Embed Size (px)

Citation preview

Islamic Banking SystemA Promising Financial Architecture

Presentation by Ali Zein

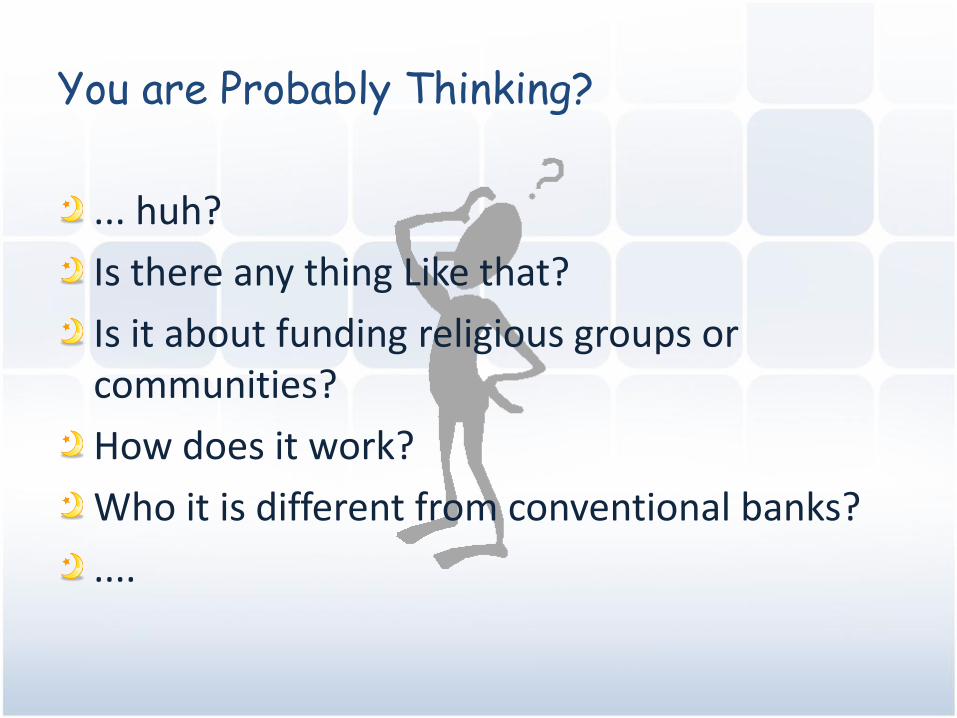

You are Probably Thinking?

... huh?

Is there any thing Like that?

Is it about funding religious groups or communities?

How does it work?

Who it is different from conventional banks?

....

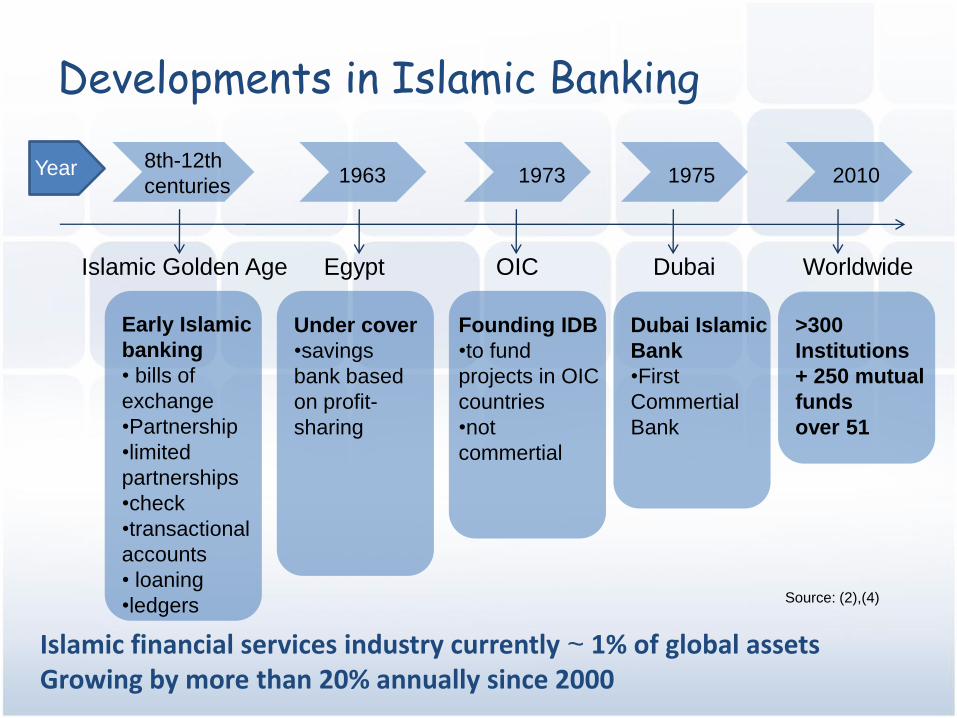

Developments in Islamic Banking

Year 8th-12th

centuries

Early Islamic

banking

• bills of

exchange

•Partnership

•limited

partnerships

•check

•transactional

accounts

• loaning

•ledgers

1963

Islamic Golden Age Egypt

Under cover

•savings

bank based

on profit-

sharing

1973

OIC

Founding IDB

•to fund

projects in OIC

countries

•not

commertial

Dubai

1975

Dubai Islamic

Bank

•First

Commertial

Bank

2010

>300

Institutions

+ 250 mutual

funds

over 51

Worldwide

Source: (2),(4)

Islamic financial services industry currently ~ 1% of global assetsGrowing by more than 20% annually since 2000

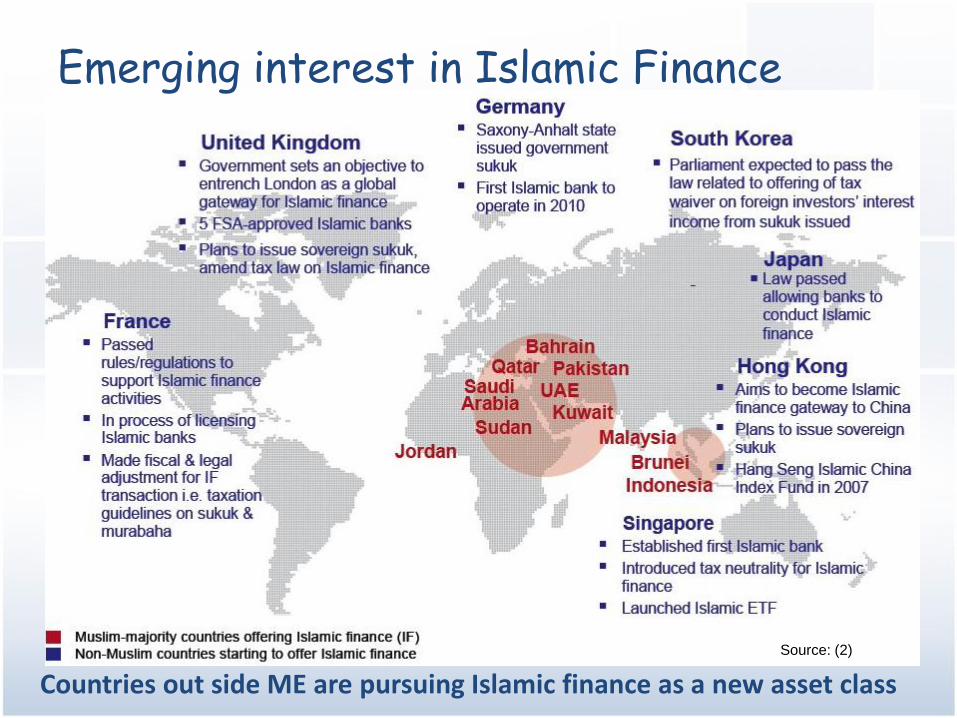

Emerging interest in Islamic Finance

Source: (2)

Countries out side ME are pursuing Islamic finance as a new asset class

Some of the key FIs in the world including 15 non-Muslim

United States: 20- Al Manzil Financial Services- American Finance House- Failaka Investments- HSBC - Ameen Housing Cooperative

Germany: 3- Bank Sepah- Commerz Bank- Deutsche Bank

Switzerland: 6

UK: 26 (primarily

branches of Gulf and

global banks)- HSBC Amanah Finance - Al Baraka International Ltd- Takafol UK Ltd- The Halal Mutual Investment Company- J Aron & Co Ltd (Goldman Sachs)

Bahrain: 26- Bahrain Islamic Bank- Al Baraka- ABC Islamic Bank - CitiIslamic Investment Bank

Malaysia: 492 - Pure Islamic Banks (Bank Islam, Bank Muamalat)Rest - conventional banks

Saudi Arabia: 10- Al Rajhi - SAMBA- Saudi Hollandi - Riyadh Bank

UAE: 9- Dubai Islamic Bank- Abu Dhabi Islamic Bank- HSBC Amanah

Qatar: 4- Qatar Islamic Bank- Qatar International Islamic

Kuwait: 5- Kuwait Finance House

Iran: 8

Egypt: 7- Alwatany Bank of Egypt- Egyptian Saudi Finance

Indonesia: 4

Sudan: 9

Pakistan: 5

India: 3

Bangladesh: 3

Turkey: 7- Faisal Finance Institution- Ihlas Finance House

Yemen: 5

Source:(3)

Islamic Financial Institutions around the world

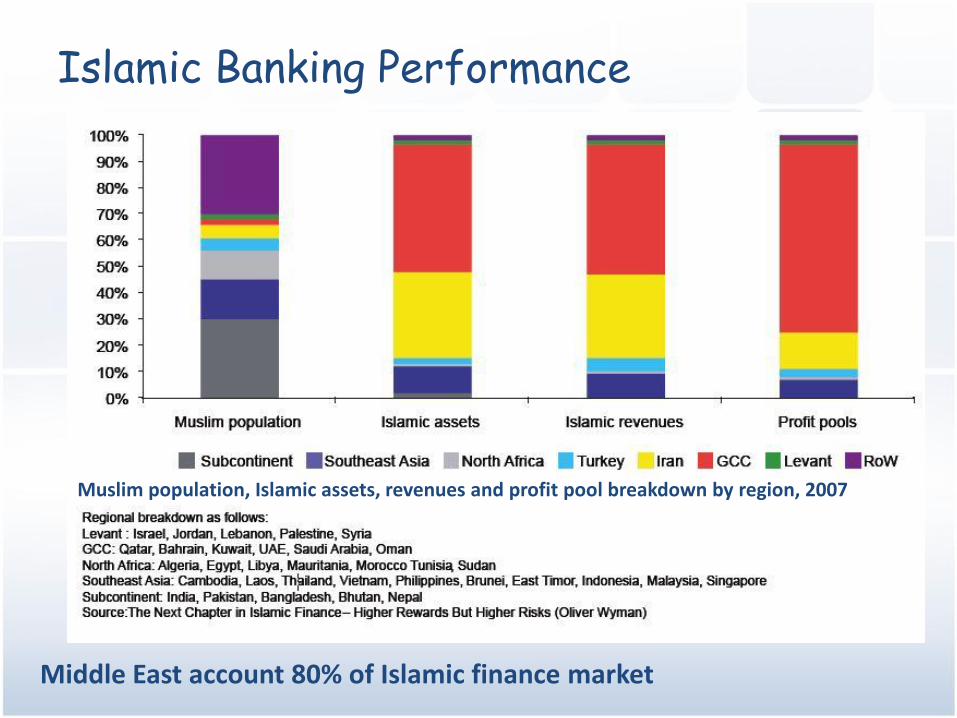

Islamic Banking Performance

Muslim population, Islamic assets, revenues and profit pool breakdown by region, 2007

Middle East account 80% of Islamic finance market

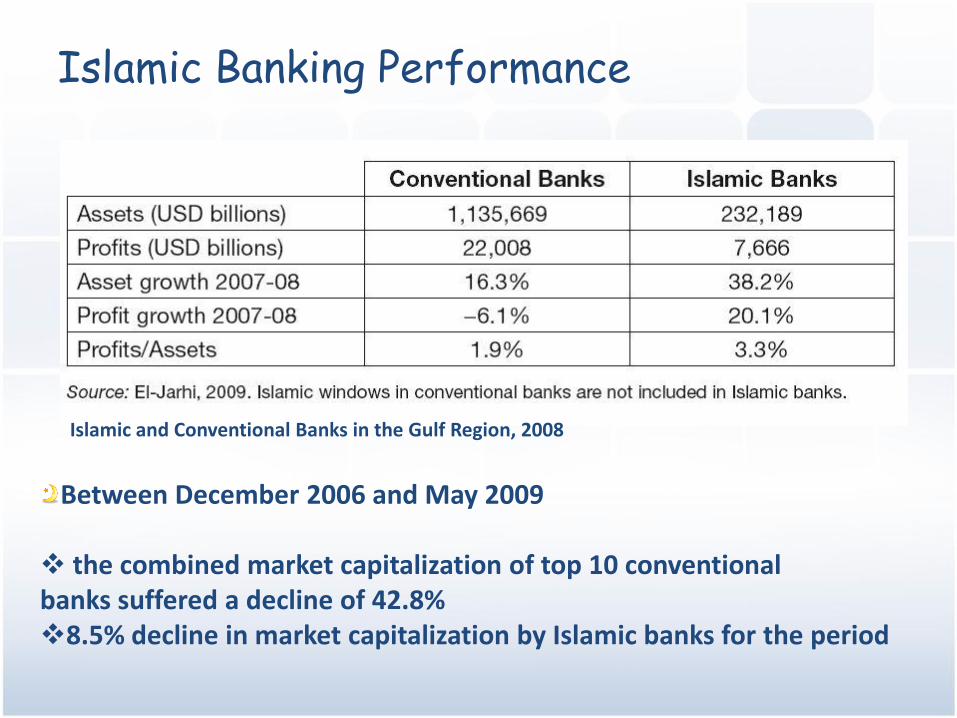

Islamic Banking Performance

Islamic and Conventional Banks in the Gulf Region, 2008

Between December 2006 and May 2009

the combined market capitalization of top 10 conventionalbanks suffered a decline of 42.8% 8.5% decline in market capitalization by Islamic banks for the period

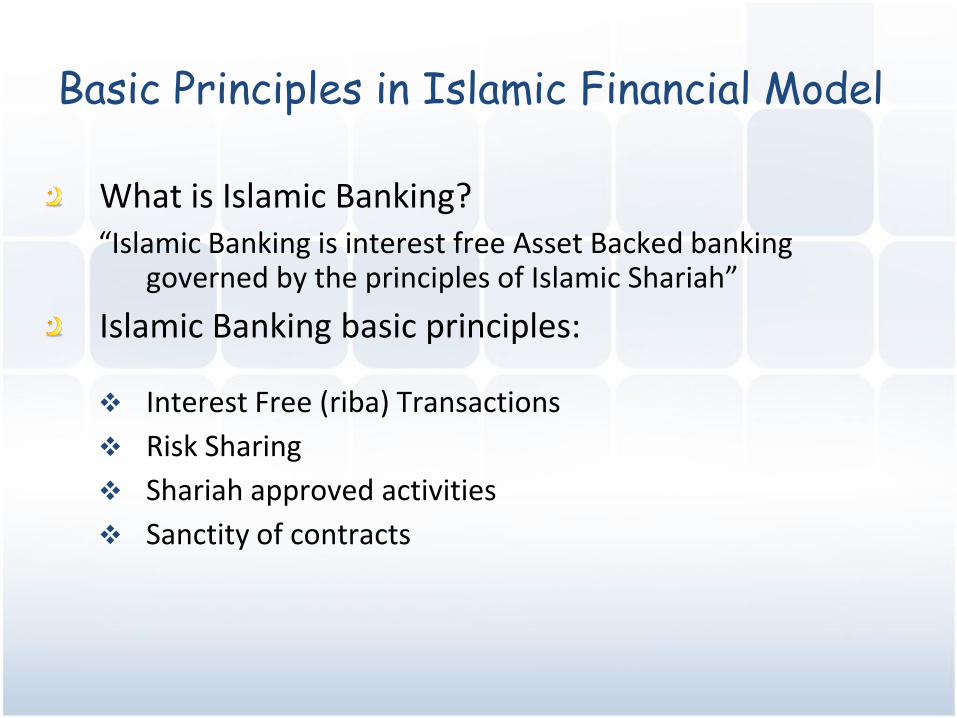

Basic Principles in Islamic Financial Model

What is Islamic Banking?“Islamic Banking is interest free Asset Backed banking

governed by the principles of Islamic Shariah”

Islamic Banking basic principles:

Interest Free (riba) Transactions

Risk Sharing

Shariah approved activities

Sanctity of contracts

“The interest which you give to increase the wealth of people, will have no increase with Allah: But that which you lay out for charity, seeking favor of Allah (He will increase): it is these who will get a recompense multiplied.”

Ar Rum 39 (First Revelation)

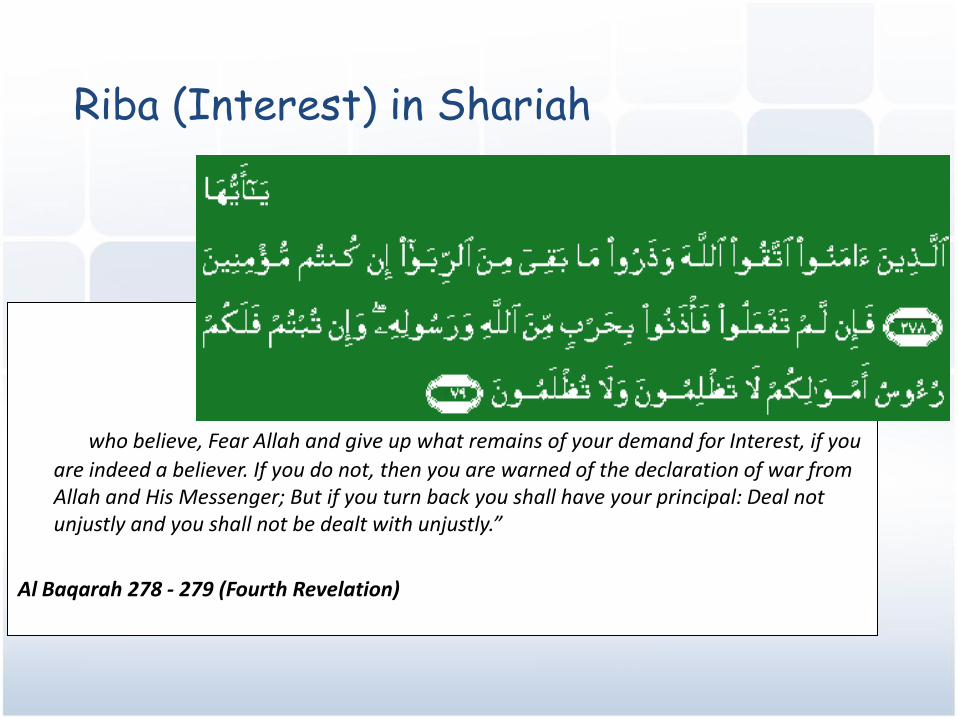

Riba (Interest) in Shariah

“O you who believe, Fear Allah and give up what remains of your demand for Interest, if you

are indeed a believer. If you do not, then you are warned of the declaration of war from Allah and His Messenger; But if you turn back you shall have your principal: Deal not unjustly and you shall not be dealt with unjustly.”

Al Baqarah 278 - 279 (Fourth Revelation)

Riba (Interest) in Shariah

taxonomy of Islamic contractsThe parallel with “conventional” finance

Salam Householders lending

Murabaha Mortgage with bank’s ownership (in the first step of contract)

Ijara Renting / Leasing

Istisna Sale of real estate under contruction

Musharaka Joint venture / investment deposits

Mudaraba Limited partnership / Investment accounts

Mudaraba Mutual funds / bank’s performance bonds

Qardh hasan Demand deposits 11(current accounts)

Takaful Insurance contract

Sukuk Asset Backed SecuritiesSource:(5)

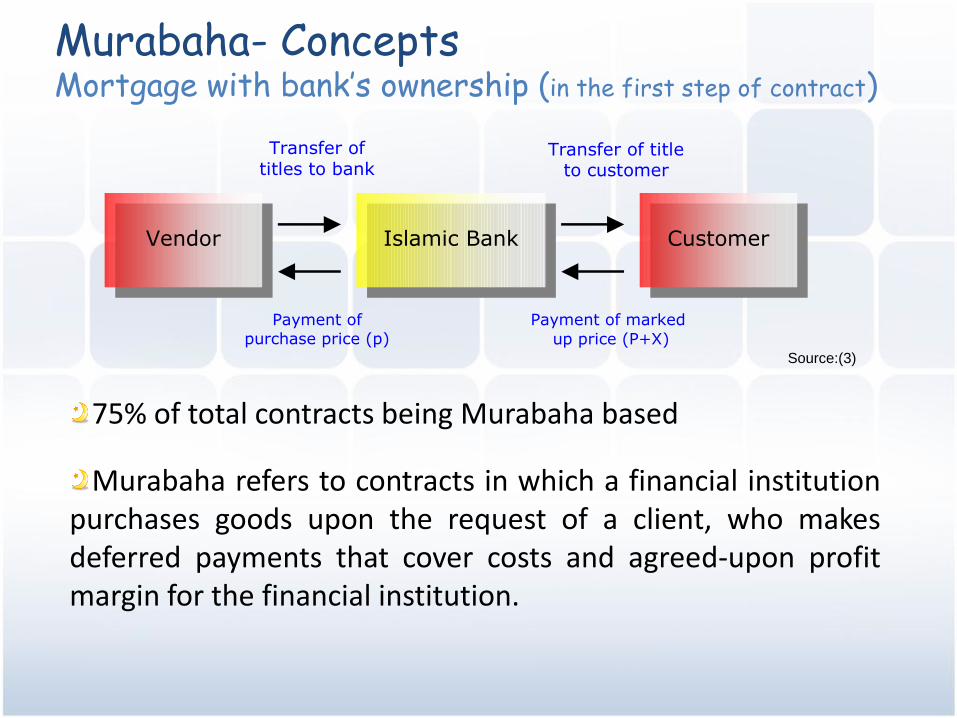

Murabaha- ConceptsMortgage with bank’s ownership (in the first step of contract)

Vendor

Customer

Islamic Bank

Payment of marked

up price (P+X)

Payment of purchase price (p)

Transfer of titles to bank

Transfer of title to customer

75% of total contracts being Murabaha based

Murabaha refers to contracts in which a financial institutionpurchases goods upon the request of a client, who makesdeferred payments that cover costs and agreed-upon profitmargin for the financial institution.

Source:(3)

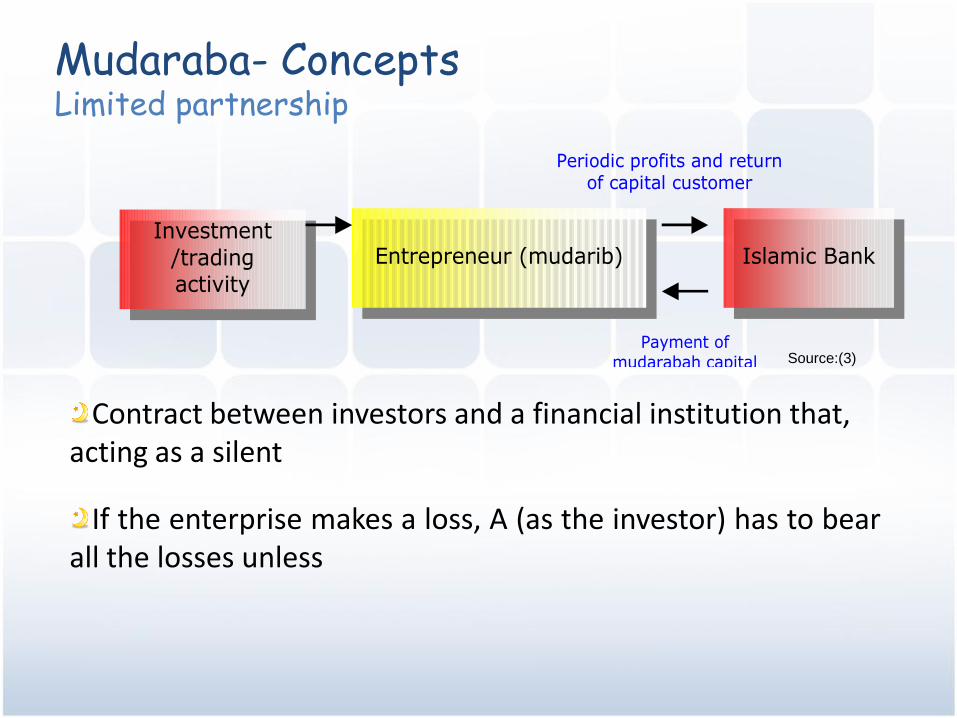

Mudaraba- ConceptsLimited partnership

Contract between investors and a financial institution that, acting as a silent

If the enterprise makes a loss, A (as the investor) has to bearall the losses unless

Source:(3)

Investment

/trading activity

Islamic Bank

Entrepreneur (mudarib)

Periodic profits and return of capital customer

Payment of mudarabah capital

customer

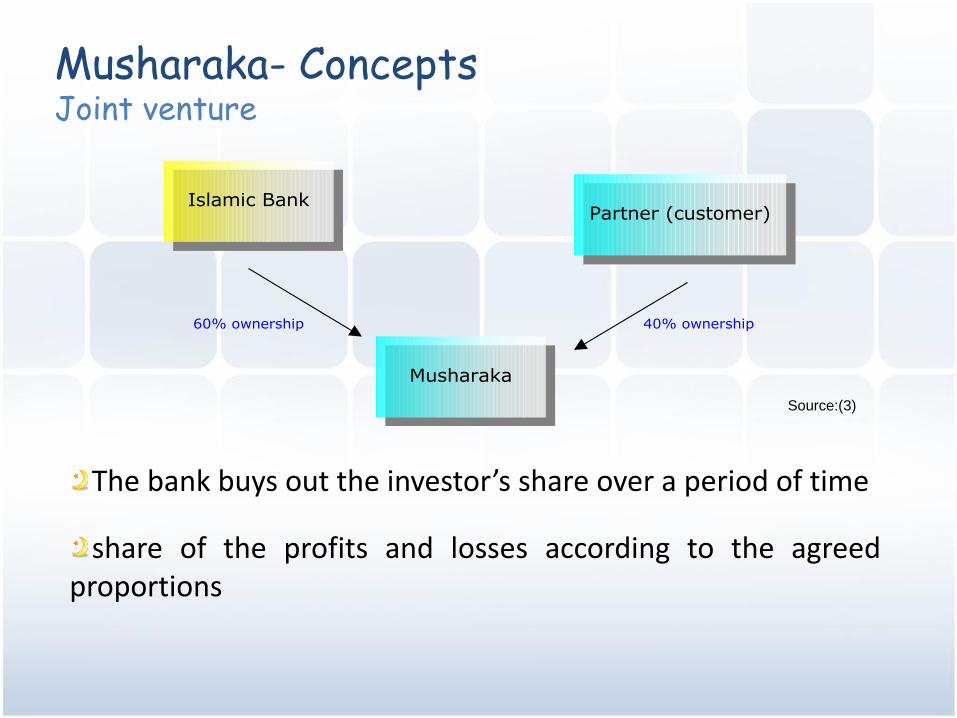

Musharaka- ConceptsJoint venture

The bank buys out the investor’s share over a period of time

share of the profits and losses according to the agreedproportions

Source:(3)

Islamic Bank

Partner (customer)

Musharaka

60% ownership

40% ownership

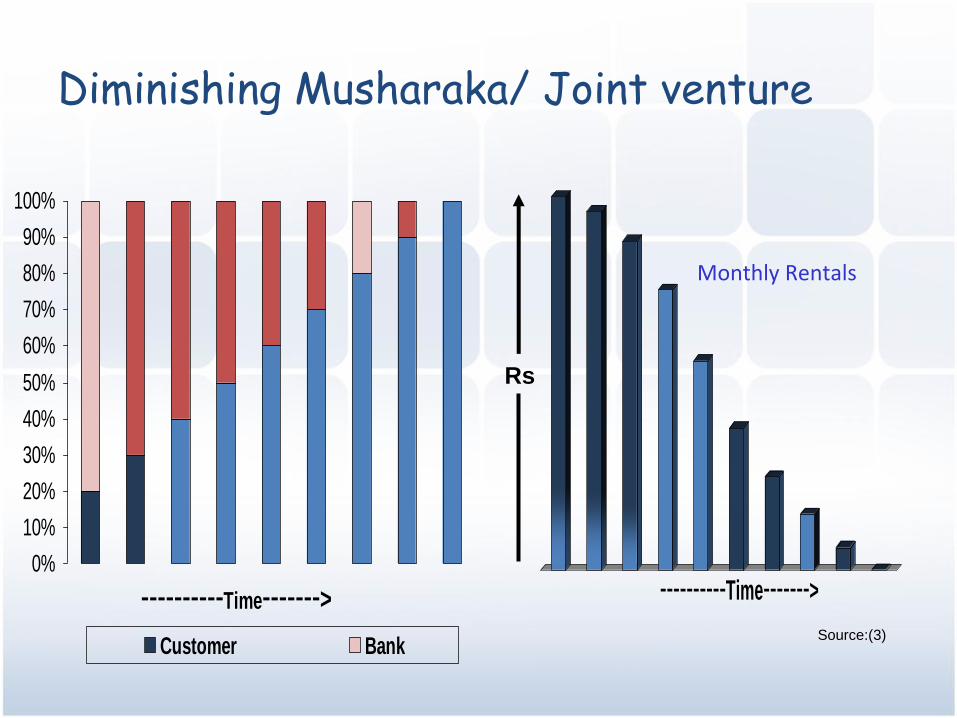

Diminishing Musharaka/ Joint venture

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Customer Bank

----------Time------->

Rs

Monthly Rentals

----------Time------->Source:(3)

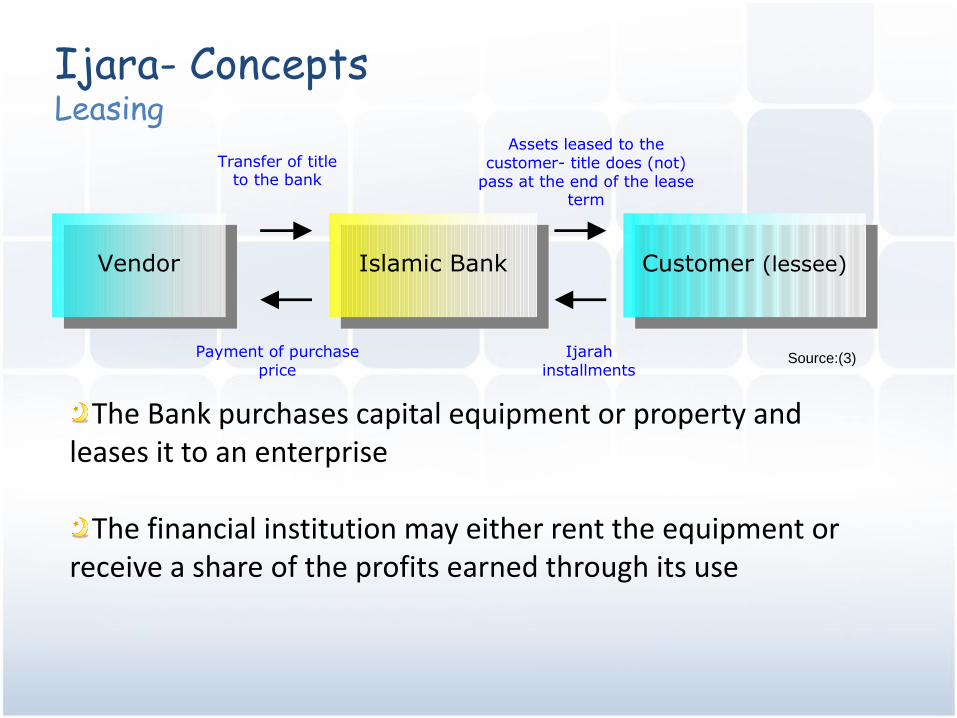

Ijara- ConceptsLeasing

The Bank purchases capital equipment or property and leases it to an enterprise

The financial institution may either rent the equipment or receive a share of the profits earned through its use

Source:(3)

Islamic Bank

Vendor

Customer (lessee)

Transfer of title to the bank

Assets leased to the customer- title does (not)

pass at the end of the lease term

Payment of purchase price

Ijarah installments

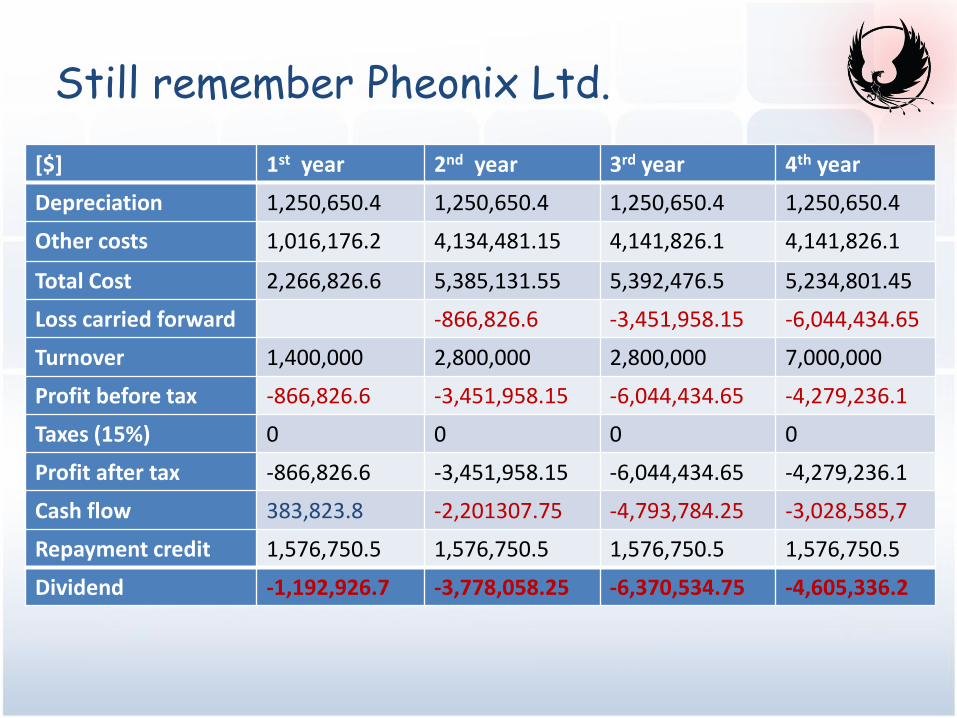

Still remember Pheonix Ltd.

Source:(3)

[$] 1st year 2nd year 3rd year 4th year

Depreciation 1,250,650.4 1,250,650.4 1,250,650.4 1,250,650.4

Other costs 1,016,176.2 4,134,481.15 4,141,826.1 4,141,826.1

Total Cost 2,266,826.6 5,385,131.55 5,392,476.5 5,234,801.45

Loss carried forward -866,826.6 -3,451,958.15 -6,044,434.65

Turnover 1,400,000 2,800,000 2,800,000 7,000,000

Profit before tax -866,826.6 -3,451,958.15 -6,044,434.65 -4,279,236.1

Taxes (15%) 0 0 0 0

Profit after tax -866,826.6 -3,451,958.15 -6,044,434.65 -4,279,236.1

Cash flow 383,823.8 -2,201307.75 -4,793,784.25 -3,028,585,7

Repayment credit 1,576,750.5 1,576,750.5 1,576,750.5 1,576,750.5

Dividend -1,192,926.7 -3,778,058.25 -6,370,534.75 -4,605,336.2

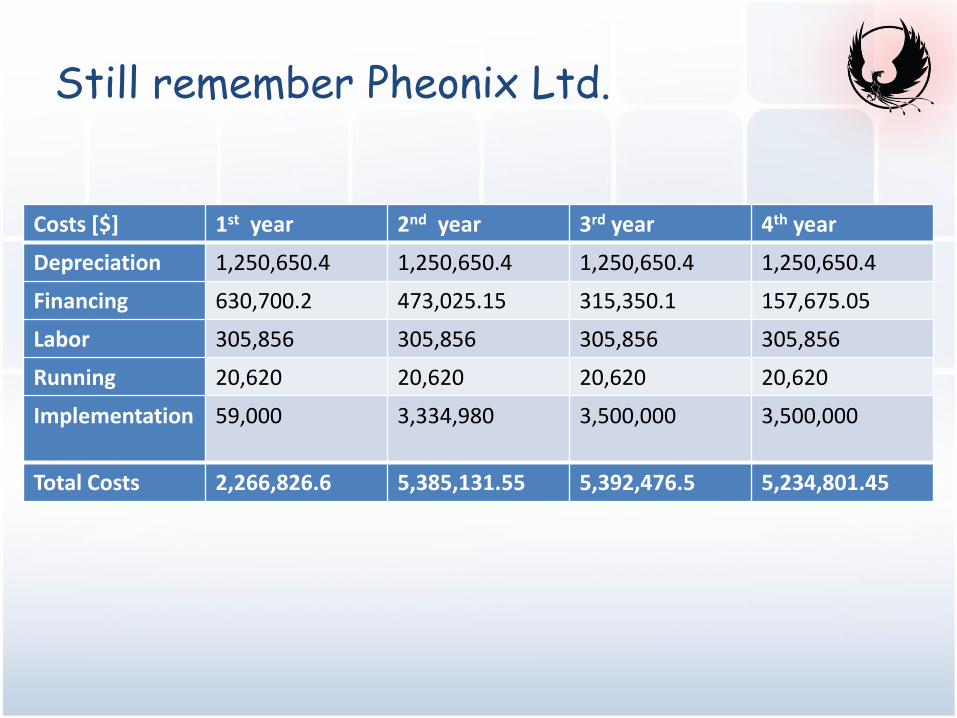

Still remember Pheonix Ltd.

Source:(3)

Costs [$] 1st year 2nd year 3rd year 4th year

Depreciation 1,250,650.4 1,250,650.4 1,250,650.4 1,250,650.4

Financing 630,700.2 473,025.15 315,350.1 157,675.05

Labor 305,856 305,856 305,856 305,856

Running 20,620 20,620 20,620 20,620

Implementation 59,000 3,334,980 3,500,000 3,500,000

Total Costs 2,266,826.6 5,385,131.55 5,392,476.5 5,234,801.45

References

(1) World Database for Islamic Banking and Finance (www.wdibf.com/)

(2) The IFSB-IRTI-IDB publishes report on Islamic Finance: Global Financial Stability April 2010 (http://www.ifsb.org/docs/IFSB-IRTI-IDB2010.pdf )

(3) Islamic Banking Current Scenario & Way ahead Nov. 2005 by Muhammad Imran:Head of Islamic Banking Standard Chartered Bank

(4) Organization of the Islamic Conference (OIC) (www.oic-oci.org/ )

(5) Risk profile of Islamic banks Nov. 2009 by Claudio Porzio & M. Grazia Starita: University of Naples “Parthenope”

Thanks!Questions?