Temenos establish joint marketing strategy to sell T24 in the USwhile Temenos will provide licensing, enhancement, support and consulting services.

Alex Groenendyk, President of Temenos Americas, says: “We’re pleased to expand our relationship with Metavante and accelerate the growth of our T24 international banking system to US-based subsidiaries of international banks. By leveraging Metavante’s strong banking relationships, distribution network and hosting capabilities, Temenos is uniquely positioned to tap into the growing foreign banking market in the US.”

TEMENOS NEWS 7

As part of our ongoing commitment to innovation in the banking sector, Temenos, in partnership with OpusCapita and Mors Software, organised the highly successful Innovative Banking Forum 2008 in Stockholm earlier in 2008. Hosted by Temenos’ customer Swedbank, it was an opportunity for more than 50

Temenos staying ahead of the market at the Nordic Innovative Banking Forum 2008

Bank Standard, the largest, non-govern-ment- backed bank in Azerbaijan, has become the first bank in the country to go live with TEMENOS T24 (T24). T24 now provides it with centralised core banking capabilities across its retail, treasury and internet banking operations. The system – which went live in June 2008 – has been implemented at the bank’s branch in Baku, Azerbaijan, with a further 1� sites, including the head office, to go live later in the year. The system was implemented by Temenos’ Moscow-based team, which brought local expertise to the process.

Salim Kriman, Chairman at Bank Stand-ard, says: “We realised very quickly that our existing system was preventing growth because of a lack of global standards. As well as expanding the business, we wanted to establish best practice proc-esses. As an internationally established system, T24 is instrumental in helping

Bank Standard in Azerbaijan goes live with TEMENOS T24

attendees to meet leading players in the Nordic financial market, examine cutting-edge developments and discuss banking issues and trends that keep this region at the forefront of technology.

Rowan Gibson, bestselling author and global business strategist, gave a keynote speech on strategies for growth and industry reinvention, while Lindsay Baldock, Strategy Manager at Temenos, presented the advantages of a pre-configured T24 Model Bank solution. With universally positive feedback from attendees and significant progress with a number of prospects following the event, we are pleased to be committed to supporting our customers and to help shape the future of banking strategies.

“As an internationally established system, T24 is instrumental in helping us introduce global standards into our business.”Salim Kriman, Chairman, Bank Standard

Temenos launches regional websitesTemenos now has three local websites for the German, Chinese and Japanese markets. All three sites are in local languages and offer information on the Temenos products and services available in those regions. Additional country-specific Temenos websites will be launched in the coming year. They can be accessed through Temenos.com

Honda Bank GmbH integrates loan operations using TEMENOS T24

Honda Bank GmbH has chosen TEMENOS T24 (T24) to integrate its existing loan operations, which consisted of four disparate systems. The bank required a flexible system that would merge its fragmented infrastructure with minimum disruption to the business. T24 will provide a front-to-back office core banking platform to support the bank’s finance loan service, as well as front-office capabilities for its wholesale finance operations. The bank also chose TEMENOS ARC Internet Banking (ARC-IB), and the T24 Arrangement Architecture Module to help improve the bank’s competitive position in the market by delivering improved customer centricity into its business model.

Andreas Andreades, Chief Executive Officer of Temenos, comments: “Honda Bank is an important win for Temenos because it signifies our continued growth in the German market and the flexibility and ease of deployment of our T24 Model Bank in other sectors such as automotive finance, as well as in mainstream banking operations.”

us introduce these global standards into our business.”

Based on this implementation, Temenos has created the Model Bank platform for Azerbaijan, which will be used as a standard for further implementations in the country. Temenos has secured two further wins in the region with its successful Model Bank for Azerbaijan.

Jiang Hong (JH)Vice President, Bank of Shanghai In China, over the past five years, people have accumulated significant wealth. As a result, retail customers are not satisfied with the low-yield deposits products and banks have had to develop many innovative new wealth products with varied risks and yields. The credit card and personal loan businesses are booming and there is intense competition to attract both high-end and low-end customers. Banks are offering many co-branded credit-card products to attract customers.

At the same time, with the opening of the foreign currency market, many new currency settlements and financing products – such as renminbi (currency of the People’s Republic of China) and foreign currency swaps – are offered. We also see competition for high-end customers becoming intense. Banks are setting up individual wealth management centres to offer customer-oriented services. These teams are committed to the design and development of specialised financing services that cater for a wide range of customer needs.

HOW HAVE RETAIL BANKING PRODUCTS AND SERVICES CHANGED IN THE PAST SIx YEARS?

Robert Hunt (RH)Senior Research Director, TowerGroup There has been phenomenal growth in mobile banking, which is now becoming a worldwide delivery channel for banking and represents further opportunity for growth. Another dramatic change over the past several years has been the rise of Islamic banking, allowing millions of Muslims access to Shar’ia-compliant banking products.

Microfinance is another key area of growth, with millions of people gaining access to credit. We now foresee a shift from microfinance as a product offered by small non-profit organisa-tions to a product offered by leading global banks. This economic inclusion is improving the standard of living and the quality of life for people around the world.

The future of retail banking operations

TEMENOS NEWS8

Three perspectives on trends in the retail sector

RoBERT HUnTRobert Hunt is a Senior Research Director specialising in core banking and transaction processing systems for TowerGroup. His research is published within TowerGroup’s Retail Banking practice. Before joining TowerGroup, Robert held senior management positions as Director of Technology Banking for BankBoston, Managing Director of BayBank Systems, Inc., and Senior Vice President at the Irving Trust Company.

As one of the largest sectors of the financial services industry, retail banking is at the forefront of innovation. Temenos News asked three industry experts to comment on recent changes, current developments and future trends.

RH: Banks will develop a broader range of services and products to reach new market segments. This includes a greater focus on relationship products that address all the financial needs of a market segment, rather than offering just specific savings or loan products. On a global basis, green banking is becoming more important, with the delivery of electronic customer statements and notices. But it’s not just about green banking, it’s about customer choice. In the future we’ll see customers virtually designing the product they want and choosing how it’s delivered. A bank that can respond to this product demand will have a competitive advantage.

MG: There will be some element of product innovation and a clear reduction in prices. Banks will also find themselves under greater pressure to deliver services – resulting in a concerted effort to improve customer service. This will cause a shift towards service personalisation – where banks will have to target their services to each customer’s requirements.

In many regions, banks are going back to basics. Innovation is being stamped on, because the economic downturn means they can’t afford it. The biggest innovations over the coming years may come from outside the banking sector, from telcos, for example, which have the infrastructures in place for payments and communications. Banks need to prepare themselves to be responsive to these competitors by ensuring they have the right core banking system at the heart of their business.

WHAT DOES THIS MEAN IN TERMS OF BANKING OPERATIONS AND THE TECHNOLOGY TO SUPPORT THEM?

MG: Because of increasing competition over prices, banks will be looking to reduce internal costs, so they can compete on price with new entrants to the market who have better technol-ogy and a narrower proposition to the customer.

Banks will also continue to increase automation. Looking forward, they’ll realise that they need to rationalise their structure around more efficient IT architectures.

Mark Gunning (MG)Group Strategy Director, TemenosThere are a few main areas of change. There have been changes in the diversity and importance of different delivery channels. Internet and mobile banking are becoming increasingly important to clients and they expect to see seamless delivery across all channels. We’ve also seen specialist competitors such as overseas organisations or non-banks entering the market and using their brand to sell into banking.

There is also an increased commoditisation of services and products, which are now being brought to market faster. Banks need to industrialise their product delivery processes because their competitors can copy what they are doing fairly quickly.

WHAT DRIVERS ARE EMERGING NOW THAT WILL CHANGE RETAIL BANKING IN THE FUTURE?

RH: There are two connected factors here. One is growing economies – we’re seeing a big expansion of the middle classes in countries like India, China, Russia and Brazil, all of which have huge populations. There will be a billion new banking customers in the market over the next five or six years. Over the same period, banks in developed economies will be targeting new products to minority groups. In the US, for instance, there has been tremendous growth in the Hispanic population – and the wealth of this group is increasing. The second key area is climate change. There will be a global energy conservation movement, including more people working and banking from home and an emphasis on electronic delivery of information to reduce the use of paper.

JH: With the further opening-up of the financial services industry in China, foreign banks are now permitted to conduct renminbi business. This will intensify competition for high net worth clients. There is increased awareness of wealth management and growing demand for better financial services and products. This is creating commercial banks with more market opportunity.

As the global economy slows down, banks will focus more on fee-based business to sustain and improve their profitability. In the future, the renminbi will become convertible and this loosen-ing of foreign exchange controls will have great impact on personal foreign exchange services.

MG: We will definitely see decreasing customer loyalty and increased competition, particularly on price. And there will be further regulatory changes in some core areas of retail banking profitability such as payments. There will be more developments such as the UK faster payments initiative and SEPA. To deal with these changes, banks will focus on the areas of the business that they consider to be core competencies. They won’t want to do the operations work behind the scenes, so there is an opportunity to contract out that activity by adopting an ASP model or establishing a shared services model among banks.

Larger banks will also start to break into the microfinance market. Previously, the banking business model was too expensive to serve this market. Now, there are other methods banks can use, such as scaled down branches with remote service centres, or mobile banking, which is a good example of using technology to lower costs and address an issue.

HOW DO YOU SEE RETAIL BANKING PRODUCTS AND SERVICES CHANGING IN RESPONSE TO THOSE DRIVERS?

JH: Banks have to set up customer-oriented core banking business systems. The core banking system provides a solid foundation for retail banking financial product innovation, such as establishing a renminbi and foreign currency integrated business platform and delivering multi-currency, multi-account products.

Chinese banks are also keen to strengthen customer relationship management. A key step in achieving this will be to obtain effective customer information from the data warehouse and focus on the analysis of customer needs to improve customer acquisition and retention.

TEMENOS NEWS 9

JIanG HonGJiang Hong is Vice President of the Bank of Shanghai. As the founder of the bank’s IT department, he takes responsibility for all IT and product development operations and is at the heart of growing its e-banking and credit-card businesses. Mr Jiang Hong’s experience also includes a successful academic career at China’s National University of Defense Technology.

MaRK GUnnInGMark Gunning was appointed Group Strategy Director of Temenos in June 2005 and is responsible for overall product strategy. He joined the company in 199� and has represented it in various capacities related to development, client services and sales. He has also been Regional Manager for North America.

TEMENOS NEWS10

“We believe that large banks will need to rely more on leading systems integrators and software providers to achieve a modern and flexible operating environment.”Robert Hunt, Senior Research Director, TowerGroup

CA

SE S

TUD

Y BANK OF SHANGHAIA joint stock commercial bank ranked among the top 500 banks worldwide, Bank of Shanghai has over 10 million accounts, around �,000 users and more than 220 branches.

As part of its commitment to innovation, the bank decided to replace its existing, multiple, core banking solutions with a single, more efficient technology. Transparency was a key requirement. The bank’s legacy systems only permitted staff to look at the business on an account-by-account basis, preventing a holistic approach.

Over a two-year period, the bank replaced its separate retail, corporate, treasury and trade finance systems with TEMENOS T24 (T24). It now has a customer-centric view of its business, increasing its ability to strengthen the management of both credit and operational risk. T24 also provides the bank with a safe and efficient authorisation process, allowing straight-through processing of even the higher risk products.

Much of that will be based on SOA. Banks are also moving towards standards, and Temenos has joined the Banking Industry Architecture Network (BIAN) to be at the forefront of this.

JH: To cope with the rapid rate of change in the retail banking market, banks will need a core banking system that will help them adjust products and workflows. This means having rapid parameterisation capabilities as well as flexible development tools that banks can use to create new products, channels and processes quickly. This is especially crucial for interfaces. Bank of Shanghai has achieved this by adopting advanced international banking concepts and industry standards. This has strengthened our ability to deliver international standard services to customers and made it easier for us to seize the latest international business opportunities and enhance business workflow accordingly. It also helps us create and launch new products to the market quickly, maximising our ability to compete on the world stage.

RH: We have a lot of banks that are still operating inflexible and difficult to maintain core systems. If these banks want to offer new products and services to a greater number of people, they have to become more efficient. This includes

straight-through, real-time processing capabilities and the ability to implement new, more complex banking products rapidly. Banks still using legacy core banking systems will have to develop and implement core systems modernisation plans to remain competitive.

Banks also need to improve their electronic messaging capabilities for better customer communications. Customers want information from their banks – but only if that information is valuable to them and delivered in a manner that they choose. Banks, then, need to build into their customer systems the information customers want, when they want it, and how they want it delivered.

WHERE DO YOU SEE TECHNOLOGY EVOLVING TO SUPPORT FUTURE RETAIL BANKING BUSINESS AND OPERATIONAL MODELS?

RH: Banks need to develop an IT infrastructure that can respond quickly to new requirements for products and services while maintaining a highly efficient and scalable operating environment. We believe that large banks will need to rely more on leading systems integrators and software providers to achieve a modern and flexible operating environment.

JH: At the moment, it’s hard to find truly standardised core banking products. This will change over the next few years, as banks begin to establish international hardware and software standards for the industry. Additionally, SOA-based development promises to become more widely used – giving banks an opportunity to support their businesses more flexibly.

MG: Banks need an agile environment in the long term. They want IT support that is efficient and adaptable. As the rate of change speeds up, they will need a modern IT environment that can process business efficiently now and adapt to all the changes they may demand of it tomorrow.

Agility is the key. T24 is highly flexible, so you can change the product without resorting to code. It’s open – we don’t tie people to one particular platform. All the functionality can be exposed to other services and applications within or outside the bank. So a lot of the fundamental characteristics of the banking system that you need are already there. We’re working closely with the Temenos Management Consultancy group to help define banking processes, and our membership of BIAN will provide another dimension, helping banks to be agile and use standards as they materialise.

TEMENOS NEWS 11

Visit us on Stand S06

ü View TEMENOS T24™ & scanned images

direct from TEMENOS T24™

ü Uses standard TEMENOS T24™ enquiry

screens

ü Allows faster customer query resolution,

validity checks, and fi nancial analysis

ü Seamless integration

www.efstechnology.com

For more information

please email

View Documents from TEMENOS T24™

AutoFORM LaserNet T24 Archive Link

Temenos_advert_feb08_t24.indd 9/30/2008, 12:39 PM1

BIAN – a standard for the futureThe Banking Industry Architecture Network (BIAN) is one of the latest industry bodies to hit the press. With so many different acronyms around, deciphering them all – and establishing their value – can be difficult.

BIAN was established in 2008 by leading global banks, including Deutsche Bank, Credit Suisse, ING,

Deutsche Postbank, Standard Bank and Zürcher Kantonalbank. An independent body committed to the promotion and development of industry standards suitable for SOA, its founding membership also includes forward-thinking technology vendors with strong footings in the financial services sector, such as Temenos, Microsoft, SAP, SunGard and SWIFT.

The association’s main objective is to ease the journey of banks moving to an SOA by building a community that will openly share domain and technical expertise in the application of SOA principles and methodologies. As part of this process, financial institutions, software vendors, service providers and technology partners are invited to join the association to play a collaborative role among other industry leaders towards the definition, building and implementation of next-generation banking platforms.

Ultimately, BIAN will help create a common vision for the industry, one that will assist banks – and technology vendors – in making successful changes as efficiently as possible. Standards you can bank on The benefits of BIAN are clear. Koen van den Brande, Worldwide Core Banking Industry Manager, Microsoft, says: “The increased use of standards will help banks lower the cost and risk of change.” This is especially crucial for larger banks that need to take a gradual approach to core renewal. Often, SOA will be their migration method of choice – a trend that makes standards invaluable for success. Crucially, BIAN encourages banks to be clear about their aims. It provides a framework for them to discuss issues such as what a services landscape should look like, as well as the services and capabilities they want to support their business. Although BIAN – and the introduction of new standards it promotes – will have the most immediate benefit for large retail banks, it also promises to make technology more accessible to smaller financial institutions.

There are benefits for vendors too. By providing a forum for banks to clarify their needs, the committee gives vendors an opportunity to develop their solutions in line with industry needs. BIAN members Temenos and Microsoft are clearly excited by this two-way, consensual approach.

As one of the technology industry’s largest players, Microsoft has a lot to bring to the table, including an extensive partner ecosystem and the ubiquity needed to drive standards. It has already been instrumental in establishing web services standards that are ideal for SOA. Van den Brande says: “Membership of BIAN is important for us because, as a responsible member of the industry, we have to work towards achieving what the industry needs. By extension, the benefit for vendors is that they receive first-hand information that will help them develop solutions that are more effective and cost-efficient than the systems banks could develop in-house.”

Helping to establish an independent association such as BIAN is part of Temenos’ ongoing commitment to industry standards, its support of SOA and its dedication to the retail banking market. Barrie Neill, Retail Banking Strategy Manger, Temenos, says: “BIAN is a really positive move for the industry because it will help drive forward the use of standards – and, by extension, SOA. Temenos has a crucial role to play here, because our products are already SOA-ready and we have valuable expertise and experience to offer. For us, establishing an active participation in BIAN is a strategic move that increases our ability to support clients with larger retail banking operations that are implementing SOA. It also gives us an opportunity to take our strategy to the next level by actively contributing to the development of standards. This puts us in an even stronger position to ensure that our products continue to support SOA.” An unbiased perspective The analyst community also has its views on BIAN. Robert Hunt, Senior Research Director at TowerGroup thinks that the rising cost, not only of developing and implementing new systems but also of maintaining them, is bringing things to a head. He sees BIAN as the next stage in a decade-long process that has included the creation of IFx and other messaging and payments standards. Hunt says: “I think BIAN is great for the industry. What we have today is a technology Tower of Babel – systems written at different times using different software structures and sometimes different programming languages. This results in systems that are difficult and expensive to maintain and prevents banks from

12 TEMENOS NEWS

The Banking Industry Architecture Network is being hailed in the press as the latest victory in the battle for workable industry standards. But what is its real significance for banks and technology vendors? Temenos News investigates, and asks three experts drawn from the analyst and technology worlds to share their views.

Visit us on Stand S06

ü View TEMENOS T24™ & scanned images

direct from TEMENOS T24™

ü Uses standard TEMENOS T24™ enquiry

screens

ü Allows faster customer query resolution,

validity checks, and fi nancial analysis

ü Seamless integration

www.efstechnology.com

For more information

please email

View Documents from TEMENOS T24™

AutoFORM LaserNet T24 Archive Link

Temenos_advert_feb08_t24.indd 9/30/2008, 12:39 PM1

TEMENOS NEWS 1�

implementing new products in a timely manner. We need an industry group that can define banking services and develop a more standardised approach to software development. A single vendor cannot accomplish this task, so BIAN represents a great opportunity for the industry. As we develop SOA standards and services, banks and vendors should be able to develop and maintain systems at a much lower cost. This is another stage in the maturity of bank information technology. “

One of the things that make BIAN stand out is its perspective. Don Free, Research Director, Gartner, says: “It’s essential to address standards in a business process context.” BIAN also has the potential to help the entire banking industry by encouraging investment that will benefit financial institutions of all tiers.

Free says: “Standards adoption and investment is growing within the larger retail banks to simplify integration, mostly due to differing data semantics among their complex systems. As more vendors get behind standards, investment by both banks and vendors will trickle down and benefit smaller banks that will be able to access more agile, cost-effective technology.”

Clearly, BIAN is good news from every angle – and a crucial step forward for the banking technology industry. With an independent body behind them, banks will gain confidence in SOA and its ability to provide a long-term solution to their issues. This should prompt a number of financial institutions to begin their SOA journey in earnest.

Temenos and BIANFor Temenos, membership of BIAN is part of an ongoing commitment to industry standards. Andreas Andreades, Chief Executive Officer, Temenos, says: “Our involvement with BIAN is part of our company’s increasing commitment to SOA. We recognise the importance of SOA and have invested significantly in our product thus far, and continue to do so. We invest around 20 per cent of our yearly revenues back into our R&D programme – more than any of our peers. We are well positioned to help our customers align their businesses to take full advantage of current technology trends and develop a successful, long-term strategy.”

TEMENOS NEWS14

The road to Rome: Temenos Client Forum 2008

A major topic for discussion was the way in which the present economic climate is changing banking approaches. For example, many analysts see technology as an ongoing priority for firms looking to offset their losses. By investing in the right technology, banks can future proof their business and maintain their competitive advantage in the face of economic crises.

The globalisation of banking, the need for increasingly complex products and services and merger and acquisition activity, are also major challenges that IT systems are often too inflexible to meet. Financial institutions are realising that there are strong imperatives for renewing core systems. Temenos delivers a low-risk implementation model to help banks effect this change in a rapid and meaningful fashion. During the conference, speakers looked at where core banking systems are today, and how they are likely to develop in the future. Speakers discussed how financial institutions can derive maximum benefit from their banking systems and reinforce their market position by building future-proof processes.

While sporting fans turned their thoughts to Beijing and the world’s greatest sporting contest, Temenos had its eyes fixed firmly on another important event, in Rome. The 2008 Temenos Client Forum (TCF), a key event in the core banking calendar, was held at the Marriott Hotel and attracted around 600 delegates, including clients, partners, analysts and journalists. TCF aims to inform delegates of the latest industry developments, as well as company and product news from Temenos. It also gives Temenos’ industry partners an opportunity to showcase their products and customers to share their experience, relate success stories and build on their knowledge.

The theme – 21st Century Core Processing – reflected the challenges faced by financial institutions after a turbulent year for the banking industry and demonstrated how technology can boost their competitive edge. This sums up the Temenos approach – helping customers to address challenges, take advantage of new opportunities and maximise return on invest-ment with T24, the most modern, flexible and feature-rich core banking system available.

Delegates experienced a mixture of presenta-tions and real-life customer reference studies based on key industry themes such as SOA, migration paths and preparing for growth. There were 4� sessions and presenters included Banque Libano-Française, Swedbank, Raiffeisen Poland and Saudi Hollandi Bank. They were joined by a number of guest speakers – industry experts such as Chris Skinner, independent com-mentator on the financial markets, and Elton Cane, content director at Finextra.

The ‘Product Expo’ ran alongside the main programme and Temenos representatives and business partners were available at their exhibition stands to meet delegates. This gave Temenos’ customers and prospects an opportu-nity to learn about new complementary products and services first hand.

Temenos accentuated its customer focus with lavish hospitality – delegates were invited to attend festive evening events, including a night of food and entertainment at a 1�th-century Palazzo in Rome and a gala dinner. Lastly, the Internet Café provided access to the TCF site, which housed a variety of event information.

Throughout the event, Temenos demonstrated its client focus and strong commitment to product development, as well as its continued focus on implementation services.

We are pleased to announce that the Temenos Client Forum 2008 will take place in Rome, Italy.

www.temenos.com/events

28-30 May, 2008

Location: Rome, Italynumber of delegates: 600Breakout sessions: 4�Platinum sponsor: Microsoft CorporationGold sponsor: Hewlett PackardSilver sponsor: ValidataBronze sponsor: IBM

Breakout sessions included:

• T24 in an advanced SOA environment: Banque Libano-Française

• Datawarehouse and business intelligence in detail: Temenos

• Rolling out a multi-country solution: Temenos and JP Morgan Chase

• T24 to support retail banking growth: Raiffeisen Poland

• Asset management and Temenos: Temenos

• Modern Islamic banking using T24: Finance House

• T24 and Microsoft SQL Server – mission-critical platform for core processing: Microsoft Corporation

The theme – 21st Century Core Processing – reflected the challenges faced by financial institutions and demonstrated how technology can boost their competitive edge.

KEY FaCTS

DaTE FoR

YoUR DIaRYTemenos Client Forum 2009 4 – 6 May 2009Monaco

as retail banks struggle to find new ways to differentiate themselves, mobile banking is becoming a hot industry topic. as with any innovation, banks need to consider a number of issues before they take the plunge. and, as well as thinking about how they can make mobile banking a successful, profitable service in a world of shrinking maturity cycles, banks must assess the extent of the threat from competition and identify its source. They must also ensure that they’re creating a valuable channel for their business rather than just layering another expense on their existing channel infrastructure.

Before addressing any of these issues, banks must first ask themselves a crucial question: what is mobile banking and what are the delivery options?

Mobile banking is not just an extension of internet banking. There is a real difference between internet banking services delivered through a handset and a true mobile banking model that is designed for security, performance and optimal user experience. In the first instance, the user receives standard internet banking services through a web browser. This quality of service relies on the reliability of the internet service delivered. As a result, it can lack end-to-end security and cannot guarantee delivery of instructions – which is important when making transfers and payments.

Turning to true mobile banking, there are a variety of solutions on the market that make use of different technologies and mobile operators’ services. The most basic, SMS/USSD may suit all handsets, but offers little security and message delivery is not guaranteed. It has the same shortcomings as browser handset solutions and the user is often confronted with complex menus.

Solutions based on handset applications offer the strongest security, greater opportunities for branding and an intuitive user experience that is widely accessible across the majority of handsets that are available today. This may be the best approach to differentiation in what might otherwise be a commodity area of banking.

So, the technology exists to deliver a range of services to the mobile phone, while protecting and promoting the brand. But what about the market potential and the business case justification?

The youth segment of the market offers huge potential for mobile banking, allowing the bank to reach out into a market that is not as receptive to traditional channels such as the branch, or indeed the internet. But the challenge here has always been one of low returns in the short term, with the hope of retention that will eventually create value for the bank. So the short-term objective must be to serve these customers at a cost that makes economic sense while building and maintaining long-term loyalty.

Serving this segment is no less stringent when it comes to security, functionality and reliability. In fact, in terms of customer experience, it is probably the most demanding customer segment for the mobile channel, comparing usability and experience to a host of other download services.

The secret to success is to build a secure, robust mobile banking platform as cost-effectively as possible. Reusing features and functions that already exist within the core banking system helps keep the costs down, as does having the mobile channel pre-integrated with the core banking system. Using the same customer data file is imperative for real-time consistency across channels. The ideal approach to providing a secure solution is to support the service through a small downloadable application on the handset – something that the younger market tends to take in its stride.

The design principles that Temenos adopted for ARC Mobile Banking bring the reality of a cost-effective solution closer for our T24 clients, as can be observed by the strong uptake of ARC, especially over the past year.

TEMENOS NEWS 15

BaRRIE nEILL RETAIL BANKING STRATEGY MANAGER, TEMENOS

Youthful mobility

The secret to success is to build a secure, robust mobile banking platform as cost-effectively as possible by reusing features and functions that already exist within the core banking system.

RETaIL BanKInG

16 TEMENOS NEWS

Risky business

In the wake of the credit crisis, the issue of risk has never been so prominent. While many banks are thinking about customer or trading risk, universal banks, especially niche players, are particularly concerned with operational risk and the damage done to a business following operational failure. Every bank knows its business may be damaged by operational risk – the only questions are by how much and for how long. Unsurprisingly, banks are keen to avoid operational issues at all costs.

A key factor with operational risk is that it creates a snowball effect. When it crystallises, it can lead to a deadly variant – reputational risk. It could take years for a bank’s share value to recover from a core system failure and it is doubtful that it could recover from a second failure. To protect their business, banks need to safeguard their reputation as well as their operations.

Naturally, many banks look to technology vendors to deal with these issues. But, while operational risk may be at the forefront of current thinking, many industry voices concentrate on the reactive approach – business continuity planning and disaster recovery methodologies. And, while these measures are both vital and necessary, they are not the only way to deal with risk.

At Temenos, we take a three-pronged, preventative approach to operational risk that starts at the implementation stage and is based on internal integration, straight-through processing and a proven, low-risk implementation methodology based on T24 Model Bank. Crucially, our engagement does not end once the implementation is complete. A number of our customers also enlist Temenos Professional Services consultants to provide onsite support following go-live to further reduce the risk of operational failure.

All of these features combine to inherently reduce operational risk. As part of our commitment to continuous improvement, we are already looking beyond this to expand the ways in which we help our clients deal with risk, for example by including quantitative operational risk capabilities into forthcoming releases of T24. In fact, risk mitigation is a key thread of our entire methodology – because, like all experienced practitioners, we believe that prevention is better than cure.

UnIVERSaL BanKInG

LInDSaY BaLDoCK CORPORATE & CORRESPONDENT BANKING STRATEGY MANAGER, TEMENOS

UNIVERSAL BANKING STRATEGY MANAGER, TEMENOS

Conventional wisdom holds that with the march towards globalisation and the pursuit of greater efficiency and reduced costs, corporates with operations in more than one country should aim to consolidate their banking relationships. This trend is underlined by initiatives such as SEPA, which will break down national barriers and encourage international businesses to rationalise their accounts, on the basis that a single bank can accommodate payments operations across a number of countries.

In the current economic climate, however, corporates are being forced to re-evaluate this imperative. The lack of market liquidity and the tightening of banks’ credit criteria have as profound an effect on corporates as they do on consumers. At the same time, reduced appetite in capital markets means that it is a lot harder to raise funds.

Corporate treasurers must still ensure they have adequate group borrowing facilities in place. So to guarantee a greater supply of credit and mitigate the risks of relying on one source of funding, they are expanding their banking relationships.

Another consequence of the recent economic downturn is that some of the largest banks have seen their ratings hit. In response, corporates that have in the past operated a single cash management arrangement with one global bank are more inclined to safeguard themselves by spreading their surplus funds and putting alternative cash management facilities in place.

So if multi-bank policies are the new vogue, does that mean corporates will lose the advantages of centralised control and cash optimisation?

Not necessarily, because businesses can aggregate accounts at different institutions for reporting through one main partner. This represents a valuable opportunity for banks, and using Temenos T24 is a great way to take up the right position. The system integrates intra- and end-of-day balance reports from any number of sources to produce a single, consolidated view of a group’s cash position – an invaluable asset for a corporate treasurer.

Against the grain

CoRPoRaTE & CoRRESPonDEnT BanKInG

17TEMENOS NEWS

In the past, private banking was a heady haze of golf, dinners and biannual meetings. Now, with budgets shrinking and customers demanding more online services, this cost-heavy, face-to-face operating model is becoming a thing of the past. In short, it’s time for private banking to go online.

Advisory- and execution-only models present a real challenge for asset managers who draw their revenues, not from transaction flow, but from service charges. To keep profits up, they must find new ways to service their clients effectively and add value.

There is also a regulatory implication. One of the impacts of MiFID is that the bank has to fully understand client objectives and levels of understanding – and ensure that any investments made on their behalf are in line with this. To avoid regulatory breach, private banks must keep a keen eye on what their discretionary- and execution-only clients are doing. The only way they can do this is to establish an electronic channel to capture and monitor client activity. The challenge lies in finding a means of doing this that will appeal to – and benefit – the client.

This is where online channels can help. Private banks can enhance their service offering by providing customers with a form of direct market access – for example, a web portal that helps them access research reports, market information and portfolio management tools, making it easier for the customer to execute trades independently while still using the services of the bank.

Of course, to make this kind of service work, banks need strong internet banking and risk management capabilities. At least one large tier 1 bank and a number of smaller banks in the Temenos customer base are already doing this. In fact, the need to deliver sophisticated online services to high net worth customers is one of the crucial factors driving the core banking selection process. Smaller players would do well to observe what they are doing, and take heed.

BREnT RanDaLL PRIVATE WEALTH MANAGEMENT STRATEGY MANAGER TEMENOS

T24 – best practice in core bankingUsing its knowledge and expertise across each banking sector, Temenos has developed T24 Model Bank, which includes pre-configured products and processes for banking best practice to address the needs of specific markets. T24 Model Bank and its associated methodology can achieve a 50 per cent lower implementation timeframe, minimise customisation, dramatically increase return on investment and reduce implementation risk through much tighter control over a project scope and deliverables.

Wishes, buses and wise men

MICRoFInanCE & CoMMUnITY BanKInG

MURRaY GaRDInERMICROFINANCE & COMMUNITY BANKING STRATEGY MANAGER, TEMENOS

In life, some things seem to come in threes. The microfinance market is no exception. Essentially, it can be divided into three market segments – social microfinance, mutual societies and banks. Each of these segments faces different business challenges – but technology is common to all three.

Social microfinance organisations need to improve their commercial awareness and increase their use of technology to compete with newer, more narrowly focused market entrants. Many smaller microfinance organisations simply cannot afford to implement sophisticated technology. This difficulty can be circumvented by partnering with networked organisations – companies that can commit to a larger investment, assemble support resources and pass on economies of scale. At Temenos, we’re working with several networked organisations, including Opportunity International, to deliver T24 for Microfinance and Community Banking to smaller microfinance institutions.

For microfinance banks, the challenge lies in balancing strategic business goals against socially oriented microfinance objectives. Temenos is in a unique position to address these challenges. We deliver proven applications that help banks calculate profits and the social impact of their activities. Because our software is information rich, it can help financial institutions adapt to the complex financial and social factors involved in delivering microfinance – known as the double bottom line.

Mutual societies in emerging markets, such as credit unions, serve more narrowly defined member requirements. This requires member-centric technology, which is catered for by Temenos. But, often, mutual societies have difficulty agreeing on a common regional technology strategy – and this affects their ability to achieve scale.

The changing microfinance landscape poses challenges for all market participants – and vendors must learn to provide them with appropriate support throughout this time of transition. Our in-depth market experience means we’re well equipped to help them. In more ways than three.

Online challengesPRIVaTE wEaLTH ManaGEMEnT

For any bank considering a new data centre solution, benchmarks are crucial. And, although some are sceptical, in the right circumstances, they can deliver invaluable insights.

Interpreting benchmarks requires common sense. Instead of relying solely on ‘high water’ benchmarking based on state-of-the-art hardware, banks should also rely on benchmarks that deal with real-life scenarios. Temenos’ continuous benchmarking programme uses standard hardware, mixed transaction volumes and criteria appropriate to working banks. This helps prospective customers to see how our technology can work for their business.

Vendor priorities are also vital because they give a real flavour for the strengths of the technology on offer. Our partners play an instrumental role in the benchmarking process and are equally committed to helping banks make the right decisions. IBM concentrates on meeting ongoing challenges – including data privacy and minimising compliance risks, to maximising IT infrastructure performance and reducing cost. Its open standards-based multi-platform data server, IBM DB2® is the only hybrid data server optimised for managing both relational and pure xML data.

For Microsoft, the focus is on delivering enterprise-class performance for retail banking and providing high availability and data security with low total cost of ownership. Microsoft SQL Server is a scalable business intelligence platform that helps produce trend analysis, fraud detection and business reports in real time.

Oracle delivers secure, reliable and scalable systems for retail banks while providing adequate controls. The Oracle Database Platform provides industrial-strength capabilities to support business goals. Temenos also has its own database server, jBASE, a fast, robust, economical solution that has proven itself at a large range of T24 sites. By examining various vendor strengths and priorities, banks can make the right choice.

The final piece of key advice here is ‘try before you buy’. Banks must do their own research. All financial institutions have an in-house testing environment and, ultimately, any data centre technology will have to prove its mettle in a live environment. This makes it vital for banks to assess the worth of any solution they consider buying.

On the benchDaTaBaSE SPoTLIGHT

18 TEMENOS NEWS

CLIVE KETTERIDGEDATABASE STRATEGY DIRECTOR, TEMENOS

ISLaMIC BanKInG

The three pillars of Islamic private banking

DR. MoHaMED GonEIDBUSINESS DEVELOPMENT MANAGER MIDDLE EAST & GULF, TEMENOS

With the number of high net worth and ultra-high net worth individuals in Southeast Asia and the Middle East booming, and investors seeking to put their wealth in domestic markets, Islamic banks are turning their thoughts to private banking. Yet, while many feel they should be offering Islamic private wealth manage-ment services, few are entirely sure what form it should take and what their activities will entail. In the absence of any concrete industry vision, there is an opportunity for entrepreneurial banks to carve a niche by defining the market. Until they do, here are three scenarios exploring what Islamic private banking could look like in the future:

• Customer-level Shar’ia. In the same way that individual banks have their own Shar’ia committee, Islamic asset managers could well construct portfolios around individual client ethics. In traditional private banking, this personalised level of services is only delivered to ultra-high net worth clients with exceptionally large portfolios. If Islamic banks have to deliver individually customised services to all their customers, the cost of providing this service may skew the market in the direction of ultra-high net worth individuals.

• Company indexing. Like ethical funds, Islamic private banks will need to ensure that the companies in which they invest comply with Islamic law. In fact, some data providers have already started to add an Islamic marker to company statistics. But banks will have to create their own indexes to reflect their individual interpretations of Shar’ia law.

• Community matters. Since the remit of Islamic finance in general is to serve the community as a whole, should Islamic private banks take a more social view of their investments, beyond the mere accrual of investor wealth? If the answer is yes, it would have an impact on the way portfolios are managed. It would also pose a conundrum for asset managers, because to deliver significant returns for their clients while benefiting the community they will need to be creative and flexible.

T24 supports a full range of private banking capabilities and Islamic finance products, including Islamic banking clients operating in the three aforementioned scenarios. This mature functionality puts Temenos in a unique position to help Islamic banks define an operating model that will keep them at the forefront of the industry.

C

M

Y

CM

MY

CY

CMY

K