Embed Size (px)

DESCRIPTION

November 2008. Islam & Riba/Interest. Presentation Outline. The WIIFM factor (What’s In It For Me?) Definition of Interest Interest in Quran Interest in Hadith Types of Riba/Interest Why Interest is such a Sin? Some common myths Some common questions ... and their answers. - PowerPoint PPT Presentation

Citation preview

November 2008

The WIIFM factor (What’s In It For Me?) Definition of Interest Interest in Quran Interest in Hadith Types of Riba/Interest Why Interest is such a Sin? Some common myths Some common questions ... and their

answers

2

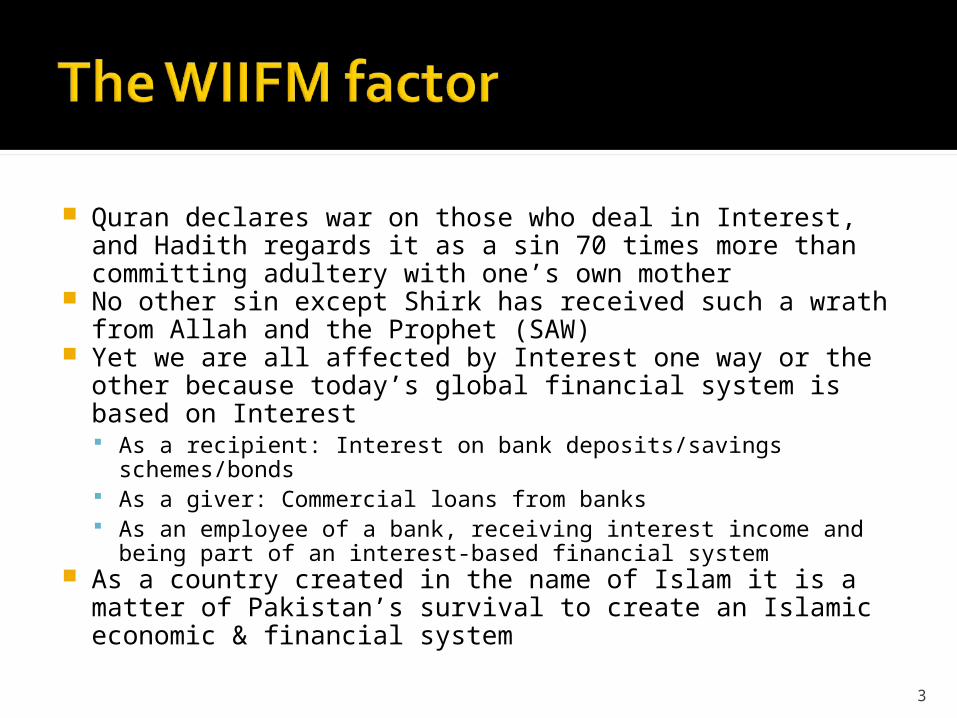

Quran declares war on those who deal in Interest, and Hadith regards it as a sin 70 times more than committing adultery with one’s own mother

No other sin except Shirk has received such a wrath from Allah and the Prophet (SAW)

Yet we are all affected by Interest one way or the other because today’s global financial system is based on Interest As a recipient: Interest on bank deposits/savings schemes/bonds As a giver: Commercial loans from banks As an employee of a bank, receiving interest income and being

part of an interest-based financial system As a country created in the name of Islam it is a matter of

Pakistan’s survival to create an Islamic economic & financial system

3

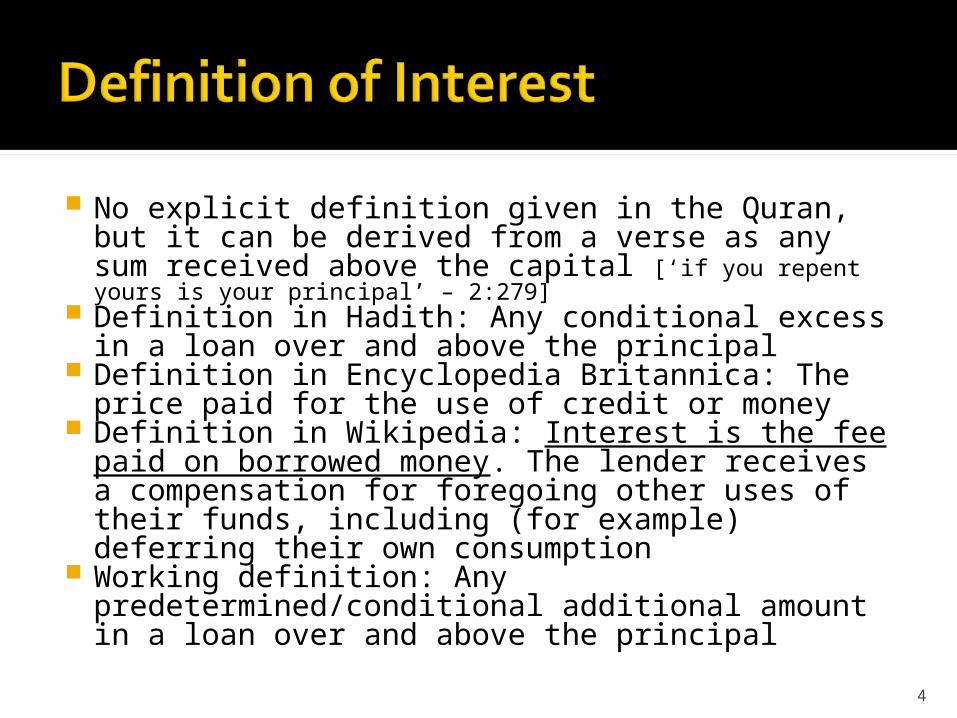

No explicit definition given in the Quran, but it can be derived from a verse as any sum received above the capital [‘if you repent yours is your principal’ – 2:279]

Definition in Hadith: Any conditional excess in a loan over and above the principal

Definition in Encyclopedia Britannica: The price paid for the use of credit or money

Definition in Wikipedia: Interest is the fee paid on borrowed money. The lender receives a compensation for foregoing other uses of their funds, including (for example) deferring their own consumption

Working definition: Any predetermined/conditional additional amount in a loan over and above the principal

4

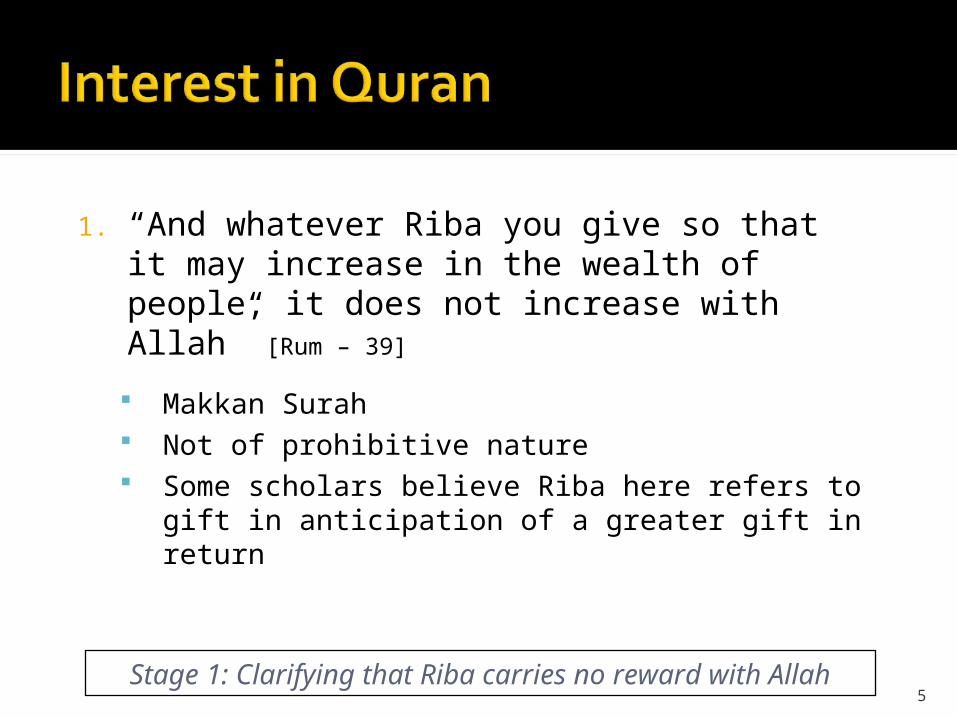

1. “And whatever Riba you give so that it may increase in the wealth of people, it does not increase with Allah” [Rum – 39]

Makkan Surah Not of prohibitive nature Some scholars believe Riba here refers to

gift in anticipation of a greater gift in return

5

Stage 1: Clarifying that Riba carries no reward with Allah

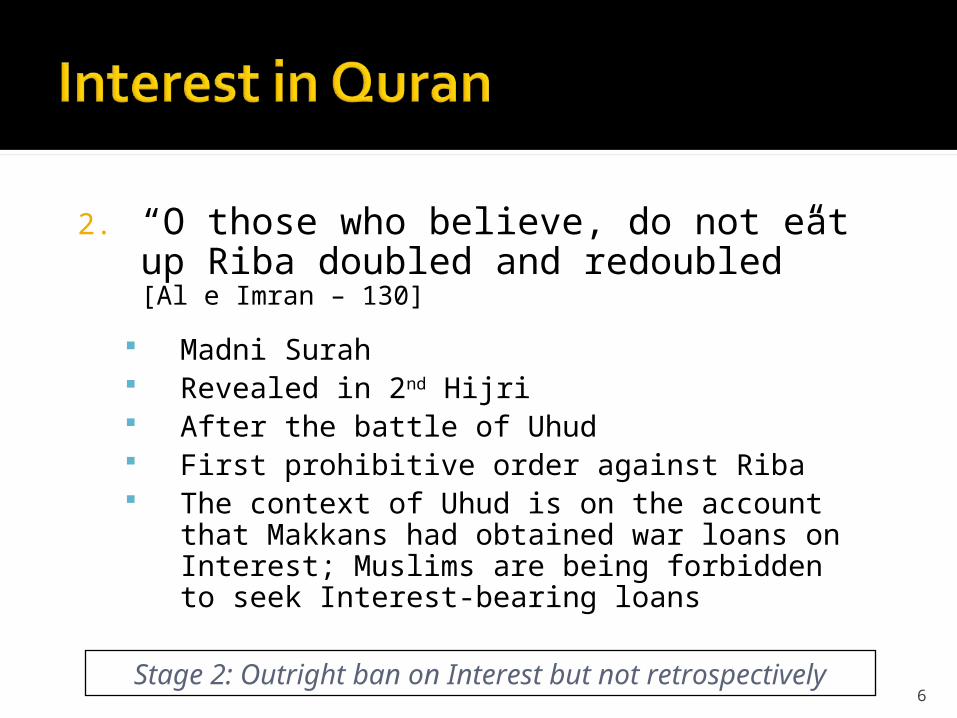

2. “O those who believe, do not eat up Riba doubled and redoubled” [Al e Imran – 130]

Madni Surah Revealed in 2nd Hijri After the battle of Uhud First prohibitive order against Riba The context of Uhud is on the account that

Makkans had obtained war loans on Interest; Muslims are being forbidden to seek Interest-bearing loans

6

Stage 2: Outright ban on Interest but not retrospectively

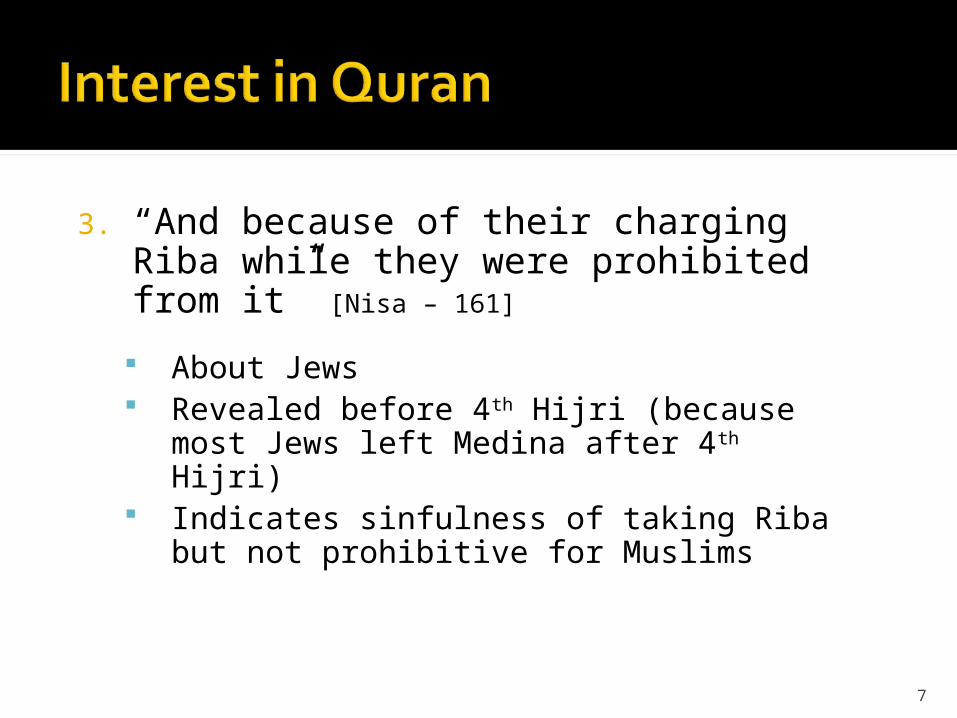

3. “And because of their charging Riba while they were prohibited from it” [Nisa – 161]

About Jews Revealed before 4th Hijri (because most

Jews left Medina after 4th Hijri) Indicates sinfulness of taking Riba but not

prohibitive for Muslims

7

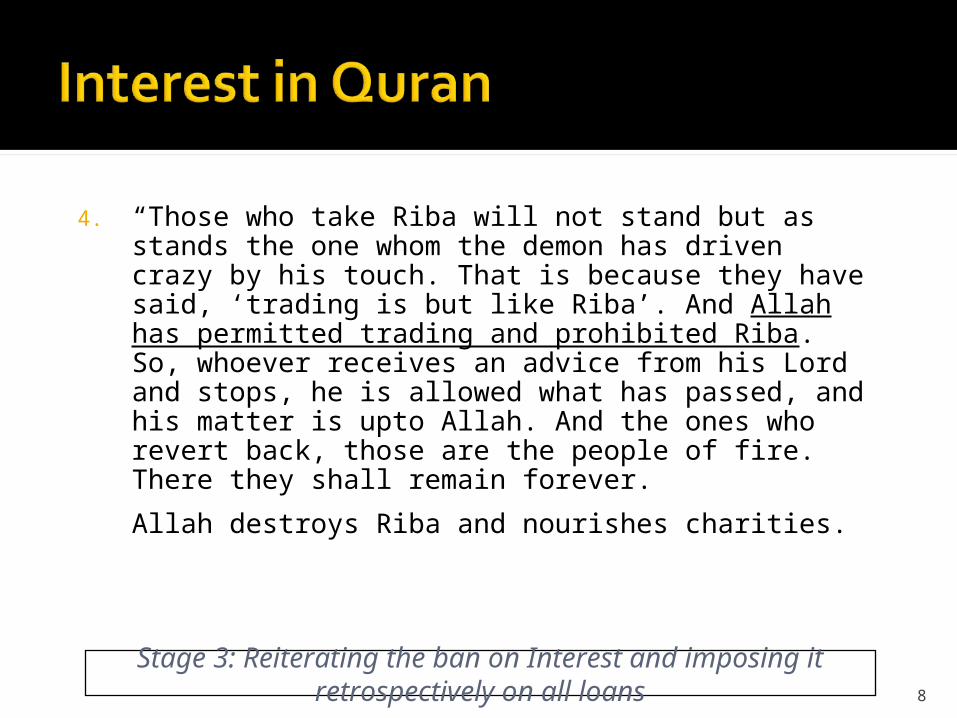

4. “Those who take Riba will not stand but as stands the one whom the demon has driven crazy by his touch. That is because they have said, ‘trading is but like Riba’. And Allah has permitted trading and prohibited Riba. So, whoever receives an advice from his Lord and stops, he is allowed what has passed, and his matter is upto Allah. And the ones who revert back, those are the people of fire. There they shall remain forever.

Allah destroys Riba and nourishes charities.

8

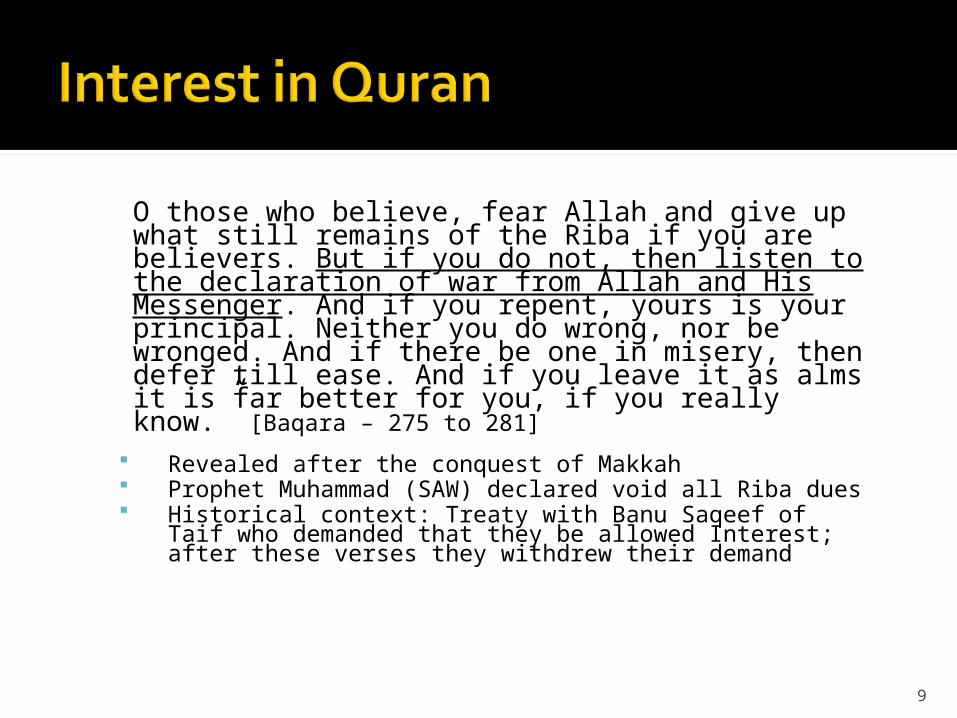

Stage 3: Reiterating the ban on Interest and imposing it retrospectively on all loans

O those who believe, fear Allah and give up what still remains of the Riba if you are believers. But if you do not, then listen to the declaration of war from Allah and His Messenger. And if you repent, yours is your principal. Neither you do wrong, nor be wronged. And if there be one in misery, then defer till ease. And if you leave it as alms it is far better for you, if you really know.” [Baqara – 275 to 281]

Revealed after the conquest of Makkah Prophet Muhammad (SAW) declared void all Riba dues Historical context: Treaty with Banu Saqeef of Taif

who demanded that they be allowed Interest; after these verses they withdrew their demand

9

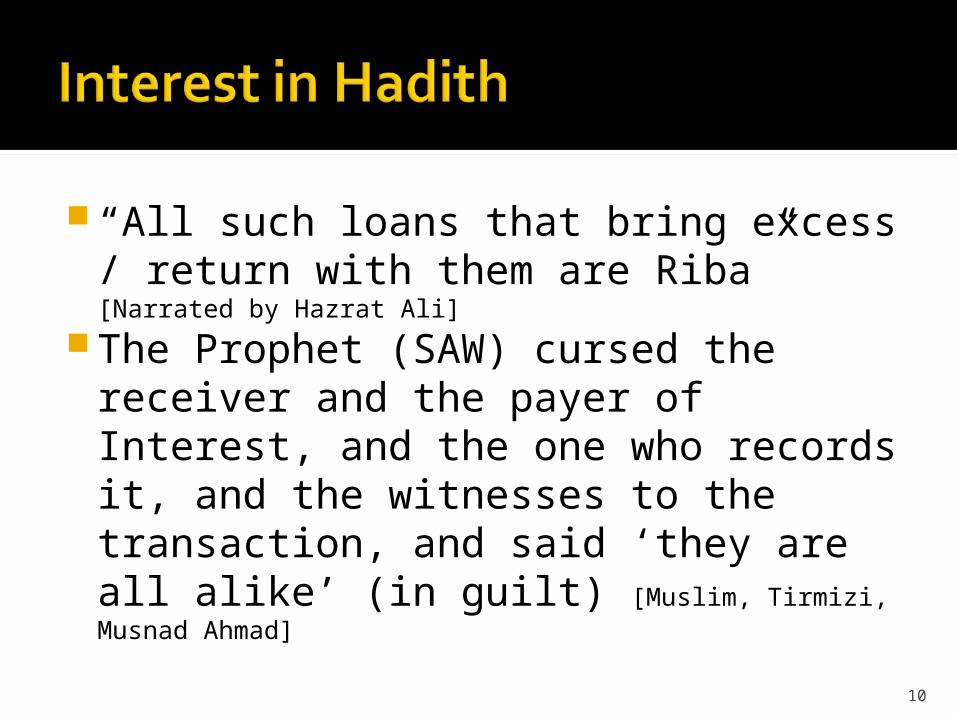

“All such loans that bring excess / return with them are Riba” [Narrated by Hazrat Ali]

The Prophet (SAW) cursed the receiver and the payer of Interest, and the one who records it, and the witnesses to the transaction, and said ‘they are all alike’ (in guilt) [Muslim, Tirmizi, Musnad Ahmad]

10

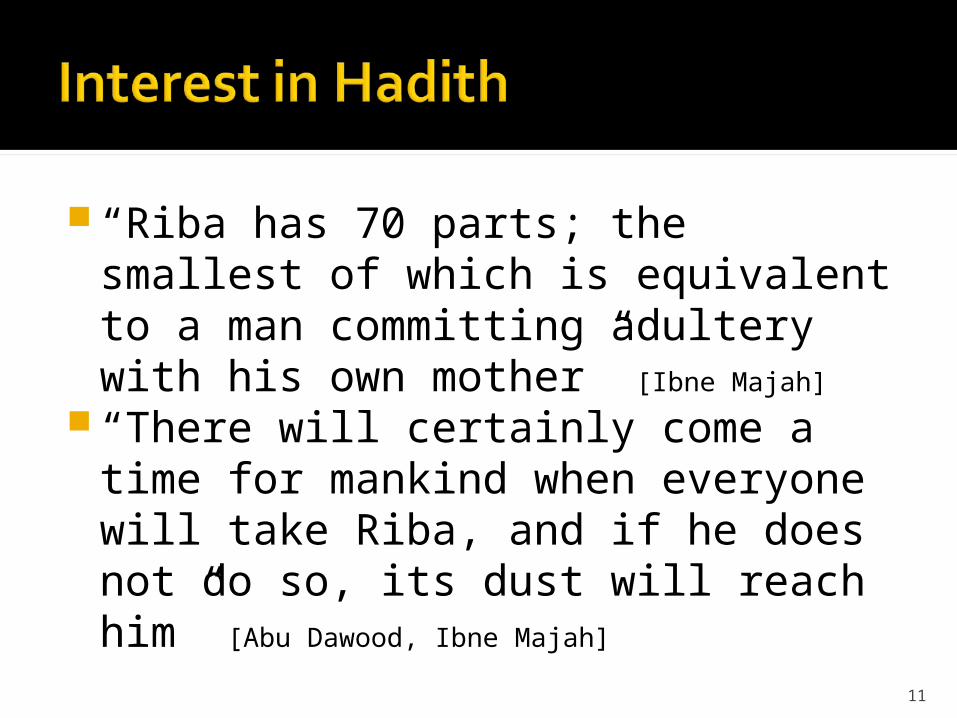

“Riba has 70 parts; the smallest of which is equivalent to a man committing adultery with his own mother” [Ibne Majah]

“There will certainly come a time for mankind when everyone will take Riba, and if he does not do so, its dust will reach him” [Abu Dawood, Ibne Majah]

11

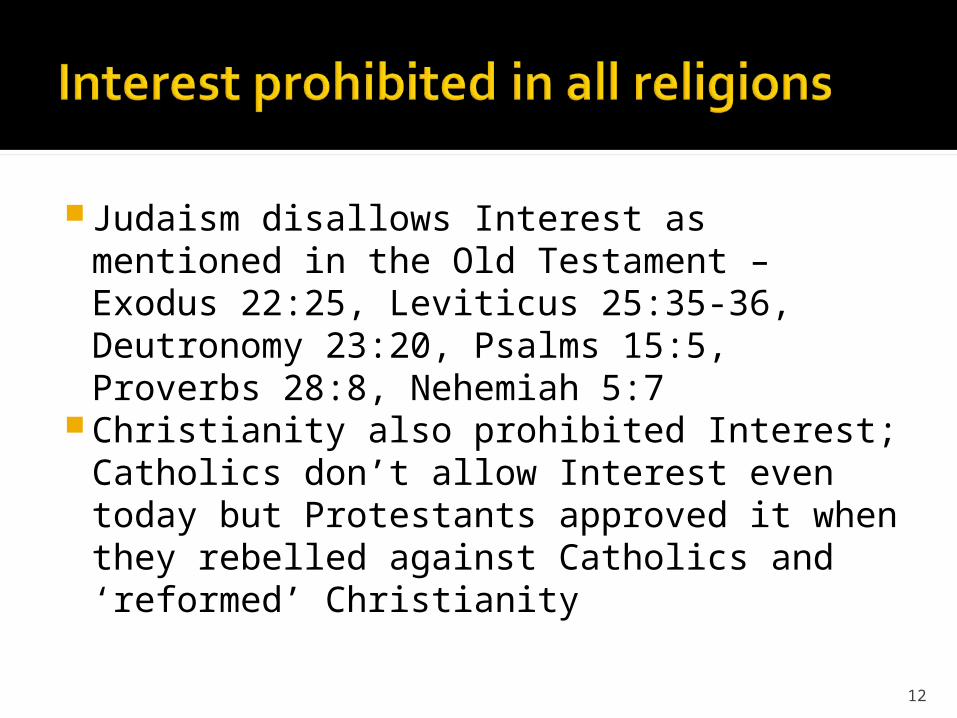

Judaism disallows Interest as mentioned in the Old Testament – Exodus 22:25, Leviticus 25:35-36, Deutronomy 23:20, Psalms 15:5, Proverbs 28:8, Nehemiah 5:7

Christianity also prohibited Interest; Catholics don’t allow Interest even today but Protestants approved it when they rebelled against Catholics and ‘reformed’ Christianity

12

There are two types of Riba, and both are prohibited1. Riba al Quran – also called Riba al Nasiyah

or Riba al Jahiliyyah (any predetermined/conditional increase over principal amount)

2. Riba al Hadith – also called Riba al Fazl or Riba al Bai (currency exchange in the form of commodities, especially in barter trading)

As the names suggest, Quran mentions the first type of Riba while Hadith also prohibits the second type

13

Real and primary form of Riba Had several forms in Arabia

Loan given on predetermined Interest rate for a defined period; the principal along with Interest to be repaid at the end of the term

The creditor would charge a monthly Interest from the debtor while the principal would remain intact upto the day of maturity

If the borrower could not pay at the end of the term, the lender would allow more time against additional Interest

14

Islam considers lending as a charitable, not commercial transaction

“Gold for gold, silver for silver, wheat for wheat, barley for barley, dates for dates, and salt for salt; like for like, hand to hand, in equal amounts, and any increase is Riba” [Abu Saeed Khudri in Muslim]

When Bilal (RA) told the Prophet (SAW) that he traded two volumes of lower quality dates with one volume of high quality dates he said that it was precisely the forbidden Riba [Abu Saeed Khudri in Muslim]

15

Against the core objective of Shariah – to establish justice (Adl) in the world

Economic slavery perpetrated by an Interest-based economic system deprives human beings from basic human dignity and relegates them to the status of mere economic animals

Unique nature of money Overall effects of Interest on economy

and society

16

Fundamental difference between Islam and Capitalism – Is Money a God to be worshipped or is it a tool to serve humanity?

Capitalism holds Money capital much superior to other sources of production (eg land, labour)

Capitalism treats money as a commodity which can be sold, leased, etc while Islam believes money is distinct from other commodities in several ways (eg differences in intrinsic value/utility, quality, identifiability)

17

Modern-day capitalism has mastered the art of stealing a man’s rights, and then selling them

back to him as a privilege

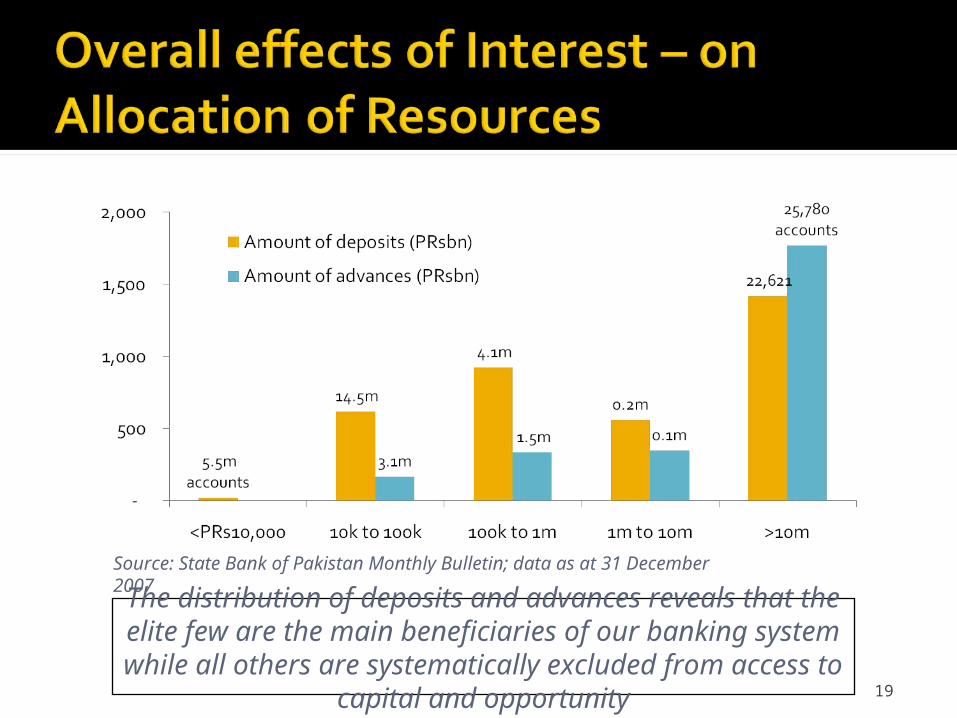

Loans are typically advanced to those who can offer collateral; serving only the big and already rich, thus reinforcing unequal distribution of capital

As of Dec 2007, 25,780 or 0.5% out of a total 4.9m borrowers having a loan amount of >PRs10m were recipients of 68% or PRs1.8 trillion of total loans/advances [Source: State Bank of Pakistan Monthly Bulletin Dec 2007]

18

Depositors of PRs10,000 to PRs100,000 make up 60% of total depositor base, but their share of

total deposit amount is only 17%

19

The distribution of deposits and advances reveals that the elite few are the main beneficiaries of our banking system while all others are systematically excluded from access to capital and opportunity

Source: State Bank of Pakistan Monthly Bulletin; data as at 31 December 2007

Since collateral based lending does not care about the actual purpose the loan is put to use, it encourages conspicuous consumption – by individuals, businesses and governments

Conspicuous consumption at macro level results in high government debts

20

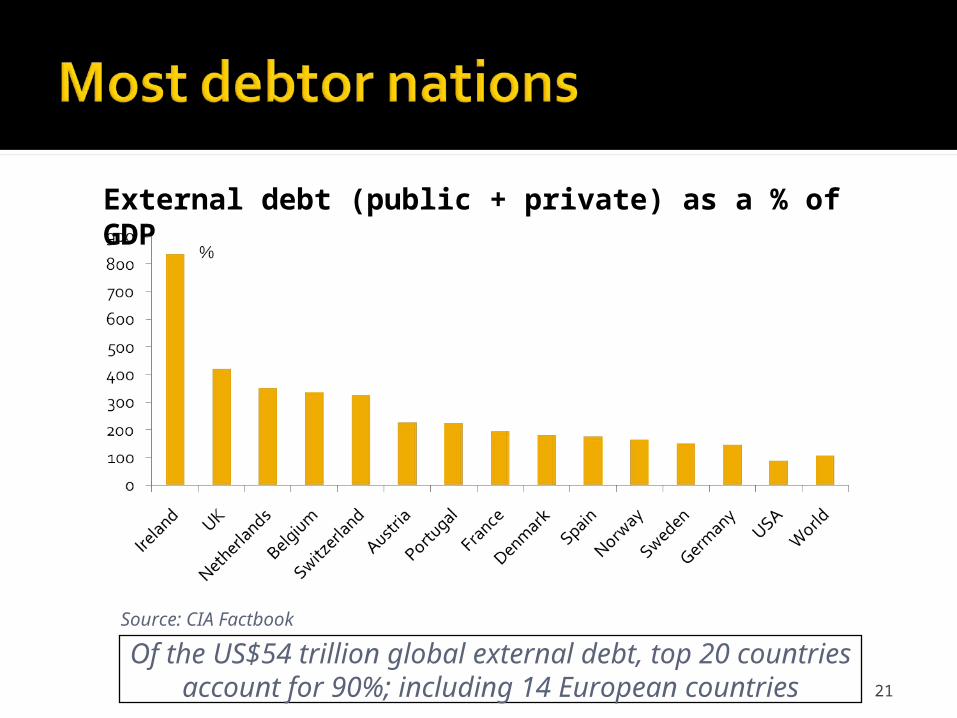

21

Of the US$54 trillion global external debt, top 20 countries account for 90%; including 14 European

countries

External debt (public + private) as a % of GDP

Source: CIA Factbook

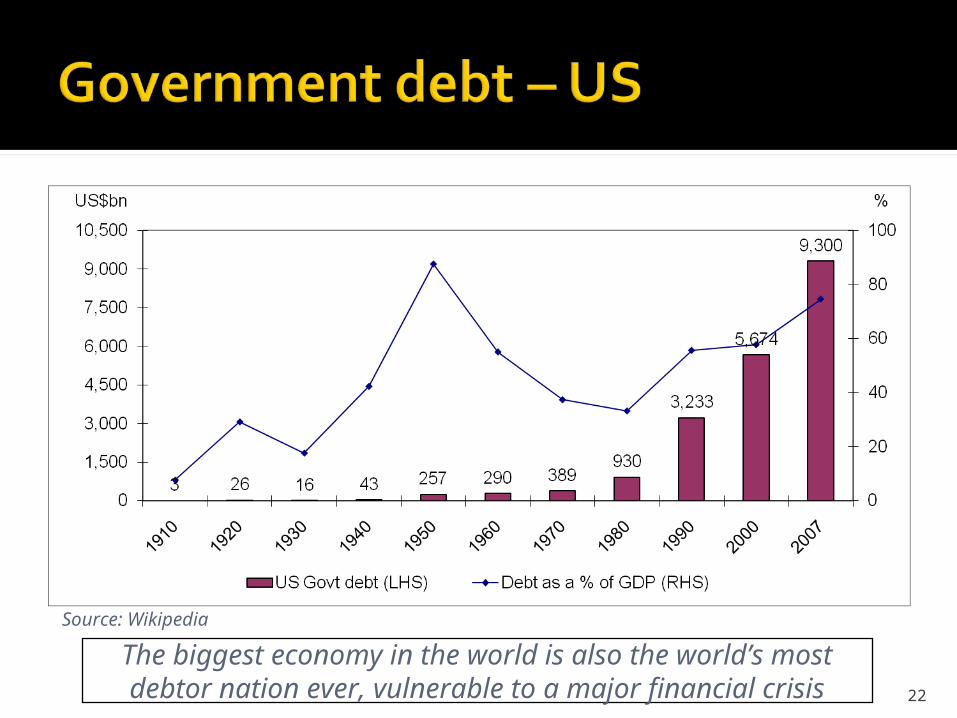

22

Source: WikipediaThe biggest economy in the world is also the world’s

most debtor nation ever, vulnerable to a major financial crisis

Interest based system either inflicts injustice to the borrower (if the business fails but he still has to repay the debt with Interest) or lender (if the borrower makes a huge profit from lender’s money but only pays a small amount in Interest)

20-30% of an industrial project is typically financed by equity contribution while 70-80% through bank loan, which is really depositors’ money. Profit earned on such projects is largely kept by the business groups while a small portion comes to depositors via the bank as Interest

This means that 25,780 borrowers are also the major beneficiaries of other people’s money in great disproportion of their contribution to wealth generation process. This is a systematic transfer of wealth from poor people to rich people

23

24

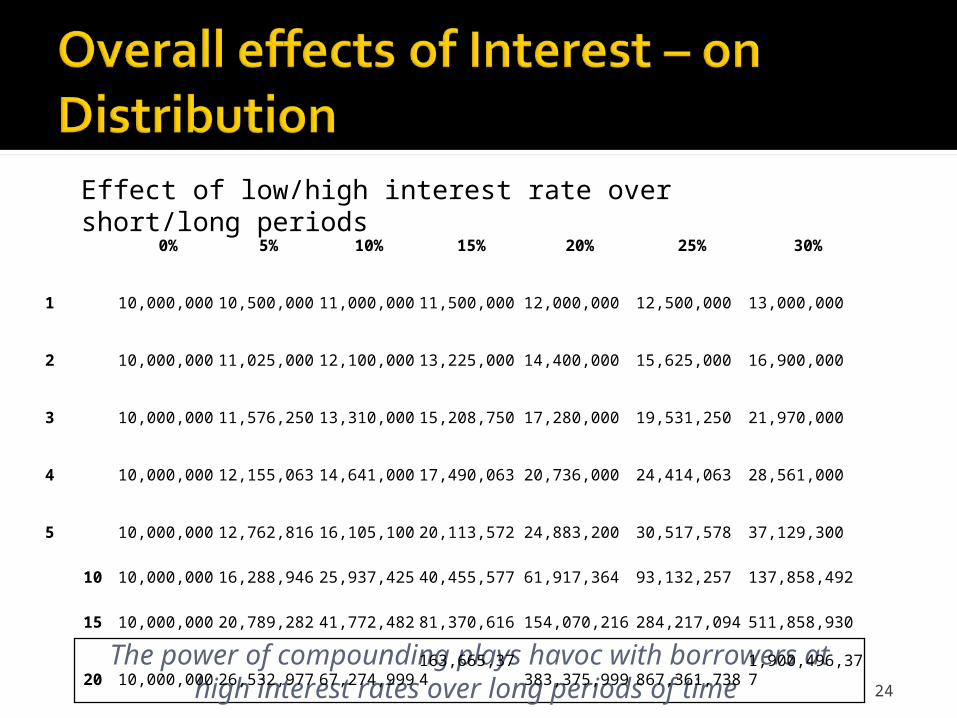

Effect of low/high interest rate over short/long periods

The power of compounding plays havoc with borrowers at high interest rates over long periods of

time

0% 5% 10% 15% 20% 25% 30%

1 10,000,000 10,500,000 11,000,000 11,500,000 12,000,000 12,500,000 13,000,000

2 10,000,000 11,025,000 12,100,000 13,225,000 14,400,000 15,625,000 16,900,000

3 10,000,000 11,576,250 13,310,000 15,208,750 17,280,000 19,531,250 21,970,000

4 10,000,000 12,155,063 14,641,000 17,490,063 20,736,000 24,414,063 28,561,000

5 10,000,000 12,762,816 16,105,100 20,113,572 24,883,200 30,517,578 37,129,300

10 10,000,000 16,288,946 25,937,425 40,455,577 61,917,364 93,132,257 137,858,492

15 10,000,000 20,789,282 41,772,482 81,370,616 154,070,216 284,217,094 511,858,930

20 10,000,000 26,532,977 67,274,999 163,665,374 383,375,999 867,361,738 1,900,496,377

Since Interest-bearing loans have no obvious/direct connection with actual production, there is a serious mismatch between the loans advanced by the banking system and the goods & services produced in the economy. This is a basic reason for Inflation

This phenomenon is aggravated by the “money creation’’ characteristic of modern banking, through which banks are able to create “money out of nothing’’ by way of fractional reserve banking system

This artificial money is the bubble that bursts in a financial crisis

25

“The collapse of the global marketplace would be a traumatic event with unimaginable consequences. Yet I find this easier to imagine than the continuation of

the present regime” George Soros

26

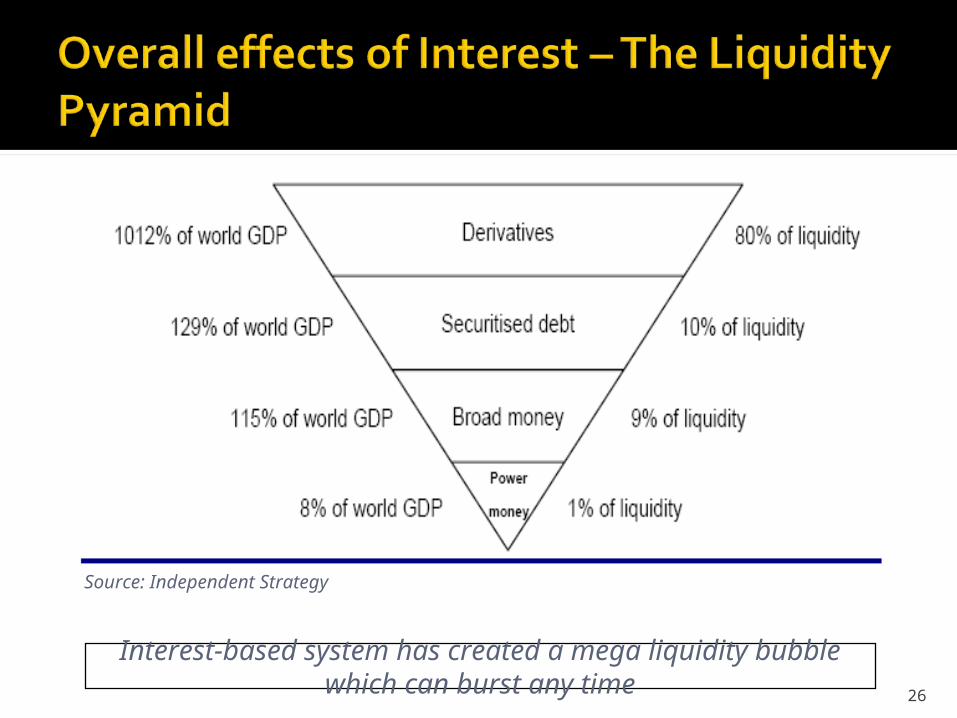

Source: Independent Strategy

Interest-based system has created a mega liquidity bubble which can burst any time

27

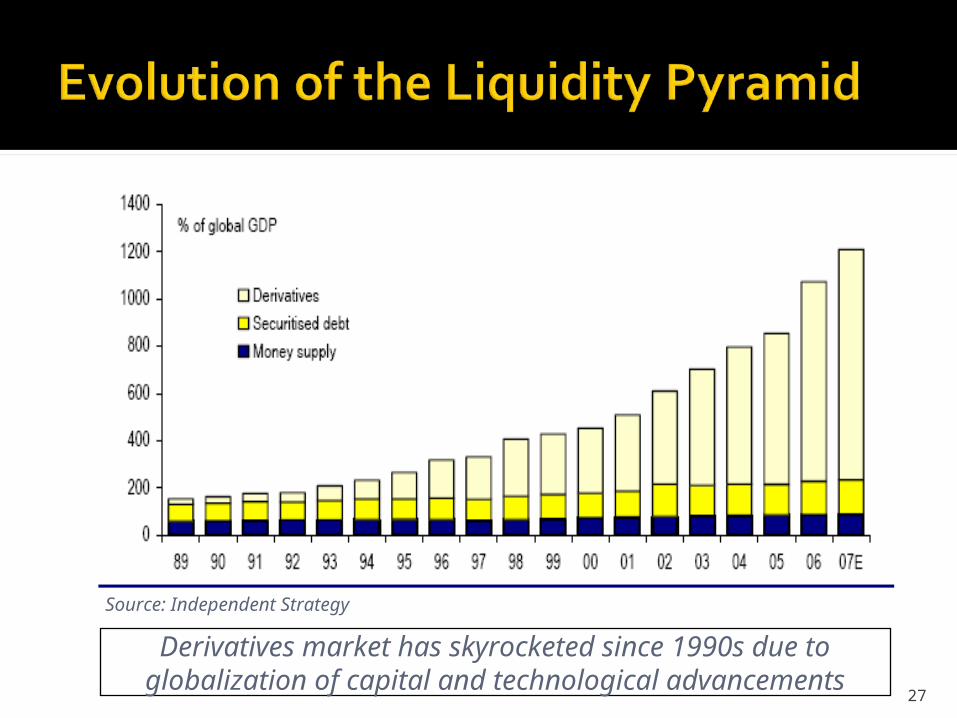

Source: Independent Strategy

Derivatives market has skyrocketed since 1990s due to globalization of capital and technological

advancements

28

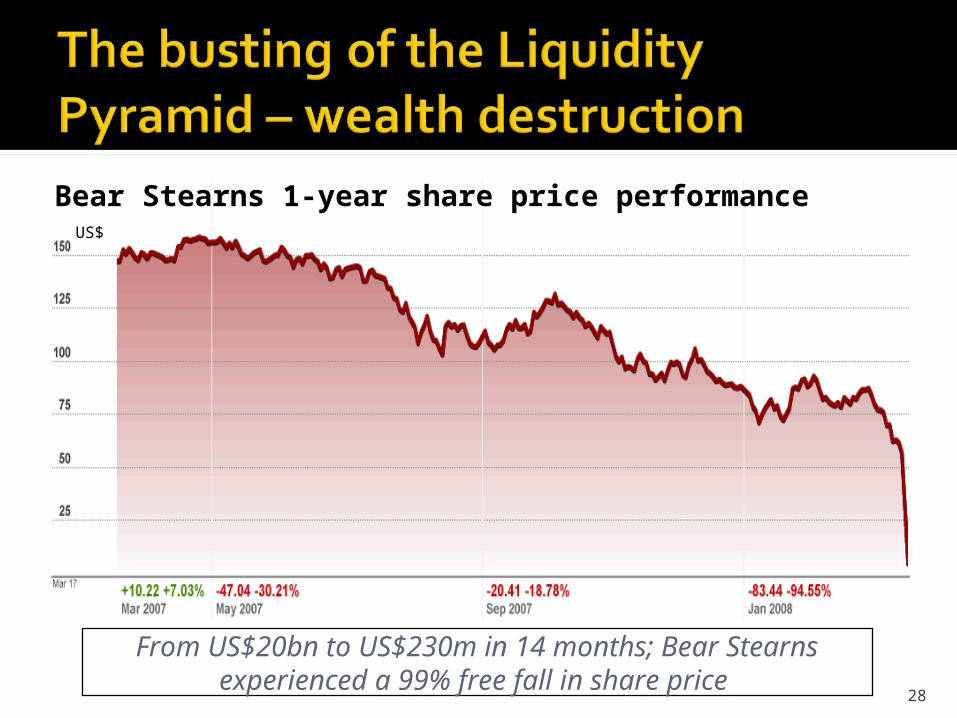

From US$20bn to US$230m in 14 months; Bear Stearns experienced a 99% free fall in share price

Bear Stearns 1-year share price performance US$

The crisis has been called a sub-prime crisis, which led to a liquidity crunch. But it is really a debt crisis involving the entire mortgage industry, bond re-insurers, credit card debt, corporate debt, etc.

The prosperity created in recent years was simply not real or sustainable, it was financial engineering run amok. Real work was shipped to China and India while investment bankers in the West created wealth out of thin air, using leverage like a magician uses sleight of hand during magic tricks to dazzle the audience. Well, the party is over and the effects of de-leveraging will be very painful. [Acamar Economic Journal, March 2008]

29

0

10

20

30

40

50

60

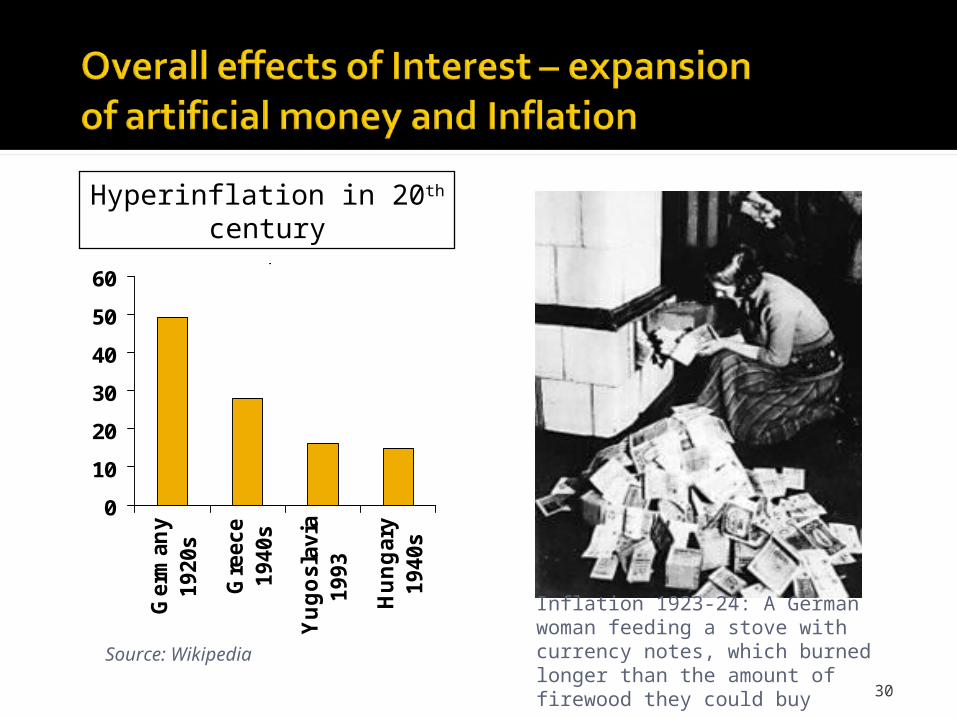

Germany

1920s

Greece

1940s

Yugoslavia

1993

Hungary

1940s

No. of hours before prices double

No. of hours before prices double

30

Inflation 1923-24: A German woman feeding a stove with currency notes, which burned longer than the amount of firewood they could buy

Source: Wikipedia

Hyperinflation in 20th century

Some common myths

31

“O those who believe, do not eat up Riba doubled and redoubled” [Ale Imran – 130]

“And if you repent, yours is your principal” [Baqara – 275 to 281]

The words doubled and redoubled are not restrictive and only used to reflect the worst practice

Also, Hadith clarifies/explains the Quran and we see no evidence that it differentiates between excessive and low rates of Interest

Logically, who will decide what rate of Interest is excessive? Also, excessive is a relative term

32

The basic premise here is that the poor take consumption loans while the rich take commercial loans; charging Interest to the poor is wrong while it is ok to the rich

Some also argue that commercial loans were not there during the time of the Prophet, so the Quran’s references are only for consumption loans

Validity of a transaction is not based on the financial status of a party

Neither the Quran nor the Hadith differentiates between consumption and commercial loans

It is factually incorrect to say that commercial loans were not common at the time of the Prophet (SAW)

Banking transactions go back to 2000 BC Trade related commercial loans were common in Arabia

33

The argument here is that the basic cause (illat) of prohibition of Riba is Zulm (“neither you do wrong nor be wronged” – Baqara 279); if Zulm is not there then the prohibition should not apply

There are two assumptions in the above argument: Basic illat of the prohibition is Zulm There is no Zulm in the modern Interest-based

transactions Zulm is not the illat but the hikmat of

prohibition

34

Illat is the basic feature of a transaction on which the application of the law depends

Hikmat is the wisdom behind the law Example: When the red light is on, every

car has to stop regardless of whether there is traffic or not. Here the illat is the red light while the hikmat is the prevention of accidents

In a loan transaction the basic illat is the predetermined excess over principal, not the Zulm

35

Some argue that Interest has become such an integral part of modern day economy that it is impossible to avoid; it should therefore be permitted using the law of necessity

Shariah acknowledges the doctrine of necessity but only in life-threatening or extreme emergency situations where no other alternative exists, and it is also time-bound

For most of the Muslims today there is no extreme need to take or give interest or participate in such transactions

To a limited extent in foreign transactions only, the law of necessity may be applied by a government transiting to an Islamic economic system

36

Mutashabihat refer to two types of things Initial wordings of some of the Surahs which

were not explained by the Prophet (SAW) Qualities / features of Allah which are beyond

human understanding (eg the hand of Allah) Shariah has not made people

responsible to know the Mutashabihat or act based on them

Then how can Quran declare a war on those who take Riba without first ensuring its proper understanding?

37

No. Quranic verse prohibiting Riba (Ale Imran 130) was revealed as early as in 2nd Hijri

It was only reconfirmed by the Prophet (SAW) in his last sermon

Hazrat Umar’s (RA) statement: The Prophet passed away without adequately explaining Riba, so avoid Riba and everything Riba-like

Here he is referring to Riba al Fazl (which is more complex and dynamic), not Riba al Quran

38

Some common questions…

and their answers

39

It is not necessary to have a ready-made Fatwa on everything we do

Hand on our heart, we should ask ourselves what is right and what is wrong (Hadith: Istafti Qalbak)

Some things are clear-cut black or white, and Interest is one of these

Now we have to decide which side of the fence we want to be on – with Allah and His Messenger or fighting Allah and His Messenger?

40

No Government bonds and other saving

schemes promise a guaranteed fixed return (Interest) along with safety of principal

Islamic alternative Sukuk has recently been introduced and may become available to individual investors in Pakistan in a few years

41

Lottery: A chance for a prize for a price (essential ingredient is to put one’s money at stake in expectation of a reward – not to fulfil a genuine need)

Lotteries of all types are Haram due to the element of Qimar (gambling) which is prohibited in Shariah

Some scholars allow buying prize bonds as long as the intention is to use them as a way to save money (not to benefit from the possible reward); however, if other avenues of saving are available this should not be practised

Some recent lottery schemes are more complex and demand extra care (eg some Internet marketing schemes, TV/radio shows rewarding callers with big prizes on dialling high-priced numbers)

42

Yes, with some restrictions and avoiding certain market practices

Shares/stocks are essentially undivided stakes in the assets of a business; their sale/purchase is allowed in the secondary market

However, (1) the business itself must be Halal, (2) the company should have a mix of liquid and illiquid assets (3) it should not have a large amount of Interest-bearing debt

Some market practices like day-trading (very short term sale/purchase of shares), short selling (selling without owning), borrowing shares on rent, etc are not allowed

In short, simple buying and holding shares (except the negative list as mentioned above) in expectation of dividend and/or capital gains is allowed

43

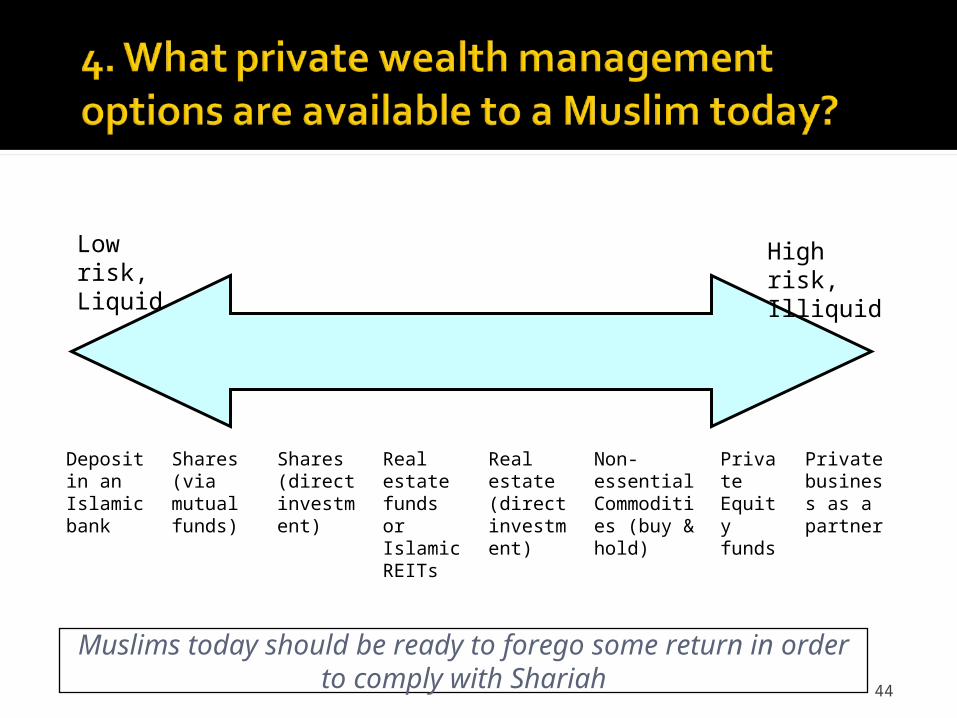

For unsophisticated investors Islamic mutual funds are an excellent way to earn decent returns at a

manageable level of risk

Deposit in an Islamic bank

Shares (via mutual funds)

Shares (direct investment)

Real estate funds or Islamic REITs

Real estate (direct investment)

Non-essential Commodities (buy & hold)

Private Equity funds

Private business as a partner

44

Low risk, Liquid

High risk, Illiquid

Muslims today should be ready to forego some return in order to comply with Shariah

Today’s Islamic banking is just a start, a small step to create an alternative to mainstream conventional banking

Islamic banking is an attempt to help people come out of absolute haram, but it is far away from the true and ideal Islamic financial system

Generally Islamic banking products are designed to comply with the form of Shariah but not necessarily its spirit

A second generation of Islamic banking products is needed – based on real sharing of risk and return – to move from Shariah compliance to Shariah-based or Shariah-driven products

45

Today’s Islamic banking does not fulfill the objectives of Shariah; it is a start but not the end

Islamic car financing scheme or car Ijarah is essentially a rental arrangement, almost similar to rent-a-car schemes

Here the bank is like the owner of rent-a-car business that allows the client to use the car against a monthly rental. Bank assumes all ownership risks

Since current market rental of rent-a-car model is the same as what the bank charges, the scheme is Islamic in nature. However, sale of the car to client at the end of lease period at a deep discount to its market price or as a gift is questionable

46

Leasing a car for personal or company use from a conventional bank under conventional finance lease

arrangement is prohibited

Islamic housing finance is typically done on a Diminishing Musharakah basis, in which both the bank and the client become partners in a property

The client being the resident in the property pays market rental on the bank’s share while under a separate independent arrangement it also buys back periodically the bank’s share at a pre-agreed price

As the client buys the property his rental is reduced and after the mortgage period he becomes 100% owner of the property

47

Obtaining a mortgage for house / commercial property from a conventional bank under

conventional mortgage schemes is not permissible

Islamic financing is always asset-based or asset-backed

Murabaha is the most popular product (>80% of all transactions) for Islamic working capital finance, which is a (deferred) sale on declared profit

The bank buys the required raw material or inventory for the client from a supplier, adds its profit and sells it to the client who pays over 3-12 months period

48

Murabaha is not an ideal mode of Islamic financing, but it is a good first step to get out of absolute haram

If credit cards are used to obtain ‘credit’ (spend now, pay later in instalments on interest) it is not permissible at all

If there is no other option (eg for a frequent traveller) and payment is made to the issuing bank at the end of each month promptly then one is allowed to have a credit card

However, it is not preferable since agreement to pay interest on the outstanding amount is one of the stipulated conditions

The spirit of credit cards (consumerism on borrowed money) is against the spirit of Shariah as well as common sense and financial prudence

It is best to have a debit card, which is totally permissible

49

US is drowned under US$915bn credit card debt; Pakistan has started with US$1bn and will follow the

same path if people do not resist

Bank Interest is haram as explicitly mentioned in the Quran & Hadith, and formally endorsed by the Supreme Court’s detailed verdict in 1999

Present financial system is based on Interest and therefore at war with Allah and His Messenger

We are obligated not to be a part of this system We should try to change the system by:

Switching our bank deposits to current account or accounts in Islamic banks

Switching to permissible financing alternatives for business expansion and personal financing needs

Switching one’s job from conventional banks or insurance companies

50

The essence of Islam is Halal & Haram; the one who does not follow the essence is likely to lose out even if

he is particular about the details

Thank you Questions?

51

The Supreme Court’s Historic Judgment on Interest by Justice (Retd.) Taqi Usmani

Why Islam has prohibited Interest and Islamic alternatives for financing by 1st Ethical Ltd., UK

Introduction to Islamic Finance by Justice (Retd.) Taqi Usmani

New Monetarism by David Roche and Bob McKee (Independent Strategy)

52

Additions: A slide on IndexationMovie clip – In Debt We Trust

53

“They say there are no atheists in a foxhole,” said Harvard economist Jeffrey Frankel, a former Clinton administration official. “Well, there are no libertarians in a financial crisis, either.” (Bloomberg, 15 July 2008)

“To be fair, he's facing problems that no one has ever faced before.” says Peter Wallison, a fellow at the American Enterprise Institute in Washington and a former Treasury general counsel about Henry Paulson, US Treasury Secretary. (Bloomberg, 15 July 2008)

The Securities and Exchange Commission has issued an emergency, temporary rule to curb some short selling in Fannie Mae, Freddie Mac and other financial firms. The rule will be in effect Monday through July 29 and could be extended. The move is the commission's latest effort to crack down on market manipulation. According to the SEC, short selling may exacerbate a loss of confidence in financial markets, prompting panic sales. (Reuters, 15 July 2008)

54

(The regulator) allowed Fannie and Freddie to operate with tiny amounts of capital. The two groups had core capital (as defined by their regulator) of $83.2 billion at the end of 2007; this supported around $5.2 trillion of debt and guarantees, a gearing ratio of 65 to one. According to CreditSights, a research group, Fannie and Freddie were counterparties in $2.3 trillion-worth of derivative transactions, related to their hedging activities. (build a reverse pyramid or bubble chart with size of the bubble showing these amounts)

55

The U.S. Commodities Futures Trading Commission announced on July 18 that it was reclassifying some trading positions that it had reported as commercial hedging positions as noncommercial speculative positions. (Reuters – 6 August 2008)

Revised data show speculators controlled 48% of NYMEX oil futures

CFTC data also reveals one trader controlled 10% of oil futures on exchange (460m barrels)

56

Merrill Lynch’s losses in the past 18 months amount to about a quarter of the profits it has made in its 36 years as a listed company (Financial Times, 1 Sept 2008). [15 days later Bank of America acquired it for US$50bn in an all-stock deal]

“What we had was a financial system where leverage increased quite substantially while credit controls declined. Financial instruments were introduced and nobody had any idea about the risks.” David Dodge, ex-governor, Bank of Canada

57

“All of us didn't recognize the extent to which these off-balance-sheet products would come back to hurt financial institutions. There was a sense that if they were off balance sheet, they couldn't hurt. These products were designed to avoid capital reserves. It was ridiculous.” David Dodge, ex-governor, Bank of Canada

58

So long as AIG continued to be flattered by generous, even unrealistic, credit agency ratings, it seemed to be an excellent counter-party. It increased its systemic importance as it became less stable. This shows yet again how big a mistake lawmakers and regulators have made in putting so much faith in the credit-rating agencies. An alternative method must be found. (FT editorial, 17 Sept. 2008)

59

Bear Stearns' holdings posed a greater risk to the nation's financial institution than did Lehman's. Bear Stearns had $9 trillion worth of financial instruments known as derivatives, much of it shared with other financial institutions such as its eventual buyer, JPMorgan Chase. Lehman had about a tenth that much exposure. "Lehman was only incompetent enough to blow up and destroy themselves, where as Bear's degree of incompetence was enough to threaten the entire financial system," says Barry Ritholtz, CEO of Fusion IQ (FT, 17 Sept 2008)

60

After crackdowns in the U.S. and the U.K. on short selling, Australia, Taiwan and the Netherlands announced restrictions to the strategy. Australia banned short selling of any stock, Taiwan plans to restrict short selling of the market's 150 top stocks and the Dutch regulator prohibited naked short selling of banks for three months. (The Wall Street Journal, 22 Sept 2008)

61

“America is more communist than China right now. This is welfare for the rich” (Jim Rogers, a renowned investor as quoted by Fortune, October 2008)

“The US will lose its status as the superpower of the world financial system. This world will become multi-polar with the emergence of stronger, better capitalized centers in Asia and Europe,” Peer Steinbrück, the German finance minister told the German parliament. “The world will never be the same again.” (FT.com, 26 Sept. 2008)

62

The global derivatives market topped $530 trillion as of June 30, 2008, including $55 trillion in the suddenly popular credit-default swaps; that $530 trillion represents all contracts outstanding. The total dollars at risk is much smaller, but still a hefty $2.7 trillion, according to an estimate by the International Swaps and Derivatives Association. (Washington Post, 15 October 2008)

63