Embed Size (px)

Citation preview

IP OVER SATELLITE

Research Seminar on Telecommunications Business II

Jarkko Viinamäki

Helsinki University of Technology

April 6th 2004

2

Agenda

• Introduction

• Satellite IP Technology

• Current Market Status

• Future Prospects

• Case Study: TiscaliSat

• Conclusion

3

Introduction

• The number of Internet users is growing rapidly (~720 million in March 2004)

• Need for broadband connections

• Many areas do not have high speed terrestrial networks

• Satellites can be used to route Internet traffic without expensive infrastructure

4

Satellite IP Technology

• Satellite access equipment

• Positioning

• Operating frequencies

• Service models

• Standards

• Pros & cons

• Comparision to other technologies

5

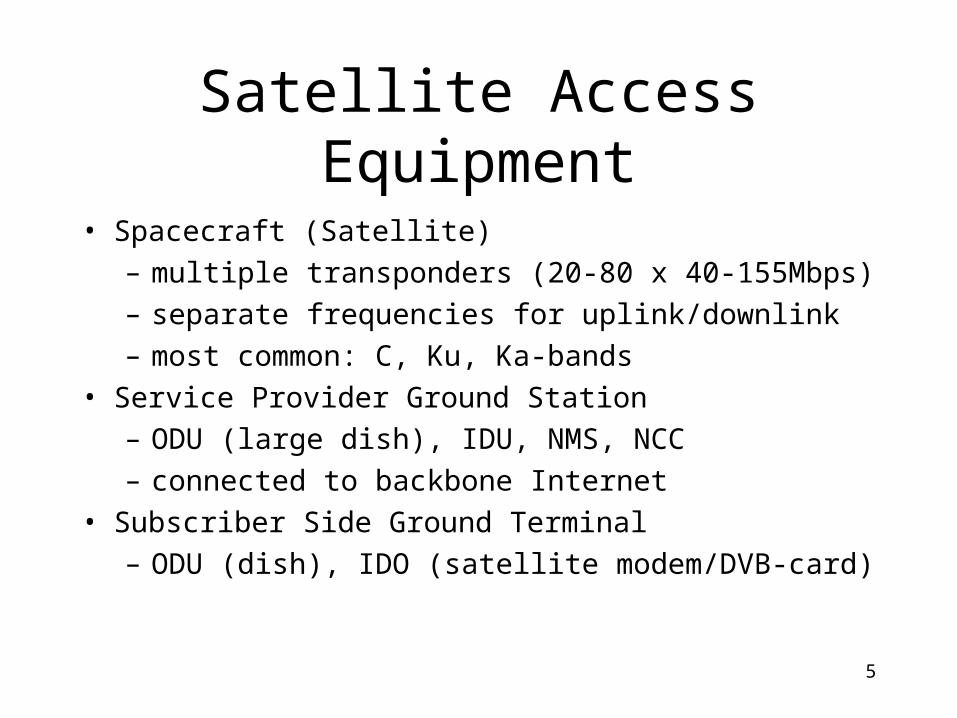

Satellite Access Equipment

• Spacecraft (Satellite)

– multiple transponders (20-80 x 40-155Mbps)

– separate frequencies for uplink/downlink

– most common: C, Ku, Ka-bands

• Service Provider Ground Station

– ODU (large dish), IDU, NMS, NCC

– connected to backbone Internet

• Subscriber Side Ground Terminal

– ODU (dish), IDO (satellite modem/DVB-card)

6

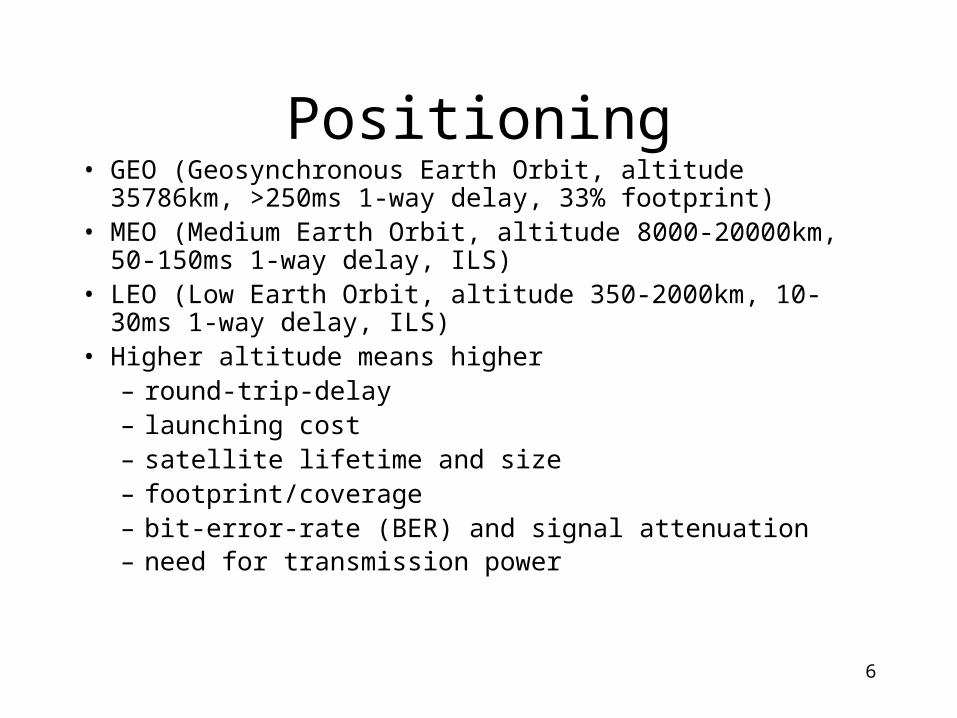

Positioning• GEO (Geosynchronous Earth Orbit, altitude 35786km, >250ms 1-way

delay, 33% footprint)• MEO (Medium Earth Orbit, altitude 8000-20000km, 50-150ms 1-way

delay, ILS)• LEO (Low Earth Orbit, altitude 350-2000km, 10-30ms 1-way delay,

ILS)• Higher altitude means higher

– round-trip-delay– launching cost– satellite lifetime and size– footprint/coverage– bit-error-rate (BER) and signal attenuation– need for transmission power

7

Operating Frequencies

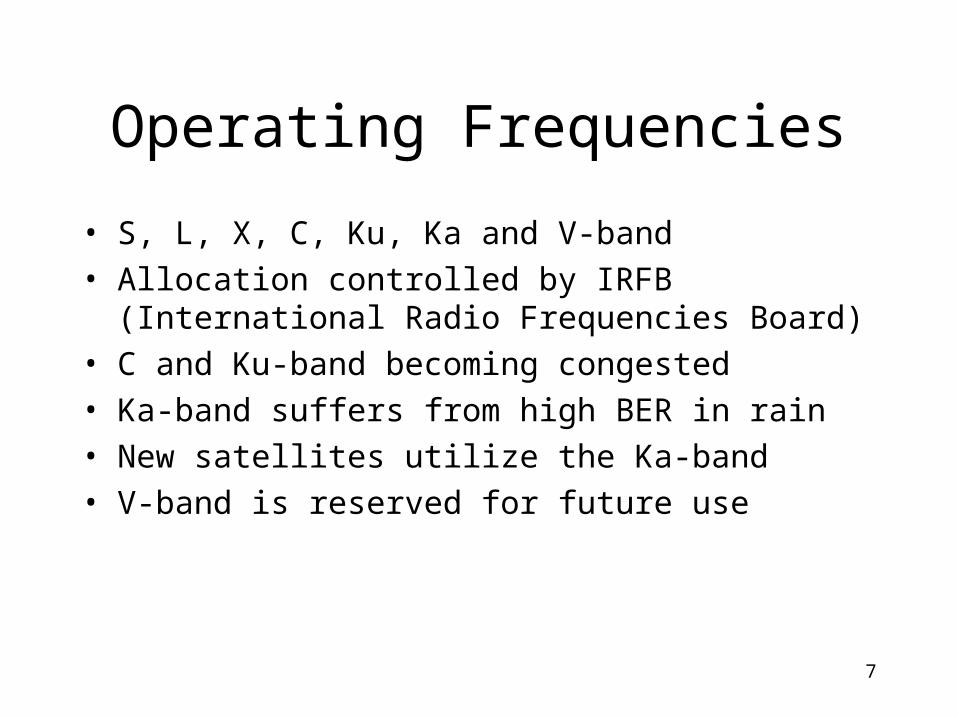

• S, L, X, C, Ku, Ka and V-band

• Allocation controlled by IRFB (International Radio Frequencies Board)

• C and Ku-band becoming congested

• Ka-band suffers from high BER in rain

• New satellites utilize the Ka-band

• V-band is reserved for future use

8

Service Models

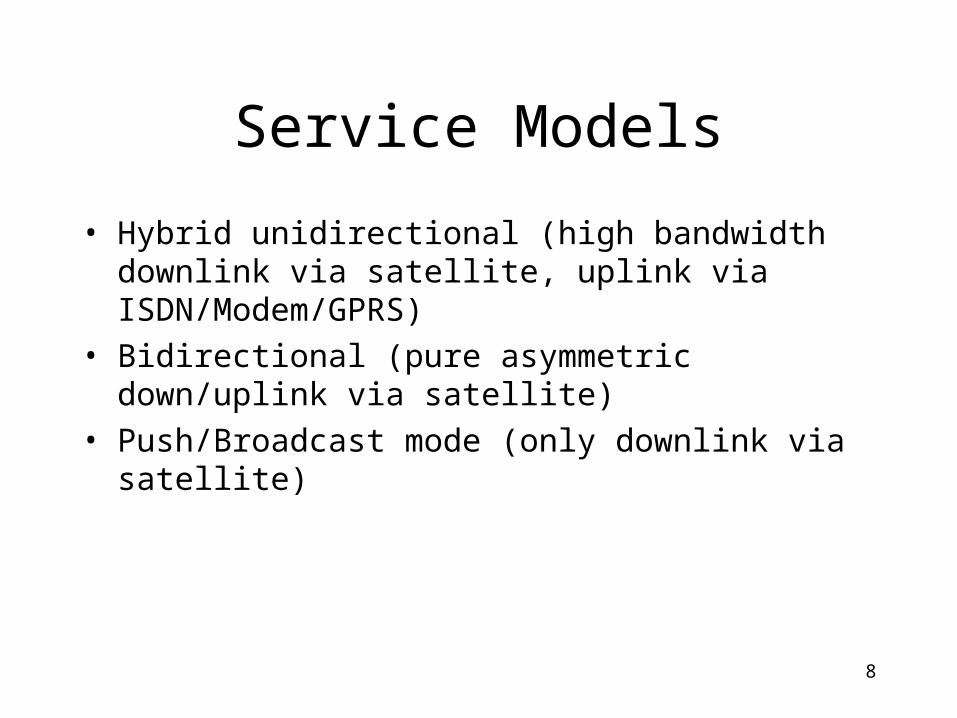

• Hybrid unidirectional (high bandwidth downlink via satellite, uplink via ISDN/Modem/GPRS)

• Bidirectional (pure asymmetric down/uplink via satellite)

• Push/Broadcast mode (only downlink via satellite)

9

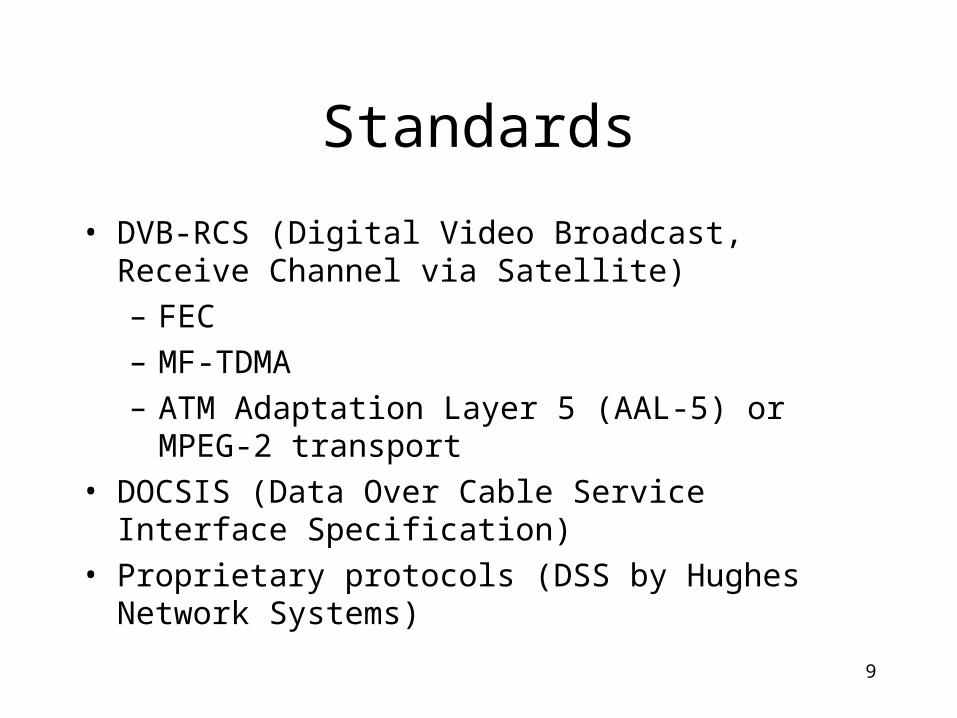

Standards

• DVB-RCS (Digital Video Broadcast, Receive Channel via Satellite)

– FEC

– MF-TDMA

– ATM Adaptation Layer 5 (AAL-5) or MPEG-2 transport

• DOCSIS (Data Over Cable Service Interface Specification)

• Proprietary protocols (DSS by Hughes Network Systems)

10

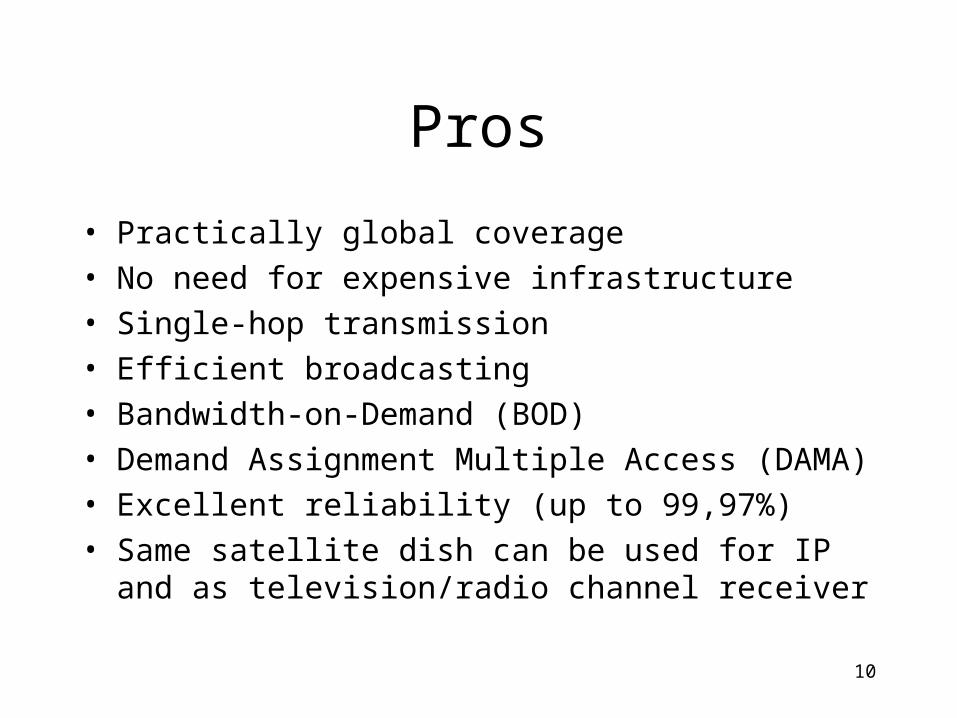

Pros

• Practically global coverage

• No need for expensive infrastructure

• Single-hop transmission

• Efficient broadcasting

• Bandwidth-on-Demand (BOD)

• Demand Assignment Multiple Access (DAMA)

• Excellent reliability (up to 99,97%)

• Same satellite dish can be used for IP and as television/radio channel receiver

11

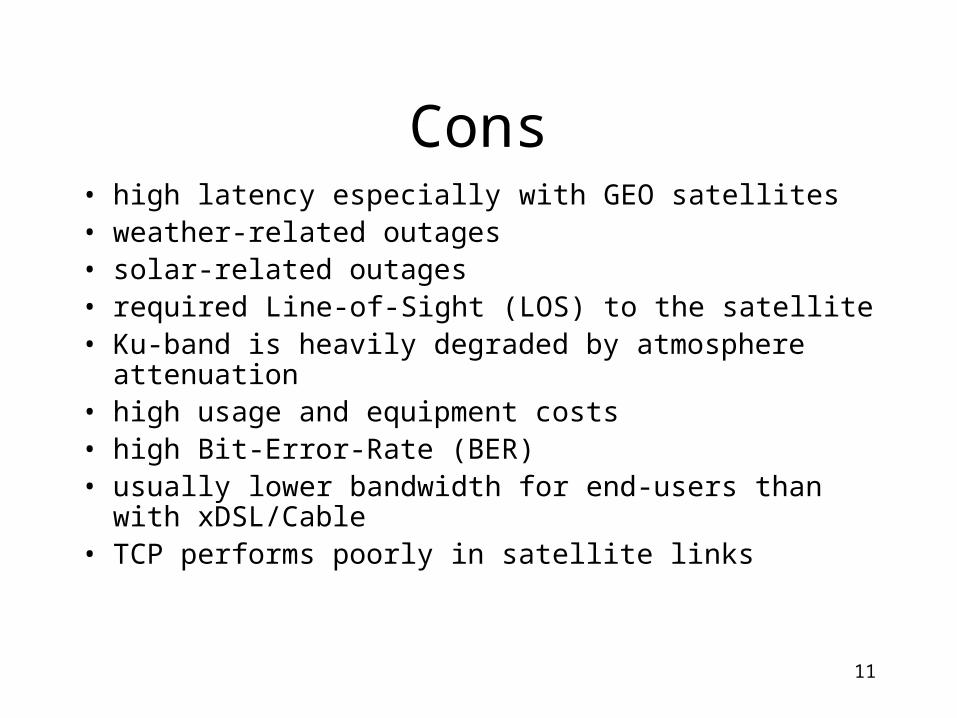

Cons• high latency especially with GEO satellites• weather-related outages• solar-related outages• required Line-of-Sight (LOS) to the satellite• Ku-band is heavily degraded by atmosphere attenuation• high usage and equipment costs• high Bit-Error-Rate (BER) • usually lower bandwidth for end-users than with

xDSL/Cable• TCP performs poorly in satellite links

12

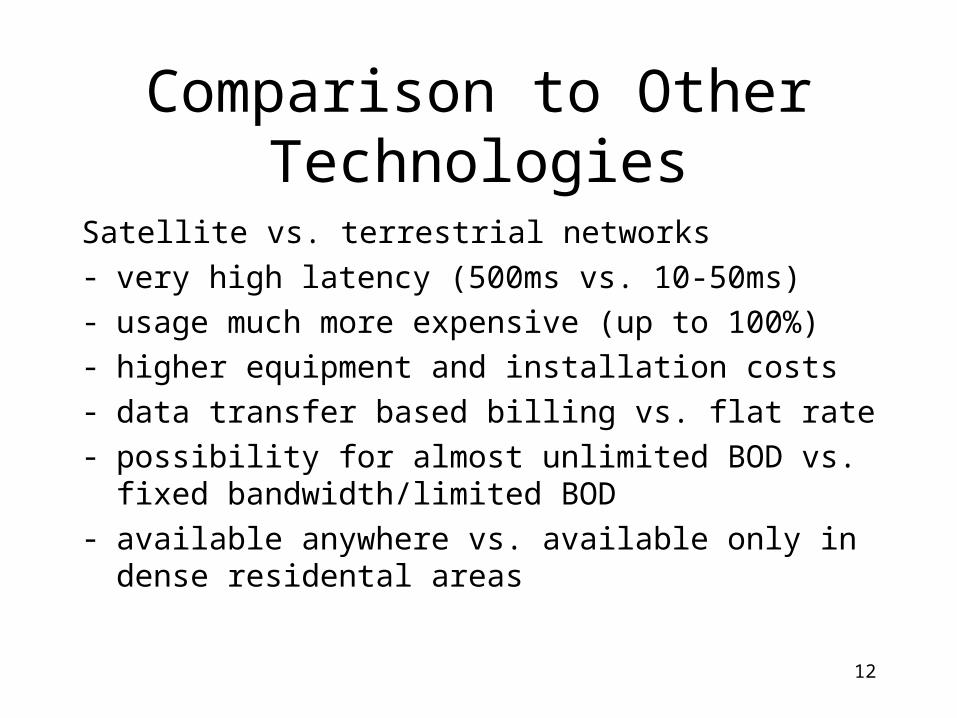

Comparison to Other Technologies

Satellite vs. terrestrial networks

- very high latency (500ms vs. 10-50ms)

- usage much more expensive (up to 100%)

- higher equipment and installation costs

- data transfer based billing vs. flat rate

- possibility for almost unlimited BOD vs. fixed bandwidth/limited BOD

- available anywhere vs. available only in dense residental areas

13

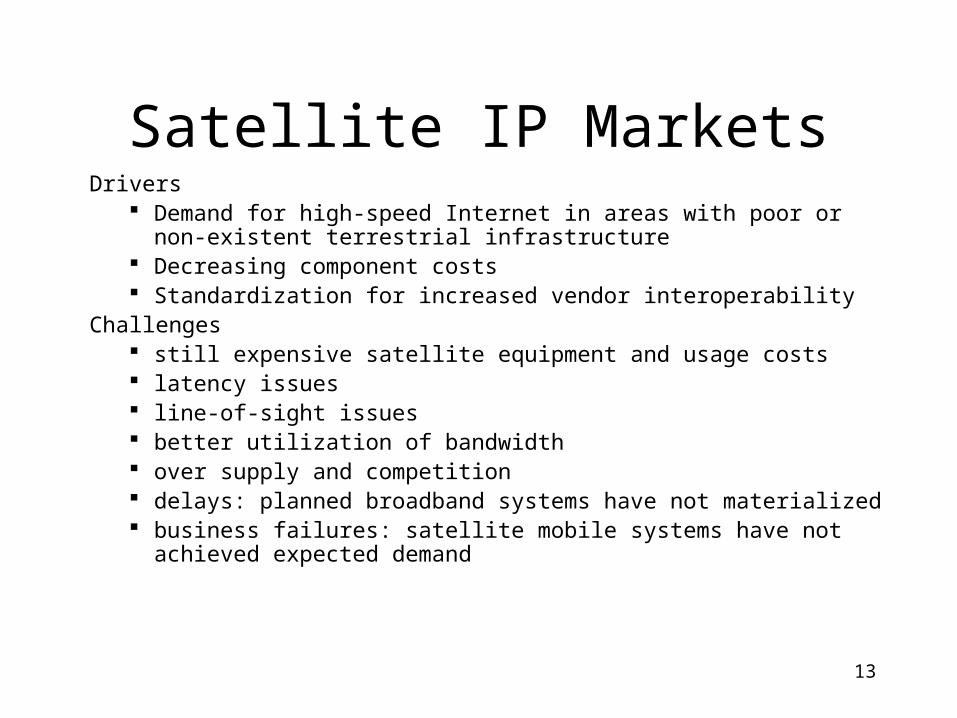

Satellite IP MarketsDrivers

Demand for high-speed Internet in areas with poor or non-existent terrestrial infrastructure

Decreasing component costs Standardization for increased vendor interoperability

Challenges still expensive satellite equipment and usage costs latency issues line-of-sight issues better utilization of bandwidth over supply and competition delays: planned broadband systems have not materialized business failures: satellite mobile systems have not achieved expected

demand

14

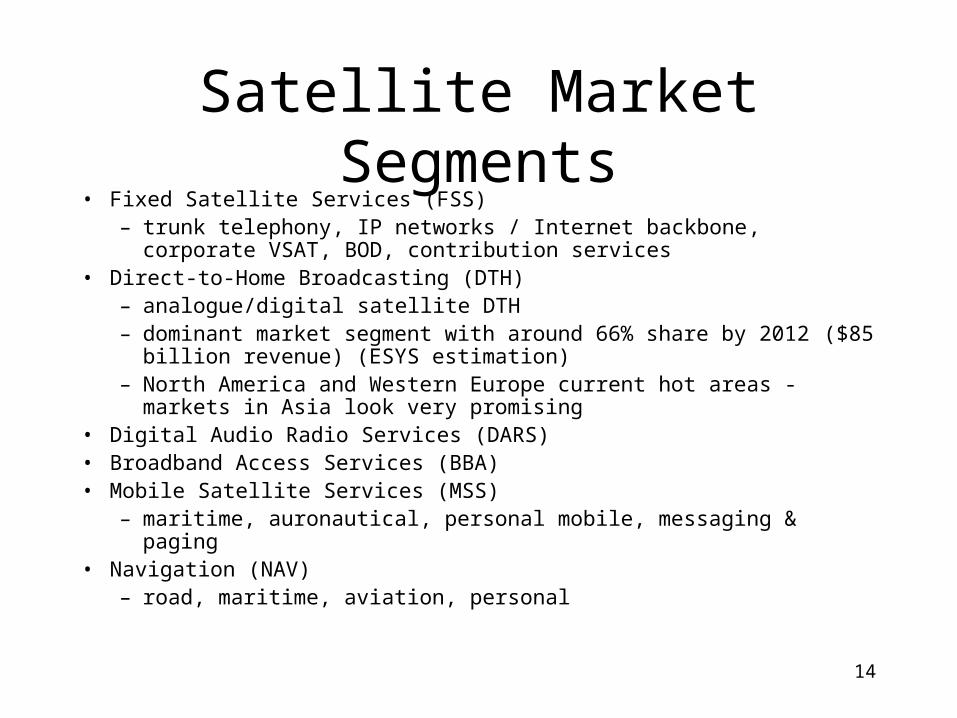

Satellite Market Segments• Fixed Satellite Services (FSS)

– trunk telephony, IP networks / Internet backbone, corporate VSAT, BOD, contribution services

• Direct-to-Home Broadcasting (DTH)– analogue/digital satellite DTH– dominant market segment with around 66% share by 2012 ($85 billion

revenue) (ESYS estimation)– North America and Western Europe current hot areas - markets in Asia look

very promising• Digital Audio Radio Services (DARS)• Broadband Access Services (BBA)• Mobile Satellite Services (MSS)

– maritime, auronautical, personal mobile, messaging & paging• Navigation (NAV)

– road, maritime, aviation, personal

15

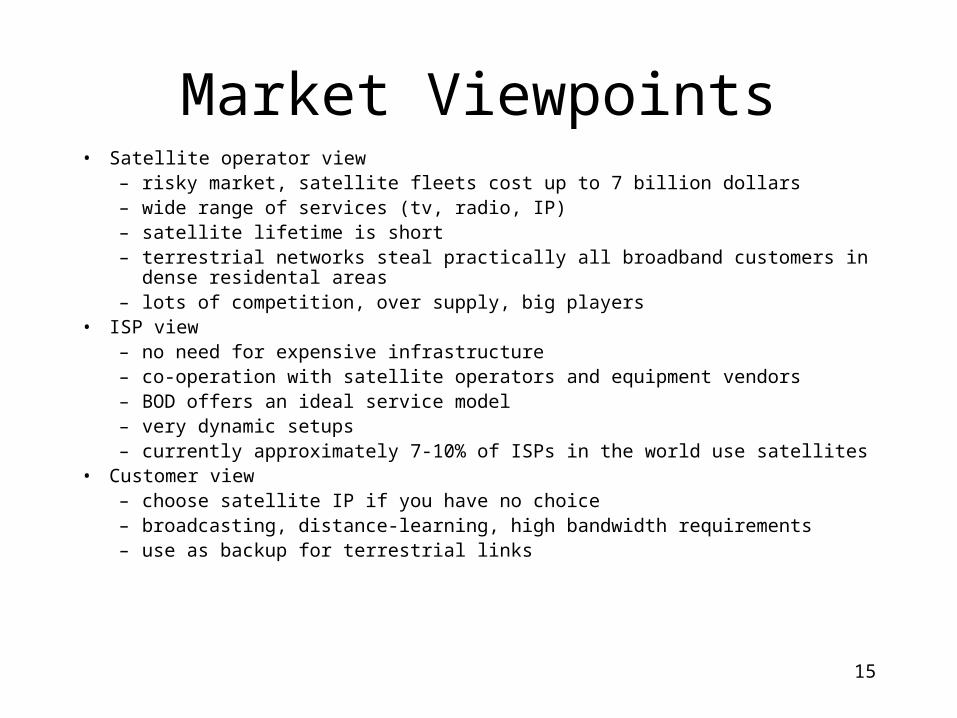

Market Viewpoints• Satellite operator view

– risky market, satellite fleets cost up to 7 billion dollars– wide range of services (tv, radio, IP)– satellite lifetime is short– terrestrial networks steal practically all broadband customers in dense residental areas– lots of competition, over supply, big players

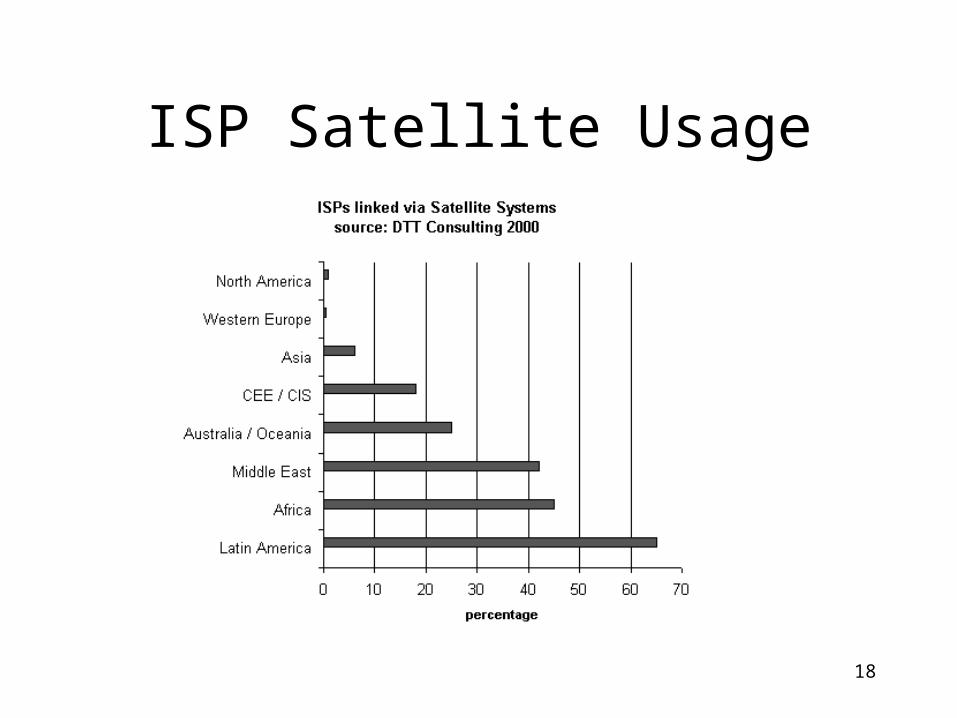

• ISP view– no need for expensive infrastructure– co-operation with satellite operators and equipment vendors– BOD offers an ideal service model– very dynamic setups– currently approximately 7-10% of ISPs in the world use satellites

• Customer view– choose satellite IP if you have no choice– broadcasting, distance-learning, high bandwidth requirements– use as backup for terrestrial links

16

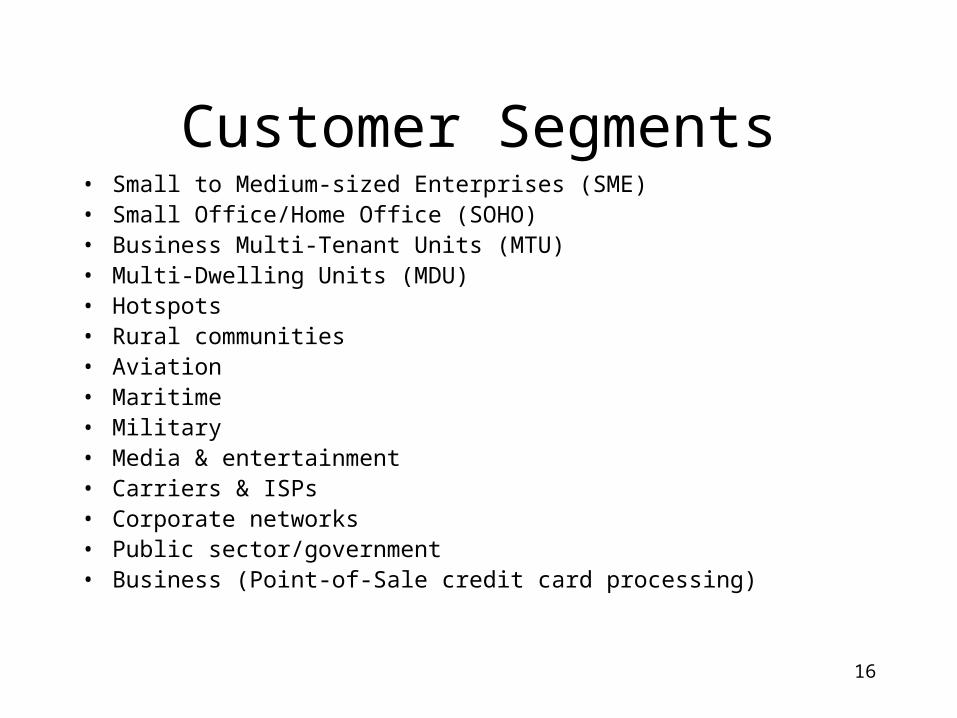

Customer Segments• Small to Medium-sized Enterprises (SME)• Small Office/Home Office (SOHO)• Business Multi-Tenant Units (MTU)• Multi-Dwelling Units (MDU)• Hotspots• Rural communities• Aviation• Maritime• Military• Media & entertainment• Carriers & ISPs• Corporate networks• Public sector/government• Business (Point-of-Sale credit card processing)

17

Current Market Status• currently satellite systems only have 1.5% of the

broadband market and may ultimately gain 6-7% of the global market according to guru Dr. J. Pelton

• lots of competition, over supply, hype

• complex pricing models, not enough focus

• clear customer segments where customers have no other choice than satellite IP

• satellite IP market growth has been radically overestimated

• projects fail, plans are changed

18

ISP Satellite Usage

19

Pricing Models

• Per month pricing (flat rate)

– rare, expensive

• Transfer based billing

• Hybrid models

– limited transfer amount

– monthly fee + transfer limit + extra cost/Mb

– lowered bandwidth when limits exceeded

– priority traffic with extra cost

– unlimited BOD

20

Future Estimations• Most satellite ventures delayed (global recession,

investments down)• European broadcast market near saturation• Terrestrial network usage prices going down• DVB-RCS equipment prices must fall by 50-60% to gain

momentum• Pioneer Consulting expects global broadband satellite market

to grow from $1 billion (2001) to $27 billion (2008)!• Northern Sky Research expects enterprise installed satellite

base to grow from 76000 (2002) to 420000 (2007) and customer base from 71000 (2002) to 701000 (2007) in Europe

21

Future Estimations (cont.)

• figures may be radical overestimates according to some gurus

• affecting factors: rollout of new Ka-band satellites, improvements on technology, pricing, improvement of business models

• connection price and latency issues are the most critical

22

Case Study: TiscaliSat• TiscaliSat offers satellite Internet connections in Finland using EUTELSAT

satellites• Covers entire Finland – for remote areas a slightly larger dish is required• Two service models: 1-way hybrid, 2-way pure satellite• Customer needs a small satellite dish (150EUR) and a DVB PC-card

(150EUR)• 1-way hybrid model:

– 400-2000kbps downlink with 800Mb limit for 40 EUR per month. Customer needs ISDN/Modem for uplink

– 40 EUR/month, installation 50 EUR + uplink costs• 2-way model:

– 400/150kbps (downlink/uplink) bandwidth with 1,3Gb limit (after limit 64-200kbps)

– 79 EUR/month, installation 1170EUR

23

Conclusion

• There is a clear need and market niche for satellite IP connectivity. The customers are there, the money is there.

• Customers are mainly those who can’t use terrestrial broadband networks, need high BOD or high level broadcasting ability

• Prices are high

• Some critical technological problems

• Market hype, over supply

Thank you for your attention!

Q & A