Embed Size (px)

Citation preview

Telecommunications

1

Irish consolidation: a reality check

● The second precedent since Austria: In our 400-page sector piece on the prospects for in-market mobile consolidation (see Telecommunications - Mobile consolidation: a reality check, Volume 1: Thematic thinking, dated 18 June 2013), we discussed the potential for in-market consolidation to come to the rescue of the struggling European mobile market. We concluded that a cautious stance on European mobile consolidation prospects was appropriate, not because of a zealous belief that consolidation will not happen but because we believe the Austrian precedent shows that the EC will take a remedy-heavy approach to in-market mobile consolidation. Thus consolidation prospects will be defined by where remedies are likely to be least effective. With Hutchison announcing its acquisition of O2 in Ireland, the EC is likely to once again take a tough stance on remedies.

● The EC sequel – expect Irish remedies to be far-reaching: We expect the EC to look to impose far-reaching remedies on the Irish market. The combined Hutchison-O2 business will see revenue share concentration peak above other potential consolidation opportunities in Europe, giving it a 61% share of the mobile broadband market and 50% of the postpaid segment. In addition, if we take the Austrian precedent on spectrum, the combined business may need to divest to a new entrant over 20MHz of sub-1GHz spectrum, which could be auctioned if ComReg decides to go ahead and auction the 1.5GHz band in the next couple of years. Pricing in the Irish market stands out as being neither particularly expensive nor cheap, while the immature MVNO segment would likely make MVNO obligations another EC remedy, as it was in Austria. However, Irish margins are low and Hutchison as the smallest MNO is still losing money. This arguably makes any new entrant opportunity unappealing. Hence, in the case of Ireland, we can see the arguments why remedies may not have the impact they could in stronger markets.

● What Irish consolidation means for the rest of Europe: Ireland could provide another test case, along the lines of the Austrian example. Given an immature MVNO sector and a high spectrum concentration though, this deal will also likely be accompanied by material remedies on both regulated MVNO access and substantial spectrum divestments – possibly to a new entrant. However, also like Austria, the Irish market seems to be suffering from a distressed situation, with low margins and Hutchison still losing money in the market. The calculation may therefore be that, as in Austria, the new entrant threat and MVNO threat are viewed as immaterial, due to the lack of attractiveness of the market. Our view remains that consolidation will be based on the potential effectiveness of remedies; we see Germany and France as the two best-placed EU 4-player markets to deal with those remedies.

26 June 2013

Paul Marsch Analyst +44 20 3207 7857 [email protected]

Stuart Gordon Analyst + 44 20 3207 7858 [email protected]

Barry Zeitoune Analyst +44 20 3207 7859 [email protected]

Usman Ghazi

Analyst +44 20 3207 7824 [email protected]

Wassil El Hebil Analyst +44 3207 7862 [email protected]

Laura Janssens

Marketing Analyst +44 20 3465 2639 [email protected]

Julia Thannheiser Specialist Sales +44 20 3465 2676 [email protected]

Telecommunications

Irish consolidation will result in large concentrations, especially in the mobile broadband market

Following on from the Austrian precedent, the EC has another test case, which will have far-reaching implications for European mobile consolidation. In Austria, despite the Hutchison-Orange combination having less than 25% market share, the EC competition authority decided to make an example of what it will do to protect consumers from increasing prices. This included MVNO access obligations, as well as spectrum divestments and new spectrum reserved for a new entrant.

Why the Hutchison-O2 deal in Ireland falls under the EC remit

On pp.44-45 of our note Telecommunications - Mobile consolidation: a reality check, Volume 1: Thematic thinking, we go through the EC approval process in detail.

A combined Hutchison and O2 Ireland will have over EUR5bn of worldwide turnover and over EUR250m in the EU.

In addition more than two-thirds of its EU turnover will reside in Ireland.

As such, it will qualify as a “concentration” with a “community dimension”.

In addition, the combined entity will have a 35% subscriber share, as well as a 61% share of the mobile broadband market and 50% of the postpaid market. This is significantly above the 25% threshold below which the EC does not necessarily need to review the transaction.

A significant increase in concentration

In Exhibit 1, we show the current market shares and HHI (Herfindahl–Hirschman Index) before consolidation in the EC market. This shows that while Vodafone is the market leader for non-mobile broadband subscription, followed by O2, Hutchison is the market leader in mobile broadband. Although there is a decent MVNO in Tesco, it is almost exclusively focused on the prepaid market, which makes up 59% of the Irish market.

In Exhibit 2, we show how concentration would look following the Hutchison-O2 acquisition. Excluding mobile broadband, the combination will be left with a combined 35% market share – still significantly more than Hutchison-Orange has in Austria. Secondly, at 12% penetration, mobile broadband is a relevant market in Ireland. The combined Hutchison-O2 business will have 61% market share, making it highly concentrated. In addition, the combined business will have 50% postpaid share, although this is affected by the mobile broadband market too.

So based on the EC’s substation testing, the high concentration of O2 and Hutchison in the mobile broadband market could flag up issues that the EC seeks to address through remedies.

Telecommunications

Exhibit 1: Irish mobile stats pre-consolidation

Source: Berenberg, Comreg

Subscribers (ex-mobile BB) Subscribers mobile BB Postpaid subscribers Prepaid subscribers Total revenues (€ millions)

Vodafone 1,990 154 770 1,374 173

Telefonica 1,379 149 790 738 101

Eircom 1,007 60 330 738 66

Tesco (O2 MVNO) 186 0 11 174 5

Hutchison 328 180 331 177 38

TOTAL 4,890 542 2,231 3,201 383

27.87764936

Subscribers (ex-mobile BB) Subscribers mobile BB Postpaid subscribers Prepaid subscribers Total revenues (€ millions)

Vodafone 40.7% 28.3% 34.5% 42.9% 45.2%

Telefonica 28.2% 27.4% 35.4% 23.0% 26.3%

Eircom 20.6% 11.1% 14.8% 23.0% 17.3%

Tesco (O2 MVNO) 3.8% 0.0% 0.5% 5.5% 1.2%

Hutchison 6.7% 33.2% 14.8% 5.5% 10.0%

TOTAL 100.0% 100.0% 100.0% 100.0% 100.0%

Subscribers (ex-mobile BB) Subscribers mobile BB Postpaid subscribers Prepaid subscribers Total revenues (€ millions)

Vodafone 1,656 801 1,190 1,842 2,043

Telefonica 795 751 1,253 531 692

Eircom 424 123 219 531 299

Tesco (O2 MVNO) 14 0 0 30 1

Hutchison 45 1,102 219 31 100

Total 2,935 2,777 2,881 2,965 3,135

Q1 2013 data Ireland data points

Q1 2013 data Ireland market share

Q1 2013 data Ireland HHI

Telecommunications

Exhibit 2: Irish mobile stats post-consolidation

Source: Berenberg, Comreg

Subscribers (ex-mobile BB) Subscribers mobile BB Postpaid subscribers Prepaid subscribers Total revenues (€ millions)

Vodafone 1,990 154 770 1,374 173

Eircom 1,007 60 330 738 66

Tesco (O2 MVNO) 186 0 11 174 5

Hutchison 1,707 329 1,120 915 139

TOTAL 4,890 542 2,231 3,201 383

Subscribers (ex-mobile BB) Subscribers mobile BB Postpaid subscribers Prepaid subscribers Total revenues (€ millions)

Vodafone 40.7% 28.3% 34.5% 42.9% 45.2%

Eircom 20.6% 11.1% 14.8% 23.0% 17.3%

Tesco (O2 MVNO) 3.8% 0.0% 0.5% 5.5% 1.2%

Hutchison 34.9% 60.6% 50.2% 28.6% 36.3%

TOTAL 100.0% 100.0% 100.0% 100.0% 100.0%

Subscribers (ex-mobile BB) Subscribers mobile BB Postpaid subscribers Prepaid subscribers Total revenues (€ millions)

Vodafone 1,656 801 1,190 1,842 2,043

Eircom 424 123 219 531 299

Tesco (O2 MVNO) 14 0 0 30 1

Hutchison 1,218 3,672 2,521 817 1,318

Total 3,313 4,596 3,930 3,220 3,661

Q1 2013 data Ireland HHI

Q1 2013 data Ireland data points post deal

Q1 2013 data Ireland market share

Telecommunications

2

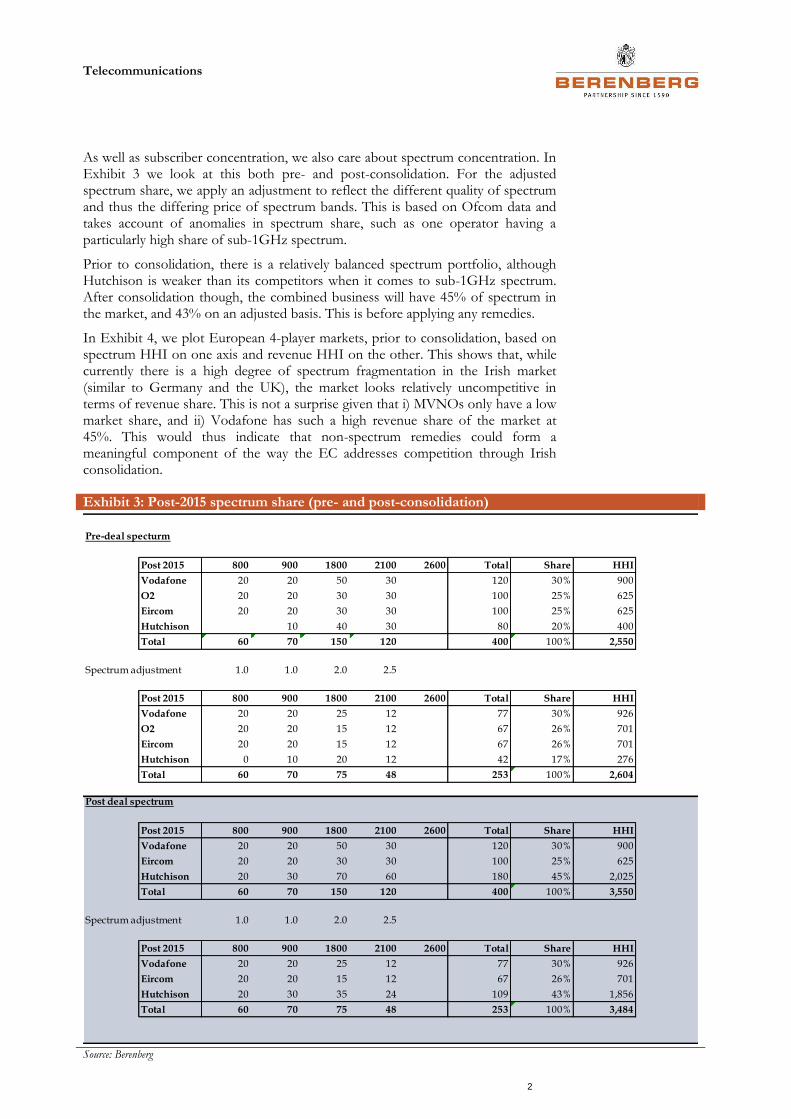

As well as subscriber concentration, we also care about spectrum concentration. In Exhibit 3 we look at this both pre- and post-consolidation. For the adjusted spectrum share, we apply an adjustment to reflect the different quality of spectrum and thus the differing price of spectrum bands. This is based on Ofcom data and takes account of anomalies in spectrum share, such as one operator having a particularly high share of sub-1GHz spectrum.

Prior to consolidation, there is a relatively balanced spectrum portfolio, although Hutchison is weaker than its competitors when it comes to sub-1GHz spectrum. After consolidation though, the combined business will have 45% of spectrum in the market, and 43% on an adjusted basis. This is before applying any remedies.

In Exhibit 4, we plot European 4-player markets, prior to consolidation, based on spectrum HHI on one axis and revenue HHI on the other. This shows that, while currently there is a high degree of spectrum fragmentation in the Irish market (similar to Germany and the UK), the market looks relatively uncompetitive in terms of revenue share. This is not a surprise given that i) MVNOs only have a low market share, and ii) Vodafone has such a high revenue share of the market at 45%. This would thus indicate that non-spectrum remedies could form a meaningful component of the way the EC addresses competition through Irish consolidation.

Exhibit 3: Post-2015 spectrum share (pre- and post-consolidation)

Source: Berenberg

Pre-deal specturm

Post 2015 800 900 1800 2100 2600 Total Share HHI

Vodafone 20 20 50 30 120 30% 900

O2 20 20 30 30 100 25% 625

Eircom 20 20 30 30 100 25% 625

Hutchison 10 40 30 80 20% 400

Total 60 70 150 120 400 100% 2,550

Spectrum adjustment 1.0 1.0 2.0 2.5

Post 2015 800 900 1800 2100 2600 Total Share HHI

Vodafone 20 20 25 12 77 30% 926

O2 20 20 15 12 67 26% 701

Eircom 20 20 15 12 67 26% 701

Hutchison 0 10 20 12 42 17% 276

Total 60 70 75 48 253 100% 2,604

Post deal spectrum

Post 2015 800 900 1800 2100 2600 Total Share HHI

Vodafone 20 20 50 30 120 30% 900

Eircom 20 20 30 30 100 25% 625

Hutchison 20 30 70 60 180 45% 2,025

Total 60 70 150 120 400 100% 3,550

Spectrum adjustment 1.0 1.0 2.0 2.5

Post 2015 800 900 1800 2100 2600 Total Share HHI

Vodafone 20 20 25 12 77 30% 926

Eircom 20 20 15 12 67 26% 701

Hutchison 20 30 35 24 109 43% 1,856

Total 60 70 75 48 253 100% 3,484

Telecommunications

3

Exhibit 4: Pre-consolidation, Ireland has a low adjusted spectrum HHI, but a high service revenue HHI

Source: Berenberg

In Exhibit 5, we show the same chart but assuming the most likely consolidation in each EC 4-player market. For the Irish market this comes with some very interesting conclusions.

Firstly, this chart shows the EC precedent of what we have seen with the Austrian deal. As a result of the 2.6GHz spectrum to be given to a new operator, and the 800MHz spectrum reserved for the same new entrant, spectrum remedies will see the adjusted spectrum HHI fall from 3,297 to 2,904 – should these remedies be successfully implemented.

With regard to Ireland, the resulting spectrum concentration of 3,484 puts it marginally above the average, but also comfortably above the concentration seen in Austria. With a 43% adjusted spectrum share, the combined Hutchison-O2 business will likely face Austrian-style spectrum divestments.

However, what really stands out in the Irish market is the service revenue HHI, which after consolidation would be the highest of all the potential consolidation opportunities in Europe. Clearly, remedies will not stop at spectrum as this position would leave market revenues particularly highly concentrated.

NDL

Swe

FR

DK

ES

UK

IT

GE

Avg.

IL

2200

2400

2600

2800

3000

3200

3400

3600

2400 2900 3400 3900

Se

rvic

e R

ev

en

ue

HH

I

Adjusted Spectrum HHI

Adjusted spectrum concentration vs market concentration

AU

Telecommunications

4

Exhibit 5: Post-consolidation, Ireland has the highest service revenue HHI

Source: Berenberg

The remedies the high concentration indicates

Following the above work on concentration, we would expect remedies in Ireland to take three forms. Firstly, the spectrum share will be addressed, possibly by requiring spectrum divestments to a new entrant. Secondly, given the immature MVNO market, access obligations will form another meaningful component. Finally, the high concentration in the mobile broadband segment could in our view mean divestments if the EC’s substitution tests capture it.

Spectrum: If we take the Austrian precedent, to get to an adjusted spectrum HHI of 2,904, the Irish consolidated entity would have to divest just over 20MHz of premium sub-1GHz spectrum to a new entrant. Outside spectrum auctions, Comreg has indicated little in terms of new auctions to come. 2.6GHz spectrum is currently being used by UPC and is unlikely to be auctioned until 2016, while the 700MHz band needs to be harmonised, which could be five years away. Comreg is however likely to launch an auction consultation for the 1500MHz band next year, and this could be used as a medium for reallocating any spectrum to a new entrant.

MVNO access: The O2/Tesco JV MVNO will likely have its share protected. Given limited MVNO share, the EC may try and boost this.

Divestments: Although not formally required by the EC, Hutchison did divest its Yesss! brand as part of its Austrian consolidation. The combined O2 and Hutchison in Ireland will have a 61% market share in mobile broadband, and a 50% market share in postpaid; thus we would not be surprised to see divestments in Ireland.

NDLSwe

FR

DK

ES

UK

IT

GE

Avg.

AU

AU post remedies

IL

2200

2400

2600

2800

3000

3200

3400

3600

2400 2900 3400 3900

Se

rvic

e R

ev

en

ue

HH

I

Adjusted Spectrum HHI

Adjusted spectrum concentration vs market concentration (with consol.)

Telecommunications

5

How effective will remedies be in Ireland?

When looking to score markets on consolidation potential, we did it according to how effective we thought remedies might be. This was based on the following criteria.

Pricing levels/bundles: Put simply, we assume that where prices are already low, consolidation, even with remedies, may stand a better chance of resulting in market repair as low price levels will deter new entrants.

MVNO presence: Where MVNOs are already a powerful force in the market, there will be less scope for regulators to use MVNO remedies to counterbalance consolidation. Where MVNOs with strong distribution channels are not already present, the introduction of MVNOs could present a good counterbalance to consolidation.

Herfindahl-Hirschman Index (HHI) (pre- and post-MVNOs): Where HHI is low, the market would appear to already be very competitive. Hence the consolidation of two players may be more acceptable, and may leave little scope for new entrants to make an impact, or for the introduction of more consumer-friendly MVNO privileges.

Extent of network-sharing: Where network-sharing is prevalent, there should be less scope for regulators to enforce access to shared infrastructure as a remedy. However, too much network-sharing, or arrangements that are too complex, could act to prevent operators pursuing full consolidation. Also, network-sharing without consolidation at the point of sale to the customers (to remove actual competitive tension in the market) should serve simply to allow operators to extract efficiencies. These will then just be passed onto consumers in the form of lower prices, sustaining competitive tension. This can be particularly important where smaller operators share infrastructure (as in Sweden and Denmark) to gain enough scale to compete with the incumbent.

Strength of competition in distribution: Where the customer has lots of choice at the point of sale, there should be less scope for remedies to make a difference. The presence of strong reseller/retail distribution channels (such as Carphone Warehouse in the UK) should add to the impression that the consumer already has a broad choice of alternatives. Likewise, if the consolidation of operators can also reduce the level of competition at the point of sale without being offset by regulatory remedies, this should be good for market repair.

Spectrum balance among competitors: Where there is an equal distribution of spectrum among competitors (post-consolidation), there is less scope for regulators to enforce spectrum reallocation remedies. Likewise, where there is a significant imbalance between operators’ share of subscribers and spectrum, the scope exists for one or more residual competitors to price disruptively, possibly irrespective of consolidation. We ask whether consolidation could remove potentially disruptive excess capacity from the market, and whether spectrum divestments could create such an opportunity for a new entrant (eg for MVNOs’ ongoing own-network, or for wireline competitors looking to enter mobile).

The opportunity cost of no consolidation: Maybe consolidation will not result in a more rational market, but perhaps it could result in a less disruptive one – it is all relative. Can we identify which markets have a

Telecommunications

6

high opportunity cost of not pursuing consolidation? Put another way, there may be markets where consolidation is worth pursuing, even with significant remedies, simply because the current competitive environment is so irrational that any level of improvement would be welcome. We compare recent mobile market service revenue growth trends with our medium-term expectations for growth in order to assess which markets face a high opportunity cost from not seeing consolidation.

We have already addressed many of these factors in the previous section. We use this section to look at pricing, MVNOs, network sharing, distribution and the opportunity cost of not seeing consolidation, to look at the prospects for whether remedies will be effective.

Pricing

When we look at pricing in the Irish market, it appears close to the average for a mid-end postpaid subscriber, and at the high end for the important prepaid market.

Exhibit 6: On postpaid medium user pricing, Ireland is close to the average

Source: Berenberg, OECD

Exhibit 7: High-end pricing is closely bunched

Source: Berenberg

All rates are in € O2 Vodafone

emobile

(Eircom) 3 Tesco

€5 usage

Package name O2 open RED Unlimited Ultimate flex na

Voice calls (in min) unlimited unlimited unlimited unlimited unlimited

Data Mb pcm 1GB 1GB 15GB unlimited unlimited

SMS umlimited umlimited umlimited umlimited umlimited

Period (months) 1 1 18 1 na

Monthly Flat rate tariff (base) 40.0 40.0 64.0 39.8 na

Monthly Flat rate tariff (promotion) 40.0 40.0 32.0 39.8 na

Telecommunications

7

Exhibit 8: Prepaid users, who represent 60% of the Irish market, show it to be expensive

Source: Berenberg, OECD

Exhibit 9: Unlimited voice/SMS packages are expensive

Source: Berenberg

In our view, favourable MVNO contract terms, imposed by the regulator, could disrupt the pricing environment in both the prepaid market and the high value market. In the low value segment, Ireland is 0.9% more expensive than the benchmarked country average. In the mid-value market, Ireland is 16.2% cheaper than the European benchmark average.

MVNO presence

The MVNO market in Ireland is immature. Back in 2010, Ofcom noted that the MVNO market in Ireland was non-existent. However there are now six MVNO agreements in Ireland, of which two are owned by the MNOs. Tesco is the largest MVNO in the market, and is a 50:50 JV between O2 UK and Tesco PLC.

10.0

20.0

30.0

40.0

50.0

60.0

70.0

FR AU UK DK Avg. Swe GE IT IL ES NDL

€p

cm

Typical unlimited (voice & SMS) SIM-only big bundles

Telecommunications

8

Who could benefit from an imposed MVNO offer?

In terms of fixed broadband subscribers’ market shares, Eircom has 40% share, followed by UPC (28.1%) and Vodafone (17.1%). Imagine and Digiweb have 3.7% and 2.5% respectively.

Vodafone, which is the second-largest mobile operator, is also the key alternative DSL operator in Ireland.

Neither Digiweb (unbundled operator) nor UPC (main cable operator) has a mobile offer.

In our view, UPC may be best placed to benefit from an MVNO agreement in the Irish market. However, it is interesting that as an MVNO in Austria, UPC has done little thus far to disrupt the market.

Network sharing

O2 and Eircom have a network-sharing agreement signed in 2011; this includes cooperation on site equipment, power supply, technology and transmission sharing. Where possible, existing sites of both operators will be consolidated and new sites will be jointly built. The sharing arrangement does not include spectrum, however.

In addition, Vodafone and Hutchison have a network-sharing agreement, based on 2,000 sites – although both companies continue to run their radio equipment and spectrum independently.

This does provide a complicating factor to the agreement between Hutchison and O2, although this has likely been thought through as part of the current agreement.

Opportunity cost

This is where consolidation looks particularly appealing. O2 makes only a 20% margin in the Irish market, Eircom made a 7% mobile margin last quarter, while Hutchison is still losing money in Ireland. Margins have been affected by competition as well as the very difficult macroeconomic backdrop. This is likely to be a key driver to consolidation, and the low margins in the market will likely deter any new entrant opportunity.

Telecommunications

9

Contacts: Investment Banking

Equity Research E-mail: [email protected]; Internet www.berenberg.de

BANKS ECONOMICS MID-CAP GENERAL

Nick Anderson +44 (0) 20 3207 7838 Dr. Holger Schmieding +44 (0) 20 3207 7889 Gunnar Cohrs +44 (0) 20 3207 7894

James Chappell +44 (0) 20 3207 7844 Dr. Christian Schulz +44 (0) 20 3207 7878 Bjoern Lippe +44 (0) 20 3207 7845

Andrew Lowe +44 (0) 20 3465 2743 Robert Wood +44 (0) 20 3207 7822 Anna Patrice +44 (0) 20 3207 7863

Eoin Mullany +44 (0) 20 3207 7854 Stanislaus von Thurn und Taxis +44 (0) 20 3465 2631

Eleni Papoula +44 (0) 20 3465 2741 FOOD MANUFACTURING

Michelle Wilson +44 (0) 20 3465 2663 Fintan Ryan +44 (0) 20 3465 2748 OIL & GAS

Andrew Steele +44 (0) 20 3207 7926 Asad Farid +44 (0) 20 3207 7932

BEVERAGES James Targett +44 (0) 20 3207 7873 Jaideep Pandya +44 (0) 20 3207 7890

Philip Morrisey +44 (0) 20 3207 7892

Josh Puddle +44 (0) 20 3207 7881 GENERAL RETAIL & LUXURY GOODS REAL ESTATE

Bassel Choughari +44 (0) 20 3465 2675 Kai Klose +44 (0) 20 3207 7888

BUSINESS SERVICES John Guy +44 (0) 20 3465 2674 Estelle Weingrod +44 (0) 20 3207 7931

William Foggon +44 (0) 20 3207 7882

Simon Mezzanotte +44 (0) 20 3207 7917 HEALTHCARE TECHNOLOGY

Arash Roshan Zamir +44 (0) 20 3465 2636 Scott Bardo +44 (0) 20 3207 7869 Adnaan Ahmad +44 (0) 20 3207 7851

Konrad Zomer +44 (0) 20 3207 7920 Alistair Campbell +44 (0) 20 3207 7876 Sebastian Grabert +44 (0) 20 3207 7834

Charles Cooper +44 (0) 20 3465 2637 Daud Khan +44 (0) 20 3465 2638

CAPITAL GOODS Louise Hinds +44 (0) 20 3465 2747 Ali Khwaja +44 (0) 20 3207 7852

Frederik Bitter +44 (0) 20 3207 7916 Adrian Howd +44 (0) 20 3207 7874 Tammy Qiu +44 (0) 20 3465 2673

Benjamin Glaeser +44 (0) 20 3207 7918 Tom Jones +44 (0) 20 3207 7877

William Mackie +44 (0) 20 3207 7837 TELECOMMUNICATIONS

Margaret Paxton +44 (0) 20 3207 7934 HOUSEHOLD & PERSONAL CARE Wassil El Hebil +44 (0) 20 3207 7862

Alexander Virgo +44 (0) 20 3207 7856 Jade Barkett +44 (0) 20 3207 7937 Usman Ghazi +44 (0) 20 3207 7824

Felix Wienen +44 (0) 20 3207 7915 Seth Peterson +44 (0) 20 3207 7891 Stuart Gordon +44 (0) 20 3207 7858

Laura Janssens +44 (0) 20 3465 2639

CHEMICALS INSURANCE Paul Marsch +44 (0) 20 3207 7857

John Philipp Klein +44 (0) 20 3207 7930 Tom Carstairs +44 (0) 20 3207 7823 Barry Zeitoune +44 (0) 20 3207 7859

Evgenia Molotova +44 (0) 20 3465 2664 Peter Eliot +44 (0) 20 3207 7880

Jaideep Pandya +44 (0) 20 3207 7890 Kai Mueller +44 (0) 20 3465 2681 TOBACCO

Matthew Preston +44 (0) 20 3207 7913 Erik Bloomquist +44 (0) 20 3207 7870

CONSTRUCTION Sami Taipalus +44 (0) 20 3207 7866 Kate Kalashnikova +44 (0) 20 3465 2665

Chris Moore +44 (0) 20 3465 2737

Robert Muir +44 (0) 20 3207 7860 MEDIA UTILITIES

Michael Watts +44 (0) 20 3207 7928 Robert Berg +44 (0) 20 3465 2680 Robert Chantry +44 (0) 20 3207 7861

Emma Coulby +44 (0) 20 3207 7821 Andrew Fisher +44 (0) 20 3207 7937

DIVERSIFIED FINANCIALS Laura Janssens +44 (0) 20 3465 2639 Oliver Salvesen +44 (0) 20 3207 7818

Pras Jeyanandhan +44 (0) 20 3207 7899 Sarah Simon +44 (0) 20 3207 7830 Lawson Steele +44 (0) 20 3207 7887

Sales E-mail: [email protected]; Internet www.berenberg.de

Specialist Sales Sales Sales Trading

BANKS LONDON HAMBURG

Iro Papadopoulou +44 (0) 20 3207 7924 John von Berenberg-Consbruch +44 (0) 20 3207 7805 Paul Dontenwill +49 (0) 40 350 60 563

Matt Chawner +44 (0) 20 3207 7847 Alexander Heinz +49 (0) 40 350 60 359

CONSUMER Toby Flaux +44 (0) 20 3465 2745 Gregor Labahn +49 (0) 40 350 60 571

Rupert Trotter +44 (0) 20 3207 7815 Karl Hancock +44 (0) 20 3207 7803 Chris McKeand +49 (0) 40 350 60 798

Sean Heath +44 (0) 20 3465 2742 Fin Schaffer +49 (0) 40 350 60 596

INSURANCE David Hogg +44 (0) 20 3465 2628 Lars Schwartau +49 (0) 40 350 60 450

Trevor Moss +44 (0) 20 3207 7893 Zubin Hubner +44 (0) 20 3207 7885 Marvin Schweden +49 (0) 40 350 60 576

Ben Hutton +44 (0) 20 3207 7804 Tim Storm +49 (0) 40 350 60 415

HEALTHCARE James Matthews +44 (0) 20 3207 7807 Philipp Wiechmann +49 (0) 40 350 60 346

Frazer Hall +44 (0) 20 3207 7875 David Mortlock +44 (0) 20 3207 7850

Peter Nichols +44 (0) 20 3207 7810 LONDON

INDUSTRIALS Richard Payman +44 (0) 20 3207 7825 Mike Berry +44 (0) 20 3465 2755

Chris Armstrong +44 (0) 20 3207 7809 George Smibert +44 (0) 20 3207 7911 Stewart Cook +44 (0) 20 3465 2752

Kaj Alftan +44 (0) 20 3207 7879 Anita Surana +44 (0) 20 3207 7855 Simon Messman +44 (0) 20 3465 2754

Paul Walker +44 (0) 20 3465 2632 Stephen O'Donohoe +44 (0) 20 3465 2753

MEDIA

Julia Thannheiser +44 (0) 20 3465 2676 PARIS PARIS

Christophe Choquart +33 (0) 1 5844 9508 Sylvain Granjoux +33 (0) 1 5844 9509

TECHNOLOGY Dalila Farigoule +33 (0) 1 5844 9510

Jean Beaubois +44 (0) 20 3207 7835 Clémence La Clavière-Peyraud +33 (0) 1 5844 9521 SOVEREIGN WEALTH FUNDS

Olivier Thibert +33 (0) 1 5844 9512 Max von Doetinchem +44 (0) 20 3207 7826

TELECOMMUNICATIONS

Julia Thannheiser +44 (0) 20 3465 2676 ZURICH CORPORATE ACCESS

Stephan Hofer +41 (0) 44 283 2029 Patricia Nehring +44 (0) 20 3207 7811

UTILITIES Carsten Kinder +41 (0) 44 283 2024

Benita Barretto +44 (0) 20 3207 7829 Gianni Lavigna +41 (0) 44 283 2038 EVENTS

Benjamin Stillfried +41 (0) 44 283 2033 Natalie Meech +44 (0) 20 3207 7831

Sales Charlotte Kilby +44 (0) 20 3207 7832

FRANKFURT BENELUX Charlotte Reeves +44 (0) 20 3465 2671

Michael Brauburger +49 (0) 69 91 30 90 741 Miel Bakker (London) +44 (0) 20 3207 7808 Hannah Whitehead +44 (0) 20 3207 7922

Nina Buechs +49 (0) 69 91 30 90 735 Susette Mantzel (Hamburg) +49 (0) 40 350 60 694

André Grosskurth +49 (0) 69 91 30 90 734 Alexander Wace (London) +44 (0) 20 3465 2670 CRM

Boris Koegel +49 (0) 69 91 30 90 740 Greg Swallow +44 (0) 20 3207 7833

Joerg Wenzel +49 (0) 69 91 30 90 743 SCANDINAVIA Laura Cooper +44 (0) 20 3207 7806

Ronald Bernette (London) +44 (0) 20 3207 7828

Marco Weiss (Hamburg) +49 (0) 40 350 60 719

US Sales E-mail: [email protected]

BERENBERG CAPITAL MARKETS LLC

Member FINRA & SIPC

Andrew Holder +1 (617) 292 8222 Burr Clark +1 (617) 292 8282 Kieran O'Sullivan +1 (617) 292 8292

Colin Andrade +1 (617) 292 8230 Julie Doherty +1 (617) 292 8228 Emily Mouret +1 (646) 445 7204

Cathal Carroll +1 (646) 445 7206 Kelleigh Faldi +1 (617) 292 8288 Jonathan Saxon +1 (646) 445 7202

Telecommunications

10

Disclaimer

Please note:

For disclosures, historical price targets and rating changes pertaining to the companies included in this publication as well as analyst certifications, please visit the disclosure listing page of

Joh.Berenberg, Gossler & Co. KG (hereinafter referred to as “the Bank”) on the website at:

or refer to our research comments and reports which are available for download (password required) at:

https://www.berenberg.de/cgi-bin/crm.cgi?rm=login&lang=englisch

or on demand ([email protected]).

Please note that the disclosures, historical price targets and rating changes reflect the status of the most recently published comments or reports on the companies.

Valuation basis/rating key

The recommendations for companies analysed by the Bank’s equity research department are either made on an absolute basis (“absolute rating system”) or relative to the sector (“relative rating system“), which is clearly stated in the financial analysis. For both absolute and relative rating system, the three-step rating key “Buy”, “Hold” and “Sell” is applied. For a detailed explanation of our rating system, please refer to our website at

http://www.berenberg.de/research.html?&L=1

NB: During periods of high market, sector or stock volatility, or in special situations, the rating system criteria as described on our website may be breached temporarily.

Competent supervisory authority

Bundesanstalt für Finanzdienstleistungsaufsicht - BaFin - (Federal Financial Supervisory Authority),

Graurheindorfer Straße 108, 53117 Bonn and Lurgiallee 12, 60439 Frankfurt am Main, Germany

General investment-related disclosures

The Bank has made every effort to carefully research all information contained in this document. The information on which the research note is based has been obtained from sources which the Bank believes to be reliable such as, for example, Thomson Reuters, Bloomberg and the relevant specialised press as well as the company which is the subject of this research note. Only that part of the document is made available to the issuer, who is the subject of this analysis, which is necessary to properly reconcile with the facts. Should this result in considerable changes, a reference is made in the research note. Opinions expressed in this research note are the Bank’s current opinions as of the issuing date indicated on this document. The companies analysed by the Bank are divided into two groups: those under “full coverage” (regular updates provided); and those under “screening coverage” (updates provided as and when required at irregular intervals). The functional job title of the person/s responsible for the recommendations contained in this report is “Equity Research Analyst”, unless otherwise stated on the cover.

The following internet links provide further remarks on the Bank’s financial analyses:

http://www.berenberg.de/research.html?&L=1&no_cache=1

Telecommunications

11

Legal disclaimer

This document has been prepared by Joh. Berenberg, Gossler & Co. KG. This document does not claim completeness regarding all the information on the stocks, stock markets or developments referred to in it. On no account should the document be regarded as a substitute for the recipient procuring information for himself/herself or exercising his/her own judgements. The document has been produced for information purposes for institutional clients or market professionals. Private customers, into whose possession this document comes, should discuss possible investment decisions with their customer service officer as differing views and opinions may exist with regard to the stocks referred to in this document. This document is not a solicitation or an offer to buy or sell the mentioned stock. The document may include certain descriptions, statements, estimates, and conclusions underlining potential market and company developments. These reflect assumptions, which may turn out to be incorrect. The Bank and/or its employees accept no liability whatsoever for any direct or consequential loss or damages of any kind arising out of the use of this document or any part of its content. The Bank and/or its employees may hold, buy or sell positions in any securities mentioned in this document, derivatives thereon or related financial products. The Bank and/or its employees may underwrite issues for any securities mentioned in this document, derivatives thereon or related financial products or seek to perform capital market or underwriting services.

Remarks regarding foreign investors The preparation of this document is subject to regulation by German law. The distribution of this document in other jurisdictions may be restricted by law, and persons into whose possession this document comes should inform themselves about, and observe, any such restrictions.

United Kingdom This document is meant exclusively for institutional investors and market professionals, but not for private customers. It is not for distribution to or the use of private investors or private customers.

United States of America This document has been prepared exclusively by Joh. Berenberg, Gossler & Co. KG. Although Berenberg Capital Markets LLC, an affiliate of the Bank and registered US broker-dealer, distributes this document to certain customers, Berenberg Capital Markets LLC does not provide input into its contents, nor does this document constitute research of Berenberg Capital Markets LLC. In addition, this document is meant exclusively for institutional investors and market professionals, but not for private customers. It is not for distribution to or the use of private investors or private customers. This document is classified as objective for the purposes of FINRA rules. Please contact Berenberg Capital Markets LLC (+1 617.292.8200), if you require additional information.

Copyright The Bank reserves all the rights in this document. No part of the document or its content may be rewritten, copied, photocopied or duplicated in any form by any means or redistributed without the Bank’s prior written consent. © May 2013 Joh. Berenberg, Gossler & Co. KG