Embed Size (px)

Citation preview

IP Valuation Methods – Income Approach (2/2)

Recap of yesterday’s session – Introduction to DCF Methodologies

3© 2017

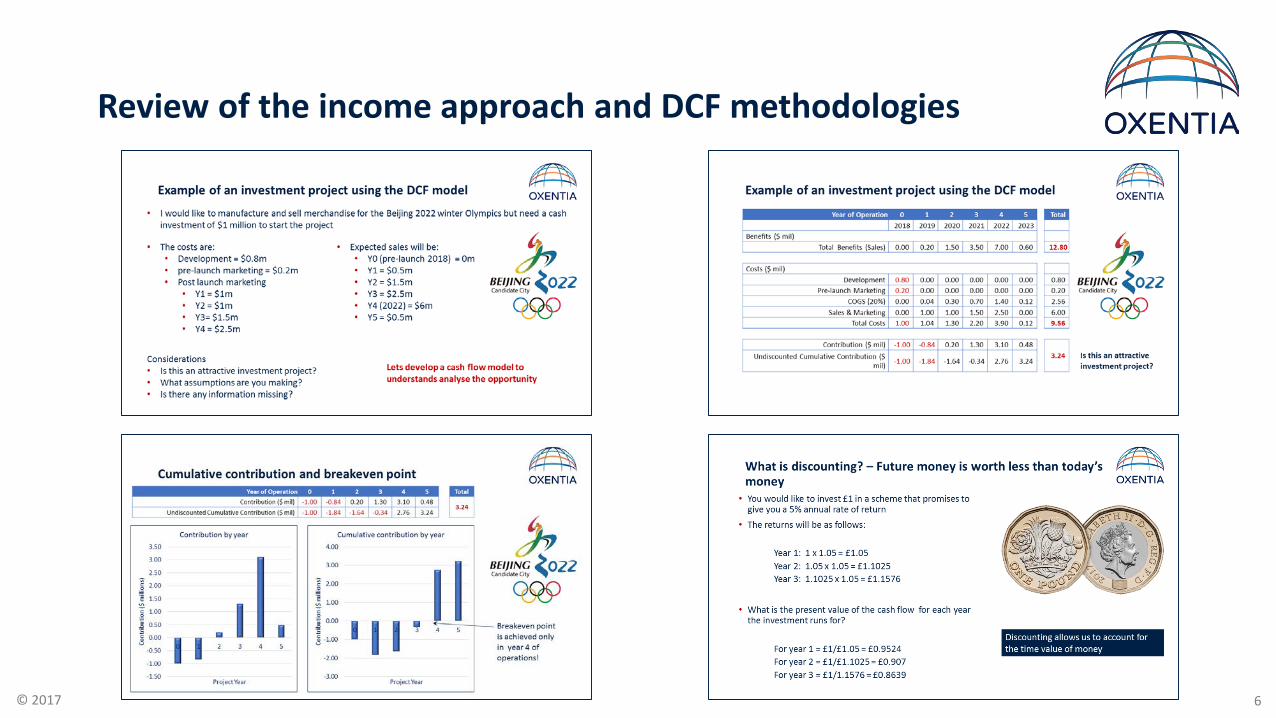

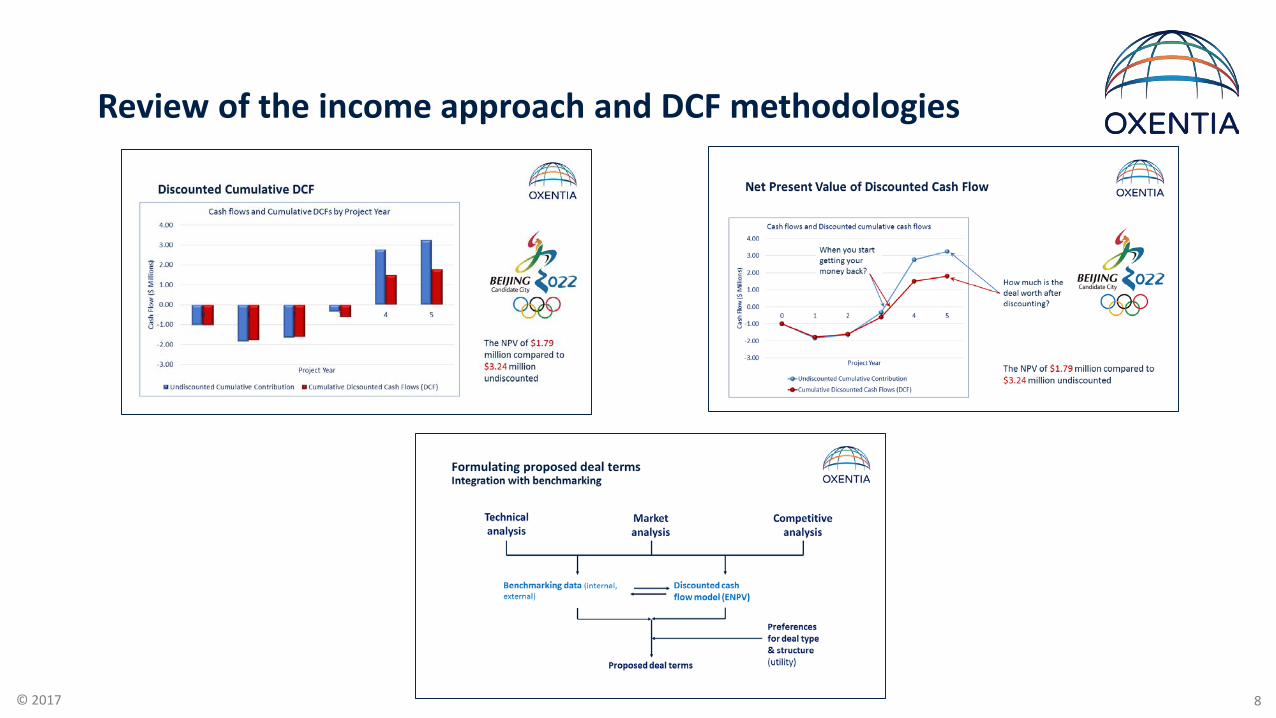

Review of the income approach and DCF methodologies

4© 2017

Review of the income approach and DCF methodologies

5© 2017

Review of the income approach and DCF methodologies

6© 2017

Review of the income approach and DCF methodologies

7© 2017

Review of the income approach and DCF methodologies

8© 2017

Review of the income approach and DCF methodologies

9© 2017

Formulating proposed deal termsIntegration with benchmarking

Discounted cash flow model (NPV)

Benchmarking data (internal, external)

Proposed deal terms

Preferences for deal type & structure(utility)

Marketanalysis

Technicalanalysis

Competitiveanalysis

10© 2017

• Can we improve our DCF model by making

better assumptions for:

• Sales projections

• Cost Of Goods sold (COGS)

• Sales & Marketing (S&M)

• General and Administrative costs

(G&A)

• How do we account for development risk?

• Success/Attrition rates

Image source: uscibooks.com

11© 2017

Learning Outcomes

• Refining the DCF model to refine assumptions:

• Adjusting for development risk

• Defining the development process for your technology

• Understanding the probability of success (attrition rate)

• Developing a risk adjusted DCF model

• Calculating an Expected Net present Value

• Understand the Internal rate of return (IRR) and how it is used in valuation of assets

12© 2017

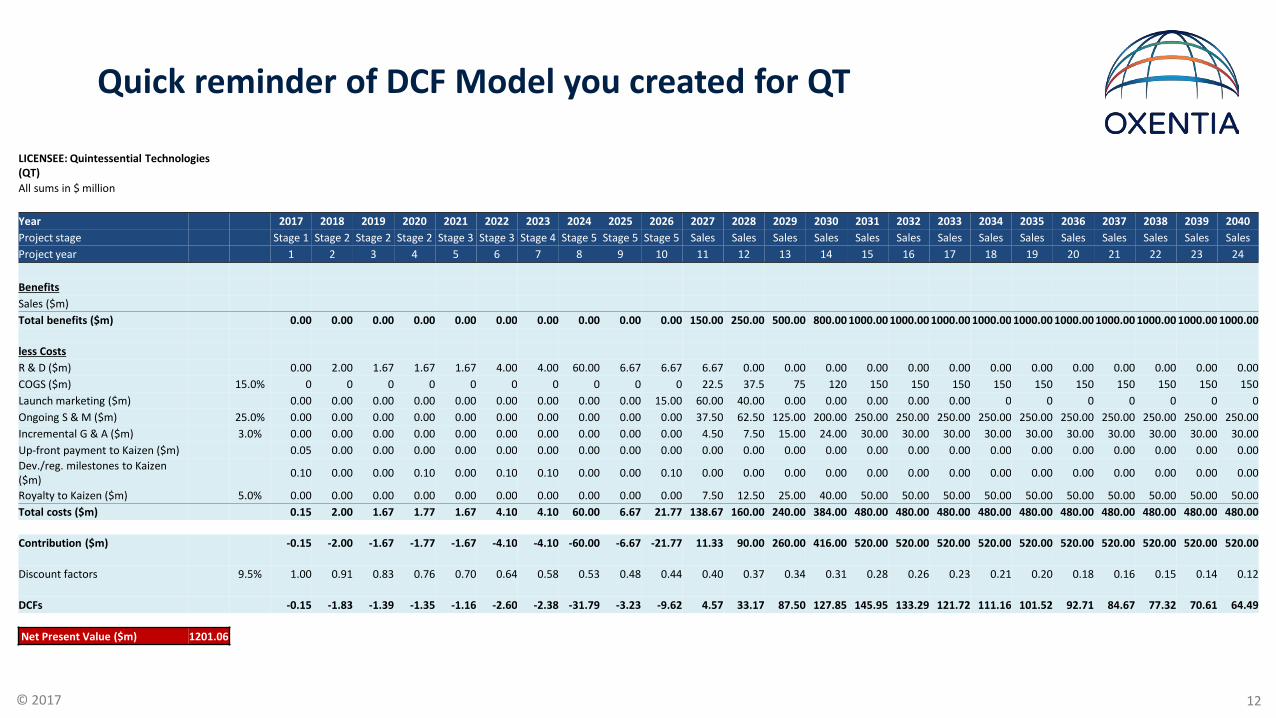

Quick reminder of DCF Model you created for QT

LICENSEE: Quintessential Technologies (QT)All sums in $ million

Year 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040Project stage Stage 1 Stage 2 Stage 2 Stage 2 Stage 3 Stage 3 Stage 4 Stage 5 Stage 5 Stage 5 Sales Sales Sales Sales Sales Sales Sales Sales Sales Sales Sales Sales Sales SalesProject year 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

BenefitsSales ($m)Total benefits ($m) 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 150.00 250.00 500.00 800.00 1000.00 1000.00 1000.00 1000.00 1000.00 1000.00 1000.00 1000.00 1000.00 1000.00

less CostsR & D ($m) 0.00 2.00 1.67 1.67 1.67 4.00 4.00 60.00 6.67 6.67 6.67 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00COGS ($m) 15.0% 0 0 0 0 0 0 0 0 0 0 22.5 37.5 75 120 150 150 150 150 150 150 150 150 150 150Launch marketing ($m) 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 15.00 60.00 40.00 0.00 0.00 0.00 0.00 0.00 0 0 0 0 0 0 0Ongoing S & M ($m) 25.0% 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 37.50 62.50 125.00 200.00 250.00 250.00 250.00 250.00 250.00 250.00 250.00 250.00 250.00 250.00Incremental G & A ($m) 3.0% 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 4.50 7.50 15.00 24.00 30.00 30.00 30.00 30.00 30.00 30.00 30.00 30.00 30.00 30.00Up-front payment to Kaizen ($m) 0.05 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00Dev./reg. milestones to Kaizen ($m) 0.10 0.00 0.00 0.10 0.00 0.10 0.10 0.00 0.00 0.10 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Royalty to Kaizen ($m) 5.0% 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 7.50 12.50 25.00 40.00 50.00 50.00 50.00 50.00 50.00 50.00 50.00 50.00 50.00 50.00Total costs ($m) 0.15 2.00 1.67 1.77 1.67 4.10 4.10 60.00 6.67 21.77 138.67 160.00 240.00 384.00 480.00 480.00 480.00 480.00 480.00 480.00 480.00 480.00 480.00 480.00

Contribution ($m) -0.15 -2.00 -1.67 -1.77 -1.67 -4.10 -4.10 -60.00 -6.67 -21.77 11.33 90.00 260.00 416.00 520.00 520.00 520.00 520.00 520.00 520.00 520.00 520.00 520.00 520.00

Discount factors 9.5% 1.00 0.91 0.83 0.76 0.70 0.64 0.58 0.53 0.48 0.44 0.40 0.37 0.34 0.31 0.28 0.26 0.23 0.21 0.20 0.18 0.16 0.15 0.14 0.12

DCFs -0.15 -1.83 -1.39 -1.35 -1.16 -2.60 -2.38 -31.79 -3.23 -9.62 4.57 33.17 87.50 127.85 145.95 133.29 121.72 111.16 101.52 92.71 84.67 77.32 70.61 64.49

Net Present Value ($m) 1201.06

13© 2017

Quick reminder of DCF Model you created for QB

-100.00

0.00

100.00

200.00

300.00

400.00

500.00

600.00

2017 2020 2023 2026 2029 2032 2035 2038

Cont

ribut

ion

($ M

illio

ns)

Year

Contributions and DCFs for IP-1 technology – Licensee’s Perspective

Contribution (£m) DCFs (£m)

Do we have reasonable assumptions for these DCF values?

14© 2017

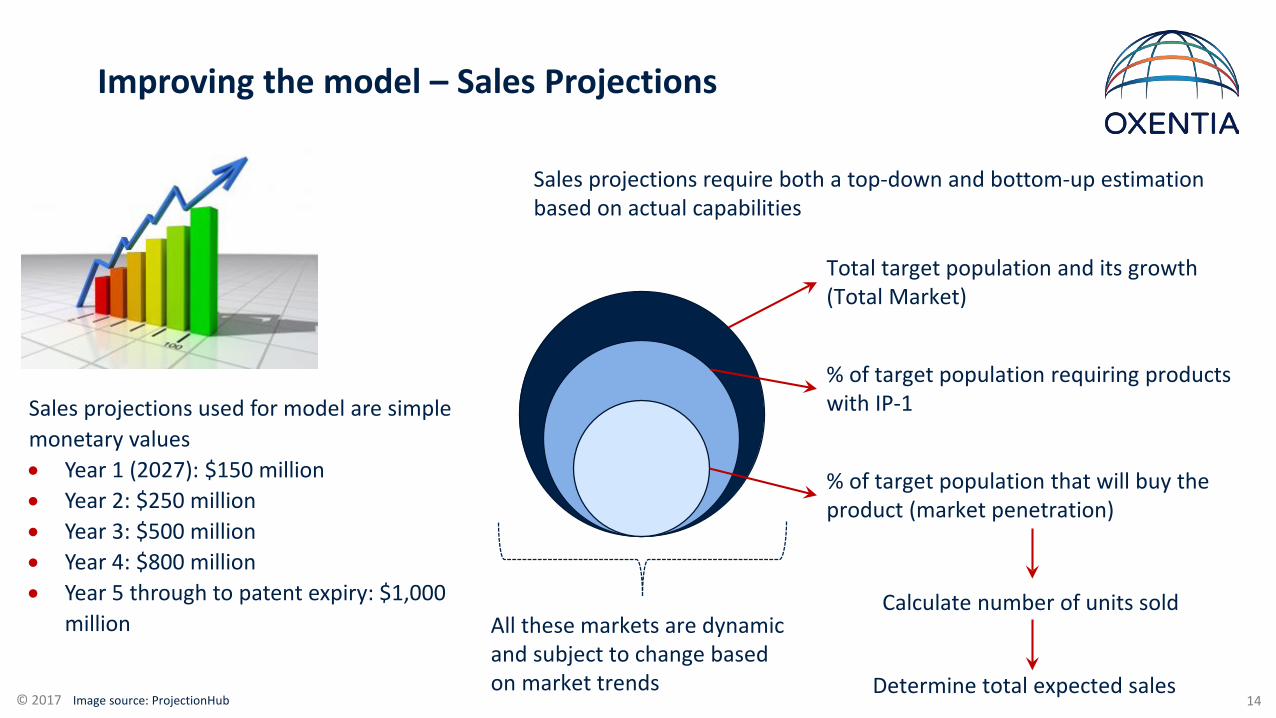

Improving the model – Sales Projections

Image source: ProjectionHub

Sales projections used for model are simple monetary values• Year 1 (2027): $150 million• Year 2: $250 million• Year 3: $500 million• Year 4: $800 million• Year 5 through to patent expiry: $1,000

million

Sales projections require both a top-down and bottom-up estimation based on actual capabilities

% of target population that will buy the product (market penetration)

Total target population and its growth (Total Market)

% of target population requiring products with IP-1

Calculate number of units sold

Determine total expected sales

All these markets are dynamic and subject to change based on market trends

15© 2017

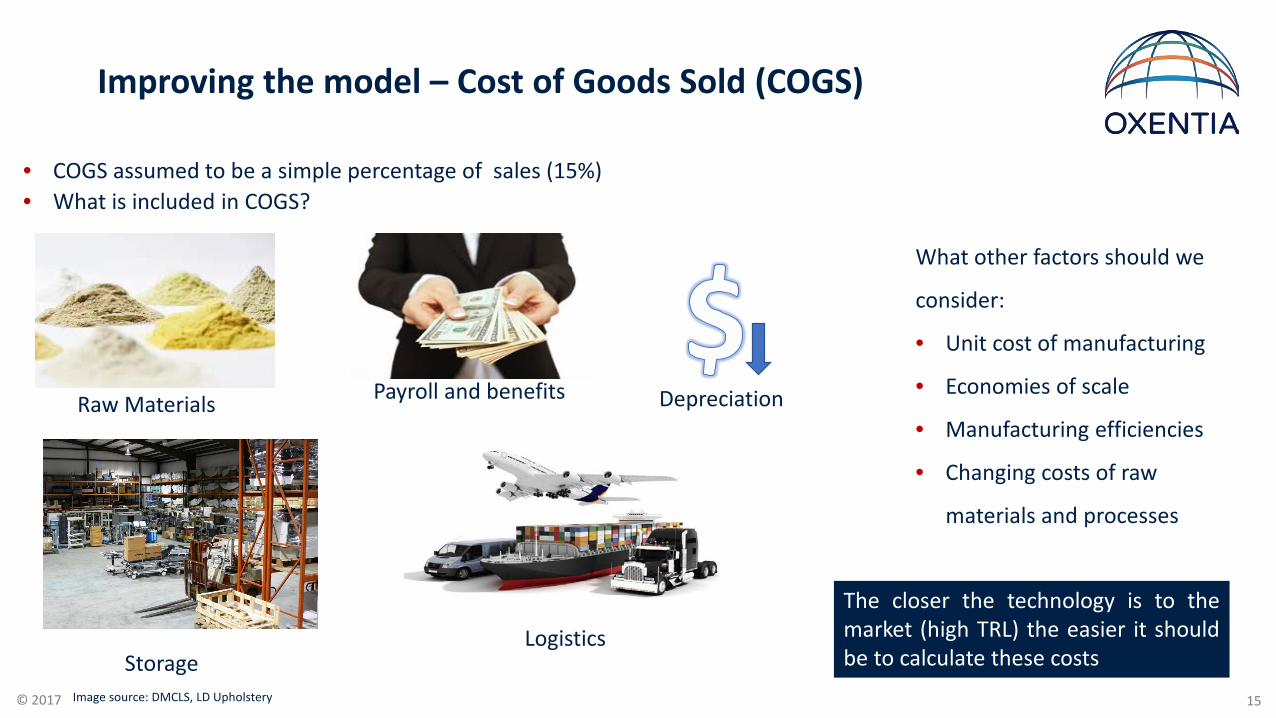

Improving the model – Cost of Goods Sold (COGS)

Image source: DMCLS, LD Upholstery

• COGS assumed to be a simple percentage of sales (15%)• What is included in COGS?

Payroll and benefitsRaw Materials

LogisticsStorage

Depreciation

What other factors should we

consider:

• Unit cost of manufacturing

• Economies of scale

• Manufacturing efficiencies

• Changing costs of raw

materials and processes

The closer the technology is to themarket (high TRL) the easier it shouldbe to calculate these costs

16© 2017

Improving the model – S&M and G&A Costs

Image source: Alternatives.ie, Andrea Umbach

• The model estimates S&M costs to equal 25% of sales

• Would S&M be higher pre-launch or in the first years

of sales?

• What if S&M costs were for B2C instead of B2B?

Sales and Marketing (S&M) General and Administrative

• The model estimates G&A costs to equal 3% of sales

• What is included?

• patent costs, admin support, operating costs

(office space and equipment), other assets?

• What can the licensee truly justify as a G&A cost?

17© 2017

Adjusting for Risk

18© 2017

Developmental product valuationDCF models and ENPV calculation

Risk-adjustedDiscounted Cash Flow (DCF) model

Project Expected Net Present (ENPV)

Marketanalysis

Technicalanalysis

Competitiveanalysis

19© 2017

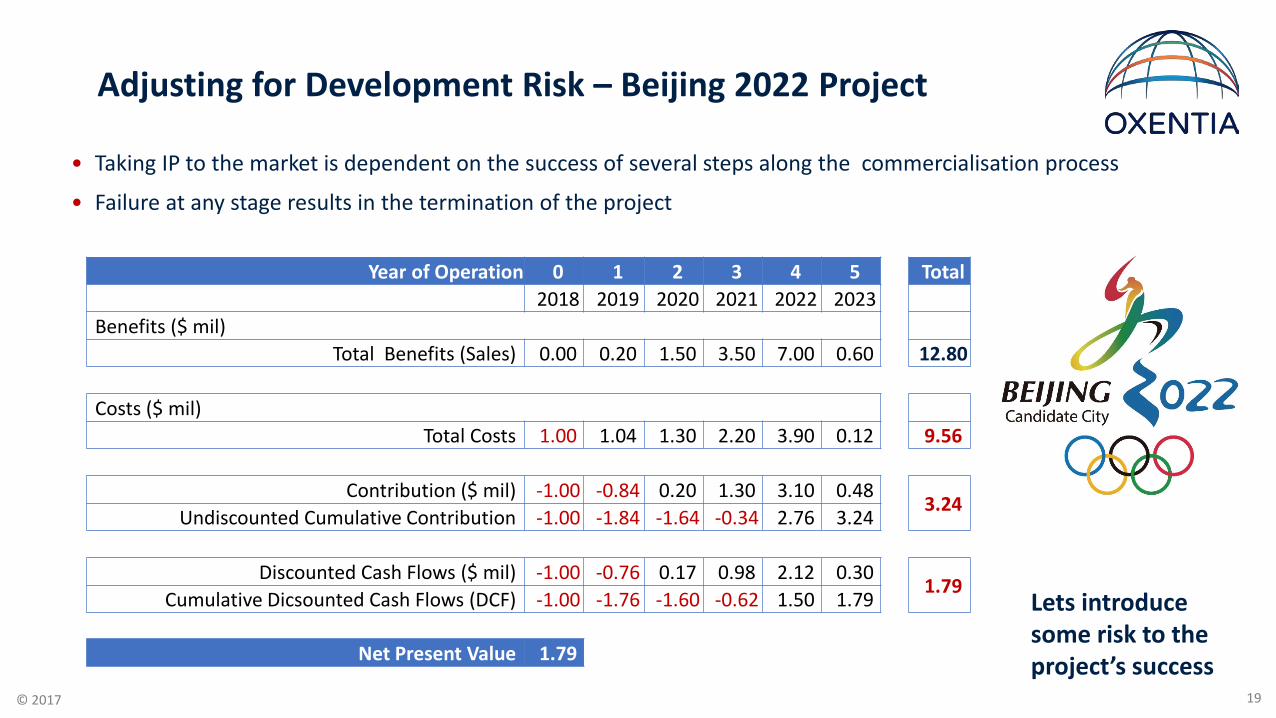

Adjusting for Development Risk – Beijing 2022 Project

• Taking IP to the market is dependent on the success of several steps along the commercialisation process

• Failure at any stage results in the termination of the project

Year of Operation 0 1 2 3 4 5 Total2018 2019 2020 2021 2022 2023

Benefits ($ mil)Total Benefits (Sales) 0.00 0.20 1.50 3.50 7.00 0.60 12.80

Costs ($ mil)Total Costs 1.00 1.04 1.30 2.20 3.90 0.12 9.56

Contribution ($ mil) -1.00 -0.84 0.20 1.30 3.10 0.483.24

Undiscounted Cumulative Contribution -1.00 -1.84 -1.64 -0.34 2.76 3.24

Discounted Cash Flows ($ mil) -1.00 -0.76 0.17 0.98 2.12 0.301.79

Cumulative Dicsounted Cash Flows (DCF) -1.00 -1.76 -1.60 -0.62 1.50 1.79

Net Present Value 1.79

Lets introduce some risk to the project’s success

20© 2017

Adjusting for Development Risk – Beijing 2022 Project

• The project requires $1 million cash investment

• What if the project had a 70% probability of success in the year before sales begin and also falls to 50% chance of success the year after the tournament

• This risk can be built into a risk-adjusted DCF (raDCF) model

• In a similar way to NPV calculations, the sum of all raDCFs for the project horizon yields the Expected Net Present Value (ENPV)

Year 02018

12019

22020

32021

42022

52023

-$1 million

Sales

Project Failure

70%

30%

Sales

Project Terminated

50%

50%

21© 2017

Year of Operation 0 1 2 3 4 5 Total2018 2019 2020 2021 2022 2023

Benefits ($ mil)Total Benefits (Sales) 0.00 0.20 1.50 3.50 7.00 0.60 12.80

Costs ($ mil)Total Costs 1.00 1.04 1.30 2.20 3.90 0.12 9.56

Contribution ($ mil) -1.00 -0.84 0.20 1.30 3.10 0.48 3.24Undiscounted Cumulative Contribution -1.00 -1.84 -1.64 -0.34 2.76 3.24

Probability of success 100% 70% 70% 70% 70% 50%risk adjusted contribution -1.00 -1.29 -1.15 -0.24 1.93 1.62

Discounted Cash Flows ($ mil) -1.00 -0.76 0.17 0.98 2.12 0.30 1.79

risk adjusted DCF (raDCF) -1.00 -1.17 -0.95 -0.18 1.32 1.01 -0.97cumulative raDCF -1.00 -2.17 -3.12 -3.30 -1.98 -0.97

Expected Net Present Value (ENPV) -0.97

Adjusting for Development Risk – Beijing 2022 Project

Undiscounted = $3.24 milNPV = $1.79 mil

ENPV = $-0.97 mil

22© 2017

Risk Adjustment for Multi-stage Development Projects

• Commercialisation of technologies typically involves multiple sequential stages

• Each stage has its own timescale, cost and risk

Phase I Phase II Phase III Registration

Fail

60%

40%

Fail

35%

65%

Fail

62%

38%

Fail

90%

10%

Fail

70%

30%

Sales (< 12%)

Data from Tufts Center for the Study of Drug Development (2014)

Development steps in a human therapeutic drug candidate project.

23© 2017

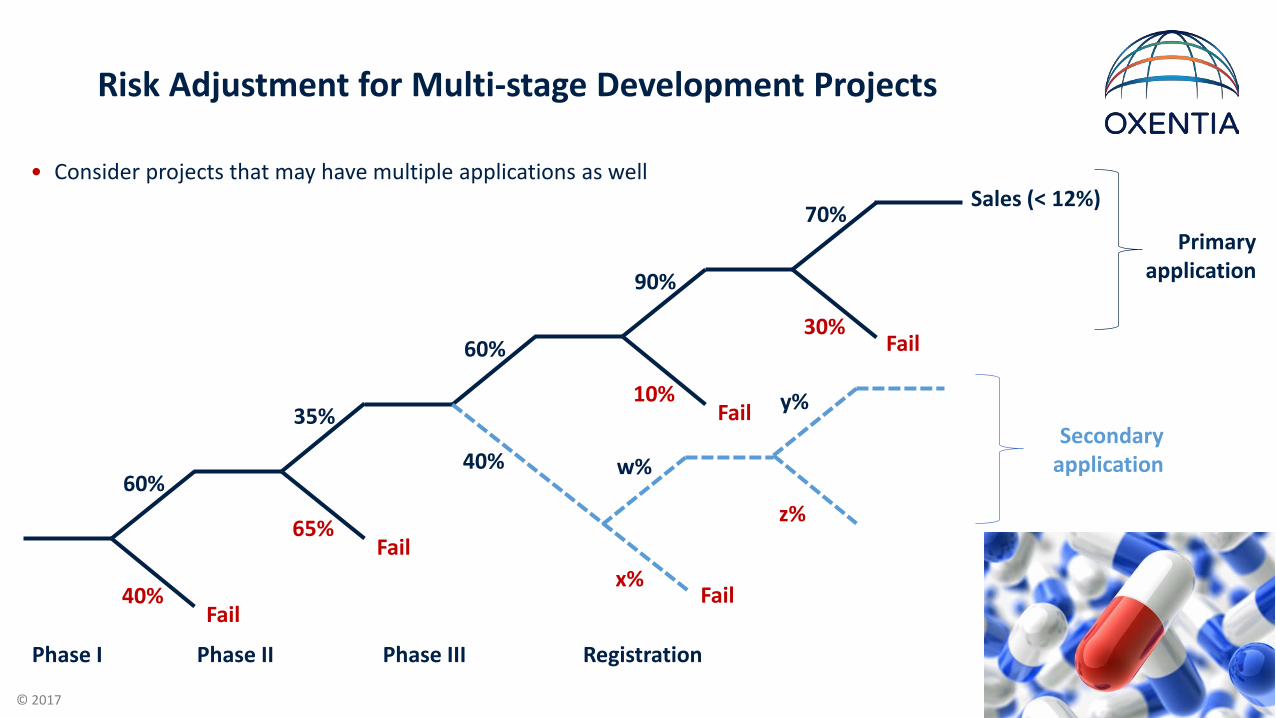

Risk Adjustment for Multi-stage Development Projects

• Consider projects that may have multiple applications as well

Phase I Phase II Phase III Registration

Fail

60%

40%

Fail

35%

65%

Fail

60%

40%

Fail

90%

10%

Fail

70%

30%

Sales (< 12%)

w%

x%

y%

z%

Primary application

Secondary application

24© 2017

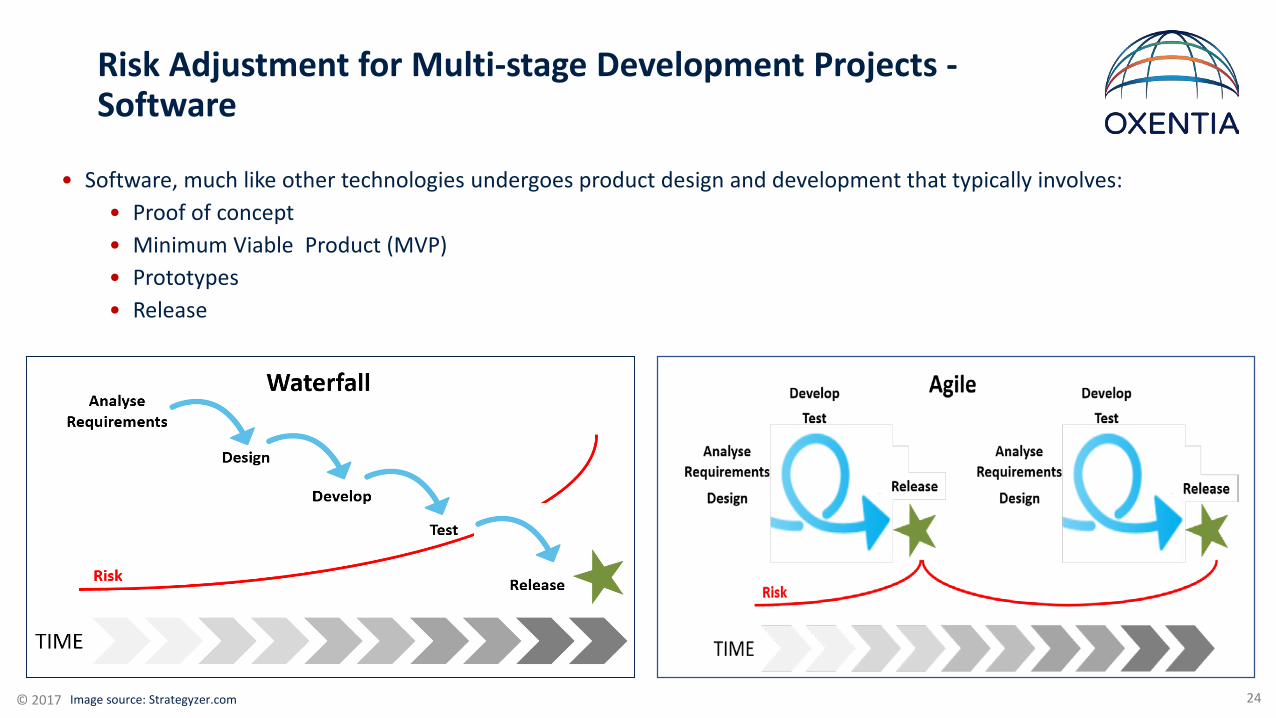

Risk Adjustment for Multi-stage Development Projects -Software

• Software, much like other technologies undergoes product design and development that typically involves:• Proof of concept • Minimum Viable Product (MVP) • Prototypes• Release

Image source: Strategyzer.com

25© 2017

Risk Adjustment for Multi-stage Development Projects –Physical Sciences

Image source: Serkan Botan, NASA project

26© 2017

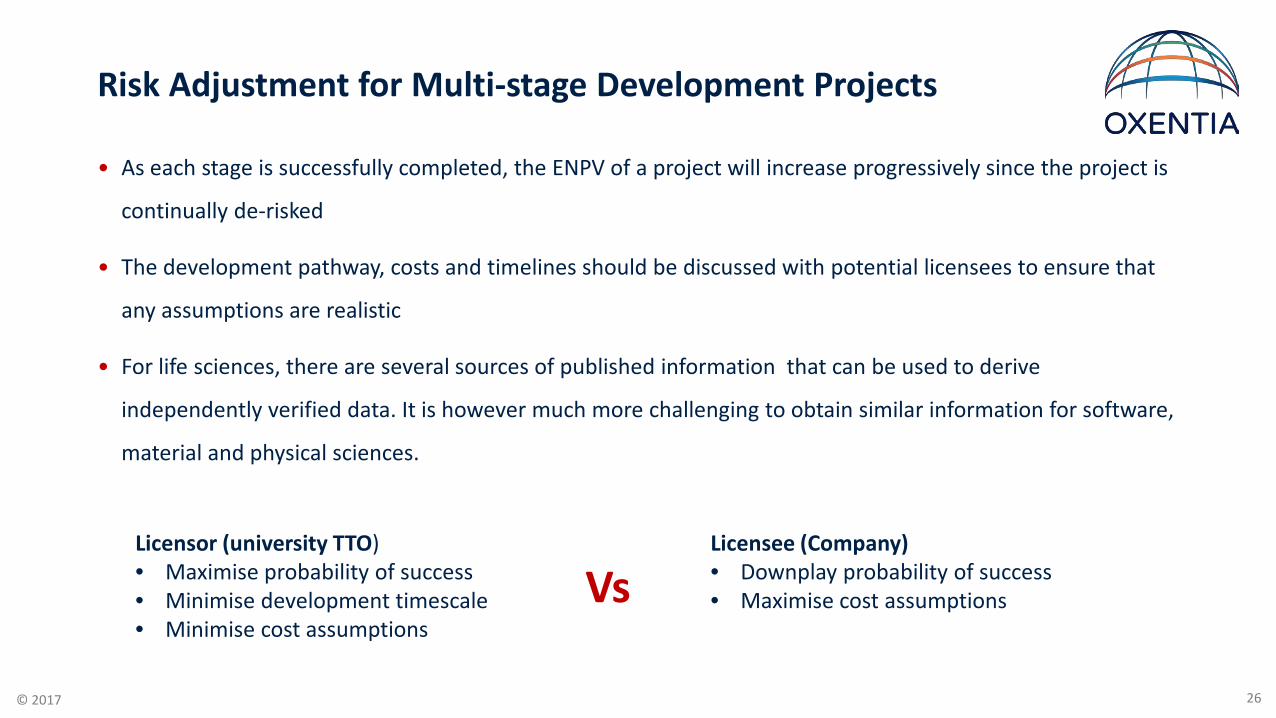

Risk Adjustment for Multi-stage Development Projects

• As each stage is successfully completed, the ENPV of a project will increase progressively since the project is

continually de-risked

• The development pathway, costs and timelines should be discussed with potential licensees to ensure that

any assumptions are realistic

• For life sciences, there are several sources of published information that can be used to derive

independently verified data. It is however much more challenging to obtain similar information for software,

material and physical sciences.

Licensor (university TTO)• Maximise probability of success• Minimise development timescale• Minimise cost assumptions

Licensee (Company)• Downplay probability of success• Maximise cost assumptionsVs

27© 2017

Internal Rate of Return (IRR)

• It is used to determine the profitability of a project and is

commonly used by companies to determine which projects to

invest in.

• The higher the IRR, the more attractive a project is

• Limitations:

• Shifts focus from monetary value (NPV) to relative value (%)

• High IRR projects which generate lower sums of money are

favoured over lower IRR projects that return more money

IRR (%)

NPV ($)

Discount Rate (%)

• The internal rate of return (IRR) is the discount rate when the net present value (NPV) from a project equal zero.

The IRR is an indicator of a project’s profitability and efficiency of a project while the NPV indicates the net value added by undertaking a project.

28© 2017

IRR –Investment Project Beijing 2022

Year of Operation 0 1 2 3 4 5 Total2018 2019 2020 2021 2022 2023

Benefits ($ mil)Total Benefits (Sales) 0.00 0.20 1.50 3.50 7.00 0.60 12.80

Costs ($ mil)Total Costs 1.00 1.04 1.30 2.20 3.90 0.12 9.56

Contribution ($ mil) -1.00 -0.84 0.20 1.30 3.10 0.483.24

Undiscounted Cumulative Contribution -1.00 -1.84 -1.64 -0.34 2.76 3.24

Discounted Cash Flows ($ mil) -1.00 -0.62 0.11 0.51 0.89 0.10 0.00

Net Present Value 0.00

Discount Rate 36.5% The IRR is 36.5%, much higher than the10% discount rate applied to the project

29© 2017

Formulating financial terms of a license deal using ENPV

30© 2017

A Look at recent deals in Pharma

Financial Terms Amount ($ Millions)

Upfront payments $640

Development costs $750

Sales milestone $375

Research Funding $ 160

Immuno-oncology deal termsLicensee Licensor

Financial Terms Amount ($ Millions)

Upfront paymentsResearch funding

Pre-clinical milestones payments

$36

Other milestones (clinical trial success, sales) $754

Royalties Not disclosed

Antibody platform deal terms

31© 2017

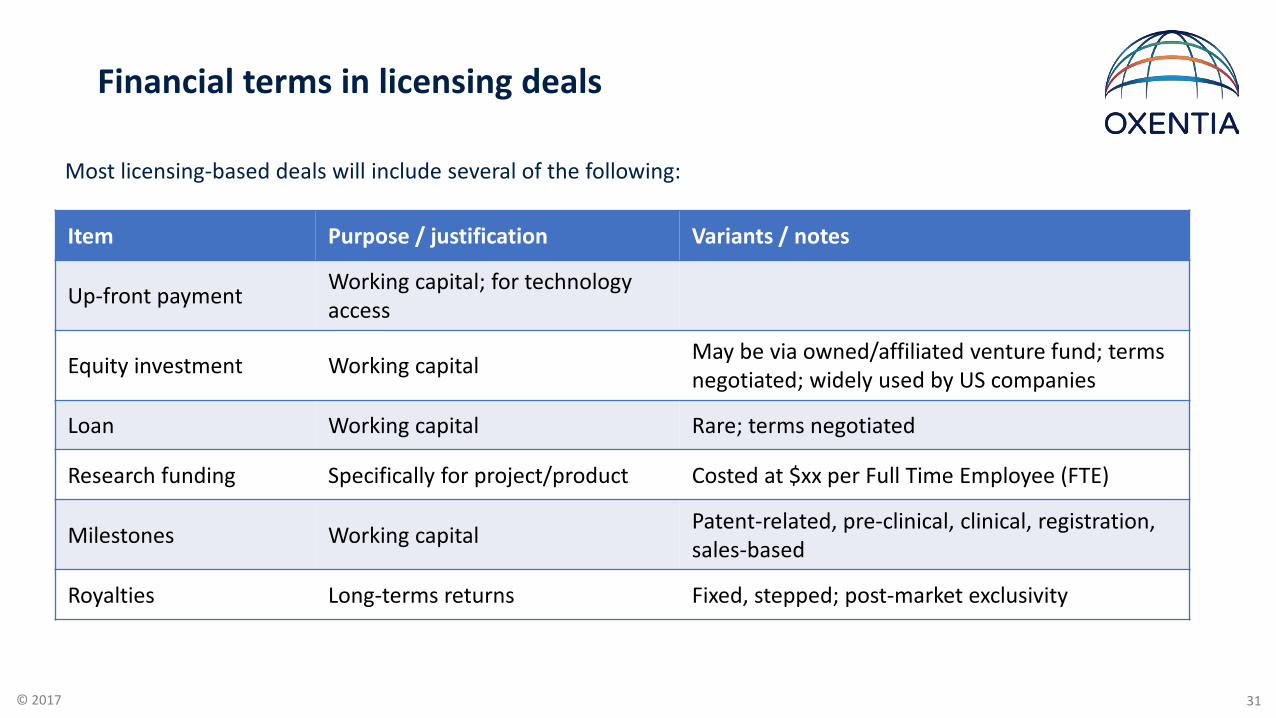

Financial terms in licensing deals

Most licensing-based deals will include several of the following:

Item Purpose / justification Variants / notes

Up-front payment Working capital; for technologyaccess

Equity investment Working capital May be via owned/affiliated venture fund; terms negotiated; widely used by US companies

Loan Working capital Rare; terms negotiated

Research funding Specifically for project/product Costed at $xx per Full Time Employee (FTE)

Milestones Working capital Patent-related, pre-clinical, clinical, registration, sales-based

Royalties Long-terms returns Fixed, stepped; post-market exclusivity

32© 2017

Standard in-licensing process

Find the Asset Evaluate the Asset Acquire the AssetDevelop, and sell asset successfully

• Identify opportunities

• Initial technical evaluation

• Detailed technical and commercial evaluation

• More assessments• Contract negotiations

• Project implementation

• Research strategy• Licensing• External TTO

Step

Activity

Team involved

• Corporate BD• Market research• Manufacturing/Process• Corporate finance• IP & licensing

• Corporate BD• Legal/Contracts• Marketing• Corporate finance

• Research• Manufacturing/Process

Regular review and approvals conducted and guidance from senior management

33© 2017

“…the general who wins a battle makes many calculations…..before the battle is fought.…..Thus do many calculations lead to victory and few calculations to defeat.”

Sun Tzu, Art of War

34© 2017

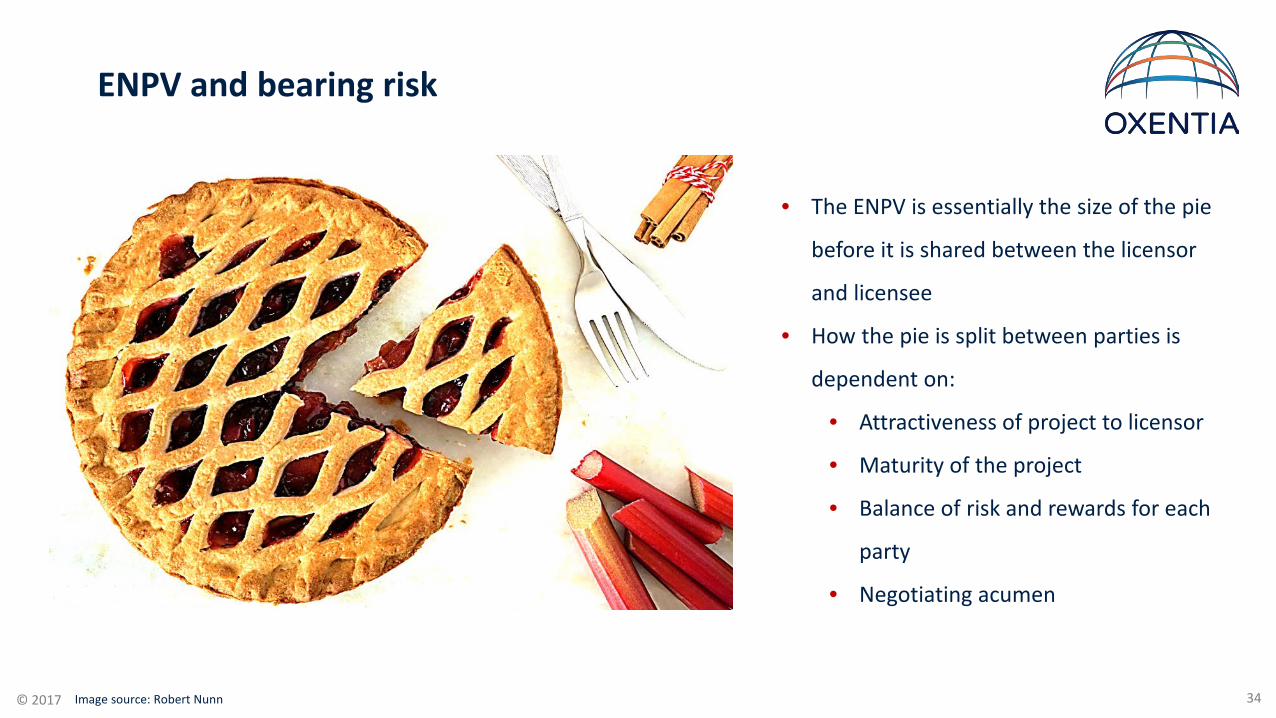

ENPV and bearing risk

• The ENPV is essentially the size of the pie

before it is shared between the licensor

and licensee

• How the pie is split between parties is

dependent on:

• Attractiveness of project to licensor

• Maturity of the project

• Balance of risk and rewards for each

party

• Negotiating acumen

Image source: Robert Nunn

35© 2017

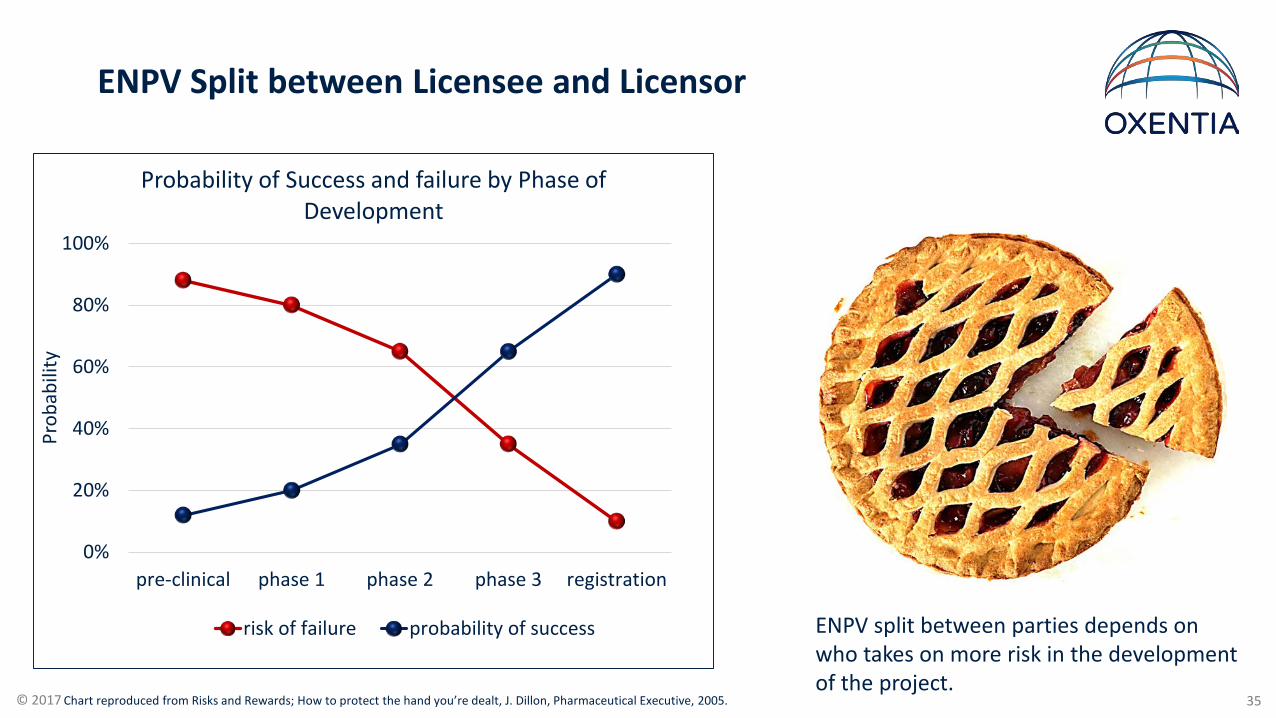

ENPV Split between Licensee and Licensor

0%

20%

40%

60%

80%

100%

pre-clinical phase 1 phase 2 phase 3 registration

Prob

abili

ty

Probability of Success and failure by Phase of Development

risk of failure probability of success

Chart reproduced from Risks and Rewards; How to protect the hand you’re dealt, J. Dillon, Pharmaceutical Executive, 2005.

ENPV split between parties depends on who takes on more risk in the development of the project.

36© 2017

ENPV Split Guidelines

Lice

nsor

’s %

of E

NPV

10%

20%

30%

40%

15% - 20%

20% - 25%

25% - 35%

PHASE I PHASE II PHASE IIIPRE-CLIN.ADV. RES.

8% - 12%

10% - 20%

TRL 5 TRL 6 TRL 7 - 8TRL 3 - 4TRL 2 - 3

Life sciences

Material and Physical sciences

37© 2017

ENPV Split example

Licensor

Licensee

Prior to 1st Human Dose

Licensor

Licensee

End of Phase 1

Licensor

Licensee

End of Phase 2

Licensor

Licensee

End of Phase 3

Data reproduced from Get better Deals by Understanding the Negotiation Practices of Multinational Pharmaceutical Companies, R. brown, Plexus Ventures, 2006

38© 2017

ENPV Split between Licensee and Licensor

ENPV

LicenseeLicensor

All financial terms are included in this share:

• Upfront payments

• Milestone fees

• Research funding

• Royalties (%) on sales

• Equity

Image source: Robert Nunn

39© 2017

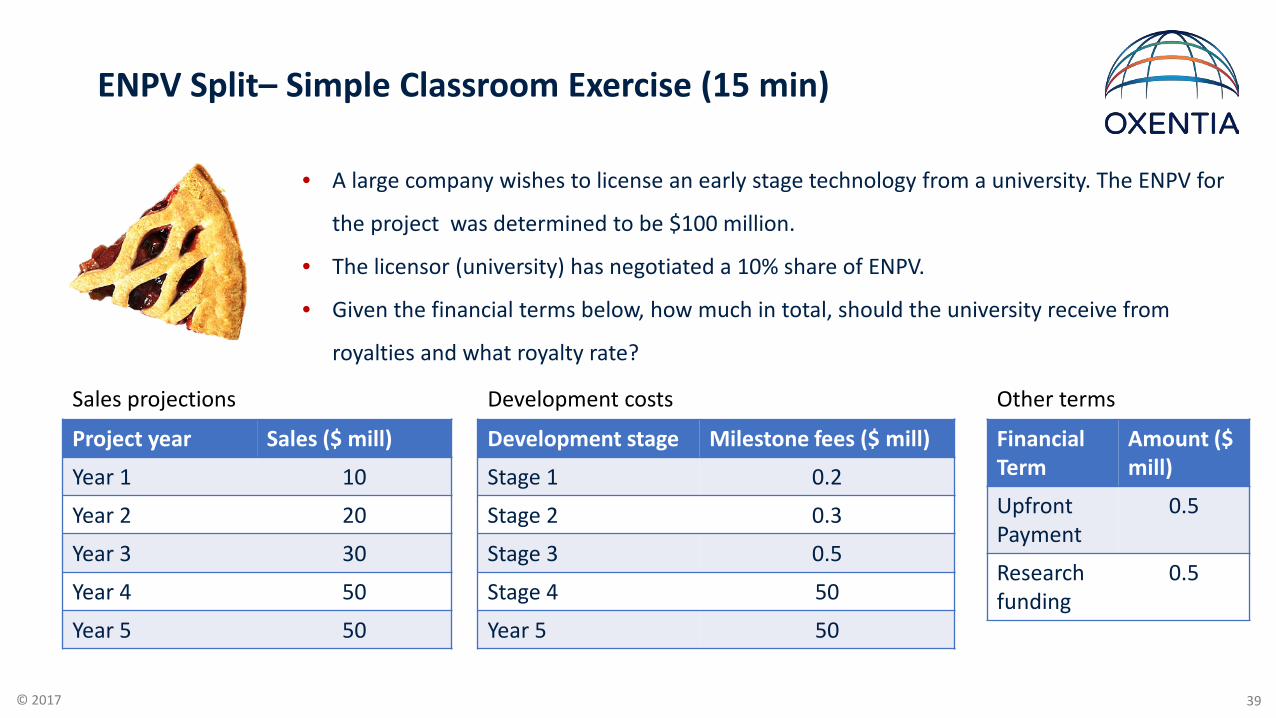

ENPV Split– Simple Classroom Exercise (15 min)

Project year Sales ($ mill)

Year 1 10

Year 2 20

Year 3 30

Year 4 50

Year 5 50

Development stage Milestone fees ($ mill)

Stage 1 0.2

Stage 2 0.3

Stage 3 0.5

Stage 4 50

Year 5 50

Sales projections Other terms

FinancialTerm

Amount ($ mill)

UpfrontPayment

0.5

Research funding

0.5

Development costs

• A large company wishes to license an early stage technology from a university. The ENPV for

the project was determined to be $100 million.

• The licensor (university) has negotiated a 10% share of ENPV.

• Given the financial terms below, how much in total, should the university receive from

royalties and what royalty rate?

40© 2017

Summary

• ENPV approach is based on capturing all relevant cash flows, discounting them to express the

contribution in today’s money and then applying an appropriate adjustment for technical risk.

• ENPV calculated from raDCFs is the industry standard approach to valuing investment projects

• It is important to bear in mind the assumptions and approximations used to arrive at the ENPV

and how these may change

• The IRR is a measure of a project’s profitability

• ENPV represents the size of the opportunity and is split between parties depending on project

maturity, risk sharing and negotiation