Embed Size (px)

Citation preview

Is your business ready for 2014?

The Affordable Care Act Awaits

Presented By:

Joshua Weinstein, DIA, SVP, Employee Benefits Consultant

WELCOME!

Agenda

IntroductionsACA RecapCurrent ChangesWhat’s to ComeOur Role as Consultants

Q & A

Do you agree or disagree?

Lack of insurance is one of the most

significant barriers to healthcare access.

Main Affordable Care Act Goals

Access – through job or otherwise

Affordable – help is available

Quality – plans must be “good enough”

Get and Stay Well – new wellness benefits

Reduce Waste

Pay for Performance not Transactions

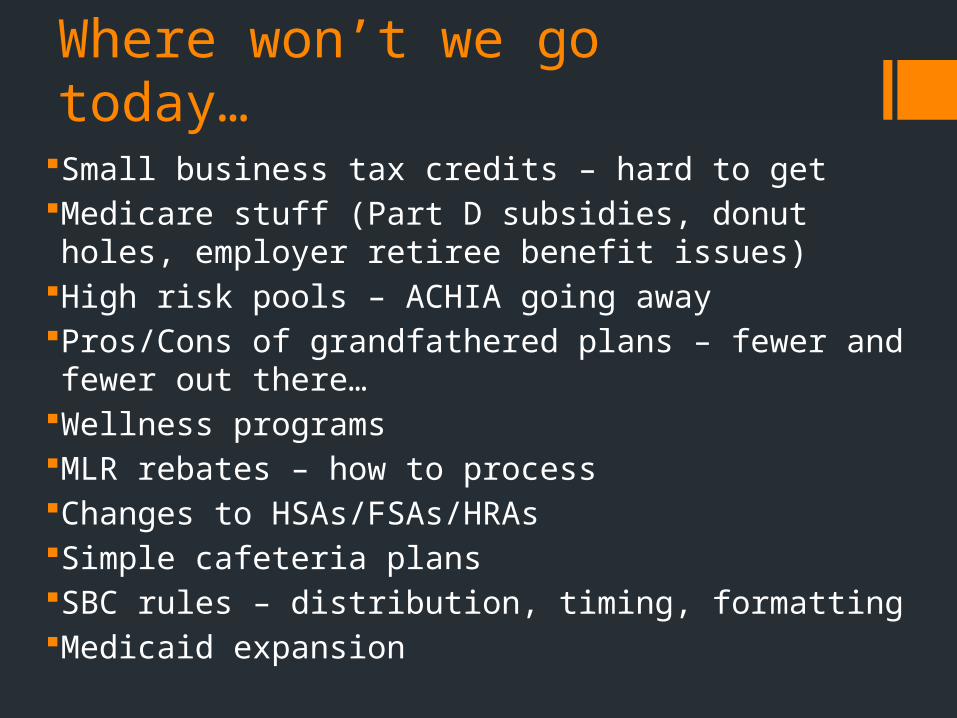

Where won’t we go today…Small business tax credits – hard to getMedicare stuff (Part D subsidies, donut holes, employer retiree benefit issues)

High risk pools – ACHIA going awayPros/Cons of grandfathered plans – fewer and fewer out there…

Wellness programsMLR rebates – how to processChanges to HSAs/FSAs/HRAsSimple cafeteria plansSBC rules – distribution, timing, formattingMedicaid expansion

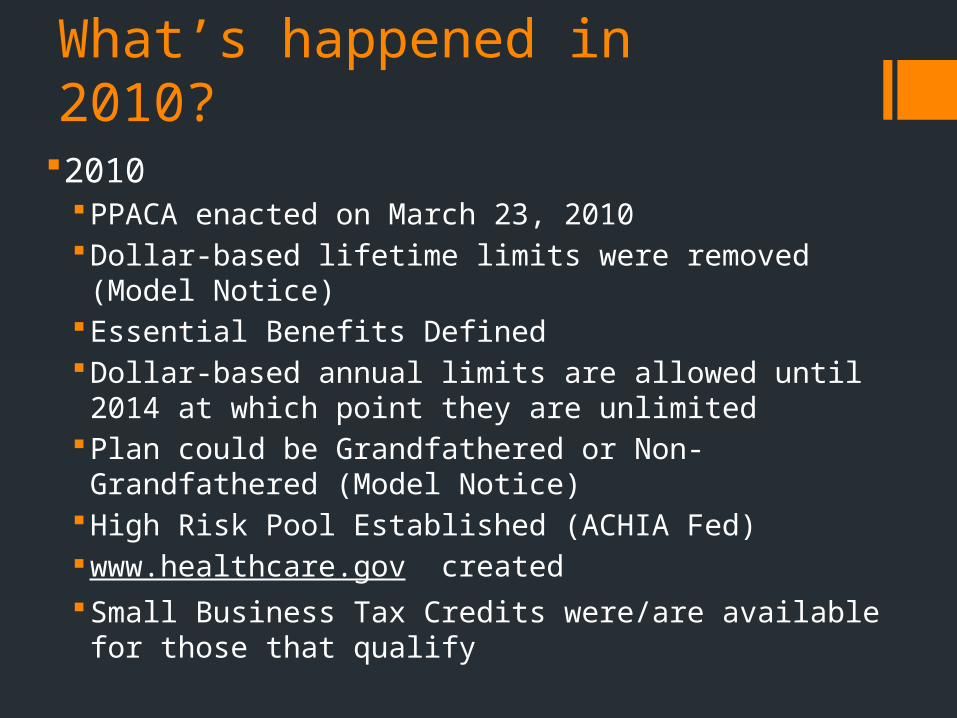

What’s happened in 2010?2010

PPACA enacted on March 23, 2010Dollar-based lifetime limits were removed (Model Notice)Essential Benefits DefinedDollar-based annual limits are allowed until 2014 at which

point they are unlimitedPlan could be Grandfathered or Non-Grandfathered

(Model Notice)High Risk Pool Established (ACHIA Fed)www.healthcare.gov createdSmall Business Tax Credits were/are available for those

that qualify

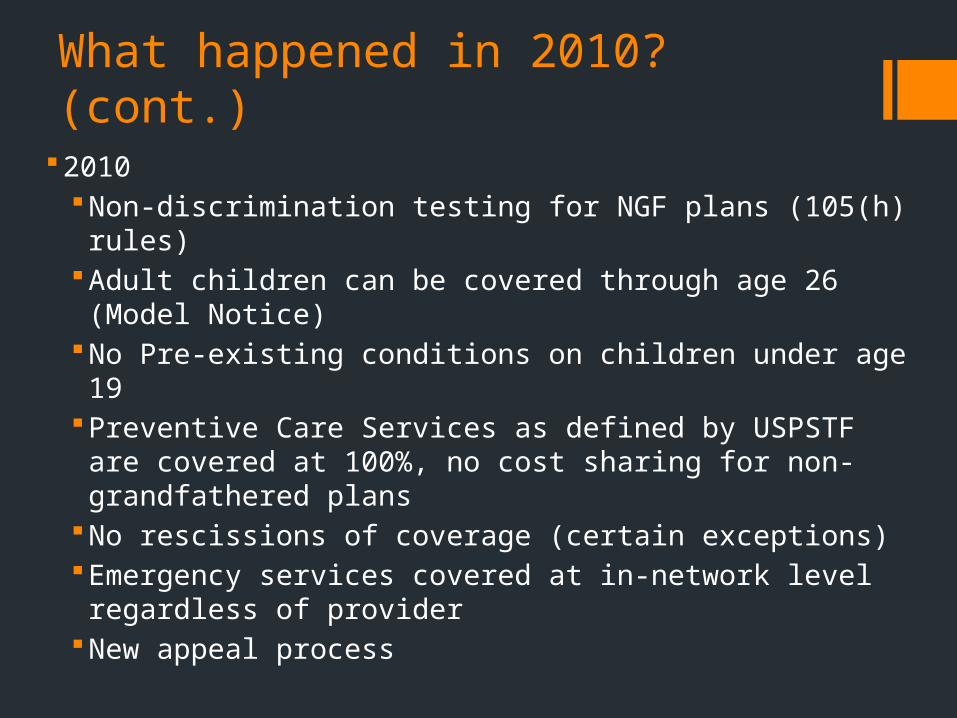

What happened in 2010? (cont.)2010

Non-discrimination testing for NGF plans (105(h) rules)Adult children can be covered through age 26 (Model

Notice)No Pre-existing conditions on children under age 19Preventive Care Services as defined by USPSTF are

covered at 100%, no cost sharing for non-grandfathered plans

No rescissions of coverage (certain exceptions)Emergency services covered at in-network level

regardless of providerNew appeal process

What happened in 2011?

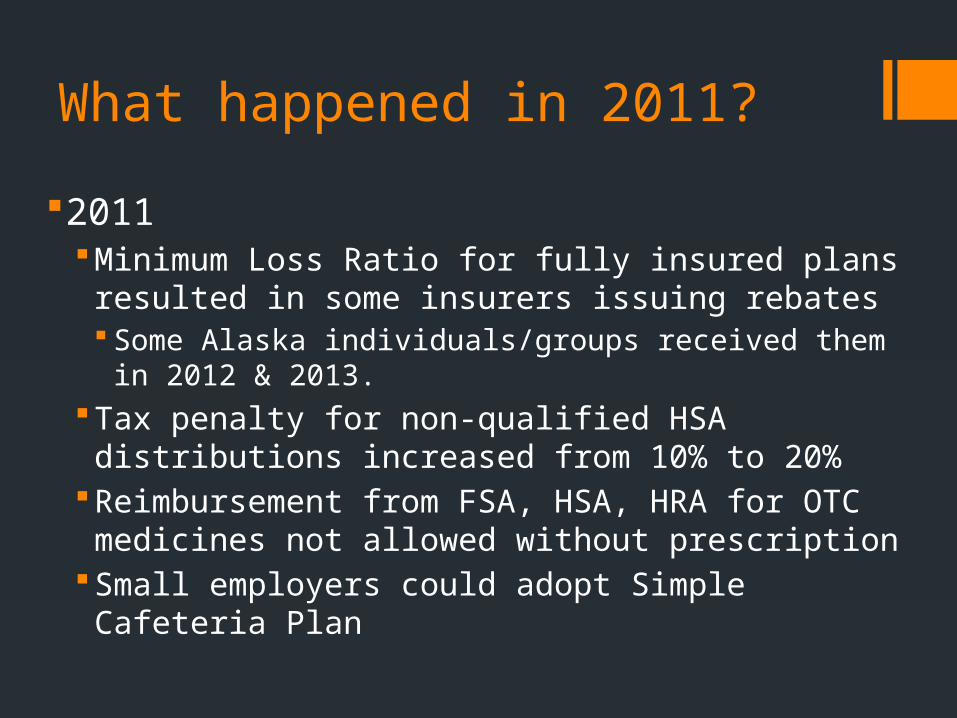

2011Minimum Loss Ratio for fully insured plans resulted in

some insurers issuing rebates Some Alaska individuals/groups received them in 2012 &

2013.Tax penalty for non-qualified HSA distributions increased

from 10% to 20%Reimbursement from FSA, HSA, HRA for OTC medicines

not allowed without prescriptionSmall employers could adopt Simple Cafeteria Plan

What happened in 2012?

2012Summary of Benefits & Coverage (SBC) must be

distributed for groups with renewals 10/1/2012 forwardW-2 reporting for employers filing 250 or more W-2’s in

calendar year (2013)Expansion of Women’s Health Preventive Services,

including no cost-sharing for contraceptives

What happened 2013?2013

PCORI Tax on fully insured and self-funded group health plans (HRA’s affected)

FSA medical - employee contributions are capped at $2,500 per year

Medicare payroll tax increases 0.9% for individual filers over $200K and joint filers over $250K Additional 3.8% Medicare contribution on certain unearned income

for high income individuals

Itemization of unreimbursed medical expenses increases from 7.5% of AGI to 10% of AGI

Notice of Exchange/Marketplace by 10/1/2013

What’s coming next

?

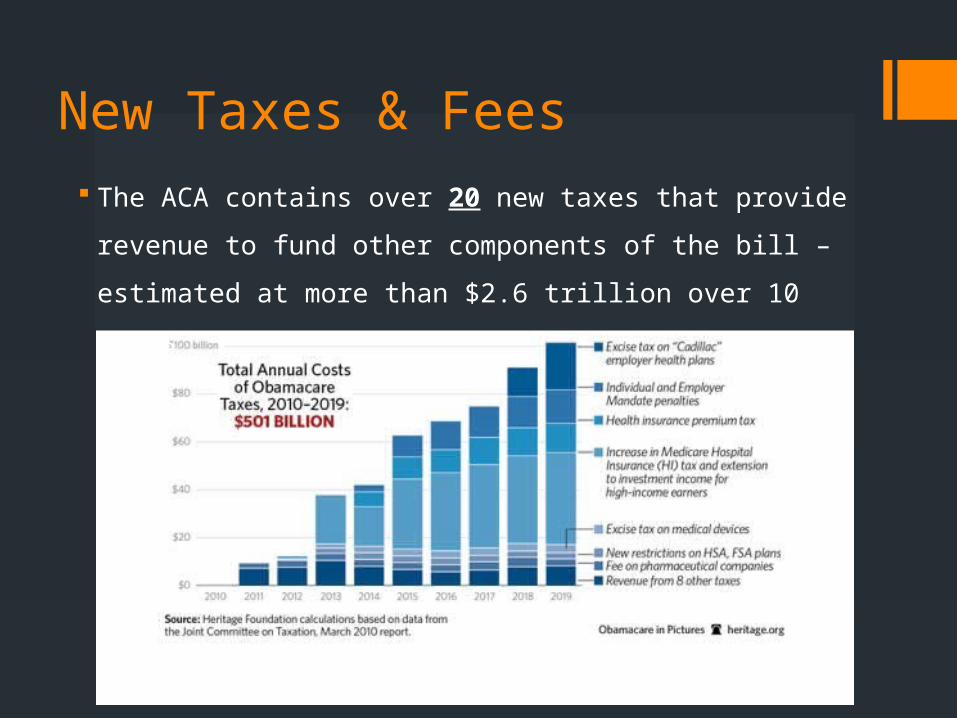

New Taxes & Fees The ACA contains over 20 new taxes that provide revenue to fund

other components of the bill – estimated at more than $2.6 trillion

over 10 years

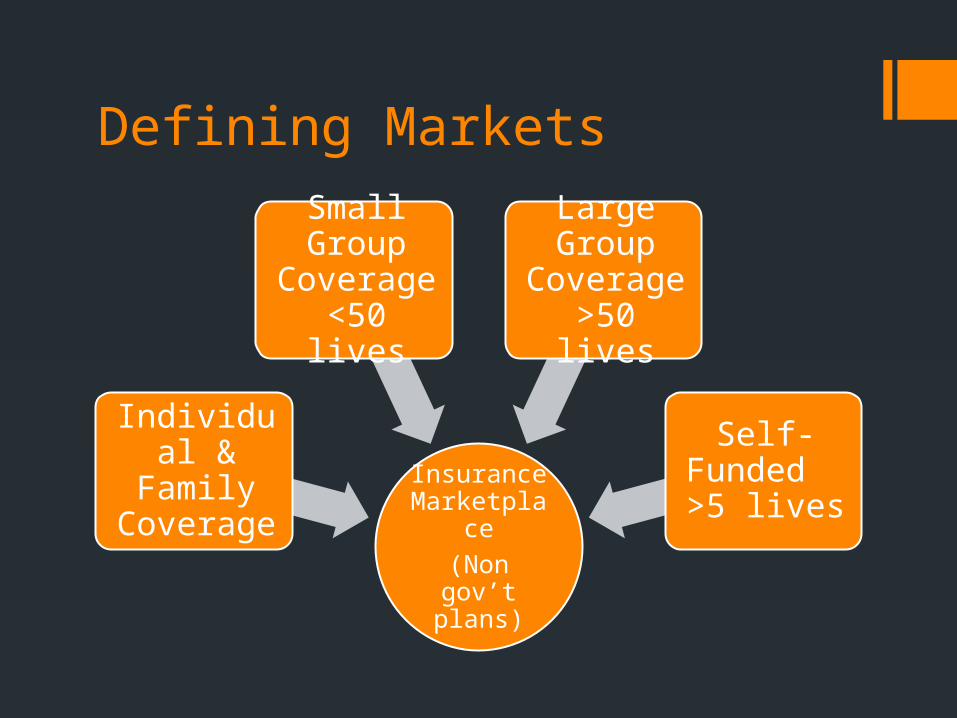

Defining Markets

Insurance Marketplace

(Non gov’t plans)

Individual & Family

Coverage

Small Group

Coverage <50 lives

Large Group

Coverage >50 lives

Self-Funded >5 lives

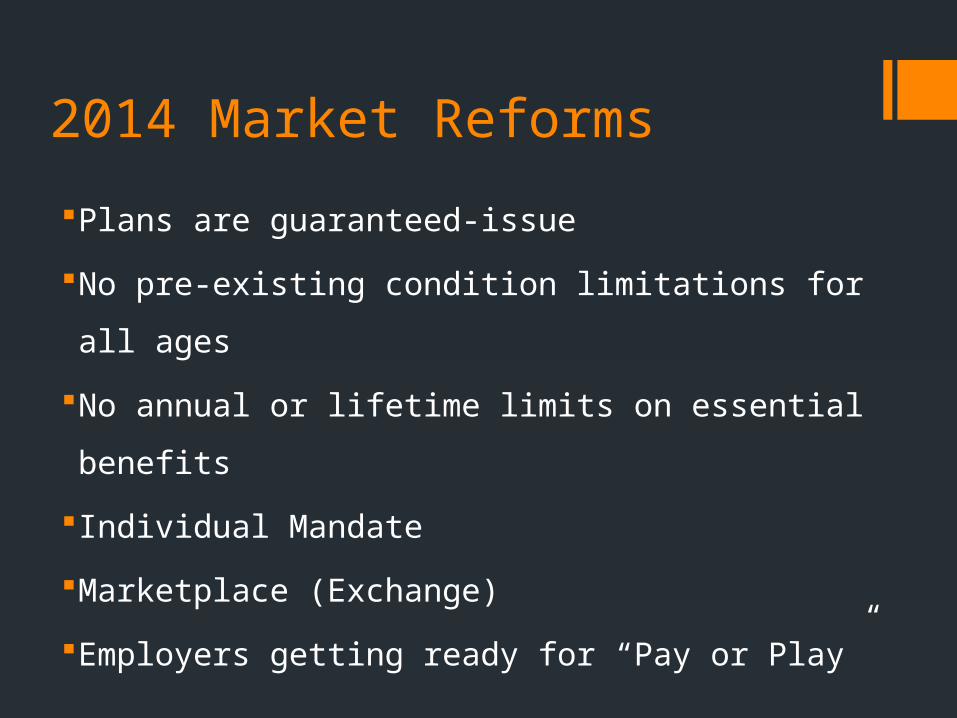

2014 Market Reforms

Plans are guaranteed-issue

No pre-existing condition limitations for all ages

No annual or lifetime limits on essential benefits

Individual Mandate

Marketplace (Exchange)

Employers getting ready for “Pay or Play”

Individual & Family Coverage

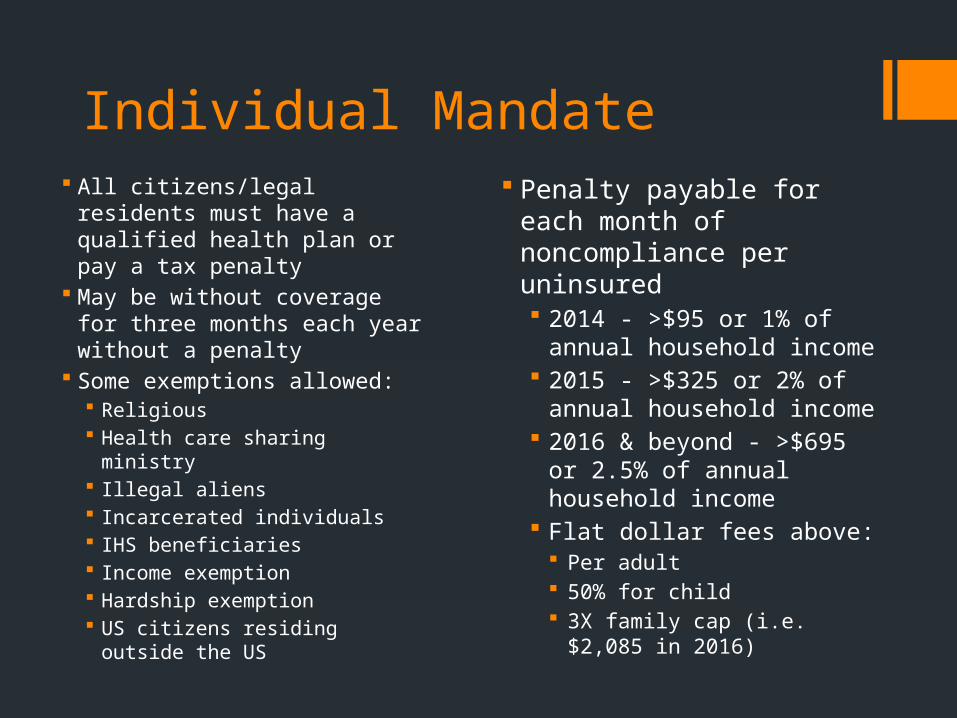

Individual Mandate All citizens/legal residents

must have a qualified health plan or pay a tax penalty

May be without coverage for three months each year without a penalty

Some exemptions allowed: Religious Health care sharing ministry Illegal aliens Incarcerated individuals IHS beneficiaries Income exemption Hardship exemption US citizens residing outside

the US

Penalty payable for each month of noncompliance per uninsured 2014 - >$95 or 1% of annual

household income 2015 - >$325 or 2% of annual

household income 2016 & beyond - >$695 or

2.5% of annual household income

Flat dollar fees above: Per adult 50% for child 3X family cap (i.e. $2,085 in

2016)

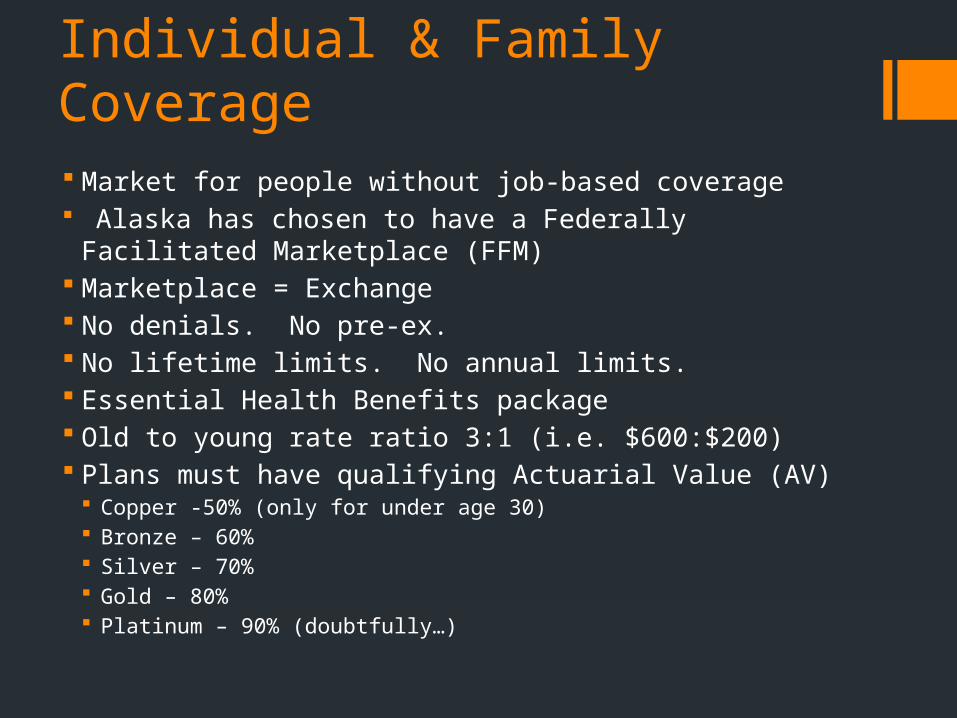

Individual & Family Coverage Market for people without job-based coverage Alaska has chosen to have a Federally Facilitated Marketplace

(FFM) Marketplace = Exchange No denials. No pre-ex. No lifetime limits. No annual limits. Essential Health Benefits package Old to young rate ratio 3:1 (i.e. $600:$200) Plans must have qualifying Actuarial Value (AV)

Copper -50% (only for under age 30) Bronze – 60% Silver – 70% Gold – 80% Platinum – 90% (doubtfully…)

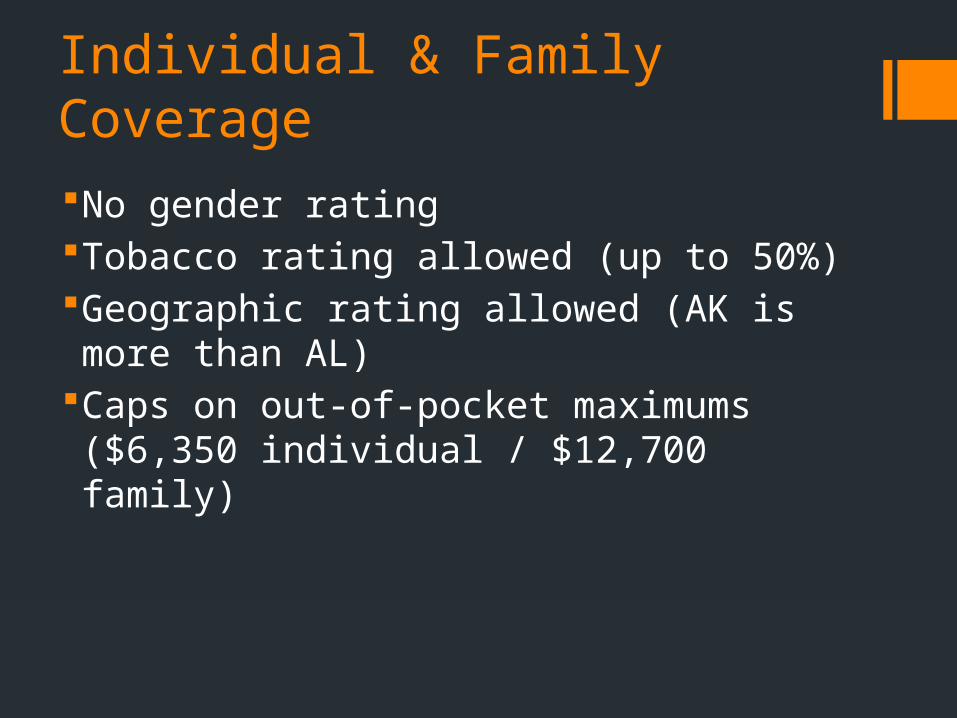

Individual & Family CoverageNo gender ratingTobacco rating allowed (up to 50%)Geographic rating allowed (AK is more than AL)

Caps on out-of-pocket maximums ($6,350 individual / $12,700 family)

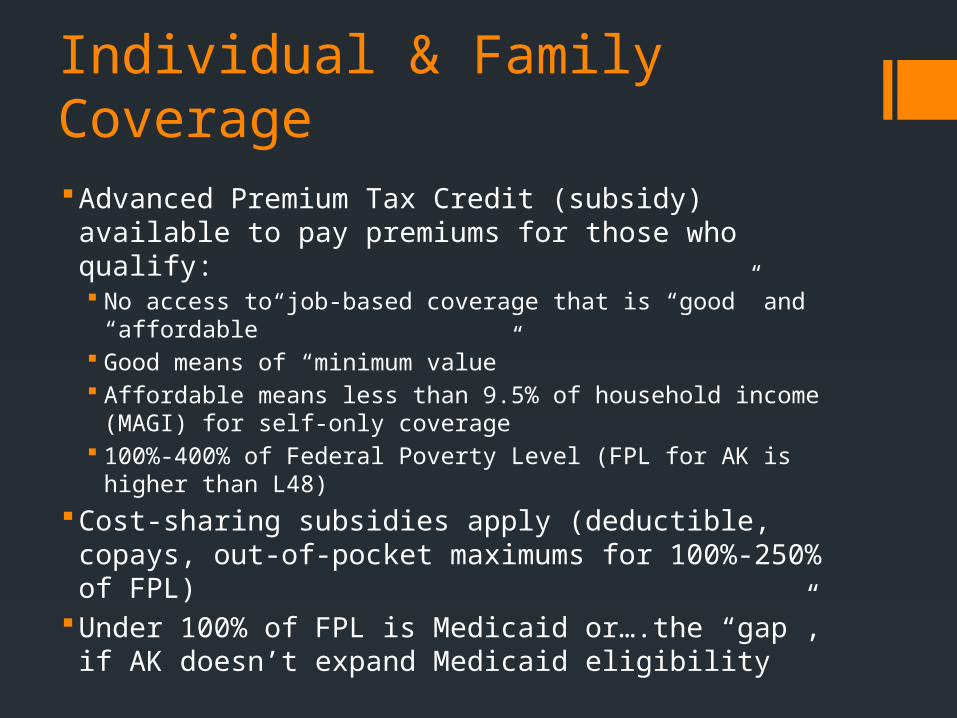

Individual & Family CoverageAdvanced Premium Tax Credit (subsidy) available to

pay premiums for those who qualify: No access to job-based coverage that is “good” and

“affordable” Good means of “minimum value” Affordable means less than 9.5% of household income (MAGI)

for self-only coverage 100%-400% of Federal Poverty Level (FPL for AK is higher

than L48)

Cost-sharing subsidies apply (deductible, copays, out-of-pocket maximums for 100%-250% of FPL)

Under 100% of FPL is Medicaid or….the “gap”, if AK doesn’t expand Medicaid eligibility

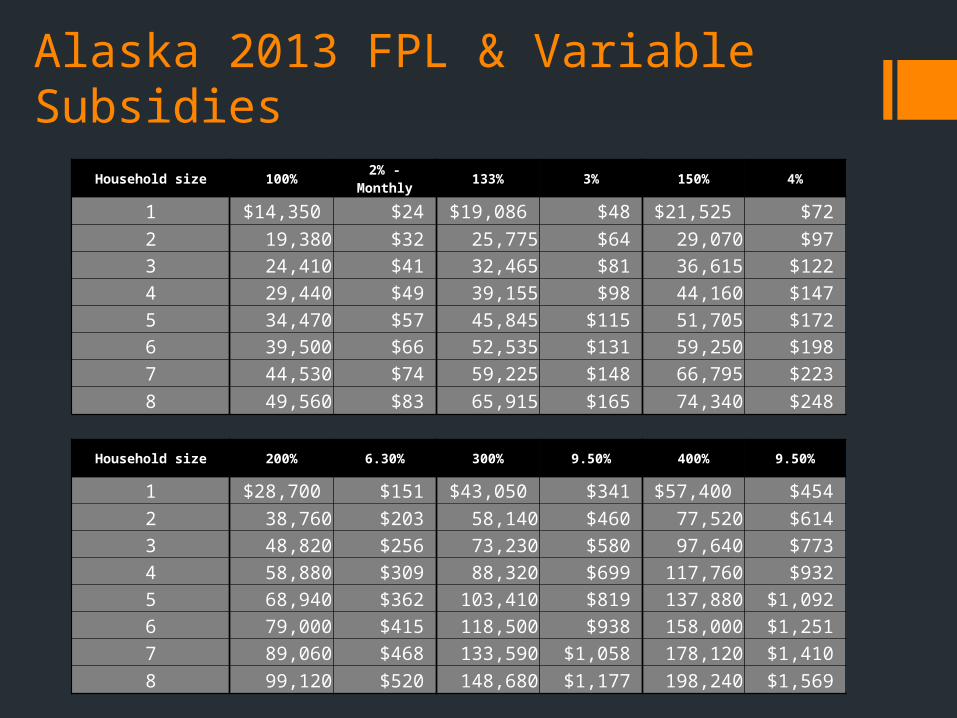

Alaska 2013 FPL & Variable SubsidiesHousehold size 100% 2% -

Monthly133% 3% 150% 4%

1 $14,350 $24 $19,086 $48 $21,525 $72

2 19,380 $32 25,775 $64 29,070 $97 3 24,410 $41 32,465 $81 36,615 $122 4 29,440 $49 39,155 $98 44,160 $147 5 34,470 $57 45,845 $115 51,705 $172 6 39,500 $66 52,535 $131 59,250 $198 7 44,530 $74 59,225 $148 66,795 $223

8 49,560 $83 65,915 $165 74,340 $248

Household size 200% 6.30% 300% 9.50% 400% 9.50%

1 $28,700 $151 $43,050 $341 $57,400 $454

2 38,760 $203 58,140 $460 77,520 $614 3 48,820 $256 73,230 $580 97,640 $773 4 58,880 $309 88,320 $699 117,760 $932 5 68,940 $362 103,410 $819 137,880 $1,092 6 79,000 $415 118,500 $938 158,000 $1,251 7 89,060 $468 133,590 $1,058 178,120 $1,410

8 99,120 $520 148,680 $1,177 198,240 $1,569

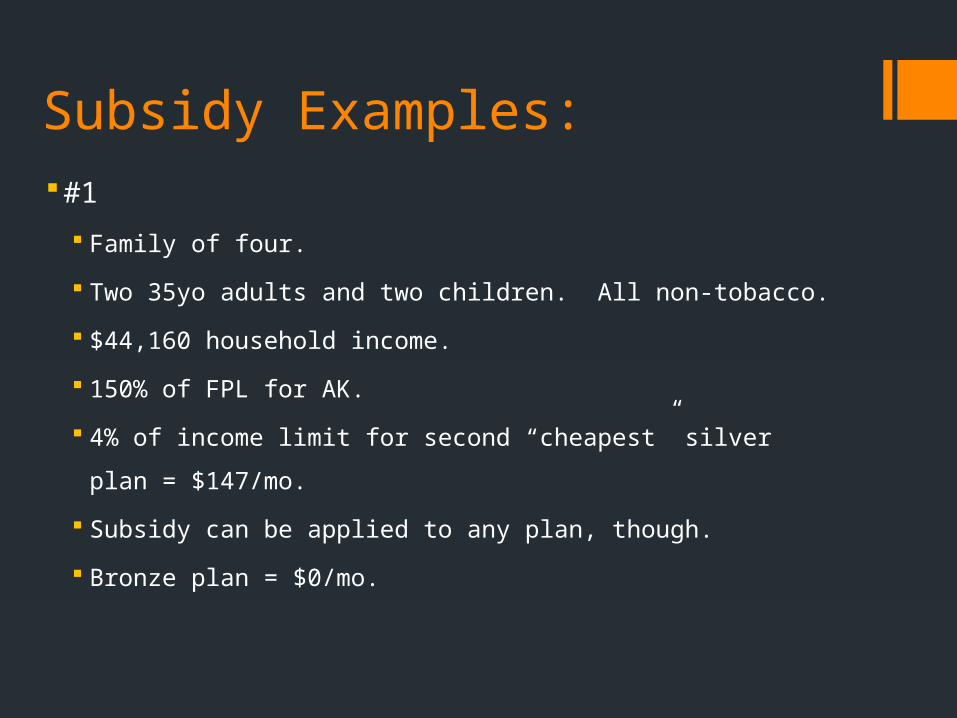

Subsidy Examples:#1

Family of four.

Two 35yo adults and two children. All non-tobacco.

$44,160 household income.

150% of FPL for AK.

4% of income limit for second “cheapest” silver plan =

$147/mo.

Subsidy can be applied to any plan, though.

Bronze plan = $0/mo.

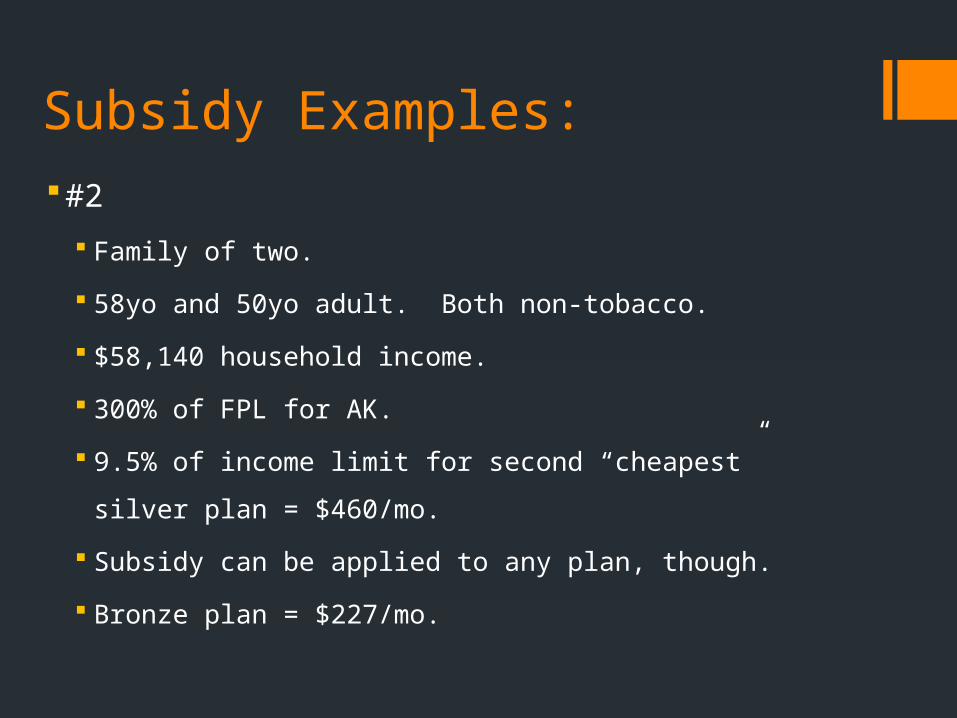

Subsidy Examples:#2

Family of two.

58yo and 50yo adult. Both non-tobacco.

$58,140 household income.

300% of FPL for AK.

9.5% of income limit for second “cheapest” silver plan =

$460/mo.

Subsidy can be applied to any plan, though.

Bronze plan = $227/mo.

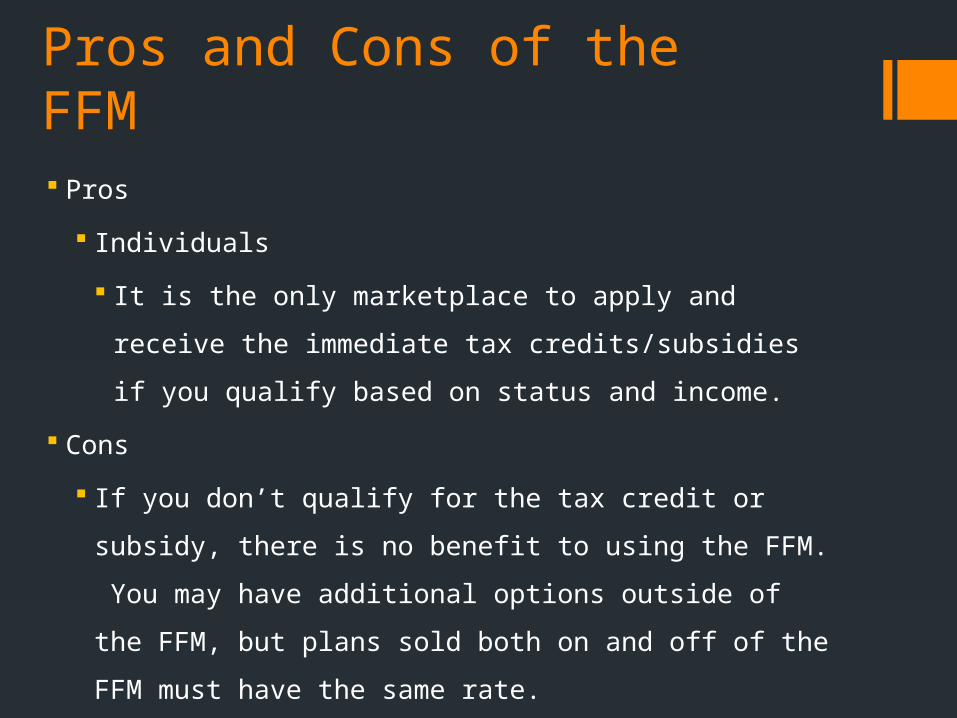

Pros and Cons of the FFM Pros

Individuals

It is the only marketplace to apply and receive the immediate

tax credits/subsidies if you qualify based on status and

income.

Cons

If you don’t qualify for the tax credit or subsidy, there is no

benefit to using the FFM. You may have additional options

outside of the FFM, but plans sold both on and off of the FFM

must have the same rate.

Employer Sponsored Coverage

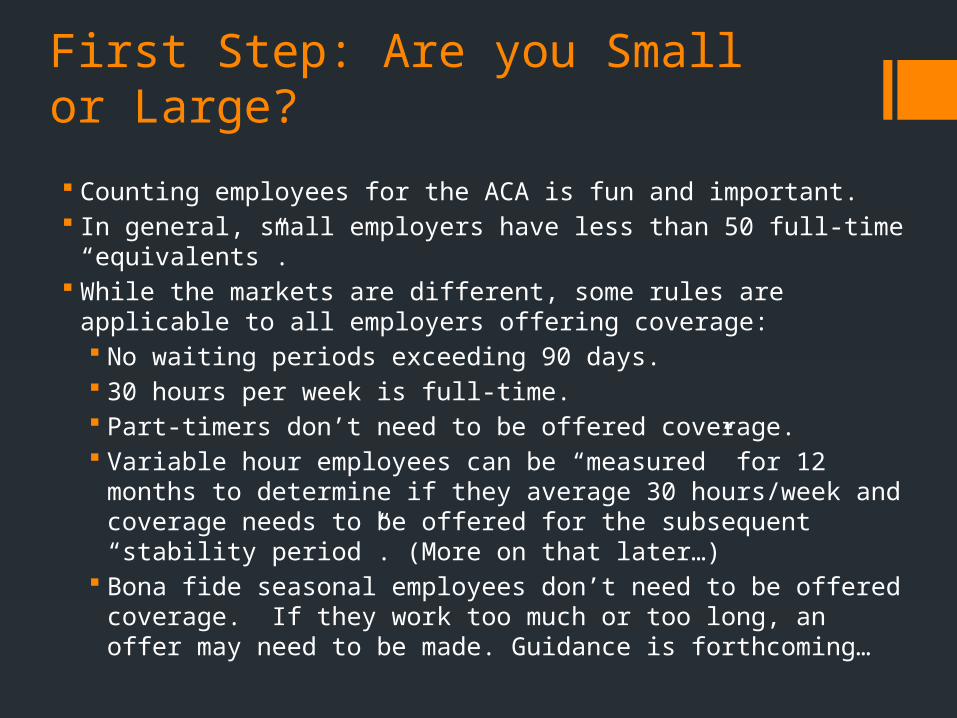

First Step: Are you Small or Large?

Counting employees for the ACA is fun and important. In general, small employers have less than 50 full-time “equivalents”. While the markets are different, some rules are applicable to all

employers offering coverage: No waiting periods exceeding 90 days. 30 hours per week is full-time. Part-timers don’t need to be offered coverage. Variable hour employees can be “measured” for 12 months to

determine if they average 30 hours/week and coverage needs to be offered for the subsequent “stability period”. (More on that later…)

Bona fide seasonal employees don’t need to be offered coverage. If they work too much or too long, an offer may need to be made. Guidance is forthcoming…

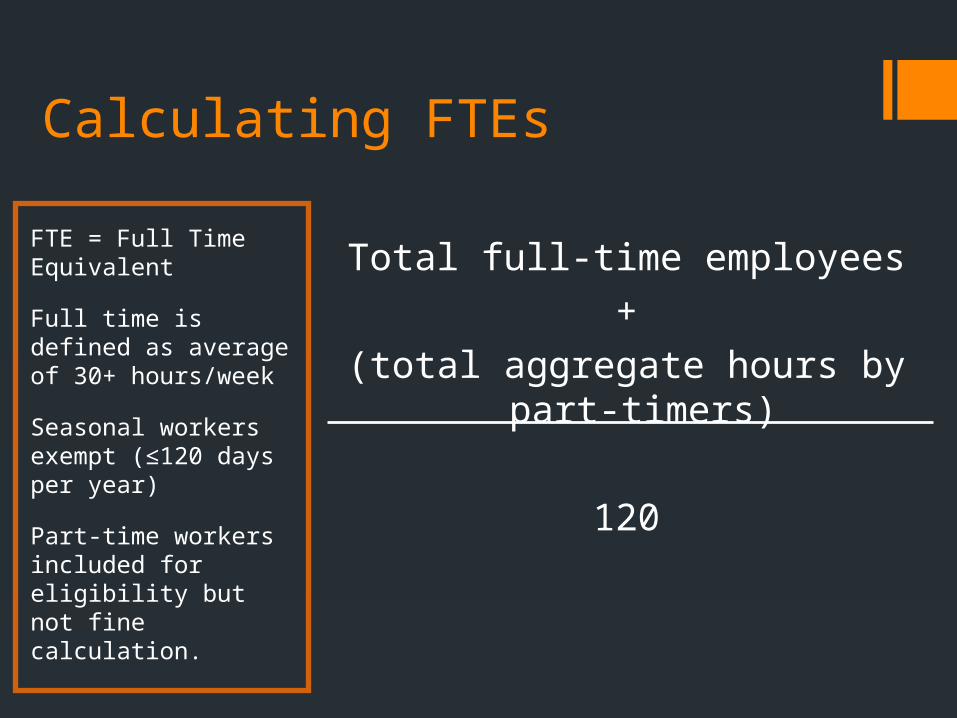

Calculating FTEs

FTE = Full Time Equivalent

Full time is defined as average of 30+ hours/week

Seasonal workers exempt (≤120 days per year)

Part-time workers included for eligibility but not fine calculation.

Total full-time employees

+

(total aggregate hours by part-timers)

120

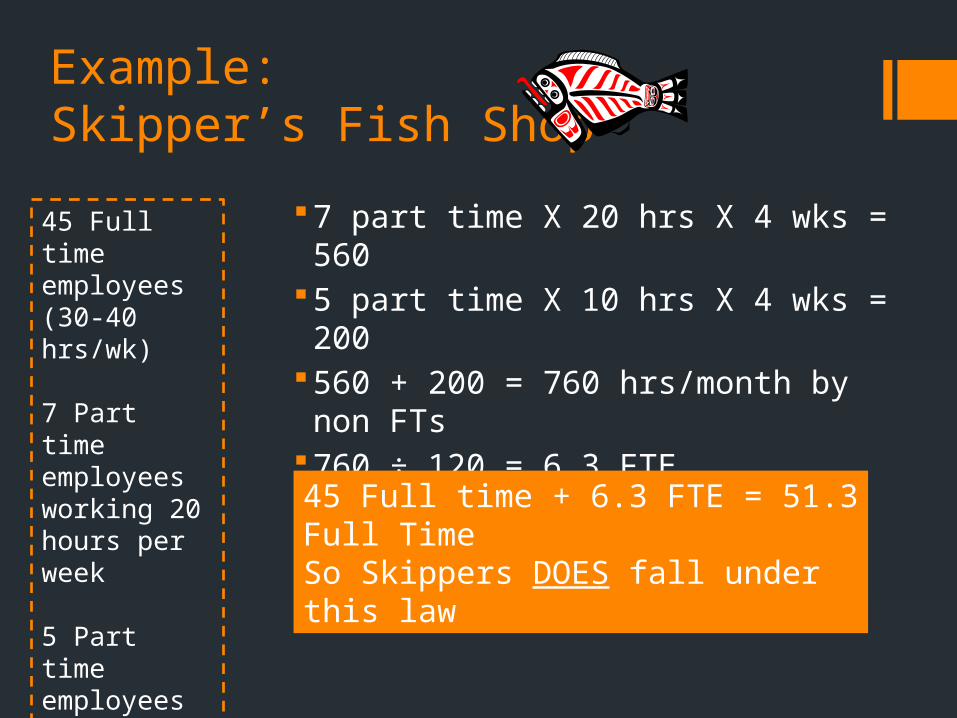

Example: Skipper’s Fish Shop

7 part time X 20 hrs X 4 wks = 5605 part time X 10 hrs X 4 wks = 200560 + 200 = 760 hrs/month by non FTs760 ÷ 120 = 6.3 FTE

45 Full time employees (30-40 hrs/wk)

7 Part time employees working 20 hours per week

5 Part time employees working 10 hours a week

45 Full time + 6.3 FTE = 51.3 Full TimeSo Skippers DOES fall under this law

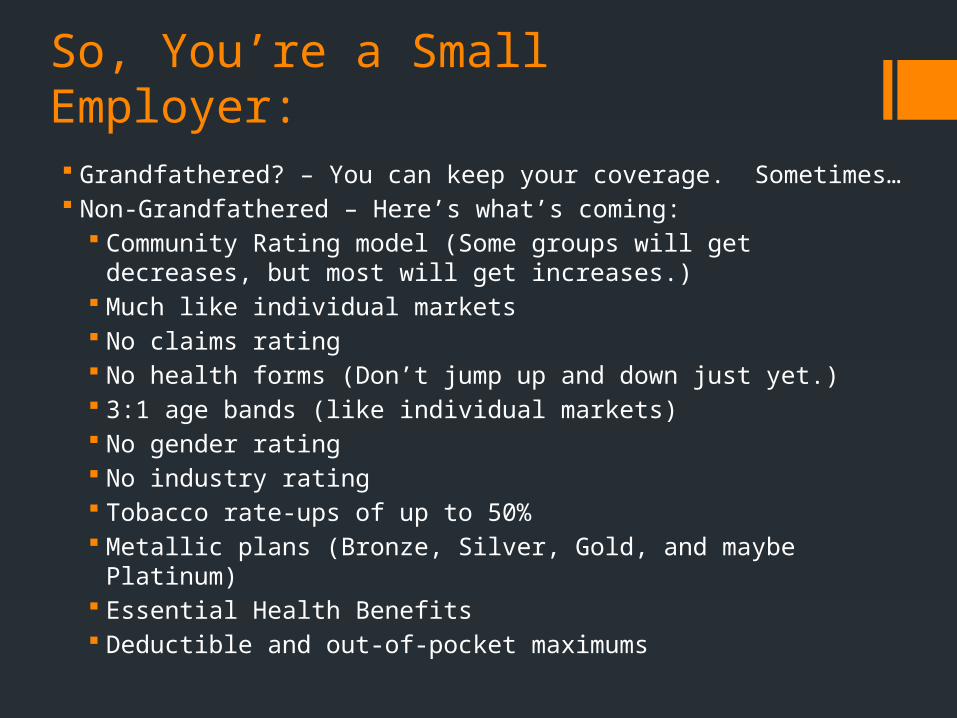

So, You’re a Small Employer: Grandfathered? – You can keep your coverage. Sometimes… Non-Grandfathered – Here’s what’s coming:

Community Rating model (Some groups will get decreases, but most will get increases.)

Much like individual markets No claims rating No health forms (Don’t jump up and down just yet.) 3:1 age bands (like individual markets) No gender rating No industry rating Tobacco rate-ups of up to 50% Metallic plans (Bronze, Silver, Gold, and maybe Platinum) Essential Health Benefits Deductible and out-of-pocket maximums

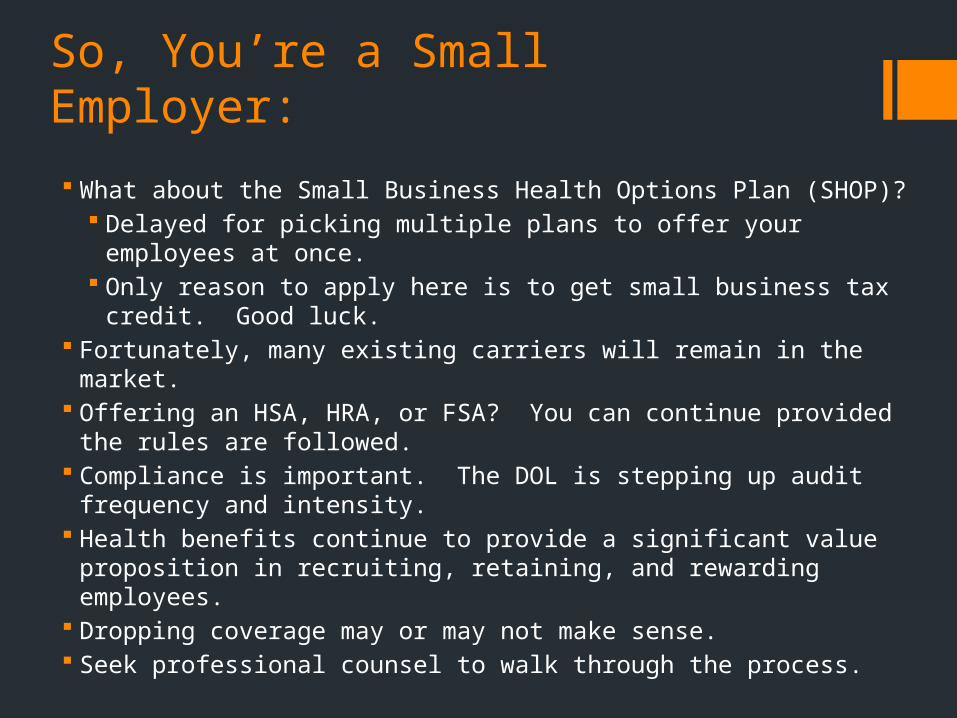

So, You’re a Small Employer:

What about the Small Business Health Options Plan (SHOP)? Delayed for picking multiple plans to offer your employees at once. Only reason to apply here is to get small business tax credit. Good

luck. Fortunately, many existing carriers will remain in the market. Offering an HSA, HRA, or FSA? You can continue provided the rules

are followed. Compliance is important. The DOL is stepping up audit frequency

and intensity. Health benefits continue to provide a significant value proposition in

recruiting, retaining, and rewarding employees. Dropping coverage may or may not make sense. Seek professional counsel to walk through the process.

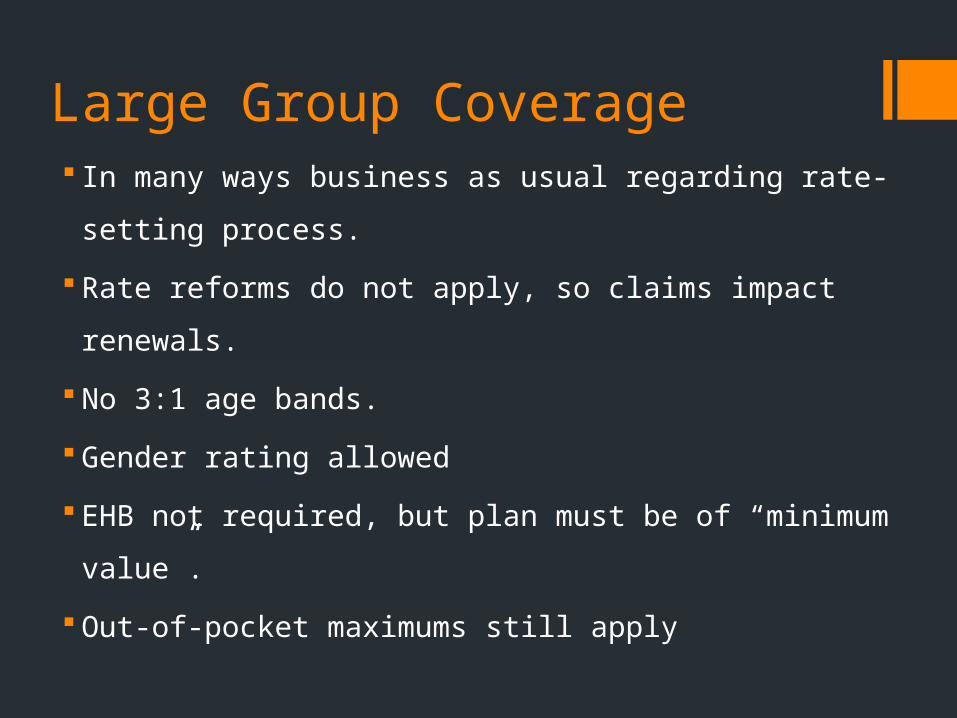

Large Group Coverage In many ways business as usual regarding rate-setting process.

Rate reforms do not apply, so claims impact renewals.

No 3:1 age bands.

Gender rating allowed

EHB not required, but plan must be of “minimum value”.

Out-of-pocket maximums still apply

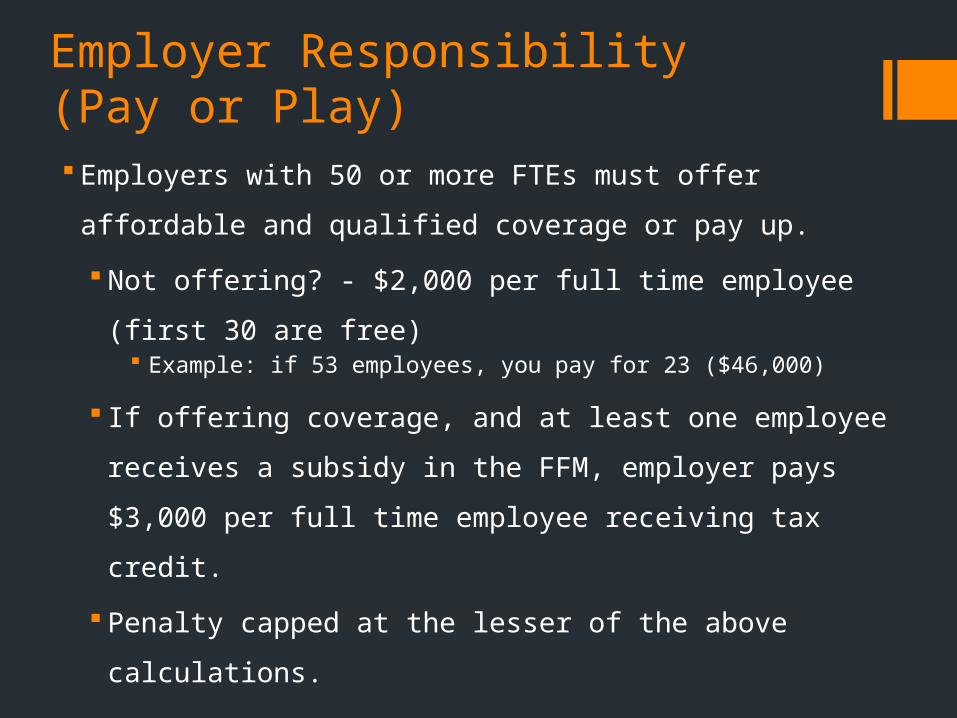

Employer Responsibility(Pay or Play) Employers with 50 or more FTEs must offer affordable and

qualified coverage or pay up.

Not offering? - $2,000 per full time employee (first 30 are

free) Example: if 53 employees, you pay for 23 ($46,000)

If offering coverage, and at least one employee receives a

subsidy in the FFM, employer pays $3,000 per full time

employee receiving tax credit.

Penalty capped at the lesser of the above calculations.

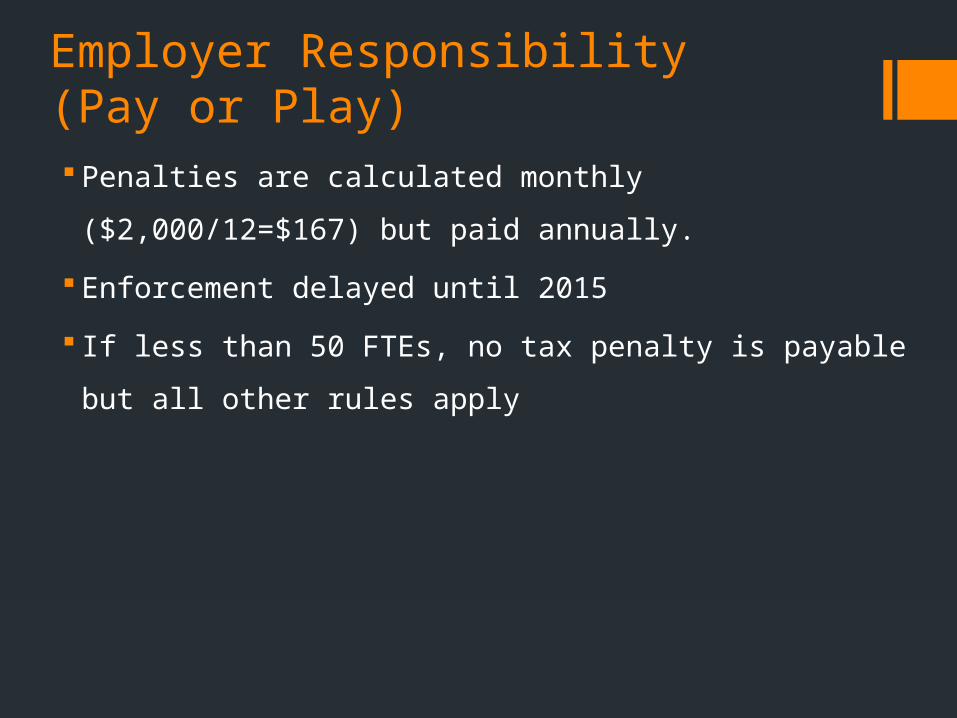

Employer Responsibility(Pay or Play) Penalties are calculated monthly ($2,000/12=$167) but paid

annually.

Enforcement delayed until 2015

If less than 50 FTEs, no tax penalty is payable but all other

rules apply

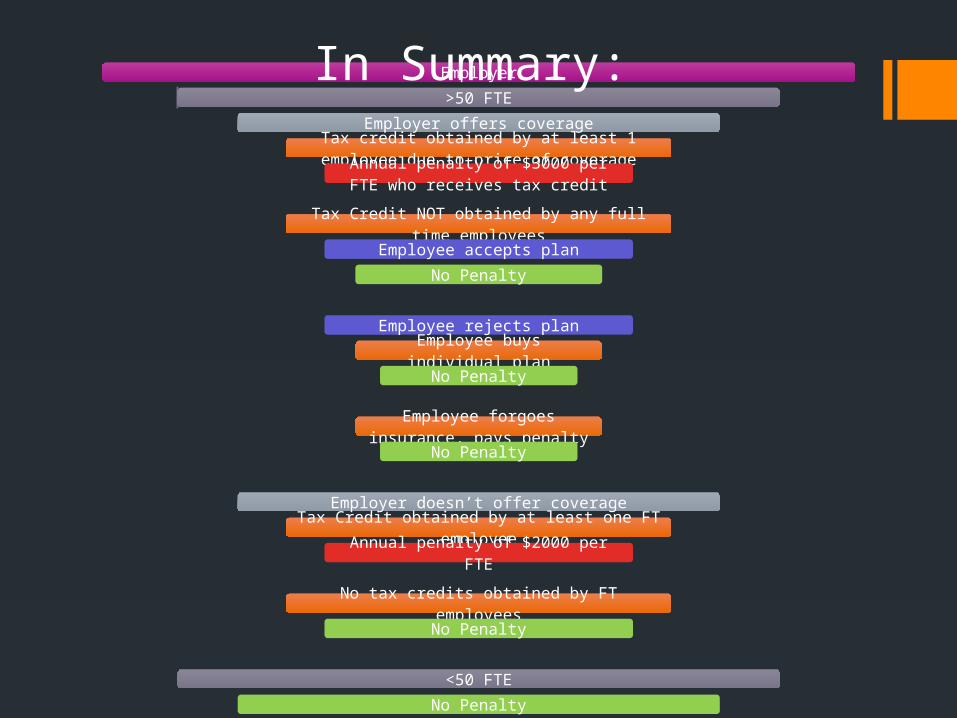

Employer

>50 FTE

Employer offers coverageTax credit obtained by at least 1 employee due to

price of coverageAnnual penalty of $3000 per FTE who receives tax credit

Tax Credit NOT obtained by any full time employees

Employee accepts plan

No Penalty

Employee rejects plan

Employee buys individual plan

No Penalty

Employee forgoes insurance, pays penaltyNo Penalty

Employer doesn’t offer coverage

Tax Credit obtained by at least one FT employee

Annual penalty of $2000 per FTE

No tax credits obtained by FT employees

No Penalty

<50 FTE

No Penalty

In Summary:

Safe Harbors for Applicable Employers – 30 hour rule Safe harbor rules are available if you want to examine your

employee population to determine more precisely who should be

deemed full time under the proposed regulations.

You do not have to use these safe harbors but they are available.

The basic concept of the safe harbor is to utilize both a look back

or measurement period and a look forward or stability period.

Utilization of the safe harbor may be a good idea for your ongoing

employees if you are uncertain on average how many hours per

week your non-exempt employees actually work.

Auto-EnrollmentEmployers with 200+ employeesAuto-enroll all new employees in employer planWaiting period 90 days or less okayEmployees may opt out if other coverage

NOTE: Effective date is unclear – may be sooner or later…or never.

Self-Funded Plans Expected growth area for group health plans Available to groups with at least 5 employees Escape some (but not all) taxation versus fully insured plans Allows greater customization of plan design State mandates are optional. Use of stop-loss coverage to insure large claims and manage

financial exposure. Offers potential for savings with known “maximum costs”. Not subject to new rating rules of small group markets

Cadillac Tax 2018 All group plans, including self-funded Paid by insurer or TPA, but passed on to employer 40% excise tax on plans with value exceeding:

$10,200 for individual coverage $27,500 for family coverage Higher thresholds for retirees over 55 & high risk professions

Tax indexed annually for inflation (CPI)

Not very popular provision and most likely will be modified

Who is NBG?

Full service agency providing insurance solutions for both individuals and businesses

Alaskan owned and operated Alaskan-based businesses

with 2-1,000 employees In business for over 35 years Affiliate of Northrim Bank

since 2005

Customer Service Wide variety of products

and services On-site consultations and

education meetings Transparency regarding all

fees and costs Creative Fully licensed firm and staff

For a more details visit our website: northrimbenefits.com

What about Alaskans without Job-Based Coverage?

Historically, individual markets have been “tricky” due to

denials of coverage and a challenging underwriting process.

The challenges change in 2014.

While coverage is guaranteed, main hurdles to overcome are:

Getting education about the ACA

Figuring out subsidy eligibility (i.e. “Can I get financial help?”)

Working with new Marketplace

Sorting through multiple plans (Bronzes, Silvers, Golds…)

Going through the cumbersome application process

NBG saw a huge opportunity…

We can help individual markets, but how do we

go about it?

Build a new division of NBG!

Say a Welcome to:

Enroll Alaska is a division of NBG

Focused on individual health coverage for ALL uninsured and underinsured Alaskans.

Goals• Enroll the 66,000 uninsured Alaskans without

access to other coverage.

• Identify those who qualifying for help paying for premiums

• For example, a family of 4 making $44,000 will pay no more than $147/month for a “silver” plan and $0 for a “bronze” plan with a higher deductible.

How are we getting it done?

Teaming with Health Care Facilities

• Enroll Alaska will have presence in most major hospitals and clinics.

State-wide Marketing/Education/Advertising Campaign

• Massive media campaign to launch August 19th and run until March 31st.

Support from Northrim Bank

• Presence in the branches with educational material and teller communications to individuals.

Thank you for your time.

What’s on your mind?