Embed Size (px)

Citation preview

1

Munich, 20 September 2017

Investor Presentation

Baader Investment Conference

Disclaimer

2

This presentation contains assumptions and prospects in respect of the future development of the Sixt Group. These assumptions and prospects are expressed both orally and in writing by the terms “expect”, “anticipate”, “aim”, “plan”, “believe”, “aspire”, “estimate”, “will” and by words with a similar meaning as the aforementioned. These forecasts are based inter alia on our assessment of the economic development in certain countries as well as of the development of the mobility sector. We based our assessment on the information available to us and we deem it to be realistic at the time this presentation was prepared. Our assessments bear a certain amount of risk and future developments may differ from our expectations.

In particular, a totally different performance can ensue from an unexpected slump in demand or economic stagnationon our key markets in Western Europe, in particular in Germany.

The actual performance can differ materially from the forecasts made in this presentation, in case one of theaforementioned risks or other risks not mentioned here should materialize and/or the assumption on which we havebased our forecasts and prospects turn out to be wrong.

We will not subsequently update the forward-looking statements made in this presentation and in their context.

For the above reasons, we assume no liability for any trust placed in the occurrence of our forecasts and in our expectations and assumptions.

Due to rounding it is possible that individual figures presented in this presentation may not add up exactly to the totals shown and that the full-year figures listed may not follow from adding up the individual quarterly figures. For the same reason, the percentage figures presented may not exactly reflect the absolute figures they relate to.

The bar/stock diagrams in the presentation serve as visualisation of the results. They do not follow a consisting scaling. The values stated in the diagrams are authoritative.

Agenda

3

03SIXT GROUP: OVERVIEW AND BUSINESS MODEL –Providing mobility from one minute to five yearsA.

22PERFORMANCE REVIEW 2016 & UPDATE H1/17 – Sustainable growth through internationalisation as well as new business models and new productsB.

33REVISED OUTLOOK 2017 – Solid growth in consolidated operating revenue and significant increase in Group EBT expectedC.

35APPENDIX – Selected key figures for the Sixt GroupD.

Sixt's history – Entrepreneurial operations over four generations

1) Including franchise network

4

Overview Sixt history1912 Martin Sixt founds the "Sixt Autofahrten und Selbstfahrer" company. He starts with seven cars, four Mercedes and

three Luxus-Deutz-Landaulets. Sixt owns one of the first Rent-a-Car companies in Germany

2013 Conversion of Sixt Aktiengesellschaft to a European Stock Corporation (Societas Europaea) – "Sixt SE"

1946 Relaunch of the business after the second world war with the Mercedes 230 Landaulet as a chauffeured limousine –Setting up of the Export-Taxi fleet for members of the US Army

1967 "Auto Sixt" is the first German company to launch a leasing program for vehicles

1969 Erich Sixt, now Chairman of the Board of Sixt, is the third generation offspring to step into the family business

1986 Establishment and initial public offering of "Sixt Aktiengesellschaft“

1990 Sixt in Europe – Sixt Autovermietung Switzerland takes up business

2015 Successful IPO of subsidiary Sixt Leasing SE

2011 Sixt starts its expansion in the USA by establishing rental stations in Florida. The premium car sharing joint venture DriveNow is launched in Munich and Berlin. Founding of Sixt Mobility Consulting GmbH

2016 Around 2,200 points of sales and a fleet of 215,000 vehicles in more than 100 countries1)

The Sixt family is majority shareholder of the ordinary shares

Source: Voting rights announcements until 30 June 2017

5

Sixt SE – Ownership structure of ordinary shares as of 30 June 2017 [%]

Initial public offering in 1986 Ownership structure is basis for

stability and sustainability of the Sixt Group development

In addition, 16,576,246 preference shares outstanding – 100.0% free float

COMMENTS

Total of ordinary shares: 30,367,112

61.6%

35.3%

3.1%

Other shareholders

Erich SixtVermögensver-waltung GmbH(Sixt family)

Deutsche Asset & Wealth Management

Investment GmbH

Free float 38.4%

Sixt is managed by an experienced senior management team

6

Sixt SE – Managing Board

Erich Sixt Detlev Pätsch Dr. Julian zu Putlitz Alexander Sixt Konstantin Sixt

Chief Executive Officer Chairman of the Board Born in 1944 Joined the company in 1969 Third generation to lead the

company Responsible for IT, strategic

human resource, marketing, public relations, international franchising

Chief Operations Officer Born in 1951 Joined the company in 1986 Responsible for customer

service, operations, purchase and sale of vehicles, quality management, repair/damage

Chief Financial Officer Born in 1967 Joined the company in 2009 Holds a Doctorate in

Economics Responsible for finance,

treasury and accounting, controlling, legal, auditing, risk management

Chief Administration Officer Born in 1979 Joined the company in 2009 Responsible for Group

strategy, M&A, central procurement, process and product management, global operating human resources, global service operations, new mobility services

Chief Sales Officer Born in 1982 Joined the company in 2005 Responsible for national

and international sales, global e-commerce business

Sixt is among the leading and most profitable car rental companies worldwide

1) Hertz Global Holdings 2) Avis Budget Group 3) Figure for Sixt: Operating Revenue 4) Average 2016 exchange rate USD – EUR of 1.10295 5) "EBT Margin" equates to "Return on sales"Sources: Annual reports, company information, Bloomberg

7

Vehicle rental industry – Peer group analysis 2016

REVENUE [USD m]

EBT MARGIN5) [%]241 157 279 -470EBT

[USD m]

MARKET CAPITALISATION 31/12 [USD m]

EQUITY RATIO [%]

Europcar4)4)Hertz1)1)

ABG2)2)

Sixt3)4)3)4)

8,659

2,3432,372

8,8032,421

1,790

Sixt4) Hertz1)ABG2)

3,122

Europcar4)

1,552

10.3

Hertz1)

-5.3

Europcar4)2)

6.6 3.2

Sixt3)4)3)4) ABG2))

13.926.8

Hertz1)1)

Sixt ABG2)

2)

1.35.6

Europcar

Sixt business model at a glance

1) Figures for 2016, based on revenue 2) Average number of cars under operation including international corporate excluding franchise3) Figures for 2016, based on contracts (including order book)4) Including international finance and full-service lease and fleet management, excluding franchisees and cooperation partners 5) Based on operating revenue

8

Customer need for mobilitySIXT RENT-A-CAR

One of the largest independent leasing providers in Germany Contract portfolio3): 42% fleet leasing 24% online retail leasing 34% fleet management

SIXT LEASE-A-CAR Market leader in Germany Balanced customer portfolio1): 58% retail/ tourists 34% corporate 3% replacement business 5% other businesses

Rental vehicles2)

Operating revenue [EUR m]International share5)

108,0001,703.451.7%

98,2001,519.348.0%

20162015Contracts4)

Operating revenue [EUR m]International share5)

113,600420.313.5%

103,200419.814.9%

20162015

Sixt provides mobility from one minute to five years

Sixt's performance is built on a premium product, broad coverage, trusted brand, and lean cost structures

9

"Drive premium –pay economy"

47% in value of the car rental fleet in 2016 consists of premium brands (Audi, BMW and Mercedes-Benz)

International presence 12 corporate countries More than 90 franchise

countries

COMMENTSVehicles & services

"Premium Product"

Network & distribution

"Broad Coverage"

Brand &marketing

"Trusted Brand"

Vehicle rental – Service proposition

Organisation & infrastructure

"Lean (Cost) Structures"

Market leader in Germany and number 2 in Europe

10

Vehicle rental – Market shares 2015 [%]

1) Only Sixt corporate countries (excl. Luxembourg and Monaco), excluding franchise countriesSource: Euromonitor (Survey 2016 for previous year 2015), own estimates

34%

Sixt

12%

19%

Hertz

Others

ABG

9%

27% Europcar

22%

Sixt12%

Hertz

12%

Europcar

11%ABG

43%

Others

EUROPE1)GERMANY USA

Enterprise23%Hertz

<1%

17%ABG

Sixt

50%

9%

Others

Further expansion of station network

11

Vehicle rental – Station network

483 508 509 515

571 555 531 510

2177

1,123

International

Franchise

H1/2017

1,239

2016

2,264+47 +64-24

National

2015

1,090

2,153 2,200

1,160

2014

Sixt Europe

CorporateFranchise

Sixt Worldwide

GEOGRAPHIC COVERAGE STATIONS [No.]

-33

-16

+25

+70

-24

+1

+79

-21

+6

Ongoing US expansion

1) Franchise stations

12

Vehicle rental – US expansion as of 31 December 2016

MAJOR AIRPORT STATIONS

17

489

10

2

2011 2016

58

2013

26

IATAMIAFLLMCOATLPHXSEALASMSPPHLLAXSFODFWSJC

AirportMiamiFt. LauderdaleOrlandoAtlantaPhoenixSeattleLas VegasMinneapolis1)

Philadelphia1)

Los AngelesSan FranciscoDallasSan Jose

REGIONAL EXPANSIONSTATIONS [No.]

CorporateFranchise

2

Since February 2017, Italy is operated as a corporate country

13

Italy going-forward

12 stations to be opened until mid of 2017 Bergamo Bologna Florence Milan-Linate Milan-Malpensa (T1) Milan-Malpensa (T2) Pisa Rome-Ciampino Rome-Fiumicino Turin Venice Verona

Wish list of around 25 stations in total to be opened in the short-term

Current focus on Northern area of Italy

COMMENTS

Global trends change mobility needs

14

DRIVERS OF CHANGE USE CASES1) URBANISATION

2) CHANGE IN VALUES

4) ECONOMIC EFFICIENCY

3) SUSTAINABILITY

Increasing traffic volume Poor parking situation More demand for short-haul routes

Car loses its role as status symbol Desire to own a car decreases Trend ″from owning to sharing″

Demand for ecological mobility solutions Environmentally conscious generations Management of traffic and vehicle

admissions in large cities

Inefficient asset (only 4% utilisation) 39 km = average driving distance of

a passenger car in Germany per day

1) REPLACEMENT OF COMPANY CARS

2) EMPLOYEE INCENTIVES

4) SOLUTION FOR EXPATS

3) COMPENSATION FOR DOWNSIZING COMPANY CARS

Offers employees more flexible mobility solution

Increases employee motivation Various target groups: from Junior

Manager to Senior Manager

Decreasing company fleet by offering valuable alternatives

Reduction in costs

Expats need mobility services in different countries/cities

Various Sixt services depending on the individual situation and needs

DriveNow: Successful internationalisation continued

15

DriveNow – Highlights 2016 / Update H1/2017

INNOVATION / EXPANSIONPRESENCE

1) At the end of the respective period

MEMBERS1) ['000] Handshake (seamless switch of a

vehicle between customers) Process digitalisation (online validation

for registration) Digital fuel card (TOTAL, Berlin) Share of electric vehicles 20% Brussels since July 2016 Milan since October 2016 Helsinki

– Since May 2017– 150 cars in an area of 40 square

kilometres (BMW X1 and 2 series, MINI, BMW i3)

– Operated by a franchisee

815

580

390

215

75

925

2016 H1/172015201420132012

2011

2012

2013

2014

2015

2016

2017

MUNICH

DUSSELDORF

HAMBURG

BERLIN

COLOGNE

VIENNA LONDON

COPENHAGEN STOCKHOLM

BRUSSELS MILAN

75

215

390

580

815925

<HELSINKI

Sixt is well-known for its marketing and advertisements

16

Examples

Sixt maintains partnerships with numerous airlines and other partners and holds various high-profile awards

17

Strategic partnerships and awards – Examples

AIRLINES & FFPs AWARDS

Sixt Cards

Credit Card Web 2.0

TelecomTravel Office Sol.

Retail

OTHER PARTNERSHIPSAward Year and category

2007-09/11-13: "Best rent-a-car company in Germany"

2010/12/13/14: "Best Vehicle Rental Company in Germany"

2013/14/15/16: "Best rent-a-car company for business travelers"; 2010/11/14/15: "Best rent-a-car company in Germany"

2013/14/16: "Best Luxury Car Rental Company of the World"

2012-2016: "World's Leading Luxury Car Rental Company“ & “World's Leading Luxury Chauffeur Service”

…and +50 more!

Hotels

Sixt Leasing is a provider of mobility services with a highly attractive and customer-centric product offering

18

Leasing – Service proposition

Mid-sized and large corporates Private and business customersCustomer focus

Full Service Leasing Fleet Management Classic Leasing / Vario Financingand Services Key products

Top 3 Non-Captive Top 3 Fleet Managers First MoverMarket position in Germany

Value proposition

One-Stop-Online-Shop for >30 OEM Price Transparency Convenience Digital processes

OEM independent optimisation of Total Cost of Ownership (TCO) Know-how Purchasing power Outsourcing

Fleet Leasing Fleet Management Online Retail

Balance Sheet & Know-how Know-how Purchase Power & ServiceSuccess factors

Significant increase in leasing contract portfolio – Growth driven by Fleet Management and Online Retail

19

Leasing : Contract development ['000]

FLEET MANAGEMENTCONTRACTS1)

1) Including order book

ONLINE RETAIL1)

38,838,733,831,4

+0,4%

H1/172016

+14,3%

+7,6%

2014 2015 H1/17

+29.9%+33.7%

42.5

20152014

27.421.1

15.8

2016

+54.9%

11

62.2

12 13

76.2

56.3

15

103.2

14

97.4

16

113.6

128.9

H1/17

31.4 33.838.7 38.8

Successful product innovation at Sixt Leasing: The ″Flat Rate for the Road″ campaign

20

Flexible new vehicle leasing ranging from 12 to 30 months with Flexi-Lease option

Unrivalled low price of EUR 99.99 per month for a fully-equipped Peugeot 208 (incl. insurance, tax, transfer and registration – No upfront payment)

Seamless digital ordering process with video-ident, eSign and online credit check

1&1 cooperation as example for successful new sales

Sixt's fleet is to a large extent covered by buy-back agreements – Resilient risk profile

1) Based on vehicles added to the fleet in the fiscal year 2016 2) Based on number of contracts as at 31 December 2016 in the business fields fleet leasing and online retail, including lease assets, inventories and order book

21

Sixt rental and leasing fleet KPIs 2016

Buy-back agreements lead to low exposure to residual value risks as well as low earnings volatility

Majority of buy-back agreements in the vehicle rental business with car manufacturers

Majority of buy-back agreements in the leasing business for fleet leasing vehicles (large fleets with identical, customer-specific configuration) –Online Retail leasing vehicles with lower buy-back ratio due to higher marketability of vehicles

Typically holding periods of 6 months in vehicle rental (passenger cars) and 3-4 years in leasing

94%

RENTAL: CAR ORDERS1) LEASING: CONTRACTS2)

95%Buy-back

5%Non-Buy-back

COMMENTS

Non Buy-back

Buy-back

57%43%

Agenda

22

03SIXT GROUP: OVERVIEW AND BUSINESS MODEL –Providing mobility from one minute to five yearsA.

22PERFORMANCE REVIEW 2016 & UPDATE H1/17 – Sustainable growth through internationalisation as well as new business models and new productsB.

33REVISED OUTLOOK 2017 – Solid growth in consolidated operating revenue and significant increase in Group EBT expectedC.

35APPENDIX – Selected key figures for the Sixt GroupD.

Sustainable growth through internationalisation, new business models and products – Highlights 2016

23

RENT

ALRE

NTAL

New business models and products – MaaS1), DriveNow, myDriver

Successful Internationalisation – Rental revenue share abroad above 50%

Strong equity ratio above the defined minimum of 20%

Successful financing in an amount of more than EUR 1 billion in 2016

Dynamic growth in contract portfolio – Online Retail +30%, Fleet Management +14%

Acquisition of autohaus24.de as part of the growth strategy Online RetailLEAS

ING

LEAS

ING

GROU

PGR

OUP

Record dividend of EUR 77.8 million as proposed by the Managing Board

1) MaaS = Mobility as a Service

2

1

3

4

6

5

7

Sixt Group – Highlights 2016

Sixt Group generated an EBT of EUR 218 m and a consolidated profit of EUR 157 m in 2016

1) Figures 2013 adjusted for “at equity” consolidation of joint ventures2) Before minority interests

24

Group results 2011-2016 – Key figures [EUR m]1)

OPERATING REVENUE EBIT EBTEBITDA

199.2221.8

177.3167.7189.8

2011 20162013

255.8

2012 2014 2015

118.6157.0

137.6138.9

185.2

2014 2015 20162011 20132012

218.3

511.5 481.8 496.2 546.3 633.2 Cons.profit2) 97.5 79.2 94.4 110.0 128.2Group

revenue 1,564 1,596 1,653 1,796 2,179

1,016

961,426

393383

954

89

142

Leasingrevenue 420

1,377Rental

revenue

1,645

Otherrevenue

1,939

417

1,120

108

896

1,373

394

83

1,505

1,534

420

1702,124

20162012 20132011 20152014

2,413 756.5 156.6

Sixt Group EBT by business unit– Considerable earnings improvements in both segments

25

Consolidated financial statements 2011-2016 – EBT by segments [EUR m]1)

GROUP2) VEHICLE RENTAL2) LEASINGReturn onsales2) [%]

2016

218.3

137.6138.9

20152012

185.2

2013 2014

157.0

118.6

2011 2014

25.6

2013

16.3

2011

25.4

20152012

21.030.3 31.6

2016

119.6

2011 2014

160.4

2013

122.3

2015

136.8

2012

106.4

2016

181.0

10.1 8.3 9.1 9.5 9.6 12.2 10.2 11.0 11.1 10.6 6.5 4.3 5.3 6.1 7.210.3 10.6 7.5

1) EBT Segment Other is not shown2) Includes in 2016 a one-off effect in a mid single-digit million range from a release of a provision for legal risks 3) Related to operating revenue

Total assets have risen to EUR 4.03 bn –With 26.8% Group equity ratio remained clearly above minimum target

1) Figures 2013 adjusted for "at equity" consolidation of joint ventures2) Since fiscal year 2015 the figures presented in current and non-current financial liabilities include current and non-current finance lease liabilities, which have previously been included in other liabilities.

Prior-year figures have been adjusted accordingly.

26

Consolidated financial statements 2011-2016 – Key figures [EUR m]1)

TOTAL ASSETS FINANCIAL LIABILITIES2) EQUITY RATIO [%]Equity[EUR m]

26.3

2013

28.5

2014

28.9

2015

25.6

2012

29.1

2011 2016

26.8

855

2011

790

256289

2012

1,131

1,111977187

1,173

528

645

2013

909

921

1,420

2014

Non-current

Current

2015

1,8302,132

1,370

762

2016

Target:≥ 20%

675 775 958

457 583

939

740

926

5081,262

2,371

2012

1,763

2,174

2,8182,328

20132011

3,660

2015

1,013

654

1,196

902

2014

1,021

1,957

2016

1,050

4,028

Rentalvehicles

Others

Leaseassets

596 633 676 742 1,059 1,080

Continued focus on diversifying financial instruments and on balancing Sixt Group's maturity profile

27

Sixt Group – Maturities of financial liabilities as of 31 December 2016 [EUR m]

Bond of EUR 250 m with a tenor of 6 years successfully placed in 2016

In addition, Sixt Leasing SE issued a bond of EUR 250 m with a tenor of 4 years in January 2017

Sufficient headroom through unutilised bilateral credit lines in the amount of several EUR 100 m

Intensified cooperation with OEMs by utilisation of OEM operating lease facilities... sufficient headroom available through unutilised bilateral credit lines,

OEM operating lease facilities and commercial paper programme

Financial liabilities1) 2017 2018 2019 2020 2021 2022 2023 Total

Bonds - 250.0 - 253.82) - 250.0 - 753.8Borrower's note loans 245.0 - 93.0 30.0 224.5 - 150.5 743.0

Commercial paper 188.0 - - - - - - 188.0

Subtotal 433.0 250.0 93.0 283.8 224.5 250.0 150.5 1,684.8

Utilisation of bilateral credit lines3)

269.4 1.3 - - - - - 270.7

ABS 44.7 44.6 44.4 28.9 2.4 - - 165.0

Total 747.1 295.9 137.4 312.7 226.9 250.0 150.5 2,120.5

COMMENTS

1) Repayment amounts excluding accrued and in future payable interest 2) EUR 3.8 m (2020) refer to employee participation programme (matching stock programme)3) Incl. finance leases

Continued shareholder-friendly dividend policy –Increase in total payout by 8.9%

28

Sixt SE – Dividend proposal by management

TOTAL DIVIDEND PAYOUT [EUR m]DIVIDEND PROPOSAL

Bonusdividend

+8.9%

Dividend

2016

77.8

2015

71.5

43.0

28.5

1) As a percentage of consolidated profit after minority interests

2015 2016Proposal for ordinary shares EUR 1.50 EUR 1.65Proposal for preference shares EUR 1.52 EUR 1.67

Total dividend EUR 71.5 m EUR 77.8 m Dividend EUR 43.0 m EUR 77.8 m Bonus dividend EUR 28.5 m -

Dividend payout ratio1) 62.1% 54.7%

Sixt shares continue to show a highly attractive return profile

29

Sixt SE – Dividend per share [EUR]

PREFERENCE SHARESORDINARY SHARES

Dividend

Bonusdividend

2016

1.67

2015

1.52

0.92

0.60

2014

1.22

0.82

0.40

2013

1.02

0.67

0.35

2012

1.02

0.57

0.45

2011

0.77

0.62

0.15

Dividend

1.65

Bonusdividend

20162015

1.50

0.90

2011

0.75

0.60

0.15

0.60

2014

1.20

0.80

0.40

2013

1.00

0.65

0.35

2012

1.00

0.55

0.45

3.2%Dividendyield1)

1) Including bonus dividend and based on year-end closing price of ordinary shares and preference shares, respectively

4.3%Dividendyield1)

5.5% 6.4% 4.3% 3.7% 3.2% 6.2% 7.4% 5.3% 4.7% 4.0%

H1/17 Update: Sixt Group generated an EBT of EUR 102.6 m and a consolidated profit of EUR 72.9 m in H1/17

1) Before minority interests

30

Sixt Group – Key figures H1/17 [EUR m]

EBTREVENUE CONSOLIDATED PROFIT1)

Operatingrevenue

H1/17

1,066.8

147.0Other

1,213.8+5.7%

1,148.5145.0

H1/16

1,003.5

+1.4%

+6.3%

H1/16

81.9102.6

H1/17

+25.3%

EBIT 100.9 119.1

56.7

+28.5%

72.9

H1/16 H1/17

H1/17 Update: Sixt Group EBT by business unit –Earnings improvement in both segments

31

Sixt Group – EBT H1/17 by business unit1) [EUR m]

VEHICLE RENTALGROUP LEASINGEBTmargin2)

[%]

8.3 9.5

81.9

H1/16 H1/17

102.625.3%

H1/17

66.180.3

+21.5%

H1/16 H1/17

+3.2%

16.8

H1/16

16.2

7.9 7.78.2 9.6 EBTmargin2)

[%]

EBTmargin2)

[%]

1) Segment Other with EBT of EUR 5.5 m in H1/17 (H1/16 EUR -0.5 m)2) Based on operating revenue

H1/17 Update: Total assets have risen to almost EUR 4.6 bn –With 23.2% Group equity ratio has remained at a high level

32

Sixt Group – Key figures H1/17 [EUR m]

FINANCIAL LIABILITIESTOTAL ASSETS EQUITY RATIO [%]1,079.7 1,060.6Equity

[EUR m]

4,562.0

H1/17

Other1,098.3

Leaseassets

+533.5

2,370.3Rentalvehicles

2016

1,050.7

1,020.8

1,957.0

1,093.4

4,028.5

H1/17

761.6

2,132.0

1,370.4

2016

884.9

2,412.0

1,527.1Non-current

+280.0

Current 23.226.8

2016 H1/17

Target:≥ 20%

Agenda

33

03SIXT GROUP: OVERVIEW AND BUSINESS MODEL –Providing mobility from one minute to five yearsA.

22PERFORMANCE REVIEW 2016 & UPDATE H1/17 – Sustainable growth through internationalisation as well as new business models and new productsB.

33REVISED OUTLOOK 2017 – Solid growth in consolidated operating revenue and significant increase in Group EBT expectedC.

35APPENDIX – Selected key figures for the Sixt GroupD.

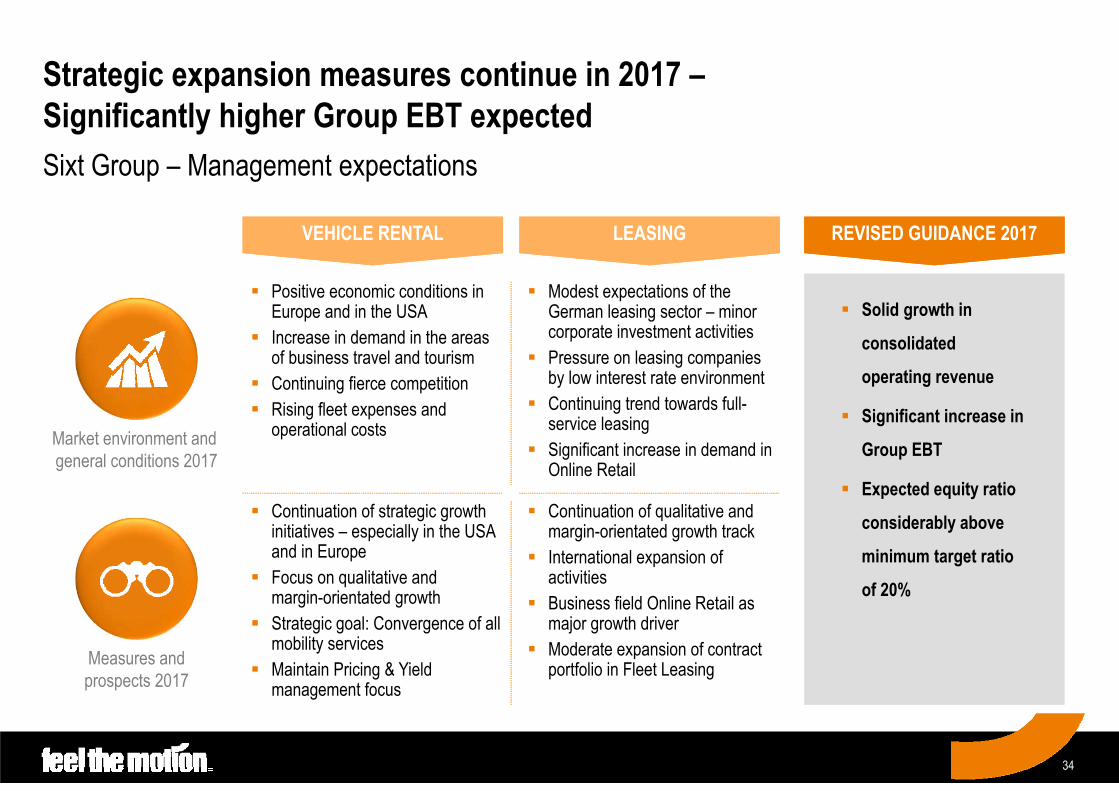

Strategic expansion measures continue in 2017 –Significantly higher Group EBT expected

34

Sixt Group – Management expectations

Market environment and general conditions 2017

Measures andprospects 2017

VEHICLE RENTALVEHICLE RENTAL LEASINGLEASING REVISED GUIDANCE 2017REVISED GUIDANCE 2017

Positive economic conditions in Europe and in the USA

Increase in demand in the areas of business travel and tourism

Continuing fierce competition Rising fleet expenses and

operational costs

Continuation of strategic growth initiatives – especially in the USA and in Europe

Focus on qualitative andmargin-orientated growth

Strategic goal: Convergence of all mobility services

Maintain Pricing & Yield management focus

Modest expectations of the German leasing sector – minor corporate investment activities

Pressure on leasing companies by low interest rate environment

Continuing trend towards full-service leasing

Significant increase in demand in Online Retail

Continuation of qualitative and margin-orientated growth track

International expansion of activities

Business field Online Retail as major growth driver

Moderate expansion of contract portfolio in Fleet Leasing

Solid growth in

consolidated

operating revenue

Significant increase in

Group EBT

Expected equity ratio

considerably above

minimum target ratio

of 20%

Agenda

35

03SIXT GROUP: OVERVIEW AND BUSINESS MODEL –Providing mobility from one minute to five yearsA.

22PERFORMANCE REVIEW 2016 & UPDATE H1/17 – Sustainable growth through internationalisation as well as new business models and new productsB.

33REVISED OUTLOOK 2017 – Solid growth in consolidated operating revenue and significant increase in Group EBT expectedC.

35APPENDIX – Selected key figures for the Sixt GroupD.

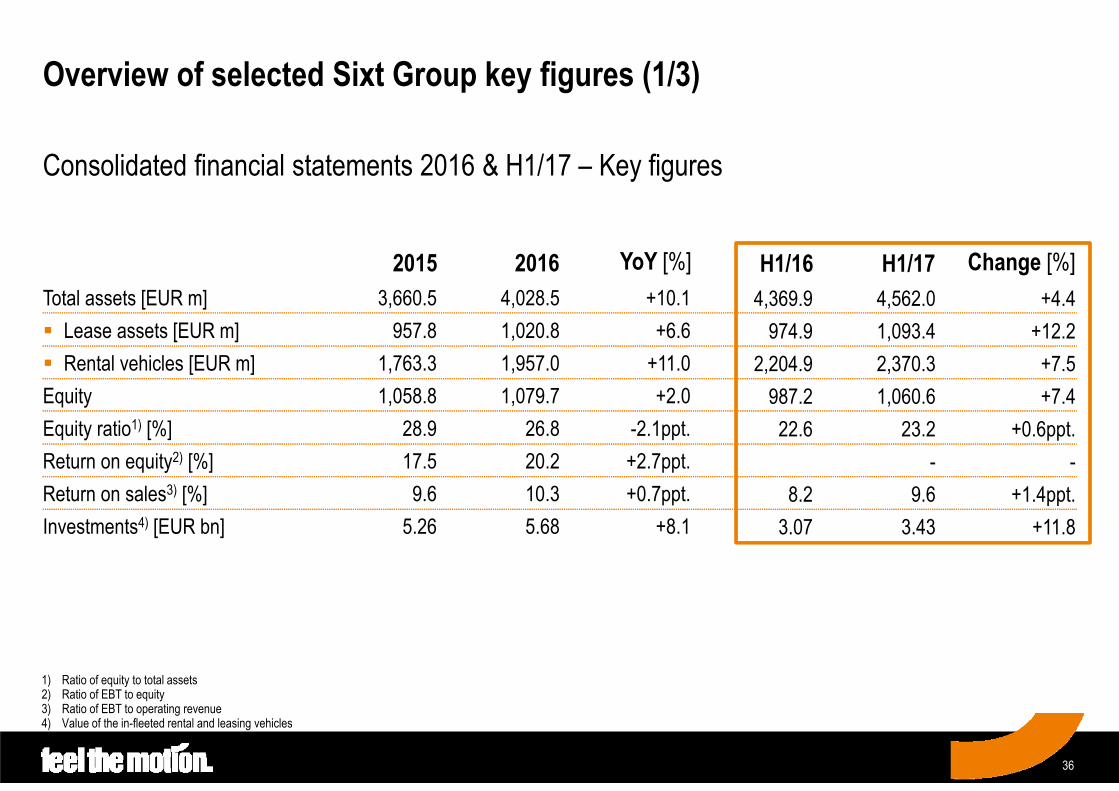

Overview of selected Sixt Group key figures (1/3)

36

Consolidated financial statements 2016 & H1/17 – Key figures

Total assets [EUR m] Lease assets [EUR m] Rental vehicles [EUR m]EquityEquity ratio1) [%]Return on equity2) [%]Return on sales3) [%]Investments4) [EUR bn]

3,660.5957.8

1,763.31,058.8

28.917.59.6

5.26

+10.1+6.6

+11.0+2.0

-2.1ppt.+2.7ppt.+0.7ppt.

+8.1

4,028.51,020.81,957.01,079.7

26.820.210.35.68

2015 2016 YoY [%]

1) Ratio of equity to total assets 2) Ratio of EBT to equity 3) Ratio of EBT to operating revenue4) Value of the in-fleeted rental and leasing vehicles

4,369.9974.9

2,204.9987.222.6

8.23.07

+4.4+12.2+7.5+7.4

+0.6ppt.-

+1.4ppt.+11.8

4,562.01,093.42,370.31,060.6

23.2-

9.63.43

H1/16 H1/17 Change [%]

Overview of selected Sixt Group key figures (2/3)

37

Income statement 2016 & H1/17 [EUR m]

Consolidated total revenueFleet expenses and cost of lease assetsPersonnel expensesDepreciation and amortisation expenseNet other operating income/expensesEBITNet finance costsEBTIncome tax expenseConsolidated profit1)

2,179.3814.4274.5411.4

-457.1221.8-36.6185.257.0

128.2

+10.7+4.4

+21.9+21.7+3.1

+15.3+2.5

+17.9+8.1

+22.2

2,412.7850.0334.7500.7

-471.5255.8-37.5218.361.7

156.6

2015 2016 YoY [%]

1) Before minority interests

1,148.5420.1148.7240.3

-238.5100.9-19.081.925.256.7

+5.7+1.1

+14.8+5.7+2.8

+18.0-13.3+25.3+18.0+28.5

1,213.8424.8170.7253.9

-245.3119.1-16.5102.629.772.9

H1/16 H1/17 YoY [%]

Overview of selected Sixt Group key figures (3/3)

38

Consolidated financial statements 2016 & H1/17 – Key figures per business unit [EUR m]

LEASING BUSINESS UNITVEHICLE RENTAL BUSINESS UNIT

H1/17848.3

766.1

82.3453.180.3

9.5204.0162.0-14.3

Total rental revenue Thereof revenue

from vehicle rental Other revenue from

rental business Thereof abroadEBTEBT margin1) [%]Fleet expensesDepreciation expenseNet finance costs

H1/16348.6

206.1

142.544.016.2

7.9217.588.1

-10.9

Total leasing revenue Thereof leasing

revenue Thereof sales

revenue Thereof abroadEBTEBT margin1) [%]Cost of lease assetsDepreciation expenseNet finance costs

H1/17363.5

218.4

145.145.916.8

7.7227.590.7-9.6

H1/16797.3

718.0

79.3403.466.1

8.3209.1151.3-11.8

YoY [%]+6.4

+6.7

+3.7+12.3+21.5

+1.2ppt.-2.5+7.1

+21.8

YoY [%]+4.3

+6.0

+1.8+4.3+3.2

-0.2ppt.+4.6+2.9

-12.3

1) Ratio of EBT to operating revenue

20161,703.4

1,533.5

169.9880.8181.010.6

422.9321.3-27.5

20151,519.3

1,376.9

142.4728.6160.410.6

419.9239.1-23.9

YoY [%]+12.1

+11.4

+19.3+20.9+12.8

+0.0ppt.+0.7

+34.4+15.1

2015655.4

419.8

235.586.230.3

7.2408.5171.5-21.3

2016704.2

420.3

283.987.831.6

7.5439.3177.5-19.5

YoY [%]+7.5

+0.1

+20.5+1.8+4.3

+0.3ppt.+7.5+3.5-8.5

Contact details

39

Sixt SEZugspitzstrasse 182049 Pullach

Dr. Julian zu Putlitz Dieter HanelCFO Managing Director Finance & AccountingT: +49 (0)89 74444 - 4256 T: +49 (0)89 74444 - 4281F: +49 (0)89 74444 – 8 4256 F: +49 (0)89 74444 – 8 4281Email: [email protected] Email: [email protected]