Embed Size (px)

Citation preview

Is Charitable Giving by NonitemizersResponsive to Tax Incentives?

New Evidence

Christopher M.DuquetteCenter for NavalAnalysis,The CNA Corporation,Alexandria, VA 22302

Abstract - Was nonitemizer giving responsive to the 1982-6"ahove-the-line" tax deduction provided for in the 1981 EconomicRecovery Tax Act? Here, a Tobit model is applied to Treasury Indi-vidual Tax Model file data for 1985 and 1986 to estimate the priceelasticity of nonitemizer giving. Nonitemizer giving is found to beprice-responsive. The responsiveness is, however, smaller than thatfor itemizer giving (at least for 1986 when the nonitemizer deduc-tion was fully phased in), suggesting diminishing returns fromextending the itemizers-only deduction to nonitemizers. These find-ings also question whether the nonitemizer deduction can be toutedas a highly efficient tax subsidy.

INTRODUCTION

A t present, the U.S. tax code only permits taxpayers whoXA. itemize their deductions to deduct for tax purposes thevalue of their charitable giving. Nonitemizers claim the stan-dard deduction in lieu of reporting any itemized deductions.But this has not always been the case. Best remembered forslashing individual and corporate marginal tax rates and sub-sequently indexing the tax brackets for inflation, the 1981 Eco-nomic Recovery Tax Act (ERTA) also contained a provisionphasing in a tax deduction for charitable contributions bynonitemizers. This "above-the-line" deduction was treatedas an experiment and was scheduled to expire at the end of1986. Since the Tax Reform Act of 1986 was silent on thisprovision, it expired as scheduled. The existence of the above-the-line deduction permits an estimation of the responsive-ness of nonitemizer giving to tax incentives. It then Isecomespossible to directly compare the responsiveness ofnonitemizer giving to that of giving by itennizers. Such a com-parison can be instructive in light of current proposals toreinstitute a tax deduction for nonitemizer giving as well asproposals for other sorts of above-the-line deductions (suchas education savings accotints, medical savings accounts, etc.).

The ERTA provided for the phasing in of the above-the-line contributions deduction over the five-year period 1982-6. During the first three years of the phase-in period, therewere strict dollar limits on the amount of giving thatnonitemizers could deduct for tax purposes. In 1982 and 1983,

195

Year

19821983198419851986

NATIONAL TAX JOURNAL

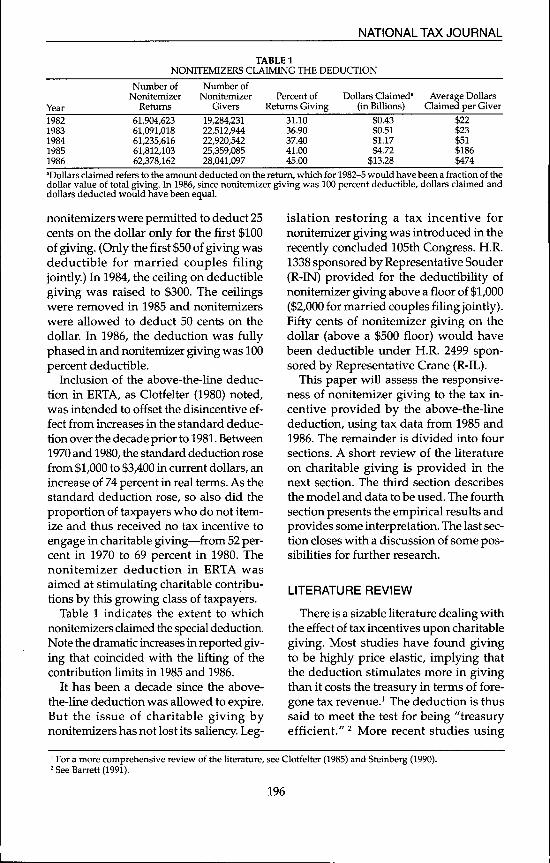

TABLE 1NONITEMIZERS CLAIMING THE DEDUCTION

Number ofNonitemizer

Retums

61,904,62361,091,01861,235,61661,812,10362,378,162

Number ofNonitemizer

Givers

19,284,23122,512,94422,920,54225,359,08528,041,097

Percent ofRetums Giving

31.1036.9037.4041.0045.00

Dollars Claimed'(in Billions)

$0.43$0.51$1.17$4.72

$13.28

' Average DollarsClaimed per Giver

$22$23$51$186$474

'Dollars claimed refers to the amount deducted on the retum, which for 1982-5 would have been a fraction of thedollar value of total giving. In 1986, since nonitemizer giving was 100 percent deductible, dollars claimed anddollars deducted would have been equal.

nonitemizers were permitted to deduct 25cents on the dollar only for the first $100of giving. (Only the first $50 of giving wasdeductible for married couples filingjointly.) In 1984, the ceiling on deductiblegiving was raised to $300. The ceilingswere removed in 1985 and nonitemizerswere allowed to deduct 50 cents on thedollar. In 1986, the deduction was fullyphased in and nonitemizer giving was 100percent deductible.

Inclusion of the above-the-line deduc-tion in ERTA, as Clotfelter (1980) noted,was intended to offset the disincentive ef-fect from increases in the standard deduc-tion over the decade prior to 1981. Between1970 and 1980, the standard deduction rosefrom $1,000 to $3,400 in current dollars, anincrease of 74 percent in real terms. As thestandard deduction rose, so also did theproportion of taxpayers who do not item-ize and thus received no tax incentive toengage in charitable giving—from 52 per-cent in 1970 to 69 percent in 1980. Thenonitemizer deduction in ERTA wasaimed at stimulating charitable contribu-tions by this growing class of taxpayers.

Table 1 indicates the extent to whichnonitemizers claimed the special deduction.Note the dramatic increases in reported giv-ing that coincided with the lifting of thecontribution limits in 1985 and 1986.

It has been a decade since the above-the-line deduction was allowed to expire.But the issue of charitable giving bynonitemizers has not lost its saliency. Leg-

islation restoring a tax incentive fornonitemizer giving was introduced in therecently concluded 105th Congress. H.R.1338 sponsored by Representative Souder(R-IN) provided for the deductibility ofnonitemizer giving above a floor of $1,000($2,000 for married couples filing jointly).Eifty cents of nonitemizer giving on thedollar (above a $500 floor) would havebeen deductible under H.R. 2499 spon-sored by Representative Crane (R-IL).

This paper will assess the responsive-ness of nonitemizer giving to the tax in-centive provided by the above-the-linededuction, using tax data from 1985 and1986. The remainder is divided into foursections. A short review of the literatureon charitable giving is provided in thenext section. The third section describesthe model and data to be used. The fourthsection presents the empirical results andprovides some interpretation. The last sec-tion closes with a discussion of some pos-sibilities for further research.

LITERATURE REVIEW

There is a sizable literature dealing withthe effect of tax incentives upon charitablegiving. Most studies have found givingto be highly price elastic, implying thatthe deduction stimulates more in givingthan it costs the treasury in terms of fore-gone tax revenue.^ The deduction is thussaid to meet the test for being "treasuryefficient." ^ More recent studies using

' For a more comprehensive review of the literature, see Clotfelter (1985) and Steinberg (1990).2 See Barrett (1991).

196

Charitable Giving by Nonitemizers

panel data, such as Bron\an (1989),Ricketts and Westfall (1993), Randolph(1995), and Barrett, McGuirk, andSteinberg (1997), have challenged the con-clusion of treasury efficiency, estimatingconsiderably smaller magnitude priceelasticities. Income elasticity is generallyestimated between 0.5 and 1.0.

Only a handful of studies, though, hasaddressed the specific question ofnonitemizer giving, and the issue remainsunsettled. Dye (1978) used data from a sur-vey of low-to-middle income households toinvestigate the existence of an "itemizationeffect"—whether the observed differencesin contributions across households mightsimply reflect the effect of itemization sta-tus rather than price. The coefficient on adummy variable representing itemizationstatus was estimated to be positive and sig-nificant, a result which was interpreted asevidence in favor of such an effect. Usingthe same data set as Dye but focusing on anarrower income range, Boskin andFeldstein (1977) obtained results that arguedagainst an itemization effect's existence. Thehypothesis of an itemization effect was alsotested for and rejected by Brown (1987).

A small number of studies have simu-lated the consequences of extending theitemizers-only deduction to nonitemizers.These include Feldstein and Taylor (1976)and Clotfelter (1980). Extending the de-duction to nonitemizers was concluded tostimulate more in giving than it wouldcost the treasury in foregone revenue.Since the findings were driven by the as-sumption of identical price elasticities forboth nonitemizers and itemizers, though,they may be suspect.

Only two studies have explicitly esti-mated the price elasticity of nonitemizergiving. The first of the two, Robinson

(1990), used tax data from 1985 and ob-tained results that were, due to the largestandard errors, inconclusive.' Morerecently, Dimbar and Phillips (1997) esti-mated a nonitemizer price elasticity us-ing a set of panel data covering both 1985and 1986. A model of year-to-year changesin contributions similar to that employedby Broman (1989) was estimated. It wasshown that the above-the-line deductionwas a highly efficient tax subsidy, with theprice elasticity of nonitemizer giving es-timated at -3.36. It was also demonstratedthat the boosting of the deductible por-tion of nonitemizer giving from 50 per-cent in 1985 to 100 percent in 1986prompted 1985 nongivers to become giv-ers in 1986. In light of these findings, theauthors questioned the wisdom of Con-gress' permitting the nonitemizer deduc-tion to expire in 1986 as scheduled.

MODEL AND DATA

This study will follow the standard prac-tice of modeling charitable giving bymeans of a double-log specification. Thelogged value of charitable contributions isrepresented as a linear function of the logof the after-tax "price" of giving, loggeddisposable income, number of dependentchildren, and dummy variables for bothmarital status and age. A Tobit regressionis used to account for the non-negativityconstraint on total giving.'' For itemizers,the difference between Tobit and ordinaryleast squares (OLS) is unimportant, as thevast majority of itemizers reported positivegiving. But for nonitemizers, the majorityof whom did not claim the above-the-linededuction, Tobit is the more appropriateregression.^ Following is a description ofeach of the regression variables.

^ The price elasticity of nonitemizer donations was estimated to be insignificantly different from zero, as well asinsignificantly different from the price elasticity of donations by itemizers.

* One could also motivate the use of Tobit by the possibility tbat some nonitemizers witb positive giving mayhave failed to claim tbe deduction due to a lack of sophistication about tbe tax code, a failure to keep records,or a fear of tbe IRS.

* The superiority of Tobit over OLS for nonitemizer giving is discussed in detail by Robinson (1990).

197

NATIONAL TAX JOURNAL

GIVING. In 1985 and 1986, bothitemizers and nonitemizers could receivea tax break by reporting charitable contri-butions on their tax returns. Fornonitemizers in 1986, as well as foritemizers in both years, donations weredeductible on a doUar-for-doUar basis. In1985, nonitemizers could only deduct onedollar for every two in contributions, sothat year's contributions deduction wouldhave to be doubled to determine total giv-ing. To avoid taking the log of zero, thestandard practice is to adjust reported giv-ing upward by some nominal amount, inthis case $10.

PRICE. The price variable is defined asthe after-tax cost to the donor of contrib-uting $1 to charity.* For itemizers and 1986nonitemizers, the federal tax deductionreduces the after-tax price of a $1 cashdonation to $1 minus the marginal taxrate. For 1985 nonitemizers, the after-taxprice of donating $1 cash would be $1minus half the marginal tax rate. To avoidthe endogeneity bias arising from the de-pendence of marginal tax rate on total giv-ing, the standard practice is to use theafter-tax price corresponding to the firstdollar of giving, as well as to exclude so-called "borderline itemizers" for whomcharitable contributions represent the dif-ference between the decision to itemize ornot to itemize.'

Because in 1985 and 1986 the tax codefavored noncash gifts over cash gifts,separate prices were calculated for the two

types of gifts and filers were grouped byincome class with separate weights calcu-lated for each class. Further reducing theprice of giving are state-level tax deduc-tions.' While state tax rates are smallerthan federal rates, their effect is nottrivial.' In 1985, for example, income taxeswere levied by 44 states plus the Districtof Columbia, with 36 permitting the de-duction of charitable contributions. Mar-ginal tax rates exceeded 10 percent in nineof those states, topping out at 16 percentin Minnesota. Following other studies, fil-ers subject to the peculiar rate structureof the altemative minimum tax were ex-cluded from the final sample.

INCOME. Disposable income is takento be the difference between before-taxincome and exogenous-of-giving taxes.For before-tax income, many studies havesimply used adjusted gross income (AGI).But AGI alone provides an incomplete pic-ture of pretax income. Certain forms of in-come are partially excluded from AGI,and there are numerous "adjustments toincome" that are subtracted out prior tofiguring AGI. An altemative is to use AGIplus the excluded part of pension income,dividend income. Social Security income,and unemployment compensation, aswell as the adjustments for the two-eamermarried deduction, IRA and Keogh plancontributions, and penalties for earlywithdrawal of savings.'" This should pro-vide a more accurate picture of before-taxincome." From this measure of before-tax

^ An altemative would bave been to employ expected future price and lagged price, but tbat would baverequired panel data to wbicb tbe autbor did not bave access.

' Conversely, there is tbe possibility tbat some filers wbo would otherwise bave itemized migbt cboose tobecome nonitemizers in 1985 and 1986 to take advantage of the standard deduction and above-the-linenonitemizer deduction. Since tbe data do not provide information on these filers' otber potential deductions,bowever, it was not possible to delete tbose so-called borderline nonitemizers.

' Since state income taxes are deductible at the federal level and federal income taxes are deductible in certainstates, tbere is an interaction between the federal and state deductions. This interaction was accounted for inconstructing tbe price term.

' Estimation of state tax rates for all taxpayers was not possible since the 1985 and 1986 ITM data sets sup-pressed the state indicator for taxpayers with adjusted gross income (AGI) exceeding $200,000.

'" Excluded capital gains were not added back since 1986 capital gains realizations contain a large transitorycomponent due to taxpayers' response to enactment of the Tax Reform Act of 1986 and its boosting of tbe toptax rate on capital gains.

" While this is preferable as a measure of pretax income, tbe results were not dependent upon its use.

198

Charitable Giving by Nonitemizers

income is subtracted the tax liability as-sociated with a charity deduction of zero.If instead the actual tax liability was sub-tracted from before-tax income, an ele-ment of bias could be intrqduced due tothe dependence of tax liability on totalcharitable contributions. To avoid takingthe log of zero or a negative number, fil-ers whose disposable income wasnonpositive were excluded from the finalsample.

Additional variables are used for de-pendents, marital status, and age. Thedependents term is defined as the sum ofthe number of exemptions claimed fordependent children living at home and fordependent children living away fromhome. Marital status and age are repre-sented by dummy variables. The maritalstatus dummy is set equal to one for mar-ried taxpayers filing jointly and zero forsingle filers. Following Slemrod (1989),married taxpayers filing separately wereexcluded due to the possibility that theirinclusion could bias the estimated priceand income elasticities. The age dummyis set equal to one if any age exemptionswere claimed, and zero otherwise.

Two sets of tax data are used, the 1985and 1986 Individual Tax Model (ITM)files, compiled by the Statistics of Incomedivision of the IRS.'̂ Of the 108,840 re-tums in the unweighted 1985 ITM dataset, 3,104 were prior-year retums. Delet-ing those left 105,736 retums, of which75,331 (71.2 percent) were itemized and30,405 (28.8 percent) claimed the standarddeduction. The relatively high proportion

of itemized returns reflects theoversampling of high-income returns,which are more likely to be itemized.(Overall, 39 percent of the 101.7 millionretums filed in 1985 itemized their deduc-tions.") A total of 72,203 (95.8 percent) ofthe itemizers and 11,000 (36.2 percent) ofthe nonitemizers reported positive giving.For the 1986 ITM set, the figures were75,400 retums, of which 1,913 were prior-year retums, leaving 73,487 retums splitbetween 53,598 (72.9 percent) itemizersand 19,889 (27.1 percent) nonitemizers.Charitable contributions were claimed by51,344 (95.8 percent) of those itemizersand 7,439 (37.4 percent) of thenonitemizers. As for the borderlineitemizers, the contributions deductionrepresented the difference between thedecision to itemize or claim the standarddeduction for 1,462 (1.9 percent) of the

1985 itemizers and 381 (0.7 percent) of the1986 itemizers.

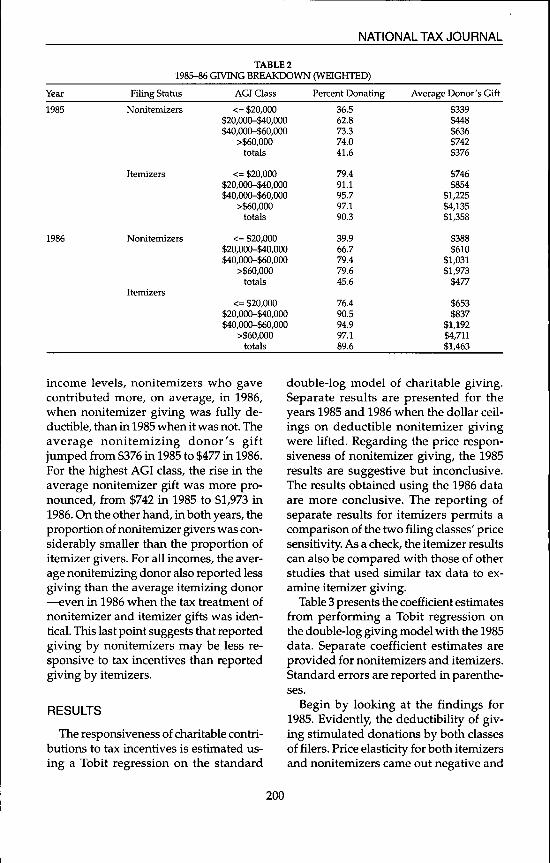

Some interesting observations can bedrawn from employing the sampleweights and breaking d.own reported giv-ing in the 1985 and 1986 ITM sets by AGIclass. Such a breakdown is presented onthe following page (Table 2).

An inspection of the weighted data sug-gests that nonitemizer giving appearedresponsive to the enhancement of the taxincentive from 1985 to 1986." Between1985 and 1986, the proportion of non-itemizers who gave rose across all incomeclasses, while the proportion of itemizers(for whom the tax treatment was notsweetened) who donated did not. At all

Tbe decision to focus on those years bas to do witb the specifics of the nonitemizer charity deduction. Al-though tbe special deduction existed from 1982 through 1986 and it is possible to obtain ITM files for all fiveyears, for the years 1982-4, nonitemizers were permitted to deduct only token amounts.Clotfelter (1990).The evidence from Table 2 is not conclusive on this point, because in 1985 and 1986, the criteria differ forwbether it is advantageous to tbe taxpayer to be an itemizer. Conceivably, some 1985 itemizers may baveopted to become 1986 nonitemizers to take advantage of the combination of tbe standard deduction and thejump from 50 to 100 percent in tbe contributions deduction. An example is a filer wbo donates generously tocharity but for wbom all otber potentially itemizable deductions total less than tbe standard deduction. Fortbat filer, it would be advantageous to itemize in 1985 but switch to nonitemizer status in 1986. Some of theboost in nonitemizer giving in 1986 could be an indication of sucb cbanges in filing status by large donorsratber than a behavioral response to the more favorable tax treatment.

199

NATIONAL TAX JOURNAL

Year

1985

1986

TABLE 21985-^6 GIVING BREAKDOWN (WEIGHTED)

Filing Status

Nonitemizers

Itemizers

Nonitemizers

Itemizers

AGI Class

<= $20,000$20,000-$40,000$40,000-$60,000

>$60,000totals

<= $20,000$20,000-$40,000$40,000-$60,000

>$60,000totals

<= $20,000$20,000-$40,000$40,000-$60,000

>$60,000totals

<= $20,000$20,000-$40,000$40,000-$60,000

>$60,000totals

Percent Donating Average Donor's Gift

36.562.873.374.041.6

79.491.195.797.190.3

39.966.779.479.645.6

76.490.594.997.189.6

$339$448$636$742$376

$746$854

$1,225$4,135$1,358

$388$610

$1,031$1,973

$477

$653$837

$1,192$4,711$1,463

income levels, nonitemizers who gavecontributed more, on average, in 1986,when nonitemizer giving was fully de-ductible, than in 1985 when it was not. Theaverage nonitemizing donor's giftjumped from $376 in 1985 to $477 in 1986.For the highest AGI class, the rise in theaverage nonitemizer gift was more pro-nounced, from $742 Ln 1985 to $1,973 in1986. On the other hand, in both years, theproportion of nonitemizer givers was con-siderably smaller than the proportion ofitemizer givers. For all incomes, the aver-age nonitemizing donor also reported lessgiving than the average itemizing donor—even in 1986 when the tax treatment ofnonitemizer and itemizer gifts was iden-tical. This last point suggests that reportedgiving by nonitemizers may be less re-sponsive to tax incentives than reportedgiving by itemizers.

RESULTS

The responsiveness of charitable contri-butions to tax incentives is estimated us-ing a Tobit regression on the standard

double-log model of charitable giving.Separate results are presented for theyears 1985 and 1986 when the dollar ceil-ings on deductible nonitemizer givingwere lifted. Regarding the price respon-siveness of nonitemizer giving, the 1985results are suggestive but inconclusive.The results obtained using the 1986 dataare more conclusive. The reporting ofseparate results for itemizers permits acomparison of the two filing classes' pricesensitivity. As a check, the itemizer resultscan also be compared with those of otherstudies that used similar tax data to ex-amine itemizer giving.

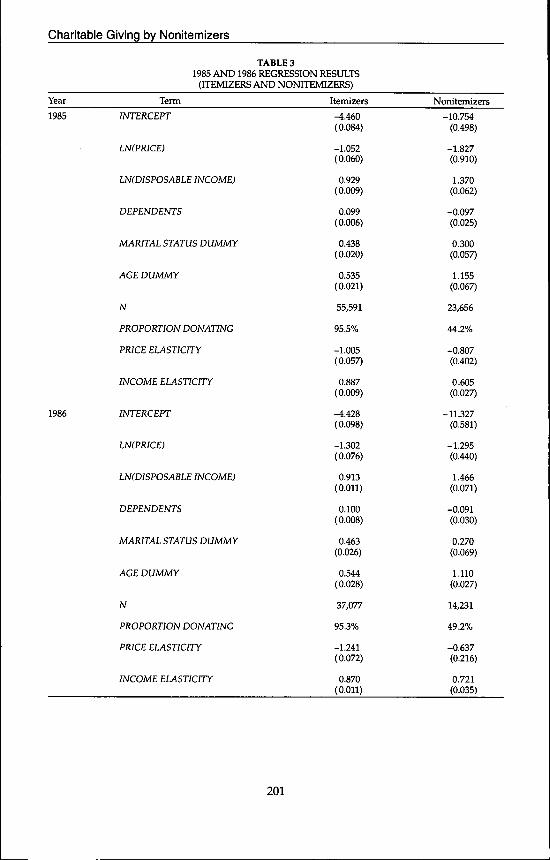

Table 3 presents the coefficient estimatesfrom performing a Tobit regression onthe double-log giving model with the 1985data. Separate coefficient estimates areprovided for nonitemizers and itemizers.Standard errors are reported in parenthe-ses.

Begin by looking at the findings for1985. Evidently, the deductibility of giv-ing stimulated donations by both classesof filers. Price elasticity for both itemizersand nonitemizers came out negative and

200

Charitable Giving by Nonitemizers

TABLE 31985 AND 1986 REGRESSION RESULTS

(ITEMIZERS AND NONITEMIZERS)

Year

1985

Term Itemizers Nonitemizers

1986

INTERCEPT

LN(PRICE)

LN(DISPOSABLE INCOME)

DEPENDENTS

MARITAL STATUS DUMMY

AGE DUMMY

N

PROPORTION DONATING

PRICE ELASTICITY

INCOME ELASTICITY

INTERCEPT

LN(PRICE)

LMDISPOSABLE INCOME)

DEPENDENTS

MARITAL STATUS DUMMY

AGE DUMMY

N

PROPORTION DONATING

PRICE ELASTICITY

INCOME ELASTICITY

^ .460(0.084)

-1.052(0.060)

0.929(0.009)

0.099(0.006)

0.438(0.020)

0.535(0.021)

55,591

95.5%

-1.005(0.057)

0.887(0.009)

-4.428(0.098)

-1.302(0.076)

0.913(0.011)

0.100(0.008)

0.463(0.026)

0.544(0.028)

37,077

95.3%

-1.241(0.072)

0.870(0.011)

-10.754(0.498)

-1.827(0.910)

1.370(0.062)

-0.097(0.025)

0.300(0.057)

1.155(0.067)

23,656

44.2%

-0.807(0.402)

0.605(0.027)

-11.327(0.581)

-1.295(0.440)

1.466(0.071)

-0.091(0.030)

0.270(0.069)

1.110(0.027)

14,231

49.2%

-0.637(0.216)

0.721(0.035)

201

NATIONAL TAX JOURNAL

significant. While the nonitemizer pointestimate came out smaller than theitemizer point estimate, the hypothesisthat price elasticity for the two filingclasses was equal could not be rejected,nor could the hypothesis that thenonitemizer price elasticity is equal to the-1 critical value for treasury efficiency.Income elasticity was estimated to be posi-tive and in the inelastic range for both fil-ing classes.

More conclusive are the results ob-tained using the 1986 data. As with 1985,for both fHing classes, price elasticity cameout negative and significant. This time,though, due largely to the decline in thesize of the standard error associated withthe nonitemizer price elasticity, the hy-pothesis that the two elasticities wereequal could be rejected. Evidently, in 1986,donations by nonitemizers were less re-sponsive to the tax subsidy than weredonations by itemizers, even though giftsby the two filing classes received identi-cal tax treatment. Alternately, the hypoth-esis that nonitemizer price elasticity isequal to the -1 critical value still could notbe rejected, although the margin nar-rowed. Estimates of income elasticity forthe two filing classes again came out inthe positive and inelastic range.

Both the 1985 and 1986 results, though,have certain shortcomings. For the 1985results, the drawback is the large standarderror associated with the nonitemizerprice elasticity. Going from 1985 to 1986,the standard error on the nonitemizerprice elasticity dropped by half. This drop-off is likely attributable to the increase inthe size of the range over which thenonitemizer price variable varied. Only 50percent of nonitemizer giving was deduct-ible in 1985, while 100 percent of

nonitemizer giving was deductible in1986. For 1986, then, there would begreater variation across taxpayers in theprice term than in 1985.'' Giving byitemizers, on the other hand, was 100 per-cent deductible in both years. Hence, therewas little change between 1985 and 1986in the standard error associated with theitemizer price elasticity.

For the 1986 results, the drawback is ofa different nature. There is the possibilitythat the 1986 giving data may be contami-nated by taxpayer timing behavior relatedto the landmark tax reforms enacted thatyear. The Tax Reform Act of 1986 mayhave influenced the timing of charitablecontributions in two ways. First, marginaltax rates fell (from 1986 to 1988, the toprate was slashed from 50 to 28 percent),thereby reducing the tax subsidy for de-ducting contributions. Filers claiming adeduction for their donations would havefaced a strong temptation to move post-1986 giving forward into 1986 in order tocapitalize on the larger tax subsidy. Theextent to which itemizers, and particularlyhigh-income itemizers, moved giving for-ward into 1986 in response to the 1986 taxreforms has been examined by Auten,Cilke, and Randolph (1992). Plus, the TaxReform Act of 1986 permitted the expira-tion of the nonitemizer deduction at theend of 1986, encouraging nonitemizers toaccelerate post-1986 giving into 1986. Suchtiming behavior is less of a concem for the1985 data, as the 1986 tax reforms didn'treally take shape and begin to gain politi-cal momentum until early 1986.̂ '

Despite those shortcomings, some sig-nificant generalizations can be drawnfrom Table 3. First, it appears that chari-table giving by nonitemizers is responsiveto tax incentives. The estimated price elas-

" For a nonitemizer facing the lowest (0 percent) federal marginal tax rate, the after-tax price of donating onedollar cash would be one dollar in 1985 and 1986 (ignoring state taxes). The after-tax price of making the samedonation for a nonitemizer facing the top federal marginal tax rate (50 percent) would be only 75 cents in 1985and 50 cents in 1986, hence the larger variation in the price term for 1986.

" See Bimbaum and Murray (1987) for a superb account of the maneuverings through Congress of the TaxReform Act of 1986.

202

Charitable Giving by Nonitemizers

ticities are negative and significant forboth 1985 and 1986. Sirrular estimates ofprice elasticity were obtained for both setsof nonitemizer regressions, despite thefact that the tax treatment of charitablegiving by that class of filers was not con-stant during 1985-6. The after-tax price ofgiving by nonitemizers fell dramaticallywhen contributions went from being 50percent deductible in 1985 to 100 percentdeductible in 1986. The similarity of theprice elasticity estimates despite thechanged tax treatment of nonitemizer giv-ing is persuasive.

While giving by nonitemizers appearsresponsive to tax incentives, it seems thatthe degree of responsiveness is smallerthan that for itemizers—at least for 1986when the above-the-line deduction wasfully phased in and giving by both filingclasses was deductible on a doUar-for-doUar basis. This is a potentially impor-tant finding. If giving by nonitemizers isless price responsive, then extending thededuction to nonitemizers would yield asmaller boost to giving than that impliedby estimates of the price elasticity foritemizers. Studies such as Feldstein andTaylor (1976) and Clotfelter (1980), whichsimulated the effect of enacting anonitemizer deduction by assuming thetwo classes of taxpayers to have identicalprice elasticities, would, then, have over-stated the boost to giving. This findingalso implies diminishing retums from ex-tending the itemizers-only deduction tononitemizers. Those taxpayers whose giv-ing is the most price sensitive, theitemizers, can of course already claim thededuction. Extending the itemizers-onlydeduction to nonitemizers would thensimply have the effect of making availablea tax deduction to a group of taxpayerswhose giving is less sensitive to tax incen-tives. Total giving increases, but at a di-minished rate.

Why might nonitemizers be less priceresponsive? One explanation has to dowith income. Nonitemizers have, on av-

erage, lower disposable incomes than doitemizers. The existence of disparities indisposable income between nonitemizersand itemizers is noteworthy, because thereis some evidence that the price responsive-ness of giving may rise with income. Afinding that high-income filers may bemore responsive than their lower-incomecounterparts was presented by Feldsteinand Taylor (1976) and Auten, Cilke, andRandolph (1992). The evidence on thispoint, however, is not conclusive, as thefindings of two other studies—Clotfelterand Steuerle (1981) and Robinson (1990)—were ambiguous.

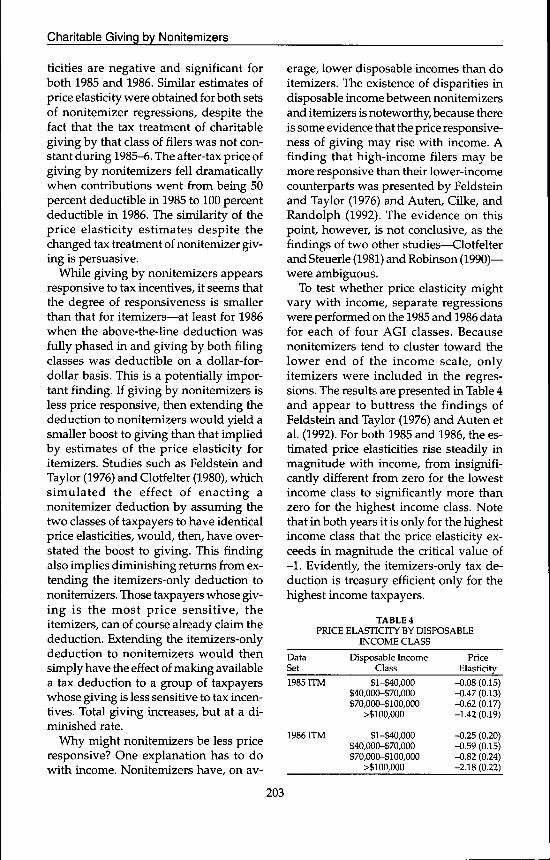

To test whether price elasticity mightvary with income, separate regressionswere performed on the 1985 and 1986 datafor each of four AGI classes. Becausenonitemizers tend to cluster toward thelower end of the income scale, onlyitemizers were included in the regres-sions. The results are presented in Table 4and appear to buttress the findings ofFeldstein and Taylor (1976) and Auten etal. (1992). For both 1985 and 1986, the es-timated price elasticities rise steadily inmagnitude with income, from insignifi-cantly different from zero for the lowestincome class to significantly more thanzero for the highest income class. Notethat in both years it is only for the highestincome class that the price elasticity ex-ceeds in magnitude the critical value of- 1 . Evidently, the itemizers-only tax de-duction is treasury efficient only for thehighest income taxpayers.

TABLE 4PRICE ELASTICITY BY DISPOSABLE

INCOME CLASS

DataSet

Disposable IncomeClass

PriceElasticity

1985 ITM

1986 ITM

$l-$40,000$40,000-$70,000$70,000-$100,000

>$100,000

$l-$40,000$40,000-$70,000$70,000-$100,000

>$100,000

-0.08 (0.15)-0.47 (0.13)-0.62 (0.17)-1.42(0.19)

-0.25 (0.20)-0.59 (0.15)-0.82 (0.24)-2.18 (0.22)

203

NATIONAL TAX JOURNAL

But perhaps there's more to it than sim-ply income differences. An altemative ex-planation holds the possibility of intrinsicdifferences between nonitemizers anditemizers. Perhaps nonitemizer giving istruly less sensitive to tax considerations.How might this be? One possibility men-tioned by Robinson (1990) has to do withthe connection between itemization statusand home ownership. Most taxpayers whoitemize do so because of the deduction forhome mortgage interest. To the extent thatthere is a link between home ownership anda commitment to the community, itemizersmight be expected to contribute more tocharitable causes than non-itemizers. Thereis also the argument that nonitemizers maybe less sophisticated than itemizers in termsof understanding the tax code. Non-itemizers are, after all, a special class of tax-payers. They claim no itemized deductionsof any sort. They are not required to main-tain as many records for tax purposes. Theirlevel of expertise and ability to capitalizeon tax benefits is likely to be inferior to thatof itemizers. As such, it is entirely plausiblethat taxpayers who don't itemize would beintrinsically less responsive to tax incen-tives than those who do.

These findings also cast some doubt onthe conclusion of Dunbar and Phillips(1997) that the nonitemizer deduction is ahighly efficient tax subsidy. Recall thatDunbar and Phillips found nonitemizergiving to be highly price elastic, with aprice elasticity of -3.36—larger than all buta handful of studies have obtained foritemizers and easily exceeding the stan-dard for treasury efficiency. Here, thepoint estimates for nonitemizer price elas-ticity were considerably smaller, and forneither 1985 nor 1986 could the hypoth-esis that price elasticity equaled the criti-cal value of -1 be rejected.

CONCLUSIONS

In order to stimulate charitable givingby nonitemizers, the 1981 ERTA included

a provision phasing in, over the period1982-6, a full tax deduction for non-itemizer giving. It appears to have suc-ceeded. Charitable contributions bynonitemizers seem to have been respon-sive to the decrease in the after-tax "price"of giving occasioned by the special deduc-tion. Using Tobit to estimate a model ofgiving on 1985 and 1986 tax data, the priceelasticity of nonitemizer giving was de-termined to be negative and significant.For 1985, when nonitemizer donationswere 50 percent deductible, the price elas-ticity of nonitemizer giving was found tobe insignificantly different froni that ofitemizer giving—a result which parallelsthat of Robinson (1990). More conclusiveare the findings for 1986, when the above-the-line deduction was fully phased inand giving by both nonitemizers anditemizers was deductible on a dollar-for-doUar basis. Those results indicate a priceelasticity for nonitemizer giving smallerin magnitude than that for itemizer giv-ing. Such would imply diminishing re-turns from extending the itemizers-onlydeduction to nonitemizers. It would alsosuggest that earlier studies, which as-sumed identical price elasticities for thetwo filing classes in simulating the effectof extending the itemizer deduction tononitemizers, would have overpredictedthe boost to giving. Income elasticities ofbetween 0.5 and 1.0 were estimated forboth classes of filers.

A related issue is that of how an exten-sion of the itemizers-only deduction tononitemizers might alter the overall mixof giving. Which charities would benefitmost? It has already been noted that, onaverage, nonitemizers tend to displaylower incomes than itemizers. ButFeldstein (1975) and Clotfelter (1990) havenoted that giving by lower-income filerstends to be concentrated with religiouscharities. (Giving by high-income filersfavors other charities such as museumsand schools.) It follows, then, that exten-sion of the itemizers-only deduction to

204

Charitable Giving by Nonitemizers

nonitemizers would confer the greatestbenefit upon religious charities. That con-clusion may be of particular interest, inlight of recent proposals by SenatorAshcroft (R-MO) and others to expand therole of faith-based organizations in fight-ing poverty and meeting other socialneeds.

Acknowledgments

I wish to thank Steven Sheffrin, JayHelms, and Peter Lindert, the membersof my dissertation committee, for theirhelpful comments and advice. I am alsograteful to Jim Chalfant, Erick Eschker,and three anonymous referees. Any errorsare my own.

REFERENCES

Auten, Cerald E., James M. Cilke, andWilliam C. Randolph.

"The Effects of Tax Reform on CharitableContributions." National Tax joumal 45 No.3 (September, 1992): 267-90.

Barrett, Kevin S."Panel-Data Estimates of Charitable Civing:A Synthesis of Techniques." National TaxJournal 44 No. 3 (September, 1991): 365-81.

Barrett, Kevin S., Anya M. McCuirk, andRichard Steinberg.

"Further Evidence on the Dynamic Impactof Taxes on Charitable Giving." National TaxJournal 50 No. 2 Qune, 1997): 321-34.

Bimbaum, Jeffrey, and Alan Murray.Showdown at Gucci Gulch. New York: Ran-dom House, 1987.

Boskin, Michael, and Martin Feldstein."Effects of the Charitable Deduction on Con-tributions by Low Income and Middle In-come Households: Evidence from the Na-tional Survey of Philanthropy." The Reviewof Economics and Statistics 59 (1977): 351-4.

Broman, Amy."Statutory Tax Reform and Charitable Con-tributions: Evidence from a Recent Periodof Reform." Journal of the American TaxationAssociation 11 (1989): 7-21.

Brown, Eleanor."Tax Incentives and Charitable Civing: Evi-dence from New Survey Data." Public Fi-nance Quarterly 15 (1987): 386-96.

Clotfelter, Charles."Tax Incentives and Charitable Civing: Evi-dence from a Panel of Taxpayers." Journal ofPublic Economics 13 (1980): 319-40.

Clotfelter, Charles.Federal Tax Policy and Charitable Giving. Chi-cago: University of Chicago Press, 1985.

Clotfelter, Charles."The Impact of Tax Reform on CharitableCiving: A 1989 Perspective." In Do TaxesMatter? The Impact of the Tax Reform Act of1986, edited by Joel Slemrod, 203-25. Cam-bridge: MTT Press, 1990.

Clotfelter, Charles, and C. Eugene Steuerle."Charitable Contributions." In How TaxesAffect Economic Behavior, edited by H. Aaronand J. Pechman, 403-46. Washington, D.C:The Brookings Institution, 1981.

Dunbar, Amy, and John Phillips."The Effect of Tax Policy on Charitable Con-tributions: The Case of Nonitemizing Tax-payers." Journal of the American Taxation As-sociation 19 (1997): 1-20.

Dye, Richard."Personal Charitable Contributions: Tax Ef-fects and Other Motives." In Proceedings ofthe 70th Annual Conference of the National TaxAssociation, 311-21. Washington, D.C: Na-tional Tax Association, 1978.

Feenberg, Daniel."Are Tax Price Models Really Identified: TheCase of Charitable Civing." National TaxJournal 40 No. 4 (December, 1987): 629-33.

Feldstein, Martin."The Income Tax and Charitable Contribu-tions: Part n— T̂he Impact on Religious, Edu-cational, and Other Organizations." NationalTax Journal 28 No. 2 Qune, 1975): 209-26.

Feldstein, Martin, and A. Taylor."The Income Tax and Charitable Contribu-tions." Econometrica 44 (1976): 1201-22.

Lankford, R. Hamilton, and James Wyckoff."Modeling Charitable Civing Using a Box-Cox Standard Tobit Model." The Review ofEconomics and Statistics 73 (1991): 460-70.

205

NATIONAL TAX JOURNAL

McDonald, John, and Robert Moffitt."The Uses of Tobit Analysis." The Review ofEconomics and Statistics 62 (1979): 318-21.

Randolph, William."Dynamic Income, Progressive Taxes, and theTmning of Charitable Contributions." Journalof Political Economy 103 (1995): 709-38.

Ricketts, Robert, and Peter Westfall."New Evidence on the Price Elasticity ofCharitable Contributions." Journal of theAmerican Taxation Association 15 (1993): 1-25.

Robinson, John."Estimates of the Price Elasticity of Chari-table Giving: A Reappraisal Using 1985Itemizer and Norutemizer Charitable De-duction Data." The Journal of the AmericanTaxation Association 12 (1990): 39-50.

Slemrod, Joel."Are Estimated Tax Elasticities Really JustTax Evasion Elasticities? The Case of Chari-table Contributions." The Review of Econom-ics and Statistics 11 (1989): 517-22.

Steinberg, Richard."Taxes and Giving: New Findings." Voluntas1 (1990): 61-79.

U.S. Department of the Treasury.Tax Reform for Fairness, Simplicity, and Eco-nomic Growth: The Treasury DepartmentReport to the President. Vol. 2. Washington,D.C: U.S. Government Printing Office,1984.

U.S. Internal Revenue Service.Individual Income Tax Returns. Washington,D.C: U.S. Government Printing Office.

206