Embed Size (px)

Citation preview

NOVEMBER 2019

INVESTORS

PRESENTATION

LEGAL DISCLAIMER

1

The presentation is dated the day it is given. The delivery of this presentationshall not, under any circumstances, create any implication that there has been nochange in the affairs of the Company since such date. The third party informationand statistical data in this presentation have been obtained from sources theCompany believes to be reliable but in no way are warranted by the Company asto accuracy or completeness. This presentation may not contain all materialinformation concerning the Company and the information set forth in this materialis subject to change without notice.

These materials included herein that are not historical facts are forward-lookingstatements. Such forward looking statements involve a number of risks anduncertainties and are subject to change at any time. In the event such risks oruncertainties materialise, AAV’s results could be materially affected. The risks anduncertainties include, but are not limited to, risks associated with the inherentuncertainty of airline travel, seasonality issues, volatile jet fuel prices, worldterrorism, perceived safe destination for travel, Government regulation changes andapproval, including but not limited to the expected landing rights into newdestinations.

This presentation is strictly not to be distributed without the explicit consent ofCompany’s management under any circumstances.

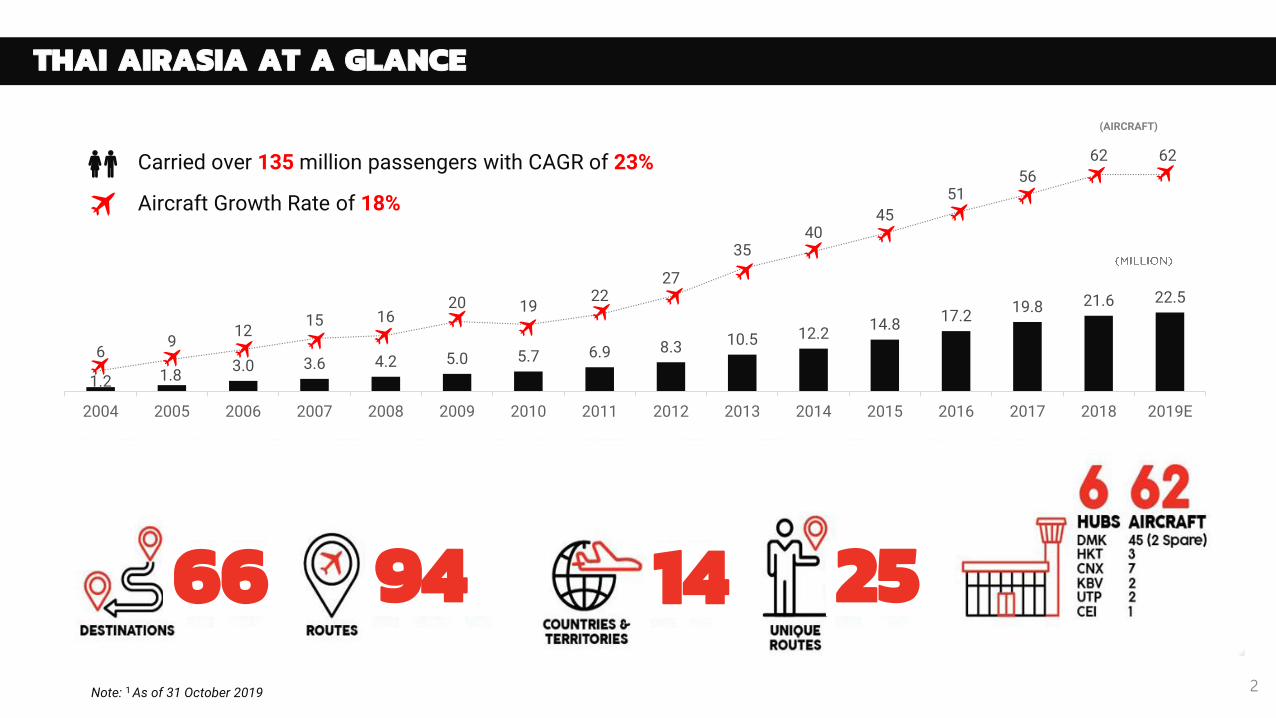

1.2 1.83.0 3.6 4.2 5.0 5.7 6.9 8.3 10.5 12.2

14.817.2

19.8 21.6 22.5

69

1215 16

20 1922

27

3540

45

5156

62 62

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019E

(AIRCRAFT)

Aircraft Growth Rate of 18%

THAI AIRASIA AT A GLANCE

Note: 1 As of 31 October 2019 2

66 94

Carried over 135 million passengers with CAGR of 23%

2514

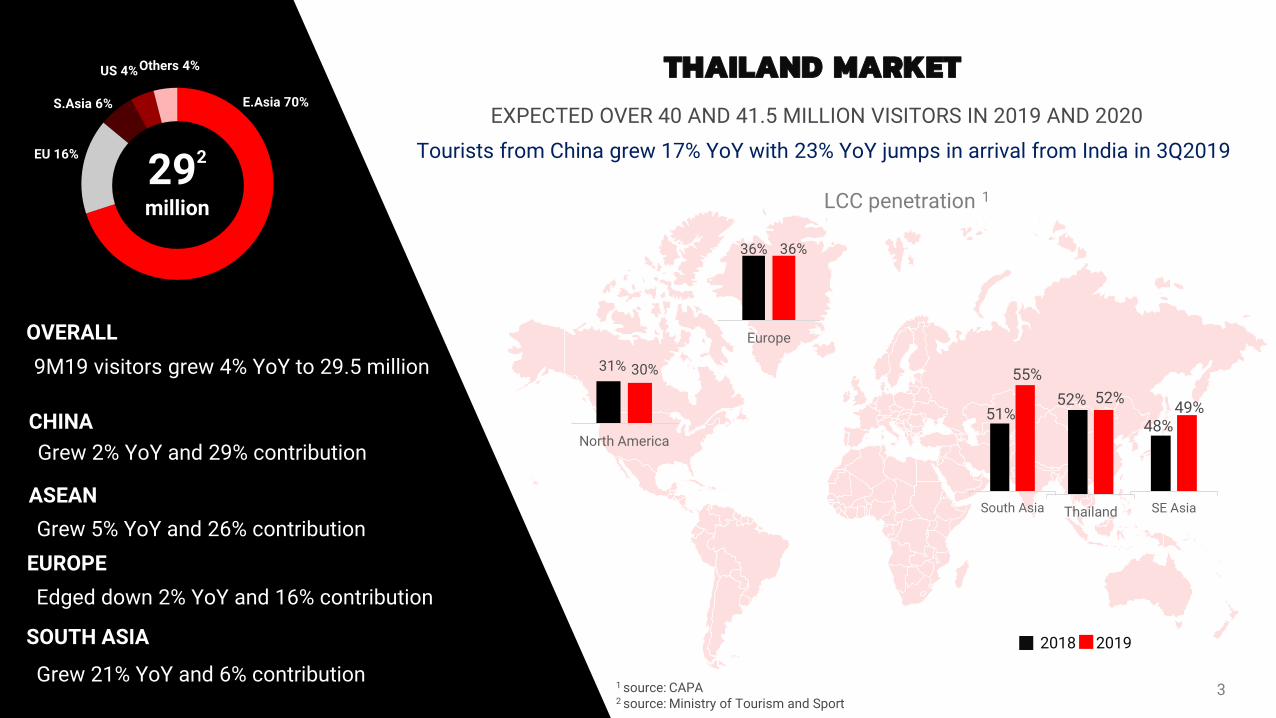

THAILAND MARKET

3

31% 30%

North America

36% 36%

Europe

51%

55%

South Asia

48%49%

SE Asia

LCC penetration 1

52% 52%

Thailand

2018 2019

CHINA

Grew 2% YoY and 29% contribution

ASEAN

Grew 5% YoY and 26% contribution

EUROPE

Edged down 2% YoY and 16% contribution

SOUTH ASIA

OVERALL

9M19 visitors grew 4% YoY to 29.5 million

E.Asia 70%

EU 16%

S.Asia 6%

US 4%Others 4%

292

million

Tourists from China grew 17% YoY with 23% YoY jumps in arrival from India in 3Q2019

Grew 21% YoY and 6% contribution

EXPECTED OVER 40 AND 41.5 MILLION VISITORS IN 2019 AND 2020

1 source: CAPA 2 source: Ministry of Tourism and Sport

ANCILLARY PERFORMANCE

ON TRACK TO ACHIEVE 2019 BT 343 PER PAX (+4%YoY)

9M19 achieved 5.7bn (+8%YoY) or Bt 339 per pax (+4%YoY) 4

5,2

37

5,6

77

FLY-THRU

• 9M19 up by 55% from additional flights among AOCs, reflected in a 59% growth in traffics

• No. Fly-Thru accounted for 6% of total pax

CHECKED BAGGAGE

• 9M19 inched up by 2% YoY, relating to an expansion in international route

IN-FLIGHT SERVICES

• Continue promoting pre-book In-flight combo set• Enhance house-brand on F&B and merchandise

SEAT SELECTION

• 9M19 up by 24% YoY, relating to an expansion in international route and dynamic pricing

• Persuasive advertising influences demand on value

pack and seat selection

OTHERS (Cargo, Tune, Fees)

• Freight revenues was 4% of ancillaries• Fee structure adjustment; processing fee• Upsell on Fly-Thru lounge access

19%

Revenues 50%

8%

8%

6%

28%

9M18 9M19

+8%YoY

Percent contribution to total ancillary revenue

Un

it :

Mill

ion

5

MARKET SHARE1 BY PAX FLOWN65%

12

23

33.2%

18.0% 16.7%

9.4%7.1%

9.9%5.7%

32.4%

18.1% 18.1%

9.3%7.3%

9.7%

4.9%

9M2019 FY2018

Note: 1 9M2019 compared to FY2018 (Source: AAV, AOT and Department of Airport)2 Capacity share as of FY2019 (source : OAG)3 As of October 31 2019

DOMESTIC MARKET

Regional Capacity2

Unique Routes3

Cities

AirAsia Nok Lion Smile Thai Bangkok Vietjet

21Transfer Routes

6

27.24

48.38 49.55 47.51

2013 2014 2015 2016 2017 2018 2019

THAILAND DOMESTIC CAPACITY

(source : OAG)

Peers

Unit : million

Thai Lion Air67%

Thai Airways Group 18%

Nok Air 9%

Bangkok Airways 5%Thai VietJet 1%

Hubs

RE

DU

CT

ION

Competitors have decreased its

capacity by 1.8 million seats, particularly DMK hub.

Thailand domestic market capacity over the past 5-year had grown by 15%,resulting in intense competition and the price war. Recently, the market has a more rational environment, reflected in a 4% decline in capacity.

BKKDMK

DECELERATED GROWTH SPUR THE AVERAGE FARE

7

16.7 18.1

6.24.4

AAV THAI NOK BA

83 8087

68

AAV THAI NOK BA

1.53

2.20 2.17

3.52

AAV THAI NOK BA

17

1210

13

AAV THAI NOK BA

Percent

HIGHEST PAX GROWTH LOWEST CASK*

HIGHEST EBITDAR MARGIN1

BahtMillion passengers

+5% -3% -8% +2% YoY * Cost excluded finance costs and tax expense

HIGHEST ASK GROWTHPercent

Source: 1 SET filing, Company data, AAV estimates based on 9M2019 Results ( NOK excluding Nokscoot)EBITDAR Margin: Earning before finance cost, income tax, depreciation and amortisation, rental / Totalsales and service

ASK Growth +10% -3% -10% -2% YoY

LISTED-AIRLINE PERFORMANCE

8

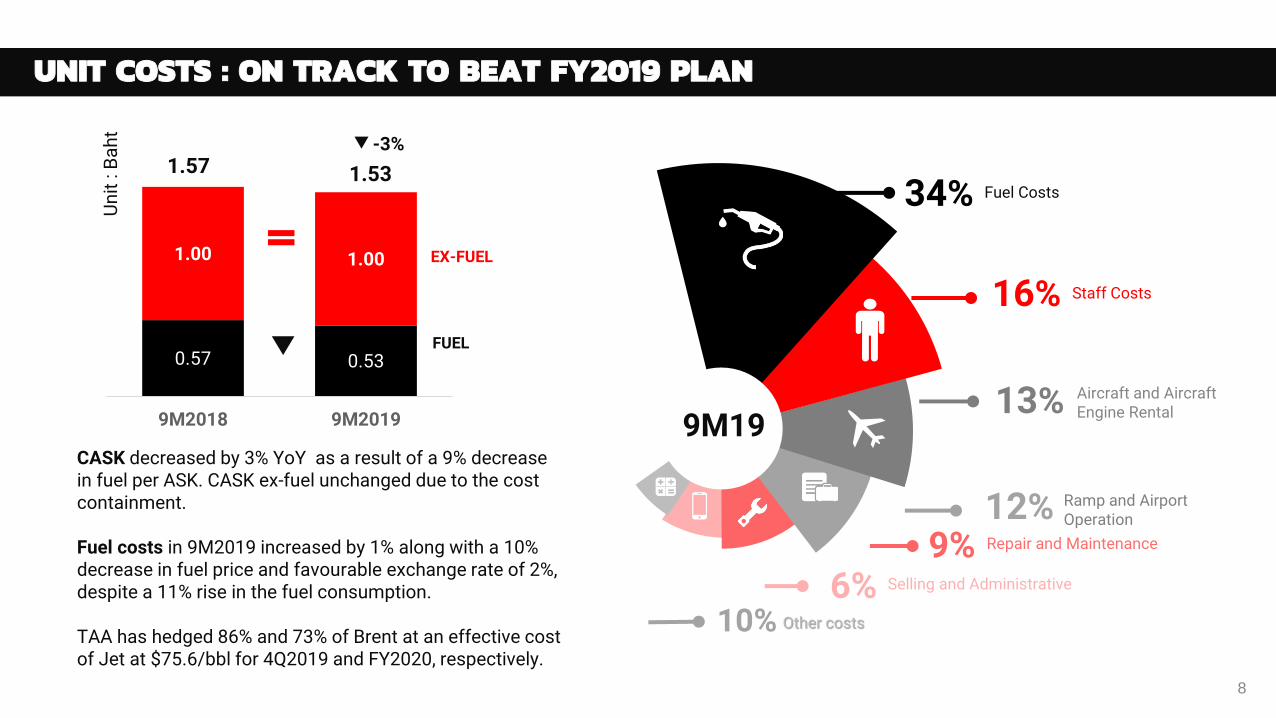

CASK decreased by 3% YoY as a result of a 9% decrease in fuel per ASK. CASK ex-fuel unchanged due to the cost containment.

Fuel costs in 9M2019 increased by 1% along with a 10% decrease in fuel price and favourable exchange rate of 2%, despite a 11% rise in the fuel consumption.

TAA has hedged 86% and 73% of Brent at an effective cost of Jet at $75.6/bbl for 4Q2019 and FY2020, respectively.

34% Fuel Costs

16% Staff Costs

13% Aircraft and Aircraft Engine Rental

9% Repair and Maintenance

12% Ramp and Airport Operation

6% Selling and Administrative

10% Other costs

9M19

UNIT COSTS : ON TRACK TO BEAT FY2019 PLAN

0.57 0.53

1.00 1.00

9M2018 9M2019

1.57 1.53

Un

it :

Ba

ht

-3%

FUEL

EX-FUEL

9

NETWORK REALLOCATION TO MAXIMISE OPERATIONAL RETURNS

* JUL 2019 – OCT 2019** WINTER SEASON*** DEC 2019 – JAN 2020

CNX – DanangDMK – Nha TrangDMK – Can ThoCEI – ShenzhenCNX – ShenzhenDMK – AhmedabadHKT – Phnom Penh

DMK – Narathiwat(7x > 11x)*

DMK – Jaipur (4x > 7x)**DMK – Nan(28x > 31x)***

DMK – Sihanoukville

DMK – VaranasiCEI – Hangzhou

ADD FREQUENCIES: NEW ROUTES:

2Q

/20

19

3Q

/20

19

4Q

/20

19

DMK – Roi EtDMK – Khon KeanDMK – ShenzhenCNX – Taipei (6x > 7x)

10

GROWTH STRATEGIES

Efficient Operation Digital Transform

• AVA• FACES

• Invest in pilot training academy and flight simulator center

• Aim to reduce cost >100 MB

Training Academy

• Green flight operation• Flight plan efficiency

Growth in ancillary to revenue each year, expected to see 25% in next 5 yrs

+1%

+10%Growth in cargo revenue each year, cooperate with TeleportDOMESTIC,

45%

CHINA, 20%

CLMV, 15%

ASEAN ex CLMV, 10%

SOUTH ASIA, 10%

+2% Growth in Fly-Thru passengerseach year

Revenues by routes in 5-year

DiversifyNetwork

CostReduction

Revenue Growth

11

GROWTH

COSTS

COMMERCIAL

• FY2019 capacity growth expected between 5 and 6% driven by disciplined network expansion

• First A321neo delivered in December and entry to service during 1Q/2020

• ASK growth in 2019 between 10 and 11% on the back of international route expansion

• Passengers to achieve at 22.5 million on due to waiving VOA fees till 30 Apr 2020 and other tourism measures;

expect to achieve at 86% of load factor

• On track to achieve 2019 goal; CASK guidance narrowed to -2.0 to 0.0% ; CASK ex-fuel unchanged

• Maintain a cost advantage over competitors, even under the same or different business models

• Cost initiative; transferred call centre services to AVA with 24/7 automated chat system

• Taking immediate capacity actions to address near-term RASK weakness, driven by some new routes taking

longer than usual to mature; network reallocation continues to ramp during the peak seasons

• Maintaining its favourable operating performance (OTP) to more than 85%; which is key in positive brand

awareness

• On track to deliver ancillary revenue; engaging in dynamic pricing of its products & adding a bundled products

• Maintain the goal to ensure that our guests feel like they get the great value from the company’s low fare

COMPANY GUIDANCE

RELEVANT MATERIALS

https://www.aavplc.com/en/investor-relations/home

DOCUMENT LOCATION

Investor Presentation

https://www.aavplc.com/en/investor-relations/downloads/presentations-webcasts

EarningReleases

https://www.aavplc.com/en/investor-relations/updates/news

Annual Reports

https://www.aavplc.com/en/investor-relations/downloads/annual-report

Investor Kits

https://www.aavplc.com/en/investor-relations/publications-and-download/investor-kits

Operating Statistic

https://www.aavplc.com/en/investor-relations/operating-statistics

SustainabilityReport

https://www.aavplc.com/en/investor-relations/downloads/sustainability-report

Don Mueang International Airport, 3rd Fl., Central Office Building, No.3200,Vibhavadi Rangsit Road, Sanambin, Don Mueang, Bangkok 10210

www.aavplc.com [email protected] +662 5625745-6

SHAREHOLDING STRUCTURE:

13

AirAsia Group Berhad

Management & BOD

Thai AirAsia(Operating company)

Public

100%

45%

59%

55%

AirAsia Investment

Asia Aviation(Listed company)

41%

KEY MILESTONES:

Launched second hub in Phuket

2017

2017Marketing Excellence Award, TMA

Outstanding IR Award, SET

2015

2014The World Best LCC’s

OTP Flightstats

Launched Fourth hub in Krabi 2013Launched Third hub in Chiang Mai

2012AAV was listed in the SET & increase its

shareholding in TAA to 55%

Moved back to Don Mueang Airport

Owned first aircraft in our book

2010Comprised of single aircraft type the Airbus A32020092007

Moved to Suvarnabhumi Airport

Received first delivery Airbus A320

AAV was incorporated and acquired 50% of shares in TAA

2004Began services from Bangkok to Phuket, Hat Yai, Chiang Mai and Singapore with two Boeing aircraft

2016Received the first delivery

of A320neo

2018

First Thai LCC to receive AOC Re-Certification

2006

The best of Airline from the best of Thailand awards voted by Chinese tourists

Launched Fifth hub in Utapao

OUR VISION:To be the leading sustainable travel technology company in Asia providing more than just affordable flights

OUR MISSION:1. To provide the highest quality product, embracing

technology to reduce cost and enhance service2. To create jobs across the region and be the best

company to work for where dreams come true3. To care for all our stakeholders, from Allstars, guests,

business partners, investors to communities and governments

4. To create a globally recognised, sustainable ASEAN brand focused on adding value to the economy, society and environment

(as of June 2019)

BUSINESS OVERVIEW

TFRS 16 IMPACT TO LEASED ASSET

Adoption of TFRS 16 by using the Modified Approach method whereby the leases were computed based on the present value of all its future payments based on the company's borrowing rate with the impact taken to opening retained earnings.

The chart depicts that combined depreciation and interest will be less than the operating lease amounts.

1 2 3 4 5 6 7 8 9 10

Depreciation Interest Operating lease

For a new aircraft, combined depreciation and interest will be more than the operating lease amounts during the earlier portion of the lease terms before the adoption of TFRS 16.

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Depreciation Interest Operating lease

14

TAA : KEY STATISTICS

3Q2019 3Q2018 Change 9M2019 9M2018 Change

Passenger carried (Million seats) 5.28 5.12 3% 16.73 16.07 4%

International passenger 2.23 1.97 13% 6.90 6.03 14%

Domestic passenger 3.05 3.15 -3% 9.82 10.04 -2%

Capacity (Million seats) 6.55 6.34 3% 19.81 18.84 5%

Load factor 81% 81% 0 ppt 84% 85% -1 ppt

RPK (Million) 5,444 4,979 9% 17,237 15,791 9%

ASK (Million) 6,766 6,167 10% 20,542 18,559 11%

No. of stages flown 36,253 35,105 3% 109,678 104,382 5%

Average stage length (km) 1,034 972 6% 1,037 985 5%

Fleet size (Aircraft) 62 60 +2 62 60 +2

Aircraft utilisation (Hours/day) 12.2 11.7 +0.5 12.4 12.0 +0.4

On time performance 88% 89% -1 ppt 86% 85% +1 ppt

Average fare (Baht) 1,457 1,418 +3% 1,469 1,499 -2%

RASK (Baht) 1.39 1.45 -4% 1.47 1.58 -7%

CASK (Baht) 1.49 1.60 -7% 1.53 1.57 -3%

CASK ex-fuel (Baht) 0.98 0.98 0% 1.00 1.00 0%

15

TAA STATEMENT OF COMPREHENSIVE INCOME

Unit: Baht million 3Q2019 3Q2018 Change 9M2019 9M2018 Change

Revenue from sales and services 9,419 8,945 5% 30,183 29,250 3%

Gain on exchange rate 0 104 ->100% 271 133 >100%

Other income 242 258 -6% 764 821 -7%

Total revenues 9,661 9,307 4% 31,219 30,203 3%

Cost of sales and services (9,350) (9,138) 2% (28,957) (26,897) 8%

Selling and administrative expenses (716) (704) 2% (2,409) (2,277) 6%

Loss on exchange (80) 0 n/a 0 0 n/a

Total expenses (10,146) (9,842) 3% (31,366) (29,174) 8%

EBIT (485) (535) 9% (147) 1,029 ->100%

Finance costs (198) (188) 5% (570) (536) 6%

Profit (loss) before income tax (683) (722) -5% (717) 493 ->100%

Income tax income (Expense) (77) 67 >100% (20) 118 ->100%

Net Profit (loss) (761) (656) 16% (737) 611 ->100%

16

TAA STATEMENT OF FINANCIAL POSITION

Unit: Baht million 3Q2019 FY2018 Change

Assets

Cash and Cash equivalents 2,476 4,037 -39%

Other current assets 3,635 2,238 +62%

Aircraft, leasehold improvements and equipment, net 25,104 26,129 -4%

Other non-current assets 6,019 5,514 +9%

Total assets 37,234 37,918 -2%

Liabilities

Deferred revenues 4,373 4,987 -12%

Borrowings from financial institutions 5,076 3,488 +46%

Debenture 4,096 4,095 0%

Finance lease liabilities 11,900 13,219 -10%

Other liabilities 4,881 4,351 +12%

Total liabilities 30,326 30,140 +1%

Share capital

Ordinary Share Capital 436 436 0%

Share Premium 2,629 2,629 0%

Retained earnings - legal reserve 44 43 0%

Retained earnings - unappropriate 3,800 4,670 -19%

Total share capital 6,908 7,778 -11%

Total liabilities and share capital 37,234 37,918 -2%17

3Q2019 3Q2018 Change 9M2019 9M018 Change

Earnings (loss) per Share (THB) (17.46) (15.05) -16% (16.92) 14.04 ->100%

Return on Total Assets -3.2% 4.0% -3.2% 4.0%

Return on Shareholders' Equity -16.1% 15.3% -16.1% 15.3%

EBITDAR Margin 13.2% 13.6% -0 ppt 17% 21% -4 ppt

EBIT Margin -5.1% -6.0% +1 ppt 4% 8% -4 ppt

Net Income Margin -8.1% -7.3% -1 ppt -2.4% 2.1% -4 ppt

Debt1 : Equity ratio (Times) 3.05 2.56 3.05 2.56

Net Debt2 : Equity ratio (Times) 2.69 2.08 2.69 2.08

Net Liabilities3 : Equity ratio (Times) 4.03 3.11 4.03 3.11

TAA : FINANCIAL SUMMARY

Note: 1 Debt = Borrowings from financial institutions + Finance lease liabilities + Debenture

2 Net Debt = (Borrowings from financial institutions + Finance lease liabilities + Debenture) - Cash and Cash Equivalents – Short-term Investments

3 Net Liabilities = Total liabilities – Cash and Cash Equivalents – Short-term Investments

Percentage Point (PPT)

18

AAV STATEMENT OF COMPREHENSIVE INCOME

Unit: Baht millionConsolidated

ChangeConsolidated

Change3Q2019 3Q2018 9M2019 9M2018

Revenue from sales and services 9,419 8,945 5% 30,183 29,250 3%

Gain on exchange rate 0 104 ->100% 271 133 >100%

Other income 242 258 -6% 765 821 -7%

Total revenues 9,661 9,307 4% 31,219 30,203 3%

Cost of sales and services (9,350) (9,138) 2% (28,957) (26,897) 8%

Selling and administrative expenses (714) (701) 2% (2,405) (2,273) 6%

Loss on exchange (80) 0 n/a 0 0 n/a

Total expenses (10,144) (9,838) 3% (31,362) (29,169) 8%

EBIT (482) (531) 9% (142) 1,034 ->100%

Finance costs (198) (188) 5% (570) (536) 6%

Profit (loss) before income tax (681) (719) 5% (712) 498 ->100%

Income tax income (Expense) (78) 66 >100% (21) 117 ->100%

Profit (loss) attributable to (759) (653) -16% (733) 615 ->100%

Equity holders of the company (417) (358) -16% (402) 340 ->100%

Non-controlling interests of the subsidiary (342) (295) -16% (332) 275 ->100%

Earnings (loss) per share (THB) (759) (653) -16% (733) 615 ->100%

19

Unit: Baht millionConsolidated

Change3Q2019 FY2018

AssetsCash and Cash equivalents 2,566 4,123 -38%

Other current assets 3,636 2,243 +62%Aircraft, leasehold improvements and equipment, net 25,160 26,185 -4%Intangible assets 1) 14,878 14,883 0%Goodwill 2) 8,825 8,825 0%Other non-current assets 6,001 5,488 +9%

Total assets 61,066 61,747 -1%Liabilities

Deferred revenues 4,373 4,987 -12%Accrued expenses 2,271 2,562 -11%Finance lease liabilities 11,900 13,219 -10%

Borrowings from financial institutions 5,076 3,488 +46%Debenture 4,096 4,095 0%

Other liabilities 5,594 4,773 +17%Total liabilities 33,310 33,124 +1%Share capital

Ordinary Share Capital 485 485 0%Share Premium 2,600 2,600 0%

Retained Earnings – Legal reserve 49 48 0%Retained Earnings – Unappropriated 16,847 17,322 -3%Non-controlling interests 7,776 8,167 -5%

Total share capital 27,756 28,623 -3%Total liabilities and share capital 61,066 61,747 -1%

AAV STATEMENT OF FINANCIAL POSITION

20

Load Factor = Represents the number of passengers carried as a proportion to capacity, which is the number of seats available for passengers.

Available Seat Kilometres (ASK) = which is the total number of seats available on all flights multiplied by the number of kilometres these seats were flown

Revenue Passenger Kilometres (RPK) = Revenue passenger kilometres, which is the number of paying passengers carried on all flights multiplied by the number of kilometresthose seats were flown

Average Fare = Calculated as Thai AirAsia' s total passenger revenues and fuel surcharge divided by total number of passengers carried

Revenue per ASK (RASK) = Calculated as Thai AirAsia's revenues divided by ASK

Cost per ASK (CASK) = Calculated as the sum of Thai AirAsia's operating costs, selling expenses and administrative expenses (but excluding finance costs) divided by ASK

Cost per ASK (CASK ex-fuel) = Calculated as the sum of Thai AirAsia's operating costs, selling expenses and administrative expenses (but excluding finance costs) less fuel costs divided by ASK

Average Stage Length (kilometres) = Represents the average number of kilometres flown per flight

Aircraft Utilisation = Represents the average block hours per day per aircraft during the relevant period. Block hours is calculated by measuring the duration between the time of departure of an aircraft and the time of arrival at its destination.

On Time Performance (%) = A flight is deemed "on time" if the actual departure time is no more than 15 minutes of the scheduled departure time.

21

GLOSSARY