Embed Size (px)

Citation preview

Investor Presentation

February 2015

23.02.2015

1. Strategic priorities: overall trends 2. Competitive strength 3. Strategic focus

Bangkok Bank 2015

2

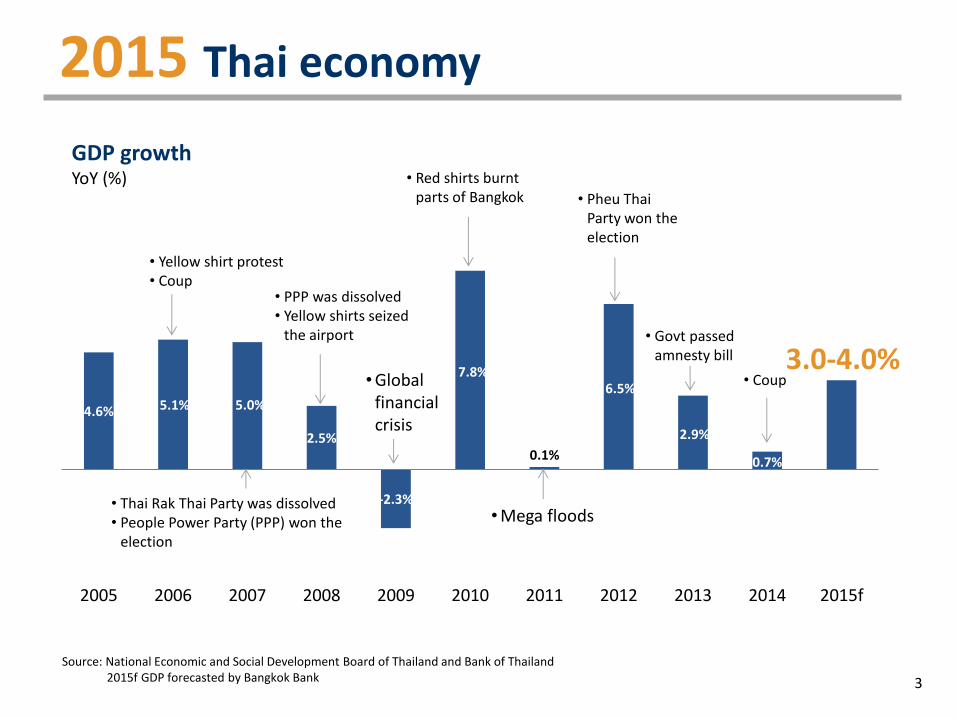

2015 Thai economy

GDP growth YoY (%)

4.6% 5.1% 5.0%

2.5%

-2.3%

7.8%

0.1%

6.5%

2.9%

0.7%

3.0-4.0%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015f

• Yellow shirt protest • Coup

• Thai Rak Thai Party was dissolved • People Power Party (PPP) won the

election

• PPP was dissolved • Yellow shirts seized

the airport

• Red shirts burnt parts of Bangkok

•Global financial crisis

•Mega floods

• Pheu Thai Party won the election

• Govt passed amnesty bill

Source: National Economic and Social Development Board of Thailand and Bank of Thailand 2015f GDP forecasted by Bangkok Bank

• Coup

3

Higher household debt to GDP

48.4% 47.6%

54.6% 55.6% 61.4% 63.0%

70.6% 77.3%

82.3% 84.8%

0%

20%

40%

60%

80%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013 Sep 2014

Source: National Economic and Social Development, Board of Thailand and Bank of Thailand

4

Source: Bank of Thailand, Center for Economic and Business Forecasting, and Thailand Stock Exchange

Thai economy is at an early stage of recovery

5

40

45

50

55

60

150

170

190

210

230

250

Aug Oct Dec2013

Feb Apr Jun Aug Oct Dec2014

Private investment index (L)

Manufactuing Production Index (L)

Business Sentiment Index (R)

-100%

-70%

-40%

-10%

20%

0

200

400

600

800

1,000

Dec2012

Mar Jun Sep Dec2013

Mar Jun Sep Dec2014

Exports

%YoY

0

30

60

90

120

150

140

142

144

146

148

150

Dec2012

Feb Apr Jun Aug Oct Dec2013

Feb Apr Jun Aug Oct Dec2014

Private Consumption index (L)

Consumer Confidence Index (R)

Exports Billion Baht

Investment indicators Index (2000=100)

Consumption indicators Index (2000=100)

Tourism indicators

0

1,000

2,000

3,000

Jan May Sep Jan May Sep Jan May Sep

Number of Foreign Tourists

Thousand persons

2014 2013 Dec

2012

405060708090

100110120

Jan-14 Mar-14 Jun-14 Aug-14 Nov-14 Jan-15

Crude Oil (Dubai)

45.69

107.54

World Economy

Source: Bloomberg, www.eppo.go.th

US$/bbl

1100

1150

1200

1250

1300

1350

1400

Jan-14 Mar-14 Jun-14 Aug-14 Nov-14 Jan-15

Gold

1,283.77

1,221.53

Source: Bloomberg, www.eppo.go.th

US$/ounce

6

U.S. Dollar Index (DXY) - Daily

Source: http://www.marketwatch.com

Commodity price (Sugar) - Daily

Source: http://www.nasdaqcom

3 Strategic priorities : overall trends

7

Regionalization

Urbanization Digitalization

Supported by

Government Policies

1. Regionalization

8

Note: Phase 1 (5 Economic zones), Phase 2 (7 Economic zones) CLMV refers to Cambodia, Laos, Myanmar and Vietnam Source: Department of Foreign Trade, www.nesdb.go.th

Linkages in the region and AEC Economic zones and border trade

Mae sai/ Chiang Saen/

Chiang Khong, Chiang Rai

Nongkhai

Nakhon Phanom

Mukdahan

Aranyaprathet, Sa Kaeo

Klongyai, Trat

Kanchanaburi

Mae Sot, Tak

Songkhla, Sadao

Narathiwat

Thailand

Laos

7.2%, +14.3%

Vietnam

5.6%, +52.2%

Cambodia

7.3%, +15.9%

Myanmar

8.5%, +17.8%

Malaysia

5.2%, -3.3%

2015f GDP, Export growth 2014

2. Urbanization

0

50

100

150

200

250

300

2001 2003 2005 2007 2009 2011

Bangkok & Vicinities Provincial

Gross regional product Index 2001=100

Source: NESDB, Bangkok Bank analysis

197.0 Bangkok & Vicinities

263.1 Provincial

0

2,000

4,000

6,000

8,000

10,000

12,000

Malaysia Thailand Indonesia Lao Cambodia

Income per capita 2013 US Dollar

Source: http://data.worldbank.org

2012

9

0

20

40

60

80

100

SG MY CHN TH INDO INDIA PH

3. Digitalization

94.3 million

Total Mobile Devices

Note: As at June 2014 Source: Digital Advertising Association (Thailand), Bank of Thailand

44.6 million

Mobile Internet Users

49% Smartphone Users

Smartphone penetration (%)

49

0

25

50

75

100

2010 2014e 2015f

Thailand Smartphone penetration (%)

63%

87 80

71

23 18 15

49%

18%

10

Promote special economic zones

Promote trade and investment outside Thailand

Promote Thailand to be a logistics hub for north ASEAN

Promote digital economy

Key economic policies of Thai government

Promote Thailand to be international headquarters

11

Key positioning and strengths SUSTAINABLE AND PROFITABLE GROWTH ACROSS BUSINESS CYCLES

12

Leading bank for business enterprises

Extensive network locally and internationally

Industry-leading position in capital and liquidity

Strong asset quality driven by prudent and independent risk management

Leading bank for consumers from large deposit base

Customer Focus Organization

Note: As at December 2014 Note: Consolidated

The leading bank for business enterprises Largest market share in lending to business enterprise across all sizes

13

29% market share in business loans

System/2 (exc. BBL)

71%

BBL

29%

Note: As at December 2014 Note: /2 System refers to 17 commercial banks Note: /4 registered in Thailand Source: Bank of Thailand (FI_CB_016_S2), Source: Bangkok Bank analysis

17% market share in total loans

System/1 (exc. BBL)

83%

BBL

17%

Note: As at December 2014 Note: /1 System refers to 17 commercial banks Note: /2 registered in Thailand Source: Bank of Thailand (FI_CB_002_S4), Source: Bangkok Bank analysis

Large Corporates

41%

Mid-sized SMEs

19%

Small-sized SMEs

11%

Consumer 13%

International 16%

A leading bank for consumers with large deposit base

19% market share in deposits

17 million deposit accounts

70% of deposits are retail deposits

14

Note: As at December 2014 /1 System refers to 17 commercial banks registered in Thailand

System/1 (exc. BBL)

81%

BBL

19%

1,197 domestic branches

30 international operations in 14 economies

Extensive network in North Asia and ASEAN

Note: As at December 2014

15

Beijing 1986

1955 Tokyo Singapore 1957

London

Kowloon 1954

Central District 1961 Hong Kong

Osaka 1970

1972 Jakarta

1965 New York Taipei

1990 Kaohshiung

Ho Chi Minh City 1992

1959 Kuala Lumpur

Hanoi 1995 Manila Taichung

Note: * Plan to open

1993 Shanghai Vientiane

1998 Xiamen

Shenzhen 2007

2009 Bangkok Bank (China)

Jalan Bakri 2010 Penang Taman Molek

2011 Bandar Botanic Klang

Surabaya 2012 • 2012

2013 Medan

2015 Myanmar*

(Rep. Office since 1995) Pakse (Laos)*

Chongqing 2014 Phnom Penh Shanghai Pilot Free Trade Zone

1944 Bangkok

Strong asset quality driven by prudent and independent risk management

16

BBL vs System

Loan loss reserves coverage ratio 204.1% vs 139.1%/1

Loan loss reserves / Loans 5.2% vs 3.7%/1

Provisioning expenses / Loans 49bps vs 79bps/1

Excess reserves over BOT requirement 177.3% vs 77.5%/2

Note: /1System refers to 17 commercial banks registered in Thailand. As at December 2014 /2System refers to 6 commercial banks. As at September 2014

17

Note: /1System refers to 17 commercial banks registered in Thailand. As at December 2014

Industry leading position in capital and liquidity

BBL vs System/1

Loan-to-Deposit Ratio 86.6% vs 94.6%

CET 1 Capital Ratio 16.0% vs 12.8%

Tier 1 Ratio 16.0% vs 13.0%

Capital adequacy Ratio 18.3% vs 16.5%

70 years of Bangkok Bank

เพอนคคด มตรคบาน

(puan koo kit mit koo baan)

18

Strategic focus

Maintain leadership position for business enterprises and consumers

Improve customer focus by building on existing relationships and understanding customer needs

Leverage scale to increase

revenues through synergy and cross selling

Further refine risk management practices

Digital proposition catered to servicing customers’ changing needs

19

International Large Corporates

Mid-sized SMEs

Small-sized SMEs

• 30 operations • 14 economies • 9/10 ASEAN countries • 16% of total loans

• 90%+ listed companies • 25 divisions • 41% of total loans

• 237 business centers • 19% of total loans

Deposits 17 million accounts

Bualuang Securities

Bangkok Life Assurance

Bangkok Insurance

Leverage leadership positions and enhance collaborations

• 237 business centers • 11% of total loans

BBL Asset Management

20

Loei

Kalasin Tak

Ratchaburi

Sa Kaeo

Prachuap Khiri Khan

11 new business centers

8 opened in border provinces

1,197 domestic branches

774 located in provinces

Nakhon Pathom

Thailand Myawaddy Border

Singkhon Border

Paoy Paet Border

Trat

Ranong

Nakhon Phanom

Yasothon

Strengthen network and operations in provincial areas

Myanmar

Laos

Vietnam

Cambodia

21

Note: Business centers opened during 2013 – 2014 Border crossing point

As at December 2014. Branches included 85 self-service. Business Centers are offices to service SME customers

Note: /1As at December 2014, and including the representative office

Continuously expand international operations

China (28 years)

Singapore (57 years)

Vietnam (22 years)

Hong Kong (60 years)

London (57 years)

Indonesia (46 years)

Malaysia (55 years)

Philippines (19 years)

Taipei (49 years)

22

30 Numbers of

International operations/1

16.4% International lending as a % of total lending

23

Promote and invest intensively in digital banking

0% 20% 40% 60% 80% 100%

Talking with advisors

Making complaints

Checking balances

Viewing transactions

Transferring money

Paying bills

Online Mobile Call Center Branch

2013 Global Survey: Preferred channels for banking activities

Simple

Convenient

Secure

• Streamline working process and paper work

• Offer most advanced cheque clearing system

• Launch online loan applications

• Launch Bualuang mBanking with new features

• All ATMs support EMV chip cards

• ATMs have 8 languages available

• Implement branch front-end view

Source: Datamonitor Financial 2013 FSCI Survey

0

10

20

30

40

50

0

2

4

6

8

10

12

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Dividend Dividend payout ratio (R)

… and results enabling steady growth in Net profit and Dividend payments

0

10

20

30

40

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

36.6%

6.50 Baht

Net profit Dividends and Payout ratio

36.3 Bn

24

Financial results Sustainable growth across business cycles

December 2014

1,143 1,256 1,470

1,604 1,753 1,782

0

500

1,000

1,500

2,000

2009 2010 2011 2012 2013 2014

Loans flattened mainly due to repayments by large corporates in the first half; however, demand started to

recover in 4Q14

Baht bn

+9.2%

-3.2% +9.9%

+17.1% +9.1%

+1.7%YTD

Loan amount Loan portfolio

26

Large Corporates

41%

Mid-sized SMEs 19%

Small-sized SMEs 11%

Consumer 13%

International 16%

55.6

45.6 42.6 42.3 43.2 45.0

0

20

40

60

80

2009 2010 2011 2012 2013 2014

Asset quality remained manageable

NPL amount Baht bn

4.4%

3.0% 2.7%

2.3% 2.2% 2.1%

0%

2%

4%

6%

2009 2010 2011 2012 2013 2014

NPL ratio

27

Steady provisioning policy with excess of reserves over required reserves by 177%

7.6 7.6

12.0

7.2 8.6

8.7

66 60

82

45 49 49

-15

0

15

30

45

60

75

90

0

5

10

15

20

2009 2010 2011 2012 2013 2014

Provisioning expenses (Baht bn)

Provisioning expenses / loans (Bps)

One-time provisioning expenses (Baht bn)

Baht bn Bps Baht bn

36.6 37.3 38.1 36.0 36.0 33.1

28.5 35.2

46.7 51.6 56.6 58.8

0

30

60

90

120

2009 2010 2011 2012 2013 2014

Excess reserves over BOT requirement(Baht bn)Allowance required by BOT (Baht bn)

87.6 92.6

84.8

72.5 65.1

91.9

Provisioning expenses Loan loss reserves

28

Loan loss reserves to NPLs and loans higher than system

29

Note: 1 As at December 2014 Note: /1 System refers to 17 commercial banks registered in Thailand

50%

100%

150%

200%

250%

2009 2010 2011 2012 2013 2014

System/1 139%

BBL 204%

Loan loss reserves / NPLs

2%

4%

6%

8%

2009 2010 2011 2012 2013 2014

System/1 3.7%

BBL 5.2%

Loan loss reserves / Loans

Retail deposits the major source of funds

30

1,361 1,394 1,588

1,835 1,935 2,059

0

500

1,000

1,500

2,000

2,500

2009 2010 2011 2012 2013 2014

Baht bn

+13.9%

+2.5% +2.9%

+15.5% +5.5%

+6.4% YTD

Lower cost of funds than system

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

2009 2010 2011 2012 2013 2014

System/1

2.2%

BBL

2.0%

Deposits

Note: 1 As at December 2014 Note: /1 System refers to 17 commercial banks registered in Thailand Source: Bangkok Bank filings

Liquid assets at 1/3 of total assets

As at December 2014

Liquid assets

33% Other assets 67%

“Liquid assets” consists of cash, interbank and money market assets, claims on securities and trading & available-for-sale securities

Deposits grew faster than loans, resulting in a lower loan to deposit ratio

31

60%

70%

80%

90%

100%

110%

2001 2003 2005 2007 2009 2011 2013

System/1 94.6%

BBL 86.6%

LDR always lower than system

Note: 1 As at December 2014 Note: /1 System refers to 17 commercial banks registered in Thailand Source: Bank of Thailand, Bangkok Bank analysis

2014

Net interest margin maintained at 2.37% although lower interest rate, due mainly to successful deposit mobilization

Note : 28 May 2013 policy rate cut by 25 bps to 2.50%, 27 Nov 2013 policy rate cut by 25 bps to 2.25% and 12 Mar 2014 policy rate cut by 25 bps to 2.00% Source: Bank of Thailand, Bangkok Bank analysis

2.76%

2.55%

2.36% 2.37%

2.28% 2.30%

2.44% 2.44%

2.32%

2.0%

2.2%

2.4%

2.6%

2.8%

2011 2012 2013 2014 4Q13 1Q14 2Q14 3Q14 4Q14

Yearly Net Interest Margin (%) Quarterly

Lending yield -9 bps Deposit cost -15 bps

Lending yield +6 bps Deposit cost +12 bps

32

Fee income better diversified. Recent growth drivers mainly came from consumer products, especially mutual funds

and bancassurance

13%

16%

26% 24%

9%

12%

Bancassurance & Mutual funds Loan-related feesCredit cards Transaction servicesGlobal market services Others

/2

4%

15%

23% 35%

16%

7%

2007 2014

Note: /1 CAGR of fee income during 2007-2014 Note: /1 CAGR +8.7% of fee income during 2007-2013 Note: /2 CAGR +28.1% of bancassurance & mutual funds during 2007-2014 Note: /2 CAGR +29.9% of bancassurance & mutual funds during 2007-2013

Bualuang Family Banking

Supply Chain

Cash Management

Debit Card

33

Net fee income growth slowed in line with economic situation. However, increase in fees from consumer products

helped compensate for lower loan-related fees.

18.1 19.1 21.2 21.7

5.1 5.2 5.3 5.5 5.8

0

5

10

15

20

25

2011 2012 2013 2014 4Q13 1Q14 2Q14 3Q14 4Q14

Baht bn

+11.1%

Net fee income

+4.8% QoQ +12.3% YoY

Yearly Net Fee Income Quarterly

+4.9% +5.5%

+2.3%

34

43

.8%

43

.5%

41

.5%

44

.5%

47

.9%

41

.4%

45

.2%

40

.9%

50

.6%

0%

10%

20%

30%

40%

50%

60%

2011 2012 2013 2014 4Q13 1Q14 2Q14 3Q14 4Q14

BBL’s cost-to-income ratio

Normalized cost to income is lower than the system, due to economies of scale and efficiency improvements

Note: /1 For 2013 operating expenses include the one-time item of the reversal of estimated loss on the impaired assets transferred to Thai Asset Management Corporation (TAMC), amounting to Baht 2.58 billion. If this is not included, the cost to income ratio would be 44.3% for 2013.

/1

35

/2

1.6%

2.5%

Cost-to-average assets

BBL System

44.5% 45.1%

Cost-to-income

Low cost-to-assets and cost-to-income ratio For 2014

Note: 1 As at December 2014 Note: /2 System refers to 17 commercial banks registered in Thailand Source: Bangkok Bank filings

Operating expenses increased in 2014 due to one-time reversal of expenses in 2013

36.1 37.1 37.9 43.1

10.6 9.4 11.0 10.7 12.1

0

10

20

30

40

50

2011 2012 2013 2014 4Q13 1Q14 2Q14 3Q14 4Q14

Operating expenses breakdown

For 2014

52%

23%

8%

17%

Personnel expenses

Premises and equipment

Tax and duties

Others

/1

Note: /1 Including directors’ remuneration /2 If excluding the one-time item of the reversal of estimated loss on the impaired assets transferred to Thai Asset Management Corporation (TAMC), amounting to Baht 2.58 billion, other operating expenses growth would be 1.6% YoY

Operating expenses

Baht bn

/3

Note: /3 For 2013 if excluding the one-time item of the reversal of estimated loss on the impaired assets transferred to TAMC, amounting to Baht 2.58 billion, operating expenses growth would be 9.1% YoY /4 If excluding the one-time item of the reversal of estimated loss on the impaired assets transferred to TAMC, amounting to Baht 2.58 billion, operating expenses growth would be 6.3% YoY

+13.1% QoQ +14.2% YoY

+2.2%

+13.5%

6.7% YoY

56.9% YoY

5.1% YoY

9.5% YoY

/2

/4

36

Proven and consistent delivery of net profits across business cycles

17.9 19.2 20.2 20.6 24.6

27.3 31.8

35.9 36.3

7.7 9.0 9.0 9.6 8.8

0

10

20

30

40

2006 2007 2008 2009 2010 2011 2012 2013 2014 4Q13 1Q14 2Q14 3Q14 4Q14

Baht bn

Note: Corporate tax rate reduced from 30% to 23% in 2012 and to 20% in 2013 onwards

+1.2%

+14.0% YoY -8.5% QoQ

+12.7%

Yearly Net profit (owners of the Bank) Quarterly

37

ROE at 12% while ROA at 1.4%. Improvement in ROE will be from growing revenues

1.1

9%

1.3

4%

1.3

6%

1.4

1%

1.4

5%

1.3

9%

1.2

0%

1.4

7%

1.3

0%

0.0%

0.5%

1.0%

1.5%

2.0%

2009 2010 2011 2012 2013 2014 4Q13 3Q14 4Q14

11

.23

%

11

.50

%

11

.57

%

12

.35

%

12

.62

%

11

.66

%

10

.47

%

12

.02

%

10

.83

%

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

2009 2010 2011 2012 2013 2014 4Q13 3Q14 4Q14

ROA ROE

Note: 2006-2009 ROE, ROA was bank only 2010-2014 ROE, ROA was consolidated

38

Progressive dividend payments, meaning payout are stable or higher in terms of absolute amount

Dividends and Payout ratio

Baht

0.75 0.75 1.00 1.00 1.00 1.00 1.50 2.00 2.00 2.00 1.00 1.25 1.75 2.00 2.00

3.00 3.50

4.00 4.50 4.50

0

10

20

30

40

50

0

2

4

6

8

10

12

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Interim (L) Final (L) Dividend payout ratio (R)

5.00

3.00 4.00

6.00 6.50 6.50

36.6%

3.00 2.75 2.00 1.75

Percent

39

Common Equity Tier 1 Capital Adequacy Ratio

Note: /1 The ratios include net profit for the second half of 2014 Note: /1 Consolidated

/1

0%

5%

10%

15%

20%

4.5%

16.0%

7.0%

Basel III

16.0%

6.0%

8.5%

Basel III

Tier 1 Capital Adequacy Ratio

18.3%

8.5%

11.0%

Basel III

Total Capital Adequacy Ratio

/1

/1

BOT’s Basel III requirements until the end of 2015

BOT’s Basel III requirements as of the year 2019

BBL’s Basel III ratio as of December 31, 2014

Capital ratio is higher than requirement under Basel 3

40

2011 2012 2013 2014

Branches

ATMs

CDMs

Employees

1,063

6,770

1,036

22,599

1,131

7,547

1,108

24,091

1,183

8,472

1,142

25,384

1,226

8,877

1,237

26,132

Note: Consolidated

+68

+777

+72

+1,492

+52

+925

+34

+748

+43

+405

+95

+1,293

Number of branches increased at a slower pace while we invested more heavily in non-branch channels

Number of employees increased mainly to improve services and increase sale effectiveness

41

This presentation is made by Bangkok Bank and may not be copied, altered, offered, sold or otherwise distributed to any other person by any recipient without the consent of Bangkok Bank. Although all reasonable effort has been made to ensure the facts stated herein are accurate and that the opinions contained herein are fair and reasonable, this document is selective in nature and is intended to provide an introduction to, and overview of, the business of Bangkok Bank. Where any information and statistics are quoted from any external source, such information or statistics should not be interpreted as having been adopted or endorsed by Bangkok bank as being accurate. Neither Bangkok Bank nor any of its directors, officers, employees, and advisors nor any other person shall have any liability whatsoever for loss howsoever arising, directly or indirectly, from any use of this information. The facts and information contained herein are as up to date as is reasonably possible and may be subject to revision in the future. Neither Bangkok Bank nor any of its directors, officers, employees or advisors nor any other person makes any representation or warranty, express or implied, as to the accuracy or completeness of the information contained in this presentation. Neither Bangkok Bank nor any of its directors, officers, employees and advisors nor any other person shall have any liability whatsoever for loss howsoever arising, directly or indirectly, from any use of this presentation. This presentation may contain projections or other forward-looking statements related to Bangkok Bank that involve risks and uncertainties. Readers are cautioned that these statements are only projections and may differ materially from actual future results or events. All forward-looking statements are based on information available to Bangkok Bank on the date of its posting and Bangkok Bank assumes no obligation to update such statements unless otherwise required by applicable law. This presentation does not constitute an offer or invitation to subscribe for, or purchase, any shares of Bangkok Bank.

Contact: Investor Relations Team Tel (66) 2 626 4981-2 Fax (66) 2 231 4890 Email: [email protected] Bangkok Bank Website www.bangkokbank.com

For further information