Embed Size (px)

Citation preview

InvestorpresentationMay 2015

Table of contents

(2)

Cautionary noteCertain statements included within this announcement contain forward-looking information, including, without limitation, those relating to (a) forecasts, projections and estimates, (b) statements of management’s plans, objectives and strategies for Hydro, such as planned expansions, investments or other projects, (c) targeted production volumes and costs, capacities or rates, start-up costs, cost reductions and profit objectives, (d) various expectations about future developments in Hydro’s markets, particularly prices, supply and demand and competition, (e) results of operations, (f) margins, (g) growth rates, (h) risk management, as well as (i) statements preceded by “expected”, “scheduled”, “targeted”, “planned”, “proposed”, “intended” or similar statements.

Although we believe that the expectations reflected in such forward-looking statements are reasonable, these forward-looking statements are based on a number of assumptions and forecasts that, by their nature, involve risk and uncertainty. Various factors could cause our actual results to differ materially from those projected in a forward-looking statement or affect the extent to which a particular projection is realized. Factors that could cause these differences include, but are not limited to: our continued ability to reposition and restructure our upstream and downstream aluminium business; changes in availability and cost of energy and raw materials; global supply and demand for aluminium and aluminium products; world economic growth, including rates of inflation and industrial production; changes in the relative value of currencies and the value of commodity contracts; trends in Hydro’s key markets and competition; and legislative, regulatory and political factors.

No assurance can be given that such expectations will prove to have been correct. Hydro disclaims any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

First quarter results 2015 3

Market 34

Business overview 45

> Hydro - Group 46

> Bauxite & Alumina 57

> Primary Metal 66

> Metal Markets 72

> Rolled Products 76

> Sapa joint venture 82

> Energy 85

Additional information 90

(3)

Q1 2015

(4)

• Record-high quarterly underlying EBIT of NOK 3 208 million• Higher sales throughout the value chain• Positive currency developments• Acquisition of advanced sorting technology in Germany• Reduced market tightness due to Chinese semis exports

Q1 highlights

(2 000)

(1 000)

0

1 000

2 000

3 000

4 000

Jan-09 Apr-10 Jul-11 Oct-12 Jan-1415 000

20 000

25 000

30 000

Jan-08 May-09 Sep-10 Jan-12 May-13 Sep-14

Demand Production

Source: CRU/Hydro* Yearly rolling average of quarterly annualized production less demand

• YTD aluminium demand growth of 1.5 % − North America ~5%− Europe ~0%− Asia ~5%− Central and South America (~5%)

Aluminium demand continues to exceed production

(5)

Demand and production (quarterly annualized)1 000 mt primary aluminium

World ex-China

Production less demand*1 000 mt primary aluminium

Mar-15 Mar-15

• Expect ~3% demand growth 2015• Production deficit around 1 million tonnes

0

20

40

60

80

100

120

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

Q1 05 Q3 07 Q1 10 Q3 12 Q1 15

IAI Other LME World ex. China inventory days

Reported inventories world ex-China decline further

(6)

Source: CRU/Hydro

Reported primary aluminium inventories1 000 mt Days

Warehouse rules in effect as of 1st of February 2015

Stock levels Detroit and VlissingenMillion tonnes Queue days

Vlissingen Detroit

400

450

500

550

600

650

700

750

800

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

May

-14

Jun-

14

Jul-1

4

Aug-

14

Sep-

14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb-

15

Mar

-15

Apr

-15

Global primary aluminium market slightly oversupplied

(7)

Demand and production (quarterly annualized)1 000 mt primary aluminium

15 000

20 000

25 000

30 000

35 000

40 000

45 000

50 000

55 000

60 000

Jan-08 May-09 Sep-10 Jan-12 May-13 Sep-14

Demand Production

Chinese overproduction exceeds World ex-China deficit

(2 000)

(1 000)

0

1 000

2 000

3 000

4 000

5 000

Jan-09 Apr-10 Jul-11 Oct-12 Jan-14

Production less demand*1 000 mt primary aluminium

• Expect ~6% demand growth 2015• Production surplus around 0.5 million tonnesMar-15

Source: CRU/Hydro* Yearly rolling average of quarterly annualized production less demand

Mar-15

Chinese exports decline from high levels in December amid reduced metal advantage

0

50

100

150

200

250

300

350

400

450

500

Jan-07 Oct-07 Jul-08 Apr-09 Jan-10 Oct-10 Jul-11 Apr-12 Jan-13 Oct-13 Jul-14 Apr-15( 400)

( 200)

0

200

400

600

800

1 000

Semis exports (Left axis) Chinese competitive adv. downstream* (Right axis)

Comp. adv. (USD/mt)

Semis exports(monthly, kmt)

* Est. metal cost China versus EuropeEurope: LME cash + European duty-paid standard ingot premiumChina: SHFE cash + avg. local premium + freight – export rebates (~13 %)

Source: CRU/Ecowin

Impr

oved

com

p. a

dv. C

hina

Standard ingot premiums fall sharply

Source: Metal Bulletin, Platts

Regional standard ingot premiumsUSD per mt

0

100

200

300

400

500

600

Jan-08 Mar-09 May-10 Jul-11 Sep-12 Nov-13 Jan-15

US Mid West Japan Europe (duty-paid)

• US Mid-West and EU duty-paid ingot premium falling to currently ~320 and 220 USD/mt, respectively

• Japan premium at 425 USD/mt in Q1, negotiations for Q2 at ~380 USD/mt

• Current Japanese spot ingot premium at ~270 USD/mt

(9)

Apr-15

Value-added premiums come down with standard ingotHydro realizes premiums on 1-2 month time lag

(10)

0

100

200

300

400

500

600

700

800

900

Jan-08 Jul-09 Jan-11 Jul-12 Jan-14

EI over ingot Ingot DDP Premium Indicator Metal Bulletin Billet Premium Indicator

Source: Metal Bulletin, Hydro

USD per mt

Apr-15

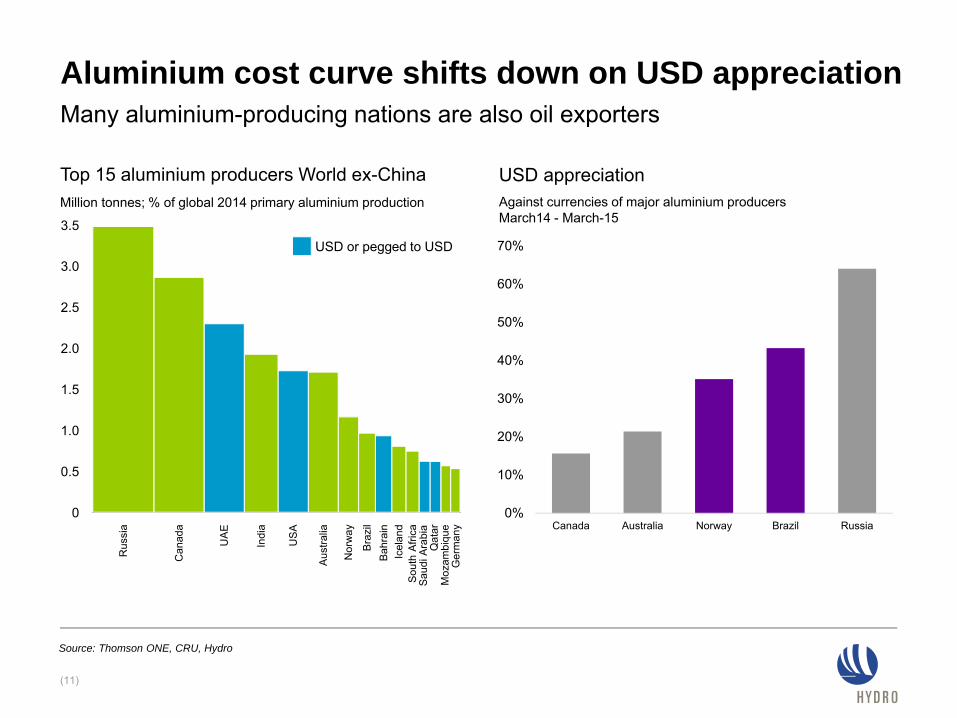

Aluminium cost curve shifts down on USD appreciationMany aluminium-producing nations are also oil exporters

(11)

Top 15 aluminium producers World ex-ChinaMillion tonnes; % of global 2014 primary aluminium production

USD appreciation Against currencies of major aluminium producers March14 - March-15

Source: Thomson ONE, CRU, Hydro

0

1.0

2.0

3.5

2.5

1.5

3.0

0.5

UA

E

Bra

zil

Nor

way

Indi

a

Aus

tralia

US

A

Icel

and

Moz

ambi

que

Sau

di A

rabi

a

Ger

man

y

Qat

ar

Bah

rain

Can

ada

Sou

th A

frica

Rus

sia

USD or pegged to USD

0%

10%

20%

30%

40%

50%

60%

70%

Canada Australia Norway Brazil Russia

Decline in all-in ingot price partly offset by weak NOK

(12)

USD/mt

Source: Metal Bulletin, MW/MJP: Platts, Reuters Ecowin* LME three month average

• 3-month LME price traded between 1 747 and 1 890 USD/mt during Q1

Primary aluminium LME* USD/mt NOK/mt

Q1 2015 averageQ1 2015 end

1 8131 790

14 06214 425

Q4 2014 averageQ4 2014 end

1 9741 859

13 56713 890

12 000

13 000

14 000

15 000

16 000

17 000

18 000

1 500

1 700

1 900

2 100

2 300

2 500

2 700

2 900

3 100

Jan 11 Jun 12 Nov 13 Apr 15

LME cashLME cash + Europe duty paidLME cash + Europe duty paid NOK (RHS)

NOK/mt

(13)

Resilient alumina prices, bauxite source diversification continues

Platts alumina index (PAX)PercentUSD/mt

12%

13%

14%

15%

16%

17%

18%

19%

20%

200

250

300

350

400

450

Aug 2010 Apr 2012 Nov 2013

PAX % of LME

Mar 2015

Source: Platts, Ecowin, China Customs,* Based on actual Q1 2015 annualized

Chinese bauxite imports by origin

0

10

20

30

40

50

60

70

80

2011 2012 2013 2014 2015e *

Indonesia Australia India Malaysia Other Pacific Atlantic

Million tonnes

15.3% 15.1% 16.1% LME%3)

269 303 300 Price2)

Lower implied alumina cost on currency developments

Q1 2014 Q4 2014 Q1 2015

Implied alumina cost and margin, USD/mt 1)• USD 4 per mt reduction in implied alumina cost from fourth quarter− BRL weakens 12% against USD from Q4

to Q1− Lower Paragominas production driven by

extended ball mill maintenance− Ball mill now back in operation

• “From B to A” improvement program progressing ahead of plan

• ICMS deferral for aluminium industry in Pará to be revisited in July 2015− Dialog ongoing

1) Realized alumina price minus underlying EBITDA for B&A, per mt alumina sales2) Realized alumina price3) Realized alumina price as % of three month LME price with one month lag

Implied EBITDA cost per mt

475

259

425

EBITDA margin per mt

10

229

74

225

75

(14)

2 174 2 574 2 510 All-in3)

1 749 1 997 1 897 LME4)

Q1 2014 Q4 2014 Q1 2015

Stable all-in implied primary aluminium cost

All-in implied primary cost and margin, USD/mt 1) • Developments Q1 vs Q4‒ Improvement efforts‒ Positive currency development‒ Increasing raw material costs

• USD 180 JV program on track, to be concluded by end-2016‒ USD 120 delivered by end-2014

1) Realized all-in aluminium price minus underlying EBITDA margin, including Qatalum, per mt aluminium sold. 2) Realized LME aluminium price minus underlying EBITDA margin, including Qatalum, per mt primary aluminium produced. 3) Realized LME plus realized premiums, including Qatalum4) Realized LME, including Qatalum

LME Implied EBITDA cost per mt

1 900

All-in EBITDA margin per mt

275

1 775

800

1 800

700

(15)

1 150 2)

1 400 2)

1 175 2)

All-in Implied EBITDA cost per mt

Strengthening recycling position towards carbon neutrality

(16)

• WMR Recycling acquired April 1‒ World’s most advanced sorting technology‒ 36 000 tonnes annual sorting capacity‒ To supply Hydro remelters‒ Located in Dormagen, Germany

• Technology to be used in Hydro’s recycling facility for used beverage cans

• Part of Hydro’s 2020 carbon neutrality ambition

Q1 2015 vs Q4 2014 Q1 2015 vs Q1 2014

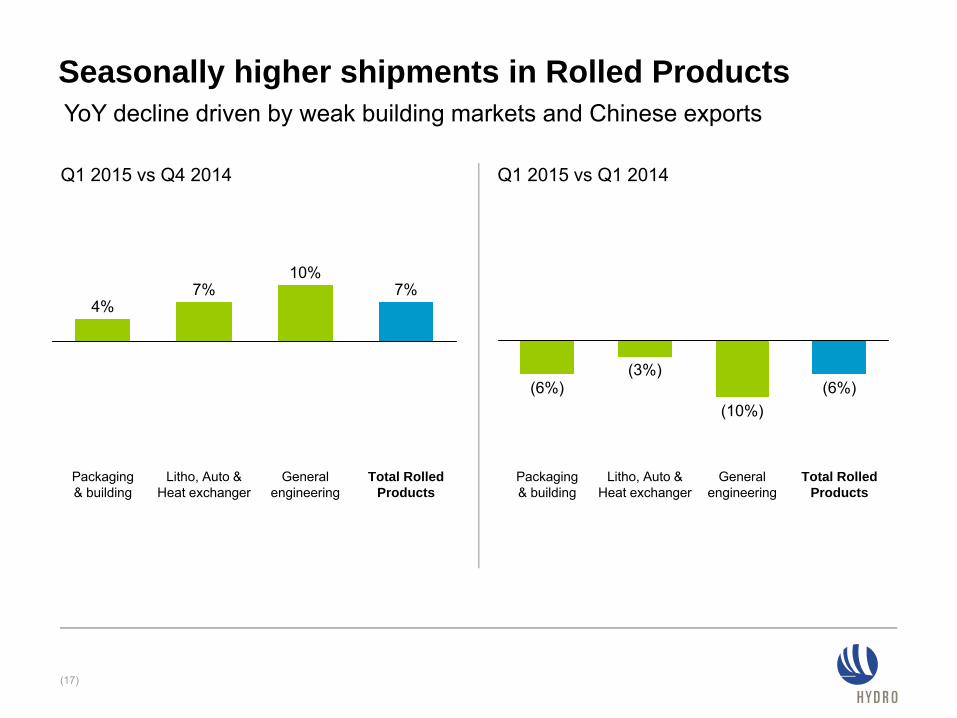

Seasonally higher shipments in Rolled Products

(17)

YoY decline driven by weak building markets and Chinese exports

Litho, Auto & Heat exchanger

General engineering

7%

Total Rolled Products

10%

Packaging & building

7%4%

(3%)(6%)

General engineering

(10%)

Packaging & building

Total Rolled Products

Litho, Auto & Heat exchanger

(6%)

(18)

• Seasonally stronger demand− 10% increase in North America− 9% increase in Europe

• Demand increased compared to same quarter last year− 11% in North America due to increased

building activity and strong automotive demand

− Stable in Europe, weak building activity continues

Seasonally stronger demand for extruded products

• Partnership to supply structural aluminium tubing− Also provide ongoing development support

for future extrusion applications

• Ford F 150 2015 Model− Aluminium-alloy body− ~700 pounds lighter than 2014 model

Sapa JV delivers solutions to Ford F-150

(19)

World’s most selling vehicle

Picture with courtesy of Ford Motors

0

100

200

300

400

500

600

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52

201320142015

0

20

40

60

80

100

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52

MIN NO2 (2002-2013)MAX NO2 (2002-2013)201320142015

(20)

Water reservoir levels Southwestern Norway (NO2)PercentNOK/MWh

Energy price NOK/MWh Q1 2015 Q4 2014 Reservoir levels Mar 31, 2015 Dec 30, 2014

Southwestern Norway (NO2)

System

238

246

248

264

Southwestern Norway (NO2)

Norway

42.7%

37.8%

77.6%

68.8%

Source: Nordpool and NVE

Market price Southwestern Norway (NO2)

Energy: High snow reservoirs, low power prices

Week Week

(20)

Record results on higher sales and currency tailwinds

(21)

NOK billion

3.2

0.9

2.9

Underlying EBIT Q1-2015

Volumes OtherUnderlying EBIT Q1-2014

Underlying EBIT Q4-2014

Net currency Cost

(0.3)

(0.3)(0.2)

0.2

0.8

Prices and margins

(22)

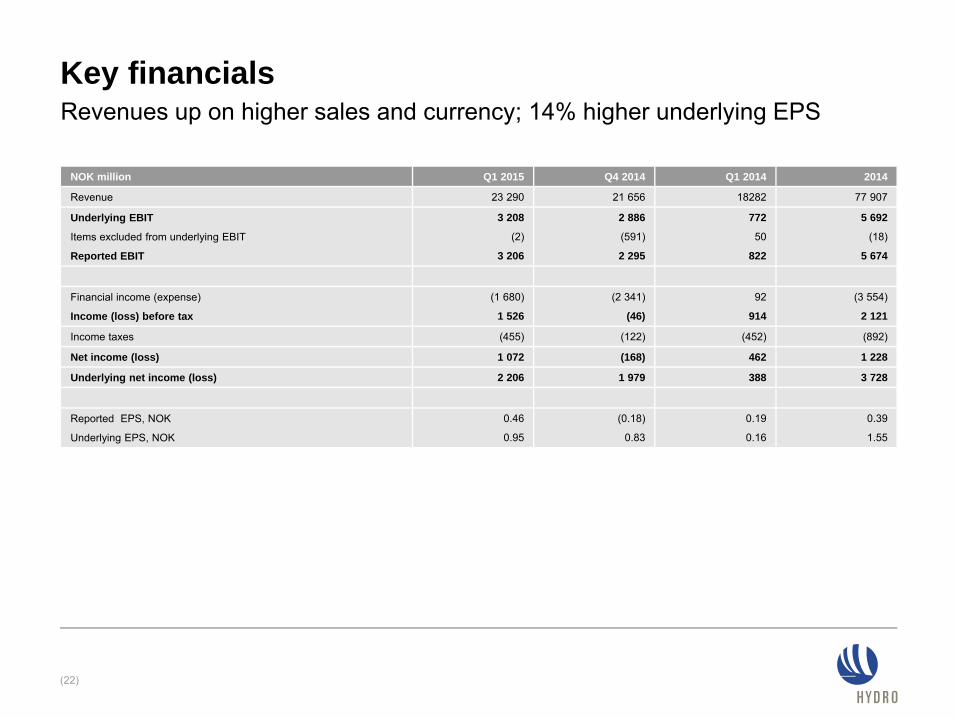

Key financials

NOK million Q1 2015 Q4 2014 Q1 2014 2014

Revenue 23 290 21 656 18282 77 907

Underlying EBIT

Items excluded from underlying EBIT

Reported EBIT

3 208

(2)

3 206

2 886

(591)

2 295

772

50

822

5 692

(18)

5 674

Financial income (expense)

Income (loss) before tax

(1 680)

1 526

(2 341)

(46)

92

914

(3 554)

2 121

Income taxes (455) (122) (452) (892)

Net income (loss) 1 072 (168) 462 1 228

Underlying net income (loss) 2 206 1 979 388 3 728

Reported EPS, NOK

Underlying EPS, NOK

0.46

0.95

(0.18)

0.83

0.19

0.16

0.39

1.55

Revenues up on higher sales and currency; 14% higher underlying EPS

(23)

NOK million Q1 2015 Q4 2014 Q1 2014 2014

Underlying EBIT 3 208 2 886 772 5 692

Unrealized effects on power and raw material contracts

Unrealized derivative effects on LME related contracts

Metal effect, Rolled Products

Rationalization charges and closure costs

Impairment charges

Gains (losses) on divestments

Other effects

Items excluded in equity accounted investment (Sapa)

151

(140)

61

-

-

-

-

(74)

(261)

-

189

-

(145)

-

(36)

(337)

175

(5)

-

-

(33)

-

-

(86)

(72)

352

449

-

(207)

8

(36)

(512)

Reported EBIT 3 206 2 295 822 5 674

Items excluded from underlying EBITOffsetting effects

Bauxite & Alumina

(24)

780

(24)

Key figuresQ1

2015Q4

2014Q1

2014

Alumina production, kmt 1 451 1 501 1 428

Total alumina sales, kmt 2 136 2 043 1 906

Realized alumina price, USD/mt 300 303 269

Implied alumina cost, USD/mt 225 229 258

Bauxite production, kmt 2 136 2 582 2 242

Underlying EBITDA, NOK million 1 240 1 046 122

Underlying EBIT, NOK million 780 528 (288)

(55)

NOK millionUnderlying EBIT

• Higher alumina sales volumes and index exposure• Lower bauxite production due to extended maintenance• Positive contribution from currency developments

• Lower alumina sales volumes • Reduced index exposure • Lower contribution from Reintegra

Q1 results

Outlook

780

(288) (269)

(26)

528

2014 2015

Higher alumina sales on index and currency developments lift results

(25)

Primary Metal

Key figuresQ1

2015Q4

2014Q1

2014

Primary aluminium production, kmt 497 499 484

Total sales, kmt 534 527 593

Realized LME price, USD/mt 1 897 1 997 1 749

Realized LME price, NOK/mt 14 383 13 355 10 702

Realized premium, USD/mt 614 575 422

Implied all-in primary cost, USD/mt * 1 800 1 775 1 900

Underlying EBITDA, NOK million 2 522 2 489 753

Underlying EBIT, NOK million 2 012 1 989 312

3 937 2 012

NOK millionUnderlying EBIT • Higher realized all-in metal prices in NOK lifted results by

~MNOK 700 • Seasonally higher sales volumes added ~ MNOK 100 • Higher costs reduced results by ~MNOK 600

• About 50 % of primary production affecting Q2 2015 results priced at ~USD 1 800 per mt, ex. Qatalum

• About 50% of premiums affecting Q2 booked at ~USD 650 per mt, ex. Qatalum

Outlook

312 420

1 216

2015

1 989

2014

2 012

* Realized all-in aluminium price minus underlying EBITDA margin, including Qatalum, per mtaluminium sold. Figures for 2014 have been restated due to a change in definition.

Q1 results

Higher realized all-in price partly offset by higher raw material cost

(26)

Qatalum results down on lower sales

Key figures – Qatalum (50%)Q1

2015Q4

2014Q1

2014

Revenue, NOK million 1 492 1 510 1 087

Underlying EBITDA, NOK million 585 614 342

Underlying EBIT, NOK million 305 371 115

Underlying Net income (loss), NOK million 246 317 75

Primary aluminium production, kmt 76 77 76

Casthouse sales, kmt 77 85 83

• Underlying net income decreased by NOK 71 million from Q4 2014 driven mainly by lower sales volumes

(27)

Metal Markets

Key figuresQ1

2015Q4

2014Q1

2014

Remelt production, kmt 145 130 139

Metal products sales, kmt 1) 626 654 776

Underlying EBITDA, NOK million 47 243 157

Underlying EBIT excl currency and inventory valuation effects, NOK million 2) 60 130 156

Underlying EBIT, NOK million 24 221 141

634 24

NOK millionUnderlying EBIT

• Seasonally higher volumes and improved margins at remelters• Negative result from sourcing and trading activities due to

falling standard ingot premiums• NOK 36 million in negative currency and ingot inventory

valuation effects vs NOK 92 million positive in Q4

• Higher sales volumes at remelters • Volatile trading and currency effects

24

141

100

171

221

2014 2015

Outlook

1) Includes external and internal sales from primary casthouse operations, remelters and third party metal sources. Sales volumes for 2014 have been restated.2) Currency effects for 2014 have been restated

Q1 results

Weak sourcing and trading performance hides strong results at remelters

(28)

Rolled Products

(28)

Key figuresQ1

2015Q4

2014Q1

2014

External sales volumes, kmt 227 213 243

Underlying EBITDA, NOK million 465 280 351

Underlying EBIT, NOK million 292 96 181

698 292

NOK millionUnderlying EBIT

• Seasonally higher shipments• Improved operating margins• Positive currency effect on USD sales

• Seasonally higher sales • Lower margins• Rheinwerk result determined by the LME and premium

development

Outlook

292

181 177

243

96

2014 2015

Q1 results

Higher shipments, margins and currency gains lift results

(29)

Energy

Key figuresQ1

2015Q4

2014Q1

2014

Power production, GWh 3 071 2 823 2 964

Net spot sales, GWh 1 610 1 339 1 581

Southwest Norway spot price (NO2), NOK/MWh 238 248 249

Underlying EBITDA, NOK million 429 402 474

Underlying EBIT, NOK million 382 360 435

• Seasonal high power production supported by high snow levels• Increased production costs• Lower spot prices

• Continuously high snow levels • Lower production costs

1 197 382

NOK millionUnderlying EBIT

Outlook 382

435

169234

360

2014 2015

Q1 results

High production partly offset by lower market prices

(30)

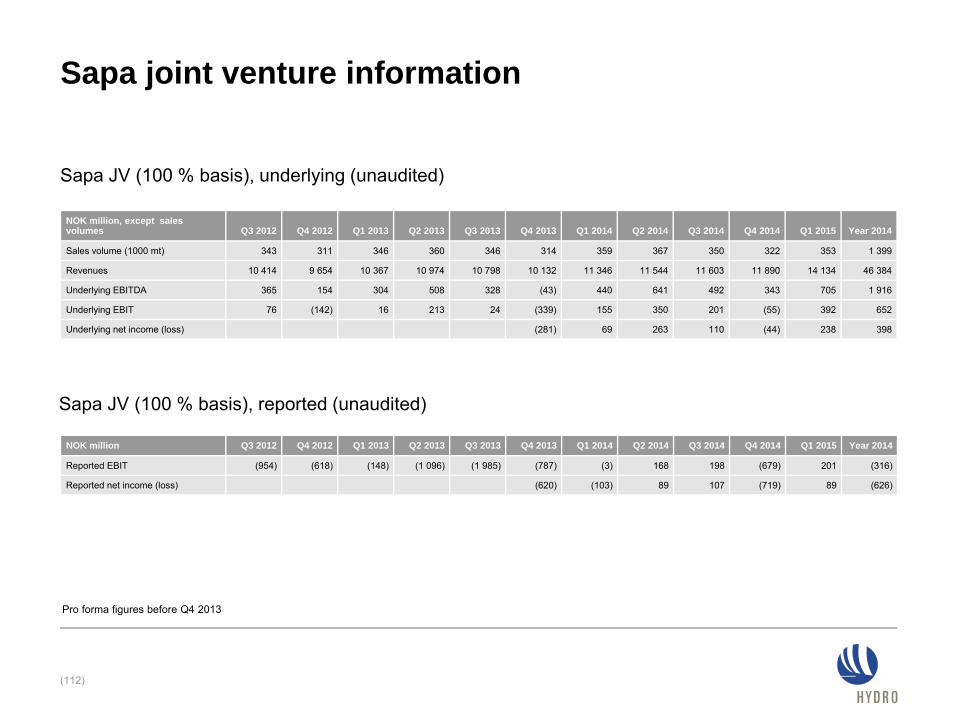

Improvement in Sapa JV results beyond seasonality

Key figures – Sapa (50%)Q1

2015Q4

2014Q1

2014

Revenue, NOK million 7 067 5 945 5 673

Underlying EBITDA, NOK million 353 171 220

Underlying EBIT, NOK million 196 (27) 78

Underlying Net income (loss), NOK million 119 (22) 35

Sales volumes (kmt) 177 161 180

• Results improved compared to the previous quarter as well as same quarter last year driven by:− Strong North-American market developments− Improvement and restructuring activities

• Quarter-on-quarter results also affected by:− Stronger seasonal demand

• Year-on-year results also supported by: − Positive currency developments

• Restructuring agenda continues ahead of plan

Other and Eliminations

(31)

Other and EliminationsQ1

2015Q4

2014Q1

2014

Sapa JV 119 (22) 35

Other (117) (118) (127)

Eliminations (284) (168) 84

Other and Eliminations (281) (308) (8)

Increased eliminations of internal inventories

Net cash(debt) development

(32)

4.4

(0.7)

End Q1-2015Operating capital

(2.9)

Investments

(0.1)

End Q4-2014

(0.9)

Currency and other

Underlying EBITDA

Taxes*

(0.1)

NOK billion Net cash flow from operationsNOK 1.4 billion

* Includes 600 MNOK reimbursement of VAT in Brazil for the earlier periods

Above seasonal build-up in operating capital

(0.3)

(33)

Priorities• Deliver on improvement efforts• ICMS dialog• Strengthen competitiveness

in uncertain markets

(34)

Market

Aluminium is the metal of the future

(35)

Properties leadto increasedmarket share

• Aluminium intensive urbanization and infrastructure• Climate challenge – aluminium as part of the solution• Recyclability more important with high energy prices

• Lightweight− 1/3 density of steel

• Recyclability− 5% of original energy

consumption− 75% of all aluminium

produced still in use

• Corrosion resistant− Oxide layer

• Formability− Extrusion, rolling, casting− Low melting point vs. steel

• Excellent conductivity− Thermal – electrical

• Alloying technology− Gives wide range of physical

properties

Aluminium demand accelerating in response to global needs

(36)

Strong demand drivers in key aluminium segments

UrbanizationSubstitution from copper

UrbanizationHousing market recovery in mature regionsEnergy neutral buildings

Improving industrial sentiment in mature regionsManufacturing activity and industrial growth in emerging countries

UrbanizationEnvironmental friendly solutions

Transport

Construction

Electrical

Machinery & equipment

Packaging

Source: CRU, Hydro Analysis

Growth in automotive vehicle productionAluminium content in cars increasingGrowth in other transport modes, e.g. railway

Primary aluminium demand growth

2020E2010200019901980

Broad-based aluminium demand growth across segments and regionsGlobal semis 2014 demand ~75 million tonnes

(37)

Global aluminium semis demand, per segmentMillion tonnes (2014)

Global aluminium semis demand, per regionMillion tonnes (2014)

Source: CRU, Hydro AnalysisCAGR = Compound annual growth rate

CAGR per segment (%), 2004-2014

8%

8%

25%

5%

9%

13%

27%

5%

4 %5 %

3 %6 %

6 %8 %

8 %5 %

0 1 2 3 4 5 6 7 8

Electrical

PackagingConsumer durables

Foil stockMachinery & Equipment

TransportConstruction

Other

12%1%

15%

4%

45%

19%

3%

8 %8 %

6 %0 %0 %

4 %17 %

0 2 4 6 8 10 12 14 16 18

Western Europe

Eastern Europe

AfricaCentral & South America

North America

ChinaOther Asia & Oceania

CAGR per region (%), 2004-2014

Infinite ideas in aluminiumMore and more sectors “discover” new areas for aluminium applications

(38)

Lightweight, non-corrosiveoffshore applications

Zero-emission electrical car ferry in 100% aluminium for light-weighting. In operation from 2015

Lightweight, non-corrosive subsea applications Electrical busbars – in aluminium

Floating aluminium bridge with a submerged floating tunnel at mid span. Under planning

Middle and high voltage cables, wireand cables for electrical applications

Transport drives global flat rolled product growth of 5%

CAGR 2014-2019, %

Source: CRU FRP quarterly February 2015, Rolled Products analysisFRP - Flat rolled productsCAGR – Compound annual growth rate

Global FRP consumption by end-use 2014

Total FRP 2014 consumption ~ 23 million tonnes

14%

4%

51%

12%

9%

10%

12%

5%

5%

5%

5%

5%

4%

Transport

Electrical

Construction

Total consumption

Machinery & Equipment

Consumer durables and other

Packaging

0

100

200

300

400

500

600

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

Automotive demand growth outperforms all other segments

Aluminium vehicle penetration, North AmericaPounds per light vehicle

(40)

Source: Ducker Worldwide, ‘2015 North American Light Vehicle Aluminum Content Study, Hydro

40 years of uninterrupted growth – accelerating from 2015 to 2025

DUCKER WORLDWIDE

In 2015, aluminium penetration will reach the critical mass for

an explosive period of growth from 2015 to 2025In 2025, light vehicles willbe the most important

global market for aluminium.

2014 2018 2022

Global Body-in-White demand – ‘000 mt

CAGR20%

500

1 400

2 100

Aluminium – a perfect fit for next-generation automotive

Source: International Aluminium Institute

• Tightening fuel economy regulations• 10% reduction in vehicle weight gives car

manufacturers a 5-7% fuel saving• 1 kg of aluminium replacing mild steel, cast

iron or high strength steel in cars saves between 15-20 kg GHG emissions

(41)

Land Rover Sport 2010

3,100 kgLand Rover Sport 2014

2,600 kg

• Higher specific energy absorption• More ductile - better crash performance

and safety • Lightweight• Better formability, alloying and extrusion

techniques - more advanced components• Recyclable, cost-effective, corrosion-

resistant

Aluminium vs. high-strength steel

Lighter weight translates to lower fuel emissions

C02 emissions327 g/100 km

C02 emissions194 g/100 km

Brittle materialDuctile material

Energy absorption

Higher raw material imports and semis exports in 2014

( 10)

( 5)

0

5

10

15

20

Fabricated SemisScrapBauxite Alumina Primary aluminium

Annualized aluminium equivalents*, million mt

Impo

rtto

Chi

naE

xpor

t fro

m C

hina

2006 2007 2008 2009 2010 2011 2012 2013

Net aluminium imports

2014

Source: CRU/Antaike/Hydro* Bauxite/alumina to aluminium conversion factor: 5.0/1.925** Jan/Feb 2015 figures annualized, March not yet available

2015**

Large and concentrated bauxite resources

(43)

1) Official reported resources in China (Not CM estimates)*) Mine site resources are known bauxite resources that do not currently qualify as reserves for various reasons**) Undeveloped resources might or might not became feasible for new mines (quality, size, access, etc.)***) Potential reserves = current reserves (economically extractible) + 70% of mine site resources. Undeveloped resources are excluded.Source: Roskill and Hydro analysis

Big-league (Top- 3)

Mid-league (Top- 10; each > 2% of world total)

Total bauxite, billion tonnes: reserves, mine site resources*, and undeveloped resources**

Potential reserves, billion tonnes: associated with currently operating mines***

41.0

6.2

Guinea

Atlantic Pacific

Billion mt

Australia9.5

5.6

China4.1 2.9

Vietnam4.7

0.5

India

3.01.0

Brazil8.7

2.5

Venezuela1.8

0.3

Jamaica

1.1 0.5

Bauxite suppliers short/medium term

But many challenges for future developments

1.00.2

Malaysia

4.0 1.5

Indonesia

(44)

Emirates Global (4.5)

Alba

Vedanta

0.4

Hydro 1.8

BHP Billiton

1.9Rio Tinto Alcan*

3.0

Alcoa/AWAC 8.3

(1.8)

UC Rusal

(0.7)

China (5.3)

Glencore/Century

2014

Alumina market is consolidating

Rusal

Dubal

Alba

Hydro

VAW

Sual

Alcan

Kaiser

BHP Billiton

Glencore

Vale

Alcoa

Pechiney

Rio Tinto

China

3.0

2.4

1.9

1.0

0.8

0.7

0.5

0.4

(0.5)

(0.6)

(0.9)

(1.0)

(1.2)

2000

Net long equity alumina position based on 2014 production, million tonnes

Source: CRU, Hydro

Hindalco

0.3

(0.4)

4.3

(1.9)

(45)

Business overview

(46)

Hydro - Group

5 6921 297 2 7255 9823 551

Hydro: a resource rich global aluminium company

(47)

Hydro underlying EBIT quarterly, NOK billion

Extruded Products classified as discontinued operations, and thereby excluded from revenues and underlying EBIT for 2011, 2012 and 2013. Figures for 2012 are adjusted reflecting IAS 19R. Figures for 2013 are adjusted reflecting IFRS 11

• Based in Norway, involved in activities in more than 50 countries

• 13 000 employees

• Operating revenues− 2013: NOK 65 billion− 2014: NOK 78 billion

• Current market capitalization− NOK 83 billion/ USD 11 billion

0

2.0

2.5

1.0

1.5

3.0

0.5

3.5

201420132010 2011 20152012

3208

Strong positions across aluminium value chain

(48)

Bauxite& Alumina

Rolled ProductsMetal Markets Sapa JV (50%)

• 2.1 million tonnes primary capacity

• High LME and USD sensitivity

• Improving cost position• Leading in technology

• 3.6 million tonnes (primary, remelt, recycling and cold metal)

• Expertise in materials• Flexible system• Strong marketing

organization• Risk management

• 1 million tonnes• Margin business• Regional business• Close to customers• Innovation• Market leading in litho

and foil

• 0.7 million tonnes (50%)• No. 1 position in North

America and Europe• Solid foothold in

emerging markets

Primary aluminium production,marketing and recycling

Energy Primary Metal

• Long-term power supply secured

• 10 TWh of renewable energy production in Norway

Raw materials processing and energy Aluminium in products

100% of volumes for assets that are fully consolidated and pro rata volumes for other assets.

• Bauxite capacity 10.8 million tonnes

• Expansion potential to 15.8 million tonnes

• Alumina capacity 6.3 million tonnes

• Expansion potential to 8.2 million tonnes first phase CAP

• Long-term sourcing contracts for bauxite and alumina

Hydro - a first tier aluminium company

Source: CRU, Hydro

Equity production in 2014 in aluminium equivalents ex-China, thousand mt

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

9 000

Alcoa/AWAC Rio Tinto Alcan* UC Rusal Norsk Hydro BHP Billiton Glencore/Century Hindalco Vedanta Emirates GlobalAluminium

Aluminium Bahrain

Alumina Aluminium

(49)

(50)

Curtailing 26% of primary metal capacity

USD 300 program

Climb From B to A

Starting up Qatalum

Acquiring bauxite and alumina assets

EstablishingSapa JV

JV-program

Hydro’s path towards global leadership

2010 20122009 2011 2013CCIP 1 CCIP 2

(51)

• Continue improvements drive

• Capture commercial opportunities

• Extend technology and innovation lead

• Turn leading HSE/CSR position into competitive advantage

• Deliver on fast-developing customer demands

• Capitalize on strong climate position over time

• Further strengthen relative industry position

• Enhance market positions and high-grade portfolio

• Mature selective growth projects for when time is right

Hydro’s aspiration for higher value creation

Sapa JV

Better: Hydro improvement drive continues at full pace

‘From B to A’

‘Energy Aspiration’

‘USD 300 program’

‘Climb’

‘JV program’2011*-2014

BNOK 3.7

Total contribution from Hydro’s improvement programs (excl. Sapa)

2015-2016** BNOK 1.5

CCIP II

* USD 300 from 2009 ** Real 2014 termsRealized improvement efforts is YTD Q314 annualized.

Bigger: A solid platform for building an even stronger Hydro

Bauxite & Alumina Primary AluminiumEnergy• Move beyond nameplate

capacity• Further improve bauxite

positions • Mature CAP project and

Paragominas expansion for when time is right

• Mature captive growth opportunities

• Raise income potential from market operations

• Leverage value from Nordic power surplus

• Enhance position inhigh-margin segments

• Realize 100,000 tonnes creep in fully-owned smelters

• Extend technology lead with Karmøy pilot plant

• Mature Qatalum 2 and Alouette expansion for when time is right

• Expand automotive capacity to 200,000 t/yrby end-2016

• Increase recycling of post-consumed scrap above 250,000 t/year*

• Build positions and lift margins through technology leadership and innovation

Rolled Products

* Includes recycling ambition in Primary Metal

(53)

Reduce emissions,increase efficiency

Maximize user-phase benefits

Increase recycling,back to the loop

Energy and primary production

Aluminium in use

‘End-of-life’

Meeting consumer needsDeveloping alloys for resource efficient cars, buildings and packaging that save energy and emissions in use

Electrolysis technology pilotDeveloping the world’s most energy efficient electrolysis cells with the most limited CO2 footprint

Circular economyRecycling R&D to improve resource efficiency and avoid export of scarce European energy. Automation technology key to sorting post consumer scrap

(54)

Greener: Hydro aims to be climate neutral by 2020

Safe and responsible operations is a top priority

(55)

10.3

7.0

6.05.4

4.0 4.1 3.9

2.9

3.7 3.83.4 3.4 3.2

2.7

2002 2004 2006 2008 2010 2012 2014

TRI Rate*

* TRI rate defined as cases per 1 million hours worked

(56)

HydroAttractive positions

throughout the value chain

Financial strength

Improvement culture and

technologicalleadership

(57)

Bauxite & Alumina

High-quality asset portfolio

(58)

Bauxite licenses

Refining and mining competencies

External supply contracts

Sales contract portfolio

Alunortealumina refinery

Paragominas bauxite mine

CAP alumina refinery project

• Full financial exposure, increase ownership to 100% by 2016

• One of the world’s largest bauxite mines

• 2014 production 9.5 million tonnes

• Nameplate capacity of 9.9 million tonnes

• Possible expansion to 15 million tonnes

• Long-life resource

• 81% ownership• Paragominas expansion to

be developed in parallel• Full utilization of the existing

bauxite pipeline

• 92% ownership• World’s largest alumina refinery• 2014 production

5.9 million tonnes• Nameplate capacity of 6.3 million

tonnes• Bauxite supplied from

Paragominas and MRN• World-class conversion cost

position

MRN bauxite mine

• 5% ownership• Volume off-take agreement for

Vale’s 40% stake• Capacity 18 million tonnes

(59)

Improvements in NOK million

0

100

200

300

400

500

600

700

800

900

1000

1100

Strengthening the competitiveness of Bauxite & AluminaFrom B to A

Improvement categories

2011 - 2014 Ambition 2015

• Increase productivity and rightsize organization• Stabilize performance at nameplate capacity• Improve logistics efficiency

• Increase productivity and rightsize organization• Support production at nameplate capacity• Improve product flow and minimize tailings

• Base bauxite and alumina pricing on fundamentals• Increase logistical flexibility and optimize

scheduling

Alunorte

Paragominas

Commercial

NOK 1 billion

(60)

Paragominas – One of the world’s largest bauxite mines

• 2014 production: 9.5 million mt• Target to deliver production

increases and stabilize• Possible expansion:

up to 15 million mt• Long-life resource base

26%

25%19%

20%

9%

Labor EnergySupport & infrastructure Maintenance/consumablesOther costs

Bauxite operational mining costs in Paragominas

(61)

• Energy cost - Power and fuel

• Labor cost− Influenced by Brazilian wage level− Productivity improvements

• Maintenance and consumables− Influenced by Brazilian inflation

• Large fixed cost base

Paragominas bauxite mining costs 2014

* Cost element definition restated in 2014

(62)

Alunorte – World’s largest alumina refinery

• 2014 production: 5.9 million mt• Targeting stable production

above 6 million tonnes• World-class conversion cost position• Modern technology• Bauxite supplied from

Paragominas and MRN

Favorable integrated alumina cost position

(63)

• Implied alumina cost position 2014− USD 250 per mt− Alunorte, Paragominas and sourced alumina

• Bauxite− Internal bauxite from Paragominas at cost, sourced

bauxite from MRN

• Energy− First-quartile energy consumption – 8 GJ/mt− Energy mix of heavy fuel oil, coal and electric power

• Caustic soda− Competitive caustic soda consumption due

to bauxite with low level of reactive silica

• Other costs− Maintenance, labor, services and other

• Sourced alumina− Alumina purchased for resale

31%

13%38%

12%

6%

Bauxite Caustic soda EnergyOther costs Sourced alumina

Implied alumina cost* position 2014USD 250 per mt

* Realized alumina price minus Underlying EBITDA for B&A, per mt alumina sales

External alumina sourcing

(64)

• ~ 2.0 million mt of external alumina sourcing in 2015

• Long term off-take agreement with Rio Tinto − 900 000 mt annually from Yarwun

• Short- and medium term contracts− To balance and optimize position

geographically− Various pricing mechanisms− Older contracts linked to LME− New contracts mostly index− Fixed USD per mt for short-term

contracts

Alumina pricing shifting from LME-link to market fundamentals

(65)

• Future pricing should reflect fundamentals of bauxite and alumina value chain

• New norm for the industry− Index pricing and short to medium-term contracts − Getting wider acceptance in the market

• Hydro’s commercial strategy− Move towards index pricing (PAX)− Focus on selling to end-users based on a

global portfolio− Establish a premium for Alunorte quality− Selling 2-3 million mt annually of MRN

bauxite externally

100%

2015 2017 2020

Internal demand LME linked sales Index exposure

Index spot price exposure

(66)

Primary Metal

World-wide production networkPrimary aluminium annual production capacity

(67)

Qatar, 300 000 tonnes• Qatalum (50%): 300 000 tonnes• Expansion potential

Germany, 235 000 tonnes• Rheinwerk* (100%): 235 000 tonnes

Canada, 120 000 tonnes• Alouette (20%): 120 000 tonnes• Expansion potential

Brazil , 235 000 tonnes• Albras: (51%): 235 000 tonnes

Australia, 70 000 tonnes• Tomago (12%): 70 000 tonnes

Norway, 1 015 000 tonnes• Sunndal (100%) : 390 000 tonnes• Årdal (100%): 190 000 tonnes• Karmøy (100%): 190 000 tonnes• Høyanger (100%): 65 000 tonnes• Husnes (100%): 180 000 tonnes

Attributable capacity: 2.1 million mt. Consolidated capacity: 2.4 million tonnes (Slovalco and Albras are consolidated). The smelters have an additional remelt capacity: 0.5 million tonnes. Consolidated casthouse capacity: 2.9 million tonnes. Qatalum is equity accounted in Hydro’s results.* Rheinwerk smelter is included in the Rolled Products division for logistical reasons

2.1million tonnes

11%

49%

15%

3%

6%

11%

Slovakia, 90 000 tonnes• Slovalco (55%): 90 000 tonnes

4%

(68)

Delivering on ambitious USD 300 improvement program

0

50

100

150

200

250

300

Total annual improvement effect of NOK ~1.5 billion

2009-2013

Improvements in USD per mt*Improvement categories

* Compared to 2009 cost level. USD 300 per mt real term target for fully owned smelters excluding Neuss with 2009 as baseline. Effect of exchange rates and raw materials cost changes are neutralized

Technology costs/spin-offs

Maintenance and relining

Investments

Procurement

Organization and manning

Casthouse product margin

Logistics

Operational improvements• Improved current efficiency • Reduced power consumption• Reduced anode consumption

Fixed cost reductionsand lean operations

Further operational improvements

(69)

Improvements in USD per mt*

0

20

40

60

80

100

120

140

160

180

* Compared to 2011 cost level. USD 180 per mt in real terms corresponds to USD 150 in nominal terms. Effect of exchange rates , LME and raw materials cost changes are neutralized. Casthouse margins and cost above plants are not included.

Primary Metal joint ventures improvement programUSD 180 per mt improvements by end-2016, corresponding to NOK 1.2billion

Fixed cost reductionsand lean operations

Operational improvements

Additional improvements

Improvement categories

2012 - 2014 Ambition 2015-16

USD 180per mt

• Improved current efficiency• Reduced power consumption• Reduced anode consumption

Improvement drive yields results in primary productionUnderlying EBITDA per mt in USD for respective primary aluminium divisions

All figures based on public accounting data, not verified by Hydro. Data not adjusted for different accounting principles and non-specified underlying items. Hydro makes no representation as to the accuracy or completeness of such information. The analyses are based on assumptions subject to uncertainty and therefore intended only for general comparisons across companies and should not be used to support any individual investment decision. All results are provided for informational purposes only. Hydro figures includes Primary Metal, Metal Markets and attributable share of EBITDA and production in Qatalum.

2H 2012 1H 20131H 2012

Hydro Peers

-100

100

300

500

700

-100

100

300

500

700

2H 2013

-100

100

300

500

700

1H 2014

-100

100

300

500

700

2H 2014

-100

100

300

500

700

-100

100

300

500

700

(71)

• Operating for several years in Sunndal and Qatar

• Operating at:− 13.5 kWh/kg− 312 kA− 1.5 mt CO2/mt aluminium

• Continuous technology upgrading based on knowledge derived from HAL4e and the R&D portfolio

• Aiming for further productivity improvement through amperage increase

HAL 300 HAL4e• Benchmark technology on process

parameters and environmental footprint

• Prototype cells in operation since 2008 at the R&D center in Årdal, Norway

• Ready for industrial verification in Karmøy Technology Pilot

• Currently operating at:− 12.5 kWh/kg− 450 kA − 1.4 mt CO2/mt aluminium

R&D portfolio• HAL 4e Ultra – future vision− Significantly lower kWh/kg− New materials and cell design− Reduced investment costs

• A low energy version of HAL4e Ultra for a section of the Karmøy Technology Pilot is under development

• Carbon program for developing anodes with higher efficiency and higher robustness wrt. variations in raw material quality

Develop technology to fulfill ambitions

(72)

Metal Markets

(73)

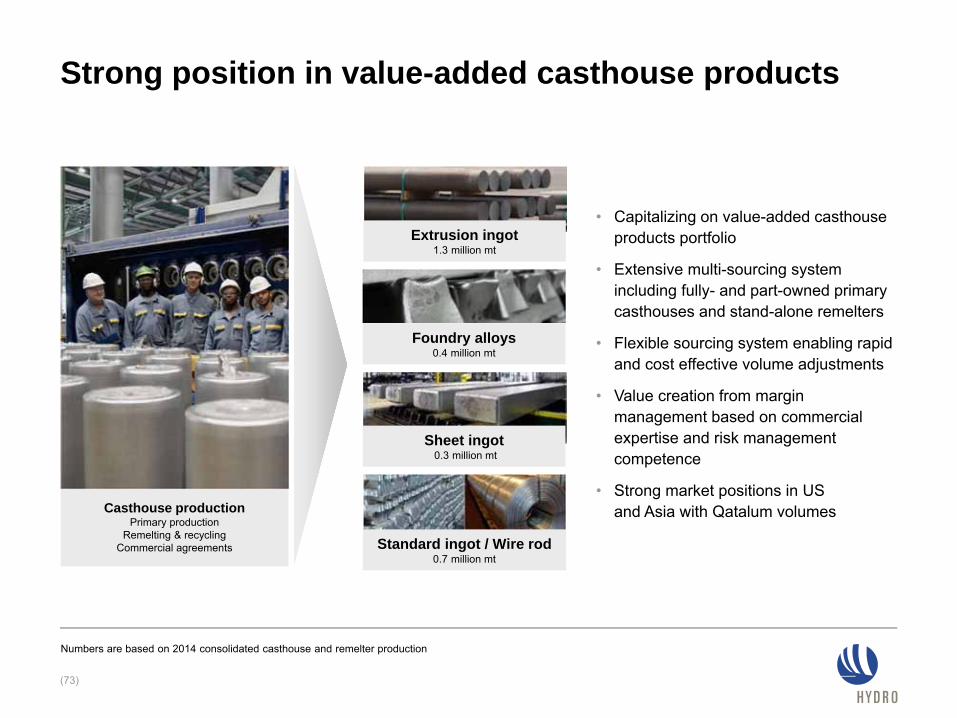

• Capitalizing on value-added casthouse products portfolio

• Extensive multi-sourcing system including fully- and part-owned primary casthouses and stand-alone remelters

• Flexible sourcing system enabling rapid and cost effective volume adjustments

• Value creation from margin management based on commercial expertise and risk management competence

• Strong market positions in US and Asia with Qatalum volumesCasthouse production

Primary productionRemelting & recycling

Commercial agreements

Strong position in value-added casthouse products

Numbers are based on 2014 consolidated casthouse and remelter production

Sheet ingot0.3 million mt

Extrusion ingot1.3 million mt

Foundry alloys0.4 million mt

Standard ingot / Wire rod0.7 million mt

Pricing of value-added products

(74)

Aluminium Standard ingot

Smelter Intermediate product Casthouse

Value added productsExtrusion ingot Foundry alloy Sheet ingot Wire rod

Traded on LME • US Midwest - 1020(in cent per pound)

• Duty paid IW Rotterdam• Duty unpaid IW Rotterdam

Traded on LME

Traded on LME & SHFE

• CIF Japan Premium (MJP)• Singapore In Warehouse• CIF South Korea

• Extrusion Ingot – Priced above standard ingot• Foundry Alloy – Priced above standard ingot• Sheet ingot – Priced above standard ingot• Wire rod - Priced above standard ingot

• Extrusion ingot – Priced above LME• Foundry Alloy – Priced partly above standard ingot and partly above LME• Sheet ingot – Priced above standard ingot• Wire rod - Priced partly above standard ingot and partly above LME

• Extrusion ingot – Priced partly above standard ingot and partly above LME• Foundry Alloy – Priced partly above standard ingot and partly above LME• Sheet ingot – Priced partly above standard ingot and partly above LME

US

Eur

ope

Asia

( 50)

0

50

100

150

200

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

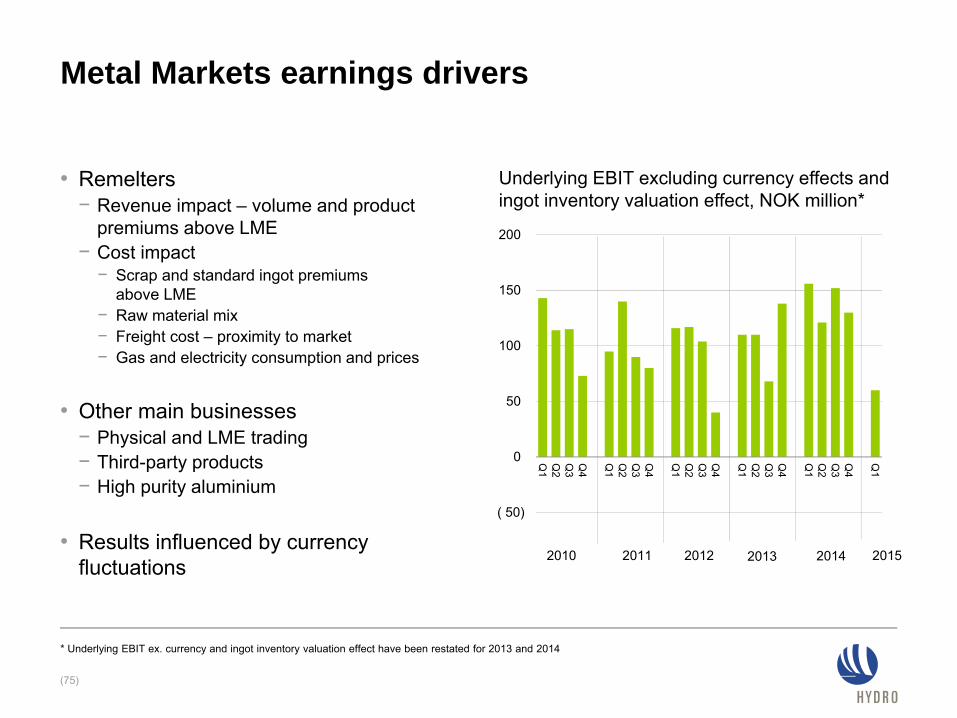

Metal Markets earnings drivers

(75)

• Remelters− Revenue impact – volume and product

premiums above LME− Cost impact − Scrap and standard ingot premiums

above LME− Raw material mix− Freight cost – proximity to market− Gas and electricity consumption and prices

• Other main businesses− Physical and LME trading− Third-party products− High purity aluminium

• Results influenced by currency fluctuations

Underlying EBIT excluding currency effects and ingot inventory valuation effect, NOK million*

2010 2011 2012 2013 2014 2015

* Underlying EBIT ex. currency and ingot inventory valuation effect have been restated for 2013 and 2014

(76)

Rolled Products

No. 1 flat rolled products producer in Europe

(77)

• World leader in high-end products foil and litho− Alunorf (JV 50%) – world’s largest rolling mill− Grevenbroich plant – world’s largest finishing mill

• High-grading product portfolio− Margin management and cash generation− Portfolio adjustment towards higher margins

• Capitalize on automotive market growth − Investment in new automotive capacity− Commissioning expected for 2nd half of 2016

• Extend recycling position − Installation of a Used Beverage Can (UBC)

recycling line beginning of 2016

12%

18%

8%

11%4%

28%

19%

Foil CanBuilding and other AutoHeat exchanger General engineeringLitho

External sales in tonnages 2014Total 946 kT

(78)

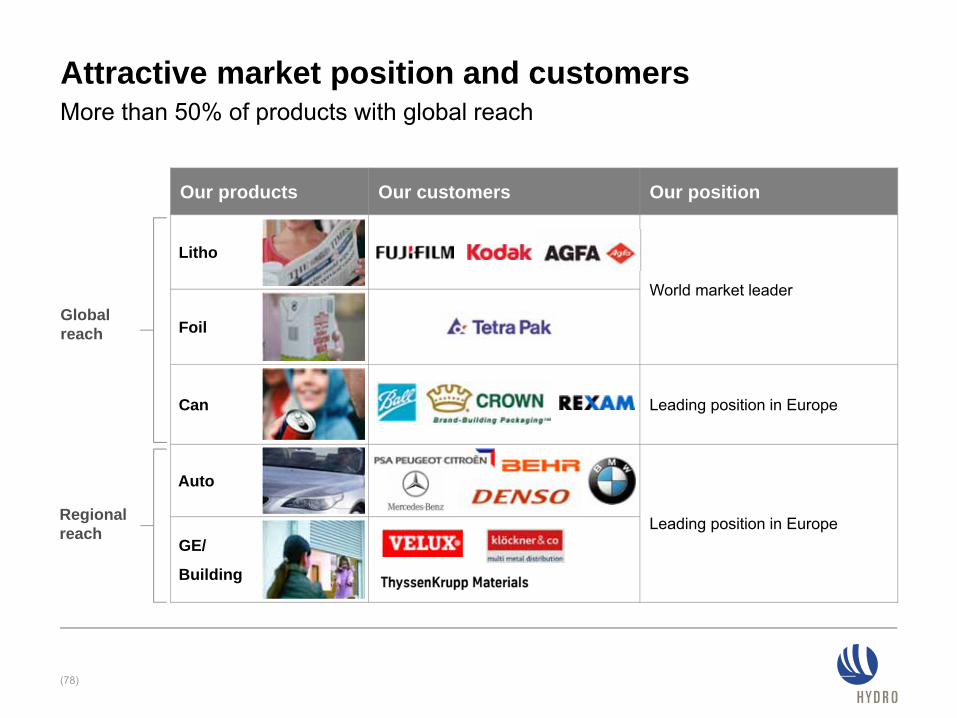

Our products Our customers Our position

Litho

World market leader

Foil

Can Leading position in Europe

Auto

Leading position in EuropeGE/

Building

Globalreach

Regionalreach

Attractive market position and customersMore than 50% of products with global reach

Hydro inside Hydro supplies premium European carmakers with aluminium

(79)

BMW 7 series

“Aluminium plays a major role in lightweight construction at the BMW Group”

“Audi believes aluminium still offers abundant potential, especially in the shape of the new,

higher-strength alloys”

“Lightweight construction is a core elementof Jaguar’s DNA and Jaguar is at the cutting-edge of aluminium technology

in the automotive industry”

New Mercedes C Class T

Peugeot 308

Audi Q7

Audi A6

Audi Q7

Porsche Macan

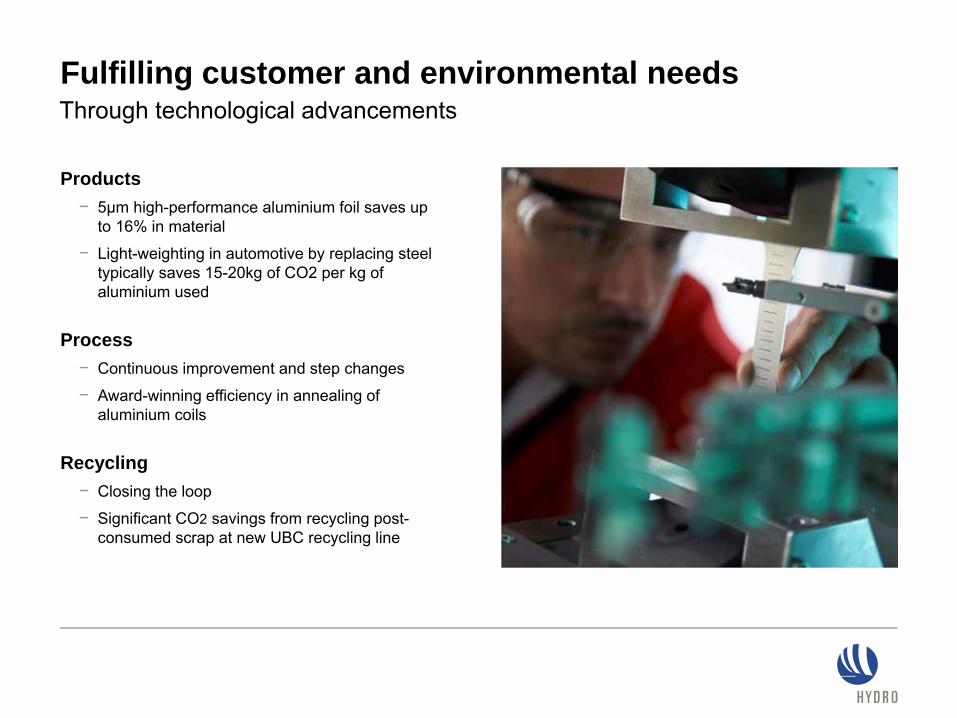

Fulfilling customer and environmental needsThrough technological advancements

Products− 5µm high-performance aluminium foil saves up

to 16% in material

− Light-weighting in automotive by replacing steel typically saves 15-20kg of CO2 per kg of aluminium used

Process− Continuous improvement and step changes

− Award-winning efficiency in annealing of aluminium coils

Recycling− Closing the loop

− Significant CO2 savings from recycling post-consumed scrap at new UBC recycling line

(400)

(200)

0

200

400

600

800

1 000

1 200

1 400

Rolled Products earnings drivers

(81)

• Contract structure− Margin business based on conversion price − LME element passed on to customers

− Range from spot contracts to multi-year contracts

• High share of fixed costs - volume sensitive

• Preferred supplier market position in high-end products

Underlying EBIT per tonne, NOK

2010 2011 2012 2013 2014 2015

2013 are adjusted to reflect IFRS11

(82)

Sapajoint venture

Sapa – global leader in extruded products

(83)

• 50/50 joint venture between Hydro and Orkla, established September 1, 2013, with 23,000 employees

• No. 1 position in North America and Europe

• Strong foothold in emerging markets

• Hydro supplies the new company with extrusion billets, ~400 000 tonnes per year at market prices

• Positioned for restructuring and value creation

Extrusions Europe

42%

Extrusions Americas

43%

Extrusions Asia2%

Building System

6%

Precision Tubing

7%

External sales of 1.4 million tonnes (2014)

Heavyweight company – lightweight material

• Partnership to supply structural aluminium tubing− Also provide ongoing development

support for future extrusion applications

• Ford F-150 2015 Model− Aluminium-alloy body− ~700 pounds lighter than 2014 model

Sapa JV delivers solutions to Ford F-150

(84)

World’s most selling vehicle

Picture with courtesy of Ford Motors

(85)

Energy

Power production increased to 10 TWh

(86)

• Power producing assets and ongoing projects− Maintain cost control in operations and projects− Holsbru and Vasstøl power plants into operation in

2012− Rjukan upgrade project ongoing – second outage

period during summer 2014− Vigeland acquisition completed, exemption from

concession requirement granted - no time limitations

• New growth projects− Mature new equity growth options− Growth potential around 0.5 TWh

• Framework conditions− Reversion regime secures full value of energy

assets− El-certificates support investments in new capacity

Power production capacity (TWh), per region and reversion year

0.2

3.2

3.1

3.0

0.52044-2049

2051-2057

No reversion

Telemark

Røldal-Suldal

Sogn

Normal production

10

Vigeland

2023

No reversion

Hydro’s energy map

(87)

North AmericaPower 1.7 TWh

Australia/AsiaPower 1.0 TWh

Middle EastPower 4.6 TWh

South AmericaPower 4.6 TWhCoal 5.3 TWhFuel oil 7.3 TWh

EuropePower 16.7 TWhNatural gas 3.3 TWh

Energy consumption in alumina refineries, smelters and rolling mills

Based on Hydro’s equity production end-2013

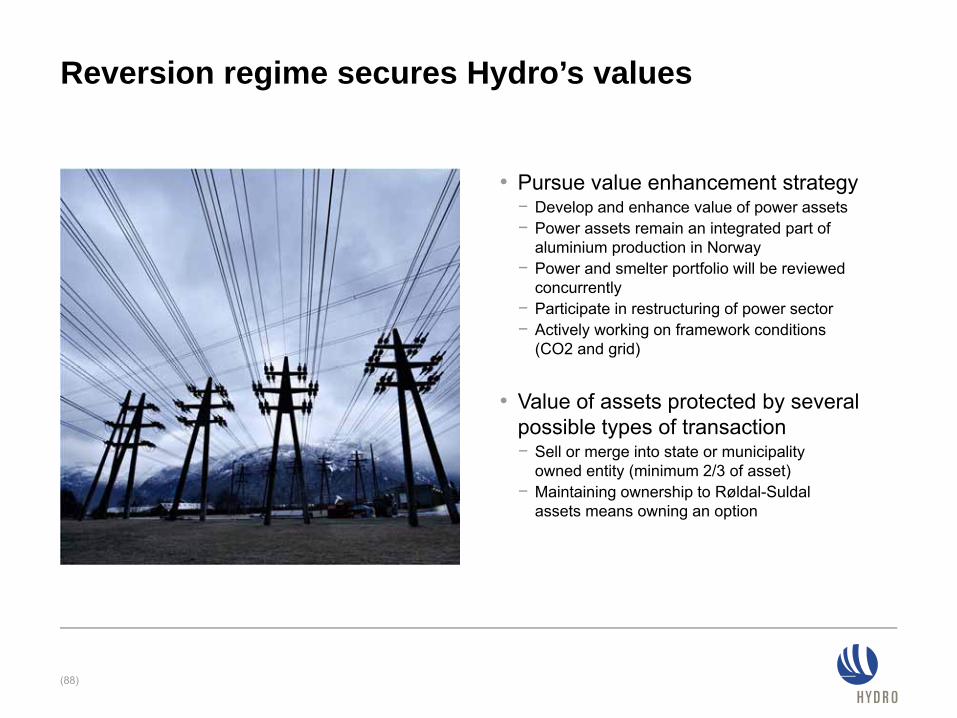

Reversion regime secures Hydro’s values

(88)

• Pursue value enhancement strategy− Develop and enhance value of power assets− Power assets remain an integrated part of

aluminium production in Norway− Power and smelter portfolio will be reviewed

concurrently− Participate in restructuring of power sector− Actively working on framework conditions

(CO2 and grid)

• Value of assets protected by several possible types of transaction− Sell or merge into state or municipality

owned entity (minimum 2/3 of asset)− Maintaining ownership to Røldal-Suldal

assets means owning an option

Energy earnings drivers

(89)

• Production and market prices strongly linked to hydrological conditions

• Stable annual EBIT contribution

• Seasonal market variations in demand and supply

• Occasional delink between area prices

• Power portfolio optimized versus market

• Stable cost base

Underlying EBIT* and spot price

Underlying EBIT and spot price

* Underlying EBIT 2003–2006 based on USGAAP

NOK million

NOK million

NOK/MWh

NOK/MWh

Underlying EBIT Spot price

0

100

200

300

400

500

600

0

200

400

600

800

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

0

100

200

300

400

500

0

500

1000

1500

2000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

(90)

Hydro’s value proposition• Improve relative industry

position• Capitalize on raw material positions• Maintain financial strength

and flexibility • Ensure competitive

shareholder return

(91)

Additional information

Shareholder and financial policy

(92)

• Hydro aims to give its shareholders competitive returns compared to alternative investments in peers

• Maintained dividend policy− Ordinary dividend: 40% of net income over the cycle− Average ordinary pay-out ratio 2010-2014 is ~95%*− Share buybacks and extraordinary dividends as supplement in

periods with strong financials

• Maintain investment-grade rating− Currently: BBB (S&P) & Baa2 (Moody’s) stable outlook− Competitive access to capital and important for Hydro’s business

model (counterparty risk and partnerships)

• Financial ratios over the business cycle− Funds from operations to net adjusted debt > 40%− Net adjusted debt to equity < 0.55

• USD 1.7 billion in multi-currency revolving credit facility maturing in 2019− Potential to extend through one-year extension option

• NOK 1.5 billion bond maturing in 2019

* NOK 1 2014 dividend per share proposed by Board of Directors, dependent on approval from the Annual General Meeting May 6, 2015

Hedging policy

(93)

• Bauxite & Alumina, Primary Metal− Remain primarily exposed to LME prices− Operational LME hedging

− One-month forward sales

− Currency exposure, mainly USD, NOK and BRL− Policy of maintaining long-term debt in USD

• Metal Markets, Rolled Products− Operational LME and currency hedging to

secure margin

• Volatility mitigated by strong balance sheet

• Flexibility to hedge LME or currency in certain cases

Adjusted net debt development Q1 2015

NOK billionMar 31

2015Dec 31

2014Sep 30

2014

Cash and cash equivalentsShort-term investmentsShort-term debtLong-term debt

7.22.5

(4.2)(5.7)

9.31.8

(6.0)(5.1)

6.01.7

(5.0)(4.8)

Net cash/(debt) (0.3) (0.1) (2.1)

Net pension liability at fair value, net of expected tax benefit

Other adjustments1

(7.8)

(5.3)

(8.2)

(5.3)

(6.6)

(5.4)

Net adjusted cash/(debt) (13.4) (13.6) (14.1)

1) Operating lease commitments and other obligations

(94)

Capital allocation mainly upstream

(95)

NOK billion • Long-term sustaining capex NOK ~3.5 billion annually

• Sustaining projects for 2014-2016:- Red mud disposal area- Bauxite tailing dam- Smelter relining

• Some growth projects impacting 2015:- RP Automotive line- RP UBC recycling line

• The majority of sustaining capital allocated upstream

2009 2010 2011 2012 2013 2014 2015E Long-term

Debt-financed investments QatalumInvestments QatalumGrowth capexSustaining capex

3.4 (3)

6.2

10.2

4.6 (1)

4.1

2.9 (2)

1) Excluding Vale assets acquisition2) Excluding Extruded Products and non-cash elements relating to capitalized lease obligations and the Vigeland acquisition.3) Excluding non-cash effects

~3.5

~6.8

0

150

300

450

600

750

900

Caustic soda (USD/mt)

Commodity prices drive industry costs

(96)

Source: Reuters Ecowin, PACE, CMAI/Harriman, Platts Bolivar Index, ANP

0

150

300

450

600

750

Fuel oil A1 (USD/mt)

0

30

60

90

120

150

180

Steam coal (USD/mt)

0

100

200

300

400

500

600

Petroleum coke FOB USG (USD/mt)

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

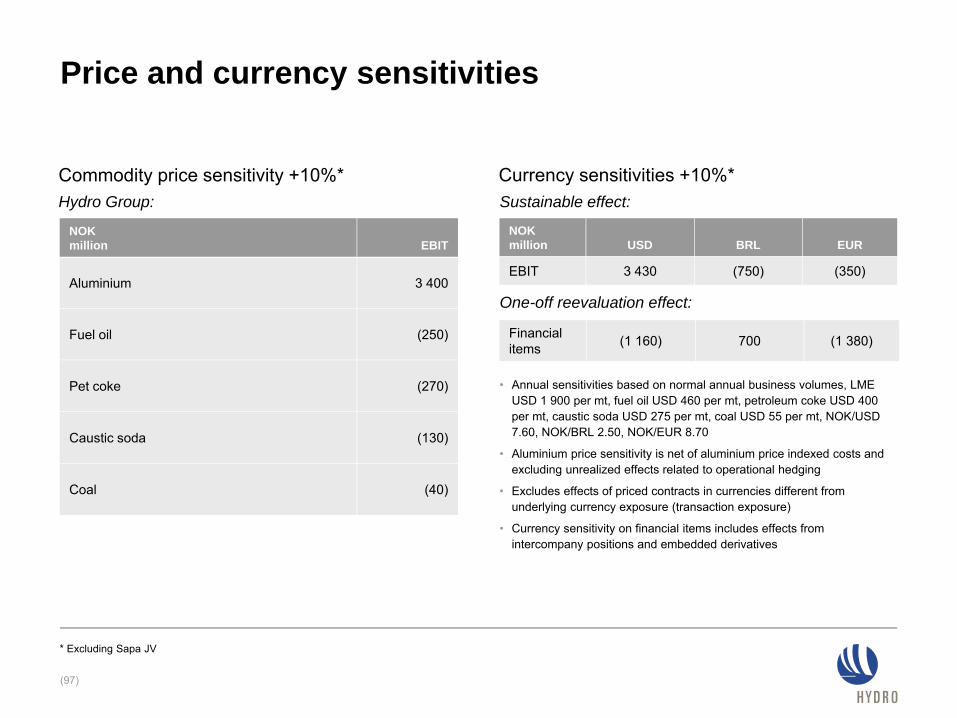

NOK million EBIT

Aluminium 3 400

Fuel oil (250)

Pet coke (270)

Caustic soda (130)

Coal (40)

NOK million USD BRL EUR

EBIT 3 430 (750) (350)

Currency sensitivities +10%*Commodity price sensitivity +10%*

• Annual sensitivities based on normal annual business volumes, LME USD 1 900 per mt, fuel oil USD 460 per mt, petroleum coke USD 400 per mt, caustic soda USD 275 per mt, coal USD 55 per mt, NOK/USD 7.60, NOK/BRL 2.50, NOK/EUR 8.70

• Aluminium price sensitivity is net of aluminium price indexed costs and excluding unrealized effects related to operational hedging

• Excludes effects of priced contracts in currencies different from underlying currency exposure (transaction exposure)

• Currency sensitivity on financial items includes effects from intercompany positions and embedded derivatives

* Excluding Sapa JV

(97)

Price and currency sensitivities

Sustainable effect:

One-off reevaluation effect:

Financial items (1 160) 700 (1 380)

Hydro Group:

Bauxite & Alumina sensitivities

(98)

Revenue impact• ~14.5% of 3-month LME price per tonne alumina

• ~One month lag• Realized alumina price lags PAX by one month

Cost impactBauxite• ~2.45 tonnes bauxite per tonne alumina• Pricing partly LME-linked for bauxite from MRN

Caustic soda• ~0.1 tonnes per tonne alumina• Prices based on IHS Chemical, pricing mainly monthly per

shipment

Energy• ~0.11 tonnes coal per tonne alumina, Platts prices, one year

volume contracts, weekly per shipment pricing• ~0.11 tonnes heavy fuel oil per tonne alumina, prices set by

ANP/Petrobras in Brazil, weekly pricing (ANP) or anytime (Petrobras)

• Increased use of coal as energy source in AlunorteUSD 1 900

per mtUSD 460

per mtUSD 275

per mtUSD 55per mt

USD 340 per mt

* 2015 Platts alumina index exposureCurrency rates used: NOK/USD 7.60, NOK/BRL 2.50, NOK/EUR 8.70

Sensitivities on underlying EBIT if +10% in priceNOK million

(40)(130)

(250)

525

835

Fuel oilPAX* CoalAluminium Caustic soda

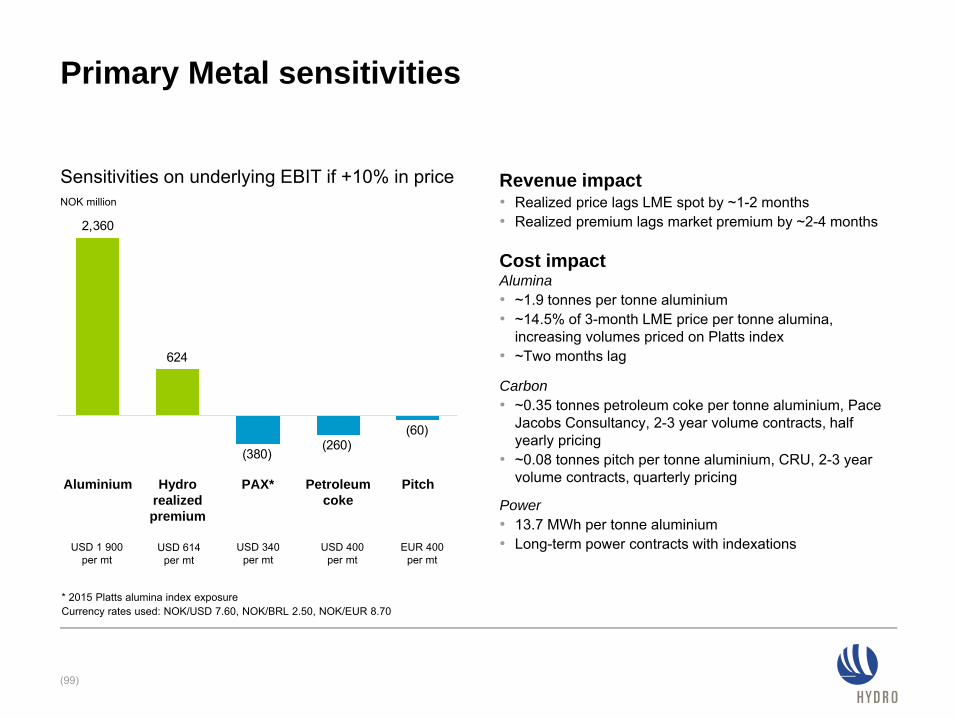

Primary Metal sensitivities

(99)

Revenue impact• Realized price lags LME spot by ~1-2 months• Realized premium lags market premium by ~2-4 months

Cost impactAlumina• ~1.9 tonnes per tonne aluminium• ~14.5% of 3-month LME price per tonne alumina,

increasing volumes priced on Platts index• ~Two months lag

Carbon• ~0.35 tonnes petroleum coke per tonne aluminium, Pace

Jacobs Consultancy, 2-3 year volume contracts, half yearly pricing

• ~0.08 tonnes pitch per tonne aluminium, CRU, 2-3 year volume contracts, quarterly pricing

Power• 13.7 MWh per tonne aluminium• Long-term power contracts with indexationsUSD 1 900

per mtUSD 400

per mtEUR 400

per mtUSD 614

per mtUSD 340

per mt

Sensitivities on underlying EBIT if +10% in priceNOK million

* 2015 Platts alumina index exposureCurrency rates used: NOK/USD 7.60, NOK/BRL 2.50, NOK/EUR 8.70

(60)(260)

(380)

624

2,360

PAX*Hydro realized premium

Aluminium Petroleum coke

Pitch

Percent USD EUR BRLNOK & Others

Bauxite & Alumina 100%

Primary Metal 25% 20% 55%

Metal Markets 25% 75%

Rolled Products 90% 10%

Energy 100%

Other & Eliminations 100%

(100)

Depreciation by currency and business area

Depreciation currency exposure by business area Depreciation by business area*

39%2%

39%

1%4%

15%

Metal Markets

Rolled Products

Other & Eliminations

Energy

Bauxite and alumina

Primary Metal

* Based on 2014 depreciation figures

Total 2014 depreciation 4.6 BNOK

(101)

NOK million (+=loss/()=gain) Q1 2015

Unrealized derivative effects on LME related contracts Bauxite & alumina 3

Total impact Bauxite & alumina 3

Unrealized derivative effects on LME related contracts Primary metal 54

Unrealized effects on power contracts Primary metal 2

Total impact Primary metal 56

Unrealized derivative effects on LME related contracts Metal markets 146

Total impact Metal markets 146

Unrealized derivative effects on LME related contracts Rolled products (80)

Metal effect Rolled products (61)

Total impact Rolled products (141)

Unrealized derivative effects on power contracts Energy 1

Total impact Energy 1

Unrealized derivative effects on power contracts Other and eliminations (154)

Unrealized derivative effects on LME related contracts Other and eliminations 17

Items excluded in equity accounted investment (Sapa) Other and eliminations 74

Total impact Other and eliminations (63)

Total EBIT Hydro 2

Net foreign exchange (gain)/loss Hydro 1 587

Income (loss) before tax Hydro 1 589

Calculated income tax effect Hydro (454)

Net income (loss) Hydro 1 134

Items excluded from underlying results - 2015

(102)

NOK million (+=loss/()=gain) Q1 2014 Q2 2014 Q3 2014 Q4 2014 2014

Unrealized derivative effects on LME related contracts Bauxite & Alumina (4) (1) (2) (10) (16)

Total impact Bauxite & Alumina (4) (1) (2) (10) (16)

Unrealized derivative effects on LME related contracts Primary metal (12) (38) (36) - (86)

Unrealized effects on power contracts Primary metal 43 (8) 1 27 63

Unrealized derivative effects on power contracts (Søral) Primary metal (33) 24 (64) 57 (16)

Unrealized derivative effects on raw material contracts Primary metal 10 9 9 10 37

Impairment charges (Qatalum) Primary metal - - 28 - 28

Insurance compensation (Qatalum) Primary metal - - - (55) (55)

Transaction effects Søral acquisition Primary metal - - - 38 38

Total impact Primary metal 8 (14) (62) 77 9

Unrealized derivative effects on LME related contracts Metal Markets 35 6 (94) (64) (117)

Impairment charges Metal Markets 33 - - - 33

Total impact Metal Markets 69 6 (94) (64) (83)

Unrealized derivative effects on LME related contracts Rolled Products (16) (101) (79) 76 (119)

Metal effect Rolled Products - (58) (202) (189) (449)

Impairment charges Rolled Products - - - 145 145

Total impact Rolled Products (16) (159) (281) 32 (423)

Unrealized derivative effects on power contracts Energy 3 4 (1) (2) 4

Total impact Energy 3 4 (1) (2) 4

Unrealized derivative effects on power contracts Other and Eliminations (198) 12 1 170 (16)

Unrealized derivative effects on LME related contracts Other and Eliminations 1 (2) (9) (3) (13)

(Gains)/Losses on divestments Other and Eliminations - (8) - - (8)

Items excluded in equity accounted investment (Sapa) Other and Eliminations 86 87 2 337 512

Other effects Other and Eliminations - - - 53 53

Total impact Other and Eliminations (111) 88 (7) 558 528

Total EBIT Hydro (50) (75) (447) 591 18

Net foreign exchange (gain)/loss Hydro (193) 101 1 001 2 252 3 161

Income (loss) before tax Hydro (244) 26 554 2 843 3 179

Calculated income tax effect Hydro 170 23 (176) (696) (680)

Net income (loss) Hydro (74) 49 378 2 147 2 499

Items excluded from underlying results - 2014

Underlying EBIT

Underlying EBITDA

2013 are adjusted to reflect IFRS11

(103)

NOK million Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Year 2013 Year 2014

Bauxite & Alumina (63) (244) (370) (379) (288) (269) (26) 528 780 (1 057) (55)

Primary Metal 364 237 337 484 312 420 1 216 1 989 2 012 1 422 3 937

Metal Markets 146 147 111 190 141 100 171 221 24 594 634

Rolled Products 152 183 181 100 181 177 243 96 292 615 698

Energy 517 268 485 383 435 169 234 360 382 1 653 1 197

Other and Eliminations (38) (70) (87) (306) (8) (52) (349) (308) (281) (502) (717)

Total 1 076 520 658 471 772 544 1 490 2 886 3 208 2 725 5 692

NOK million Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Year 2013 Year 2014

Bauxite & Alumina 366 203 47 45 122 162 417 1 046 1 240 662 1 747

Primary Metal 838 713 802 940 753 852 1 651 2 489 2 522 3 293 5 745

Metal Markets 163 165 149 214 157 120 192 243 47 691 712

Rolled Products 311 346 351 284 351 350 417 280 465 1 293 1 398

Energy 557 302 523 420 474 209 275 402 429 1 803 1 360

Other and Eliminations (24) (55) (72) (285) 4 (40) (336) (290) (267) (435) (662)

Total 2 212 1 674 1 801 1 619 1 861 1 653 2 615 4 170 4 437 7 306 10 299

Operating segment information

EBIT

EBITDA

(104)

2013 are adjusted to reflect IFRS11

NOK million Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Year 2013 Year 2014

Bauxite & Alumina (76) (241) (370) (491) (284) (269) (23) 537 776 (1 178) (39)

Primary Metal 19 122 338 377 303 434 1 278 1 912 1 956 855 3 928

Metal Markets 228 121 116 202 73 93 265 285 (122) 666 717

Rolled Products 110 (19) 74 (83) 197 336 525 64 433 83 1 121

Energy 513 271 481 391 431 165 235 362 381 1 657 1 193

Other and Eliminations (89) 122 (43) (410) 102 (140) (342) (866) (218) (420) (1 245)

Total 704 376 596 (14) 822 620 1 937 2 295 3 206 1 663 5 674

NOK million Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Year 2013 Year 2014

Bauxite & Alumina 353 207 47 (67) 125 163 419 1 056 1 237 540 1 763

Primary Metal 492 597 803 833 745 866 1 713 2 413 2 467 2 726 5 736

Metal Markets 245 139 153 226 122 114 286 307 (99) 764 829

Rolled Products 270 144 245 102 367 508 698 393 607 761 1 966

Energy 553 306 519 429 471 205 276 404 428 1 807 1 355

Other and Eliminations (74) 138 (28) (309) 115 (127) (329) (848) (204) (274) (1 190)

Total 1 839 1 531 1 739 1 214 1 944 1 728 3 062 3 725 4 436 6 323 10 460

Operating segment information

Total revenue

External revenue

(105)

2013 are adjusted to reflect IFRS 11

NOK million Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Year 2013 Year 2014

Bauxite & Alumina 3 304 3 147 3 354 3 546 3 511 3 828 3 737 4 770 5 461 13 350 15 847

Primary Metal 5 945 5 896 5 884 5 554 6 618 6 384 6 986 8 075 9 096 23 279 28 064

Metal Markets 9 853 9 880 9 061 8 996 10 292 10 109 10 919 11 709 12 181 37 791 43 029

Rolled Products 5 015 5 205 5 005 4 868 5 238 5 275 5 618 5 324 6 170 20 092 21 455

Energy 1 762 1 246 1 674 1 596 1 539 1 381 1 492 1 891 1 553 6 279 6 303

Other and Eliminations (9 770) (9 322) (8 833) (7 990) (8 917) (8 706) (9 055) (10 112) (11 171) (35 914) (36 790)

Total 16 109 16 052 16 145 16 570 18 282 18 272 19 698 21 656 23 290 64 877 77 907

NOK million Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Year 2013 Year 2014

Bauxite & Alumina 1 982 1 894 2 077 2 171 2 208 2 404 2 257 2 699 3 387 8 124 9 568

Primary Metal 813 1 040 1 025 988 1 227 1 337 1 590 2 242 1 789 3 866 6 397

Metal Markets 7 429 7 321 7 228 7 668 8 719 8 853 9 784 10 625 11 315 29 646 37 981

Rolled Products 5 032 5 284 5 002 4 968 5 290 5 212 5 498 5 345 6 079 20 286 21 345

Energy 826 489 779 737 807 436 540 710 698 2 830 2 492

Other and Eliminations 28 24 34 38 31 29 28 35 21 124 124

Total 16 109 16 052 16 145 16 570 18 282 18 272 19 698 21 656 23 290 64 877 77 907

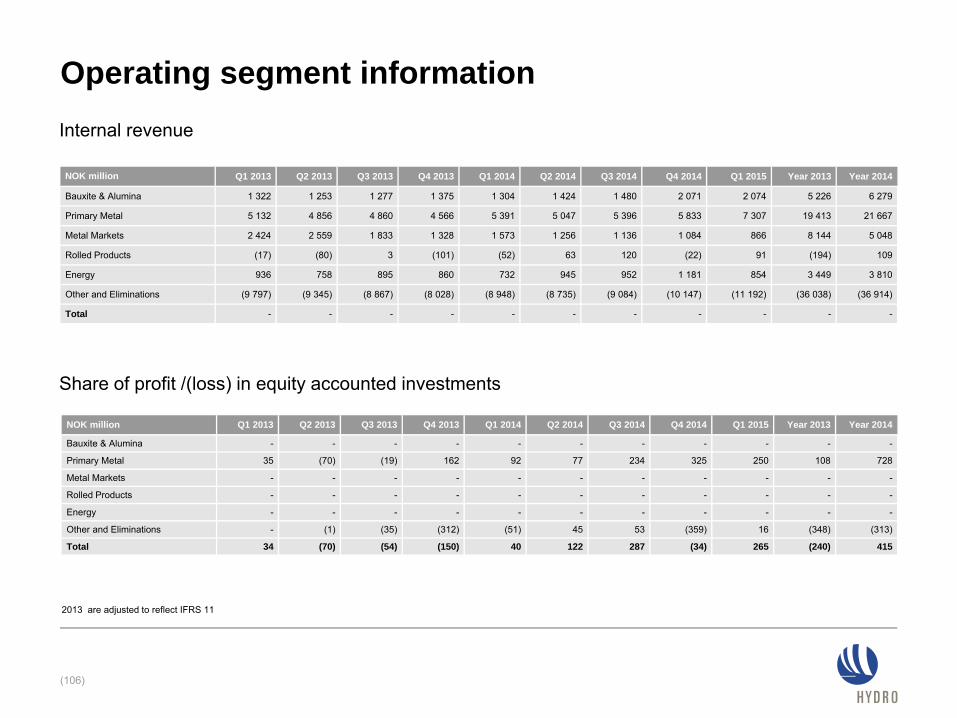

Operating segment information

Internal revenue

Share of profit /(loss) in equity accounted investments

(106)

2013 are adjusted to reflect IFRS 11

NOK million Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Year 2013 Year 2014

Bauxite & Alumina 1 322 1 253 1 277 1 375 1 304 1 424 1 480 2 071 2 074 5 226 6 279

Primary Metal 5 132 4 856 4 860 4 566 5 391 5 047 5 396 5 833 7 307 19 413 21 667

Metal Markets 2 424 2 559 1 833 1 328 1 573 1 256 1 136 1 084 866 8 144 5 048

Rolled Products (17) (80) 3 (101) (52) 63 120 (22) 91 (194) 109

Energy 936 758 895 860 732 945 952 1 181 854 3 449 3 810

Other and Eliminations (9 797) (9 345) (8 867) (8 028) (8 948) (8 735) (9 084) (10 147) (11 192) (36 038) (36 914)

Total - - - - - - - - - - -

NOK million Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Year 2013 Year 2014

Bauxite & Alumina - - - - - - - - - - -

Primary Metal 35 (70) (19) 162 92 77 234 325 250 108 728

Metal Markets - - - - - - - - - - -

Rolled Products - - - - - - - - - - -

Energy - - - - - - - - - - -

Other and Eliminations - (1) (35) (312) (51) 45 53 (359) 16 (348) (313)

Total 34 (70) (54) (150) 40 122 287 (34) 265 (240) 415

Operating segment information

Graph excludes NOK 1 billion in capital employed in Other and Eliminations

Capital employed – upstream focus

(107)

Operating segment information

NOK million Mar 31, 2015

Bauxite & Alumina 32 636

Primary Metal 30 547

Metal Markets 3 539

Rolled Products 10 493

Energy 2 857

Other and Eliminations (992)

Total 79 079

Bauxite & Alumina 41%

Primary Metal 38%

Metal Markets 4%

Rolled Products 13%

Energy 4%

NOK million Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Year 2013 Year 2014

Bauxite & Alumina 429 448 417 424 410 431 442 519 460 1 718 1 802

Primary Metal 470 472 461 452 437 427 431 499 511 1 855 1 794

Metal Markets 18 18 38 24 49 21 21 22 23 98 112

Rolled Products 160 163 170 184 170 172 174 329 173 677 845

Energy 40 35 37 37 39 40 41 42 47 150 162

Other and Eliminations 15 15 15 101 13 13 13 17 15 146 55

Total 1 131 1 150 1 139 1 223 1 117 1 104 1 121 1 428 1 229 4 644 4 771

Depreciation, amortization and impairment

2013 are adjusted to reflect IFRS 11

Income statements

(108)

NOK million Q1 2015 Q4 2014 Q1 2014 Year 2014

RevenueShare of the profit (loss) in equity accounted investmentsOther income, net

23 290265271

21 656(34)327

18 28240

132

77 907415751

Total revenue and income 23 827 21 948 18 454 79 073

Raw material and energy expenseEmployee benefit expenseDepreciation, amortization and impairmentOther expenses

14 6622 2951 2292 435

13 6972 1041 4282 424

12 2872 0331 1172 194

51 4808 0894 7719 059

Earnings before financial items and tax (EBIT) 3 206 2 295 822 5 674

Financial incomeFinancial expense

88(1 768)

115(2 456)

6329

347(3 900)

Income (loss) from continuing operations before taxIncome taxes

1 526(455)

(46)(122)

914(452)

2 121(892)

Net income (loss) 1 072 (168) 462 1 228

Net income (loss) attributable to minority interestNet income (loss) attributable to Hydro shareholders

124948

202(370)

69393

432797

Earnings per share attributable to Hydro shareholders 0.46 (0.18) 0.19 0.39

NOK million Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Year2013 Year2014

Net income (loss) 263 (665) 321 (758) 462 269 665 (168) 1 072 (839) 1 228

Underlying net income (loss) 649 427 393 140 388 318 1 043 1 979 2 206 1 610 3 728

Earnings per share 0.14 (0.31) 0.11 (0.39) 0.19 0.09 0.29 (0.18) 0.46 (0.45) 0.39

Underlying earnings per share 0.30 0.19 0.14 0.02 0.16 0.13 0.43 0.83 0.95 0.65 1.55

2013 are adjusted to reflect IFRS 11

(109)

NOK million Mar 31 2015 Dec 31 2014 Sep 30 2014 Jun 30 2014 Mar 31 2014

Cash and cash equivalentsShort-term investmentsAccounts receivableInventoriesOther current assets

7 1722 456

15 12213 392

272

9 2531 786

11 70312 642

543

6 0451 745

11 28010 334

345

6 6171 765

10 83510 213

371

6 4763 081

11 1169 599

325

Property, plant and equipmentIntangible assetsInvestments accounted for using the equity methodPrepaid pensionOther non-current assets

50 9525 332

18 6793 7536 015

55 7195 947

18 0952 8817 703

51 6305 481

17 4422 8977 075

54 0415 828

16 7173 1787 082

52 5595 598

16 7753 8016 394

Total assets 123 145 126 273 114 275 116 647 115 724

Bank-loans and other interest-bearing short-term debtTrade and other payablesOther current liabilities

4 23910 5934 373

6 0399 6633 414

5 0078 5892 904

6 1418 9362 608

6 2559 0733 002

Long-term debtProvisionsPension liabilitiesDeferred tax liabilitiesOther non-current liabilities

5 7222 802

13 4071 3183 146

5 1283 993

12 7961 6763 622

4 8502 583

10 7722 4952 476

4 0932 857

10 2572 8942 599

3 9412 7149 7982 8332 133

Equity attributable to Hydro shareholdersMinority interest

72 0685 477

74 0305 911

69 1155 484

70 5425 720

70 5335 443

Total liabilities and equity 123 145 126 273 114 275 116 647 115 724

Balance sheets

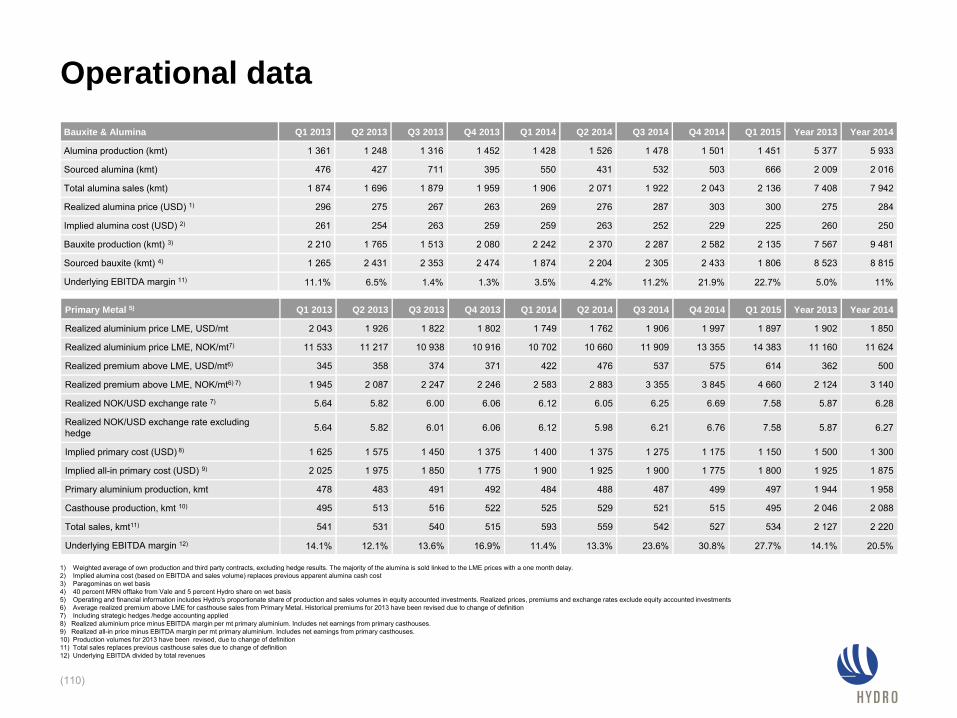

1) Weighted average of own production and third party contracts, excluding hedge results. The majority of the alumina is sold linked to the LME prices with a one month delay.2) Implied alumina cost (based on EBITDA and sales volume) replaces previous apparent alumina cash cost3) Paragominas on wet basis4) 40 percent MRN offtake from Vale and 5 percent Hydro share on wet basis5) Operating and financial information includes Hydro's proportionate share of production and sales volumes in equity accounted investments. Realized prices, premiums and exchange rates exclude equity accounted investments6) Average realized premium above LME for casthouse sales from Primary Metal. Historical premiums for 2013 have been revised due to change of definition7) Including strategic hedges /hedge accounting applied8) Realized aluminium price minus EBITDA margin per mt primary aluminium. Includes net earnings from primary casthouses.9) Realized all-in price minus EBITDA margin per mt primary aluminium. Includes net earnings from primary casthouses.10) Production volumes for 2013 have been revised, due to change of definition11) Total sales replaces previous casthouse sales due to change of definition12) Underlying EBITDA divided by total revenues

(110)

Bauxite & Alumina Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Year 2013 Year 2014

Alumina production (kmt) 1 361 1 248 1 316 1 452 1 428 1 526 1 478 1 501 1 451 5 377 5 933

Sourced alumina (kmt) 476 427 711 395 550 431 532 503 666 2 009 2 016

Total alumina sales (kmt) 1 874 1 696 1 879 1 959 1 906 2 071 1 922 2 043 2 136 7 408 7 942

Realized alumina price (USD) 1) 296 275 267 263 269 276 287 303 300 275 284

Implied alumina cost (USD) 2) 261 254 263 259 259 263 252 229 225 260 250