Embed Size (px)

Citation preview

IPCC Paper 4: TaxationChapter 4

CA. Naveen Rajpurohit

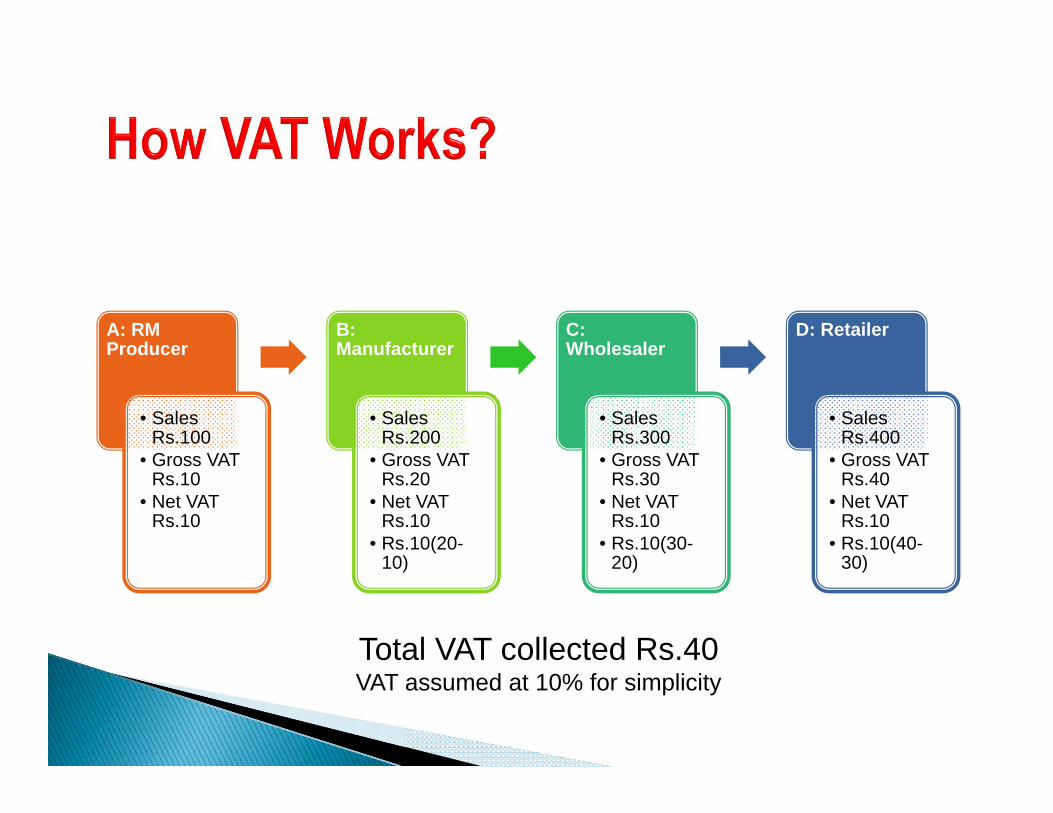

How VAT Works? Historical Background VAT variants Computation Method VAT merits and demerits VAT - Indian Context

A: RM Producer

• Sales Rs.100

• Gross VAT Rs.10

• Net VAT Rs.10

B: Manufacturer

• Sales Rs.200

• Gross VAT Rs.20

• Net VAT Rs.10

• Rs.10(20-10)

C: Wholesaler

• Sales Rs.300

• Gross VAT Rs.30

• Net VAT Rs.10

• Rs.10(30-20)

D: Retailer

• Sales Rs.400

• Gross VAT Rs.40

• Net VAT Rs.10

• Rs.10(40-30)

Total VAT collected Rs.40VAT assumed at 10% for simplicity

An Intro.

First proposed by Dr. Wilhelm Von Siemens for Germany in 1919

In 1921, VAT was suggested by Prof Thomas S Adams for USA

This was also recommended by the Shoup Mission for the reconstruction of the Japanese Economy in 1949

However, France was the first Country to adopt VAT in 1954

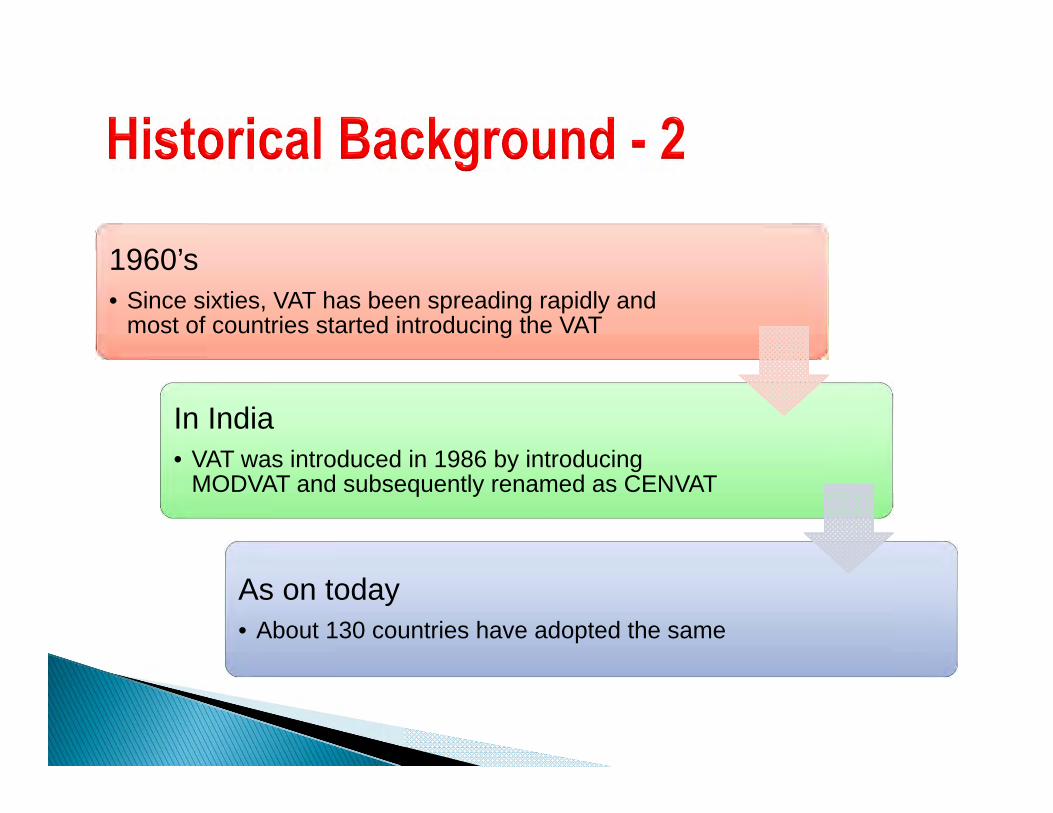

1960’s• Since sixties, VAT has been spreading rapidly and

most of countries started introducing the VAT

In India• VAT was introduced in 1986 by introducing

MODVAT and subsequently renamed as CENVAT

As on today• About 130 countries have adopted the same

VAT not adopted in pure form in most countries

Multiple tax rates prevalent

Differential rates for necessities and luxury goods

Peak rate of tax in Europe - 25%, Asia - 35%

Lowest rate in Singapore – 5%

VAT replaces sales tax, excise duty and service tax

Many countries have a negative list of commodities which are not under VAT

Many countries have special treatment of levying tax by way of composite scheme for small dealers

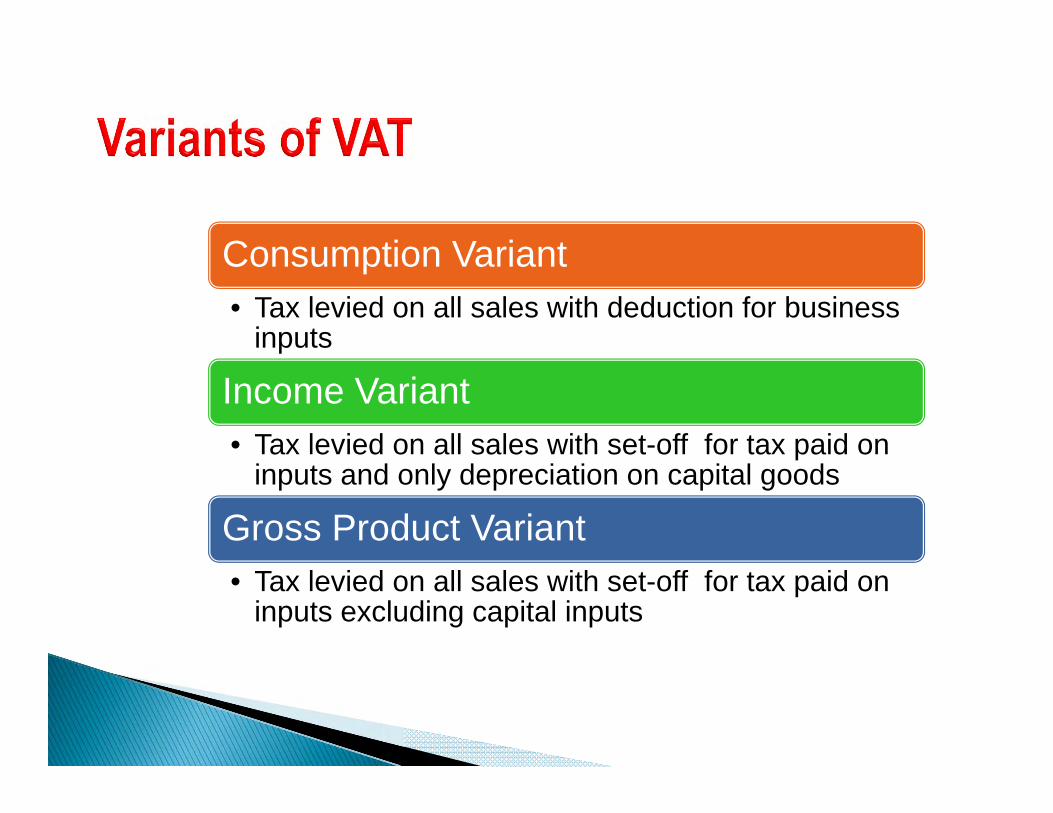

VAT Variants

Consumption

IncomeGross Production

Consumption Variant• Tax levied on all sales with deduction for business

inputs

Income Variant• Tax levied on all sales with set-off for tax paid on

inputs and only depreciation on capital goods

Gross Product Variant• Tax levied on all sales with set-off for tax paid on

inputs excluding capital inputs

An Intro.

Commonly Used

Methods

Addition Method • Aggregating all the

factor payments and profit;

Invoice Method • Deducting tax on

inputs from tax on sales;

Subtraction Method• Direct Subtraction

Method• Intermediate

Method

Other Methods

Direct Subtraction method• Deducting aggregate

value of purchase exclusive of tax from the aggregate value of sales exclusive of tax

Intermediate Subtraction method• Deducting tax inclusive

value of purchases from the sales and taxing difference between them

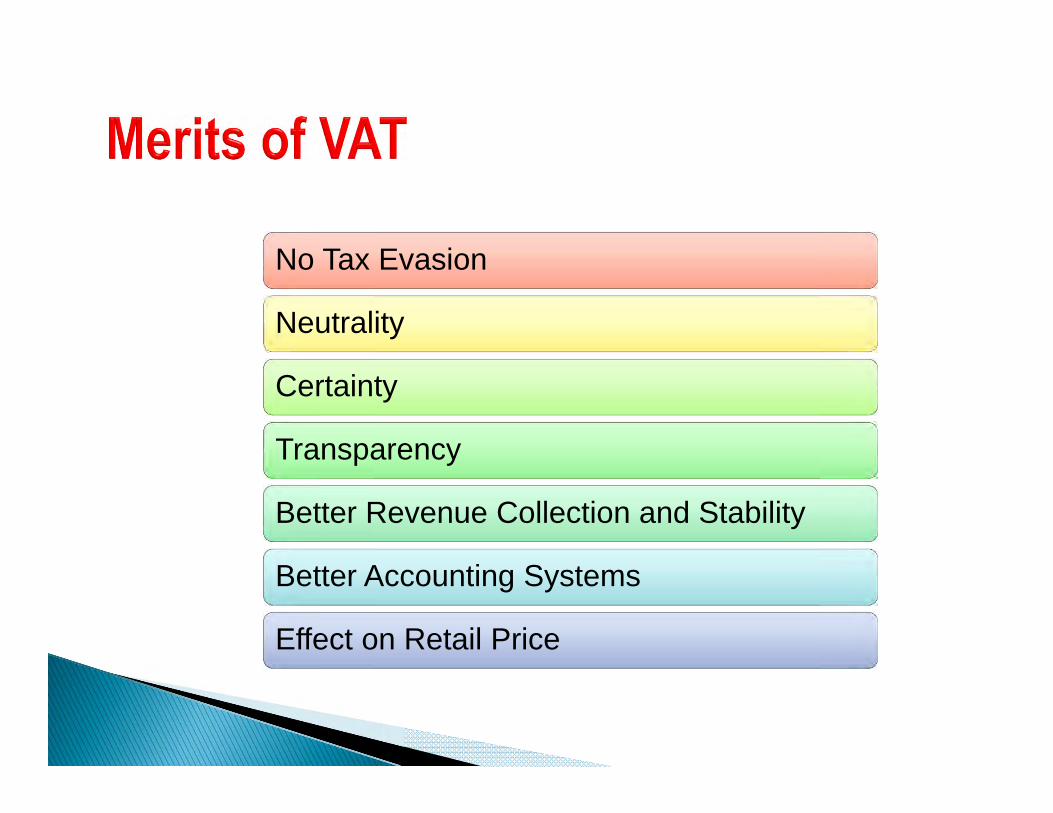

No Tax Evasion

Neutrality

Certainty

Transparency

Better Revenue Collection and Stability

Better Accounting Systems

Effect on Retail Price

The merits accrue in full measure provided there is only one VAT rate and applicable to all commodities

In federal structure like India, so long as all the taxes are not integrated, it will be difficult to put the purchases from other States at par with the State purchases

The cost of maintaining accounts will increase

VAT is regressive since it is charged on the end consumer on all goods including necessities

Since it is payable at all stage – it would increase the working capital requirements and the interest burden on the same;

Administration cost to the State will also increase as the number of dealers to be administered will go up significantly

An Intro.

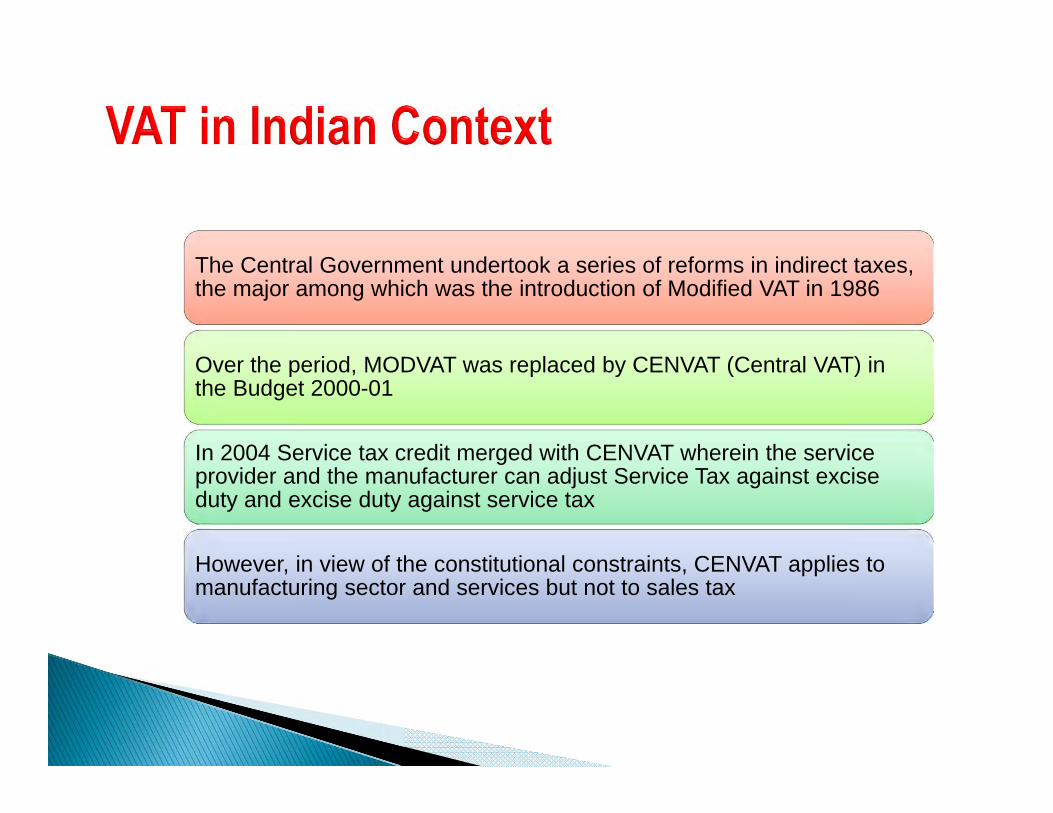

The Central Government undertook a series of reforms in indirect taxes, the major among which was the introduction of Modified VAT in 1986

Over the period, MODVAT was replaced by CENVAT (Central VAT) in the Budget 2000-01

In 2004 Service tax credit merged with CENVAT wherein the service provider and the manufacturer can adjust Service Tax against excise duty and excise duty against service tax

However, in view of the constitutional constraints, CENVAT applies to manufacturing sector and services but not to sales tax

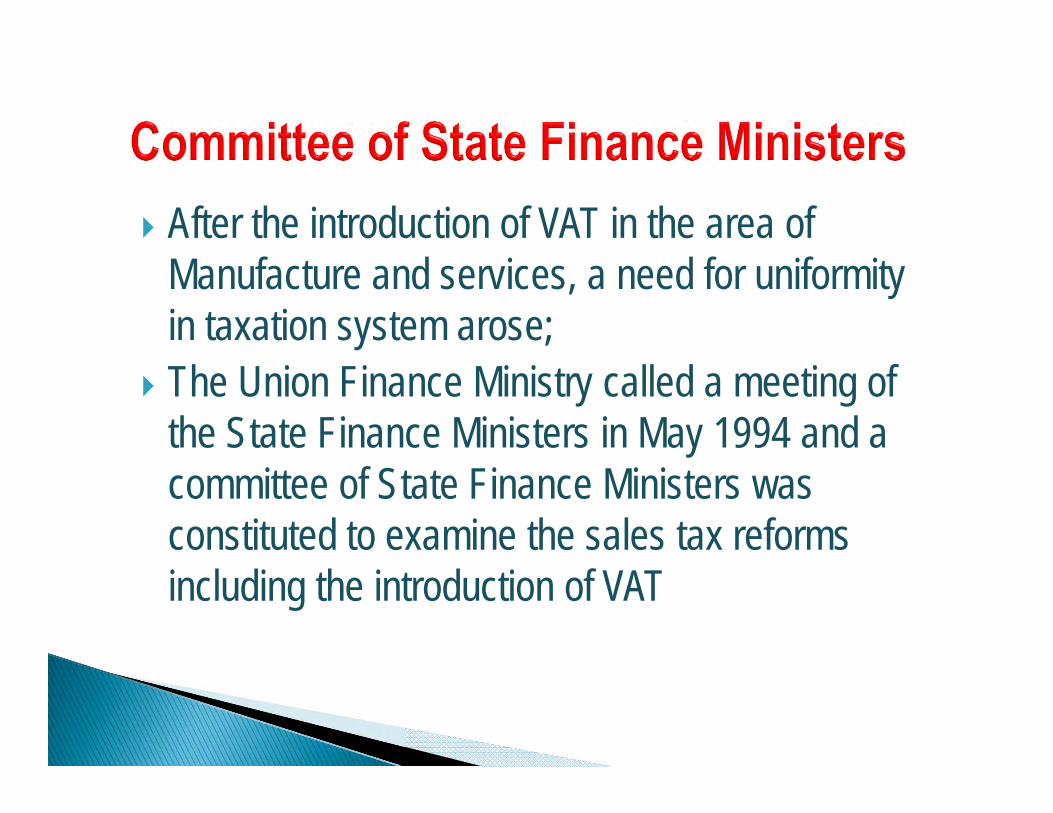

After the introduction of VAT in the area of Manufacture and services, a need for uniformity in taxation system arose;

The Union Finance Ministry called a meeting of the State Finance Ministers in May 1994 and a committee of State Finance Ministers was constituted to examine the sales tax reforms including the introduction of VAT

The committee has recommended:◦ Four general floor rates (0, 4, 8 & 12) and two special

floor rates (1 & 20);◦ Keeping exemption to minimum;◦ Preparing the list of exempt goods;◦ Done away with the sales tax incentives for industries

For implementing the above decisions, an empowered committee of State Finance Ministers was set up.

Brought out a white paper on 17.01.2005 which provided a base for the preparation of various State VAT legislation. Broadly the White Paper consists of the following:◦ Justification of VAT and background;◦ Design of State-Level VAT;◦ Steps taken by the States

In the white paper the more importance is given for ‘self-assessment’ and ‘audit’.

Record Keeping Tax Planning Negotiation with Suppliers to reduce price Handling the Audit by Departmental Officers External Audit for VAT records

VAT was first introduced in Haryana in 2003; Majority of the States implemented the VAT in 2005; As on date, all the States are under VAT regime; Discontinuance of the CST law – by reducing the

rates from 4% to 3%, 2% and 1% GST – likely to be implemented from 2013.

The legislature passed this Act under its powers available to it vide Entry 54, List II of the Seventh Schedule to the Constitution which reads:◦ “Taxes on sale or purchase of goods other than

newspaper, subject to the provisions of Entry 92 A of List I of the Seventh Schedule”

The legislative powers is inter-alia subject to restrictions and conditions relating to sales vide Article 286(1) and 286(2) of the Constitution of India read section 3, 4, 14, & 15

Article 286(1) speaks about the restriction on the State to impose Tax on:◦ Sale outside State◦ Import or Export

Article 286(2) speaks about the formulation of principle in the above cases.

Goods and Service Tax - It means any tax on supply ofgoods or services or both except taxes on the supply offollowing goods namely: Petroleum crude, High speed diesel, Petrol, Natural gas,

Aviation turbine fuel, Alcoholic liquor for human consumption Major indirect tax law at both Central and State level will

be subsumed with GST Will have three laws – CGST, SGST and IGST