Embed Size (px)

Citation preview

IRS Targets Captive Insurance Companies:

Structuring Section 831(b)-Compliant

Operating Documents Avoiding Tax Penalties, Navigating IRS Safe Harbors, and Ensuring Premium Deductibility

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

TUESDAY, MAY 5, 2015

Presenting a live 90-minute webinar with interactive Q&A

Beckett G. Cantley, Professor of Tax Law, John Marshall Law School, Atlanta

John Colvin, Partner, Colvin & Hallett, Seattle

F. Hale Stewart, Owner, The Law Office of Hale Stewart, Houston

Robert J. Walling, III, Principal and Consulting Actuary, Pinnacle Actuarial Resources,

Bloomington, Ind.

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the

instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-

926-7926 ext. 10.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone listening is no longer permitted.

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-873-1442 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

NOTE: If you are seeking CPE credit, you must listen via your computer — phone listening is no longer permitted.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

For CLE credits, please let us know how many people are listening online by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of attendees at your location

• Click the SEND button beside the box

In order for us to process your CLE, you must confirm your participation by completing and submitting an Official

Record of Attendance (CLE Form) to Strafford within 10 days following the program.

The CLE form is included in your dial in instructions email and in a thank you email that you will receive at the

end of this program.

Strafford will send your CLE credit confirmation within approximately 30 days of receiving the completed CLE form.

For CPE credits, attendees must listen throughout the program, including the Q & A session, and record verification

codes in the corresponding spaces found on the CPE form, in order to qualify for full continuing education credits.

Strafford is required to monitor attendance.

If you have not printed out the “CPE Form,” please print it now.

Please refer to the instructions emailed to registrants for additional information. If you have any questions, please

contact Customer Service at 1-800-926-7926 ext. 10.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-hand column on your

screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's

program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

F. Hale Stewart, JD, LL.M.

Masters in Domestic and International taxation,

TJSL School of Law

Magna Cum Laude

Co-Author of US Captive Insurance Law, 2nd

Edition

Tax Analysts’ Author

Domestic and International Tax Structuring

at The Law Office of Hale Stewart and US

Global Tax

5

What is Insurance?

• Insurance Factors

– Definite Risk

– Fortuity

– Insurable Interest

– Risk Shifting

– Risk distribution

– Harper Test

• (1) whether the arrangement involves the existence of “insurance

risk”;

• (2) whether there was both risk shifting and risk distribution; and

• (3) whether the arrangement was for “insurance” in its commonly

accepted sense.

6

Captive Insurance

and Market Failure

• Starting in the 1950s, certain businesses either couldn’t find insurance, or could only find very expensive insurance.

– Flood Cases

– Oil and Gas

– Large Contractors (Stearns Rogers)

– Hospitals (Humana)

• In the 1970s, the US insurance industry was sued under four causes of action

– Asbestos

– Professional Liability (Med Mal)

– Environmental Claims

– Products Liability

• These cases were very expensive leading to some bankruptcies and major payouts.

• Starting in the late 1970s, the insurance industry started to greatly limit their actual exposure, slowly eliminating expensive insurance coverage.

7

All Common Insurance Policies

Have Large Exemptions

• CGL

– Employment Claims

– Employee Fidelity (employee theft)

– Cyber-Risk

– Products Liability

– Products Recall

– Loss of key contract/loss of key person

• Property

– Pollution

– Mold Remediation

– Flooding

– Windstorm Deductible

8

The Captive Insurance Story Arc

• From the late 1970s to the late 1980s, the IRS won

most of their cases.

• Why?

– Better Prepared

– Taxpayers put on terrible cases

– Courts were unsophisticated

– Lack of solid insurance definition

9

The Captive Insurance Story Arc

• From the latest 1980s to 2002, taxpayers won most of

the cases.

• Why?

– Better prepared

– IRS’ argument starts to unravel

– Courts are more sophisticated

10

Pre-UPS Risk

Subjective Intent

• 1.) Ocean Drilling and Exploration Co. v. United States, 24 Cl. Ct. 714, 715 (1991) (‘‘Because of the limited experience in insuring the new rigs and a number of substantial losses on these rigs, insurance rates increased sharply’’);

• 2.) Kidde Industries Inc. v. United States, 40 Fed. Cl. 42 (1977) (‘‘In 1976, in the midst of a products liability insurance crisis in which many insurance companies either ceased or significantly restricted their coverage of products liability. . . . Travelers informed Kidde that it would not renew Kidde’s products liability insurance policy for 1977’’);

• 3.) Malone and Hyde Inc. v. Commissioner, T.C. Memo. 1989-604 (‘‘By the mid-1970s, the Hyde Insurance Agency found that insurance premiums were increasing each year and certain insurance was not obtainable for some clients’’);

11

Pre-UPS Subjective

Intent: The

Humana Decision

Tree

1. Going naked: not an option when several successful

wrongful death claims could bankrupt the company

2. Forming a reserve: rejected because there were no

tax benefits

3. Forming a group captive: this was rejected out of

concern the other participants had financial problems

4. Forming a captive: accepted and approved

12

Objective Substance

of Early

Captive Structures

After Humana, taxpayers opted for one

of two strategies to create sufficient

substance:

The Presence of 3rd Party Risk

For example, Harper Group had 30%

Sears had 90%+

Sufficient Distribution Within the

Corporate Group

Humana 12+ entities

13

Safe Harbor Guidance,

Part I

Under Harper, a captive must comply

with a three prong test:

(1) whether the arrangement involves the existence of “insurance risk”;

(2) whether there was both risk shifting and risk distribution; and

(3) whether the arrangement was for “insurance” in its commonly accepted sense.

The duck test – does the company “walk and talk” like an insurance company?

14

Safe Harbor Guidance,

Part II

The IRS has issued several Revenue

Rulings that provide further safe harbor

guidance

A captive must derive at least 50% of

its insurance revenue from a non-

parent.

Or, a captive must have at least 12

subsidiaries in order to have sufficient

risk distribution.

15

Slide Intentionally Left Blank

IRS TARGETS CAPTIVE INSURANCE COMPANIES: STRUCTURING

SECTION 831(B)-COMPLIANT OPERATING DOCUMENTS

MAY 5, 2015

BECKETT G. CANTLEY Atlanta’s John Marshall Law School &

Atlanta Law Group

IRS Judicial Weapons: Anti-Avoidance Rules

• Substance over form

• Business Purpose

• The Sham Transaction

• Economic Substance

• The Step Transaction

18

Substance Over Form

• The facts that make up the transaction is its “form”.

• The “substance” of the transaction is what is actually below the surface of the facts, sometimes where such facts are created solely for such substance.

• This doctrine disregards the form in favor of the true substance to disallow the tax benefits generated by the artificial nature of the transaction.

19

IRC 831(b) Example

• IRC 162 deduction for ordinary & necessary expenses, potentially including insurance.

• Assume a risk pool is used to create the insurance, & risk is being kidnapped.

• An oil and gas executive who spends 6 mos in Nigeria needs a kidnapping & ransom policy. A dentist in Boulder, Colorado does not.

• The form is the risk pool, the substance is an unnecessary expense creating a deduction.

20

The Economic Substance Doctrine Now Codified

• Prong 1: The transaction is rationally related to a plausible non-tax business purpose

• Prong 2: The transaction results in a meaningful and appreciable enhancement in the net economic position of the taxpayer other than to reduce tax.

• Code: penalties as high as 75% and there is no way to use a tax opinion to use “reasonable cause” as a defense.

21

IRC 831(b) Example Loan Backs

• Insured deducts premium paid to CIC. The insured (or its owner) immediately borrows significant funds back out without paying taxes on the money.

• Rev. Rul. 2002-89, the IRS Manual, and case law indicate such CIC loan backs are at least subject to strict scrutiny, and may be prohibited under certain circumstances.

• The IRS has asked for comments on the facts & circumstances that would give rise to loan back determinations.

• This issue has come up as a focus in audits.

• IRS may challenge as an improper tax-free distribution.

22

IRC 831(b) Example Loan Backs

• Prong One: Hard to argue that the transaction is rationally related to a useful non-tax business purpose. If you needed the money enough to have it loaned out shortly after paying it, why did you make the premium payment to start with other than to get the tax deduction?

23

IRC 831(b) Example Loan Backs (4 of 4)

• Prong Two: Transaction appears that there is no meaningful enhancement in the net economic position of the taxpayer other than to reduce tax. Your position is identical before and after the transaction with respect to the loaned funds. The only difference is that you have deducted the premium.

24

IRS Statutory Weapons

• Listed Transaction Designation

• Transaction of Interest Designation

• Promoter Investigations

• List Maintenance Requests

• Criminal Investigations

25

Listed Transaction Designation

• IRS can designate a transaction as “listed” and trigger reporting requirements and potentially severe penalties for taxpayers and advisors.

• IRS rarely does this, so it is usually reserved for transactions that are done across the US among numerous taxpayers.

• IRS states its position in the listing notice, and judiciary has taken this designation seriously.

26

IRC 831(b) Example

• In early 2000’s IRS designated a captive variant structure as a listed transaction.

• The IRS eventually withdrew the listing on a go forward basis, apparently in part because the deal was not widespread enough.

• Given the popularity of 831(b) captives, and the promoter exams that are ongoing, it seems like only a matter of time until something becomes a listed transaction.

27

Transaction of Interest Designation

• IRS can put a transaction with certain attributes on a sort of “watch list” where the IRS thinks the transaction is abusive, but is not ready to “list” the transaction permanently.

• Transactions of interest have similar reporting and penalty attributes to listed transactions.

• It is up to taxpayers and advisors to keep up with what the IRS posts to this list. There is no ignorance defense.

28

IRC 831(b) Example

• It would not be surprising to find a captive transaction that involves a captive being used as a tax deductible vehicle to fund some sort of investment, and either (a) severely overstates coverage costs, or (b) improperly distributes risk, as a transaction of interest.

29

Promoter Investigations

• If IRS finds several taxpayers who have a common advisor or pool that appear to be taking the same abusive activity, IRS may open a promoter examination of the advisor.

• If IRS determines the advisor is a promoter, IRS may penalize them as such at the close of the investigation.

30

IRC 831(b) Example (1 of 2)

• IRS Personnel Statements Include:

– IRS planning on bringing “a great many” CIC cases

– IRS planning on “expanding” promoter exams

– IRS seems very interested in the “investments” as driver for CIC formation & operation

– IRS concerned with promotional material that focuses on tax benefits & investment return

– IRS hiring private sector forensic personnel required for ramping up caseload

31

IRC 831(b) Example (2 of 2)

• Forensic audits of taxpayers.

– IRS will drill down deep into a case

– Determining issues that should concern IRS

– Common touch points across other cases

– Specific professionals or risk pools in common

• Open 6700 promoter examinations of:

– Risk Pools

– CIC companies

32

List Maintenance Requests

• The IRS can request a list of all clients of an advisor, or pool participants if investigation is of a pool.

• Where IRS has found an offending taxpayer, this tool allows IRS to quickly locate a large number of potential taxpayers to audit that may have done the same thing.

• IRS will look for similar touch points among taxpayers to map out the web of promoters.

33

IRC 831(b) Example

• IRS finds one captive that has risk distributed improperly in a pool.

• IRS will request the pool to provide a list of all participants, and then will audit some or all of the participants, to see if the pool has improperly risk distributed all its participant captives.

34

Criminal Investigations

• CID investigations can now progress simultaneously with civil promoter examinations.

• A promoter exam can be referred to CID for potential criminal prosecution.

• This is obviously reserved for the worst actors.

• To date, these cases appear to involve “pretend we are doing it right” discussions with taxpayers.

35

IRC 831(b) Example

• Criminal warrants issued in cases in several states.

– Risk Pools

– Captive professionals

• Grand jury indictment in one advanced case.

– Clients told better not to make claims

– Promoters focused on tax savings (not insurance)

36

Dirty Dozen Listing

• Covering Ordinary or Implausible Risks

• Structured Maximized Premiums

• Poor Actuarial Substantiation

• Excessive Fees Charged to Unsophisticated Taxpayers

37

Senate Finance Committee

• Raise premium cap to $2.2m but lose 831(b) qualification if no more than 20% of premium from one insured.

• Proposal tabled, while IRS investigates estate planning in captives.

• Sen. Grassley is a very serious opponent to abusive tax avoidance transactions.

• IRS will take investigation seriously.

• Legislation is likely to result to curb abuses.

38

Where is this Going? IRS Investigation Pattern Familiar

• First: targeted forensic audits

• Discover common denominators

• Begin 6700 promoter investigations

• Begin criminal investigations

• Broad based warnings to taxpayers

• We are here

• Issue broad based guidance

• Start broad audit program based on guidance

39

THE END

FOR MORE INFO:

http://aegiscaptive.com/articles/

Slide Intentionally Left Blank

John M. Colvin Colvin + Hallett

T: (206) 223-0800

Email: [email protected]

Tax Controversy Issues Pertaining to Captive Insurance Companies

Issues with Risk Distribution: Related Insureds

Gulf Oil Corp. v. Comm’r, 89 T.C. 1010, 1025-26 (1987) (Dicta: “[U]nrelated risks need not be those of unrelated parties; a single insured can have sufficient unrelated risks to achieve adequate risk distribution.”)

IRS Position: Number of Exposure Units alone not sufficient PLR 200837041 IRS focuses on “number of policyholders” – not clear what this means, especially in group master policies, or situations where

there are multiple named insureds (e.g. doctors in a professional practice), all of whom presumably is a “policyholder”

Distribution among related parties: Number of insureds required? Rev. Rul. 2002-90 - 12 brother-sister insureds each with between 5-15% premium volume

Rev. Rul. 2002-91 - Suggests 7 group captive insureds are sufficient (equal owners - each with less than 15% ownership, vote and premium volume)

PLR 200837041 suggests 5 insureds are sufficient

Rev. Rul. 2005-40 –

One insured is not sufficient

12 disregarded LLCs held by one owner are not sufficient because just “one insured” for tax purposes.

12 LLCs are sufficient if classified as corporations (separate entities) for tax purposes.

43

Risk Distribution: Amount of Unrelated Risks Required

ODECO (Fed. Cl.): 44% unrelated is sufficient

Rev. Rul. 2002-89: 50% unrelated is sufficient

10% unrelated is not sufficient

PLR 201126038 30 percent of the company's risks was unrelated insurance through

reinsurance and a reinsurance pool

IRS suggested that an insurance company must have both sufficient number of insureds (per RevRuls) or sufficient unrelated business. If too concentrated will fail.

44

Rent-A-Center: Facts

Insurance sub (Legacy) insured brother-sisters (15 subs)

Handled first layer – claims up to $350,000, then reinsured with a commercial

reinsurer for the excess – reasonable business arrangement for high

frequency, low severity claims

3,000 stores, 20,000 employees, 8,000 vehicles

No third party business

Relatively high risk concentration in one sub (RAC East , over 50%)

Premiums actuarially determined (monthly payroll, vehicles, stores)

45

Rent-A-Center: Potential Problems

RAC issued guarantee (of Legacy’s deferred tax asset DTA) in order to meet Bermuda solvency requirement The DTAs were deferred tax assets arising from timing differences in amount of taxes payable for tax versus financial

accounting purposes – would take effect if tax laws changed that impaired the tax asset Failure to qualify as an insurance company for US tax purposes might have impaired these assets? Guarantee limited to $25M – small in comparison to $264M in premium

Bermuda regulator gave Legacy permission to treat DTAs as general business assets At the end of 2006, RAC canceled the guarantee because Legacy met the regulator’s solvency margins without it

Payment of premiums and claims largely by journal entry Legacy did not have much 3P investments, buying RAC treasury stock, non-dividend paying (had

approval of regulator for this investment)

High premium to surplus ration (compared to commercial insurers) Bermuda requires $120,000 or 10% of loss and loss expense provisions, plus reserves or 20% of first $6 million of net

premiums up to $6M, 10% of premium over $6M $9.9M capital under % of premium formula

Tax consequences were considered in structuring arrangement

46

Rent-A-Center: Preliminary Matters

Netting of premiums/claims was permissible

Premiums actuarially determined and reasonable in amount

Valid business reasons for arrangement

Premium-to-surplus ration was not unreasonable – commercial insurers

make money on investment side (surplus). Captives need not do this.

Workers comp, automobile and general liability are true insurance risks

Arrangement similar to those “commonly accepted” as insurance. Legacy

issued policies, charged actuarially determined premiums and paid claims.

47

Rent-A-Center: Risk Shifting and Risk Distribution

Risk Shifting

Follows 6th Circuit in Humana (reversing Tax Court) in accepting that brother-sister arrangements

may shift risks

Need not be risk shifting “comparable to that provided by a commercial insurance company” as

suggested by IRS expert

Separate and viable entity capable of meeting obligations

R expert admitted that if respect form, then shifted risk

Guarantees and investment in parent’s stock did not alter this conclusion

Risk shifting from S perspective not altered by P guarantee

Risk Distribution

Agrees risk distribution was met based on number of risks (employees, locations, automobiles)

Did not analyze risk distribution based on number of entities or “level of concentration of risks”

48

Rent-A-Center: Concurring and Dissenting Opinions

Concurrence – (Buch) Agreed with analysis, but thought the discussion of sibling argument (Humana) was

unnecessary because IRS had abandoned that position in Rev. Rul. 2001-31 (Rauenhorst – IRS is deemed to have conceded arguments which are contrary to Revenue Rulings)

Dissent (Lauber) “Not arm’s length”

Inadequately capitalized – effect of parental guarantees

Not operate like a real insurance (COMMERCIAL) company would No non-RAC employees

Netting of premiums/loss payments – looks more like a bank account/reserve fund from which to pay “self insurance”

Dissent (Halpern) Should not have overruled prior conclusion in Humana.

49

Securitas Holdings, Inc. & Subs. v. Commissioner, T.C. Memo. 2014-225 – Facts

Operating subsidiaries employed 2000,000 people in 20 countries in security,

alarm and cash handling businesses

P acquired a Vermont captive (Protectors), which had been in runoff

Set up new Irish captive reinsurer (SGRL). Protectors reinsured all risks of

operating subs with SGRL

P guaranteed performance of Protectors with respect to policies issued to subs with

purpose of prevent losing §501(c)(15) status of other member of controlled group)

3 largest subs each had more than 15% of the risks/premium (20%, 25% and 37%)

Protectors lent all but $1 million of capital to P, with approval of VT regulators

50

Securitas: Risk Shifting

Holdings guarantee of Protectors’ obligation did not shift risk of loss to P

Purpose of guarantee was to preserve § 501(c)(15) status of other member of controlled group

No amounts were ever paid on guarantee

Protectors was not undercapitalized

Premium to surplus ration was very low considering “net insurance” premium (Protectors reinsured 100% of risks)

o SGRL was adequately capitalized

• Journal entry payment system did not result in P maintaining risk of loss

51

Securitas: Risk Distribution

Despite underlying premiums/risks related to dozens of entities, IRS argued that risk assumed by SGRL all came from Protectors (the initial insurer)

Court looks through entities to large number of employees, offices, vehicles and services, finding a large poop of statistically independent risks, which did not vanish because brought together in one entity

Note: The IRS argument in this case was contrary to its previously stated position that risk distribution in the reinsurance setting is determined by looking through to the insureds on the underlying policies. Rev. Rul. 2009-26 (direct), PLRs 200950016 and 200950017 (layers)

52

Consequences of Invalid Section 953(d) Election (AM 2014-002)

If the captive is foreign and there is a § 953(d) election in place, the election terminates if the company ceases to be “an insurance company.”

Being an “insurance company” means more than half of the business during the taxable year is issuing insurance or annuity contracts. § 816(a) via § 831(c). PLR 201019001

Exception for companies in runoff? Must insurer continue to take in premium to qualify?

Consequences of termination include:

§ 367 tax event – deemed transfer of the company’s assets to a foreign corporation and an exchange that is taxable to the domestic corporation (Chapman Glen, Ltd. v. CIR, 140 T.C. No. 15 (2013) in Tax Court and Rev.Rul. 2003-47) on first day of subsequent taxable year

Subpart F inclusions in later years (or PFIC treatment if more widely owned)

Foreign Insurance Excise Tax under 4371

Essentially any deferral benefits end when stops taking in significant premium, but perhaps before all of the insured risks have been resolved.

Filing of Form 1120 does not protect shareholders because no Form 5471 was filed by shareholders (statute extended pursuant to § 6501(c)(8)). AM 2014-002.

53

Risks of Failure to Maintain 831(b) Status

Generally to maintain § 831(b) status, more than half of TP business is the issuance of insurance contracts The legislative history of 2004 revisions to insurance provisions provides, "[i]t is not intended that a company whose sole

activity is the run-off of risks under the company's insurance contracts be treated as a company other than an insurance company, even if the company has little or no premium income." H.R. Conf. Rep. No. 108-457, 2d Sess. 50-51 (2004).

PLR 201031001 – Exception for taxpayer in runoff status Insurance company was in receivership under control of state insurance commissioner and not taking in any new premium;

“[A]t no time during the period Taxpayer has been in liquidation could Taxpayer's investment activity be considered in excess of its requirements to pay claims.”

TP remains eligible for §831(b) status

What if investment activity is significantly in excess of amounts needed to pay claims and/or risk exposure terminates? Inclusion of prior premium in income to extent not required to reserve?

54

Failure to Qualify as § 501(c)(15) - TAM 201517018

Facts Captive for group of companies in real estate development and petroleum business, providing “non-

traditional coverages,” covering risks that are not covered by commercial insurers. “Administrative actions” “employment practices” “excess general liability” and “special

risks/medical” coverages, primarily issued to two entities Insurance amounted to 1% to 2% of total revenue in two years and 24% in a third year Held real estate as investment assets (and paid management fees to related parties) Paid a claim, but may have been outside policy coverage

Ruling Insurance was not primary and predominant activity – majority of business was related to

businesses other than insurance. Treasury Reg. § 1.831-3(a) Analyze type of risks separately (homogeneity) – insufficient distribution because only one policy

holder in each type of coverage for two of the coverages Claim payment appears to have been a business cost for real estate development ventures.

(Business risk not insurance risk)

55

Homogeneity

Risks in the same line of coverage

Is risk distribution tested in the aggregate or line-by-line?

No court has required homogeneity

FSA 1998-578 (April 1, 2002), Rev. Rul. 2002-89 and Rev. Rul. 2005-40 all

suggest that the IRS requires homogeneity

Notice 2005-49 sought comments on the relevance of homogeneity

ILM 200849013 (July 24, 2008) instructed Exam to determine whether

homogeneity is a relevant factor

56

Amount of Premium

Premiums based on arm's length commercial rates (always good fact in cases) or high quality actuarial work

IRS gets suspicious if premiums appear to be based on the $1.2 million section 831(b) amount. NSAR 20020160 (April 17, 2002)

Premiums should not be based on deduction sought and/or the owner's available cash flow. Salty Brine I, Ltd. v. U.S., Docket No. 10-cv-108 (N.D. Tex. May 16, 2013)

57

Adequate Capitalization

Guarantees from owner(s)

Indemnification or hold-harmless agreements

Letters of credit from owner(s)

Circular cash flows/loan-backs

Recent cases suggest that courts will be receptive to captives that depart from commercial premium/capital ratios (4:1 to 2:1)

Often captives have low capital in early years (funded primarily with deductible premium), then capital increases as profits accumulate

Accumulated Earnings Tax Issues

58

Risk Pooling

ILM 200844011 (Oct. 31, 2008) Contractual pooling arrangement

“Pool” constitutes a foreign entity such that premiums paid are subject to Federal Excise Tax

PLR 200907006 Company that participated in a reinsurance pool with several unrelated insurers qualified as an

insurance company

PLRs 201224018, and 201030014 Each taxpayer's risks for each line of business were those of at least 12 underlying insureds with no

single underlying insured representing more than 15 percent of taxpayer's total risk

PLRs 201219009, 201219010 and 201219011 Originally TPs received favorable rulings

IRS examined later and found language in contacts that appeared to preclude an individual captive entity from making a claim without having to repay the pool with interest (negated risk shifting).

59

Insurance Risk vs. Business/Investment Risk

IRS Position: Not all contracts that transfer risk are insurance policies. Contracts that protect against the failure to achieve a desired investment return protect against investment risk, not insurance risk. Insurance risk requires a fortuitous event or hazard and not a mere timing or investment risk. A fortuitous event (such as a fire or accident) is at the heart of any contract of insurance. CIR v. Treganowan, 183 F.2d 288, 290-91 (2d Cir. 1950)

LeGierse, 312 U.S. at 542 (the risk must not be merely an investment risk)

SEC v. United Benefit Life Insurance Co., 387 U.S. 202, 211 (1967) (the transfer of an investment risk cannot by itself create insurance)

Rev. Rul. 89-96, 1989-2 C.B. 114 (risks transferred were in the nature of investment risk, not insurance risk);

Rev. Rul. 68-27, 1968-1 C.B. 315 (although an element of risk existed, it was predominantly a normal business risk of an organization engaged in furnishing medical services on a fixed price basis rather than an insurance risk)

Rev. Rul. 2007-47, 2007-30 I.R.B. 127 (the arrangement lacked the requisite insurance risk to constitute insurance because the arrangement lacked fortuity and the risk at issue was akin to the timing and investment risks of Rev. Rul. 89-96).

60

Insurance Risk vs. Business/Investment Risk: Foreign Exchange Insurance

Foreign Exchange Risk not insurance risk. ILM 201511021

Statement of Statutory Accounting No. 60, “Financial Guaranty Insurance,” describes such insurance as providing “protection against financial loss as a result of . . . fluctuations in exchange rates between currencies.”

Subs entered into contracts with the captive insurance company to mitigate risk in foreign currency exchange rate fluctuations through indemnification of loss of earnings caused by the fluctuations.

The contracts had many features found in insurance policies, and an outside actuary performed an actuarial review.

IRS rules not insurance risk: currency fluctuation risk is part of general business risk

61

Insurance Risk vs. Business/Investment Risk: Residual Value Insurance

RVI Guaranty Co., Ltd. & Subs. v. CIR, Tax Court Docket No. 27319-12, TAM 201149021

Case has been tried and briefed

Coverage at issue provides payments if assets (real estate, commercial vehicles, equipment) have a residual value less than expected at the end of a lease term

Stay tuned!

62

IRS Warning IR 2015-19 (February 3, 2015) Some Captives Are Abusive

“In the abusive structure, unscrupulous promoters persuade closely held entities to participate in this scheme by assisting entities to create captive insurance companies onshore or offshore, drafting organizational documents and preparing initial filings to state insurance authorities and the IRS. The promoters assist with creating and ‘selling’ to the entities often times poorly drafted ‘insurance’ binders and policies to cover ordinary business risks or esoteric, implausible risks for exorbitant ‘premiums,’ while maintaining their economical commercial coverage with traditional insurers.”

“Total amounts of annual premiums often equal the amount of deductions business

entities need to reduce income for the year; or, for a wealthy entity, total premiums amount to $1.2 million annually to take full advantage of the Code provision [§ 831(b)]. Underwriting and actuarial substantiation for the insurance premiums paid are either missing or insufficient. The promoters manage the entities’ captive insurance companies year after year for hefty fees, assisting taxpayers unsophisticated in insurance to continue the charade.”

63

IRS Disclosure of Similar Captive Arrangements in Audit/Litigation ILM 201250020

The IRS suggests that third party pattern evidence demonstrating that the arrangements did not take into account each participant’s individual risk profile could be used to show that the arrangements were not insurance. For example, if the documents demonstrated that the arrangement entered into by the other taxpayers was not tailored to those taxpayers' individual situation and risk because the other taxpayers' insurance documents were identical to B-1's and C-1's documents, this pattern evidence would demonstrate the arrangement was not “insurance” in the other taxpayers' case and would satisfy the “item test [of Section 6103(h)(4)(B)].”

With respect to the argument that specific captive insurance arrangements lack economic substance, “pattern evidence” from other participants showing that all the arrangements were designed, implemented, and operated identically can be used to demonstrate that the arrangement was not designed with a specific taxpayer's business needs in mind and therefore lacked a bona fide business purpose other than tax benefits.

64

FATCA/IGAs

For captives domiciled outside the U.S., even if a § 953(d) election is in place, the entity will be either An FFI, if provides cash value life insurance/annuity products; or

An NFFE, if only provides casualty insurance

February 2014 revisions to FATCA regulations now permit foreign captive insurance companies with 953(d) election in place to avoid foreign treatment, provided licensed to do business in at least one state

The entity will likely have to fill out the painful new Form W-8(BEN-E) for FATCA purposes, even though W-9 required for all other purposes (§§ 6041-6049).

Financial Institutions who have to report to the IRS will do due diligence (based on account size) on the captive and its owners. NFEEs - “substantial ownership” (Regs 10%) vs. ”controlling persons” (IGA follows FATF – ordinarily 25% but falls to 10% for high risk customers)

65

Captive Insurance: IRS Guidance Plan

The IRS apparently plans to issue additional guidance on captive

insurance issues. On August 26, 2014, the IRS placed “captive

insurance issues” in its priority guidance plan for the 2014/2015 fiscal

year. (Topic No. 7 in Insurance issues)

http://www.irs.gov/file_source/pub/irs-utl/2014-2015_pgp_initial.pdf

http://www.irs.gov/file_source/pub/irs-utl/2014-

2015_pgp_2nd_quarter_update.pdf (January 29, 2015)

Stay tuned!

66

Slide Intentionally Left Blank

Robert J. Walling III, FCAS, MAAA, CERA

309.807.2320

Avoiding IRS Scrutiny in Captive Insurance

Companies –

An Actuarial Perspective

May 5, 2015

69

The Captive Trend

Why Form a Captive?

What Makes it a Captive INSURANCE COMPANY?

Funding Approaches

Outline

70

Continued Growth of Captives

Source: Business Insurance – March 17, 2014

71

Rank Domicile 2013 2012 Change (#) Change (%)

1 Bermuda 831 856 -25 -3%

2 Cayman 759 740 19 3%

3 Vermont 588 586 2 0%

4 Guernsey 344 333 11 3%

5 Utah 342 287 55 19%

6 Delaware 298 212 86 41%

7 Anguilla 295 291 4 1%

8 Nevis 276 203 73 36%

9 Barbados 264 261 3 1%

10 Luxembourg 225 238 -13 -5%

Changes by Domicile

Source: Business Insurance – March 17, 2014

72

More Risk Sophistication In Middle Market

Drives Growth of Cell, Series and Group Captives

U.S. Healthcare Changes

Increased Benefits Coverage in Captives

Maturation of Captives

Increased Expansion of Captive Programs (e.g. Small Captives and Group Captives)

Softening of U.S. Property/Casualty Market

Increased Interest in Captives (e.g. CA Workers Compensation)

Increased Use of Captives by Insurers (e.g. Agency Captives, RRG purchases)

Increased Taxation

Increased Use of Series Captives by Smaller Companies

Increased IRS Scrutiny of Risk Transfer and Risk Distribution

Key Drivers and Trends

73

Control...of Claims Costs (Risk Management/Loss Prevention)

Control...of Underwriting Expenses

Control...of Underwriting Profits

Control...of Insurance Costs (and Access to Reinsurance)

Control...of Coverage (Customizable)

Control...of Collateral and Cash Flow

Control...of Investment of Assets/Investment Income

Control...of Insured vs. Uninsured Losses

Control...of Tax Position

Why Form a Captive?

74

Primary business activity must be insurance

(a.k.a. Legitimate Business Purpose)

Needs to be operated like an insurance company

Have Sufficient Capitalization

Underwrite Coverage

Issue Policies

Provide Loss Prevention/Loss Control

Collect Premiums

Pay Claims

Maintain Appropriate Loss Reserves for Unpaid Claims

Invest Assets

Produce Financial Statements

Many of the Professional Services are Typically Out-Sourced

What makes it a Captive INSURANCE COMPANY?

75

Premiums and policies must be

Market-comparable

Risk-based

Established at arms length

Actuarial support is strongly encouraged

Initial capitalization must be adequate

4:1 (premiums to capital)

Often Minimum Capital Requirements ($100K, $250K, or $1M)

Insurance transaction

Risk Transfer

Risk Distribution

What makes it a Captive INSURANCE COMPANY?

76

Risk Transfer

Must involve shifting of risk

Must involve significant chance of a significant economic loss

Risk Distribution

Brother-Sister Model

“Unrelated Related” Model

Risk Transfer and Distribution

77

Experience Rating

Rely on insured(s) experience to the greatest extent possible.

Exposure Rating

Market Comparable Pricing

Industry Benchmarks (ISO, NCCI, etc.)

Frequency & Severity

Reinsurance Techniques (Rate on Line)

Approaches to Funding Studies

78

Experience Rating

Loss Initial Reported Incurred Losses Expected Estimated Ultimate Losses Selected

Line of Evaluation Loss Total Excess of % of Ult. Loss Dev B - F Ultimate

Coverage Policy Period Date Cost Limits $250,000 Reported Method Method Losses

(1) (2) (3) (4) (5a) (5b) (6) (7) (8) (9)

WC 12/31/12 - 12/31/13 03/29/13 1.09 213,192 0 13.92% 1,531,463 1,070,043 1,070,043

12/31/11 - 12/31/12 03/29/13 1.08 942,757 0 77.98% 1,208,900 1,149,397 1,149,397

12/31/10 - 12/31/11 03/29/13 1.07 950,826 0 88.57% 1,073,504 1,053,698 1,063,601

12/31/09 - 12/31/10 03/29/13 1.06 724,760 0 91.39% 793,009 805,458 799,233

12/31/08 - 12/31/09 03/29/13 1.05 411,026 0 92.99% 442,001 465,307 465,307

12/31/07 - 12/31/08 03/29/13 1.04 791,333 67,190 94.49% 766,399 763,952 765,175

Total 1.06 4,033,894 67,190 5,815,276 5,307,856 5,312,758

Selected Benefit

Line of Ultimate Level Loss Trend Trended

Coverage Policy Period Losses Factor Exposure Cost Factor Loss Cost Weights

(1) (2) (9) (10) (11) (12) (13) (14) (15)

WC 12/31/12 - 12/31/13 1,070,043 1.0000 946,226 1.13 1.010 1.14 0.240

12/31/11 - 12/31/12 1,149,397 1.0000 901,168 1.28 1.020 1.30 1.000

12/31/10 - 12/31/11 1,063,601 1.0015 872,932 1.22 1.030 1.26 1.000

12/31/09 - 12/31/10 799,233 1.0020 918,359 0.87 1.041 0.91 1.000

12/31/08 - 12/31/09 465,307 1.0045 766,211 0.61 1.051 0.64 0.500 *

12/31/07 - 12/31/08 765,175 1.0110 721,371 1.07 1.062 1.14 1.000

Total 5,312,758 5,126,267 1.04 1.10

79

Experience Rating

Anticipated

Indicated Credit for Indicated Indicated

Line of SIR Projected $250,000 Claims Management $250,000 Indicated Excess Total

Coverage Level Exposure Loss Cost Savings Loss Fund Loss Layer Ratio Funding Funding

(1a) (1b) (2) (3) (4) (5) (6a) (6b) (6c) (7)

WC 250,000 993,538 1.10 0.900 984,297 984,297

350,000 100 x 250 3.5% 34,450 1,018,747

500,000 250 x 250 6.0% 59,058 1,043,354

Column

(2) Exposure base: WC is Payroll (00's)

(3) Exhibit B, Total Col (14)

(4) Reflects credit for claims management savings

(5) Col (2) x Col (3) x Col (4)

(6a) Provided by MO School District

(6b) Exhibit C, Total Col (13)

(6c) Col (5) x Col (6b)

(7) Col (5) + Col (6c)

80

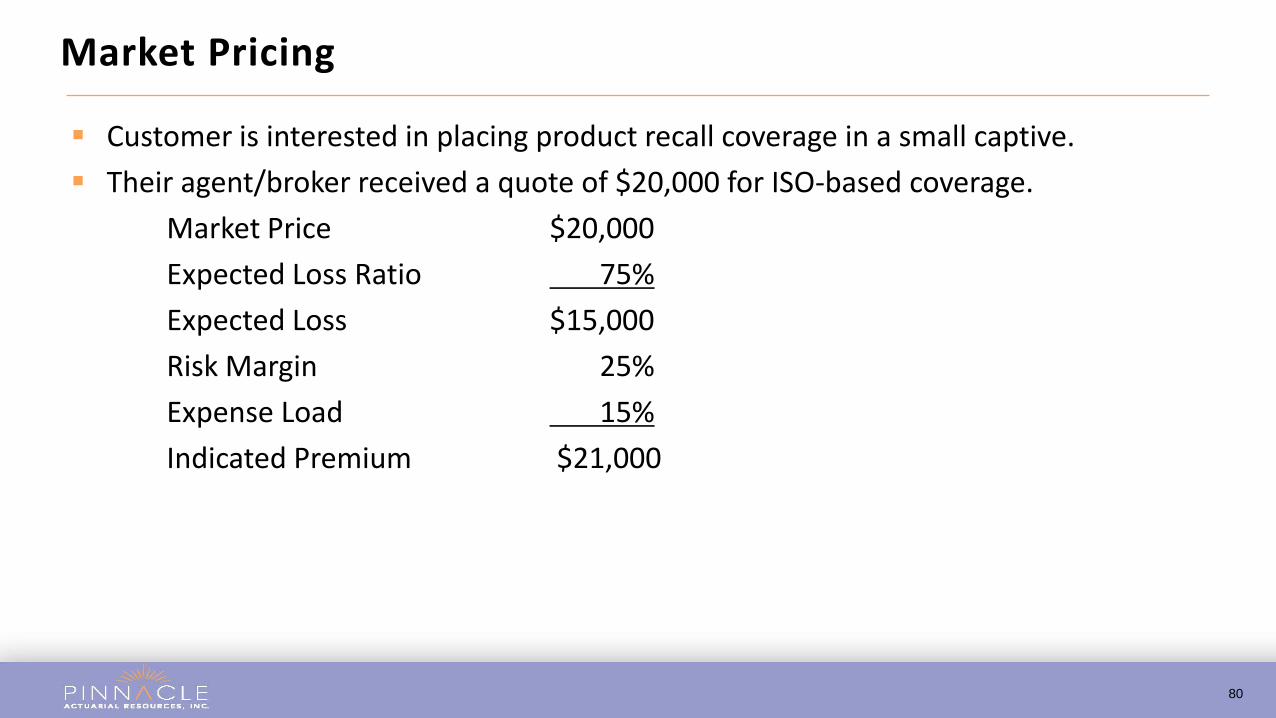

Customer is interested in placing product recall coverage in a small captive.

Their agent/broker received a quote of $20,000 for ISO-based coverage.

Market Price $20,000

Expected Loss Ratio 75%

Expected Loss $15,000

Risk Margin 25%

Expense Load 15%

Indicated Premium $21,000

Market Pricing

81

Customer is interested in placing product recall coverage in a small captive.

Company Revenues $45M Benchmark Products Loss Cost per (000) 1.40

Deductible/Increased Limits 1.50

Product Recall as a % of Products Liability 25%

Expected Loss $23,625

Risk Margin 25%

Expense Load 15%

Indicated Premium $33,075

Benchmark Pricing

82

Customer is interested in placing product recall coverage in a small captive with a $500,000 per occurrence and aggregate limit.

Expected Claims per Year 0.125

Expected Average Severity $250,000

Expected Loss $31,250

Risk Margin 25%

Expense Load 15%

Indicated Premium $43,750

Frequency & Severity

83

Customer is interested in placing product recall coverage in a small captive.

Coverage Limit $500,000

Rate on Line 6.25%

Expected Loss $31,250

Risk Margin 25%

Expense Load 15%

Indicated Premium $43,750

6.25% rate on line is equivalent to a 16 year return period.

Rate on Line