Embed Size (px)

Citation preview

Investor PresentationJune 2010June 2010

1Enterprise ● Energy ● Endurance

Table of contents

1. Company Overview

2. Company Financials

3. Key Highlights

4 Company Highlights4. Company Highlights

2

Section 1:Company Overview

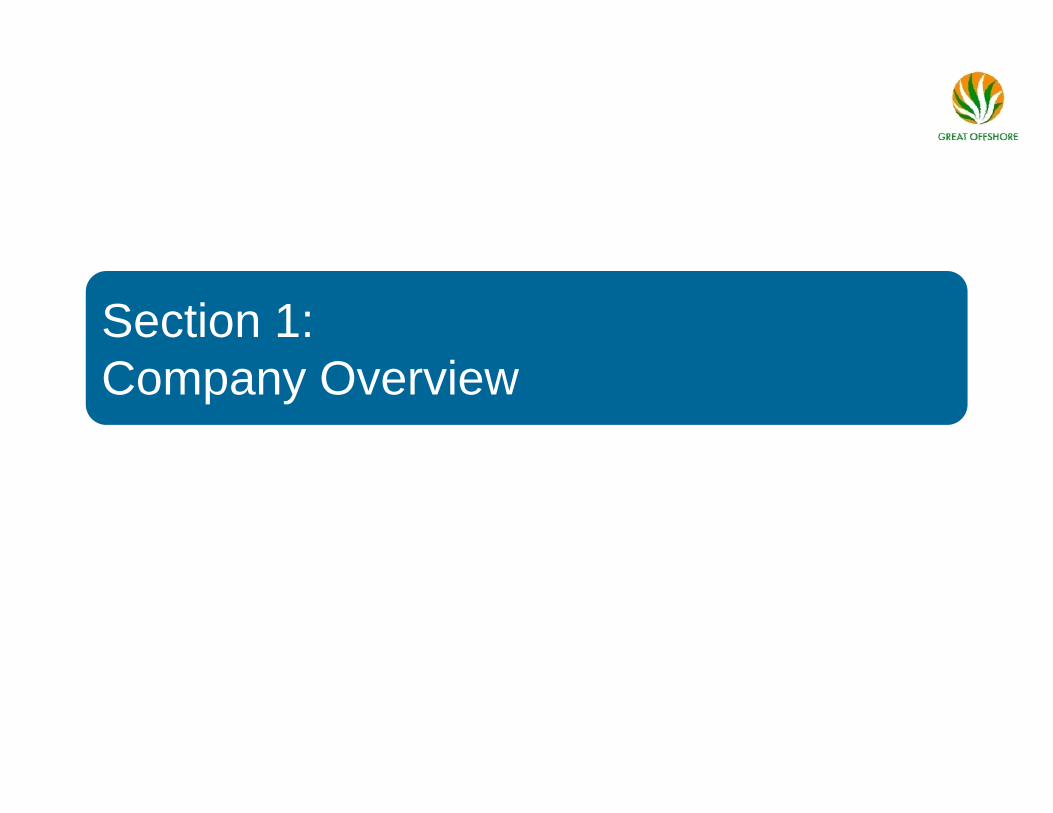

Serving the entire E&P value chainLeading to lower cyclicality in performance

5 yrs 15 yrs 20 yrs

Seismic SamplingExploration

Great Offshore

Exploration Drilling

Production Drilling

Fabrication/

Drilling

is present

across major

portion of the

E&P value

chain therefore

Engineering Fabrication/Construction

Product & technology Assembly

Drilling

chain therefore

there is limited

impact on its

performance

due to oil price

Heavy Lift Subsea ConstructionInstallation

Platform Production & Production & Maintenance & Production p

volatilitysupply Operations Modifications

Heavy Lift Decommissioning

Production

Abandonment

4

E&P value chainRepairs

GOL is an offshore oilfield services provider to the oil and gas E&P sector in India and internationally with a diversified fleet of maritime assets.

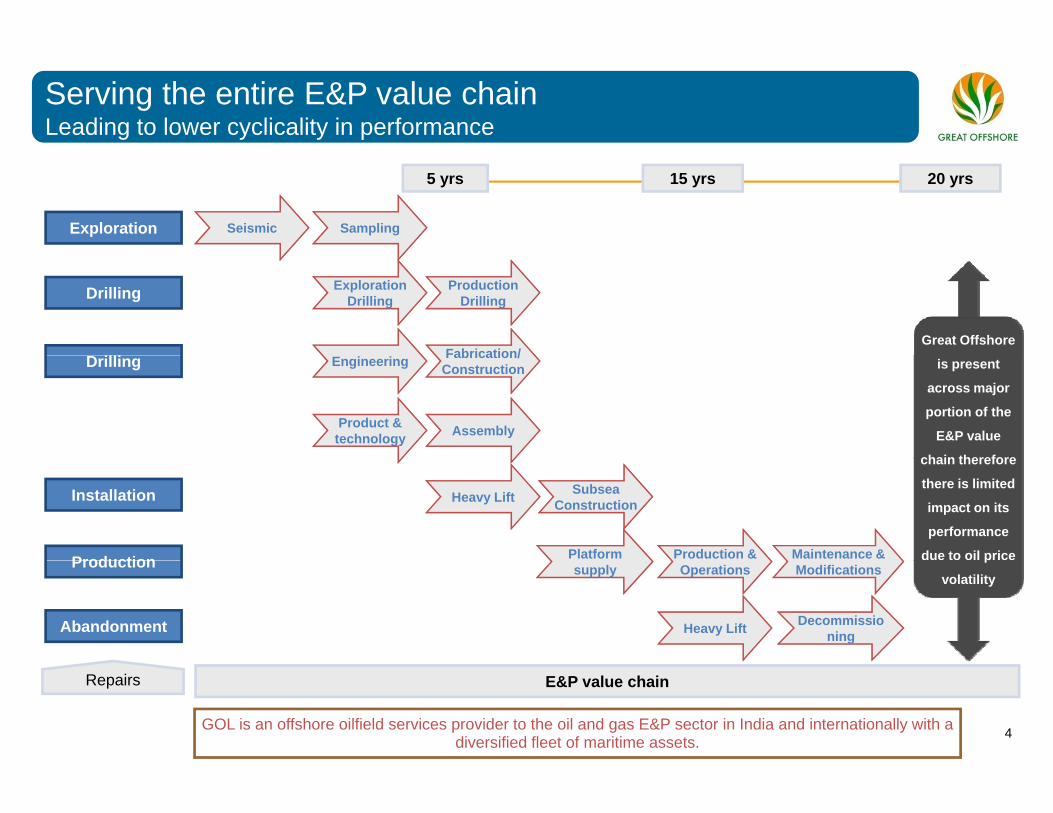

Genesis of Great Offshore Limited (GOL)

• Great Offshore Limited (GOL) was a offshore division of the Great Eastern Shipping (GES), which had been in existence for 20+ years

Started as a business division of the Great Eastern Shipping Co. Ltd. (Pre Oct-06 )1

• Since commissioning its operations in 1983, Great Offshore has serviced major E&P operators in India as well as in the international waters of the North Sea, the Middle East, South Africa and South East Asia

• Through a Scheme of Arrangement, GOL was demerged into a separate company

• December 2006 GOL lists at the stock exchanges• December 2006 - GOL lists at the stock exchanges

2 Emergence of Bharati Shipyard as the single largest shareholder (May-09 – Present Day)

• May 09 – Personal pledge invoked of erstwhile promoter

• 14.89% of the total shareholding transferred to Bharati Shipyard Limited

• Two bidders (Bharati Shipyard and ABG Shipyard) make simultaneous Open Offer to minority shareholders

• Bharati Shipyard emerged as the single largest shareholder in GOL

5

GOL has a tremendous track record of over 25 years of operational experience

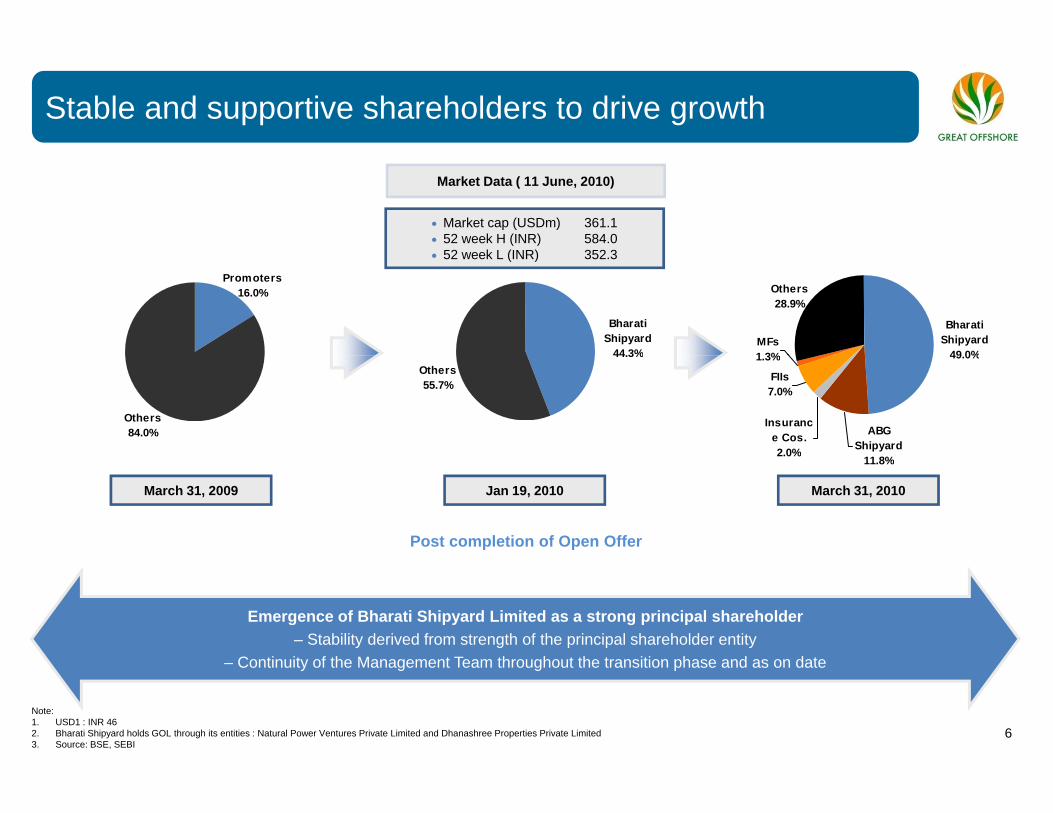

Stable and supportive shareholders to drive growth

• Market cap (USDm) 361.1• 52 week H (INR) 584.0

52 week L (INR) 352 3

Market Data ( 11 June, 2010)

Promoters16.0%

BharatiShipyard

44.3%

• 52 week L (INR) 352.3

MFs1 3%

Others28.9%

Bharati Shipyard

49 0%

Others84.0%

44.3%Others55.7%

FIIs7.0%

1.3%

Insurance Cos.2.0%

49.0%

ABG Shipyard

11 8%

March 31, 2009 Jan 19, 2010

11.8%

March 31, 2010

Post completion of Open Offer

Emergence of Bharati Shipyard Limited as a strong principal shareholder– Stability derived from strength of the principal shareholder entity

– Continuity of the Management Team throughout the transition phase and as on date

6

Note:1. USD1 : INR 462. Bharati Shipyard holds GOL through its entities : Natural Power Ventures Private Limited and Dhanashree Properties Private Limited3. Source: BSE, SEBI

– Continuity of the Management Team throughout the transition phase and as on date

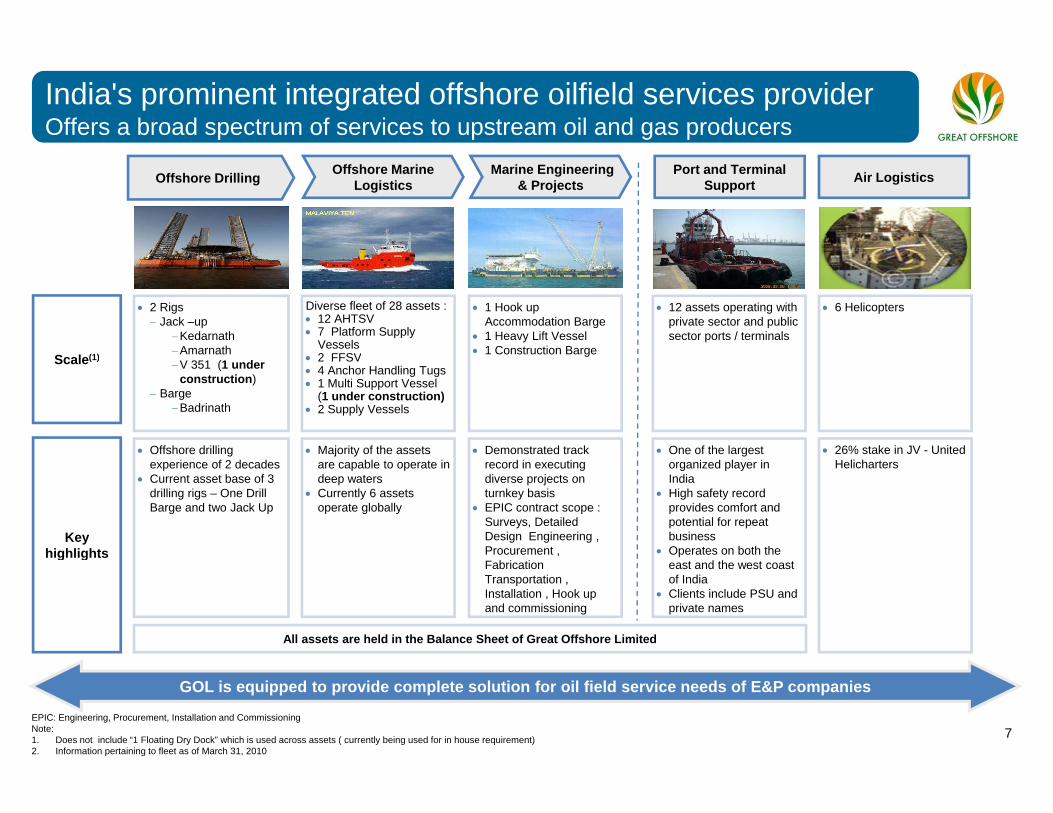

India's prominent integrated offshore oilfield services providerOffers a broad spectrum of services to upstream oil and gas producers

Offshore Drilling Marine Engineering & Projects

Offshore Marine Logistics

Port and Terminal Support Air Logistics

• 2 Rigs− Jack –up

−Kedarnath−Amarnath

Diverse fleet of 28 assets :• 12 AHTSV• 7 Platform Supply

Vessels2 FFSVS l (1)

• 1 Hook up Accommodation Barge

• 1 Heavy Lift Vessel• 1 Construction Barge

• 12 assets operating with private sector and public sector ports / terminals

• 6 Helicopters

−V 351 (1 under construction)

− Barge−Badrinath

• 2 FFSV• 4 Anchor Handling Tugs • 1 Multi Support Vessel

(1 under construction)• 2 Supply Vessels

Scale(1) g

• Offshore drilling • Demonstrated track • One of the largest • Majority of the assets • 26% stake in JV - United experience of 2 decades

• Current asset base of 3 drilling rigs – One Drill Barge and two Jack Up

record in executing diverse projects on turnkey basis

• EPIC contract scope : Surveys, Detailed Design Engineering , Procurement , F b i i

organized player in India

• High safety record provides comfort and potential for repeat business

• Operates on both the d h

Key highlights

are capable to operate in deep waters

• Currently 6 assets operate globally

Helicharters

Fabrication Transportation , Installation , Hook up and commissioning

east and the west coast of India

• Clients include PSU and private names

g g

All assets are held in the Balance Sheet of Great Offshore Limited

7EPIC: Engineering, Procurement, Installation and Commissioning Note:1. Does not include “1 Floating Dry Dock” which is used across assets ( currently being used for in house requirement)2. Information pertaining to fleet as of March 31, 2010

GOL is equipped to provide complete solution for oil field service needs of E&P companies

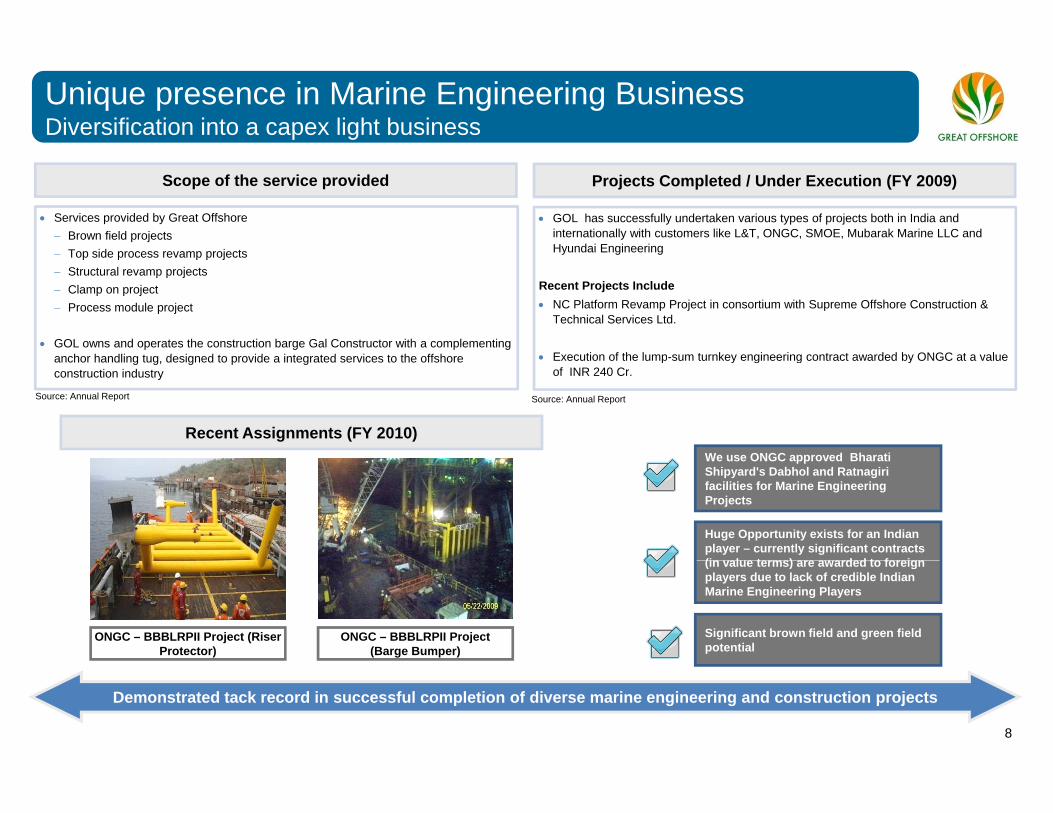

Unique presence in Marine Engineering BusinessDiversification into a capex light business

• Services provided by Great Offshore− Brown field projects

Top side process revamp projects

Scope of the service provided Projects Completed / Under Execution (FY 2009)

• GOL has successfully undertaken various types of projects both in India and internationally with customers like L&T, ONGC, SMOE, Mubarak Marine LLC and Hyundai Engineering− Top side process revamp projects

− Structural revamp projects− Clamp on project− Process module project

• GOL owns and operates the construction barge Gal Constructor with a complementing h h dli t d i d t id i t t d i t th ff h

y g g

Recent Projects Include• NC Platform Revamp Project in consortium with Supreme Offshore Construction &

Technical Services Ltd.

• Execution of the lump sum turnkey engineering contract awarded by ONGC at a valueanchor handling tug, designed to provide a integrated services to the offshore construction industry

Recent Assignments (FY 2010)

• Execution of the lump-sum turnkey engineering contract awarded by ONGC at a value of INR 240 Cr.

Source: Annual Report Source: Annual Report

We use ONGC approved BharatiWe use ONGC approved Bharati Shipyard's Dabhol and Ratnagiri facilities for Marine Engineering Projects

Huge Opportunity exists for an Indian player – currently significant contracts (in value terms) are awarded to foreign

ONGC – BBBLRPII Project (Riser Protector)

ONGC – BBBLRPII Project (Barge Bumper)

(in value terms) are awarded to foreign players due to lack of credible Indian Marine Engineering Players

Significant brown field and green field potential

8

Demonstrated tack record in successful completion of diverse marine engineering and construction projects

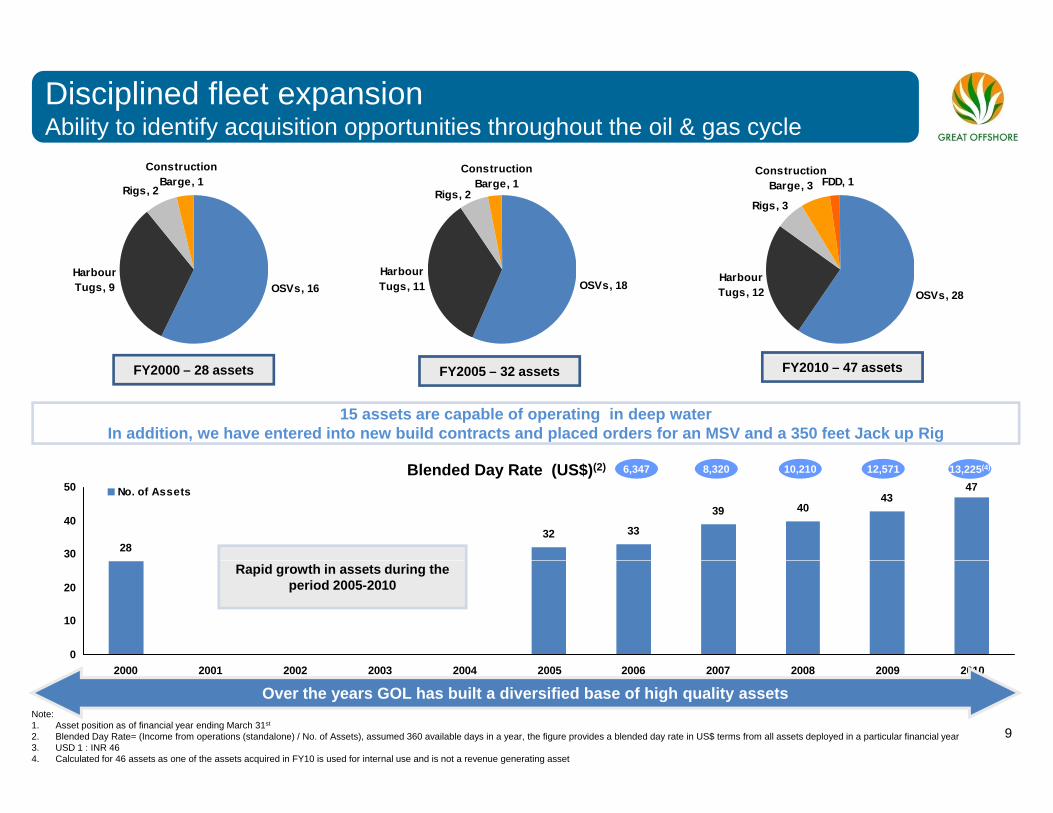

Disciplined fleet expansion Ability to identify acquisition opportunities throughout the oil & gas cycle

Rigs, 2

ConstructionBarge, 1

ConstructionBarge, 1

Rigs, 2

ConstructionBarge, 3 FDD, 1

Rigs, 3

OSVs, 16HarbourTugs, 9 OSVs, 18

HarbourTugs, 11

OSVs, 28HarbourTugs, 12

FY2000 – 28 assets FY2005 – 32 assets FY2010 – 47 assets

15 assets are capable of operating in deep waterIn addition, we have entered into new build contracts and placed orders for an MSV and a 350 feet Jack up Rig

2832 33

39 4043

47

30

40

50 No. of Assets

Blended Day Rate (US$)(2) 12,57110,2108,3206,347 13,225(4)

0

10

20Rapid growth in assets during the

period 2005-2010

9

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Over the years GOL has built a diversified base of high quality assetsNote:1. Asset position as of financial year ending March 31st

2. Blended Day Rate= (Income from operations (standalone) / No. of Assets), assumed 360 available days in a year, the figure provides a blended day rate in US$ terms from all assets deployed in a particular financial year3. USD 1 : INR 464. Calculated for 46 assets as one of the assets acquired in FY10 is used for internal use and is not a revenue generating asset

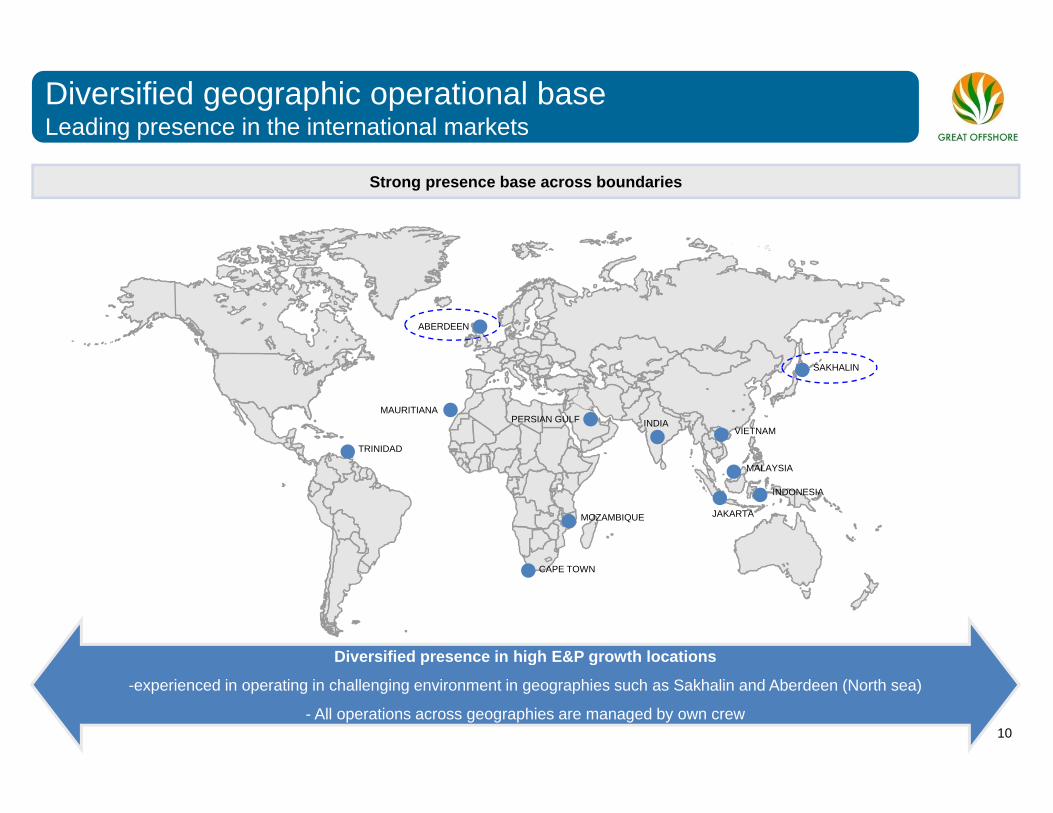

Diversified geographic operational baseLeading presence in the international markets

Strong presence base across boundaries

ABERDEEN

VIETNAMINDIAPERSIAN GULF

TRINIDAD

MAURITIANA

SAKHALIN

MALAYSIA

JAKARTAMOZAMBIQUE

INDONESIA

Diversified presence in high E&P growth locations

CAPE TOWN

10

p g g

-experienced in operating in challenging environment in geographies such as Sakhalin and Aberdeen (North sea)

- All operations across geographies are managed by own crew

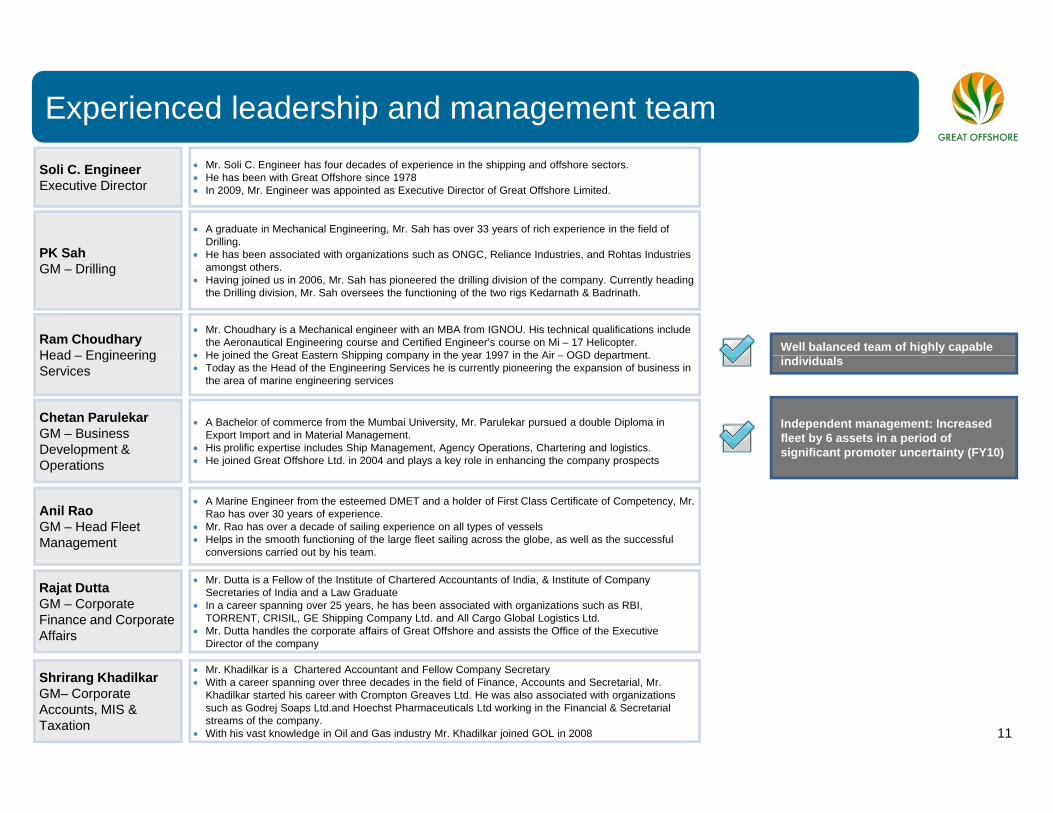

Experienced leadership and management team

PK Sah

• A graduate in Mechanical Engineering, Mr. Sah has over 33 years of rich experience in the field of Drilling. He has been associated with organizations such as ONGC Reliance Industries and Rohtas Industries

Soli C. Engineer Executive Director

• Mr. Soli C. Engineer has four decades of experience in the shipping and offshore sectors. • He has been with Great Offshore since 1978• In 2009, Mr. Engineer was appointed as Executive Director of Great Offshore Limited.

PK SahGM – Drilling

• He has been associated with organizations such as ONGC, Reliance Industries, and Rohtas Industries amongst others.

• Having joined us in 2006, Mr. Sah has pioneered the drilling division of the company. Currently heading the Drilling division, Mr. Sah oversees the functioning of the two rigs Kedarnath & Badrinath.

Ram Choudhary Head Engineering

• Mr. Choudhary is a Mechanical engineer with an MBA from IGNOU. His technical qualifications include the Aeronautical Engineering course and Certified Engineer’s course on Mi – 17 Helicopter.

• He joined the Great Eastern Shipping company in the year 1997 in the Air – OGD departmentWell balanced team of highly capable Head – Engineering

Services • He joined the Great Eastern Shipping company in the year 1997 in the Air – OGD department. • Today as the Head of the Engineering Services he is currently pioneering the expansion of business in

the area of marine engineering services

Chetan Parulekar GM – Business Development &

• A Bachelor of commerce from the Mumbai University, Mr. Parulekar pursued a double Diploma in Export Import and in Material Management.

• His prolific expertise includes Ship Management, Agency Operations, Chartering and logistics. H j i d G t Off h Ltd i 2004 d l k l i h i th t

individuals

Independent management: Increased fleet by 6 assets in a period of significant promoter uncertainty (FY10)

Operations • He joined Great Offshore Ltd. in 2004 and plays a key role in enhancing the company prospects

Anil Rao GM – Head Fleet Management

• A Marine Engineer from the esteemed DMET and a holder of First Class Certificate of Competency, Mr. Rao has over 30 years of experience.

• Mr. Rao has over a decade of sailing experience on all types of vessels• Helps in the smooth functioning of the large fleet sailing across the globe, as well as the successful

conversions carried out by his team.

g p y ( )

Rajat Dutta GM – Corporate Finance and Corporate Affairs

• Mr. Dutta is a Fellow of the Institute of Chartered Accountants of India, & Institute of Company Secretaries of India and a Law Graduate

• In a career spanning over 25 years, he has been associated with organizations such as RBI, TORRENT, CRISIL, GE Shipping Company Ltd. and All Cargo Global Logistics Ltd.

• Mr. Dutta handles the corporate affairs of Great Offshore and assists the Office of the Executive Director of the company

11

Shrirang KhadilkarGM– Corporate Accounts, MIS & Taxation

• Mr. Khadilkar is a Chartered Accountant and Fellow Company Secretary• With a career spanning over three decades in the field of Finance, Accounts and Secretarial, Mr.

Khadilkar started his career with Crompton Greaves Ltd. He was also associated with organizations such as Godrej Soaps Ltd.and Hoechst Pharmaceuticals Ltd working in the Financial & Secretarial streams of the company.

• With his vast knowledge in Oil and Gas industry Mr. Khadilkar joined GOL in 2008

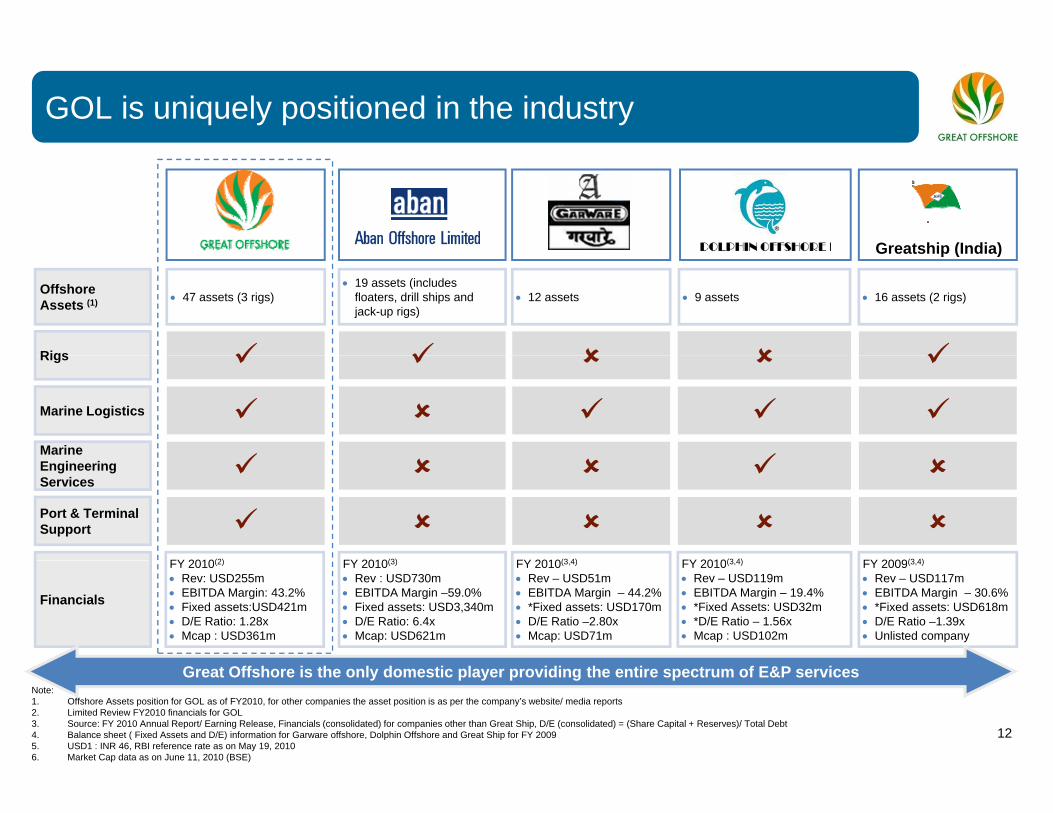

GOL is uniquely positioned in the industry

Great Offshore Great Offshore Great Offshore Great Offshore Great Offshore

Greatship (India)Greatship (India)

Offshore Assets (1) • 47 assets (3 rigs)

• 19 assets (includes floaters, drill ships and jack-up rigs)

• 12 assets • 16 assets (2 rigs)

Rigs

• 9 assets

Rigs

Marine

Marine Logistics

Engineering Services

Port & Terminal Support

FY 2010(2) FY 2010(3) FY 2010(3 4) FY 2010(3 4) FY 2009(3 4)

Financials

FY 2010(2)

• Rev: USD255m• EBITDA Margin: 43.2%• Fixed assets:USD421m• D/E Ratio: 1.28x• Mcap : USD361m

FY 2010(3)

• Rev : USD730m• EBITDA Margin –59.0%• Fixed assets: USD3,340m• D/E Ratio: 6.4x• Mcap: USD621m

FY 2010(3,4)

• Rev – USD51m• EBITDA Margin – 44.2%• *Fixed assets: USD170m• D/E Ratio –2.80x• Mcap: USD71m

FY 2010(3,4)

• Rev – USD119m• EBITDA Margin – 19.4%• *Fixed Assets: USD32m• *D/E Ratio – 1.56x• Mcap : USD102m

FY 2009(3,4)

• Rev – USD117m• EBITDA Margin – 30.6%• *Fixed assets: USD618m• D/E Ratio –1.39x• Unlisted company

12

Note:1. Offshore Assets position for GOL as of FY2010, for other companies the asset position is as per the company’s website/ media reports2. Limited Review FY2010 financials for GOL3. Source: FY 2010 Annual Report/ Earning Release, Financials (consolidated) for companies other than Great Ship, D/E (consolidated) = (Share Capital + Reserves)/ Total Debt4. Balance sheet ( Fixed Assets and D/E) information for Garware offshore, Dolphin Offshore and Great Ship for FY 20095. USD1 : INR 46, RBI reference rate as on May 19, 20106. Market Cap data as on June 11, 2010 (BSE)

Great Offshore is the only domestic player providing the entire spectrum of E&P services

Section 2:Company Financials

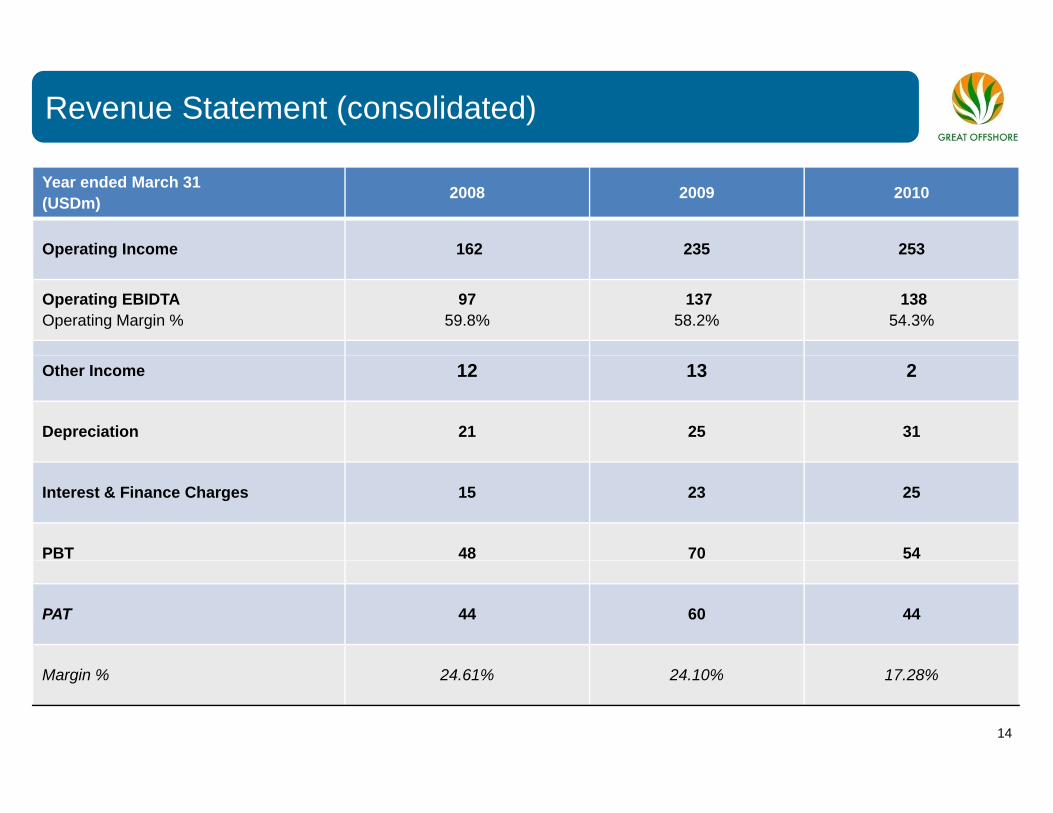

Revenue Statement (consolidated)

Year ended March 31(USDm) 2008 2009 2010

Operating Income 162 235 253Operating Income 162 235 253

Operating EBIDTAOperating Margin %

97 59.8%

137 58.2%

138 54.3%

Other Income 12 13 2

Depreciation 21 25 31

Interest & Finance Charges 15 23 25

PBT 48 70 54

PAT 44 60 44

14

Margin % 24.61% 24.10% 17.28%

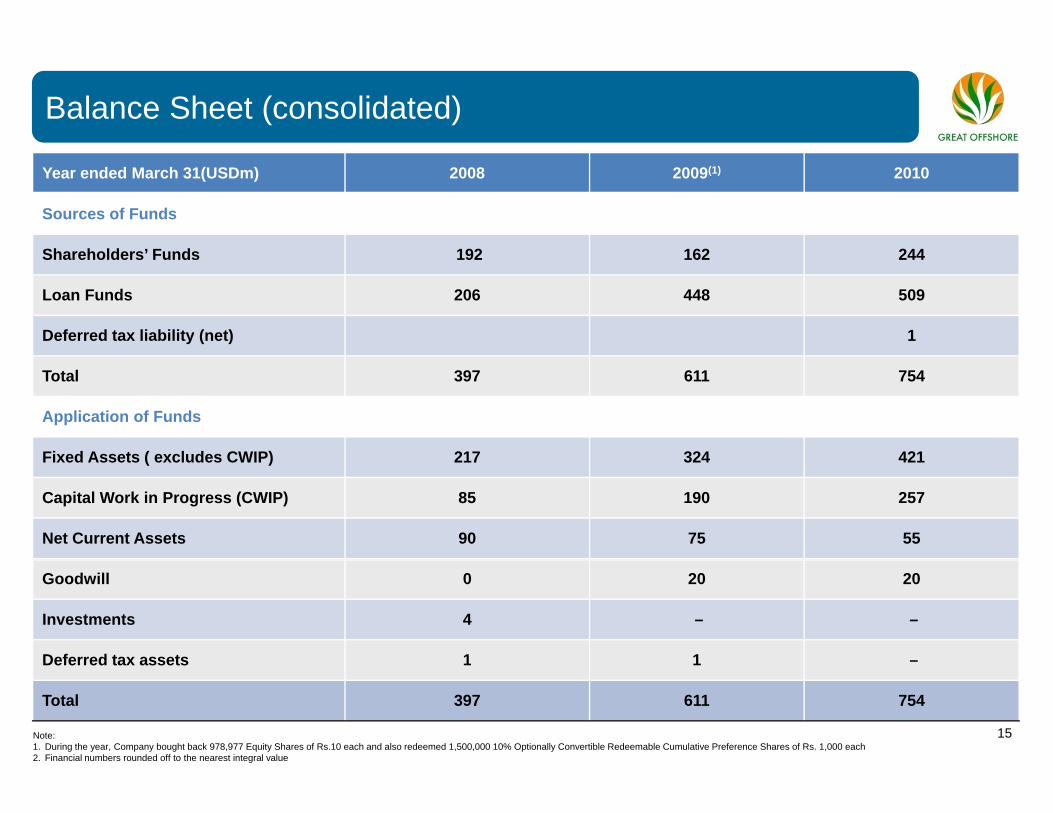

Balance Sheet (consolidated)

Year ended March 31(USDm) 2008 2009(1) 2010

Sources of Funds

Shareholders’ Funds 192 162 244Shareholders’ Funds 192 162 244

Loan Funds 206 448 509

Deferred tax liability (net) 1

Total 397 611 754

Application of Funds

Fixed Assets ( excludes CWIP) 217 324 421Fixed Assets ( excludes CWIP) 217 324 421

Capital Work in Progress (CWIP) 85 190 257

Net Current Assets 90 75 55

Goodwill 0 20 20

Investments 4 – –

Deferred tax assets 1 1 –

15

Deferred tax assets 1 1

Total 397 611 754

Note:1. During the year, Company bought back 978,977 Equity Shares of Rs.10 each and also redeemed 1,500,000 10% Optionally Convertible Redeemable Cumulative Preference Shares of Rs. 1,000 each2. Financial numbers rounded off to the nearest integral value

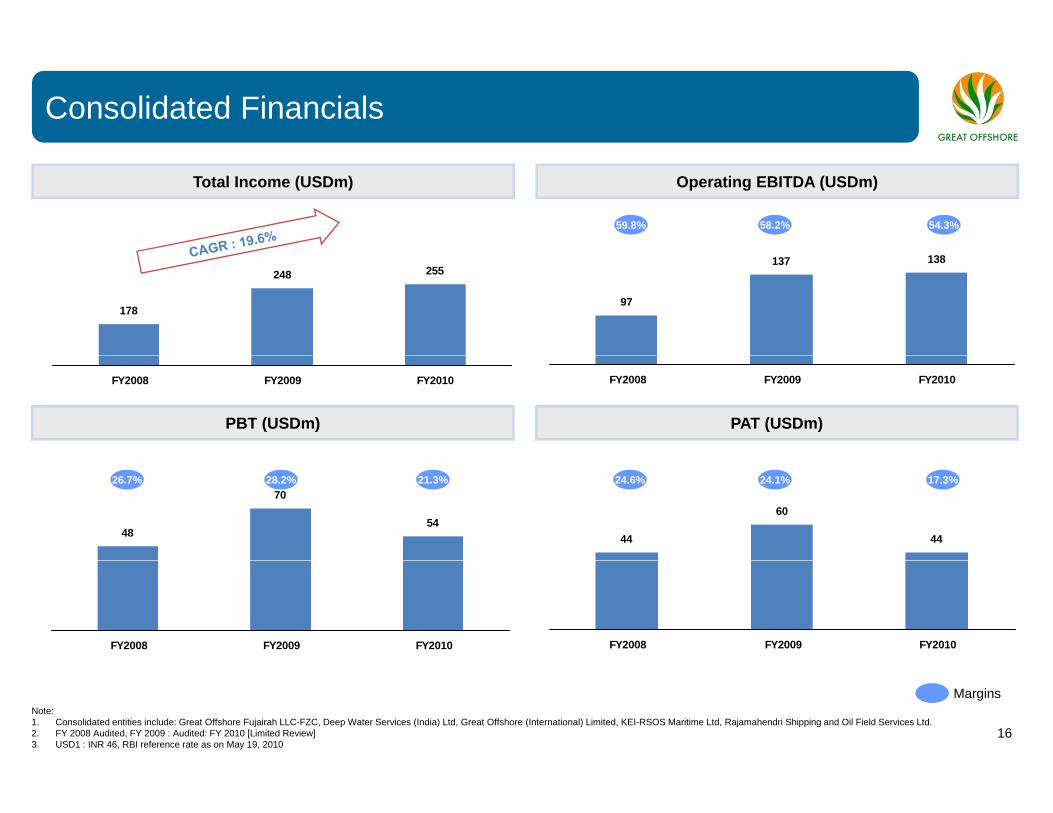

Consolidated Financials

59.8% 58.2% 54.3%

Total Income (USDm) Operating EBITDA (USDm)

178

248 255

97

137 138

FY2008 FY2009 FY2010 FY2008 FY2009 FY2010

PBT (USDm) PAT (USDm)

48

70

5444

60

44

26.7% 28.2% 21.3% 24.6% 24.1% 17.3%

FY2008 FY2009 FY2010 FY2008 FY2009 FY2010

16

MarginsNote:1. Consolidated entities include: Great Offshore Fujairah LLC-FZC, Deep Water Services (India) Ltd, Great Offshore (International) Limited, KEI-RSOS Maritime Ltd, Rajamahendri Shipping and Oil Field Services Ltd.2. FY 2008 Audited, FY 2009 : Audited: FY 2010 [Limited Review]3. USD1 : INR 46, RBI reference rate as on May 19, 2010

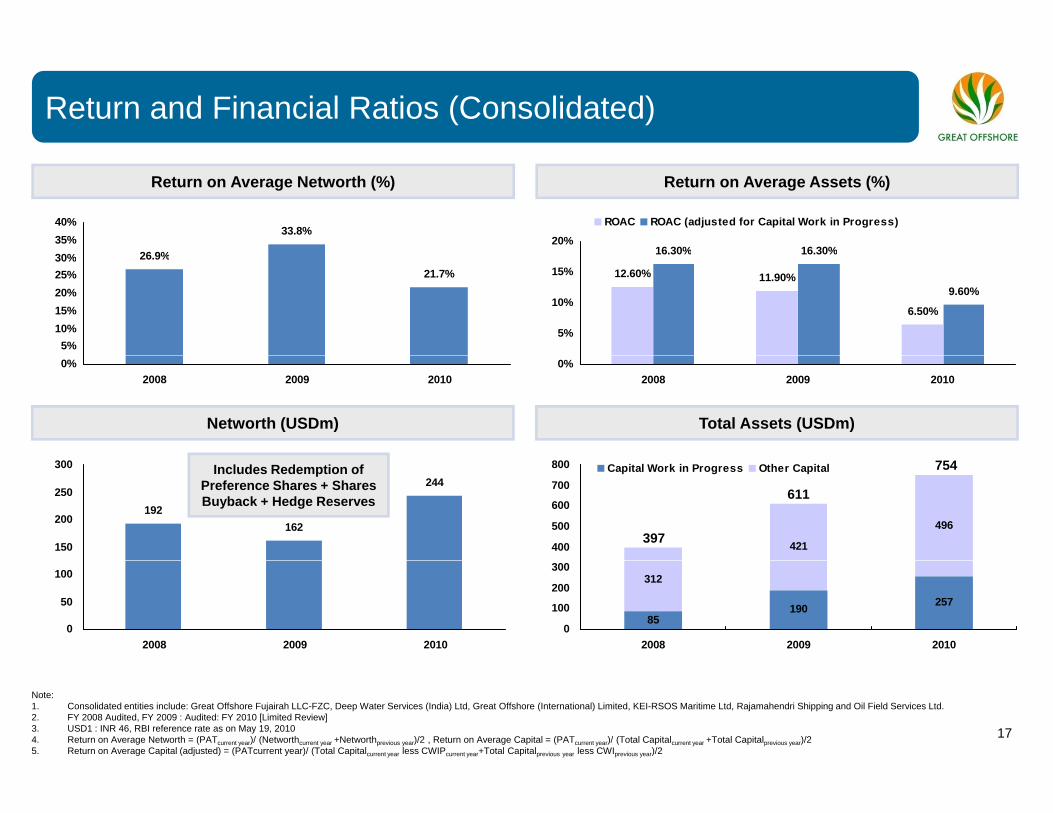

Return and Financial Ratios (Consolidated)

26 9%

33.8%35%40%

16.30% 16.30%20%

ROAC ROAC (adjusted for Capital Work in Progress)

Return on Average Networth (%) Return on Average Assets (%)

26.9%21.7%

5%10%15%20%25%30%

12.60% 11.90%

6.50%

16.30% 16.30%

9.60%

5%

10%

15%

0%2008 2009 2010

0%2008 2009 2010

Networth (USDm) Total Assets (USDm)

192162

244

150

200

250

300

421

496

400

500

600

700

800 Capital Work in Progress Other CapitalIncludes Redemption of Preference Shares + Shares Buyback + Hedge Reserves

397

611

754

0

50

100

2008 2009 2010

85190 257

312

0

100

200

300

2008 2009 2010

17

Note:1. Consolidated entities include: Great Offshore Fujairah LLC-FZC, Deep Water Services (India) Ltd, Great Offshore (International) Limited, KEI-RSOS Maritime Ltd, Rajamahendri Shipping and Oil Field Services Ltd.2. FY 2008 Audited, FY 2009 : Audited: FY 2010 [Limited Review]3. USD1 : INR 46, RBI reference rate as on May 19, 20104. Return on Average Networth = (PATcurrent year)/ (Networthcurrent year +Networthprevious year)/2 , Return on Average Capital = (PATcurrent year)/ (Total Capitalcurrent year +Total Capitalprevious year)/2 5. Return on Average Capital (adjusted) = (PATcurrent year)/ (Total Capitalcurrent year less CWIPcurrent year+Total Capitalprevious year less CWIprevious year)/2

Section 3:Industry Highlights

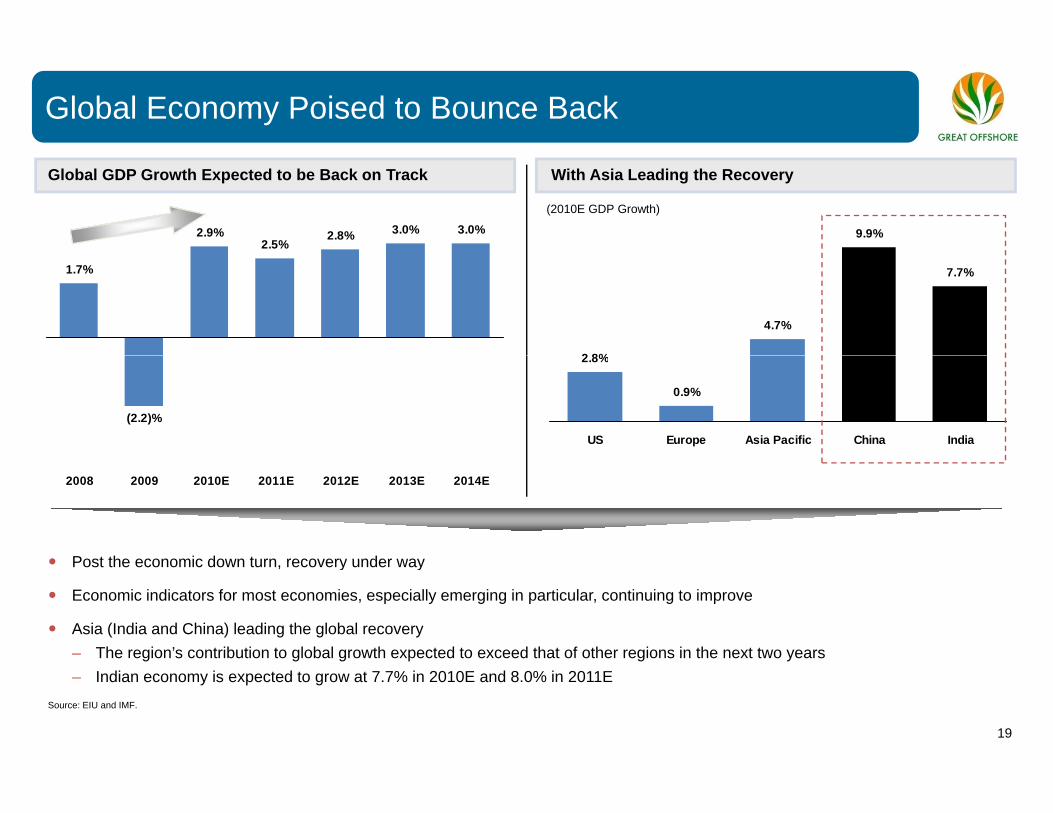

Global Economy Poised to Bounce Back

Global GDP Growth Expected to be Back on Track With Asia Leading the Recovery

2.9%2.5%

2.8% 3.0% 3.0% 9.9%

(2010E GDP Growth)

1.7%

2 8%

4.7%

7.7%

(2.2)%

2.8%

0.9%

US Europe Asia Pacific China India

Post the economic down turn recovery under way

2008 2009 2010E 2011E 2012E 2013E 2014E

Post the economic down turn, recovery under way

Economic indicators for most economies, especially emerging in particular, continuing to improve

Asia (India and China) leading the global recovery– The region’s contribution to global growth expected to exceed that of other regions in the next two years

19

Source: EIU and IMF.

– Indian economy is expected to grow at 7.7% in 2010E and 8.0% in 2011E

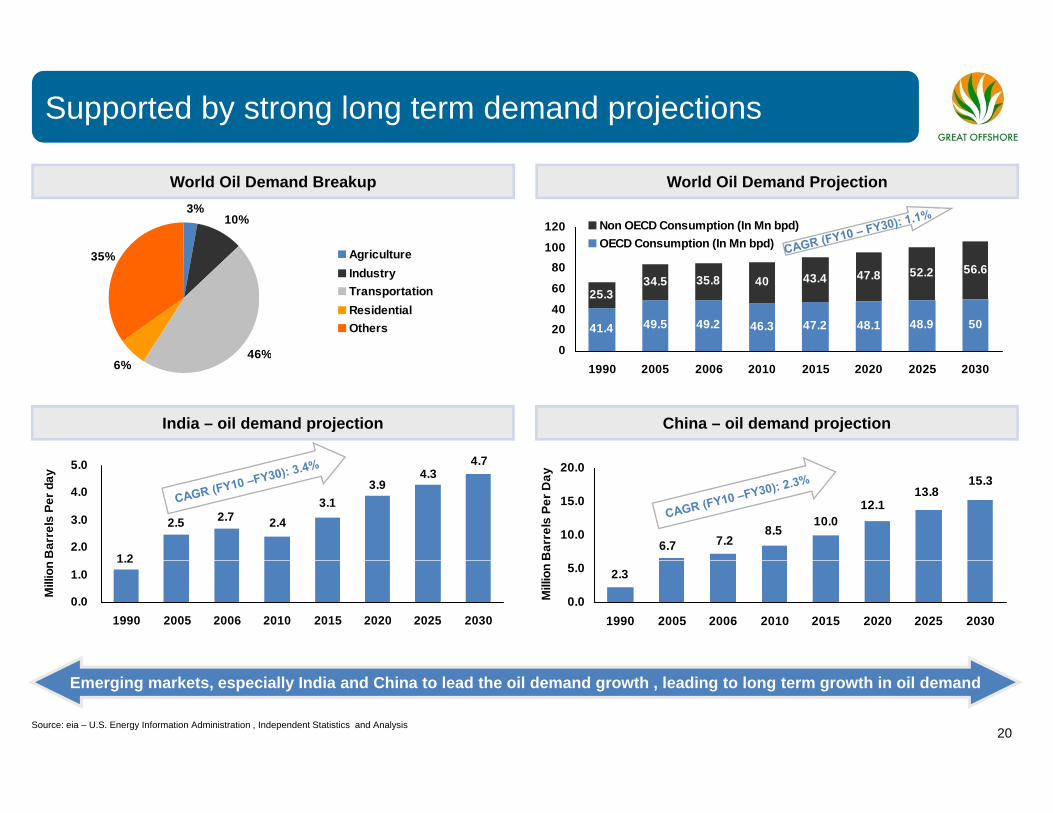

Supported by strong long term demand projections

100

120 Non OECD Consumption (In Mn bpd)OECD Consumption (In Mn bpd)

3%10%

35% Agriculture

World Oil Demand Breakup World Oil Demand Projection

41.4 49.5 49.2 46.3 47.2 48.1 48.9 50

25.334.5 35.8 40 43.4 47.8 52.2 56.6

0

2040

60

80

46%

35% AgricultureIndustryTransportationResidentialOthers

1990 2005 2006 2010 2015 2020 2025 2030

4 7

46%6%

Transportation accounts for a sizeable chunk of the demandIndia – oil demand projection China – oil demand projection

4.74.3

3.93.1

2.42.72.5

1 22.0

3.0

4.0

5.0

Bar

rels

Per

day 15.3

13.812.1

10.08.5

7.26.710.0

15.0

20.0

Bar

rels

Per

Day

1.2

0.0

1.0

1990 2005 2006 2010 2015 2020 2025 2030

Mill

ion

2.3

0.0

5.0

1990 2005 2006 2010 2015 2020 2025 2030

Mill

ion

20

Emerging markets, especially India and China to lead the oil demand growth , leading to long term growth in oil demand

Source: eia – U.S. Energy Information Administration , Independent Statistics and Analysis

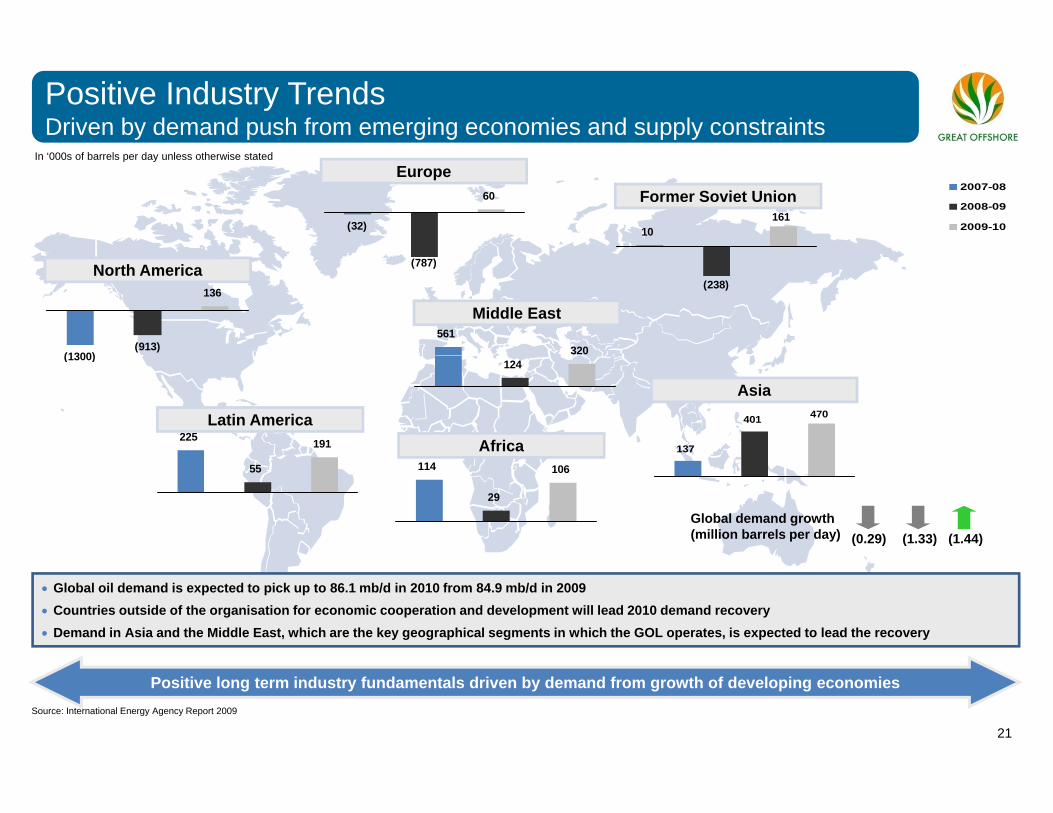

Positive Industry TrendsDriven by demand push from emerging economies and supply constraints

(32)

60

Europe

10161

Former Soviet Union2007-08

2008-09

2009-10

In ‘000s of barrels per day unless otherwise stated

(1300)(913)

136

North America (787)

(238)

561320

Middle East

(1300)

225 191

Latin AmericaAfrica

124

137

401 470

Asia

55 114

29

106

Global demand growth(million barrels per day) (0.29) (1.33) (1.44)

• Global oil demand is expected to pick up to 86.1 mb/d in 2010 from 84.9 mb/d in 2009• Countries outside of the organisation for economic cooperation and development will lead 2010 demand recovery• Demand in Asia and the Middle East, which are the key geographical segments in which the GOL operates, is expected to lead the recovery

21

Source: International Energy Agency Report 2009

Positive long term industry fundamentals driven by demand from growth of developing economies

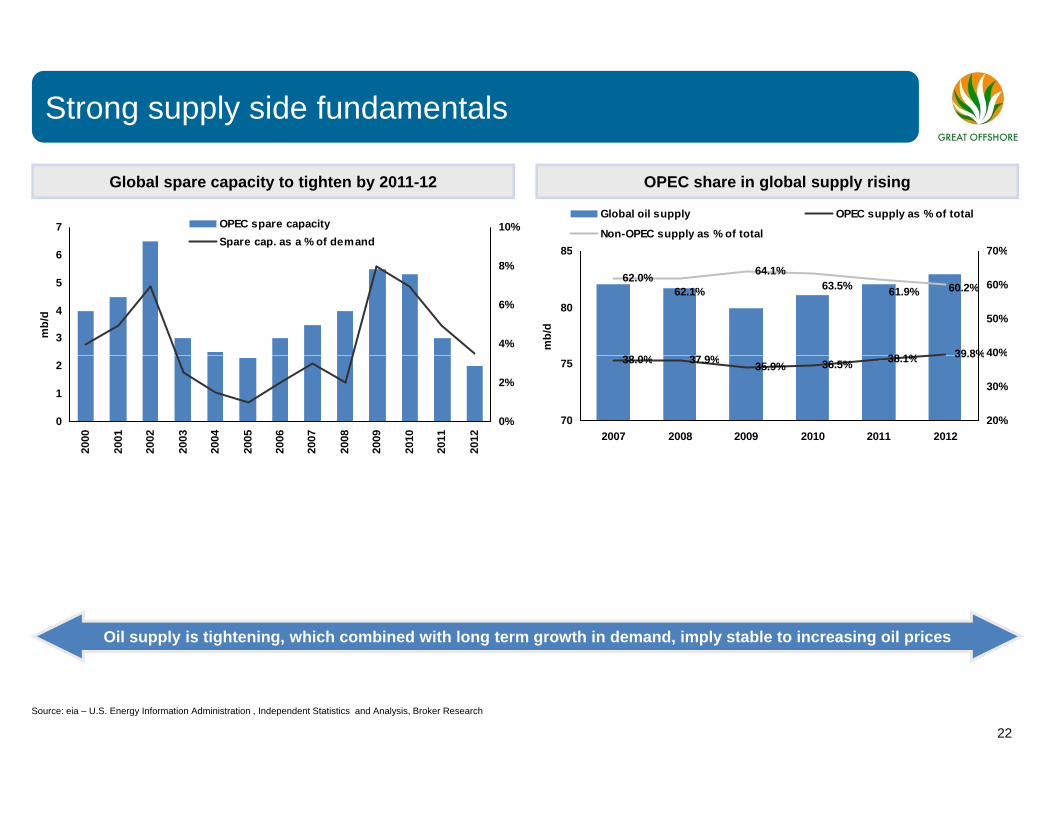

Strong supply side fundamentals

6

7 10%OPEC spare capacitySpare cap. as a % of demand

85 70%

Global oil supply OPEC supply as % of total

Non-OPEC supply as % of total

Global spare capacity to tighten by 2011-12 OPEC share in global supply rising

3

4

5

6

mb/

d

4%

6%

8%

38 0% 37 9% 38 1% 39 8%

62.0% 64.1%

62.1% 63.5% 61.9% 60.2%

80

85

mb/

d

40%

50%

60%

70%

0

1

2

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

0%

2%

38.0% 37.9% 35.9% 36.5% 38.1% 39.8%

70

75

2007 2008 2009 2010 2011 201220%

30%

40%

Oil supply is tightening, which combined with long term growth in demand, imply stable to increasing oil prices

22

Source: eia – U.S. Energy Information Administration , Independent Statistics and Analysis, Broker Research

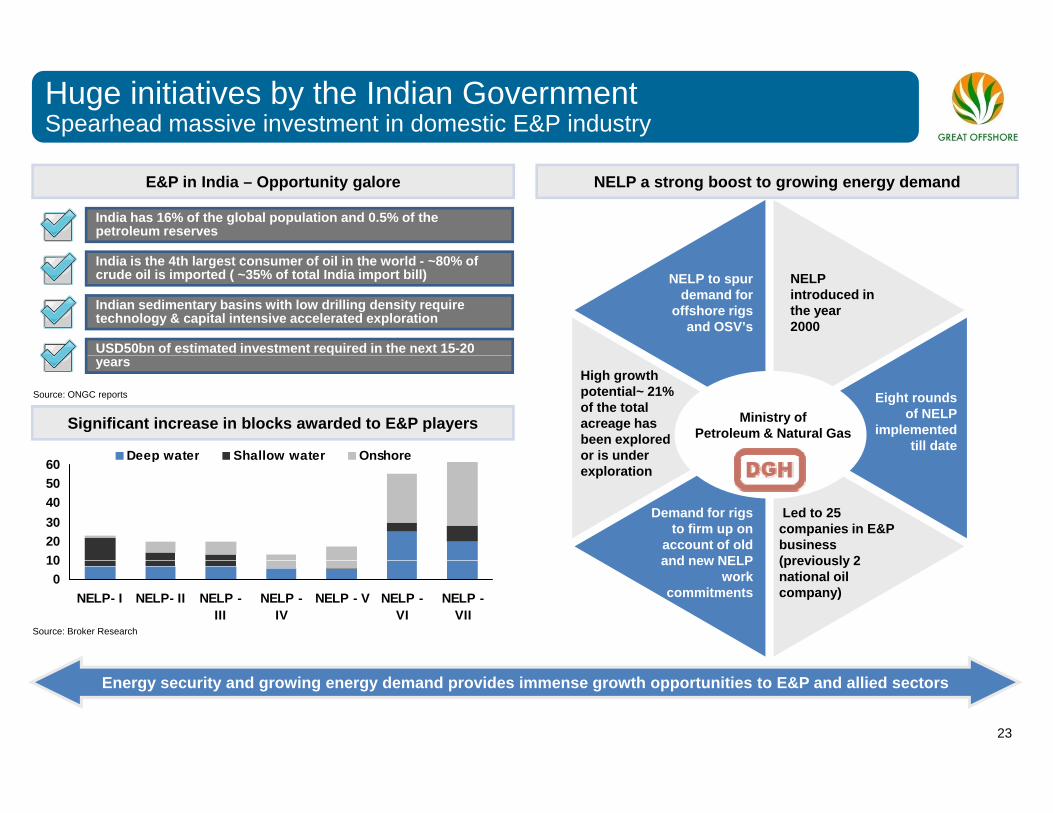

Huge initiatives by the Indian GovernmentSpearhead massive investment in domestic E&P industry

India has 16% of the global population and 0.5% of the petroleum reserves

E&P in India – Opportunity galore NELP a strong boost to growing energy demand

NELP introduced in the year2000

NELP to spur demand for

offshore rigs and OSV’s

India is the 4th largest consumer of oil in the world - ~80% of crude oil is imported ( ~35% of total India import bill)

Indian sedimentary basins with low drilling density require technology & capital intensive accelerated exploration

USD50bn of estimated investment required in the next 15-20

Eight rounds of NELP

implemented till date

High growth potential~ 21% of the total acreage has been explored or is under

Ministry of Petroleum & Natural Gas

Source: ONGC reports

Deep water Shallow water Onshore

years

Significant increase in blocks awarded to E&P players

Led to 25 companies in E&P business (previously 2

Demand for rigsto firm up on

account of old and new NELP

or is under exploration

102030405060

Deep water Shallow water Onshore

(previously 2 national oil company)

and new NELP work

commitments

Source: Broker Research

010

NELP- I NELP- II NELP -III

NELP -IV

NELP - V NELP -VI

NELP -VII

23

Energy security and growing energy demand provides immense growth opportunities to E&P and allied sectors

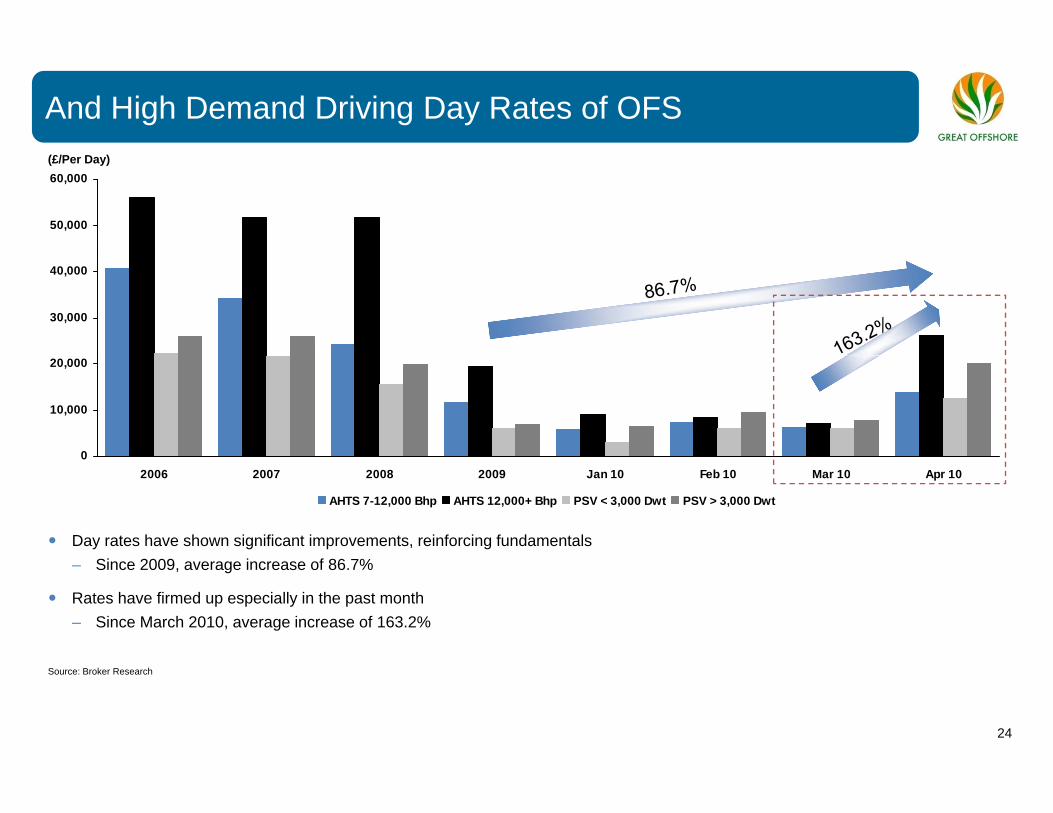

And High Demand Driving Day Rates of OFS (£/Per Day)

50,000

60,000

30,000

40,000

0

10,000

20,000

02006 2007 2008 2009 Jan 10 Feb 10 Mar 10 Apr 10

AHTS 7-12,000 Bhp AHTS 12,000+ Bhp PSV < 3,000 Dwt PSV > 3,000 Dwt

Day rates have shown significant improvements, reinforcing fundamentalsSi 2009 i f 86 7%– Since 2009, average increase of 86.7%

Rates have firmed up especially in the past month– Since March 2010, average increase of 163.2%

24

Source: Broker Research

Section 4:Company Highlights

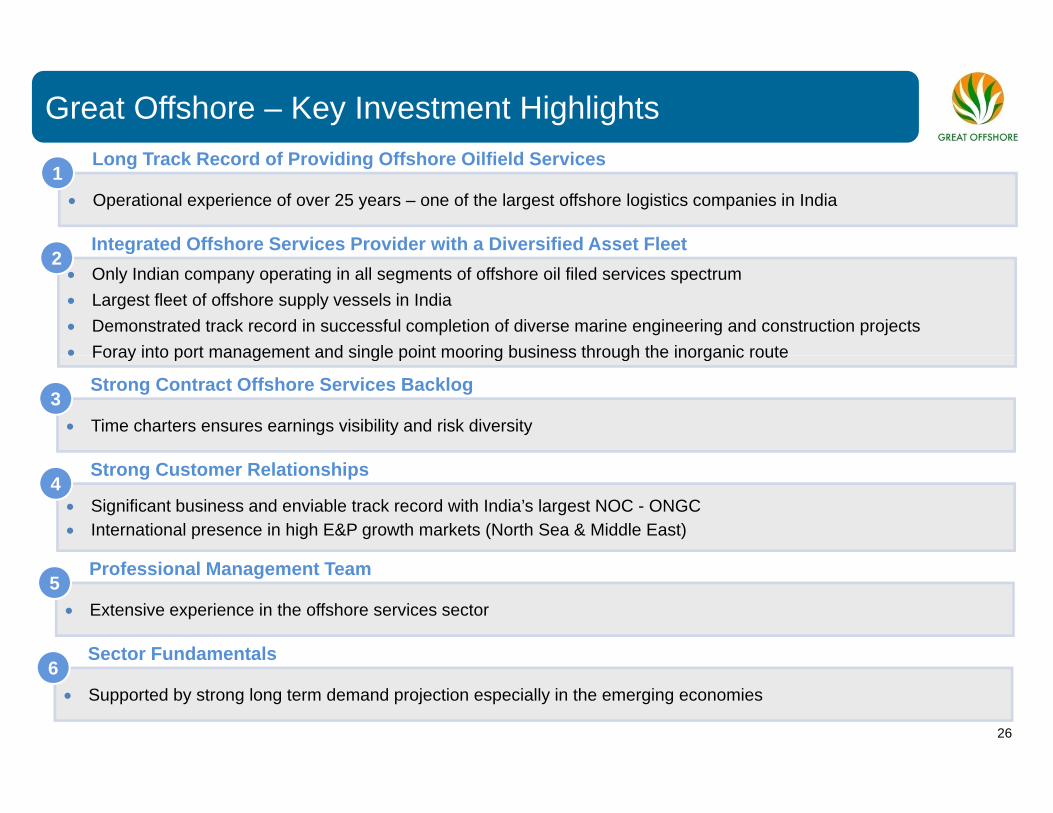

Great Offshore – Key Investment Highlights

• Operational experience of over 25 years – one of the largest offshore logistics companies in India1

Long Track Record of Providing Offshore Oilfield Services

2Integrated Offshore Services Provider with a Diversified Asset Fleet

• Only Indian company operating in all segments of offshore oil filed services spectrum• Largest fleet of offshore supply vessels in India • Demonstrated track record in successful completion of diverse marine engineering and construction projects • Foray into port management and single point mooring business through the inorganic route

2g

• Time charters ensures earnings visibility and risk diversity3

Strong Contract Offshore Services Backlog

• Foray into port management and single point mooring business through the inorganic route

• Significant business and enviable track record with India’s largest NOC - ONGC• International presence in high E&P growth markets (North Sea & Middle East)

4Strong Customer Relationships

• Extensive experience in the offshore services sector5

Professional Management Team

6Sector Fundamentals

26

• Supported by strong long term demand projection especially in the emerging economies6

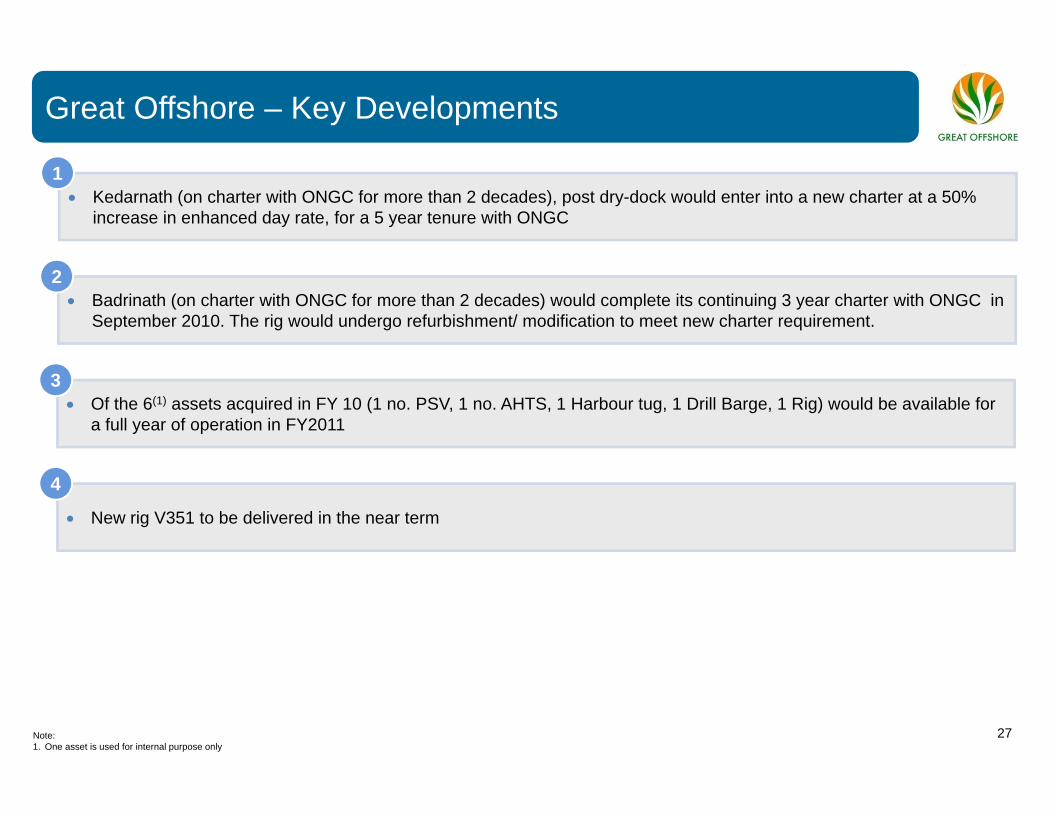

Great Offshore – Key Developments

• Kedarnath (on charter with ONGC for more than 2 decades), post dry-dock would enter into a new charter at a 50% increase in enhanced day rate, for a 5 year tenure with ONGC

1

• Badrinath (on charter with ONGC for more than 2 decades) would complete its continuing 3 year charter with ONGC in September 2010. The rig would undergo refurbishment/ modification to meet new charter requirement.

2

• Of the 6(1) assets acquired in FY 10 (1 no. PSV, 1 no. AHTS, 1 Harbour tug, 1 Drill Barge, 1 Rig) would be available for a full year of operation in FY2011

3

• New rig V351 to be delivered in the near term

4

27Note:1. One asset is used for internal purpose only

28