Embed Size (px)

Citation preview

PULSE REPORT

IRI Pulse Report Confectionery

Welcome to the Pulse H1 2015 edition for confectionery. Please do

not hesitate to contact us if you have any questions or comments at

H1 2015

IRIworldwide.com

PULSE REPORT

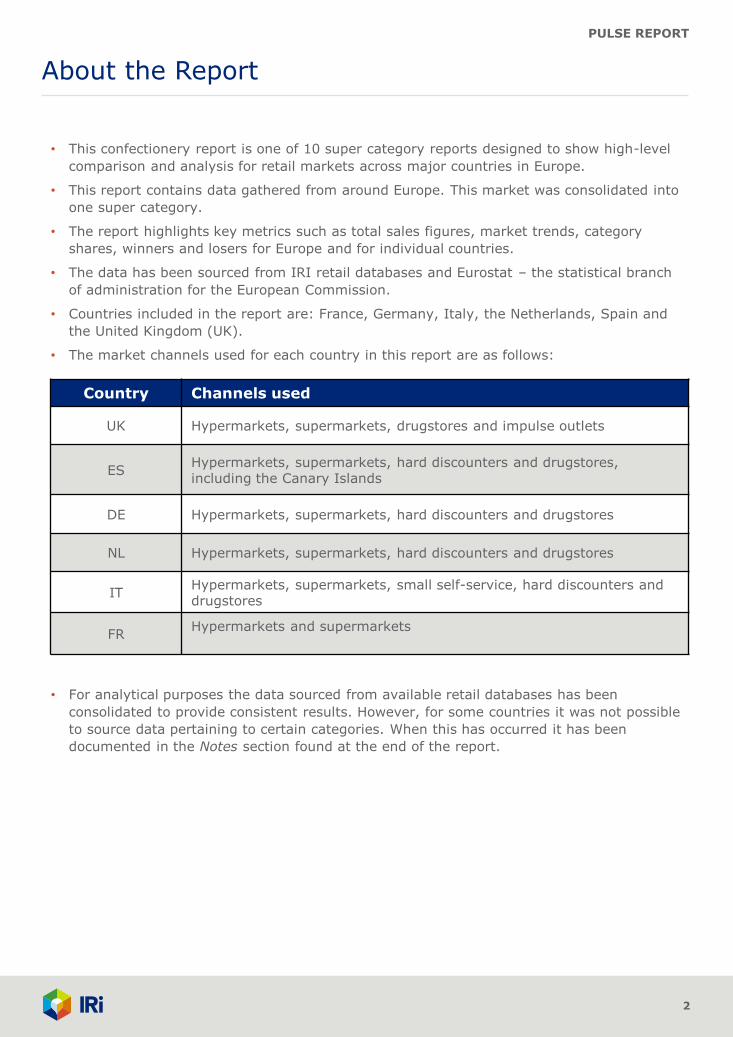

About the Report

2

• This confectionery report is one of 10 super category reports designed to show high-level

comparison and analysis for retail markets across major countries in Europe.

• This report contains data gathered from around Europe. This market was consolidated into

one super category.

• The report highlights key metrics such as total sales figures, market trends, category

shares, winners and losers for Europe and for individual countries.

• The data has been sourced from IRI retail databases and Eurostat – the statistical branch

of administration for the European Commission.

• Countries included in the report are: France, Germany, Italy, the Netherlands, Spain and

the United Kingdom (UK).

• The market channels used for each country in this report are as follows:

Country Channels used

UK Hypermarkets, supermarkets, drugstores and impulse outlets

ES Hypermarkets, supermarkets, hard discounters and drugstores, including the Canary Islands

DE Hypermarkets, supermarkets, hard discounters and drugstores

NL Hypermarkets, supermarkets, hard discounters and drugstores

IT Hypermarkets, supermarkets, small self-service, hard discounters and drugstores

FR Hypermarkets and supermarkets

• For analytical purposes the data sourced from available retail databases has been

consolidated to provide consistent results. However, for some countries it was not possible

to source data pertaining to certain categories. When this has occurred it has been

documented in the Notes section found at the end of the report.

PULSE REPORT

On the Radar

3

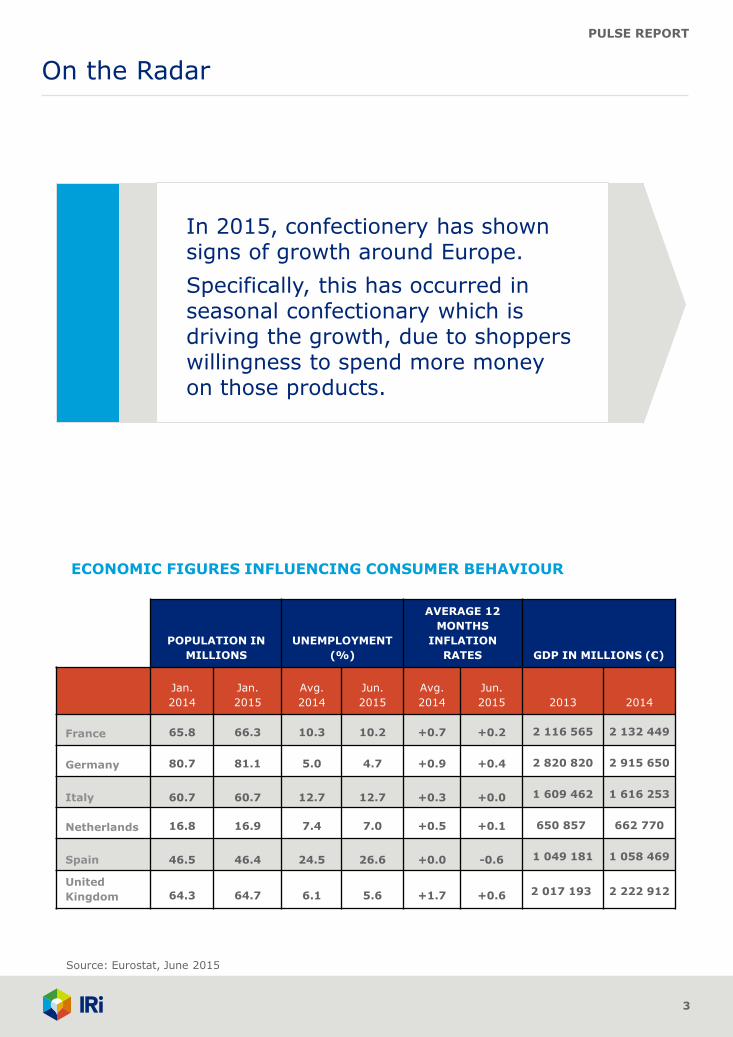

ECONOMIC FIGURES INFLUENCING CONSUMER BEHAVIOUR

In 2015, confectionery has shown signs of growth around Europe.

Specifically, this has occurred in seasonal confectionary which is driving the growth, due to shoppers willingness to spend more money on those products.

POPULATION IN

MILLIONS

UNEMPLOYMENT

(%)

AVERAGE 12

MONTHS

INFLATION

RATES GDP IN MILLIONS (€)

Jan.

2014

Jan.

2015

Avg.

2014

Jun.

2015

Avg.

2014

Jun.

2015 2013 2014

France 65.8 66.3 10.3 10.2 +0.7 +0.2 2 116 565 2 132 449

Germany 80.7 81.1 5.0 4.7 +0.9 +0.4 2 820 820 2 915 650

Italy 60.7 60.7 12.7 12.7 +0.3 +0.0 1 609 462 1 616 253

Netherlands 16.8 16.9 7.4 7.0 +0.5 +0.1 650 857 662 770

Spain 46.5 46.4 24.5 26.6 +0.0 -0.6 1 049 181 1 058 469

United

Kingdom 64.3 64.7 6.1 5.6 +1.7 +0.6 2 017 193 2 222 912

Source: Eurostat, June 2015

PULSE REPORT

1 655 1 704 1 394

1 937 1 744 1 640

257 212

181

466 273 215

218 211

187

233 223

214 490

593

297

602 595

493

1 566 1 553 1 537

2 467

1 652 1 586

806 930

680

1 439

1 039

705

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

30-mar-14 29-jun-14 28-sep-14 28-dic-14 29-mar-15 28-jun-15

Eu

ro

s, in

millio

ns

Period Ending

France

Germany

Italy

Netherlands

Spain

UK

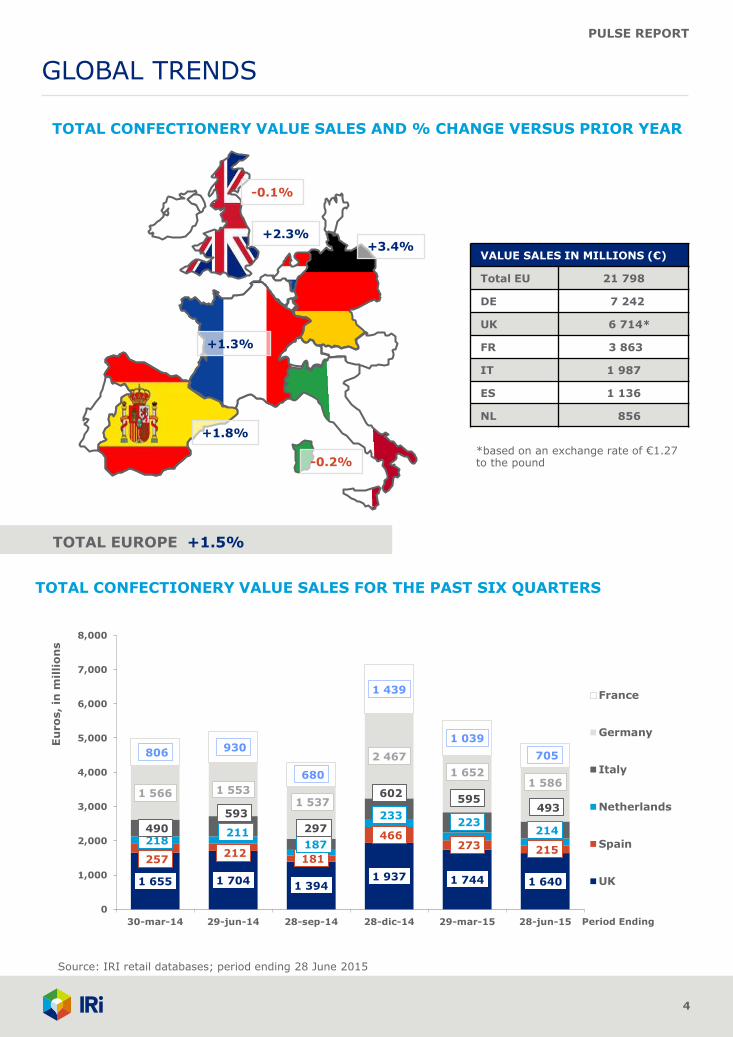

GLOBAL TRENDS

4

-0.2%

+3.4%

-0.1%

TOTAL EUROPE +1.5%

VALUE SALES IN MILLIONS (€)

Total EU 21 798

DE 7 242

UK 6 714*

FR 3 863

IT 1 987

ES 1 136

NL 856

TOTAL CONFECTIONERY VALUE SALES AND % CHANGE VERSUS PRIOR YEAR

*based on an exchange rate of €1.27 to the pound

+1.8%

+1.3%

+2.3%

TOTAL CONFECTIONERY VALUE SALES FOR THE PAST SIX QUARTERS

Source: IRI retail databases; period ending 28 June 2015

PULSE REPORT

19 015

2 783

1.5 1.6

Non Seasonal Confectionery Seasonal Confectionery

Eu

ros,

in m

illio

ns

Euro Sales % € vs. YA

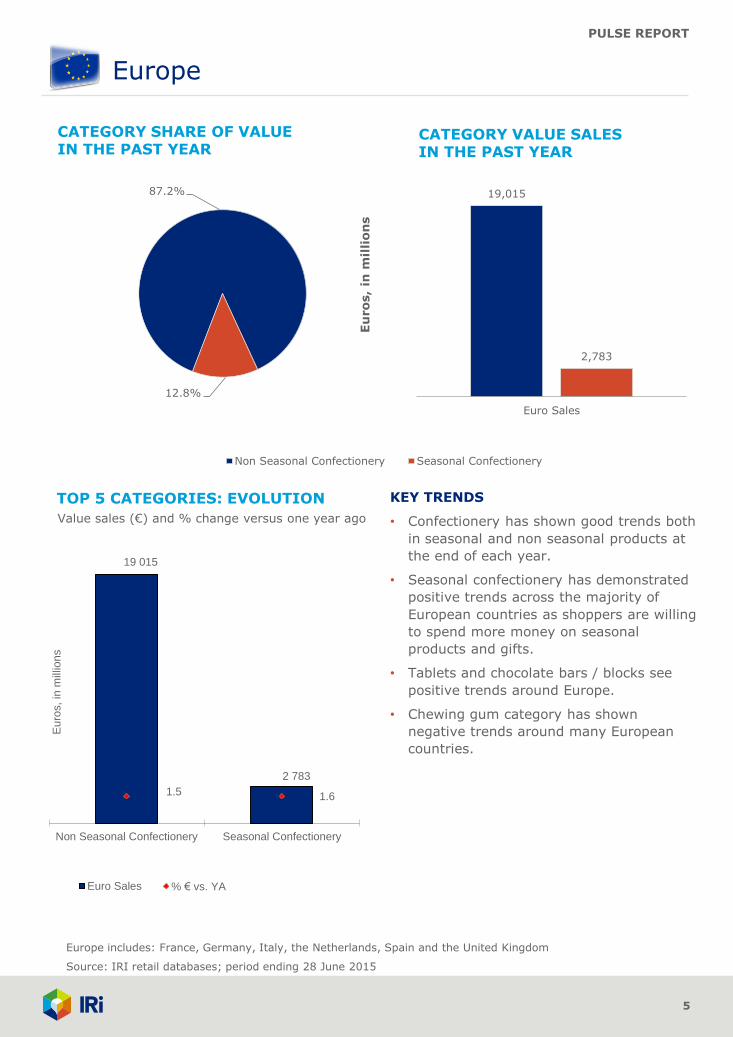

87.2%

12.8%

Non Seasonal Confectionery Seasonal Confectionery

Europe

5

19,015

2,783

Euro Sales

Eu

ros,

in m

illi

on

s

CATEGORY VALUE SALES IN THE PAST YEAR

CATEGORY SHARE OF VALUE IN THE PAST YEAR

Europe includes: France, Germany, Italy, the Netherlands, Spain and the United Kingdom

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change versus one year ago

Source: IRI retail databases; period ending 28 June 2015

KEY TRENDS

• Confectionery has shown good trends both

in seasonal and non seasonal products at

the end of each year.

• Seasonal confectionery has demonstrated

positive trends across the majority of

European countries as shoppers are willing

to spend more money on seasonal

products and gifts.

• Tablets and chocolate bars / blocks see

positive trends around Europe.

• Chewing gum category has shown

negative trends around many European

countries.

PULSE REPORT

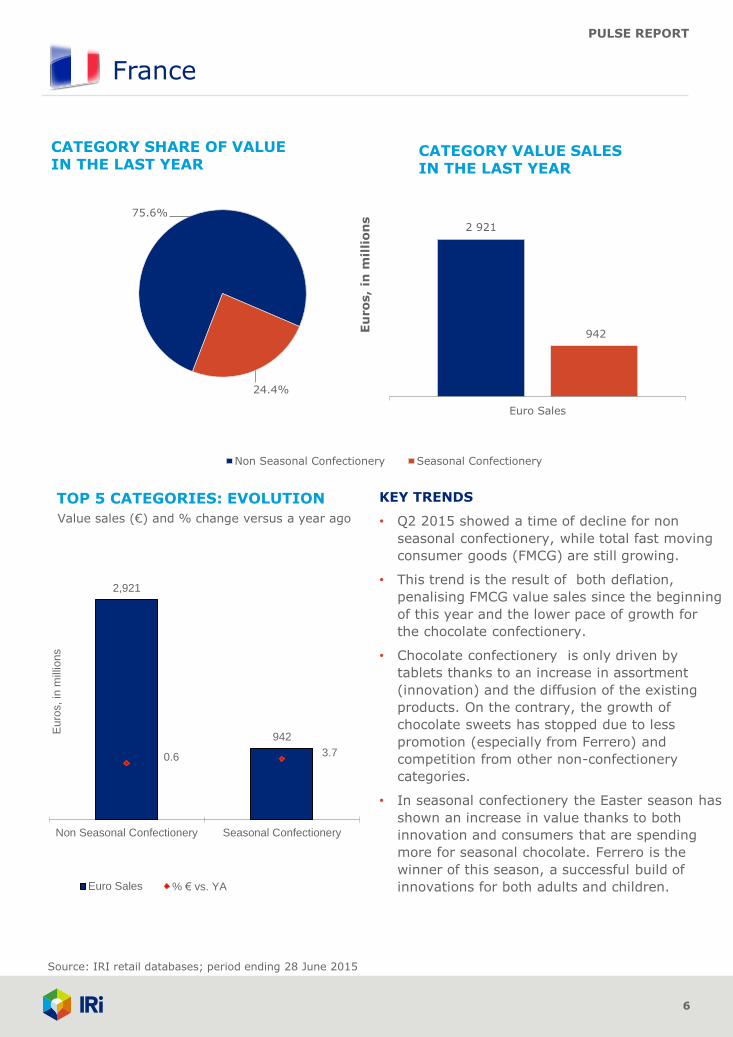

2,921

942

0.6 3.7

Non Seasonal Confectionery Seasonal Confectionery

Eu

ros,

in m

illio

ns

Euro Sales % € vs. YA

75.6%

24.4%

Non Seasonal Confectionery Seasonal Confectionery

France

6

KEY TRENDS

• Q2 2015 showed a time of decline for non

seasonal confectionery, while total fast moving

consumer goods (FMCG) are still growing.

• This trend is the result of both deflation,

penalising FMCG value sales since the beginning

of this year and the lower pace of growth for

the chocolate confectionery.

• Chocolate confectionery is only driven by

tablets thanks to an increase in assortment

(innovation) and the diffusion of the existing

products. On the contrary, the growth of

chocolate sweets has stopped due to less

promotion (especially from Ferrero) and

competition from other non-confectionery

categories.

• In seasonal confectionery the Easter season has

shown an increase in value thanks to both

innovation and consumers that are spending

more for seasonal chocolate. Ferrero is the

winner of this season, a successful build of

innovations for both adults and children.

2 921

942

Euro Sales

Eu

ros,

in m

illi

on

s

CATEGORY VALUE SALES IN THE LAST YEAR

CATEGORY SHARE OF VALUE IN THE LAST YEAR

Source: IRI retail databases; period ending 28 June 2015

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change versus a year ago

PULSE REPORT

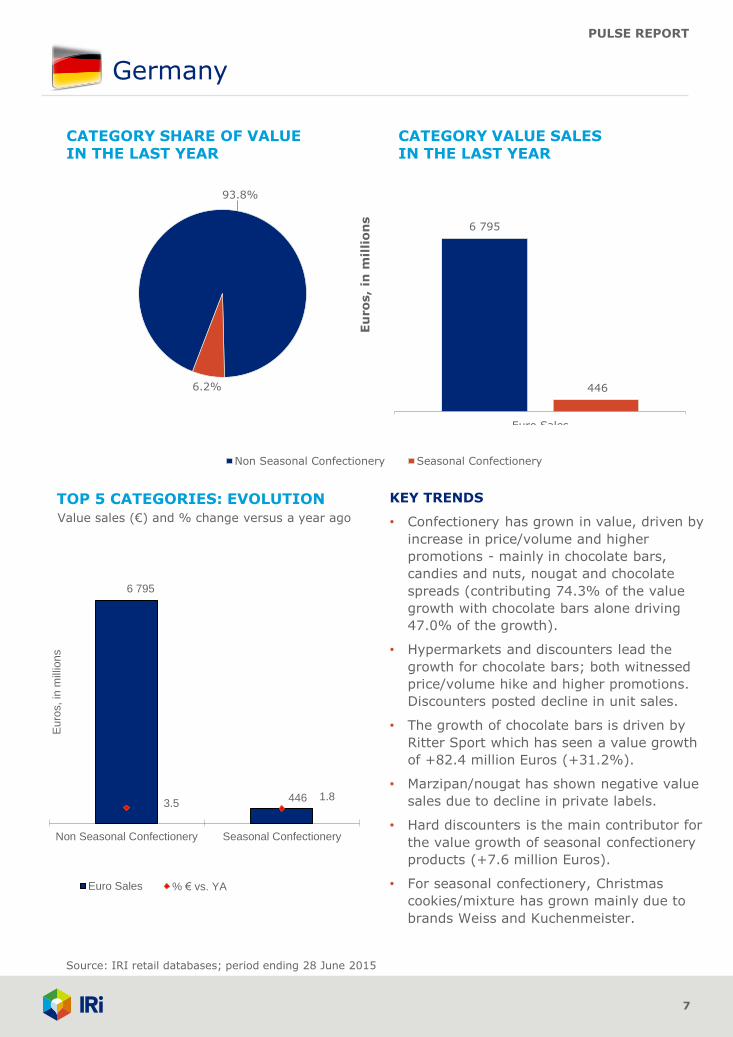

6 795

446 3.5

1.8

Non Seasonal Confectionery Seasonal Confectionery

Eu

ros,

in m

illio

ns

Euro Sales % € vs. YA

93.8%

6.2%

Non Seasonal Confectionery Seasonal Confectionery

Germany

7

KEY TRENDS

• Confectionery has grown in value, driven by

increase in price/volume and higher

promotions - mainly in chocolate bars,

candies and nuts, nougat and chocolate

spreads (contributing 74.3% of the value

growth with chocolate bars alone driving

47.0% of the growth).

• Hypermarkets and discounters lead the

growth for chocolate bars; both witnessed

price/volume hike and higher promotions.

Discounters posted decline in unit sales.

• The growth of chocolate bars is driven by

Ritter Sport which has seen a value growth

of +82.4 million Euros (+31.2%).

• Marzipan/nougat has shown negative value

sales due to decline in private labels.

• Hard discounters is the main contributor for

the value growth of seasonal confectionery

products (+7.6 million Euros).

• For seasonal confectionery, Christmas

cookies/mixture has grown mainly due to

brands Weiss and Kuchenmeister.

6 795

446

Euro Sales

Eu

ros,

in m

illi

on

s

CATEGORY VALUE SALES IN THE LAST YEAR

CATEGORY SHARE OF VALUE IN THE LAST YEAR

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change versus a year ago

Source: IRI retail databases; period ending 28 June 2015

PULSE REPORT

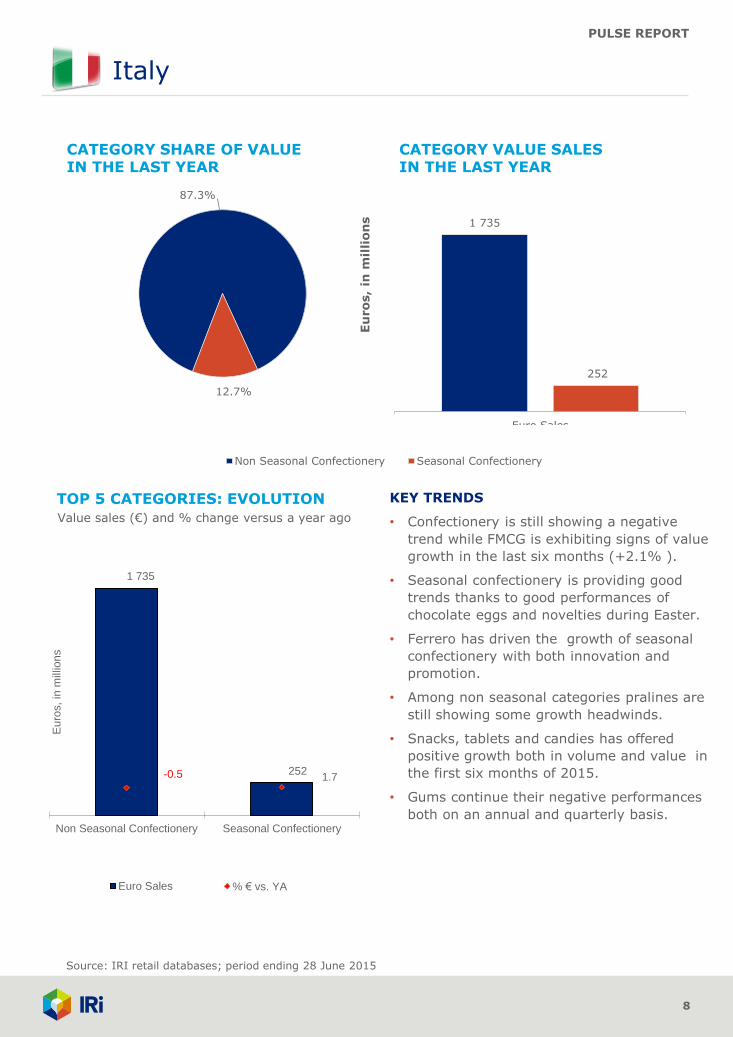

1 735

252 -0.5 1.7

Non Seasonal Confectionery Seasonal Confectionery

Eu

ros,

in m

illio

ns

Euro Sales % € vs. YA

87.3%

12.7%

Non Seasonal Confectionery Seasonal Confectionery

Italy

8

KEY TRENDS

• Confectionery is still showing a negative

trend while FMCG is exhibiting signs of value

growth in the last six months (+2.1% ).

• Seasonal confectionery is providing good

trends thanks to good performances of

chocolate eggs and novelties during Easter.

• Ferrero has driven the growth of seasonal

confectionery with both innovation and

promotion.

• Among non seasonal categories pralines are

still showing some growth headwinds.

• Snacks, tablets and candies has offered

positive growth both in volume and value in

the first six months of 2015.

• Gums continue their negative performances

both on an annual and quarterly basis.

1 735

252

Euro Sales

Eu

ros,

in m

illi

on

s

CATEGORY VALUE SALES IN THE LAST YEAR

CATEGORY SHARE OF VALUE IN THE LAST YEAR

Source: IRI retail databases; period ending 28 June 2015

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change versus a year ago

PULSE REPORT

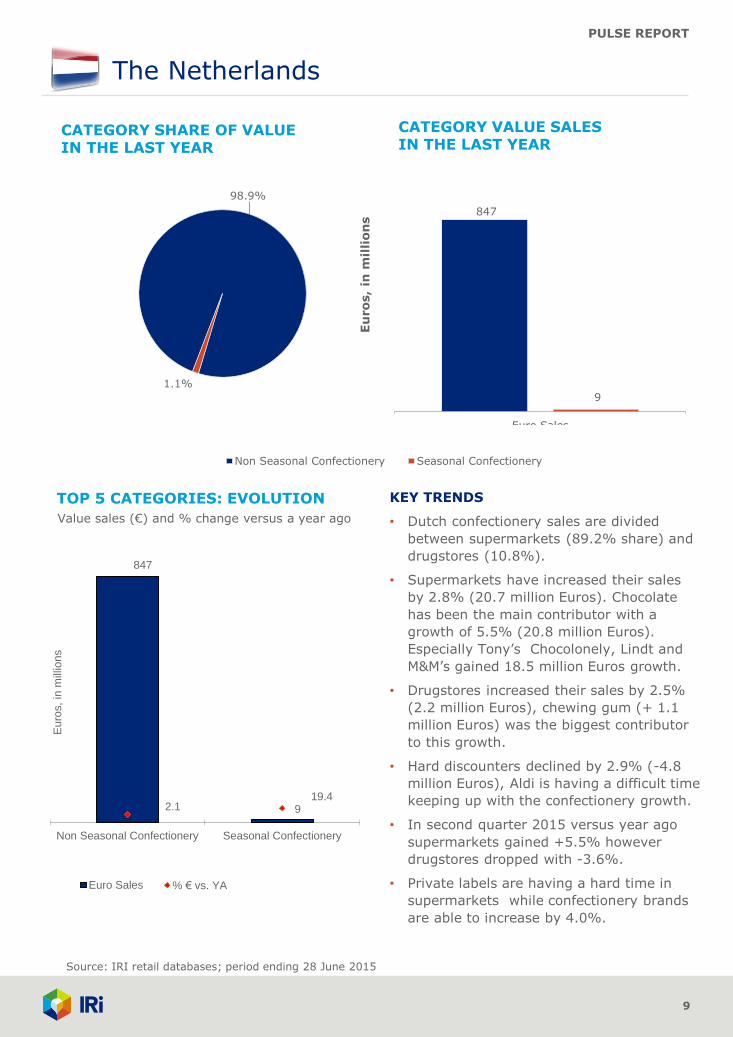

847

9 2.1 19.4

Non Seasonal Confectionery Seasonal Confectionery

Eu

ros,

in m

illio

ns

Euro Sales % € vs. YA

98.9%

1.1%

Non Seasonal Confectionery Seasonal Confectionery

The Netherlands

9

847

9

Euro Sales

Eu

ros,

in m

illi

on

s

CATEGORY VALUE SALES IN THE LAST YEAR

CATEGORY SHARE OF VALUE IN THE LAST YEAR

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change versus a year ago

Source: IRI retail databases; period ending 28 June 2015

KEY TRENDS

• Dutch confectionery sales are divided

between supermarkets (89.2% share) and

drugstores (10.8%).

• Supermarkets have increased their sales

by 2.8% (20.7 million Euros). Chocolate

has been the main contributor with a

growth of 5.5% (20.8 million Euros).

Especially Tony’s Chocolonely, Lindt and

M&M’s gained 18.5 million Euros growth.

• Drugstores increased their sales by 2.5%

(2.2 million Euros), chewing gum (+ 1.1

million Euros) was the biggest contributor

to this growth.

• Hard discounters declined by 2.9% (-4.8

million Euros), Aldi is having a difficult time

keeping up with the confectionery growth.

• In second quarter 2015 versus year ago

supermarkets gained +5.5% however

drugstores dropped with -3.6%.

• Private labels are having a hard time in

supermarkets while confectionery brands

are able to increase by 4.0%.

PULSE REPORT

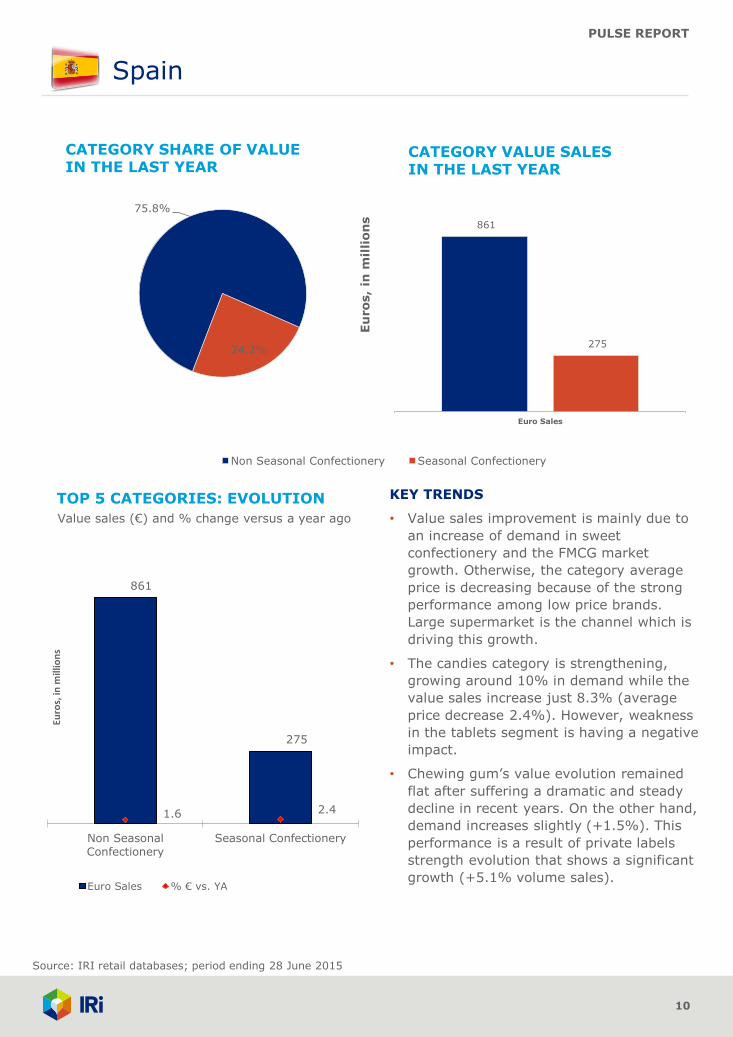

861

275

1.6 2.4

Non SeasonalConfectionery

Seasonal Confectionery

Euro

s, in

mill

ion

s

Euro Sales % € vs. YA

75.8%

24.2%

Non Seasonal Confectionery Seasonal Confectionery

Spain

10

KEY TRENDS

• Value sales improvement is mainly due to

an increase of demand in sweet

confectionery and the FMCG market

growth. Otherwise, the category average

price is decreasing because of the strong

performance among low price brands.

Large supermarket is the channel which is

driving this growth.

• The candies category is strengthening,

growing around 10% in demand while the

value sales increase just 8.3% (average

price decrease 2.4%). However, weakness

in the tablets segment is having a negative

impact.

• Chewing gum’s value evolution remained

flat after suffering a dramatic and steady

decline in recent years. On the other hand,

demand increases slightly (+1.5%). This

performance is a result of private labels

strength evolution that shows a significant

growth (+5.1% volume sales).

861

275

Euro Sales

Eu

ros,

in m

illi

on

s

CATEGORY VALUE SALES IN THE LAST YEAR

CATEGORY SHARE OF VALUE IN THE LAST YEAR

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change versus a year ago

Source: IRI retail databases; period ending 28 June 2015

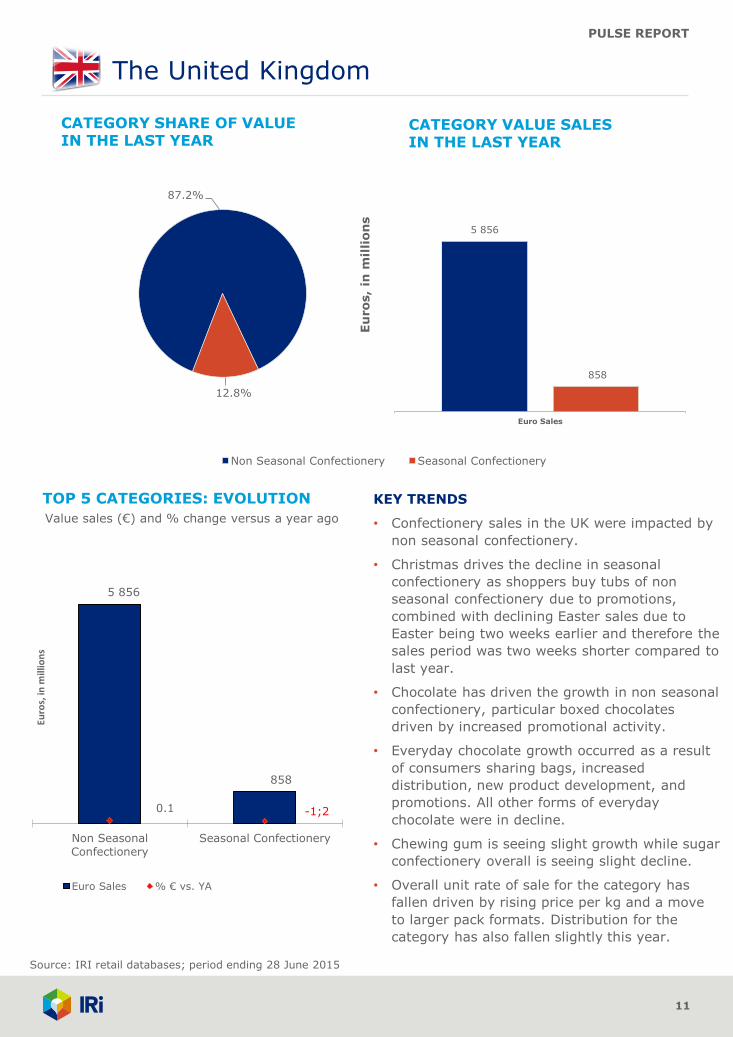

PULSE REPORT

5 856

858

0.1 -1;2

Non SeasonalConfectionery

Seasonal Confectionery

Euro

s, in

mill

ion

s

Euro Sales % € vs. YA

87.2%

12.8%

Non Seasonal Confectionery Seasonal Confectionery

The United Kingdom

11

KEY TRENDS

• Confectionery sales in the UK were impacted by

non seasonal confectionery.

• Christmas drives the decline in seasonal

confectionery as shoppers buy tubs of non

seasonal confectionery due to promotions,

combined with declining Easter sales due to

Easter being two weeks earlier and therefore the

sales period was two weeks shorter compared to

last year.

• Chocolate has driven the growth in non seasonal

confectionery, particular boxed chocolates

driven by increased promotional activity.

• Everyday chocolate growth occurred as a result

of consumers sharing bags, increased

distribution, new product development, and

promotions. All other forms of everyday

chocolate were in decline.

• Chewing gum is seeing slight growth while sugar

confectionery overall is seeing slight decline.

• Overall unit rate of sale for the category has

fallen driven by rising price per kg and a move

to larger pack formats. Distribution for the

category has also fallen slightly this year.

5 856

858

Euro Sales

Eu

ros,

in m

illi

on

s

CATEGORY VALUE SALES IN THE LAST YEAR

CATEGORY SHARE OF VALUE IN THE LAST YEAR

TOP 5 CATEGORIES: EVOLUTION

Value sales (€) and % change versus a year ago

Source: IRI retail databases; period ending 28 June 2015

PULSE REPORT

Final Notes

12

Notes on category definitions for countries

Due to the diverse products found in individual countries across this market it was necessary to

consolidate the available data into the categories in this report. In some cases it wasn’t always

possible to align products across all six countries hence the need to highlight any anomalies in

the report. Those exceptions are listed below:

Confectionery

• The Netherlands and Italy data in this report includes toffee products whereas the other

countries do not.

PULSE REPORT

Resources

13

About IRI. IRI is a leader in delivering powerful market and shopper information, predictive analysis and the foresight

that leads to action. We go beyond the data to ignite extraordinary growth for our clients in the CPG, retail and over-

the-counter healthcare industries by pinpointing what matters and illuminating how it can impact their businesses

across sales and marketing. Move your business forward at IRIworldwide.eu

Arlington Square, Downshire Way, Bracknell, Berkshire RG12 1WA, Tel +44 (0) 1344 746000

Copyright © 2015 Information Resources, Inc. (IRI). All rights reserved. IRI, the IRI logo and the names of IRI products and services

referenced herein are either trademarks or registered trademarks of IRI. All other trademarks are the property of their respective owners.

FOR MORE INFORMATION

Please contact Cristina Lazzaroni, Consultant, IRI at

+ 39 02 52579 333with questions or comments about this report.

To gain insight into opportunities across specific categories, segments, channels, or retailers,

contact your IRI client service representative regarding custom analysis leveraging the

following resources:

• InfoScan Census® is a syndicated retail tracking service that enables manufacturers and

retailers to acquire industry insights used to make better business decisions. InfoScan

Census utilizes the data that IRI collects from grocery, drug, and mass merchandise retailers

to provide the most comprehensive and accurate syndicated data offering in the FMCG

sector. With access to accurate, granular detail by category, geography, measure, and time

period, clients have the tools needed to develop marketing and sales strategies based on

product performance, distribution, and promotion responsiveness. All data about

confectionery comes from InfoScan Census.

• IRI Consulting provides strategic insights and advice leveraging a variety of data sources,

predictive analytics, enabling technologies, and business analyses to help FMCG

manufacturers and retailers address significant sales and marketing issues effectively.