Embed Size (px)

Citation preview

Investor Presentation

Acquisition of Huntsman’s Integrated EO/PO Assets

8 August 2019

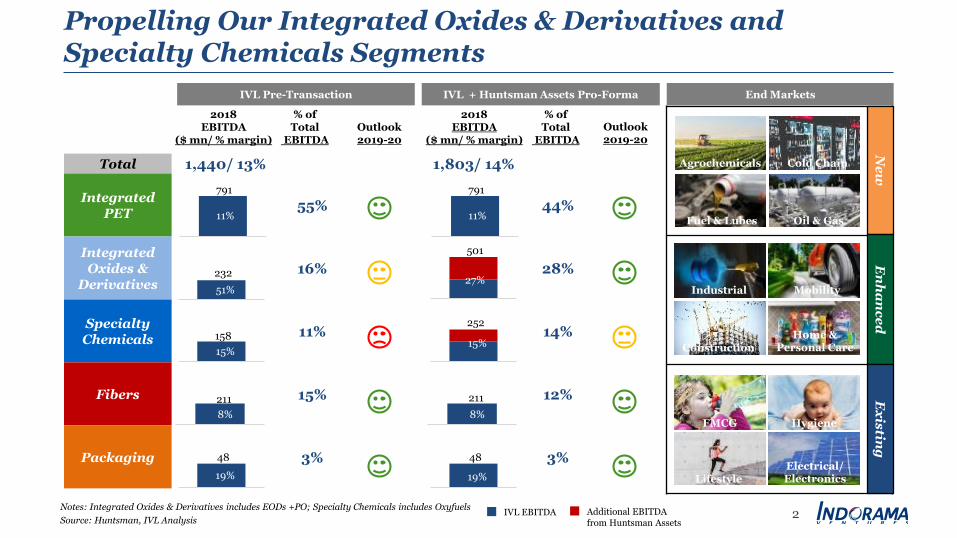

Total 1,440/ 13% 1,803/ 14%

Integrated PET

55% 44%

Integrated Oxides &

Derivatives16% 28%

SpecialtyChemicals

11% 14%

Fibers 15% 12%

Packaging 3% 3%

791

232

158

48

211

2018EBITDA

($ mn/ % margin)

% of Total

EBITDAOutlook2019-20

IVL + Huntsman Assets Pro-Forma

% of Total

EBITDA

Outlook2019-20

791

501

252

48

211

Propelling Our Integrated Oxides & Derivatives and Specialty Chemicals Segments

Notes: Integrated Oxides & Derivatives includes EODs +PO; Specialty Chemicals includes Oxyfuels

Source: Huntsman, IVL Analysis

11%

51%

15%

8%

19%

11%

27%

15%

8%

19%

IVL EBITDA Additional EBITDA from Huntsman Assets

2018EBITDA

($ mn/ % margin)

IVL Pre-Transaction End Markets

Ne

wE

nh

an

ce

dE

xis

ting

Construction

Industrial

Home & Personal Care

Mobility

FMCG Hygiene

Electrical/ElectronicsLifestyle

Fuel & Lubes

Agrochemicals

Oil & Gas

Cold Chain

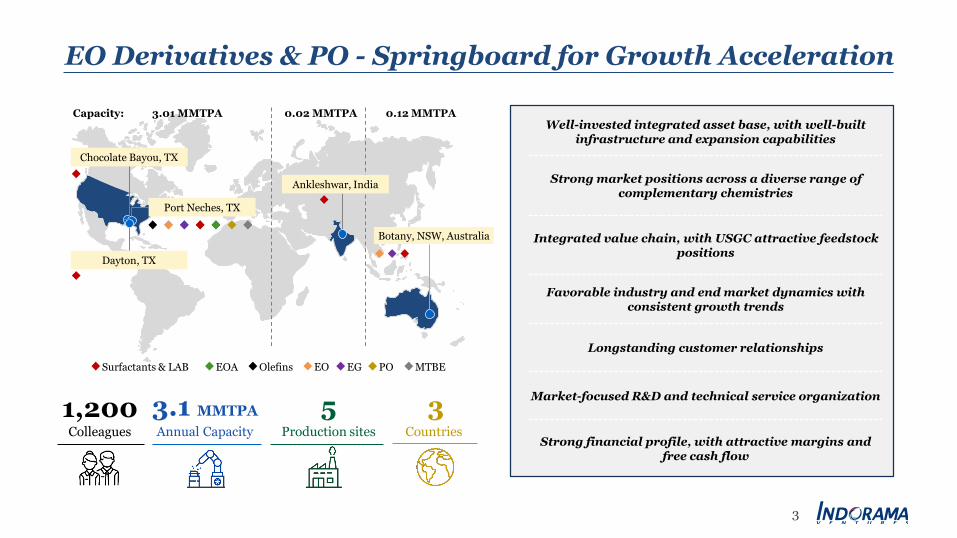

2

5Production sites

3Countries

EO Derivatives & PO - Springboard for Growth Acceleration

1,200Colleagues

3.1 MMTPA

Annual Capacity

Chocolate Bayou, TX

Port Neches, TX

Dayton, TX

Botany, NSW, Australia

EOA EGSurfactants & LAB MTBEOlefins EO PO

Well-invested integrated asset base, with well-built infrastructure and expansion capabilities

Strong market positions across a diverse range of complementary chemistries

Integrated value chain, with USGC attractive feedstock positions

Favorable industry and end market dynamics with consistent growth trends

Longstanding customer relationships

Market-focused R&D and technical service organization

Strong financial profile, with attractive margins and free cash flow

Capacity: 3.01 MMTPA 0.02 MMTPA 0.12 MMTPA

Ankleshwar, India

3

Home & Personal Care(i.e. Detergents, Cleansers and Shampoo)

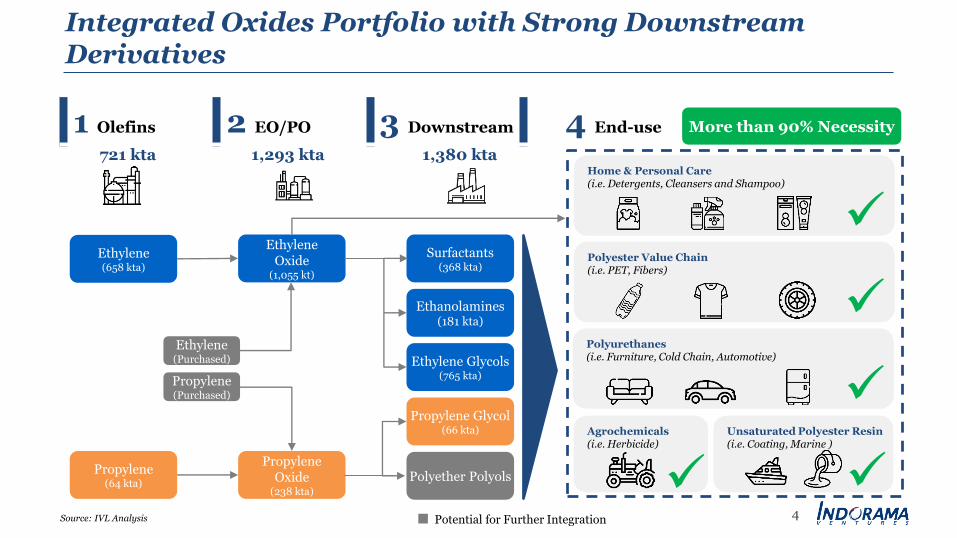

Integrated Oxides Portfolio with Strong Downstream Derivatives

4Source: IVL Analysis

Ethylene(658 kta)

EthyleneOxide

(1,055 kt)

Surfactants(368 kta)

Ethanolamines(181 kta)

Ethylene Glycols(765 kta)

Propylene(64 kta)

PropyleneOxide

(238 kta)

Propylene Glycol(66 kta)

Polyether Polyols

1 Olefins 2 EO/PO 3 Downstream 4 End-use

Agrochemicals(i.e. Herbicide)

Polyester Value Chain(i.e. PET, Fibers)

Polyurethanes(i.e. Furniture, Cold Chain, Automotive)

Unsaturated Polyester Resin(i.e. Coating, Marine )

721 kta 1,293 kta 1,380 kta

More than 90% Necessity

Potential for Further Integration

Ethylene(Purchased)

Propylene(Purchased)

IVL’s Downstream Integration and Portfolio Diversification Strategy Provides Steady and Visible Earnings

0%

5%

10%

15%

20%

2014 2015 2016 2017 2018

Asian Petchems IVL + Huntsman's Assets Pro-Forma

EBITDA Margin

IVL Pro-Forma vs. Asian Petchems(*)

5Note: *Asian Petchems include: Hanwha, PTTGC, Lotte Chemical, and Formosa Petrochemical

Source: Eikon, IVL Analysis

Key Products

IVL+

Huntsman Assets

Typical AsianPetchem

Companies

Integrated PTA/PET

Surfactants

Ethylene Oxide

Propylene Oxide

Ethylene Glycol

Fiber

Polyethylene

Polypropylene

Ethylene Glycol

Aromatics (BTX)

Refined Products

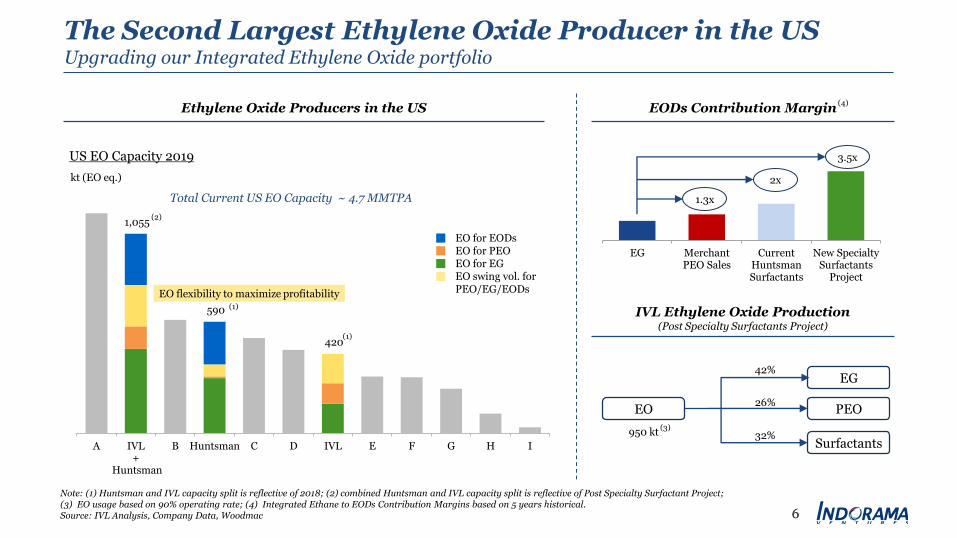

1,055

590

420

A IVL+

Huntsman

B Huntsman C D IVL E F G H I

Note: (1) Huntsman and IVL capacity split is reflective of 2018; (2) combined Huntsman and IVL capacity split is reflective of Post Specialty Surfactant Project; (3) EO usage based on 90% operating rate; (4) Integrated Ethane to EODs Contribution Margins based on 5 years historical.Source: IVL Analysis, Company Data, Woodmac

The Second Largest Ethylene Oxide Producer in the USUpgrading our Integrated Ethylene Oxide portfolio

Total Current US EO Capacity ~ 4.7 MMTPA

kt (EO eq.)

Ethylene Oxide Producers in the US

EO for EODsEO for PEOEO for EGEO swing vol. for PEO/EG/EODs

US EO Capacity 2019

6

EG MerchantPEO Sales

CurrentHuntsmanSurfactants

New SpecialtySurfactants

Project

EODs Contribution Margin

IVL Ethylene Oxide Production(Post Specialty Surfactants Project)

1.3x

2x

3.5x

EO flexibility to maximize profitability(1)

(1)

(2)

EO

EG

PEO

Surfactants

42%

26%

32%950 kt(3)

(4)

6

7Note: EODs excluding EG

Source: Woodmac, Valence Group, IVL Analysis

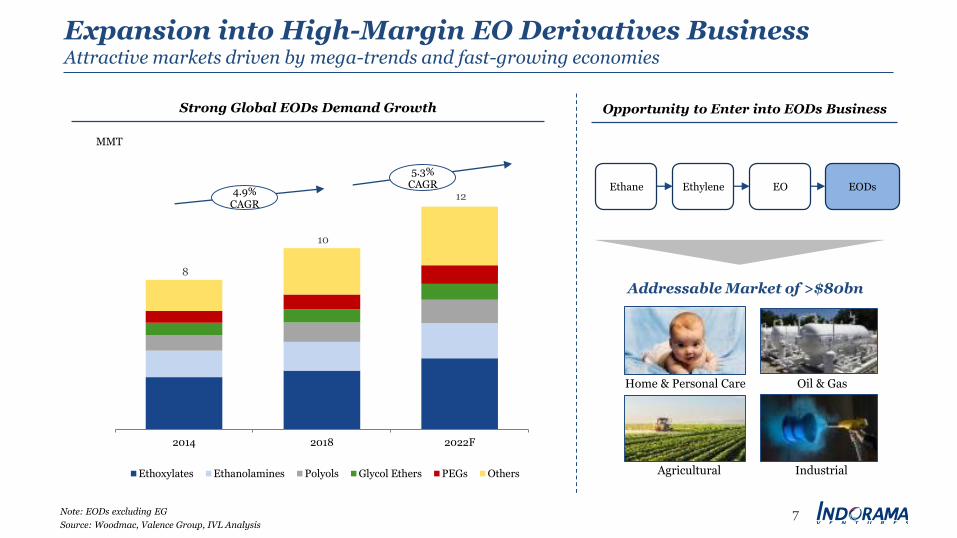

Expansion into High-Margin EO Derivatives BusinessAttractive markets driven by mega-trends and fast-growing economies

8

10

12

2014 2018 2022F

Ethoxylates Ethanolamines Polyols Glycol Ethers PEGs Others

4.9%CAGR

5.3%CAGR

Strong Global EODs Demand Growth

MMT

Opportunity to Enter into EODs Business

Ethane Ethylene EO EODs

Home & Personal Care

Agricultural

Oil & Gas

Industrial

Addressable Market of >$80bn

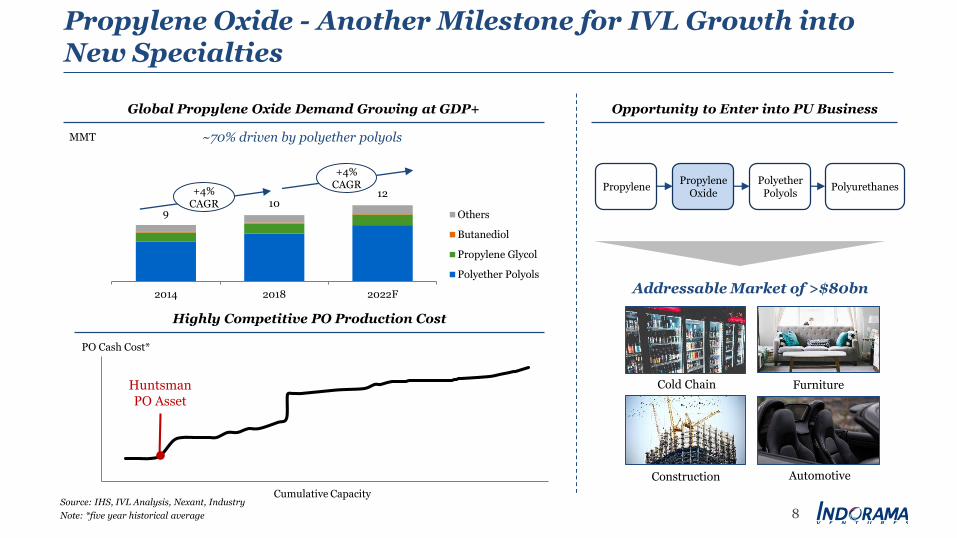

910

12

2014 2018 2022F

Others

Butanediol

Propylene Glycol

Polyether Polyols

8Source: IHS, IVL Analysis, Nexant, Industry

Note: *five year historical average

Propylene Oxide - Another Milestone for IVL Growth into New Specialties

Global Propylene Oxide Demand Growing at GDP+

MMT

Opportunity to Enter into PU Business

~70% driven by polyether polyols

PropylenePropylene

OxidePolyether

PolyolsPolyurethanes+4%

CAGR

+4%CAGR

Highly Competitive PO Production Cost

Cold Chain

Construction Automotive

Furniture

Addressable Market of >$80bn

0

500

1,000

1,500

2,000

0 1000 2000 3000 4000 5000 6000 7000 8000 9000 10000

PO Cash Cost*

Cumulative Capacity

HuntsmanPO Asset

9Source: Nexant, IHS, Platts, IVL Analysis

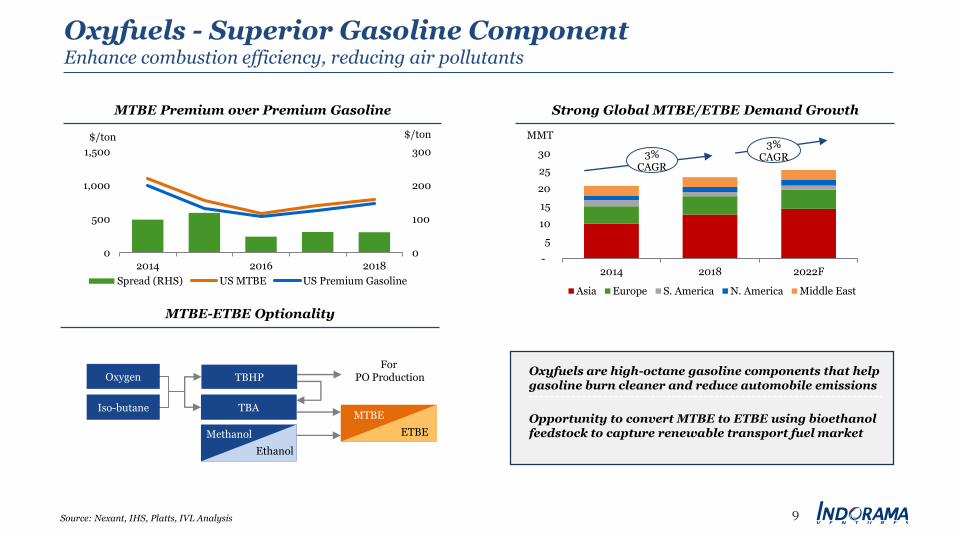

Oxyfuels - Superior Gasoline ComponentEnhance combustion efficiency, reducing air pollutants

MTBE Premium over Premium Gasoline Strong Global MTBE/ETBE Demand Growth

MTBE-ETBE Optionality

0

100

200

300

0

500

1,000

1,500

2014 2016 2018

Spread (RHS) US MTBE US Premium Gasoline

$/ton $/ton

-

5

10

15

20

25

30

2014 2018 2022F

Asia Europe S. America N. America Middle East

3%CAGR

3%CAGR

MMT

TBA

Methanol

Ethanol

MTBE

ETBE

TBHP

Iso-butane

OxygenFor

PO ProductionOxyfuels are high-octane gasoline components that help gasoline burn cleaner and reduce automobile emissions

Opportunity to convert MTBE to ETBE using bioethanolfeedstock to capture renewable transport fuel market

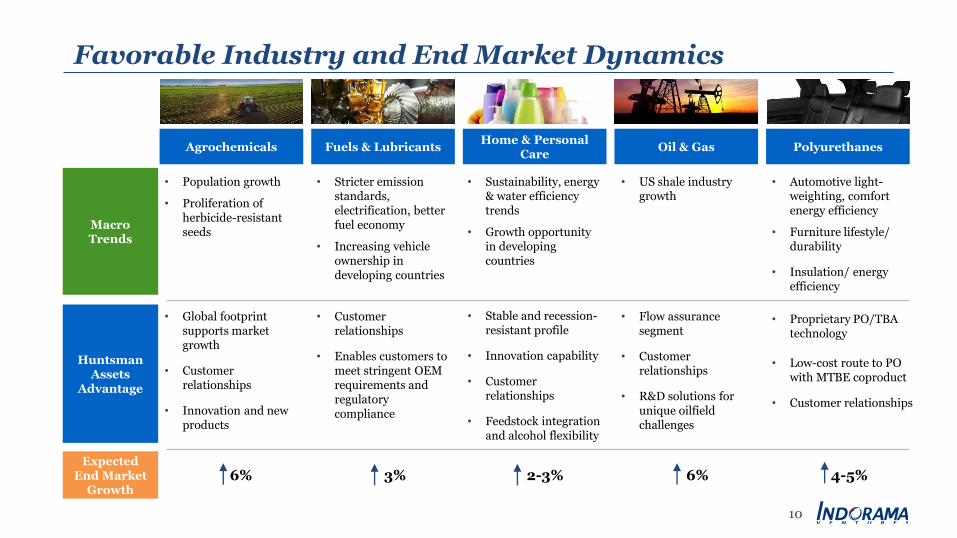

Favorable Industry and End Market Dynamics

• Population growth

• Proliferation of herbicide-resistant seeds

• Global footprint supports market growth

• Customerrelationships

• Innovation and new products

Huntsman Assets

Advantage

Macro Trends

Agrochemicals Fuels & LubricantsHome & Personal

CareOil & Gas Polyurethanes

• Stricter emission standards, electrification, better fuel economy

• Increasing vehicle ownership in developing countries

• Customerrelationships

• Enables customers to meet stringent OEM requirements and regulatory compliance

• Sustainability, energy & water efficiency trends

• Growth opportunity in developing countries

• Stable and recession-resistant profile

• Innovation capability

• Customerrelationships

• Feedstock integration and alcohol flexibility

• US shale industry growth

• Flow assurance segment

• Customerrelationships

• R&D solutions for unique oilfield challenges

• Automotive light-weighting, comfort energy efficiency

• Furniture lifestyle/ durability

• Insulation/ energy efficiency

• Proprietary PO/TBA technology

• Low-cost route to PO with MTBE coproduct

• Customer relationships

Expected End Market

Growth

10

6% 3% 2-3% 6% 4-5%

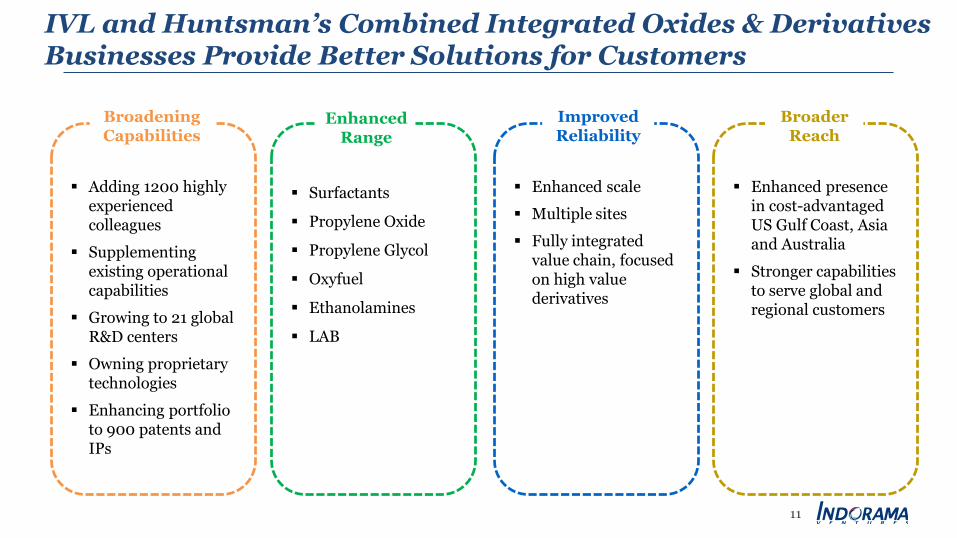

IVL and Huntsman’s Combined Integrated Oxides & Derivatives Businesses Provide Better Solutions for Customers

11

Surfactants

Propylene Oxide

Propylene Glycol

Oxyfuel

Ethanolamines

LAB

Enhanced Range

Enhanced scale

Multiple sites

Fully integrated value chain, focused on high value derivatives

Improved Reliability

Adding 1200 highly experienced colleagues

Supplementing existing operational capabilities

Growing to 21 global R&D centers

Owning proprietary technologies

Enhancing portfolio to 900 patents and IPs

Broadening Capabilities

Enhanced presence in cost-advantaged US Gulf Coast, Asia and Australia

Stronger capabilities to serve global and regional customers

Broader Reach

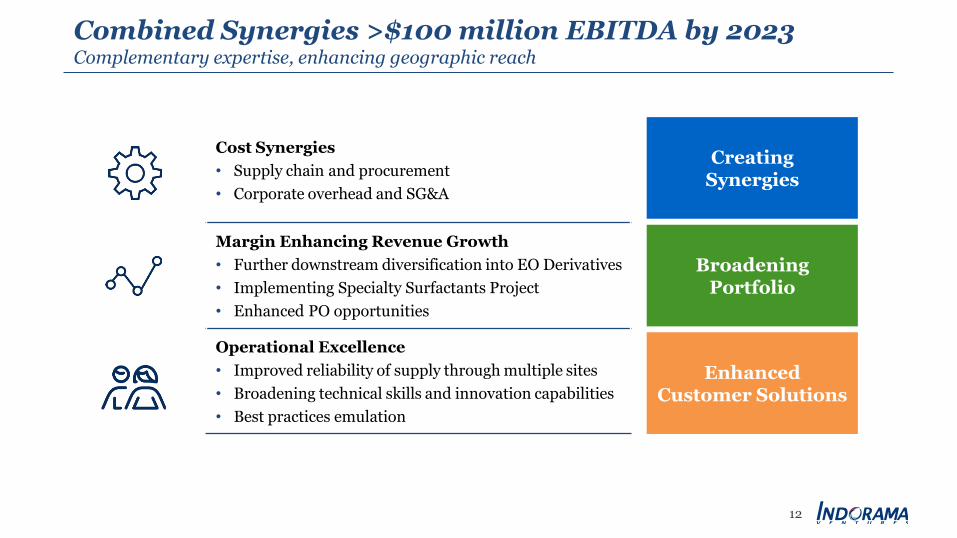

Cost Synergies

• Supply chain and procurement

• Corporate overhead and SG&A

Margin Enhancing Revenue Growth

• Further downstream diversification into EO Derivatives

• Implementing Specialty Surfactants Project

• Enhanced PO opportunities

Operational Excellence

• Improved reliability of supply through multiple sites

• Broadening technical skills and innovation capabilities

• Best practices emulation

Combined Synergies >$100 million EBITDA by 2023Complementary expertise, enhancing geographic reach

12

Creating Synergies

Broadening Portfolio

Enhanced Customer Solutions

13

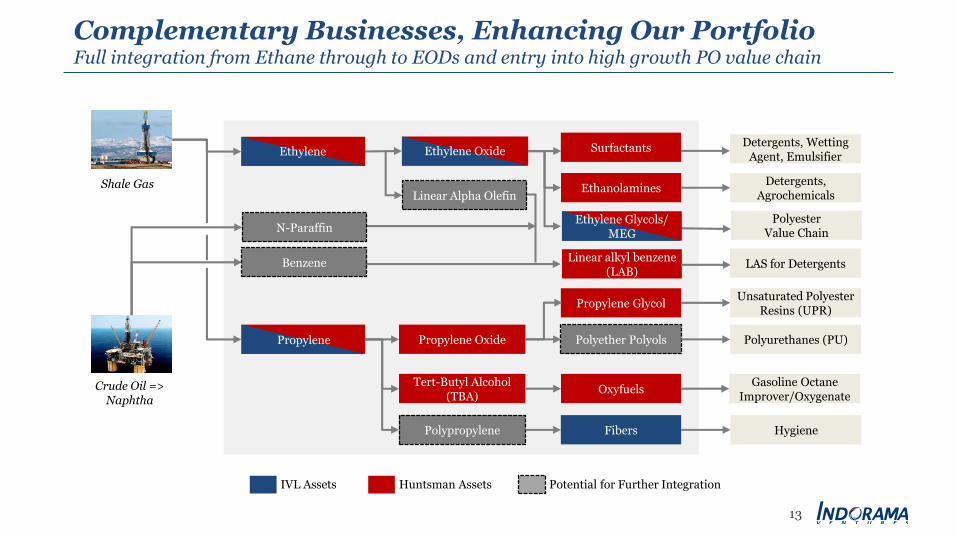

Complementary Businesses, Enhancing Our PortfolioFull integration from Ethane through to EODs and entry into high growth PO value chain

Shale Gas

Crude Oil => Naphtha

IVL Assets

Propylene Oxide Polyether Polyols Polyurethanes (PU)

Ethanolamines

Surfactants

Tert-Butyl Alcohol (TBA)

Oxyfuels

Linear alkyl benzene(LAB)

Gasoline Octane Improver/Oxygenate

Detergents, Wetting Agent, Emulsifier

Detergents, Agrochemicals

Huntsman Assets

Ethylene OxideEthylene

Ethylene Glycols/ MEG

Propylene

Polypropylene Fibers

Potential for Further Integration

Hygiene

Propylene GlycolUnsaturated Polyester

Resins (UPR)

Polyester Value Chain

LAS for Detergents

Linear Alpha Olefin

N-Paraffin

Benzene

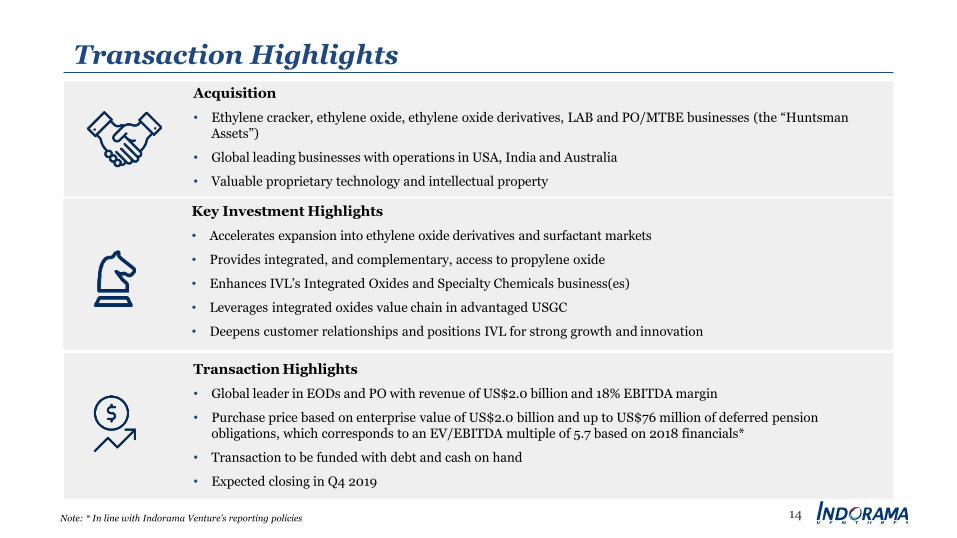

Acquisition

• Ethylene cracker, ethylene oxide, ethylene oxide derivatives, LAB and PO/MTBE businesses (the “Huntsman Assets”)

• Global leading businesses with operations in USA, India and Australia

• Valuable proprietary technology and intellectual property

Key Investment Highlights

• Accelerates expansion into ethylene oxide derivatives and surfactant markets

• Provides integrated, and complementary, access to propylene oxide

• Enhances IVL’s Integrated Oxides and Specialty Chemicals business(es)

• Leverages integrated oxides value chain in advantaged USGC

• Deepens customer relationships and positions IVL for strong growth and innovation

Transaction Highlights

• Global leader in EODs and PO with revenue of US$2.0 billion and 18% EBITDA margin

• Purchase price based on enterprise value of US$2.0 billion and up to US$76 million of deferred pension obligations, which corresponds to an EV/EBITDA multiple of 5.7 based on 2018 financials*

• Transaction to be funded with debt and cash on hand

• Expected closing in Q4 2019

14Note: * In line with Indorama Venture’s reporting policies

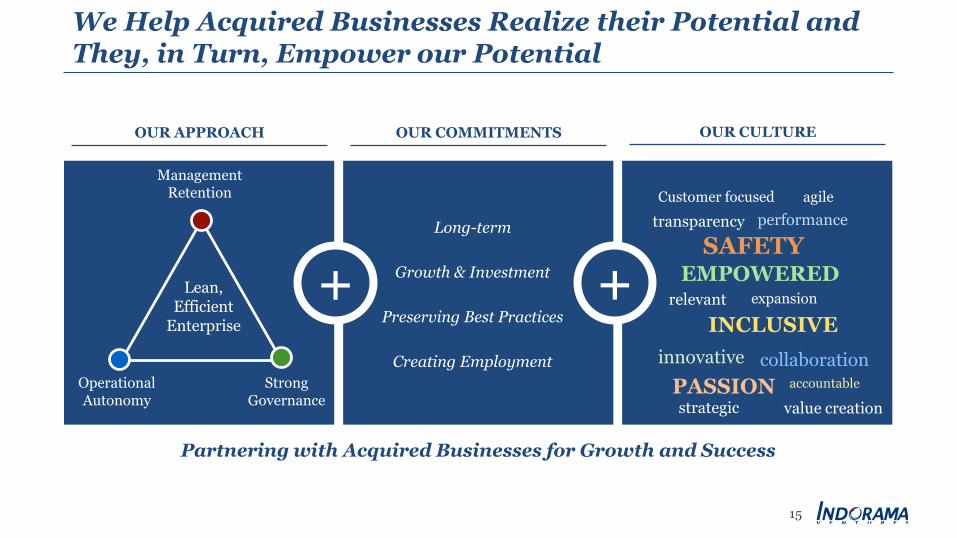

Transaction Highlights

15

OUR APPROACH OUR COMMITMENTS OUR CULTURE

Long-term

Growth & Investment

Preserving Best Practices

Creating Employment

EMPOWERED

INCLUSIVE

strategic

PASSION

transparency

relevant

Customer focused

accountable

SAFETY

value creation

performance

expansion

innovative

agile

collaboration

Lean, Efficient

Enterprise

Management Retention

Strong Governance

Operational Autonomy

+ +

Partnering with Acquired Businesses for Growth and Success

We Help Acquired Businesses Realize their Potential and They, in Turn, Empower our Potential

This presentation contains “forward-looking” statements of Indorama Ventures Public Company Limited (the “Company”)1 that relate to future events, which are, by their nature, subject to significant risks and uncertainties. All statements, other than statements of historical fact contained herein, including, without limitation, those regarding the future financial position and results of operations, strategy, plans, objectives, goals and targets, future developments in the markets where the Company participates or is seeking to participate and anystatements preceded by, followed by or that include the words “target”, “believe”, “expect”, “aim”, “intend”, “will”, “may”, “anticipate”, “would”, “plan”, “could”, “should, “predict”, “project”, “estimate”, “foresee”, “forecast”, “seek” or similar words or expressions areforward-looking statements.

Such forward-looking statements involve known and unknown risks, uncertainties and other important factors beyond the Company’s control that could cause the actual results, performance or achievements of the Company to be materially different from the future results, performance or achievements expressed or implied by such forward-looking statements. These forward-looking statements are based onnumerous assumptions regarding the Company’s present and future business strategies and the environment in which the Company will operate in the future and are not a guarantee of future performance.

Such forward-looking statements speak only as at the date of this presentation, and the Company does not undertake any duty or obligation to supplement, amend, update or revise any such statements. The Company does not make any representation, warranty or prediction that the results anticipated by such forward-looking statements will be achieved.

1Where the context requires, it means the Company, its subsidiaries, joint ventures and associated companies as a group or as members of such group.

Disclaimer