Embed Size (px)

Citation preview

Investor Presentation2015

Strictly private and confidential

2

This presentation has been prepared by Nordax Bank AB (publ) (“Nordax”) in connection with a potential issue by a Nordax subsidiary (the “Issuer”) of asset backed securities (“ABS”) backed by a portfolio of Swedish consumer loans (the “Notes”), for information purposes only. By attending a meeting where the presentation is made, or by reading or otherwise accessing the presentation, you will be deemed to have (i) agreed to the following limitations, notifications and restrictions and (ii) acknowledged that you understand the legal and regulatory sanctions attached to the misuse, disclosure or improper circulation of the presentation.

This presentation is strictly confidential and is being provided to you solely for your information and may not be distributed, published, reproduced or otherwise disclosed in whole or in part under any circumstances to any person. The information in the presentation is directed only at persons to whom such information may be lawfully communicated, including without limitation (a) for the purposes of the U.S. Securities Act of 1933, as amended (the “Securities Act”), persons who are not U.S. persons within the meaning of Regulation S under the Securities Act, (b) persons in member states of the European Economic Area who are qualified investors within the meaning of Article 2(1)(e) of the Prospectus Directive and (c) persons in the United Kingdom who are investment professionals within the meaning of article 19 of the Financial Services And Markets Act 2000 (Financial Promotion) Order 2005. Failure to comply with this restriction may constitute a violation of applicable securities laws.

This presentation is not a prospectus and has not been approved by any regulatory authority and does not constitute or form part of, and should not be construed as, an offer to sell or issue or the solicitation of an offer to buy or acquire securities of Nordax nor the Issuer or an inducement to enter into investment activity in any jurisdiction. This presentation is subject in its entirety to content of the final prospectus, and neither this presentation, nor any part thereof, nor the fact of its use, should form the basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever.

Furthermore, nothing herein constitutes legal, tax, accounting, investment or other advice or a recommendation with respect to any securities or financial instruments. You must make your own independent evaluation of the information contained herein (including without limitation its relevance and adequacy) and consult with such of your advisers and make such other investigations as you consider necessary in connection therewith. None of Nordax nor Citigroup Global Markets Limited (“Citigroup”) shall act as an adviser to, or owe any fiduciary duty to, you or any other recipient of any of the information contained herein, nor are any of them responsible for any advice you may receive from any third party.

The information contained in this presentation has not been independently verified and is subject to change without notice and none of Nordax, Citigroup, or an affiliate thereof or any other party is under any obligation to update or keep current the information contained herein.

No representation or warranty, express or implied, is made or given by or on behalf of Nordax or Citigroup, or any other party (or any of their respective members, directors, officers, employees or Nordax or Citigroup or any other person) as to the accuracy, completeness or fairness of the information or opinions contained in this presentation, and any reliance you place on such information or opinions will be at your sole risk. None of Nordax, Citigroup nor any other party (or any of their respective members, directors, officers, employees or Nordax or Citigroup or any other person) accepts any liability whatsoever for any loss howsoever arising from any use of this presentation or its contents or otherwise arising directly or indirectly in connection therewith.

This presentation does not in itself constitute an offer to purchase or subscribe for any securities of Nordax or the Issuer and any investment decision should thus not be based on the information contained herein.An investment in the Notes involves a high level of risk and several factors could cause the actual results or performance of the Notes to be different from what may be expressed or implied by statements contained in this presentation. By attending a meeting where this presentation is presented, or by reading or otherwise accessing the presentation, you acknowledge that you will be solely responsible for your own assessment of the potential investment and the market and that you will conduct your own analysis and be solely responsible for forming your own view of the potential future performance of the Notes.

The content of this presentation is not to be construed as legal, credit, business, investment or tax advice. Each recipient should consult with its own legal, credit, business, investment and tax advisers to receive legal, credit, business, investment and tax advice.

This presentation may contain certain forward-looking statements that reflect Nordax’ current views or expectations with respect to future events and financial and operational performance. Although Nordax believes that these statements are based on reasonable assumptions and expectations, Nordax cannot give any assurances that such statements will materialize. Because these forward-looking statements involve known and unknown risks and uncertainties, the outcome could differ materially from those set out in the forward-looking statement. The forward-looking statements speak only as at the date of the presentation and Nordaxundertakes no obligation to update such forward-looking statements.

This presentation contains market data and industry forecasts, including information related to the sizes of the markets in which Nordax and its subsidiaries participates. The information has been extracted from a number of sources. Although Nordax regards these sources as reliable, the information contained in them has not been independently verified and therefore no assurance can be given that this information is accurate and complete. In addition to the above, certain data in the presentation is also derived from estimates made by Nordax.

The information and opinions contained in this presentation are provided as at the date of this presentation and are subject to change without notice. Neither this presentation nor any part or copy of it may be distributed in any jurisdiction where such distribution would require any prospectus, registration or measures other than those required under Swedish law, or otherwise would conflict with regulations in such jurisdiction. Persons into whose possession this presentation may come are required to inform themselves about, and comply with such restrictions. Any failure to comply with such restrictions may result in a violation of applicable securities regulations.

The presentation as well as any other information provided by Nordax or the Issuer in respect of the Notes is governed by Swedish law, and any claims or disputes in relation thereto shall be interpreted under Swedish law with the City Court of Stockholm (Sw. Stockholms tingsrätt) as the court of first instance.

Citigroup Global Markets Limited is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority of the United Kingdom.

Any reference to “Citigroup” or “Nordax” herein includes any of their respective affiliated or associated companies and/or their respective directors, representatives or employees and/or any persons connected with them.

Disclaimer

Agenda

3

Section Page

32

Deal structure 41

Market and product overview 18

Risk management, credit underwriting and operating platform

14

8

Funding

23

4

Appendix

5

6

Overview of Nordax2

3

Z

Deal structure1

4

Deal structure

• All tranches will be floating rate based on 1 month Stibor

• Two years revolving and one year amortizing

• No cross currency swap

Class Size (SEK m) % of Total CE** Rating (F/D) WAL

(Years)* Legal Final Step-Up ([36] month) Coupon

A [1,059,000,000] [60%] [40%] [AAAsf / AAA (sf)] [2.84] [Dec 2038] [2x] 1mS + [●]B [264,750,000 ] [15%] [25%] [AAsf / AA(sf)] [3.03] [Dec 2038] [2x] 1mS + [●]C [176,500,000 ] [10%] [15%] [Asf / A(sf)] [3.03] [Dec 2038] [2x] 1mS + [●]D [105,900,000 ] [6%] [9%] [BBB+sf / BBB(sf)] [3.03] [Dec 2038] [2x] retainedE [158,850,000 ] [9%] - [NR] [3.03] [Dec 2038] retained

Total [1,765,000,000] 100%LiquidityReserve [22,062,500] 1.25%

Sale of promissory notesConsumer

loan portfolio

Nordax (“Originator and

Servicer”)

Issuer (“wholly owned

subsidiary of Nordax”)Purchase price

Servicing Agreement

[AAAsf / AAA (sf)]

[AAsf / AA(sf)]

[Asf / A(sf)]

NR

Principal and Interest

Note Proceeds

Liquidity Reserve

[BBB+sf / BBB(sf)]

Capital Structure

Transaction Structure

*Note: Based on 15% CPR, no defaults/ delinquencies and assumed call on the Step-Up Date**Note: CE consists of overcollateralisation and does not include excess spread or the non-amortising liquidity reserve, which is sized at 1.25% of the initial pool balance

5

6

Portfolio Overview

Overview

(All Balances in SEK) Total Max Min AverageOriginal Balance 1,625,598,528 400,000 6,000 149,770

Outstanding Balance 1,831,700,664 410,054 4,036 168,758

By Balance

Average Remaining Term (Months) 119.9

Average Seasoning (Months)(1) 27.9

Average Yield 12.2%

Home Owner(2) / Renter / Other 53.97% / 43.45% / 2.58%

0,00%

5,00%

10,00%

15,00%

20,00%

25,00%

30,00%

x ≤25k 25k < x ≤50k

50k < x ≤75k

75k < x ≤100k

100k < x ≤125k

125k < x ≤150k

150k < x ≤200k

200k < x ≤250k

250k < x ≤350k

x>350k

Number of Loans Capital Balance

Outstanding Balance(SEK)

Original Balance(SEK)

0,00%

2,00%

4,00%

6,00%

8,00%

10,00%

12,00%

14,00%

16,00%

18,00%

20,00%

x ≤25k 25k < x ≤50k

50k < x ≤75k

75k < x ≤100k

100k < x ≤125k

125k < x ≤150k

150k < x ≤200k

200k < x ≤250k

250k < x ≤300k

x >300k

Number of Loans Capital Balance

6

(1) Using origination date(2) Includes House and Apartment Owners

7

Portfolio Overview

7

Seasoning(Months)

Remaining Term(Months) Origination Channels

Distribution by Yield

0,00%

5,00%

10,00%

15,00%

20,00%

25,00%

30,00%

x ≤20 20< x ≤4040< x ≤6060< x ≤80 80< x ≤100

100< x ≤120

120< x ≤140

140< x ≤160

160< x

Number of Loans Capital Balance

0,00%

10,00%

20,00%

30,00%

40,00%

50,00%

60,00%

70,00%

80,00%

Direct Mail Broker Other

Number of Loans Capital Balance

0,00%

5,00%

10,00%

15,00%

20,00%

25,00%

30,00%

35,00%

40,00%

x ≤5% 5%< x ≤10% 10%< x ≤12%12%< x ≤14%14%< x ≤16%16%< x ≤18% 18%< x

Number of Loans Capital Balance

0,00%

5,00%

10,00%

15,00%

20,00%

25,00%

30,00%

x ≤10 10< x ≤2020< x ≤3030< x ≤4040< x ≤5050< x ≤6060< x ≤7070< x ≤80 80< x

Number of Loans Capital Balance

8

Z

Overview of Nordax2

• A leading niche bank in the Nordic region providing more than 85,000 consumer loans and 25,000 deposit accounts (1)

– Offering also includes payment protection insurance• Established in 2003 and operating from a centralised platform in Stockholm• Focus on large personal loans – Nordax’s customers are financially stable, targeted using predominantly direct mail / push marketing

channels (2)

• Core analytical capabilities within decision science and advanced underwriting enabling high marketing efficiency and good credit quality• Diversified funding across products, markets and currencies• Regulated by SFSA since launch, banking license since December 2014• Listed on NASDAQ Stockholm since June 2015

Nordax Bank: A Leading Niche Bank in the Nordics

Loans outstanding(30 Sept 2015, SEK bn)

Centralised operations with about 175employees in Stockholm

1. Number of loans and deposit accounts as of 30 September 20152. Push marketing refers to Nordax sending materials / initiating contact with customers

9

Loans portfolio split by geography (30 Sept 2015)

0,7

1,6

3,2

5

6,3

5,3 5,2

6,6

7,5

8,4

1010,6

2004 05 06 07 08 09 10 11 12 13 14 Q32015

39%

37%

18%

4% 2%

Z

10

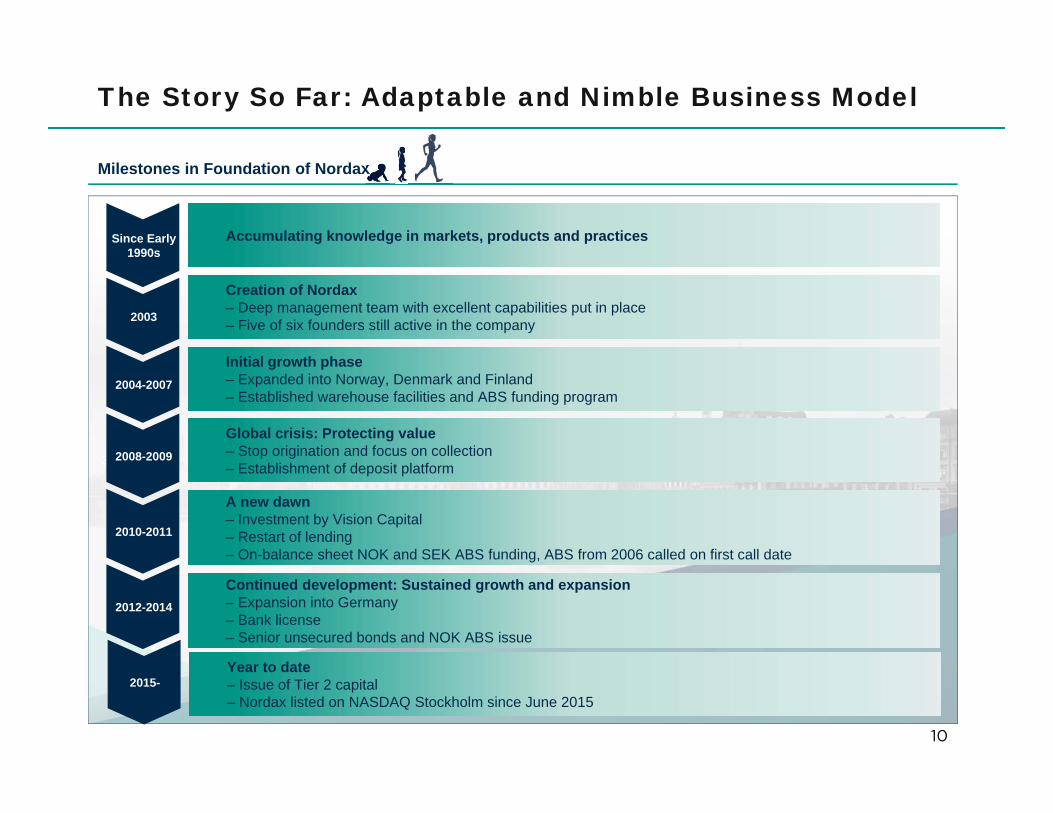

Milestones in Foundation of Nordax

Global crisis: Protecting value – Stop origination and focus on collection– Establishment of deposit platform

Continued development: Sustained growth and expansion– Expansion into Germany – Bank license– Senior unsecured bonds and NOK ABS issue

A new dawn – Investment by Vision Capital– Restart of lending– On-balance sheet NOK and SEK ABS funding, ABS from 2006 called on first call date

Creation of Nordax – Deep management team with excellent capabilities put in place– Five of six founders still active in the company

Initial growth phase – Expanded into Norway, Denmark and Finland– Established warehouse facilities and ABS funding program

Since Early 1990s

Accumulating knowledge in markets, products and practices

2003

2004-2007

2008-2009

2010-2011

2012-2014

The Story So Far: Adaptable and Nimble Business Model

Year to date– Issue of Tier 2 capital– Nordax listed on NASDAQ Stockholm since June 2015

2015-

11

Licensed by the Swedish FSA

• Nordax has been under the Swedish FSA’s regulation since 2004 as a “Credit Market Company”, and received status as a “Bank” in December 2014

• The regulatory status entails fulfilling qualitative and quantitative requirements with regards to compliance, risk management, capital adequacy and governance

• All business carried out from Stockholm and cross-border into Norway, Denmark, Finland and Germany in accordance with EU regulations

• Deposits – Swedish, Norwegian and Finnish – are covered by the Swedish deposit insurance guarantee

• Entitled to offer payment protection insurances to eligible customers in all countries of operations

Risk and Compliance Focus

• Nordax was founded by risk managers and this mentality is still embedded in the business

• As with all lending, risk evaluation is central in the business and Nordax has a low risk tolerance and takes a conservative approach to risk taking

• Risk strategy and risk appetite is decided – and assessed regularly – by the board of directors

• To achieve a robust internal control framework, Nordax has adopted “three lines of defence” which includes risk owners in the business functions, independent compliance and risk control functions, and an outsourced internal audit function

Risk Control Framework

1st Line of DefenseFunctions

2nd Line of Defense

Risk Control Compliance

3rd Line of Defense

Internal Audit

ManagementTeam

CEO

Board ofDirectors

1 2 3

Risk and control environment is a part of day-to-day business -business functions are responsible to measure, control and monitor1

Facilitates and monitor implementation of risk management practises – independence assured through organisational separation

2

Highest level of independence and objectivity to ensure effectiveness of governance risk management and internal control3

Governance, Risk and Control

Highlights of financial development

12

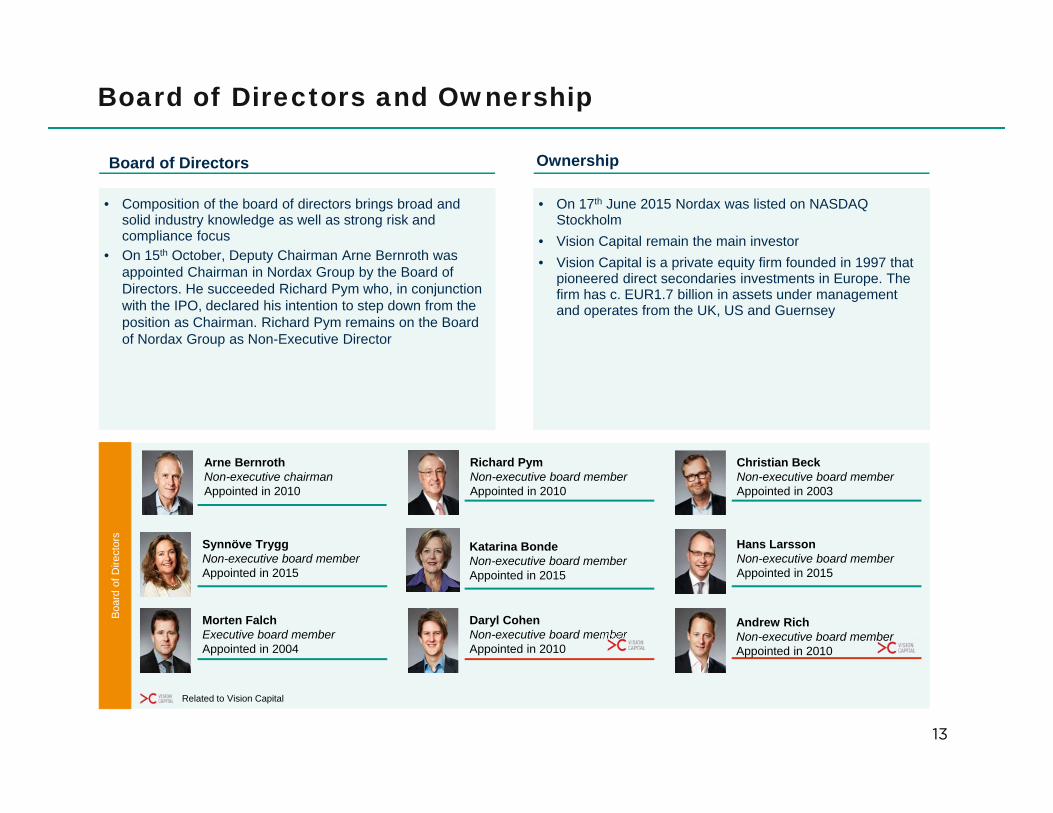

Board of Directors and Ownership

13

Ownership

• On 17th June 2015 Nordax was listed on NASDAQ Stockholm

• Vision Capital remain the main investor• Vision Capital is a private equity firm founded in 1997 that

pioneered direct secondaries investments in Europe. The firm has c. EUR1.7 billion in assets under management and operates from the UK, US and Guernsey

Boa

rd o

f Dire

ctor

s

• Composition of the board of directors brings broad and solid industry knowledge as well as strong risk and compliance focus

• On 15th October, Deputy Chairman Arne Bernroth was appointed Chairman in Nordax Group by the Board of Directors. He succeeded Richard Pym who, in conjunction with the IPO, declared his intention to step down from the position as Chairman. Richard Pym remains on the Board of Nordax Group as Non-Executive Director

Board of Directors

Related to Vision Capital

Richard PymNon-executive board memberAppointed in 2010

Christian Beck Non-executive board memberAppointed in 2003

Arne BernrothNon-executive chairmanAppointed in 2010

Synnöve Trygg Non-executive board memberAppointed in 2015

Katarina BondeNon-executive board member Appointed in 2015

Hans LarssonNon-executive board member Appointed in 2015

Morten FalchExecutive board memberAppointed in 2004

Andrew RichNon-executive board memberAppointed in 2010

Daryl CohenNon-executive board memberAppointed in 2010

14

Z

Funding3

28%

11%

61%

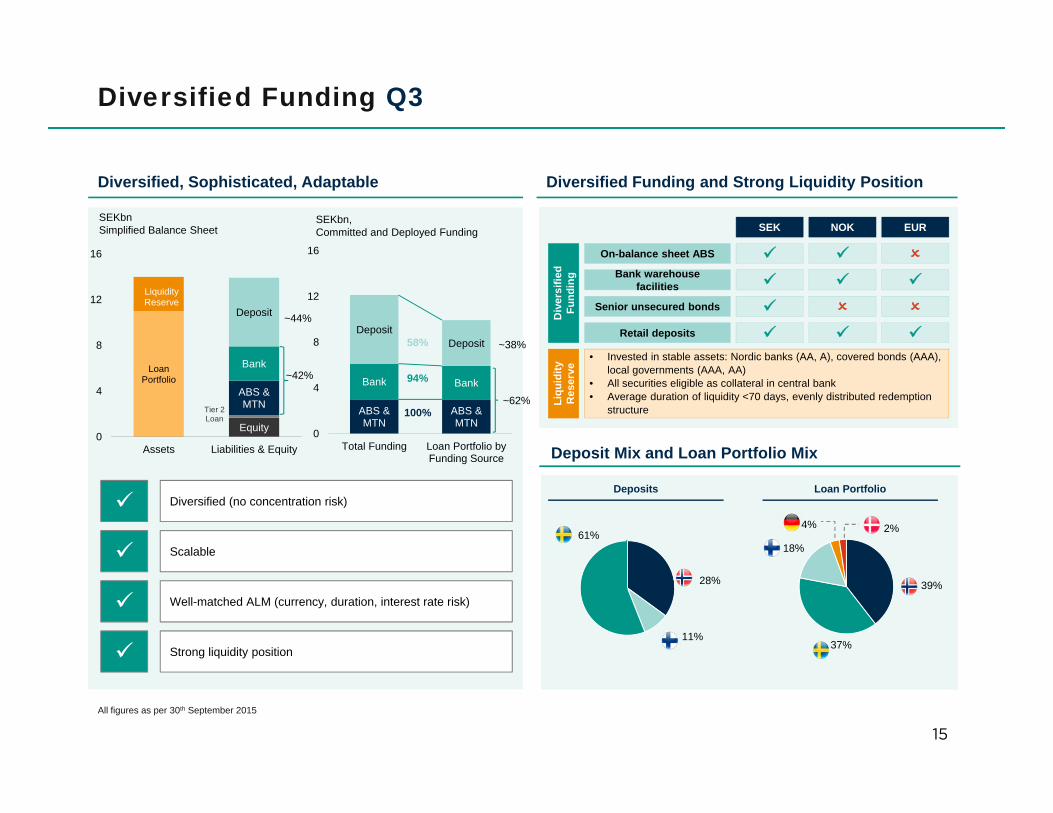

Diversified, Sophisticated, Adaptable

15

Diversified Funding and Strong Liquidity Position

Diversified (no concentration risk)

Scalable

Strong liquidity position

Well-matched ALM (currency, duration, interest rate risk)

Loan Portfolio

Liquidity Reserve

Equity

Tier 2 Loan

ABS & MTN

Bank

Deposit

0

4

8

12

16

Assets Liabilities & Equity

ABS & MTN

ABS & MTN

Bank Bank

DepositDeposit

0

4

8

12

16

Total Funding Loan Portfolio byFunding Source

100%

94%

58%

SEKbnSimplified Balance Sheet

SEKbn, Committed and Deployed Funding

Diversified Funding Q3

~38%

~62%

~42%

~44%

Deposit Mix and Loan Portfolio Mix

Deposits Loan Portfolio

39%

37%

18%

4% 2%

Div

ersi

fied

Fund

ing

SEK NOK EUR

On-balance sheet ABS Bank warehouse

facilities

Retail deposits

Senior unsecured bonds

Liqu

idity

R

eser

ve

• Invested in stable assets: Nordic banks (AA, A), covered bonds (AAA),local governments (AAA, AA)

• All securities eligible as collateral in central bank• Average duration of liquidity <70 days, evenly distributed redemption

structure

All figures as per 30th September 2015

16

Collateralised and Unsecured Funding

Financing Overview

SEK 500m senior unsecured

notes

Nordax Holding

AB(HoldCo)

Nordax Bank AB

(publ)

Nordax Sverige

AB

Nordax Nordic 3

AB (publ)

Nordax Sverige

3 AB (publ)

Nordax Nordic

AB (publ)

Nordax Nordic 2

AB

SEK 250mT2 capital

ABS / SCL II WHWH ABS/ SCL III ABS / SCL IV

Deposits from the general public

Nordax Sverige

4 AB (publ)

ABS/ SCL V

Recurring obligations• Financial reports are disclosed to the market in accordance with the Securities Market Listing Rules issued by the Irish Stock Exchange and the

Rulebook for Debt Issuers issued by NASDAQ Stockholm• In addition, monthly cash management reports for the ABS-deals are published on the SCL webpage and submitted to Bloomberg, relevant rating

agencies etc.

Non-recurring continuing obligations• Regulated information (including inside information/price sensitive information) is released to the market in accordance with Nordax’

Communication Policy

Information to the capital market

• ABS - The Scandinavian Consumer Loan Program is a securitisation program of Scandinavian consumer loans. All issues have been listed on ISE

• SCL was closed on July 6, 2006. Underlying assets constituted by a portfolio of Swedish unsecured consumer loans. SCL was called on first call date on June 15, 2011

• SCL II was closed on July 5, 2011, Norwegian unsecured consumer loans

• SCL III was closed on December 8, 2011, Swedish unsecured consumer loans

• SCL IV was closed on June 5, 2014, Norwegian unsecured consumer loans

• Tier 2 capital, listed on Nasdaq Stockholm, Nordic investor base. Due 2025 and callable from 2020

• Senior unsecured notes listed on Nasdaq Stockholm, Swedish investor base. Due March 2016

Outstanding transactions

Deposits and Liquidity Q3

17

Deposits as a Strategic Funding Source

• Nordax started taking retail deposits in Sweden in January 2009, in Norway in October 2009 and in Finland in February 2011

• In November 2012, a deposit cooperation was launched with Avanza: Sparkonto+ at Avanza’s internet platform

• The products are on-demand, fully variable interest savings accounts • Deposits are mainly marketed via internet search price comparison sites• Nordax is able to adjust customer flows according to needs with high

accuracy• Usage is conservative, targeted liquidity buffer is 40% (limit of 25%) of

total deposited amount• All deposit products – Swedish, Norwegian and Finnish – are covered by

the Swedish deposit insurance guarantee (up to EUR 100,000)

Outstanding Retail Deposits by Country

SEKm

0

1

2

3

4

5

6

7

8

jan-09 jul-09 jan-10 jul-10 jan-11 jul-11 jan-12 jul-12 jan-13 jul-13 jan-14 jul-14

Sweden Norway Finland Sweden via Avanza

Strong Liquidity Coverage and Stable Funding

Actual Q3 2015 Min / Target

LCR 704% Min 60% (Oct 2015)

NSFR 130% Min 100% (2018)

Liquidity Reserve Build-up

Nordic Banks, 52%

Swedish Municipal

Bonds, 32%

Swedish Covered Bonds,

16%

• All investments are rated from A+ to AAA (S&P) with the average rating being AA

• The average maturity is <55 days and all reserves placed with Nordic banks are available on demand and all securities are eligible as collateral with the central bank Total: SEK 2.6bn

Q3 2015, SEKm

17

18

Z

Market and product overview4

Direct marketing (DM,

UDM, Cooperation

Partners)58%

Repeat sales23%

Web and advertising

7%

Brokers/Credit intermediaries

13%

Focus on Direct Distributed Personal Loans

Origination by channel 2014 (by value), Nordax’ all geographical markets

Push marketing –Nordax targets customers

Pull marketing

Up to 15 years maturities (amortising) – typical duration at time of origination ~9 years

Loan sizes up to SEK 400,000 - average original loan size of SEK ~140,000 (1)

Offering also includes payment protection insurance

Average original monthly payment of SEK~2,500

Typical uses: Consolidation and consumption

Clear Product Utility – Longer Duration Allows for Larger Borrowing Amount

191. Original average instalment balance weighted average loan size

Direct Distributed Personal Loans With Clear Product Utility

Closed-ended with option to pre-pay without additional fee and ability to add additional loan Direct

marketing 63%

Other5%

Brokers32%

Channel distribution SCL V, eligibility criteria

Repeat sales in SCL V included in the original origination channel

SEK

20

Key Takeaways Sensitivity to Interest Rate and Duration

• The monthly instalment has a low sensitivity to changes of the interest rate due to the long durations.

– Allows for management and optimisation of margins

• Reveals clear product utility as enables affordable loans of satisfactory size to meet the customer need

9% 10% 11% 12% 13% 14% 15%

7Y 2,655 2,739 2,825 2,913 3,002 3,092 3,184

8Y 2,417 2,504 2,592 2,682 2,773 2,866 2,961

9Y 2,235 2,323 2,413 2,505 2,599 2,695 2,793

10Y 2,090 2,180 2,273 2,367 2,464 2,562 2,662

11Y 1,974 2,066 2,160 2,257 2,356 2,456 2,559

12Y 1,878 1,972 2,068 2,167 2,268 2,371 2,476

13Y 1,798 1,894 1,992 2,093 2,196 2,302 2,409

Dur

atio

n

Interest Rate

Illustrative Nordax loan

Assuming SEK165,000 loan with annuity amortisation

Product Utility

211. Loan customers since re-launch of loan origination in 2010 until 15 January 2015 (at time of application)2. Includes co-applicants who are retired due to disability3. National average household income (should be compared to co applicants)4. Source: Statistics Sweden (2013), Statistics Norway (2012), Statistics Finland (2013) and Statistisches Bundesamt (2010)

Target Prime Customers (1)

€ ‘000, Average annual income

%, Type of employment

%, Home ownership

39

54 43

28

64

88

69

41 31

54

38 36

0

25

50

75

100

60

83 91

50 59

83

69

44

0

25

50

75

100

Single Applicant Co Applicants National Average (4)

%, Age distribution

4

15

33 35

14 7

24

33 26

10

0

12

41 38

8 2

14

39 36

8

0

15

30

45

60

Below 31 31–40 41–50 51–60 Above 60

Nordax Borrowers National Average (4)

84

8 2 5

83

12

14

90

61

4

86

80 6

0

25

50

75

100

Salary Retired Temporary Self employed

Focus on Low Risk Customers… …With Stable and Steady Cash Flows…

…Annual Income Levels Above National Averages… …And Majority of Customers are Home Owners

(2)

(3)

Clear Target Group: Middle-Aged Prime Customers

High Street Banks’ Current Position

Nordic Consumer and Specialty Finance

22

Nordax Well Positioned in Competitive Landscape

High Street BanksBank Focused with Tail of Independent Specialists

Nordax position:

• Leader in direct mail with accumulated experience since the early 90s

• Established proprietary distribution model through DM and Repeat Sales

• Highly scalable model: Operations, Governance, Funding

• Proven credit underwriting model with ability to underwrite large ticket loans

• Model diversified across distribution channels and countriesWhat to expect from the high

street banks going forward?

• High street banks offer unsecured loans, however typically with a different focus than Nordax

– Focus on existing clients and do not focus on Direct Marketing (‘offer rather than market’)

• Product utility differs from Nordax - Banks do not have the same ability to meet customer need: i) right balance, ii) long tenors, and consequently iii) low monthly instalments

• Culture of low tolerance for losses and lending on back of collateral expected to remain

• Have consumer loans as peripheral product to avoid cannibalising on other products

• RoE in retail Segments already in line with Nordax RoE

High level of concentration with the major six players holding the majority of the Nordic market

Large tail of specialists, both local and foreign players

23

Z

Risk management, credit underwriting and operating platform5

Credit Bureau Information

• Available credit bureau information varies between the countries, which impacts the structure of the underwriting processes. • Sweden, Norway and Germany have extensive credit bureau information whereas Denmark and Finland have mostly derogatory

information.• Lack of credit bureau information implies that more verification documents need to be submitted by the customers, which in turn

gives a more manual handling of the applications.

Sweden Norway Denmark Finland Germany

Positive and negative information from the bureau

Positive and negative information from the bureau

Only derogatory information from the bureau

Mostly derogatory information from the bureau

Positive and negative information from the bureau

• 100% match due to unique social security number

• Name and address information (incl. previous addresses and date for change of address)

• 2 years of income and tax information

• Marital status

• Spouse’s social security number

• Property ownership information

• Credit inquiries

• Credit history (balance, type of credit, number of credits)

• Bad debt information

• Generic score

• 100% match due to unique social security number

• Name and address information (incl. date for change of address)

• 2 years of income and tax information

• Marital status

• Bad debt information

• Generic score

• Property ownership information

• 100% match due to unique social security number

• Name and address information

• Bad debt information

• 100% match due to unique social security number

• Name and address information, incl. time at address

• Marital status

• House ownership

• Bad debt information

• Match on name, address and date of birth – 90-95% match

• Name and address information –current and previous address

• Credit information – number of loans, type of loans, balance at origination, opening date and duration

• Bad debt information

• Generic score

No verification required by the customer

• Verification by the customer:

• Debt information verified throughtax return

• Salary slip required to confirm income and to detect wage garnish

• Verification by the customer:

• Income- and debt information verified through salary slip and tax return submitted by the customer

• Verification by the customer:

• Income- and debt information verified through salary slip and tax return submitted by the customer

• Verification by the customer:

• Income- and debt verification through salary slip and bank account statement submitted by the customer

24

Traceability

In the Nordics, traceability is very high due to the linkage between an individual’s national ID number and nearly all facets of its public life

Uses of national ID number in Sweden

Change address

Job change

Public support

Healthcare

Subscribe to a service

Making payments

Bank and insurance

Tax, police and legal system

The Swedish national ID number consist of 10 digits, where the first 6 are date of birth, and shown on ID-cards and drivers’ licenses

• Necessary to officially register a change of address

• Employers require it in order to disburse salary and pay taxes

• Needed to receive parental subsidies, unemployment benefits, student grants/loans

• Required to access public health system (private alternatives are very expensive)

• Required as identification by the authorities

• Legally required to open a bank account, get a mortgage, buy insurance

• Required for mobile phones, cable television and basic utilities contracts

• It is customary to require ID with national ID number when paying with credit cards without PIN

Example:

Swedish national ID number

25

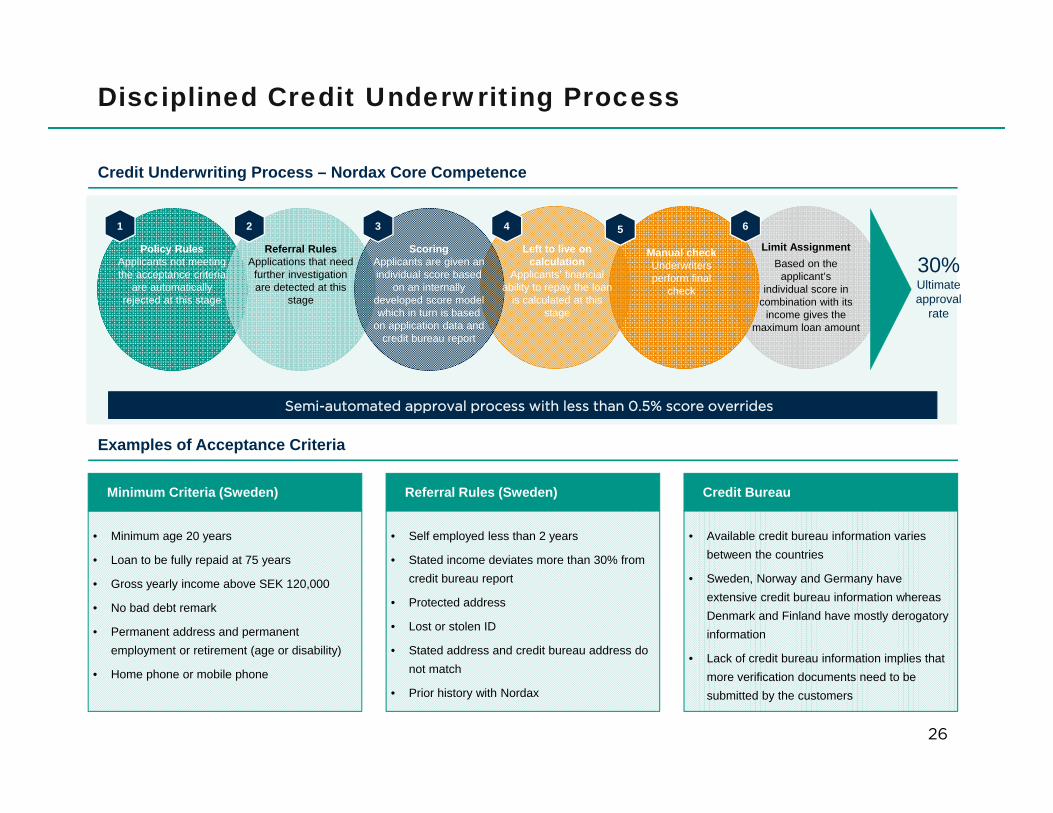

Disciplined Credit Underwriting Process

26

Credit Underwriting Process – Nordax Core Competence

Examples of Acceptance Criteria

• Minimum age 20 years

• Loan to be fully repaid at 75 years

• Gross yearly income above SEK 120,000

• No bad debt remark

• Permanent address and permanent employment or retirement (age or disability)

• Home phone or mobile phone

Minimum Criteria (Sweden) Referral Rules (Sweden) Credit Bureau

• Self employed less than 2 years

• Stated income deviates more than 30% from credit bureau report

• Protected address

• Lost or stolen ID

• Stated address and credit bureau address donot match

• Prior history with Nordax

• Available credit bureau information varies between the countries

• Sweden, Norway and Germany have extensive credit bureau information whereas Denmark and Finland have mostly derogatory information

• Lack of credit bureau information implies that more verification documents need to be submitted by the customers

Semi-automated approval process with less than 0.5% score overrides

Policy RulesApplicants not meeting the acceptance criteria

are automatically rejected at this stage

Referral RulesApplications that need

further investigation are detected at this

stage

Scoring Applicants are given an individual score based

on an internally developed score model which in turn is based

on application data and credit bureau report

Left to live on calculation

Applicants’ financial ability to repay the loan

is calculated at this stage

Limit AssignmentBased on the

applicant’sindividual score in

combination with its income gives the

maximum loan amount

4321 6

30%Ultimate approval

rate

5

Manual checkUnderwriters perform final

check

27

Major Underwriting Changes from 2012 and Onwards

Type of Underwriting Changes 2012-> Reason for ChangeDate of Change

New scorecard implemented Enough data has been gathered in order to develop a model adjusted for different sourcing channels. In connection with the new scorecard the score cut off for Freedom Finance has been increased

May 2012

Organizational change The Underwriting department has moved organizationally from Credit risk to Operations

September 2012

Introducing an additional credit bureau - Bisnode Bisnode have additional information such as sms loan inquiries March 2014

New scorecard implemented The model has been adjusted to the new information from Bisnode

March 2014

Increase of score cut off for Freedom Finance To reduce the risk and align it to the DM channel March 2014

Launch of SEK 400,000/15 years SEK 400,000 will be offered to low risk customers with high income

May 2014

Introducing affordability calculation Requirements from authorities and increased focus on affordability, to ensure that the customer has the ability to repay the loan

December 2014

Adjustments in scorecard Adjustment of current scorecard based on performance February 2015

Major underwriting changes are preceded by a decision in the Credit Risk Forum. Changes that potentially have negative impact on credit risk always need approval from the board

28

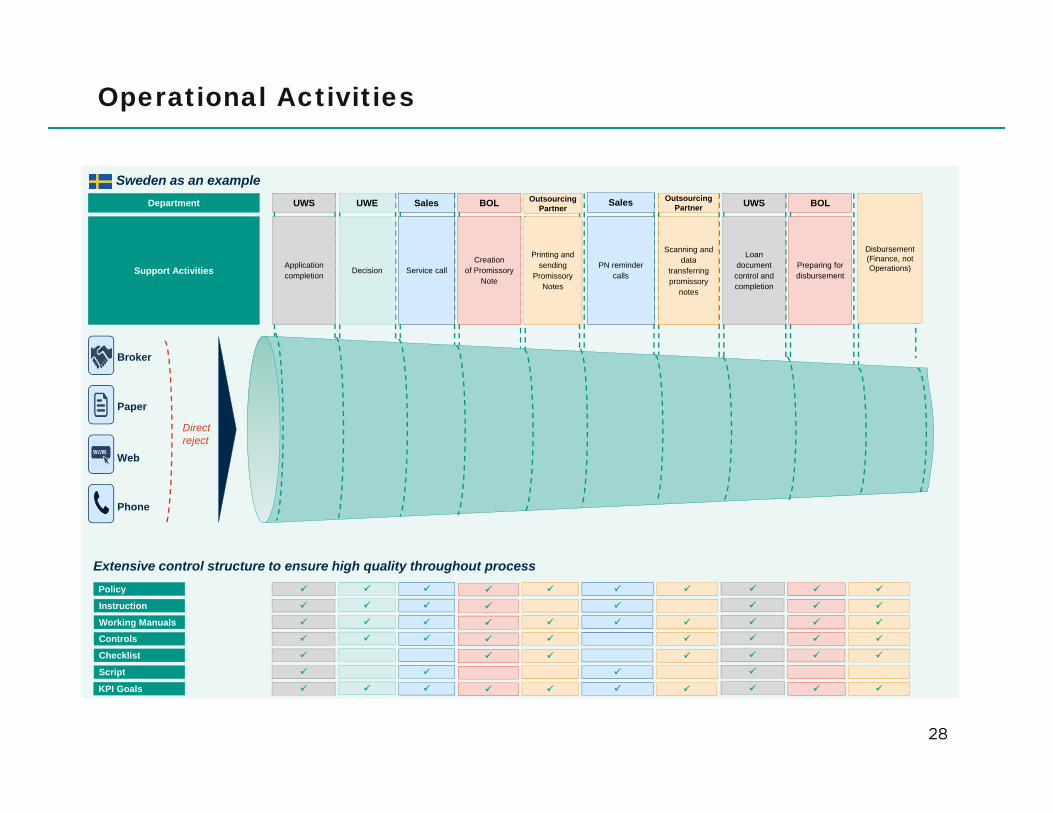

Operational Activities

Extensive control structure to ensure high quality throughout process

Broker

Paper

Web

Phone

Department

Support Activities

Printing and sending

Promissory Notes

UWS

Applicationcompletion

UWE

Decision

Sales

Service call

BOL

Creation of Promissory

Note

Sales

PN reminder calls

UWS

Loan document control and completion

BOL

Preparing for disbursement

Outsourcing Partner

Scanning and data

transferring promissory

notes

Outsourcing Partner

Direct reject

Disbursement (Finance, not Operations)

Policy

Instruction

Working Manuals

Controls

Script

Checklist

KPI Goals

Sweden as an example

29

Key Success Factors

Overview of Collection Strategy

Internal collections strategy includes using a collection score model and focus on treating customers fairly

Nordax carries out internal collections for up to 100 days, after which the collection process is outsourced

Well balanced curing measures

Call client; a semi-automated dialler that prioritize calls based on a collection scoring model

Close DCA management and measuring of performance

Committed team, a flexible temporary pool and an efficient incentive program

Early reach out call to customers that has fallen behind on payment (grace calls)

Arrears level

External collections agency (DCA)Internal collections

Days Past Due

Prioritisation

Collection Action

Individual Handling

0-10 11-40 71-10041-70

Collection callsReminder letters

E-mail / SMSCuring measures

DCA prioritization model

DCA prioritization model

101-130 131-160

First Payment DefaultCollection score

First Payment DefaultCollection score

101-130 131-180

1 2 3 4 5 6

Champion/challenger strategyIndividual budgets

Monthly performance phone meetingsCampaigns

First Payment DefaultCollection score

Service calls E-mail / SMS

Booked as a write-down/financial loss

Efficient Collection Platform

30

Seizure of Property (1)

Seizure of Salary

n/a

Period of Limitation

(Years)

15 (absolute limitation from first collection

effort)

10(prolonged by legal actions or debtor)

30(with court title – can

be renewed by legal actions)

10 (prolonged to infinity

by notification or payment)

10 (prolonged to infinity

by notification or payment)

Prioritization

1. Tax, child support etc.

2. Proportional collection between creditors

1. Tax, child support etc.

2. Creditors first in line is first to collect

1. Tax, child support etc.

2. Creditors first in line is first to collect

1. Tax, child support etc.

2. Creditors first in line is first to collect

1. Tax, child support etc.

2. Proportional collection between creditors

Recovery Rates

(expected recovery by

region)

94%

18%

TBD

76%

84%

Debtor Incentives

• High penalty fees• Derogatory information available and a remark

stays for 2 years (can be renewed)• Negative info results in problems getting new

credit, phone subscriptions, rental agreements, etc.

• Derogatory information in terms of blacklist and remark stays for 5 years if not repaid

• No major impact of negative remark, except for new credit

• Medium high fees

• Negative remarks in Schufa remain until settled plus 3 years after settlement

• Negative info results in problems getting new credit, phone subscriptions, rental agreements, etc.

• Possible imprisonment to ensure seizure, if incorrectly sworn oath regarding assets

• Derogatory information available and payment remark stays for 4 years

• Negative info results in problems getting new credit, phone subscriptions, rental agreements, etc.

• Extensive derogatory information available, and a remark stays for 3 years

• Negative info results in problems getting new credit, phone subscriptions, rental agreements, etc.

• Low penalty

Lender Friendly Legal Collection Environment in Nordic Markets

n/a

Efficiency Management

Official / governmental body

1. All available but not always efficient for unsecured consumer credit2. Efficient if seizure of salary fails due to the exempt threshold for earned income and as means of pressure for voluntary solutions

(2)

Backup Servicing

31

Emric

• Emric has 185 employees and 75 individual banks and financial companies as clients. • 60 full time employees working with servicing operations for 45,000 loan customers in Kalix (northern Sweden). • Emric offers lenders and banks business knowledge, product solutions and managed services within leasing and lending. • Services provided are processing services, portfolio management services (customer service, accounting, reporting,

administration, arrears management and payments), SaaS and hosting services as well as standby services..

Servicing and standby

servicing clients

• Servicing clients: Avanza Bank, Bluestep, Danske Bank, Deutsche Leasing, Carnegie, Resurs Bank, Stanley, Nordnet, Svensk Hypotekspension and Retail Finance.

• Rated transactions where Emric is standby servicer: Nordax Bank (Scandinavian Consumer Loans IV) rated by S&P and Fitch, Bluestep (Bluestep Mortgage Securities No. 2 Limited) rated by S&P and Svensk Hypotekspension (Svensk Hypotekspension Fond 1 AB (publ)) rated by Fitch.

Servicing take over procedure

• The stand-by servicing agreement entails clear timelines according to which Emric must undertake certain steps. Within 20 days Emric will perform under the servicing agreement.

• Lifecycle management of portfolio (Excluding Cash Management Services)• No system integration needed to Nordax system to perform the Services, full access to current IT system (Entra card) with

Tieto.12 months agreement with Tieto, enabling a controlled migration. • Emric will inform the Swedish Supervisory Authority (FI), the storage company (Recall) and third party providers e.g. debt

collection agencies, printing house of it’s appointment as servicer.• Emric may not terminate the stand-by servicing agreement without giving at least 6 months’ notice and finding a

satisfactory substitute stand-by servicer.• Emric has the right to receive all necessary information required in accordance with the data protection act.

Emric Services (Emric Finance Process Outsourcing AB) will act as standby servicer in SCL V

32

Z

Appendix6

33

The Organisation

Legal (3)

Treasury (7)

Accounting and Control (14)Operations (117)Marketing (9)Credit Risk and MIS (9)

Investor Relations (1)

IT and Security (20)

Decision Science (2)

Annual General MeetingExternal Audit

Internal Audit

Compliance (2)

Risk Control (2)

Board of Directors

Remuneration Committee

Risk Committee

CEO and Executive Management (7)

HR (3)

Nomination Committee

Audit Committee

• Underwriting evaluation: Responsible for making credit decisions, including interest negotiations

• Underwriting support:Responsible for loan application completion and performs loan document controls

• Front office: Manages all inbound calls from loans and deposits. Responsible for customer relationship management and sales, servicing new and existing customers

• Sales: Manages outbound sales calls to new and existing customer. Provides sales and service to new and potential loan customers, including interest negotiations

• Back office - Loan:Responsible for administrative tasks related to loan process, from application to disbursement and account management

• Back office - Deposit:Responsible for administrative tasks related to deposit customers, such as new accounts, withdrawals and account management

• Payment consulting:Reaches out to distressed loan takers in order to help them and minimize future financial losses.

• Legal collection:Manages advanced delinquency cases and outsourced debt collection activities to maximize recovery

Operations Director (1)

Deputy Operations Director (1)

Team Managers (8)

Operating Outsourcing Partners (7)

Debt Collection Partners (10)

Business Support (1)

Performance Manager (1)

Business Development Mgr (1)

Process Manager (1)

Maintenance Manager (1)

Risk and Compliance Mgr (1) First Line Risk and Compliance (3)

CollectionsBack OfficeFront OfficeUnderwriting

UWE (11)

Team Specialists(2)

UWS (10) FO (19) BOL (12)

Team Specialist (1)

BOD (7)

Team Specialist (1)

PCT (16) LC (7)

Team Specialist (2)

Training Expert (1)

Sales (7)

Team Specialist (2)

Business core functions

Underwriting

Front Office

Back Office

Collections

175 fulltime employees

Affordability Calculation

Left to Live on Calculation

• Calculation of ability to pay back the loan

• Calculation setup varies across countries, but general assumptions include costs of housing, loans and living expenses

Debt Burden Ratio

• Calculated as total debt to gross annual income to ensure secure relationship between income and debt

• Allowed maximum levels vary across risk classes

Max Unsecured Debt

• Additional rules related to the absolute levels of unsecured debt

Sweden

Limit Assignment

Yearly Gross Income SEK for One Applicant

Nordax Score

0–580

581–640

641–690

691–740

741+

120,000–180,999

-

50 000

50 000

100 000

100 000

181,000–240,999

-

50 000

100 000

200 000

200 000

241,000–300,999

-

50 000

150 000

250 000

300 000

301.000+

-

150 000

250 000

400 000

400 000

34

Affordability and Limit Assignment

• Based on risk score and income

• Varies by country

• Will depend on joint or single applicants

SEK = Maximum amount to be approved

Solid Routines to Prevent Fraud

35

Low Actual Fraud Experience

1. Only external controls

Description Number of ChecksResponsible Function

Pre-Processing

Rules that are automatically checked when an application is entered in the application processing system

7Credit Specialist Team

Underwriting

Underwriters presented with different flags and queues from the decision tree in application form that indicate possible fraud

13Underwriting Evaluation

Loan Agreement

Loan agreement is sent to the customers’ verified address

1Back Office

DocumentControl

Together with the loan agreement, customer needs to send in a valid ID

2Back Office

DisbursementControl

Internal and external fraud controls. Some checks are also done to verify that UW has performed the controls needed

7 (1)Economy

Fraud Statistics Overview

Fraud cases since start of business

Active cases, non written off #

Active cases, written off # Paid off

7 46 11

3 25 2

3 14 0

1 0 0

36

Curing Measures – Help Customers Suffering Temporary Payment Difficulties

Curing tools are available for customers with temporary problems, but are applied cautiously and never for the purpose of pushing losses into the future

Waiveof Late Fee

DurationExtension

Capitalisation

Payment Plan

Interest Rate

Reduction

• Offered to customers in arrears level 1-3

• Waive one or more late fees to motivate the customer to become current

• Offered to customers in arrears level 1-3 who are squeezed due to set backs or duration set too short at origination

• Total duration can never exceed 15 years from the latest disbursement

• Only done once during a loan’s lifetime and shall be documented by an amendment agreement.

• All amounts in arrears are capitalized, giving the customer a current status

• Offered to customers in arrears level 1-2 (other than in connection with payment plans)

• Only done once during a loan’s lifetime and shall be documented by an amendment agreement

• Offered to customers with temporary problems, can last for a maximum of 6 months

• Should be reserved to customers in arrears level 3 throughout the period of the agreed payment plan

• Monthly payments reduced to min. 50% of interest amount incurred per month. Arrears amount can be capitalized . Only done once during a loan’s lifetime and shall be documented by an amendment agreement

• Max reduction 2%; encourages the customer to perform according to the original agreement

• Normally used in combination with capitalization or payment plan

• Only done once during a loan’s lifetime and shall be documented by an amendment agreement

No Limit

No Limit

Up to 3% of total portfolio per annum

Max 0.75% of portfolio at any time

Extremely Rare(<30 cases to date)

a

b

c

d

e

Limit of Cases

37

License Matters

• Granted license to conduct financing business in January 2004 and to conduct banking business in December 2014 by the SFSA• Conducts cross-border consumer lending in Norway, Denmark, Finland and Germany through platform in Stockholm, in accordance

with the European Parliament and Council Directive 2013/36/EU of 26 June 2013 on access to the activity of credit institutions and the prudential supervision of credit institutions and investment firms

• Retail deposit taking in Sweden and licensed (through pass porting) for cross-border deposit taking in Norway and Finland. All deposit products are confirmed to be covered by the Swedish deposit insurance scheme by the Swedish National Debt Office

• Licensed as tied insurance intermediary with the Swedish Companies Registration Office and is through pass porting entitled to offer PPI in all countries of business

Corporate Governance

• Banking limited liability company governed by, inter alia, the Swedish Companies Act, the Swedish Banking and Financing Business Act, the Swedish Deposit Insurance Act, and its Articles of Association

• Subject to the supervision of the SFSA and governed by the official regulations and guidelines issued by the SFSA, and technical standards and guidelines issued by the European Banking Authority, ESMA etc.

• Pursuant to the capital requirements regulation and directive (CRR/CRD IV), Nordax is obliged to comply with regulatory capital requirements. Nordax is also subject to ownership and management assessment by the SFSA.

• Day-to-day management is governed by internal governing documents including, inter alia; the rules of procedures for the Board, instructions for the CEO, the risk management policies, the credit policies, collection and provisioning policies, the remuneration policy, the outsourcing policy, the liquidity contingency plan and the complaints management policy

Local Regulatory Framework

• Nordax’ operations are subject to legislation, regulations, codes of conduct etc. in the jurisdictions in which it conducts business and in relation to the products it markets and sells

• To ensure compliance with applicable local regulatory framework including, inter alia, consumer protection legislation, Nordax has appointed prominent local law firms as advisors in each market. Through these law firms, Nordax receives quarterly regulatory updates and matter-specific advice

New Legislation

• Nordax operates in an area of business with great focus on regulations and with many initiatives for regulatory changes• To meet the intensified regulatory environment, Nordax has built an organizational structure with three line of defense, works efficiently

with Audit, Risk, and Remuneration Committees, independent Compliance and Risk Control functions and outsourced Internal Audit function. Nordax also obtains quarterly regulatory updates on new or proposed regulations, court rulings, official guidelines etc. from local law firms in all markets

Litigations

• Neither Nordax, nor any other member of the Nordax group, is subject to any material court or administrative proceedings which could have a significant adverse effect on Nordax’ financial position or profitability, nor is it subject to any investigation or any review by regulators.

• Members of the Nordax group are however parties to lawsuits and other disputes from time to time in the course of their normal operations, e.g. collection matters

Overview of Compliance and Legal Matters

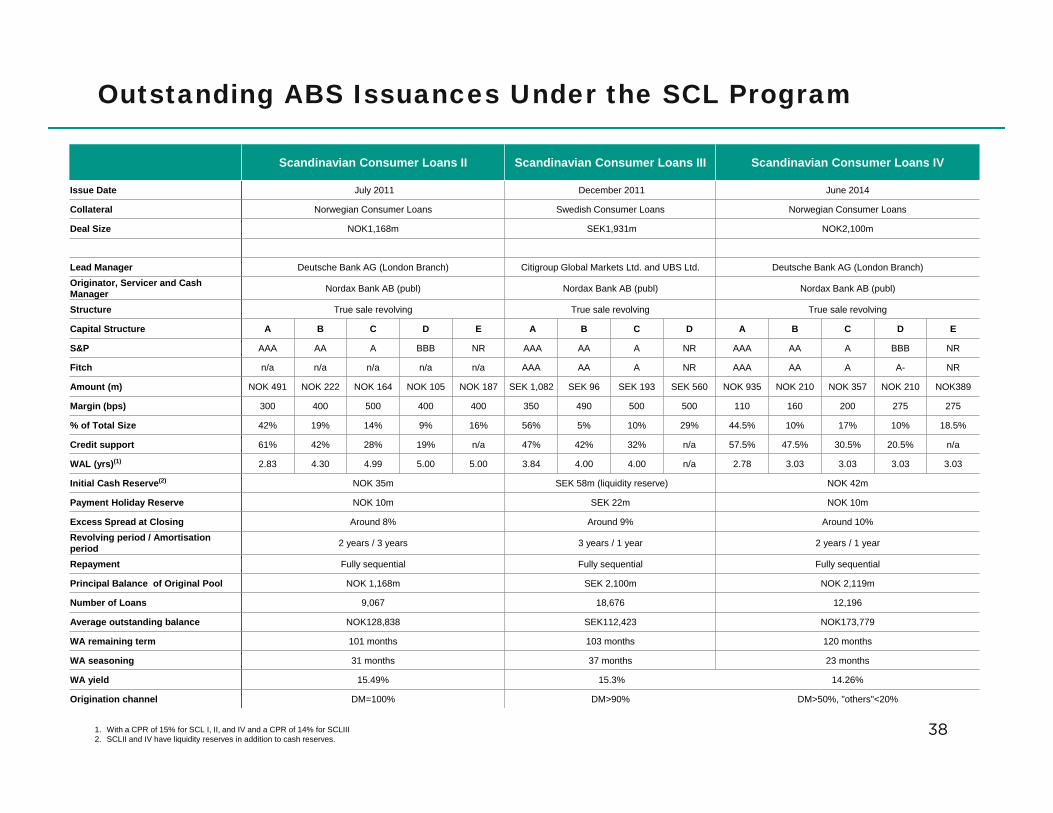

Scandinavian Consumer Loans II Scandinavian Consumer Loans III Scandinavian Consumer Loans IV

Issue Date July 2011 December 2011 June 2014

Collateral Norwegian Consumer Loans Swedish Consumer Loans Norwegian Consumer Loans

Deal Size NOK1,168m SEK1,931m NOK2,100m

Lead Manager Deutsche Bank AG (London Branch) Citigroup Global Markets Ltd. and UBS Ltd. Deutsche Bank AG (London Branch)

Originator, Servicer and Cash Manager Nordax Bank AB (publ) Nordax Bank AB (publ) Nordax Bank AB (publ)

Structure True sale revolving True sale revolving True sale revolving

Capital Structure A B C D E A B C D A B C D E

S&P AAA AA A BBB NR AAA AA A NR AAA AA A BBB NR

Fitch n/a n/a n/a n/a n/a AAA AA A NR AAA AA A A- NR

Amount (m) NOK 491 NOK 222 NOK 164 NOK 105 NOK 187 SEK 1,082 SEK 96 SEK 193 SEK 560 NOK 935 NOK 210 NOK 357 NOK 210 NOK389

Margin (bps) 300 400 500 400 400 350 490 500 500 110 160 200 275 275

% of Total Size 42% 19% 14% 9% 16% 56% 5% 10% 29% 44.5% 10% 17% 10% 18.5%

Credit support 61% 42% 28% 19% n/a 47% 42% 32% n/a 57.5% 47.5% 30.5% 20.5% n/a

WAL (yrs)(1) 2.83 4.30 4.99 5.00 5.00 3.84 4.00 4.00 n/a 2.78 3.03 3.03 3.03 3.03

Initial Cash Reserve(2) NOK 35m SEK 58m (liquidity reserve) NOK 42m

Payment Holiday Reserve NOK 10m SEK 22m NOK 10m

Excess Spread at Closing Around 8% Around 9% Around 10%

Revolving period / Amortisation period 2 years / 3 years 3 years / 1 year 2 years / 1 year

Repayment Fully sequential Fully sequential Fully sequential

Principal Balance of Original Pool NOK 1,168m SEK 2,100m NOK 2,119m

Number of Loans 9,067 18,676 12,196

Average outstanding balance NOK128,838 SEK112,423 NOK173,779

WA remaining term 101 months 103 months 120 months

WA seasoning 31 months 37 months 23 months

WA yield 15.49% 15.3% 14.26%

Origination channel DM=100% DM>90% DM>50%, "others"<20%

Outstanding ABS Issuances Under the SCL Program

1. With a CPR of 15% for SCL I, II, and IV and a CPR of 14% for SCLIII2. SCLII and IV have liquidity reserves in addition to cash reserves.

38

39

Cumulative Write-Off

Swedish Loan Portfolio (1)

1. The 2009 Cumulative Write-Off curve has not been included as it is based on a significantly small population and therefore is not representative. The vintages are modelled using the close-restart method i.e. if a customer takes an add-on loan the old loan is closed.

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 61 65 69 73 77 81 85 89 93 97 101 105 109 113 117 121 125 129

2004 2005 2006 2007 2008 2010 2011 2012 2013 2014 2015

40

Cumulative Write-Off per Origination Channel

Other Selective Loan Eligibility Criteria

Direct Mail Broker

• Origination Channel: i. Originated via Direct Mail will be not less than 63%ii. Originated via Broker will not be more than 32%iii. Originated in Other channels (different than Direct Mail and Broker) will not

represent more than 5%iv. No broker originated promissory notes prior 01/09/2012• Maximum Maturity: Maximum Legal Maturity of 15 years and 1 month• Minimum Term: Minimum Remaining Legal Maturity of 1 month• Weighted Average Remaining Term: The Weighted Average Remaining Term

of Portfolio will be no more than 7% greater than the Weighted Average Remaining Term of the Portfolio as the Final Pool Cut Date

• Loan Value: maximum principal outstanding of SEK 420,000• High Value loans: no more than 35% of Promissory Notes with a principal

amount outstanding in excess of SEK 320,000• Direct Debit: at least 70% of Promissory Notes customers pay via DD• Risk Class E: No greater than 0% of Portfolio• Risk Class D : % of Promissory Notes (by balance) no greater than 15%• Risk Class C and D: % of Promissory Notes (by balance) no greater than 60%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 61 65 69 73 77 81 85 89 93 97 101

105

109

113

117

121

125

129

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 61 65 69 73 77 81 85 89 93 97 101

105

109

113

117

121

125

129

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 61 65 69 73 77 81 85 89 93 97 101

105

109

113

117

121

125

129

41

Cumulative Write-Off per Risk Class of Loan

Class C

(1) The percentage of Promissory Notes in the Portfolio (by balance) falling in Risk Class D cannot be greater than 15% of the total Portfolio, as per Loan Criteria(2) The Cumulative Write-Off of years 2004, 2005 and 2006 for Class D Loans have not been included due to their non representative reduced size

Class D(1,2)

Class A Class B

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 61 65 69 73 77 81 85 89 93 97 101

105

109

113

117

121

125

129

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 61 65 69 73 77 81 85 89 93 97 101

105

109

113

117

121

125

129

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 61 65 69 73 77 81 85 89 93 97 101

105

109

113

117

121

125

129

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 61 65 69 73 77 81 85 89 93 97 101

105

109

113

117

121

125

129

42

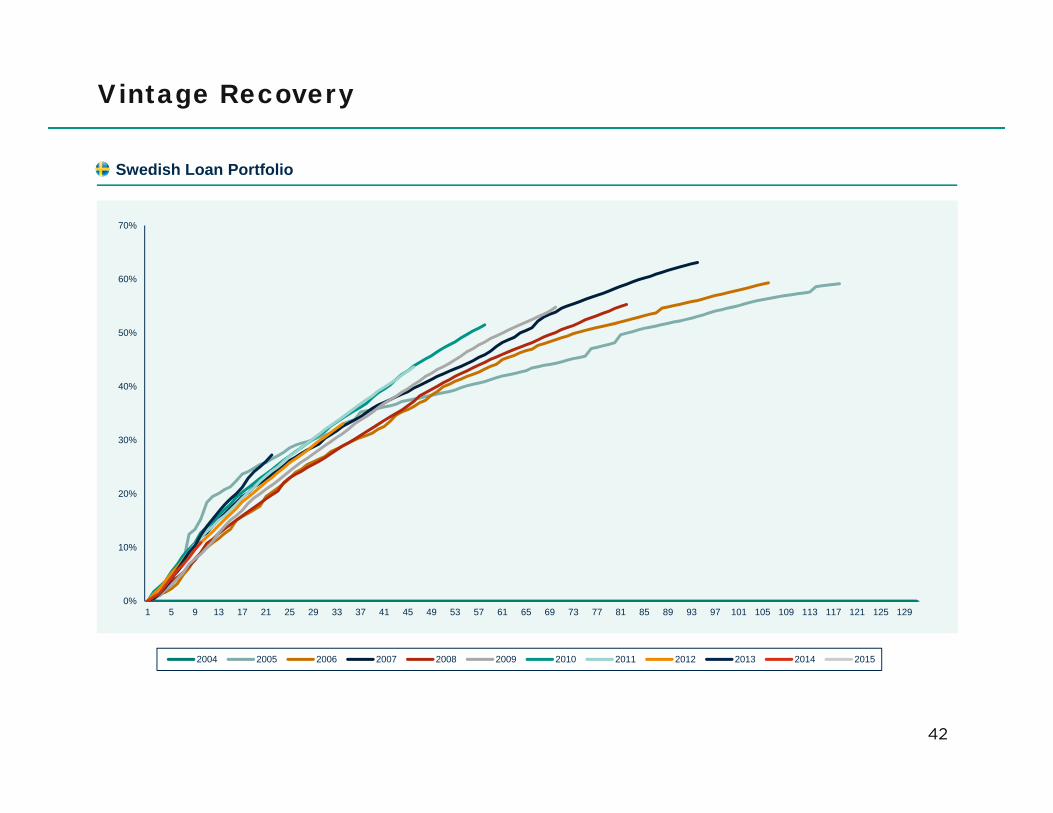

Vintage Recovery

Swedish Loan Portfolio

0%

10%

20%

30%

40%

50%

60%

70%

1 5 9 13 17 21 25 29 33 37 41 45 49 53 57 61 65 69 73 77 81 85 89 93 97 101 105 109 113 117 121 125 129

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

43

Delinquencies and Prepayment

Prepayment

Delinquencies

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0% 30+ dpd 60+ dpd 90+ dpd

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

35,0%

44

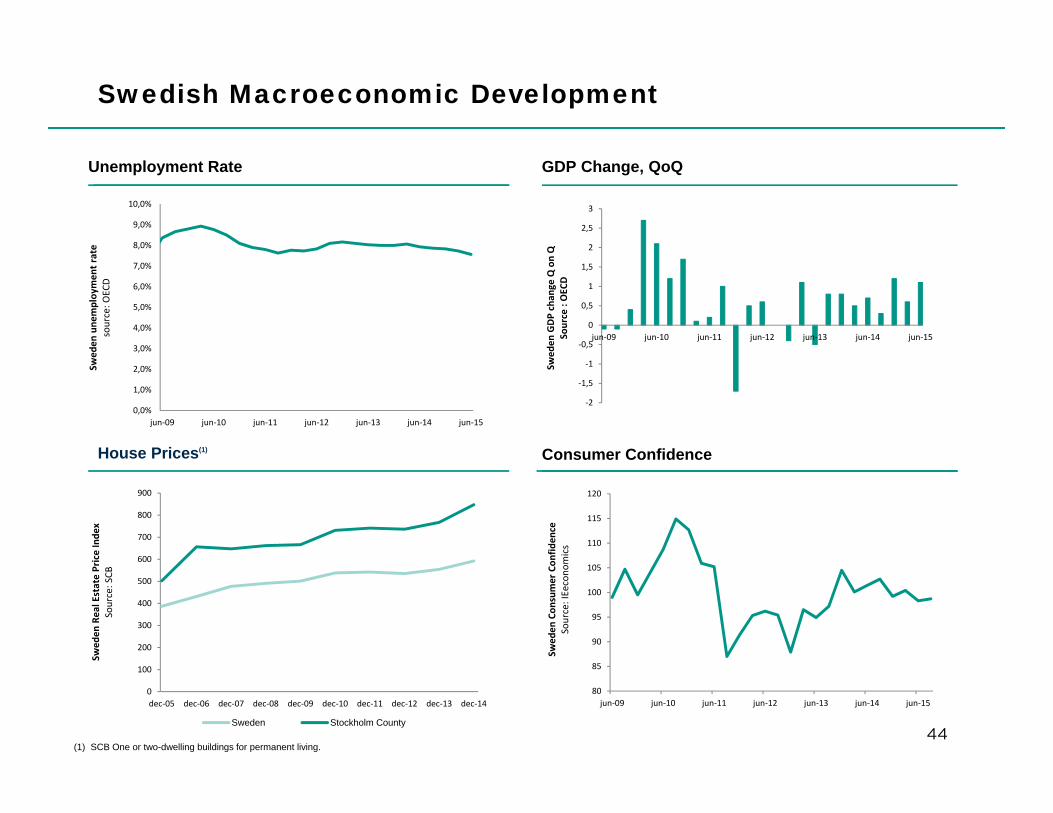

Swedish Macroeconomic Development

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

8,0%

9,0%

10,0%

jun‐09 jun‐10 jun‐11 jun‐12 jun‐13 jun‐14 jun‐15

Swed

en une

mploy

men

t rate

source: O

ECD

‐2

‐1,5

‐1

‐0,5

0

0,5

1

1,5

2

2,5

3

jun‐09 jun‐10 jun‐11 jun‐12 jun‐13 jun‐14 jun‐15

Swed

en GDP chan

ge Q on Q

Source : OEC

D

0

100

200

300

400

500

600

700

800

900

dec‐05 dec‐06 dec‐07 dec‐08 dec‐09 dec‐10 dec‐11 dec‐12 dec‐13 dec‐14

Swed

en Real Estate Price Inde

xSource: SCB

Sweden Stockholm County

House Prices(1)

(1) SCB One or two-dwelling buildings for permanent living.

80

85

90

95

100

105

110

115

120

jun‐09 jun‐10 jun‐11 jun‐12 jun‐13 jun‐14 jun‐15

Swed

en Con

sumer Con

fiden

ceSource: IEecono

mics

Consumer Confidence

Unemployment Rate GDP Change, QoQ