Embed Size (px)

DESCRIPTION

newsletter

Citation preview

C O M M U N I C A T O R

YOUR WINDOWINTO THE WORLD

OF FINANCIAL

PLANNING

In this issue:Page 1:Market Commentary

Page 2: RDSP - In the NewsINVESTWISE team update

Page 3: Insurance - Critical Illness

Page 4: Strategy - Dollar-Cost Averaging

ISSUE 21October 2010

Upcoming EventsStay InformedAs part of our ongoing effort to educate our clients with relevant & timely information, we are very pleased to offer our INVESTWISE Client Education Workshop Series.

We believe strongly in the importance of education. The aim of these workshops is to bring to light new concepts and ideas that you may not have considered before—or clear up some old misconceptions that you may have had about others.

We encourage and value your participation in as many workshops as possible. We will notify you personally if we feel that a presentation is of particular interest to you. In the meantime, if you have any questions about future workshops, or would like to register, please call us at (905) 470-5989 or e-mail us at [email protected].

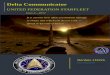

Market CommentaryThe summer months were mixed for the equity markets as most economic indica-tors continued to trend negatively while corporations fared better than expectations in Q2’s earnings result. Canadian housing starts have been declining slowly since April, with the same trend being seen in home sales. The housing situation was especially the worst in the US with new home sales at the lowest level since any data was ever collected. Furthermore, Canadian retail sales remain disappointing, while the Government of Ireland suffered from having their credit rating lowered to AA- due to yet another European bank bailout. There was some positive news toward the end of August: the US unemployment claims saw a slight reduction for July (although a reduction of unemployment claims does not necessarily equate to a stronger employment market) and the Canadian budget deficit has narrowed. The mixed news sent equity markets on a rollercoaster ride.

The INVESTWISE team anticipates elevated market volatility for the remainder of this year. Despite the occasional optimism seen in the equity markets, we advise investors to focus on the economic fundamentals that ultimately drive the economy. The weak housing data pose serious questions on the general population’s financial ability; while a high Canadian Dollar continues to hurt our manufacturing sector. The high US unemployment rate, lagging Q2 GDP results and weak consumer con-fidence points to many economic uncertainties.

Despite all that, we advise clients not to jump on the fear mongering band-wagon. We continue to observe the market carefully and take advantage of any market anomalies and opportunities that may become available. Take advantage of any fear induced selling to buy cheap assets. As veteran inves-tor Warren Buffett has once said, “Be fearful when others are greedy and be greedy when others are fearful”.

Contact InformationDundee Securities Corporation202-80 Tiverton Court,Markham, ON L3R 0G4Phone: 905-470-5989Fax: 905-470-5979Web: www.investwise.com

Danny W. LeungCFP ®, CIM, Ch.P., FMA, FCSI, TEPDirector, Private Client Group, Portfolio Manager, Branch ManagerExt: 208Email: [email protected]

Beverly CulbertsonAdministratorExt: 212Email: [email protected]

Edmun TsangAssociate AnalystExt: 210Email: [email protected]

Elin LeungOffice ManagerExt: 206Email: [email protected]

We’d love to hear more feedback from you about your experiences with us as part of the INVESTWISE family. Please feel free to send us your questions, concerns, and testimonials by calling us at 905-470-5989 or by emailing [email protected]

Spreading the risk with Dollar-Cost Averaging

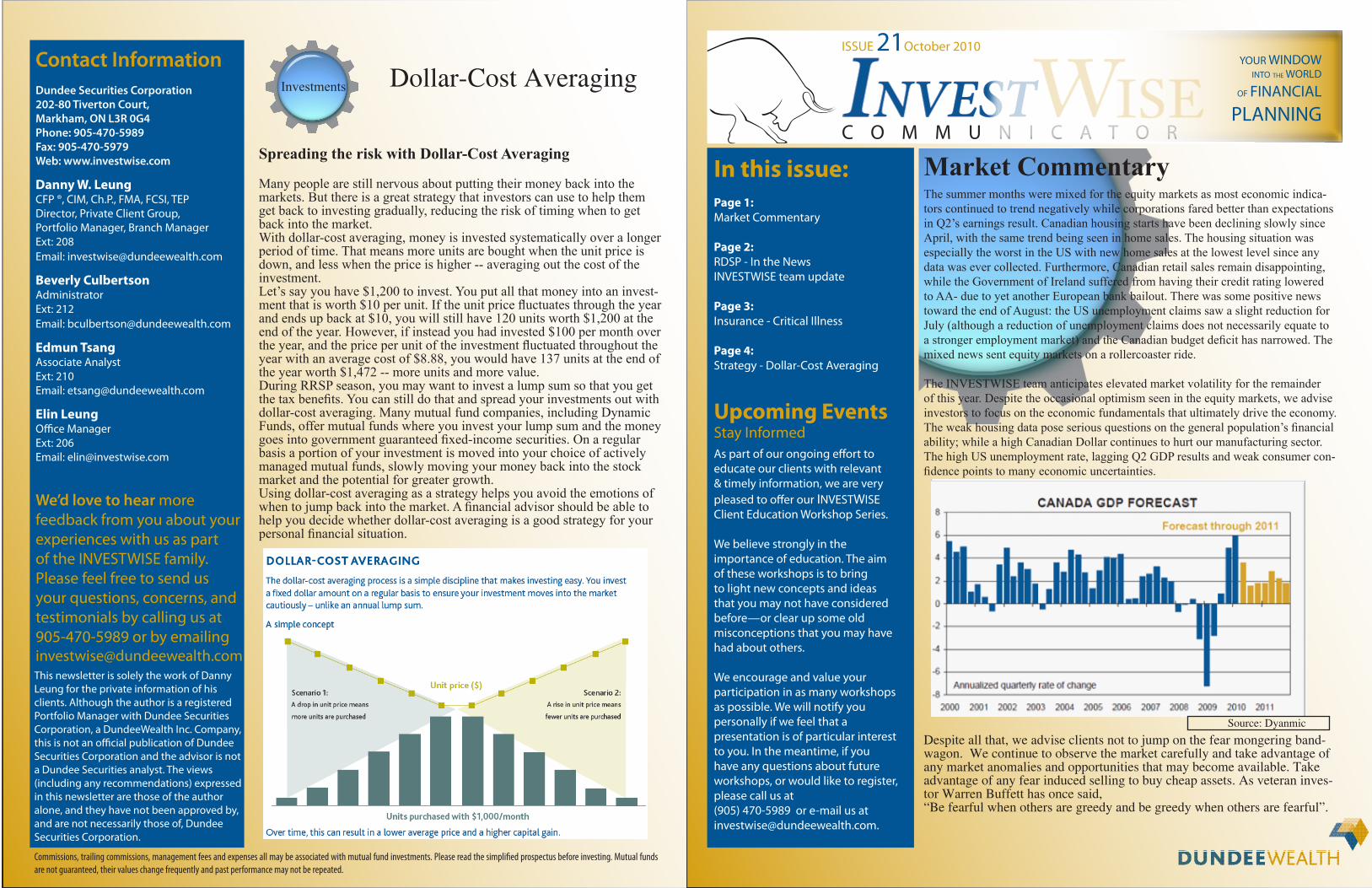

Many people are still nervous about putting their money back into the markets. But there is a great strategy that investors can use to help them get back to investing gradually, reducing the risk of timing when to get back into the market.With dollar-cost averaging, money is invested systematically over a longer period of time. That means more units are bought when the unit price is down, and less when the price is higher -- averaging out the cost of the investment.Let’s say you have $1,200 to invest. You put all that money into an invest-ment that is worth $10 per unit. If the unit price fluctuates through the year and ends up back at $10, you will still have 120 units worth $1,200 at the end of the year. However, if instead you had invested $100 per month over the year, and the price per unit of the investment fluctuated throughout the year with an average cost of $8.88, you would have 137 units at the end of the year worth $1,472 -- more units and more value.During RRSP season, you may want to invest a lump sum so that you get the tax benefits. You can still do that and spread your investments out with dollar-cost averaging. Many mutual fund companies, including Dynamic Funds, offer mutual funds where you invest your lump sum and the money goes into government guaranteed fixed-income securities. On a regular basis a portion of your investment is moved into your choice of actively managed mutual funds, slowly moving your money back into the stock market and the potential for greater growth.Using dollar-cost averaging as a strategy helps you avoid the emotions of when to jump back into the market. A financial advisor should be able to help you decide whether dollar-cost averaging is a good strategy for your personal financial situation.

Dollar-Cost AveragingInvestments

This newsletter is solely the work of Danny Leung for the private information of his clients. Although the author is a registered Portfolio Manager with Dundee Securities Corporation, a DundeeWealth Inc. Company, this is not an official publication of Dundee Securities Corporation and the advisor is not a Dundee Securities analyst. The views (including any recommendations) expressed in this newsletter are those of the author alone, and they have not been approved by, and are not necessarily those of, Dundee Securities Corporation.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the simplified prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

Source: Dyanmic

Looking for the Best Rates? Contact Us Today

Long-Term GIC Rates1 Year 1.75%

18 Months 1.75%

2 Years 2.10%

2.5 Years 2.10%

3 Years 2.40%

4 Years 2.70%

5 Years 3.05%

Short-Term GIC Deposits

30 Days 0.75%

60 Days 1.00%

90 Days 1.25%

120 Days 1.25%

180 Days 1.45%

270 Days 1.45%

All rates are annualized and subject to change without notice at any time. GIC rates shown are as of September 15, 2010 based on information received from the issuers.DundeeWealth does not guarantee the rates posted will remain in effect for the entire business day. Please contact our office for accurate rates at the time of interest. Minimum investment amounts apply.

Mortgage Rates (Prime Rate 3.00%)

TERM*

6 Month 3.95%

1 Year 2.44%

2 Years 2.99%

3 Years 3.45%

4 Years 3.59%

5 Years 3.79%

7 Years 4.85%

10 Years 5.19%

VARIABLE** RATE

5 Years 2.85%

*Rates calculated semi-annually, not in advance.** Rate is Prime Rate minus a factor of 0.15%. Rate changes when Prime Rate changes. Rate is calculated daily.

All interest rates shown above are as of September 15, 2010, and may change without notice. They are calculated on a per annum basis, unless indicated otherwise.

DundeeWealth Mortgages provided by Invis.

Here are some very scary statistics: According to the Canadian Cancer So-ciety, 3,200 Canadians are diagnosed with cancer every week. There will be more than 166,000 new cases in Canada this year with over 73,000 people dying of their disease. Based on current rates, 39% of women and 45% of men will develop cancer during their lifetime. Meanwhile, the Heart and Stroke Foundation says a Canadian dies from a heart attack or stroke every seven minutes. Cardiovascular disease accounts for about one third of all deaths in Canada. We all know that there is nothing more certain in life than death and taxes. Life insurance can protect your family from the financial impact of your untimely death, but what happens if you develop one of these critical dis-eases and you survive? Life insurance is paid on death, not illness. There are 70,000 heart attacks each year in Canada but only 19,000 of those die. Mean-while, thousands of Canadians are living through cancer treatments. This is where you may want to talk to your financial advisor about buying critical illness insurance. Critical illness insurance provides you with a tax free lump sum if you are diagnosed with, and survive, one of a specified list of diseases or afflictions. Different insurance companies will cover different illnesses but the standard four are cancer, coronary bypass surgery, heart attack and stroke. You can usually add other diseases and medical conditions to the policy for addi-tional costs. The lump sum you receive can be used for any purpose. You can reduce your financial commitments such as paying off your mortgage. Or, if necessary the money can help you modify your home or vehicle to help you with mobility issues. You can pay for domestic help during recovery or the money can allow a family member to take time off work to help look after you. If you don’t have a good disability plan at work, you can use the money to replace your income and keep your household going while you recuper-ate. You could also use the money to access medical services or treatments that are not covered by private or government plans. Or, you could take a trip around the world. Critical illness insurance is not cheap however. Costs depend on your age and health factors, plus features you may want to add. For example, a policy paying me a $50,000 lump sum payment would cost $49.19 a month for the first ten years of a policy lasting until I was 75. However, the monthly cost would go up every ten years. (This is called a ten-year renewable plan.) If I bought a policy that leveled my payments until I was 75 it would cost me $70.83 a month. I could also add another $34.79 per month to take advantage of the insurance company’s premium payback term. If I remain healthy until age 75 I would receive all my premiums back – totaling $34,220. Critical insurance may be an option to provide you with financial peace of mind when it comes to your future health. Speak to your financial advi-sor about balancing your peace of mind with your budget and what type of policy might be best for you.

Critical Illness InsuranceInsuranceINVESTWISE Team Update

We would like to take this opportunity to send our well wishes andthanks to Andrea Trant, who has contributed most of her time and effort to the Investwise team and has made a change in her career path after spending almost 7 years working as an Administator and Client Service Manager for the INVESTWISE team. We will most certainly miss her presence around the office, and wish her the best on her journey in her ongoing career.

Notice of Assessment (NOA)

Each year you file your income taxes, the Canada Revenue Agency will provide you with a Notice of Assessment (NOA). Among other things, this NOA will indicate your unused RRSP contribution room for the upcoming tax year. Once you get your NOA please take a moment to forward us a copy either by email, mail or fax. This will assist us in providing the best possible financial recommendations to you in your specific situation.

DID YOU KNOW? Disability Tax Credit“ if credit is available for disabled persons and is 15% of $7,239 – or $1,086 – for 2010. “ The credit can betransferred in certain cases. Provincial credits are also available.

DID YOU KNOW?

By having access to Dundee WealthTracker™ you may view, print or save PDF cop-ies of your past Dundee Securi-ties Corporation statements. If you have not been signed up for this free online service yet but are interested, please call Beverly at 905-470-5989 ext. 212 or email her [email protected]

In the NewsThe Registered Disability Savings Plan (RDSP) is a new savings plan that can assist families in planning for the long-term financial security of our relatives and loved ones with disabilities. This savings plan became available in Decem-ber 2008 and it is available for all residents in Canada under the age of 60 with a disability. Similar to a Registered Education Savings Plan, the RDSP will allow funds to be invested tax-free until withdrawal. Anyone, family and friends, can contribute to someone’s RDSP; furthermore, this contribution is matched by the federal government through the Canada Disability Savings Grant. For families with limited financial means, the Canada Disability Savings Bond will contrib-ute $1000 per year without any contribution. Both the Grant and the Bond are available until the beneficiary reaches the age of 49. There is a $200,000 lifetime contribution limit, but there is no annual limit on contributions. Also, there are no restrictions on when the money can be used and for what purpose. Any individual can be designated as a beneficiary of RDSP if he or she:• is eligible for the disability amount (a non-refundable disability tax credit for people with a qualifying impairment);• has a valid social insurance number (SIN);• is a resident in Canada and at the time the plan is entered into; • is under the age of 60. This age limit is not applicable when a benefi- ciary’s RDSP is opened as a result of a transfer from the beneficiary’s prior RDSP. Upon withdrawal, the growth, including the grant and bond portions, will be taxed in the hands of the beneficiary, but this will likely be at a lower rate, there-fore making the RDSP another useful tool in reducing personal taxes. Several Canadian provinces including Ontario have exempted the RDSP as an asset and income when determining a person’s eligibility for disability benefits. The RDSP is expected to improve the quality of life for as many as 500,000 Canadians liv-ing with disabilities. If you are interested in learning more about RDSP, please contact our office and we will be happy to provide assistance.

The Registered Disability Savings Plan -