Embed Size (px)

Citation preview

Investor PresentationFebruary 2017

1

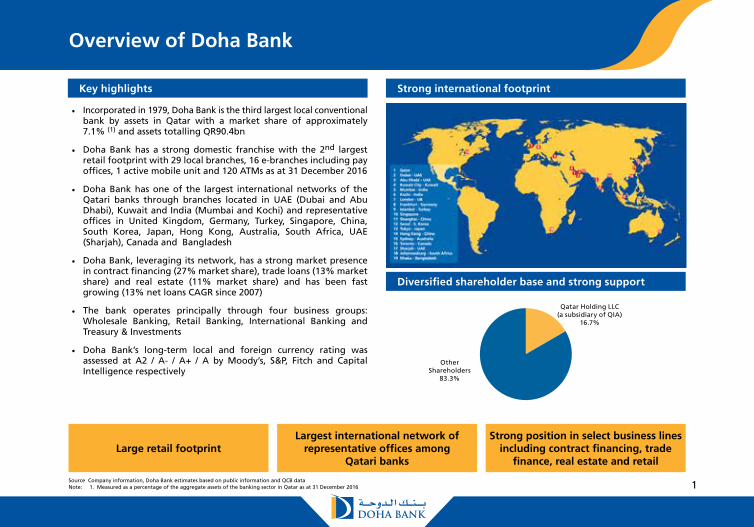

Overview of Doha Bank

Key highlights Strong international footprint

Diversified shareholder base and strong support

• Incorporated in 1979, Doha Bank is the third largest local conventional bank by assets in Qatar with a market share of approximately 7.1% (1) and assets totalling QR90.4bn

• Doha Bank has a strong domestic franchise with the 2nd largest retail footprint with 29 local branches, 16 e-branches including pay offices, 1 active mobile unit and 120 ATMs as at 31 December 2016

• Doha Bank has one of the largest international networks of the Qatari banks through branches located in UAE (Dubai and Abu Dhabi), Kuwait and India (Mumbai and Kochi) and representative offices in United Kingdom, Germany, Turkey, Singapore, China, South Korea, Japan, Hong Kong, Australia, South Africa, UAE (Sharjah), Canada and Bangladesh

• Doha Bank, leveraging its network, has a strong market presence in contract financing (27% market share), trade loans (13% market share) and real estate (11% market share) and has been fast growing (13% net loans CAGR since 2007)

• The bank operates principally through four business groups: Wholesale Banking, Retail Banking, International Banking and Treasury & Investments

• Doha Bank’s long-term local and foreign currency rating was assessed at A2 / A- / A+ / A by Moody’s, S&P, Fitch and Capital Intelligence respectively

Large retail footprintLargest international network of

representative offices among Qatari banks

Strong position in select business lines including contract financing, trade

finance, real estate and retail

Source Company information, Doha Bank estimates based on public information and QCB dataNote: 1. Measured as a percentage of the aggregate assets of the banking sector in Qatar as at 31 December 2016

Qatar Holding LLC(a subsidiary of QIA)

16.7%

OtherShareholders

83.3%

2

Source QCB banks’ monthly statements and annual reports

Source Company information*Among conventional banks

Source Company information*Among conventional banks

Source QCB banks’ monthly statements and annual reports

Source QCB banks’ monthly statements and annual reports

120 167

212 247 307

364

458

548 601

650 727

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

2006 – 2016 CAGR: 20%

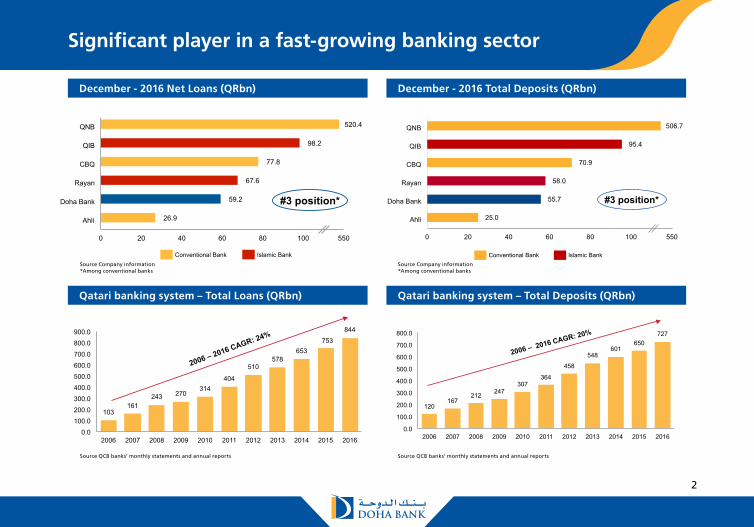

Significant player in a fast-growing banking sector

Source QCB banks’ monthly statements and annual reports

103 161

243 270 314

404

510 578

653 753

844

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

2006 – 2016 CAGR: 24%

December - 2016 Net Loans (QRbn)

Qatari banking system – Total Loans (QRbn)

December - 2016 Total Deposits (QRbn)

Qatari banking system – Total Deposits (QRbn)

520.4

98.2

77.8

67.6

59.2

26.9

0 20 40 60 80 100 550

QNB

QIB

CBQ

Rayan

Doha Bank

Ahli

Conventional Bank Islamic Bank

#3 position*

506.7

95.4

70.9

58.0

55.7

25.0

0 20 40 60 80 100 550

QNB

QIB

CBQ

Rayan

Doha Bank

Ahli

Conventional Bank Islamic Bank

#3 position*

3

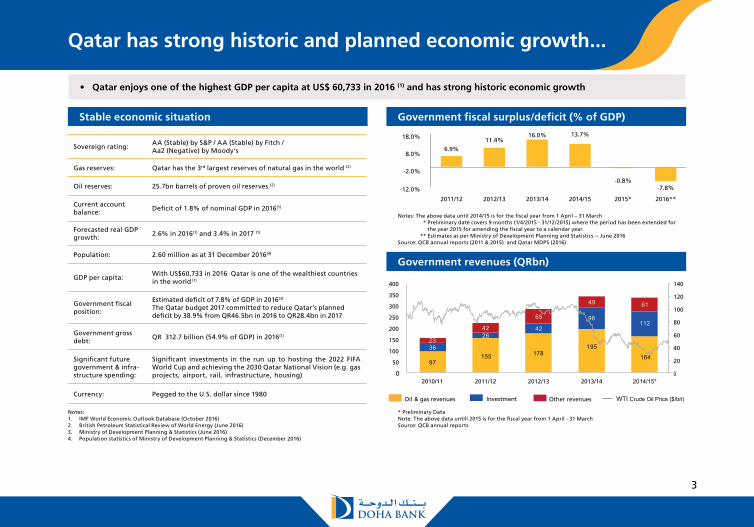

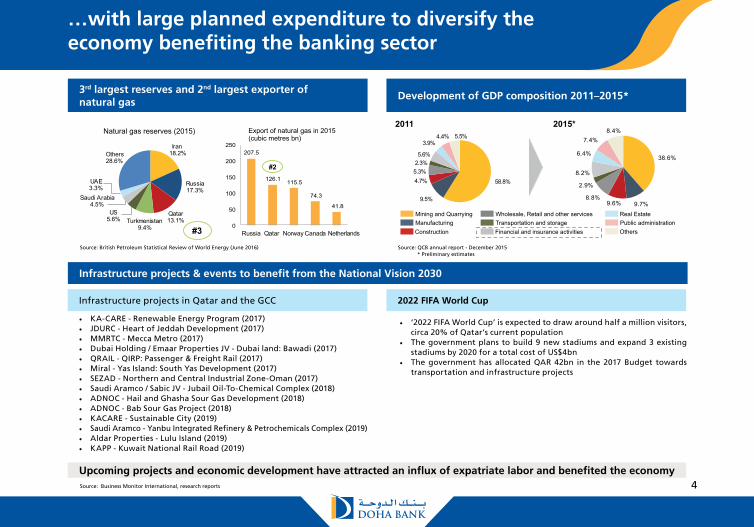

• Qatar enjoys one of the highest GDP per capita at US$ 60,733 in 2016 (1) and has strong historic economic growth

Qatar has strong historic and planned economic growth...

6.9%11.4%

16.0% 13.7%

-0.8%-7.8%-12.0%

-2.0%

8.0%

18.0%

2011/12 2012/13 2013/14 2014/15 2015* 2016**

2642

98112

23

42

65

49 61

Oil & gas revenues Other revenuesInvestment

97155 178

195

16436

2642

98112

23

42

65

49 61

0

50

100

150

200

250

300

350

400

2010/11 2011/12 2012/13 2013/14 2014/15*0

20

40

60

80

100

120

140

WTI Crude Oil Price ($/brl)

Sovereign rating:AA (Stable) by S&P / AA (Stable) by Fitch / Aa2 (Negative) by Moody’s

Gas reserves: Qatar has the 3rd largest reserves of natural gas in the world (2)

Oil reserves: 25.7bn barrels of proven oil reserves (2)

Current account balance:

Deficit of 1.8% of nominal GDP in 2016(1)

Forecasted real GDP growth:

2.6% in 2016(1) and 3.4% in 2017 (1)

Population: 2.60 million as at 31 December 2016(4)

GDP per capita:With US$60,733 in 2016 Qatar is one of the wealthiest countries in the world (1)

Government fiscal position:

Estimated deficit of 7.8% of GDP in 2016(3)

The Qatar budget 2017 committed to reduce Qatar’s planned deficit by 38.9% from QR46.5bn in 2016 to QR28.4bn in 2017

Government gross debt:

QR 312.7 billion (54.9% of GDP) in 2016(1)

Significant future government & infra-structure spending:

Significant investments in the run up to hosting the 2022 FIFA World Cup and achieving the 2030 Qatar National Vision (e.g. gas projects, airport, rail, infrastructure, housing)

Currency: Pegged to the U.S. dollar since 1980

Notes:1. IMF World Economic Outlook Database (October 2016)2. British Petroleum Statistical Review of World Energy (June 2016)3. Ministry of Development Planning & Statistics (June 2016)4. Population statistics of Ministry of Development Planning & Statistics (December 2016)

Notes: The above data until 2014/15 is for the fiscal year from 1 April – 31 March * Preliminary date covers 9 months (1/4/2015 - 31/12/2015) where the period has been extended for the year 2015 for amending the fiscal year to a calendar year. ** Estimates as per Ministry of Development Planning and Statistics -- June 2016Source: QCB annual reports (2011 & 2015) and Qatar MDPS (2016)

* Preliminary Data Note: The above data untill 2015 is for the fiscal year from 1 April - 31 MarchSource: QCB annual reports

Stable economic situation Government fiscal surplus/deficit (% of GDP)

Government revenues (QRbn)

4

…with large planned expenditure to diversify the economy benefiting the banking sector

Russia 17.3%

Iran 18.2%

Qatar 13.1% Turkmenistan

9.4%

Saudi Arabia 4.5%

US 5.6%

UAE 3.3%

Others 28.6%

#3

Natural gas reserves (2015)

Russia Qatar Norway Canada Netherlands

207.5

126.1 115.5

74.3

41.8

0

50

100

150

200

250

5102 ni sag larutan fo tropxE(cubic metres bn)

#2

Source: British Petroleum Statistical Review of World Energy (June 2016)

Source: Business Monitor International, research reports

Source: QCB annual report - December 2015 * Preliminary estimates

Upcoming projects and economic development have attracted an influx of expatriate labor and benefited the economy

Infrastructure projects in Qatar and the GCC 2022 FIFA World Cup

• KA-CARE - Renewable Energy Program (2017)• JDURC - Heart of Jeddah Development (2017)• MMRTC - Mecca Metro (2017)• Dubai Holding / Emaar Properties JV - Dubai land: Bawadi (2017)• QRAIL - QIRP: Passenger & Freight Rail (2017)• Miral - Yas Island: South Yas Development (2017)• SEZAD - Northern and Central Industrial Zone-Oman (2017)• Saudi Aramco / Sabic JV - Jubail Oil-To-Chemical Complex (2018)• ADNOC - Hail and Ghasha Sour Gas Development (2018)• ADNOC - Bab Sour Gas Project (2018)• KACARE - Sustainable City (2019)• Saudi Aramco - Yanbu Integrated Refinery & Petrochemicals Complex (2019)• Aldar Properties - Lulu Island (2019)• KAPP - Kuwait National Rail Road (2019)

• ‘2022 FIFA World Cup’ is expected to draw around half a million visitors, circa 20% of Qatar’s current population

• The government plans to build 9 new stadiums and expand 3 existing stadiums by 2020 for a total cost of US$4bn

• The government has allocated QAR 42bn in the 2017 Budget towards transportation and infrastructure projects

Mining and Quarrying Wholesale, Retail and other services Manufacturing Transportation and storage Construction

2011 2015*

Financial and insurance activities

Real Estate Public administration Others

58.8%

9.5%

4.7%5.3%2.3%5.6%

3.9%4.4% 5.5%

38.6%

9.7%9.6%8.8%

2.9%

8.2%

6.4%

7.4%8.4%

3rd largest reserves and 2nd largest exporter ofnatural gas

Infrastructure projects & events to benefit from the National Vision 2030

Development of GDP composition 2011–2015*

5

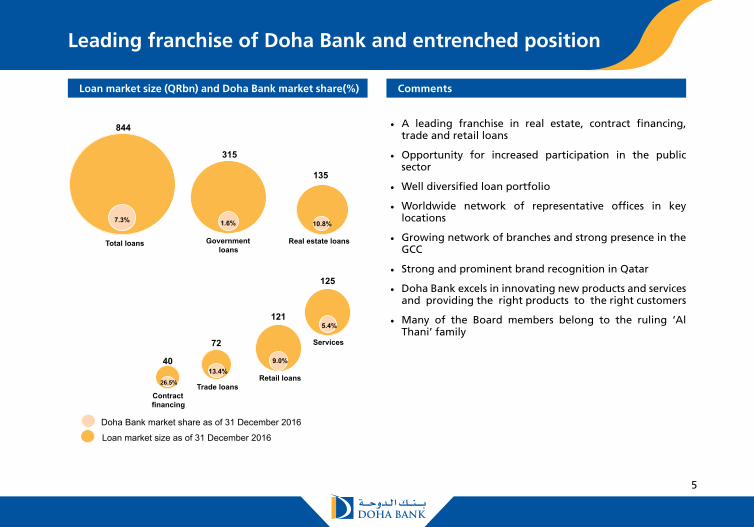

Leading franchise of Doha Bank and entrenched position

844

7.3%

Total loans

125

5.4%

Services

135

10.8%

Real estate loans

72

13.4%

Trade loans

40

26.5%

Contract financing

Doha Bank market share as of 31 December 2016

Loan market size as of 31 December 2016

1.6%

Government loans

315

121

9.0%

Retail loans

• A leading franchise in real estate, contract financing, trade and retail loans

• Opportunity for increased participation in the public sector

• Well diversified loan portfolio

• Worldwide network of representative offices in key locations

• Growing network of branches and strong presence in the GCC

• Strong and prominent brand recognition in Qatar

• Doha Bank excels in innovating new products and services and providing the right products to the right customers

• Many of the Board members belong to the ruling ‘Al Thani’ family

Loan market size (QRbn) and Doha Bank market share(%) Comments

6

Real estate Contract financing Trade Services

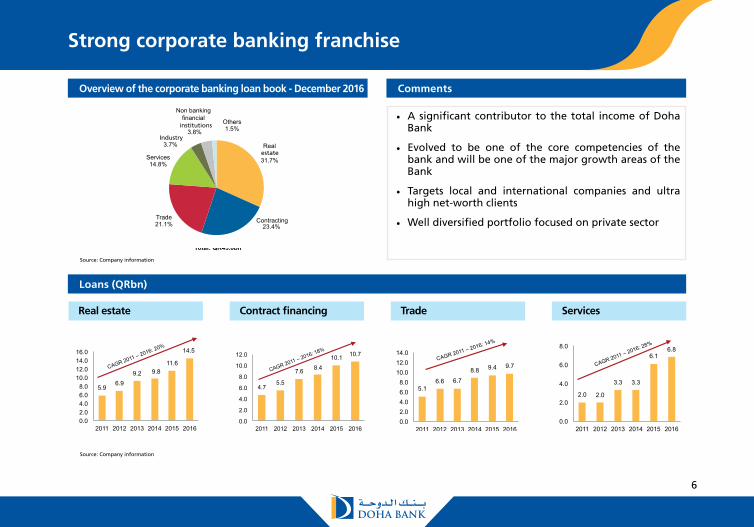

• A significant contributor to the total income of Doha Bank

• Evolved to be one of the core competencies of the bank and will be one of the major growth areas of the Bank

• Targets local and international companies and ultra high net-worth clients

• Well diversified portfolio focused on private sector

Total: QR45.8bn Source Company information

Real estate 31.7%

Contracting23.4%

Trade 21.1%

Services 14.8%

Industry 3.7%

Non banking financial

institutions3.8%

Others 1.5%

5.9 6.9

9.2 9.8 11.6

14.5

0.0 2.0 4.0 6.0 8.0

10.0 12.0 14.0 16.0

2011 2012 2013 2014 2015 2016

CAGR 2011 – 2016: 20%

4.7 5.5

7.6 8.4 10.1 10.7

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2011 2012 2013 2014 2015 2016

CAGR 2011 – 2016: 18%

5.1 6.6 6.7

8.8 9.4 9.7

0.0 2.0 4.0 6.0 8.0

10.0 12.0 14.0

2011 2012 2013 2014 2015 2016

CAGR 2011 – 2016: 14%

2.0 2.0

3.3 3.3

6.1 6.8

0.0

2.0

4.0

6.0

8.0

2011 2012 2013 2014 2015 2016

CAGR 2011 – 2016: 28%

Strong corporate banking franchise

Overview of the corporate banking loan book - December 2016

Loans (QRbn)

Comments

Source: Company information

Source: Company information

7

% of total December 2016 loans portfolio

Source Company information and QCB data

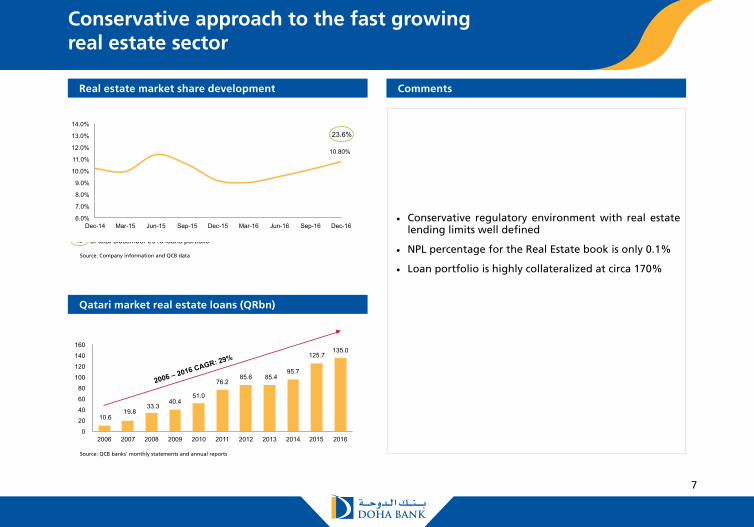

10.80%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16

23.6%

Source QCB banks’ monthly statements and annual reports

10.6 19.8

33.3 40.4

51.0

76.2 85.6 85.4

95.7

125.7 135.0

0

20

40

60

80

100

120

140

160

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

2006 – 2016 CAGR: 29%

Conservative approach to the fast growing real estate sector

Real estate market share development

Qatari market real estate loans (QRbn)

Source: Company information and QCB data

Source: QCB banks’ monthly statements and annual reports

• Conservative regulatory environment with real estate lending limits well defined

• NPL percentage for the Real Estate book is only 0.1%

• Loan portfolio is highly collateralized at circa 170%

Comments

8

% of total December 2016 loans portfolio Source Company information and QCB data

26.50%

20.0%

22.0%

24.0%

26.0%

28.0%

30.0%

32.0%

34.0%

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16

17.4%

Source QCB banks’ monthly statements and annual reports

5.1 8.2

11.5 13.0

18.4 16.2

18.2

23.3

32.0

38.9 40.4

0

10

20

30

40

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

2006 – 2016 CAGR: 23%

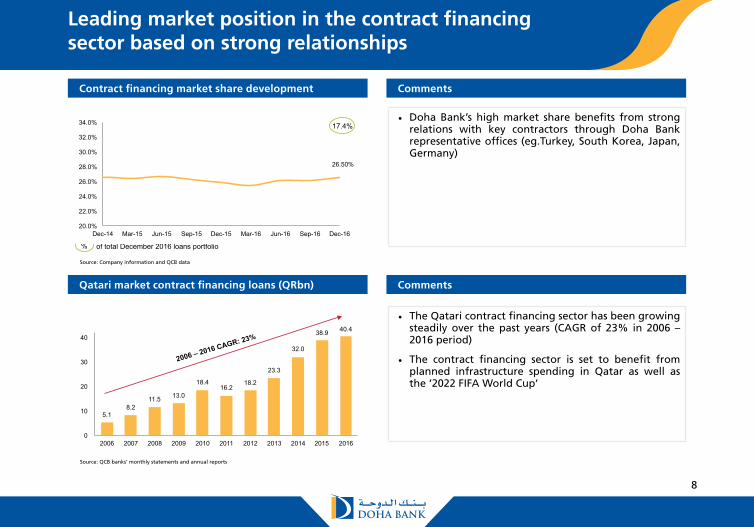

• Doha Bank’s high market share benefits from strong relations with key contractors through Doha Bank representative offices (eg.Turkey, South Korea, Japan, Germany)

• The Qatari contract financing sector has been growing steadily over the past years (CAGR of 23% in 2006 – 2016 period)

• The contract financing sector is set to benefit from planned infrastructure spending in Qatar as well as the ‘2022 FIFA World Cup’

Leading market position in the contract financing sector based on strong relationships

Contract financing market share development

Qatari market contract financing loans (QRbn)

Comments

Comments

Source: Company information and QCB data

Source: QCB banks’ monthly statements and annual reports

9

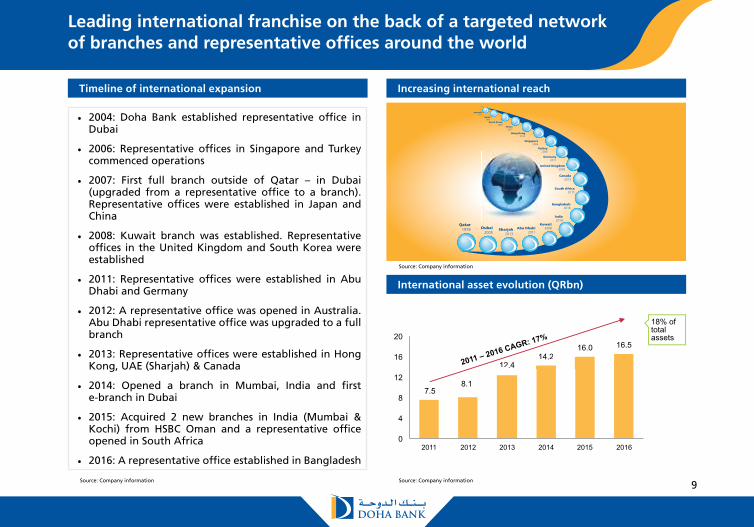

• 2004: Doha Bank established representative office in Dubai

• 2006: Representative offices in Singapore and Turkey commenced operations

• 2007: First full branch outside of Qatar – in Dubai (upgraded from a representative office to a branch). Representative offices were established in Japan and China

• 2008: Kuwait branch was established. Representative offices in the United Kingdom and South Korea were established

• 2011: Representative offices were established in Abu Dhabi and Germany

• 2012: A representative office was opened in Australia. Abu Dhabi representative office was upgraded to a full branch

• 2013: Representative offices were established in Hong Kong, UAE (Sharjah) & Canada

• 2014: Opened a branch in Mumbai, India and first e-branch in Dubai

• 2015: Acquired 2 new branches in India (Mumbai & Kochi) from HSBC Oman and a representative office opened in South Africa

• 2016: A representative office established in Bangladesh

Leading international franchise on the back of a targeted network of branches and representative offices around the world

7.5 8.1

12.4 14.2

16.0 16.5

0

4

8

12

16

20

2011 2012 2013 2014 2015 2016

12.4 14.2

2011 – 2016 CAGR: 17%

18% of total assets

Bangladesh2016

Timeline of international expansion Increasing international reach

International asset evolution (QRbn)

Source: Company information

Source: Company information

Source: Company information

10

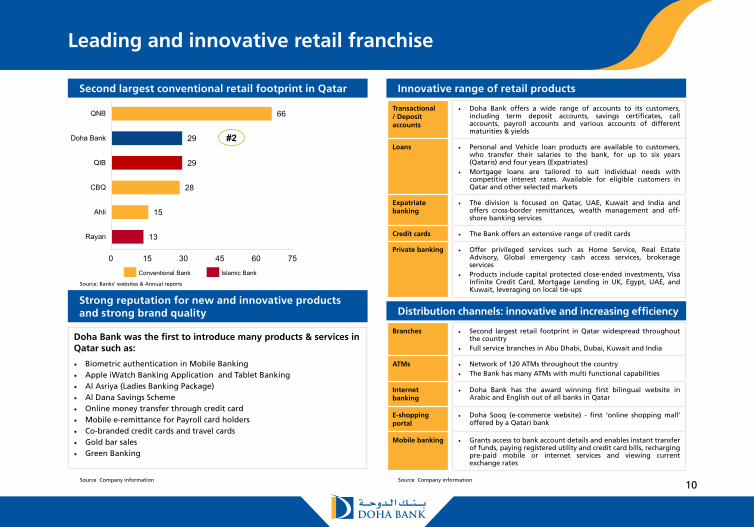

Branches • Second largest retail footprint in Qatar widespread throughout the country

• Full service branches in Abu Dhabi, Dubai, Kuwait and India

ATMs • Network of 120 ATMs throughout the country • The Bank has many ATMs with multi functional capabilities

Internet banking

• Doha Bank has the award winning first bilingual website in Arabic and English out of all banks in Qatar

E-shopping portal

• Doha Sooq (e-commerce website) - first ‘online shopping mall’ offered by a Qatari bank

Mobile banking • Grants access to bank account details and enables instant transfer of funds, paying registered utility and credit card bills, recharging pre-paid mobile or internet services and viewing current exchange rates

Transactional / Deposit accounts

• Doha Bank offers a wide range of accounts to its customers, including term deposit accounts, savings certificates, call accounts, payroll accounts and various accounts of different maturities & yields

Loans • Personal and Vehicle loan products are available to customers, who transfer their salaries to the bank, for up to six years (Qataris) and four years (Expatriates)

• Mortgage loans are tailored to suit individual needs with competitive interest rates. Available for eligible customers in Qatar and other selected markets

Expatriate banking

• The division is focused on Qatar, UAE, Kuwait and India and offers cross-border remittances, wealth management and off-shore banking services

Credit cards • The Bank offers an extensive range of credit cards

Private banking • Offer privileged services such as Home Service, Real Estate Advisory, Global emergency cash access services, brokerage services

• Products include capital protected close-ended investments, Visa Infinite Credit Card, Mortgage Lending in UK, Egypt, UAE, and Kuwait, leveraging on local tie-ups

Leading and innovative retail franchise

Source Company information Source Company information

Doha Bank was the first to introduce many products & services in Qatar such as:

• Biometric authentication in Mobile Banking• Apple iWatch Banking Application and Tablet Banking• Al Asriya (Ladies Banking Package)• Al Dana Savings Scheme• Online money transfer through credit card• Mobile e-remittance for Payroll card holders• Co-branded credit cards and travel cards• Gold bar sales• Green Banking

Second largest conventional retail footprint in Qatar

Strong reputation for new and innovative products and strong brand quality

Innovative range of retail products

Distribution channels: innovative and increasing efficiency

Source: Banks’ websites & Annual reports

13

15

28

29

29

66

0 15 30 45 60 75

Rayan

Ahli

CBQ

QIB

Doha Bank

QNB

Conventional Bank Islamic Bank

#2

11

Strong credit quality

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

(200)

300

800

1,300

1,800

2,300

2,800

Loan loss provision balance (QRmn) Coverage ratio % Source Company information

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

(100)

400

900

1,400

1,900

2,400

2,900

786 845

1,230

1,775 2,070

2,409

74%

87% 97%

114% 110%

120%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

(100)

400

900

1,400

1,900

2,400

2,900

2011 2012 2013 2014 2015 2016

188% including risk reserve

NPL (QRmn) NPL %

(0.70%)

(0.20%)

0.30%

0.80%

1.30%

1.80%

2.30%

2.80%

3.30%

400

800

1,200

1,600

2,000

2,400

1,055 974

1,273

1,560

1,881 2,012

3.32% 2.81%

3.01% 3.10% 3.26% 3.27%

(0.70%)

(0.20%)

0.30%

0.80%

1.30%

1.80%

2.30%

2.80%

3.30%

0

400

800

1,200

1,600

2,000

2,400

2011 2012 2013 2014 2015 2016

(0.70%)

(0.20%)

0.30%

0.80%

1.30%

10 60

110 160 210 260 310 360 410 460 510 560 610 660

Net impairment loss on loans (QRmn) Cost of Risk %

Source Company information

271 190

318

439

313

480

0.94% 0.59%

0.85% 0.98%

0.60% 0.84%

(1.90%)

(1.40%)

(0.90%)

(0.40%)

0.10%

0.60%

1.10%

10 60

110 160 210 260 310 360 410 460 510 560 610 660

2011 2012 2013 2014 2015 2016

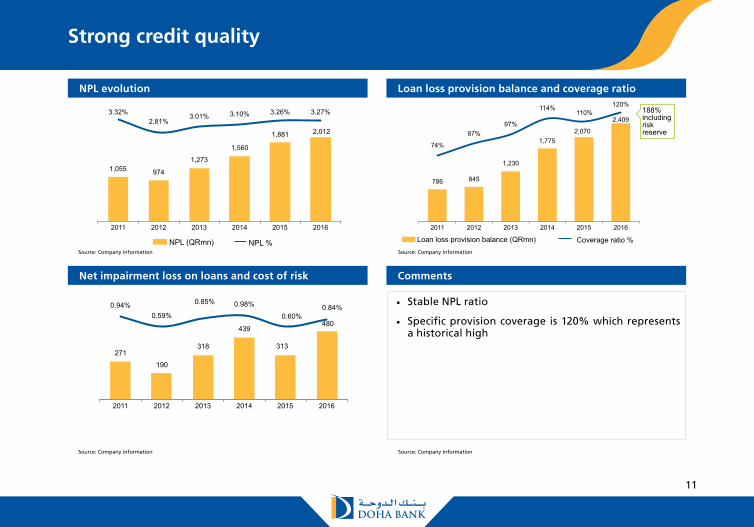

• Stable NPL ratio

• Specific provision coverage is 120% which represents a historical high

Source: Company information

Source: Company information

Source: Company information

Source: Company information

NPL evolution

Net impairment loss on loans and cost of risk

Loan loss provision balance and coverage ratio

Comments

12

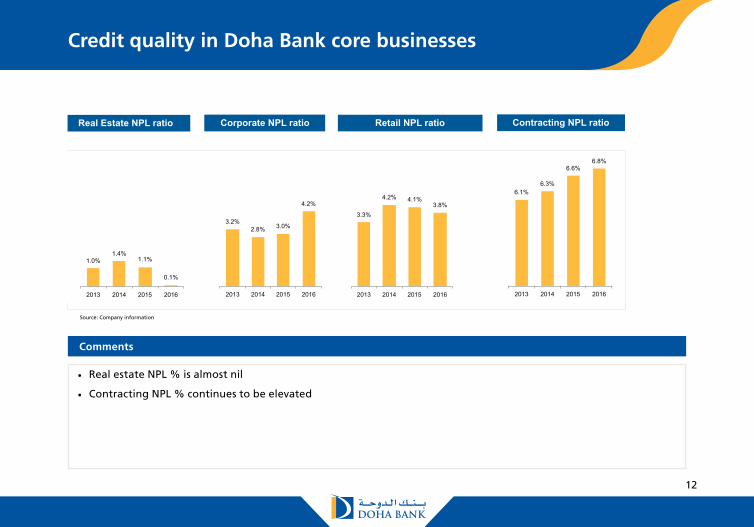

Credit quality in Doha Bank core businesses

Real Estate NPL ratio Contracting NPL ratio

4.0%

5.0%

6.0%

7.0%

Source Company information

• Real estate NPL % is almost nil

• Contracting and Corporate NPL % continues to be elevated

Comments

Corporate NPL ratio

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

Retail NPL ratio

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

1.0% 1.4%

1.1%

0.1% 0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2013 2014 2015 2016

3.2% 2.8% 3.0%

4.2%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2013 2014 2015 2016

3.3%

4.2% 4.1% 3.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

2013 2014 2015 2016

6.1% 6.3%

6.6% 6.8%

4.0%

5.0%

6.0%

7.0%

2013 2014 2015 2016

• Real estate NPL % is almost nil

• Contracting NPL % continues to be elevated

Source: Company information

Comments

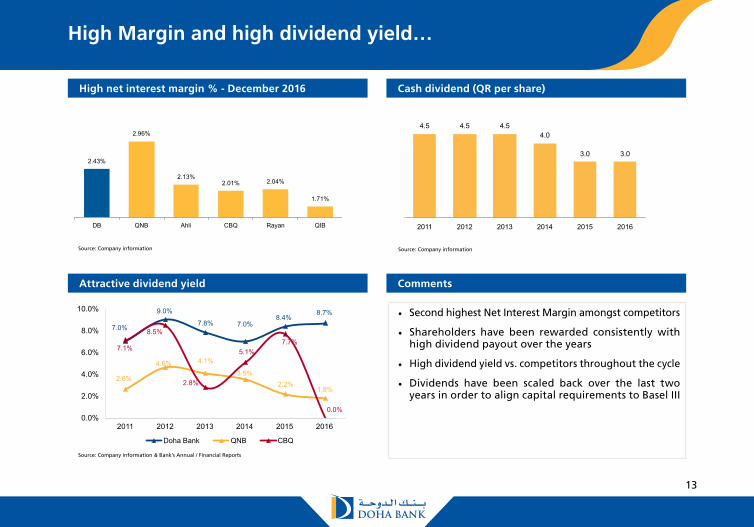

13

4.5 4.5 4.5 4.0

3.0 3.0

2011 2012 2013 2014 2015 2016

7.0%

9.0% 7.8% 7.0%

8.4% 8.7%

2.6%

4.6% 4.1%

3.5% 2.2%

1.8%

7.1%

8.5%

2.8%

5.1% 7.7%

7.2%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0% 9.0%

10.0%

2011 2012 2013 2014 2015 2016

Doha Bank QNB CBQ* *CBQ 2016 data based on Q3 16 information Source: Company Information & Bank's Annual / Financial Reports

• Second highest Net Interest Margin amongst competitors

• Shareholders have been rewarded consistently with high dividend payout over the years

• High dividend yield vs. competitors throughout the cycle

• Dividends have been scaled back over the last two years in order to align capital requirements to Basel III

High Margin and high dividend yield…

Source: Company information

Source: Company information & Bank’s Annual / Financial Reports

Source: Company information

High net interest margin % - December 2016

Attractive dividend yield

Cash dividend (QR per share)

Comments

2.43%

2.96%

2.13% 2.01% 2.04%

1.71%

DB QNB Ahli CBQ Rayan QIB

7.0%

9.0%

7.8% 7.0% 8.4%

8.7%

2.6%

4.6% 4.1%

3.5% 2.2%

1.8%

7.1%

8.5%

2.8%

5.1% 7.7%

0.0% 0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

۲۰۱۱ ۲۰۱۲ ۲۰۱۳ ۲۰۱٤ ۲۰۱٥ ۲۰۱٦

Doha Bank QNB CBQ

7.0%

9.0%

7.8% 7.0% 8.4%

8.7%

2.6%

4.6% 4.1%

3.5% 2.2%

1.8%

7.1%

8.5%

2.8%

5.1% 7.7%

0.0% 0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

۲۰۱۱ ۲۰۱۲ ۲۰۱۳ ۲۰۱٤ ۲۰۱٥ ۲۰۱٦

Doha Bank QNB CBQ

14

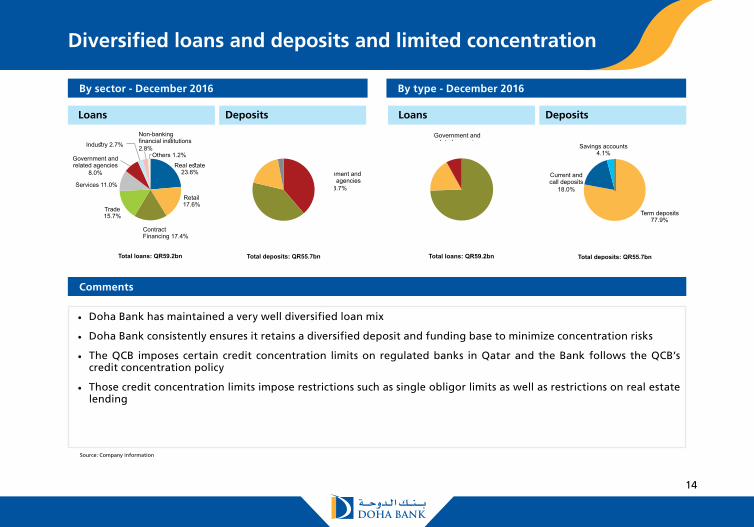

LoansLoans DepositsDeposits

Retail 17.6%

Real estate 23.6%

Trade 15.7%

Contract Financing 17.4%

Government and related agencies

8.0%

Services 11.0%

Industry 2.7% Others 1.2%

Non-banking financial institutions 2.8%

Total loans: QR59.2bn

Non-banking financial institutions

3.0%

Government and related agencies

38.7%

Individual 18.3%

Corporate 40.0%

Total deposits: QR55.7bn

Corporate 74.4%

Retail 17.6%

Government and related agencies

8.0%

Total loans: QR59.2bn

Term deposits 77.9%

Savings accounts 4.1%

Current and call deposits

18.0%

Total deposits: QR55.7bn

• Doha Bank has maintained a very well diversified loan mix

• Doha Bank consistently ensures it retains a diversified deposit and funding base to minimize concentration risks

• The QCB imposes certain credit concentration limits on regulated banks in Qatar and the Bank follows the QCB’s credit concentration policy

• Those credit concentration limits impose restrictions such as single obligor limits as well as restrictions on real estate lending

Diversified loans and deposits and limited concentration

By sector - December 2016

Comments

By type - December 2016

Source: Company information

15

• Conservative investment philosophy

- Low hard limits for discretionary trading / investments

• Majority of portfolio in local sovereign fixed income

• State of Qatar portfolio repo-able with central bank to the extent liquidity is needed

• Conservative investments limits linked to Tier 1 capital as per QCB

Total (QR14,706mn)

State of Qatar debt securities

67.8%

Equities 6.9%

Other debt securities

24.9%

Mutual funds 0.4%

4,385 4,544 5,622 5,292 6,457 8,3093,192

5,0376,082

4,5275,724

6,392

7,577 9,581

11,704 9,856

12,198 14,706

0

4,000

8,000

12,000

16,000

2011 2012 2013 2014 2015 2016Available for Sale Held to Maturity

Available for Sale (QR8,309mn)

State of Qatar debt securities

59.4%

Equities12.3%

Other debt securities

27.6%

Mutual funds0.7%

Held to Maturity (QR6,392mn)

State of Qatar debt securities

78.6%

Other debt securities 21.4%

...and a conservative investment philosophy

Portfolio overview

Investment portfolio - Evolution by Classification QRmn

Investment Portfolio by type - December 2016 (%)

Source: Company information

16

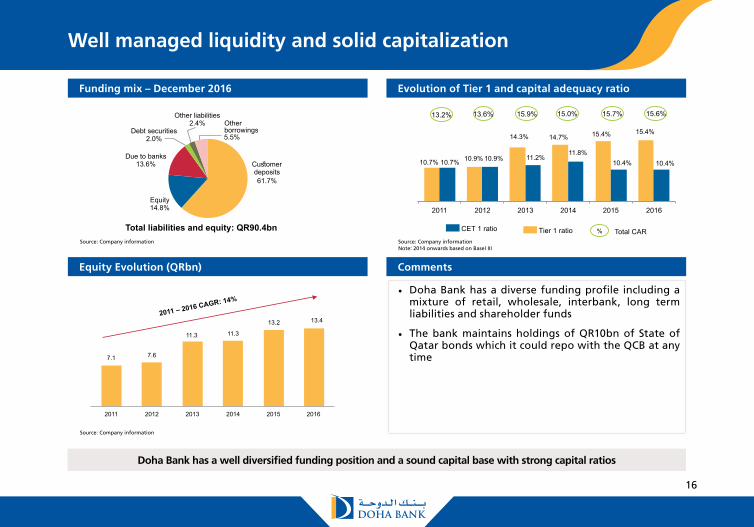

Doha Bank has a well diversified funding position and a sound capital base with strong capital ratios

• Doha Bank has a diverse funding profile including a mixture of retail, wholesale, interbank, long term liabilities and shareholder funds

• The bank maintains holdings of QR10bn of State of Qatar bonds which it could repo with the QCB at any time

Total liabilities and equity: QR90.4bn

Debt securities 2.0%

Due to banks 13.6%

Equity 14.8%

Customer deposits 61.7%

Other liabilities 2.4% Other

borrowings 5.5%

Note: 2014 onwards based on Basel III

10.7% 10.9%

14.3% 14.7% 15.4% 15.4%

10.7% 10.9% 11.2% 11.8%

10.4% 10.4%

2011 2012 2013 2014 2015 2016

CET 1 ratio Tier 1 ratio % Total CAR

Note: 2014 onwards based on Basel III

15.9% 13.2% 13.6% 15.0% 15.7% 15.6%

Well managed liquidity and solid capitalization

Source Company information

7.1 7.6

11.3 11.3

13.2 13.4

2011 2012 2013 2014 2015 2016

2011 – 2016 CAGR: 14%

Funding mix – December 2016

Equity Evolution (QRbn)

Evolution of Tier 1 and capital adequacy ratio

Comments

Source: Company information

Source: Company information

Source: Company informationNote: 2014 onwards based on Basel III

17

• Further develop existing operations in the UAE, Kuwait and India and position Doha Bank at thecentre of the infrastructure growth of the GCC economies

Further developregional branch

network

Furtherconsolidate Qatari

position

••

•

Doha Bank intends to further continue its targeted international expansion strategyExpand and further leverage the trade finance business through the network of representativeoffices, by further developing relations with companies doing business with Qatar, UAE, Kuwait and IndiaDoha Bank established its 13th Representative Office in Bangladesh

Continuetargeted

internationalexpansion

• Leverage on strong existing distribution channels to expand loan book, generatemore revenues and improve efficiency

• Identify areas of potential operational and cost efficiency improvements

Furtherimprove

efficiency

• Maintain conservative and cautious approach to underwriting in particularwith regards to contracting sector

• Continue improvement in risk management procedures and systems

Maintain creditquality

Source Company information

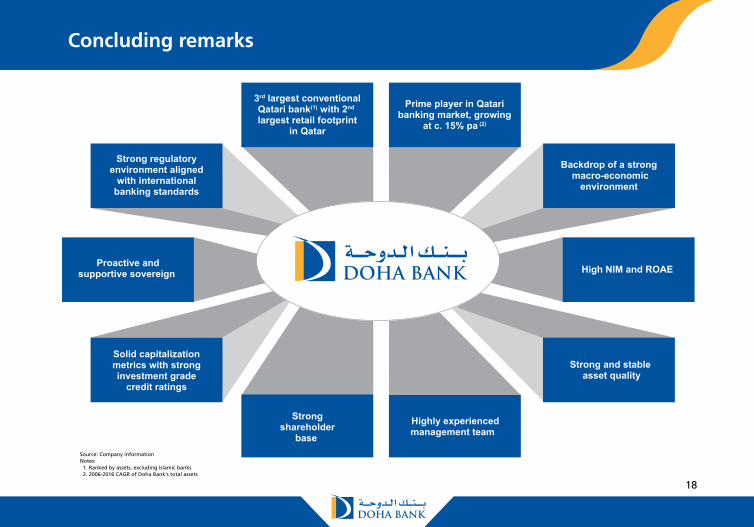

• With stable capital adequacy ratios, Doha Bank is positioned to capture the upcoming infrastructure growth in Qatar

Doha Bank strategy – clear path to future growth

Source: Company information

18

Source Company informationNotes1. Ranked by assets, excluding Islamic banks2. 2006-2016 CAGR of Doha Bank’s total assets

High NIM and ROAE Proactive andsupportive sovereign

Highly experiencedmanagement team

3rd largest conventionalQatari bank(1) with 2nd largest retail footprint

in Qatar

Strong and stable asset quality

Strongshareholder

base

Prime player in Qataribanking market, growing

at c. 15% pa (2)

Backdrop of a strong macro-economic

environment

Strong regulatoryenvironment aligned

with internationalbanking standards

Solid capitalizationmetrics with stronginvestment grade

credit ratings

Concluding remarks

Source: Company informationNotes: 1. Ranked by assets, excluding Islamic banks 2. 2006-2016 CAGR of Doha Bank’s total assets