Embed Size (px)

Citation preview

IRA Trusts in Estate Planning for Tax Savings and Asset Preservation

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

THURSDAY, MAY 31, 2012

Presenting a live 90-minute webinar with interactive Q&A

Scott K. Tippett, Director, Carruthers & Roth, Greensboro, N.C.

Gregory Herman-Giddens, President, TrustCounsel, Chapel Hill, N.C.

Conference Materials

If you have not printed the conference materials for this program, please complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Continuing Education Credits

For CLE purposes, please let us know how many people are listening at your location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of attendees at your location

• Click the SEND button beside the box

FOR LIVE EVENT ONLY

Tips for Optimal Quality

Sound Quality If you are listening via your computer speakers, please note that the quality of your sound will vary depending on the speed and quality of your internet connection. If the sound quality is not satisfactory and you are listening via your computer speakers, you may listen via the phone: dial 1-866-961-9091 and enter your PIN -when prompted. Otherwise, please send us a chat or e-mail [email protected] immediately so we can address the problem. If you dialed in and have any difficulties during the call, press *0 for assistance. Viewing Quality To maximize your screen, press the F11 key on your keyboard. To exit full screen, press the F11 key again.

IRA Trusts Advantages of IRA Trusts

presented by: Scott K. Tippett

Carruthers & Roth, P.A. Phone: 336-478-1130

E-mail: [email protected]

Advantages of IRA Trusts Why Use A Trust?

John Smith is 74. He owns substantial

business and investment assets. He also has $4 million in an IRA, which includes amounts rolled over from profit sharing and 401(k) plans. He currently receives RMDs and wants to leave as much as possible for the benefit of this three grandchildren Mckenzie (35), Kenan (22), and Cameron (20).

6

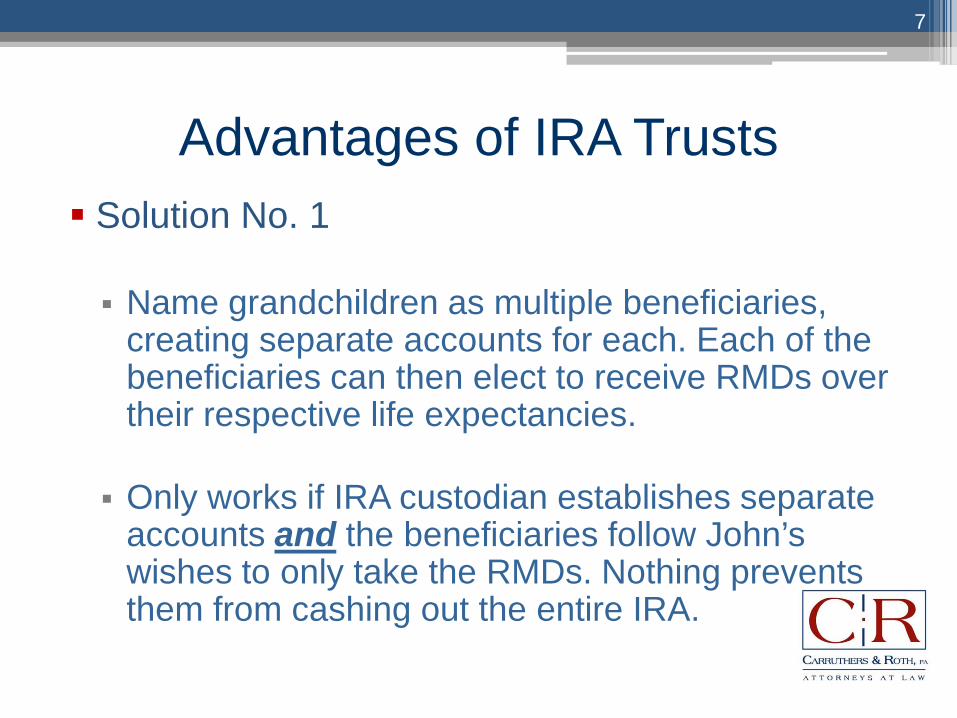

Advantages of IRA Trusts Solution No. 1

Name grandchildren as multiple beneficiaries,

creating separate accounts for each. Each of the beneficiaries can then elect to receive RMDs over their respective life expectancies.

Only works if IRA custodian establishes separate accounts and the beneficiaries follow John’s wishes to only take the RMDs. Nothing prevents them from cashing out the entire IRA.

7

Advantages of IRA Trusts

Problems With Naming Individuals as Benes. Most inherited IRAs are withdrawn almost

immediately, foregoing future benefits. Anecdotal evidence suggests that 80% to 90%

of IRAs that could be stretched are not. Short story, Stretch IRA likely will not happen.

8

Advantages of IRA Trusts Solution No. 2 Establish a trust for the benefit of Mckenzie,

Kenan, and Cameron and name the trust as the beneficiary of John’s IRA.

So long as the trust qualifies as a designated beneficiary the trust can elect to receive only the RMDs and nothing more, thereby preventing the grandchildren from cashing out the IRA.

However, because Mckenzie’s life (as the oldest beneficiary) will be used to calculate RMDs for all three grandchildren.

9

Advantages of IRA Trusts

Solution No. 3 Create a trust for the benefit of John’s

grandchildren with a separate sub-trust for each of Mckenzie, Kenan, and Cameron. Each sub-trust would be named as an equal beneficiary of the IRA. With this approach each sub-trust will use the respective sub-trust’s beneficiary’s life as the measuring life for RMDs for that sub-trust.

10

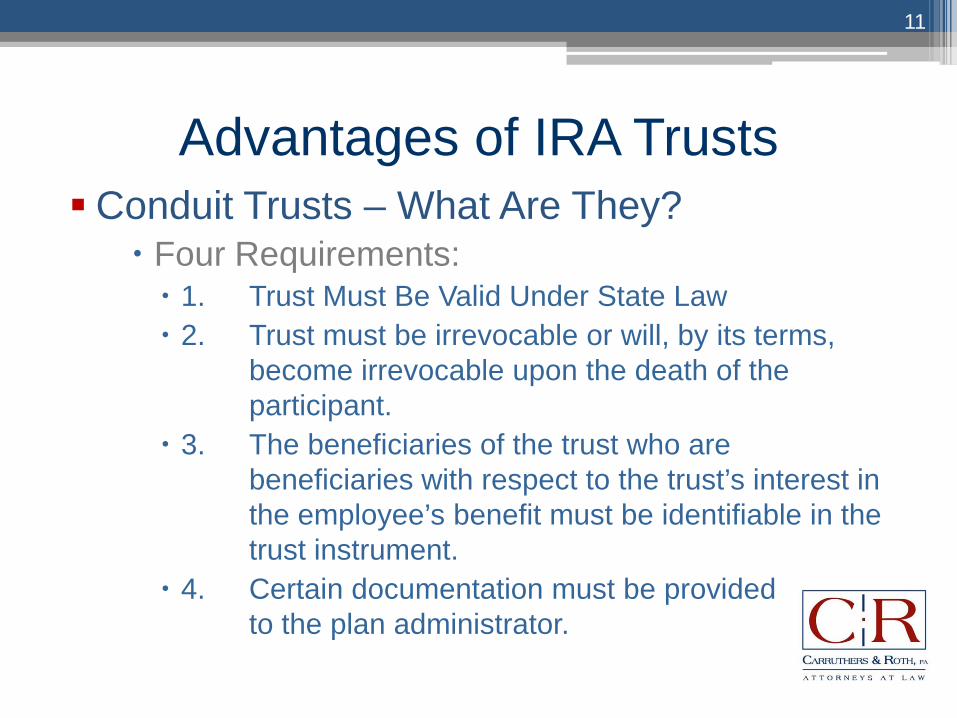

Advantages of IRA Trusts Conduit Trusts – What Are They?

Four Requirements: 1. Trust Must Be Valid Under State Law 2. Trust must be irrevocable or will, by its terms,

become irrevocable upon the death of the participant.

3. The beneficiaries of the trust who are beneficiaries with respect to the trust’s interest in the employee’s benefit must be identifiable in the trust instrument.

4. Certain documentation must be provided to the plan administrator.

11

Advantages of IRA Trusts

Conduit Trusts – The Fifth Rule 5. All beneficiaries must be individuals.

A conduit trust permits you to look through the

trust and treat the trust’s beneficiaries as if they were directly named as the Participant’s beneficiaries.

12

Advantages of IRA Trusts

Conduit Trust Uses A. QTIP

1. A Stretch QTIP? If the surviving spouse

is the sole beneficiary and the QTIP Trust is structured as a conduit trust, it will last longer because the surviving spouse’s life expectancy is recalculated annually for RMD purposes.

13

Advantages of IRA Trusts

QTIP as Conduit Trust cont’d 2. Deferral. Where the Participant dies

before the year in which the Participant attains the age of 70 ½ , RMDs can be deferred until the year in which the Participant would have attained 70 ½ , which allows a longer period of tax-deferred growth.

14

Advantages of IRA Trusts B. Older Beneficiaries The Problem: If a beneficiary is named as a direct

beneficiary of an IRA, the beneficiary must take RMDs over their life expectancy, which in the case of an older beneficiary does not leave as much time for tax deferred growth.

The Solution: Use a conduit trust naming the older bene as

the remainder bene of the trust because under Treas. Reg. § 1.401(a)(9)-5,A-7(c), successor (remainder) benes of the trust will not be considered a bene for the purposes of determining who is the bene with the shortest life expectancy.

15

Advantages of IRA Trusts PLR 201021038 shows how the typical provisions of a family revocable trust, inserted to obtain

maximum flexibility, can defeat the Participant’s goal to stretch the IRA. PLR 201203033 shows what must be addressed to enable a family trust to qualify as a conduit

trust to permit a spousal rollover and permit children to transfer their shares to inherited IRAs. This PLR also discusses the use of a disclaimer preserve the “stretch-out” of RMDs over a beneficiary’s life expectancy. This PLR provides a good road map for cleaning up a problem trust.

PLR 201210045 reinforces the necessity to comply with the “separate account” rule when naming

of the beneficiaries of an individual’s IRA account.

PLR 201203033 shows how retirement benefits payable to a trust can qualify for the stretch out notwithstanding a broad power of appointment exercisable in favor of a class of permissible appointees, along with a charity as the ultimate beneficiary.

Can a trust taxed as a grantor trust for income tax purposes be an IRA beneficiary? PLRs 200620025 (okay to transfer inherited IRA to a special needs trust) and PLR 200826008 (okay to transfer minor’s beneficiary share of decedent’s IRA to a grantor trust) say yes, but…

PLR 201117042 says no when the Participant wanted to transfer his IRA to a special needs trust

that was a grantor trust for income tax purposes.

16

Advantages of IRA Trusts When Would You Want a Trust as Beneficiary, Just Not a Conduit Trust?

Mckenzie is going through a divorce. Her soon to be ex-husband hired Gloria

All Red who is trying to get all of Mckenzie’s assets in a divorce settlement. Kenan invented a process to use fiber optics in place of printed circuit boards in

all computers, thereby increasing their speed a thousand fold. He has more money than he can count.

Cameron is a financial nightmare. He not only spends money as soon as he

gets it, but before he gets it. While his siblings have lengthy good credit reports, the local courthouse has a lengthy judgment roll with numerous outstanding judgments against Cameron.

John also wants to help his nephew who has severe autism. See PLR 2011-

50037 for a novel approach.

17

Advantages of IRA Trusts More Complications

John has a younger sister, Penn, who is 65 and

has never married. She rarely spends anything and manages to feed herself and her 33 cats on her Social Security income.

John’s current wife is his second wife, who he married late in life. They have no kids together, but John has two children from his first marriage.

18

Advantages of IRA Trusts

What Do All These Situations Have In Common? All are situations where a conduit trust would

not be the best choice. A more flexible approach would be to use an

accumulation trust.

19

Advantages of IRA Trusts

An “accumulation trust” is any trust that is not a conduit trust, which means the trustee has the power to “accumulate” plan distributions within the trust.

20

Advantages of IRA Trusts Issues With Accumulation Trusts Some or all of the potential remainder beneficiaries

are not disregarded for RMD purposes, which means an accumulation trust should not include remainder beneficiaries older than the lifetime beneficiary.

Contingent beneficiaries may not include one or more charities or an undetermined surviving spouse, otherwise it may be deemed to have no designated oldest beneficiary.

An accumulation trust may not include a limited testamentary power of appointment in favor of charities, surviving spouses, or older beneficiaries.

21

Advantages of IRA Trusts Modified Accumulation Trust* Features of a Modified Accumulation Trust An A share and a B share; the A share receives

benefits from all qualified plans and IRAs, the B share is everything else

Testamentary appointees of the A share are limited to descendants of the primary current beneficiary in the same or younger generation as the primary current beneficiary.

If surviving spouse is permitted appointee of the A share, specify that surviving spouse is no older than a designated number of years older than the primary beneficiary.

22

Advantages of IRA Trusts

Modified Accumulation Trust Provides that certain remaindermen are

deemed to be predeceased in the event the current beneficiary dies before the trust terminates. These remindermen can receive a preferential distribution of the B share. Can provide for an adjustment mechanism to offset any difference in tax consequences between the A share and B share beneficiaries.

23

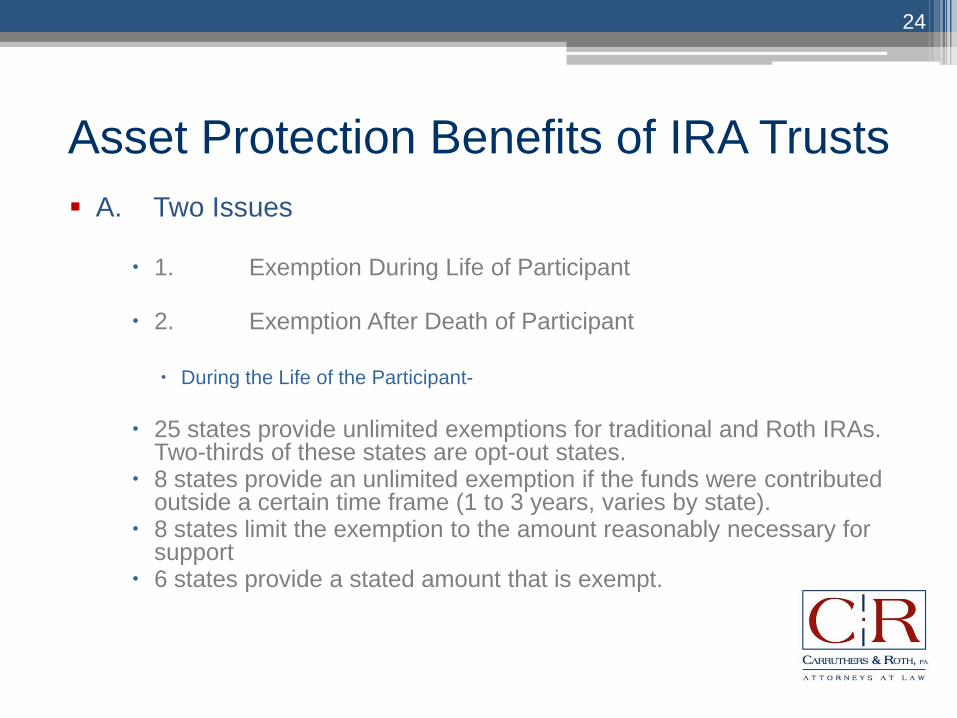

Asset Protection Benefits of IRA Trusts A. Two Issues

1. Exemption During Life of Participant

2. Exemption After Death of Participant

During the Life of the Participant-

25 states provide unlimited exemptions for traditional and Roth IRAs.

Two-thirds of these states are opt-out states. 8 states provide an unlimited exemption if the funds were contributed

outside a certain time frame (1 to 3 years, varies by state). 8 states limit the exemption to the amount reasonably necessary for

support 6 states provide a stated amount that is exempt.

24

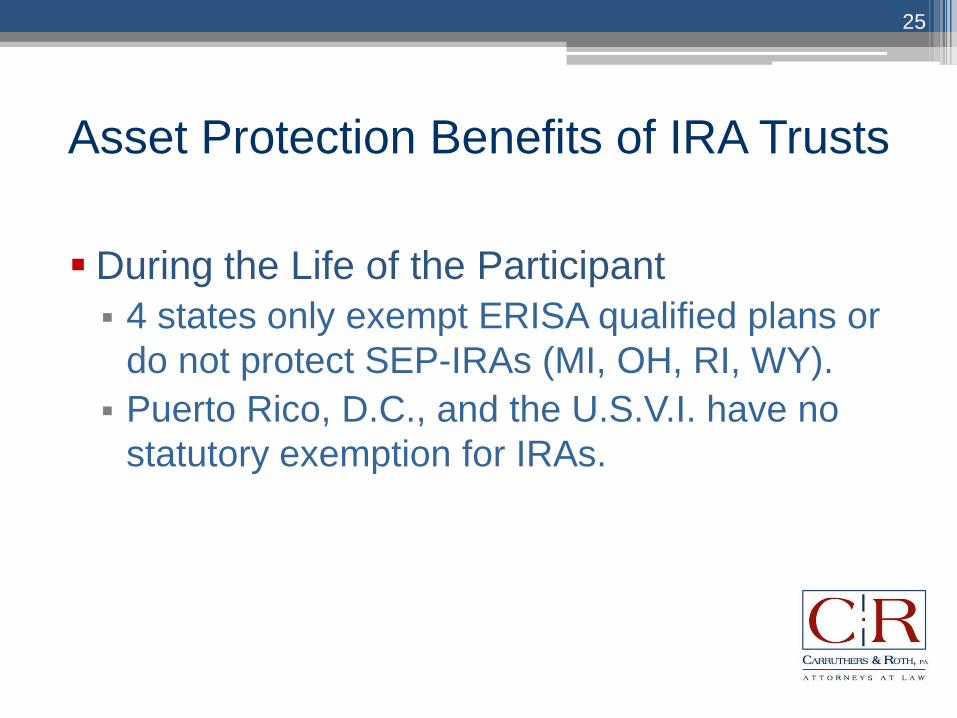

Asset Protection Benefits of IRA Trusts

During the Life of the Participant 4 states only exempt ERISA qualified plans or

do not protect SEP-IRAs (MI, OH, RI, WY). Puerto Rico, D.C., and the U.S.V.I. have no

statutory exemption for IRAs.

25

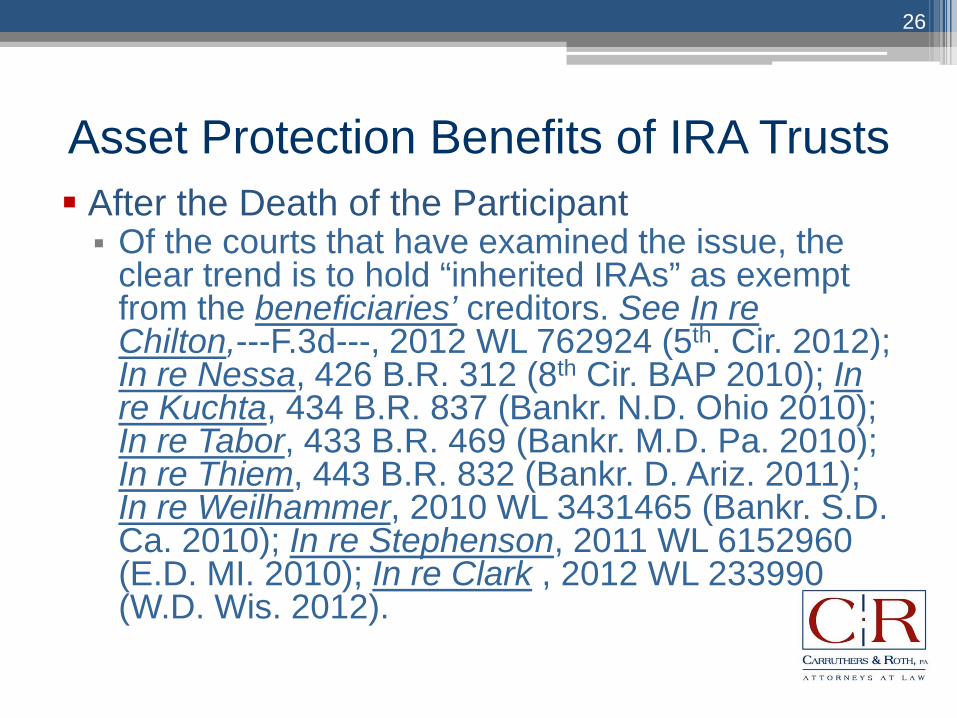

Asset Protection Benefits of IRA Trusts After the Death of the Participant Of the courts that have examined the issue, the

clear trend is to hold “inherited IRAs” as exempt from the beneficiaries’ creditors. See In re Chilton,---F.3d---, 2012 WL 762924 (5th. Cir. 2012); In re Nessa, 426 B.R. 312 (8th Cir. BAP 2010); In re Kuchta, 434 B.R. 837 (Bankr. N.D. Ohio 2010); In re Tabor, 433 B.R. 469 (Bankr. M.D. Pa. 2010); In re Thiem, 443 B.R. 832 (Bankr. D. Ariz. 2011); In re Weilhammer, 2010 WL 3431465 (Bankr. S.D. Ca. 2010); In re Stephenson, 2011 WL 6152960 (E.D. MI. 2010); In re Clark , 2012 WL 233990 (W.D. Wis. 2012).

26

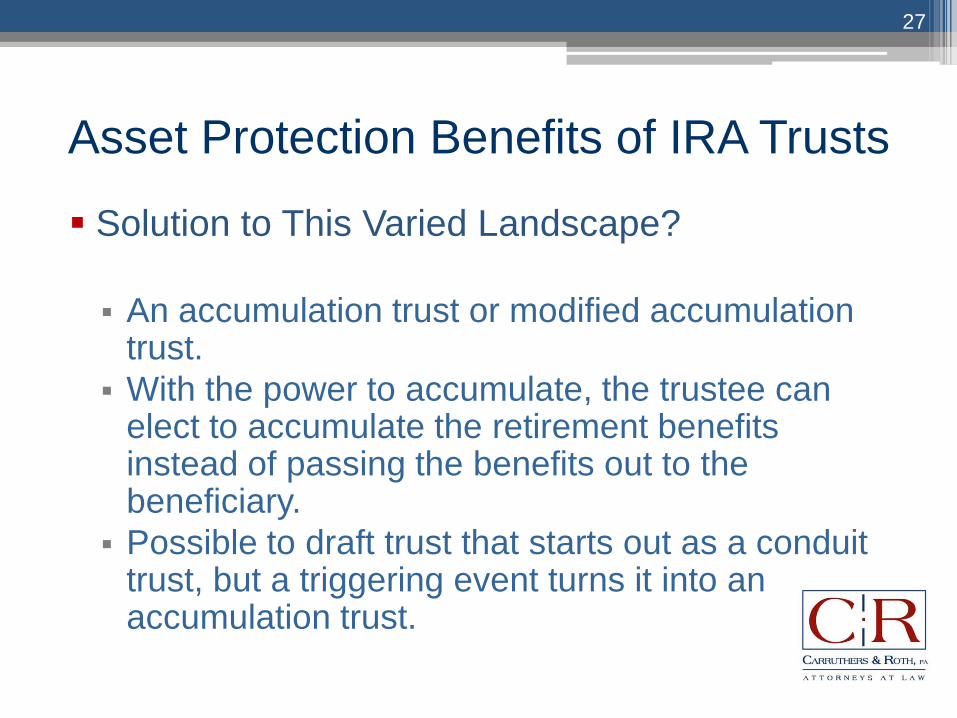

Asset Protection Benefits of IRA Trusts

Solution to This Varied Landscape? An accumulation trust or modified accumulation

trust. With the power to accumulate, the trustee can

elect to accumulate the retirement benefits instead of passing the benefits out to the beneficiary.

Possible to draft trust that starts out as a conduit trust, but a triggering event turns it into an accumulation trust.

27

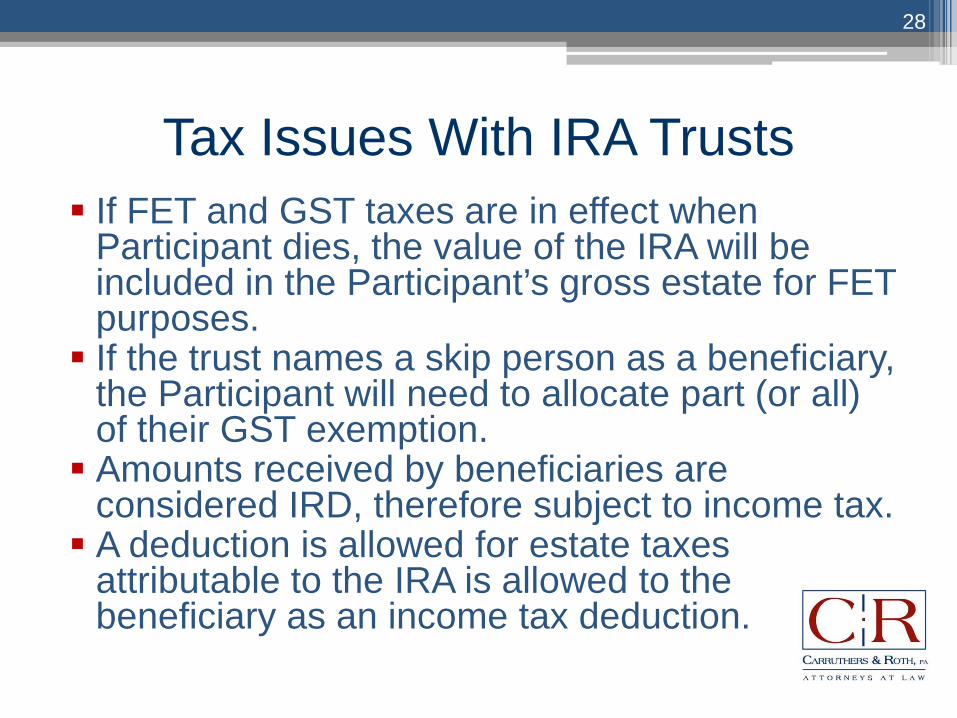

Tax Issues With IRA Trusts If FET and GST taxes are in effect when

Participant dies, the value of the IRA will be included in the Participant’s gross estate for FET purposes. If the trust names a skip person as a beneficiary,

the Participant will need to allocate part (or all) of their GST exemption. Amounts received by beneficiaries are

considered IRD, therefore subject to income tax. A deduction is allowed for estate taxes

attributable to the IRA is allowed to the beneficiary as an income tax deduction.

28

Leveraging IRA Trusts in Estate Planning May 31, 2012

Gregory Herman-Giddens, JD, LLM, TEP, CFP Attorney at Law

North Carolina ▪ Florida ▪ New York 800-201-0413

[email protected] www.trustcounselpa.com

Main Office 205 Providence Rd., Chapel Hill, NC 27514

With thanks and credit to Robert S. Keebler, CPA, the source of a majority of the slides (used with permission, all rights reserved)

Required Minimum Distribution Rules

and Other Rules Applicable to IRAs

30

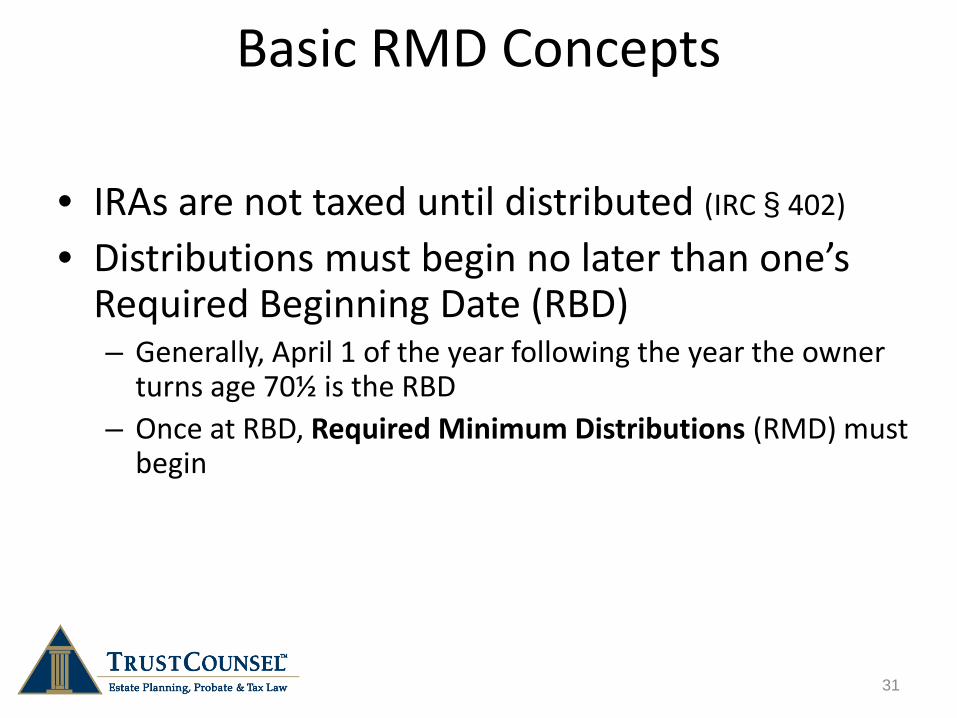

Basic RMD Concepts

• IRAs are not taxed until distributed (IRC § 402)

• Distributions must begin no later than one’s Required Beginning Date (RBD) – Generally, April 1 of the year following the year the owner

turns age 70½ is the RBD – Once at RBD, Required Minimum Distributions (RMD) must

begin

31 31

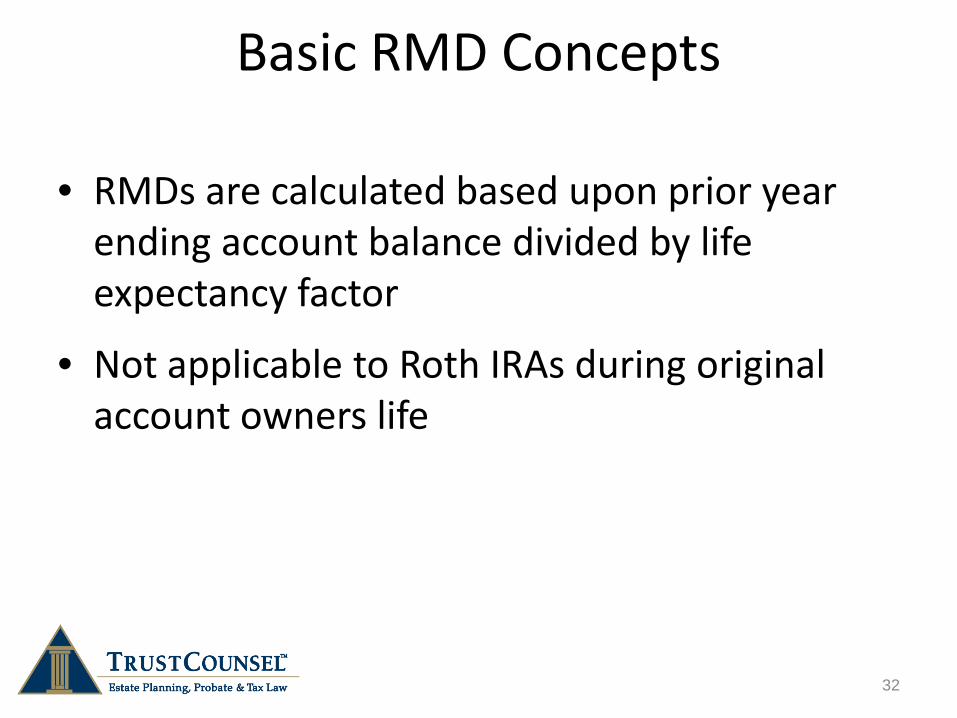

Basic RMD Concepts

• RMDs are calculated based upon prior year ending account balance divided by life expectancy factor

• Not applicable to Roth IRAs during original account owners life

32 32

Expectancy Factor RMD =

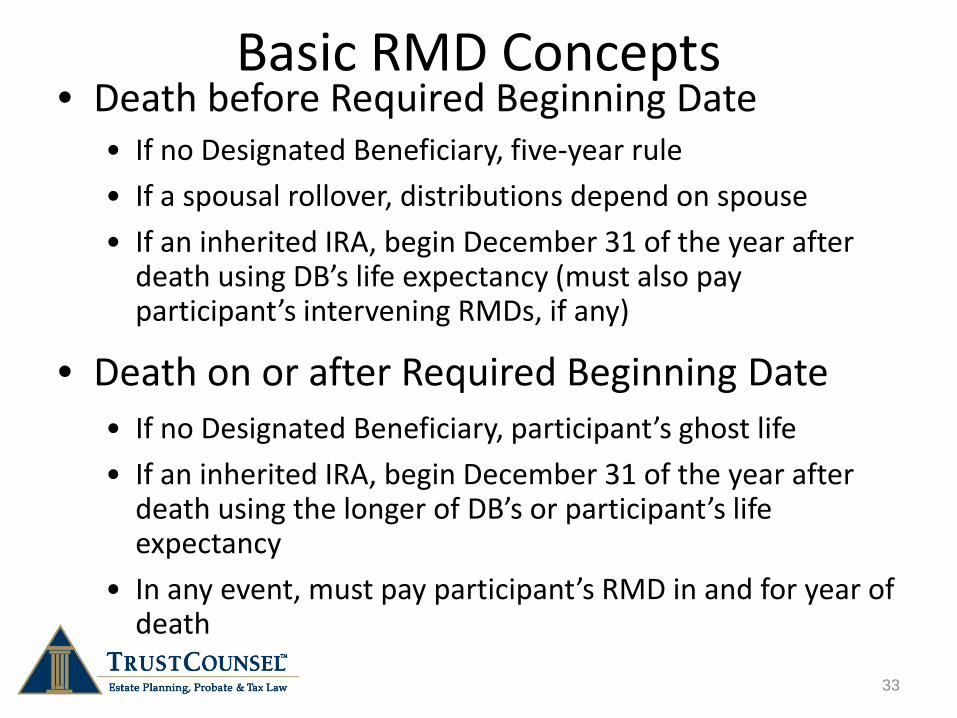

Basic RMD Concepts • Death before Required Beginning Date

• If no Designated Beneficiary, five-year rule • If a spousal rollover, distributions depend on spouse • If an inherited IRA, begin December 31 of the year after

death using DB’s life expectancy (must also pay participant’s intervening RMDs, if any)

• Death on or after Required Beginning Date • If no Designated Beneficiary, participant’s ghost life • If an inherited IRA, begin December 31 of the year after

death using the longer of DB’s or participant’s life expectancy

• In any event, must pay participant’s RMD in and for year of death

33 33

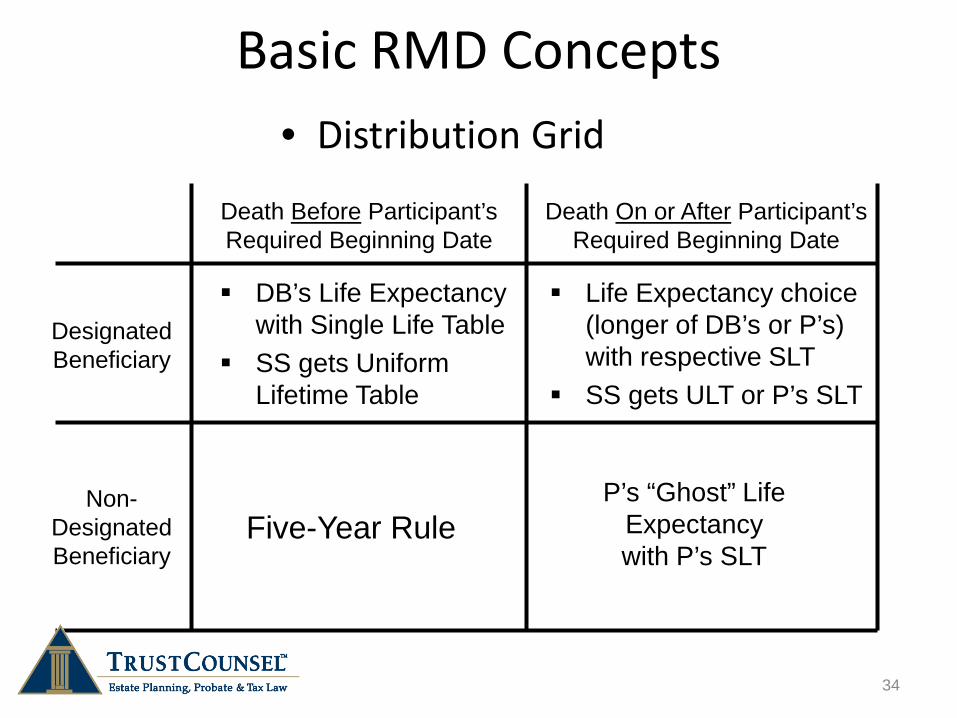

Basic RMD Concepts • Distribution Grid

34

Five-Year Rule

Death Before Participant’s Required Beginning Date

Death On or After Participant’s Required Beginning Date

Designated Beneficiary

Non-Designated Beneficiary

P’s “Ghost” Life Expectancy with P’s SLT

DB’s Life Expectancy with Single Life Table

SS gets Uniform Lifetime Table

Life Expectancy choice (longer of DB’s or P’s) with respective SLT

SS gets ULT or P’s SLT

Basic RMD Concepts

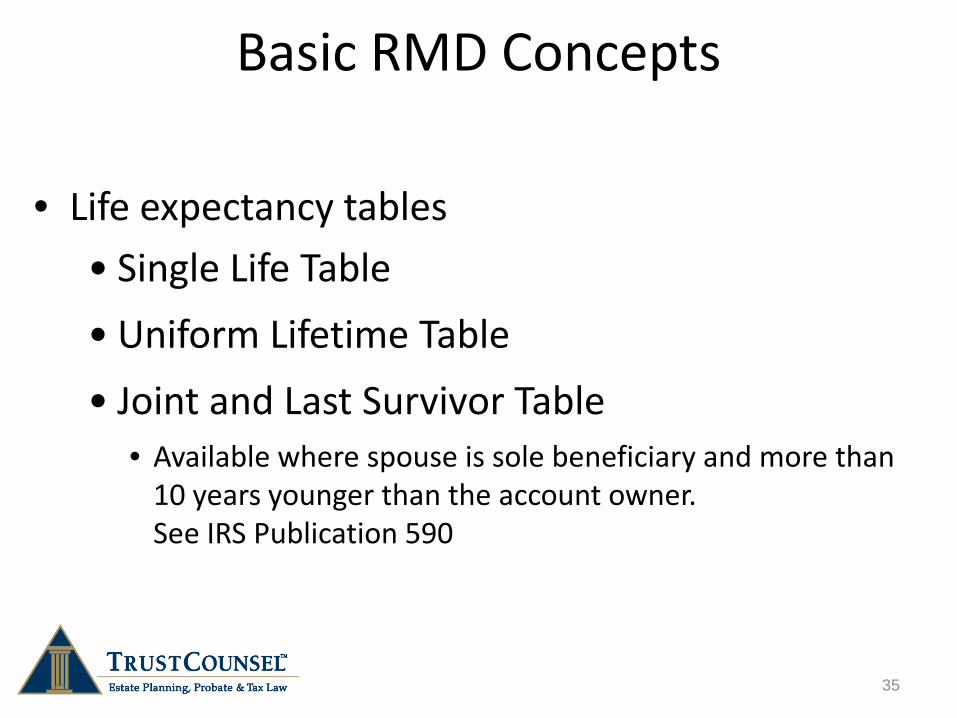

• Life expectancy tables • Single Life Table • Uniform Lifetime Table • Joint and Last Survivor Table

• Available where spouse is sole beneficiary and more than 10 years younger than the account owner. See IRS Publication 590

35 35

Basic RMD Concepts

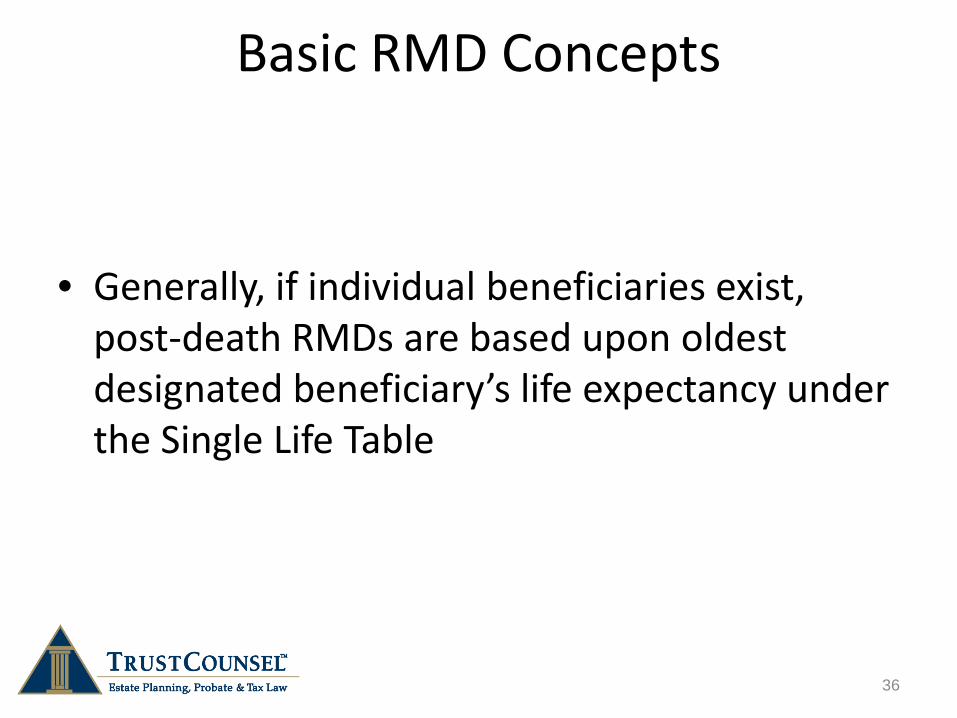

• Generally, if individual beneficiaries exist, post-death RMDs are based upon oldest designated beneficiary’s life expectancy under the Single Life Table

36 36

Basic RMD Concepts

• Post-death RMDs based on whether “designated beneficiary” exists • Only “individuals” with quantifiable life expectancy can be

“designated beneficiaries”

• If trust qualifies, can “look through” to underlying trust beneficiaries • Simply distributing out of trust to beneficiary does not make the

beneficiary the “designated beneficiary”

• An estate is not a designated beneficiary

37 37

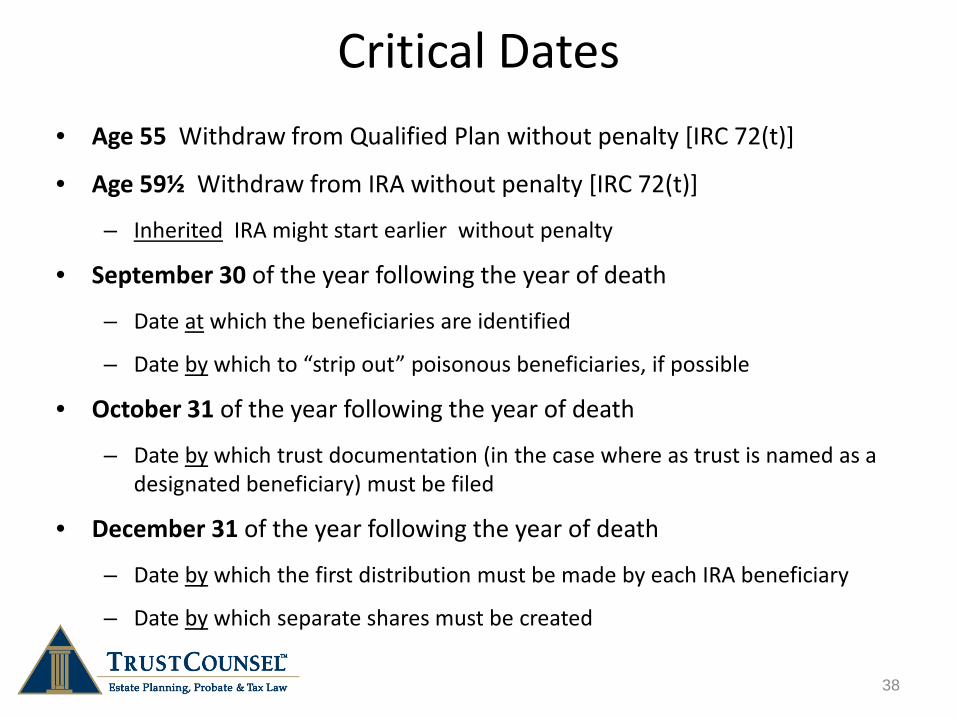

Critical Dates • Age 55 Withdraw from Qualified Plan without penalty [IRC 72(t)]

• Age 59½ Withdraw from IRA without penalty [IRC 72(t)]

– Inherited IRA might start earlier without penalty

• September 30 of the year following the year of death

– Date at which the beneficiaries are identified

– Date by which to “strip out” poisonous beneficiaries, if possible

• October 31 of the year following the year of death

– Date by which trust documentation (in the case where as trust is named as a designated beneficiary) must be filed

• December 31 of the year following the year of death

– Date by which the first distribution must be made by each IRA beneficiary

– Date by which separate shares must be created

38

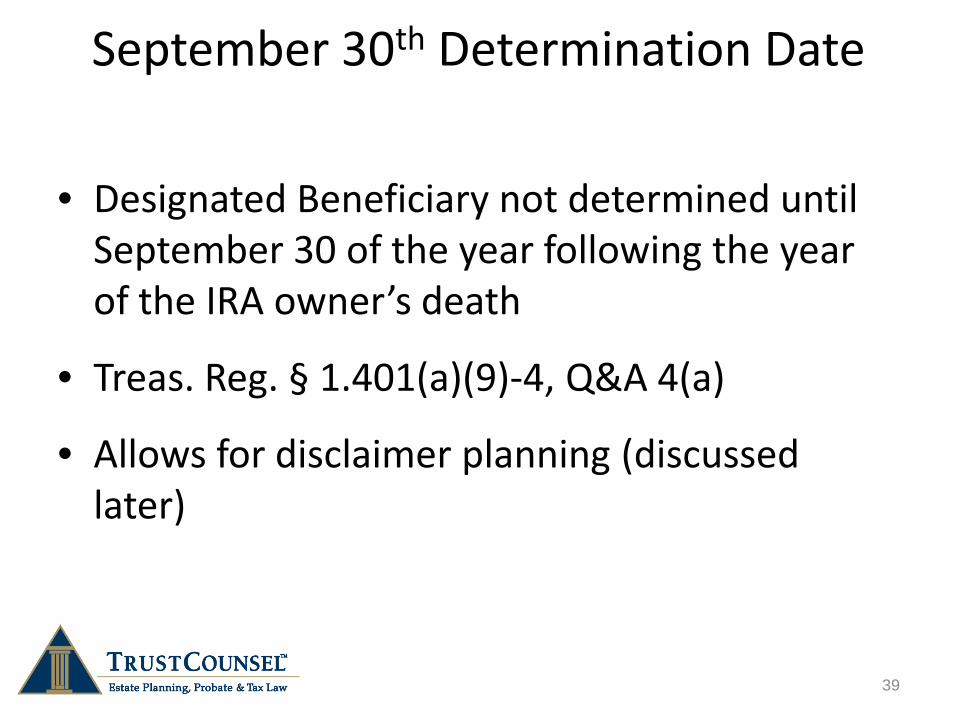

September 30th Determination Date

• Designated Beneficiary not determined until September 30 of the year following the year of the IRA owner’s death

• Treas. Reg. § 1.401(a)(9)-4, Q&A 4(a)

• Allows for disclaimer planning (discussed later)

39 39

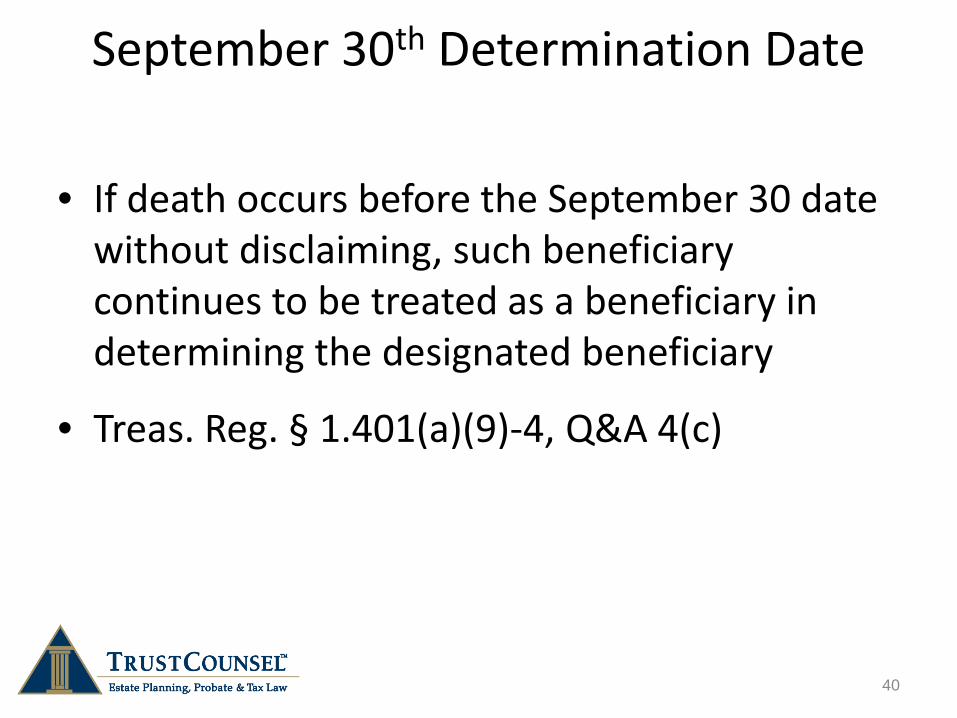

September 30th Determination Date

• If death occurs before the September 30 date without disclaiming, such beneficiary continues to be treated as a beneficiary in determining the designated beneficiary

• Treas. Reg. § 1.401(a)(9)-4, Q&A 4(c)

40 40

September 30th Determination Date Example

• Jane names a trust as beneficiary of her IRA. 90% of the trust is payable to her children over their lifetimes. 10% of the trust is payable to Jane’s favorite charity.

• If the charity’s 10% is separated and paid out of the trust by September 30th of the year following the year of Jane’s death, the charity’s interest will not taint the rest of the trust.

• See PLR 200218039 (Michelle L. Ward and Robert S. Keebler)

41 41

September 30th Determination Date Example

• John names his wife as primary beneficiary of his IRA and his grandchild as contingent beneficiary.

• If John’s wife executes a qualified disclaimer by September 30th of the year following the year of John’s death, RMDs can be calculated based on the grandchild’s life expectancy.

42 42

September 30th Determination Date Example

• John names his sister as primary beneficiary of his IRA and his nephew as contingent beneficiary.

• If John’s sister dies before September 30th of the year following the year of John’s death without performing a qualified disclaimer , RMDs are still calculated based on the sister’s life expectancy.

43 43

Disclaimer Planning

Disclaimer must be “qualified” (IRC § 2518) • In writing • Within 9 months • No acceptance of the property interest or any of its

benefits * • Interest passes without any direction on the part of

the person making the disclaimer * Rev. Rul. 2005-36 allows disclaimer of the IRA balance even though, prior to

disclaimer, the beneficiary receives the RMD for the year of the decedent’s death.

44 44

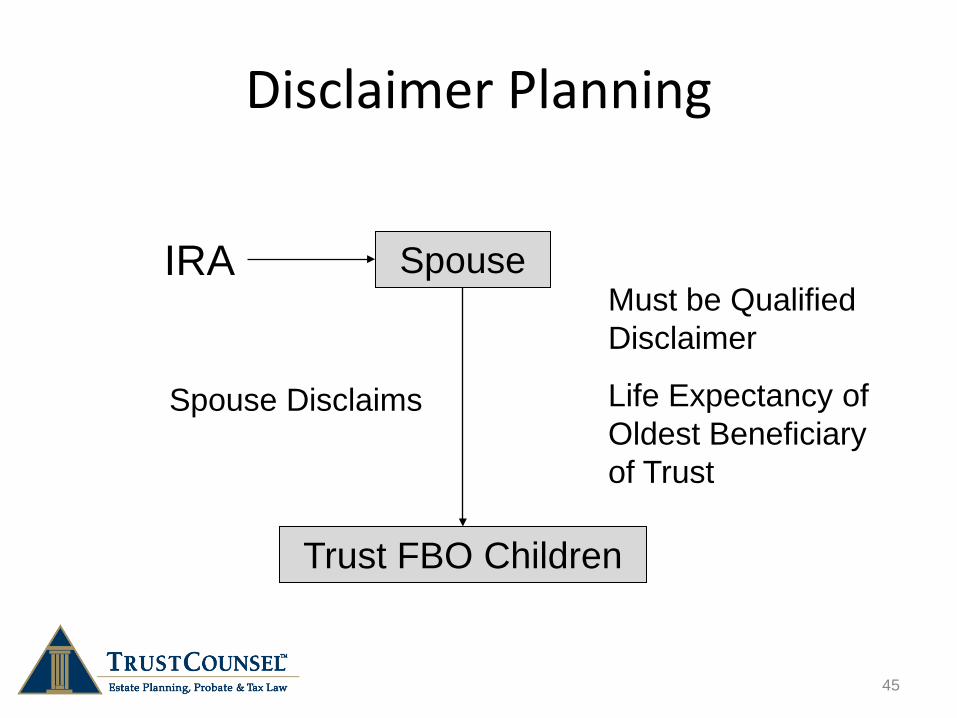

45

Disclaimer Planning

45

IRA Spouse Must be Qualified Disclaimer

Life Expectancy of Oldest Beneficiary of Trust

Trust FBO Children

Spouse Disclaims

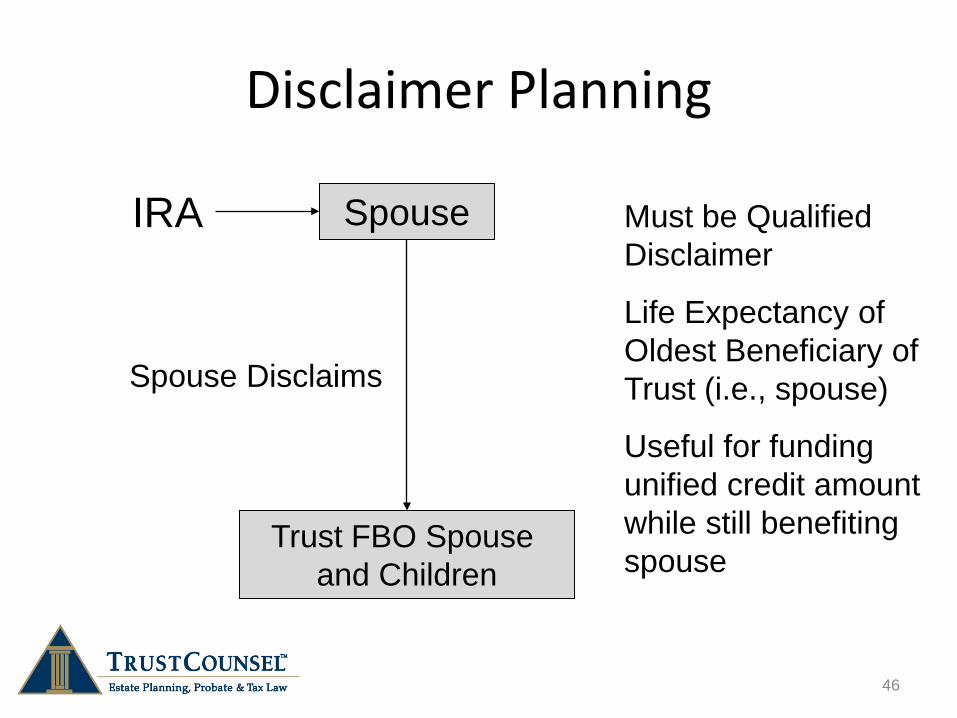

46

Disclaimer Planning

46

IRA Spouse Must be Qualified Disclaimer

Life Expectancy of Oldest Beneficiary of Trust (i.e., spouse)

Useful for funding unified credit amount while still benefiting spouse

Trust FBO Spouse and Children

Spouse Disclaims

47

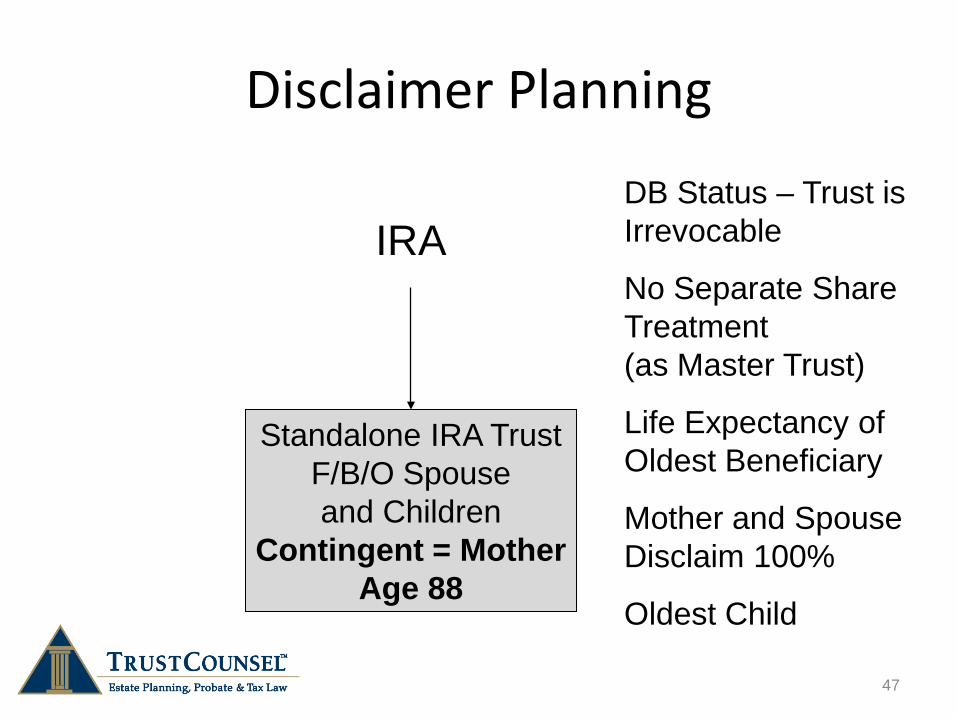

Disclaimer Planning

47

IRA

Standalone IRA Trust F/B/O Spouse and Children

Contingent = Mother Age 88

DB Status – Trust is Irrevocable

No Separate Share Treatment (as Master Trust)

Life Expectancy of Oldest Beneficiary

Mother and Spouse Disclaim 100%

Oldest Child is DB

Naming a Trust as a “Designated Beneficiary”

48 48

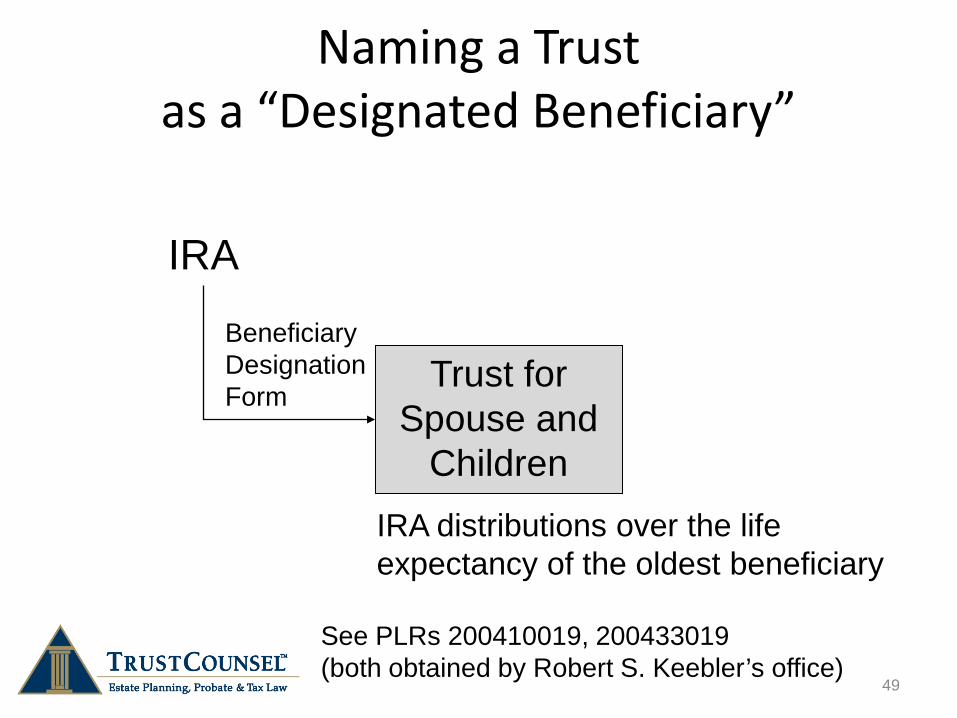

49

Naming a Trust as a “Designated Beneficiary”

49

An IRA Can Be Payable to a Trust

See PLRs 200410019, 200433019 (both obtained by Robert S. Keebler’s office)

IRA distributions over the life expectancy of the oldest beneficiary

Trust for Spouse and

Children

IRA

Beneficiary Designation Form

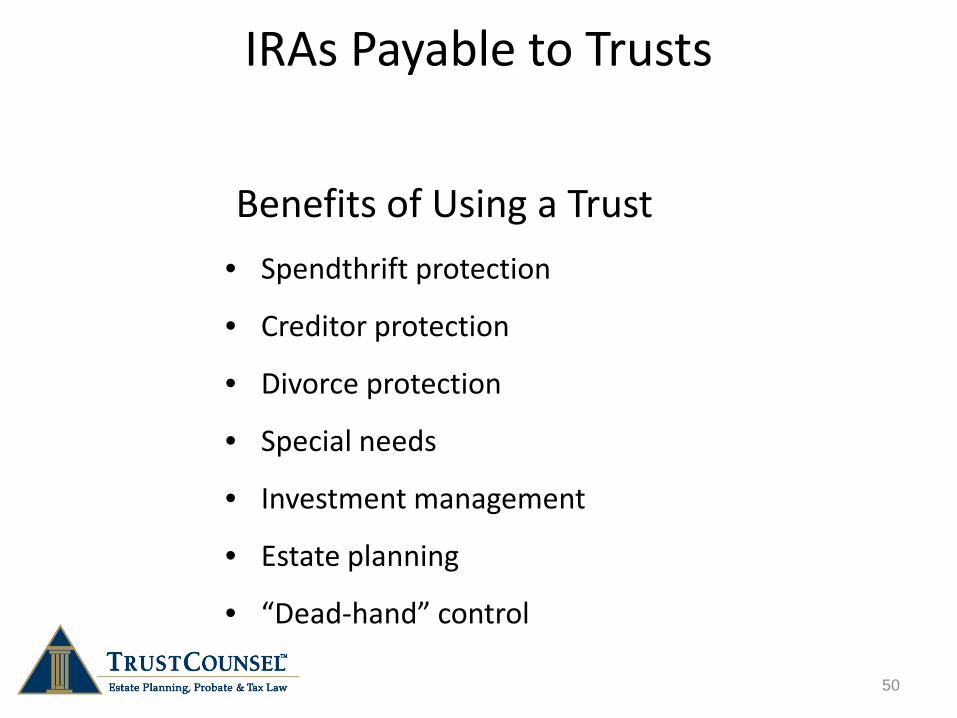

IRAs Payable to Trusts

Benefits of Using a Trust • Spendthrift protection

• Creditor protection

• Divorce protection

• Special needs

• Investment management

• Estate planning

• “Dead-hand” control

50

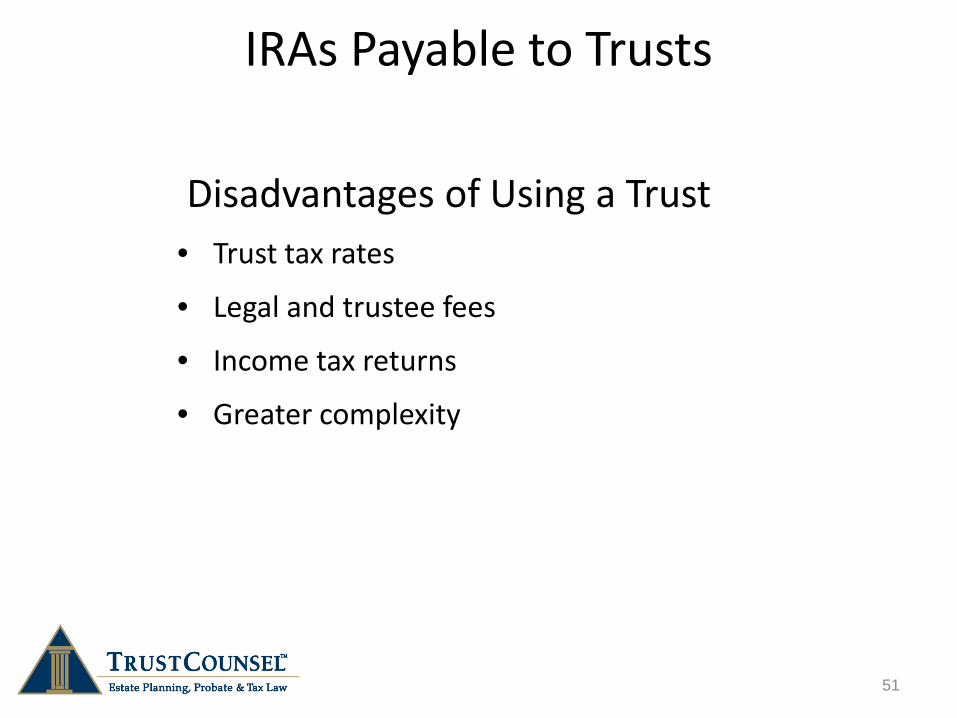

IRAs Payable to Trusts

Disadvantages of Using a Trust • Trust tax rates

• Legal and trustee fees

• Income tax returns

• Greater complexity

51

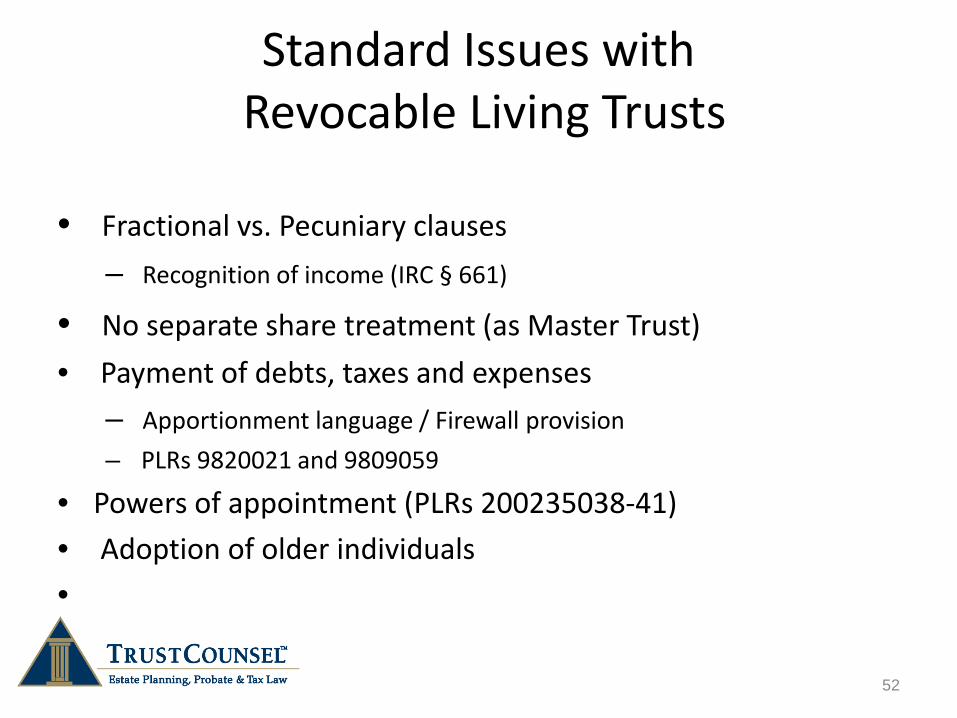

Standard Issues with Revocable Living Trusts

• Fractional vs. Pecuniary clauses – Recognition of income (IRC § 661)

• No separate share treatment (as Master Trust) • Payment of debts, taxes and expenses

– Apportionment language / Firewall provision – PLRs 9820021 and 9809059

• Powers of appointment (PLRs 200235038-41) • Adoption of older individuals •

52 52

IRAs Payable to Trusts

Other Considerations • Older or unidentifiable contingent beneficiary • Estate as contingent beneficiary • Failure of beneficiaries clause • Failure to provide trust document to custodian by October 31 of year following year of death • Making lump sum IRA distribution to trust

53

Structuring IRA Trusts

54

Structuring IRA Trusts

Four Requirements of All IRA Trusts 1. Trust is valid under state law

2. Trust is irrevocable upon death of owner

3. Beneficiaries of the trust are identifiable from the trust instrument

4. Documentation requirement is satisfied

55

Four Requirements for ALL Trusts

Number One • Trust is valid under state law

• Treas. Reg. § 1.401(a)(9)-4, Q&A 5(b)(1)

• Easily met

56 56

Four Requirements for ALL Trusts

Number Two

• Trust is irrevocable upon death of owner

• Treas. Reg. § 1.401(a)(9)-4, Q&A 5(b)(2)

• Difficult to satisfy when using joint revocable trust

57 57

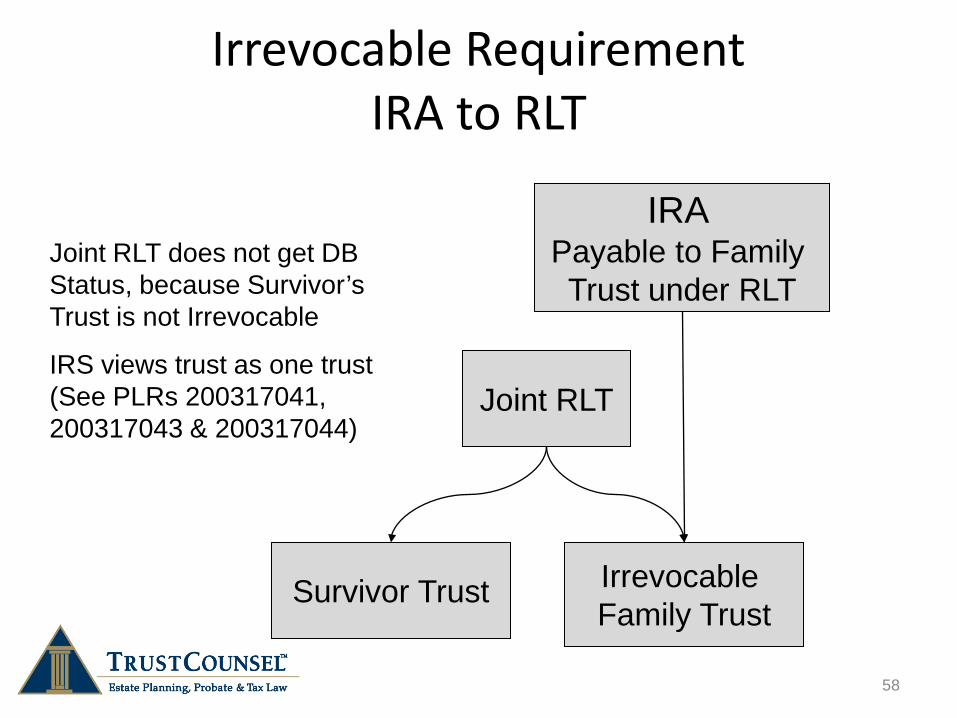

Irrevocable Requirement IRA to RLT

58 58

IRA Payable to Family Trust under RLT

Joint RLT

Joint RLT does not get DB Status, because Survivor’s Trust is not Irrevocable

IRS views trust as one trust (See PLRs 200317041, 200317043 & 200317044)

Survivor Trust Irrevocable Family Trust

Four Requirements for ALL Trusts

Number Three • Beneficiaries of the trust are identifiable from the

trust instrument

• Treas. Reg. § 1.401(a)(9)-4, Q&A 5(b)(3)

59 59

Four Requirements for ALL Trusts

Number Four • Documentation requirement is satisfied

(October 31st) • Treas. Reg. § 1.401(a)(9)-4, Q&A 5(b)(4)

60 60

IRAs Payable to Trusts

Separate Shares • In proper circumstances, the IRS allows the division of

the IRA into separate shares per beneficiary

• In the case of an individual beneficiary, this must be determined by December 31 of the year following the year of death

– Separate shares established when divided

• No separate shares available for estates

• Disclaimers are permitted

• Death by September 30

61

IRAs Payable to Trusts

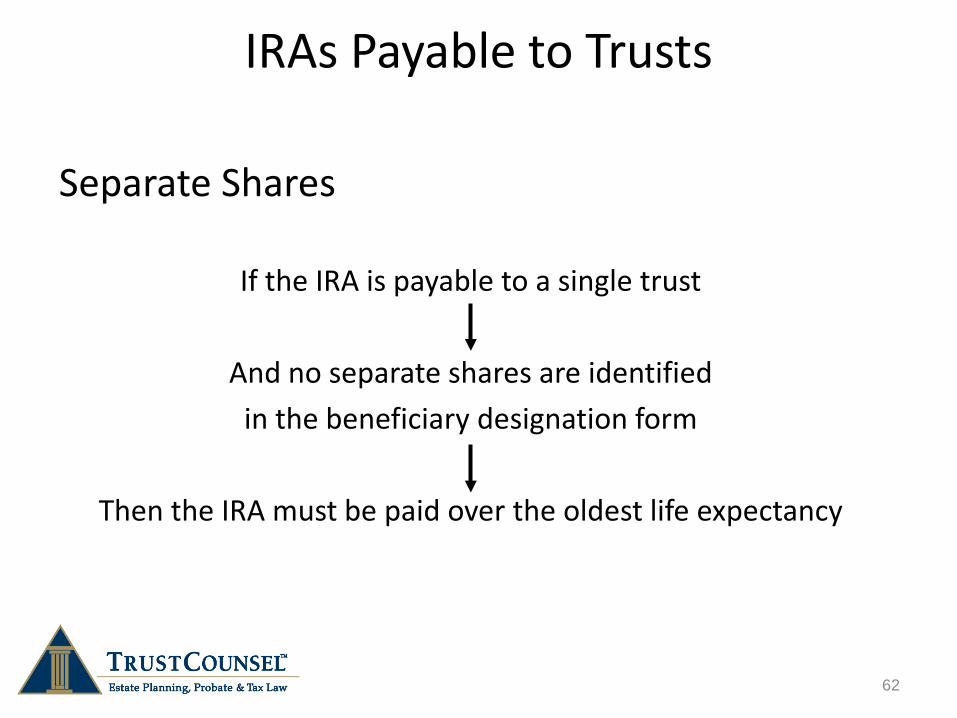

Separate Shares

If the IRA is payable to a single trust

And no separate shares are identified in the beneficiary designation form

Then the IRA must be paid over the oldest life expectancy

62

IRAs Payable to Trusts

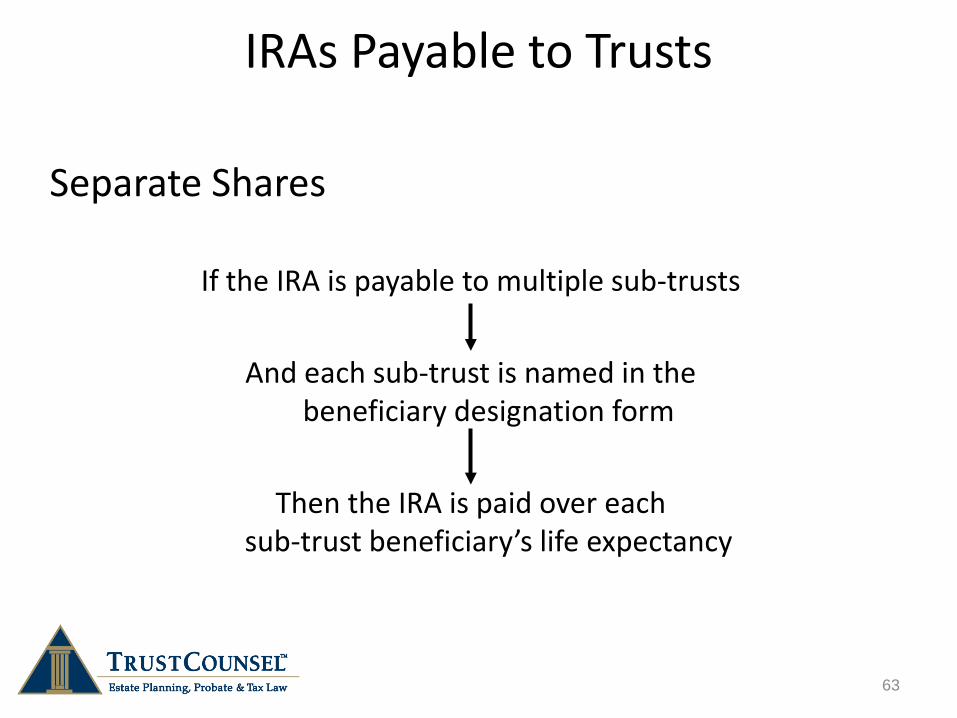

Separate Shares

If the IRA is payable to multiple sub-trusts

And each sub-trust is named in the beneficiary designation form

Then the IRA is paid over each

sub-trust beneficiary’s life expectancy

63

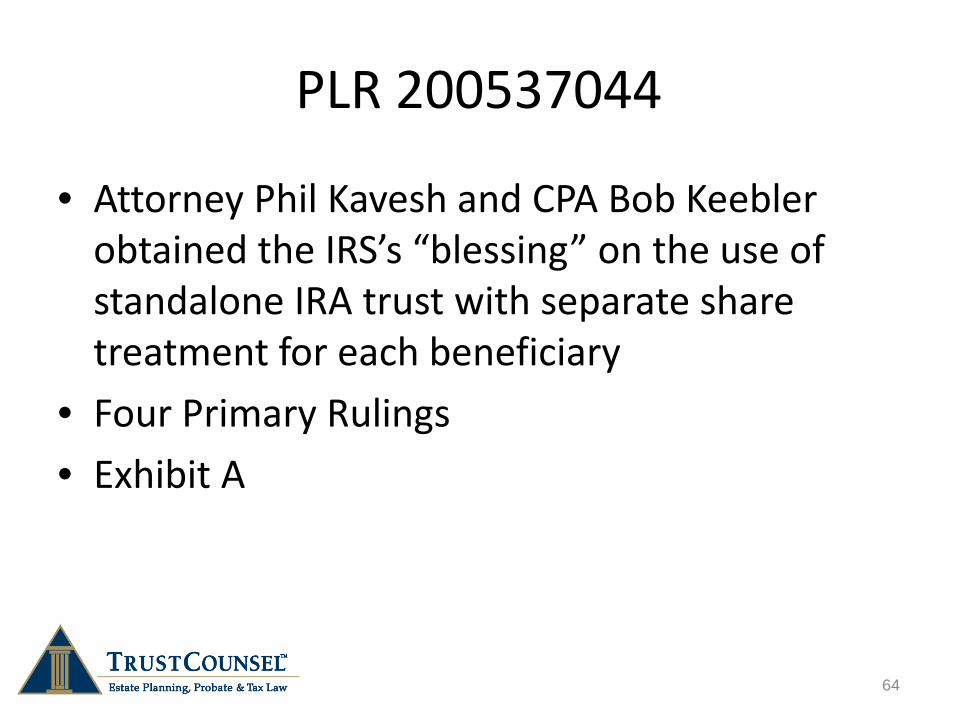

PLR 200537044

• Attorney Phil Kavesh and CPA Bob Keebler obtained the IRS’s “blessing” on the use of standalone IRA trust with separate share treatment for each beneficiary

• Four Primary Rulings • Exhibit A

64

IRA Trust PLR Rulings • Ruling 1: Each Beneficiary’s Trust Share Qualified for

Maximum Stretch. – Upon the death of the Settlor, the IRA standalone trust creates

separate shares for each beneficiary (in this case, separate shares for 9 beneficiaries), each trust share “treated effective ab initio to the date of the Decedent’s death” and each share functioned as a “separate and distinct trust” for the beneficiary.

– The beneficiary designation form named each separate share as a primary beneficiary of the IRA.

– Before the December 31st deadline, the IRA was divided into separate accounts for each share.

– Held: Separate account is treatment permitted; MRD of the IRA for each separate trust share is measured by the life of its sole beneficiary for whom the share was created.

65

– PLR 200537044

IRA Trust PLR Rulings

• Ruling 2: Allowance of One-Time “Toggle” from Conduit Trust to Accumulation Trust. – Each separate share in the IRA standalone trust had language

structuring the separate share as a conduit trust. – The trust provided for an independent 3rd party, as “trust protector”

to transform each sub-trust to an accumulation trust in the protector’s sole discretion by voiding the conduit provisions ab initio.

– Trust Protector had the authority to limit the initial trust beneficiary ab initio.

– After Participant’s date of death, Trust Protector exercised “toggle” and converted one share to an accumulation trust.

– Held: Each share can use the life expectancy of its initial beneficiary to measure the MRD for that share.

66

Separate Shares – PLR 200537044

IRA Trust PLR Rulings

• Ruling 3: Payment of Expenses from IRA not considered an accumulation. – The trust provided that “Trust expenses may be deducted prior to

any such payment to or for the benefit of the beneficiary of the trust share if the deduction does not disqualify the status of the trust as a conduit trust. This paragraph may be rendered void, ab initio, by the Trust Protector. . .”

– Held: Each share can use that the life expectancy of its initial beneficiary to measure the MRD for that share.

Why? Even with the deduction for payment of trust expenses, no amounts distributed to the trust during the beneficiary’s lifetime would be accumulated in the trust, and thus would not be kept in the trust for the benefit of any future beneficiaries. Treas. Reg. § 1.401(a)(9)-5 Q&A 7(c)(3), Example 2.

67

Separate Shares – PLR 200537044

IRA Trust PLR Rulings

• Ruling 4: The trust assets of the primary beneficiary’s separate share will not be included in that beneficiary’s estate upon that beneficiary’s death. – Each trust share would accumulate the net income of the trust, and

the trustee had discretion to distribute accumulated income and principal to the primary beneficiary only for his or her health, education, maintenance and support.

– The document did not grant any beneficiary a general power of appointment over his or her share.

– Held: Upon the death of the primary beneficiary of each separate trust, the trust assets will not be included in such beneficiary’s estate.

68

Separate Shares – PLR 200537044

Two Types of Trusts

• Accumulation Trusts • Conduit Trusts

• Treas. Reg. § 1.401(a)(9)-4, Q&A 5

Requirements apply to both types

69 69

Conduit Trust

• A trust in which all distributions from the IRA are immediately distributed to the trust beneficiary/beneficiaries.

70 70

Accumulation Trust

• A trust in which distributions from the IRA are allowed to accumulate within the trust.

71 71

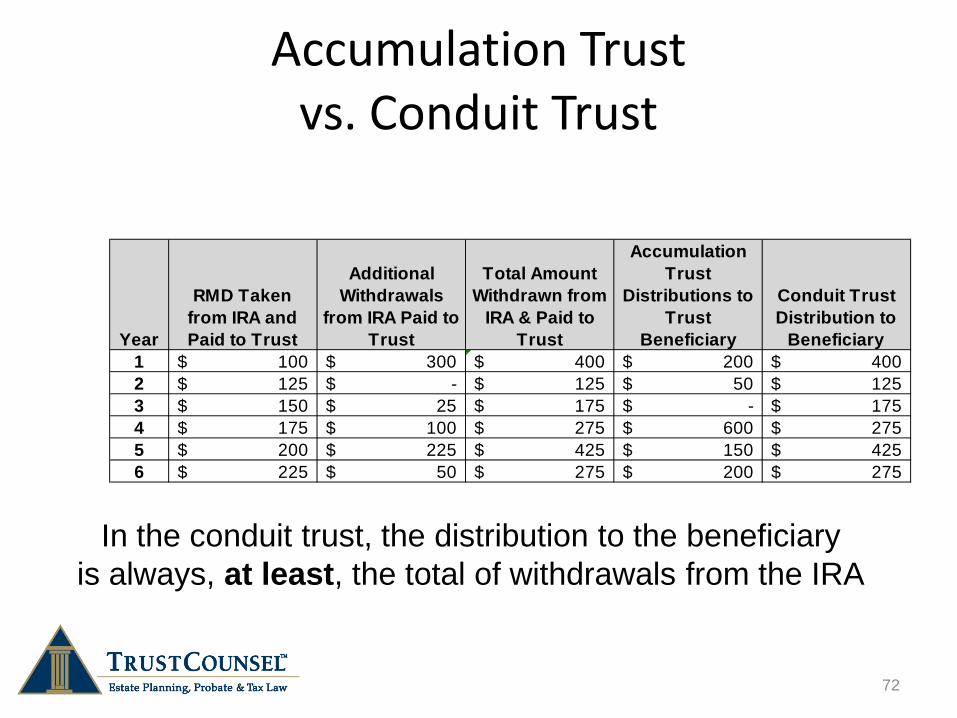

Accumulation Trust vs. Conduit Trust

Year

RMD Taken from IRA and Paid to Trust

Additional Withdrawals

from IRA Paid to Trust

Total Amount Withdrawn from

IRA & Paid to Trust

Accumulation Trust

Distributions to Trust

Beneficiary

Conduit Trust Distribution to

Beneficiary1 100$ 300$ 400$ 200$ 400$ 2 125$ -$ 125$ 50$ 125$ 3 150$ 25$ 175$ -$ 175$ 4 175$ 100$ 275$ 600$ 275$ 5 200$ 225$ 425$ 150$ 425$ 6 225$ 50$ 275$ 200$ 275$

72 72

In the conduit trust, the distribution to the beneficiary is always, at least, the total of withdrawals from the IRA

Accumulation Trust

• The key issue in analyzing an accumulation trust is to determine which beneficiaries are “countable.”

• All beneficiaries are countable unless such beneficiary is deemed to be a “mere potential successor” beneficiary.

73 73

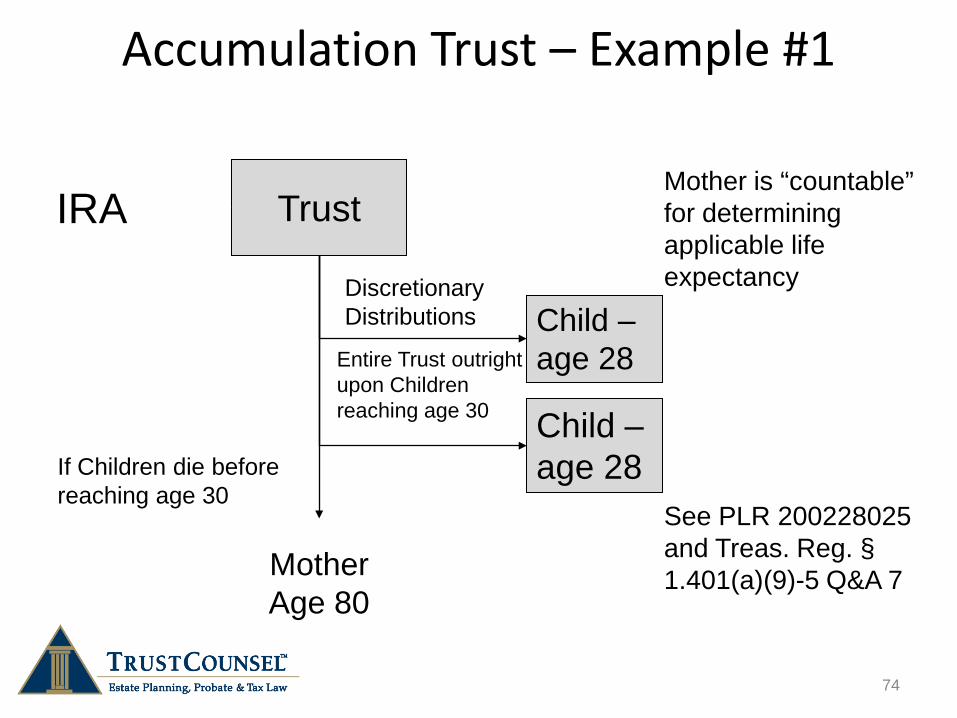

Accumulation Trust – Example #1

74 74

Mother Age 80

Trust

Discretionary Distributions

Entire Trust outright upon Children reaching age 30

If Children die before reaching age 30

Mother is “countable” for determining applicable life expectancy

See PLR 200228025 and Treas. Reg. § 1.401(a)(9)-5 Q&A 7

Child – age 28

Child – age 28

IRA

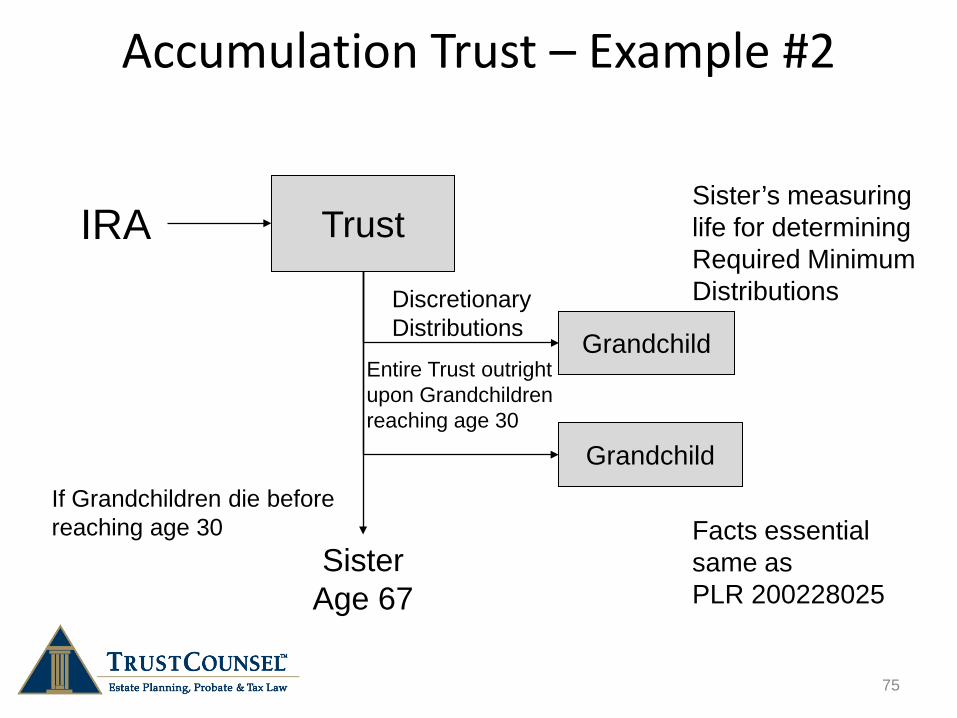

Accumulation Trust – Example #2

75 75

IRA

Sister Age 67

Grandchild

Trust

Discretionary Distributions

Grandchild

Entire Trust outright upon Grandchildren reaching age 30

If Grandchildren die before reaching age 30

Sister’s measuring life for determining Required Minimum Distributions

Facts essential same as PLR 200228025

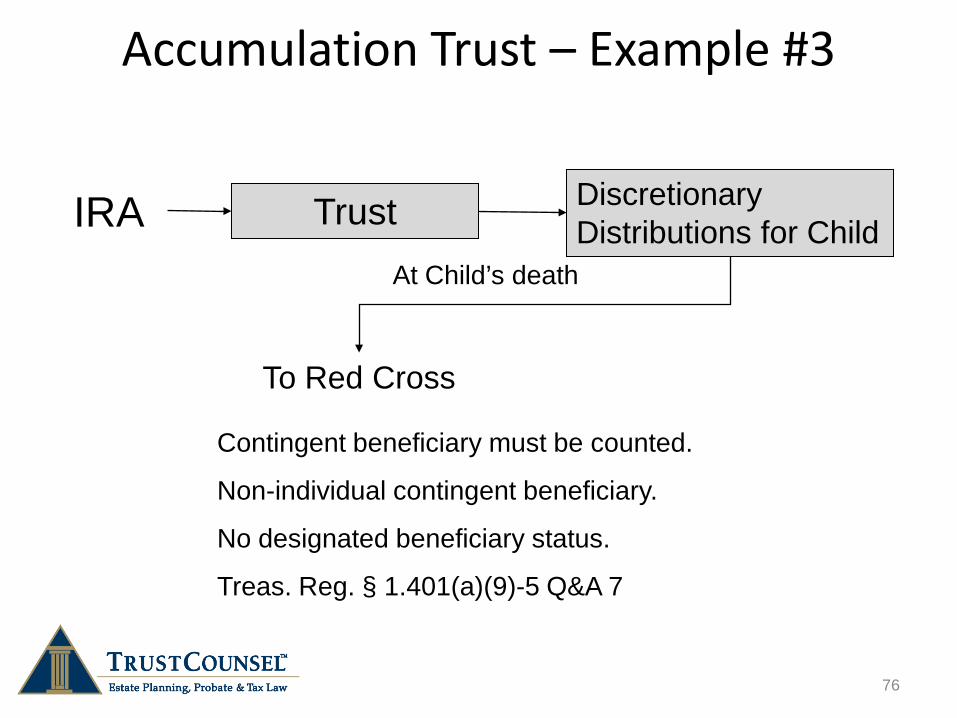

Accumulation Trust – Example #3

76 76

Trust IRA

To Red Cross

Discretionary Distributions for Child

At Child’s death

Contingent beneficiary must be counted.

Non-individual contingent beneficiary.

No designated beneficiary status.

Treas. Reg. § 1.401(a)(9)-5 Q&A 7

Conduit Trust

Allows for Easier Identification of Beneficiaries

77 77

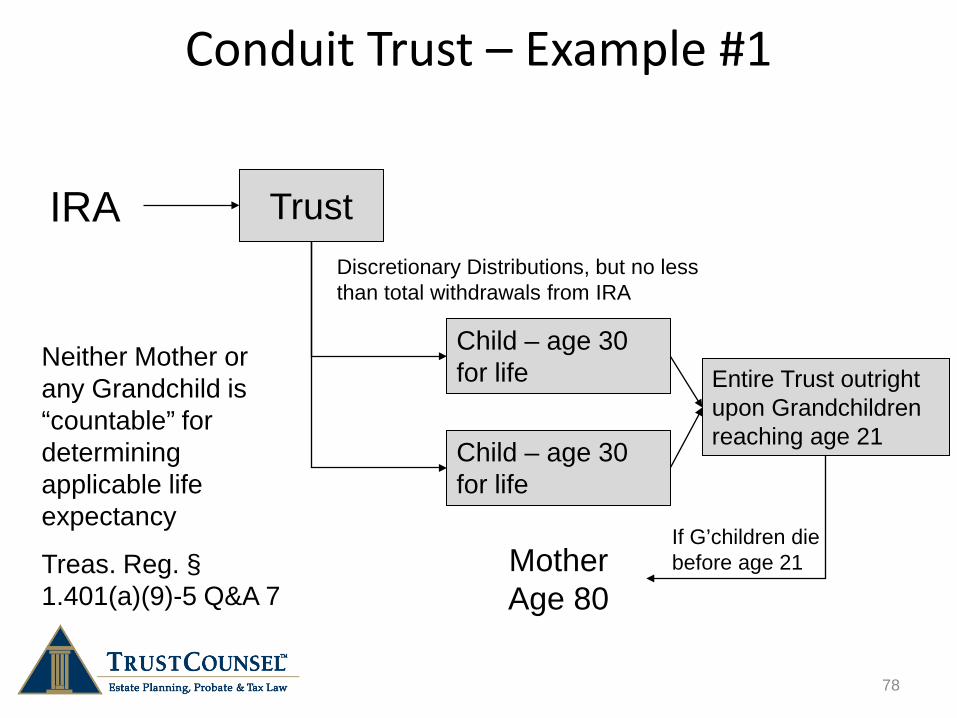

Conduit Trust – Example #1

78 78

Mother Age 80

Trust

Entire Trust outright upon Grandchildren reaching age 21

If G’children die before age 21

Neither Mother or any Grandchild is “countable” for determining applicable life expectancy

Treas. Reg. § 1.401(a)(9)-5 Q&A 7

IRA

Child – age 30 for life

Child – age 30 for life

Discretionary Distributions, but no less than total withdrawals from IRA

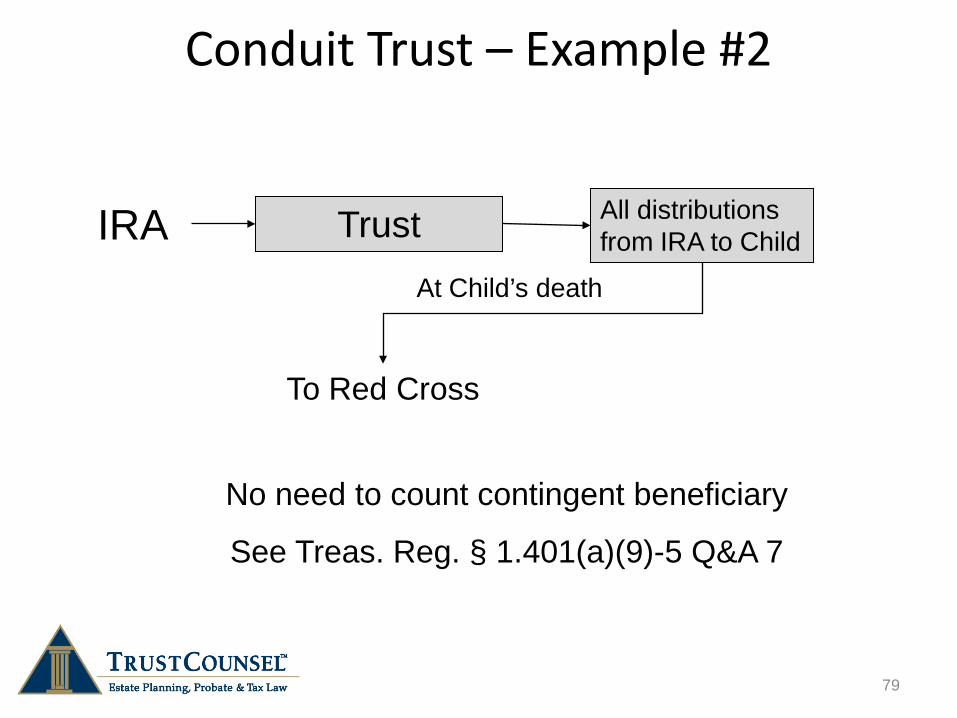

Conduit Trust – Example #2

79 79

Trust IRA

To Red Cross

All distributions from IRA to Child

At Child’s death

No need to count contingent beneficiary

See Treas. Reg. § 1.401(a)(9)-5 Q&A 7

Conduit Trust – Example #2

All distributions from the IRA are required to be distributed to the beneficiary. If Child lives to life expectancy, the entire IRA will be distributed to Child. Therefore, Child is the only “countable” beneficiary, and the Red Cross can be ignored.

80 80

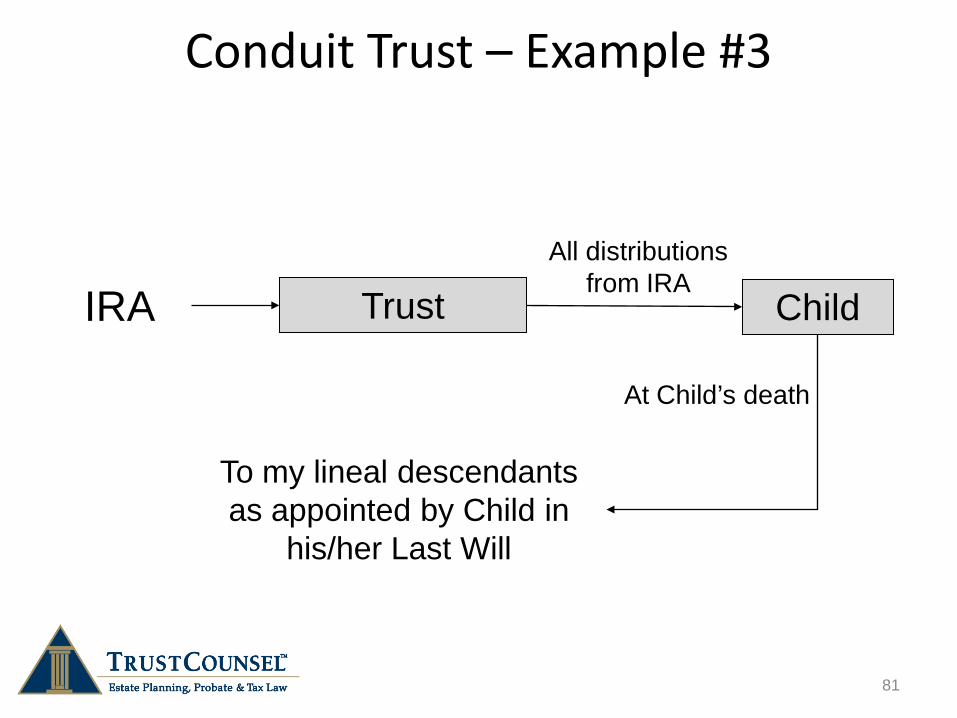

Conduit Trust – Example #3

81 81

Trust

To my lineal descendants as appointed by Child in

his/her Last Will

Child All distributions

from IRA

At Child’s death

IRA

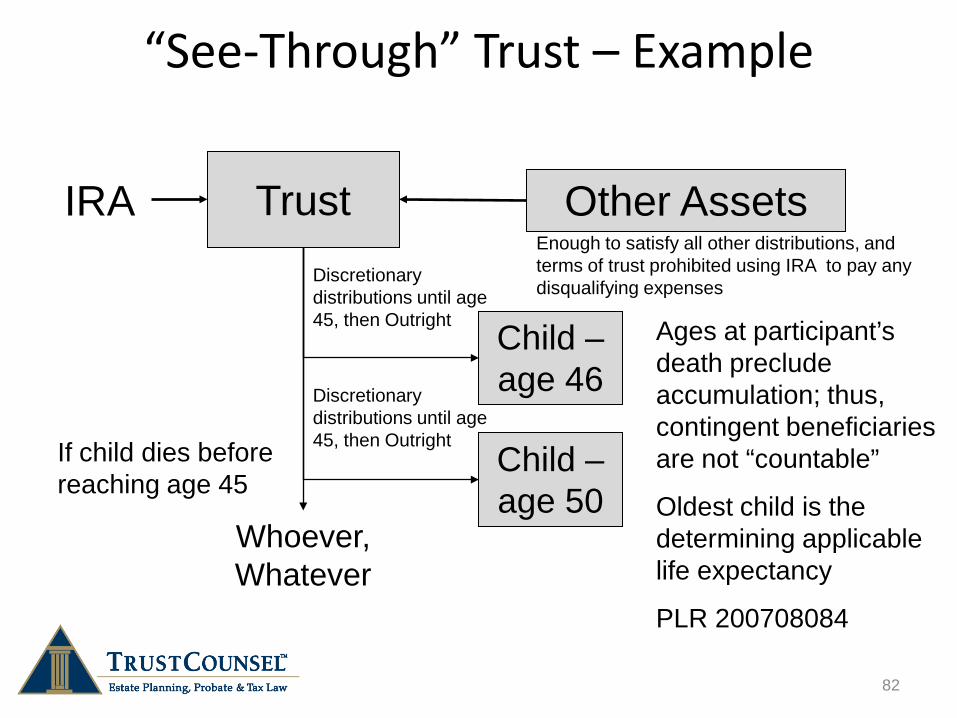

“See-Through” Trust – Example

82 82

Whoever, Whatever

Trust

Discretionary distributions until age 45, then Outright If child dies before

reaching age 45

Ages at participant’s death preclude accumulation; thus, contingent beneficiaries are not “countable”

Oldest child is the determining applicable life expectancy

PLR 200708084

IRA

Child – age 46

Child – age 50

Discretionary distributions until age 45, then Outright

Other Assets Enough to satisfy all other distributions, and terms of trust prohibited using IRA to pay any disqualifying expenses

Other Drafting Considerations

• IRA Trusts can contain Credit-Shelter and QTIP Trusts for benefit of surviving spouse

• Proper structuring of Beneficiary Designation allows disclaimer planning by spouse and other beneficiaries

• No further stretch allowed after death of spouse with regard to IRAs in CST or QTIP trusts

83

Other Drafting Considerations

• Beneficiary Designations – Custom drafted forms required to allow proper

disclaimer planning and separate share treatment • Generally – 1) spouse; 2) if spouse disclaims, IRA Trust

(for funding of CST/QTIP); and 3) if spouse is deceased, to the separate shares for descendants, per stirpes

• Children can disclaim to allow grandchildren to stretch

– Some custodians will not accept custom forms, especially for “smaller” accounts (under $500k)

84

85

Fine Tuning Use of Exemption Amount Through Disclaimer

Example: Alex dies at age 70. Spouse disclaims amount of Alex’s estate tax exemption amount to bypass trust for benefit of spouse and children

• Disclaimer must occur within nine months • Disclaimer served on IRA custodian • Disclaimer must be fractional

85

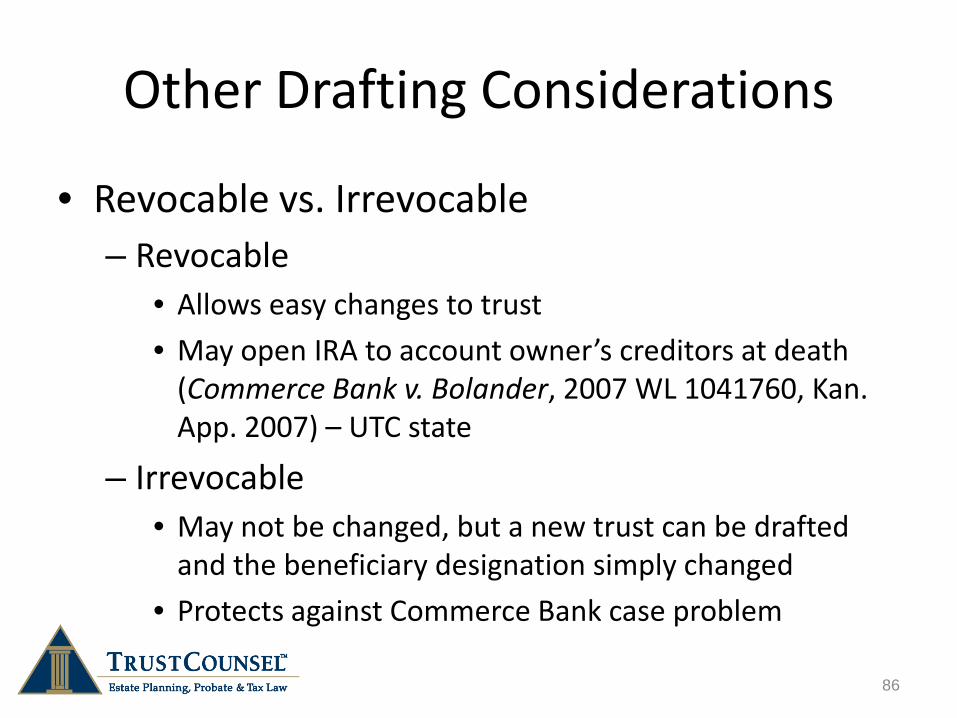

Other Drafting Considerations

• Revocable vs. Irrevocable – Revocable

• Allows easy changes to trust • May open IRA to account owner’s creditors at death

(Commerce Bank v. Bolander, 2007 WL 1041760, Kan. App. 2007) – UTC state

– Irrevocable • May not be changed, but a new trust can be drafted

and the beneficiary designation simply changed • Protects against Commerce Bank case problem

86

Resources on IRA Rules

• Life and Death Planning for Retirement Benefits by Natalie Choate 2011- 7th Ed. www.ataxplan.com

• www.irahelp.com (Ed Slott, CPA) • Robert Keebler, CPA

www.keeblerandassociates.com • IRS Publication 590

http://www.irs.gov/pub/irs-pdf/p590.pdf

87

Contact Information

Gregory Herman-Giddens, JD, LLM, TEP, CFP Attorney at Law (NC, FL, TN, NY)

Offices in North Carolina, Miami and New York City 800-201-0413

919-493-6355 (fax) [email protected]

www.trustcounselpa.com www.trustprotectorllc.com

www.ncestateplanningblog.com

88 88

Thank You for Attending!