Embed Size (px)

Citation preview

1

Investor PresentationMay – July 2018

2

Safe Harbor Statement & Disclosures

This presentation includes forward-looking comments subject to important risks and

uncertainties. It may also contain financial measures that are not in conformance with

accounting principles generally accepted in the United States of America (GAAP).

Refer to Deere’s reports filed on Forms 8-K (current), 10-Q (quarterly), and 10-K (annual) for

information on factors that could cause actual results to differ materially from information in this

presentation and for information reconciling financial measures to GAAP. Past performance may

not be representative of future results.

Guidance noted in the following slides was effective as of the company’s most recent earnings

release and earnings call (18 May 2018). Nothing in this presentation should be construed as

reaffirming or disaffirming such guidance.

This presentation is not an offer to sell or a solicitation of offers to buy any of Deere’s securities.

3

Table of Contents

Slide

John Deere Strategy 4

Use-of-Cash 17

Global Markets 22

John Deere Financial Services 33

Agriculture Fundamentals 38

Construction & Forestry Fundamentals 44

Appendix 49

4

John Deere Strategy

5

6

Exceptional Operating Performance - OROAEquipment Operations

* Operating Return on Operating Assets** Shareholder Value Added; for reconciliation to GAAP see “SVA* Reconciliation to GAAP” slide in Appendix

21.0% OROA* in 2017

12%

20%

28%

2001

2002

2003

2004

20052006

20072008

2009

2010

2011

2012

2013

2014

20152016

2017

-10%

0%

10%

20%

30%

40%

12% OROA (SVA** Neutral)

% of Mid-Cycle Volume

80% 100% 120%

7

Exceptional Operating Performance – SVAEquipment Operations

* Shareholder Value Added; for reconciliation to GAAP see “SVA* Reconciliation to GAAP” slide in Appendix

$1.2 billion SVA* in 2017

-$2,000

-$1,000

$0

$1,000

$2,000

$3,000

$4,000

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

$ M

illions

Adoption of SVA Model

8

Exceptional Operating Performance – Net Cash FlowEquipment Operations

* Shareholder Value AddedNote: Over $8 billion in Pension/OPEB contributions from 2001-2017

$2.4 billion Net Cash Flow in 2017

$0

$1,000

$2,000

$3,000

$4,000

$5,000

1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

$ M

illions

Sale of Trade Receivables to John Deere Financial

Adoption of SVA* Model

9

Asset Management

Receivable level in 2017 lower than 1998, with more than 2x the sales

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

Trade Receivables Net Sales

$ M

illions

1998 2017

10

Productivity Improvement

Net Sales and Revenues per Employee

$0

$100

$200

$300

$400

$500

$600

$700

1989 1993 1997 2001 2005 2009 2013 2017

$ T

housands

~ 5% CAGR* over 30 years

* Compound Annual Growth Rate

11

Investment in New Products and Technologies

Source: Deere & Company and competitor SEC filings

0%

2%

4%

6%

8%

$0

$300

$600

$900

$1,200

$1,500

$1,800

2003 2005 2007 2009 2011 2013 2015 2017

Deere R&D $ Deere % Competitor A % Competitor B %

Consistently spending at or above competition on technology and innovation

R&D as Percent of Net Sales

$ M

illions

12

Automated. Easy to Use. More Precise.Bigger. Faster. Stronger.

Next Frontier of AgricultureTraditional Agriculture

13

Precision AgThe Future of Farming Has Always Been Led by John Deere

Our commitment to game-changing innovation makes farming easier, smarter and more precise

14

Better machine performance

Precision AgEquipment + Technology + Services

Better job performance Better agronomic decisions

– Ensure machines function as expected

– Maximize machine performance & uptime

− John Deere Connected Support uses predictive analytics to generate notifications and repair instructions to minimize machine downtime

– Ease of use increases operator consistency

– Ensure best outcome for each pass across the field

– Coordinate machines to execute jobs more effectively and efficiently

– Monitor job progress and adjust operational plans in near real time

– See, collaborate and direct information when needed and where needed with an online set of tools

– Automate collection and transfer of data from the machine to platform

– Manage the farm from anywhere and any device

15

+Precision Ag Equipment

Precision Ag Technology

Dealer Services & Support+ =

15

16

Net Sales by Product CategoryEquipment Operations – Fiscal 2017

Agriculture & Turf$20.2 billion

Construction & Forestry$5.7 billion

Small Ag

Turf

Compact

Construction

Forestry

Other

Large Ag

17

Use-of-Cash

18

Manage the balance sheet, including liquidity, to support a rating that provides access to low-cost and readily available short- and long-term funding mechanisms

Reflects the strategic nature of our financial services operation

Committed to “A” Rating

Cash from Operations

Fund Operating and Growth Needs

Common Stock Dividend

Share Repurchase

Fund value-creating investments in our businesses

Consistently and moderately raise dividend targeting a 25%-35% payout ratio of mid-cycle earnings

Consider share repurchase as a means to deploy excess cash to shareholders, once above requirements are met and repurchase is viewed as value-enhancing

Deere Use-of-Cash Priorities

19

$0.11

$0.28

$0.60

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

2004 2005 2006 2007* 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Deere Quarterly Dividends Declared 1Q 2004 – 2Q 2018

* Adjusted for 2 for 1 stock split on 26 November 2007

Dividend raised 114% since 2010

20

Share RepurchaseAs Part of Publicly Announced Plans

* All shares adjusted for two-for-one stock split effective 26 November 2007

2004–2Q 2018:

Cumulative cost of repurchases $16.5 billion

Shares repurchased 245.0 million

Average repurchase price $67.08

December 2013 authorization of $8 billion:

Amount remaining $3.2 billion

29 April 2018 period ended basic shares 324.3 million

2Q 2018 average diluted shares 329.2 million$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

0

10

20

30

40

2004 2006 2008 2010 2012 2014 2016 2018

YTD

$ B

illions

Millions o

f Share

s*

Shares Repurchased Amount Spent

Share Repurchase

35% net share reduction since 2004

21

$4,287$8,168

$37,440

$665 $146

$10,652

$1,345

$7,848

$13,904

$621

$0

$10,000

$20,000

$30,000

$40,000

$50,000

Beginning Cash

& Cash

Equivalents

(Fiscal 2004)

Cash From

Operations

Divestitures,

net of

Acquisitions

Net Change in

Debt and

Intercompany

Balances

Capital

Expenditures

Investment in

Financial

Services

Dividends Share

Repurchase, net

of Common

Stock Issuances

Other* Ending Cash &

Cash

Equivalents

(Fiscal 2017)

Sources and Uses of Cash Fiscal 2004-2017Equipment Operations

$ M

illions

~ 58% of cash from operations returned to

shareholders

* Other includes proceeds from maturities and sales of marketable securities and purchases of marketable securities and reconciliation for non-cash items including the effect of exchange rates on cash and cash equivalentsNote: “Cash from Operations” adjusted with the adoption of FASB ASU No. 2016-09 “Improvements to Employee Share-Based Payment Accounting”Source: Deere & Company SEC filings

= Source of Cash

= Use of Cash

22

Global Markets

23

Net Sales by Major MarketsEquipment Operations

$ Billions* U.S. & Canada not to scale with other markets

$17.4

$20.8$21.8

$20.2

$16.6

$14.5 $15.1

2011 2012 2013 2014 2015 2016 2017

U.S. & Canada*

$4.4 $4.3 $4.4 $4.4

$3.3 $3.2 $3.3

2011 2012 2013 2014 2015 2016 2017

Western Europe

$3.6 $3.6$4.3 $4.1

$2.4 $2.4$3.2

2011 2012 2013 2014 2015 2016 2017

Latin America

$1.9 $2.1 $2.1 $2.0 $1.9$1.4 $1.7

2011 2012 2013 2014 2015 2016 2017

Asia, Africa & Middle East

$1.4 $1.7 $1.6 $1.4 $1.0 $1.2$1.7

2011 2012 2013 2014 2015 2016 2017

Central Europe & CIS

$0.8 $1.0 $0.8 $0.8 $0.6 $0.7 $0.9

2011 2012 2013 2014 2015 2016 2017

Asia Pacific, Australia & New Zealand

24

U.S. and CanadaFactory Locations

Iowa, USA• Cotton Harvesting Equipment• Planting Equipment• Spraying Equipment• Tillage Equipment• Ag Tractors• Components• Foundry• Engines•Hay & Forage Equipment• Articulated Dump Trucks• 4WD Loaders•Motor Graders• Skidders•Wheeled Feller Bunchers• Backhoes• Compact Tracked Loaders• Crawler Dozers•High-Speed Dozers• Knuckleboom Loaders• Skid Steer Loaders• Tracked Feller Bunchers• Tracked Harvesters•High Clearance Sprayers (JV)

British Columbia, Canada• Log Loaders & Specialty Products

Alberta, Canada• Remanufactured Components

North Dakota, USA• Air Seeding Equipment• Electronics• Tillage Equipment

Wisconsin, USA• Lawn & Garden Equipment•Utility Vehicles•Golf & Turf Reel Mowers

Illinois, USA• Combine Harvesters•Headers• Planting Equipment•Hydraulic Cylinders

Tennessee, USA• Lawn Tractors

North Carolina, USA• Commercial Mowers•Golf & Turf Mowers•Utility Vehicles•Hydraulic Excavators

Georgia, USA•Utility Tractors• Compact Utility Tractors

Louisiana, USA• Sugarcane Harvesting Equipment• Tractor Loaders• Scrapers• Cotton Strippers

Missouri, USA• Remanufactured Components

Kansas, USA• Power Transmission Equipment

California, USA• Satellite Receivers

25

EU 28Factory Locations

Joensuu, Finland•Wheel Forwarders•Wheel Harvesters• Forestry Attachments

GermanyMannheim• Tractors

Zweibrücken• Combines & Forage Harvesters

Stadtlohn•Headers

Bruchsal• Tractor & Harvesting Cabs

Gummersbach•Walk-Behind & Autonomous Mowers

Windhagen•Wirtgen Milling Machines, Concrete Paving, Recyclers, Surface Miners

Tirschenreuth•Hamm Compactors

Ludwigshafen• Vögele Asphalt Paving

Göppingen • Kleemann Crushers & Screens

Mülheim• Benninghoven Asphalt Plants

Wittlich• Benninghoven Asphalt Plants

Madrid, Spain• Components

Arc-les-Gray, France• Balers• Ag Loaders

Largeasse, France• Planting Equipment

Saran, France• Engines

Horst, The Netherlands• Spraying Equipment

Ravenna, Italy• Sprayers

26

BrazilFactory Locations

Catalão, Brazil• Sugarcane Harvesters• Sprayers

Indaiatuba, Brazil• Backhoe Loaders• 4WD Loaders• Crawler Dozers• Excavators (JV)

Montenegro, Brazil• Tractors

Horizontina, Brazil• Combine Harvesters• Planters

Porto Alegre, Brazil•Wirtgen Milling Machines• Vögele Pavers•Hamm Rollers• Ciber Asphalt Mixing Plants

27

CISFactory Locations

Domodedovo, Russia• Tractors• Combine Harvesters•Motor Graders

Orenburg, Russia• Seeding Equipment• Tillage Equipment

28

ChinaFactory Locations

Jiamusi, China• Combine Harvesters• Cotton Pickers• Round Balers

Tianjin (TEDA), China• 4WD Loaders• Excavators• Engines (85-254 hp)• Tractors (85-320 hp)

Ningbo, China• Tractors (30-55 hp)• Cane Harvesters

Langfang, China•Wirtgen Milling Machines• Vögele Asphalt Paving•Hamm Rollers

29

IndiaFactory Locations

Pune, India• Engines• Transmissions• Tractors (36-75 hp)• Electronics•Hamm Rollers• Kleemann Screens• Vögele Pavers

Sirhind, India• Combine Harvesters

Dewas, India• Tractors (36-50 hp)

30

Other RegionsFactory Locations

Ramos, Mexico• Ag Loaders• Compact Utility Tractor Loaders•Utility Tractor Cabs•Hydraulic Cylinders

Monterrey, Mexico• Rotary Cutters• Implements• Components

Saltillo, Mexico• Ag Tractors• Transaxles

Torreon, Mexico• Axles• Engines• Electronics

Rosario, Argentina• Engines• Tractors• Combines

Kibbutz Beit Hashita, Israel• Cotton Picker Components

Tokoroa, New Zealand• Forestry Harvester Heads

Campana, Argentina• Carbon Fiber Technology Products

31

Worldwide Parts ServicesSupporting the Growth of Our Equipment Operations

Highlights:

– Miami, Florida (United States)– Directly supports the Latin America dealer

network, operational November 2017

– China footprint– Strategic distribution locations to support

China market, operational 2016

– Campinas, Brazil– Expansion of existing facility, operational

March 2015

Anchor Parts Distribution Centers

Regional Parts Distribution Centers or Depots

32

Engine Emissions2018 Worldwide Off-Road Emissions Regulations > 75 hp

Stage II/Tier 2

Stage IIIA/Tier 3/TREM 3A/MAR 1/China NR III

Stage IV/Final Tier 4 (> 75-750 hp)

* Includes some non-EU28 countries that follow EU28 emissions regulations

U.S. and CanadaFinal Tier 4

RussiaAg tractors: Stage II

EU28*Stage V – starting 2019

ChinaChina NR III

IndiaTREM 3A >50hp

BrazilMAR 1:• Construction equipment• Ag equipment >100hp

33

John Deere Financial Services

34

John Deere Financial ServicesSupporting the Growth of Our Equipment Operations

Owned Operations

Bank/Finance Company Partners

Retail programs through JDF not currently offered

35

John Deere Financial Services

Net Income

-$2,000

-$1,000

$0

$1,000

$2,000

$3,000

$4,000

1989 1993 1997 2001 2005 2009 2013 2017

John Deere Financial (attributable to Deere & Company) Deere & Company

$ M

illions

Consistent earnings throughout the cycle

36

Portfolio Composition by Segment

John Deere Financial Services

Portfolio Composition by Geography Portfolio Composition by Product

A&T

84%

C&F

16%

Installment

and Finance

Lease

55%

Wholesale/

Floorplan

19%

Revolving

Credit

9%

Operating

Lease

17%

U.S.

72%

Canada

11%

Europe

6%

Latin

America

7%

Australia

3% Asia

1%

Note: Information above includes all Deere & Company lending activities worldwide. John Deere Capital Corporation is the largest lending operation of Deere & Company.

$40.0 billion Net Owned Portfolio as of 29 October 2017

37

John Deere Capital Corporation

Agriculture & Turf* Construction & Forestry

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

1983 1988 1993 1998 2003 2008 2013

Net Write-offs (Ag) Installments 60+DPD (Ag)

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

1995 2000 2005 2010 2015

Net Write-offs (C&F) Installments 60+DPD (C&F)

* 1983–1985 includes construction; 1986-1994 includes lawn & grounds care; 2009 forward includes ag & turf equipment; as % of owned losses after dealer reserve charges Source: 1983–1994 internal reporting, 1995-2011 JDCC 10-K filings, 2012-2017 internal reporting

Continued extremely low write-offs in Agriculture & Turf and Construction & Forestry

38

Agriculture Fundamentals

39

Global Stocks-to-Use Ratios

Source: USDA, 10 May 2018

0%

20%

40%

60%

80%

100%

120%

0%

10%

20%

30%

40%

50%

60%

1994 1997 2000 2003 2006 2009 2012 2015 2018P

Cotto

n R

atio

s

CottonWheat

Corn

Soybeans

40

Source: USDA, 10 May 2018

Global Grain Supply and Demand

0

500

1,000

1,500

2,000

2,500

3,000

93/94 95/96 97/98 99/00 01/02 03/04 05/06 07/08 09/10 11/12 13/14 15/16 17/18

Million M

etr

ic T

ons

Production Consumption

41

0

1,000

2,000

3,000

2006 2008 2010 2012 2014 2016 2018F

Million M

etr

ic T

ons

Consumption without biofuel use

Global Grain DemandWith and Without Biofuel Use

0

1,000

2,000

3,000

2006 2008 2010 2012 2014 2016 2018F

Million M

etr

ic T

ons

Consumption with biofuel use

* Compound Annual Growth RateSource: OECD-FAO Agricultural Outlook 2017-2026, July 2017

42

U.S. Farm Cash Receipts

$0

$100

$200

$300

$400

$500

2002 2004 2006 2008 2010 2012 2014 2016 2018F

$ B

illions

Crops Livestock Government Payments

Source: 2001–2016: USDA, 7 February 20182017F–2018F: Deere & Company forecast as of 18 May 2018

43

U.S. Farm Balance Sheet

10%

15%

20%

25%

30%

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

1974 1978 1982 1986 1990 1994 1998 2002 2006 2010 2014 2018F

$ B

illions

Farm Debt Farm Equity Debt to Equity Ratio (%) Debt to Asset Ratio (%)

Source: 1974–2016: USDA, 7 February 20182017F–2018F: Deere & Company forecast as of 18 May 2018

44

Construction & Forestry Fundamentals

45

U.S. Housing Starts

0.0

0.5

1.0

1.5

2.0

2.5

1968 1973 1978 1983 1988 1993 1998 2003 2008 2013 2018F

Multi-Family Housing Starts Single-Family Housing Starts

Source: 1968–2016: U.S. Census Bureau, April 20182017F–2018F: Deere & Company forecast as of 18 May 2018

Millions o

f U

nits

46

-160%

-140%

-120%

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

$0

$400

$800

$1,200

$1,600

$2,000

$2,400

1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018F

% T

ota

l Constru

ctio

n S

pend

$ B

illions*

Government Infrastructure Investment Government Investment in Structures

Nonresidential Investment in Structures Residential Investment in Permanent Structures

U.S. Construction Spending

* 2009$ baseSource: 1998–2016: U.S. Bureau of Economic Analysis, April 2018

2017F–2018F: Deere & Company forecast as of 18 May 2018

47

Transaction provides greater exposure to transportation infrastructure, a faster growing, less cyclical sector than broader construction

− Attractive margin opportunity with significant growth tailwinds

− Road construction AND repair emphasized in many countries, resulting in a large installed base of equipment

Road Construction Equipment Spend Construction vs. Transportation Spend

50

100

150

200

250

300

2004 2006 2008 2010 2012 2014Spendin

g I

ndex (

2004=

100)

Total Construction Spending Total Transporatation Spending

Source: BCG; indexed using 2016 figures Source: IHS Global Insight

0

50

100

150

200

2016 2017E 2018E 2019E 2020E 2021E 2022E

Total Transportation Spending

Wirtgen AcquisitionAttractive Industry Fundamentals

48

End to End Road Construction Portfolio

49

Appendix

50

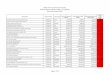

SVA* Reconciliation to GAAPEquipment Operations

* Shareholder Value Added

($ millions except where noted) 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Net Sales 6,479 7,663 8,830 9,640 11,082 11,926 9,701 11,169 11,077 11,703 13,349 17,673 19,401

Average Identifiable AssetsWith Inventories at LIFOWith Inventories at Standard Cost

5,4496,442

5,5516,494

6,1877,131

6,5027,488

6,6827,703

7,6728,711

7,7248,739

8,0699,039

8,7439,678

6,2297,147

5,9656,925

6,4827,477

7,2488,312

Operating ProfitPercent of Net Sales

2423.7%

84711.1%

1,00611.4%

1,12511.7%

1,40212.6%

1,47612.4%

2722.8%

6936.2%

(46)(0.4%)

4013.4%

7085.3%

1,90510.8%

1,8429.5%

Operating Return on AssetsWith Inventories at LIFOWith Inventories at Standard Cost

4.4%3.8%

15.3%13.0%

16.3%14.1%

17.3%15.0%

21.0%18.2%

19.3%16.9%

3.5%3.1%

8.6%7.7%

(0.5%)(0.5%)

6.4%5.6%

11.9%10.2%

29.4%25.5%

25.4%22.2%

SVA Cost of Assets (773) (780) (856) (898) (924) (1,045) (1,049) (1,085) (1,162) (858) (831) (897) (998)

SVA (531) 68 150 226 477 431 (776) (392) (1,208) (457) (123) 1,008 844

($ millions except where noted) 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Net Sales 19,884 21,489 25,803 20,756 23,573 29,466 33,501 34,998 32,961 25,775 23,387 25,885

Average Identifiable AssetsWith Inventories at LIFOWith Inventories at Standard Cost

7,5468,634

8,0929,205

9,65210,812

9,64710,950

9,19610,494

11,51612,875

13,59414,965

14,56915,924

14,11315,493

12,49113,840

11,81613,092

12,15013,421

Operating ProfitPercent of Net Sales

1,9059.6%

2,31810.8%

2,92711.3%

1,3656.6%

2,90912.3%

3,83913.0%

4,39713.1%

5,05814.5%

4,29713.0%

2,1778.4%

1,8808.0%

2,82110.9%

Operating Return on AssetsWith Inventories at LIFOWith Inventories at Standard Cost

25.2%22.1%

28.6%25.2%

30.3%27.1%

14.1%12.5%

31.6%27.7%

33.3%29.8%

32.3%29.4%

34.7%31.8%

30.4%27.7%

17.4%15.7%

15.9%14.4%

23.2%21.0%

SVA Cost of Assets (1,036) (1,094) (1,284) (1,301) (1,259) (1,545) (1,795) (1,911) (1,860) (1,661) (1,570) (1,611)

SVA 869 1,224 1,643 64 1,650 2,294 2,602 3,147 2,437 516 310 1,210