Embed Size (px)

Citation preview

Economics and Accounting JournalVol.1, No.1, January 2018

11

IS ISLAMIC BANKING RIBA FREE ?(CASE STUDY : MURABAHA CONTRACT)

Adi MartonoUniversity of Pamulang

Abstract

Islamic banks is established to provide solutions on the need for transactions andfinancing facilities to the Moslem who want to avoid riba and gharar. From the previousresearches, author obtains facts and conditions : 1) Moslem people think Islamic banksstill implement contract and transaction contain riba or they do not comply with HolyQur’an and Sunnah of Prophet. 2) In executing murabaha contract, Islamic banks understudy have not possessed or controled the goods before they sells it to the customer. Tofind out how and why those facts and conditions happen in Islamic bank, author uses casestudy as research methodology. After after analyzing the implementation of murabahacontract from previous researches and comparing it to the sharia standards, authorfound there are gaps between the murabaha contract that has been implemented inseveral Islamic bank and in sharia standard. In this case, author uses sharia standardissued by Accounting and Auditing Organization for Islamic Financial Institution(AAOIFI). Those gaps are implementation of wakalah contract, possession of goods andimplementation of murabaha contract. Islamic bank should improve the process ormechanism of those contract. The conclusion is because lack of understanding about thatIslamic banks have to improve the process of Murabaha contract, such as the process ofacquisition of goods so the process refers to the Holy Qur’an and the Sunnah of Prophet.

Keywords : Murabaha, Case Study, Islamic Bank

1. INTRODUCTION

The first Indonesia Islamic bank hadestablised since 1992, by moslembusinessman and moslem scholar. Theobjective of setting up the Islamic bankis to fulfill the aspiration of moslempeople about a bank which complieswith the Holy Qur’an and the Sunnah ofProphet.

After 25 years, the development ofIslamic Banks in Indonesia are really

significant. Table 1, FinancialServices Authority, Republic ofIndonesia data (Financial ServicesAuthority, 2017b) shows several bank’sindicators have grown such as TotalAsset, Receivables From Non Bank(Murabaha), Third Party Fund for period2014 – December 2017.

Economics and Accounting JournalVol.1, No.1, January 2018

12

Table 1. The Development of Islamic Bank

Informations 2014 2015 2016 2017

Number of Banks- Sharia Commercial Bank- Sharia Business Unit Operations

12

22

12

22

13

21

13

21

Asset (Billions Rupiah)- Sharia Commercial Bank- Sharia Business Unit Operations

204,961

67,383

213,423

82,839

254,184

102,320

288,027

136,154

Receivables from non Bank, Murabaha(Billions Rupiah)- Sharia Commercial Bank- Sharia Business Unit Operations

91.867

25,504

93.642

28,469

113.971

29,473

114,494

35,818

Third Party Funding (Billions Rupiah)- Sharia Commercial Bank- Sharia Business Unit Operations

170,723

47,136

174,895

56,280

206,497

72,928

238,225

96,495

Financing Deposit Ratio (%)- Sharia Commercial Bank- Sharia Business Unit Operations

86.66

109.02

88.03

104.88

85.99

96.70

79.65

99,39

Source : Financial Services Authority. 2017. Sharia Banking Statistics, December 2017

Islamic bankings have played inimportant role in Indonesia financialindustry and contributed to Indonesia’s

economics growth. They become anintermediary between funder andbusiness owner.

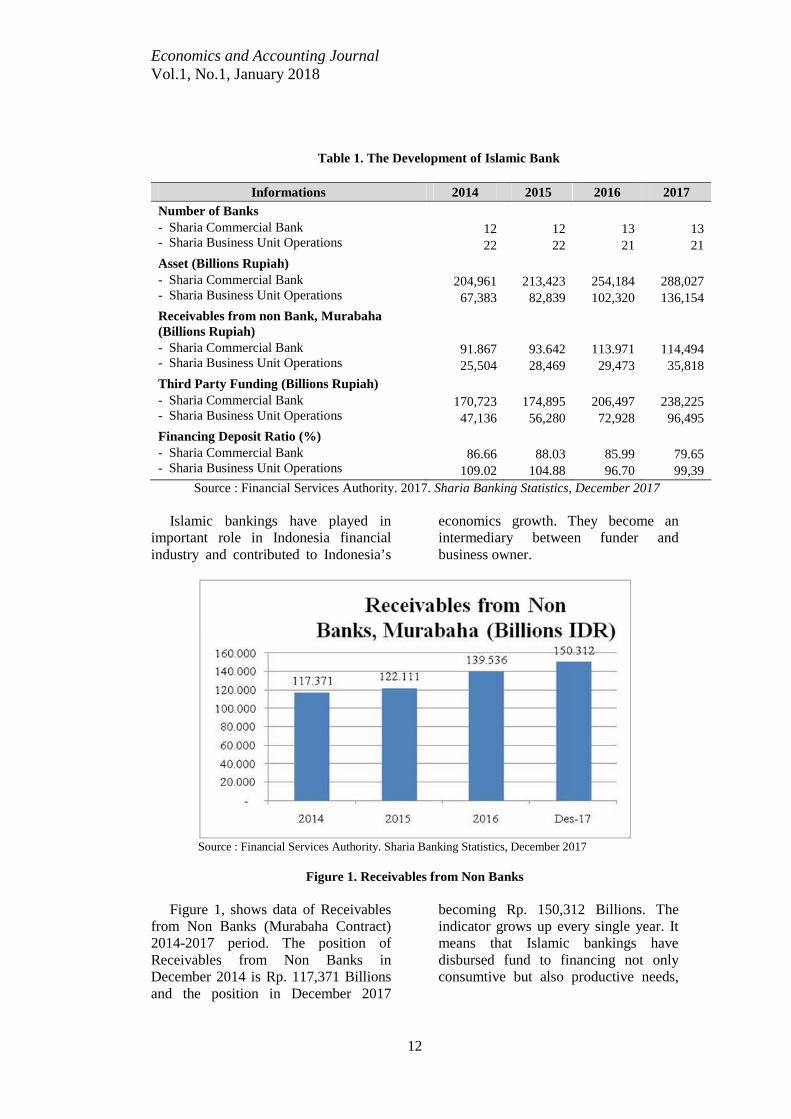

Source : Financial Services Authority. Sharia Banking Statistics, December 2017

Figure 1. Receivables from Non Banks

Figure 1, shows data of Receivablesfrom Non Banks (Murabaha Contract)2014-2017 period. The position ofReceivables from Non Banks inDecember 2014 is Rp. 117,371 Billionsand the position in December 2017

becoming Rp. 150,312 Billions. Theindicator grows up every single year. Itmeans that Islamic bankings havedisbursed fund to financing not onlyconsumtive but also productive needs,

Economics and Accounting JournalVol.1, No.1, January 2018

13

such as buying house, machine, office or raw material.

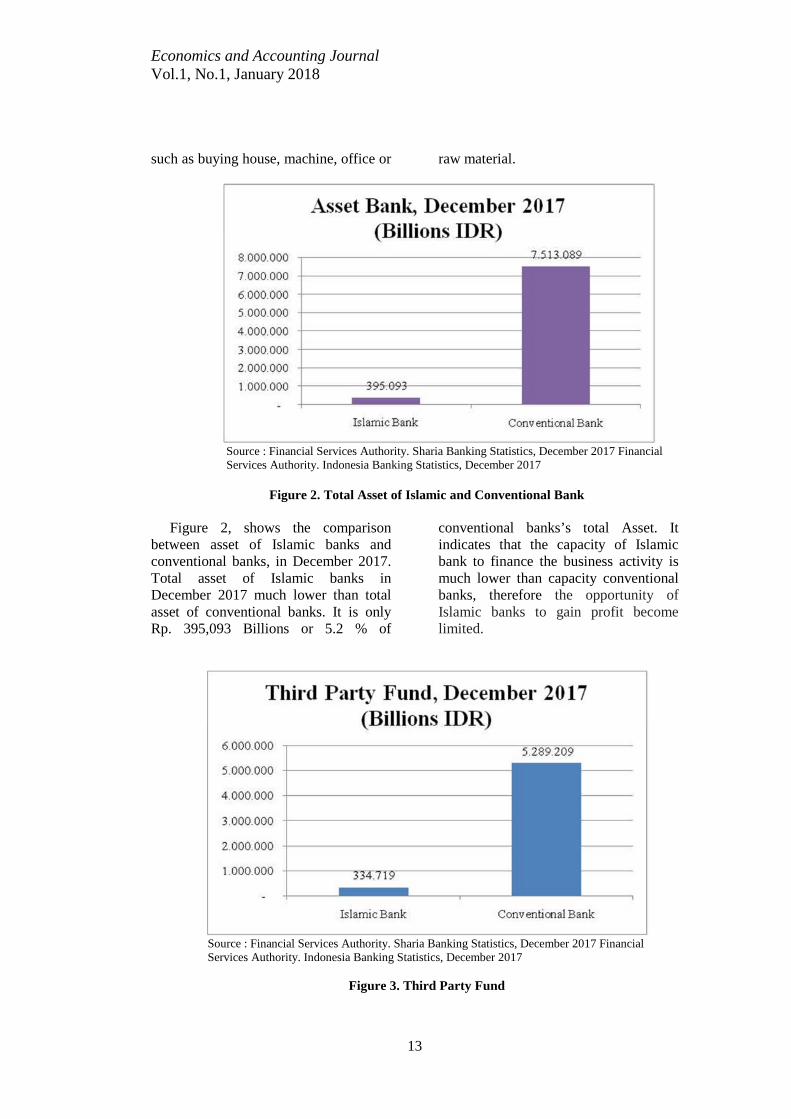

Source : Financial Services Authority. Sharia Banking Statistics, December 2017 FinancialServices Authority. Indonesia Banking Statistics, December 2017

Figure 2. Total Asset of Islamic and Conventional Bank

Figure 2, shows the comparisonbetween asset of Islamic banks andconventional banks, in December 2017.Total asset of Islamic banks inDecember 2017 much lower than totalasset of conventional banks. It is onlyRp. 395,093 Billions or 5.2 % of

conventional banks’s total Asset. Itindicates that the capacity of Islamicbank to finance the business activity ismuch lower than capacity conventionalbanks, therefore the opportunity ofIslamic banks to gain profit becomelimited.

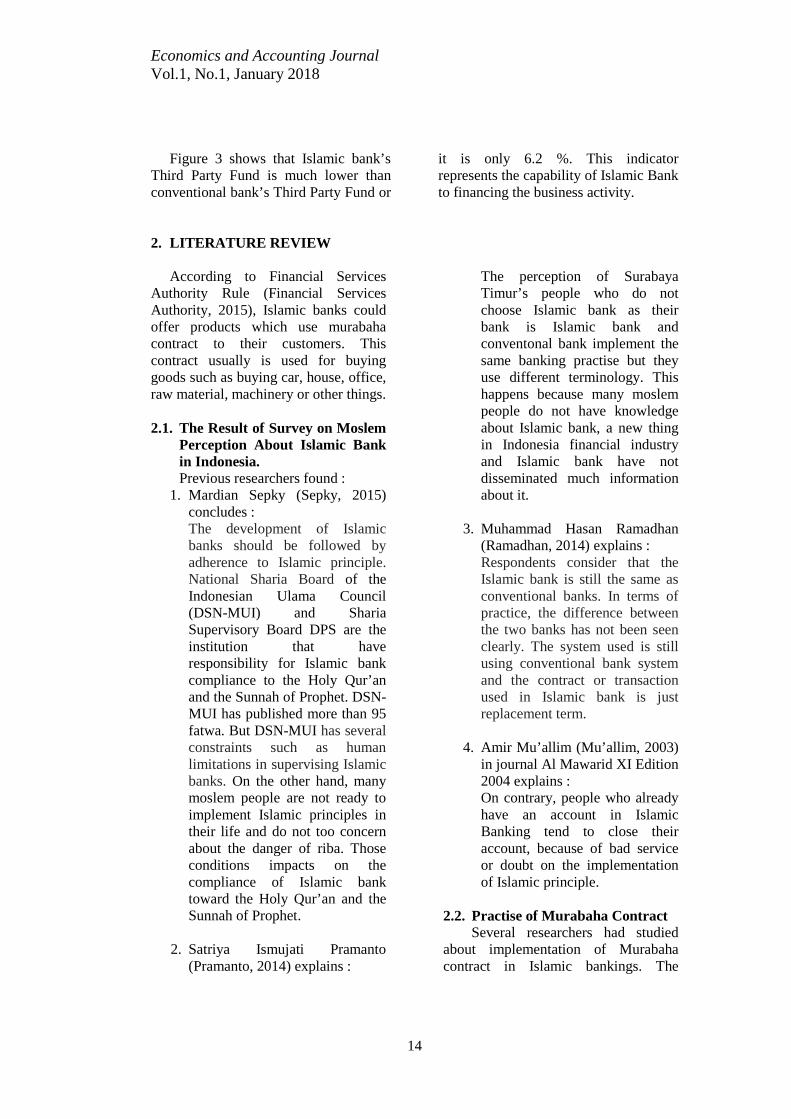

Source : Financial Services Authority. Sharia Banking Statistics, December 2017 FinancialServices Authority. Indonesia Banking Statistics, December 2017

Figure 3. Third Party Fund

Economics and Accounting JournalVol.1, No.1, January 2018

14

Figure 3 shows that Islamic bank’sThird Party Fund is much lower thanconventional bank’s Third Party Fund or

it is only 6.2 %. This indicatorrepresents the capability of Islamic Bankto financing the business activity.

2. LITERATURE REVIEW

According to Financial ServicesAuthority Rule (Financial ServicesAuthority, 2015), Islamic banks couldoffer products which use murabahacontract to their customers. Thiscontract usually is used for buyinggoods such as buying car, house, office,raw material, machinery or other things.

2.1. The Result of Survey on MoslemPerception About Islamic Bankin Indonesia.Previous researchers found :

1. Mardian Sepky (Sepky, 2015)concludes :The development of Islamicbanks should be followed byadherence to Islamic principle.National Sharia Board of theIndonesian Ulama Council(DSN-MUI) and ShariaSupervisory Board DPS are theinstitution that haveresponsibility for Islamic bankcompliance to the Holy Qur’anand the Sunnah of Prophet. DSN-MUI has published more than 95fatwa. But DSN-MUI has severalconstraints such as humanlimitations in supervising Islamicbanks. On the other hand, manymoslem people are not ready toimplement Islamic principles intheir life and do not too concernabout the danger of riba. Thoseconditions impacts on thecompliance of Islamic banktoward the Holy Qur’an and theSunnah of Prophet.

2. Satriya Ismujati Pramanto(Pramanto, 2014) explains :

The perception of SurabayaTimur’s people who do notchoose Islamic bank as theirbank is Islamic bank andconventonal bank implement thesame banking practise but theyuse different terminology. Thishappens because many moslempeople do not have knowledgeabout Islamic bank, a new thingin Indonesia financial industryand Islamic bank have notdisseminated much informationabout it.

3. Muhammad Hasan Ramadhan(Ramadhan, 2014) explains :Respondents consider that theIslamic bank is still the same asconventional banks. In terms ofpractice, the difference betweenthe two banks has not been seenclearly. The system used is stillusing conventional bank systemand the contract or transactionused in Islamic bank is justreplacement term.

4. Amir Mu’allim (Mu’allim, 2003)in journal Al Mawarid XI Edition2004 explains :On contrary, people who alreadyhave an account in IslamicBanking tend to close theiraccount, because of bad serviceor doubt on the implementationof Islamic principle.

2.2. Practise of Murabaha ContractSeveral researchers had studied

about implementation of Murabahacontract in Islamic bankings. The

Economics and Accounting JournalVol.1, No.1, January 2018

15

reseaches had been done in several cityand different Islamic banks.

According to a December 2017report by Financial Services Authority (Financial Services Authority, 2017b),there are 13 Islamic banks and 21Sharia Business Unit Operations andprevious researchers do the research inseveral Islamic banks.

1. Pipit Setyaningtyas(Setyaningtyas, 2016) in herstudy :“eventhough Bank SyariahMandiri, Purwokerto branch useswakalah contract but in the realtransaction, customer still doesnot get the money from bank forbuying the goods eventhoughbank becomes a principle.Processe that occures, banktransfer the money to customeraccount and at the same timebank will debet the money andthe transfer it to the supplier ’saccount (the owner ofhouse/car/goods). ”wakalahcontract is used to prove thatthere is a sale and purchasetransaction between bank andsupplier“

2. Zulia Hanum (Z. Hanum, 2014)explain that in bank’s standardoperating procedure :a. After the branch manager

approves the financingproposal, financing comitteewill make a financingmemorandum and based onthat memorandum, notary willmake a deed of debtrecognition and binding ofwarranty goods.

b. After all document requiredare completed, financingadministration supervisor willdisburse the money.

c. Staf at financingadminitration will maintainthe customer account and

transfer/credit the money tocustomer’s account.

3. Muhammad Ali Fauzi et.al(Fauzi, Adnan, & Harahap, 2015)in journal Law DoctoralProgram, University of SebelasMaret explains :According to the Indonesia Law,the implementation of mortgagefinancing in Bank SyariahMandiri : bank has made a saleand purchase transaction ofhouse that have owned bycustomer. This is indicated :customer have signed a notaryact of sale and purchasetransaction with propertydeveloper before signingmurabaha contract with bank.

4. Aulia Hanum (A. Hanum, 2015)has conducted a research in BankMuamalat Indonesia, Bank BRISyariah, Bank Syariah Mandiriand Bank CIMB Niaga, MalangBranch, explains :Impementation of murabaha bilwakalah contract in those banksare different from each other.Implementation of murabahacontract in Bank MuamalatIndonesia and Bank BRI Syariah,Malang branch almost complyIslamic principle. Contrary tothat, Implementation ofmurabaha contract in BankSyariah Mandiri and Bank CIMBNiaga Syariah, still do notcomply. Such as Bank SyariahMandiri does not executewakalah contract. Even, BankCIMB Niaga Syariah which hassharia business unit, it really doesnot do Islamic principle.

5. Achmad Subchan (Subchan,2015) in his research explains :In implementing murabahacontract, Bank BCA Syariah uses

Economics and Accounting JournalVol.1, No.1, January 2018

16

wakalah contract but itsimplementation does not complywith Islamic principle. In thiscase bank makes a sale andpurchase transaction of goods butthe goods has not been owned orcontroled. Bank gives anauthority to customer to buy theproduct which he wants and banklends some money to thecustomer.

6. Pedagogita Rakhma (Rakhmah,2014) she explains :In BTPN Syariah, murabahacontract is known as murabahabil wakalah. Bank makes twocontracts, prior to makingwakalah contract, bank makesmurabaha contract withcustomer. Bank gives anauthority to the customer to buythe goods from the seller that hewants, then seller will deliverythe goods to customer. It isknown by bank and bank willreceive an receipt from customer.

7. Pajar Rahmatuloh (RahmatulohPajar, 2015) concludes :In the implementation, there arethree different form of murabahacontract. The most widelyimplemented form is the signingof wakalah contracts andmurabaha contracts donesimultaneously.

2.3. Murabaha-WakalahTransaction and, Qabdhaccording to Holy Qur’an andSunnah of Prophet :There are many discussion

about terminology of contract, term& condition and rukun Murabahaand Wakalah contract and Qabdhwhich is done by moslem scholar,Islamic bankers and the financialauthority.

On this section, author willfocus the study on murabahacontract principle, Wakalah andQabdh which is often ignored.

2.4. Promising or Wa’ad betweencustomer and Islamic bank.Prof DR. Wahbah Az-Zubaili

(Wahbah, 2011) explains : In itsoperation, Islamic bank implementbay’ul murabahah lil aamirbisysyiraa :

There are two promises :customer’s promise to buy a goodsfrom bank and bank’s promise tosell a goods to customer inmurabaha contract.

The argument is based onopinion of Imam Syafi’i in his bookAl-Umm, as well as Imam Maliki’sopinion.

2.5. Selling a good before the sellerown the good.

Prof DR. Wahbah Az-Zubaili(Wahbah, 2011) says Imam Hanafi,Imam Maliki, Imam Hanbali, ImamSyafi’i and Imam Ahmad argue that donot sell goods whose ownership statusis unclear :

Imam Ahmad narated from Hakim binHizam ra, he said, “I said, ‘Prophet, Ialways buy goods, so what is halal andunlawful for me ?”The Prophet (peacebe upon him) answer : “If you buygoods, do not sell those goods until youget them from the seller”. The Prophet(peace be upon him) have said “You arenot permissible to get profit if you donot have the goods and you should notsell the goods that you do not own orcontrol”

Sayyid Sabiq (Sayyid, 2009)explains that a seller should not sell thegoods which is bought from the suppieruntil he possesses or controls the goods.

Economics and Accounting JournalVol.1, No.1, January 2018

17

The wisdom of the implementationof this hadits : if a seller sells goods andbuyer has not acquired the goods, so theseller still has to be responsible if goodsis damage or lost. And seller should notget profit if he does not want to takebusiness risk.

2.6. Qabdh or Taking PossessionA murabaha contract is valid when

the goods has been taken possession bythe buyer.

In general there are two kinds ofpossession goods :

1. Qabd Hukmi : delivery nonphysical goods. According tothe law, someone has a right tocontrol the goods even it couldnot be moved physically, suchas land, building etc. Thepossession of those goods isindicated by people could livein the house or the building orplant something on that land.

2. Qabd Haqiqi : deliveryphysical good, someone has aright to control that goodsphysically. Sayyid Sabiq(Sayyid, 2009) explains :delivery goods could be doneby : 1) fullfiling the measure orscales if the amount is known2) to moving the goods from itsorigin if the amount could notbe measured 3) following thetradition/custom if the goods isnot include in category 1 & 2.

2.7. Wakalah contract, Wakil orCustomerThe explanations about wakalah

contract has been discussed by previousresearchers. On this section, author willfocus on the implication of wakalahcontract : principle (al-muwakkil) andagent (al-wakil).

Prof Dr Wahbah Az-Zubaili(Wahbah, 2011) explains that principle

and agent, each party has obligationsand authorities :

Principle (Al-Muwakkil) :1. Obligation :a. Paying the goods that has been

bought.b. Taking risk/loss in case of

agent is not misconduct,negligence or breach thecontract.

Customer :2. Obligation :a. Buying the goods at common

price and not defective.b. Buying the goods that has been

determined by principle if it isnot, agent buys the goods forhimself.

3. Authority :a. Buying buy the goods in lower

prices that has been determinedby principle.

2.8. Sharia Standard according toAccounting, Auditing,Organization for IslamicFinancial Institution (AAOIFI)1. Taking Possession (AAOIFI,

2015a) :a. Based on custom or

tradition, form of possessioncould be differed dependson the nature of good anddifferences among peopleabout a good.

b. Actual possession forimmovable goods is if thegood could be released andenable to be transacted.

c. Actual possession formovable good is if thegoods has been moved ordelivered to buyer’slocation.

d. Actual possession for nonphisical good or constrcutivepossession is such aspossession by the

Economics and Accounting JournalVol.1, No.1, January 2018

18

beneficiary of a bank draft,personel cheque, possessionof document like bills oflading, warehouse receiptand a deposit by a person ofan amount in a bankaccount.

2. Wakalah contract according toSharia Standard (AAOIFI,2015b)Rules as principle/bank (AlMuwakkil) and agent/customer(wakil) :a. Principle :

1) Having legal standing tomake a contract.

2) Having a right to sell orbuying an asset.

b. Agent/customer :1) Having legal standing to

make a contract.2) Committing to

implement what is statedin the contract

Commitment principle (AlMuwakkil) and agent (wakil) :a. Principle :

1) For procurementgood/service, principlebears all costs incurred,including transporationexpense, warehousingexpense, tax andmaintenance expense.

b. Agent/customer.1) Customer does not have

responsibility to replacethe goods if the goods isdefective, except thecustomer is misconduct,negligence or breach thecontract.

3. Murabaha Contract accordingto Sharia Standard (AAOIFI,2015c)Procedures prior to MurabahaContract.

a. Bank may purchase thegood that customers wish aslong as it complies withIslamic principle. Bankcould buy the good fromseller that customer wants,but bank could refuse it ifthe supplier is not reliable.

b. The customer wish to buysomething does not mean apromise except it isexpressed in documentincluding :1) Customer’s desire for

bank to buy the good.2) Bank’s promise to buy

the good that customerwants.

c. Offering letter to the bankshould be witten bysupplier, a sales and puchasetransaction between bankand supplier is valid whenbank agrees with theoffering.

The Position of Bank Relatedto Customer’s Aplication ofMurabaha.a. If there is a sales

purchase transactionbetween customer andsupplier, bank should notdo murabaha contract.And bank could ask thecustomer to cancel thetransaction.

b. Bank has to ensure thatthe seller of the goods isreal supplier notcustomer or his/heragent.

c. Bank and customer arenot permissible to makeagreement that they areagree to make anpartnership in a salespurchase transaction andone party promise to buy

Economics and Accounting JournalVol.1, No.1, January 2018

19

the other share by cash orinstallment.

d. Murabaha contract is notvalid for :1) The object of

transaction are gold,silver or currency.

2) Re-financing.

Promise from the customera. The promise between

bank and customer are notbinding. The argument : abinding agreement issimilar to a sale andpurchase transaction for agood but seller has notalready owned the good.

b. In murabaha contract,promise from customer tobuy the goods is not anobligation. It just a wayfor the bank to ensure,customer will buy thegoods that bank has beenbought.

c. Since murabaha contracthas not been concluded,all clause could bechanged such as price,deffered payment etc. aslong as both party agree.

d. In buying goods from thesupplier, bank has to askseller an option for certainperiod if there is acancelation of sale andpurchase transaction.

Collateral :a. If customer ask a certain

supplier, bank could askcustomer a collateral.Collateral is used as asubstitute for losses if thesupplier does notcomplete his contract. Itis include : incorrectspesification, everything

that causes loss (time,resource, property etc.)

b. During storage ordelivery, if the good isdamage, bank has to beresponsible to replace itwith a new one.

c. For customer’spromising, bank couldask hamish jiddiyyahھامش الجدیة or securitydeposit, to the customer.The deposit is used tocompansate if customerbreach the promise.

3. RESEARCH METHOD

3.1. Research ApproachCase study is one of the research

methodology that has been known andit can be group as a qualitative research(Yin, 2012). This methodology hasbeen using in researching psychology,business, economic, politic area andused to explore about a complexphenomena on an event such asmanagement process or organization(Yin, 2014).

3.2. Research ObjectThis paper is based on author

observation to the development ofIslamic bank in Indonesia in last 5 yearsand author’s experience as banker for16.5 years. The object of research is theimplementation of murabaha contract inIslamic bank especially forconsumptive financing.

3.3. Data SourceTo complete the information and

data for the purpose of this study,author collects the result of researchesconducted within the last 10 years,namely:

1. Research on people perceptionabout Islamic bank inIndonesia.

Economics and Accounting JournalVol.1, No.1, January 2018

20

2. Research on implementation ofmurabaha contract in Islamicbank.

Research conducted by researchersboth at the level of Bachelor andGraduate, either thesis or journal.

Another data are secondary datapublished by government institutionssuch as the Financial ServicesAuthority and Central Bureau ofStatistics. As data comparison, authoruses Sharia Standard issued by thecompetent institution Accounting andAuditing Organization for IslamicFinancial Institution (AAOIFI).

3.4. Data Collection TechniqueTo collect data, author uses :

3.4.1. Document AnalysisAnalyze relevant documents in

the form of contracts and the results ofprevious researches on implementationof Murabaha contracts in severalsyariah banks.3.4.2. Observation

The author’s experience aspractitioners in Islamic banks andauthor’s interaction with Islamicbanking to date, became a way tocollect data and information about theimplementation of Murabaha contract.

The analytical technique used is tocompare between the result of previousresearches and the author's experienceabout implementation murabahacontract in Islamic banking with ShariaStandards issued by AAOIFI which

refers to Holy Qur’an and Sunnah ofProphet.

4. RESULT AND DISCUSSION

Before discussing, “Why” and“How” so that the implementation ofmurabaha contract still contains ribaand gharar, we have to see thecondition of moslem people and Islamicbanking in Indonesia today.

Figures 2 and 3 shows thecomparison asset - third party funds ofIslamic banks with asset - third partyfunds of conventional banks. Accordingto those data, asset - third party funds ofIslamic banks is very small. Thishappens since the first Islamic bankestablished in 1992. If we looks thenumber of moslem in Indonesia whichis more than 200 million people(Central Bureau of Statistics, 2011), itindicates that moslem people still havenot used Islamic banks as their bank forfinancial transactions and fundingsources.

On the other hand, according to datain Figure 1, the product with murabahacontract increases in volume over theyears. It indicates that there are moslempeople uses Islamic bank to getfinancing for buying house, car, office,machinery etc. They depend on theexistence of Islamic bank and chooseIslamic banks as an alternative besideconventional banks.

Table 2. Gaps between Impelementation and Sharia Standard

No Problem Implementation Sharia Standard

1. Wakalah Contract a. Implemented but customerhas bought the goods beforehe signs wakalah contract.Customer has paid downpayment or booking fee tosupplier.

b. Customer signs wakalahcontract simultaneously withprocess of application.

Wakalah is signed beforeMurabaha contract isconcluded and Bank asprinciple is responsible forthings done by customer.

Economics and Accounting JournalVol.1, No.1, January 2018

21

c. The responsibility of bankand customer are unclear.

2. Possession a. Customer buys goods whichis not possessed or controledby bank.

b. There is no handover goodsbetween the supplier and thebank.

The handover of the goods tothe customer is implementedafter the bankpossess/controls the goods.

3. Murabaha contract The signing of murabahacontract is done withoutconsidering the process ofhandover of goods between thesupplier and the bank

For buying goods , customermake a promise with thebank. And bank could askcustomer giving a collateralas compensation if customerbreach his promise.

5. CONCLUSION

The conclusion of this research are :5.1. There are many important things,

according to sharia standards, thathave not been done in theimplementation of the wakalahcontract, taking possession andmurabah contract, it can be seen intable 2.

5.2. By ignoring sharia standard, publicperception about Islamic bank stillcontains riba and gharar becomestrue.

5.3. Causes of the occurrence of thiscondition:

5.3.1. Moslem people and practisionerare less aware of muamala shariaso they can not distinguishbetween right and wrong contractsuch as wakalah contract,murabaha contract etc.

5.3.2. The supervisory agency has notperformed its function optimallyso that the improvement processin Islamic bank has not runproperly.

5.4. Moslem people and practitioners ofIslamic banking have to improvetheir understanding aboutmuamalah sharia concept so thatIslamic banks can operate inaccordance with Holy Qur'an andSunnah of Prophet. Thus, moslempeople can play an active role in

development of Indonesiaeconomic.

REFERENCES

AAOIFI. (2015a). SS (18) Possession(Qabd). In Shari’ah Standards (p.489). Manama: Accounting andAuditing Organization for IslamicFinancial Institution (AAOIFI).

AAOIFI. (2015b). SS (23) Agency andthe Act of an UncommissionedAgent. In Shari’ah Standards (p.605). Manama: Accounting andAuditing Organization for IslamicFinancial Institution (AAOIFI).

AAOIFI. (2015c). SS (8) Murabahah. InShari’ah Standards (p. 195).Manama: Accounting and AuditingOrganization for Islamic FinancialInstitution (AAOIFI).

Central Statistic Bereau. (2011).Citizenship, Ethnicity, Religion andLanguage Everyday IndonesianPopulation, Result of PopulationCensus 2010.

Fauzi, M., Adnan, M., & Harahap, B.(2015). Problem of MurabahahFinancing of Home Ownership atBank Syariah Mandiri. JurnalPasca Sarjana Hukum UNS, III, No2. Retrieved from

Economics and Accounting JournalVol.1, No.1, January 2018

22

http://www.jurnal.hukum.uns.ac.id/index.php/pasca/article/view/781

Hanum, A. (2015). Analysis MurabahahBil Wakalah Contract (Case Studi :Bank Muamalat Indonesia , BankBRI Syariah, Bank Syariah Mandiridan Bank CIMB Niaga MalangBranch Office). FEB, UniversitasBrawijaya. Universitas Brawijaya,Malang.

Hanum, Z. (2014). Analysis ofApplication of MurabahaTransaction on PT. BankPembiayaan Rakyat (BPR) SyariahGebu Prima Medan. JurnalEkonomikawan, 14, No. 1(2015).Retrieved fromhttp://jurnal.umsu.ac.id/index.php/ekawan/article/view/221

Mu’allim, A. (2003). Public perceptionon Islamic Financial Instution. Al-Mawarid, X. Retrieved fromhttps://media.neliti.com/media/publications/25992-EN-persepsi-masyarakat-terhadap-lembaga-keuangan-syariah.pdf

Otoritas Jasa Keuangan. (2015). CircularLetter of Financial ServiceAuthority No. 36/SEOJK.03/2015.Jakarta: Otoritas Jasa Keuangan.Retrieved fromhttp://www.ojk.go.id/id/kanal/perbankan/regulasi/surat-edaran-ojk/Documents/Kodifikasi Produkdan Aktivitas BUS UUS.pdf

Otoritas Jasa Keuangan. (2017a).Indonesia Banking Statistic.https://doi.org/http://www.ojk.go.id/id/kanal/perbankan/data-dan-statistik/statistik-perbankan-indonesia/Documents/Pages/Statistik-Perbankan-Indonesia---September-2017/SPI%20September%202017.pdf

Otoritas Jasa Keuangan. (2017b). ShariaBanking Statistik Retrieved fromhttp://www.ojk.go.id/id/kanal/syariah/data-dan-statistik/statistik-perbankan-

syariah/Documents/Pages/Statistik-Perbankan-Syariah---September-2017/SPS September 2017.pdf

Pramanto, S. I. (2014). Faktors thatcause People not Choosing IslamicBank viewed from Marketing MixAspect (Study at Surabaya TimurArea). UIN Sunan Ampel,Surabaya. Retrieved fromhttp://digilib.uinsby.ac.id/1758/

Rahmatuloh Pajar. (2015). Murabahacontract and Implementation of theSharia is connected with theprologue of Murabaha practiseaccording to Ulama | Unisba -Pascasarjana. Retrieved August 26,2017, fromhttp://pasca.unisba.ac.id/akad-murabahah-dan-implementasinya-pada-syariah-dihubungkan-dengan-kebolehan-praktek-murabahah-menurut-para-ulama/

Rakhmah, P. (2014). Application ofMurabaha Contract with AdditionalFines to SME BTPN SyariahSurabaya in Islamic LawPerspective. Universitas SunanAmpel, Surabaya. Retrieved fromhttp://digilib.uinsby.ac.id/916/

Ramadhan, M. H. (2014). Perseption ofaccounting students toward IslamicBanking as Islamic FinancialInstitution. UIN Maulana MalikIbrahim, Malang. Retrieved fromhttp://etheses.uin-malang.ac.id/2002/

Sayyid, S. (2009). Agency (Wakalah). InFikih Sunnah Vol 5 (1st ed., pp.296–305). Jakarta: CakrawalaPublishing.

Sepky, M. (2015). Level of ShariaCompliance at Islamic FinancialInstitution. Jurnal Akuntansi DanKeuangan Islam, 3, No. 1(2015).Retrieved fromhttp://jurnal.sebi.ac.id/index.php/jaki/article/view/46

Setyaningtyas, P. (2016).Implementation of MurabahaContract on KPR financing

Economics and Accounting JournalVol.1, No.1, January 2018

23

Product at Bank Syariah MandiriPurwokerto Branch. Institut AgamaIslam Negeri Purwokerto.

Subchan, A. (2015). Implication ofWakalah on Murabaha Contract byBank BCA Syariah (Study at BankBCA Syariah Semarang Branch).Universitas Negeri Semarang,Semarang.

Wahbah, A.-Z. (2011). Various Kinds ofFasid Sale and Purchase FiqihIslam Wa Adillatuhu Jilid 5 (10thed., pp. 139–141). Gema Insani:Gema Insani.

Yin, R. K. (2012). Applications of CaseStudy Research - Robert K. Yin -

Google Books (3rd ed.). SagePublications Inc. Retrieved fromhttps://books.google.co.id/books?id=-1Y2J0sFaWgC&printsec=frontcover&dq=robert+K+yin&hl=en&sa=X&redir_esc=y#v=onepage&q=robert K yin&f=false

Yin, R. K. (2014). Case Study Research:Design and Methods - Robert K.Yin - Google Books (5th ed.). SagePublications Inc. Retrieved fromhttp://www.madeira-edu.pt/LinkClick.aspx?fileticket=Fgm4GJWVTRs%3D&tabid=3004