Embed Size (px)

Citation preview

Page 1 | Proprietary and Copyrighted Information

IPSASB: Update

Angela Ryan

IPSASB Incoming Deputy Chair & Principal Accounting Adviser, New Zealand Treasury

ACCA Virtual ConferenceNovember 24th 2016

Page 2 | Proprietary and Copyrighted Information

IPSASB introduction and background:Session outline

• IPSASB development phases to date• The composition of IPSASB• Strategic Objective• High Level Look at Work Program• Structure and Governance• Momentum in IPSAS adoption• Challenges, demands and opportunities

Page 3 | Proprietary and Copyrighted Information

IPSAS development phases to date

1997 - 2001• IFAC PSC starts IPSAS development programme• First 21 IPSASs based on IASB equivalents, interpreted as necessary

2002 - 2009• Development of first public sector specific IPSASs (22 - 24)• IFRS convergence (IPSASs 25 – 32)• Start of Conceptual Framework project

2010 - 2015• Conceptual Framework completed 2014• First Time Adoption & IFRS convergence maintained (IPSASs 33-38)• First public work plan consultation

Page 4 | Proprietary and Copyrighted Information

Where do the IPSASB members come from?

Latin America/Caribbean

North America

Europe

Africa/Middle East Australasia/Oceania

Asia

Page 5 | Proprietary and Copyrighted Information

IPSASB Strategic Objective

Strengthening Public Financial Management and knowledge globally through increasing adoption of accrual-based IPSASs by:

• Developing high-quality financial reporting standards

• Developing other publications for the public sector

• Raising awareness of the IPSASs and the benefits of their adoption

Page 6 | Proprietary and Copyrighted Information

Current work programme – Emphasis on public seector specific project but also maintaining IFRS alignment

Project Public sector

specific

IFRS converge

nceSocial Benefits Revenue & Non-Exchange Expenditure Financial Instruments

Heritage

Public Sector Measurement (starting Autumn)

Infrastructure Assets (starting Autumn)

Page 7 | Proprietary and Copyrighted Information

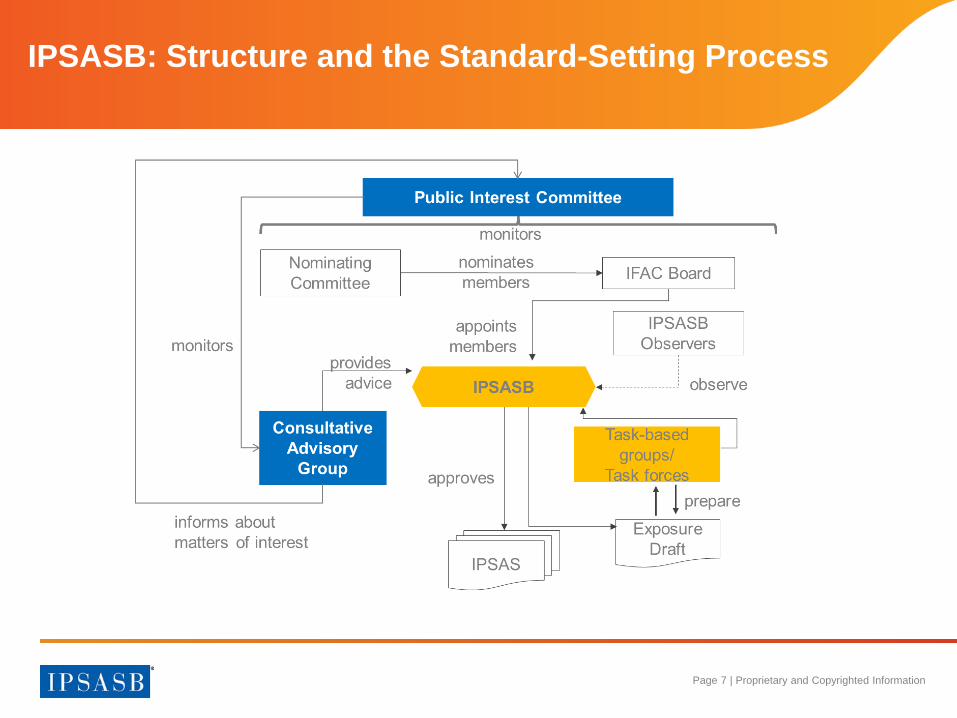

IPSASB: Structure and the Standard-Setting Process

Page 8 | Proprietary and Copyrighted Information

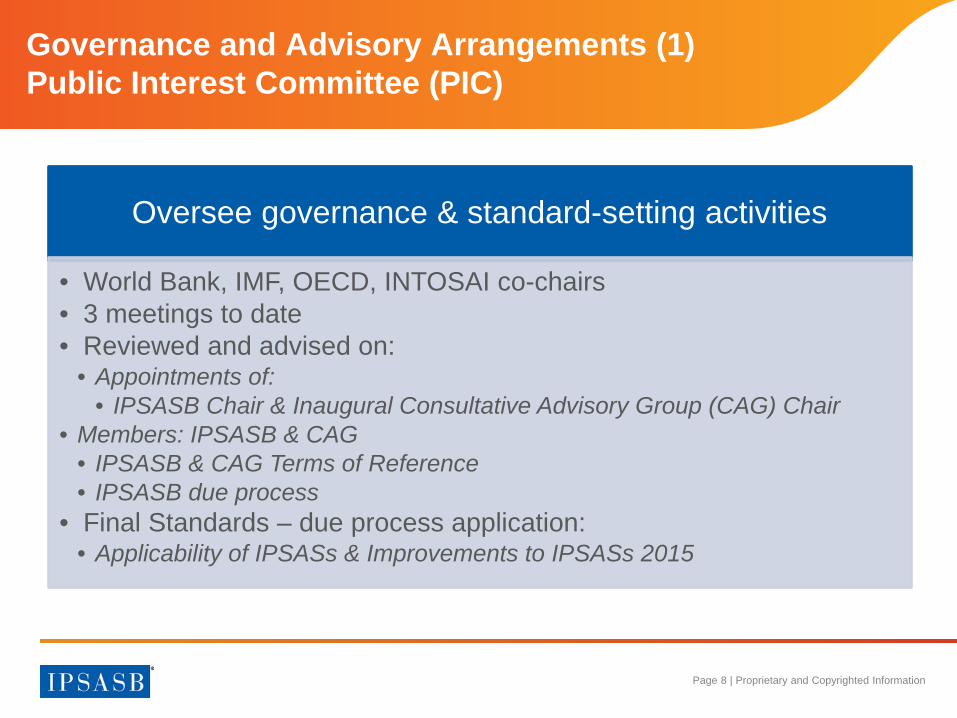

Governance and Advisory Arrangements (1)Public Interest Committee (PIC)

Oversee governance & standard-setting activities

• World Bank, IMF, OECD, INTOSAI co-chairs• 3 meetings to date• Reviewed and advised on:

• Appointments of:• IPSASB Chair & Inaugural Consultative Advisory Group (CAG) Chair

• Members: IPSASB & CAG• IPSASB & CAG Terms of Reference• IPSASB due process

• Final Standards – due process application:• Applicability of IPSASs & Improvements to IPSASs 2015

Page 9 | Proprietary and Copyrighted Information

Advise IPSASB on key project issues, strategy, work plan• Inaugural Chair & Members appointed• Composition:

• 50% – Preparers/Users• Audit organizations – Including Forum of Firms Representative • Economic development and regulatory organizations• Regulatory organizations• Professional Accountancy Bodies• Individuals

• Initial meeting: June 2016 - Toronto, Canada• Second Meeting: December 2016 – Stellenbosch, South Africa

Stronger Governance and Advisory Arrangements (2)Consultative Advisory Group (CAG)

Page 10 | Proprietary and Copyrighted Information

• Over 40 countries apply accrual IPSAS:• Directly e.g. Chile, Colombia, Austria, Estonia, Lithuania• Indirectly through National Standards e.g. South Africa, Brazil,

Indonesia, Malaysia, Spain, New Zealand

• Some apply IPSAS for lower levels of governmente.g. Prefecture of Tokyo, State of Geneva

• International organsiations reporting on IPSAS basis:Entire UN System, European Commission, OECD, NATO, Interpol

• Most countries in Latin America, and many in South East Asia, and Africa planning to adopt IPSASs

10

IPSASs: Momentum in adoption

Page 11 | Proprietary and Copyrighted Information

• Delivering the work plan:• 6 important public sector projects being developed from scratch • Technically difficult

e.g. first Social Benefits project put on hold after 6 years pending completion of Conceptual Framework

• Longer timelines due to need for stakeholder engagement (CP, ED then IPSAS)

• Building relationships with national standard setters: – Inaugural Public Sector Standard Setters Forum

• Strengthening advocacy from key international institutions – IMF, World Bank, regional development banks

• Bedding down relationships with PIC and CAG11

Challenges

Page 12 | Proprietary and Copyrighted Information

• PIC:– Deliver key projects – Social Benefits in particular– Increasing Board diversity (geography and gender balance)

• Existing and potential adopters:– Tackle long list of other potential public sector projects

e.g. sovereign powers / natural resources – Maintain IFRS convergence– Requests for adoption and implementation guidance– Expand scope to include not-for-profits?

• Potential funders:– Perceptions and clarity about IPSASB / IFAC relationship and

mechanics important12

External demands

Page 13 | Proprietary and Copyrighted Information

Opportunities

• European Public Sector Accounting Standards (EPSAS) – Active monitoring and engagement

• Growth in IPSAS Adoption– Latin America, SE Asia, Africa, Canada initial strategic question,

• 2017 = 20th Anniversary of starting IPSASs development

• Working with IFAC Accountability. Now.• Next Strategy Work Plan consultation (in

2018 for 2019 onwards?)

Page 14 | Proprietary and Copyrighted Information

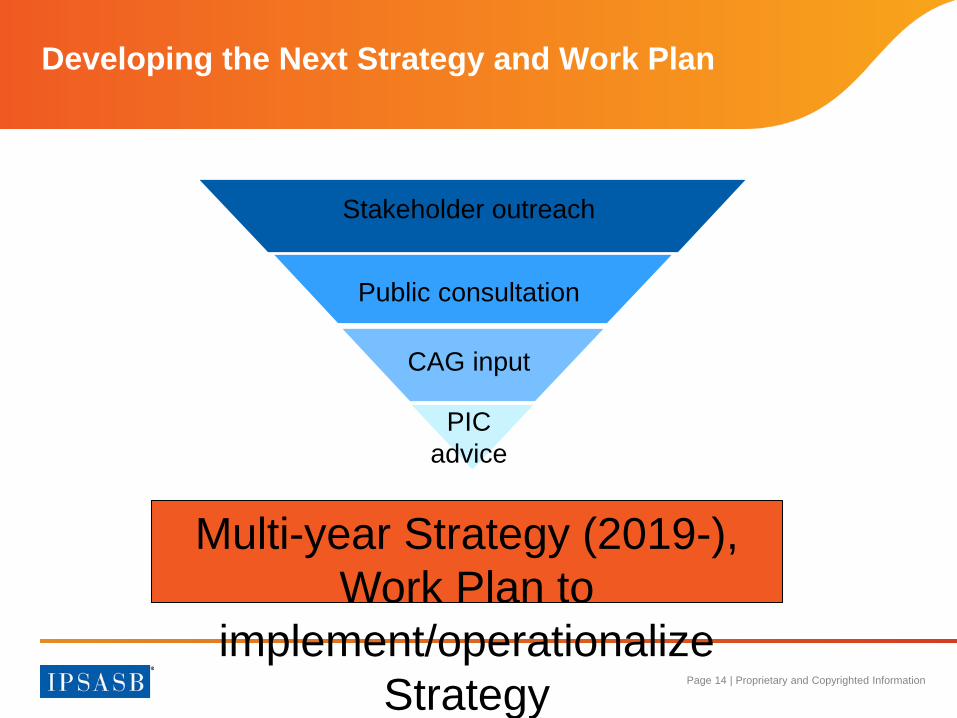

Developing the Next Strategy and Work Plan

Multi-year Strategy (2019-), Work Plan to

implement/operationalize Strategy

PIC advice

CAG input

Public consultation

Stakeholder outreach

Page 15 | Proprietary and Copyrighted Information

Questions, Discussion & Further Information

• Visit our webpage http://www.ipsasb.org/ • Or contact us by e-mail :

IPSASB Chair: [email protected] Director: [email protected]

Page 1 | Proprietary and Copyrighted Information

IPSASB Work Plan

John Stanford

Technical Director

ACCA Virtual ConferenceNovember 24th 2016

Page 2 | Proprietary and Copyrighted Information

IPSASB progress to date during 2016

Final pronouncements approved to date:• Applicability of IPSASs• Minor Improvements• Update of IPSAS 25, Employee Benefits – IPSAS 39

Consultation paper issued for comment:• Public Sector Financial Instruments – monetary authority issues (January 31st

2017

Consultation responses being analyzed:• ED 60, Public Sector Combinations (possible approval @ December meeting

- IPSAS 40?)• ED 61, Update of Cash Basis IPSAS (Limited Scope) (closed July 31st)• Consultation Paper, Accounting for Social Benefits (closed July 31st)

Page 3 | Proprietary and Copyrighted Information

Applicability of IPSASCommunicating entities for which IPSASB is developing IPSAS and RPGs

• Higher level approach recognizing role of regulators in determining financial reporting requirements for jurisdictions

• Deletion of definition of Government Business Enterprise (GBE) and supporting guidance

• Removal of statement in most IPSAS that GBEs apply IFRS• Focus on non-commercial public sector entities with explanation

and characteristics in IPSAS Preface1. Service delivery and/or income/wealth distribution2. Mainly finance of activities, directly or indirectly, by taxes,

transfers, social contributions, debt or fees3. Do not have primary profit-making objective

Page 4 | Proprietary and Copyrighted Information

IPSAS 25 / 39 – Employee Benefits update

• IPSAS 25 updated to maintain convergence with IAS19• Removal of option to defer recognition of changes in the

net defined benefit liability (the “corridor approach”)• Introduction of net interest approach for defined benefit

plans• Amendment of certain disclosure requirements for defined

benefit plans and multi-employer plans • Removal of requirements for composite social security

programs• Large number of text changes so clearer to issue new

standard - IPSAS 39 (effective 1 January 2018)

Page 5 | Proprietary and Copyrighted Information

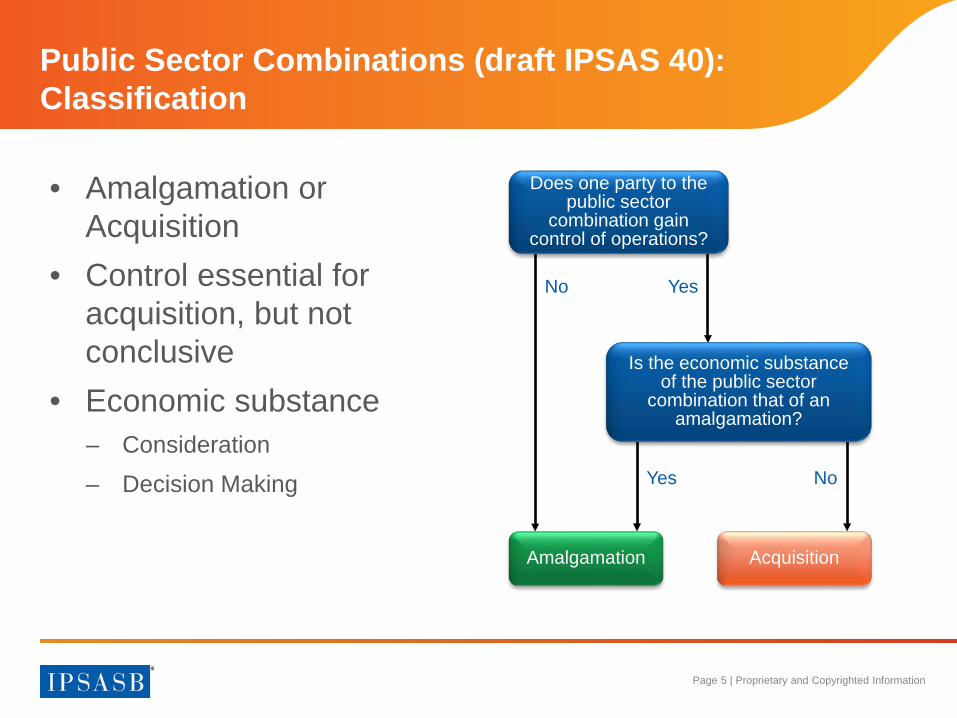

• Amalgamation or Acquisition

• Control essential for acquisition, but not conclusive

• Economic substance– Consideration– Decision Making

Public Sector Combinations (draft IPSAS 40): Classification

No Yes

NoYes

Does one party to the public sector

combination gain control of operations?

Is the economic substance of the public sector

combination that of an amalgamation?

Amalgamation Acquisition

Page 6 | Proprietary and Copyrighted Information

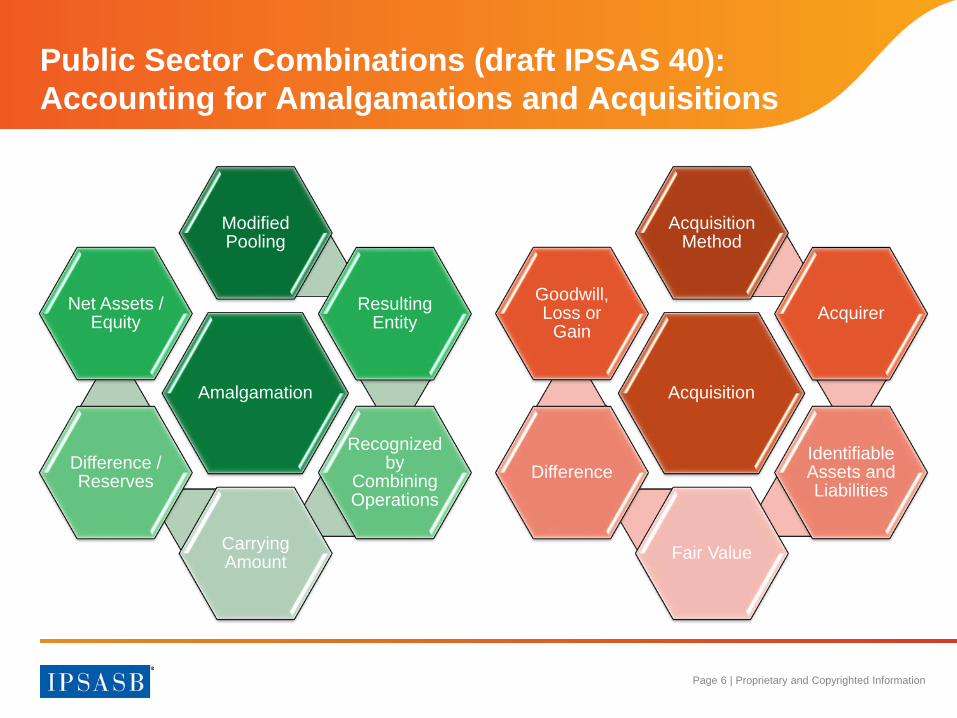

Amalgamation

Modified Pooling

Resulting Entity

Recognized by

Combining Operations

Carrying Amount

Difference / Reserves

Net Assets / Equity

Acquisition

Acquisition Method

Acquirer

Identifiable Assets and Liabilities

Fair Value

Difference

Goodwill, Loss or

Gain

Public Sector Combinations (draft IPSAS 40): Accounting for Amalgamations and Acquisitions

Page 7 | Proprietary and Copyrighted Information

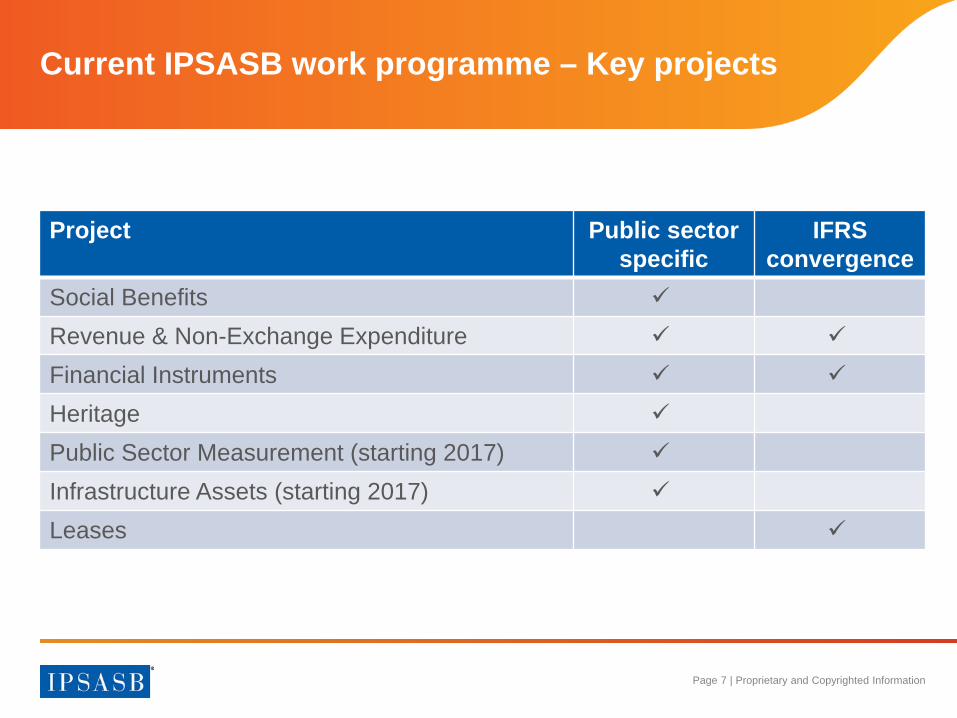

Current IPSASB work programme – Key projects

Project Public sector specific

IFRS convergence

Social Benefits

Revenue & Non-Exchange Expenditure

Financial Instruments

Heritage

Public Sector Measurement (starting 2017)

Infrastructure Assets (starting 2017)

Leases

Page 8 | Proprietary and Copyrighted Information

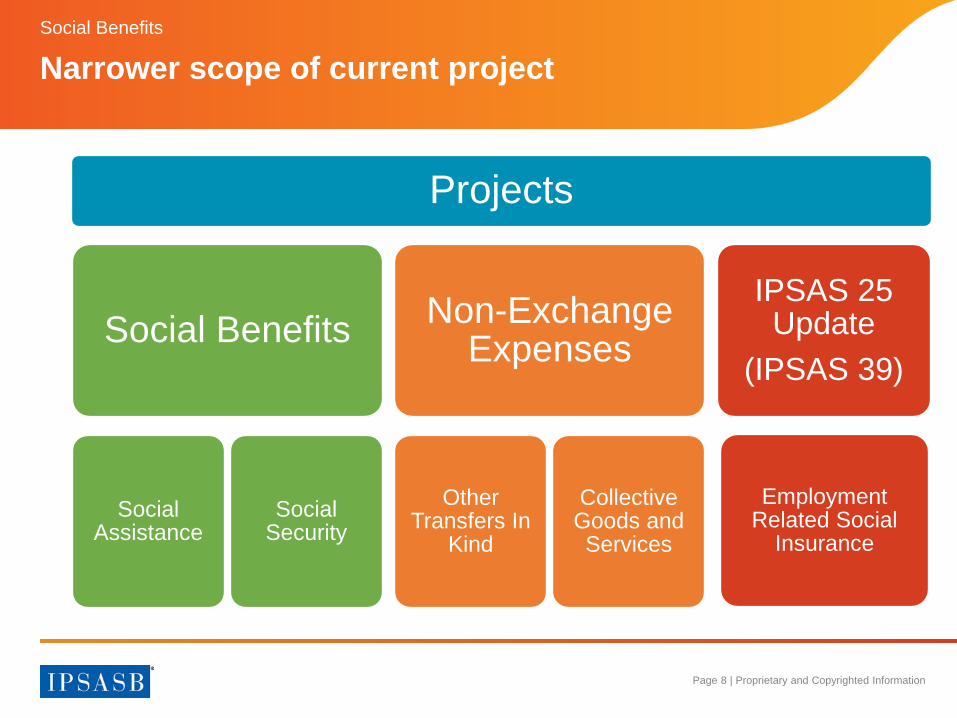

Narrower scope of current projectSocial Benefits

Projects

Social Benefits

Social Assistance

Social Security

Non-Exchange Expenses

Other Transfers In

Kind

Collective Goods and Services

IPSAS 25 Update

(IPSAS 39)

Employment Related Social

Insurance

Page 9 | Proprietary and Copyrighted Information

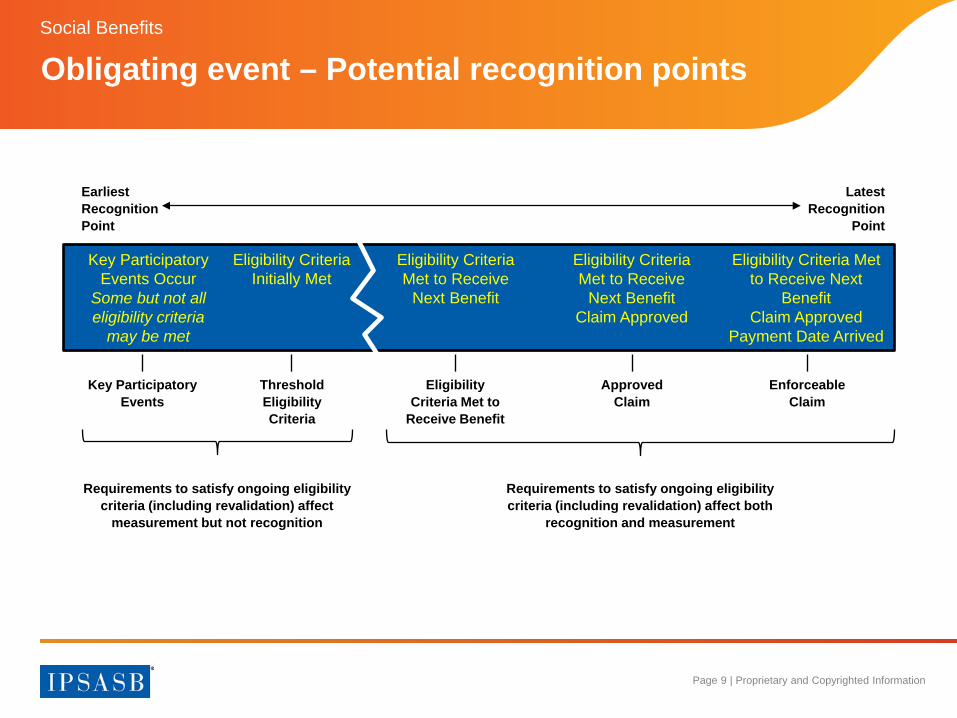

Obligating event – Potential recognition pointsSocial Benefits

Eligibility Criteria Met to Receive Next

BenefitClaim Approved

Payment Date Arrived

Eligibility Criteria Met to Receive

Next BenefitClaim Approved

Eligibility Criteria Met to Receive

Next Benefit

Eligibility Criteria Initially Met

Key Participatory Events Occur

Some but not all eligibility criteria

may be met

Key ParticipatoryEvents

Eligibility Criteria Met to

Receive Benefit

ThresholdEligibilityCriteria

ApprovedClaim

EnforceableClaim

Earliest Recognition Point

Latest Recognition

Point

Requirements to satisfy ongoing eligibility criteria (including revalidation) affect

measurement but not recognition

Requirements to satisfy ongoing eligibility criteria (including revalidation) affect both

recognition and measurement

Page 10 | Proprietary and Copyrighted Information

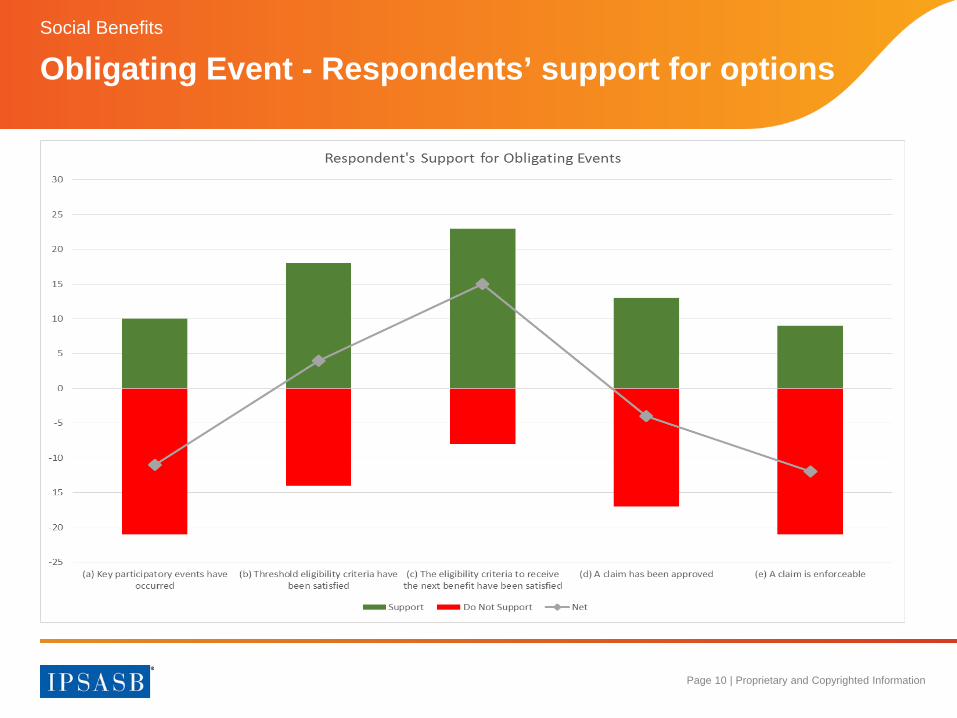

Obligating Event - Respondents’ support for optionsSocial Benefits

Page 11 | Proprietary and Copyrighted Information

Revenue and Non-Exchange Expenditure

• Current literature on Revenue– IPSAS 23 (Non-Exchange Revenue: Taxes and Transfers)– IPSAS 9 (Revenue from Exchange Transactions)– IPSAS 11 (Construction Contracts)– IFRS 15 (Revenue from Contracts with Customers)

• Assessment of extent that IFRS15 performance obligation approach can be applied to public sector revenues

• Address issues identified with application of IPSAS 23• Single CP to address need for common approach between

Non-Exchange Revenue and Expenditure (e.g. grants)

Page 12 | Proprietary and Copyrighted Information

IPSAS 23 implementation issues

• Global standard – high level Implementation Guidance on main tax types

• Deals with initial recognition not subsequent measurement Exchange/non-exchange classification

• Transfers –’lumpy grants’: – Stipulations - time requirements – Capital grants

• Options: – Stipulations - time as a condition? – ‘Other Resources’ and ‘Other Obligations’?– Disclosure

Page 13 | Proprietary and Copyrighted Information

Applying the IPSAS 15 performance based approach in the public sector

Applying a performance obligation approach to revenue and expense transactions?

Page 14 | Proprietary and Copyrighted Information

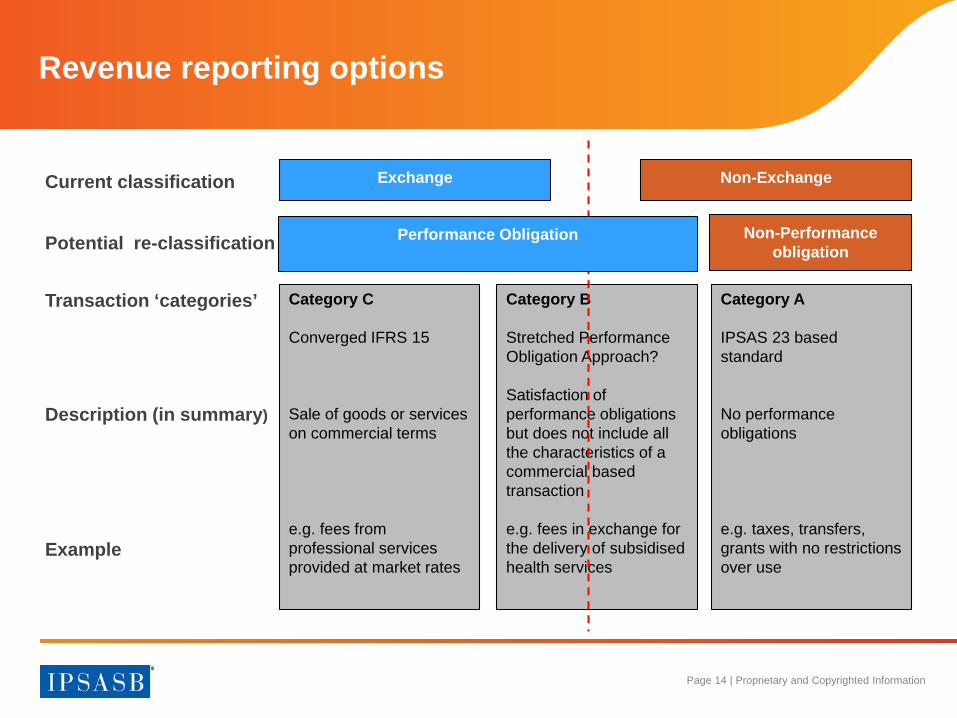

Category C

Converged IFRS 15

Sale of goods or services on commercial terms

e.g. fees from professional services provided at market rates

Category B

Stretched Performance Obligation Approach?

Satisfaction of performance obligations but does not include all the characteristics of a commercial based transaction

e.g. fees in exchange for the delivery of subsidised health services

Category A

IPSAS 23 based standard

No performance obligations

e.g. taxes, transfers, grants with no restrictions over use

Transaction ‘categories’

Current classification

Potential re-classification

Description (in summary)

Example

Non-Performance obligation

Performance Obligation

Exchange Non-Exchange

Revenue reporting options

Page 15 | Proprietary and Copyrighted Information

Non-Exchange Expenditure (1)

• No current IPSAS dealing with non-exchange expenses– Some preparers use IPSAS 19, Provisions, Contingent Liabilities &

Contingent Assets• Non-exchange expenses outside Social Benefits project:

– Collective goods and services• E,g, Defense, policing, street lighting

– Other transfers in kind• Universal education and healthcare

– Transfers and grants to other entities• Both general and specific

• Consistency / links with Social Benefits

Page 16 | Proprietary and Copyrighted Information

Non-Exchange Expenditure (2)

• Three potential approaches:– Expanded IPSAS 19 – Public sector performance obligation approach (reverse of

revenue)– IPSAS 23 Reverse

• No obligating event for Collective Goods and Services, or Other Transfers in Kind?

• Obligating event limited to transfers /grants to other entities?

Page 17 | Proprietary and Copyrighted Information

Heritage – Project overview

• Provide requirements and guidance to replace provisional guidance in IPSAS 17

• Consultation Paper as initial step• Heritage items defined• Possible items included considered using UNESCO

conventions• Discussion in terms of Conceptual Framework (CF) asset

and liability definitions• CF impact on recognition, measurement and disclosure

Page 18 | Proprietary and Copyrighted Information

Heritage – Potential Preliminary Views

• Special characteristics do not prevent Heritage items meeting definition of asset in CF

• Should be recognised in Statement of Financial Position if meet CF recognition criteria

• Historical cost, replacement cost, restoration cost and market value could all be appropriate measurement bases

• Special characteristics do not of themselves give rise to liabilities

• Presentation requirements to hold entity accountable and help decision making (e.g. on allocations)

Page 19 | Proprietary and Copyrighted Information

Leases

• Existing IPSAS 13 based on IAS 17• IFRS convergence project – responding to new IFRS 16• Changes lessee recognition model• More on balance sheet – fiscal impact? • No change not an option – mixed groups• Public Sector needs symmetry between lessee and lessor

accounting – lessor / lessee arrangements common e.g. property

• Current Board view that IFRS 16 lessor accounting inappropriate for public sector: other models under consideration including right of use model

Page 20 | Proprietary and Copyrighted Information

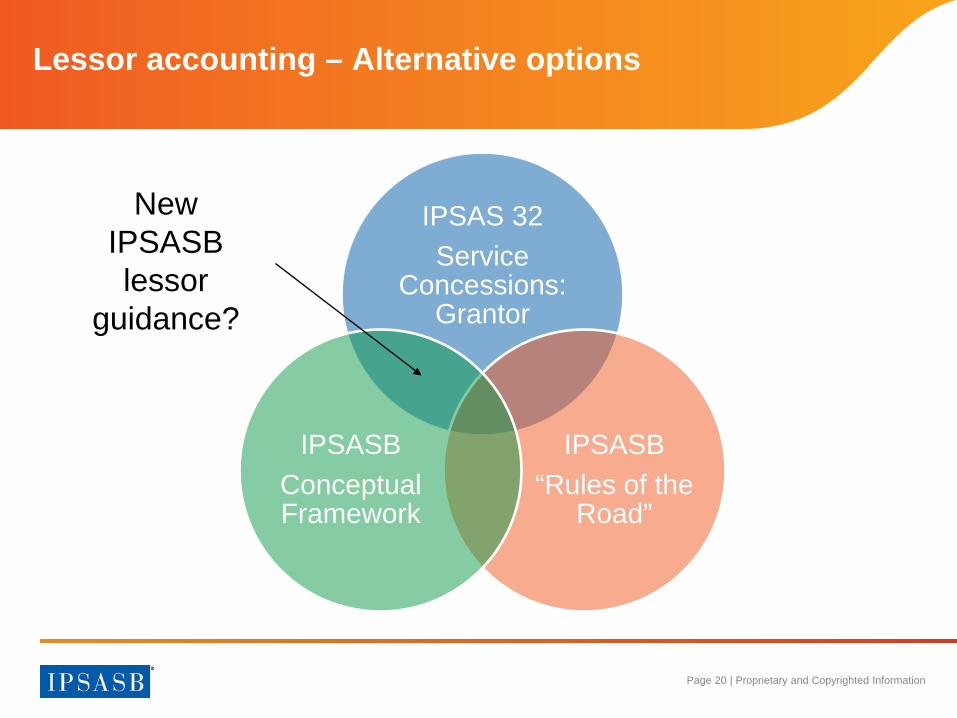

Lessor Accounting—Context of Development of Options

Lessor accounting – Alternative options

IPSAS 32Service

Concessions: Grantor

IPSASB“Rules of the

Road”

IPSASBConceptual Framework

New IPSASBlessor

guidance?

Page 21 | Proprietary and Copyrighted Information

Public Sector Specific• Monetary authority

issues (often central bank)

• Monetary gold• Notes and coins in

circulation• IMF Quotas• IMF Special Drawing

Rights

Update of IPSAS 28-30• Need top reflect IFRS 9• Initial Measurement• Classification

– Subsequent Measurement

• Impairment– Expected Loss Model

• Hedging

Financial Instruments-Two projects

Page 22 | Proprietary and Copyrighted Information

Questions, discussion & further information

• Visit our webpage http://www.ipsasb.org/ • Or contact us by e-mail :

IPSASB Chair: [email protected] Director: [email protected]