Embed Size (px)

Citation preview

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Long-Lived Nonmonetary Assets and Their Amortization

© The McGraw-Hill Companies, Inc., 1999

7Part One: Financial Accounting

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

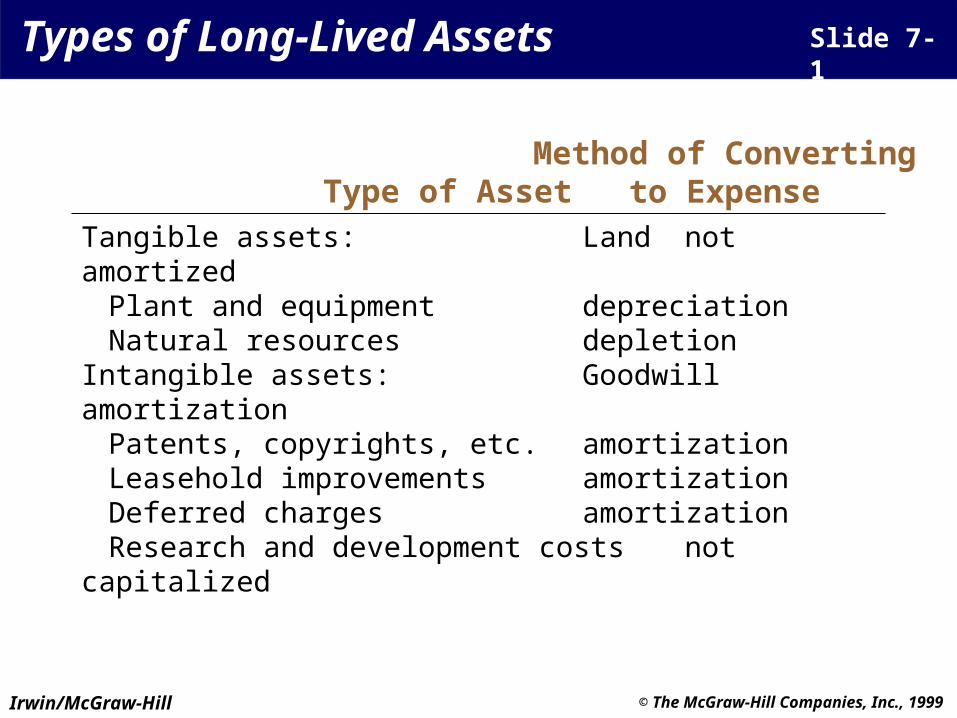

Tangible assets:Land not amortizedPlant and equipment depreciationNatural resources depletion

Intangible assets:Goodwill amortizationPatents, copyrights, etc. amortizationLeasehold improvements amortizationDeferred charges amortizationResearch and development costs not capitalized

Types of Long-Lived Assets Slide 7-1

Type of AssetMethod of Converting

to Expense

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Purchase priceSales taxTransportation costs Installation cost

Items Included in Cost Slide 7-2

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

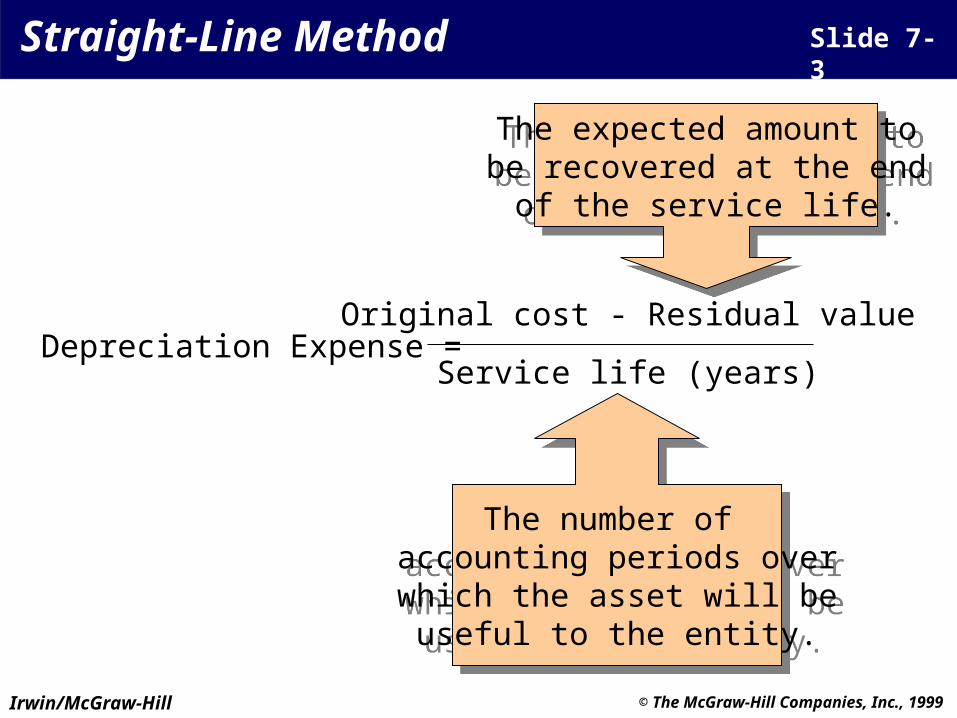

Straight-Line Method Slide 7-3

Depreciation Expense =Original cost - Residual value

Service life (years)

The number of accounting periods overwhich the asset will be

useful to the entity.

The number of accounting periods overwhich the asset will be

useful to the entity.

The expected amount tobe recovered at the end

of the service life.

The expected amount tobe recovered at the end

of the service life.

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Straight-Line Method Slide 7-4

Depreciation Expense =Original cost - Residual value

Service life (years)

Depreciation Expense =$10,000 - $1,000

5 years

Depreciation Expense = $1,800

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

$10,000

Year 1: $10,000 x .40 = $4,000 6,000

Year 2: $6,000 x .40 = 2,400 3,600

Year 3: $3,600 x. 40 = 1,440 2,160

Year 4: $2,160 x .40 = 864 1,296

Year 5: $1,296 - $1,000 = 296 1,000

Declining-Balance Method Slide 7-5

Note that this amount reduces the book value to the salvage value.

Note that this amount reduces the book value to the salvage value.

DepreciationExpense

BookValue

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

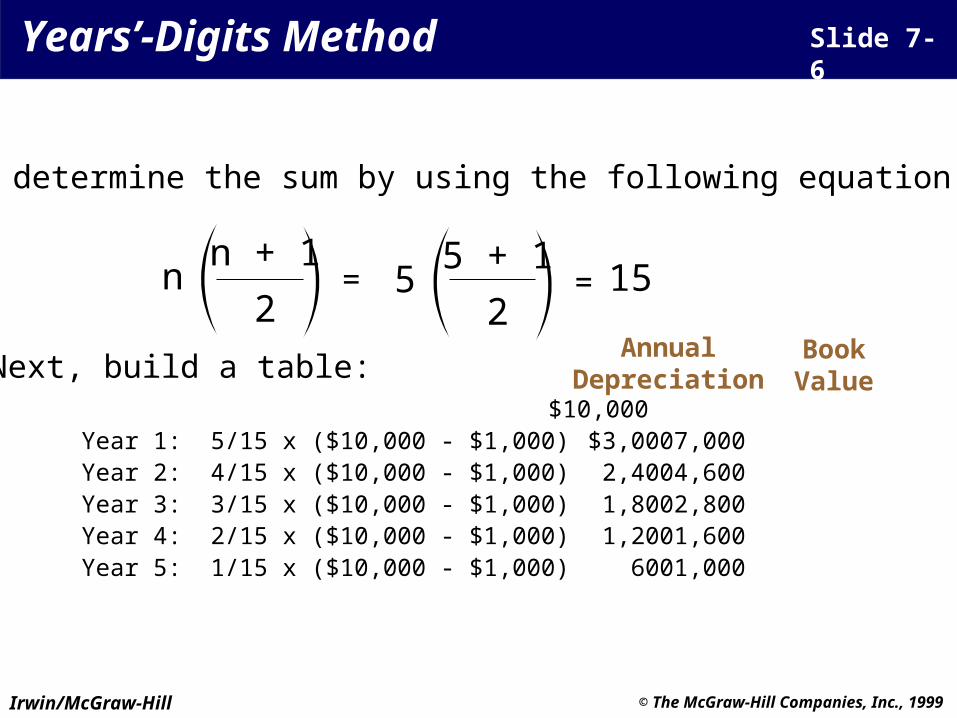

$10,000Year 1: 5/15 x ($10,000 - $1,000) $3,000 7,000Year 2: 4/15 x ($10,000 - $1,000) 2,400 4,600Year 3: 3/15 x ($10,000 - $1,000) 1,800 2,800Year 4: 2/15 x ($10,000 - $1,000) 1,200 1,600Year 5: 1/15 x ($10,000 - $1,000) 600 1,000

n + 1

2

Years’-Digits Method Slide 7-6

First, determine the sum by using the following equation:

n =5 + 1

25 = 15

Next, build a table:Annual

DepreciationBookValue

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

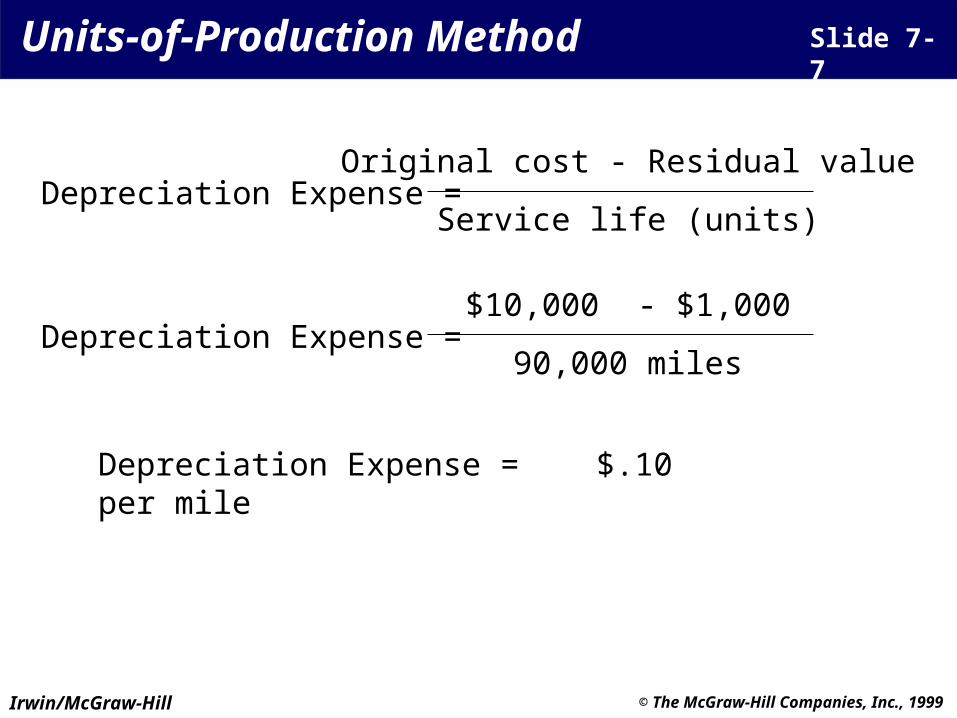

Units-of-Production Method Slide 7-7

Depreciation Expense =Original cost - Residual value

Service life (units)

Depreciation Expense =$10,000 - $1,000

90,000 miles

Depreciation Expense = $.10 per mile

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

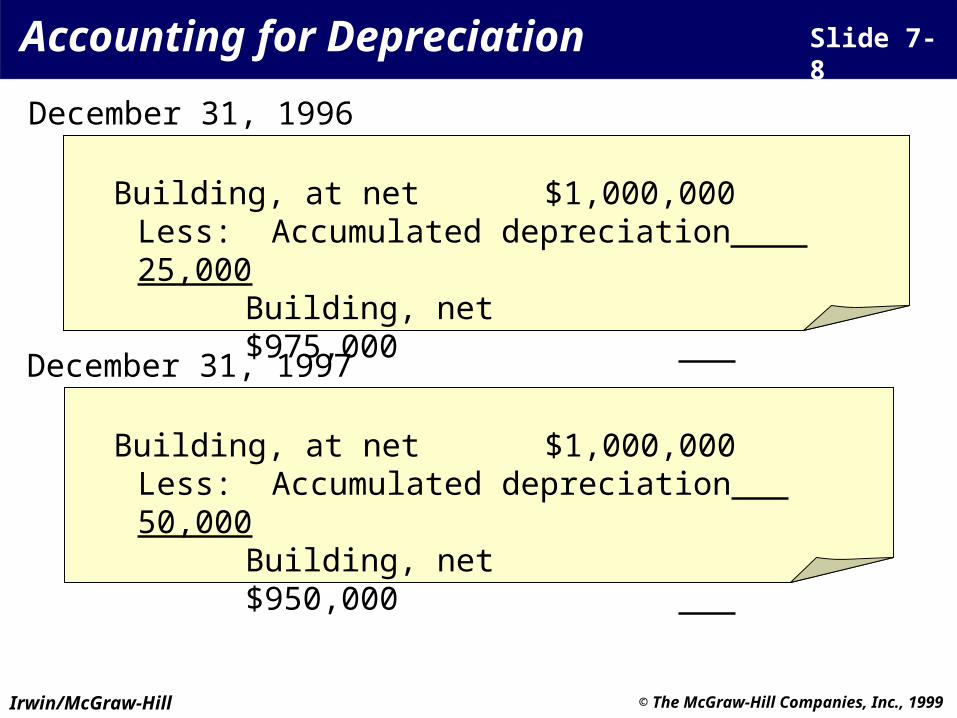

Accounting for Depreciation Slide 7-8

Building, at net $1,000,000Less: Accumulated depreciation 25,000

Building, net$975,000

December 31, 1996

Building, at net $1,000,000Less: Accumulated depreciation 50,000

Building, net$950,000

December 31, 1997

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Accounting for Depreciation Slide 7-9

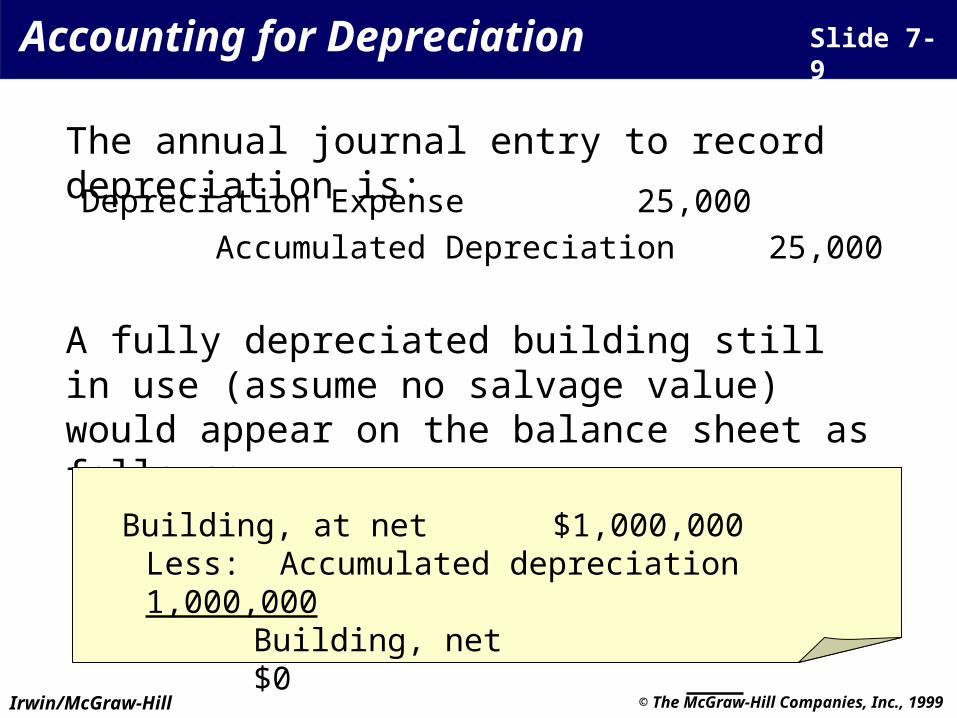

The annual journal entry to record depreciation is:

Depreciation Expense 25,000

Accumulated Depreciation 25,000

A fully depreciated building still in use (assume no salvage value) would appear on the balance sheet as follows:

Building, at net $1,000,000Less: Accumulated depreciation 1,000,000

Building, net$0

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Disposal of Plant and Equipment Slide 7-10

A building is sold for its book value of $750,000:

Cash 750,000

Accumulated Depreciation 250,000

Building 1,000,000

Assume instead that the building was sold for $650,000:Cash 650,000

Accumulated Depreciation 250,000

Loss on Sale of Building 100,000

Building 1,000,000

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

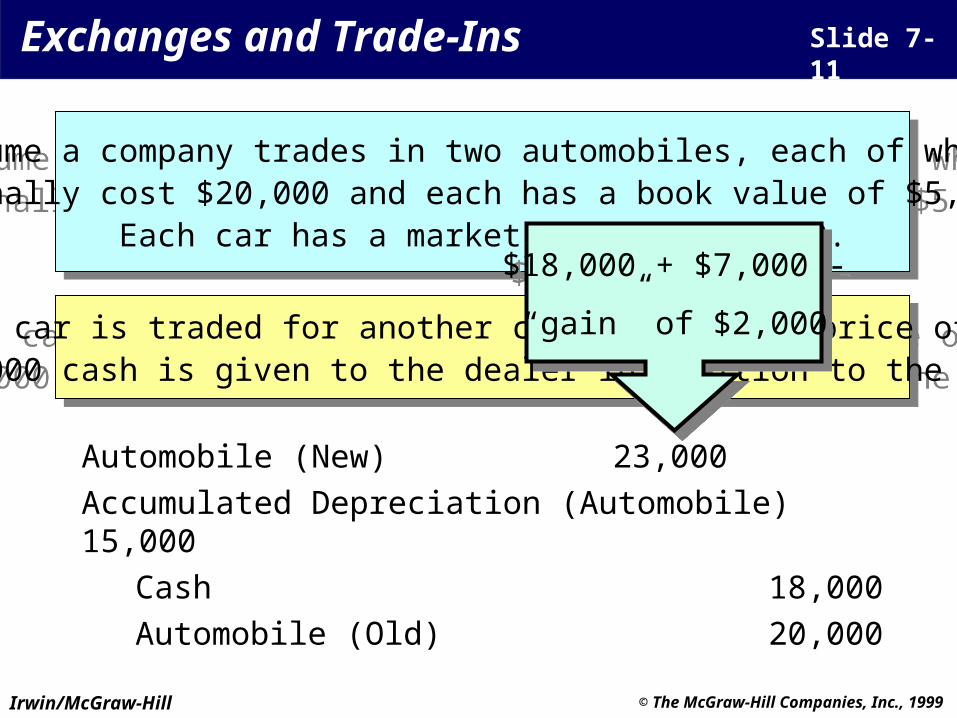

Exchanges and Trade-Ins Slide 7-11

Assume a company trades in two automobiles, each of which originally cost $20,000 and each has a book value of $5,000.

Each car has a market value of $7,000.

Assume a company trades in two automobiles, each of which originally cost $20,000 and each has a book value of $5,000.

Each car has a market value of $7,000.

The first car is traded for another car with a list price of $30,000,and $18,000 cash is given to the dealer in addition to the trade-in.

The first car is traded for another car with a list price of $30,000,and $18,000 cash is given to the dealer in addition to the trade-in.

Automobile (New) 23,000

Accumulated Depreciation (Automobile) 15,000

Cash 18,000

Automobile (Old) 20,000

$18,000 + $7,000 -

“gain” of $2,000

$18,000 + $7,000 -

“gain” of $2,000

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

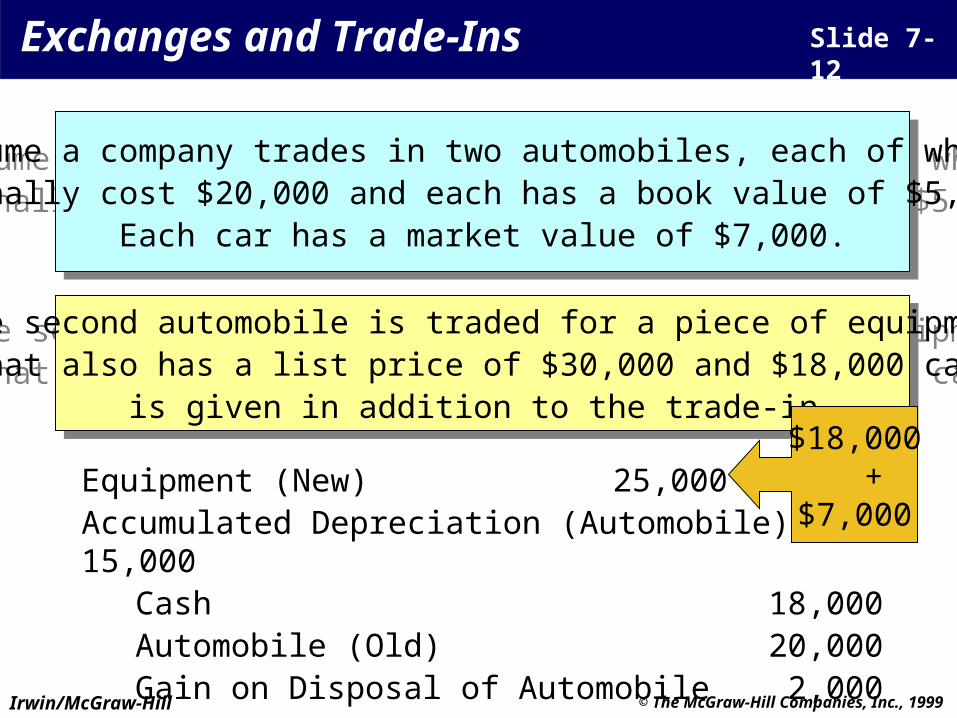

Exchanges and Trade-Ins Slide 7-12

Assume a company trades in two automobiles, each of which originally cost $20,000 and each has a book value of $5,000.

Each car has a market value of $7,000.

Assume a company trades in two automobiles, each of which originally cost $20,000 and each has a book value of $5,000.

Each car has a market value of $7,000.

The second automobile is traded for a piece of equipmentthat also has a list price of $30,000 and $18,000 cash

is given in addition to the trade-in.

The second automobile is traded for a piece of equipmentthat also has a list price of $30,000 and $18,000 cash

is given in addition to the trade-in.

Equipment (New) 25,000Accumulated Depreciation (Automobile) 15,000

Cash 18,000Automobile (Old) 20,000Gain on Disposal of Automobile 2,000

$18,000 +

$7,000

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

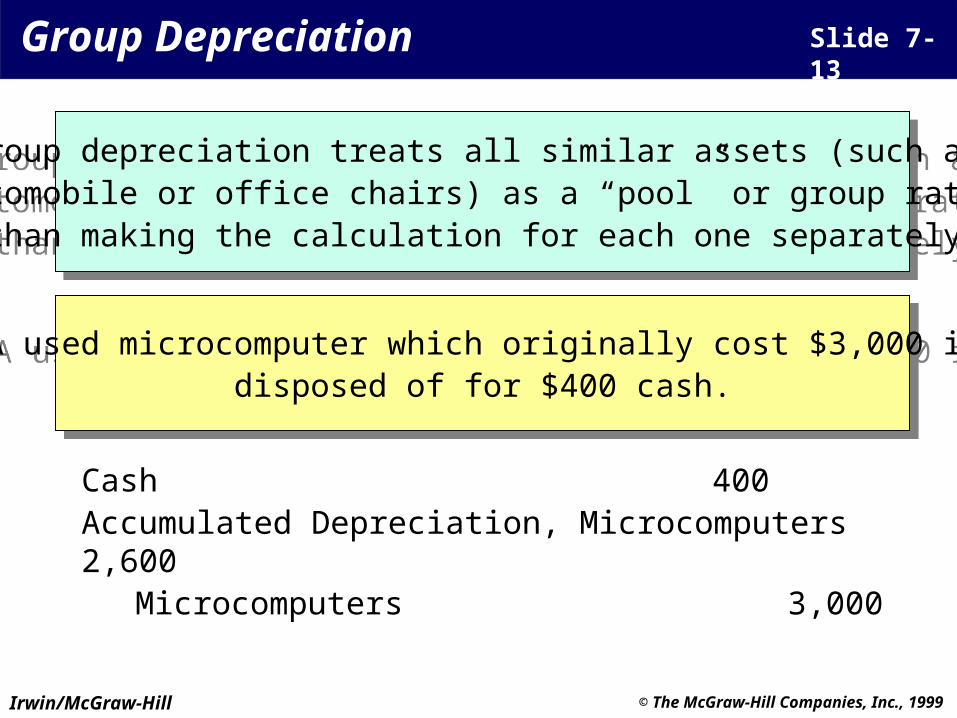

Group Depreciation Slide 7-13

Group depreciation treats all similar assets (such as automobile or office chairs) as a “pool” or group rather

than making the calculation for each one separately.

Group depreciation treats all similar assets (such as automobile or office chairs) as a “pool” or group rather

than making the calculation for each one separately.

A used microcomputer which originally cost $3,000 isdisposed of for $400 cash.

A used microcomputer which originally cost $3,000 isdisposed of for $400 cash.

Cash 400Accumulated Depreciation, Microcomputers 2,600

Microcomputers 3,000

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

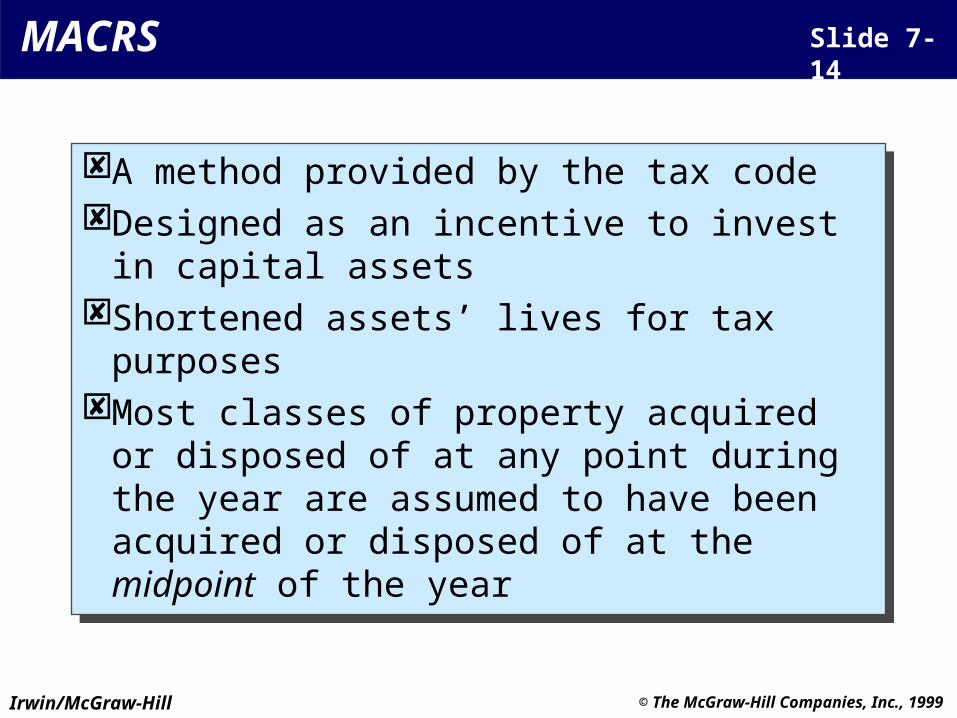

A method provided by the tax codeDesigned as an incentive to invest in capital

assetsShortened assets’ lives for tax purposesMost classes of property acquired or

disposed of at any point during the year are assumed to have been acquired or disposed of at the midpoint of the year

A method provided by the tax codeDesigned as an incentive to invest in capital

assetsShortened assets’ lives for tax purposesMost classes of property acquired or

disposed of at any point during the year are assumed to have been acquired or disposed of at the midpoint of the year

MACRS Slide 7-14

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

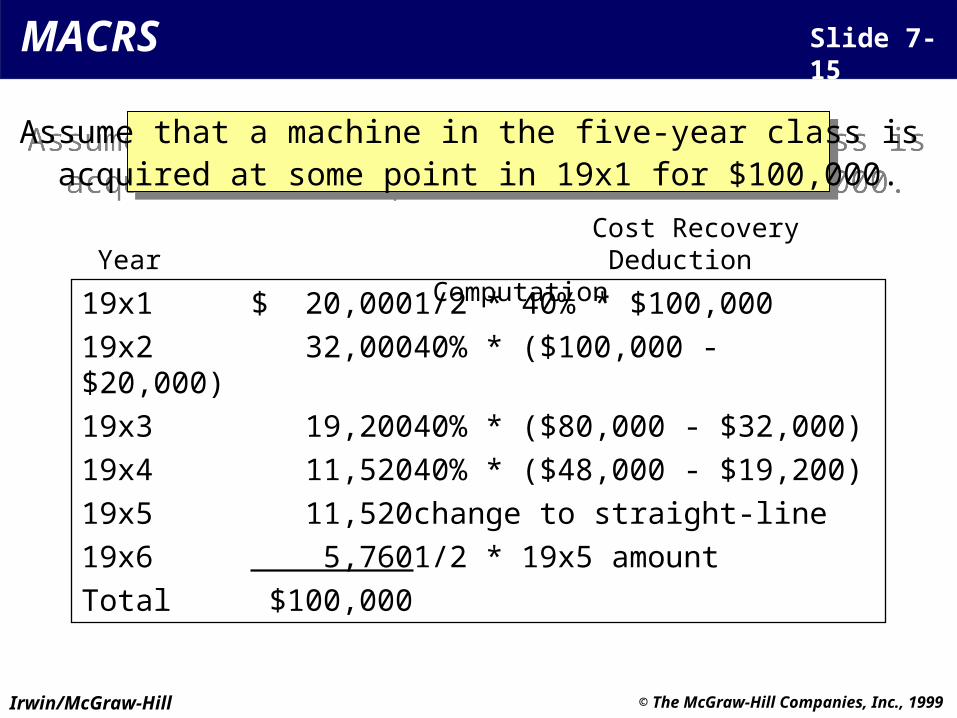

19x1 $ 20,000 1/2 * 40% * $100,000

19x2 32,000 40% * ($100,000 - $20,000)

19x3 19,200 40% * ($80,000 - $32,000)

19x4 11,520 40% * ($48,000 - $19,200)

19x5 11,520 change to straight-line

19x6 5,760 1/2 * 19x5 amount

Total $100,000

MACRS Slide 7-15

Assume that a machine in the five-year class is acquired at some point in 19x1 for $100,000.

Assume that a machine in the five-year class is acquired at some point in 19x1 for $100,000.

Cost Recovery Year Deduction Computation

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Investment Tax Credit Slide 7-16

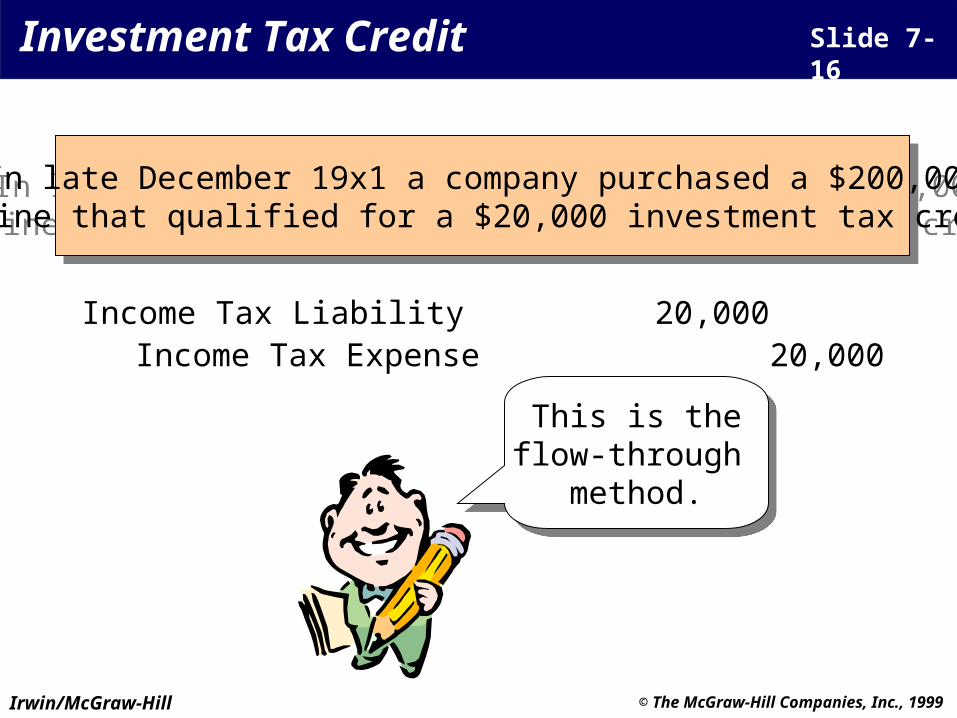

In late December 19x1 a company purchased a $200,000machine that qualified for a $20,000 investment tax credit.

In late December 19x1 a company purchased a $200,000machine that qualified for a $20,000 investment tax credit.

Income Tax Liability 20,000 Income Tax Expense 20,000

This is theflow-through

method.

This is theflow-through

method.

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Investment Tax Credit Slide 7-17

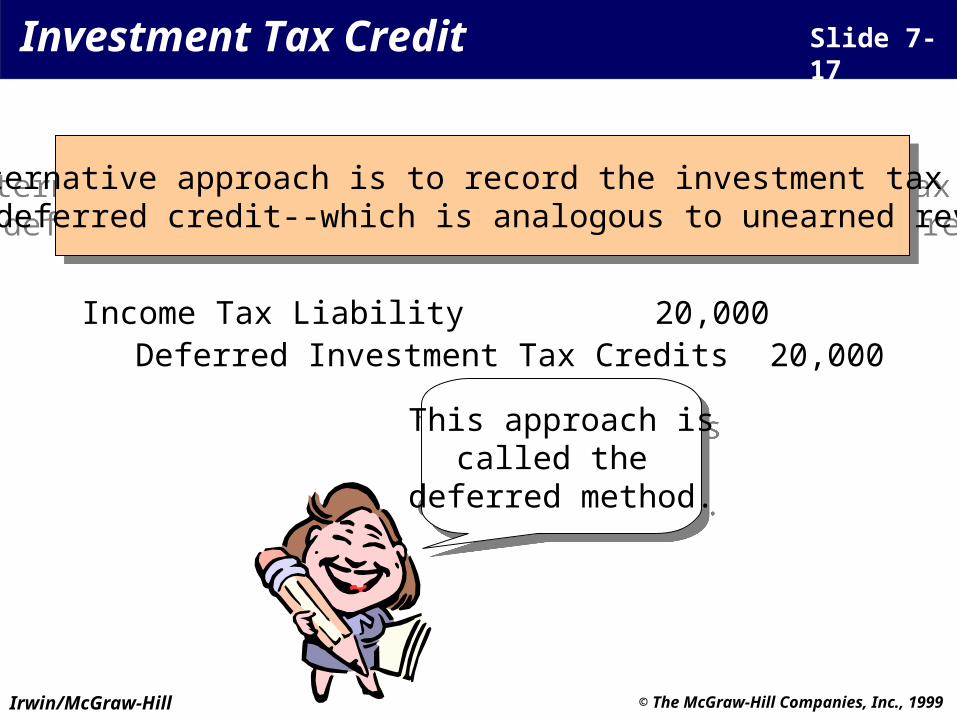

An alternative approach is to record the investment tax creditas a deferred credit--which is analogous to unearned revenue.

An alternative approach is to record the investment tax creditas a deferred credit--which is analogous to unearned revenue.

Income Tax Liability 20,000 Deferred Investment Tax Credits 20,000

This approach iscalled the

deferred method.

This approach iscalled the

deferred method.

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Investment Tax Credit Slide 7-18

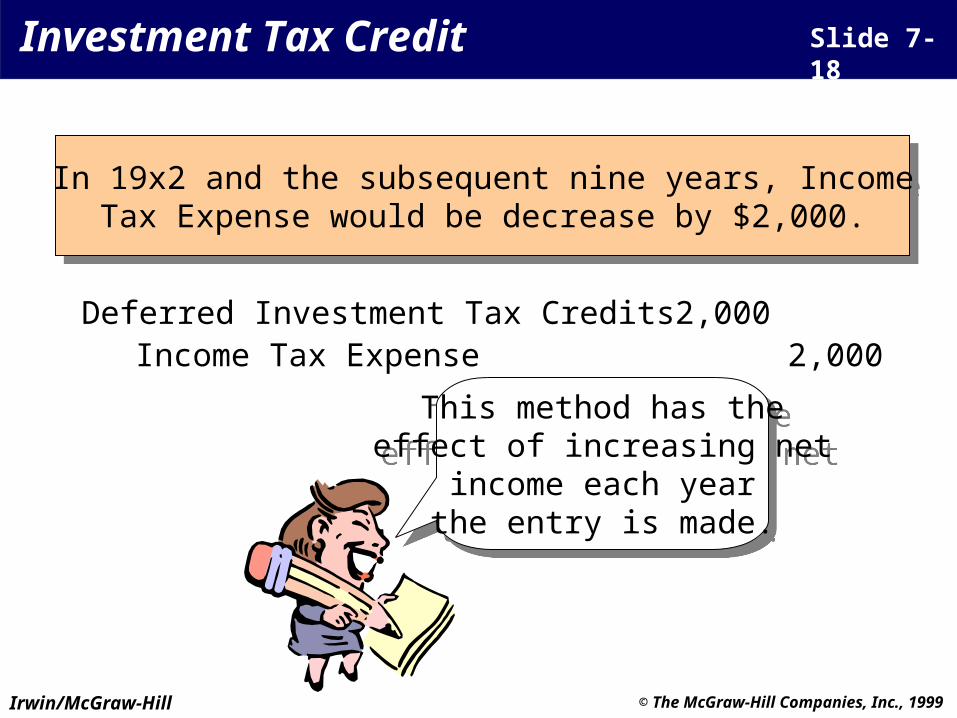

In 19x2 and the subsequent nine years, IncomeTax Expense would be decrease by $2,000.

In 19x2 and the subsequent nine years, IncomeTax Expense would be decrease by $2,000.

Deferred Investment Tax Credits 2,000Income Tax Expense 2,000

This method has theeffect of increasing net

income each yearthe entry is made.

This method has theeffect of increasing net

income each yearthe entry is made.

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Depletion Expense Slide 7-19

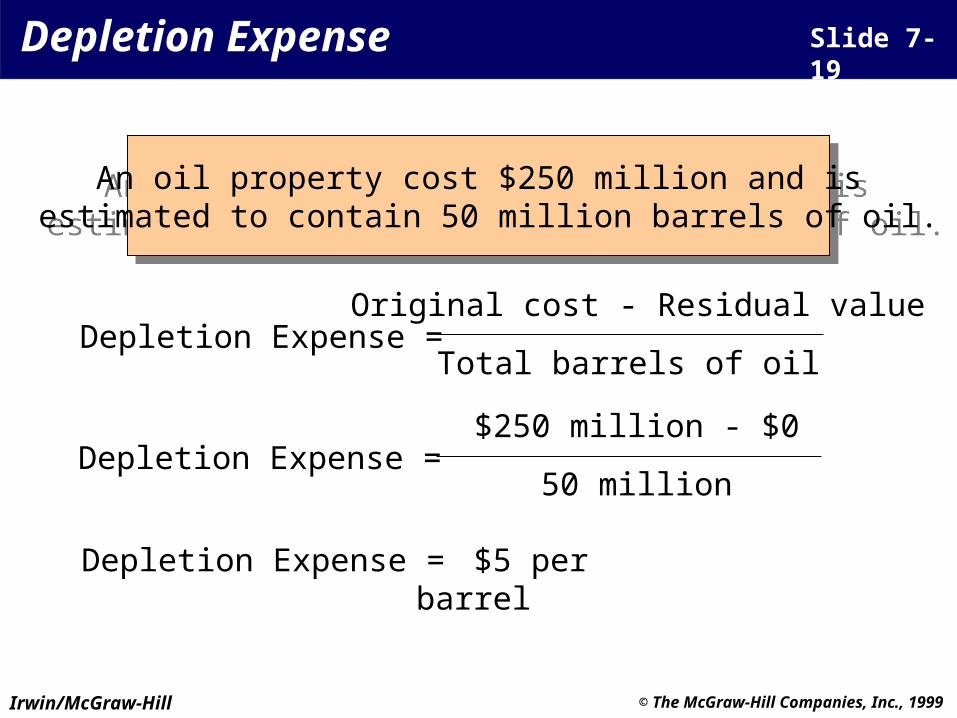

An oil property cost $250 million and is estimated to contain 50 million barrels of oil.

An oil property cost $250 million and is estimated to contain 50 million barrels of oil.

Depletion Expense =Original cost - Residual value

Total barrels of oil

Depletion Expense =$250 million - $0

50 million

Depletion Expense = $5 per barrel

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

• Goodwill• Patent• Copyrights• Franchise rights• Leasehold improvements• Deferred charges• Research and development costs

Intangible Assets Slide 7-20

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Chapter 7

The End