Embed Size (px)

Citation preview

IS NOW A GOOD TIME TO LOOK AT EMERGING MARKET DEBT?

OCTOBER 2018

L. BRYAN CARTER

2

Not your father’s benchmark

Sources: BNP Paribas AM, JP Morgan Global Index, October 2018

Estimated index weights provided by JP Morgan

JPM EMBI Global Diversified Hard Currency Index

Top 5 Countries (%)

3

EMFI a large and well established asset class

Sources: JP Morgan, Bloomberg, end May 2018

2000 2009 2018 YTD

EM local market Corporates 0 1.975 7.793

EM Local Market Sovereigns 204 4.367 8.380

EM External Sovereign 0 481 1.070

EM External Corporates 120 605 2.169

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

18.000

20.000

US

D B

illio

n

EM Debt Outstanding

EMFI sub-asset class returns – Dispersion increasing as

market matures

4

Source: JP Morgan, October 2018Past performance is not indicative of current or future performance.

-40%

-20%

0%

20%

40%

60%

80%

100%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018YTD July

EMFI sub-asset class returns - High level of dispersion

EM USD Government Debt returns EM USD Corporate Debt returns

EM Local Currency Government Debt returns (USD unhedged) EM Local Currency Government Debt returns (USD hedged)

0%

20%

40%

60%

80%

100%

120%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

EM Local Currency – Quantile Dispersion

Top/Bottom 10% Return Dispersion

Three themes for 2019:

1) China is about to change

everything

5

Positive steps policymakers to open up capital market

October

2016

March

2017

June 2017

July 2017

November

2017

• Inclusion in the IMF Special Drawing Rights (SDR) basket

• Bloomberg Barclays launched a new Global Aggregate + China index, as well as EM + China

indices

• Citigroup announced that it would include China’s bonds in Emerging Market and Regional

indices

• MSCI announced that it would include China A-shares in the MSCI Emerging Markets Index

• Launch of the Bond Connect program for easier access to the onshore bond market by

offshore investors

• International credit rating agencies given access to rate onshore issuers

• PBOC issued detailed operational guidance for foreign investors’ onshore RMB bond

investments, including on account registration, settlements and tax rates

• China announced further opening up of its capital account by reducing limits around foreign

ownership in select finance businesses, as well as reducing tariffs on certain sectors

6

Source: BNPP AM, March 2018

March

2018

• Bloomberg announced that it would include onshore Chinese government and policy bank

bonds in the Bloomberg Barclays Global Aggregate Bond Index beginning in April 2019,

phased over 20 months, conditional upon resolving certain operational aspects

IMF -= International Monetary Fund; EM = Emerging Markets; PBoC = People’s Bank of China

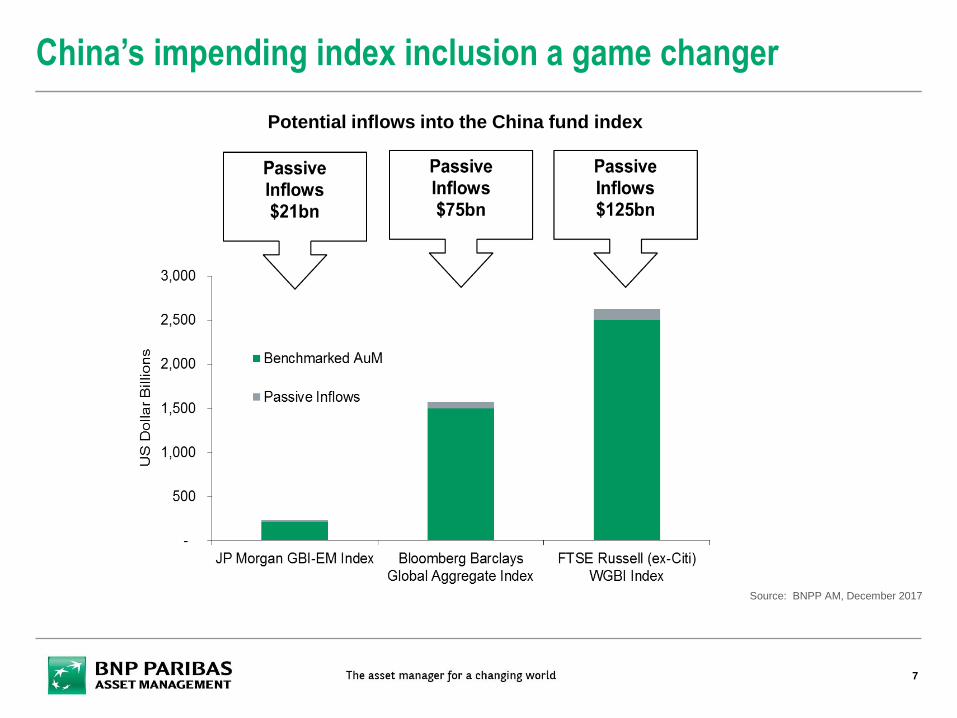

China’s impending index inclusion a game changer

7

Source: BNPP AM, December 2017

Potential inflows into the China fund index

Scale of Onshore Chinese bond market

8

Source: BNPP AM, Wind, April 2018CP = Commercial Paper; SCP = Super & short-term commercial paper; NCD = Negotiable Certificate of Deposit;

MTN = Medium term notes; PPN = Private placement notes

Foreign ownership of China onshore bonds

Foreign ownership of China onshore bonds

9

Source: PBOC, ChinaBond, JP Morgan, August 2018

Three themes for 2019:

2) GCC injects quality back into

the asset class

10

Regional Breakdown before and after inclusion of

GCC Countries

11

Source: BNP Paribas, JP Morgan EMGI Global

Diversified Index, October 2018

Latam37%

Europe25%

Middle East6%

Asia20%

Africa12%

Current Weight %

Latam32%

Europe22%

Middle East18%

Asia17%

Africa11%

Estimated Weights, inclusive of GCC

GCC Investments

12

Source: BNP Paribas, JP Morgan EMGI Global

Diversified Index, October 2018

• EMBI Index Inclusion in 2019: Saudi Arabia (3.1%), Qatar (2.7%), United Arab

Emirates (UAE, 2.6%), Kuwait (2.1%) & Bahrain (0.8%)

• Represents approximately 11.2% of index - $111billion face amount outstanding

from 15 eligible issuers

• EMBI Index will increase to 72 countries (from 67 countries), increasing

diversification

• Meaningful spread tightening (c.21bps) while the investment grade weight of

the index increases to 60% (though the average rating remains at BB+)

• Phased inclusion over 9 months

Three themes for 2019:

3) There is a debt crisis in EM

13

Frontier debt under pressure

14

Source: BNP Paribas, JP Morgan, October 2018

Four Sovereign defaults over the past 1.5 years:

• Venezuela

• Mozambique

• Congo

• Barbados

EM Sovereign historical defaults

HIPC & G7 debt

relief initiatives

EMBI Global Diversified Index

15

Source: BNP Paribas, JP Morgan,

October 2018

*Countries we consider “default candidates”

Country Mkt Cap % IG or HY "Default Candidates"

Mexico 5.2 IG

China 4.5 IG

Indonesia 4.3 IG

Russia 3.5 IG

Philippines 3.3 IG

Turkey 3.3 HY

Brazil 3.1 HY

Colombia 3.0 IG

Panama 2.9 IG

Peru 2.9 IG

Kazakhstan 2.8 HY

Chile 2.8 IG

Argentina 2.8 HY

Hungary 2.8 IG

South Africa 2.7 HY

Dominican Republic 2.7 HY

Malaysia 2.6 IG

Oman 2.6 IG

Ukraine 2.6 HY *Ecuador 2.5 HY

Egypt 2.5 HY

Uruguay 2.5 IG

Lebanon 2.3 IG

Poland 2.1 IG

Sri Lanka 2.0 HY

Country Mkt Cap % IG or HY "Default Candidates"

Croatia 1.7 HY

Nigeria 1.5 HY

Romania 1.4 IG

Azerbaijan 1.2 HY

El Salvador 1.1 HY

Pakistan 1.1 HY

Costa Rica 1.1 HY

Jamaica 1.1 HY

Angola 1.0 HY *Lithuania 1.0 IG

India 1.0 IG

Venezuela 0.9 HY *Cote D'Ivoire 0.8 HY

Ghana 0.8 HY

Kenya 0.7 HY

Serbia 0.7 HY

Paraguay 0.7 HY

Mongolia 0.7 HY *Iraq 0.7 HY

Jordan 0.5 HY

Guatemala 0.5 HY

Senegal 0.4 HY

Morocco 0.4 HY

Zambia 0.4 HY *Trinidad And Tobago 0.4 HY

Country Mkt Cap % IG or HY "Default Candidates"

Gabon 0.4 HY *Belarus 0.4 HY

Bolivia 0.4 HY

Honduras 0.4 HY

Vietnam 0.3 HY

Slovakia 0.3 IG

Namibia 0.2 HY

Georgia 0.2 HY

Armenia 0.2 HY

Ethiopia 0.2 HY

Tunisia 0.2 HY

Cameroon 0.2 HY

Latvia 0.1 IG

Mozambique 0.1 HY *Suriname 0.1 HY

Tajikistan 0.1 HY

Belize 0.1 HY *Congo N/A HY *

Investment Grade 51.3

High Yield 48.7

In Conclusion

16

• For the first time in years, the asset class is alpha-rich

• Can outperform by avoiding blow-ups!

Source: BNP Paribas, October 2018

Recent EMFI Market Performance

and Flows Update

17

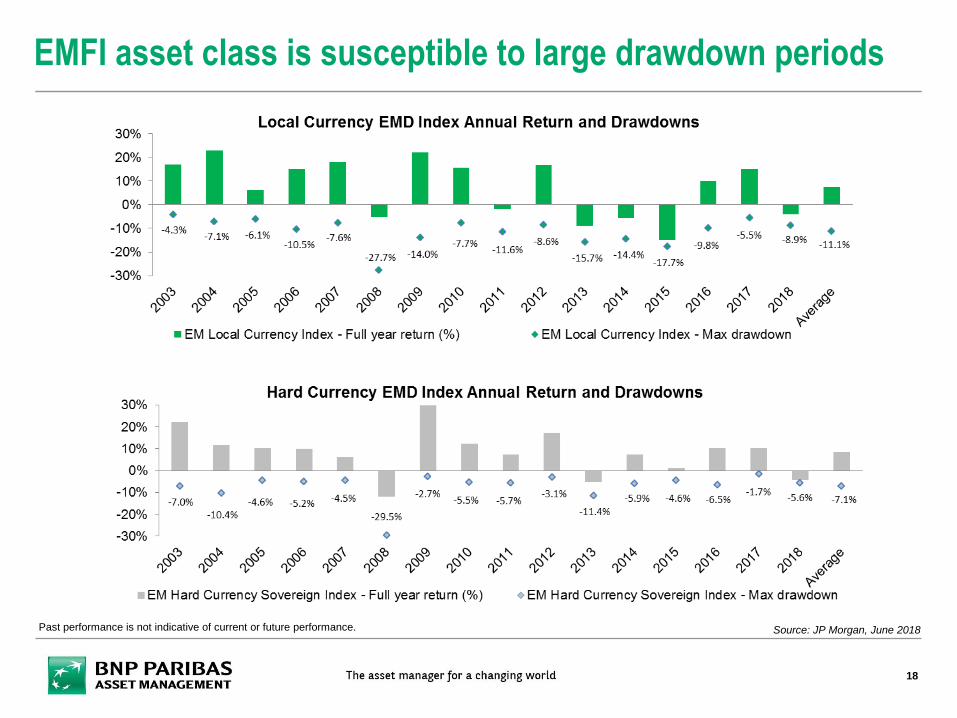

EMFI asset class is susceptible to large drawdown periods

18

Source: JP Morgan, June 2018Past performance is not indicative of current or future performance.

EMFI asset class selloff broad based in 2018 YTD

19

EMFI = Emerging Market Fixed Income; YTD = Year to Date

Source: BNP Paribas AM, JP Morgan, end September 2018Past performance is not indicative of current or future performance.

VIX Spike

EM Growth

Shock

Turkey &

Argentina

Contagion

8,0%

10,0%

12,0%

14,0%

16,0%

18,0%

20,0%

22,0%

24,0%

26,0%

28,0%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Recent EMFI outflows; foreign ownership has fallen

20

EM Foreign ownership of EMFI

ex China local curency government bonds: weighted average

% of amount outstanding

Source: JP Morgan, official sources, August 2018

Annual foreign purchases of EMFI

ex China local currency government bonds

USD billion, by region

Source: JP Morgan, official sources, August 2018

High 27.4%

Current 24.4%

-40

-20

0

20

40

60

80

100

120

140

160

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Latin America EMEA EM EM Asia (ex China)

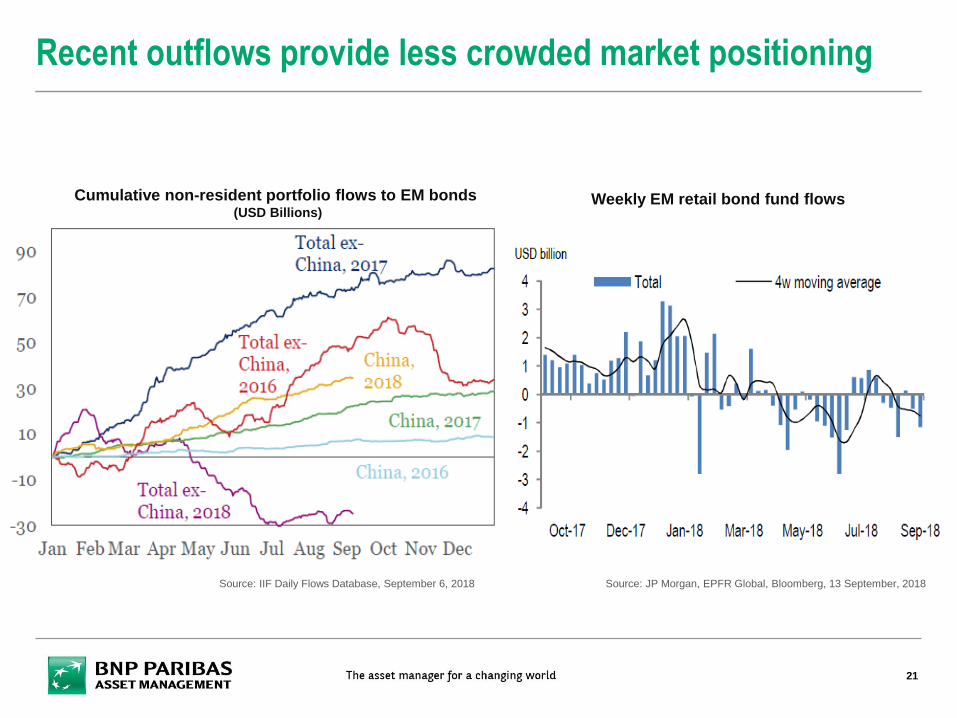

Recent outflows provide less crowded market positioning

21

Weekly EM retail bond fund flows

Source: IIF Daily Flows Database, September 6, 2018 Source: JP Morgan, EPFR Global, Bloomberg, 13 September, 2018

Cumulative non-resident portfolio flows to EM bonds (USD Billions)

EM proportion in global funds well below peak levels

22

Emerging vs. Mature Markets: Fund Portfolio Weights

Source: EPFR, IIF estimates; includes mutual funds and ETFs August 2018

LHS: Left Hand Side; RHS: Right Hand Side

10

11

12

13

14

15

16

17

18

19

20

81

82

83

84

85

86

87

88

89

90

2008 2010 2012 2014 2016 2018

% of global bond/equity allocation

Emerging markets (RHS)

Mature markets (LHS)

INTEGRATING ESG

23

24

SSocial

GInstitutions

• Renewables on

energy ratio• Corruption

perceptions index

• Press freedom

index

• School enrolment

gender parity index

• Internet access

ratio

EEnvironmental

Factors included in proprietary ESG screen for EMFI

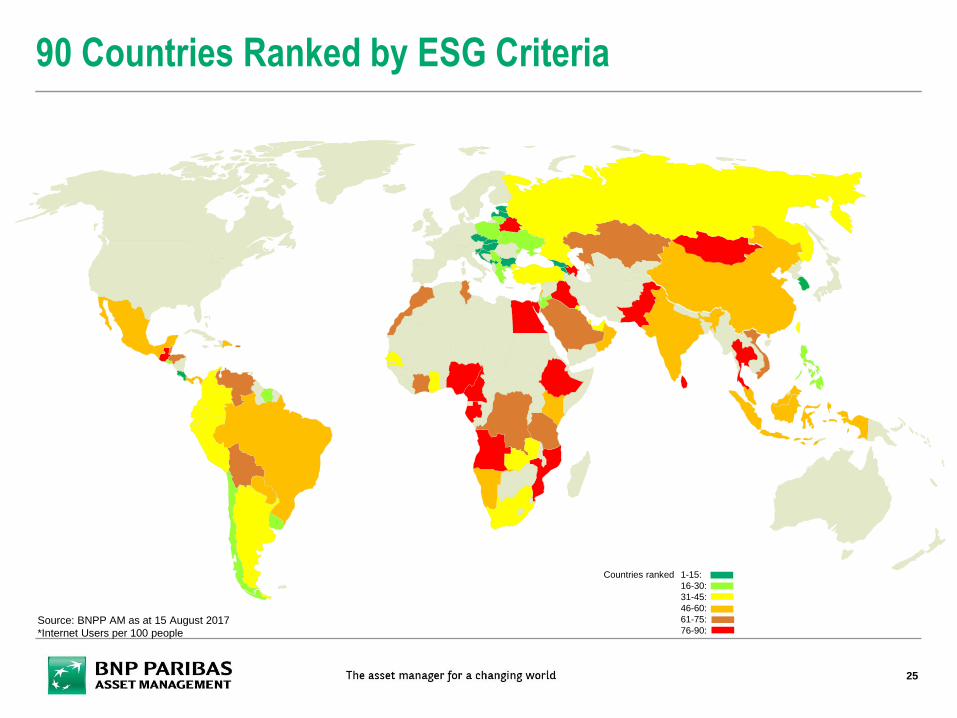

90 Countries Ranked by ESG Criteria

Source: BNPP AM as at 15 August 2017

*Internet Users per 100 people

Countries ranked 1-15:

16-30:

31-45:

46-60:

61-75:

76-90:

25

90 Countries Ranked by ESG Criteria

16

URUGUAY

SSocial

GInstitutions

• Renewables on

energy ratio(%):

18.94

• Corruption

perceptions index

(rank): 21

• Press freedom

index (rank): 20

• School enrolment

gender parity

index: 0.98

• Internet access

ratio*: 64.6

EEnvironmental

Countries ranked 1-15:

16-30:

31-45:

46-60:

61-75:

76-90:Source: BNPP AM as at 15 August 2017

*Internet Users per 100 people

26

90 Countries Ranked by ESG Criteria

90

ANGOLA

Countries ranked 1-15:

16-30:

31-45:

46-60:

61-75:

76-90:

SSocial

GInstitutions

• Renewables on

energy ratio(%):

2.95

• Corruption

perceptions index

(rank): 164

• Press freedom

index (rank): 123

• School enrolment

gender parity

index: 0.64

• Internet access

ratio*: 12.4

EEnvironmental

Source: BNPP AM as at 15 August 2017

*Internet Users per 100 people

27

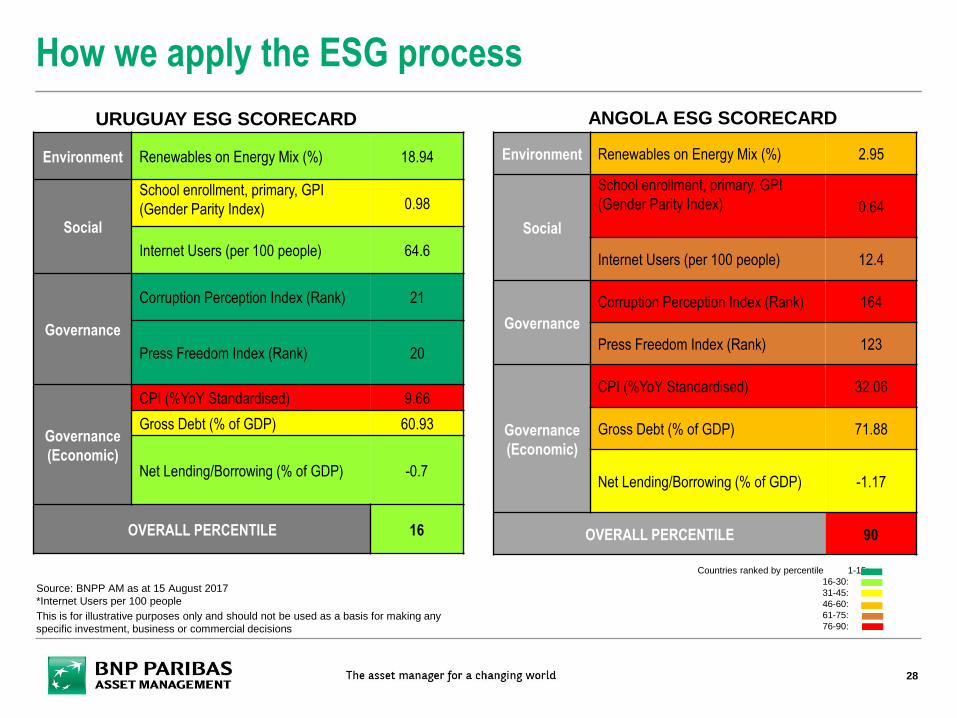

How we apply the ESG process

Environment Renewables on Energy Mix (%) 18.94

Social

School enrollment, primary, GPI

(Gender Parity Index) 0.98

Internet Users (per 100 people) 64.6

Governance

Corruption Perception Index (Rank) 21

Press Freedom Index (Rank) 20

Governance

(Economic)

CPI (%YoY Standardised) 9.66

Gross Debt (% of GDP) 60.93

Net Lending/Borrowing (% of GDP) -0.7

OVERALL PERCENTILE 16

Countries ranked by percentile 1-15:

16-30:

31-45:

46-60:

61-75:

76-90:

Environment Renewables on Energy Mix (%) 2.95

Social

School enrollment, primary, GPI

(Gender Parity Index) 0.64

Internet Users (per 100 people) 12.4

Governance

Corruption Perception Index (Rank) 164

Press Freedom Index (Rank) 123

Governance

(Economic)

CPI (%YoY Standardised) 32.06

Gross Debt (% of GDP) 71.88

Net Lending/Borrowing (% of GDP) -1.17

OVERALL PERCENTILE 90

URUGUAY ESG SCORECARD ANGOLA ESG SCORECARD

This is for illustrative purposes only and should not be used as a basis for making any

specific investment, business or commercial decisions

Source: BNPP AM as at 15 August 2017

*Internet Users per 100 people

28

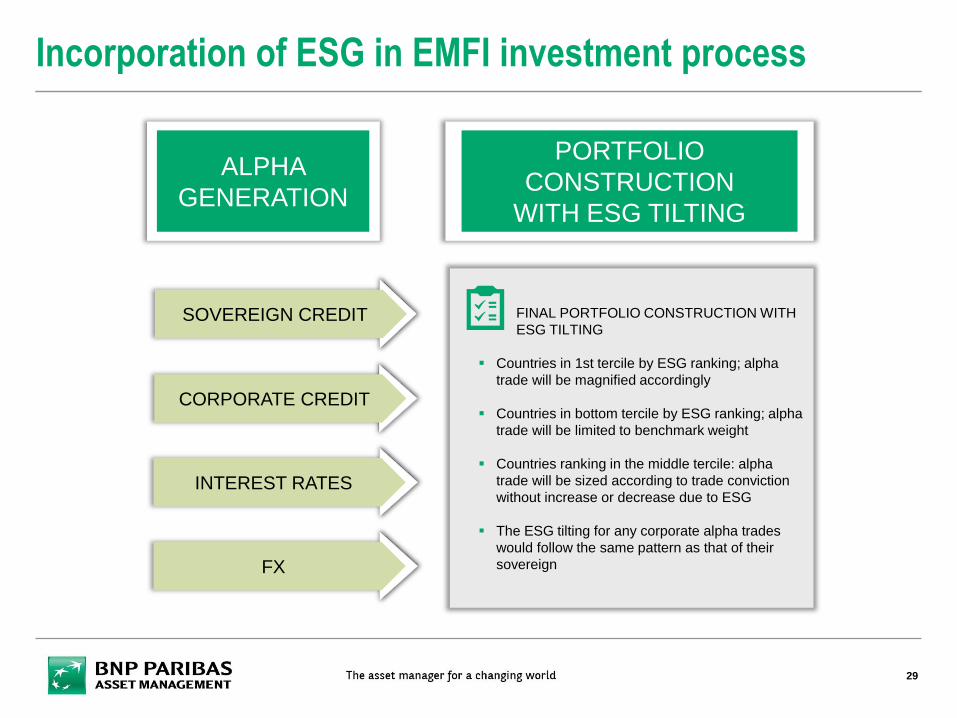

29

FINAL PORTFOLIO CONSTRUCTION WITH

ESG TILTING

Countries in 1st tercile by ESG ranking; alpha

trade will be magnified accordingly

Countries in bottom tercile by ESG ranking; alpha

trade will be limited to benchmark weight

Countries ranking in the middle tercile: alpha

trade will be sized according to trade conviction

without increase or decrease due to ESG

The ESG tilting for any corporate alpha trades

would follow the same pattern as that of their

sovereign

SOVEREIGN CREDIT

CORPORATE CREDIT

INTEREST RATES

FX

ALPHA

GENERATION

PORTFOLIO

CONSTRUCTION

WITH ESG TILTING

Incorporation of ESG in EMFI investment process

Green Bonds: Assessment Process

30

ESG decile: assessment of the issuer’s ESG credentials.

Customized to client needs (e.g. decile 9 and 10 are OUT).

Taxonomy: the projects to be funded must be in line with our

definition of eligible activities. If the issuer plans to finance

excluded activities, the recommendation is OUT.

BNPP IP’s Green Bond score:

• If the issuer’s final green bond score is lower than the

minimum score for eligibility, the recommendation is OUT.

• If the issuer’s final green bond score is superior or equal to

the minimum score for eligibility, the recommendation is IN

for one year.

Ex post reporting: if the issuer doesn’t provide a reporting

and/or if the proceeds are not fully allocated within a reasonable

time, the recommendation is OUT.

Engagement with the issuer: dialogue on the actual proceeds

allocation, output indicators and impact indicators. If engagement

is satisfactory, the recommendation is IN for another year. If not,

it is OUT.

1st filter

2nd filter

3rd filter

4th filter

5th filter

EX A

NTE

EX P

OST

Biographies

31

Disclaimer

32

BNP PARIBAS ASSET MANAGEMENT UK Limited, “the investment company”, is authorised and regulated by the Financial Conduct Authority. Registered in England No: 02474627,

registered office: 5 Aldermanbury Square, London, England, EC2V 7BP, United Kingdom.

This material is produced for information purposes only and does not constitute:

1. an offer to buy nor a solicitation to sell, nor shall it form the basis of or be relied upon in connection with any contract or commitment whatsoever or

2. investment advice.

This material makes reference to certain financial instruments authorised and regulated in their jurisdiction(s) of incorporation.

No action has been taken which would permit the public offering of the financial instrument(s) in any other jurisdiction, except as indicated in the most recent prospectus and the Key

Investor Information Document (KIID) of the relevant financial instrument(s) where such action would be required, in particular, in the United States, to US persons (as such term is defined

in Regulation S of the United States Securities Act of 1933). Prior to any subscription in a country in which such financial instrument(s) is/are registered, investors should verify any legal

constraints or restrictions there may be in connection with the subscription, purchase, possession or sale of the financial instrument(s).

Investors considering subscribing to the financial instrument(s) should read carefully the most recent prospectus and Key Investor Information Document (KIID) and consult the financial

instrument(s’) most recent financial reports. These documents are available on the website.

Opinions included in this material constitute the judgement of the investment company at the time specified and may be subject to change without notice. The investment company is not

obliged to update or alter the information or opinions contained within this material. Investors should consult their own legal and tax advisors in respect of legal, accounting, domicile and

tax advice prior to investing in the financial instrument(s) in order to make an independent determination of the suitability and consequences of an investment therein, if permitted. Please

note that different types of investments, if contained within this material, involve varying degrees of risk and there can be no assurance that any specific investment may either be suitable,

appropriate or profitable for an investor’s investment portfolio.

Given the economic and market risks, there can be no assurance that the financial instrument(s) will achieve its/their investment objectives. Returns may be affected by, amongst other

things, investment strategies or objectives of the financial instrument(s) and material market and economic conditions, including interest rates, market terms and general market conditions.

The different strategies applied to financial instruments may have a significant effect on the results presented in this material. Past performance is not a guide to future performance and

the value of the investments in financial instrument(s) may go down as well as up. Investors may not get back the amount they originally invested.

Gross of fees performance included in this material do not reflect the deduction of commission, fees and other expenses incurred. Returns will be reduced after the deduction of such fees.

This document is directed only at person(s) who have professional experience in matters relating to investments (“relevant persons”). Any investment or investment activity to which this

document relates is available only to and will be engaged in only with Professional Clients as defined in the rules of the Financial Conduct Authority. Any person who is not a relevant

person should not act or rely on this document or any of its contents.

All information referred to in the present document is available on www.bnpparibas-am.com

![Fixed Income Index Guide - BlackRock · [10] FIXED INCOME INDEX GUIDE Bloomberg Barclays index family ... Broad family of fixed income indices, including: aggregate, government, corporate,](https://img.pdfslide.us/doc/110x75/5b0274907f8b9af1148fb575/fixed-income-index-guide-blackrock-10-fixed-income-index-guide-bloomberg-barclays.jpg)